Braskem day basics petrochemicals unit presentation - manoel carnaúba

36

Basic Petrochemicals Unit Manoel Carnaúba

-

Upload

braskemri -

Category

Technology

-

view

752 -

download

10

description

Transcript of Braskem day basics petrochemicals unit presentation - manoel carnaúba

Basic Petrochemicals UnitManoel Carnaúba

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

2

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

3

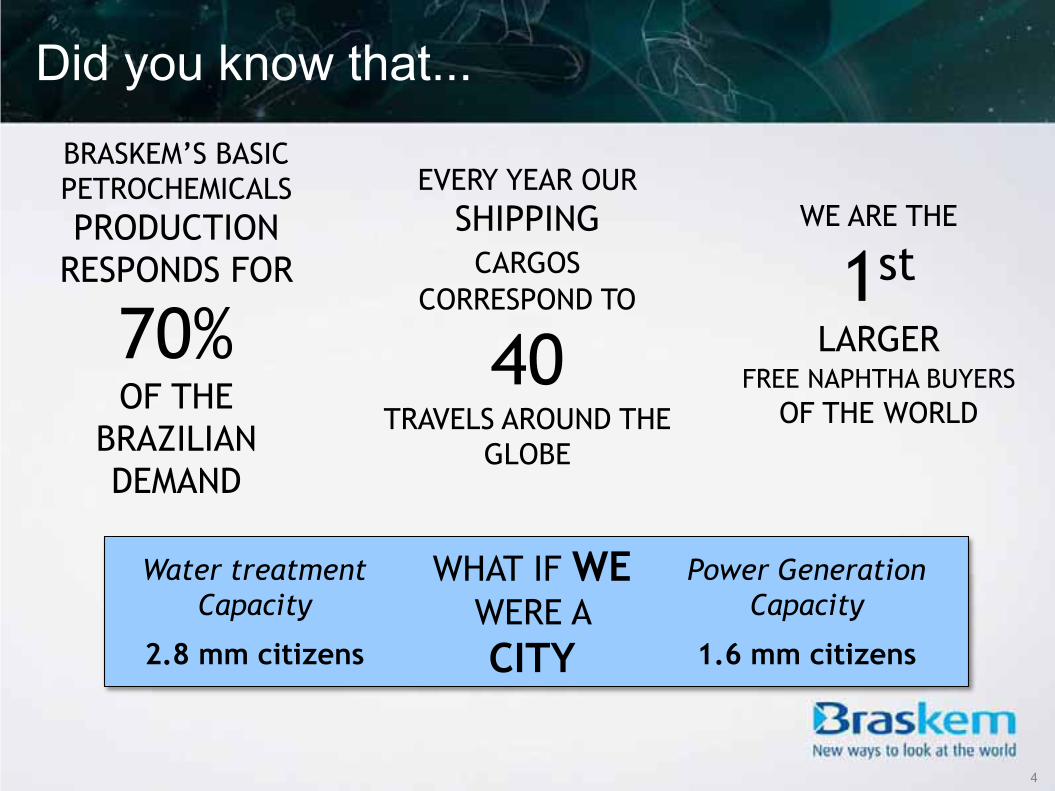

Did you know that...

BRASKEM’S BASIC PETROCHEMICALS PRODUCTION

RESPONDS FOR

70%OF THE

BRAZILIANDEMAND

EVERY YEAR OUR SHIPPING

CARGOSCORRESPOND TO

40TRAVELS AROUND THE

GLOBE

WE ARE THE

1st

LARGER FREE NAPHTHA BUYERS

OF THE WORLD

Water treatment Capacity

2.8 mm citizens

WHAT IF WEWERE A CITY

Power Generation Capacity

1.6 mm citizens

4

Main priorities

� Be a world reference in HSE, Sustainability and Social Responsibility;

� Develop opportunities with clients to ensure operation at full capacity;

� Implement actions to optimize costs and be a world reference in our segment, with focus on reducing physical losses and energy consumption at industrial plants;

� Ensuring Energy Efficiency and competitive sources for acquisition;

� Develop leaders to meet growth projects, acquisitions and international challenges, identifying and preparing new generations for Greenfields projects.

5

Vice-President

Manoel Carnaúba

CEO

Bernardo Gradin

Industrial - RS

Ademir Zaparoli

Supply Chain

Hardi Schuck

Human Resources

Andrea Jucá

New Business Development

Renato Costa

Controlling and Planning

Vinícius Patel

Energy

Andre Gohn

Commercial

Isabel Figueiredo

Industrial - BA

José Kelso Moraes

Structure

6

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

7

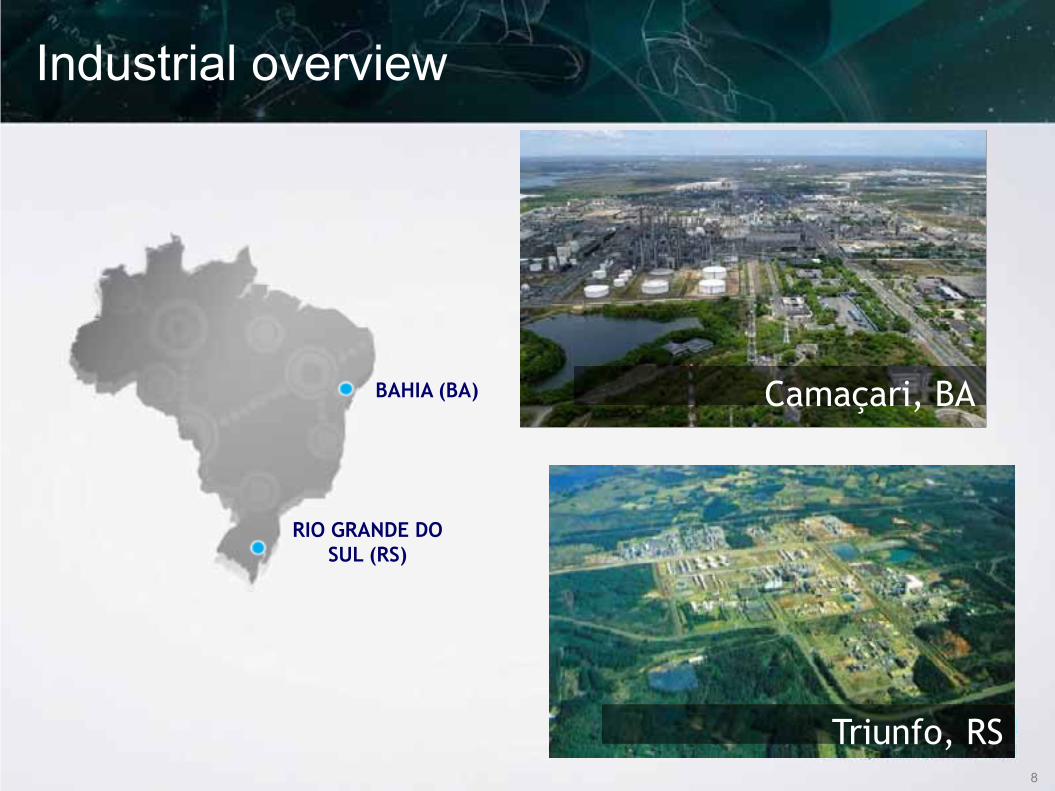

RIO GRANDE DO SUL (RS)

BAHIA (BA) Camaçari, BA

Triunfo, RS

Industrial overview

8

FORDMONSANTO

QUATTORDOW TDI

BRASKEM - BASIC PETROCHEMICALS

PE-3

COPENOR

PE-1

P. FAFEN

ABB

DETENCPLPETPE-2 PVC

OXITENO

ACRINORCHLOR ALKALI

ELEKEIROZ

DUPONT

EMCAKORDSA

BASF

CONTINENTAL

BRASKEM - BASIC PETROCHEMICALS

BRASKEM

9

Industrial Overview – State of Bahia (BA)

9

Liquid and Gas Terminal

Aratu Terminal (BA):� petrochemical exports and feedstock imports

Industrial Overview – State of Bahia (BA)

ARATU TERMINALULTRACARGO

LIQUIDS

Tanks 85

Storage capacity 192.600 m3

GASES

Tanks 8

Storage capacity 44.600 m3

10

Camaçari, BA

Triunfo, RS

RIO GRANDE DO SUL (RS)

BAHIA (BA)

Industrial overview

11

PP-2 / PE-5PP-1 DSM

OXITENOINNOVA

PE-4

PE-6

LANXESS

BRASKEM - BASIC PETROCHEMICALS

BRASKEM - BASIC PETROCHEMICALS

BRASKEM

12

Industrial Overview – State of Rio Grande do Sul (RS)

12

Santa Clara Terminal

Privately-owned terminal

extending for 4.6 miles,

with 3 petrochemical docks

and 2 ethanol tanks

Industrial Overview – State of Rio Grande do Sul (RS)

13

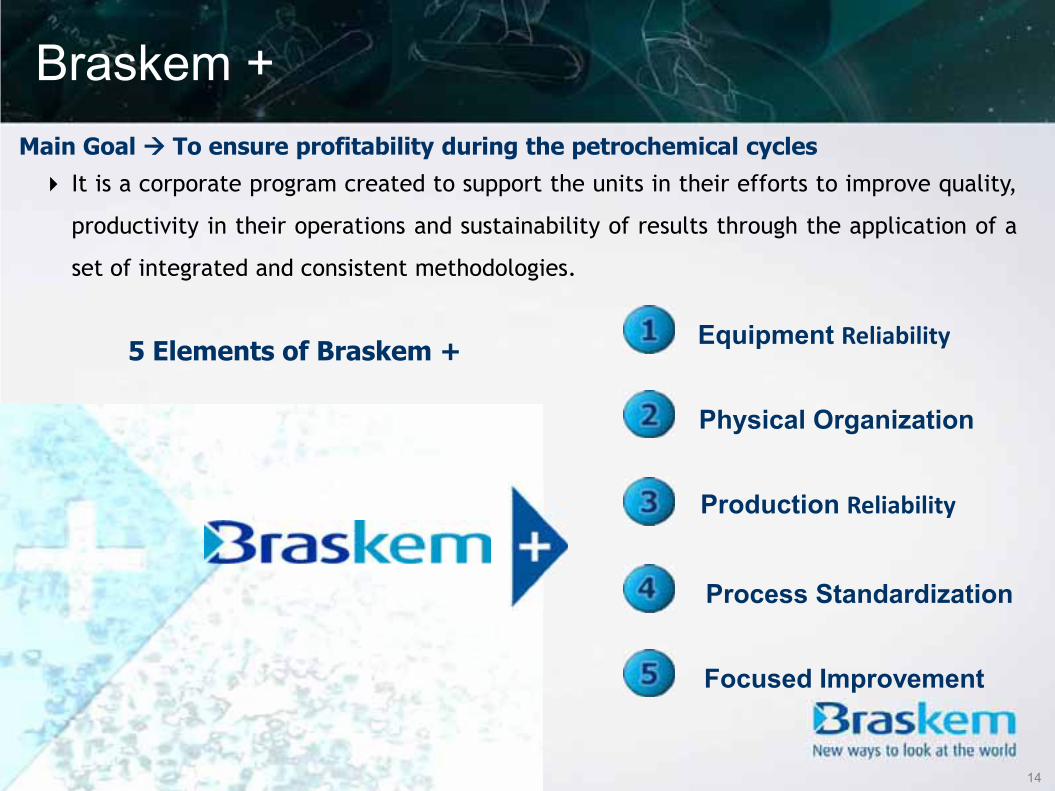

� It is a corporate program created to support the units in their efforts to improve quality,

productivity in their operations and sustainability of results through the application of a

set of integrated and consistent methodologies.

Main Goal �� To ensure profitability during the petrochemical cycles

5 Elements of Braskem + Equipment Reliability

Physical Organization

Production Reliability

Process Standardization

Focused Improvement

Braskem +

14

� The Six Sigma culture is present in the Basic Petrochemicals Unit spread in several areas,

mostly located in operational areas, where are the greatest opportunities for gains in

safety, environmental improvements and economic return.

Six Sigma �� One of the tools used in Braskem +

Braskem + Lean Six Sigma

* Cumulative value until May/10

15

Gains of Six Sigma (US$ MM)

21.15.29.6

21.1 23.6

30.0

2006 2007 2008 2009 2010

*

Participants Define Content

1

Design Data Structure

2

Verification, Analysis,Generation

of Results

4

D

Results / Presentation

5

Presentation

Data Collection & Transfer

3

& Transfe

Evaluation of Indicators (KPIs)

1

Gaps Capture Plan

Periodicity: Each 2 years

BenchmarkingResearch

� We use Benchmark Solomon for Olefins andUtilities

� We use Phillip Towsend (PTAI) for Aromatics

Process benchmarking

16

Benchmarking Analysis

INDEXES ANALYSIS2009

HPPBA1 BA2 RS1 RS2

Operation Rate - Olefins (%) 84.3 93.9 87.6 94.7 98.9

Energy Consumption (BTU/lb_HVC) 6454 5992 5556 4762 5360

Maintenance Effectiveness (%RVA) 4.11 2.87 3.65 2.43 1.8

Maintenance Reliability Index (%) 4.37 2.75 4.27 3.05 2.50

Physical Losses (%) 1.11 0.65 0.81 0.65 0.45

Yield of pyrolysis - Chemicals YIR (%) 105.4 104.9 106.7 100.7 99.1

Chemicals Production Cost (US$/t) 775.4 726.8 808.0 680.0 690.0

-500

50100150200250

0 5 10 15 20 25 30 35 40 45 50

US$/

t_HV

C

Nº DE PARTICIPANTES - BASE NAFTA

Série1 BA1 BA2 RS1 RS2

1º Quarter

2º Quarter

3º Quarter

4º Quarter

* Indexes related to naphta feedstocks group

-505

1015202530

0 5 10 15 20 25 30 35 40 45 50

%VR

Nº DE PARTICIPANTES - BASE NAFTA

Série1 BA1 BA2 RS1 RS2

Olefins Net Margin (US$/t_HVC)

Olefins Profitability (% RVA)

Process benchmarking

17

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

18

Ethylene – Clients and markets

19

UTILITIESAROMATICSOLEFINS

Polyethylenes Vinyls Ethylene Oxide Styrenes

Braskem Braskem PVC (AL and BA)Braskem DCE (AL)

Oxiteno (BA)Oxiteno (RS)

Unigel (BA)Innova (RS)

BagsYogurt packagingFilms for agriculture

PVC: Pipes and fittings PVC: ToysVAM: Paint PVA

Yarn and PolyesterPETCosmetics

PS: disposablesPS: appliancesEPS: Expanded polystyrene

ETHYLENE

Annual Production Capacity: 2,532,000 t

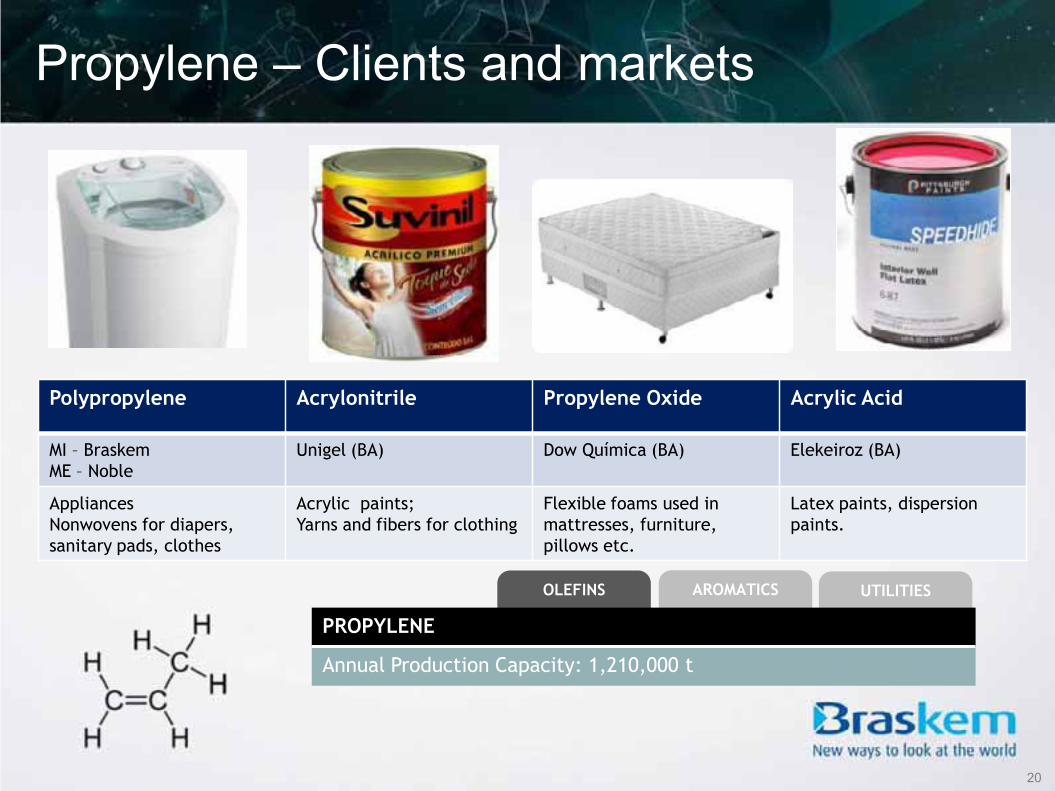

Propylene – Clients and markets

20

Polypropylene Acrylonitrile Propylene Oxide Acrylic Acid

MI – BraskemME – Noble

Unigel (BA) Dow Química (BA) Elekeiroz (BA)

AppliancesNonwovens for diapers, sanitary pads, clothes

Acrylic paints;Yarns and fibers for clothing

Flexible foams used in mattresses, furniture, pillows etc.

Latex paints, dispersion paints.

UTILITIESAROMATICSOLEFINS

PROPYLENE

Annual Production Capacity: 1,210,000 t

Butadiene – Clients and markets

21

Polybutadiene SBRStyrene Butadiene Rubber

SSBRSolution SBR

NBRAcrylonitrile Butadiene Rubber

TR (TPR)Thermoplastic Rubber

Lanxess Lanxess Lanxess Lanxess Lanxess

TiresShoes Treadmills

TiresShoesTreadmills

Tires (high performance)Ring, seals and hoses

Aircraft material, fuel hoses, medical gloves

Flip-flopsShoes,Artefacts

BUTADIENE

Annual Production Capacity: 286,000 t

Benzene – Clients and markets

UTILITIESAROMATICSOLEFINS

Styrenes LABLinear Alkyl Benzene

Unigel (BA)Innova (RS)

Deten (BA)

PS: disposablesPS: appliancesEPS: expanded polystyrene

Household detergents Industrial detergents Soap powder

BENZENE

Annual Production Capacity: 714,000 t

22

Toluene – Clients and markets

23

UTILITIESAROMATICSOLEFINS

Solvents TDIToluene di-isocyanate

AB9

Retail Market DOW (BA) Retail Market

Paints and varnish Thinners, turpentineAdhesives

Flexible foam (upholstery) Rigid foams (Bumpers and sandals)

Agrochemicals

TOLUENE

Annual Production Capacity: 135,000 t

Gasoline + ETBE – Clients and markets

24

VEHICLE GASOLINE

Annual Production Capacity: 731,000 t

ETBE

Annual Production Capacity: 372,000 t

GASOLINE ADDITIVE

Export

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

25

Source: Tecnon Parpinelli

0,2 0,02,0

4,1

-1,0 -1,7

3,4

-8,2

-1,7 -1,9-1,0

1,0

-10

-8

-6

-4

-2

0

2

4

6

8

10

-20

-15

-10

-5

0

5

10

15

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2015 2020

US$

/bbl

MM

t

World Surplus (Deficit) Crack spread

� Global naphtha balance points to oversupply in the following years

� Naphtha crack spread will remain negative

� Naphtha petrochemical demand in the U.S. will decrease as a consequence of low-cost ethane

� Ethane will increase its share of the U.S. feedstock slate

� U.S. government regulations call for more ethanol in gasoline (bearish factor fornaphtha demand)

� In Brazil, increasing ethanol demand and new Petrobras refineries will ensure naphthasupply.

Naphtha market forecast

26

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

27

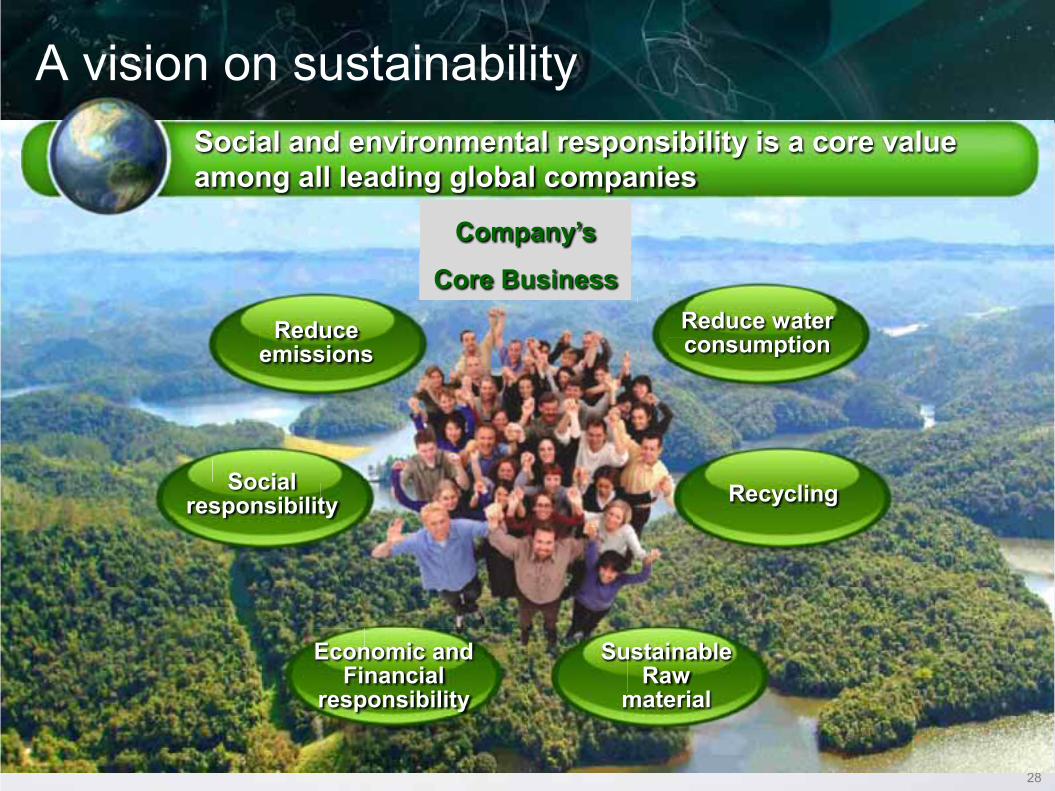

A vision on sustainability

28

Social and environmental responsibility is a core value among all leading global companies

Recycling

Reduce water consumptionReduce

emissions

Social responsibility

Economic and Financial

responsibility

Company’s

Core Business

Sustainable Raw

material

Sugar Cane Brazil

Sugar cane, Brazil and Braskem – a unique combination

29

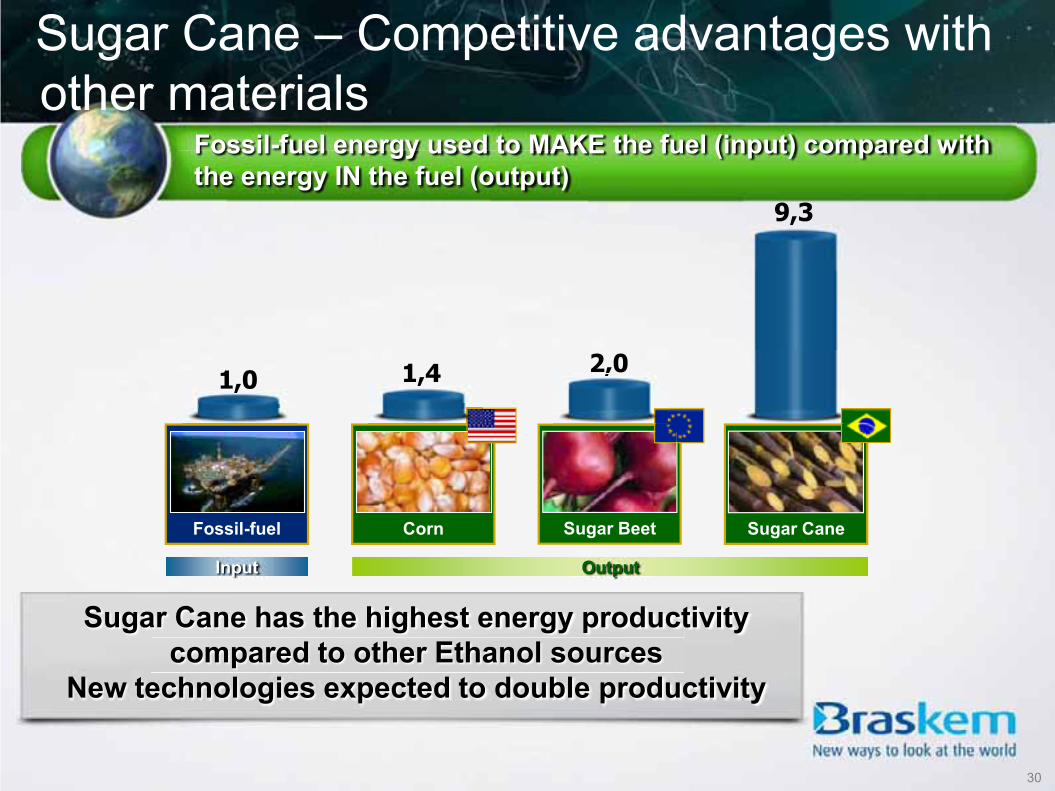

Fossil-fuel energy used to MAKE the fuel (input) compared with the energy IN the fuel (output)

Sugar Cane has the highest energy productivity compared to other Ethanol sources

New technologies expected to double productivity

1,4 2,0

9,3

1,0

Corn Sugar Beet Sugar CaneFossil-fuel

, , ,

,

Input Output

Sugar Cane – Competitive advantages with other materials

30

Overview of the Ethanol MarketFundamentals and balance� Growth in domestic demand

� Flex-fuel vehicles may account for 50% of the Brazilian vehicle fleet by 2011

� Expansion of ethanol use in the chemical industry

� Sugarcane industry is facing a consolidation process, mainly through foreign capital

� Production is exceptionally dependent on weather conditions

� Ethanol availability is connected to sugar profitability

� Environmental legislation worldwide is a driver for increasing global ethanol consumption.

Source: ANP and UNICA31

0

5

10

15

20

01020304050607080

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

MM

de

m³

MM

de

m³

Brazilian balance

0

5

10

15

20

01020304050607080

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

MM

de

m³

MM

de

m³

Brazilian balance

Production Total consumption Surplus (right axis)Production Total consumption Surplus (right axis)

Market share of the five biggest groups of producers

% of the mills with external capital holdings

27%12%

2004/05 2009/10

2007/08 2010/11e

7% 22%

Market share of the five biggest groups of producers

% of the mills with external capital holdings

2004/05004/05 2009/10009/10

2007/08 2010/11e010/11et

� Growth in domestic demand

• Flex-fuel vehicles may account for 50% of the Brazilian vehicle fleet by 2011

• Expansion of ethanol use in the chemical industry

� Sugarcane industry is facing a consolidation process, mainly through foreign capital

� Production is exceptionally dependent on weather conditions

� Ethanol availability is connected to sugar profitability

� Environmental legislation worldwide is a driver for increasing global ethanolconsumption.

Source: Itaú BBA and UNICA

Overview of the Ethanol MarketFundamentals and balance

32

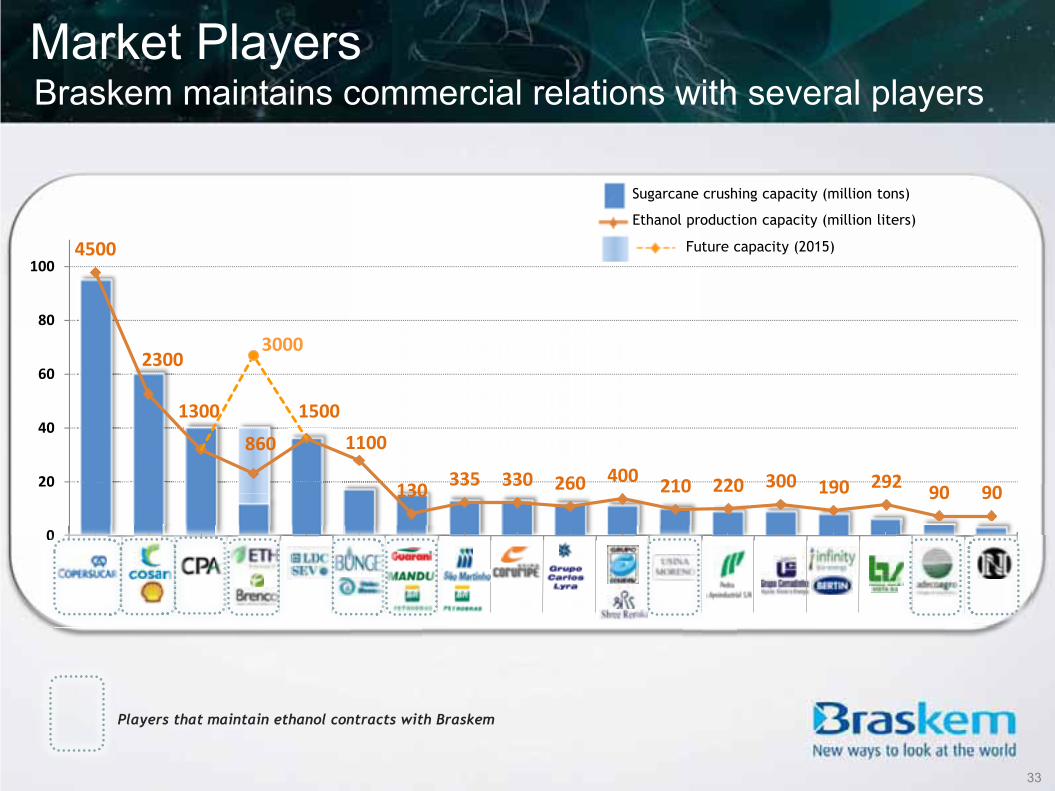

0

20

40

60

80

1004500

2300

1300

860

15001100

130 335 330 260 400 210 220 300 190 292 90 90

3000

Sugarcane crushing capacity (million tons)

Ethanol production capacity (million liters)

Future capacity (2015)

Market PlayersBraskem maintains commercial relations with several players

0000000000000

Players that maintain ethanol contracts with Braskem

33

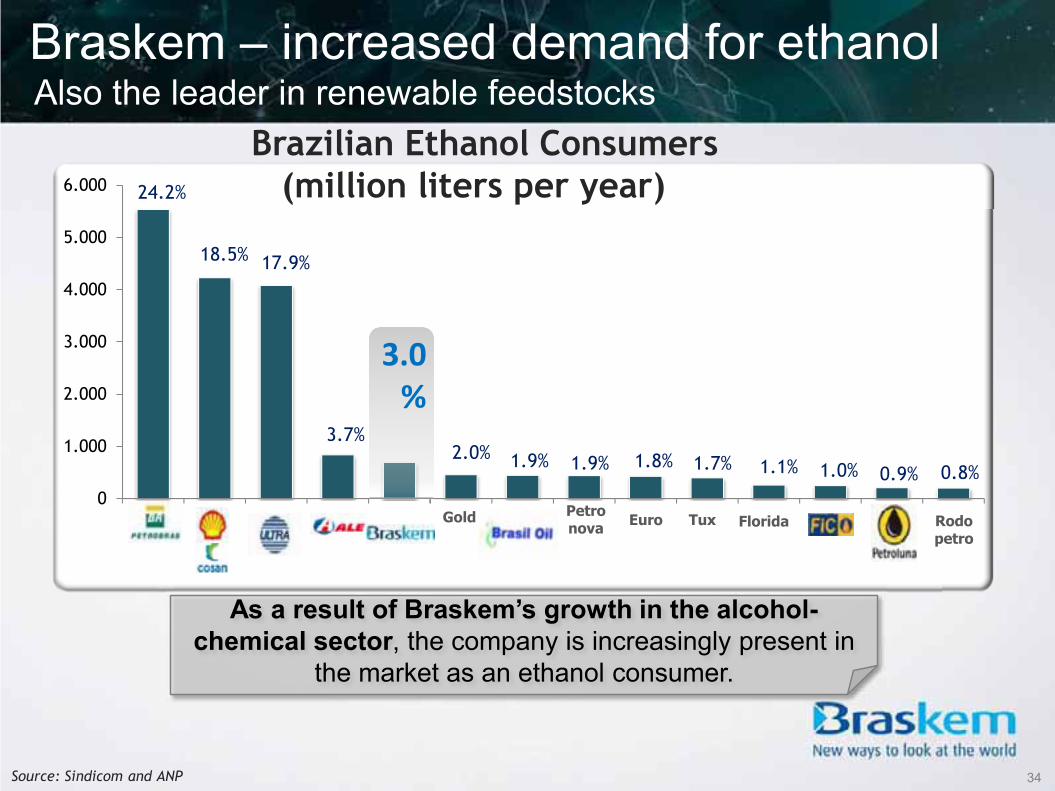

Braskem – increased demand for ethanolAlso the leader in renewable feedstocks

Source: Sindicom and ANP

0

1.000

2.000

3.000

4.000

5.000

6.000

Gold Euro Tux Florida Rodopetro

Petronova

24.2%

17.9%18.5%

3.7%2.0% 1.9% 1.9% 1.8% 1.7% 1.0%1.1% 0.9% 0.8%

Brazilian Ethanol Consumers (million liters per year)

3.0%

As a result of Braskem’s growth in the alcohol-chemical sector, the company is increasingly present in

the market as an ethanol consumer.

34

SUSTAINABLE

Sugar Cane

Ethanol

Ethylene oxide - MEG Styrene - PS

Green Ethylene Derivatives

Green Polyethylene

Green ethyleneAn alternative to ethylene derivatives

35

Agenda

�Business overview and main priorities

� Industrial overview

�Products and markets

�Naphtha

�Ethanol

�Questions

36