Bunker & Residual Fuel - Platts · Bunker & Residual Fuel ... Oil Service Global Gas Model LNG...

23

© Wood Mackenzie 0 Delivering commercial insight www.woodmac.com Bunker & Residual Fuel New Dynamics of Supply & Demand Platts Bunker Fuel and Residual Conference 22 nd June 2011, Houston, Texas Skip York Vice President - Downstream Consulting (Americas)

Transcript of Bunker & Residual Fuel - Platts · Bunker & Residual Fuel ... Oil Service Global Gas Model LNG...

© Wood Mackenzie 0

Delivering commercial insight

www.woodmac.com

Bunker & Residual FuelNew Dynamics of Supply & Demand

Platts Bunker Fuel and Residual Conference22nd June 2011, Houston, Texas

Skip YorkVice President - Downstream Consulting (Americas)

© Wood Mackenzie 1

Delivering commercial insight

www.woodmac.com

Calgary

Houston

BostonLondon

EdinburghMoscow

Beijing

Singapore

Sydney

Kuala Lumpur

Tokyo

New York

Dubai

Rio de Janerio

Mexico

Wood Mackenzie Offices

Perth Brisbane

AnnapolisDenver

Our global research, consulting, and account management team is a client advantage

Downstream Team Base Locations

Seoul

© Wood Mackenzie 2

Delivering commercial insight

www.woodmac.com

Our knowledge and expertise extends across the energy value chain

© Wood Mackenzie 3

Delivering commercial insight

www.woodmac.com

Our research is integrated across the energy value chain

ProductMarketsService

Refinery EvaluationModel

DownstreamOil Service

Global Gas Model

LNG Service

Gas & PowerService

Macro OilsService

UpstreamService

Global OilSupplyTool

© Wood Mackenzie 4

Delivering commercial insight

www.woodmac.com

11 Global fuel oil marketsGlobal fuel oil markets

2 Bunkers, ECAs and SECAs

3 Trade and balancing markets

© Wood Mackenzie 5

Delivering commercial insight

www.woodmac.com

Our ‘business as usual’ view of fuel demand sees growth in bunkers offsetting steady decline in Inland use

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2005 2010 2015 2020 2025

Bp

d

Unconstrained Inland Marine

Global Fuel Oil Demand Outlook (unconstrained)

Kb

d

© Wood Mackenzie 6

Delivering commercial insight

www.woodmac.com

Expected refinery investments scheduled to come on-stream over the next 5 years will result in a growing theoretical ‘deficit’ in fuel oil

Global Fuel Oil ‘Deficit’ – Base Case Supply versus Base Case Demand

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2005 2010 2015 2020 2025

Su

pp

ly /

De

ma

nd

, k

bd

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Imb

ala

nc

e, k

bd

Global Demand Global Supply Theoretical Deficit (RHS)

© Wood Mackenzie 7

Delivering commercial insight

www.woodmac.com

Global rebalancing of fuel oil markets incentivised by higher fuel oil prices – but no step change in pricing mechanism is expected

Small increase in the fuel oil price relative to other products will incentivise additional production

Altering fuel oil production at one refinery also alters production of other products

Result is a complex process such that supply/demand for each individual product and every refinery are re-balanced

Fuel oil tightness is not expected to be solved via yields changes, but rather by higher prices destroying fuel oil demand

0

100

200

300

400

500

600

0 50 100 150 200 250

Cumulative FO Production, Mt

Complex &Coker

FCC &HCK

HCK

FCC

HSK

Pseudo-HSK

Refinery Fuel Oil Supply Dynamics

FCC refineries – as the most exposed in terms of refining margin – will switch to a pseudo hydroskimming mode through a relative reduction of their FCC unit throughputs

FCC refineries – as the most exposed in terms of refining margin – will switch to a pseudo hydroskimming mode through a relative reduction of their FCC unit throughputs

Fuel Oil supply increased through increases of price at the margin, rather than a step change to a different mechanism of

production

Fuel Oil supply increased through increases of price at the margin, rather than a step change to a different mechanism of

production

© Wood Mackenzie 8

Delivering commercial insight

www.woodmac.com

1 Global fuel oil markets

22 Bunkers, ECAs and SECAsBunkers, ECAs and SECAs

3 Trade and balancing markets

© Wood Mackenzie 9

Delivering commercial insight

www.woodmac.com

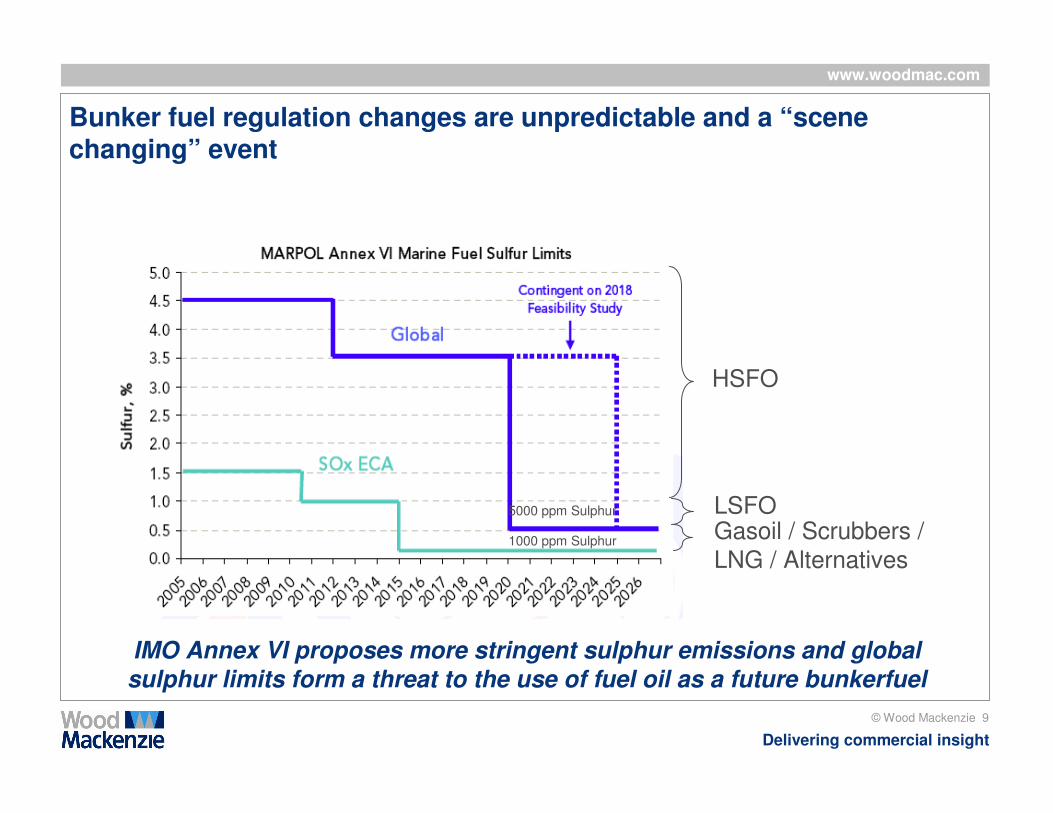

Bunker fuel regulation changes are unpredictable and a “scene changing” event

1000 ppm Sulphur

5000 ppm Sulphur

HSFO

LSFOGasoil / Scrubbers /

LNG / Alternatives

IMO Annex VI proposes more stringent sulphur emissions and global

sulphur limits form a threat to the use of fuel oil as a future bunkerfuel

Black Swan events?

© Wood Mackenzie 10

Delivering commercial insight

www.woodmac.com

2012 reduction to 3.5% sulphur in international bunkers is unlikely to cause any material issues in refining or fuel supply

Regional average bunker fuel sulphur content, and future changes

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

US West Coast US Gulf Coast US East Coast Rotterdam Fujairah Singapore

Su

lph

ur

co

nte

nt,

wt%

2012

Mandate2020

Mandate

© Wood Mackenzie 11

Delivering commercial insight

www.woodmac.com

Our analysis reflects a switch of over 500 kbd of heavy fuel oil demand to gasoil in 2015 in the European SECAs and the North American ECA

Current fuel sulphur limit for ECAs and SECA bunkers is

1.0% sulfur and further reduced to 0.1% sulphur in

January 2015

Shift to 0.1% would require switch from fuel oil to distillate

in the ECA and SECAs

EPA forecasts that by 2020, 290 kb/d (15.6 Mt) of residual

fuel oil (FO) would be consumed within the ECA if a

sulphur limit was not in force.

– We estimate the size of the market to be 250 kbd in 2015

– We assume all FO consumed in the ECA will be replaced

by distillate gasoil from 2015

Demand switch in the SECAs is similar in magnitude

ECA Zone. Source: US Environmental Protection Agency.

© Wood Mackenzie 12

Delivering commercial insight

www.woodmac.com

The 2020 IMO target – if met entirely by low sulphur fuels – would result in structural changes to the refining industry

Indicative Investment Costs of Fuel Oil Conversion to Meet 2020 IMO Specification

Our expectation is that either there will be an uptake of ship scrubbing technology by 2020, or a deferral of the specification implementation

Our expectation is that either there will be an uptake of ship scrubbing technology by 2020, or a deferral of the specification implementation

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Asia

Pacific

Greater

Europe

North

America

Middle

East

FSU Sub-

Saharan

Africa

Latin

America

Nu

mb

er

of

pro

jec

ts

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Cu

mu

lati

ve

co

sts

, U

S$

bil

No. of Cokers (LHS) Cumulative Cost, US$ bil (RHS)

Total cost for all

regions = US$85 bil

© Wood Mackenzie 13

Delivering commercial insight

www.woodmac.com

Ship flue gas scrubbing technology is commercially imminent providing an alternative to gasoil bunkers

Short shipping purely within the SECA probably would be met through FO use on vessels fitting seawater scrubbing

Extent and speed of retrofitting equipment to vessels are critical drivers

Price spread between gasoil and fuel oil is a powerful price signal

We expect significant up-take 2015+

Seawater Scrubbing Payback

0

10

20

30

40

50

60

10 20 30 40 50

Percent of time in SECA

Pa

yb

ac

k i

n y

ea

rs

Source Wood M ackenzie

© Wood Mackenzie 14

Delivering commercial insight

www.woodmac.com

Bunker market in NW Europe grows and shifts towards low sulphur fuel oil and gasoil use unless there up-take of seawater scrubbing

NWE bunker market consumed 60 kbd MGO in 2009, due to the nature of the vessels rather than legislation

SECA regulations drive demand for 1% S HFO, AND increases MGO demand for use in port (emission limit equivalent to 0.1%S)

Beyond 2015, we estimate 130 kbd of short sea shipping fuel demand, which could be met with HFO if vessels are fitted with scrubbing technology

NW European Bunkers

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

tho

us

an

d t

on

s

3.5%S 1.5%S 1.0%S 0.1%S

MGO demand based

on vessel engine type

SECA restrictions

on use in port

increase MGO

demand

SECA regulations

drive demand

shifts

© Wood Mackenzie 15

Delivering commercial insight

www.woodmac.com

1 Global fuel oil markets

2 Bunkers, ECAs and SECAs

33 Trade and balancing marketsTrade and balancing markets

© Wood Mackenzie 16

Delivering commercial insight

www.woodmac.com

N America heavy high sulphur fuel oil surpluses projected to grow

-600

-400

-200

0

200

400

600

800

1,000

LSFO HSFO

Bala

nces, kb/d

.

2005 2009 2010 2015 2020

Surplus

Deficit

Source Wood Mackenzie

© Wood Mackenzie 17

Delivering commercial insight

www.woodmac.com

Changes to the regional fuel oil supply/demand balance outlook are likely to result in new material trade flows by 2015 and beyond

Regional Fuel Oil Balances

Key shifts in regional balances driving new trade flowsKey shifts in regional balances driving new trade flows

-1,500

-1,000

-500

-

500

1,000

1,500

Asia Pacific Middle East North America Latin America Greater Europe FSU SSA

Re

gio

na

l im

ba

lan

ce

, k

bd

2005 2010 2015 2020

© Wood Mackenzie 18

Delivering commercial insight

www.woodmac.com

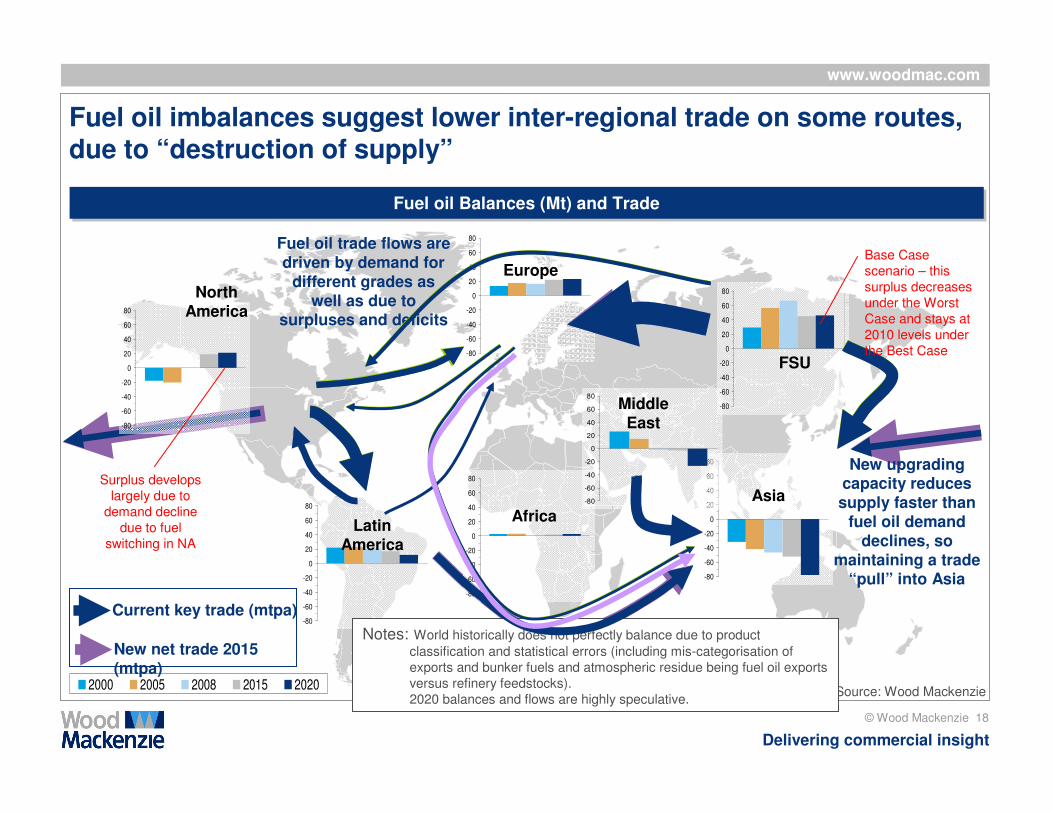

Fuel oil imbalances suggest lower inter-regional trade on some routes, due to “destruction of supply”

Current key trade (mtpa)

Fuel oil Balances (Mt) and TradeFuel oil Balances (Mt) and Trade

Source: Wood Mackenzie

-80

-60

-40

-20

0

20

40

60

80

2000 2005 2008 2015 2020

New net trade 2015 (mtpa)

Fuel oil trade flows are driven by demand for

different grades as well as due to

surpluses and deficits

-80

-60

-40

-20

0

20

40

60

80

-80

-60

-40

-20

0

20

40

60

80

-80

-60

-40

-20

0

20

40

60

80

-80

-60

-40

-20

0

20

40

60

80

-80

-60

-40

-20

0

20

40

60

80

Asia

FSU

Europe

Africa

Middle East

Latin America

New upgrading capacity reduces supply faster than

fuel oil demand declines, so

maintaining a trade “pull” into Asia

Notes: World historically does not perfectly balance due to product

classification and statistical errors (including mis-categorisation of

exports and bunker fuels and atmospheric residue being fuel oil exports

versus refinery feedstocks).

2020 balances and flows are highly speculative.

-80

-60

-40

-20

0

20

40

60

80

North America

Base Case

scenario – this

surplus decreases

under the Worst

Case and stays at

2010 levels under

the Best Case

Surplus develops

largely due to

demand decline

due to fuel

switching in NA

© Wood Mackenzie 19

Delivering commercial insight

www.woodmac.com

• Changes to the regional fuel oil supply/demand result in trade flows by 2015

• A consequence of change is almost always uncertainty which results in higher (price) volatility

• How does price volatility impact scrubbing investment decisions?

Conclusions and Implications

© Wood Mackenzie 20

Delivering commercial insight

www.woodmac.com

Harold “Skip” York Vice President – Downstream Oil (Americas)

T + 1 713 470 1667

Skip York is the global lead of Wood Mackenzie’s Downstream Transaction Support offering

and has almost 20 years of worldwide experience across the energy value chain. He has

deep expertise in petroleum market economics specializing in strategy, commercial

optimization (including asset valuation and transaction support), and market price-setting

mechanisms.

Skip has led a number of projects involving feasibility studies, valuations, and transaction due

diligence projects across the petroleum industry. In particular, he has experience in valuing

non-fungible crudes across a number of markets, such as supporting transactions involving

Canadian oil sands assets and target refineries.

Prior to joining Wood Mackenzie, Skip worked for ExxonMobil in a variety of strategic

planning assignments. He held roles as the global expert on joint venture negotiation best

practices, managing new business development downstream opportunities in Asia Pacific,

and leading research teams on studies of the economic impact of large-scale oil investments

on the economy of Russia. He also has consulted for clients at McKinsey & Company and

Charles River Associates.

Skip holds a PhD Economics from the University of Virginia, as well as, a Masters of Science

and Bachelor of Science also in Economics from the University of Wyoming.

© Wood Mackenzie 21

Delivering commercial insight

www.woodmac.com

Wood Mackenzie Disclaimer

This presentation has been prepared by Wood Mackenzie Inc for delivery at the PlattsBunker Fuel Conference in Houston in June 2011. It has not been prepared for the benefit of any particular attendee and may not be relied upon by any attendee or other third party. If, notwithstanding the foregoing, this presentation is relied upon by any person, Wood Mackenzie Inc does not accept, and disclaims, all liability for loss and damage suffered as a result.

The information contained in these slides may be retained by attendees. However, these slides and the contents of this presentation may not be disclosed to any other person or published by any means without Wood Mackenzie Inc's prior written permission.

© Wood Mackenzie 22

Delivering commercial insight

www.woodmac.com

Wood Mackenzie

Kintore House

74-77 Queen Street

Edinburgh EH2 4NS

Global Contact Details

Europe +44 (0)131 243 4400

Americas +1 713 470 1600

Asia Pacific +65 6518 0800

Email [email protected]

Global Offices

Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States

Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better

business decisions. For more information visit: www.woodmac.com