BRAND SOUTH AFRICA · Contents Brand SA Mandate & Strategy Overview of Brand SA Research Nation...

91

BRAND SOUTH AFRICA Research & Nation Brand Performance Presentation Prepared by Brand South Africa Research Updated 29 September 2015 1

Transcript of BRAND SOUTH AFRICA · Contents Brand SA Mandate & Strategy Overview of Brand SA Research Nation...

BRAND SOUTH AFRICA

Research & Nation Brand Performance

Presentation

Prepared by Brand South Africa Research

Updated 29 September 2015

1

Contents ● Brand SA Mandate & Strategy

● Overview of Brand SA Research

● Nation Brand Performance – three realms of governance

– Global governance

– Political governance

– Corporate & economic governance

– Top five Ease of Doing Business destinations vs South Africa

– SA inbound & outbound investment profile

– Human & social development indicators

● Brand Reputation

– International Perceptions

● Brand SA fieldwork research – The SA Inc Series

– Project background & findings per market

– Overall findings

● Brand SA Research

– Domestic Perceptions

Presentation prepared by Brand SA.

Readers are welcome to use the data contained in this report for their own purposes provided they acknowledge

the source as: Brand South Africa, Research & Nation Brand Performance Presentation, September 2015, available

at: www.brandsouthafrica.com

2

3

BRAND SA MANDATE & STRATEGY

4

Brand SA – Core Functions

Six core functions:

1. Information, insights & ideas

2.Marketing, advertising &

branding

3. Issues management

4.Promotions & events

5.Media relationships

6.Stakeholder relationships

5

Key strategic considerations

• SA is a middle power that projects its influence primarily through soft

power interventions, with a view to long-term transformation of the world

system.

• Domestic economic challenges are amplified by domestic issues of

unemployment (especially among youth), and slow GDP growth in the

medium term.

SA’s nation brand strategy needs to focus on:

• Supporting & facilitating the NDP

• Increasing familiarity with SA in international markets

• Positioning SA as an innovative and inspiring bridge between developing

nations

• Positioning SA as a facilitator of human development through new global

partnerships

• Indicators clearly show that the African continent, BRICS, and other key

emerging markets (e.g. “the Next 11”) will remain drivers of global

growth

6

Global target audiences

Note: this list of stakeholders is not exhaustive and will change to meet new circumstances

Government

• Political leaders

• National government

• Local government

• Trade & tourism entities

• Political parties

Business

• Business Associations

• Corporates

• International Chambers

• International Trade Councils

• Export Councils

• Tourism players

• Film makers

• Conference organisers

• Economists & Analysts

• Public

• Political Parties

• NGO’s

• FBO’s

• Labour leaders

• Youth Formations

• Academia

• Gender advocacy groups

• Clubs, societies & special

interest groups (e.g.

photographers, wildlife

enthusiasts, jazz lovers,

designers, etc.)

Civil Society

Media

Influential forums

• United Nations

• AU

• SADC

• World Bank

• IMF

• BRICS

• World Economic Forum

• IATA

• WWF

Opinion leaders

7

Critical Stakeholder Collaboration & Responsibility Matrix

Brand South Africa

Department of Communications

Proudly South African

South African Tourism

TISA

National value proposition and positioning development & articulation

Brand awareness and positive image domestically

Brand awareness and positive image domestically

Define National Pride, Patriotism, Social Cohesion & Buy Local Activism

Primary agency responsible for marketing of South African Tourism

opportunities

Trade and investment

Brand awareness and positive image domestically

Communicate

nation brand attributes (Country branding)

Communicate

Government services

Communicate

products and services attributes

Communicate tourism

brand attributes (Destination marketing)

Communicate

investment offering domestically

Brand awareness and positive image internationally

Communicate

nation brand attributes (Country

Communicate local

companies’ products & services to South Africans

Communicate tourism

brand attributes (Destination marketing)

Communicate

investment offering internationally

Strategic Approach

Public Relations

Advertorials

Opinion Pieces

Thought Leadership

Articles

Advertising

Digital Platform and Social Media

The integrated multi-channel

communication approach will ensure Brand

SA reaches the Focused Stakeholder

Groupings as identified aligned to

frequency, impact and the reach objectives.

This approach will also be applied by the

various Country/Programme Managers

and Agencies in Market.

Country

Managers

8

OVERVIEW OF BRAND SA

RESEARCH

9

Brand SA takes an eclectic approach to target audience perceptions & rankings

analysis and draws insights from various research surveys and indices:

Domestic

Perceptions

Domestic Perceptions Research

Research Reference Groups

Brand SA stakeholder survey

Nation Brand

Reputation

Roper GfK. Nation Brand Index

Roper GfK. City Brands Index

Brand SA –Fieldwork in African markets (2014/15: Kenya, Ghana, Nigeria;

2015/16: DRC, Angola, Senegal, Russian Federation & BRICS)

Global

Competitiveness

World Economic Forum – Global Competitiveness Index

IMD – Competitiveness Year Book

Mo Ibrahim Index on African Governance

World Bank Ease of Doing Business etc.

Investor

Perceptions Brand SA Project Thrive on International Investor Perceptions

Media Reputation Media Tenor - Media Reputation Tracker and Analysis

Brand SA – Country Office and Agencies Media Analysis

10 10

High Level Summary of Indices and Perceptions Findings

Domestic

Perceptions

• 92% of the population are proud to be South African • Sport is one of South Africa’s highest celebrated achievements • Over 85% of the population believe that SA is a competitive and innovative nation • 95% of South Africans have a sense of belonging in the country • Despite the problems there is a strong desire to stay in the country.

Nation Brand

Reputation

• • 37/50 in 2014 – for three previous years ranked at 36/50 • Stable reputation with minor changes in some pillars • 2014 improvements in Exports, Governance, and Immigration & Investment • 2014 ranking in Tourism, People, and Culture drops

Global

Competitiveness

• 56th out of 144 economies (WEF) • 4th out of 52 African countries (IIAG) • Strengths: securities exchange regulation, auditing standards, corporate boards, banks,

financial market development, financial services, public management • Areas requiring attention: labour markets, cost of business, education, health, personal safety

Investor

Perceptions

• 40% familiarity gap - low overall familiarity with SA as a business destination • Increasingly seen as a potential growth market, rich in resources • Associations with crime and corruption issues

Media Reputation

• Slight drop off from 56.41 to 47.4 • Our biggest supporters are BRIC countries (excluding Russia) • Africa- Europe is hard on us and low coverage Middle East and South America • Key drivers were tourism, business, international diplomacy (BRICS)

11 11

NATION BRAND PERFORMANCE

Nation Brand Performance

● Governance plays a critical role in shaping the reputation of the

Nation Brand

● For this reason the updated Brand SA Nation Brand Performance

presentation will be anchored by perspectives on governance in

three realms of activity as outlined below

Governance

International

Political Corporate

13

Nation Brand Performance – Three realms of Governance

14

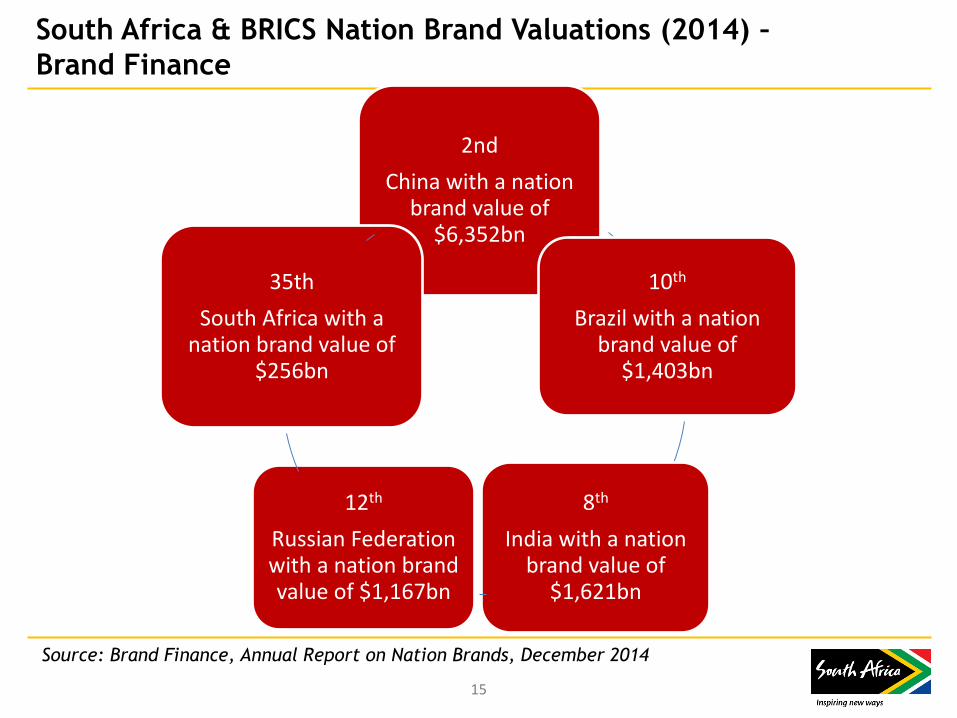

South Africa & BRICS Nation Brand Valuations (2014) –

Brand Finance

2nd

China with a nation brand value of

$6,352bn

10th

Brazil with a nation brand value of

$1,403bn

8th

India with a nation brand value of

$1,621bn

12th

Russian Federation with a nation brand value of $1,167bn

35th

South Africa with a nation brand value of

$256bn

Source: Brand Finance, Annual Report on Nation Brands, December 2014

15

GLOBAL GOVERNANCE

Nation Brand Performance

Nation Brand Performance – Global Governance

The Nation Brand’s global and domestic reputation is to a large extent

shaped by perceptions of efficient internal governance, while the

nation brand’s contribution to global governance has a direct bearing

on international perceptions

Global Governance Contribution

Peaceful internally negotiated

political settlement

Active role in transforming OAU to

AU & contribution to Peace &

Security on the African continent

Served 2 terms as non-permanent

member of the UN Security Council

Champion of New Partnership for

Africa’s Development

Plays an active role in the G20 Included as fifth member of BRICS

17

POLITICAL GOVERNANCE

Nation Brand Performance

Nation Brand Performance – Political Governance

Constitution of the Republic of South Africa

Preamble

We, the people of South Africa,

Recognise the injustices of our past;

Honour those who suffered for justice and freedom in our land;

Respect those who have worked to build and develop our country; and

Believe that South Africa belongs to all who live in it, united in our diversity.

We therefore, through our freely elected representatives, adopt this Constitution as the

supreme law of the Republic so as to

• Heal the divisions of the past and establish a society based on democratic values, social

justice and fundamental human rights;

• Lay the foundations for a democratic and open society in which government is based on the

will of the people and every citizen is equally protected by law;

• Improve the quality of life of all citizens and free the potential of each person; and

• Build a united and democratic South Africa able to take its rightful place as a sovereign state

in the family of nations.

May God protect our people.

Nkosi Sikelel’ iAfrika. Morena boloka setjhaba sa heso.

God seën Suid-Afrika. God bless South Africa.

Mudzimu fhatutshedza Afurika. Hosi katekisa Afrika.

19

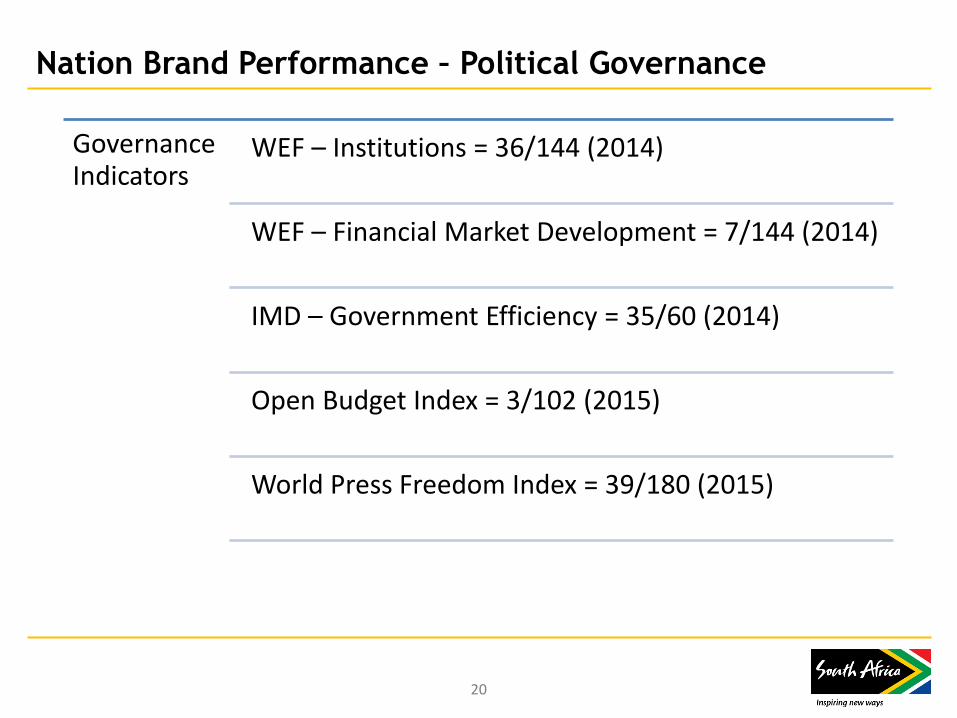

Nation Brand Performance – Political Governance

Governance Indicators

WEF – Institutions = 36/144 (2014)

WEF – Financial Market Development = 7/144 (2014)

IMD – Government Efficiency = 35/60 (2014)

Open Budget Index = 3/102 (2015)

World Press Freedom Index = 39/180 (2015)

20

African Peer Review Mechanism Country Report 2014 Highlights

Democracy and Political Governance

● Initiatives launched to improve transparency and accountability in the

governance of the country include Corruption Watch (luanched by COSATU,

BUSA and the National Anti-Corruption Forum) and the National Anti-Corruption

Hotline (managed by Public Service Commission)

South Africa improved its score from 2013 to 2014 in Transparency

International’s Corruption Perception Index – from 42 to 44 on a scale of 0-100.

In terms of perceptions of public sector corruption, it performs better than its

BRICS partners, ranking 67th out of 175 countries and lies above the regional

average (33/100).

Nation Brand Performance: Political Governance

The APRM – an instrument voluntarily acceded to by AU member states – was established to foster the adoption of policies, standards and practices that lead to political stability, high economic growth, sustainable development and accelerated subregional and continental economic integration. This objective is achieved through sharing of experiences and reinforcement of successful and best practices.

21

The Mo Ibrahim Index of African Governance 2014 (1)

● The Mo Ibrahim Foundation defines governance as the provision of the

political, social and economic goods that any citizen has the right to expect

from his or her state, and that any state has the responsibility to deliver to

its citizens.

● IIAG: annual assessment of quality of governance in every African country

● IIAG combines over 100 variables from over 30 independent sources; most

comprehensive collection of data on African governance

● Assesses governance provision within four distinct conceptual categories:

Nation Brand Performance: Political Governance

Safety &

Rule of Law

Sustainable

Economic

Opportunity

Participation

& Human

Rights

Human

Development

22

The Mo Ibrahim Index of African Governance 2014 (2)

● South Africa ranks 4th out of 52 countries overall

● Scores in the Top 10 in all four categories

Nation Brand Performance: Political Governance

Safety &

Rule of Law

Sustainable

Economic

Opportunity

Participation

& Human

Rights

Human

Development

2nd 6th 4th 8th

23

The Mo Ibrahim Index of African Governance 2014 (3)

Nation Brand Performance: Political Governance

SUSTAINABLE ECONOMIC OPPORTUNITY

PARTICIPATION AND HUMAN RIGHTS

SAFETY AND SECURITY

HUMAN DEVELOPMENT

Source: Mo Ibrahim Foundation, 2014 IIAG

24

CORPORATE & ECONOMIC

GOVERNANCE

Nation Brand Performance

King Code on Corporate Governance for South Africa

● In 1992, at a time when South Africans were adjusting to the fact that

they would be moving towards a new democratic society, former

South African Supreme Court Judge Mervyn King was asked to chair a

private‐sector body to draft corporate governance guidelines.

● The body became known as the King Committee, and its first report,

issued in 1994, was regarded by many as ahead of its time in adopting

an integrated and inclusive approach to the business life of

companies, embracing stakeholders other than shareholders.

● The Committee subsequently revised its report in 2002, and more

recently in 2009. The current King Code on Corporate Governance for

South Africa (also called "King III") is again pointing to the next level

in governance by encouraging the integration of governance and

sustainability into the strategy, operations, and reporting of an

organization.

Nation Brand Performance:Corporate Governance

26

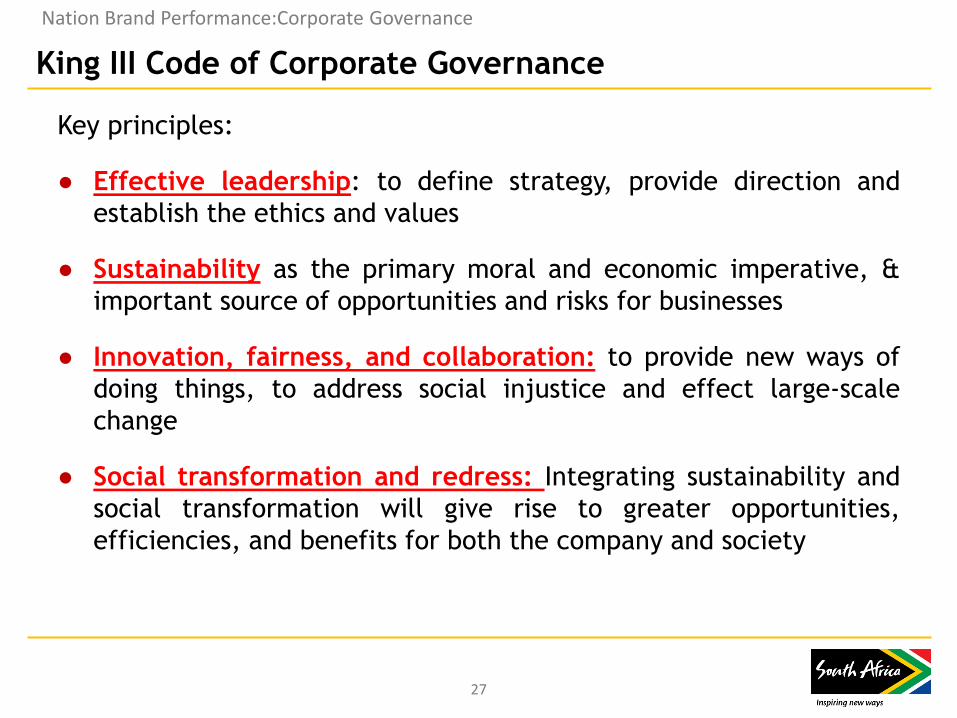

King III Code of Corporate Governance

Key principles:

● Effective leadership: to define strategy, provide direction and

establish the ethics and values

● Sustainability as the primary moral and economic imperative, &

important source of opportunities and risks for businesses

● Innovation, fairness, and collaboration: to provide new ways of

doing things, to address social injustice and effect large-scale

change

● Social transformation and redress: Integrating sustainability and

social transformation will give rise to greater opportunities,

efficiencies, and benefits for both the company and society

Nation Brand Performance:Corporate Governance

27

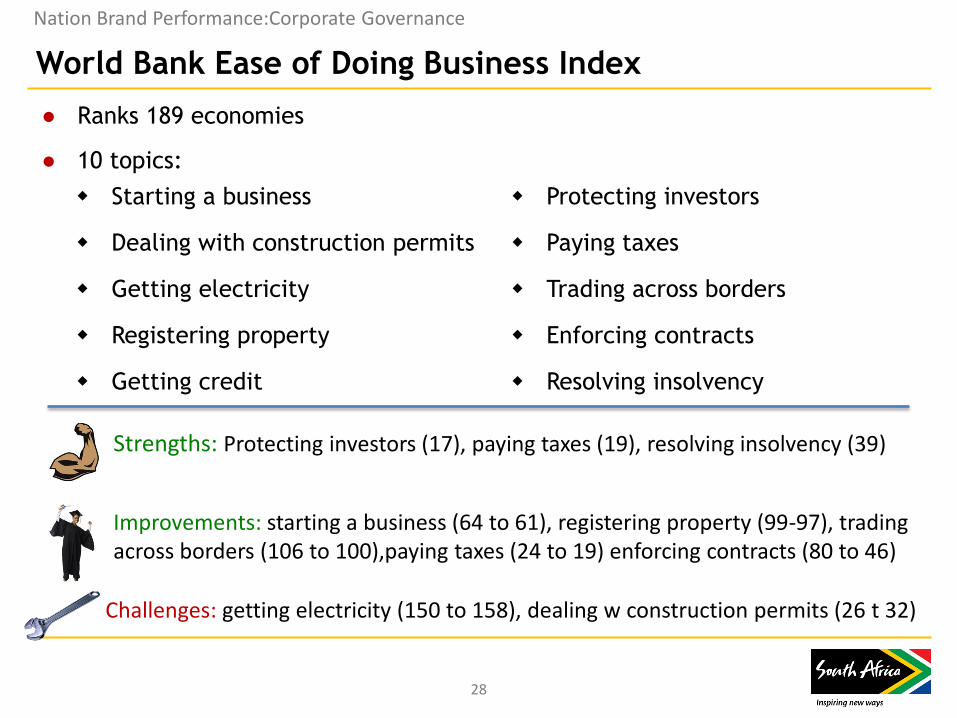

Starting a business Protecting investors

Dealing with construction permits Paying taxes

Getting electricity Trading across borders

Registering property Enforcing contracts

Getting credit Resolving insolvency

World Bank Ease of Doing Business Index

● Ranks 189 economies

● 10 topics:

Nation Brand Performance:Corporate Governance

Strengths: Protecting investors (17), paying taxes (19), resolving insolvency (39)

Improvements: starting a business (64 to 61), registering property (99-97), trading across borders (106 to 100),paying taxes (24 to 19) enforcing contracts (80 to 46)

Challenges: getting electricity (150 to 158), dealing w construction permits (26 t 32)

28

WEF Competitiveness Report

Nation Brand Performance:Corporate Governance

● Ranks 144 economies, SA and Mauritius are top African performers

● 12 competitiveness pillars:

Institutions Labor market efficiency

Infrastructure Financial market development

Macroeconomic environment Technological readiness

Health and primary education Market size

Higher education and training Business sophistication

Goods and market efficiency Innovation

Strengths: Institutions (36), Goods and market efficiency (32), Business sophistication (31), financial market development (7), market size (25)

Improvements: infrastructure (66 to 60), health and primary education (135 to 132)

Challenges: labour market efficiency (113), innovation (39 to 43)

29

TOP 5 COUNTRIES VS SOUTH

AFRICA

World Bank Ease of Doing Business Index 2015

South Africa vs Korea

EDB Overall Ranking-2015 South Africa: 43 Korea: 5

World Bank Ease of Doing Business Index 2015

Source: World Bank (2014): Doing Business 2015: Going Beyond Efficiency

31

South Africa vs Denmark

32

EDB Overall Ranking-2015 South Africa: 43 Denmark: 4

World Bank Ease of Doing Business Index 2015

Source: World Bank (2014): Doing Business 2015: Going Beyond Efficiency

South Africa vs Hong Kong

EDB Overall Ranking-2015 South Africa: 43 Hong Kong: 3

World Bank Ease of Doing Business Index 2015

Source: World Bank (2014): Doing Business 2015: Going Beyond Efficiency

33

South Africa vs New Zealand

EDB Overall Ranking-2015 South Africa: 43 New Zealand: 2

World Bank Ease of Doing Business Index 2015

Source: World Bank (2014): Doing Business 2015: Going Beyond Efficiency

34

South Africa vs Singapore

EDB Overall Ranking-2015 South Africa: 43 Singapore: 1

World Bank Ease of Doing Business Index 2015

Source: World Bank (2014): Doing Business 2015: Going Beyond Efficiency

35

WB Ease of Doing Business Index 2015: The Next 11

36

World Bank Ease of Doing Business Index 2015

Source: World Bank (2014): Doing Business 2015: Going Beyond Efficiency

SA INBOUND & OUTBOUND

INVESTMENT PROFILE

Nation Brand Performance

Inbound Investment

Director-General of the Department of Trade & Industry – Mr Lionel

October

● Investment is the most reliable predictor of future economic

growth.

● The fastest growing developing countries have Gross Domestic

Fixed Investment (GDFI) to Gross Domestic Product (GDP) ratios of

above 30% while SA’s is around 20% against the NDP target of 30%.

● At the aggregate level, the challenge South Africa faces is that

private-sector investment is not growing fast enough to grow the

economy by 5%.

SA Investment Profile

38

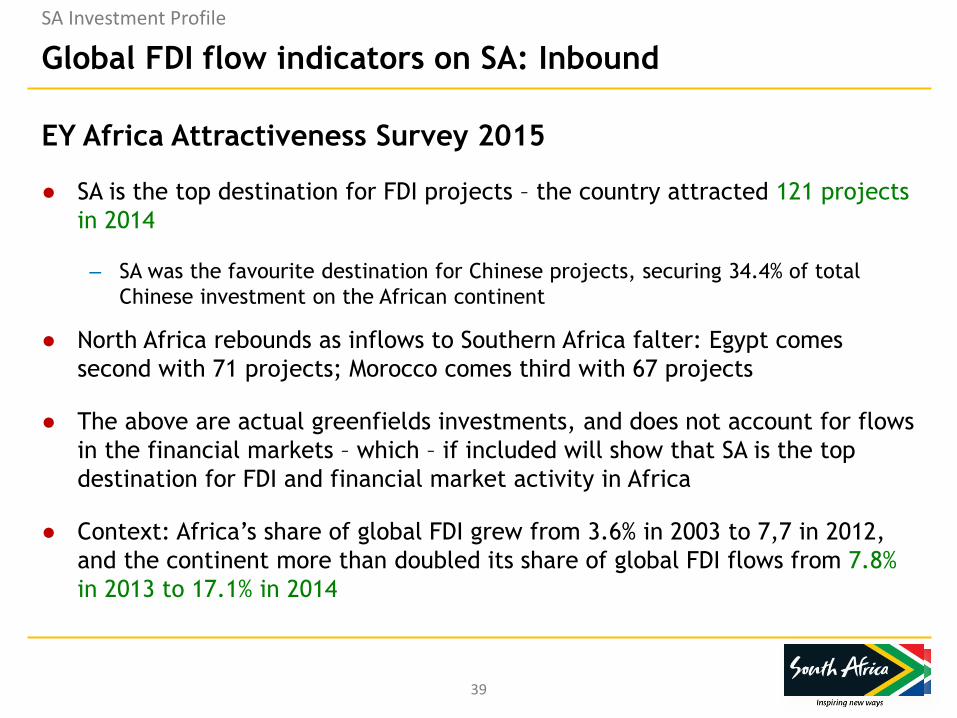

Global FDI flow indicators on SA: Inbound

EY Africa Attractiveness Survey 2015

● SA is the top destination for FDI projects – the country attracted 121 projects

in 2014

– SA was the favourite destination for Chinese projects, securing 34.4% of total

Chinese investment on the African continent

● North Africa rebounds as inflows to Southern Africa falter: Egypt comes

second with 71 projects; Morocco comes third with 67 projects

● The above are actual greenfields investments, and does not account for flows

in the financial markets – which – if included will show that SA is the top

destination for FDI and financial market activity in Africa

● Context: Africa’s share of global FDI grew from 3.6% in 2003 to 7,7 in 2012,

and the continent more than doubled its share of global FDI flows from 7.8%

in 2013 to 17.1% in 2014

SA Investment Profile

39

Global FDI flow indicators on SA: Inbound

SA Investment Profile

EY Africa Attractiveness Survey 2015: SA remains on top

Source: EY Africa Attractiveness Survey 2015

40

Outbound Investment

● 2013 budget speech of then minister of Finance, Pravin Gordhan, indicated that

during the 2008-2013 period the South African Reserve Bank approved nearly 1

000 large investments by South African corporations into 36 African countries

● NDP underlines critical importance of boosting intra-African trade and

integration of regional markets

● Johannesburg Stock Exchange currently ranked the 19th largest stock exchange

in the world by market capitalisation and the largest exchange in Africa

● Industrial Development Corporation (IDC) has investments in 60 projects across

20 countries that creates a cumulative African investment portfolio of R7.5

billion by March 2014

● With so many SA and multinational corporates that operate from Joburg into

other African markets, the city’s logistical, air, inland port, and related soft

infrastructure provides a solid base for corporates to establish regional

headquarters

SA Investment Profile

41

Global FDI flow indicators on SA: Outbound

EY – Africa Attractiveness Survey (2015)

● South Africa is the second largest source of FDI into the African

continent (53 projects launched in 2014).

● SA is the leading intra-regional investor in the financial services

sector (16 projects launched in 2014)

SA Investment Profile

42

Intra-SADC investment

SA Investment Profile

• South Africa plays pivotal role

in the economic revival of the

continent

• Contributes 68% of SADC GDP

• SA invested USD1,4b in 75

new FDI projects in Africa

(2012)

• Created 50,000 jobs Africa-

wide

Source: Inside Southern Africa, September 2015

43

Department of Trade and Industry

● Department of Trade & Industry FDI trend data:

– Gross Domestic Fixed Investment has been growing steadily since the

Global Financial Crisis.

– FDI in 2013 was boosted by the R20bn Barclays investment.

– Latest FDI data show that SA attracted over R140bn in 2013-14.

– Global FDI fell by 16% in 2014.

– SA FDI inflows also slowed in 2014 but remain at a level almost double

the level of FDI in 2012.

● SA FDI performance is not unusual as:

– many multinationals already operate in SA,

– we have sophisticated financial markets to raise domestic capital, and

– our FDI stock is already high by international standards (42%).

SA Investment Profile

44

SA Investment Profile

480

500

520

540

560

580

600

620

640

R b

illio

ns

SA Annual Real GDFI 2009-14 (Rb 2010-Prices)

Source: SARB, 2015, Quarterly Bulletin

-

10

20

30

40

50

60

70

80

90

R b

illio

ns

SA Annual FDI 2009-14 (Rb Current-Prices)

Source: SARB, 2015, Quarterly Bulletin

45

Countries investing in South Africa

Top investors:

UK – 32%

USA – 23%

China – 13%

Italy – 7%

Mauritius – 4%

France – 4%

Japan – 3%

Germany – 2%

Spain – 2%

Other , 4%

Netherlands, 1%

Belgium, 1%

UAE, 1%

Switzerland, 1%

Canada, 1%

India, 1%

Spain, 2%

Germany, 2%

Japan, 3%

France, 4%

Mauritius, 4%

Italy, 7%

China, 13%

USA, 23%

UK, 32%

Countries investing in South Africa 2014

SA Investment Profile

Source: FDIMarkets

46

DTI’s National Initiative: One Stop Investment Centre (1)

● DTI working on implementing this national initiative

● Gauteng Growth and Development Agency’s successful One Stop Shop at

GIC, Sandton (government services represented e.g. SARS, Home Affairs)

● National centre: central operational structure to act as implementing body

and serve as convener for one stop investment centre

● Will improve investment climate and ease of doing business by identifying

bottlenecks, administrative barriers & have plan of action to improve

service delivery

● Focus: reducing regulatory inefficiencies, setting up norms and standards,

turnaround times, coordinate, fast track, unblock and reduce red tape for

all investors

SA Investment Profile

47

Infrastructure

Indicators

WEF – Quality of road = 37/144 (2014)

WEF – Quality of railroad infrastructure = 44/144 (2014)

IMD – Overall improvement on infrastructure from 58/60 -55/60 (2013-2014)

IIAG – Overall Infrastructure 3/52 (2014); road network

SA Investment Profile : Infrastructure (1)

Road and Rail Transport

A massive motorway improvement scheme has seen extra

lanes added, a sophisticated electronic toll system

introduced and interchanges drastically renovated

The Gautrain rapid rail system links the OR Tambo

International Airport with stations in Johannesburg and

Pretoria

South Africa has world-class infrastructure, including an excellent transport network, low-cost energy and sophisticated telecommunications facilities

48

SA Investment Profile : Infrastructure (2)

Ports

Most advanced port infrastructure on the African continent

Saldanha Bay in the Western Cape is the largest natural anchorage with the deepest water, 60 nautical miles northwest of Cape Town

The Durban port in KZN handles the greatest volume of sea-going traffic of all SA ports

The Richards Bay Port in KZN can handle a total of 1 782 ships with a gross tonnage of 65 994 515 in a year

The Port Elizabeth Port in the Eastern Cape handled a total of 1,176 ships during the 2011/12 financial year

The Cape Town Port in the Western Cape competes with Alexandria for recognition as the most famous port in Africa

Infrastructure

Indicators

WEF – Quality of transport infrastructure 32/144 (good by regional standards)

WEF – Quality of port infrastructure = 46/144 (2014)

IMD – Improvements on basic infrastructure from 56/60 to 52/60 (2011-2014)

49

SA Investment Profile : Infrastructure (3)

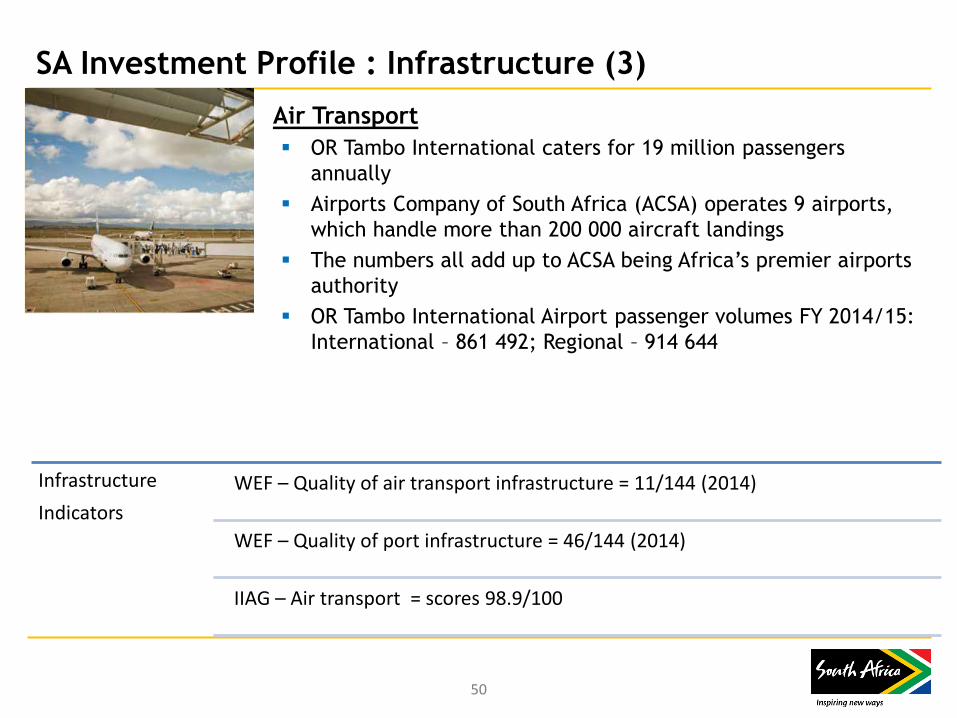

Air Transport

OR Tambo International caters for 19 million passengers

annually

Airports Company of South Africa (ACSA) operates 9 airports,

which handle more than 200 000 aircraft landings

The numbers all add up to ACSA being Africa’s premier airports

authority

OR Tambo International Airport passenger volumes FY 2014/15:

International – 861 492; Regional – 914 644

Infrastructure

Indicators

WEF – Quality of air transport infrastructure = 11/144 (2014)

WEF – Quality of port infrastructure = 46/144 (2014)

IIAG – Air transport = scores 98.9/100

50

SA Investment Profile : Infrastructure (4)

Infrastructure

Indicators

WEF – Quality of overall infrastructure = 52/144 (2014)

IMD – Overall improvement on infrastructure from 58 to 55/60 (2013-2014)

IMD – Improvements on basic infrastructure from 56 to 52/60 (2011-2014)

IIAG – Overall Infrastructure 3/52 (2014)

51

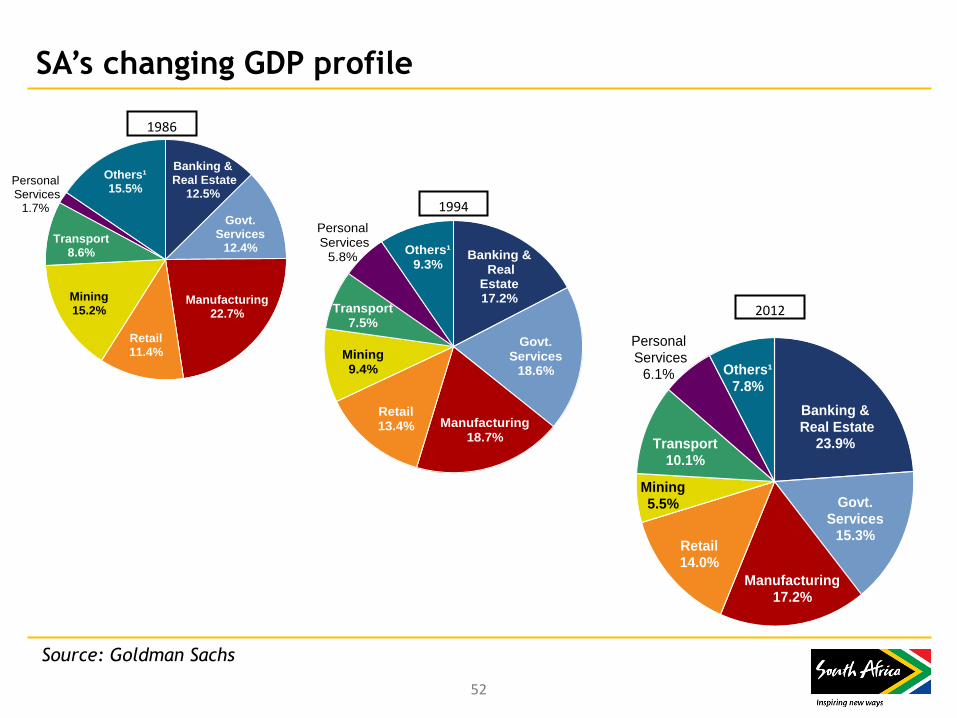

SA’s changing GDP profile

Banking &Real Estate

12.5%

Govt. Services

12.4%

Manufacturing22.7%

Retail11.4%

Mining15.2%

Transport8.6%

PersonalServices

1.7%

Others¹15.5%

Banking &Real

Estate17.2%

Govt. Services

18.6%

Manufacturing18.7%

Retail13.4%

Mining9.4%

Transport7.5%

PersonalServices

5.8%Others¹

9.3%

Banking &Real Estate

23.9%

Govt. Services

15.3%

Manufacturing17.2%

Retail14.0%

Mining5.5%

Transport10.1%

PersonalServices

6.1% Others¹7.8%

1986

1994

2012

Source: Goldman Sachs

52

HUMAN & SOCIAL

DEVELOPMENT INDICATORS

Nation Brand Performance

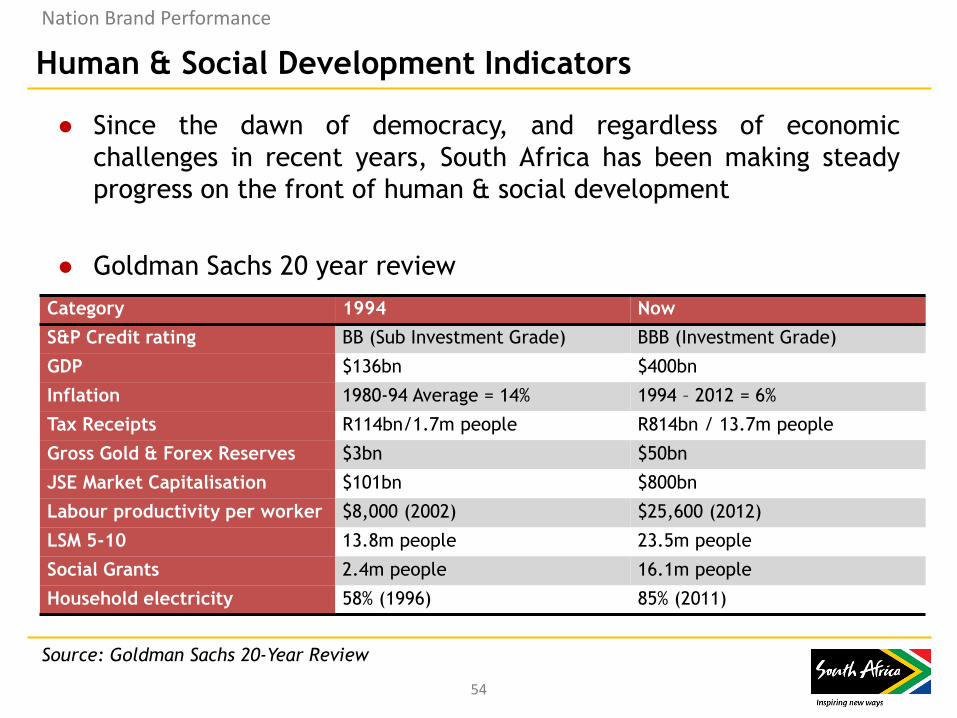

Human & Social Development Indicators

● Since the dawn of democracy, and regardless of economic

challenges in recent years, South Africa has been making steady

progress on the front of human & social development

● Goldman Sachs 20 year review

Category 1994 Now

S&P Credit rating BB (Sub Investment Grade) BBB (Investment Grade)

GDP $136bn $400bn

Inflation 1980-94 Average = 14% 1994 – 2012 = 6%

Tax Receipts R114bn/1.7m people R814bn / 13.7m people

Gross Gold & Forex Reserves $3bn $50bn

JSE Market Capitalisation $101bn $800bn

Labour productivity per worker $8,000 (2002) $25,600 (2012)

LSM 5-10 13.8m people 23.5m people

Social Grants 2.4m people 16.1m people

Household electricity 58% (1996) 85% (2011)

Nation Brand Performance

Source: Goldman Sachs 20-Year Review

54

Human & Social Development Indicators

South Africa HDR indicators

Year Rank HDR value Life

expectancy

Mean yrs of

schooling

Expected

yrs of

schooling

Gross national

income

2013/14 118 0.658 56.9 9.9 13.1 $ 11,788

(PPP)

2012/13 121 0.629 53.4 8.5 13.1 $ 9594

(PPP)

2011 123 0.619 52.8 8.5 13.1 $ 9469

(PPP)

Nation Brand Performance

Source: UNDP, Human Development Report 2014

55

INTERNATIONAL PERCEPTIONS

Brand Reputation

High level findings on SA’s global reputation

Nation Brand Index

Over-all position 37/50 (stable reputation with minor score changes in NBI

hexagon pillars)

City Brand Index

SA cities rank relatively low on the CBI

Cape Town 42/50

Johannesburg 44/50 – Johannesburg makes a marked improvement in the 2013 CBI

Durban 47/50

Brand Reputation: International Perceptions

57

Exports Tourism

Governance

Culture and Heritage

People Skills and openness

Investment Potential and

attractiveness to outsiders

Commercial and cultural

products and sporting prowess

Competency fair

governance, human

rights, international

contribution

Potential attractiveness

and economical

contribution

Level of

satisfaction with

country’s products

and services

Investment &

immigration

South Africa’s Performance on the Nation Brand Index 2014

58

Brand Reputation: International Perceptions

Source: Anholt-GfK Roper Nation Brands Index

58

SA Reputation Rankings - Strengths

• SA’s reputation globally remains stable in years of global financial turmoil that impacted negatively on developed markets

• South Africa’s Culture remains its strongest asset (27th), esp. admired for sporting excellence

• With a strong People profile (34th globally), South Africans are admired across most panel countries, esp. strong in Commonwealth and Western Europe, India and China

• South Africa continues to rank 34th globally on Tourism, with strong perceptions as being naturally beautiful (15th).

• SA seen as making a significant contribution to global culture

• Potential for Higher Education opportunities

• SA is seen as a growing economy with potential for development

• SA’s infrastructure is a key attractiveness feature for international business

• SA’s transition to democracy and diversity seen as important reputation enhancers

Brand Reputation: International Perceptions

Sources: Nation Brand Index, City Brand Index & Project Thrive

59

SA Reputation Rankings – Challenges & Weaknesses

• South Africa faces most difficulty on Governance

• On Immigration/Investment (38th), the Index ranking is pulled down by a 41st-place ranking on quality of life but has strong anchor as place to work and live (34th)

• Safety & security/crime impacts negatively on perceptions of SA

• Corruption

• Poverty alleviation

• Not perceived as technologically advanced, esp. Central and Eastern Europe, South Korea, Mexico and Japan

• SA products mostly associated with agriculture, crafts & food – calls for need to profile other SA products, manufactured goods & services (NBI)

• Findings on reputation of SA cities indicate a need for more concerted effort to build awareness & reputation – perceptions of key city offerings have direct impact on Nation Brand (Johannesburg’s performance improved)

60

Brand Reputation: International Perceptions

Sources: Nation Brand Index, City Brand Index & Project Thrive

61

THE SA INC SERIES

PROJECT BACKGROUND & FINDINGS

PER MARKET

Brand SA Fieldwork Research

62

The SA Inc. Research Project (1)

The SA Inc project aims to:

Contribute to the development of a framework of analysis that considers all

the elements of South Africa’s strategic economic, diplomatic, multilateral,

as well as peace & security engagements on the continent – all of these

elements shape the brand reputation;

The project Rationale:

South Africa’s reputation is shaped by more than foreign policy, or trade

interactions. It is shaped by a divergent sets of relationships and

interests. Therefore depends on, and is influenced by a range of

governmental, non-governmental, and business relationships;

Towards an integrated nation brand analysis:

In addition such a framework of analysis will provide Brand South Africa with

an integrated view of South Africa’s footprint on the continent for strategic

marketing, communications, and reputation management projects.

Brand SA Fieldwork Research

63

The SA Inc. Research Project (2)

Baseline of SA footprint per key African market - identify key reputational drivers (threats & opportunities)

Multilateral & Bilateral Relations

Peace & Security

Investment

Trade, FDI, Business

Inputs: Peace & Security;

Trade; FDI; Bilateral;

Multilateral activities and

associated value of such

activities

Output: Integrated

Framework of Analysis

Brand SA Fieldwork Research

64

Cycle 1 – 2014/15: Kenya, Nigeria, Ghana

● Brand SA’s Africa strategy: development of SA presence & reputation

in select markets/multilateral environments (e.g. BRICS, and

selected key strategic markets);

● South Africa In(c) series research reports based on:

– direct fieldwork studies

– desktop research

• The SA In(c) series aims to develop holistic/integrated understanding

of SA footprint in international markets

Brand SA Fieldwork Research

The SA Inc. Project: Fieldwork

65

The SA Inc. Project: Objectives

● Development of framework of analysis that considers all elements

of SA’s strategic economic, diplomatic, multilateral, and peace &

security engagements on the continent

● Rationale: SA’s reputation is shaped by foreign policy, trade

interactions, AND relationships and interests. Therefore depends

on, and is influenced by a range of governmental, non-

governmental, and business relationships

● Framework will provide Brand SA with integrated view of SA

footprint on continent for strategic marketing, communications,

and reputation management projects

Brand SA Fieldwork Research

66

SA Inc. Project: Kenya – South Africa Bilateral Trade

Total Bilateral Trade (2014)

Kenya Imports from SA

R 7 822 930 304

SA Imports from Kenya

R 366 206 571

Total Bilateral Trade R 8,189,136, 875

Brand SA Fieldwork Research

67

SA Inc. Project: Kenya Key Findings

The fieldwork yielded several insights regarding both challenges and

opportunities for interaction between the countries.

From a reputational point of view SA has major influence on two fronts:

1. As a result of SA democratic transition, strong institutions;

2. As a result of major interest in SA music & culture.

However, through the fieldwork it has become apparent that:

1. SA is seen as losing its competitive edge, & that it is not doing enough

to promote internal development;

2. The SA character or personality perceived as imposing and aggressive;

3. SA companies losing to local competition due to poor market entry

strategies and ‘know it all’ attitudes.

Brand SA Fieldwork Research

68

SA Inc. Project: Nigeria – South Africa Bilateral Trade

Total Bilateral Trade (2014)

Nigeria Imports from SA

R 10 546 842 578

SA Imports from Nigeria

R 55 704 188 272

Total Bilateral Trade R 66 251 030 850

Brand SA Fieldwork Research

69

SA Inc. Project: Nigeria Key Findings From a reputational point of view SA has major influence on several fronts:

1. With more than 150 companies active in the market, SA is highly visible, and

respected in many areas of national competency

2. SA’s democratic transition, institutional & infrastructural profile appreciated

& often referenced as key attractiveness feature

3. Nigerian respondents keen to interact with & explore opportunities with SA

for business & investment interactions and for cultural, music, tourism &

related experiences

However, through the fieldwork it has become apparent that:

1. While SA has a major business and investment footprint in market, concerns

exist about the South African character and business culture

2. With Nigeria’s rebased GDP some consider SA to be losing competitive edge

3. SA character/business persona at times perceived as imposing & aggressive

4. SA companies losing to local competition due to quick adaptation & learning

by local competition and lack of identifying & involving local partners in

market entry, maintenance, and expansion strategies

Brand SA Fieldwork Research

70

SA Inc. Project: Ghana– South Africa Bilateral Trade

Total Bilateral Trade (2014)

Ghana Imports from SA

R 3 723 629 774

SA Imports from Ghana

R 7 101 559 112

Total Bilateral Trade R 10 825 188 886

Brand SA Fieldwork Research

71

SA Inc. Project: Ghana Key Findings

South Africans & their corporate governance, managerial, technical, & other

expertise respected; reflects positively on reputation of the nation brand

Strong people-to-people relations & potential for expansion in creative

spheres

Nation’s reputation in international markets rely on more than government-

to-government relations, & mostly shaped by experience & perceptions of

South African individuals and corporate brands

SA corporates & their products & services widely known & utilised in market

Ghanaians appear to prefer ‘international brands’, incl. those from SA

Tremendous potential in building deeper social & cultural relations via music,

arts, design and cultural diplomacy

SA entrepreneurs use Accra as regional base/hub for West African business

operations

Brand SA Fieldwork Research

72

SA INC PROJECT – OVERALL

FINDINGS

Brand SA Fieldwork Research

73

1. The Nation Brand concept and the execution of nation brand

marketing strategy depends on stakeholder interactions, and

challenges Brand SA to be open to changing domestic and

international environments

2. The initial fieldwork findings indicate unique nation brand

reputational strengths in areas such as: culture, music, business

sophistication, infrastructure, political management of democratic

transitions

3. On the negative side South Africans are perceived as imposing,

aggressive, and unwilling to listen to local advice

The SA Inc. Project: Key Findings (1)

Brand SA Fieldwork Research

74

The SA Inc. Project: Key Findings (2)

4. From a business perspective it implies that more attention needs to

be paid to the manner in which South Africans interact with African

peers, and how market entry strategies are designed by

incorporating soft factors such as business culture;

5. From a political point of view South Africa is seen as progressive,

that it has strong institutions, and democratic credentials to

underpin its constitution. However, internal developmental

challenges, xenophobia, and misplaced perceptions about African

expats in South Africa is a cause for concern in Kenya and Nigeria;

6. While the above is a sensitive issue, it should be noted that South

African music, art, and cultural products are well received,

followed, and fieldwork finds a keen interest in expanded

interaction in these realms.

Brand SA Fieldwork Research

75

The SA Inc. Project: Publications

A lesson for Brand SA from Nigeria - Be bold, keep it real, and

make it quick - a conversation on the art of Nollywood success.

23 August 2014, Brand South Africa Research Note. By: Dr Petrus de

Kock

Researching the Nation Brand – background to the concept, and

initial findings from fieldwork in Kenya and Nigeria. 18

September 2014. South Africa In(c) Series Research Report #1 By: Dr

Petrus de Kock

African market entry strategy – learning to listen & listening to

learn. 12 December 2014. Brand South Africa Research Note #2.

2014. By: Dr Petrus de Kock

Brand SA Fieldwork Research

DOMESTIC PERCEPTIONS

Brand SA Research

Research Design

• n=2 524 Interviews were conducted via face-to-face, door-to-door interviews in the homes of respondents, using a structured (Computer Aided Personal Interviewing) CAPI questionnaire.

How

• The sample included male and female adults aged 15+

• Nationally representative across age, race, gender, income, community size and region

Who

• All urban areas covering 94% of SA’s adult population

• The sample includes all metros and cities and a representative sample of towns and villages

Where

• Fieldwork conducted by service provider AC Nielsen contracted for 2014-2017 When

78

80 68 73

Pride Index Active Citizenship Index Social Cohesion Index

National Level Indices

Summary

How do we make it stronger?

Focus on the youth – need to highlight the enablers for their growth in South Africa

Low score driven by lack of time to actively participate in community building activities by the working class & lack of motivation of the unemployed

• Stronger & clearer communication about Play Your Part initiative

• Leverage non traditional media

• Drive inclusiveness among the coloured, the elderly & the lower LSMs

79

69

14 13 4

Black White Coloured Indian

Who they are

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 QPD1 – Race; QPD17 – LSM; Q1 - Age

RACE

38%

17%

15%

9%

6%

6% 5% 2% 2%

GP WC KZN EC FS MP NW LP NC

PROVINCE AGE

23%

27% 19%

13%

18%

15-24 yrs 25-34 yrs 35-44 yrs 45-54 yrs 55+ yrs

80

Who they are Over the past 10 years people have become more affluent

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 - QPD17 – LSM & Source: AMPS (Weighted by Population)

29 22 18

27 35 40

11 17 21 11 15

16

2004 2009 2014

LSM 9/10

LSM 7/8

LSM 5/6

LSM 3/4

22 32 37

10% 5%

7% 5%

7% 4%

45%

31%

24%

LSM 4-6 LSM 7-8 LSM 9-10

LSM

81

Beliefs With the rise of the middle class and people focusing more on career aspirations, they choose to spend limited spare time at their disposal with family rather than joining

local / community initiatives

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q9. I am going to read out some statements that may or may not apply to you. For each I read out, please tell me to what extent you agree or disagree with that statement. Now, to what extent do you agree or disagree that …? [SA per statement] / Q14. I am now going to read out a list of actions, and for each one I would like you to tell me how important it is for members of society to participate in each? [SA per statement]

48

48

43

38

38

35

12

Revert to close family when needadvice

Family orientated and spend most ofspare time with them

Can handle anything that gets thrownyour way

Work plays an important part in yourlife

In your spare time, you prefer to stayat home rather than be out and about

An Optimistic Individual

Friends replace family

61

58

56

51

49

40

40

36

Voting in elections

Keeping informed about country…

Keeping informed about community…

Helping the needy

Supporting local businesses

Making time to focus on interests

Watching sporting events

Joining local / community initiatives

82

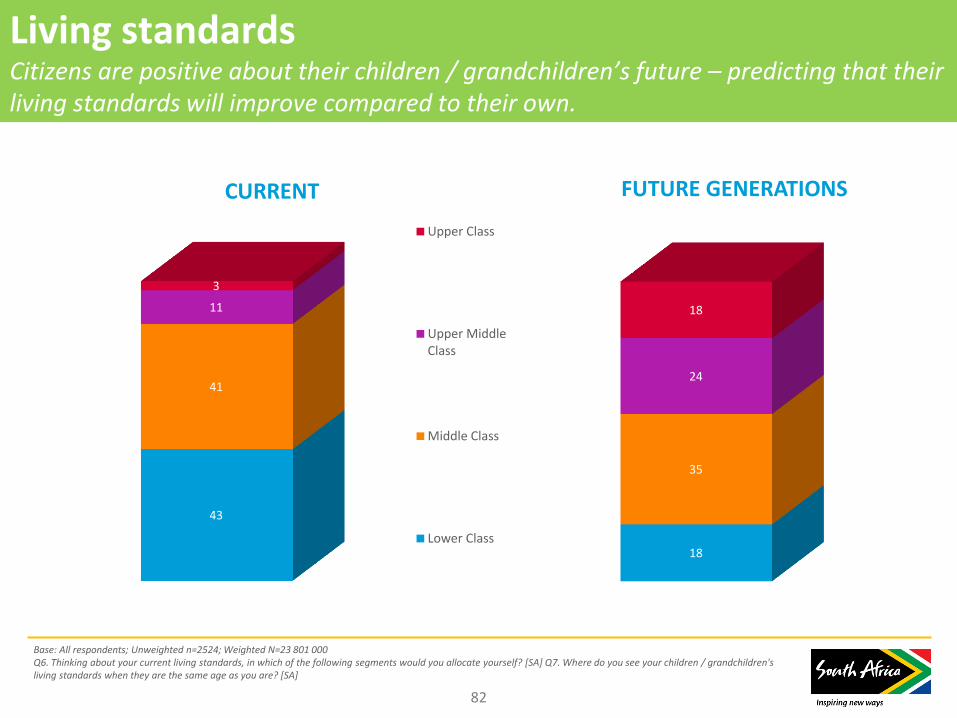

Living standards Citizens are positive about their children / grandchildren’s future – predicting that their living standards will improve compared to their own.

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q6. Thinking about your current living standards, in which of the following segments would you allocate yourself? [SA] Q7. Where do you see your children / grandchildren's living standards when they are the same age as you are? [SA]

43

41

11

3

CURRENT

Upper Class

Upper MiddleClass

Middle Class

Lower Class18

35

24

18

FUTURE GENERATIONS

83

Citizens display high levels of patriotism towards South Africa

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q46. Different people say different things about South Africa. I am again going to read out some statements that have been made about our country. Please tell me to what extent you agree or disagree with each statement. [SA per statement]

85 85 73 78

69 57

9 11

15 12 15

17

6 4 12 10 15

25

Despite the problems,you have no desire to

leave SA

SA's social and culturaldiversity is a major

advantage

Compared to a year agoyou're more likely toopenly criticize the

government

While the governmenthas made a lot of

mistakes, they havedone many good things

Don't think that thingsare better elsewhere;you believe you swap

one set of problems foranother.

The media in SouthAfrica are much too

negative about SA - theydon't show the good

things

T2B (Agree) Neither agree nor disagree B2B (Disagree)

WAY OF PERSONALLY DEALING WITH SITUATIONS IN SA

84

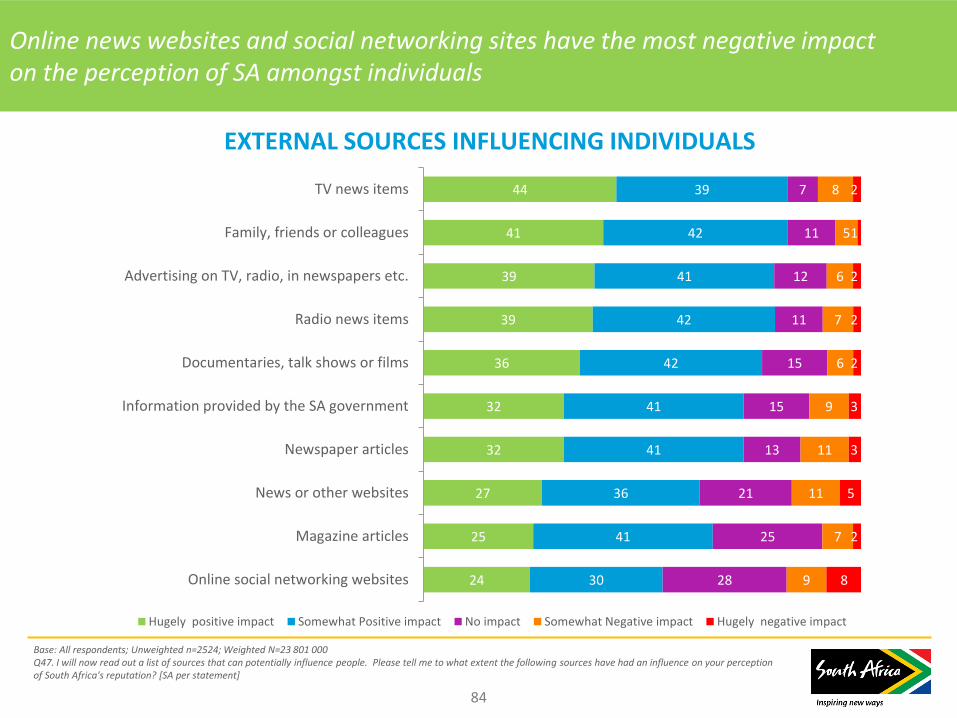

Online news websites and social networking sites have the most negative impact on the perception of SA amongst individuals

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q47. I will now read out a list of sources that can potentially influence people. Please tell me to what extent the following sources have had an influence on your perception of South Africa's reputation? [SA per statement]

44

41

39

39

36

32

32

27

25

24

39

42

41

42

42

41

41

36

41

30

7

11

12

11

15

15

13

21

25

28

8

5

6

7

6

9

11

11

7

9

2

1

2

2

2

3

3

5

2

8

TV news items

Family, friends or colleagues

Advertising on TV, radio, in newspapers etc.

Radio news items

Documentaries, talk shows or films

Information provided by the SA government

Newspaper articles

News or other websites

Magazine articles

Online social networking websites

Hugely positive impact Somewhat Positive impact No impact Somewhat Negative impact Hugely negative impact

EXTERNAL SOURCES INFLUENCING INDIVIDUALS

85

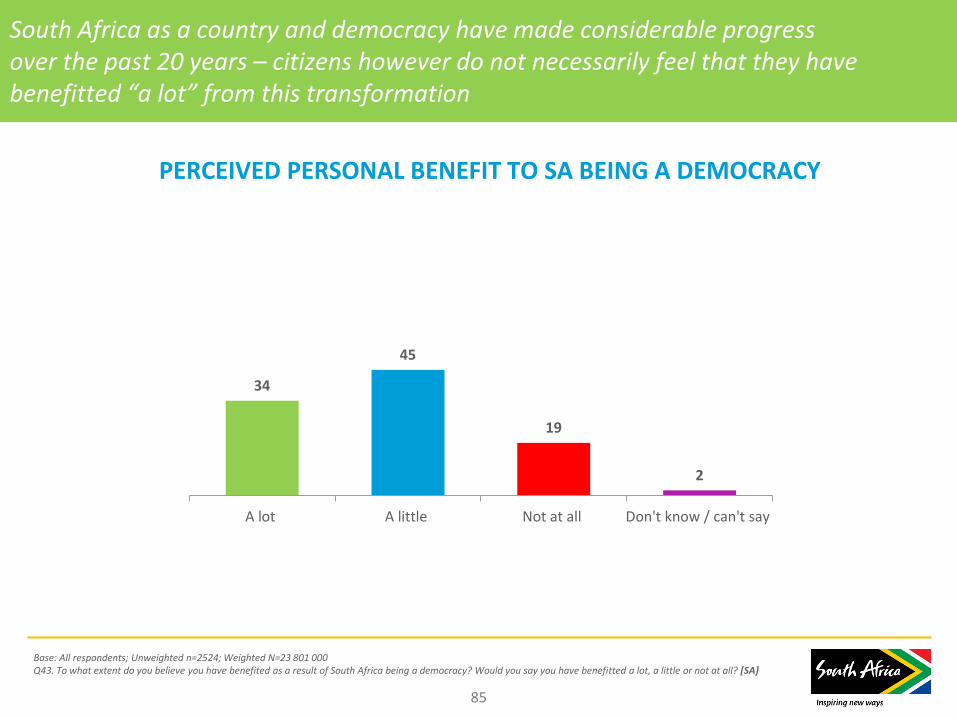

South Africa as a country and democracy have made considerable progress over the past 20 years – citizens however do not necessarily feel that they have benefitted “a lot” from this transformation

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q43. To what extent do you believe you have benefited as a result of South Africa being a democracy? Would you say you have benefitted a lot, a little or not at all? [SA]

34

45

19

2

A lot A little Not at all Don't know / can't say

PERCEIVED PERSONAL BENEFIT TO SA BEING A DEMOCRACY

86

Most are registered voters and prepared to take accountability for reporting community crime; a fair amount – 1 in every 2, are also willing to provide additional personal time or finances – i.e. to take active part in committees or forums, or to pay more taxes for infrastructure upkeep

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q31. Please indicate whether you agree or disagree with each of the following statements? [SA per statement]

50

85 88

49

50

15 12

51

You are part of a communityforum/church committee/local

sports committee

You are a registered voter You believe that it is yourresponsibility to work with theauthorities in making efforts tocombat crime by ensuring you

report the crimes in yourcommunity

You are willing to pay more taxesto contribute to the

infrastructure upkeep in SouthAfrica

Agree Disagree

TAKING PART IN ACTIVITIES / ACTIONS

87

Pride Index (PI) Citizens show a strong devotion to their country – with the majority of citizens displaying the same affection

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 *Low base

PRIDE INDEX

80

1% 7% 34% 58%

Very weak (0-20) Weak (27-40) Moderate (47-53) Good (60-73) Strong (80-100)

0 32 53 72 89

PRIDE INDEX

88

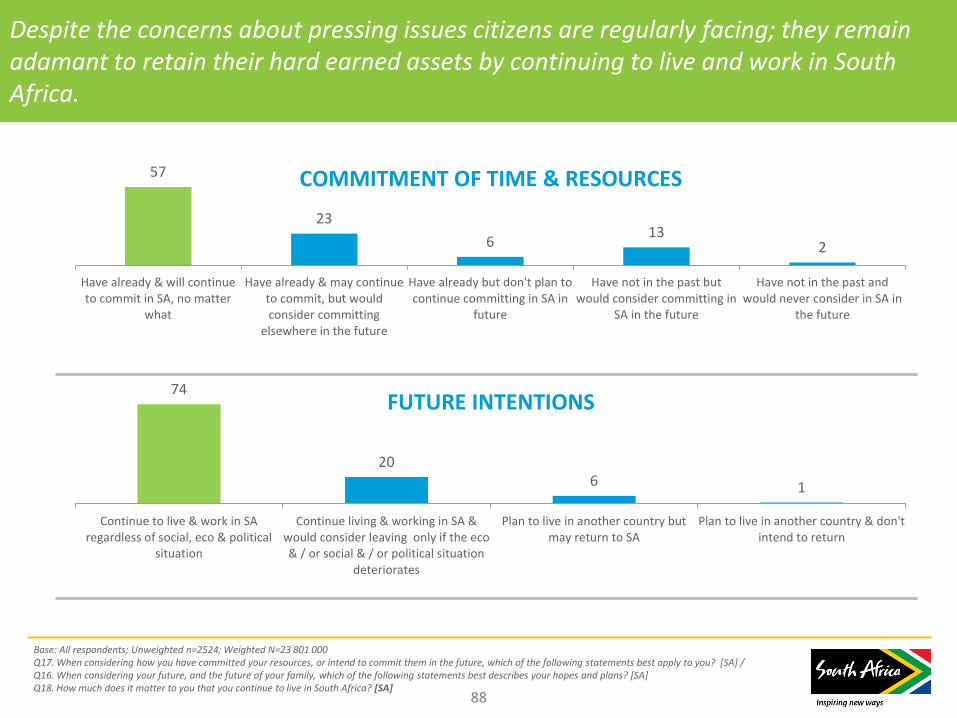

Despite the concerns about pressing issues citizens are regularly facing; they remain adamant to retain their hard earned assets by continuing to live and work in South Africa.

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q17. When considering how you have committed your resources, or intend to commit them in the future, which of the following statements best apply to you? [SA] / Q16. When considering your future, and the future of your family, which of the following statements best describes your hopes and plans? [SA] Q18. How much does it matter to you that you continue to live in South Africa? [SA]

57

23

6 13

2

Have already & will continueto commit in SA, no matter

what

Have already & may continueto commit, but wouldconsider committing

elsewhere in the future

Have already but don't plan tocontinue committing in SA in

future

Have not in the past butwould consider committing in

SA in the future

Have not in the past andwould never consider in SA in

the future

COMMITMENT OF TIME & RESOURCES

74

20 6 1

Continue to live & work in SAregardless of social, eco & political

situation

Continue living & working in SA &would consider leaving only if the eco& / or social & / or political situation

deteriorates

Plan to live in another country butmay return to SA

Plan to live in another country & don'tintend to return

FUTURE INTENTIONS

89

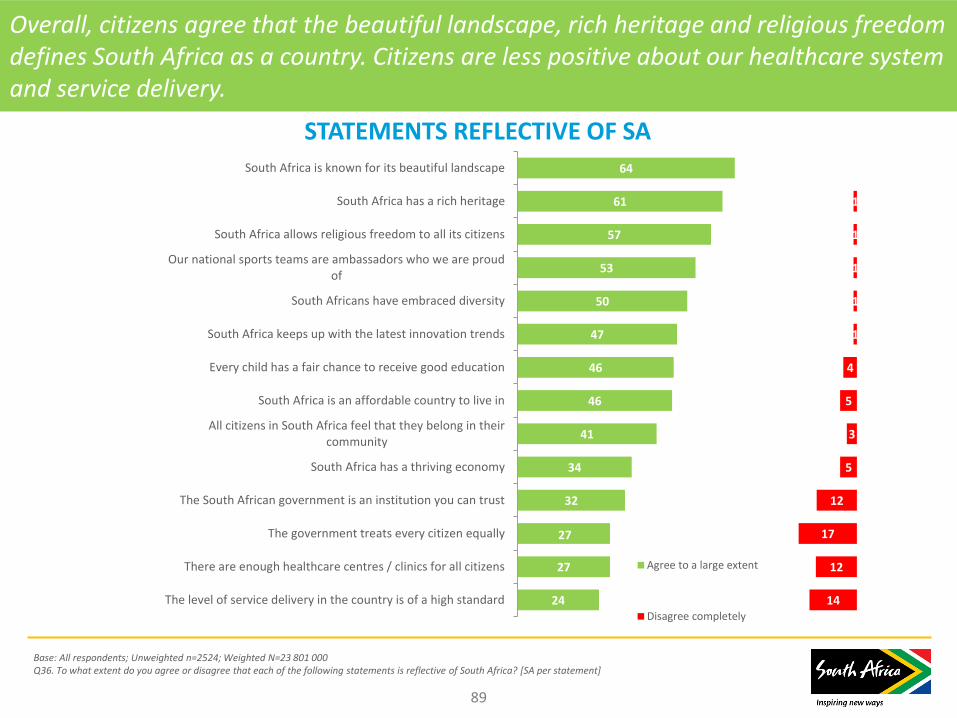

Overall, citizens agree that the beautiful landscape, rich heritage and religious freedom defines South Africa as a country. Citizens are less positive about our healthcare system and service delivery.

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q36. To what extent do you agree or disagree that each of the following statements is reflective of South Africa? [SA per statement]

STATEMENTS REFLECTIVE OF SA 64

61

57

53

50

47

46

46

41

34

32

27

27

24

28

31

33

35

38

38

35

34

38

40

31

28

33

31

6

6

7

9

8

10

9

9

11

14

13

12

11

13

2

2

2

3

3

4

6

7

7

8

13

15

16

18

1

1

1

1

1

4

5

3

5

12

17

12

14

South Africa is known for its beautiful landscape

South Africa has a rich heritage

South Africa allows religious freedom to all its citizens

Our national sports teams are ambassadors who we are proudof

South Africans have embraced diversity

South Africa keeps up with the latest innovation trends

Every child has a fair chance to receive good education

South Africa is an affordable country to live in

All citizens in South Africa feel that they belong in theircommunity

South Africa has a thriving economy

The South African government is an institution you can trust

The government treats every citizen equally

There are enough healthcare centres / clinics for all citizens

The level of service delivery in the country is of a high standard

Agree to a large extentAgree to some extentNeither agree nor disagreeDisagree to some extentDisagree completely

90

Almost two thirds of South African citizens claim that they are extremely proud to be South African

Base: All respondents; Unweighted n=2524; Weighted N=23 801 000 Q37. Using this scale from 1 to 5, where 1 is “Very proud to be South African” and 5 is “Not at all proud to be South African” , are you: [SA] / Q38. ASKED IF PROUD IN Q37: What makes you most proud to be South African, or about South Africa? / Q39. ASKED IF NEUTRAL OR NOT PROUD IN Q37: What is it about South Africa that makes you feel that way?

61%

35%

2% 1%

1%

Extremely proud to be South African

Somewhat proud to be South African

No feelings either way

Not very proud to be South African

Not at all proud to be South African

LEVEL OF PRIDE TO BE A SA CITIZEN

TOP 4 - FACTORS DRIVING PRIDE

%

1 The beautiful landscape 56

2 The cultural diversity 49

3 The people in general 49

4 Achievements of our democracy 41

TOP 3 - FACTORS DETRACTING FROM PRIDE

%

1 The Government is corrupt 27

2 Too much crime and thugs 26

3 Lack of job opportunities 17

Prepared by Brand SA Research

Contact:

Dr Petrus de Kock, GM – Research

Dr Judy Smith-Höhn, Research

Manager

Readers are welcome to use the data

contained in this report for their own

purposes provided they acknowledge

the source as: Brand South Africa,

Research & Nation Brand Performance

Presentation, September 2015,

available at:

www.brandsouthafrica.com

91