BTG plc Acquisition - Boston Scientific

18

BTG plc Acquisition Jeff Mirviss, SVP & President, Peripheral Interventions Mike Mahoney, Chairman & CEO

Transcript of BTG plc Acquisition - Boston Scientific

BTG plc Acquisition

Jeff Mirviss, SVP & President, Peripheral Interventions

Mike Mahoney, Chairman & CEO

2

Safe Harbor for Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of

the Securities Exchange Act of 1934. Forward-looking statements may be identified by words like “anticipate,” “expect,” “project,”

“believe,” “plan,” “estimate,” “intend” and similar words. These forward-looking statements are based on our beliefs, assumptions and

estimates using information available to us at the time and are not intended to be guarantees of future events or performance. If our

underlying assumptions turn out to be incorrect, or if certain risks or uncertainties materialize, actual results could differ materially from the

expectations and projections expressed or implied by our forward-looking statements.

Factors that may cause such differences can be found in our most recent Form 10-K and Forms 10-Q filed or to be filed with the Securities

and Exchange Commission under the headings “Risk Factors” and “Safe Harbor for Forward-Looking Statements.” Accordingly, you are

cautioned not to place undue reliance on any of our forward-looking statements. We disclaim any intention or obligation to publicly

update or revise any forward-looking statements to reflect any change in our expectations or in events, conditions, or circumstances on

which they may be based, or that may affect the likelihood that actual results will differ from those contained in the forward-looking

statements.

Non-GAAP Measures:

This document contains non-GAAP measures (denoted with *) in talking about our company’s performance. Please refer to the

addendum to this presentation for further information regarding these non-GAAP measures and the Investor Relations section of our

website at www.bostonscientific.com.

Market Estimates:

Unless noted otherwise, all references to market sizes, market share positions, and market growth rates are BSX internal estimates.

3

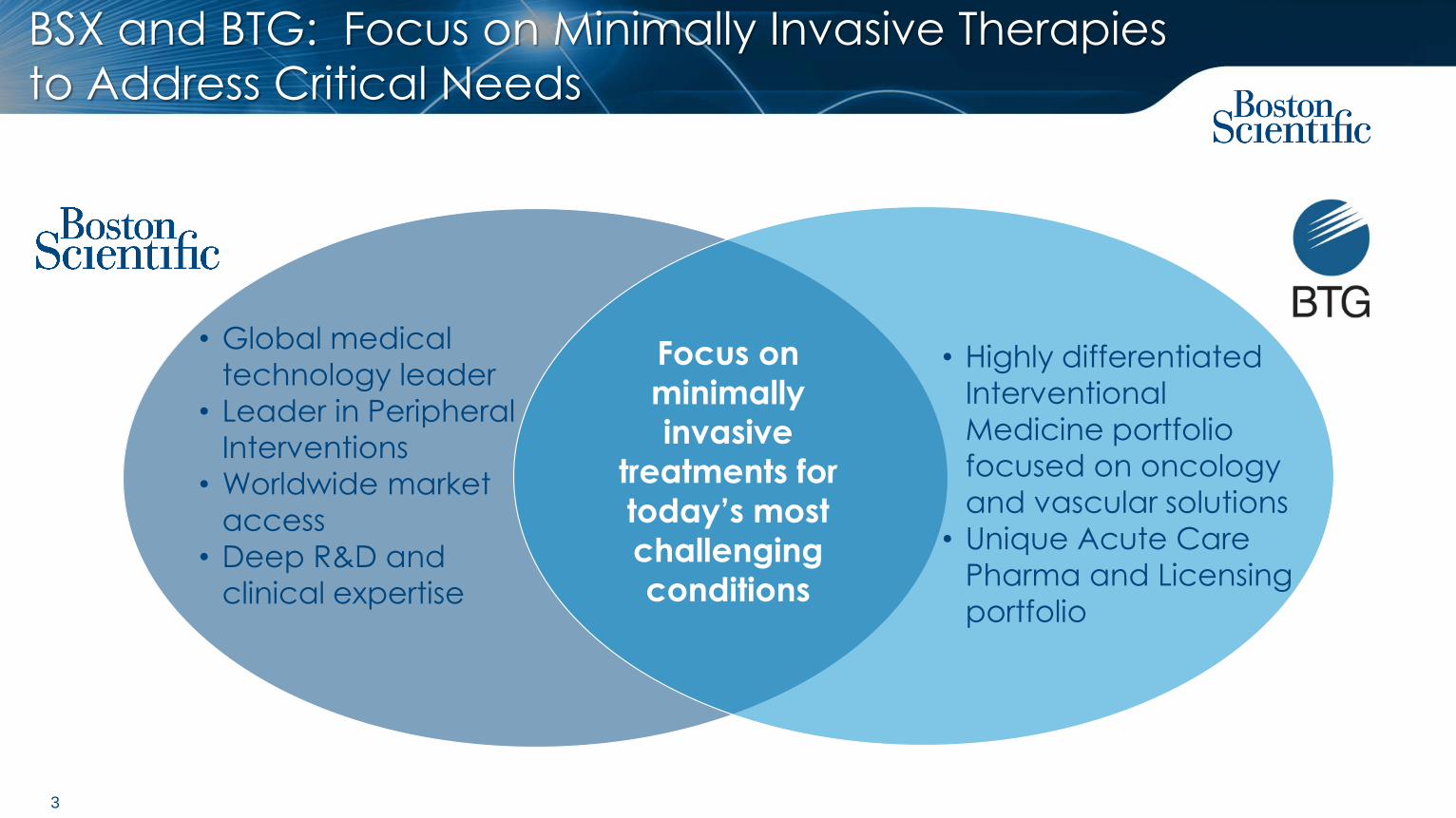

BSX and BTG: Focus on Minimally Invasive Therapies

to Address Critical Needs

Focus on

minimally

invasive

treatments for

today’s most

challenging

conditions

• Highly differentiated

Interventional

Medicine portfolio

focused on oncology

and vascular solutions

• Unique Acute Care

Pharma and Licensing

portfolio

• Global medical

technology leader

• Leader in Peripheral

Interventions

• Worldwide market

access

• Deep R&D and

clinical expertise

4

Clear Strategic & Financial Rationale

High Growth

Cancer Expansion

Highly Synergistic

to BSX PI

Strong Margin &

Cash Flow

Compelling

Shareholder

Returns

Execution Sweet

Spot

• Advances category leadership strategy with complementary IM business

• Adds $400M+ (2019E1) of double digit growth revenue to $1B+ BSX PI business

• Adj. margins in line with BSX today, and accretive to BSX and PI in year 3

• High growth Interventional Medicine (IM) business accretive to BSX and PI

• BTG platform technologies (TheraSphere™, Galil) enable BSX to continue to

expand treatment options for cancer patients worldwide

• BTG Acute Care Specialty Pharma franchise is a differentiated, profitable

business along with cash generating Licensing assets

• Immediately $0.02-$0.03 accretive to BSX 2019 adjusted EPS*; more so thereafter

• Significant synergies of $175M+ expected (yr. 3); adj. ROIC* 7-8% in yr. 3; 9-10% in yr. 5

• Maintains flexibility for future M&A and commitment to investment grade ratings

• Tuck-in acquisition very complementary to BSX PI infrastructure/call point

• Leverages BSX track record and experience with this transaction type

1BSX Estimate for calendar year 2019

5

BTG Background & Deal Terms

• BTG (LSE: BTG) Headquartered in London, United Kingdom

– Founded 1948, listed London Stock Exchange 1995

– 1,600+ employees globally

• Three business segments:

– Interventional Medicine: Interventional Oncology & Interventional Vascular

– Acute Specialty Pharmaceuticals: portfolio of antidotes (CroFab™, DigiFab™, Voraxaze™)

– Licensing: portfolio of licensed healthcare products (Zytiga™, etc.)

• Offering 840 pence in cash per share; committed debt financing in place

• Total equity value of £3.3B (U.S. $4.2B), total enterprise value of £3.1B (U.S. $4.0B)

(U.S. values based on November 19 exchange rates)

• The transaction is expected to be effected by way of an English Court sanctioned Scheme of

Arrangement, with closing targeted for H1:2019, subject to receipt of BTG shareholder approval,

customary regulatory approvals and the approval of the English Court

Key

Deal

Terms

6

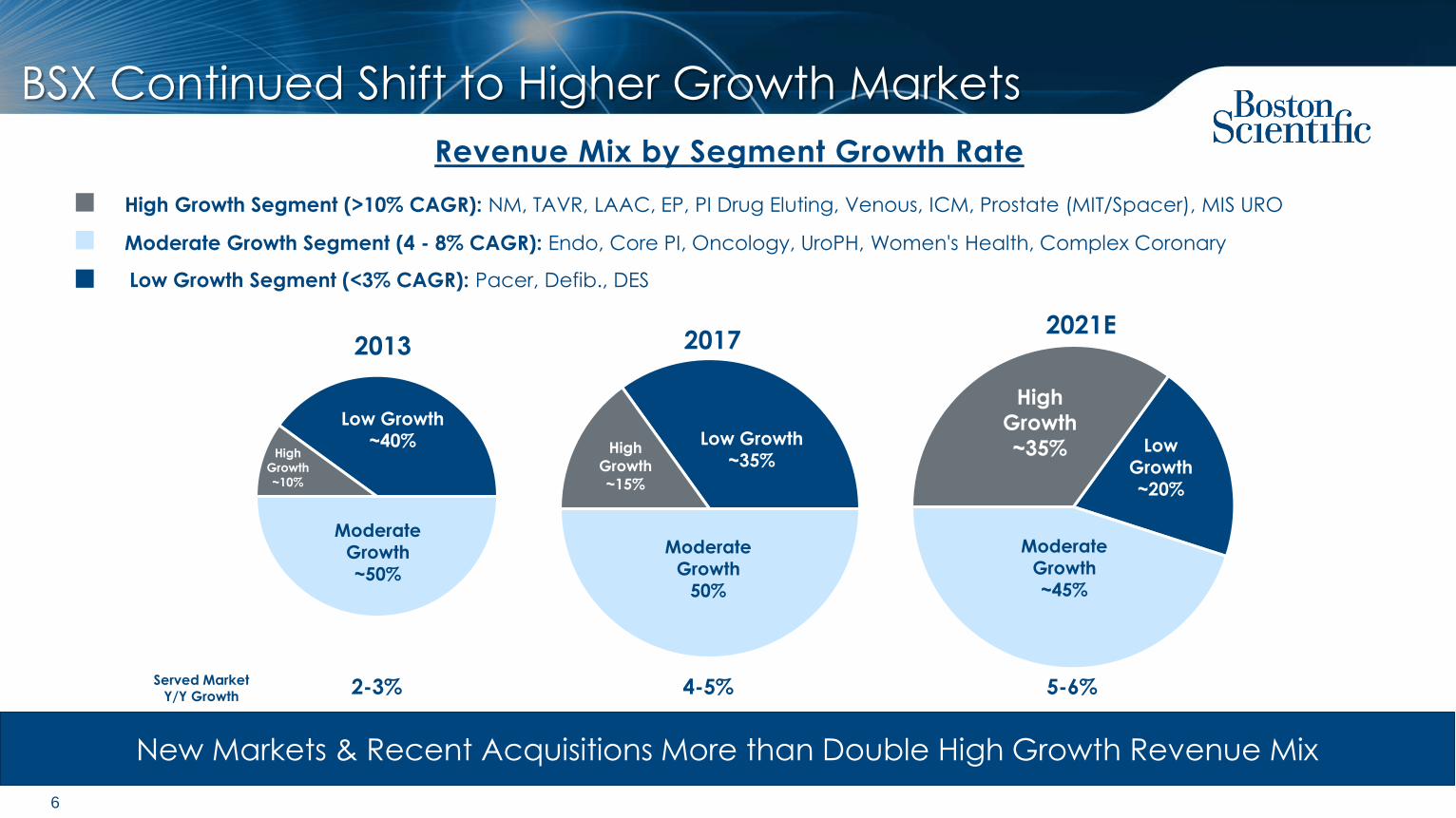

BSX Continued Shift to Higher Growth Markets

High Growth Segment (>10% CAGR): NM, TAVR, LAAC, EP, PI Drug Eluting, Venous, ICM, Prostate (MIT/Spacer), MIS URO

Low Growth Segment (<3% CAGR): Pacer, Defib., DES

Moderate Growth Segment (4 - 8% CAGR): Endo, Core PI, Oncology, UroPH, Women's Health, Complex Coronary

20172021E

2013

Revenue Mix by Segment Growth Rate

2-3% 5-6%Served Market

Y/Y Growth

Low Growth

~40%

Moderate

Growth

~50%

Low

Growth

~20%

Moderate

Growth

~45%

High

Growth

~35%High

Growth

~10%

New Markets & Recent Acquisitions More than Double High Growth Revenue Mix

High

Growth

~15%

Low Growth

~35%

4-5%

Moderate

Growth

50%

7

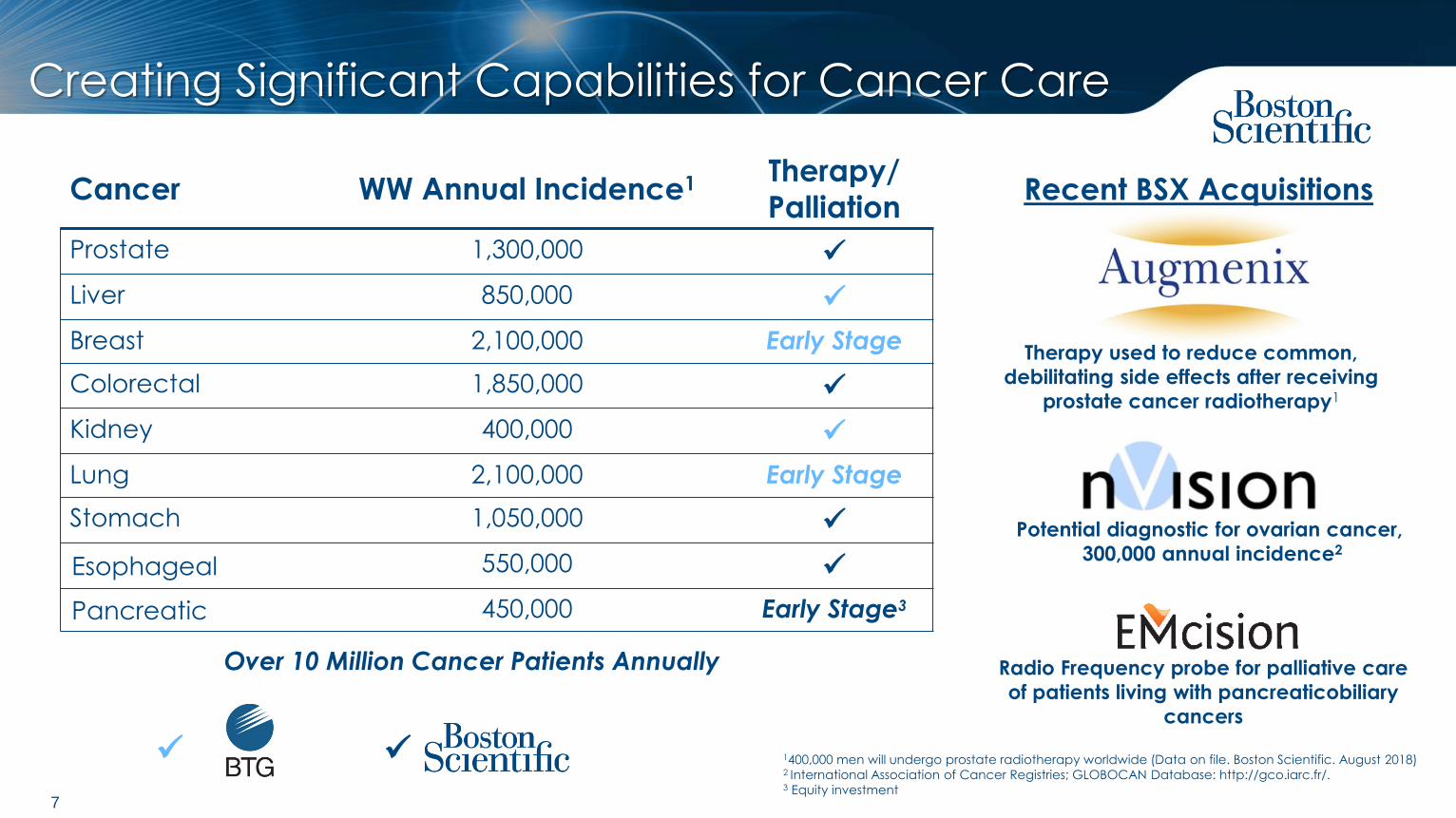

Creating Significant Capabilities for Cancer Care

Cancer WW Annual Incidence1 Therapy/

Palliation

Prostate 1,300,000 ✓

Liver 850,000 ✓

Breast 2,100,000 Early Stage

Colorectal 1,850,000 ✓

Kidney 400,000 ✓

Lung 2,100,000 Early Stage

Stomach 1,050,000 ✓

Esophageal 550,000 ✓

Pancreatic 450,000 Early Stage3

✓ ✓

Over 10 Million Cancer Patients Annually

1400,000 men will undergo prostate radiotherapy worldwide (Data on file. Boston Scientific. August 2018)2 International Association of Cancer Registries; GLOBOCAN Database: http://gco.iarc.fr/. 3 Equity investment

Potential diagnostic for ovarian cancer,

300,000 annual incidence2

Therapy used to reduce common,

debilitating side effects after receiving

prostate cancer radiotherapy1

Radio Frequency probe for palliative care

of patients living with pancreaticobiliary

cancers

Recent BSX Acquisitions

8

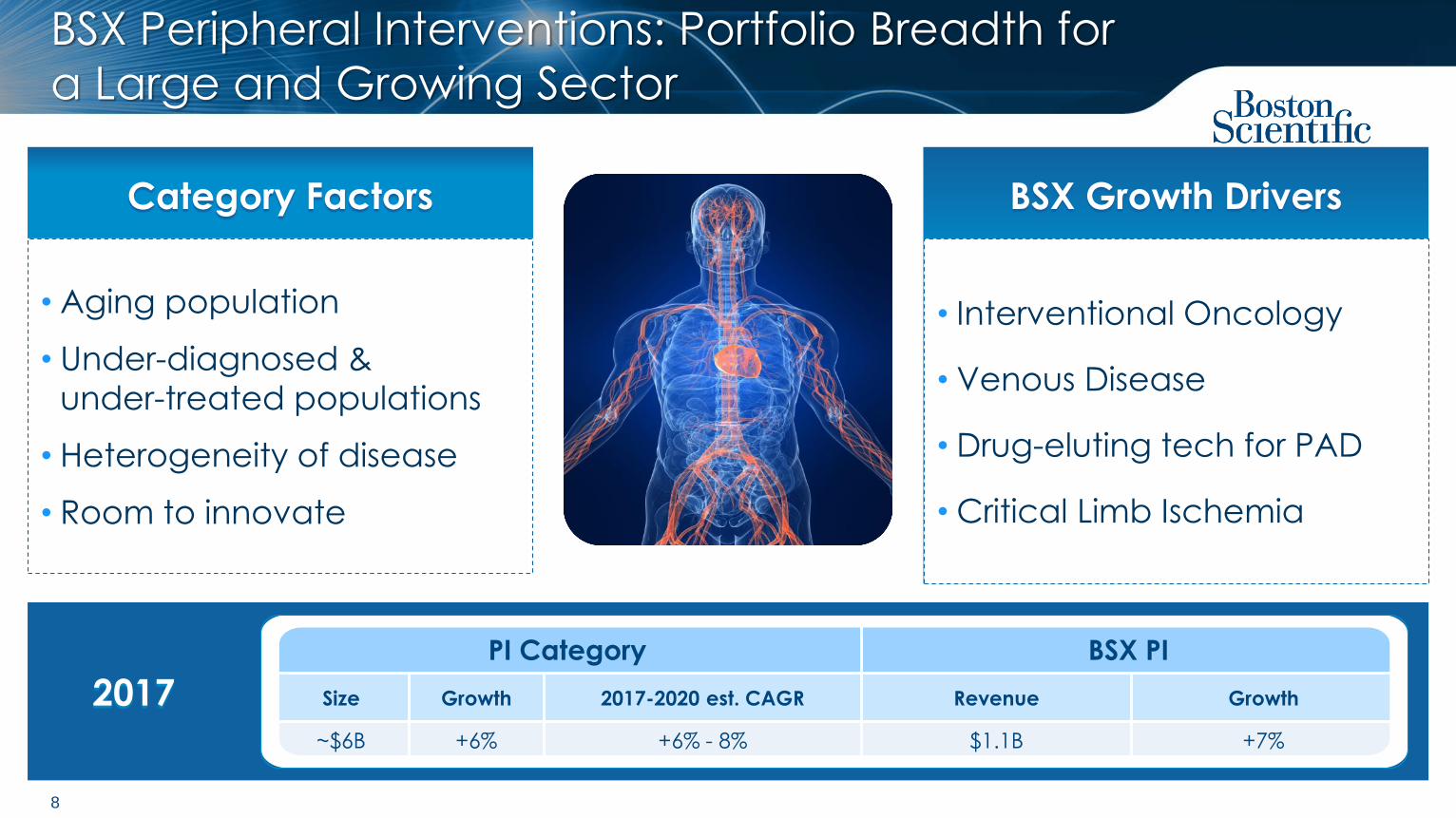

BSX Peripheral Interventions: Portfolio Breadth for

a Large and Growing Sector

2017

PI Category BSX PI

Size Growth 2017-2020 est. CAGR Revenue Growth

~$6B +6% +6% - 8% $1.1B +7%

Category Factors BSX Growth Drivers

• Aging population

• Under-diagnosed &

under-treated populations

• Heterogeneity of disease

• Room to innovate

• Interventional Oncology

• Venous Disease

• Drug-eluting tech for PAD

• Critical Limb Ischemia

9

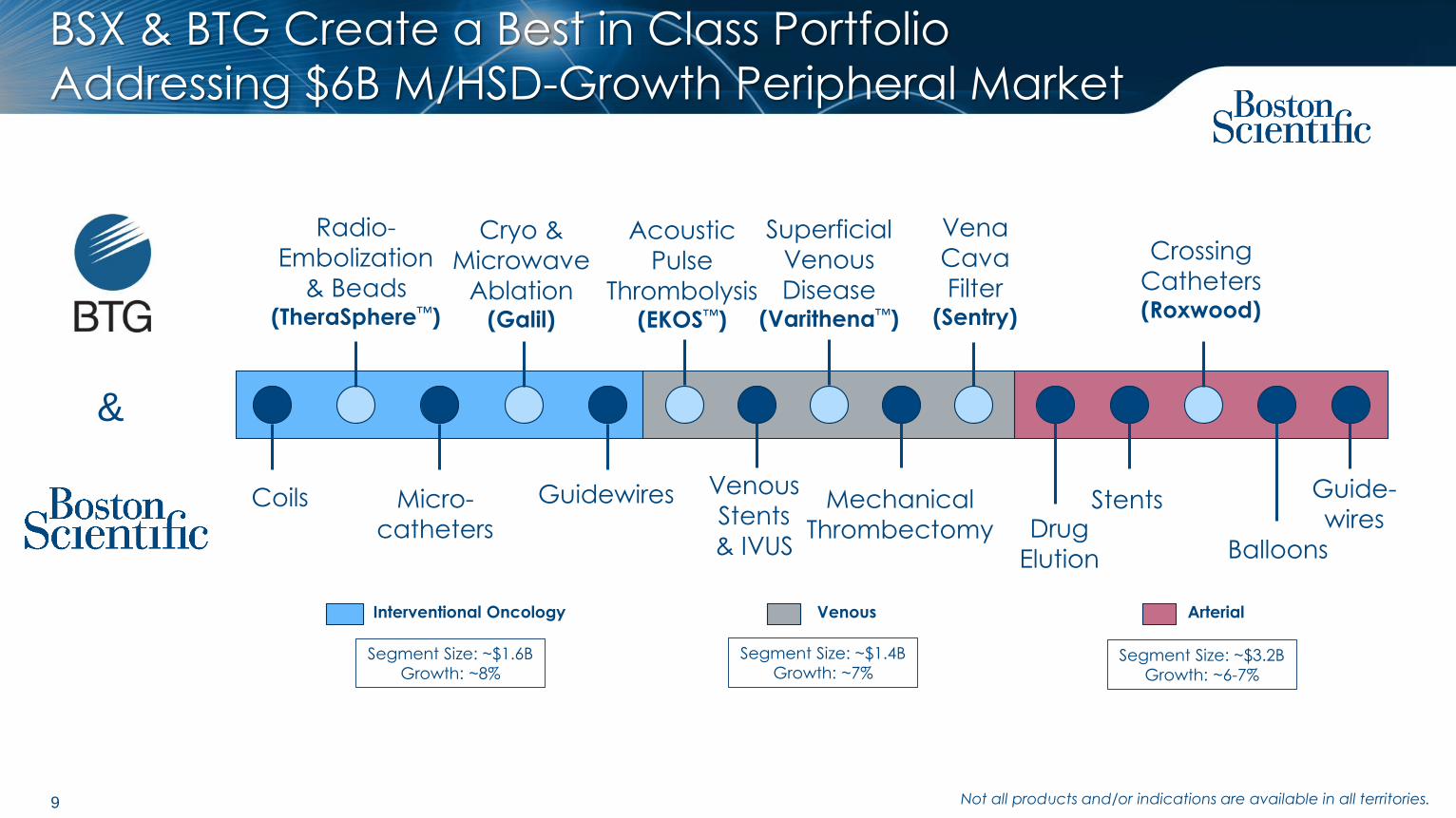

BSX & BTG Create a Best in Class Portfolio

Addressing $6B M/HSD-Growth Peripheral Market

Guide-

wiresDrug

Elution

Stents

Balloons

Crossing

Catheters(Roxwood)

Vena

Cava

Filter(Sentry)

Coils Micro-

catheters

Guidewires

Radio-

Embolization

& Beads(TheraSphere™)

Cryo &

Microwave

Ablation(Galil)

Acoustic

Pulse

Thrombolysis(EKOS™)

Superficial

Venous

Disease(Varithena™)

Venous

Stents

& IVUS

Mechanical

Thrombectomy

&

Interventional Oncology Venous Arterial

Segment Size: ~$1.6B

Growth: ~8%

Segment Size: ~$1.4B

Growth: ~7% Segment Size: ~$3.2B

Growth: ~6-7%

Not all products and/or indications are available in all territories.

10

Highly Differentiated Cancer Therapies for Large

Patient Populations

TheraSphere™ Y90 Radiotherapy

• Only U.S. approved therapy for

primary liver cancer (HCC)

Pipeline:

• Clinical trials in follow up target expanded

indications (STOP-HCC & EPOCH)

• Geographic expansion, especially Asia

Galil Cryoablation Therapy

• Unique therapy in kidney cancer

• Microwave system in development

• Over 400,000 patients

diagnosed with kidney

cancer WW annually1

• Ablation modality of

choice to treat kidney

cancers

Pipeline:

• Microwave ablation platform in development

• Flexible needles for use in other cancers

~850,000

patients

diagnosed

with liver

cancer WW

annually1

1International Association of Cancer Registries; GLOBOCAN Database: http://gco.iarc.fr/.

11

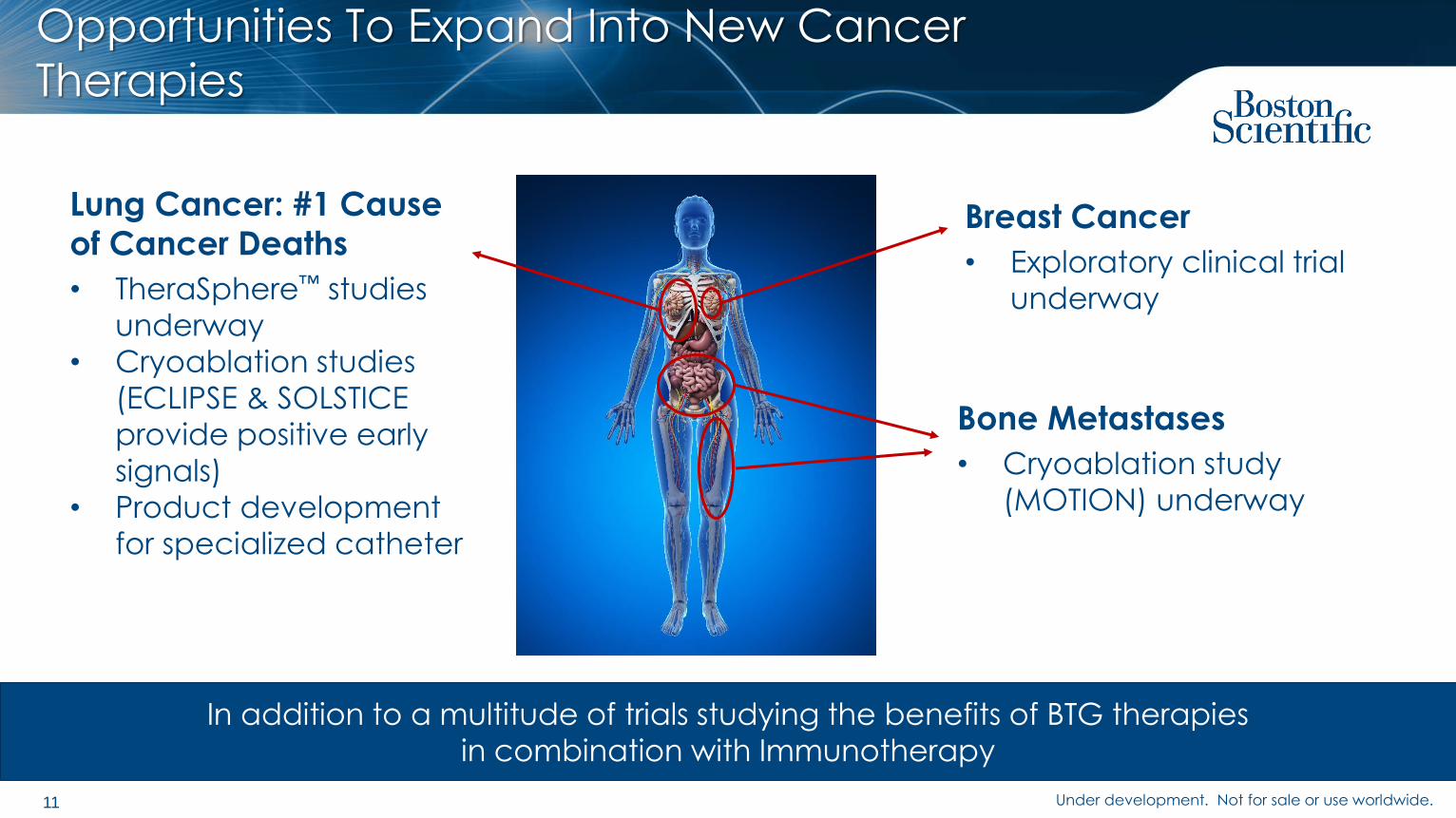

Opportunities To Expand Into New Cancer

Therapies

Lung Cancer: #1 Cause

of Cancer Deaths

• TheraSphere™ studies

underway

• Cryoablation studies

(ECLIPSE & SOLSTICE

provide positive early

signals)

• Product development

for specialized catheter

Bone Metastases

• Cryoablation study

(MOTION) underway

Breast Cancer

• Exploratory clinical trial

underway

In addition to a multitude of trials studying the benefits of BTG therapies

in combination with Immunotherapy

Under development. Not for sale or use worldwide.

12

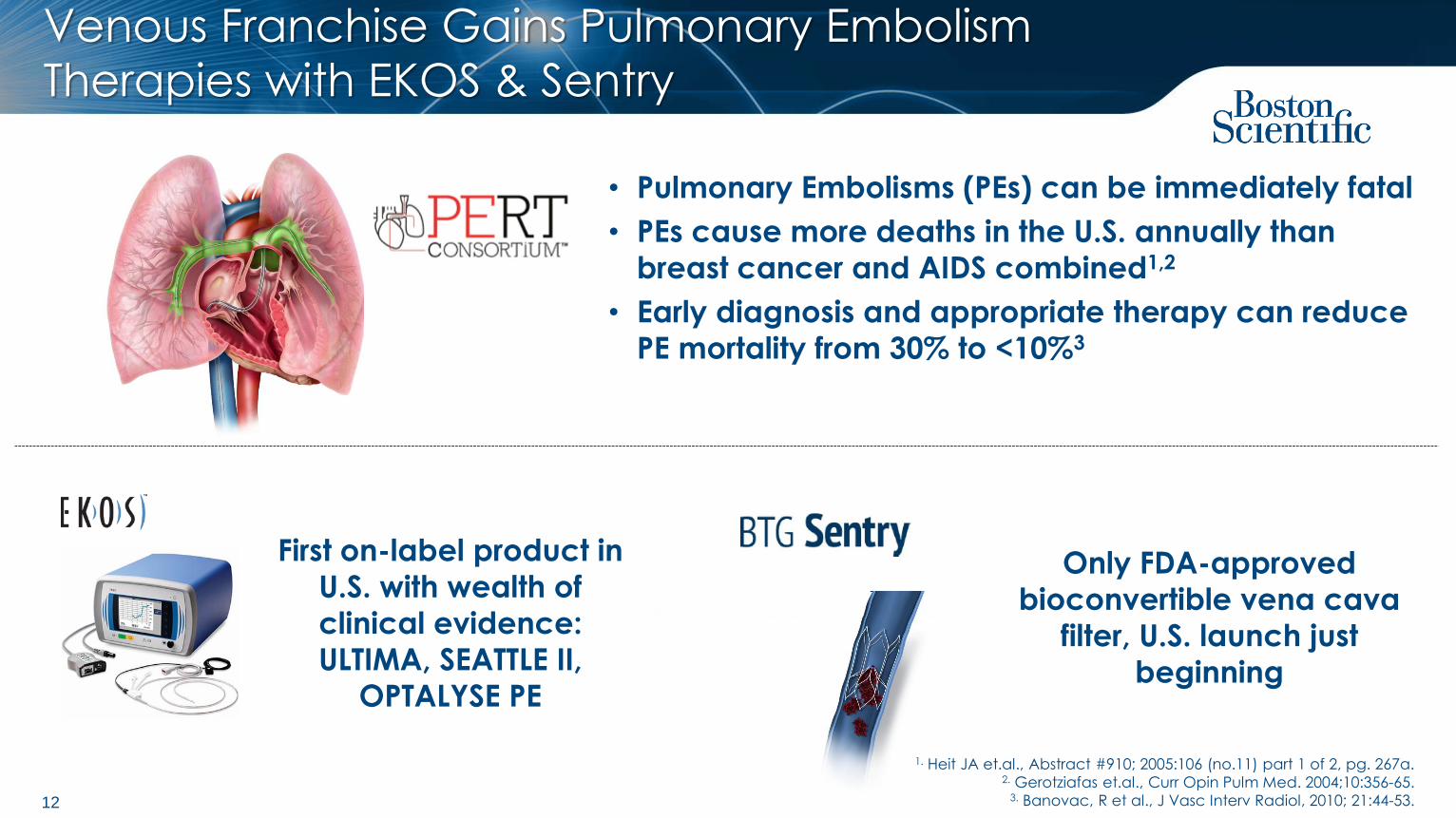

Venous Franchise Gains Pulmonary Embolism

Therapies with EKOS & Sentry

• Pulmonary Embolisms (PEs) can be immediately fatal

• PEs cause more deaths in the U.S. annually than

breast cancer and AIDS combined1,2

• Early diagnosis and appropriate therapy can reduce

PE mortality from 30% to <10%3

First on-label product in

U.S. with wealth of

clinical evidence:

ULTIMA, SEATTLE II,

OPTALYSE PE

Only FDA-approved

bioconvertible vena cava

filter, U.S. launch just

beginning

1. Heit JA et.al., Abstract #910; 2005:106 (no.11) part 1 of 2, pg. 267a.2. Gerotziafas et.al., Curr Opin Pulm Med. 2004;10:356-65.

3. Banovac, R et al., J Vasc Interv Radiol, 2010; 21:44-53.

13

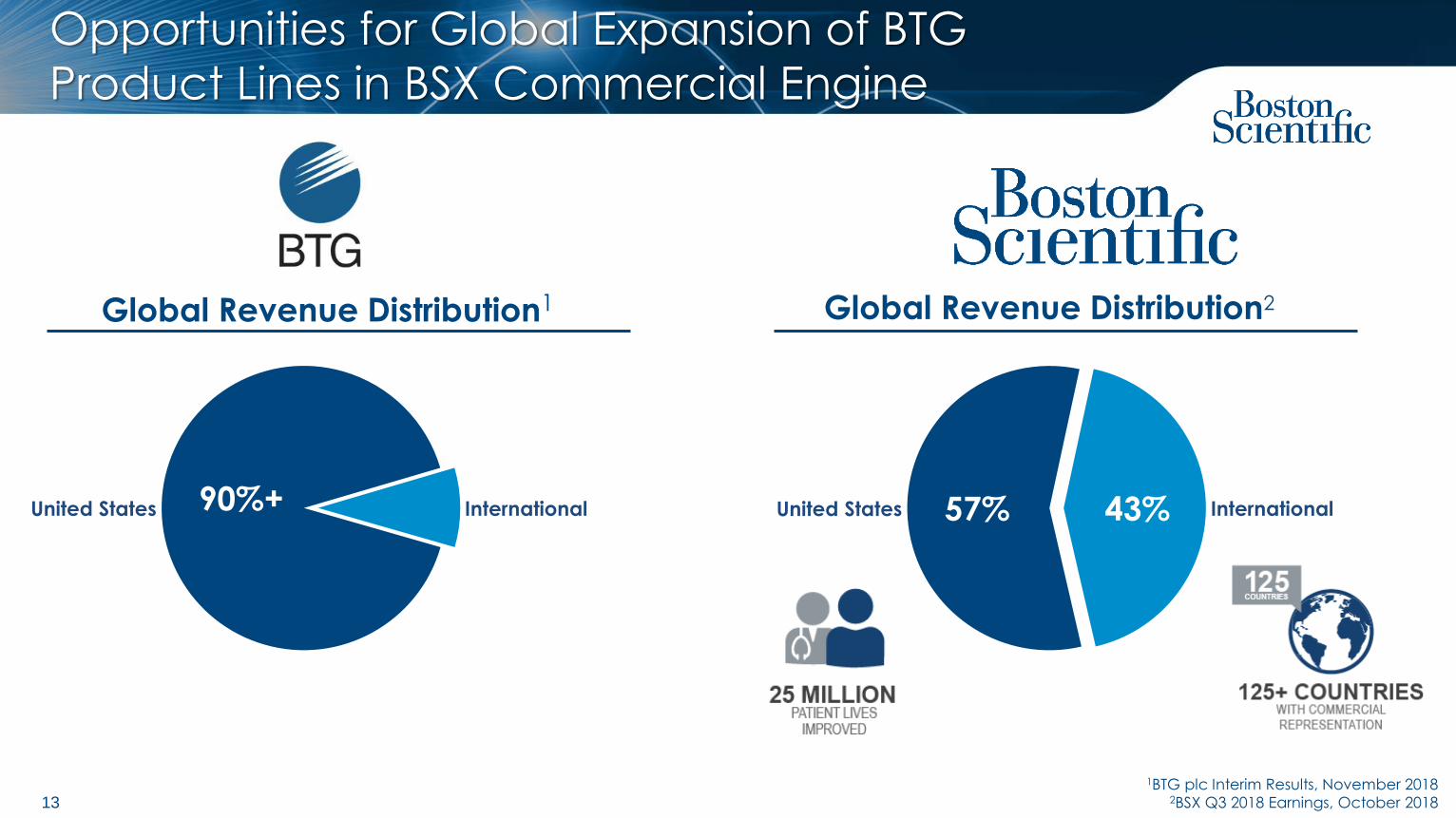

Opportunities for Global Expansion of BTG

Product Lines in BSX Commercial Engine

United States International90%+

Global Revenue Distribution1

InternationalUnited States 57% 43%

Global Revenue Distribution2

1BTG plc Interim Results, November 2018 2BSX Q3 2018 Earnings, October 2018

14

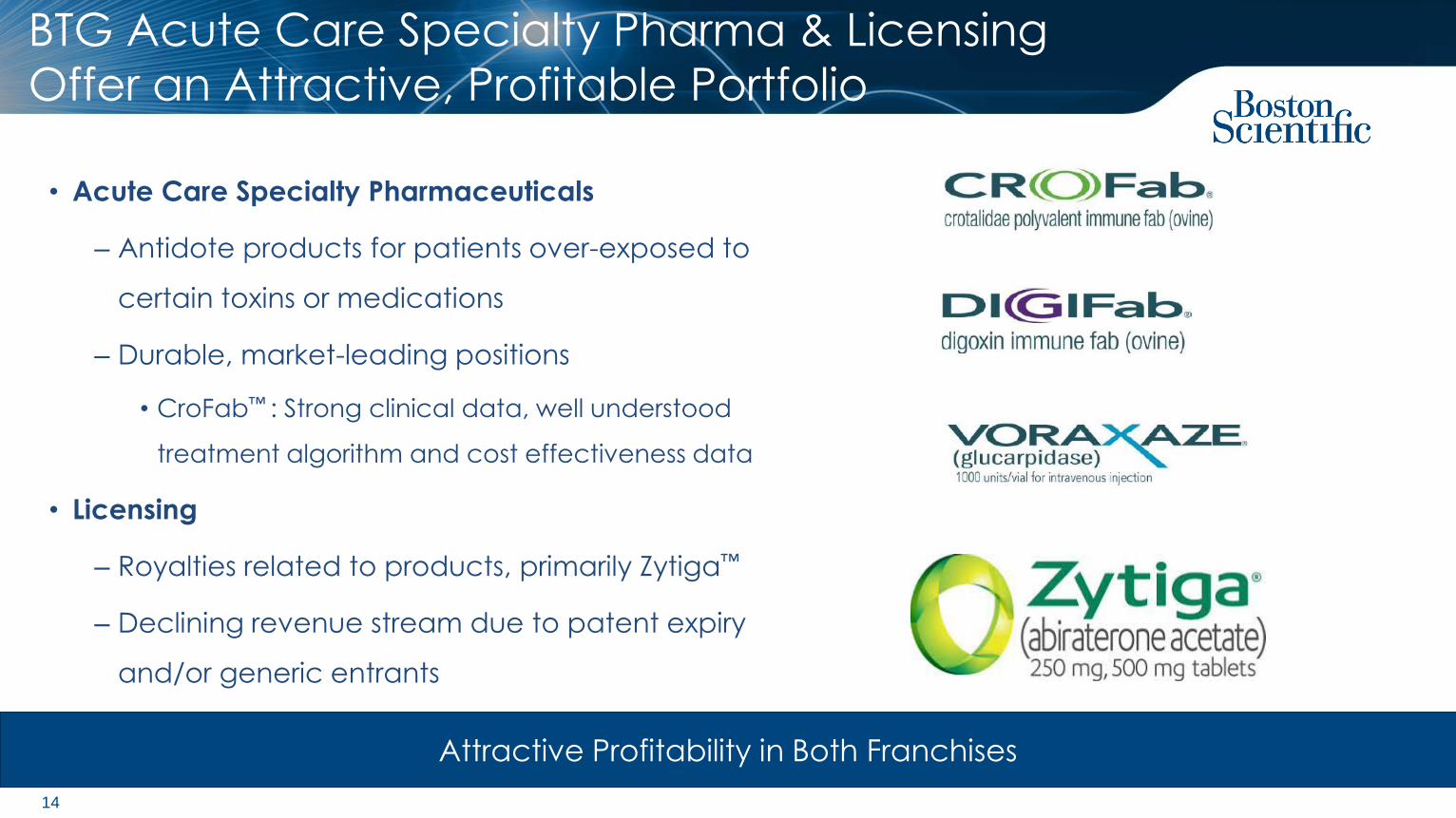

BTG Acute Care Specialty Pharma & Licensing

Offer an Attractive, Profitable Portfolio

• Acute Care Specialty Pharmaceuticals

– Antidote products for patients over-exposed to

certain toxins or medications

– Durable, market-leading positions

• CroFab™ : Strong clinical data, well understood

treatment algorithm and cost effectiveness data

• Licensing

– Royalties related to products, primarily Zytiga™

– Declining revenue stream due to patent expiry

and/or generic entrants

Attractive Profitability in Both Franchises

15

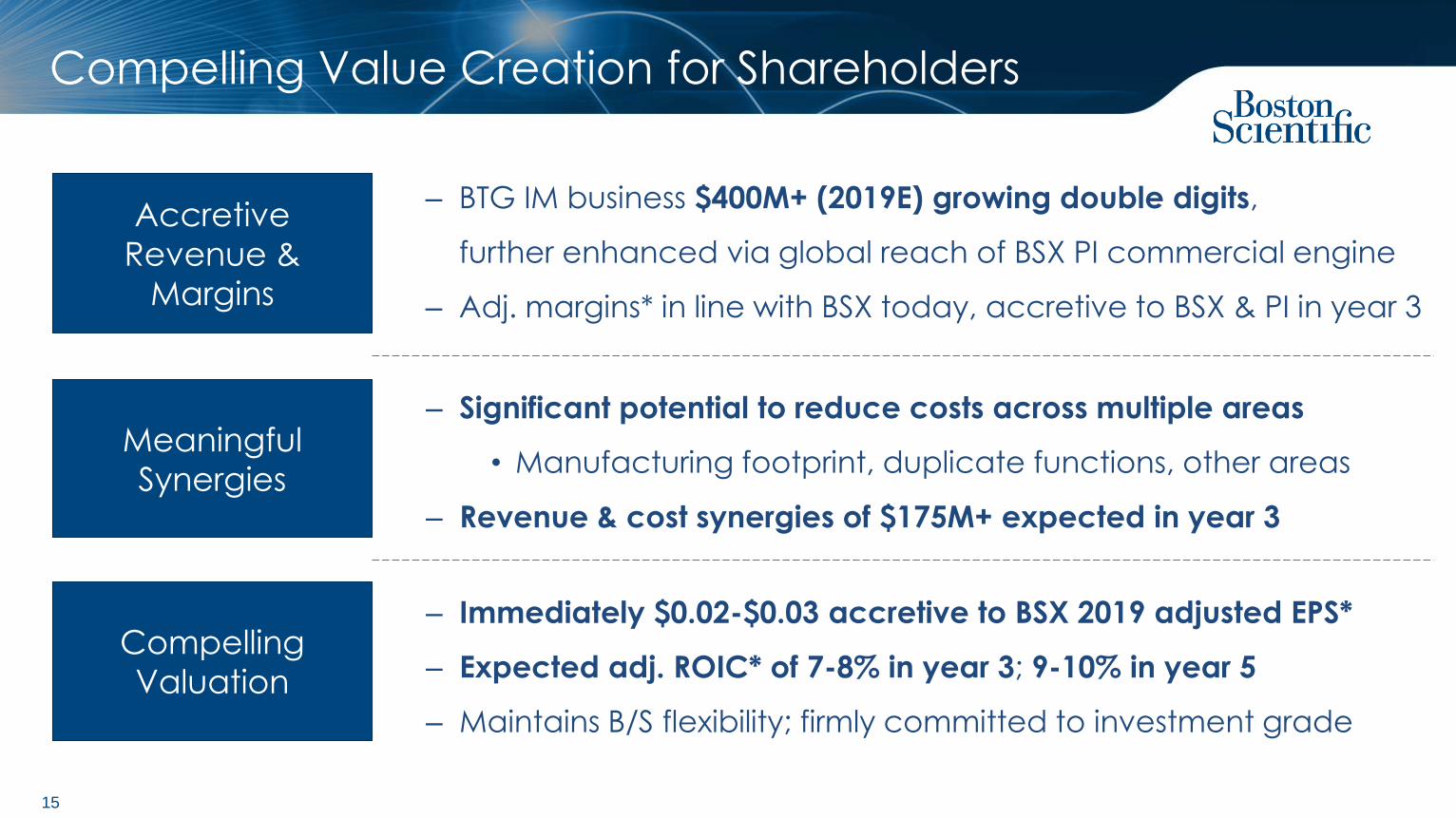

Compelling Value Creation for Shareholders

– Significant potential to reduce costs across multiple areas

• Manufacturing footprint, duplicate functions, other areas

– Revenue & cost synergies of $175M+ expected in year 3

Accretive

Revenue &

Margins

Meaningful

Synergies

Compelling

Valuation

– Immediately $0.02-$0.03 accretive to BSX 2019 adjusted EPS*

– Expected adj. ROIC* of 7-8% in year 3; 9-10% in year 5

– Maintains B/S flexibility; firmly committed to investment grade

– BTG IM business $400M+ (2019E) growing double digits,

further enhanced via global reach of BSX PI commercial engine

– Adj. margins* in line with BSX today, accretive to BSX & PI in year 3

Q&A

Appendix ANon-GAAP Reconciliations

18

Non-GAAP Reconciliations

Use of Non-GAAP Financial MeasuresTo supplement our consolidated financial statements presented on a GAAP basis, we disclose certain non-GAAP financial measures. These non-GAAP financial measures are not in accordance with generally accepted accounting principles in the United States and should not be considered in isolation from or as a replacement for the most directly comparable GAAP financial measures. Further, other companies may calculate these non-GAAP financial measures differently than we do, which may limit the usefulness of those measures for comparative purposes. For further information regarding our non-GAAP measures, see Part II, Item 7 - Management’s Discussion and Analysis of Financial Condition and Results of Operations in our most recent Annual Report on Form 10-K, which we may update in Quarterly Reports on Form 10-Q we have filed or will file hereafter.

Adjusted Gross Margin: To calculate adjusted gross margin certain charges and/or credits are excluded, such as amortization expense, acquisition-related net charges/credits, and restructuring and restructuring-related net charges/credits. The GAAP financial measure most directly comparable to adjusted gross margin is GAAP gross margin.

Adjusted Operating Margin: To calculate adjusted operating margin certain charges and/or credits are excluded, such as amortization expense, acquisition-related net charges/credits, and restructuring and restructuring-related net charges/credits. The GAAP financial measure most directly comparable to adjusted operating margin is GAAP operating margin.

Adjusted Earnings Per Share (EPS): To calculate adjusted EPS certain charges and/or credits are excluded, such as amortization expense, acquisition-related net charges/credits, and restructuring and restructuring-related net charges/credits. The GAAP financial measure most directly comparable to adjusted EPS is GAAP EPS. On a GAAP basis, the transaction is expected to be dilutive in 2019, and less dilutive or increasingly accretive thereafter, as the case may be, due to amortization expense andacquisition-related net charges.

Adjusted Return on Invested Capital (ROIC): Adjusted ROIC is calculated as adjusted net operating profit after tax (NOPAT) divided by invested capital (defined as purchase price enterprise value plus tax planning costs). To calculate adjusted net operating profit certain charges and/or credits are excluded, such as amortization expense, acquisition-related net charges/credits, and restructuring and restructuring-related net charges/credits. The GAAP financial measure most directly comparable to adjusted operating profit is GAAP operating profit.

Please refer to our Safe Harbor for forward-looking statements disclosure in conjunction with any forward looking information presented within.