BULLETIN OF MONETARY ECONOMICS AND BANKING · Early Warning System and Currency Volatility...

133

Transcript of BULLETIN OF MONETARY ECONOMICS AND BANKING · Early Warning System and Currency Volatility...

BULLETIN OF MONETARY ECONOMICS AND BANKINGCentral Banking Research Department

Bank Indonesia

PatronBoard of Governors

Board of Editor

Prof. Dr. Anwar NasutionProf. Dr. Miranda S. Goeltom

Prof. Dr. InsukindroProf. Dr. Iwan Jaya Azis

Prof. Iftekhar HasanProf. Dr. Masaaki Komatsu

Dr. M. SyamsuddinDr. Perry Warjiyo

Dr. Iskandar Simorangkir Dr. Solikin M. JuhroDr. Haris Munandar

Dr. M. Edhie PurnawanDr. Burhanuddin Abdullah

Dr. Andi M. Alfian Parewangi

Editorial ChairmanDr. Perry Warjiyo

Managing EditorDr. Darsono

Dr. Siti AstiyahDr. Andi M. Alfian Parewangi

SecretariatIr. Triatmo Doriyanto, M.S

Nurhemi, S.E., M.ATri Subandoro, S.E

This bulletin is published by Bank Indonesia, Central Banking Research Department. Contents and results research in the writings in this bulletin entirely the responsibility of the authors and not an official view of Bank Indonesia.

We invite all parties to write in this bulletin paper delivered in the form files to Central Banking Research Department, Bank Indonesia, Tower Sjafruddin Prawiranegara Floor 21; Jl. M.H. Thamrin No. 2, Central Jakarta, email: [email protected].

The Bulletin is published quarterly in April, July, October and January,

Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia:

Quarter III, 2016

TM. Arief Machmud, Syachman Perdymer, Muslimin Anwar,

Nurkholisoh Ibnu Aman, Tri Kurnia Ayu K,

Anggita Cinditya Mutiara K, Illinia Ayudhia Riyadi

Early Warning System and Currency Volatility Management In Emerging Market

Natasia Engeline S, Salomo Posmauli Matondang

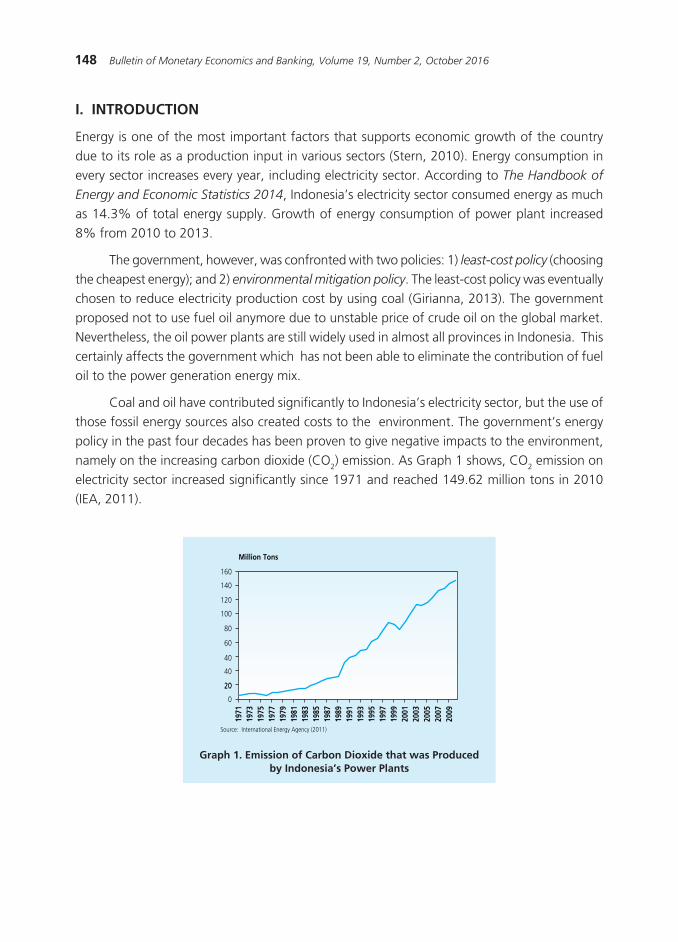

The Impact of Geothermal Energy Sector Development on Electricity Sector

In Indonesia Economy

Nayasari Aissa, Djoni Hartono

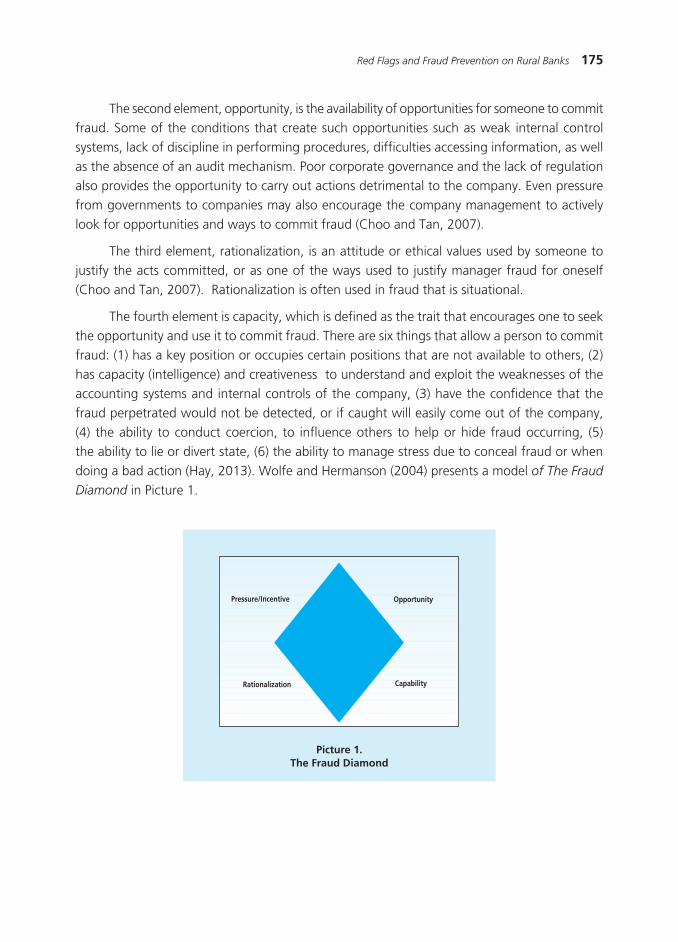

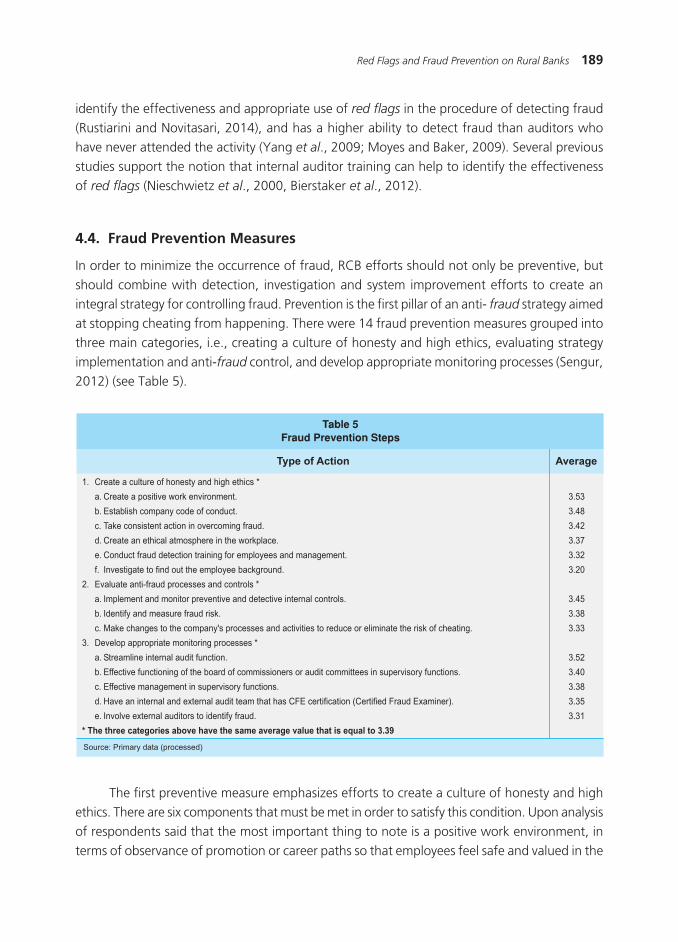

Red Flags and Fraud Prevention on Rural Banks

Ni Wayan Rustiarini, Ni Nyoman Ayu Suryandari, I Kadek Satria Nova

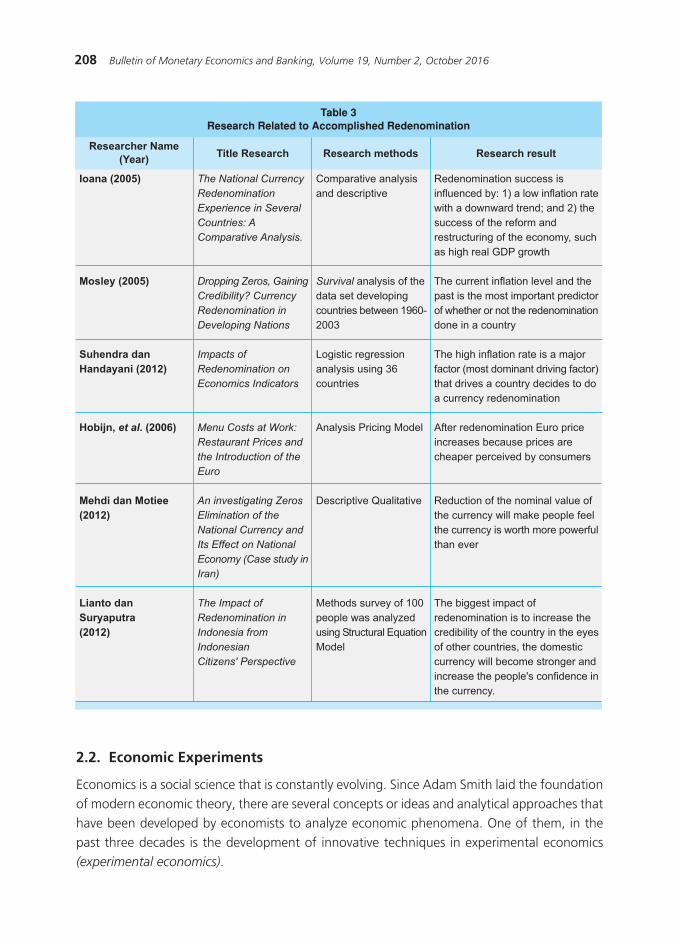

Impact of Redenomination on Price, Volume, and Value of Transaction:

An Experimental Economic Approach

Danti Astrini, Bambang Juanda, Noer Azam Achsani

Volume 19, Number 2, October 2016

123

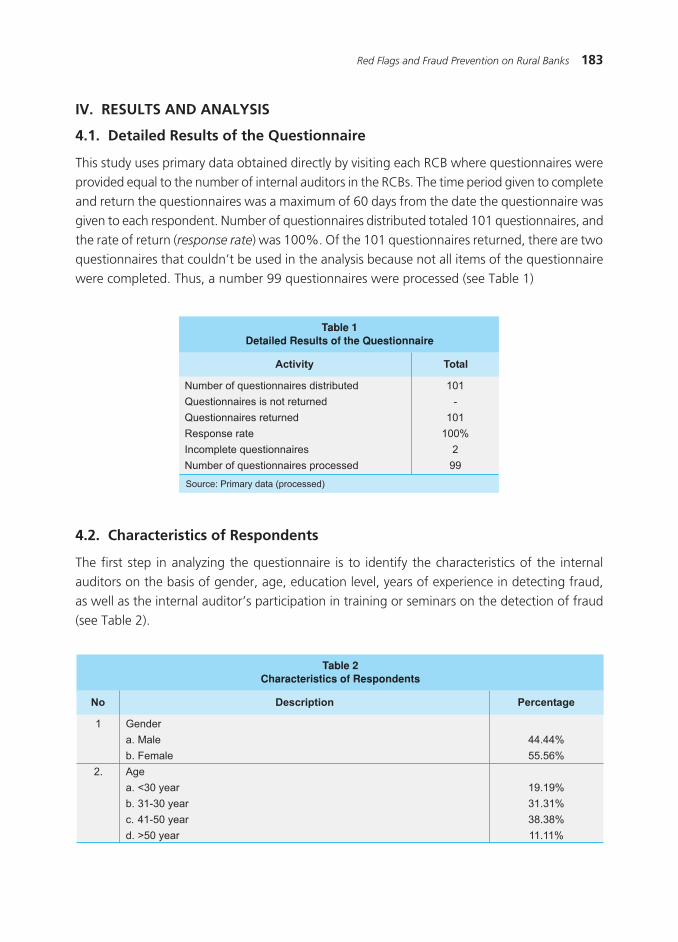

171

103

147

199

BULLETIN of moNETary EcoNomIcsaNd BaNkINg

This page intentionally left blank

103Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

TM. Arief Machmud, Syachman Perdymer, Muslimin Anwar, Nurkholisoh Ibnu Aman, Tri Kurnia Ayu K,

Anggita Cinditya Mutiara K, Illinia Ayudhia Riyadi1

1 Authors are researcher on Monetary and Economic Policy Department (DKEM). TM_Arief Machmud ([email protected]); Syachman Perdymer ([email protected]); Muslimin AAnwar ([email protected]); Nurkholisoh Ibnu Aman ([email protected]); Tri Kurnia Ayu K ([email protected]); Anggita Cinditya Mutiara K ([email protected]); Illinia Ayudhia Riyadi ([email protected]).

The growth of Indonesian economy on Quarter III, 2016 recorded positive growth with a well-

maintained financial system and macroeconomic stability. The economy grew moderately supported

by remaining strong domestic demand amidst the slow recovery of the global economy. The economic

stability is also good reflected on the low inflation, decreasing current account deficit, and relatively

stable exchange rate. An increase of domestic economy and lower global financial risk enable monetary

ease on Quarter III, 2016. Furthermore, the reduction of interest rate policy is well transmitted and is

expected to strengthen the growth momentum of the economy. Looking forward, Bank Indonesia will

keep strengthening his policy mix and macroprudential, and his coordination with the government to

ensure the inflation control, greater stimulus for growth, and the implementation of structural reform

run on the right track, and hence preserve the sustainable economic development.

Abstract

Keywords: Macroeconomy, Monetary, Economic Outlook

JEL Classification: C53, E66, F01, F41

QUARTERLY OUTLOOK ON MONETARY,BANKING, AND PAYMENT SYSTEM IN INDONESIA:

QUARTER III, 2016

104 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

I. GLOBAL DEVELOPMENT

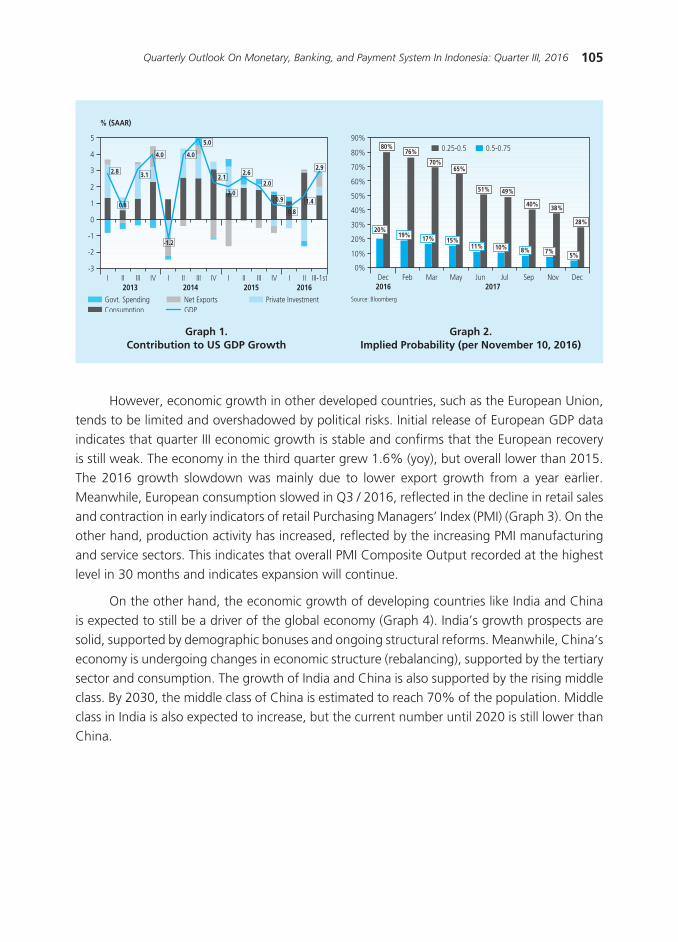

The global economic recovery is expected to be slow, but commodity prices are starting to improve. Amid rising global economic uncertainty following the US election, the US economy showed improvements as reflected by improved GDP, stable unemployment rates and rising inflation. In line with these developments, the chances of a Fed Fund Rate increase (FFR) in December 2016 are getting stronger. However, economic growth in other developed countries, such as the European Union, tends to be limited and overshadowed by political risks. On the other hand, the economic growth of developing countries such as India and China is expected to still be a driver of the global economy. In commodity markets, world oil prices are still at a low level, in line with OPEC’s high oil production. Meanwhile, some of Indonesia’s export commodity prices continue to improve, such as palm oil, coal, and some other mining goods. Going forward, Bank Indonesia will keep a close watch on developments in the transitional period of US government and the policies to be pursued in the US, in particular with regard to fiscal policy, interest rates and international trade.

The US economy is showing better progress. US economic growth in Q3 / 2016 reached 2.9% (SAAR), driven mainly by increased export growth and greater investment from lower consumption growth (Graph 1). Increased US exports, driven mainly by increased exports of soybeans. Meanwhile, investment growth was mainly driven by improvements in non-farm inventories. In terms of labor, the improvement in the US economy was reflected in stable unemployment rates, at 4.9%, in the period from June to September 2016. Meanwhile, the increase in non-farm payroll (NFP) employment in September was 191,000, higher than month previous. The improving US economy is also reflected in rising inflation. The inflation of Personal Consumption Expenditures (PCE) and Consumer Price Index (CPI) in September 2016 increased, mainly contributed by the core group and the shrinking contraction of the energy group. PCE inflation in September 2016 was 1.2% (yoy), up from the previous month at 1% (yoy). Meanwhile, September 2016 CPI inflation stood at 1.5% (yoy).

In line with these developments, the Fed Fund Rate (FFR) rate increase in December 2016 is getting stronger (Graph 2). An increase in FFR is expected to occur on the Federal Open Market Committee (FOMC) on 13-14 December 2016, taking into account developments such as rising inflation, improved GDP (GDP), and stable labor. Market participants confidence over the FFR increase in December 2016 is reflected in implied probability of FFR reaching 80 percent.

105Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

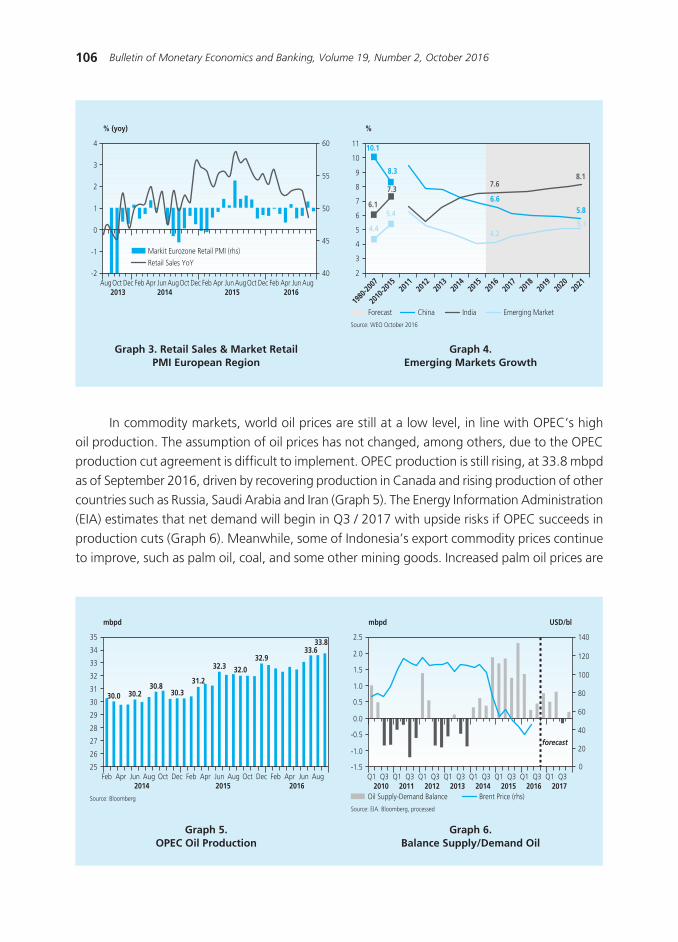

However, economic growth in other developed countries, such as the European Union, tends to be limited and overshadowed by political risks. Initial release of European GDP data indicates that quarter III economic growth is stable and confirms that the European recovery is still weak. The economy in the third quarter grew 1.6% (yoy), but overall lower than 2015. The 2016 growth slowdown was mainly due to lower export growth from a year earlier. Meanwhile, European consumption slowed in Q3 / 2016, reflected in the decline in retail sales and contraction in early indicators of retail Purchasing Managers’ Index (PMI) (Graph 3). On the other hand, production activity has increased, reflected by the increasing PMI manufacturing and service sectors. This indicates that overall PMI Composite Output recorded at the highest level in 30 months and indicates expansion will continue.

On the other hand, the economic growth of developing countries like India and China is expected to still be a driver of the global economy (Graph 4). India’s growth prospects are solid, supported by demographic bonuses and ongoing structural reforms. Meanwhile, China’s economy is undergoing changes in economic structure (rebalancing), supported by the tertiary sector and consumption. The growth of India and China is also supported by the rising middle class. By 2030, the middle class of China is estimated to reach 70% of the population. Middle class in India is also expected to increase, but the current number until 2020 is still lower than China.

Graph 1.Contribution to US GDP Growth

Graph 2.Implied Probability (per November 10, 2016)

2.8

0.8

3.1

-1.2

4.0 4.0

2.1

2.0

2.6

2.0

0.9

0.8

1.4

2.9

5.0

Govt. SpendingConsumption

Net ExportsGDP

Private Investment

��

���

���

���

���

���

���

���

���

���

��� ��� �� ��� � �� ��� ��� ������� ����

�������� ��������

������ ��� ���

��� ��� �� ����

������

������

��� ���

��� ���

���

�� ����������� �

106 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

In commodity markets, world oil prices are still at a low level, in line with OPEC’s high oil production. The assumption of oil prices has not changed, among others, due to the OPEC production cut agreement is difficult to implement. OPEC production is still rising, at 33.8 mbpd as of September 2016, driven by recovering production in Canada and rising production of other countries such as Russia, Saudi Arabia and Iran (Graph 5). The Energy Information Administration (EIA) estimates that net demand will begin in Q3 / 2017 with upside risks if OPEC succeeds in production cuts (Graph 6). Meanwhile, some of Indonesia’s export commodity prices continue to improve, such as palm oil, coal, and some other mining goods. Increased palm oil prices are

Graph 3. Retail Sales & Market RetailPMI European Region

Graph 5.OPEC Oil Production

Graph 4.Emerging Markets Growth

Graph 6.Balance Supply/Demand Oil

�������

��

��

�

�

�

�

� ��

��

��

��

�������� ��� ��� � � �������� ��� ��� � � �������� ��� ��� � � �����

���� ���� ���� ����

���������������������������� ���������������

�������

��

�������

������

����

����

����

����

����

����

����

����

����

����

�

�

�

�

�

�

�

�

�

��

�� ����

���

���

������

���

���

���

���

���

���

���

�������� ��� ��� ��������������

������������������������

����

��

��

��

��

��

��

��

��

��

��

��

���� ��������

��������

���� ��������

��������

��� ��� �� ��� � �� ��� ��� �� ��� � �� ��� ��� �� ������� ���� ����

����������������

���

���

���

���

���

���

����

����

����

���� ������

�

���

���

���

��

��

��

��

�� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ������ ���� ���� ���� ���� ���� ���� ����

��������

��������� ����������� �����������������

��������� ���������������������

107Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

driven by production still disturbed due to El Nino (dry drought) and La Nina (wet drought). On the other hand, coal prices also increased due to increased demand for Chinese coal as steel production increased.

II. MACRO ECONOMIC DYNAMICS OF INDONESIA

2.1. Economic Growth

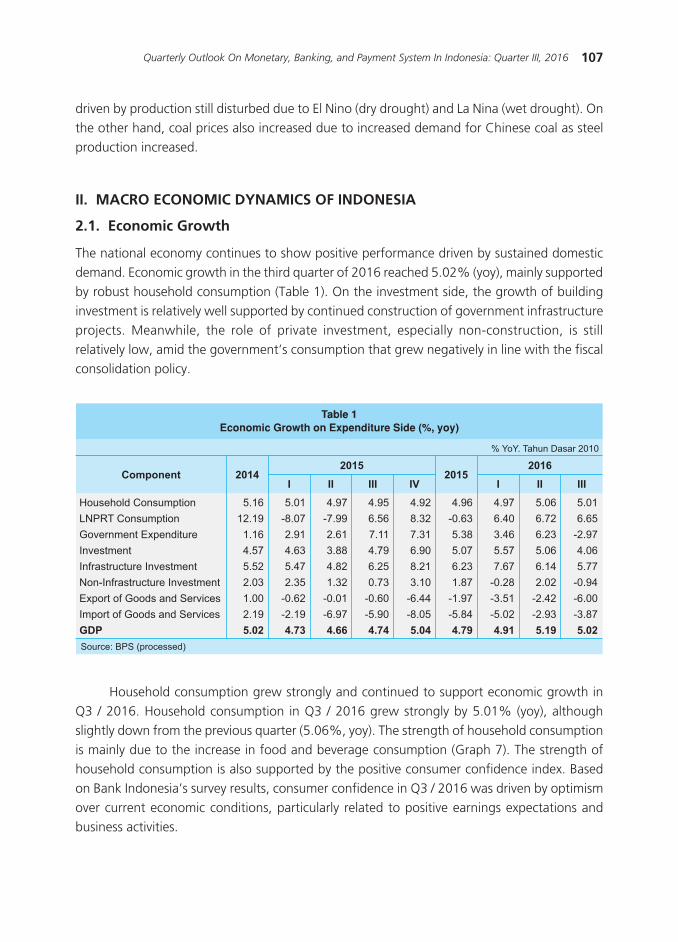

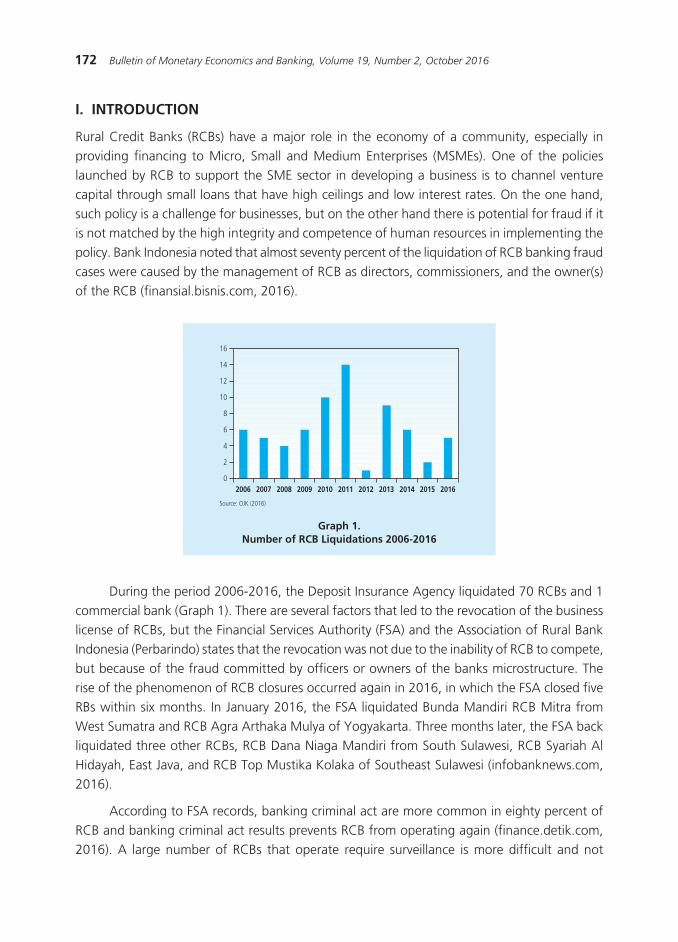

The national economy continues to show positive performance driven by sustained domestic demand. Economic growth in the third quarter of 2016 reached 5.02% (yoy), mainly supported by robust household consumption (Table 1). On the investment side, the growth of building investment is relatively well supported by continued construction of government infrastructure projects. Meanwhile, the role of private investment, especially non-construction, is still relatively low, amid the government’s consumption that grew negatively in line with the fiscal consolidation policy.

��������������������������� ���������������������

����

�����������������������

�������� ����

� �� ��� �� � �� ������������

���������� �������������� ����������������������������������������������������������������������������������������������������������������������������������������

�� �� � � ������������ ����� �� ��

��� �������� ������������������ �� ��

����������� �������� ������� ����� ��

�������� ��������������������� ��

����������� ������ �� ����������� ��

������������������ ���� ��������� �

�������������������������� ������ �

������������� ���������������� �

��� ����������������������������� ��

��������������������� �

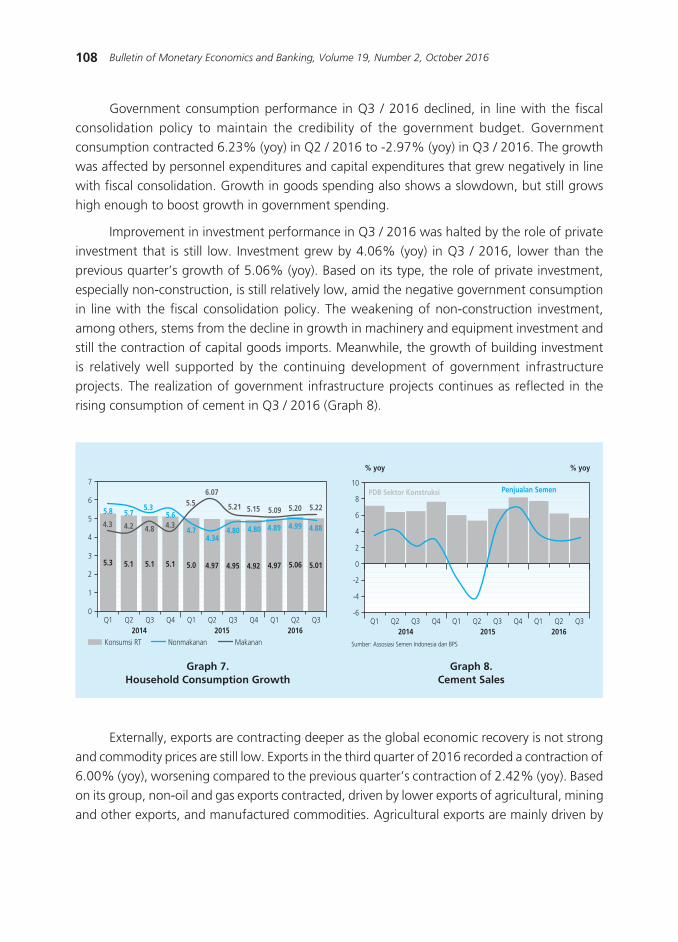

Household consumption grew strongly and continued to support economic growth in Q3 / 2016. Household consumption in Q3 / 2016 grew strongly by 5.01% (yoy), although slightly down from the previous quarter (5.06%, yoy). The strength of household consumption is mainly due to the increase in food and beverage consumption (Graph 7). The strength of household consumption is also supported by the positive consumer confidence index. Based on Bank Indonesia’s survey results, consumer confidence in Q3 / 2016 was driven by optimism over current economic conditions, particularly related to positive earnings expectations and business activities.

108 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

Graph 7.Household Consumption Growth

Graph 8.Cement Sales

Government consumption performance in Q3 / 2016 declined, in line with the fiscal consolidation policy to maintain the credibility of the government budget. Government consumption contracted 6.23% (yoy) in Q2 / 2016 to -2.97% (yoy) in Q3 / 2016. The growth was affected by personnel expenditures and capital expenditures that grew negatively in line with fiscal consolidation. Growth in goods spending also shows a slowdown, but still grows high enough to boost growth in government spending.

Improvement in investment performance in Q3 / 2016 was halted by the role of private investment that is still low. Investment grew by 4.06% (yoy) in Q3 / 2016, lower than the previous quarter’s growth of 5.06% (yoy). Based on its type, the role of private investment, especially non-construction, is still relatively low, amid the negative government consumption in line with the fiscal consolidation policy. The weakening of non-construction investment, among others, stems from the decline in growth in machinery and equipment investment and still the contraction of capital goods imports. Meanwhile, the growth of building investment is relatively well supported by the continuing development of government infrastructure projects. The realization of government infrastructure projects continues as reflected in the rising consumption of cement in Q3 / 2016 (Graph 8).

��� ������

���

�������

���� ���� ���� ���� ������� ��� ��� ���

�������

���� ���� ���� ���� ����

��� ��� ��� ��� ��� ���� ���� ���� ���� ���� ����

�

�

�

�

�

�

�

��� �� ���� �� �� �� �� �� �� ��

���� ���� �������������� ��������� �����

��������������������� ������������ ��

����� �����

��

�

�

�

�

�

��

��

���� �� �� �� �� �� �� �� �� �� ��

�� �� ��

��������� � � ����������� �������

Externally, exports are contracting deeper as the global economic recovery is not strong and commodity prices are still low. Exports in the third quarter of 2016 recorded a contraction of 6.00% (yoy), worsening compared to the previous quarter’s contraction of 2.42% (yoy). Based on its group, non-oil and gas exports contracted, driven by lower exports of agricultural, mining and other exports, and manufactured commodities. Agricultural exports are mainly driven by

109Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

contraction in food exports, especially CPO. Meanwhile, manufacturing exports also contracted due to sharp contraction in clothing exports along with declining exports to America. From the oil and gas group, export contraction is influenced by the policy to meet domestic gas needs.

In line with weakening exports and domestic demand, imports also contracted in Q3 / 2016. Imports contracted by 3.87% (yoy) in Q3 / 2016, larger than the previous quarter which contracted 2.93% (yoy). The import contraction was mainly due to the contraction of non-oil and gas imports. Based on the group, the weakening performance of non-oil and gas imports was mainly driven by the contraction in imports of capital goods, especially in the capital goods category, except for transportation equipment.

From the sectoral side, the industrial, agricultural and trade sectors are still growing positively. The industrial sector is still growing positively as reflected by the PMI indicator that is still at expansion level. The positive industrial sector is sourced from food and beverages sub-sector which is performing better performance driven by increasing number of tourists. Meanwhile, the mining sector grew positively for the first time since 2015 with an increase in the performance of the metal ore subsector as an improvement motor. The transportation and communications information sector also grew better than the previous quarter driven by the air transport subsector, along with the addition of new domestic and international flight routes.

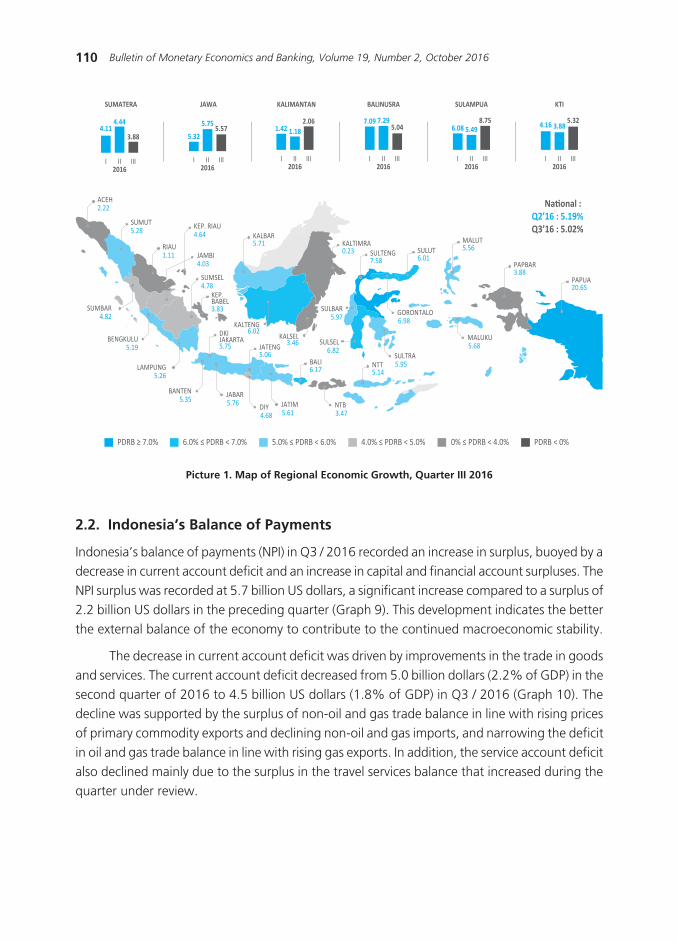

Spatially, economic growth in Java and Sumatra is still growing strongly, accompanied by increasing economic growth in Kawasan Timur Indonesia (KTI), in line with increasing mining exports and smelters of mining products (Picture 1). The strong economic growth in Java has resulted from increased agricultural performance in line with the harvest of several food commodities in West Java and Central Java. The economy of Sumatra is still strong enough to be driven by higher growth of manufacturing and trading industry sectors. The growth in the performance of the manufacturing industry is reflected in an upward trend in export sales growth, although the main export commodity prices of Sumatra-based natural resources are still retained. Meanwhile, KTI’s economic growth is driven by increased agricultural, mining and construction sectors. Increased KTI agricultural sector, among others, comes from increased cocoa exports in Southeast Sulawesi and CPO production after El Nino impact loss occurred in 2015. On the other hand, mining sector performance in KTI again grew positively after having posted negative growth in the previous quarter. The improvement in mining performance in KTI mainly occurs in Kalimantan and Papua due to the increase of global demand for coal as domestic supply decreases in China. In addition, the performance of copper mineral mining in Papua increased following the improvement of production machinery, so that producers optimized production to pursue their export targets and quotas.

110 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

2.2. Indonesia’s Balance of Payments

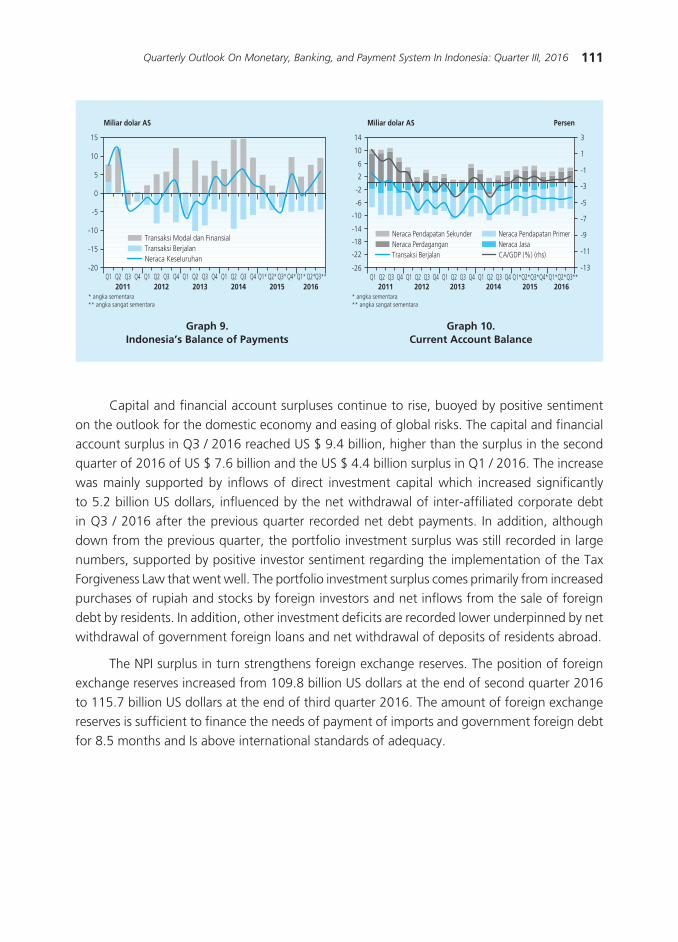

Indonesia’s balance of payments (NPI) in Q3 / 2016 recorded an increase in surplus, buoyed by a decrease in current account deficit and an increase in capital and financial account surpluses. The NPI surplus was recorded at 5.7 billion US dollars, a significant increase compared to a surplus of 2.2 billion US dollars in the preceding quarter (Graph 9). This development indicates the better the external balance of the economy to contribute to the continued macroeconomic stability.

The decrease in current account deficit was driven by improvements in the trade in goods and services. The current account deficit decreased from 5.0 billion dollars (2.2% of GDP) in the second quarter of 2016 to 4.5 billion US dollars (1.8% of GDP) in Q3 / 2016 (Graph 10). The decline was supported by the surplus of non-oil and gas trade balance in line with rising prices of primary commodity exports and declining non-oil and gas imports, and narrowing the deficit in oil and gas trade balance in line with rising gas exports. In addition, the service account deficit also declined mainly due to the surplus in the travel services balance that increased during the quarter under review.

Picture 1. Map of Regional Economic Growth, Quarter III 2016

PDRB ≥ 7.0% 5.0% ≤ PDRB < 6.0% 4.0% ≤ PDRB < 5.0% PDRB < 0%6.0% ≤ PDRB < 7.0% 0% ≤ PDRB < 4.0%

ACEH2.22

SUMUT5.28

RIAU1.11

KEP. BABEL3.83

DKI JAKARTA5.75 JATENG

5.06

SULTENG7.58

KALTIMRA0.23

KALBAR5.71

SULUT6.01

MALUT5.56

PAPBAR3.88

PAPUA20.65

BALI6.17 NTT

5.14

KEP. RIAU4.64

LAMPUNG5.26

BENGKULU5.19

BANTEN5.35

SULSEL6.82

SULBAR5.97

JABAR5.76 JATIM

5.61NTB3.47

KALTENG6.02

KALSEL3.46

GORONTALO6.98

MALUKU5.68

SULTRA5.95

SUMSEL4.78

JAMBI4.03

National : Q2’16 : 5.19%Q3’16 : 5.02%

DIY4.68

SUMBAR4.82

KALIMANTAN

I II III2016

1.42 1.182.06

BALINUSRA

I II III2016

7.09 7.295.04

SULAMPUA

I II III2016

6.08 5.498.75

KTI

I II III2016

4.16 3.885.32

JAWA

I II III2016

5.32

5.75 5.57

SUMATERA

I II III2016

4.114.44

3.88

111Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

Graph 9.Indonesia’s Balance of Payments

Graph 10.Current Account Balance

Capital and financial account surpluses continue to rise, buoyed by positive sentiment on the outlook for the domestic economy and easing of global risks. The capital and financial account surplus in Q3 / 2016 reached US $ 9.4 billion, higher than the surplus in the second quarter of 2016 of US $ 7.6 billion and the US $ 4.4 billion surplus in Q1 / 2016. The increase was mainly supported by inflows of direct investment capital which increased significantly to 5.2 billion US dollars, influenced by the net withdrawal of inter-affiliated corporate debt in Q3 / 2016 after the previous quarter recorded net debt payments. In addition, although down from the previous quarter, the portfolio investment surplus was still recorded in large numbers, supported by positive investor sentiment regarding the implementation of the Tax Forgiveness Law that went well. The portfolio investment surplus comes primarily from increased purchases of rupiah and stocks by foreign investors and net inflows from the sale of foreign debt by residents. In addition, other investment deficits are recorded lower underpinned by net withdrawal of government foreign loans and net withdrawal of deposits of residents abroad.

The NPI surplus in turn strengthens foreign exchange reserves. The position of foreign exchange reserves increased from 109.8 billion US dollars at the end of second quarter 2016 to 115.7 billion US dollars at the end of third quarter 2016. The amount of foreign exchange reserves is sufficient to finance the needs of payment of imports and government foreign debt for 8.5 months and Is above international standards of adequacy.

���

���

���

��

�

�

��

��

�� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��� ������������ ����������� ���� ���� ���� ���� ����

����������� ���������������������������������������������������

���������������

������������������������������������������

�� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �������������������������� ���� ���� ���� ���� ����

��

��

�

�

��

��

���

���

���

���

���

�

�

��

��

��

��

��

���

���

��������������� � �� �

������ �������� ������������� ������������������� ��������

������ �������� ������������ ����� ��� ��� �����

� ����� ����������� ����� ������ ���������

112 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

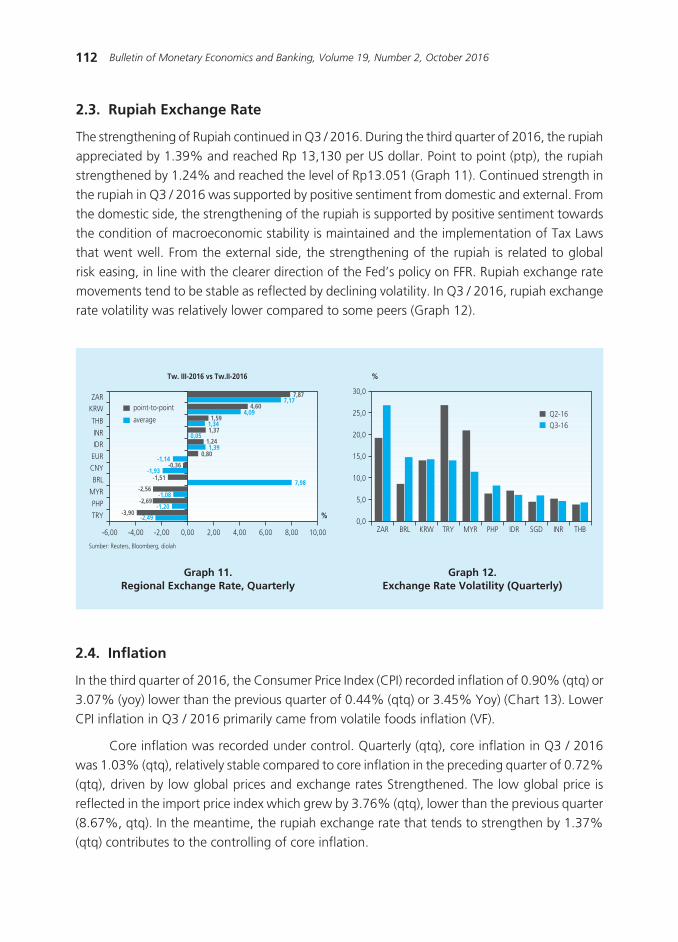

2.3. Rupiah Exchange Rate

The strengthening of Rupiah continued in Q3 / 2016. During the third quarter of 2016, the rupiah appreciated by 1.39% and reached Rp 13,130 per US dollar. Point to point (ptp), the rupiah strengthened by 1.24% and reached the level of Rp13.051 (Graph 11). Continued strength in the rupiah in Q3 / 2016 was supported by positive sentiment from domestic and external. From the domestic side, the strengthening of the rupiah is supported by positive sentiment towards the condition of macroeconomic stability is maintained and the implementation of Tax Laws that went well. From the external side, the strengthening of the rupiah is related to global risk easing, in line with the clearer direction of the Fed’s policy on FFR. Rupiah exchange rate movements tend to be stable as reflected by declining volatility. In Q3 / 2016, rupiah exchange rate volatility was relatively lower compared to some peers (Graph 12).

Graph 11.Regional Exchange Rate, Quarterly

Graph 12.Exchange Rate Volatility (Quarterly)

����

����

����

����

����

����

����

����

����

����

����

����

����������

����������

����������

����������

����������

��������������

�������

������

�� ���������� ��

���������

����� ����� ����� ���� ���� ���� ���� ���� �����

�

� ������� ������ ���������������

������������� ������������

����

����

����

����

����

���

���

�

����������

��� ��� ��� ��� �� ��� � �� �� ���

2.4. Inflation

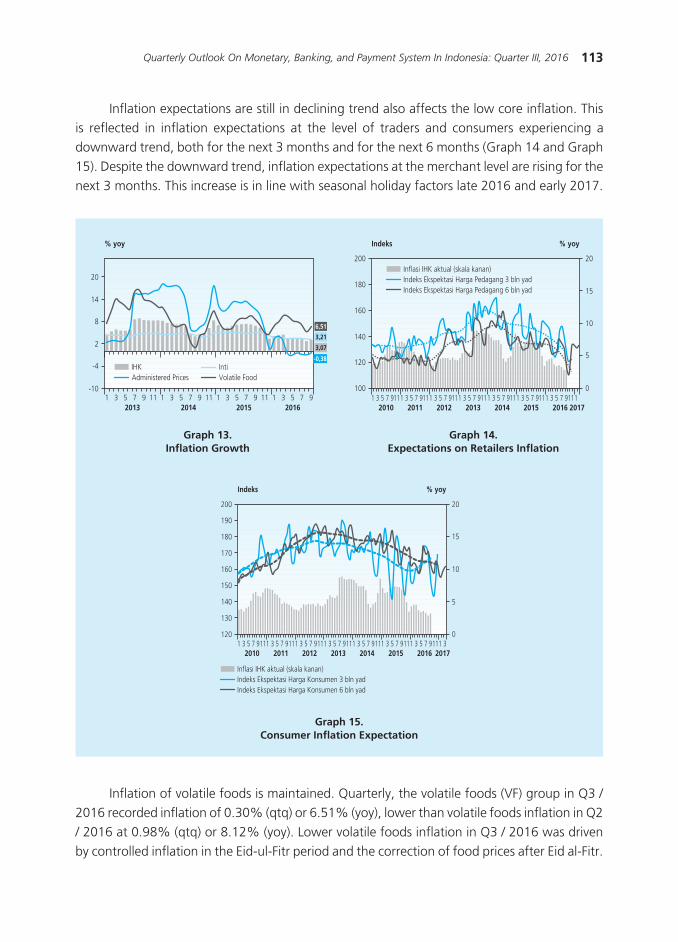

In the third quarter of 2016, the Consumer Price Index (CPI) recorded inflation of 0.90% (qtq) or 3.07% (yoy) lower than the previous quarter of 0.44% (qtq) or 3.45% Yoy) (Chart 13). Lower CPI inflation in Q3 / 2016 primarily came from volatile foods inflation (VF).

Core inflation was recorded under control. Quarterly (qtq), core inflation in Q3 / 2016 was 1.03% (qtq), relatively stable compared to core inflation in the preceding quarter of 0.72% (qtq), driven by low global prices and exchange rates Strengthened. The low global price is reflected in the import price index which grew by 3.76% (qtq), lower than the previous quarter (8.67%, qtq). In the meantime, the rupiah exchange rate that tends to strengthen by 1.37% (qtq) contributes to the controlling of core inflation.

113Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

Inflation expectations are still in declining trend also affects the low core inflation. This is reflected in inflation expectations at the level of traders and consumers experiencing a downward trend, both for the next 3 months and for the next 6 months (Graph 14 and Graph 15). Despite the downward trend, inflation expectations at the merchant level are rising for the next 3 months. This increase is in line with seasonal holiday factors late 2016 and early 2017.

Graph 13.Inflation Growth

Graph 14.Expectations on Retailers Inflation

Graph 15.Consumer Inflation Expectation

� � � � � �� � � � � � �� � � � � � �� � � � � ����� ���� ���� ����

���

��

�

�

��

��

�����

��� ������ ������������� ������������

����

����

����

�����

���

���

���

���

���

���

������

��

��

��

�

�

�����

� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� � � � �������� ���� ���� ���� ���� ���� ���� ����

��������� ������������������������������������� ���������������������������������������� �����������������������

���

���

���

���

���

���

���

���

���

��

��

��

�

�� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� �

���� ���� ���� ���� ���� ���� ���� ����

��������� ������������������������������������� ��������������������������������������� ����������������������

������ �����

Inflation of volatile foods is maintained. Quarterly, the volatile foods (VF) group in Q3 / 2016 recorded inflation of 0.30% (qtq) or 6.51% (yoy), lower than volatile foods inflation in Q2 / 2016 at 0.98% (qtq) or 8.12% (yoy). Lower volatile foods inflation in Q3 / 2016 was driven by controlled inflation in the Eid-ul-Fitr period and the correction of food prices after Eid al-Fitr.

114 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

Administered Prices Group (AP) in Q3 / 2016 recorded inflation, after two previous quarterly deflation. AP inflation was recorded at 0.93% (qtq) or an annual deflation of 0.38% (yoy), higher than the second quarter of 2016 which recorded a deflation of 0.73% (qtq) or 0.50% (yoy). Inflation in the AP group was mainly driven by the rise in electricity, cigarette and drinking water tariffs. Meanwhile, deflation occurred in inter-city transportation tariff and sea freight driven by post-Eid al-Fitr correction.

III. MONETARY DEVELOPMENT, BANKING AND PAYMENT SYSTEM

3.1. Monetary

Transmission of monetary policy easing through the interest rate channel continued in Q3 / 2016. Bank Indonesia lowered the BI 7-day Reverse Repo Rate (BI 7-day RR Rate) in September 2016 by 25 bps to 5.00%, followed by lower interest rates Deposit Facility (DF) to 4.25% and Lending Facility (LF) to 5.75%. The decline was followed by a decrease in the overnight interbank rate in both the O / N tenor and the longer tenor.

Liquidity conditions in the money market remain intact, despite pressure. The overnight interbank rates in Q3 / 2016 fell from 4.88% in Q2 / 2016 to 4.76% in Q3 / 2016. BI 7-day RR Rate Implementation replaced the BI Rate on August 19, 2016 and the policy of interest rate reduction The September 2016 policy also helped to push down the short tenor interest rate. However, the decline was not followed by the tenor of PUAB over 1 month which tended to increase. The condition of liquidity slightly under pressure in Q3 / 2016 was reflected in the average volume of overnight interbank money market and Deposit Facility (DF) which fell to Rp7.56 trillion and Rp63.7 trillion from the previous quarter Rp8.06 trillion and Rp64, 01 trillion. On the other hand, the average spread on overnight inter-market P / A interest rates increased from 23 bps in Q2 / 2016 to 32 bps in Q3 / 2016. The increase in the overnight interbank spread was influenced by the government’s lack of optimum spending, while the contraction of the Government continued to increase Related to tax revenue in line with the deadline for the implementation of the Phase I Amnesty program on September 30, 2016.

In line with the stance of monetary policy easing, bank deposit rates fell. Compared to second quarter of 2016, the weighted average (RRT) of deposit rates in Q3 / 2016 fell by 8 bps to 6.86%. Thus, on a year-to-date basis (ytd), the weighted average of time deposit rates in Q3 / 2016 had dropped by 108 bps. The decline in deposit rates occurred in all tenors. The biggest decline occurred in the 24-month tenor, which decreased by 148 bps (qtq) to 7.68% followed by the 6-month tenor, which fell by 43 bps (qtq) to 7.31%. The smallest decline occurred in short tenor 3 and 12 months which only decreased by 16 bps (qtq) to 6.84% and 7.60% respectively.

In line with the deposit interest rate, bank lending rates in Q3 / 2016 also fell. Compared to second quarter 2016, lending rates in quarter III 2016 fell by 15 bps to 12.23%. Year to date

115Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

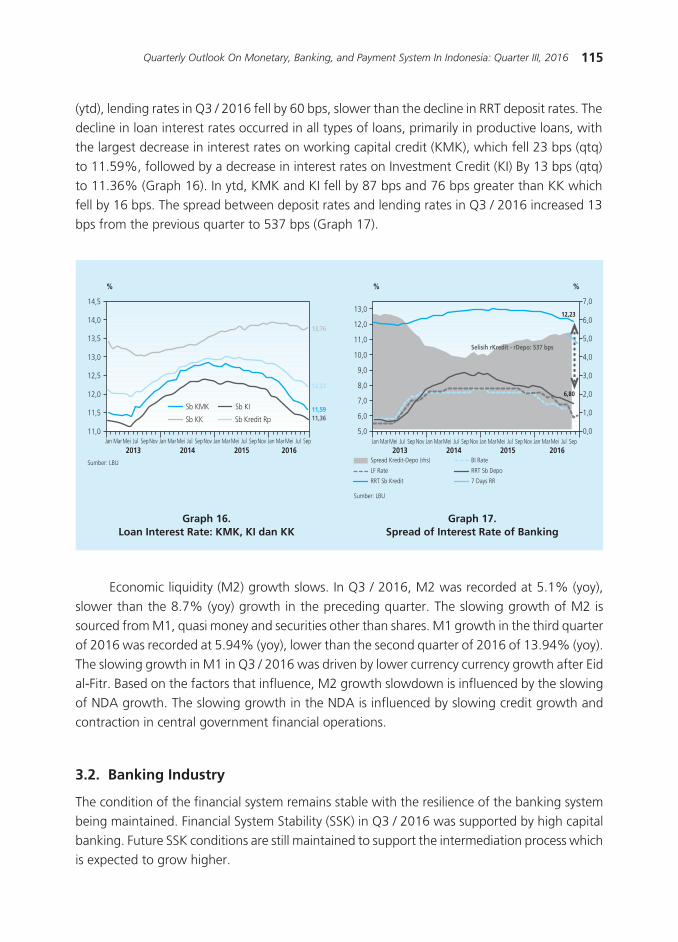

(ytd), lending rates in Q3 / 2016 fell by 60 bps, slower than the decline in RRT deposit rates. The decline in loan interest rates occurred in all types of loans, primarily in productive loans, with the largest decrease in interest rates on working capital credit (KMK), which fell 23 bps (qtq) to 11.59%, followed by a decrease in interest rates on Investment Credit (KI) By 13 bps (qtq) to 11.36% (Graph 16). In ytd, KMK and KI fell by 87 bps and 76 bps greater than KK which fell by 16 bps. The spread between deposit rates and lending rates in Q3 / 2016 increased 13 bps from the previous quarter to 537 bps (Graph 17).

Graph 16.Loan Interest Rate: KMK, KI dan KK

Graph 17.Spread of Interest Rate of Banking

����

����

����

����

����

����

����

����

�

�����

�����

����������

��� ������ ��� ��� �� ��� ������ ��� ��� �� ��� ������ ��� ��� �� ��� ������ ��� ������� ���� ���� ����

���������

����� ����

���� �����������

����

����

����

����

���

���

���

���

���

� �

���

���

���

���

���

���

���

������ ������ � � ���� ��� ������ � � ���� ��� ������ � � ���� ��� ������ � � ��

�������� ���� ����

�������������� ��������������

�����

����

����������������������

��� ���

�� ���

��������

����������� �������

� ��������

Economic liquidity (M2) growth slows. In Q3 / 2016, M2 was recorded at 5.1% (yoy), slower than the 8.7% (yoy) growth in the preceding quarter. The slowing growth of M2 is sourced from M1, quasi money and securities other than shares. M1 growth in the third quarter of 2016 was recorded at 5.94% (yoy), lower than the second quarter of 2016 of 13.94% (yoy). The slowing growth in M1 in Q3 / 2016 was driven by lower currency currency growth after Eid al-Fitr. Based on the factors that influence, M2 growth slowdown is influenced by the slowing of NDA growth. The slowing growth in the NDA is influenced by slowing credit growth and contraction in central government financial operations.

3.2. Banking Industry

The condition of the financial system remains stable with the resilience of the banking system being maintained. Financial System Stability (SSK) in Q3 / 2016 was supported by high capital banking. Future SSK conditions are still maintained to support the intermediation process which is expected to grow higher.

116 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

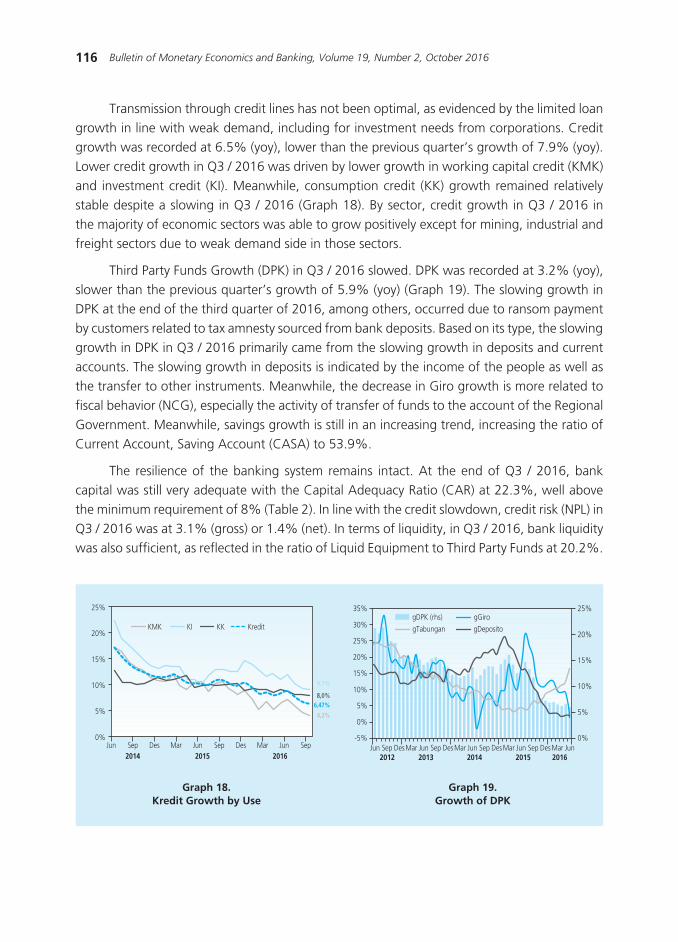

Transmission through credit lines has not been optimal, as evidenced by the limited loan growth in line with weak demand, including for investment needs from corporations. Credit growth was recorded at 6.5% (yoy), lower than the previous quarter’s growth of 7.9% (yoy). Lower credit growth in Q3 / 2016 was driven by lower growth in working capital credit (KMK) and investment credit (KI). Meanwhile, consumption credit (KK) growth remained relatively stable despite a slowing in Q3 / 2016 (Graph 18). By sector, credit growth in Q3 / 2016 in the majority of economic sectors was able to grow positively except for mining, industrial and freight sectors due to weak demand side in those sectors.

Third Party Funds Growth (DPK) in Q3 / 2016 slowed. DPK was recorded at 3.2% (yoy), slower than the previous quarter’s growth of 5.9% (yoy) (Graph 19). The slowing growth in DPK at the end of the third quarter of 2016, among others, occurred due to ransom payment by customers related to tax amnesty sourced from bank deposits. Based on its type, the slowing growth in DPK in Q3 / 2016 primarily came from the slowing growth in deposits and current accounts. The slowing growth in deposits is indicated by the income of the people as well as the transfer to other instruments. Meanwhile, the decrease in Giro growth is more related to fiscal behavior (NCG), especially the activity of transfer of funds to the account of the Regional Government. Meanwhile, savings growth is still in an increasing trend, increasing the ratio of Current Account, Saving Account (CASA) to 53.9%.

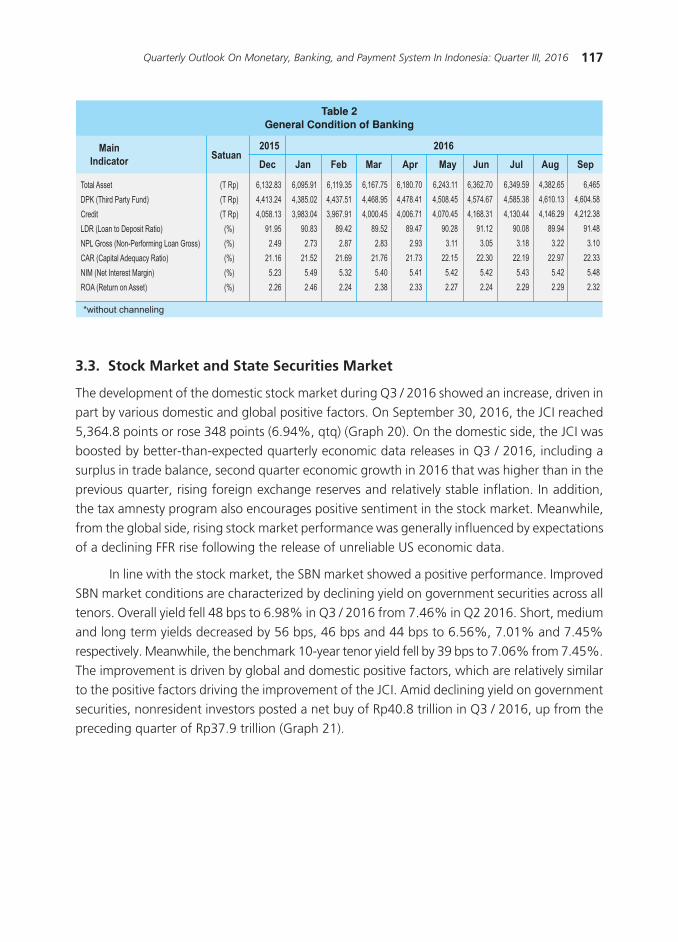

The resilience of the banking system remains intact. At the end of Q3 / 2016, bank capital was still very adequate with the Capital Adequacy Ratio (CAR) at 22.3%, well above the minimum requirement of 8% (Table 2). In line with the credit slowdown, credit risk (NPL) in Q3 / 2016 was at 3.1% (gross) or 1.4% (net). In terms of liquidity, in Q3 / 2016, bank liquidity was also sufficient, as reflected in the ratio of Liquid Equipment to Third Party Funds at 20.2%.

Graph 18.Kredit Growth by Use

Graph 19.Growth of DPK

��� ��� ��� ��� ��� ��� ��� ��� ��� ������� ���� ����

��

��

���

���

���

���

���� ��������

����

���������

����

���

���

���

���

���

���

��

��

������ ��� ��� ��� ��� ������ ��� ��� ������ ��� ��� ������ ������

���� ���� ���� ���� ����

���

���

���

��

��

���

��� ���� �� ������ ���������

117Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

3.3. Stock Market and State Securities Market

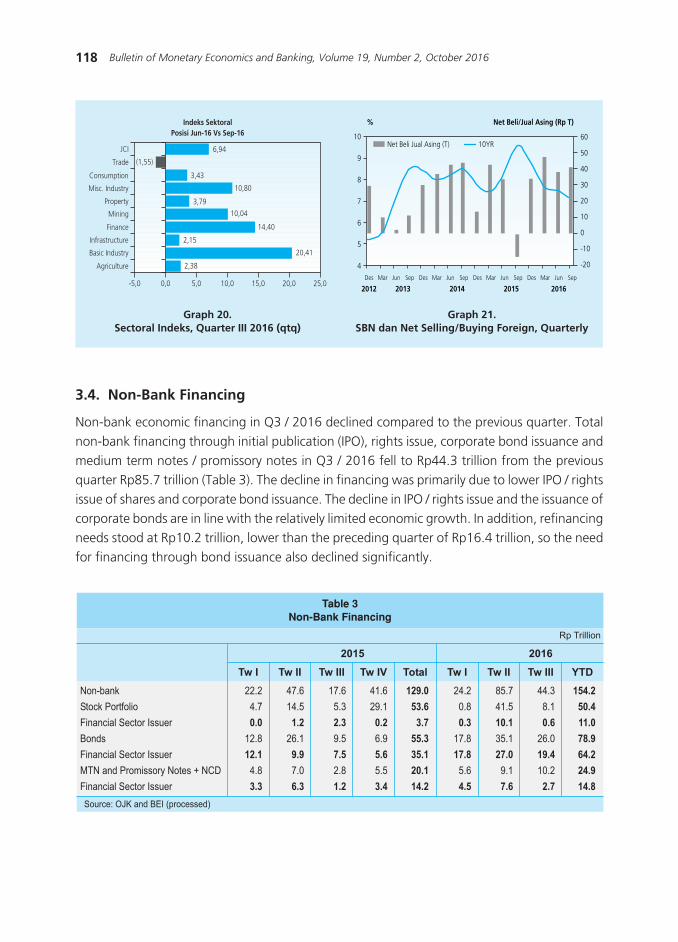

The development of the domestic stock market during Q3 / 2016 showed an increase, driven in part by various domestic and global positive factors. On September 30, 2016, the JCI reached 5,364.8 points or rose 348 points (6.94%, qtq) (Graph 20). On the domestic side, the JCI was boosted by better-than-expected quarterly economic data releases in Q3 / 2016, including a surplus in trade balance, second quarter economic growth in 2016 that was higher than in the previous quarter, rising foreign exchange reserves and relatively stable inflation. In addition, the tax amnesty program also encourages positive sentiment in the stock market. Meanwhile, from the global side, rising stock market performance was generally influenced by expectations of a declining FFR rise following the release of unreliable US economic data.

In line with the stock market, the SBN market showed a positive performance. Improved SBN market conditions are characterized by declining yield on government securities across all tenors. Overall yield fell 48 bps to 6.98% in Q3 / 2016 from 7.46% in Q2 2016. Short, medium and long term yields decreased by 56 bps, 46 bps and 44 bps to 6.56%, 7.01% and 7.45% respectively. Meanwhile, the benchmark 10-year tenor yield fell by 39 bps to 7.06% from 7.45%. The improvement is driven by global and domestic positive factors, which are relatively similar to the positive factors driving the improvement of the JCI. Amid declining yield on government securities, nonresident investors posted a net buy of Rp40.8 trillion in Q3 / 2016, up from the preceding quarter of Rp37.9 trillion (Graph 21).

����

�������������������

����������������������������������

����

���������

������������ ��� �� �� � ��� ��� ��� �� ���

�����������

� ������� ��������

����

���������������������������

� ������������ ������������������

���������������������������

�� �������������� �����

�������������������

������

������

������

���

���

���

���

���

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

��������

��������

��������

�����

����

�����

����

����

�����

��������

��������

�����

����

�����

����

����

118 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

Graph 20.Sectoral Indeks, Quarter III 2016 (qtq)

Graph 21.SBN dan Net Selling/Buying Foreign, Quarterly

3.4. Non-Bank Financing

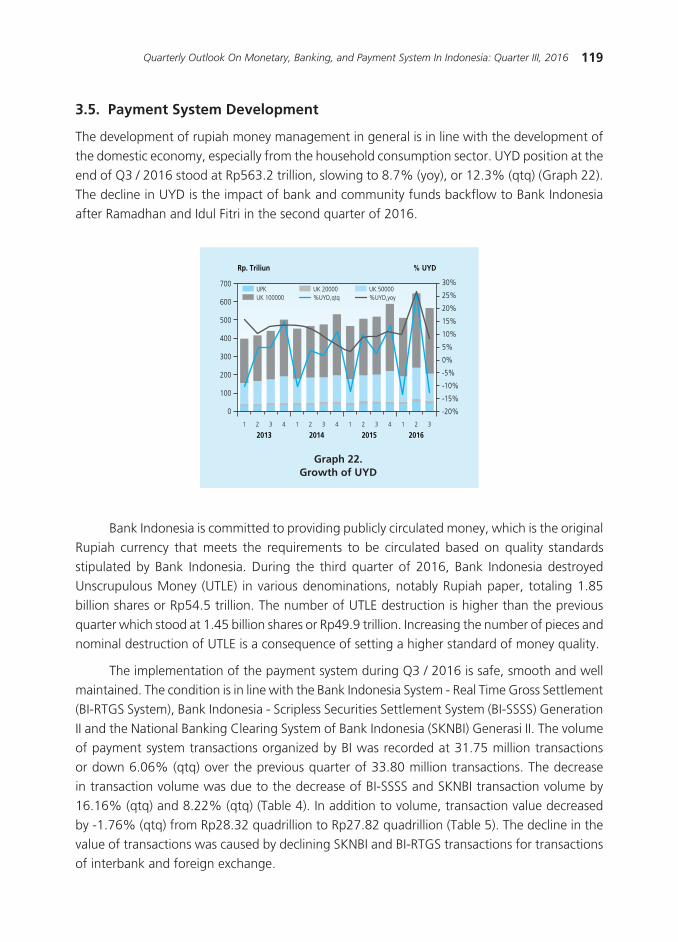

Non-bank economic financing in Q3 / 2016 declined compared to the previous quarter. Total non-bank financing through initial publication (IPO), rights issue, corporate bond issuance and medium term notes / promissory notes in Q3 / 2016 fell to Rp44.3 trillion from the previous quarter Rp85.7 trillion (Table 3). The decline in financing was primarily due to lower IPO / rights issue of shares and corporate bond issuance. The decline in IPO / rights issue and the issuance of corporate bonds are in line with the relatively limited economic growth. In addition, refinancing needs stood at Rp10.2 trillion, lower than the preceding quarter of Rp16.4 trillion, so the need for financing through bond issuance also declined significantly.

���

�����

�����������

���� ���������

�������

�����

�������

��������������

��������������

����������

����

����

�����

���������

�����

��

����

���

����

��� ��� �� ���� ��� ��� ��

�������������������������� �������� �

�������������������������

����

��������������������� ���������

����

����

�����

�����������

���������

����������

�����������������

������������������

������������

����������������

������

������������

����������������������

��������

�����������

�����������������������������

�������������� ������������������������������������������������������������������ ��������������������������������������������

����� ������ ����� ��� � ���� ����� ������ ��

� ���������

Net Beli/Jual Asing (Rp T)

2012 2013 2014 2015 2016Des Mar Jun Sep Des Mar Jun Sep Des Mar Jun Sep Des Mar Jun Sep

%

10

9

8

7

6

5

4

60

50

40

30

20

10

0

-10

-20

10YRNet Beli Jual Asing (T)

119Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

Graph 22.Growth of UYD

3.5. Payment System Development

The development of rupiah money management in general is in line with the development of the domestic economy, especially from the household consumption sector. UYD position at the end of Q3 / 2016 stood at Rp563.2 trillion, slowing to 8.7% (yoy), or 12.3% (qtq) (Graph 22). The decline in UYD is the impact of bank and community funds backflow to Bank Indonesia after Ramadhan and Idul Fitri in the second quarter of 2016.

Rp. Triliun % UYD

2013 2014 2015 2016

30%

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3

700

600

500

400

300

200

100

0

UPKUK 100000

UK 20000 UK 50000%UYD,qtq %UYD,yoy

Bank Indonesia is committed to providing publicly circulated money, which is the original Rupiah currency that meets the requirements to be circulated based on quality standards stipulated by Bank Indonesia. During the third quarter of 2016, Bank Indonesia destroyed Unscrupulous Money (UTLE) in various denominations, notably Rupiah paper, totaling 1.85 billion shares or Rp54.5 trillion. The number of UTLE destruction is higher than the previous quarter which stood at 1.45 billion shares or Rp49.9 trillion. Increasing the number of pieces and nominal destruction of UTLE is a consequence of setting a higher standard of money quality.

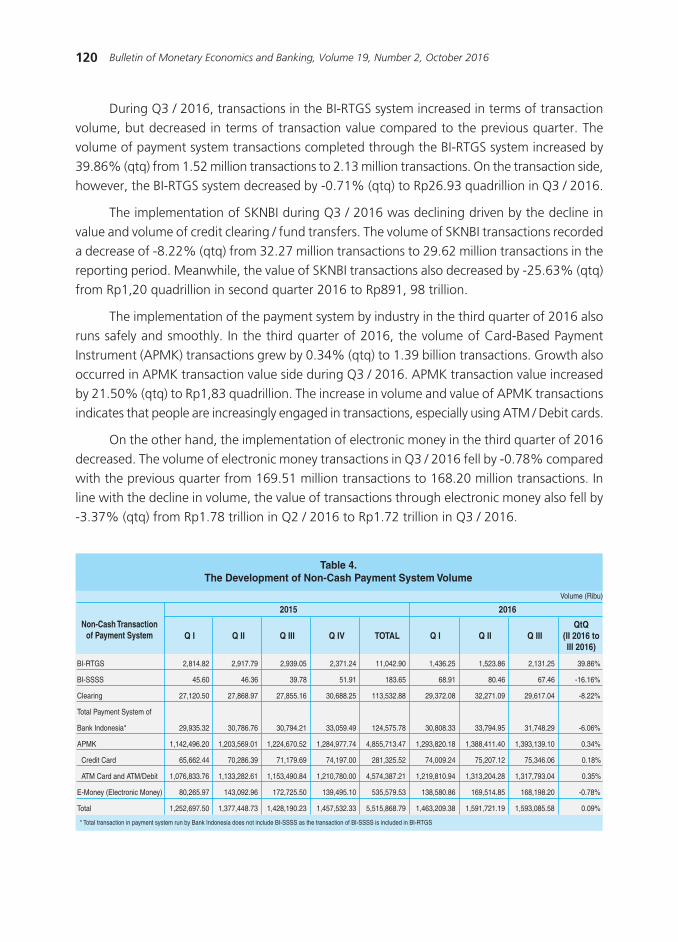

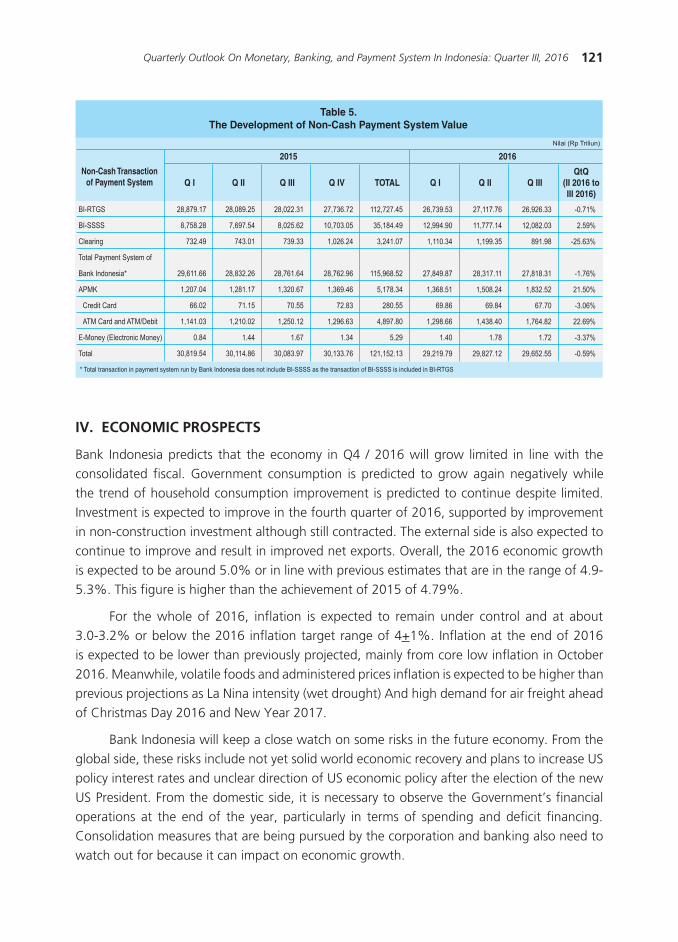

The implementation of the payment system during Q3 / 2016 is safe, smooth and well maintained. The condition is in line with the Bank Indonesia System - Real Time Gross Settlement (BI-RTGS System), Bank Indonesia - Scripless Securities Settlement System (BI-SSSS) Generation II and the National Banking Clearing System of Bank Indonesia (SKNBI) Generasi II. The volume of payment system transactions organized by BI was recorded at 31.75 million transactions or down 6.06% (qtq) over the previous quarter of 33.80 million transactions. The decrease in transaction volume was due to the decrease of BI-SSSS and SKNBI transaction volume by 16.16% (qtq) and 8.22% (qtq) (Table 4). In addition to volume, transaction value decreased by -1.76% (qtq) from Rp28.32 quadrillion to Rp27.82 quadrillion (Table 5). The decline in the value of transactions was caused by declining SKNBI and BI-RTGS transactions for transactions of interbank and foreign exchange.

120 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

During Q3 / 2016, transactions in the BI-RTGS system increased in terms of transaction volume, but decreased in terms of transaction value compared to the previous quarter. The volume of payment system transactions completed through the BI-RTGS system increased by 39.86% (qtq) from 1.52 million transactions to 2.13 million transactions. On the transaction side, however, the BI-RTGS system decreased by -0.71% (qtq) to Rp26.93 quadrillion in Q3 / 2016.

The implementation of SKNBI during Q3 / 2016 was declining driven by the decline in value and volume of credit clearing / fund transfers. The volume of SKNBI transactions recorded a decrease of -8.22% (qtq) from 32.27 million transactions to 29.62 million transactions in the reporting period. Meanwhile, the value of SKNBI transactions also decreased by -25.63% (qtq) from Rp1,20 quadrillion in second quarter 2016 to Rp891, 98 trillion.

The implementation of the payment system by industry in the third quarter of 2016 also runs safely and smoothly. In the third quarter of 2016, the volume of Card-Based Payment Instrument (APMK) transactions grew by 0.34% (qtq) to 1.39 billion transactions. Growth also occurred in APMK transaction value side during Q3 / 2016. APMK transaction value increased by 21.50% (qtq) to Rp1,83 quadrillion. The increase in volume and value of APMK transactions indicates that people are increasingly engaged in transactions, especially using ATM / Debit cards.

On the other hand, the implementation of electronic money in the third quarter of 2016 decreased. The volume of electronic money transactions in Q3 / 2016 fell by -0.78% compared with the previous quarter from 169.51 million transactions to 168.20 million transactions. In line with the decline in volume, the value of transactions through electronic money also fell by -3.37% (qtq) from Rp1.78 trillion in Q2 / 2016 to Rp1.72 trillion in Q3 / 2016.

Q I Q II Q III Q IV TOTAL Q I Q II Q IIIQtQ

(II 2016 toIII 2016)

BI-RTGS 2,814.82 2,917.79 2,939.05 2,371.24 11,042.90 1,436.25 1,523.86 2,131.25 39.86%

BI-SSSS 45.60 46.36 39.78 51.91 183.65 68.91 80.46 67.46 -16.16%

Clearing 27,120.50 27,868.97 27,855.16 30,688.25 113,532.88 29,372.08 32,271.09 29,617.04 -8.22%

Total Payment System of

Bank Indonesia* 29,935.32 30,786.76 30,794.21 33,059.49 124,575.78 30,808.33 33,794.95 31,748.29 -6.06%

APMK 1,142,496.20 1,203,569.01 1,224,670.52 1,284,977.74 4,855,713.47 1,293,820.18 1,388,411.40 1,393,139.10 0.34%

Credit Card 65,662.44 70,286.39 71,179.69 74,197.00 281,325.52 74,009.24 75,207.12 75,346.06 0.18%

ATM Card and ATM/Debit 1,076,833.76 1,133,282.61 1,153,490.84 1,210,780.00 4,574,387.21 1,219,810.94 1,313,204.28 1,317,793.04 0.35%

E-Money (Electronic Money) 80,265.97 143,092.96 172,725.50 139,495.10 535,579.53 138,580.86 169,514.85 168,198.20 -0.78%

Total 1,252,697.50 1,377,448.73 1,428,190.23 1,457,532.33 5,515,868.79 1,463,209.38 1,591,721.19 1,593,085.58 0.09%

* Total transaction in payment system run by Bank Indonesia does not include BI-SSSS as the transaction of BI-SSSS is included in BI-RTGS

Non-Cash Transactionof Payment System

2015 2016

Table 4.The Development of Non-Cash Payment System Volume

Volume (Ribu)

121Quarterly Outlook On Monetary, Banking, and Payment System In Indonesia: Quarter III, 2016

IV. ECONOMIC PROSPECTS

Bank Indonesia predicts that the economy in Q4 / 2016 will grow limited in line with the consolidated fiscal. Government consumption is predicted to grow again negatively while the trend of household consumption improvement is predicted to continue despite limited. Investment is expected to improve in the fourth quarter of 2016, supported by improvement in non-construction investment although still contracted. The external side is also expected to continue to improve and result in improved net exports. Overall, the 2016 economic growth is expected to be around 5.0% or in line with previous estimates that are in the range of 4.9- 5.3%. This figure is higher than the achievement of 2015 of 4.79%.

For the whole of 2016, inflation is expected to remain under control and at about 3.0-3.2% or below the 2016 inflation target range of 4+1%. Inflation at the end of 2016 is expected to be lower than previously projected, mainly from core low inflation in October 2016. Meanwhile, volatile foods and administered prices inflation is expected to be higher than previous projections as La Nina intensity (wet drought) And high demand for air freight ahead of Christmas Day 2016 and New Year 2017.

Bank Indonesia will keep a close watch on some risks in the future economy. From the global side, these risks include not yet solid world economic recovery and plans to increase US policy interest rates and unclear direction of US economic policy after the election of the new US President. From the domestic side, it is necessary to observe the Government’s financial operations at the end of the year, particularly in terms of spending and deficit financing. Consolidation measures that are being pursued by the corporation and banking also need to watch out for because it can impact on economic growth.

Q I Q II Q III Q IV TOTAL Q I Q II Q IIIQtQ

(II 2016 toIII 2016)

* Total transaction in payment system run by Bank Indonesia does not include BI-SSSS as the transaction of BI-SSSS is included in BI-RTGS

Non-Cash Transactionof Payment System

2015 2016

Table 5.The Development of Non-Cash Payment System Value

Nilai (Rp Triliun)

BI-RTGS

BI-SSSS

Clearing

Total Payment System of

Bank Indonesia*

APMK

Credit Card

ATM Card and ATM/Debit

E-Money (Electronic Money)

Total

28,879.17

8,758.28

732.49

29,611.66

1,207.04

66.02

1,141.03

0.84

30,819.54

28,089.25

7,697.54

743.01

28,832.26

1,281.17

71.15

1,210.02

1.44

30,114.86

28,022.31

8,025.62

739.33

28,761.64

1,320.67

70.55

1,250.12

1.67

30,083.97

27,736.72

10,703.05

1,026.24

28,762.96

1,369.46

72.83

1,296.63

1.34

30,133.76

112,727.45

35,184.49

3,241.07

115,968.52

5,178.34

280.55

4,897.80

5.29

121,152.13

26,739.53

12,994.90

1,110.34

27,849.87

1,368.51

69.86

1,298.66

1.40

29,219.79

27,117.76

11,777.14

1,199.35

28,317.11

1,508.24

69.84

1,438.40

1.78

29,827.12

26,926.33

12,082.03

891.98

27,818.31

1,832.52

67.70

1,764.82

1.72

29,652.55

-0.71%

2.59%

-25.63%

-1.76%

21.50%

-3.06%

22.69%

-3.37%

-0.59%

122 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

This page intentionally left blank

123Early Warning System and Currency Volatility Management In Emerging Market

EARLY WARNING SYSTEM AND CURRENCY VOLATILITY MANAGEMENT IN EMERGING MARKET

Natasia Engeline S1

Salomo Posmauli Matondang2

This paper adopts theoretical models from Candelon, Dumitrescu, and Hurlin and empirical model

from Commerzbank to devise a set of indicators that can serve as an early warning system (EWS) on

exchange rate. In light of the appreciation of emerging countries’ currencies during the Fed quantitative

easing period, it is important to understand on how The Fed normalization would put pressure on managing

volatility for central banks, especially for countries with large trade and fiscal deficit such as Indonesia.

All in all, using both EWS models, central banks could discern potential exchange rate depreciation for

intervention purpose.

Abstract

Keywords: Dynamic Logit Model, Foreign Exchange, Early Warning System, Emerging Countries,

Foreign Exchange Intervention

JEL Classification: C32, E58, F31, F37

1 Financial Analyst, Reserve Management Department of Bank Indonesia ([email protected])2 Financial Analyst, Reserve Management Department of Bank Indonesia ([email protected])

124 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

I. INTRODUCTION

Research on emerging countries’ exchange rate dynamics has been the subject of interest by academia, market participants, and financial regulators; considering their high volatility. Central banks especially those in emerging market economies are taking special interest in exchange rate dynamics due to their role in stabilizing exchange rate movement through intervention. Gracia et al. (2011) argued that the role of central bank intervention in exchange rate movement is desirable, especially in vulnerable emerging economies. Alder and Tovar (2011), Basu and Varoudakis (2013), and Neely (2008), identified several motives of the central bank’s intervention such as moderate exchange rate volatility, reducing exchange rate misalignment, accumulate reserves, and supply foreign exchange to the market.

More recently, following the unconventional policies of major advanced economies from 2008, emerging countries’ currencies have experienced appreciation due to massive capital inflow. Looking forward, it is important to understand on how The Federal Reserve normalization would put pressure for central banks on managing volatility, especially those with large trade and fiscal deficit such as Indonesia. In retrospect, initial reports that The Federal Reserve might begin “tapering” its quantitative easing on May 2013, caused a rush to exit from emerging countries including Indonesia, with exchange rate declines of as much as 20% in the following four months.

Considering the importance of intervention in managing emerging currencies, central banks in emerging market economies should devise a set of indicators that can serve as an early warning system (EWS); which could identify an impending depreciation before it occurs. EWS could help central banks implement optimal policies including the strategies of intervention to prevent or smooth the impact of currency depreciation.

Kaminsky, Lizondo, and Reinhart (1998) pioneered a comprehensive survey regarding EWS by proposing several case studies of devaluation episodes using structural model of balance of payment crises, signaling model for currency crises, as well as empirical study using macroeconomic and financial data for emerging countries. Berg and Patillo (1999) proposed a static panel probit model as an alternative to the signaling approach. Bussiere and Fratzcher (2006) proposed a multinominal logit EWS that consider the crisis as a ternary variable instead of binary.

Unfortunately, in previous studies, EWS have remained silent at the recent financial crisis. The difficulty to detect potential currency depreciation lies in the specificity of EWS that aimed at accurately detecting the occurrence of a currency depreciation which is translated into a binary variable that takes the value of one when depreciation occurs and the value of zero otherwise. In this context, it is not possible to directly implement the method proposed in times series econometrics such as vector autoregression. Furthermore, most previous EWS are static and assume that the depreciation probability depends only on a set of macroeconomic variables.

125Early Warning System and Currency Volatility Management In Emerging Market

3 Detail explanation on constrained maximum likelihood is available on appendix.

Candelon, Dumitrescu, and Hurlin (2010) proposed a new generation of EWS which reconcile the limited dependent property of the depreciation variable and the dynamic dimension of this phenomenon. In particular, Candelon et al. (2010) considered not only the exogenous source of depreciation persistence from macroeconomic data, but also endogenous persistence of depreciation which are lagged binary depreciation variable and past index associated to the probability of being in depreciation period. Thus, the EWS relies an autoregressive (AR) model, where the endogenous variable summarizes all the past information of the system. Given all these different specifications, an exact maximum likelihood estimation by Kauppi and Saikonnen (2008) is used to estimate the models.3

In contrast from academic EWS model, Commerzbank (2013) proposed a simple currency depreciation index that requires a shorter forecast period and does not require regular recalibration. Commerzbank used several macroeconomics indicators such as current account and industrial production as well as market indicators such as real effective exchange rate and equity market performance that translated into risk measures with equal weighting.

Perhaps the most interesting feature of our research is on how we adopt both models from Candelon et al. (2010) and Commerzbank (2013) to give a better understanding toward potential currency depreciation. All in all, using both EWS model, central banks could discern potential exchange rate depreciation for intervention purpose.

This paper is structured as follows. Section 2 describes the structure of early warning signal (EWS) by Candelon et al. (2010) and Commerzbank as well as several assumptions for the EWS index. Section 3 describes the data and construction of the EWS index. Section 4 reports the forecast evaluation and intervention strategies, while section 5 concludes.

II. THEORY

The first model is a dynamic EWS based on Candelon et al. (2010) that exploits the persistence property of the currency depreciation captured by lagged endogenous indicators. The second model is based on Commerzbank that use macroeconomics and market indicators to construct a depreciation warning index.

2.1. Dating Currency Depreciation

Before elaborating further into the EWS model, we define currency depreciation as large market movement adjusted for interest rate differentials rather that looking at composite indices of exchange rate pressure as elaborated by Kumar et al. (2002). Thus, if et is the exchange rate vis-à-vis the US dollar and rt and rt

* are domestic and foreign (US) interest rates of maturity D,

we supposed that depreciation takes place if

126 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

where g1 is a cut-off point which is set to 5 percent. Our rationale behind the cut-off point is an assumption that an exchange rate movement bigger than 5 percent is consider high in many countries that adopt manage float regime. Equation above is defined as an unanticipated

depreciation crash. Note that the product on the left hand side of this inequality is the return that an investor receives if he shorts the domestic currency for the period D then invests the proceeds in US bonds of maturity D as normally happened during risk aversion period.

Furthermore, second definition of currency depreciation or known as depreciation crashes could also be defined if

Where g2 is a cut-off point which is also set to 5 percent. Therefore, total currency

depreciation could be defined as large market movement that satisfies both the first and second definition of currency depreciation above.

2.2. Specification and Estimation of Dynamic EWS Model

First, consider the time-series version of the dynamic limited dependent EWS. Denote as the currency depreciation binary variable for country , taking the value of 1 during depreciation periods and 0 otherwise and as the matrix of explanatory variables, i.e., macroeconomic indicators.

The one-step-ahead dynamic specification taken into account exogenous macroeconomic variables (xt-1) as well as endogenous variables both lagged binary variable (yt-1) and lagged index (pt-1) takes the general form of:

where is the conditional probability given the information set we have at time is the index at time t, and F is a distribution function i.e., Gaussian in the case of the probit model and logistic for the logit model.

The main advantage of the general framework above is that it allows to estimate and to compare different alternative specifications taken the form as follows:

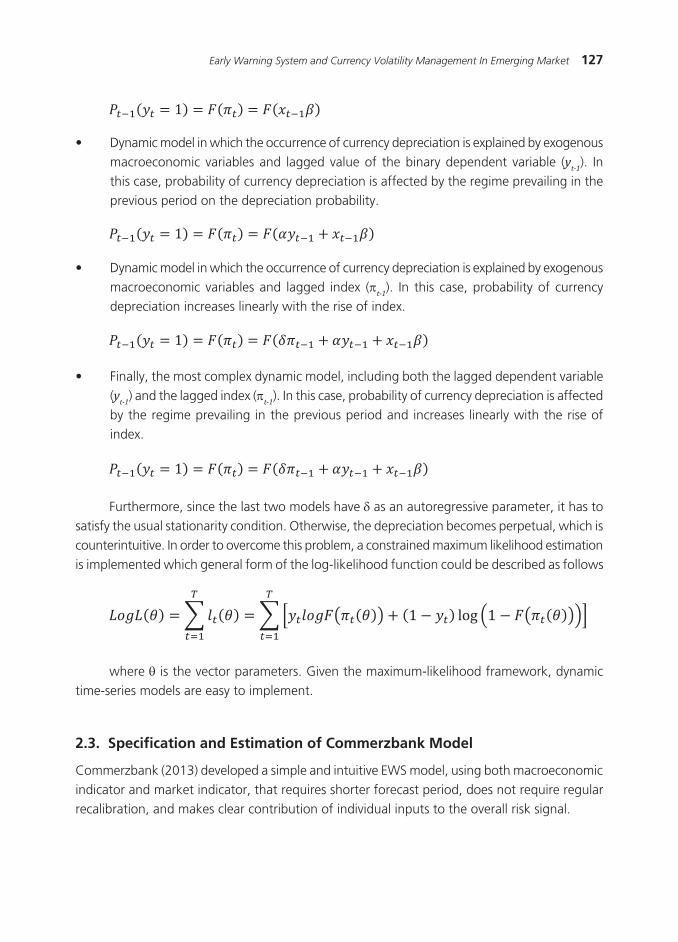

• Purestaticmodelinwhichtheoccurrenceofcurrencydepreciationisexplainedonlybyexogenous macroeconomic variables (xt-1). This model constitutes the benchmark model, in which devaluation episodes are persistent only if the changes in economic indicators are themselves persistent (exogenous persistence).

127Early Warning System and Currency Volatility Management In Emerging Market

• Dynamicmodelinwhichtheoccurrenceofcurrencydepreciationisexplainedbyexogenousmacroeconomic variables and lagged value of the binary dependent variable (yt-1). In this case, probability of currency depreciation is affected by the regime prevailing in the previous period on the depreciation probability.

• Dynamicmodelinwhichtheoccurrenceofcurrencydepreciationisexplainedbyexogenousmacroeconomic variables and lagged index (pt-1). In this case, probability of currency depreciation increases linearly with the rise of index.

• Finally,themostcomplexdynamicmodel,includingboththelaggeddependentvariable(yt-1) and the lagged index (pt-1). In this case, probability of currency depreciation is affected by the regime prevailing in the previous period and increases linearly with the rise of index.

Furthermore, since the last two models have d as an autoregressive parameter, it has to satisfy the usual stationarity condition. Otherwise, the depreciation becomes perpetual, which is counterintuitive. In order to overcome this problem, a constrained maximum likelihood estimation is implemented which general form of the log-likelihood function could be described as follows

where q is the vector parameters. Given the maximum-likelihood framework, dynamic time-series models are easy to implement.

2.3. Specification and Estimation of Commerzbank Model

Commerzbank (2013) developed a simple and intuitive EWS model, using both macroeconomic indicator and market indicator, that requires shorter forecast period, does not require regular recalibration, and makes clear contribution of individual inputs to the overall risk signal.

128 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

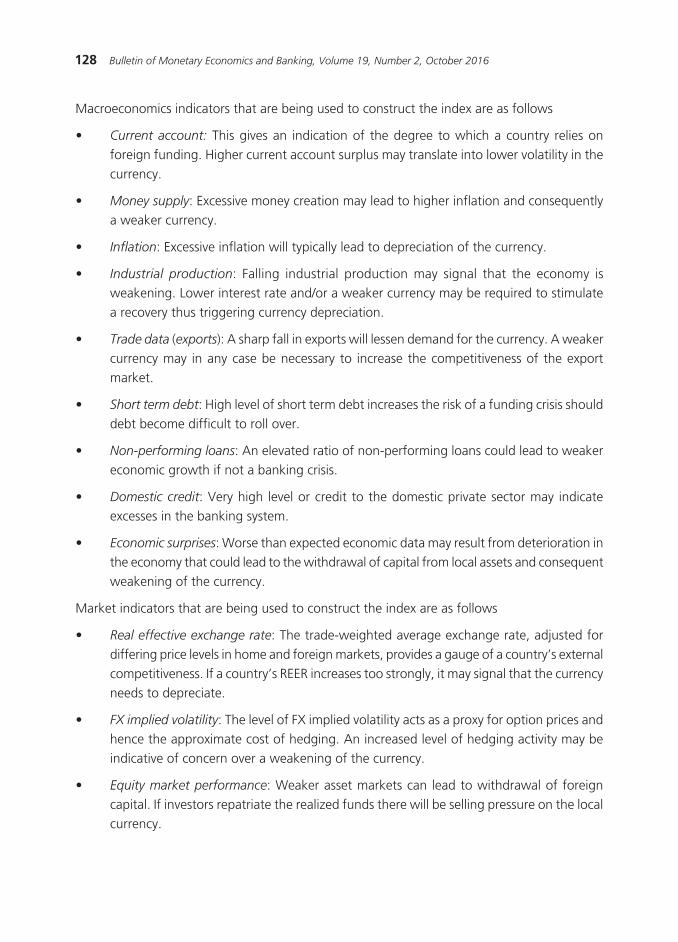

Macroeconomics indicators that are being used to construct the index are as follows

• Currentaccount: This gives an indication of the degree to which a country relies on foreign funding. Higher current account surplus may translate into lower volatility in the currency.

• Moneysupply: Excessive money creation may lead to higher inflation and consequently a weaker currency.

• Inflation: Excessive inflation will typically lead to depreciation of the currency.

• Industrial production: Falling industrial production may signal that the economy is weakening. Lower interest rate and/or a weaker currency may be required to stimulate a recovery thus triggering currency depreciation.

• Tradedata (exports): A sharp fall in exports will lessen demand for the currency. A weaker currency may in any case be necessary to increase the competitiveness of the export market.

• Shorttermdebt: High level of short term debt increases the risk of a funding crisis should debt become difficult to roll over.

• Non-performingloans: An elevated ratio of non-performing loans could lead to weaker economic growth if not a banking crisis.

• Domesticcredit: Very high level or credit to the domestic private sector may indicate excesses in the banking system.

• Economicsurprises: Worse than expected economic data may result from deterioration in the economy that could lead to the withdrawal of capital from local assets and consequent weakening of the currency.

Market indicators that are being used to construct the index are as follows

• Realeffectiveexchangerate: The trade-weighted average exchange rate, adjusted for differing price levels in home and foreign markets, provides a gauge of a country’s external competitiveness. If a country’s REER increases too strongly, it may signal that the currency needs to depreciate.

• FXimpliedvolatility: The level of FX implied volatility acts as a proxy for option prices and hence the approximate cost of hedging. An increased level of hedging activity may be indicative of concern over a weakening of the currency.

• Equitymarketperformance: Weaker asset markets can lead to withdrawal of foreign capital. If investors repatriate the realized funds there will be selling pressure on the local currency.

129Early Warning System and Currency Volatility Management In Emerging Market

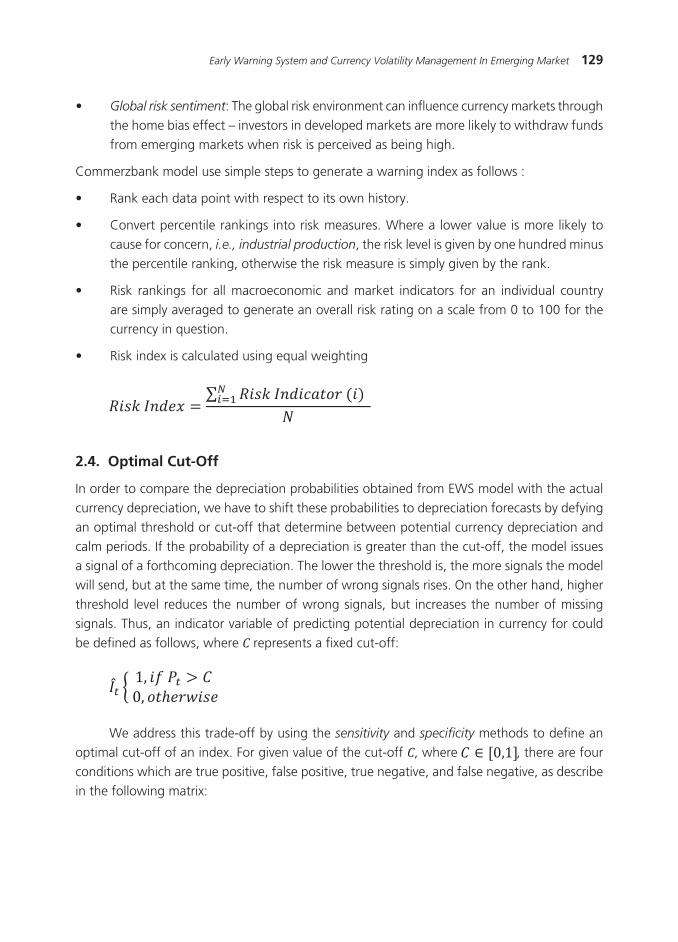

• Globalrisksentiment: The global risk environment can influence currency markets through the home bias effect – investors in developed markets are more likely to withdraw funds from emerging markets when risk is perceived as being high.

Commerzbank model use simple steps to generate a warning index as follows :

• Rankeachdatapointwithrespecttoitsownhistory.

• Convertpercentilerankings intoriskmeasures.Wherea lowervalueismorelikelytocause for concern, i.e., industrial production, the risk level is given by one hundred minus the percentile ranking, otherwise the risk measure is simply given by the rank.

• Risk rankings for allmacroeconomic andmarket indicators for an individual countryare simply averaged to generate an overall risk rating on a scale from 0 to 100 for the currency in question.

• Riskindexiscalculatedusingequalweighting

2.4. Optimal Cut-Off

In order to compare the depreciation probabilities obtained from EWS model with the actual currency depreciation, we have to shift these probabilities to depreciation forecasts by defying an optimal threshold or cut-off that determine between potential currency depreciation and calm periods. If the probability of a depreciation is greater than the cut-off, the model issues a signal of a forthcoming depreciation. The lower the threshold is, the more signals the model will send, but at the same time, the number of wrong signals rises. On the other hand, higher threshold level reduces the number of wrong signals, but increases the number of missing signals. Thus, an indicator variable of predicting potential depreciation in currency for could be defined as follows, where C represents a fixed cut-off:

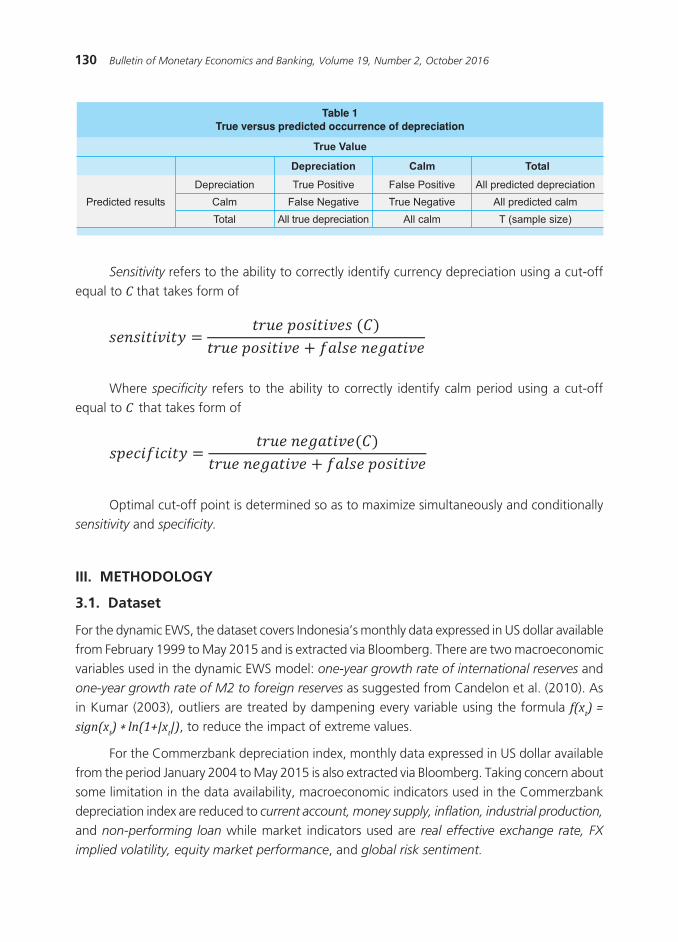

We address this trade-off by using the sensitivity and specificity methods to define an optimal cut-off of an index. For given value of the cut-off C, where , there are four conditions which are true positive, false positive, true negative, and false negative, as describe in the following matrix:

130 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

������������

������������

����

�����

������������� ���

�� ����������

������������

������ ��������������

��������������

�� ��������

��������

��������������������������

������������������

���������������

����������������������������������������� �������������

���� �����

����������

Sensitivity refers to the ability to correctly identify currency depreciation using a cut-off equal to C that takes form of

Where specificity refers to the ability to correctly identify calm period using a cut-off equal to C that takes form of

Optimal cut-off point is determined so as to maximize simultaneously and conditionally sensitivity and specificity.

III. METHODOLOGY

3.1. Dataset

For the dynamic EWS, the dataset covers Indonesia’s monthly data expressed in US dollar available from February 1999 to May 2015 and is extracted via Bloomberg. There are two macroeconomic variables used in the dynamic EWS model: one-yeargrowthrateofinternationalreserves and one-yeargrowthrateofM2toforeignreserves as suggested from Candelon et al. (2010). As in Kumar (2003), outliers are treated by dampening every variable using the formula f(xt) = sign(xt) * ln(1+|xt|), to reduce the impact of extreme values.

For the Commerzbank depreciation index, monthly data expressed in US dollar available from the period January 2004 to May 2015 is also extracted via Bloomberg. Taking concern about some limitation in the data availability, macroeconomic indicators used in the Commerzbank depreciation index are reduced to current account, money supply, inflation, industrial production, and non-performing loan while market indicators used are realeffectiveexchangerate,FXimplied volatility, equity market performance, and global risk sentiment.

131Early Warning System and Currency Volatility Management In Emerging Market

3.2. Model Evaluation and Robustness Test

In order to show the usefulness of the model, we implement the EWS evaluation by Candelon et al. (2011), especially to test their forecasting abilities (out-of-sample exercises). The main advantage of this framework is that it can be applied to any EWS outputting depreciation probabilities, both in-sample and out-of-sample. To be more precise, first, we rely on different evaluation criteria and comparison tests to identify the outperforming model. Second, we gauge the optimal model’s ability to discriminate between depreciation and calm periods by identifying the optimal cut-off for each model.

Accordingly, we consider both classic EWS evaluation measures such as the QPS criterion and newer one for the EWS literature, which take the cut-off into account in the evaluation and thus lead to a more refined diagnostic, i.e. the AreaUndertheROCcriterion(AUC). The QPS criterion is a mean-squared-error measure that compares the depreciation probabilities (the forecasts issued by the EWS, Pt-1 (yt = 1)) with the depreciation occurrence indicator yt:

At the same time, AUC is a credit-scoring criteria, that reveals the predictive abilities of an EWS by relying on all the values of the gut-off, i.e. the threshold used to compute depreciation forecasts :

Where represents the sensitivity, i.e. the proportion of depreciation correctly identified by the EWS for a given cut-off c and is the specificity, i.e. the proportion of calm periods correctly identified by the model for a cut-off equal to c.

Next, the optimal cut-offis identified by maximizing the Youden index ( ) which is an accuracy measure arbitrating between type I and type II errors (misidentified depreciation and false alarms):

where . A model’s ability to correctly discriminate between depreciation and calm periods is the given by sensitivity and specificity. For more details on the evaluation method, see Candelon et al. (2011).

132 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

IV. RESULT AND ANALYSIS

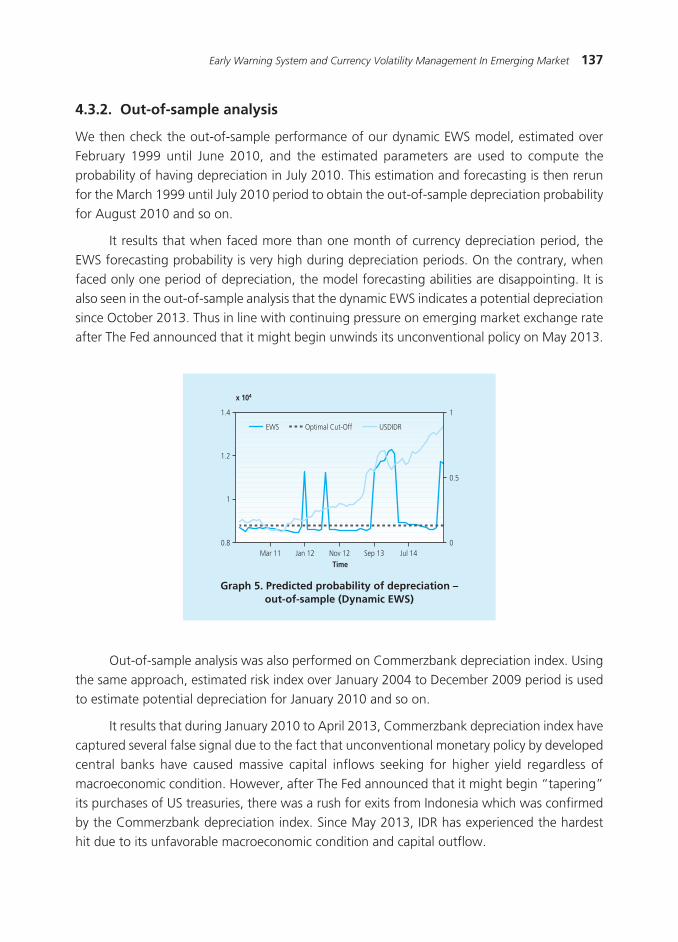

4.1. Estimation Results for Dynamic EWS

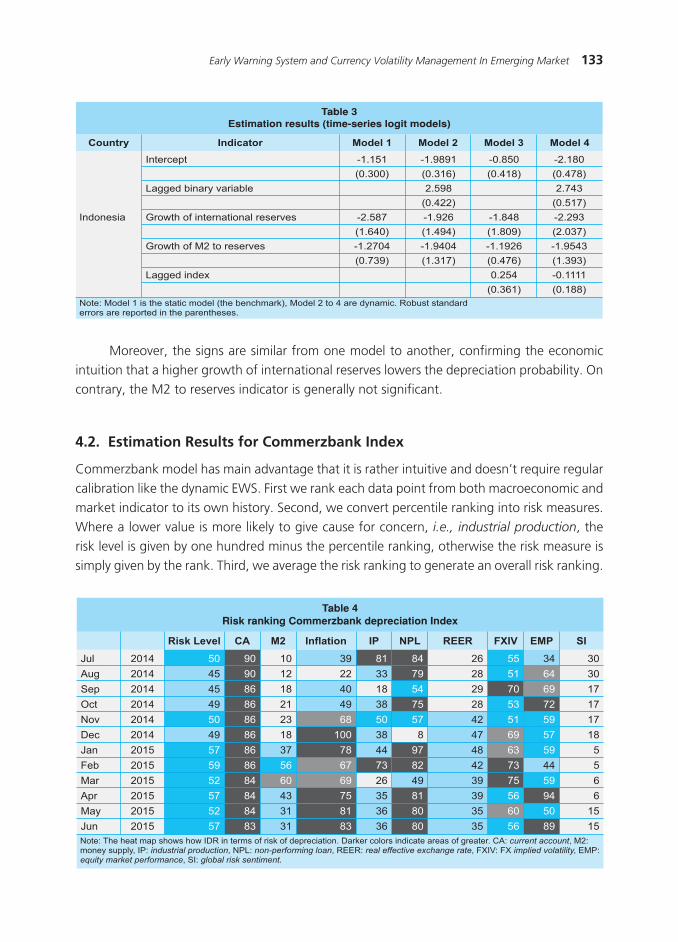

General form of dynamic EWS elaborated above has main advantage that it allows to estimate and compare different EWS specification. First, we estimate the three types of dynamic EWS as well as the benchmark which is the static EWS model under analysis in the time-series framework. Furthermore, the static model is labeled as Model 1, a dynamic one which includes the lagged binary dependent variable is labeled as Model 2, a dynamic one including the lagged index is labeled as Model 3, and finally, a dynamic model which includes both the lagged binary dependent variable and the lagged index is labeled as Model 4.

Second, we find the best goodness of fit from the four models by relying on Schwarz Information Criterion (SBC). SBC reveals that the right-hand-side variables have important explanatory power. Based on the lowest values of the SCB criterion, Model 2 that includes the lagged binary dependent variable seems to be the most adequate model to predict potential currency depreciation. Thus, SCB gives a clear indication that dynamic model generally outperform the static one.

Third, we analyze the signs of the estimated parameters for the Model 2. The result shows a negative coefficient of growth of international reserves, indicating a decline in the probability of currency depreciation is presumed with an increase in a country’s growth of international

reserves. Intuitively, an increase in growth of international reserves indicates currency non-vulnerability. For the growthofM2toreservescoefficient, it is assumed that if the growth of the amount of money in circulation overruns the growth of international reserves, the currency is perceived as unstable and a speculative attack is foreseeable. Thus, a positive coefficient of the growthofM2reserves is expected. Nonetheless, a negative coefficient that appears on growthofM2toreservesmight be due to the fact that the two macroeconomic variables capture mainly the information not filtered by the lagged binary variable. Most importantly, the coefficient of the lagged binary dependent variable is significant and has a positive sign. It means that the probability of being in a deprecation episode increases if a depreciation period prevailed in the previous period. This clearly indicates that depreciation’ persistence should be accounted for in order to improve accuracy of currency EWS.

��������� ������ ������ ������ ������

��������������������������������� �����������������������

������� ������� ������� ������� �������

��� ��� ��� ���

�� ������������ ���� � ��������� ��������������������� ��������������������������������� ��� �� ������ ��������������� ������

133Early Warning System and Currency Volatility Management In Emerging Market

Moreover, the signs are similar from one model to another, confirming the economic intuition that a higher growth of international reserves lowers the depreciation probability. On contrary, the M2 to reserves indicator is generally not significant.

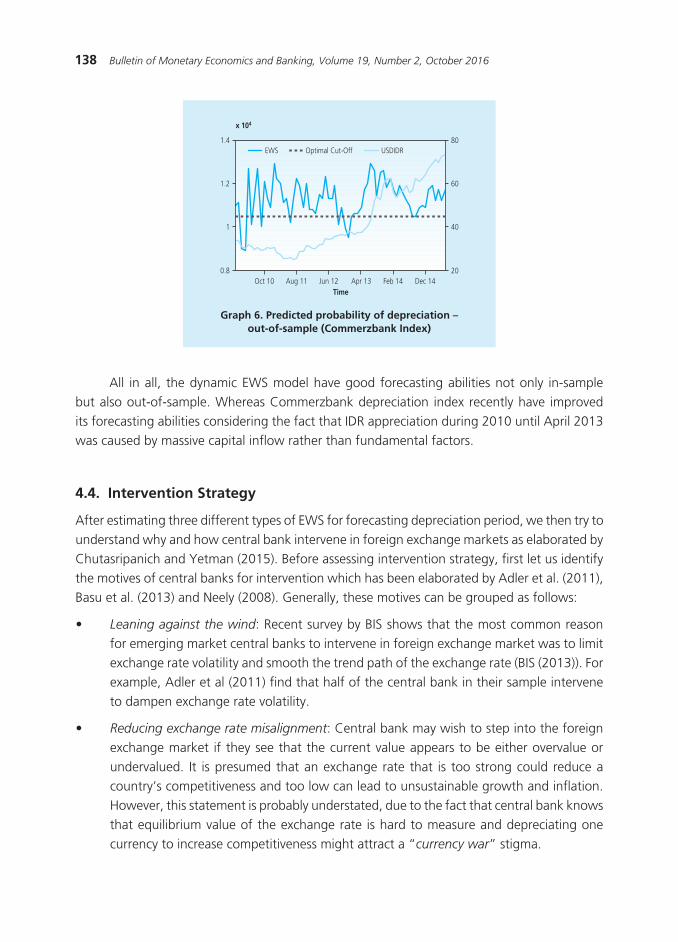

4.2. Estimation Results for Commerzbank Index

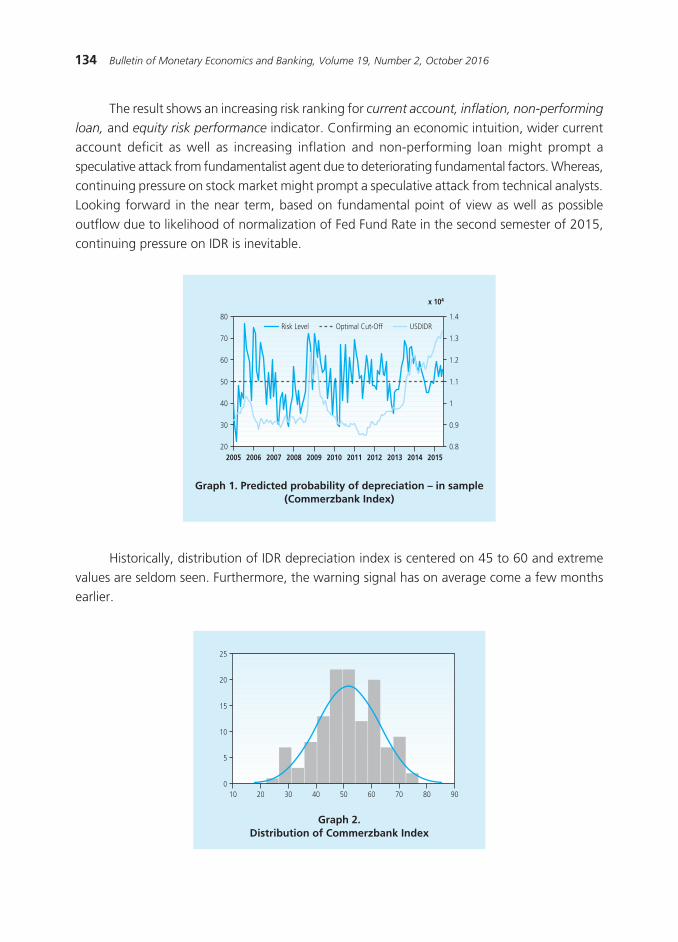

Commerzbank model has main advantage that it is rather intuitive and doesn’t require regular calibration like the dynamic EWS. First we rank each data point from both macroeconomic and market indicator to its own history. Second, we convert percentile ranking into risk measures. Where a lower value is more likely to give cause for concern, i.e., industrial production, the risk level is given by one hundred minus the percentile ranking, otherwise the risk measure is simply given by the rank. Third, we average the risk ranking to generate an overall risk ranking.

�������

���������

����������������������������������������� ����������

���������

�������������������� �

�������������������� ���������

����������������������

������������

�������������

���������� �������� ������

������������������� ����������� ���� � �������

��������� ���

���� ���������������� ������� �������

��������� ������ ������������������������ ���������������������

��������� ������� ������� ������ �������

���������� �������������������� �������������������� ������ ������������������������������������������������������������������

����������

�������������������������������� ������������ ��

���

���

������

���

���

���

�� ���

�����

�������������������������������������������������������������������������������������������������������������������������������� ������������ ������������������������� ������������������������ ������������������ ��������������� ����������������� �������� ��������������������������� ��������������������������

���������

���

���

������

���

������

���

���

�� �� ������� � �� ��� �� ��� �� ��

����

��

��

����

�

��

�

����

������

��

��

����

��

����

��

��

�����

�

�

����

��

����

��

��

��

��

��

�����

��

����

��

����

������

��

��

����

��

���

��

��

������

��

��

���

�

����

��

��

���

�

�

����

�

����

��

��

������

��

��

����

��

����

��

��

����

��

��

����

��

���

��

���

������

�

��

����

��

����

��

��

134 Bulletin of Monetary Economics and Banking, Volume 19, Number 2, October 2016

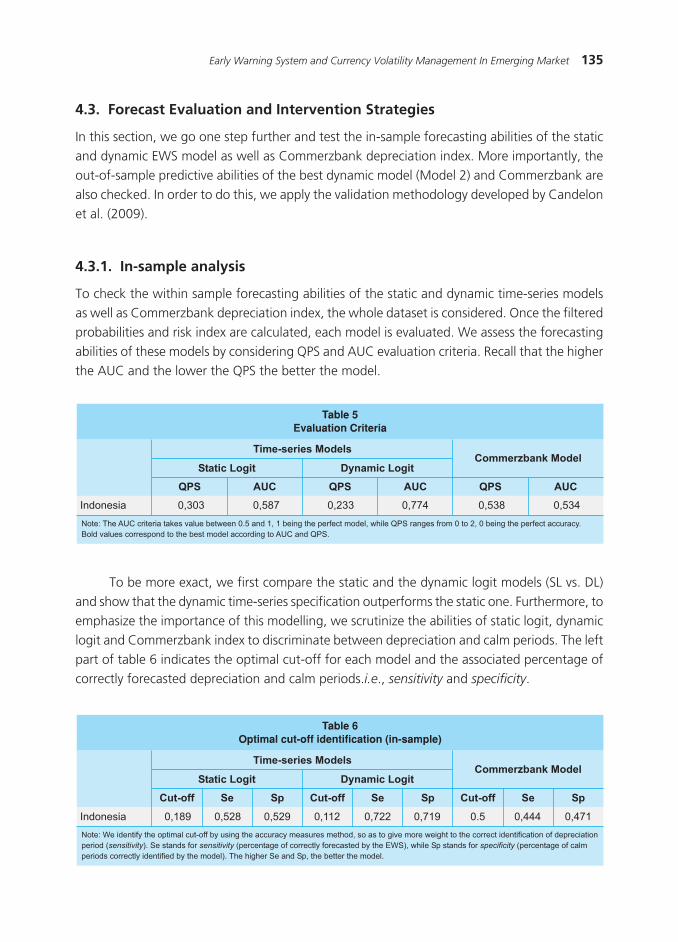

The result shows an increasing risk ranking for currentaccount,inflation,non-performingloan, and equity risk performance indicator. Confirming an economic intuition, wider current account deficit as well as increasing inflation and non-performing loan might prompt a speculative attack from fundamentalist agent due to deteriorating fundamental factors. Whereas, continuing pressure on stock market might prompt a speculative attack from technical analysts. Looking forward in the near term, based on fundamental point of view as well as possible outflow due to likelihood of normalization of Fed Fund Rate in the second semester of 2015, continuing pressure on IDR is inevitable.