Breakout: US GAAP - Ernst & Young...Breakout: US GAAP 4th Annual Financial Reporting Insights Can a...

52

The better the question. The better the answer . The better the world works. Breakout: US GAAP 4th Annual Financial Reporting Insights Can a wider look on reporting enable greater trust in business? Athens, 13 December 2017

Transcript of Breakout: US GAAP - Ernst & Young...Breakout: US GAAP 4th Annual Financial Reporting Insights Can a...

The better the question. The better the answer �.The better the world works.

Breakout: US GAAP

4th Annual Financial Reporting InsightsCan a wider look on reporting enable greater trust in business?

Athens, 13 December 2017

Page 2 Financial Reporting Insights – December 2017

1 Revenue from contracts with customers & Leases- Dimitrios Athanasopoulos & Foteini Mega

Internal control over financial reporting- Sofia Stamatelou

Consolidation- Ioannis Bravos

Credit losses- Elly denOudsten

Agenda: US GAAP

2345 Final accounting guidance 2017 & upcoming 2018+

- Elly denOudsten

FASB developments- Sofia Stamatelou6

Page 3

1a Revenue from contracts with customers

Financial Reporting Insights – December 2017

Page 4

Revenue from contracts with customersDisclosure

► Entity must present qualitative and quantitative information about:

► Contracts with customers► Significant judgments and changes in judgments made when applying the guidance to those

contracts► Assets recognized from costs to obtain or fulfill a contract

“These disclosures are an important part of the new revenue standard forinvestors, and we urge companies to treat them as such and to allocate theappropriate time and resources to them.”

— SEC Chief Accountant, Wesley Bricker

Financial Reporting Insights – December 2017

Page 5

► Contract duration► Evaluating termination clauses

► Identifying performance obligations► Assessing whether highly interrelated/highly interdependent

► Customer options► Distinguishing between a customer option and variable consideration

► Variable consideration► Constraining estimates of variable consideration► Applying the allocation exception

► Contract costs► Capitalizing costs to obtain a contract► Capitalizing costs to fulfill a contract

► Income taxes► Measuring changes in temporary differences► Assessing requirements for tax method changes

Revenue from contracts with customersAccounting implementation observations

Financial Reporting Insights – December 2017

Page 6

Shipping industry- Transition disclosures44 SEC SIC 4412 issuers based on most recent filings

0%

93%

7%

Status of assessment

Not started In progress Completed

34%

66%

0%

Impact

No impact or not expected to have a material impactNo reliable estimate or no clear indication of the expected effectMaterial impact

Financial Reporting Insights – December 2017

Page 7

Shipping industryWhat does ASC 606 mean for the Shipping industry

ASC 606

Financial Reporting Insights – December 2017

Page 8

Shipping industryQuestions

► What types of chartering activities falls under ASC 606? Voyage charters, COA…► Do certain shipping contracts include non-lease components (i.e. time charters)? Recent

developments► What is the duration of the contract? How would a cancellation clause affect timing of revenue

recognition under the new standards?► Is revenue from services for shipping contracts a single performance obligation?► Are there variable considerations in shipping contracts?► How is the recognition of demurrage and dispatch affected by the new standards?► Shipping cargo takes time to complete. When should revenue from services be recognized?► How should voyage expenses (i.e. canal dues, bunkers), operating expenses (i.e. crew cost,

lubricants, insurance cost) or address commissions be treated? What about brokeragecommissions?

► What new disclosures are required?

Financial Reporting Insights – December 2017

Page 9

Shipping industryExamples of transition disclosuresTeekay’s disclosure on most recent filing of financial statements:► “…The Company expects that the adoption of ASU 2014-09 may result in a change in the method of recognizing

revenue from voyage charters, whereby the Company’s method of determining proportional performance will changefrom discharge-to-discharge to load-to-discharge. This will result in no revenue being recognized from discharge of theprior voyage to loading of the current voyage and all revenue being recognized from loading of the current voyage todischarge of the current voyage. This change will result in revenue being recognized later in the voyage which maycause additional volatility in revenue and earnings between periods. The Company is in the process of validatingaspects of its preliminary assessment of ASU 2014-09, determining the transitional impact and completing other itemsrequired for the adoption of ASU 2014-09.”

Financial Reporting Insights – December 2017

Page 10

Shipping industryExamples of transition disclosuresArdmore’s disclosure on most recent filing of financial statements:► “…The Company expects that the adoption of ASU 2014-09 may result in a change in the method of recognizing

revenue for voyage charters, whereby the Company’s method of determining proportional performance will changefrom discharge-to-discharge to load-to-discharge. This would result in no revenue being recognized from discharge ofthe prior voyage to loading of the current voyage and all revenue being recognized from loading of the current voyageto discharge of the current voyage. In addition, the Company expects that the adoption of ASU 2014-09 may result ina change in the timing of the recognition of voyage expenses incurred during the period from discharge of the priorvoyage to loading of the current voyage. The Company’s current policy is to expense such costs as incurred, andfollowing adoption of ASU 2014-09 it is expected certain costs will be deferred and amortized over the load-to-discharge period. The Company expects that these principles will also be applied to voyage charters that are includedin revenue sharing arrangements and, consequently, a portion of the Company’s monthly net revenue allocation fromthese revenue sharing arrangements would be deferred and recognized in future months. These changes would resultin revenue and voyage expenses being recognized later than under the Company’s existing revenue and expenserecognition policies, which may cause additional volatility in revenue and earnings between periods. ASC 2014-09also changes the criteria to be used in determining whether the Company is operating as a principal or an agent in anarrangement. The Company expects that it will be considered to be the principal in certain crewing services it providesto other vessel owners and consequently the revenues earned and costs incurred will be presented on a gross basiscompared with its current net presentation. The Company is in the final stages of completing its assessment of ASU2014-09 and is focused on developing process changes, determining the transitional impact and completing otheritems required for the adoption of ASU 2014-09.”

Financial Reporting Insights – December 2017

Page 11

Shipping industryExamples of transition disclosuresPangaea ’s disclosure on most recent filing of financial statements:► “….Management has organized a working group and is currently analyzing contracts with our customers covering the

significant streams of the Company's annual revenues under the provisions of the new standard as well as changesnecessary to information technology systems, processes and internal controls to capture new data and addresschanges in financial reporting.

► While we are continuing to assess all potential impacts of the standard, the Company's preliminary expectation is thatrevenue from vessels operating on time charter will continue to be recognized under current revenue recognitionpolicies because the services being provided to its customers currently reflect the consideration to which the entityexpects to be entitled in exchange for those services, and because these arrangements qualify as single performanceobligations that meet the criteria to recognize revenue over time, as the customer is simultaneously receiving andconsuming the benefits of these services. The performance obligation in a voyage charter is also the transportationservice provided and also meets the criteria to recognize revenue over time. However, under the new standard, ourexpectation is that revenue for these voyages will be recognized over the period between load port and discharge portin contrast to the current recognition policy to recognize revenue from discharge port to discharge port. The Companyalso believes that under the new standard, it will recognize an asset from certain costs incurred to fulfill contracts thathave not begun to load if they meet the criteria outlined in this update. Such assets will be amortized pro rata over theperiod of the contract. Neither of these changes is expected to have a material impact on the consolidated financialstatements because the number of open voyages at any point in time are not a significant portion of the annual totaland the difference in revenue is expected to be only a small percentage of such voyage revenue...”

Financial Reporting Insights – December 2017

Page 12

Shipping industryExamples of transition disclosuresGenco’s disclosure on most recent filing of financial statements:► “…Management is currently analyzing contracts with our customers covering the significant streams of the Company’s

annual revenues under the provisions of the new standard as well as change necessary to information technologysystems, processes and internal controls to capture new data and address changes in financial reporting. TheCompany intends to adopt the aforementioned ASUs for the interim periods after December 31, 2017, using themodified retrospective transition method applied to those contracts which were not completed as of that date. Uponadoption, the Company will recognize the cumulative effect of adopting this guidance as an adjustment to its openingbalance of retained earnings as of January 1, 2018. Prior periods will not be retrospectively adjusted. While theassessment is still ongoing, based on the progress made to date, the Company expects that the timing of recognitionof revenue for certain ongoing charter contracts will be impacted as well as the timing of recognition of certain voyagerelated costs. The financial impact of adoption will depend on the number of spot market voyage charters and timecharter arrangements as well as their percentage of completion at January 1, 2018. The Company is also evaluatingthe presentation of revenue in its consolidated statements of operations after the adoption of ASU 2014-09.”

Financial Reporting Insights – December 2017

Page 13

Shipping industryExamples of transition disclosuresEagle Bulk ’s disclosure on most recent filing of financial statements:► “…The Company continues to make progress in its implementation and assessment of the new revenue standard.

While the assessment is still ongoing, based on the progress made to date, the Company expects that the timing ofrecognition of revenue for certain ongoing charter contracts will be impacted as well as the timing of recognition ofcertain voyage related costs. The financial impact of adoption will depend on the number of spot voyages and timecharter arrangements as well as their percentage of completion at January 1, 2018. The Company is also evaluatingthe presentation of revenue in its condensed consolidated statement of operations after the adoption of ASU 2014-09.9..”

Seacor ’s disclosure on most recent filing of financial statements:► “…. The new standard is effective for annual and interim periods beginning after December 15, 2017 and early

adoption is permitted. The Company will adopt the new standard on January 1, 2018 and expects to use the modifiedretrospective approach upon adoption. The Company is currently determining the impact, if any, the adoption of thenew accounting standard will have on its consolidated financial position, results of operations or cash flows. Principalversus agent considerations of the new standard with respect to the Company’s barge pooling arrangements mayresult in a gross presentation of operating revenues and expenses for pooled third party equipment resulting in amaterial increase in operating revenues and expenses, however operating income would remain unchanged.....”

Financial Reporting Insights – December 2017

Page 14

Shipping industryExamples of transition disclosuresShip Finance’s disclosure on most recent filing of financial statements:► “….The Company is in the process of considering the impact of the standard on its consolidated financial statements

and expects to complete the assessment during fiscal year 2017. For vessels operating on voyage charters, weexpect to continue recognizing revenue over time. The time period over which revenue will be recognized is still beingdetermined and, depending on the final conclusion, each period’s voyage results could differ materially from the sameperiod’s voyage results recognized based on the present revenue recognition guidance. However, the total voyageresults recognized over all periods would not change. The adoption of the standard is not expected to have a materialimpact on other income, primarily income earned from the commercial management of related party and third partyvessels and newbuilding supervision fees derived from related parties and third parties...”

Global Ship Lease’s disclosure on most recent filing of financial statements:► “….The adoption of this standard is not expected to have a material impact on the revenue recognized for our vessels,

as our charters qualify as operating leases and therefore are not within the scope of Topic 606. Currently we have nomaterial contracts which fall within the scope of Topic 606...”

Navigator’s disclosure on most recent filing of financial statements:► “….The Company continues to assess the potential impacts that the adoption of this guidance will have on its financial

statements and footnote disclosures, as well as the implications for the company’s internal processes, systems andcontrols. The adoption of this standard is not expected to have a material impact on the revenue recognized for ourvessels that operate on time charters. For vessels operating in the spot market, we also expect to recognize revenueover time however, the time period over which revenue is recognized is still being determined.”

Financial Reporting Insights – December 2017

Page 15

Shipping industryExamples of transition disclosuresScorpio Tanker ’s disclosure on most recent filing of financial statements:► “…The adoption of this standard is not expected to have a material impact on the revenue recognized for our vessels

that operate in pools or on time charter. These arrangements qualify as single performance obligations that meet thecriteria to recognize revenue ‘over time’ as the customer (i.e. the pool or the charterer) is simultaneously receiving andconsuming the benefits of the vessel. This method of revenue recognition is identical to our current accounting policyfor these types of employment arrangements.

► For vessels operating in the spot market, we also expect to recognize revenue over time however, the time periodover which revenue is recognized will likely change. Currently, revenue from voyage charter agreements is recognizedas voyage revenue on a pro-rata basis over the duration of the voyage on a discharge to discharge basis. In theapplication of this policy, we do not begin recognizing revenue until (i) the amount of revenue can be measuredreliably, (ii) it is probable that the economic benefits associated with the transaction will flow to the entity, (iii) thetransactions stage of completion at the balance sheet date can be measured reliably, and (iv) the costs incurred andthe costs to complete the transaction can be measured reliably. However, under IFRS 15, the performance obligationhas been identified as the transportation of cargo from one point to another. Therefore, while a decision has yet to bemade, we expect that in a spot market voyage under IFRS 15, revenue is expected to be recognized on a pro-ratabasis commencing on the date that the cargo is loaded and concluding on the date of discharge. The impact of thischange cannot be determined as it will be dependent upon the number of vessels that are operating the spot marketat the end of each period. As of the date of this report, two of our vessels are operating in the spot market and theremainder are operating in the Scorpio Group Pools or on short-term time charters...”

Financial Reporting Insights – December 2017

Page 16

1b Leases

Financial Reporting Insights – December 2017

Page 17

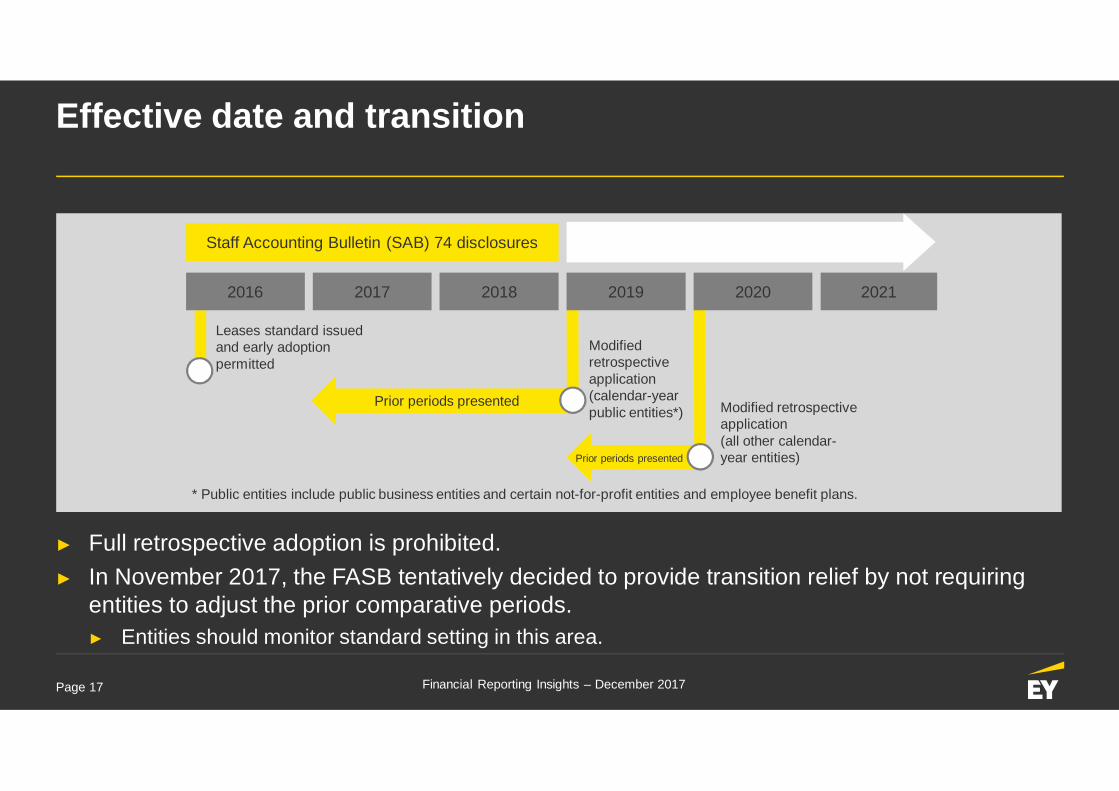

Effective date and transition

Prior periods presented

Staff Accounting Bulletin (SAB) 74 disclosures

2021201920182016

Effective

Modifiedretrospectiveapplication(calendar-yearpublic entities*)

2017

Leases standard issuedand early adoptionpermitted

Modified retrospectiveapplication(all other calendar-year entities)

2020

Prior periods presented

* Public entities include public business entities and certain not-for-profit entities and employee benefit plans.

► Full retrospective adoption is prohibited.► In November 2017, the FASB tentatively decided to provide transition relief by not requiring

entities to adjust the prior comparative periods.► Entities should monitor standard setting in this area.

Financial Reporting Insights – December 2017

Page 18

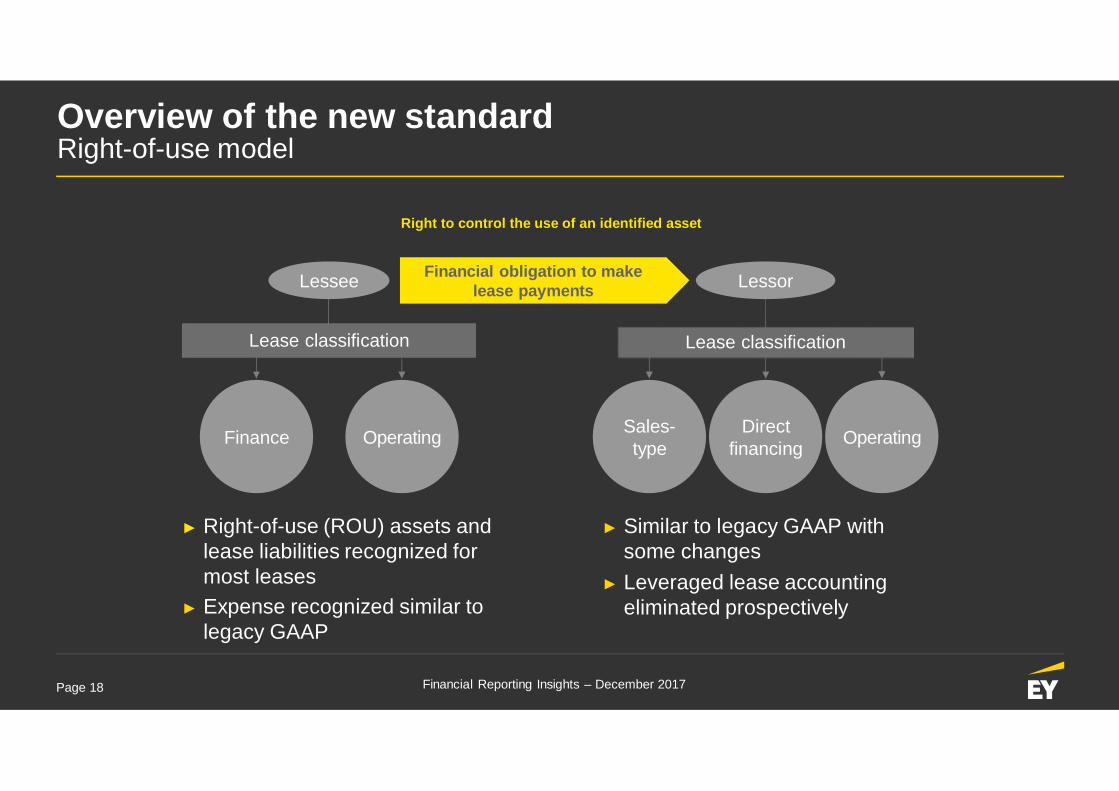

Overview of the new standardRight-of-use model

► Right-of-use (ROU) assets andlease liabilities recognized formost leases

► Expense recognized similar tolegacy GAAP

Right to control the use of an identified asset

Lessor

OperatingFinance

Financial obligation to makelease paymentsLessee

► Similar to legacy GAAP withsome changes

► Leveraged lease accountingeliminated prospectively

Directfinancing

Sales-type Operating

Lease classificationLease classification

Financial Reporting Insights – December 2017

Page 19

Overview of the new standardTransition practical expedients

► The following practical expedients can be elected by an entity in any combination:► An entity can elect to apply a package of practical expedients that allows it

not to reassess:

► An entity can make an election for all existing leases to use hindsight when determining the lease term(i.e., evaluating a lessee’s option to renew or terminate the lease or to purchase the underlying asset)and assessing impairment of ROU assets (lessees only).

► In November 2017, the FASB tentatively decided to provide a practical expedient that would permitlessors not to separate non-lease components from the related lease components if certain conditionsare met. This practical expedient could be elected by class of underlying assets, and if elected, certaindisclosures would be required.

► An entity is required to disclose which of the practical expedients it electedto apply.

Must be elected as a package and applied to all expired and existing leases

Whether contracts are orcontain leases Lease classification Whether initial direct costs

(IDCs) qualify for capitalization

Financial Reporting Insights – December 2017

Page 20

Shipping industry- Questions

► Are your shipping contracts leases? Do your shipping contracts include non-leasecomponents?

► How are shipping contracts for bareboat and time charters treated?► How are non-lease components treated by lessees? By lessors?► How are variable lease payments affected?► How should ballast voyages be treated? Is compensation or not of the ballast bonus affecting

the treatment?► How would lessees and lessors classify leases?► How would vessel sale and leaseback transactions be affected?

Financial Reporting Insights – December 2017

Page 21

2 Internal control over financial reporting

Financial Reporting Insights – December 2017

Page 22

Internal control over financial reportingOverview

► Areas of focus by the SEC and the PCAOB related to Internal Control over FinancialReporting (ICFR)

► Review Controls► Information Produced by Entity (IPE)► Implementation of new accounting standards

► Highlights on EY SOX Survey 2017

Financial Reporting Insights – December 2017

Page 23

Internal control over financial reportingRegulatory focus on Review Controls

► PCAOB inspections continue to focus on the audit of ICFR, with particular attention on reviewcontrols► ICFR audit deficiencies continue to be the most frequent inspection finding► Review controls over accounting estimates is a common area of deficiency

► SEC compliance and enforcement activities continue to focus on internal controls

“It is hard to think of an area more important than ICFR and the related assessment frameworks to our shared objective of providing high-quality financial information that investors can rely on.”

SEC Chief Accountant Wesley Bricker

Financial Reporting Insights – December 2017

Page 24

Internal control over financial reportingRegulatory Focus on Information produced by the entity

• IPE is data and reports from:• The entity’s IT applications (financial or operational)• Service organizations used by the entity

• The information provided to external specialist is IPE

Identify IPEused to perform

the reviewcontrol

Consider howthe IPE was

created

• Is the IPE in an end user computing tool (e.g., Excel or PowerPoint)?• If it is in Excel, was all information entered manually or was the original information

exported from an IT application (subject to IT general controls)?

Documentactivities that

address the riskof inappropriate

or inaccurateuser actions

• Document reviewer verification of information from an IT application, including:• Accuracy of information entered by the user to produce the report• Completeness of information transferred from an IT application to end user

computing tool• Accuracy of changes to the output information

► Management focus on IPE used in performance of review controls

Financial Reporting Insights – December 2017

Page 25

Internal control over financial reportingRegulatory focus on Review controls related to new accounting standards

► New management review controls over key implementation processes related to:► New revenue standard

► Revenue stream scoping► Contract analysis► Development of accounting polices► Estimating variable consideration► Computing transition adjustments

► Other new accounting standards, such as those on leases andcredit losses

► Internal controls over Staff Accounting Bulletin 74 transition disclosures

Financial Reporting Insights – December 2017

Page 26

Internal control over financial reporting

► Does management place unwarranted reliance on controls nor designed at a sufficient level toaddress the risks of material misstatements?

► Does management consider whether effectiveness of a controls depends on the effectivenessof other controls and are those properly assessed?

► Does management conclude on the design & operating effectiveness without sufficientevidence?

Financial Reporting Insights – December 2017

Page 27

Internal control over financial reportingHighlights on EY SOX Survey 2017

► 75% believe SOX has improved their control environmentKeys to a successful ICFR assessment:

► 70% standardizing process► 60% business recognizing the added value of having robust control environment► 45% CFO or similar involvement in the process

► 60% use outside resources to assist with SOX

► 77% view SOX as getting harder each yearICFR assessment biggest challenges:

► 66% management review controls documentation► 60% IPE testing► 45% increasing scope of auditor’s work

Financial Reporting Insights – December 2017

Page 28

Internal control over financial reportingHighlights on EY SOX Survey 2017 (continued)

► 10% consider cyber risk as part of their ICFR assessment

► Key challenges faced by ICFR function:► 57% adequacy/effectiveness of company’s resources► 53% cost vs. benefit► 47% being viewed as a compliance exercise, not as a valid added function

Financial Reporting Insights – December 2017

Page 29

3 Consolidation

Financial Reporting Insights – December 2017

Page 30

Consolidation (ASC 810)Final guidance – reminders

► Amendments to the consolidation analysis (ASU 2015-02)► Affects all entities – could change consolidation conclusions

► May trigger additional disclosures► Amends two consolidation models in ASC 810

► VIE model changes are extensive► Identification of variable interests (fees paid to a decision maker or service provider)► VIE characteristics for a limited partnership or similar entity► Primary beneficiary determination

► Voting model► Eliminates presumption that general partner consolidates► More partnerships may be VIEs

Financial Reporting Insights – December 2017

Page 31

Consolidation (ASC 810)Final accounting guidance

► Interests held through related parties that are under common control (ASU2016-17)

► Changes the variable interest entity (VIE) model for determining the primary beneficiary whenindirect interests are held by related parties under common control

► Single decision maker will consider its indirect interests held by related parties under commoncontrol on proportionate basis

Financial Reporting Insights – December 2017

Page 32

Consolidation (ASC 810)FASB developments

► Proposed accounting standards update: Targeted improvements to relatedparty guidance for variable interest entities

► Private company accounting alternative – Would allow entities that are not public businessentities to make an accounting policy election to not apply the VIE guidance for certaincommon control arrangements

► Decision-making fees – Would reduce the chances of a decision maker concluding that itsfees are a variable interest by requiring indirect interests held through related parties undercommon control to be considered on a proportionate basis

Financial Reporting Insights – December 2017

Page 33

Consolidation (ASC 810)FASB developments (continued)

Proposed accounting standards update: Targeted improvements to related party guidance forvariable interest entities (continued)► VIE related party guidance – Would eliminate today’s “most closely associated” test and

require entities to consider a new set of factors to determine which party in a related partygroup, if any, should consolidate a VIE► Consolidation by the common control parent entity would be required regardless of whether the other

parties in the related party group consolidate the VIE► Comments phase completed on 5 September 2017Consolidation reorganization and targeted improvements (project)► Initiative to reorganize the guidance and clarify certain complex terms and concepts in ASC

810

Financial Reporting Insights – December 2017

Page 34

4 Credit losses

Financial Reporting Insights – December 2017

Page 35

Credit losses (ASU 2016-13)Overview

► The new Current Expected Credit Loss (CECL)model may accelerate the recognition of creditlosses and increase earnings volatility

► Entities will be required to disclose significantlymore information

► Today’s concept of other-than-temporaryimpairment (OTTI) for AFS debt securities will beeliminated and replaced

► Implementation has begun, led by banks► Entities will be required to use more judgment and

will likely need to gather and retain additional dataand enhance modeling capabilities

CECL objective: Recognize allowance reflecting all contractual cash flows notexpected to be collected

Allowance forcredit losses

No incurredthreshold

Risk of loss, evenif that risk is

remote

Time value ofmoney

Historical lifetimeloss data (e.g.,

vintage)

Information aboutcurrent conditions

Reasonable andsupportable

forecasts

Alle

ntiti

es

Current expected credit loss (CECL) model

► Financial assets measured at amortized cost:► Trade receivables, reinsurance receivables, loans, held-to-maturity (HTM)

debt securities, reverse repos► Net investment in leases recognized by a lessor► Off-balance-sheet credit exposures not accounted for

as insurance

AFS debt security impairment model

► Available-for-sale (AFS) debt securities

Model for certain beneficial interests classified as HTM or AFS that arenot of high credit quality

Financial Reporting Insights – December 2017

Page 36

Credit losses (ASU 2016-13)Current expected credit loss model – overview

ObjectiveRecognize an allowance for credit losses that results in the financial statements reflecting the net amountexpected to be collected from the financial asset

Core concepts

Based onan asset’s

amortized cost

Reflect lossesover an asset’scontractual life

Reflect therisk of loss

Consider availablerelevant information

Amortized cost basisincludes premiums or

discounts, foreignexchange and fair value

hedge adjustments

Contractual life will beadjusted for prepayments,

but not extensions,unless a troubled debtrestructuring (TDR) isreasonably expected

The standard requires apool-based approach

when similar riskcharacteristics exist, andentities should consider

the risk of loss even whenthat risk is remote

Entities will considerinformation about past

events, current conditionsand forecasts about the

future that are reasonableand supportable

Financial Reporting Insights – December 2017

Page 37

Credit losses (ASU 2016-13)Current expected credit loss model – illustration 1

Summarized from example 5 in ASU 2016-13► Company A manufactures and sells products to a broad range of customers and provides

customers with payment terms of 90 days► Management observes that unemployment has decreased as of the report date and believes

this will result in lower loss rates. It estimates its allowance for credit losses as follows:

Past-due statusAmortized cost

basisHistorical

credit-loss rateExpected credit-loss

rate*

Allowancefor expected credit

lossesCurrent $5,984,698 0.30% 0.27% $16,159

1–30 days past due 8,272 8.00% 7.20% 59631–60 days past due 2,882 26.00% 23.40% 675

61–90 days past due 842 58.00% 52.20% 440

Over 90 days past due 1,100 82.00% 73.80% 812Total $5,997,794 $18,682

Financial Reporting Insights – December 2017

*Historical loss rate adjusted downward by 10% due to expected improvement in unemployment.

Page 38

4 Financial reporting guidance 2017 & upcoming 2018+

Financial Reporting Insights – December 2017

Page 39

Effective in 2017 for public calendar year-end entities

ASU Year

1 ASU 2015-11 Inventory (Topic 330), Simplifying the Measurement of Inventory 2017

2 ASU 2015-17 Income Taxes (Topic 740), Balance Sheet Classification of Deferred Taxes 2017

3 ASU 2016-05 Derivatives and Hedging (Topic 815), Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships 2017

4 ASU 2016-06 Derivatives and Hedging (Topic 815), Contingent Put and Call Options in Debt Instruments 2017

5 ASU 2016-07 Investments - Equity Method and Joint Ventures (Topic 323), Simplifying the Transition to the Equity Method of Accounting 2017

6 ASU 2016-09 Compensation - Stock Compensation (Topic 718), Improvements to Employee Share-Based Payment Accounting 2017

7 ASU 2016-17 Consolidation (Topic 810): Interests Held through Related Parties That Are under Common Control 2017

8 ASU 2016-19 Technical Corrections and Improvements 2017

9 ASU 2017-02 Not-for-Profit Entities — Consolidation (Subtopic 958-810), Clarifying When a Not-for-Profit Entity That Is a General Partner or aLimited Partner Should Consolidate a For-Profit Limited Partnership or Similar Entity

2017

10 ASU 2017-03 Accounting Changes and Error Corrections (Topic 250) and Investments — Equity Method and Joint Ventures (Topic 323),Amendments to SEC Paragraphs Pursuant to Staff Announcements at the September 22, 2016 and November 17, 2016 EITFMeetings (SEC Update)

2017

Financial Reporting Insights – December 2017

Page 40

Effective after 2017 for public calendar year-end entities –Revenue & Leases only

ASU Year

1 ASU 2014-09 Revenue from Contracts with Customers (Topic 606) 2018

2 ASU 2016-08 Revenue from Contracts with Customers (Topic 606), Principal versus Agent Considerations (Reporting Revenue Gross versusNet)

2018

3 ASU 2016-10 Revenue from Contracts with Customers (Topic 606), Identifying Performance Obligations and Licensing 2018

4 ASU 2016-12 Revenue from Contracts with Customers (Topic 606), Narrow-Scope Improvements and Practical Expedients 2018

5 ASU 2016-20 Technical Corrections and Improvements to Topic 606, Revenue from Contracts with Customers 2018

6 ASU 2017-05 Other Income — Gains and Losses from the Derecognition of Nonfinancial Assets (Subtopic 610-20), Clarifying the Scope ofAsset Derecognition Guidance and Accounting for Partial Sales of Nonfinancial Assets

2018

7 ASU 2017-10 Service Concession Arrangements (Topic 853), Determining the Customer of the Operation Services 2018

8 ASU 2017-13 Revenue Recognition (Topic 605), Revenue from Contracts with Customers (Topic 606), Leases (Topic 840), and Leases (Topic842)

2018

9 ASU 2016-02 Leases (Topic 842) 2019

Financial Reporting Insights – December 2017

Page 41

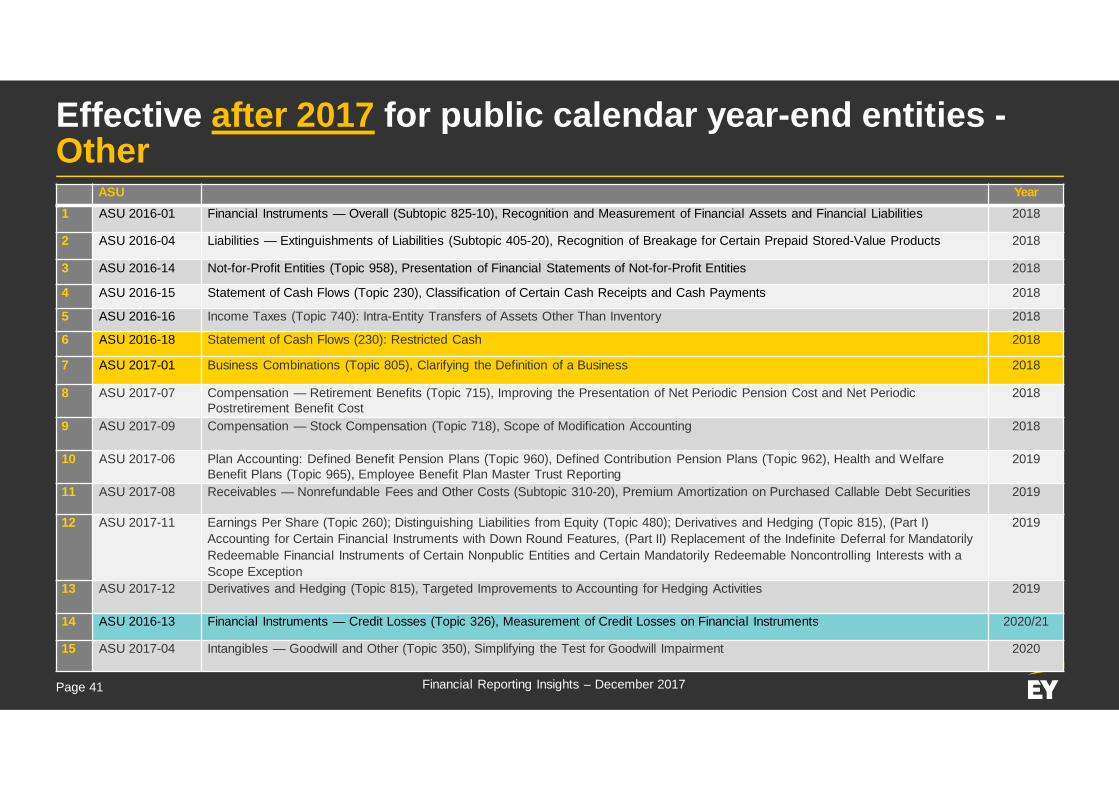

Effective after 2017 for public calendar year-end entities -Other

ASU Year

1 ASU 2016-01 Financial Instruments — Overall (Subtopic 825-10), Recognition and Measurement of Financial Assets and Financial Liabilities 2018

2 ASU 2016-04 Liabilities — Extinguishments of Liabilities (Subtopic 405-20), Recognition of Breakage for Certain Prepaid Stored-Value Products 2018

3 ASU 2016-14 Not-for-Profit Entities (Topic 958), Presentation of Financial Statements of Not-for-Profit Entities 2018

4 ASU 2016-15 Statement of Cash Flows (Topic 230), Classification of Certain Cash Receipts and Cash Payments 2018

5 ASU 2016-16 Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory 2018

6 ASU 2016-18 Statement of Cash Flows (230): Restricted Cash 2018

7 ASU 2017-01 Business Combinations (Topic 805), Clarifying the Definition of a Business 2018

8 ASU 2017-07 Compensation — Retirement Benefits (Topic 715), Improving the Presentation of Net Periodic Pension Cost and Net PeriodicPostretirement Benefit Cost

2018

9 ASU 2017-09 Compensation — Stock Compensation (Topic 718), Scope of Modification Accounting 2018

10 ASU 2017-06 Plan Accounting: Defined Benefit Pension Plans (Topic 960), Defined Contribution Pension Plans (Topic 962), Health and WelfareBenefit Plans (Topic 965), Employee Benefit Plan Master Trust Reporting

2019

11 ASU 2017-08 Receivables — Nonrefundable Fees and Other Costs (Subtopic 310-20), Premium Amortization on Purchased Callable Debt Securities 2019

12 ASU 2017-11 Earnings Per Share (Topic 260); Distinguishing Liabilities from Equity (Topic 480); Derivatives and Hedging (Topic 815), (Part I)Accounting for Certain Financial Instruments with Down Round Features, (Part II) Replacement of the Indefinite Deferral for MandatorilyRedeemable Financial Instruments of Certain Nonpublic Entities and Certain Mandatorily Redeemable Noncontrolling Interests with aScope Exception

2019

13 ASU 2017-12 Derivatives and Hedging (Topic 815), Targeted Improvements to Accounting for Hedging Activities 2019

14 ASU 2016-13 Financial Instruments — Credit Losses (Topic 326), Measurement of Credit Losses on Financial Instruments 2020/21

15 ASU 2017-04 Intangibles — Goodwill and Other (Topic 350), Simplifying the Test for Goodwill Impairment 2020

Financial Reporting Insights – December 2017

Page 42

Statement of cash flowsPresentation of restricted cash (ASU 2016-18)

► Entities will be required to:► Show the changes in the total of cash, cash equivalents, restricted cash and restricted cash

equivalents in the statement of cash flows► Entities will no longer present transfers between cash and cash equivalents and restricted cash and restricted

cash equivalents in the statement of cash flows► Reconcile the total of cash, cash equivalents, restricted cash and restricted cash equivalents on the

statement of cash flows to amounts on the balance sheet► Disclose the nature of their restricted cash and restricted cash equivalents balances

► Effective for PBEs in annual periods beginning after 15 December 2017 andinterim periods therein► For other entities, effective for annual periods beginning after 15 December 2018 and interim periods

within annual periods beginning after 15 December 2019► Early adoption is allowed

Financial Reporting Insights – December 2017

Page 43

Clarifying the definition of a business (ASU 2017-01)

► Intended to assist entities with evaluating whether a set of transferred assets and activities is abusiness► Will likely result in more acquisitions being accounted for as asset acquisitions rather than business

combinations► Entities must first apply the “substantially all” threshold

► A set is not a business when substantially all of the fair value of gross assets acquired is concentratedin a single asset or group of similar assets

► If the threshold is not met, the set must include an input and a substantive process thattogether significantly contribute to the ability to create outputs to be a business► Eliminates presumption that a set is a business when generating outputs► Provides criteria to determine whether sets with outputs and sets without outputs include a

substantive process► There is a higher standard for sets without outputs

Financial Reporting Insights – December 2017

Page 44

Clarifying the definition of a business (ASU 2017-01)(continued)

Current GAAP ASU 2017-01

Outputs defined broadly as the ability to provide return Outputs defined more narrowly to align with new revenuerecognition guidance

Evaluation of whether a market participant could replaceany missing elements is performed

Evaluation is focused on elements within the set; ASU doesnot change evaluation from a market participant perspective

If goodwill exists, the set is presumed to be a business Eliminates presumption, but goodwill may be an indicator of asubstantive process

► Effective for public business entities (PBEs) for fiscal years beginning after 15 December 2017,and interim periods therein► For all other entities, effective for fiscal years beginning after 15 December 2018, and interim periods

within fiscal years beginning after 15 December 2019► Applied prospectively► Early adoption is permitted

Financial Reporting Insights – December 2017

Page 45

Sale of nonfinancial assets – ASC 610-20 (ASU 2017-05)

The amendments in this ASU clarify questions on how entities account for the derecognition of anonfinancial asset or an in substance nonfinancial asset (ISNFA) that is not a business tocounterparties that are not customers.

Definition of a customer► ASC 606 defines a customer as “a party that has contracted with an entity to obtain goods or

services that are an output of the entity’s ordinary activities in exchange for consideration.”

Example► Company A enters into a contract to sell an entity that contains nonfinancial assets (i.e., real estate and the related

operating leases) and financial assets (i.e., lease receivables). The counterparty is not a customer, and the assetstransferred do not meet the definition of a business under ASU 2017-01. Further, substantially all of the fair value ofthe assets promised in the contract is concentrated in the real estate and the operating lease. As a result, the leasereceivables are ISNFA and all of the assets promised in the contract are in the scope of ASC 610-20.

Financial Reporting Insights – December 2017

Page 46

Sale of nonfinancial assets – ASC 610-20 (ASU 2017-05) (continued)

Apply ASC 606.Counterparty a customer?

Apply ASC 810.Business or nonprofit activity?

Apply ASC 610-20.Nonfinancial assets (and in substancenonfinancial assets)?

Apply ASC 610-20 to subsidiaries withnonfinancial assets or in substance

nonfinancial assets. Apply other guidance toremaining subsidiaries/parts.Separate parts and apply relevant US GAAP.

Transferring ownership interestin subsidiary?

Apply other GAAP.Scope of other guidance?No

No

No

No

Yes

Yes

Yes

Yes

Yes

No

Financial Reporting Insights – December 2017

Page 47

5 FASB developments

Financial Reporting Insights – December 2017

Page 48

Simplifying the balance sheet classification of debt

► Proposal would replace current rules-based guidance with a principle for classifying debt ascurrent or noncurrent► Would apply to all “debt arrangements” including convertible debt and mandatorily redeemable

financial instruments classified as liabilities► Debt would be classified as noncurrent when either:

► Liability is contractually due to be settled more than one year (or operating cycle, if longer) afterbalance sheet date

► Entity has a contractual right to defer settlement for at least one year(or operating cycle, if longer) after balance sheet date

► Emphasis would be on rights that exist as of balance sheet date► Exception for certain waivers of debt covenant violations

► Effective dates not yet determined

Financial Reporting Insights – December 2017

Page 49

Disclosure framework

► Objective is to improve the effectiveness of disclosures by clearly communicating theinformation that is most important to users

► Focus on effective disclosures, which may result in the reduction of require disclosures► Separated in two components: Board’s & Entity’s decision process► Topic-specific disclosure reviews

► Income taxes► Defined benefit plans► Fair value measurement► Inventory

► Evaluation of interim reporting requirements – more research needed► Important to understand entire suite of proposals and how they interact

Financial Reporting Insights – December 2017

Page 50

Other proposals and projects

► Technical corrections and improvements► Two proposals issued in June 2017 to supersede outdated guidance

► Collaborative arrangements► Objective is to make targeted improvements to clarify when transactions between participants in a

collaborative arrangement, as defined in ASC 808, should be accounted for as revenue transactions

► Improving the accounting for asset acquisitions and business combinations (phase 3 of thedefinition of a business project)► Objective is to address differences between the accounting for acquisitions of assets and of

businesses► Customer’s accounting for implementation, setup, and other upfront costs (implementation

costs) incurred in a cloud computing arrangement that is considered a service contract (EITFIssue 17-A)► FASB staff to perform additional research on potential accounting models

► Disclosures by business entities about government assistance

Financial Reporting Insights – December 2017

Thank you!

4th Annual Financial Reporting InsightsAthens, 13 December 2017

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services.The insights and quality services we deliver help build trust and confidencein the capital markets and in economies the world over. We developoutstanding leaders who team to deliver on our promises to all of ourstakeholders. In so doing, we play a critical role in building a better workingworld for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of themember firms of Ernst & Young Global Limited, each of which is a separatelegal entity. Ernst & Young Global Limited, a UK company limited byguarantee, does not provide services to clients. For more information aboutour organization, please visit ey.com.

About EY’s Assurance ServicesOur assurance services help our clients meet their reporting requirements byproviding an objective and independent examination of the financialstatements that are provided to investors and other stakeholders.Throughout the audit process, our teams provide a timely and constructivechallenge to management on accounting and reporting matters and a robustand clear perspective to audit committees charged with oversight. Thequality of our audits starts with our 60,000 assurance professionals, whohave the breadth of experience and ongoing professional development thatcome from auditing many of the world’s leading companies. For every client,we assemble the right multidisciplinary team with the sector knowledge andsubject matter knowledge to address your specific issues. All teams use ourGlobal Audit Methodology and latest audit tools to deliver consistent auditsworldwide.

© 2015 EYAll Rights Reserved.