Budget Highlights

3

-

Upload

karan-puri -

Category

News & Politics

-

view

152 -

download

0

Transcript of Budget Highlights

BUDGET 2017-2018Highlights

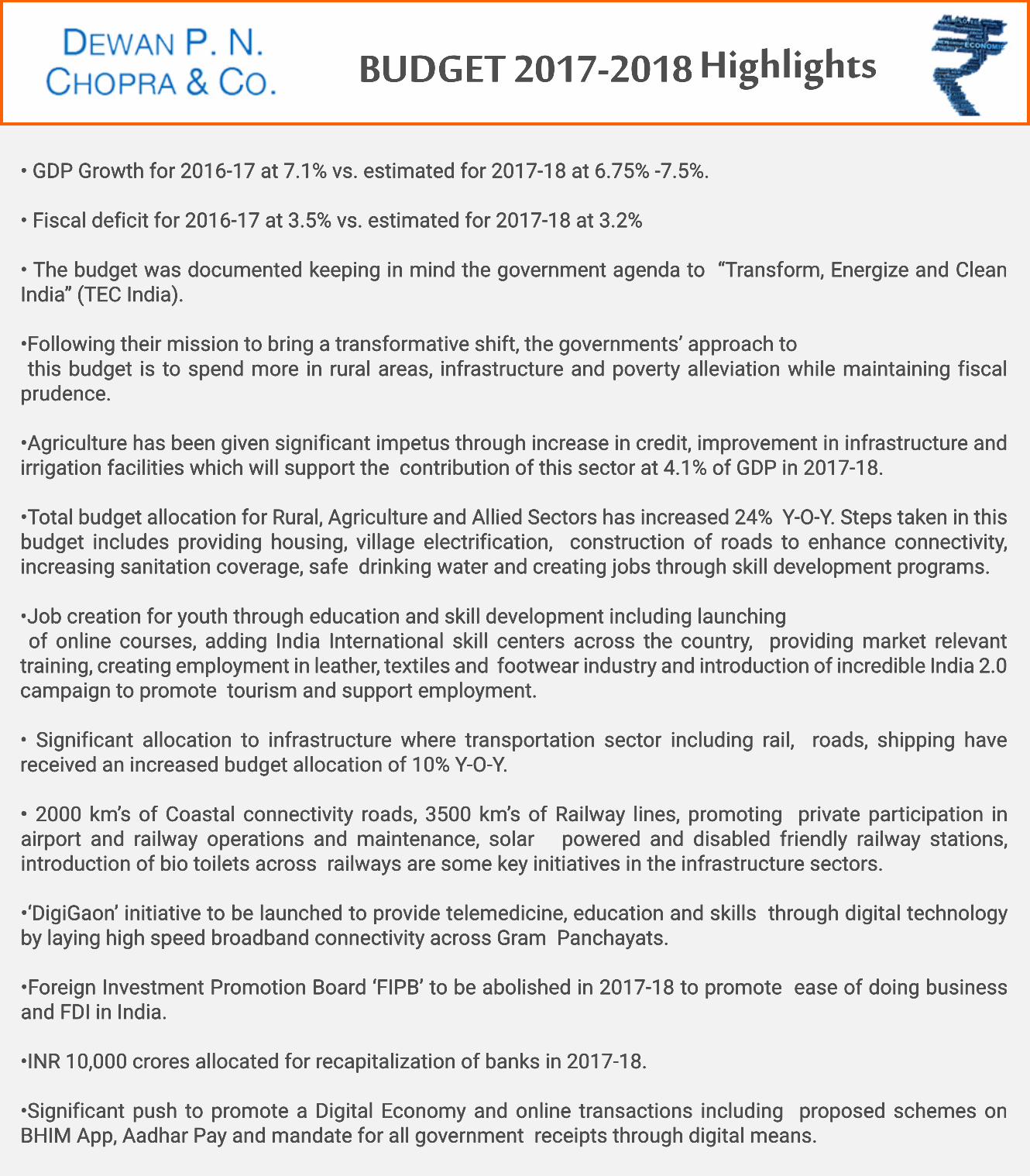

• GDP Growth for 2016-17 at 7.1% vs. estimated for 2017-18 at 6.75% -7.5%.

• Fiscal deficit for 2016-17 at 3.5% vs. estimated for 2017-18 at 3.2%

• The budget was documented keeping in mind the government agenda to “Transform, Energize and Clean India” (TEC India).

•Following their mission to bring a transformative shift, the governments’ approach to this budget is to spend more in rural areas, infrastructure and poverty alleviation while maintaining fiscal prudence.

•Agriculture has been given significant impetus through increase in credit, improvement in infrastructure and irrigation facilities which will support the contribution of this sector at 4.1% of GDP in 2017-18.

•Total budget allocation for Rural, Agriculture and Allied Sectors has increased 24% Y-O-Y. Steps taken in this budget includes providing housing, village electrification, construction of roads to enhance connectivity, increasing sanitation coverage, safe drinking water and creating jobs through skill development programs.

•Job c•Job creation for youth through education and skill development including launching of online courses, adding India International skill centers across the country, providing market relevant training, creating employment in leather, textiles and footwear industry and introduction of incredible India 2.0 campaign to promote tourism and support employment.

• Significant allocation to infrastructure where transportation sector including rail, roads, shipping have received an increased budget allocation of 10% Y-O-Y.

•• 2000 km’s of Coastal connectivity roads, 3500 km’s of Railway lines, promoting private participation in airport and railway operations and maintenance, solar powered and disabled friendly railway stations, introduction of bio toilets across railways are some key initiatives in the infrastructure sectors.

•‘DigiGaon’ initiative to be launched to provide telemedicine, education and skills through digital technology by laying high speed broadband connectivity across Gram Panchayats.

•Foreign Investment Promotion Board ‘FIPB’ to be abolished in 2017-18 to promote ease of doing business and FDI in India.

•INR 10,000 c•INR 10,000 crores allocated for recapitalization of banks in 2017-18.

•Significant push to promote a Digital Economy and online transactions including proposed schemes on BHIM App, Aadhar Pay and mandate for all government receipts through digital means.

BUDGET 2017-2018Highlights

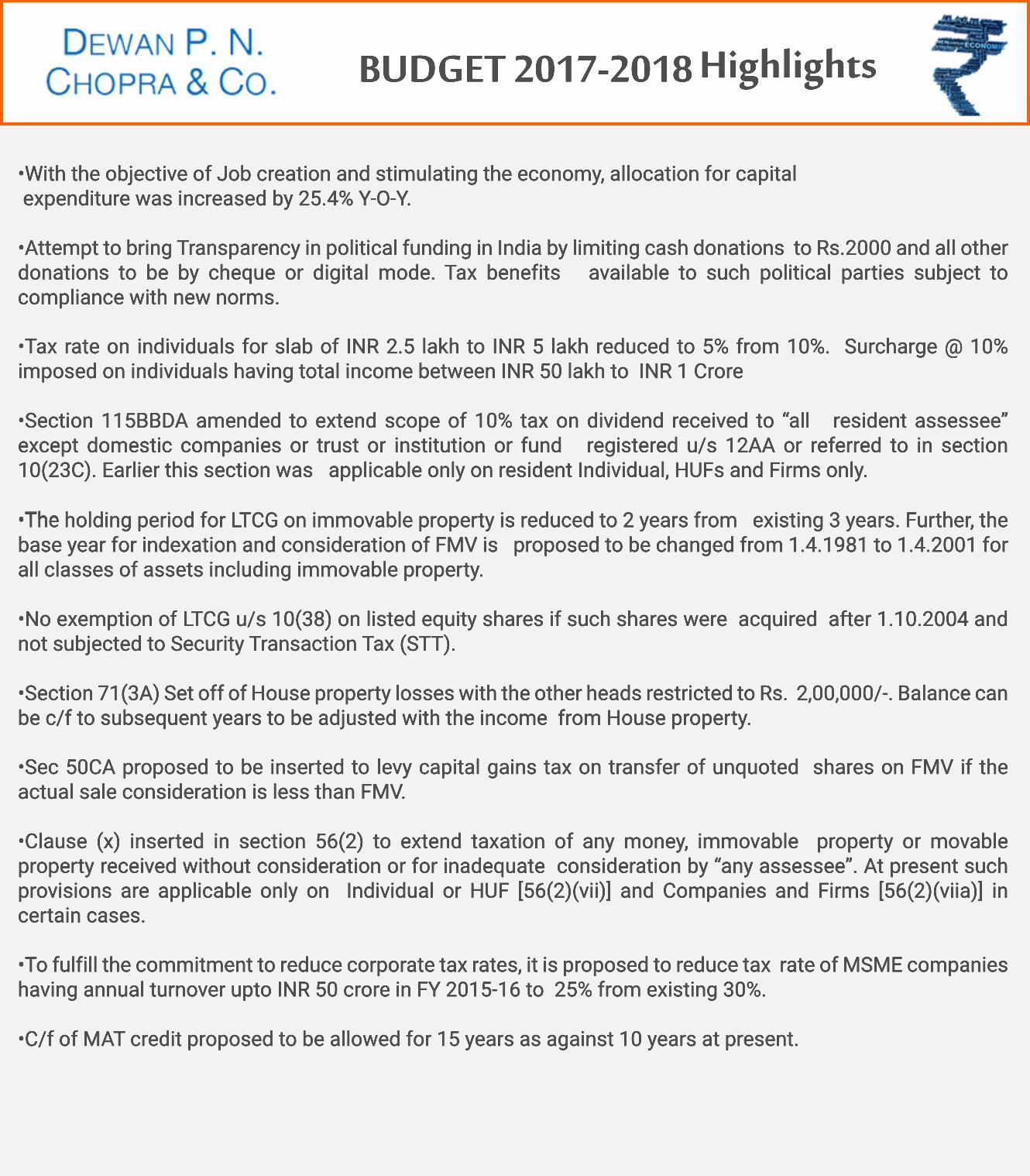

•With the objective of Job creation and stimulating the economy, allocation for capital expenditure was increased by 25.4% Y-O-Y. •Attempt to bring Transparency in political funding in India by limiting cash donations to Rs.2000 and all other donations to be by cheque or digital mode. Tax benefits available to such political parties subject to compliance with new norms.

••Tax rate on individuals for slab of INR 2.5 lakh to INR 5 lakh reduced to 5% from 10%. Surcharge @ 10% imposed on individuals having total income between INR 50 lakh to INR 1 Crore

•Section 115BBDA amended to extend scope of 10% tax on dividend received to “all resident assessee” except domestic companies or trust or institution or fund registered u/s 12AA or referred to in section 10(23C). Earlier this section was applicable only on resident Individual, HUFs and Firms only.

•The•The holding period for LTCG on immovable property is reduced to 2 years from existing 3 years. Further, the base year for indexation and consideration of FMV is proposed to be changed from 1.4.1981 to 1.4.2001 for all classes of assets including immovable property.

•No exemption of LTCG u/s 10(38) on listed equity shares if such shares were acquired after 1.10.2004 and not subjected to Security Transaction Tax (STT).

•Section 71(3A) Set off of House property losses with the other heads restricted to Rs. 2,00,000/-. Balance can be c/f to subsequent years to be adjusted with the income from House property.

•Sec•Sec 50CA proposed to be inserted to levy capital gains tax on transfer of unquoted shares on FMV if the actual sale consideration is less than FMV.

•Clause (x) inserted in section 56(2) to extend taxation of any money, immovable property or movable property received without consideration or for inadequate consideration by “any assessee”. At present such provisions are applicable only on Individual or HUF [56(2)(vii)] and Companies and Firms [56(2)(viia)] in certain cases.

••To fulfill the commitment to reduce corporate tax rates, it is proposed to reduce tax rate of MSME companies having annual turnover upto INR 50 crore in FY 2015-16 to 25% from existing 30%.

•C/f of MAT credit proposed to be allowed for 15 years as against 10 years at present.

BUDGET 2017-2018Highlights

D 295, Defence ColonyNew Delhi – 110024

D 203, Defence ColonyNew Delhi – 110024

C 109 LGF, Defence ColonyNew Delhi – 110024

C 9 LGF, Defence ColonyNew Delhi – 110024

H 57 Connaught CircusNew Delhi 110001

Branch Offices Head Office Follow us on:

•To curb black money, it is proposed to insert Sec 269ST which provides that no person shall receive an amount of INR 300,000 or more otherwise than by A/c payee cheque/ bank draft/ electronic payment. Contravention of 269ST will attract penalty u/s 271DA equivalent to the amount of such receipt.

•Law of limitation - Section 197(C) of the Finance Act’ 2016 which provided for assessment of undisclosed income relating to any period prior to Income Declaration Scheme-1 has been repealed.

•Time limit for scrutiny u/s 153 for assessment of AY 2018-19 reduced to 18 months from 21 months.

•Domestic•Domestic TP scope restricted - DTP not to apply on section 40A(2)(b) transactions.

•Foreign Portfolio Investor, Category I or II exempted from Indirect transfer provisions.

•The Finance Minister has proposed not to make any changes in current regime of excise & service tax as the same are to be replaced by GST soon.

DISCLAIMERThis document has been prepared in a concise summary form by Dewan P. N. Chopra & Co., Chartered Accountants, from public sources believed to be reliable. The information contained herein is intended only for the person to whom it is sent. While the information is believed to be accurate to the best of our knowledge, we do not make any representations or warranties, express or implied, as to the accuracy or completeness of such information. Recipients should conduct and rely upon their own examination, investigation and analysis and are advised to seek their own professional advice. The information and data contained herein is not a substitute for the recipient’s independent evaluation and analysis.and analysis. This document is not an offer, invitation, advice or solicitation of any kind. We accept no responsibility for any errors it may contain, whether caused by negligence or otherwise or for any loss, howsoever caused or

sustained, by the person who relies on it.

Phone: +91-11-2332 2359 / 1418 | Email: [email protected]