GLOBE Advisors - British Columbia’s Clean Energy Supply & Storage Sector Market Report

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 1

3PAR Inc.

Buy (PAR, $6.68)

Initiating Coverage

$8.30 Target

April 2, 2009

Analyst: Mark Kelleher (508) 655-8193 [email protected]

Senior Associate: Aron Honig (978) 658-5859 [email protected]

Conclusion

■ Storage Virtualization Platform. One of the key drivers in data center design is the ability to virtualize IT environments to drive higher efficiencies from storage and server resources. 3PAR’s products provide a comprehensive virtualized storage platform, with key abilities such as thin provisioning. 3PAR’s platform is well suited as the foundation for managed service providers which are offering shared computing environments to their service clients. Outsourcing key computational functions to service providers is referred to as Cloud Computing, an architecture gaining rapid adoption, for which 3PAR’s systems are the natural storage element.

■ Gaining market share. The company grew revenue 73% in fiscal 2007, 78% in fiscal 2008, and we project will achieve 53% growth in fiscal 2009 (ending March). The company has grown at a much higher rate over this time period than all of its competitors in the enterprise storage market. By comparison, leading competitor EMC grew product revenue 15% in 2006, 11% in 2007, and 13% in 2008. Network Appliance grew revenue 33% in calendar 2006, 22% in calendar 2007, and just 9% in calendar 2008.

■ Recommendation. We believe 3PAR’s unique architecture, built from the ground up to incorporate storage virtualization concepts such as dynamic provisioning of storage capacity, positions the company well to take advantage of new computing architectures such as Cloud Computing. We believe the company can maintain at least a 30% growth rate over the next several years. Based on a P/E/G ratio of one and a calendar 2010 EPS estimate of $0.28, we calculate a 12-month price target of $8.30. We are therefore initiating coverage of 3PAR with a Buy recommendation.

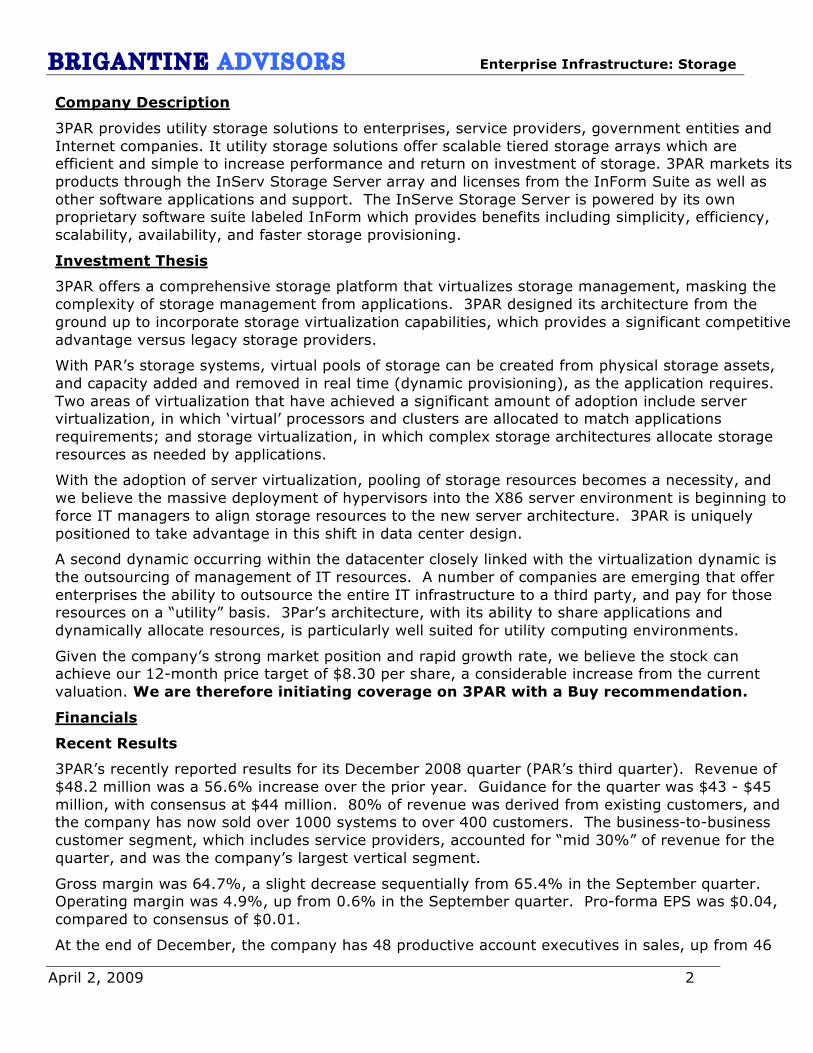

PAR $6.68 EPS 2009E 2010E 2011E Mkt. Cap $M $422 1Q 0.03 0.02 0.06

FYE Mar 2Q 0.01 0.04 0.08

DIL Shr M 63 3Q 0.04 0.04 0.09

52 hi-lo $11-$4 4Q (0.01) 0.05 0.11 P/S FY09 2.1x Year 0.07 0.14 0.34

P/Book 3.5x P/E 101.7x 46.4x 19.9x

FCF/Share $0.06 Revenue $M

FCF Yield 1% 1Q 43.0 45.0 60.0

EV/EBITDA 39.9x 2Q 45.1 49.5 63.0

Debt to Cap NA 3Q 48.2 53.5 67.0 BV/Share $1.94 4Q 44.5 57.5 70.0

Source: MSN Money Note: EPS excludes one-time items

Please see addendum for disclosures. Net Debt/Sh NA Year 180.8 205.5 260.0

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 2

Company Description

3PAR provides utility storage solutions to enterprises, service providers, government entities and Internet companies. It utility storage solutions offer scalable tiered storage arrays which are efficient and simple to increase performance and return on investment of storage. 3PAR markets its products through the InServ Storage Server array and licenses from the InForm Suite as well as other software applications and support. The InServe Storage Server is powered by its own proprietary software suite labeled InForm which provides benefits including simplicity, efficiency, scalability, availability, and faster storage provisioning.

Investment Thesis

3PAR offers a comprehensive storage platform that virtualizes storage management, masking the complexity of storage management from applications. 3PAR designed its architecture from the ground up to incorporate storage virtualization capabilities, which provides a significant competitive advantage versus legacy storage providers.

With PAR’s storage systems, virtual pools of storage can be created from physical storage assets, and capacity added and removed in real time (dynamic provisioning), as the application requires. Two areas of virtualization that have achieved a significant amount of adoption include server virtualization, in which ‘virtual’ processors and clusters are allocated to match applications requirements; and storage virtualization, in which complex storage architectures allocate storage resources as needed by applications.

With the adoption of server virtualization, pooling of storage resources becomes a necessity, and we believe the massive deployment of hypervisors into the X86 server environment is beginning to force IT managers to align storage resources to the new server architecture. 3PAR is uniquely positioned to take advantage in this shift in data center design.

A second dynamic occurring within the datacenter closely linked with the virtualization dynamic is the outsourcing of management of IT resources. A number of companies are emerging that offer enterprises the ability to outsource the entire IT infrastructure to a third party, and pay for those resources on a “utility” basis. 3Par’s architecture, with its ability to share applications and dynamically allocate resources, is particularly well suited for utility computing environments.

Given the company’s strong market position and rapid growth rate, we believe the stock can achieve our 12-month price target of $8.30 per share, a considerable increase from the current valuation. We are therefore initiating coverage on 3PAR with a Buy recommendation.

Financials

Recent Results

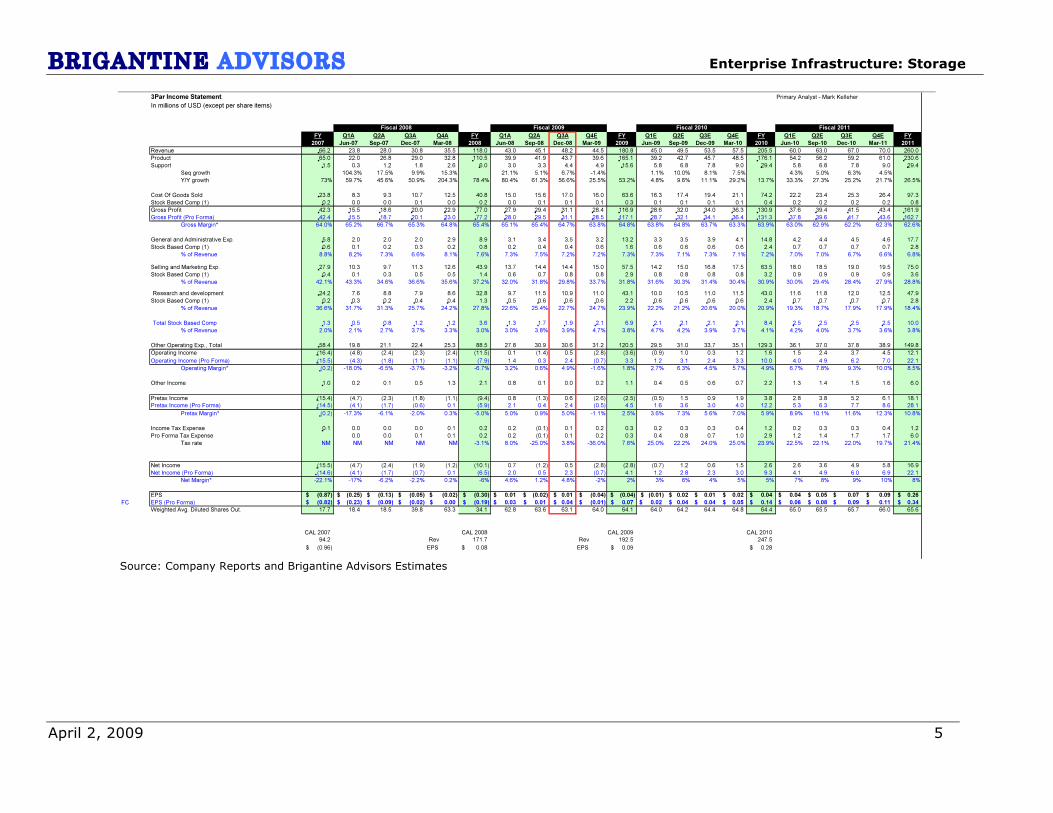

3PAR’s recently reported results for its December 2008 quarter (PAR’s third quarter). Revenue of $48.2 million was a 56.6% increase over the prior year. Guidance for the quarter was $43 - $45 million, with consensus at $44 million. 80% of revenue was derived from existing customers, and the company has now sold over 1000 systems to over 400 customers. The business-to-business customer segment, which includes service providers, accounted for “mid 30%” of revenue for the quarter, and was the company’s largest vertical segment.

Gross margin was 64.7%, a slight decrease sequentially from 65.4% in the September quarter. Operating margin was 4.9%, up from 0.6% in the September quarter. Pro-forma EPS was $0.04, compared to consensus of $0.01.

At the end of December, the company has 48 productive account executives in sales, up from 46

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 3

the previous quarter. Total employees at the end of the quarter were 572, up from 503 in the September quarter.

Although the company did see some fluctuations in its bookings stream due to macro economic factors in the December quarter, the pipeline of orders remains strong as PAR continues to take market share from larger competitors. For fiscal 2009 (ending March 2009, the current quarter), PAR increased its revenue guidance from $171 - $179 million to $178 - $184 million.

We believe the economic uncertainty helps vendors such as PAR which offer solutions to improve efficiency and save costs, as customers are more open to new approaches.

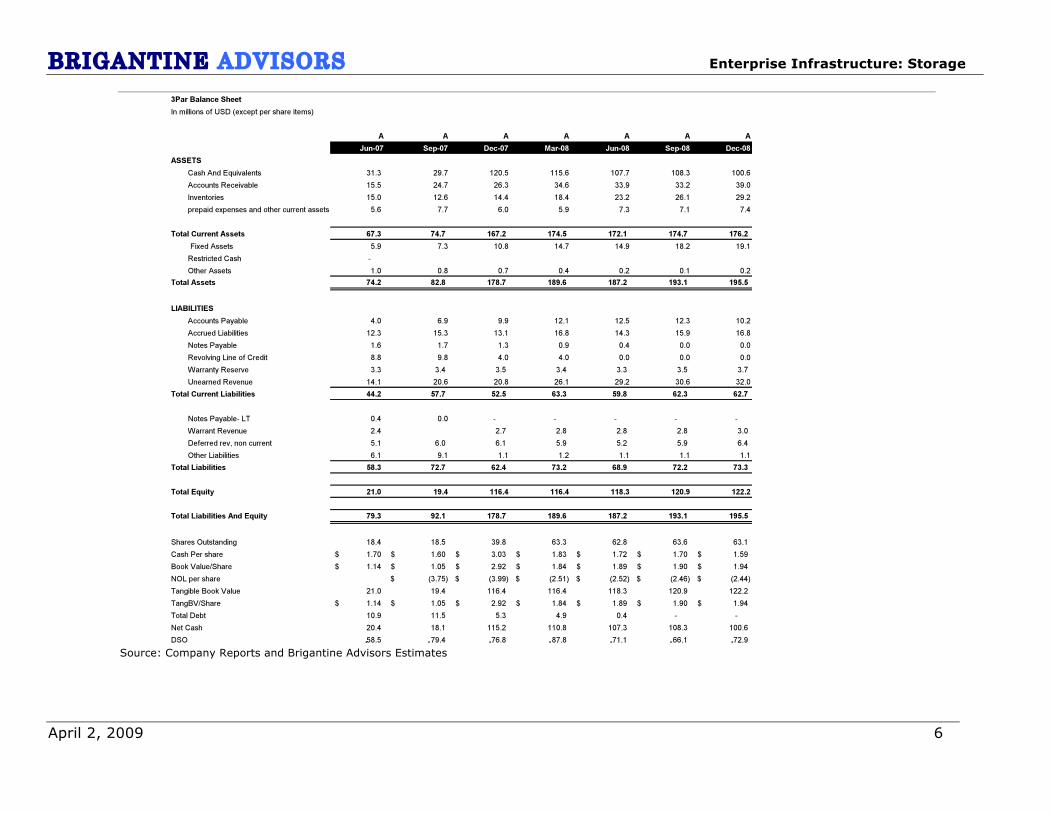

Balance Sheet The company has just over $100 million in cash at the end of December ($1.59 per share) and no debt.

Estimates For Q4, which we expect 3PAR to report in early May, we project $44.5 million in revenue, a 25% year-over-year growth rate. Guidance for the March quarter stands at $42 - $48 million. We are expecting gross margins of 63.8% and Pro Forma EPS of ($0.01). We would note that PAR benefited somewhat in gross margins and operating margins by shutting a factory at the end of December, as a precaution given economic uncertainty. That cost leverage will not repeat in the March quarter.

For fiscal 2010 (ending March 2010), we are projecting revenue $205.5 million, a 13.7% year-over-year growth rate. Given the economic uncertainty, we believe this is a prudent forecast. For EPS, we are projecting $0.14. For calendar 2010, we are estimating $247.5 million of revenue and $0.28 of EPS.

Valuation

We believe PAR can maintain a 30% earnings growth rate for the foreseeable future. Based on our $0.28 EPS estimate for calendar 2010 and a P/E/G ratio of 1, we determine a 12-month price target for 3PAR of $8.30.

Recommendation

We believe 3PAR’s storage virtualization software, built from the ground up to maximize capacity utilization within server systems, is well positioned for rapid growth. Cloud Computing is just one important architecture that requires intelligent storage solutions. Legacy architectures from large competitors such as EMC, IBM, and HP simply cannot be retro-fitted to include functionality such as thin provisioning. As a result, there is a significant opportunity for PAR to gain market share.

We believe 3PAR can continue a growth trajectory over the next several years of at least 30%. Based on this growth rate assumption and our calendar 2010 EPS estimate, we calculate a 12-month price target for 3PAR of $8.30, considerably higher than the current valuation. We are therefore initiating coverage of 3PAR with a Buy recommendation.

Risks

Competition. 3Par competes against such tier-one vendors as EMC, IBM, Hitachi Data Systems, Sun Microsystems, Hewlett Packard – as well as potential new and emerging vendors and various competing technologies. With such competition, there exists the potential for significant pricing pressure.

Market concentration. The managed services (utility computing) market segment is the largest

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 4

contributor to revenue (high 30% range of revenue). If this segment should encounter macro economic difficulties, PAR revenues may deteriorate.

Product risk. PAR operates under a single product family, InServ. If the storage market declines or 3Par’s products fails to maintain or achieve market acceptance, then future losses could be imminent.

Valuation assumption. In our valuation determination, we have made several assumptions as to earnings estimates, company growth rate, and market earnings multiples. If any of these assumptions should be less than accurate, our price target could be inaccurate.

For additional operational risks, see 3PAR’s 10-K filing with the Securities and Exchange Commission.

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 5

Source: Company Reports and Brigantine Advisors Estimates

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 6

Source: Company Reports and Brigantine Advisors Estimates

BRIGANTINE ADVISORS Enterprise Infrastructure: Storage

April 2, 2009 7

Analyst Certification The research analyst(s) primarily responsible for the preparation of this research report hereby certify that all of the views expressed in this research report accurately reflect their personal views about any and all of the subject securities or issuers. The research analyst(s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report. Stock Rating 1-Buy - The stock is expected to deliver a total return of 15% over a 12-month investment horizon. 2-Hold - The stock is expected to deliver less than a 15% positive return or less than a 10% negative return, over a 12-month investment horizon. 3-Sell - The stock is expected to deliver a negative total return of 10% over a 12-month investment horizon. Important Disclosures This report has been prepared by Brigantine Advisors LLC. This publication does not constitute an offer or solicitation of any transaction in any securities referred to herein. Any recommendation contained herein may not be suitable for all investors. Although the information contained in the subject report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This publication and any recommendation contained herein speak only as of the date hereof and are subject to change without notice. Brigantine Advisors and its employees shall have no obligation to update or amend any information or opinion contained herein. This publication is being furnished to you for informational purposes only and on the condition that it will not form the sole basis for any investment decision. Each investor must make their own determination of the appropriateness of an investment in any securities referred to herein based on the tax, or other considerations applicable to such investor and its own investment strategy. By virtue of this publication, neither Brigantine Advisors nor any of its employees, nor any data provider or any of its employees shall be responsible for any investment decision. This report may not be reproduced, distributed, or published without the prior consent of Brigantine Advisors. All rights reserved by Brigantine Advisors. Brigantine Advisors and its logo are registered trademarks of Brigantine Advisors LLC. This report may discuss numerous securities, some of which may not be qualified for sale in certain states and may therefore not be offered to investors in such states. This document should not be construed as providing investment services. Investing in non-U.S. securities including ADRs involves significant risks such as fluctuation of exchange rates that may have adverse effects on the value or price of income derived from the security. Securities of some foreign companies may be less liquid and prices more volatile than securities of U.S. companies. Securities of non-U.S. issuers may not be registered with or subject to Securities and Exchange Commission reporting requirements; therefore, information regarding such issuers may be limited.