Bthma2e Ch04 Sm

186

Chapter 4 Activity-Based Costing, Lean Production, and the Costs of Quality Quick Check Answers: QC4-1. d QC4-3. c QC4-5. c QC4-7. c QC4-9. a QC4-2. d QC4-4. c QC4-6. d QC4-8. d QC4-10. c Chapter 4 Activity-Based Costing and Other Cost Management Tools 282

-

Upload

amanda-barker -

Category

Documents

-

view

94 -

download

4

description

ch 4

Transcript of Bthma2e Ch04 Sm

Chapter 4

Activity-Based Costing, Lean Production, and the Costs of Quality

Quick Check

Answers:

QC4-1. d QC4-3. c QC4-5. c QC4-7. c QC4-9. aQC4-2. d QC4-4. c QC4-6. d QC4-8. d QC4-10. c

Chapter 4 Activity-Based Costing and Other Cost Management Tools 282

Short Exercises(5 min) S 4-1

a. Prevention costs

b. Lean production

c. Activity-based costing

d. Appraisal costs

e. Unit-level costs

f. Value-added activities

g. Internal failure costs

h. Product-level costs

i. Non-value added activities

j. External failure costs

k. Batch-level costs

l. Plantwide overhead rate

m. Cost distortion

n. Facility-level costs

Managerial Accounting 2e Solutions Manual283

(5 min) S 4-2Req. 1

JOB 392 Cutting DepartmentFinishing

DepartmentDepartmental overhead rate $10 per machine

hour$17 per direct

labor hourDirect labor hours incurred in the Finishing Department

× 6 direct labor hours

Machine hours incurred in the Cutting Department

× 8 machine hours

Allocation of manufacturing overhead $80 $102

The total manufacturing overhead allocated to Job 392 is $182. This consists of $80 of manufacturing overhead in the Cutting Department and $102 of manufacturing from the Finishing Department.

Req. 2

The manufacturing cost of Job 392 is determined by summing the three manufacturing costs assigned to the job.

Direct Materials $2,500Direct Labor ($25 per hour × 8 hours) 200Manufacturing overhead 182 Total Job Cost $2,882

Chapter 4 Activity-Based Costing and Other Cost Management Tools 284

(5-10 min) S 4-3

Req. 1

Manufacturing Overhead Machine Hours

Plant-wide Overhead Rate

$3,500,000 ÷ 17,500 = $200 per machine hour

Req. 2

Production Departments

Departmental Manufacturing

OverheadMachine

Hours

Departmental Overhead

RatesPotato Chips $1,800,000 11,250 = $160 per

machine hourCorn Chips $1,000,000 ÷ 3,450 = $289.86

(rounded) per machine hour

Cheese Puffs

$ 700,000 ÷ 2,800 = $250 per machine hour

TOTAL $3,500,000 17,500

Req. 3

The plant-wide overhead rate ($200 per machine hour) had been overcosting potato chips and undercosting corn chips and cheese puffs. The departmental rates more accurately allocate manufacturing overhead costs because they take into consideration the unique amount of manufacturing overhead and machine hours associated with each production department.

Managerial Accounting 2e Solutions Manual285

(5 min.) S 4-4

ActivityManufacturing

Overhead Cost DriverActivity Cost

Allocation Rate

Preparation $600,000 ÷12,000 preparation hours

=$50 per preparation hour

Cooking and Draining

$900,000 ÷

30,000 cooking and draining hours

=

$30 per cooking and draining hour

Packaging $300,000 ÷6,000,000 packages

=$0.05 per package

Chapter 4 Activity-Based Costing and Other Cost Management Tools 286

(5-10 min.) S 4-5

Req. 1 and 2

The total amount of manufacturing overhead allocated to the order (and the amount of manufacturing overhead per bag) is computed as follows:

Activity Cost Allocation Rate Use of Cost Driver

Allocated Manufacturing

Overhead$50 per preparation hour 16 preparation hours $ 800$30 per cooking and

draining hour32 cooking and draining hours 960

$0.05 per package 12,000 bags 600 TOTAL $2,360Number of bags ÷ 12,000Manufacturing overhead per bag $ 0.20 (rounded)

Req. 3

The total manufacturing cost of the order is the sum of the direct materials, direct labor, and manufacturing overhead assigned to the order. Therefore, in addition to the manufacturing overhead computed above, Uncle Bruce will need to determine the cost of direct materials (potatoes) and direct labor incurred by the order before he can arrive at the total cost to manufacture this order.

Managerial Accounting 2e Solutions Manual287

(5-10 min.) S 4-6

Req. 1

Activity

Estimated Total Manufacturing

Overhead Costs

(A)

Estimated Total Usage of

Cost Driver (B)

Activity Cost Allocation Rate

(A ÷ B)Machine set-

up$ 150,000 3,000 set-ups $ 50 per set-

upMachining $1,000,000 5,000 machine

hours$200 per

machine hourQuality control $ 337,500 4,500 tests run $ 75 per test

run

Req. 2

Job Cost RecordJOB #624

Manufacturing Costs

Direct Materials $1,050Direct Labor:

Evan Berg: 10 × $25 = $250Stephanie Berg: 5 × $30 = $150

400

Manufacturing Overhead:1 set-up × $50 / set-up = $505 machine hours × $200 /

machine hour = $1,0002 tests × $75 / test = $150

1,200

TOTAL JOB COST $2,650

Chapter 4 Activity-Based Costing and Other Cost Management Tools 288

(15-20 min.) S 4-7

Req. 1

Narnia TechnologyActivity Cost Allocation

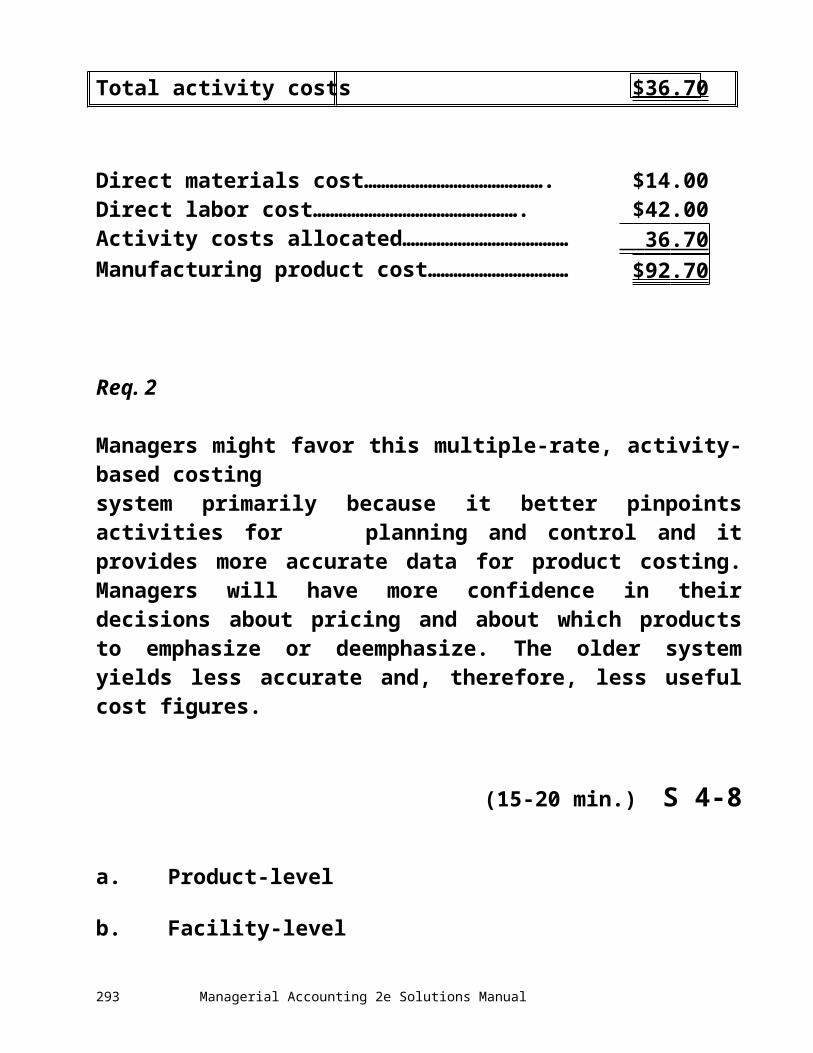

Activity Cost Allocated to Each BoardStart station 1 × $ 0.90 = $ 0.90Dip insertion 20 × $ 0.25 = 5.00Manual insertion 5 × $ 0.40 = 2.00Wave solder 1 × $ 4.50 = 4.50Backload 4 × $ 0.70 = 2.80Test 0.15 × $90.00 = 13.50Defect analysis 0.16 × $50.00 = 8 .00 Total activity costs $36 .70

Direct materials cost……………………………………. $14.00Direct labor cost…………………………………………. $42.00Activity costs allocated………………………………… 36 .70 Manufacturing product cost…………………………… $92 .70

Req. 2

Managers might favor this multiple-rate, activity-based costingsystem primarily because it better pinpoints activities for planning and control and it provides more accurate data for product costing. Managers will have more confidence in their decisions about pricing and about which products to emphasize or deemphasize. The older system yields less accurate and, therefore, less useful cost figures.

Managerial Accounting 2e Solutions Manual289

(15-20 min.) S 4-8

a. Product-level

b. Facility-level

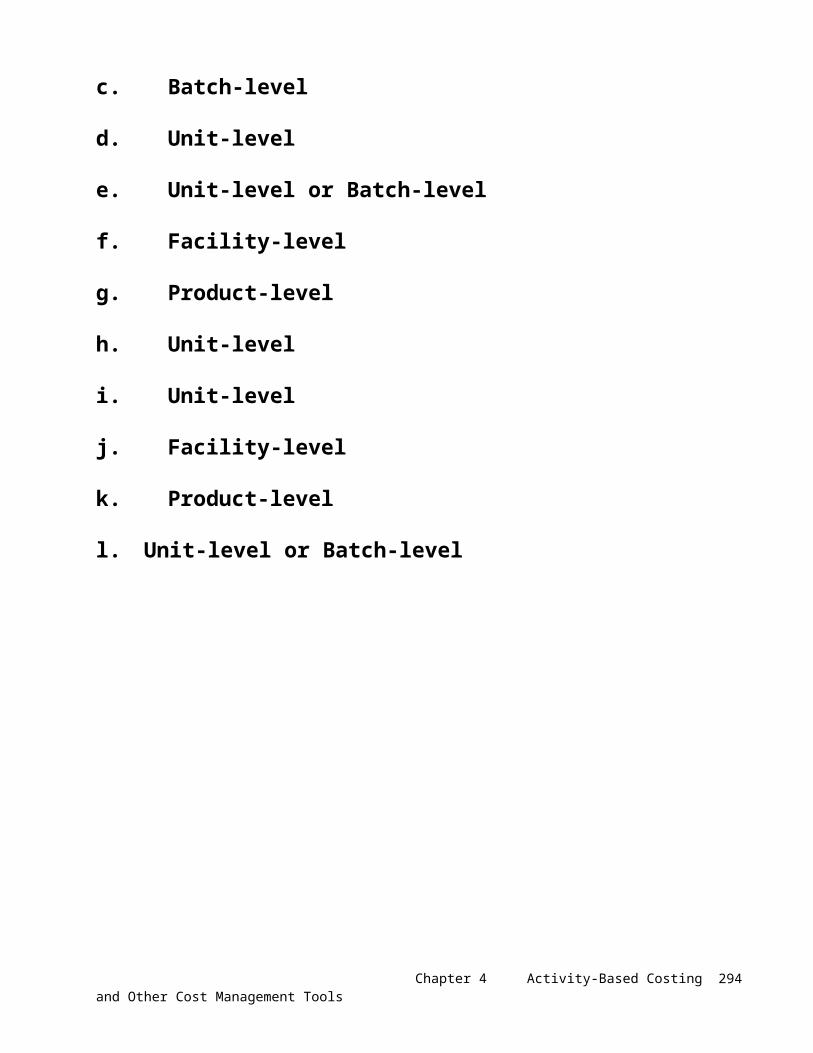

c. Batch-level

d. Unit-level

e. Unit-level or Batch-level

f. Facility-level

g. Product-level

h. Unit-level

i. Unit-level

j. Facility-level

k. Product-level

l. Unit-level or Batch-level

Chapter 4 Activity-Based Costing and Other Cost Management Tools 290

(15-20 min.) S 4-9

1. Unit-level

2. Product-level

3. Unit-level

4. Facility-level

5. Facility-level

6. Product-level

7. Batch-level

8. Product-level

9. Facility-level

10. Facility-level

Managerial Accounting 2e Solutions Manual291

(5 min) S 4-10

1. The company has re-engineered its production process but has not changed its accounting system — more likely

2. The company produces few products, and the products consume resources in a similar manner — less likely

3. The company operates in a very competitive industry — more likely

4. The company has very few indirect costs — less likely

5. The company produces high volumes of some of its products and low volumes of other products — more likely

6. In bidding for jobs, managers lose bids they expected to win and win bids they expected to lose — more likely

Chapter 4 Activity-Based Costing and Other Cost Management Tools 292

(10 min.) S 4-11

Req. 1

Indirect cost=

Estimated total indirect costsallocation rate Estimated total quantity of cost allocation base

=$706,000

5,000 hours

= $141.20 / hour

Req. 2

Webb GregDirect labor (100 hours × $350 / hour) $35,000 $35,000Indirect costs (100 hours × $141.20 / hour) 14,120 14,120 Total costs $49,120 $49,120

Each engagement used the same direct labor hours, so direct labor and indirect costs (allocated based on direct labor hours) are the same for both engagements.

Req. 3

Webb GregService revenue (150% × $35,000) $52,500 $52,500 Direct labor (from Req. 2) 35,000 35,000Indirect costs (from Req. 2) 14,120 14,120 Total costs 49,120 49,120 Operating income $ 3,380 $ 3,380

Managerial Accounting 2e Solutions Manual293

(5-10 min.) S 4-12

There are several warning signs that Mission’s cost system may be “broken”:

1. One client (Webb) is complaining that the firm's fees are too high, while the other client (Greg) called to say he is happy with the fees. This causes a question as to whether Webb’s fees are too high and Greg’s fees are too low.

2. The client complaining about the high fees is an engagement where Nelson felt especially efficient and capable. On the other hand, the client happy with his fees is a complex engagement where Nelson felt less efficient.

3. Mission's competitor (Delta Applications) is able to undercut her fees — even in Mission's area of expertise —and still earn a good profit.

4. Mission's cost system has not changed since the firm was founded.

5. Mission allocates indirect costs using a single allocation base — direct labor hours.

These signals suggest it is time for Nelson to reevaluate her cost system.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 294

(5 min.) S 4-13

Mission, Inc.ABC Cost Allocation Rates

Documentation Preparation

InformationTechnology Support Training

Estimated indirect cost of activity $100,000 $156,000 $450,000

Divide by estimated quantity

of cost allocation base ÷ 3,125 pages ÷ 780 applications ÷ 5,000 DL hours

Cost allocation rate foractivity $ 32 / page $ 200 / application $ 90 / DL

hour

Managerial Accounting 2e Solutions Manual295

(10-15 min.) S 4-14

Req. 1

Webb GregDirect labor (100 hours × $350) $35,000 $35,000Documentation preparation:

( 50 pages × $32) 1,600(300 pages × $32) 9,600

Information technology support: (1 application × $200) 200(78 applications × $200) 15,600

Training (100 hours × $90) 9,000 9,000 Total costs $45,800 $69,200

Req. 2

Webb GregService revenue (150% × $35,000) $52,500 $ 52,500 Direct labor 35,000 35,000Indirect costs:

Documentation preparation 1,600 9,600Information technology support 200 15,600Training 9,000 9,000

Total costs $45,800 $ 69,200 Operating income (loss) $ 6,700 $(16,700 )

Chapter 4 Activity-Based Costing and Other Cost Management Tools 296

(10-15 min.) S 4-15

a. Non-value added

b. Non-value added

c. Value added

d. Non-value added

e. Non-value added

f. Value added

g. Non-value added

h. Non-value added

Managerial Accounting 2e Solutions Manual297

(10-15 min.) S 4-16

1. Non-value added

2. Non-value added

3. Non-value added

4. Value added

5. Non-value added

6. Non-value added

7. Non-value added

8. Value added

Chapter 4 Activity-Based Costing and Other Cost Management Tools 298

(5-10 min.) S 4-17

a. Lean

b. Traditional

c. Traditional

d. Lean

e. Traditional

f. Lean

g. Lean

h. Traditional

i. Lean

j. Lean

k. Lean

l. Lean

m. Traditional

Managerial Accounting 2e Solutions Manual299

(5 min.) S 4-18

1. Reworking defective units — internal failure

2. Litigation costs from product liability claims — external

failure

3. Inspecting incoming raw materials — appraisal

4. Training employees — prevention

5. Warranty repairs — external failure

6. Redesigning the production process — prevention

7. Lost productivity due to machine breakdown — internal

failure

8. Inspecting products that are half the way through the

production process — appraisal

9. Incremental cost of using a higher grade raw material —

prevention

10.Cost incurred producing and disposing of defective units —

internal failure

Chapter 4 Activity-Based Costing and Other Cost Management Tools 300

(10-15 min.) S 4-19

Req. 1

Prevention costs:

Negotiating with and training suppliers to obtain higher

quality materials and on-time delivery.

Redesigning the speakers to make them easier to

manufacture.

Appraisal costs:

Additional 20 minutes of testing for each speaker.

Avoid inspection of raw materials.

Internal failure costs:

Rework avoided because of fewer defective units.

Avoid lost profits from lost production time due to rework.

External failure costs:

Reduced warranty repair costs.

Avoid lost profits from lost sales due to disappointed

customers.

Managerial Accounting 2e Solutions Manual301

(continued) S 4-19

Req. 2

Cost /<Benefit> AnalysisCosts

<Savings>

Prevention costs:Negotiating with and training suppliers to obtain

higher quality materials and on-time delivery…………. $ 300,000Redesigning the speakers to make them

easier to manufacture……………………………………… 1,400,000

Appraisal costs:Additional 20 minutes of testing for each speaker………. 600,000

Savings on Inspection of raw materials………………………. $<400,000>

Internal failure costs:Savings on Rework………………………………………………... <650,000>Savings on Lost profits from lost production time due to

rework……………………………………………………………. <300,000>

External failure costs:Savings on Warranty repair costs……………………………… <200,000>Savings on Lost profits from lost sales due to

disappointed customers…………………………………........ <850,000 >

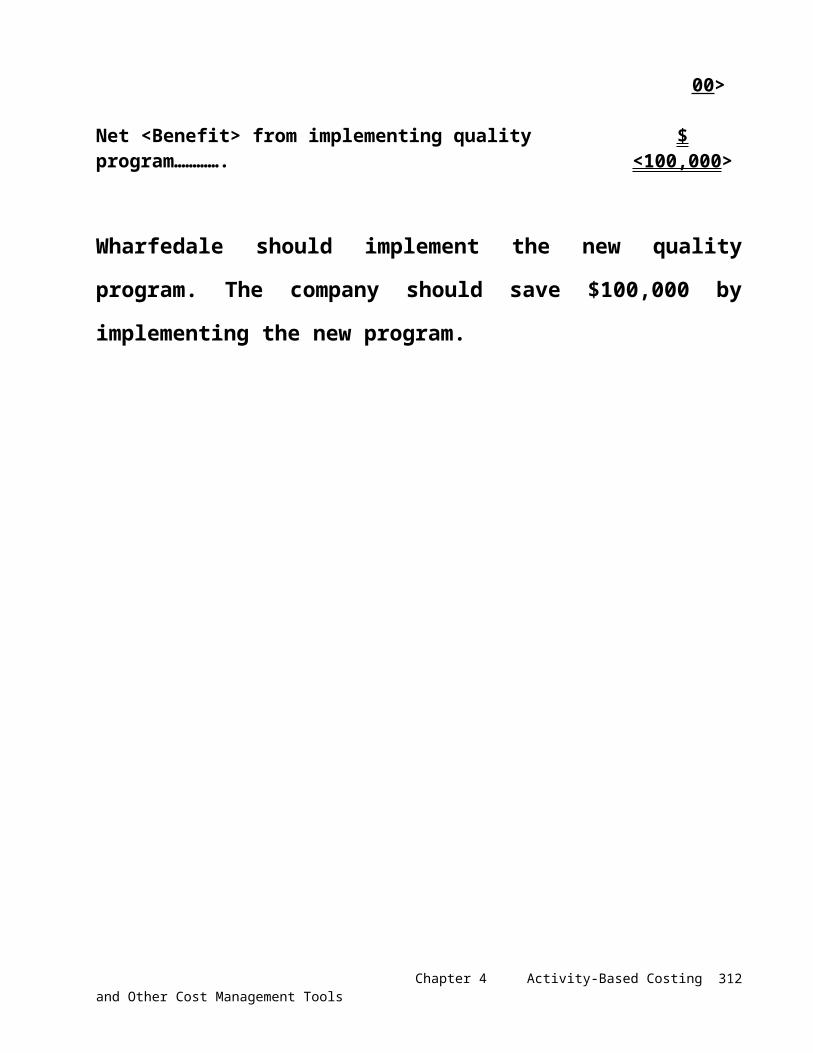

Net <Benefit> from implementing quality program…………. $ <100,000 >

Wharfedale should implement the new quality program. The

company should save $100,000 by implementing the new

program.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 302

(5-10 min.) S 4-20

1. External failure cost

2. External failure cost

3. External failure cost

4. Appraisal cost

5. Prevention cost

6. Internal failure cost

Managerial Accounting 2e Solutions Manual303

Exercises (Group A)

(15-20 min.) E 4-21A

Req. 1

Plant-wideallocation rate

==

Estimated total indirect costsEstimated total quantity of cost allocation

base

==

$1,100,00025,000* direct labor

hours

= $44 per direct labor hour

*When calculating plant-wide overhead rates, all direct labor hours incurred in the plant are used.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 304

(continued) E 4-21A

Req. 2

Departmental cost allocation rate =

Estimated total indirect costs of department

Estimated total quantity of cost allocation

base used in department

Machining Dept. overhead rate

=$750,000

15,000 machine hours

= $50 per machine hour

Finishing Dept. overhead rate

=$350,000

17,500** direct labor hours

= $20 per direct labor hour

**When calculating the finishing departmental rate, only the direct labor hours incurred in the finishing department are used.

Managerial Accounting 2e Solutions Manual305

(continued) E 4-21A

Req. 3

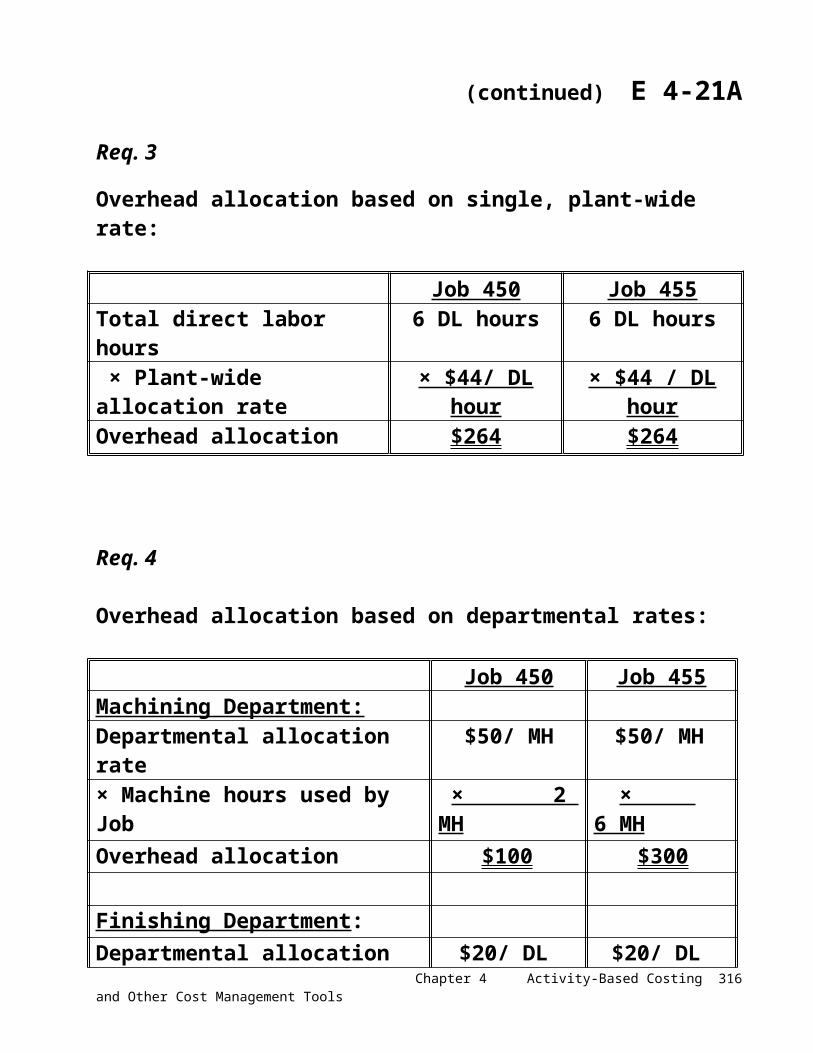

Overhead allocation based on single, plant-wide rate:

Job 450 Job 455Total direct labor hours 6 DL hours 6 DL hours × Plant-wide allocation rate × $44/ DL hour × $44 / DL hourOverhead allocation $264 $264

Req. 4 Overhead allocation based on departmental rates:

Job 450 Job 455Machining Department:Departmental allocation rate $50/ MH $50/ MH× Machine hours used by Job × 2 MH × 6 MHOverhead allocation $100 $300

Finishing Department:Departmental allocation rate $20/ DL hr $20/ DL hr× DL hours used by Job × 5 DL hrs × 4 DL hrsOverhead allocation $100 $80

Total overhead allocation (fromboth departments $200 $380

Chapter 4 Activity-Based Costing and Other Cost Management Tools 306

(continued) E 4-21A

Req. 5

The single plant-wide overhead rate assigns the same amount

of manufacturing overhead to both jobs ($264). On the other

hand, the departmental allocation rates assign $200 of

manufacturing overhead to Job 450 and $380 of manufacturing

overhead to Job 455. The single plant-wide rate overcosts Job

450 by $64 ($264 − $200) and undercosts Job 455 by $116 ($380

− $264). Since Cermak sets his sales price at 125% of cost, and

the job cost is affected by the allocation system he uses, his

sales price will also be affected by the allocation system he

uses.

Managerial Accounting 2e Solutions Manual307

(15-20 min.) E 4-22A

Req. 1

NorthstarComputation of Indirect Cost Allocation Rates

Activity

Total Estimated

Cost

Estimated Quantity of

Cost Allocation

Base

ActivityCost Allocation

RateMaterials handling $12,000 ÷ 3,000 parts = $ 4.00 per partMachine setups $ 3,400 ÷ 10 setups = $340.00 per setupInsertion of parts $48,000 ÷ 3,000 parts = $ 16.00 per partFinishing $80,000 ÷ 2,000 hours = $ 40.00 per hour

Chapter 4 Activity-Based Costing and Other Cost Management Tools 308

(continued) E 4-22A

Req. 2

The amount of manufacturing overhead to be assigned to Job 420 is computed as follows

Northstar- Job 420Manufacturing overhead allocation

Activity

Actual Quantity of Cost Allocation

Base Used

Cost Allocation

RateMOH

assignedMaterials handling 150 parts × $4.00/part = $ 600

Machine setups 1 setups × $340.00/setup = 340Insertion of parts 150 parts × $16.00/part = 2400Finishing 120 hours × $ 40.00/hr = 4800 Total manufacturing

overhead $8,140

Managerial Accounting 2e Solutions Manual309

(continued) E 4-22A

Req. 3

The amount of manufacturing overhead to be assigned to Job 510 is computed as follows

Northstar- Job 510Manufacturing overhead allocation

Activity

Actual Quantity of Cost Allocation

Base Used

Cost Allocation

RateMOH

assignedMaterials handling 425 parts × $4.00/part = $ 1700

Machine setups 2 setups × $340.00/setup = 680Insertion of parts 425 parts × $16.00/part = 6800Finishing 320 hours × $ 40.00/hr = 12,800 Total manufacturing

overhead $21,980

Chapter 4 Activity-Based Costing and Other Cost Management Tools 310

(15-20 min.) E 4-23A

Req. 1

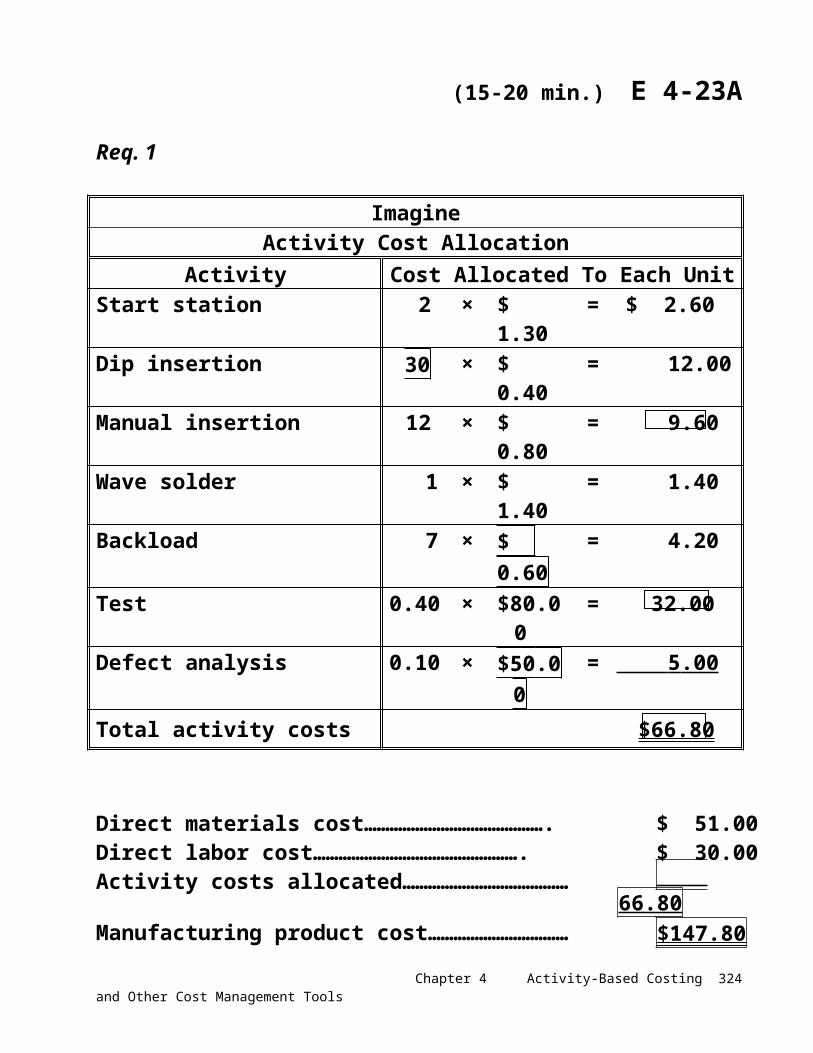

ImagineActivity Cost Allocation

Activity Cost Allocated To Each UnitStart station 2 × $ 1.30 = $ 2.60Dip insertion 30 × $ 0.40 = 12.00Manual insertion 12 × $ 0.80 = 9.60Wave solder 1 × $ 1.40 = 1.40Backload 7 × $ 0.60 = 4.20Test 0.40 × $80.00 = 32.00Defect analysis 0.10 × $50.00 = 5 .00

Total activity costs $66 .80

Direct materials cost……………………………………. $ 51.00Direct labor cost…………………………………………. $ 30.00Activity costs allocated………………………………… 66.80 Manufacturing product cost…………………………… $147.80

Req. 2

Managers might favor this multiple-rate, activity-based costing

system primarily because it better pinpoints activities for

planning and control and it provides more accurate data for

product costing. Managers will have more confidence in their

decisions about pricing and about which products to

emphasize or de-emphasize. The older system yields less

accurate, and therefore less useful, cost figures.

Managerial Accounting 2e Solutions Manual311

(15-20 min) E 4-24AReq. 1

Operatingoverhead

Total professional hours

Current operating overhead allocation rate

$234,000 ÷ 10,000 =$23.40 per

professional hour

Req. 2

Billing Calculations for the Amy Lee Kitchen Remodeling JobBased on current allocation system

Professional time (24 hours × $65 per hour) $1,560.00Operating overhead (24 hours × $23.40 per hour) + 561 .60 Total cost of job $2,121.60Markup on cost × 135 %Bill to client $2,864 .16

Req. 3

Activity CostTotal activity

allocation baseActivity

allocation rateTransportation

to clients $ 9,000 ÷15,000a

miles driven = $0.60 per mileBlueprint

copying 35,000 ÷1,000b

copies = $35 per copyOffice

support 190,000 ÷5,000c

secretarial hours =$38 per secretarial hour

To calculate the activity cost allocation rates, you must use the total activity for the year:a 3,000 + 12,000 = 15,000b 300 + 700 = 1,000c 2,200 + 2,800 = 5,000

Chapter 4 Activity-Based Costing and Other Cost Management Tools 312

(continued) E 4-24A

Req. 4

Billing Calculations for the Amy Lee Kitchen Remodeling JobBased on ABC information

Professional time (24 hours × $65 per hour) $1,560.00Operating overhead:

125 miles × $0.60 per mile = $754 blueprints × $35 per copy = $14018 secretarial hours × $38 per secretarial hour =

$684 + 899.00 Total cost of job $2,459.00Markup on cost × 135 %Bill to client $3,319.65

Req. 5

The billing system based on ABC costs should be fairer to

clients because they are charged according to the resources

they used. For example, copying blueprints is very expensive.

Under ABC, clients are charged according to how many or how

few blueprint copies their job required. The ABC system better

recognized the extent to which operating costs are incurred by

each unique client job.

Managerial Accounting 2e Solutions Manual313

Chapter 4 Activity-Based Costing and Other Cost Management Tools 314

(20-25 min.) E 4-25A

Req. 1

First, compute the current plant-wide manufacturing overhead rate:

Total manufacturing

overheadTotal direct labor hours

Plant-wide overhead rate

$800,000 ÷ 25,000 =$32 per

direct labor hour

Then, apply it to the two products:

Manufacturing CostMedium (42-inch)

Large (63 inch)

Direct materials $ 660,000 $1,240,000Direct labor 216,000 384,000Manufacturing overhead:

( 9,000 DL hours × $32) = 288,000 (16,000 DL hours × $32) = 512,000

Total manufacturing cost $1,164,000 $2,136,000Number of units produced ÷ 3,000 ÷ 4,000 Cost per unit $ 388 $ 534

Managerial Accounting 2e Solutions Manual315

(continued) E 4-25A

Req. 2

First, compute the activity cost allocation rates:

Activity

Manufacturingoverhead related

to activityTotal activity

allocation baseActivity

allocation rate

Materials handling $150,000 ÷

500a

material orders handled =

$300 per material order handled

Machine processing 560,000 ÷

40,000b machine hours =

$14 per machine hour

Packaging 90,000 ÷

10,000c packaging hours =

$9 per packaging hour

You must use the TOTAL activity for the year as follows. Since

Owens only manufactures two products, you add the activity of

each of the individual products to find the total activity:a 300 + 200 = 500b 20,000 + 20,000 = 40,000c 4,000 + 6,000 = 10,000

Chapter 4 Activity-Based Costing and Other Cost Management Tools 316

(continued) E 4-25A

Req. 2 (continued)

Then, apply them to the two products:

Manufacturing CostMedium (42-inch)

Large (63 inch)

Direct materials $ 660,000 $1,240,000Direct labor 216,000 384,000Manufacturing overhead:Medium:

(300 material orders × $300 = $90,000)

(20,000 machine hours ×$14 = $280,000)

(4,000 packaging hours × $9 = $36,000)

Total allocation of overhead 406,000 Large:

(200 material orders × $300 = $60,000)

(20,000 machine hours ×$14 = $280,000)

(6,000 packaging hours ×$9 = $54,000)

Total allocation of overhead 394,000 Total manufacturing cost $1,282,000 $2,018,000Number of units produced ÷ 3,000 ÷ 4,000 Cost per unit $ 427.33 $ 504.50

Managerial Accounting 2e Solutions Manual317

(continued) E 4-25A

Req. 3

Medium Large Cost per unit using current

system $ 388.00 $ 534.00Cost per unit using ABC 427.33 504.50 Overcosting / (Undercosting) ($ 39.33) $ 29.50Number of units × 3,000 × 4,000 Total cost distortion ($117,990)* $118,000*

* The $10 difference between the total amount overcosted and undercosted is due to the fact that unit answers were rounded to the nearest cent.

The Medium units had been undercosted and the Large units

had been overcosted. Since Owen’s sets its sales price at 300%

of manufacturing cost, the resulting sales price should have

been about $118 higher for the Medium units ($39.33 × 300%)

and about $88.50 lower for the Large units ($29.50 × 300%).

This helps to explain why Owens is the low cost leader for

Medium plasma TVs, but faces competitive pressure on the

Large plasma TVs.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 318

(20-30 min.) E 4-26A

Req. 1

EnkeTotal Budgeted Indirect Manufacturing Costs

Activity

Budgeted Quantity of

Cost Allocation Base

Activity Cost

Allocation Rate

Total Budgeted

Indirect CostMaterials handling 10,000a $ 3.75 $ 37,500Machine setups 30b $300.00 9,000Insertion of parts 10,000a $ 24.00 240,000Finishing 3,500c $ 50.00 175,000 Total budgeted indirect cost $461,500

__________a (4 × 1,000) + (6 × 1,000)b 15 + 15c (1 × 1,000) + (2.5 × 1,000)

Managerial Accounting 2e Solutions Manual319

(continued) E 4-26A

Req. 2

EnkeABC Indirect Manufacturing Cost per Unit

Activity

CostAllocation

Rate

Quantity of Cost Allocation Base

Used By:Allocated Activity Cost Per Wheel

Standard Deluxe Standard DeluxeMaterials handling

$ 3.75 4 6 $ 15.00 $ 22.50

Machine setups

$300.00 0.015* 0.015* 4.50 4.50

Insertion of parts

$ 24.00 4 6 96.00 144.00

Finishing $ 50.00 1.0 2.5 50.00 125.00 Total ABC allocated indirect cost

$165.50 $296.00

__________*15 setups ÷ 1,000 wheels = 0.015 per wheel

Chapter 4 Activity-Based Costing and Other Cost Management Tools 320

(continued) E 4-26A

Req. 3

Budgeted total manufacturing overhead cost = $461,500 (Req. 1)

Budgeted total direct labor hours = (1,000 × 2) + (1,000 × 3)= 2,000 + 3,000= 5,000

Plant-wide overhead allocation =$461,500

5,000

= $92.30 per direct labor hour

Manufacturing overhead cost per wheel:

Standard model: 2 × $92.30 = $184.60Deluxe model: 3 × $92.30 = $276.90

Chapter 4 Activity-Based Costing and Other Cost Management Tools 320

(continues E 4-26A) (15-20 min.) E 4-27A

The Manufacturing overhead costs per wheel computed in E 4-36A are as follows:

EnkeManufacturing overhead Costs per Unit

ModelStandard Deluxe

ABC costs $165.50 $296.00Plant-wide overhead rate $184.60 $276.90

Req. 1

The gross profits (using ABC Data) for the two models are:

EnkeGross profit per unit using ABC Data

Standard DeluxeSale price $300 .00 $440 .00 Direct materials 30.00 46.00Direct labor 45.00 50.00Manufacturing overhead 165 .50 296 .00 Gross profit $ 59 .50 $ 48 .00

Managerial Accounting 2e Solutions Manual321

(continued) E 4-27A

Req. 2

EnkeGross profit per unit using Plant-wide overhead Rate

Standard DeluxeSale price $300 .00 $440 .00 Direct materials 30.00 46.00Direct labor 45.00 50.00Manufacturing overhead 184 .60 276 .90 Gross profit $ 40 .40 $ 67 .10

If they rely on the plant-wide allocation rate data, Enke’s

managers will produce the deluxe model. It will appear to

maximize income.

Req. 3

The standard model is more profitable than the deluxe model.

Activity-based costing data generally are more accurate than

cost data generated by a plant-wide overhead allocation rate.

ABC systems have more cost categories (activities), each with

its own allocation base. ABC cost assignments more accurately

represent the cost of resources consumed to manufacture (and

support) products.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 322

(continued) E 4-27A

Req. 4

The ABC system is likely to pass the cost-benefit test because

Enke manufactures two different products that use different

amounts of resources. The old cost system appears “broken”

because profits at the company declined when the product mix

was shifted to the product that appeared most profitable under

the old costing system. In addition, the production process

had been reengineered but the old plantwide single-allocation-

base costing system had not.

Managerial Accounting 2e Solutions Manual323

(15-20 min.) E 4-28A

Req. 1

Either the materials handling cost or the grinding cost is

inaccurate. Both costs were assigned based on the number of

parts. Thus, the ratio of Job 409 materials handling cost to Job

622 materials handling cost should be the same as the ratio of

Job 409 grinding cost to Job 622 grinding cost. The materials

handling cost ratio is 1:3 ($500 to $1,500), but the grinding cost

ratio is 1:5 ($300 to $1,500). Job 622 cannot have three times as

many parts as Job 409 and five times as many parts

simultaneously.

Req. 2

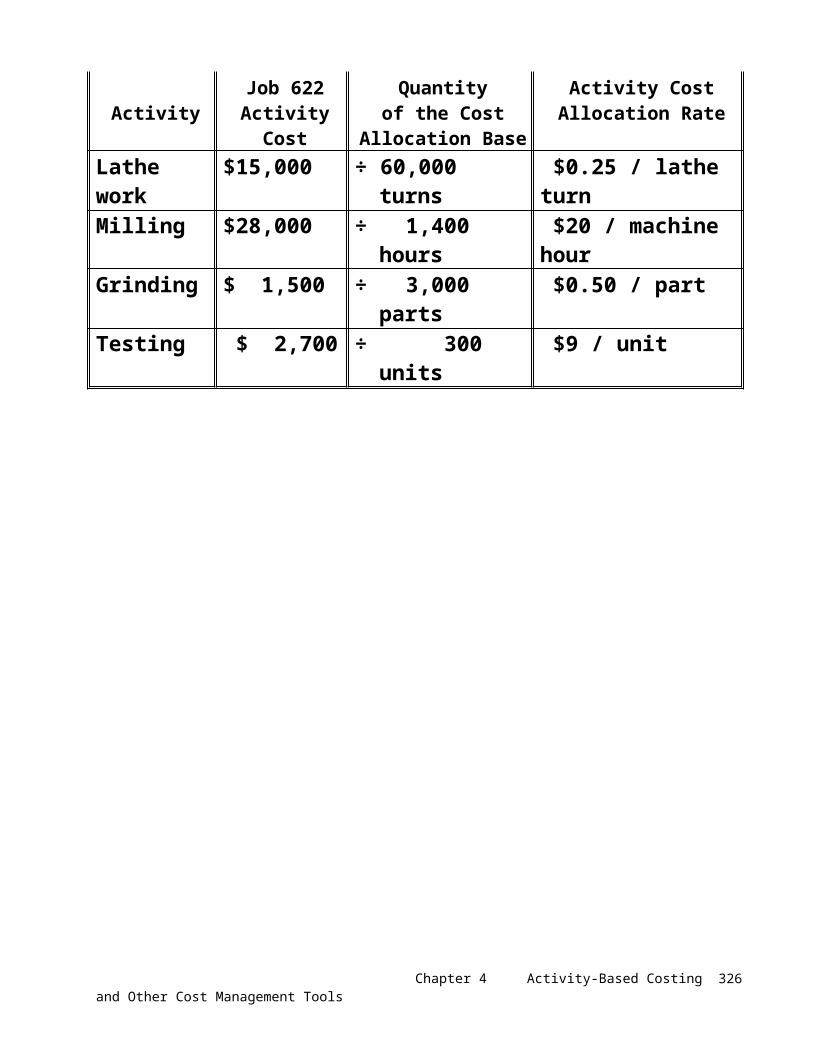

The first step is to determine the allocation rate for each of the four activities:

Channell FabricatorsABC Allocation Rates

ActivityJob 622

Activity Cost

Divide by Quantity of the Cost

Allocation BaseActivity Cost

Allocation RateLathe work $15,000 ÷ 60,000 turns $0.25 / lathe turnMilling $28,000 ÷ 1,400 hours $20 / machine hourGrinding $ 1,500 ÷ 3,000 parts $0.50 / partTesting $ 2,700 ÷ 300 units $9 / unit

Chapter 4 Activity-Based Costing and Other Cost Management Tools 324

(continued) E 4-28A

Req. 2 (continued)

The second step is to use the cost allocation rate for each activity to determine the quantity of the allocation base Job 409 used.

Channell FabricatorsQuantity of the Allocation Base Used by Job 409

ActivityJob 409

Activity CostDivide by

Activity Cost Allocation Rate

Quantity of the Allocation Base Used by Job 409

Lathe work $5,000 ÷ $0.25 / turn 20,000 turnsMilling $4,000 ÷ $20 / hour 200 hoursGrinding $ 300 ÷ $0.50 / part 600 partsTesting $ 126 ÷ $9 / unit 14 units

Req. 3

Based on the ABC information, Channell should not accept the

company's offer to test units for $13 each. Channell’s cost of

performing this activity is only $9 per unit ($2,700 ÷ 300 units

tested for Job 622).

Managerial Accounting 2e Solutions Manual325

(15-20 min) E 4-29A

Traditional and lean systems vary greatly along several dimensions of production. Some of the differences are as follows:

1. Inventory levels — Lean production systems strive to maintain low inventory levels. Lean producers try to purchase raw materials “just in time” to meet the production schedule, and have the finished inventory ready “just in time” to meet customer demand. Traditional production systems maintain greater quantities of raw materials, work in process, and finished goods inventory.

2. Batch sizes — Lean production systems produce units in much smaller batches than traditional production systems. These batches are “demand-pulled” through production, rather than “pushed through” production (like a traditional system), allowing the company to only produce what customers have ordered.

3. Set-up times — Lean production systems stress short set-up times so that they can produce and deliver the product to the end customer in a very short amount of time. By keeping set-up times short, lean producers don’t have to worry about keeping extra inventory on hand just to be able to quickly meet demand.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 326

(continued) E 4-29A

4. Physical layout of plant — Lean producers tend to physically organize their manufacturing plants by self-contained production cells. Each cell contains all of the machinery necessary to produce the product. By organizing the plant this way, lean producers are able to minimize interruptions and time spent moving materials and work in process inventory. This, in turn, reduces the time it takes to produce the product. In contrast, traditional producers tend to group like machinery together in different areas of the plant.

5. Roles of plant employees — At lean producers, plant employees tend to have broader roles. They are cross-trained to perform about every role that is needed in each production cell. They set-up, operate, and repair the machines in the cell. They also perform the quality inspections. As a result, employees tend to have higher morale. Additionally, this decreases bottlenecks caused by having to wait for the “right person” to come do the job.

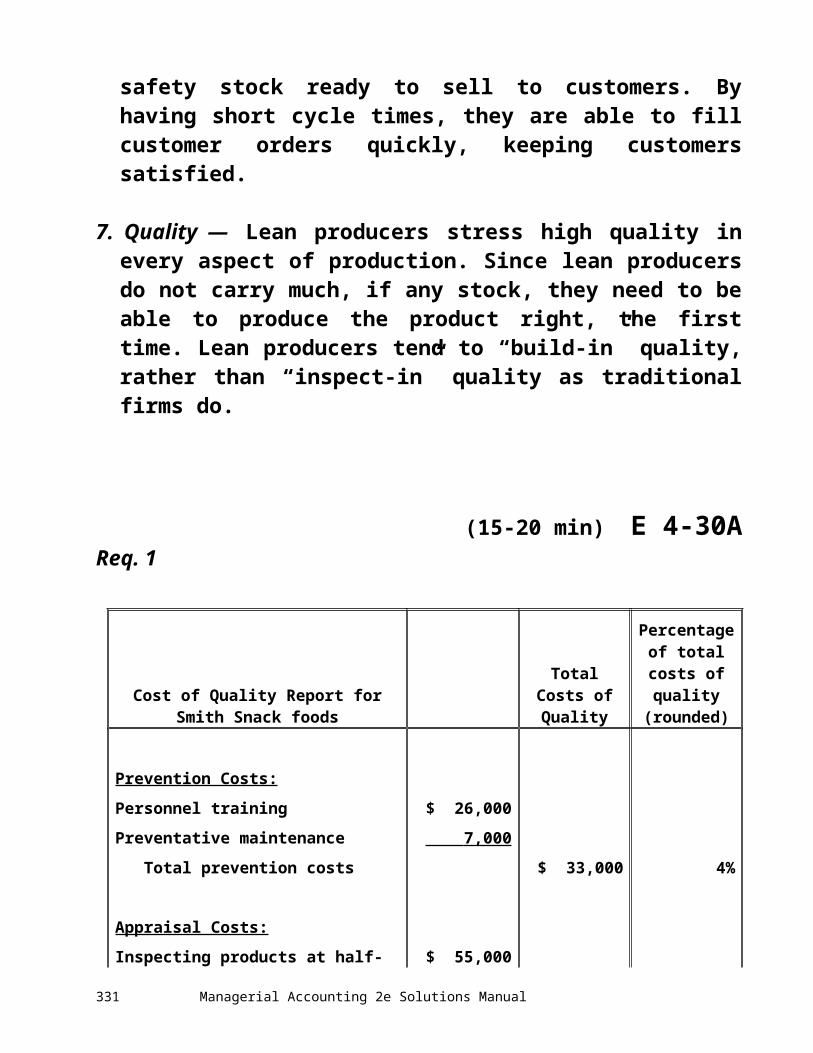

6. Manufacturing cycle times — Lean producers put great emphasis on shortening their manufacturing cycle times. Lean producers need to have short cycle times since they have very little, if any, safety stock ready to sell to customers. By having short cycle times, they are able to fill customer orders quickly, keeping customers satisfied.

7. Quality — Lean producers stress high quality in every aspect of production. Since lean producers do not carry much, if any stock, they need to be able to produce the product right, the first time. Lean producers tend to “build-in” quality, rather than “inspect-in” quality as traditional firms do.

Managerial Accounting 2e Solutions Manual327

(15-20 min) E 4-30AReq. 1

Cost of Quality Report for Smith Snack foods

Total Costs of Quality

Percentage of total costs of quality

(rounded)

Prevention Costs:

Personnel training $ 26,000

Preventative maintenance 7,000

Total prevention costs $ 33,000 4%

Appraisal Costs:

Inspecting products at half-way point $ 55,000

Inspection of raw materials 5,000

Total appraisal costs $ 60,000 7%

Internal Failure Costs:

Production loss due to machine breakdowns $ 15,000

Cost of defective products 94,000

Cost of disposing of rejected products 12,000

Total internal failure costs $121,000 15%

External Failure Costs:

Recall of Batch #59374 $175,000

Warranty claims 420,000

Total external failure costs $595,000 74%

Total Costs of Quality $809,000 100%

Chapter 4 Activity-Based Costing and Other Cost Management Tools 328

(continued) E 4-30AReq. 2

Because the company has warranty returns and has had a

product recall, the company may suffer from a reputation for

poor quality products. If so, they are probably losing profits

from losing sales. Unsatisfied customers will be reluctant to

buy from the company again. They may also tell their friends

and family not to buy from the company. This report does not

include an estimate of the lost profits arising from a reputation

for poor-quality products.

Req. 3

The Cost of Quality report shows that very little is being spent

on prevention and appraisal, which is probably why the internal

and external failure costs are so high. It appears that the

company is only inspecting the product half-way through the

production process, and not again at the end of the process.

Perhaps that is the reason their external failure costs are so

high. The CEO should use this information to develop quality

initiatives in the areas of prevention and appraisal. Such

initiatives should reduce future internal and external failure

costs.

Managerial Accounting 2e Solutions Manual329

(15-20 min.) E 4-31A

Req. 1

Prevention costs:

Training employees in TQM

Training suppliers in TQM

Identifying preferred suppliers who commit to on-time

delivery of perfect quality materials

Appraisal costs:

Strength-testing one item from each batch of panels

Avoid inspection of raw materials

Internal failure costs:

Avoid rework and spoilage

External failure costs:

Avoid lost profits from lost sales due to disappointed

customers

Avoid warranty costs

Chapter 4 Activity-Based Costing and Other Cost Management Tools 330

(continued) E 4-31A

Req. 2

Cost / <Benefit> Analysis Cost/<Savings>

Prevention costs:Training employees in TQM…………………………… $ 30,000Training suppliers in TQM……………………………... 40,000Identifying preferred suppliers who commit to on-

time delivery of perfect quality materials……….. 60,000

Appraisal costs:Strength-testing one item from each batch of

panels…………………………………………………... 65,000

Savings on Inspection of raw materials………………… $ <45,000>

Internal failure costs:Savings on Rework and spoilage…………………….. <55,000>

External failure costs:Savings on Lost profits from lost sales due to

disappointed customers……………………………. <90,000>Savings on Warranty costs……………………………….. < 15,000>

Net <Benefit> ………………………………………………... $<10,000>

Chihooli should adopt the new quality program. The program should save the company $10,000

Managerial Accounting 2e Solutions Manual331

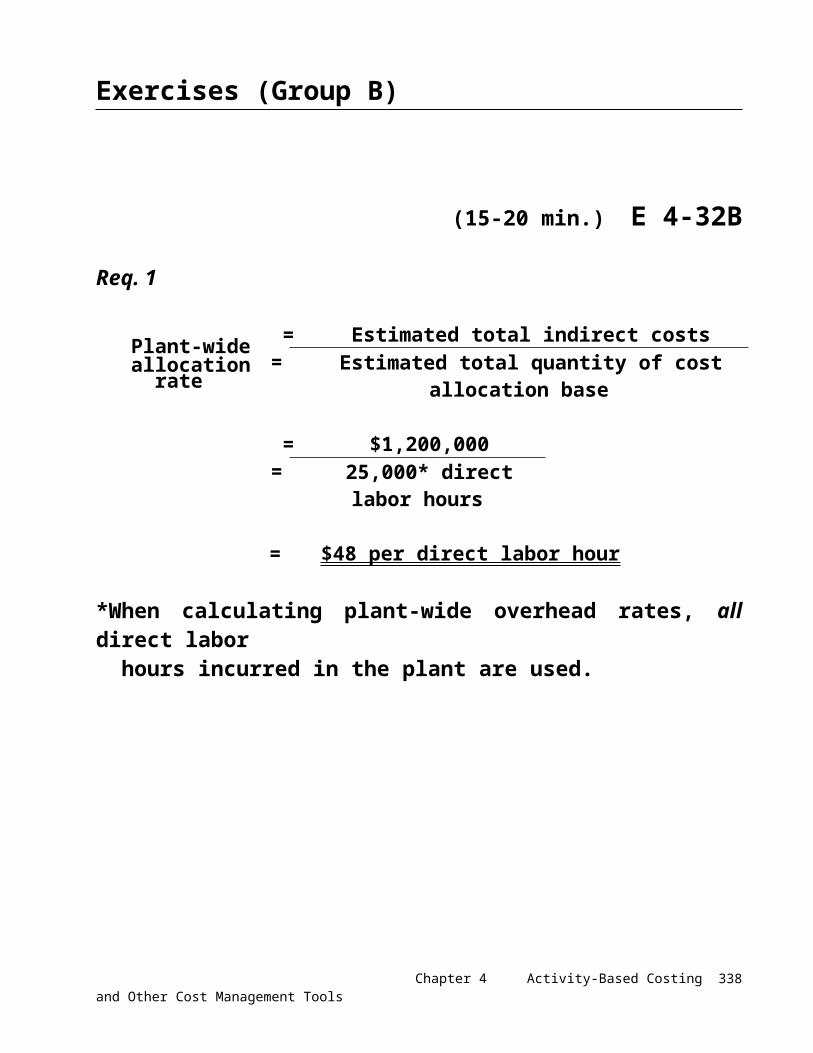

Exercises (Group B)

(15-20 min.) E 4-32B

Req. 1

Plant-wideallocation rate

==

Estimated total indirect costsEstimated total quantity of cost allocation

base

==

$1,200,00025,000* direct labor

hours

= $48 per direct labor hour

*When calculating plant-wide overhead rates, all direct labor hours incurred in the plant are used.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 332

(continued) E 4-32B

Req. 2

Departmental cost allocation rate =

Estimated total indirect costs of department

Estimated total quantity of cost allocation

base used in department

Machining Dept. overhead rate

=$800,000

15,400 machine hours

= $52 per machine hour*

Finishing Dept. overhead rate

=$400,000

17,800** direct labor hours

= $23 per direct labor hour*

*Rounded to the nearest dollar.**When calculating the finishing departmental rate, only the direct labor hours incurred in the finishing department are used.

Managerial Accounting 2e Solutions Manual333

(continued) E 4-32B

Req. 3

Overhead allocation based on single, plant-wide rate:

Job 450 Job 455Total direct labor hours 7 DL hours 7 DL hours × Plant-wide allocation rate × $48/ DL hour × $48/ DL hourOverhead allocation $336 $336

Req. 4 Overhead allocation based on departmental rates:

Job 450 Job 455Machining Department:Departmental allocation rate $52/ MH $52/ MH× Machine hours used by Job × 3 MH × 4 MHOverhead allocation $156 $208

Finishing Department:Departmental allocation rate $23/ DL hr $23/ DL hr× DL hours used by Job × 6 DL hrs × 5 DL hrsOverhead allocation $138 $115

Total overhead allocation (fromboth departments $294 $323

Chapter 4 Activity-Based Costing and Other Cost Management Tools 334

(continued) E 4-32B

Req. 5

The single plant-wide overhead rate assigns the same amount

of manufacturing overhead to both jobs ($336). On the other

hand, the departmental allocation rates assign $294 of

manufacturing overhead to Job 450 and $323 of manufacturing

overhead to Job 455. The single plant-wide rate overcosts Job

450 by $42 ($336 − $294) and overcosts Job 455 by $13 ($336 −

$323). Since Garvey sets his sales price at 125% of cost, and

the job cost is affected by the allocation system he uses, his

sales price will also be affected by the allocation system he

uses.

Managerial Accounting 2e Solutions Manual335

(15-20 min.) E 4-33B

Req. 1

Central PlainComputation of Indirect Cost Allocation Rates

Activity

Total Estimated

Cost

Estimated Quantity of

Cost Allocation

Base

ActivityCost Allocation

RateMaterials handling $ 5,600 ÷ 2,800 parts = $ 2.00 per partMachine setups $ 6,400 ÷ 20 setups = $320.00 per setupInsertion of parts $39,200 ÷ 2,800 parts = $ 14.00 per partFinishing $96,800 ÷ 2,200 hours = $ 44.00 per hour

Chapter 4 Activity-Based Costing and Other Cost Management Tools 336

(continued) E 4-33B

Req. 2

The amount of manufacturing overhead to be assigned to Job 420 is computed as follows

Central Plain - Job 420Manufacturing overhead allocation

Activity

Actual Quantity of Cost Allocation

Base Used

Cost Allocation

RateMOH

assignedMaterials handling 250 parts × $2.00/part = $ 500

Machine setups 3 setups × $320.00/setup = 960Insertion of parts 250 parts × $14.00/part = 3,500Finishing 130 hours × $ 44.00/hr = 5,720 Total manufacturing

overhead $10,680

Managerial Accounting 2e Solutions Manual337

(continued) E 4-33B

Req. 3

The amount of manufacturing overhead to be assigned to Job 510 is computed as follows

Central Plain - Job 510Manufacturing overhead allocation

Activity

Actual Quantity of Cost Allocation

Base Used

Cost Allocation

RateMOH

assignedMaterials handling 475 parts × $2.00/part = $ 950

Machine setups 6 setups × $320.00/setup = 1,920Insertion of parts 475 parts × $14.00/part = 6,650Finishing 300 hours × $ 44.00/hr = 13,200 Total manufacturing

overhead $22,720

Chapter 4 Activity-Based Costing and Other Cost Management Tools 338

(15-20 min.) E 4-34B

Req. 1

Best GadgetsActivity Cost Allocation

Activity Cost Allocated To Each UnitStart station 8 × $ 1.80 = $ 14.40Dip insertion 40 × $ 0.40 = 16.00Manual insertion 18 × $ 1.60 = 28.80Wave solder 7 × $ 2.20 = 15.40Backload 15 × $ 0.34 = 5.10Test 0.70 × $110.00 = 77.00Defect analysis 0.50 × $22.00 = 11 .00

Total activity costs $167 .70

Direct costs…………..……………………………………. $ 76.00*Activity costs allocated………………………………… 167.70 Manufacturing product cost…………………………… $243.70

* Made up of direct materials of $44 and direct labor of $32.

Req. 2

Managers might favor this multiple-rate, activity-based costing

system primarily because it better pinpoints activities for

planning and control and it provides more accurate data for

product costing. Managers will have more confidence in their

decisions about pricing and about which products to

emphasize or de-emphasize. The older system yields less

accurate, and therefore less useful, cost figures.

Managerial Accounting 2e Solutions Manual339

(15-20 min) E 4-35BReq. 1

Operatingoverhead

Total professional hours

Current operating overhead allocation rate

$236,000 ÷ 10,000 =$23.60 per

professional hour

Req. 2

Billing Calculations for the Amy Lee Kitchen Remodeling JobBased on current allocation system

Professional time (21 hours × $63 per hour) $1,323.00Operating overhead (21 hours × $23.60 per hour) + 495 .60 Total cost of job $1,818.60Markup on cost × 131 %Bill to client $2,382 .37

Req. 3

Activity CostTotal activity

allocation baseActivity

allocation rateTransportation

to clients $11,000 ÷15,000a

miles driven = $0.73 per mileBlueprint

copying 31,000 ÷1,000b

copies = $31 per copyOffice

support 194,000 ÷5,000c

secretarial hours =$38.80 per secretarial hour

To calculate the activity cost allocation rates, you must use the total activity for the year:a 4,000 + 11,000 = 15,000b 500 + 500 = 1,000

Chapter 4 Activity-Based Costing and Other Cost Management Tools 340

c 2,200 + 2,800 = 5,000

Managerial Accounting 2e Solutions Manual341

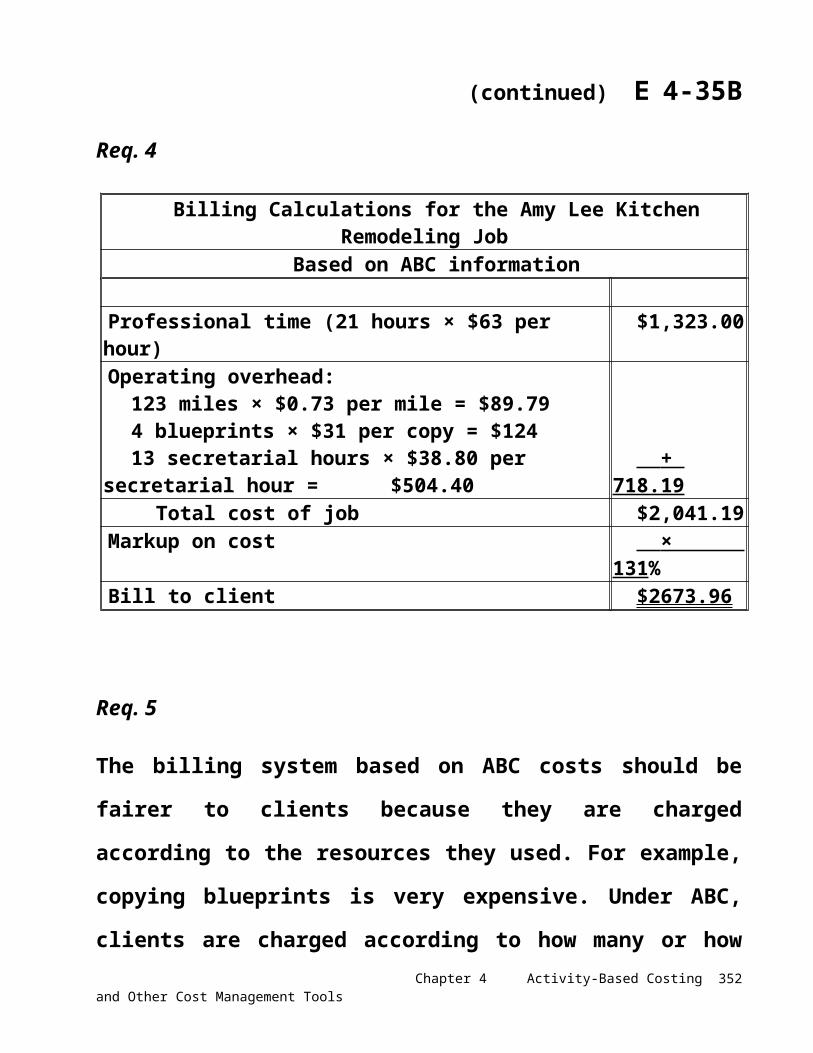

(continued) E 4-35B

Req. 4

Billing Calculations for the Amy Lee Kitchen Remodeling JobBased on ABC information

Professional time (21 hours × $63 per hour) $1,323.00Operating overhead:

123 miles × $0.73 per mile = $89.794 blueprints × $31 per copy = $12413 secretarial hours × $38.80 per secretarial hour

= $504.40 + 718.19 Total cost of job $2,041.19Markup on cost × 131 %Bill to client $2673.96

Req. 5

The billing system based on ABC costs should be fairer to

clients because they are charged according to the resources

they used. For example, copying blueprints is very expensive.

Under ABC, clients are charged according to how many or how

few blueprint copies their job required. The ABC system better

recognized the extent to which operating costs are incurred by

each unique client job.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 342

Managerial Accounting 2e Solutions Manual343

(20-25 min.) E 4-36B

Req. 1

First, compute the current plant-wide manufacturing overhead rate:

Total manufacturing

overheadTotal direct labor hours

Plant-wide overhead rate

$828,000 ÷ 26,500 =$31.25 per

direct labor hour

Then, apply it to the two products:

Manufacturing CostMedium (42-inch)

Large (63 inch)

Direct materials $ 661,000 $1,240,000Direct labor 223,000 386,000Manufacturing overhead:

( 9,600 DL hours × $31.25) = 300,000(16,900 DL hours × $31.25) = 528,125

Total manufacturing cost $1,184,000 $2,154,125Number of units produced ÷ 3,180 ÷ 4,120 Cost per unit $ 372 .33 $ 522.85

Chapter 4 Activity-Based Costing and Other Cost Management Tools 344

(continued) E 4-36B

Req. 2

First, compute the activity cost allocation rates:

Activity

Manufacturingoverhead related

to activityTotal activity

allocation baseActivity

allocation rate

Materials handling $156,000 ÷

580a

material orders handled =

$268.97 per material order handled

Machine processing 570,000 ÷

43,400b machine hours =

$13.13 per machine hour

Packaging 102,000 ÷

10,080c packaging hours =

$10.12 per packaging hour

You must use the TOTAL activity for the year as follows. Since

Owens only manufactures two products, you add the activity of

each of the individual products to find the total activity:a 340 + 240 = 580b 20,000 + 23,400 = 43,400c 4,040 + 6,040 = 10,080

Managerial Accounting 2e Solutions Manual345

(continued) E 4-36B

Req. 2 (continued)

Then, apply them to the two products:

Manufacturing CostMedium (42-inch)

Large (63 inch)

Direct materials $ 661,000 $1,240,000Direct labor 223,000 386,000Manufacturing overhead:Medium:

(340 material orders × $268.97 = $91,449.80)

(20,000 machine hours ×$13.13 = $262,600)

(4,040 packaging hours × $10.12 = $40,884.80)

Total allocation of overhead 394,935* Large:

(240 material orders × $268.97 = $64,552.80)

(23,400 machine hours ×$13.15 = $307,242)

(6,040 packaging hours ×$10.12 = $61,124.80)

Total allocation of overhead 432,920*Total manufacturing cost $1,278,935 $2,058,920Number of units produced ÷ 3,180 ÷ 4,120 Cost per unit $ 402.18 $ 499.74

* Rounded to nearest dollar

Chapter 4 Activity-Based Costing and Other Cost Management Tools 346

(continued) E 4-36B

Req. 3

Medium Large Cost per unit using current

system $ 372.33 $ 522.85Cost per unit using ABC 402.18 499.74Overcosting / (Undercosting) ($ 29.85) $ 23.11Number of units × 3,180 × 4,120 Total cost distortion ($ 94,923.00)* $95,213.20 *

* The $290.20 difference between the total amount overcosted and undercosted is due to the fact that unit answers were rounded to two decimal points.

The Medium units had been undercosted and the Large units

had been overcosted. Since Jefferis’s sets its sales price at

300% of manufacturing cost, the resulting sales price should

have been about $90 higher for the Medium units ($29.85 ×

300%) and about $70 lower for the Large units ($23.11 × 300%).

This helps to explain why Jefferis is the low cost leader for

Medium plasma TVs, but faces competitive pressure on the

Large plasma TVs.

Managerial Accounting 2e Solutions Manual347

(20-30 min.) E 4-37B

Req. 1

ZekeTotal Budgeted Indirect Manufacturing Costs

Activity

Budgeted Quantity of

Cost Allocation Base

Activity Cost

Allocation Rate

Total Budgeted

Indirect CostMaterials handling 10,000a $ 3.85 $ 38,500Machine setups 20b $345.00 6,900Insertion of parts 10,000a $ 27.00 270,000Finishing 4,600 $ 55.00 253,000 Total budgeted indirect cost $568,400

__________a (4 × 1,000) + (6 × 1,000)b 10 + 10c (1.1 × 1,000) + (3.5 × 1,000)

Chapter 4 Activity-Based Costing and Other Cost Management Tools 348

(continued) E 4-37B

Req. 2

EnkeABC Indirect Manufacturing Cost per Unit

Activity

CostAllocation

Rate

Quantity of Cost Allocation Base

Used By:Allocated Activity Cost Per Wheel

Standard Deluxe Standard DeluxeMaterials handling

$ 3.85 4 6 $ 15.40 $ 23.10

Machine setups

$345.00 0.010* 0.010* 3.45 3.45

Insertion of parts

$ 27.00 4 6 108.00 162.00

Finishing $ 55.00 1.1 3.5 60.50 192.50 Total ABC allocated indirect cost

$187.35 $381.05

__________*10 setups ÷ 1,000 wheels = 0.010 per wheel

Managerial Accounting 2e Solutions Manual349

(continued) E 4-37B

Req. 3

Budgeted total manufacturing overhead cost = $568,400 (Req. 1)

Budgeted total direct labor hours = (1,000 × 2.7) + (1,000 × 3.8)= 2,700 + 3,800= 6,500

Plant-wide overhead allocation =$568,400

6,500

= $87.45 per direct labor hour

Manufacturing overhead cost per wheel:

Standard model: 2.7 × $87.45 = $236.12Deluxe model: 3.8 × $87.45 = $332.31

Chapter 4 Activity-Based Costing and Other Cost Management Tools 350

(continues E 4-37B) (15-20 min.) E 4-38B

The Manufacturing overhead costs per wheel computed in E 4-37B are as follows:

ZekeManufacturing overhead Costs per Unit

ModelStandard Deluxe

ABC costs $187.35 $381.05Plant-wide overhead rate $236.12 $332.31

Req. 1

The gross profits (using ABC Data) for the two models are:

ZekeGross profit per unit using ABC Data

Standard DeluxeSale price $470 .00 $640 .00 Direct materials 31.00 47.00Direct labor 45.50 51.50Manufacturing overhead 187 .35 381 .05 Gross profit $ 206 .15 $ 160 .45

Managerial Accounting 2e Solutions Manual351

(continued) E 4-38B

Req. 2

ZekeGross profit per unit using Plant-wide overhead Rate

Standard DeluxeSale price $470 .00 $640 .00 Direct materials 31.00 47.00Direct labor 45.50 51.50Manufacturing overhead 236 .12 332 .31 Gross profit $ 157 .38 $ 209 .19

If they rely on the plant-wide allocation rate data, Zeke’s

managers will produce the deluxe model. It will appear to

maximize income.

Req. 3

The standard model is more profitable than the deluxe model.

Activity-based costing data generally are more accurate than

cost data generated by a plant-wide overhead allocation rate.

ABC systems have more cost categories (activities), each with

its own allocation base. ABC cost assignments more accurately

represent the cost of resources consumed to manufacture (and

support) products.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 352

(continued) E 4-38B

Req. 4

The ABC system is likely to pass the cost-benefit test because

Zeke manufactures two different products that use different

amounts of resources. The old cost system appears “broken”

because profits at the company declined when the product mix

was shifted to the product that appeared most profitable under

the old costing system. In addition, the production process

had been reengineered but the old plant-wide single-allocation-

base costing system had not.

Managerial Accounting 2e Solutions Manual353

(15-20 min.) E 4-39B

Req. 1

Either the materials handling cost or the grinding cost is

inaccurate. Both costs were assigned based on the number of

parts. Thus, the ratio of Job 409 materials handling cost to Job

622 materials handling cost should be the same as the ratio of

Job 409 grinding cost to Job 622 grinding cost. The materials

handling cost ratio is 1:3 ($400 to $1,200), but the grinding cost

ratio is 1:5 ($336 to $1,680). Job 622 cannot have three times as

many parts as Job 409 and five times as many parts

simultaneously.

Req. 2

The first step is to determine the allocation rate for each of the four activities:

Burke FabricatorsABC Allocation Rates

ActivityJob 622

Activity Cost

Divide by Quantity of the Cost

Allocation BaseActivity Cost

Allocation RateLathe work $15,500 ÷ 77,500 turns $0.20 / lathe turnMilling $26,000 ÷ 1,625 hours $16 / machine hourGrinding $ 1,680 ÷ 2,400 parts $0.70 / partTesting $ 2,500 ÷ 400 units $6.25 / unit

Chapter 4 Activity-Based Costing and Other Cost Management Tools 354

(continued) E 4-39B

Req. 2 (continued)

The second step is to use the cost allocation rate for each activity to determine the quantity of the allocation base Job 409 used.

Burke FabricatorsQuantity of the Allocation Base Used by Job 409

ActivityJob 409

Activity CostDivide by

Activity Cost Allocation Rate

Quantity of the Allocation Base Used by Job 409

Lathe work $4,700 ÷ $0.20 / turn 23,500 turnsMilling $3,600 ÷ $16 / hour 225 hoursGrinding $ 336 ÷ $0.70 / part 480 partsTesting $ 125 ÷ $6.25 / unit 20 units

Req. 3

Based on the ABC information, Burke should not accept the

company's offer to test units for $10 each. Burke’s cost of

performing this activity is only $6.25 per unit ($2,500 ÷ 400 units

tested for Job 622).

Managerial Accounting 2e Solutions Manual355

(15-20 min) E 4-40B

1. Quality tends to be “inspect-in” rather than “build-in” --traditional

2. Manufacturing plants tend to be organized with self-contained production cells –lean production

3. Maintain greater quantities of raw materials, work in process, and finished goods inventories –traditional production

4. Setup times are longer -- traditional

5. High quality is stressed in every aspect of production –lean production

6. Produced in smaller batches –lean production

7. Emphasis is placed on shortening manufacturing cycle times –lean production

8. Manufacturing plants tend to group like machinery together in different parts of the plant -- traditional

9. Setup times are shorter –lean production

10. Produced in larger batches –traditional manufacturing

11. Strives to maintain low inventory levels –lean production

12. Cycle time tends to be longer –traditional

Chapter 4 Activity-Based Costing and Other Cost Management Tools 356

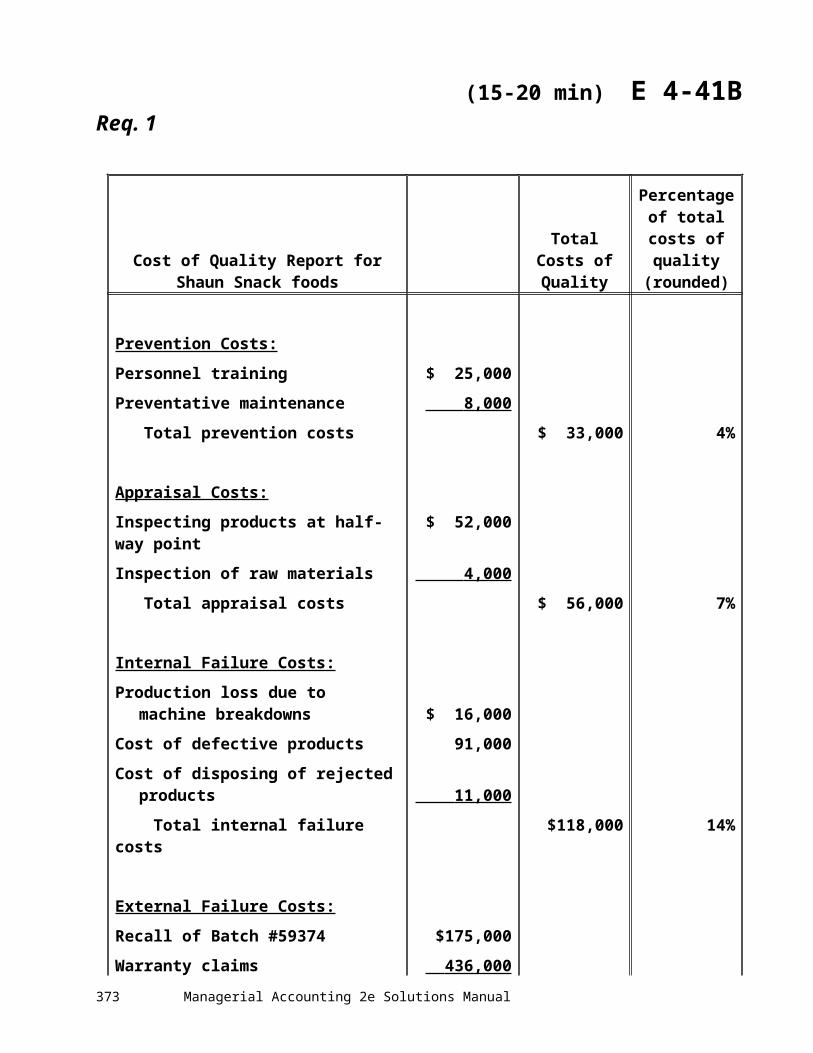

(15-20 min) E 4-41BReq. 1

Cost of Quality Report for Shaun Snack foods

Total Costs of Quality

Percentage of total costs of quality

(rounded)

Prevention Costs:

Personnel training $ 25,000

Preventative maintenance 8,000

Total prevention costs $ 33,000 4%

Appraisal Costs:

Inspecting products at half-way point $ 52,000

Inspection of raw materials 4,000

Total appraisal costs $ 56,000 7%

Internal Failure Costs:

Production loss due to machine breakdowns $ 16,000

Cost of defective products 91,000

Cost of disposing of rejected products 11,000

Total internal failure costs $118,000 14%

External Failure Costs:

Recall of Batch #59374 $175,000

Warranty claims 436,000

Total external failure costs $611,000 75%

Total Costs of Quality $818,000 100%

Managerial Accounting 2e Solutions Manual357

(continued) E 4-41BReq. 2

Because the company has warranty returns and has had a

product recall, the company may suffer from a reputation for

poor quality products. If so, they are probably losing profits

from losing sales. Unsatisfied customers will be reluctant to

buy from the company again. They may also tell their friends

and family not to buy from the company. This report does not

include an estimate of the lost profits arising from a reputation

for poor-quality products.

Req. 3

The Cost of Quality report shows that very little is being spent

on prevention and appraisal, which is probably why the internal

and external failure costs are so high. It appears that the

company is only inspecting the product half-way through the

production process, and not again at the end of the process.

Perhaps that is the reason their external failure costs are so

high. The CEO should use this information to develop quality

initiatives in the areas of prevention and appraisal. Such

initiatives should reduce future internal and external failure

costs.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 358

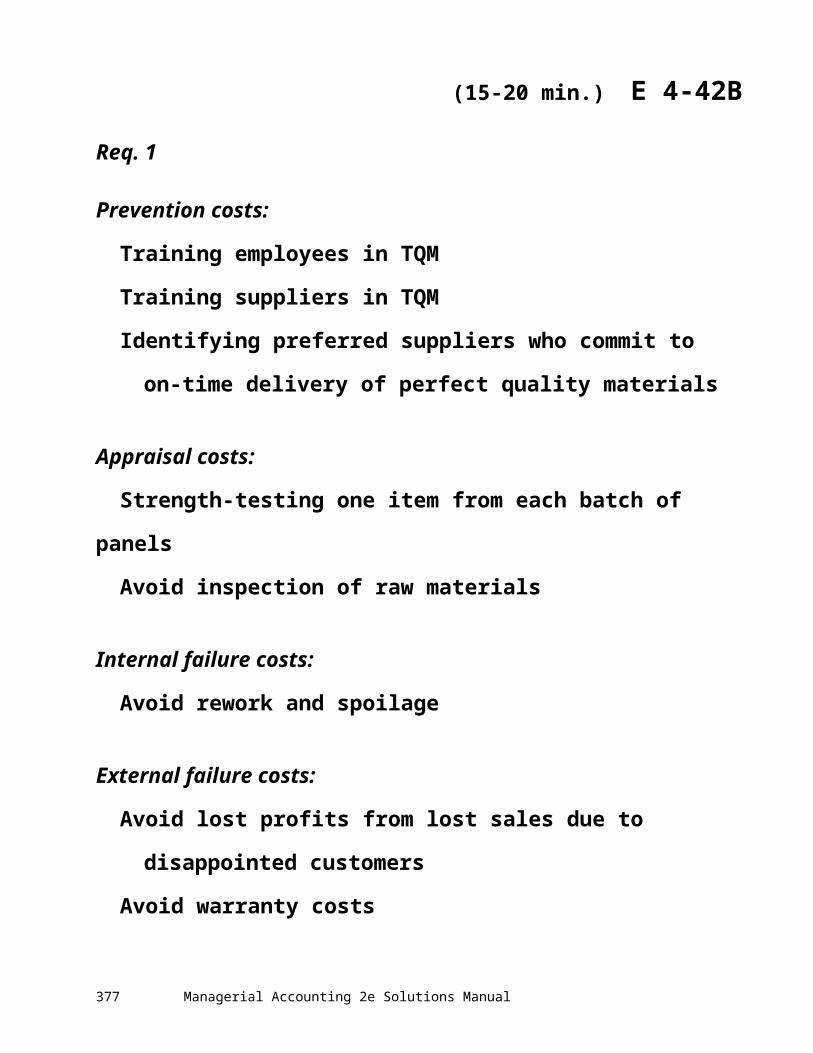

(15-20 min.) E 4-42B

Req. 1

Prevention costs:

Training employees in TQM

Training suppliers in TQM

Identifying preferred suppliers who commit to on-time

delivery of perfect quality materials

Appraisal costs:

Strength-testing one item from each batch of panels

Avoid inspection of raw materials

Internal failure costs:

Avoid rework and spoilage

External failure costs:

Avoid lost profits from lost sales due to disappointed

customers

Avoid warranty costs

Managerial Accounting 2e Solutions Manual359

(continued) E 4-42B

Req. 2

Cost / <Benefit> Analysis Cost/<Savings>

Prevention costs:Training employees in TQM…………………………… $ 30,000Training suppliers in TQM……………………………... 32,000Identifying preferred suppliers who commit to on-

time delivery of perfect quality materials……….. 60,000

Appraisal costs:Strength-testing one item from each batch of

panels…………………………………………………... 68,000

Savings on Inspection of raw materials………………… $ <57,000>

Internal failure costs:Savings on Rework and spoilage…………………….. <67,000>

External failure costs:Savings on Lost profits from lost sales due to

disappointed customers……………………………. <95,000>Savings on Warranty costs……………………………….. < 16,000>

Net <Benefit> ………………………………………………... $<45,000>

Clegg should adopt the new quality program. The program should save the company $45,000.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 360

Problems (Group A)

(40 min.) P 4-43AReq. 1

Plant-wideallocation rate =

Estimated total indirect costsEstimated total quantity of cost allocation

base

=$1,000,000

12,500* direct labor hours

= $80 per direct labor hour*When calculating plant-wide overhead rates, all direct labor hours incurred in the plant are used.

Req. 2

Departmental cost allocation

rate=

Estimated total indirect costs of department

Estimated total quantity of cost allocation

base used in department

Machining =$600,000

4,000 machine hours

= $150 per machine hour

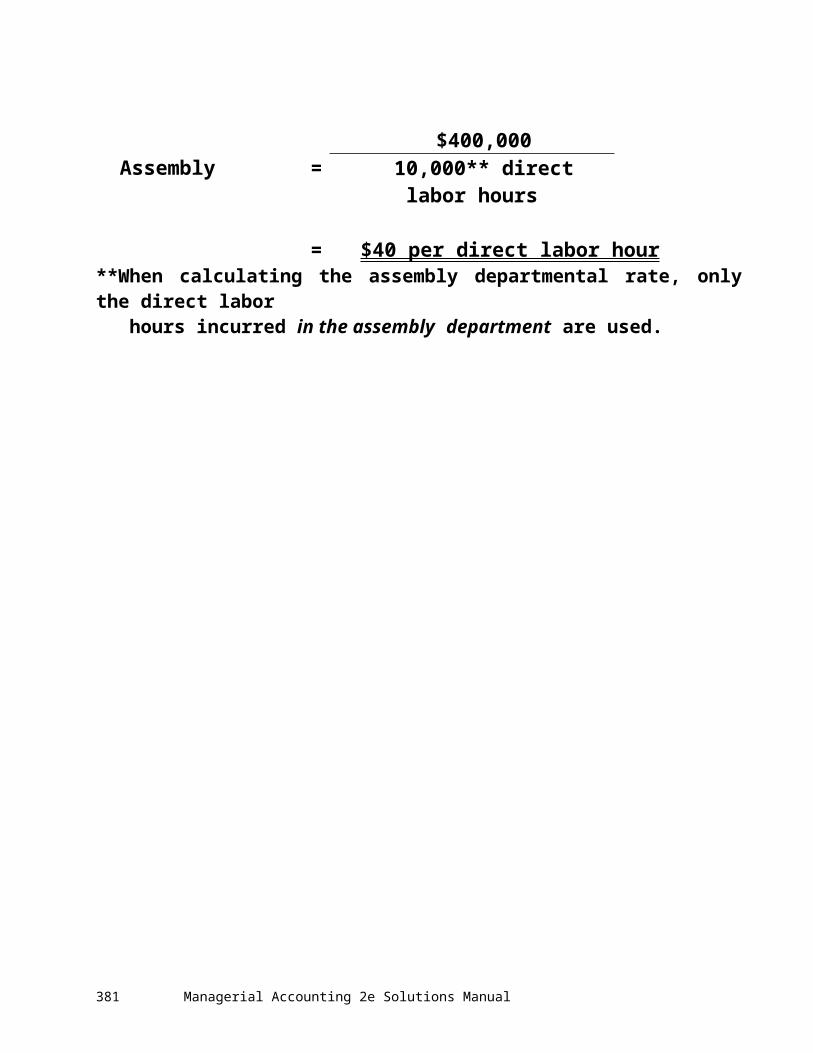

Assembly =$400,000

10,000** direct labor hours

= $40 per direct labor hour**When calculating the assembly departmental rate, only the direct labor hours incurred in the assembly department are used.

Managerial Accounting 2e Solutions Manual361

(continued) P 4-43A

Req. 3

Job #501 uses more of the company’s resources than Job 500.

While both jobs use the same number of direct labor hours in

both production departments, Job 501 uses twice as many

machine hours (6 MH) as Job 500 (3 MH). Running the

machines requires resources, such as utilities, depreciation,

and repairs and maintenance. The accounting system should

show that Job 501 actually “costs” the company more

resources to make than Job 500.

Req. 4

Overhead allocation based on single, plant-wide rate:

Job 500 Job 501Total direct labor hours 14 DL hours 14 DL hours × Plant-wide allocation rate × $80 / DL hour × $80 / DL hourOverhead allocation $1,120 $1,120

Chapter 4 Activity-Based Costing and Other Cost Management Tools 362

(continued) P 4-43A

Req. 5 Overhead allocation based on departmental rates:

Job 500 Job 501Machining Department:Departmental allocation rate $150/ MH $150/ MH× Machine hours used by Job × 3 MH × 6 MH Overhead allocation $450 $900

Assembly Department:Departmental allocation rate $40/ DL hr $40/ DL hr× DL hours used by Job × 12 DL hrs × 12 DL hrs Overhead allocation $480 $480

Total overhead allocation $930 $1,380 (from both departments)

Req. 6

The single plant-wide overhead rate assigned the same amount

of overhead to both jobs ($1,120). This doesn’t seem equitable

since Job 501 uses more of the company’s indirect resources.

On the other hand, the departmental rates assign more

overhead cost to Job 501 than Job 500 due to the extra

machine hours used by Job 501. This seems like a much

“fairer” allocation of overhead.

Managerial Accounting 2e Solutions Manual363

(continued) P 4-43A

Req. 7

Manufacturing cost and sales price using current costing system:

Job 500 Job 501Direct Materials $1,000 $1,000Direct Labor (14 DL hours × $25) 350 350Manufacturing overhead 1,120 1,120 Total manufacturing cost $2,470 $2,470Markup for pricing × 110 % × 110 % Sales price $2,717 $2,717

Req. 8

Gross profit using current costing system:

Job 500 Job 501Sales Price (from Req. 1) $2,717 $2,717

Less: Total manufacturing cost 2,470 2,470 Gross profit (loss) $ 247 $ 247

Chapter 4 Activity-Based Costing and Other Cost Management Tools 364

(continues) P 4-43A

Req. 8 (continued)

Gross profit using departmental rate costing system:

Job 500 Job 501Sales price (from Req. 7) $2,717 $2,717 Less: Total manufacturing cost: Direct Materials $1,000 $1,000 Direct Labor (14 DL hours × $25) 350 350 Manufacturing overhead 930 1,380 Total manufacturing cost $2,280 $2,730Gross profit (loss) $ 437 $ (13 )

Req. 9

Perreth thought that both jobs were equally profitable ($247)

because the original costing system assigned the same amount

of manufacturing cost to each job. However, using a refined

costing system, we see that Perreth was making more profit on

Job 500 than previously reported and actually losing money on

Job 501.

Managerial Accounting 2e Solutions Manual365

(20-30 min.) P 4-44A

Req. 1

HonePer-Unit Manufacturing Costs

StandardDesk

UnpaintedDesk

Direct materials $ 96,000 $21,000Materials handling (120,000 and 30,000) × $0.60 72,000 18,000Assembling (6,000 and 900) × $15 90,000 13,500Painting (6,000 × $5.00) 30,000 — Total manufacturing costs $288,000 $52,500Divide by number of units ÷ 6,000 ÷ 1,500 Manufacturing product cost per unit $ 48.00 $ 35.00

Req. 2

HoneFull Product Costs

Standard Desk

Unpainted Desk

Premanufacturing activities(such as product design) $ 5.00 $ 3.00

Manufacturing product costs 48.00 35.00Postmanufacturing activities

(such as distribution, marketing,and customer service) 25 .00 22 .00

Full product cost per unit $78 .00 $60 .00

Chapter 4 Activity-Based Costing and Other Cost Management Tools 366

(continued) P 4-44A

Req. 3

Manufacturing product costs computed in Req. 1 are reported

in the financial statements.

Managers use full product costs computed in Req. 2 for

decisions, such as pricing and product emphasis.

Full product cost includes the costs of pre-manufacturing

activities and post-manufacturing activities that are expensed

as incurred for external financial reporting. However, these

costs often are assigned to products for internal decisions. For

example, the sale price must exceed full product cost for the

product to be profitable.

Req. 4

Full product cost……………………. $ 78.00Desired profit………………………… 42.00 Sale price per unit…………………... $120.00

Managerial Accounting 2e Solutions Manual367

(30-40 min.) P 4-45A

Req. 1

XnetABC Cost Allocation Rates

ApplicationsDevelopment

ContentProduction Testing

Estimated indirect activity costs $1,600,000 $2,400,000 $288,000

÷ Estimated quantity of cost allocation base ÷ 4 applications ÷ 12 million lines ÷ 1,800 testing hours

Cost allocation rate $400,000/application $0.20 / line $160 / hour

Req. 2

XnetActivity Costs per Unit

X-Page X-SecureApplications development

(1 and 1) × $400,000 $400,000 $ 400,000Content production

(500,000 and 7,500,000) × $0.20 100,000 1,500,000Testing (100 and 600) × $160 16,000 96,000 Total indirect cost $516,000 $1,996,000÷ Number of units ÷ 30,000 units ÷ 10 unitsIndirect activity cost per unit $ 17.20 $ 199,600

Chapter 4 Activity-Based Costing and Other Cost Management Tools 368

(continued) P 4-45A

Req. 3

XnetCosts per Unit Under Original Direct-Labor Based System

X-Page X-SecureIndirect costs

(10,000 and 15,000) × $100 $1,000,000 $1,500,000÷ Number of units ÷ 30,000 units ÷ 10 unitsIndirect costs per unit $ 33.33* $ 150,000

__________*Rounded

Req. 4

X-Page X-SecureABC system............................... $17.20 $199,600Original system......................... $33.33 $150,000

Thus, under ABC the unit cost decreases by $16.13 for X-Page and increases $49,600 for X-Secure.

The original system overcosted X-Page and undercosted X-

Secure. The original system allocated 50% more overhead to X-

Secure ($1,500,000) than to X-Page ($1,000,000). But X-Secure

required 15 times as many lines of code ($7,500,000/500,000)

and 6 times as much testing (600/100) as X-Page. The ABC

system recognizes this difference and allocates more of the

content production and testing costs to X-Secure.

Managerial Accounting 2e Solutions Manual369

(continued) P 4-45A

Req. 5

Xnet’s different software applications use different

amounts of resources.

Xnet has high indirect costs.

Xnet produces high volumes of some software

applications (X-Page) and low volumes of other software

applications (X-Secure).

Xnet is in a competitive environment and needs

accurate product costs.

Xnet has accounting and information system expertise

to implement the system.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 370

(30-40 min.) P 4-46A

Req. 1

HCI PharmaceuticalsABC Cost Allocation Rates

Materials Handling Packaging Quality AssuranceEstimated indirect

activity costs $190,000 $400,000 $112,500÷ Estimated quantity of

cost allocation base ÷ 19,000 kilos ÷ 2,000 hours ÷ 1,875 samples Cost allocation rate $ 10 / kilo $ 200 / hour $ 60 / sample

Req. 2

HCI PharmaceuticalsActivity Costs Per Unit

Commercial Container Travel Pack

Materials handling (8,000 and 6,000) × $10 $ 80,000 $ 60,000Packaging (1,200 and 400) × $200 240,000 80,000Quality assurance (200 and 300) × $60 12,000 18,000 Total indirect costs $332,000 $158,000÷ Number of units ÷ 2,500 ÷ 50,000 Indirect activity cost per unit $ 132.80 $ 3.16

Managerial Accounting 2e Solutions Manual371

(continued) P 4-46A

Req. 3

HCI PharmaceuticalsCosts per Unit Under Original Machine-Hour Based System

Commercial Container Travel Pack

Indirect costs (1,200 and 400) × $300 $360,000 $120,000÷ Number of units ÷ 2,500 ÷ 50,000Indirect cost per unit $ 144 $ 2.40

Req. 4

Commercial Container Travel Pack

ABC System.................................... $132.80 $3.16Original System.............................. $144.00 $2.40

The original system overcosted the commercial containers and undercosted the travel packs. The original system allocated 3 times as much indirect cost to the commercial containers as to the travel packs (1,200 ÷ 400 = 3). However, commercial containers did not use 3 times as much of the material handling and quality assurance resources. Commercial containers used only 33% more material handling than travel packs (8,000 / 6,000). And commercial containers required less quality assurance than travel packs. The ABC system recognizes that commercial containers do not require 3 times as much material handling and quality assurance as travel packs. So, relative to the original system, ABC allocates less of the material handling and quality assurance costs to commercial containers.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 372

(20-30 min.) P 4-47A

Req. 1

Real ToysPredicted Quality Cost Savings

Activity

Predicted Reduction In

Activity Units

×

Activity Cost

Allocation Rate

=

PredictedReductionIn Activity

CostsInspection of incoming materials 300 $20 $ 6,000Inspection of finished goods 300 $30 9,000Defective units discovered in-house 3,200 $15 48,000Defective units discovered

by customers 900 $35 31,500Lost sales to dissatisfied customers 300 $55 16,500 Total predicted quality cost savings $111,000

Req. 2

Real ToysNet Benefit of Design Engineering Effort

Total predicted quality cost savings $111,000Cost of design engineering 60,000 Net benefit of design engineering $ 51,000

Managerial Accounting 2e Solutions Manual373

(continued) P 4-47A

Req. 3

Measuring the costs of quality-related activities is difficult.

Estimating some costs, such as the cost of design engineering

to improve the quality of a particular product, may require

allocation of engineers’ salaries. Other costs, such as the cost

of lost sales, are not recorded in the accounts and are difficult

to predict. For these reasons, many companies also monitor

non-financial measures of quality (for example, number of

machine breakdowns and number of customer complaints) and

attempt to improve them.

Chapter 4 Activity-Based Costing and Other Cost Management Tools 374

Problems (Group B)

(40 min.) P 4-48BReq. 1

Plant-wideallocation rate =

Estimated total indirect costsEstimated total quantity of cost allocation

base

=$1,090,000

14,000* direct labor hours

= $77.86 per direct labor hour*When calculating plant-wide overhead rates, all direct labor hours incurred in the plant are used.

Req. 2

Departmental cost allocation

rate=

Estimated total indirect costs of department

Estimated total quantity of cost allocation

base used in department

Machining =$670,000

4,000 machine hours

= $167.50 per machine hour

Assembly =$420,000

12,000** direct labor hours

= $35 per direct labor hour**When calculating the assembly departmental rate, only the direct labor hours incurred in the assembly department are used.

Managerial Accounting 2e Solutions Manual375

(continued) P 4-48B

Req. 3

Job #501 uses more of the company’s resources than Job 500.

While both jobs use the same number of direct labor hours in

both production departments, Job 501 uses twice as many

machine hours (16 MH) as Job 500 (8 MH). Running the

machines requires resources, such as utilities, depreciation,

and repairs and maintenance. The accounting system should

show that Job 501 actually “costs” the company more

resources to make than Job 500.

Req. 4

Overhead allocation based on single, plant-wide rate:

Job 500 Job 501Total direct labor hours 20 DL hours 20 DL hours × Plant-wide allocation rate × $77.86 / DL

hour× $77.86 / DL

hourOverhead allocation $1,557.20 $1,557.20

Chapter 4 Activity-Based Costing and Other Cost Management Tools 376

(continued) P 4-48B

Req. 5 Overhead allocation based on departmental rates:

Job 500 Job 501Machining Department:Departmental allocation rate $167.50/ MH $167.50/ MH× Machine hours used by Job × 8 MH × 16 MH Overhead allocation $1,340 $2,680

Assembly Department:Departmental allocation rate $35/ DL hr $35/ DL hr× DL hours used by Job × 15 DL hrs × 15 DL hrs Overhead allocation $525 $525

Total overhead allocation $1,865 $3,205 (from both departments)

Req. 6

The single plant-wide overhead rate assigned the same amount

of overhead to both jobs ($1,557.20). This doesn’t seem

equitable since Job 501 uses more of the company’s indirect

resources. On the other hand, the departmental rates assign

more overhead cost to Job 501 than Job 500 due to the extra

machine hours used by Job 501. This seems like a much

“fairer” allocation of overhead.

Managerial Accounting 2e Solutions Manual377

(continued) P 4-48B

Req. 7

Manufacturing cost and sales price using current costing system:

Job 500 Job 501Direct Materials $1,200 $1,200Direct Labor (20 DL hours × $30) 600 600Manufacturing overhead 1,557 .20 1,557 .20 Total manufacturing cost $3,357.20 $3,357.20Markup for pricing × 130 % × 130 % Sales price $4,364 .36 $4,364 .36

Req. 8

Gross profit using current costing system:

Job 500 Job 501Sales Price (from Req. 7) $4,364.36 $4,364.36

Less: Total manufacturing cost 3,357 .20 3,357 .20 Gross profit (loss) $ 1,007 .16 $ 1,007 .16

Chapter 4 Activity-Based Costing and Other Cost Management Tools 378

Req. 8 (continued)

Gross profit using departmental rate costing system:

Job 500 Job 501Sales price (from Req. 7) $4,364 .36 $4,364 .36 Less: Total manufacturing cost: Direct Materials $1,200.00 $1,200.00 Direct Labor (20 DL hours × $30) 600.00 600.00 Manufacturing overhead 1,865 .00 3,205 .00 Total manufacturing cost $3,365 .00 $5,005 .00 Gross profit (loss) $ 699 .36 $ (640 .64

Req. 9

Quintana thought that both jobs were equally profitable

($1,007.16) because the original costing system assigned the

same amount of manufacturing cost to each job. However,

using a refined costing system, we see that Quintana was

making more profit on Job 500 than previously reported and

actually losing money on Job 501.

Managerial Accounting 2e Solutions Manual379

(20-30 min.) P 4-49B

Req. 1

Johnston’sPer-Unit Manufacturing Costs

StandardDesk

UnpaintedDesk

Direct materials $ 98,000 $18,000Materials handling (120,500 and 30,500) × $0.60 72,300 18,300Assembling (6,300 and 1,000) × $13 81,900 13,000Painting (6,500 × $5.30) 34,450 — Total manufacturing costs $286,650 $49,300Divide by number of units ÷ 6,500 ÷ 2,000 Manufacturing product cost per unit $ 44.10 $ 24.65

Req. 2

Johnston’sFull Product Costs

Standard Desk

Unpainted Desk

Premanufacturing activities(such as product design) $ 4.00 $ 3.00

Manufacturing product costs 44.10 24.65Postmanufacturing activities

(such as distribution, marketing,and customer service) 22 .00 19 .00

Full product cost per unit $70 .10 $46 .65

Chapter 4 Activity-Based Costing and Other Cost Management Tools 380

(continued) P 4-49B

Req. 3

Manufacturing product costs computed in Req. 1 are reported

in the financial statements.

Managers use full product costs computed in Req. 2 for

decisions, such as pricing and product emphasis.

Full product cost includes the costs of pre-manufacturing

activities and post-manufacturing activities that are expensed

as incurred for external financial reporting. However, these

costs often are assigned to products for internal decisions. For

example, the sale price must exceed full product cost for the

product to be profitable.

Req. 4

Full product cost……………………. $ 70.10Desired profit………………………… 39.00 Sale price per unit…………………... $109.10

Managerial Accounting 2e Solutions Manual381

(30-40 min.) P 4-50B

Req. 1

GibsonABC Cost Allocation Rates

ApplicationsDevelopment

ContentProduction Testing

Estimated indirect activity costs $1,500,000 $2,700,000 $270,000

÷ Estimated quantity of cost allocation base ÷ 3 applications ÷ 9 million lines ÷ 1,500 testing hours

Cost allocation rate $500,000/application $0.30 / line $180 / hour

Req. 2

GibsonActivity Costs per Unit

X-Page X-SecureApplications development

(1 and 1) × $500,000 $500,000 $ 500,000Content production

(480,000 and 7,200,000) × $0.30 144,000 2,160,000Testing (70 and 420) × $180 12,600 75,600 Total indirect cost $656,600 $2,735,600÷ Number of units ÷ 25,000 units ÷ 9 unitsIndirect activity cost per unit $ 26.26* $ 303,955 .56*

*Rounded to nearest cent

Chapter 4 Activity-Based Costing and Other Cost Management Tools 382

(continued) P 4-50B

Req. 3

GibsonCosts per Unit Under Original Direct-Labor Based System

X-Page X-SecureIndirect costs

(14,000 and 21,000) × $104 $1,456,000 $2,184,000÷ Number of units ÷ 25,000 units ÷ 9 unitsIndirect costs per unit $ 58.24 $ 242,666 .67*

__________*Rounded to nearest cent

Req. 4

X-Page X-SecureABC system............................... $26.26 $303,955.56Original system......................... $58.24 $242,666.67

Thus, the cost decreased by $31.98 for X-Page and increased $61,288.89 for X-Secure.

The original system overcosted X-Page and undercosted X-

Secure. The original system allocated 50% more overhead to X-

Secure ($2,184,000) than to X-Page ($1,456,000). But X-Secure

required 15 times as many lines of code ($7,200,000/480,000)

and 6 times as much testing (420/70) as X-Page. The ABC

system recognizes this difference and allocates more of the

content production and testing costs to X-Secure.

Managerial Accounting 2e Solutions Manual383

(continued) P 4-50B

Req. 5