Brownian Motion and Ito’s Lemma - UT Mathematics Motion and Ito’s Lemma 1 Introduction 2...

42

Brownian Motion and Ito’s Lemma 1 Introduction 2 Geometric Brownian Motion 3 Ito’s Product Rule 4 Some Properties of the Stochastic Integral 5 Correlated Stock Prices 6 The Ornstein-Uhlenbeck Process

-

Upload

truongminh -

Category

Documents

-

view

227 -

download

5

Transcript of Brownian Motion and Ito’s Lemma - UT Mathematics Motion and Ito’s Lemma 1 Introduction 2...

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

Samuelson’s ModelThe Black-Scholes Assumption About

Stock Prices

• The original paper by Black and Scholes assumes that the price ofthe underlying asset is a stochastic process {St} which is solves thefollowing stochastic differential equation (in the differential form):

dSt = St [α dt + σ dZt ]

where

• α . . . denotes the continuously compounded expected return on thestock;

• σ . . . denotes the volatility;

• {Zt} . . . is a standard Brownian motion

• In other words, {St} is a geometric Brownian motion

Samuelson’s ModelThe Black-Scholes Assumption About

Stock Prices

• The original paper by Black and Scholes assumes that the price ofthe underlying asset is a stochastic process {St} which is solves thefollowing stochastic differential equation (in the differential form):

dSt = St [α dt + σ dZt ]

where

• α . . . denotes the continuously compounded expected return on thestock;

• σ . . . denotes the volatility;

• {Zt} . . . is a standard Brownian motion

• In other words, {St} is a geometric Brownian motion

Samuelson’s ModelThe Black-Scholes Assumption About

Stock Prices

• The original paper by Black and Scholes assumes that the price ofthe underlying asset is a stochastic process {St} which is solves thefollowing stochastic differential equation (in the differential form):

dSt = St [α dt + σ dZt ]

where

• α . . . denotes the continuously compounded expected return on thestock;

• σ . . . denotes the volatility;

• {Zt} . . . is a standard Brownian motion

• In other words, {St} is a geometric Brownian motion

Samuelson’s ModelThe Black-Scholes Assumption About

Stock Prices

• The original paper by Black and Scholes assumes that the price ofthe underlying asset is a stochastic process {St} which is solves thefollowing stochastic differential equation (in the differential form):

dSt = St [α dt + σ dZt ]

where

• α . . . denotes the continuously compounded expected return on thestock;

• σ . . . denotes the volatility;

• {Zt} . . . is a standard Brownian motion

• In other words, {St} is a geometric Brownian motion

Samuelson’s ModelThe Black-Scholes Assumption About

Stock Prices

• The original paper by Black and Scholes assumes that the price ofthe underlying asset is a stochastic process {St} which is solves thefollowing stochastic differential equation (in the differential form):

dSt = St [α dt + σ dZt ]

where

• α . . . denotes the continuously compounded expected return on thestock;

• σ . . . denotes the volatility;

• {Zt} . . . is a standard Brownian motion

• In other words, {St} is a geometric Brownian motion

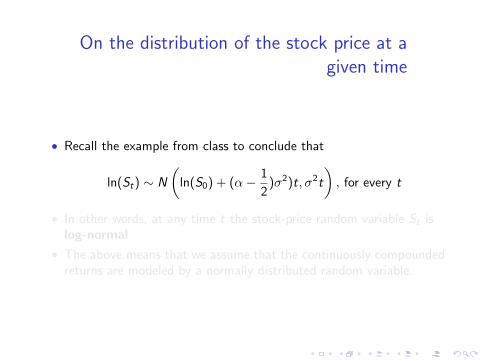

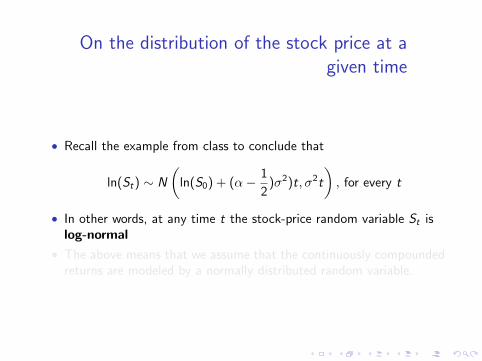

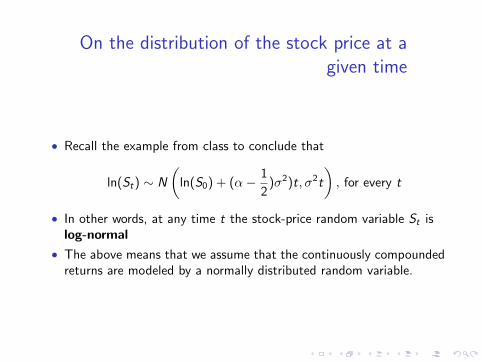

On the distribution of the stock price at agiven time

• Recall the example from class to conclude that

ln(St) ∼ N

(ln(S0) + (α− 1

2)σ2)t, σ2t

), for every t

• In other words, at any time t the stock-price random variable St islog-normal

• The above means that we assume that the continuously compoundedreturns are modeled by a normally distributed random variable.

On the distribution of the stock price at agiven time

• Recall the example from class to conclude that

ln(St) ∼ N

(ln(S0) + (α− 1

2)σ2)t, σ2t

), for every t

• In other words, at any time t the stock-price random variable St islog-normal

• The above means that we assume that the continuously compoundedreturns are modeled by a normally distributed random variable.

On the distribution of the stock price at agiven time

• Recall the example from class to conclude that

ln(St) ∼ N

(ln(S0) + (α− 1

2)σ2)t, σ2t

), for every t

• In other words, at any time t the stock-price random variable St islog-normal

• The above means that we assume that the continuously compoundedreturns are modeled by a normally distributed random variable.

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

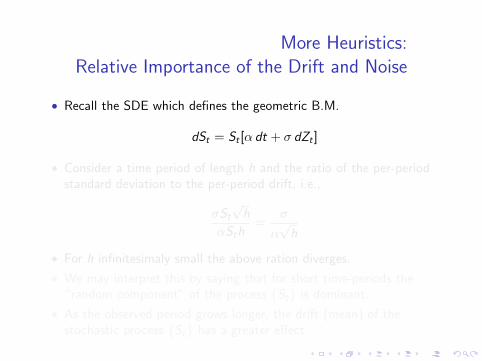

More Heuristics:Relative Importance of the Drift and Noise

• Recall the SDE which defines the geometric B.M.

dSt = St [α dt + σ dZt ]

• Consider a time period of length h and the ratio of the per-periodstandard deviation to the per-period drift, i.e.,

σSt

√h

αSth=

σ

α√

h

• For h infinitesimaly small the above ration diverges.

• We may interpret this by saying that for short time-periods the“random component” of the process {St} is dominant.

• As the observed period grows longer, the drift (mean) of thestochastic process {St} has a greater effect

More Heuristics:Relative Importance of the Drift and Noise

• Recall the SDE which defines the geometric B.M.

dSt = St [α dt + σ dZt ]

• Consider a time period of length h and the ratio of the per-periodstandard deviation to the per-period drift, i.e.,

σSt

√h

αSth=

σ

α√

h

• For h infinitesimaly small the above ration diverges.

• We may interpret this by saying that for short time-periods the“random component” of the process {St} is dominant.

• As the observed period grows longer, the drift (mean) of thestochastic process {St} has a greater effect

More Heuristics:Relative Importance of the Drift and Noise

• Recall the SDE which defines the geometric B.M.

dSt = St [α dt + σ dZt ]

• Consider a time period of length h and the ratio of the per-periodstandard deviation to the per-period drift, i.e.,

σSt

√h

αSth=

σ

α√

h

• For h infinitesimaly small the above ration diverges.

• We may interpret this by saying that for short time-periods the“random component” of the process {St} is dominant.

• As the observed period grows longer, the drift (mean) of thestochastic process {St} has a greater effect

More Heuristics:Relative Importance of the Drift and Noise

• Recall the SDE which defines the geometric B.M.

dSt = St [α dt + σ dZt ]

• Consider a time period of length h and the ratio of the per-periodstandard deviation to the per-period drift, i.e.,

σSt

√h

αSth=

σ

α√

h

• For h infinitesimaly small the above ration diverges.

• We may interpret this by saying that for short time-periods the“random component” of the process {St} is dominant.

• As the observed period grows longer, the drift (mean) of thestochastic process {St} has a greater effect

More Heuristics:Relative Importance of the Drift and Noise

• Recall the SDE which defines the geometric B.M.

dSt = St [α dt + σ dZt ]

• Consider a time period of length h and the ratio of the per-periodstandard deviation to the per-period drift, i.e.,

σSt

√h

αSth=

σ

α√

h

• For h infinitesimaly small the above ration diverges.

• We may interpret this by saying that for short time-periods the“random component” of the process {St} is dominant.

• As the observed period grows longer, the drift (mean) of thestochastic process {St} has a greater effect

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

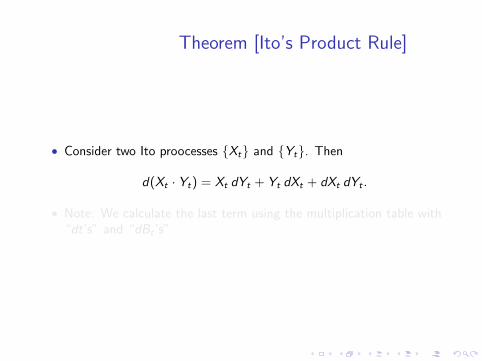

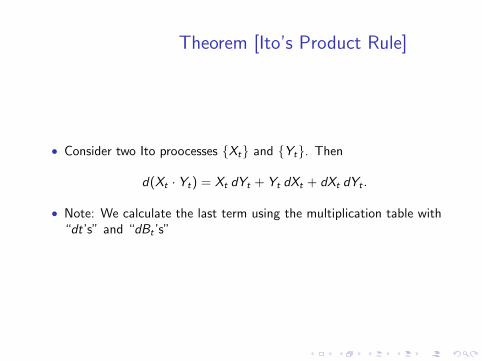

Theorem [Ito’s Product Rule]

• Consider two Ito proocesses {Xt} and {Yt}. Then

d(Xt · Yt) = Xt dYt + Yt dXt + dXt dYt .

• Note: We calculate the last term using the multiplication table with“dt’s” and “dBt ’s”

Theorem [Ito’s Product Rule]

• Consider two Ito proocesses {Xt} and {Yt}. Then

d(Xt · Yt) = Xt dYt + Yt dXt + dXt dYt .

• Note: We calculate the last term using the multiplication table with“dt’s” and “dBt ’s”

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

Martingality

• Under some integrability and regularity conditions on the integrand,the process {Yt} defined by

Yt =

∫ t

0

νs dBS ,

where {Bs} is a standard B.M. is a martingale.

• In particular

E[Yt ] = E[∫ t

0

νs dBS

]= 0, for every t

Martingality

• Under some integrability and regularity conditions on the integrand,the process {Yt} defined by

Yt =

∫ t

0

νs dBS ,

where {Bs} is a standard B.M. is a martingale.

• In particular

E[Yt ] = E[∫ t

0

νs dBS

]= 0, for every t

Ito Isometry

• Under some integrability and regularity conditions on the integrandν, let us define the process {Yt} as

Yt =

∫ t

0

νs dBS ,

where {Bs} is a standard B.M. Then

E[Y 2t ] = E[

∫ t

0

ν2s ds]

Continuity

• Under some integrability and regularity conditions on the integrandν, let us define the process {Yt} as

Yt =

∫ t

0

νs dBS ,

where {Bs} is a standard B.M. Then the paths of {Yt} are (almostsurely) continuous.

Linearity

• Moreover, for a constant c , we have that

cYt =

∫ t

0

(cνs) dBS ,

• Additionally, if {At} is a stochastic process given as

At =

∫ t

0

ξs dBs ,

for an integrand {ξt} conforming to the integrability and regularityconditions necessary for the sotchastic integral to be well-defined,then

Yt ± At =

∫ t

0

(νs ± ξS) dBS

Linearity

• Moreover, for a constant c , we have that

cYt =

∫ t

0

(cνs) dBS ,

• Additionally, if {At} is a stochastic process given as

At =

∫ t

0

ξs dBs ,

for an integrand {ξt} conforming to the integrability and regularityconditions necessary for the sotchastic integral to be well-defined,then

Yt ± At =

∫ t

0

(νs ± ξS) dBS

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

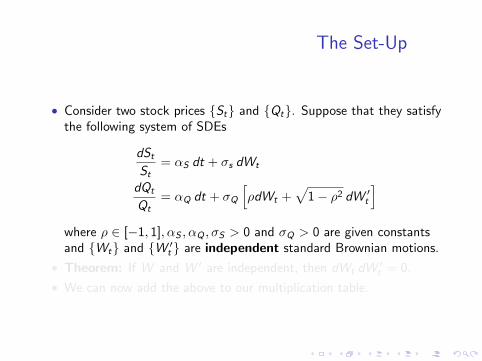

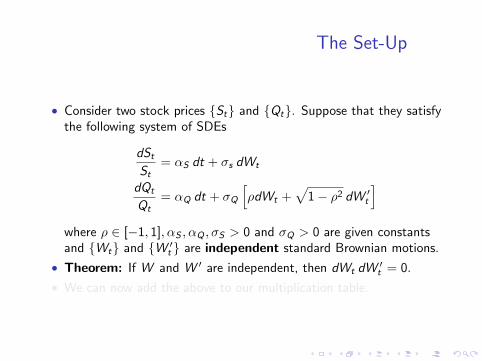

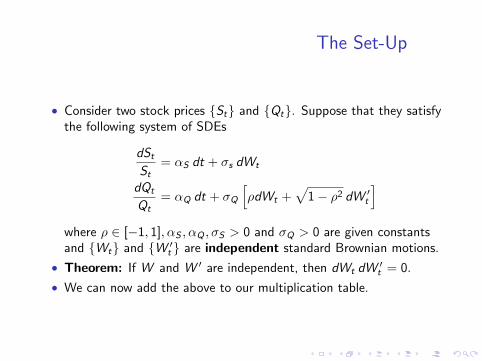

The Set-Up

• Consider two stock prices {St} and {Qt}. Suppose that they satisfythe following system of SDEs

dSt

St= αS dt + σs dWt

dQt

Qt= αQ dt + σQ

[ρdWt +

√1− ρ2 dW ′

t

]where ρ ∈ [−1, 1], αS , αQ , σS > 0 and σQ > 0 are given constantsand {Wt} and {W ′

t } are independent standard Brownian motions.

• Theorem: If W and W ′ are independent, then dWt dW ′t = 0.

• We can now add the above to our multiplication table.

The Set-Up

• Consider two stock prices {St} and {Qt}. Suppose that they satisfythe following system of SDEs

dSt

St= αS dt + σs dWt

dQt

Qt= αQ dt + σQ

[ρdWt +

√1− ρ2 dW ′

t

]where ρ ∈ [−1, 1], αS , αQ , σS > 0 and σQ > 0 are given constantsand {Wt} and {W ′

t } are independent standard Brownian motions.

• Theorem: If W and W ′ are independent, then dWt dW ′t = 0.

• We can now add the above to our multiplication table.

The Set-Up

• Consider two stock prices {St} and {Qt}. Suppose that they satisfythe following system of SDEs

dSt

St= αS dt + σs dWt

dQt

Qt= αQ dt + σQ

[ρdWt +

√1− ρ2 dW ′

t

]where ρ ∈ [−1, 1], αS , αQ , σS > 0 and σQ > 0 are given constantsand {Wt} and {W ′

t } are independent standard Brownian motions.

• Theorem: If W and W ′ are independent, then dWt dW ′t = 0.

• We can now add the above to our multiplication table.

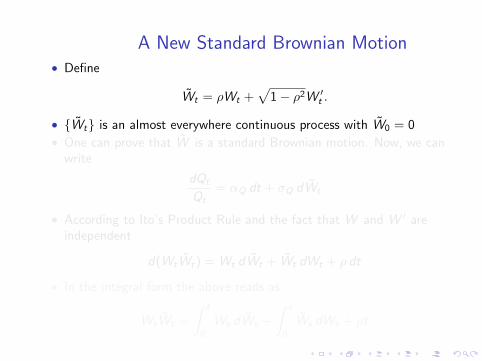

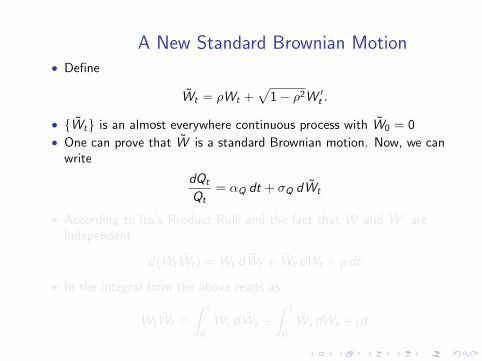

A New Standard Brownian Motion• Define

W̃t = ρWt +√

1− ρ2W ′t .

• {W̃t} is an almost everywhere continuous process with W̃0 = 0

• One can prove that W̃ is a standard Brownian motion. Now, we canwrite

dQt

Qt= αQ dt + σQ dW̃t

• According to Ito’s Product Rule and the fact that W and W ′ areindependent

d(WtW̃t) = Wt dW̃t + W̃t dWt + ρ dt

• In the integral form the above reads as

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

A New Standard Brownian Motion• Define

W̃t = ρWt +√

1− ρ2W ′t .

• {W̃t} is an almost everywhere continuous process with W̃0 = 0

• One can prove that W̃ is a standard Brownian motion. Now, we canwrite

dQt

Qt= αQ dt + σQ dW̃t

• According to Ito’s Product Rule and the fact that W and W ′ areindependent

d(WtW̃t) = Wt dW̃t + W̃t dWt + ρ dt

• In the integral form the above reads as

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

A New Standard Brownian Motion• Define

W̃t = ρWt +√

1− ρ2W ′t .

• {W̃t} is an almost everywhere continuous process with W̃0 = 0

• One can prove that W̃ is a standard Brownian motion. Now, we canwrite

dQt

Qt= αQ dt + σQ dW̃t

• According to Ito’s Product Rule and the fact that W and W ′ areindependent

d(WtW̃t) = Wt dW̃t + W̃t dWt + ρ dt

• In the integral form the above reads as

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

A New Standard Brownian Motion• Define

W̃t = ρWt +√

1− ρ2W ′t .

• {W̃t} is an almost everywhere continuous process with W̃0 = 0

• One can prove that W̃ is a standard Brownian motion. Now, we canwrite

dQt

Qt= αQ dt + σQ dW̃t

• According to Ito’s Product Rule and the fact that W and W ′ areindependent

d(WtW̃t) = Wt dW̃t + W̃t dWt + ρ dt

• In the integral form the above reads as

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

A New Standard Brownian Motion• Define

W̃t = ρWt +√

1− ρ2W ′t .

• {W̃t} is an almost everywhere continuous process with W̃0 = 0

• One can prove that W̃ is a standard Brownian motion. Now, we canwrite

dQt

Qt= αQ dt + σQ dW̃t

• According to Ito’s Product Rule and the fact that W and W ′ areindependent

d(WtW̃t) = Wt dW̃t + W̃t dWt + ρ dt

• In the integral form the above reads as

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

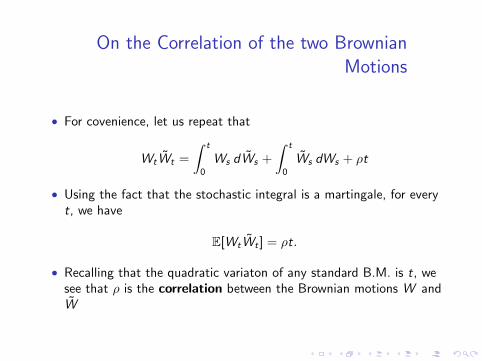

On the Correlation of the two BrownianMotions

• For covenience, let us repeat that

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

• Using the fact that the stochastic integral is a martingale, for everyt, we have

E[WtW̃t ] = ρt.

• Recalling that the quadratic variaton of any standard B.M. is t, wesee that ρ is the correlation between the Brownian motions W andW̃

On the Correlation of the two BrownianMotions

• For covenience, let us repeat that

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

• Using the fact that the stochastic integral is a martingale, for everyt, we have

E[WtW̃t ] = ρt.

• Recalling that the quadratic variaton of any standard B.M. is t, wesee that ρ is the correlation between the Brownian motions W andW̃

On the Correlation of the two BrownianMotions

• For covenience, let us repeat that

WtW̃t =

∫ t

0

Ws dW̃s +

∫ t

0

W̃s dWs + ρt

• Using the fact that the stochastic integral is a martingale, for everyt, we have

E[WtW̃t ] = ρt.

• Recalling that the quadratic variaton of any standard B.M. is t, wesee that ρ is the correlation between the Brownian motions W andW̃

Brownian Motion and Ito’s Lemma

1 Introduction

2 Geometric Brownian Motion

3 Ito’s Product Rule

4 Some Properties of the Stochastic Integral

5 Correlated Stock Prices

6 The Ornstein-Uhlenbeck Process

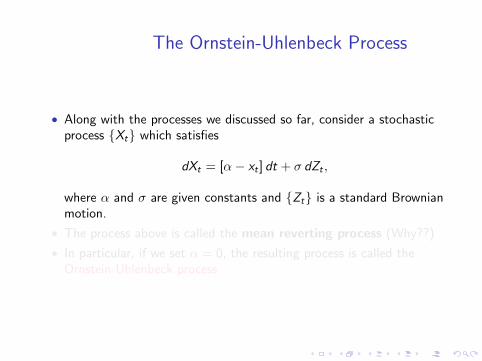

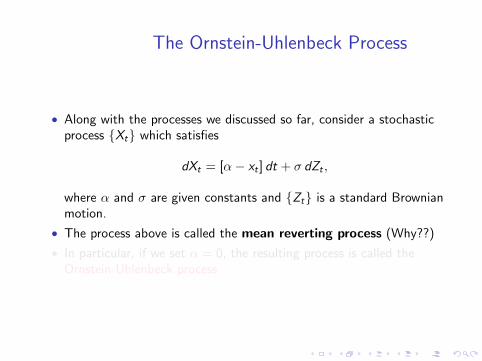

The Ornstein-Uhlenbeck Process

• Along with the processes we discussed so far, consider a stochasticprocess {Xt} which satisfies

dXt = [α− xt ] dt + σ dZt ,

where α and σ are given constants and {Zt} is a standard Brownianmotion.

• The process above is called the mean reverting process (Why??)

• In particular, if we set α = 0, the resulting process is called theOrnstein-Uhlenbeck process

The Ornstein-Uhlenbeck Process

• Along with the processes we discussed so far, consider a stochasticprocess {Xt} which satisfies

dXt = [α− xt ] dt + σ dZt ,

where α and σ are given constants and {Zt} is a standard Brownianmotion.

• The process above is called the mean reverting process (Why??)

• In particular, if we set α = 0, the resulting process is called theOrnstein-Uhlenbeck process

The Ornstein-Uhlenbeck Process

• Along with the processes we discussed so far, consider a stochasticprocess {Xt} which satisfies

dXt = [α− xt ] dt + σ dZt ,

where α and σ are given constants and {Zt} is a standard Brownianmotion.

• The process above is called the mean reverting process (Why??)

• In particular, if we set α = 0, the resulting process is called theOrnstein-Uhlenbeck process