BP second quarter 2016 results presentation slides

32

Cherry Point refinery, Washington 2Q 2016 Results 26 July 2016

-

Upload

bp -

Category

Economy & Finance

-

view

154 -

download

0

Transcript of BP second quarter 2016 results presentation slides

Cherry Point refinery, Washington

2Q 2016 Results

26 July 2016

ATA fabrication yard, Azerbaijan

Jess Mitchell

Head of Group Investor Relations

Cautionary statement

Forward-looking statements - cautionary statement

In order to utilize the ‘safe harbor’ provisions of the United States Private Securities Litigation Reform Act of 1995 (the ‘PSLRA’), BP is providing the following cautionary statement. This

presentation and the associated slides and discussion contain forward-looking statements – that is, statements related to future, not past events – with respect to the financial condition, results of

operations and business of BP and certain of the expectations, intentions, plans and objectives of BP with respect to these items, in particular statements regarding BP’s medium-term goal of

balancing organic sources and uses of cash by 2017 at $50–55/bbl; expectations regarding future oil and gas prices and market trends, including volatility and levelling out of supply; expectations

regarding BP’s growth in the near term and to 2030, including future construction and the timing thereof and future production levels and capacity; plans and expectations regarding BP’s goal of

growing sustainable free cash flow and distributions; BP’s plans and expectations regarding the sanctioning of future projects; expectations regarding BP’s share of Rosneft’s production and net

income and the amount of dividend payable by Rosneft to BP and BP’s organic capital expenditures and cash cost savings through 2017; expectations with respect to the total amounts that will

ultimately be paid by BP in relation to the Gulf of Mexico incident and the timing thereof; plans and expectations regarding Upstream growth to 2030, including increasing capacity, production and

contribution to free cash flow; plans and expectations regarding Downstream contribution to free cash flow and refining margins and growth opportunities; expectations regarding Upstream third-

quarter 2016 reported production, Downstream third-quarter 2016 turnaround activity and Other business and corporate 2016 quarterly charges; expectations regarding rebalancing of sources and

uses of cash including the effect of rebalancing on free cash flow, cash flows expected from Upstream project start-ups and from Downstream and expectations regarding future investment and

distributions to shareholders; expectations regarding the value of divestments in 2016 and thereafter, non-operating restructuring charges in 2016 and the impact on cash flow through 2017,

Upstream activities in Indonesia, Egypt and the Gulf of Mexico and Upstream base decline and production costs; and expectations regarding Downstream cost efficiencies, performance

improvement, programmes and headcount reduction and expectations regarding the fuels marketing and lubricants businesses. By their nature, forward-looking statements involve risk and

uncertainty because they relate to events and depend on circumstances that will or may occur in the future and are outside the control of BP. Actual results may differ materially from those

expressed in such statements, depending on a variety of factors, including: the specific factors identified in the discussions accompanying such forward-looking statements; the receipt of relevant

third party and/or regulatory approvals; the timing and level of maintenance and/or turnaround activity; the timing and volume of refinery additions and outages; the timing of bringing new fields

onstream; the timing, quantum and nature of certain divestments; future levels of industry product supply, demand and pricing, including supply growth in North America; OPEC quota restrictions;

PSA effects; operational and safety problems; potential lapses in product quality; economic and financial market conditions generally or in various countries and regions; political stability and

economic growth in relevant areas of the world; changes in laws and governmental regulations; regulatory or legal actions including the types of enforcement action pursued and the nature of

remedies sought or imposed; the actions of prosecutors, regulatory authorities and courts; exchange rate fluctuations; development and use of new technology; recruitment and retention of a

skilled workforce; the success or otherwise of partnering; the actions of competitors, trading partners, contractors, subcontractors, creditors, rating agencies and others; our access to future credit

resources; business disruption and crisis management; the impact on our reputation of ethical misconduct and non-compliance with regulatory obligations; trading losses; major uninsured losses;

decisions by Rosneft’s management and board of directors; the actions of contractors; natural disasters and adverse weather conditions; changes in public expectations and other changes to

business conditions; wars and acts of terrorism; cyber-attacks or sabotage; and other factors discussed under “Risk factors” in BP Annual Report and Form 20-F 2015 as filed with the US

Securities and Exchange Commission.

This document contains references to non-proved resources and production outlooks based on non-proved resources that the SEC's rules prohibit us from including in our filings with the SEC. U.S.

investors are urged to consider closely the disclosures in our Form 20-F, SEC File No. 1-06262. This form is available on our website at www.bp.com. You can also obtain this form from the SEC

by calling 1-800-SEC-0330 or by logging on to their website at www.sec.gov

Reconciliations to GAAP - This presentation also contains financial information which is not presented in accordance with generally accepted accounting principles (GAAP). A quantitative

reconciliation of this information to the most directly comparable financial measure calculated and presented in accordance with GAAP can be found on our website at www.bp.com.

Tables and projections in this presentation are BP projections unless otherwise stated.

July 2016

Deepsea Aberdeen drilling rig, North Sea

Bob Dudley

Group Chief Executive

5

Agenda

Environment

Overview

2Q 2016 results

Financial frame

Business update

Q&A

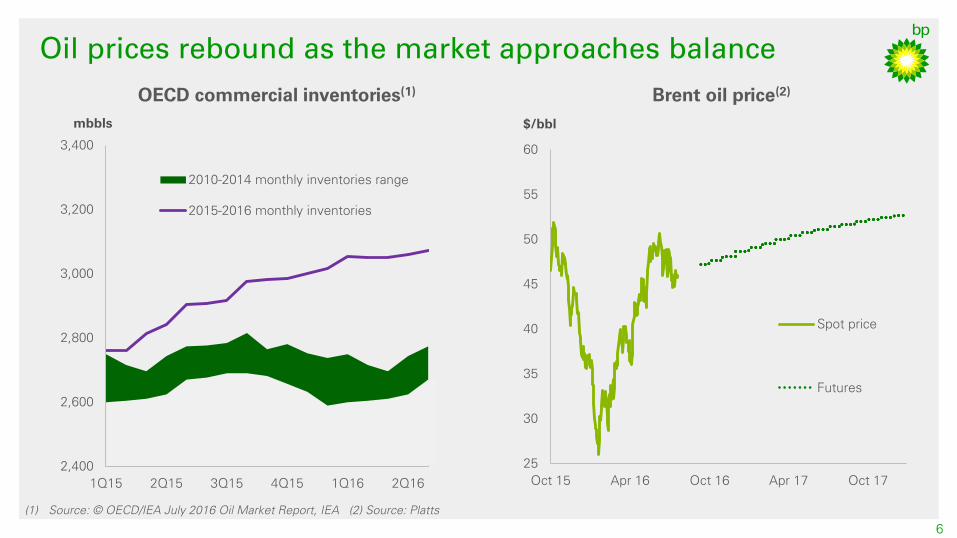

25

30

35

40

45

50

55

60

Oct 15 Apr 16 Oct 16 Apr 17 Oct 17

Spot price

Futures

Oil prices rebound as the market approaches balance

$/bbl

OECD commercial inventories(1)

(1) Source: © OECD/IEA July 2016 Oil Market Report, IEA (2) Source: Platts

Brent oil price(2)

6

mbbls

2,400

2,600

2,800

3,000

3,200

3,400

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

2010-2014 monthly inventories range

2015-2016 monthly inventories

7

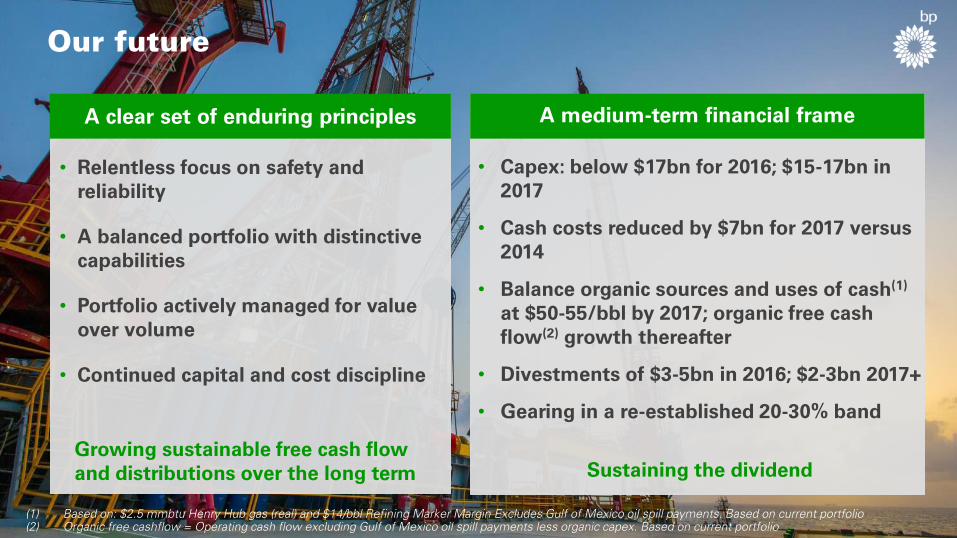

• Relentless focus on safety and reliability

• A balanced portfolio with distinctive capabilities

• Portfolio actively managed for value over volume

• Continued capital and cost discipline

• Growing sustainable free cash flow and distributions

over the long term

Sustainable value growth

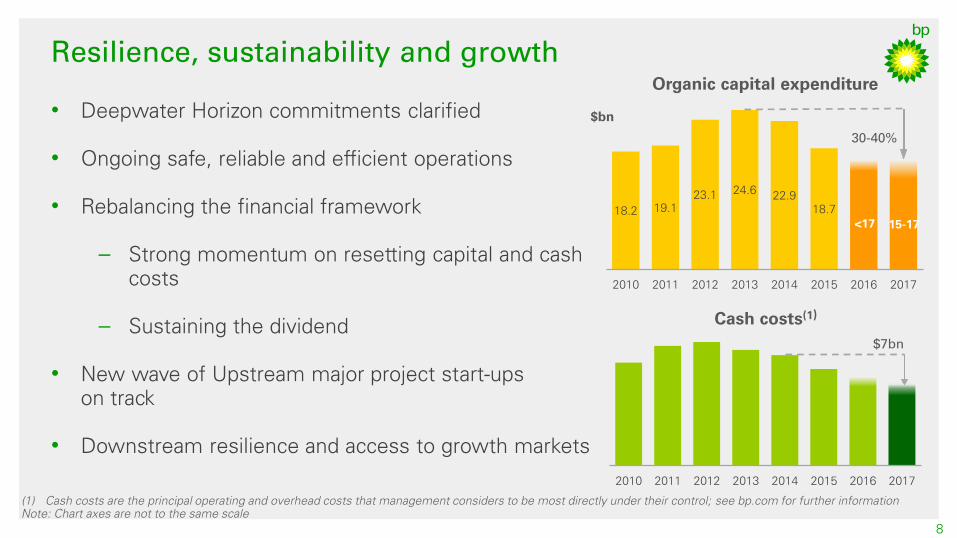

• Deepwater Horizon commitments clarified

• Ongoing safe, reliable and efficient operations

• Rebalancing the financial framework

– Strong momentum on resetting capital and cash

costs

– Sustaining the dividend

• New wave of Upstream major project start-ups

on track

• Downstream resilience and access to growth markets

18.2 19.1

23.1 24.6

22.9

18.7

2010 2011 2012 2013 2014 2015 2016 2017

Organic capital expenditure

$bn

15-17 <17

Resilience, sustainability and growth

8

30-40%

2010 2011 2012 2013 2014 2015 2016 2017

Cash costs(1)

$7bn

(1) Cash costs are the principal operating and overhead costs that management considers to be most directly under their control; see bp.com for further information

Note: Chart axes are not to the same scale

Brian Gilvary

Chief Financial Officer

Whiting refinery, Indiana

8

9

10

11

12

13

14

15

16

17

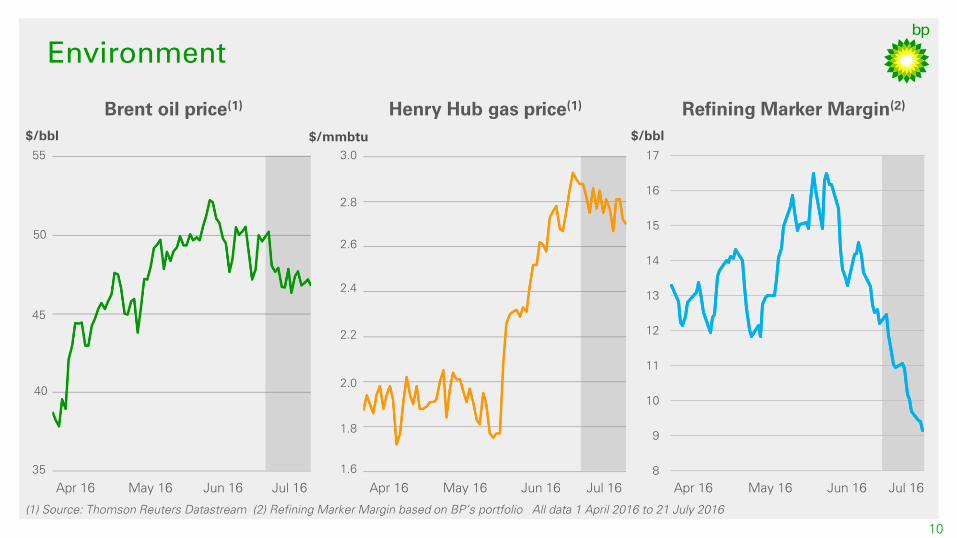

Environment

Brent oil price(1)

Henry Hub gas price(1)

Refining Marker Margin(2)

(1) Source: Thomson Reuters Datastream (2) Refining Marker Margin based on BP’s portfolio All data 1 April 2016 to 21 July 2016

10

Apr 16 May 16 Jun 16

$/bbl

Apr 16 May 16 Jun 16

40

45

50

35

Apr 16 May 16 Jun 16

2.6

2.2

2.0

1.8

1.6

2.4

$/mmbtu

55

$/bbl

2.8

3.0

Jul 16 Jul 16 Jul 16

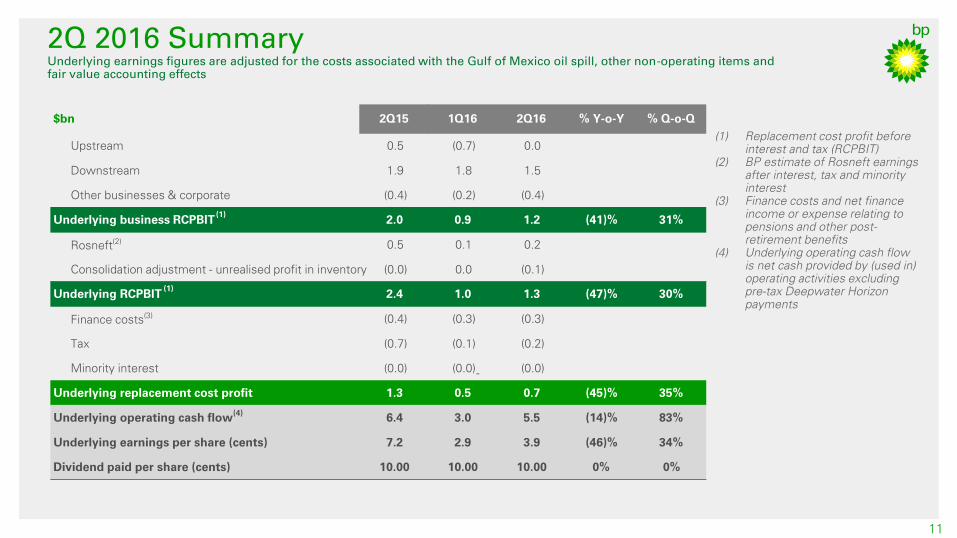

2Q 2016 Summary Underlying earnings figures are adjusted for the costs associated with the Gulf of Mexico oil spill, other non-operating items and

fair value accounting effects

11

(1) Replacement cost profit before

interest and tax (RCPBIT)

(2) BP estimate of Rosneft earnings

after interest, tax and minority

interest

(3) Finance costs and net finance

income or expense relating to

pensions and other post-

retirement benefits

(4) Underlying operating cash flow

is net cash provided by (used in)

operating activities excluding

pre-tax Deepwater Horizon

payments

-

$bn 2Q15 1Q16 2Q16 % Y-o-Y % Q-o-Q

Upstream 0.5 (0.7) 0.0

Downstream 1.9 1.8 1.5

Other businesses & corporate (0.4) (0.2) (0.4)

Underlying business RCPBIT (1)

2.0 0.9 1.2 (41)% 31%

Rosneft (2) 0.5 0.1 0.2

Consolidation adjustment - unrealised profit in inventory (0.0) 0.0 (0.1)

Underlying RCPBIT (1)

2.4 1.0 1.3 (47)% 30%

Finance costs (3) (0.4) (0.3) (0.3)

Tax (0.7) (0.1) (0.2)

Minority interest (0.0) (0.0) (0.0)

Underlying replacement cost profit 1.3 0.5 0.7 (45)% 35%

Underlying operating cash flow (4)

6.4 3.0 5.5 (14)% 83%

Underlying earnings per share (cents) 7.2 2.9 3.9 (46)% 34%

Dividend paid per share (cents) 10.00 10.00 10.00 0% 0%

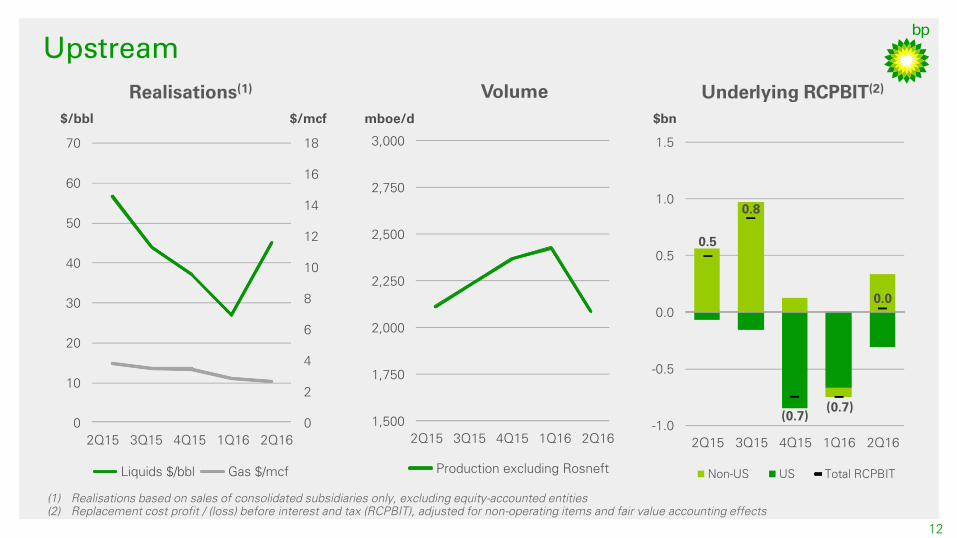

Upstream

12

Realisations(1)

Volume Underlying RCPBIT(2)

(1) Realisations based on sales of consolidated subsidiaries only, excluding equity-accounted entities

(2) Replacement cost profit / (loss) before interest and tax (RCPBIT), adjusted for non-operating items and fair value accounting effects

0

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

70

2Q15 3Q15 4Q15 1Q16 2Q16

$/mcf $/bbl

Liquids $/bbl Gas $/mcf

1,500

1,750

2,000

2,250

2,500

2,750

3,000

2Q15 3Q15 4Q15 1Q16 2Q16

Production excluding Rosneft

mboe/d

0.5

0.8

(0.7) (0.7)

0.0

- 1.0

- 0.5

0.0

0.5

1.0

1.5

2Q15 3Q15 4Q15 1Q16 2Q16

Non - US US Total RCPBIT

$bn

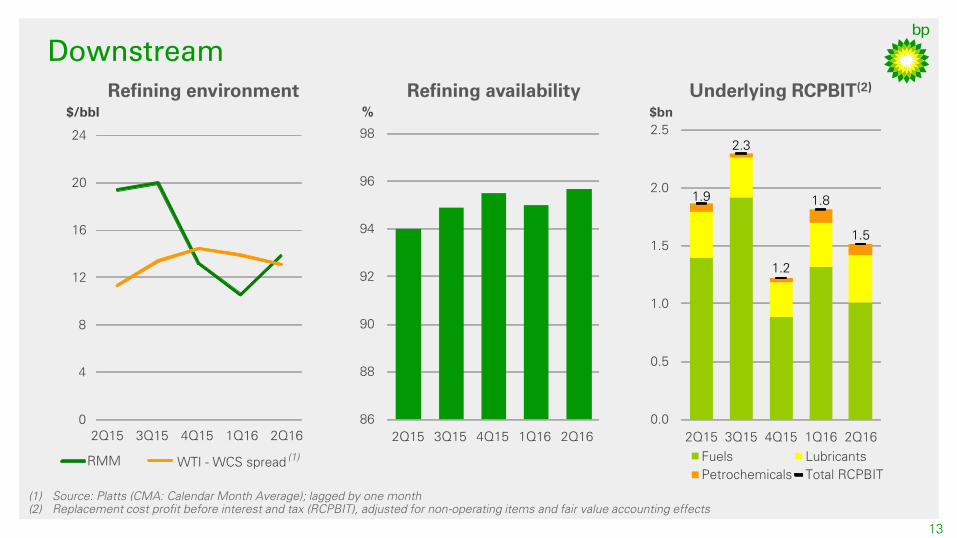

Downstream

13

Refining environment Refining availability Underlying RCPBIT(2)

(1) Source: Platts (CMA: Calendar Month Average); lagged by one month

(2) Replacement cost profit before interest and tax (RCPBIT), adjusted for non-operating items and fair value accounting effects

(1) WTI - WCS spread

0

4

8

12

16

20

24

2Q15 3Q15 4Q15 1Q16 2Q16

$/bbl

RMM

1.9

2.3

1.2

1.8

1.5

0.0

0.5

1.0

1.5

2.0

2.5

2Q15 3Q15 4Q15 1Q16 2Q16

$bn

Fuels Lubricants

Petrochemicals Total RCPBIT

86

88

90

92

94

96

98

2Q15 3Q15 4Q15 1Q16 2Q16

%

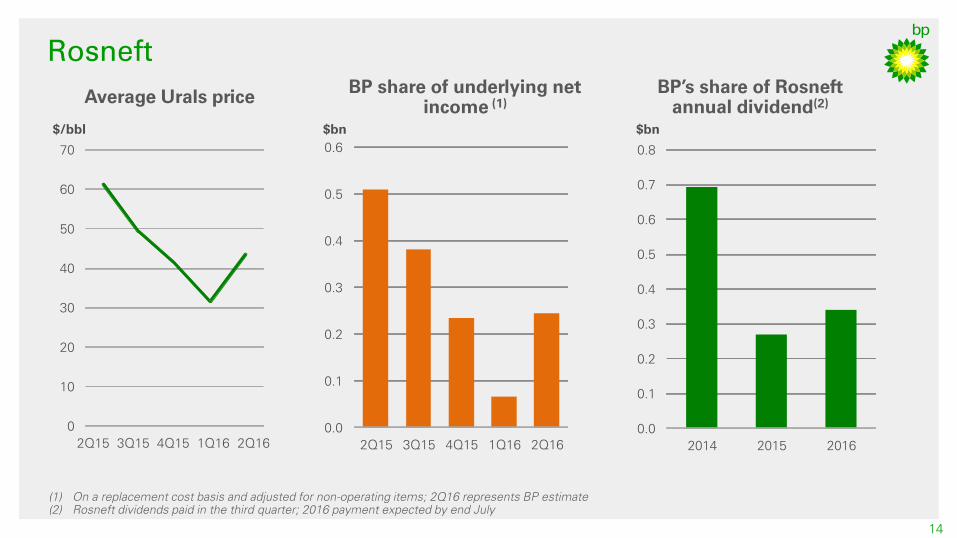

Rosneft

14

Average Urals price BP’s share of Rosneft

annual dividend(2)

BP share of underlying net

income (1)

(1) On a replacement cost basis and adjusted for non-operating items; 2Q16 represents BP estimate

(2) Rosneft dividends paid in the third quarter; 2016 payment expected by end July

0

10

20

30

40

50

60

70

2Q15 3Q15 4Q15 1Q16 2Q16

$/bbl

0.0

0.1

0.2

0.3

0.4

0.5

0.6

2Q15 3Q15 4Q15 1Q16 2Q16

$bn

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2014 2015 2016

$bn

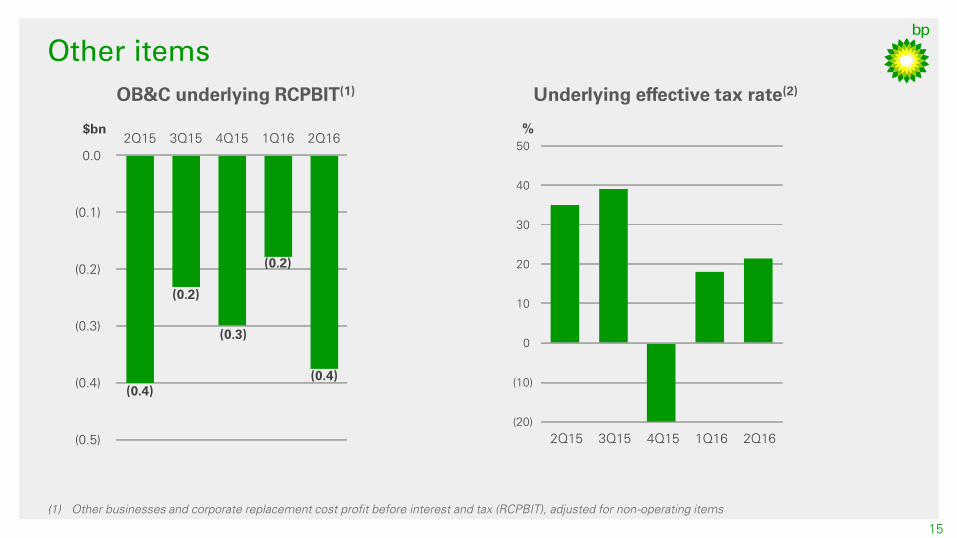

Other items

15

(1) Other businesses and corporate replacement cost profit before interest and tax (RCPBIT), adjusted for non-operating items

OB&C underlying RCPBIT(1)

Underlying effective tax rate(2)

(0.4)

(0.2)

(0.3)

(0.2)

(0.4)

(0.5)

(0.4)

(0.3)

(0.2)

(0.1)

0.0

2Q15 3Q15 4Q15 1Q16 2Q16 $bn

(20)

(10)

0

10

20

30

40

50

2Q15 3Q15 4Q15 1Q16 2Q16

%

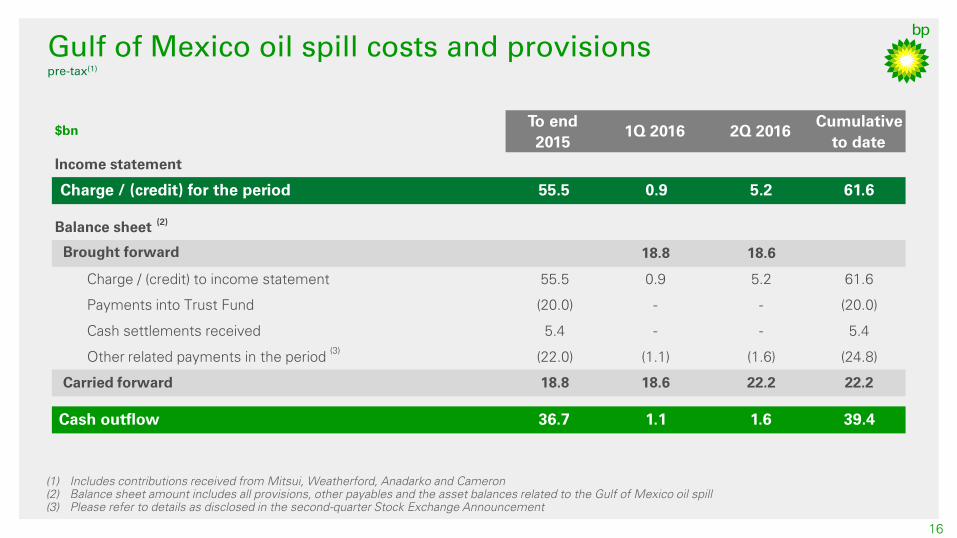

Gulf of Mexico oil spill costs and provisions

pre-tax(1)

16

(1) Includes contributions received from Mitsui, Weatherford, Anadarko and Cameron

(2) Balance sheet amount includes all provisions, other payables and the asset balances related to the Gulf of Mexico oil spill

(3) Please refer to details as disclosed in the second-quarter Stock Exchange Announcement

$bn To end

2015 1Q 2016 2Q 2016

Cumulative

to date

Income statement

Charge / (credit) for the period 55.5 0.9 5.2 61.6

Balance sheet (2)

18.8 18.6

Charge / (credit) to income statement 55.5 0.9 5.2 61.6

Payments into Trust Fund (20.0) - - (20.0)

Cash settlements received 5.4 - - 5.4

Other related payments in the period (3)

(22.0) (1.1) (1.6) (24.8)

Carried forward 18.8 18.6 22.2 22.2

Cash outflow 36.7 1.1 1.6 39.4

Brought forward

Sources and uses of cash

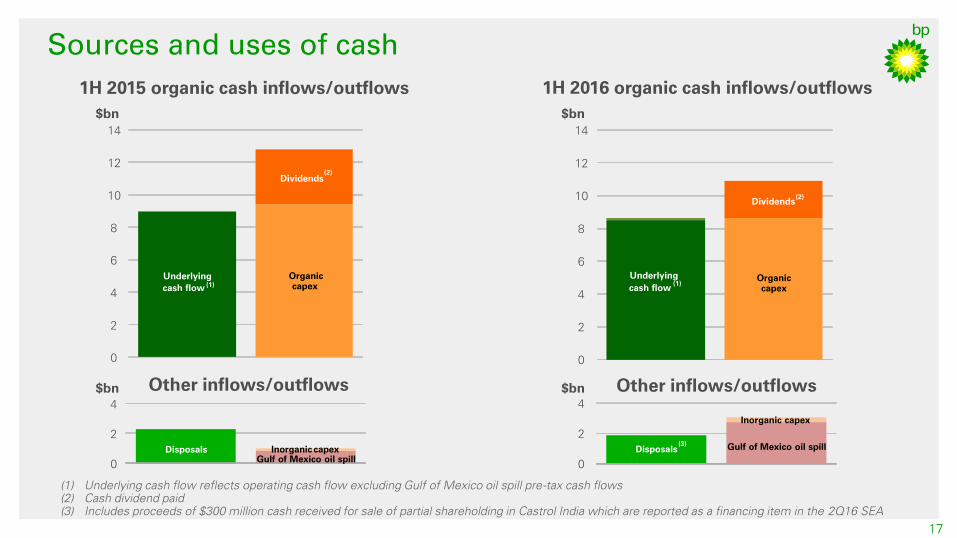

17

1H 2015 organic cash inflows/outflows

1H 2016 organic cash inflows/outflows

(1) Underlying cash flow reflects operating cash flow excluding Gulf of Mexico oil spill pre-tax cash flows

(2) Cash dividend paid

(3) Includes proceeds of $300 million cash received for sale of partial shareholding in Castrol India which are reported as a financing item in the 2Q16 SEA

Other inflows/outflows

Other inflows/outflows

$bn $bn

$bn $bn

Organic capex

Dividends

0

2

4

6

8

10

12

14

Underlying

cash flow (1)

0

2

4

Gulf of Mexico oil spill Disposals Inorganic capex

(2)

Organic capex

Dividends

0

2

4

6

8

10

12

14

Underlying

cash flow (1)

0

2

4

Gulf of Mexico oil spill Disposals

Inorganic capex

(2)

(3)

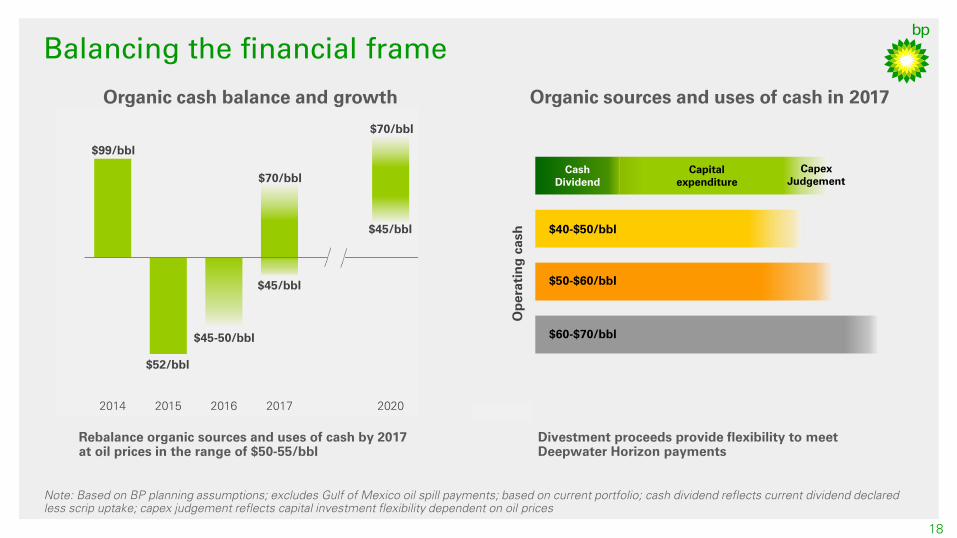

2014 2015 2016 2017 2020

18

Balancing the financial frame

Note: Based on BP planning assumptions; excludes Gulf of Mexico oil spill payments; based on current portfolio; cash dividend reflects current dividend declared

less scrip uptake; capex judgement reflects capital investment flexibility dependent on oil prices

$99/bbl

$52/bbl

$45/bbl

$70/bbl

Organic cash balance and growth Organic sources and uses of cash in 2017

Rebalance organic sources and uses of cash by 2017

at oil prices in the range of $50-55/bbl

Cash

Dividend

Capex

Judgement

Capital

expenditure

0 5 10 15 20 25 30

Op

eratin

g cash

Divestment proceeds provide flexibility to meet

Deepwater Horizon payments

$40-$50/bbl

$50-$60/bbl

$60-$70/bbl

$45/bbl

$70/bbl

$45-50/bbl

0

10

20

30

40

20-30%

10-20%

20-30%

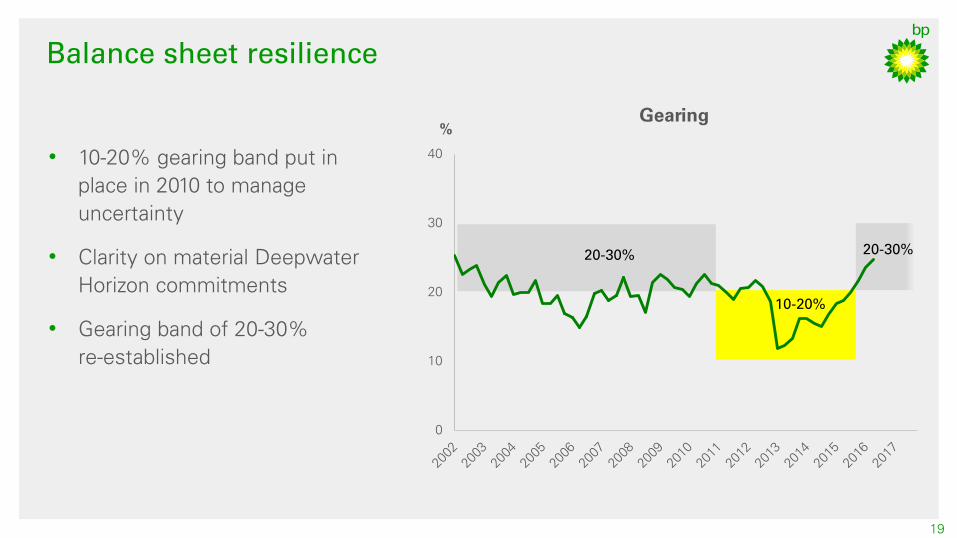

19

Balance sheet resilience

• 10-20% gearing band put in

place in 2010 to manage

uncertainty

• Clarity on material Deepwater

Horizon commitments

• Gearing band of 20-30%

re-established

%

Gearing

Bob Dudley

Group Chief Executive

Ocean Victory drilling rig, Trinidad and Tobago

Upstream key messages from Baku

21

• Safety and reliability – committed to improving year-on-year

• Portfolio – balanced, focused, resilient, creative models

• Capability – world class people, functional model driving

competitiveness

• Efficiency – cost and capital down, top quartile production cost -

more to come

• Growth – imminent, value over volume, $7-8bn free cash flow(1)

in 2020

• Future – 45bn boe, capacity to grow organically, returns focused

(1) Free cash flow proxy = Underlying RCOP+DD&A+EWO-Capex, pre-tax at $50/bbl Brent

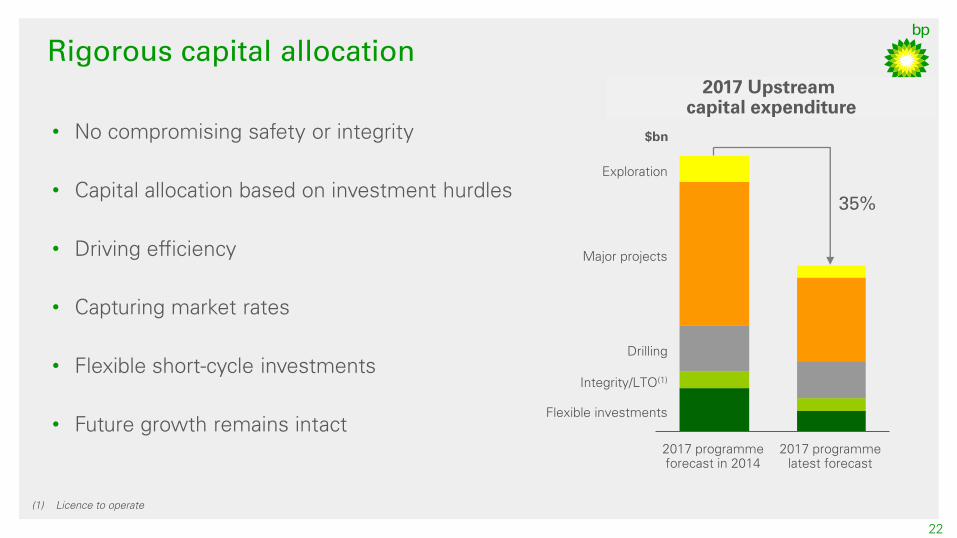

Rigorous capital allocation

22

Integrity/LTO(1)

Drilling

Flexible investments

2017 programme

latest forecast

2017 programme

forecast in 2014

Major projects

Exploration

35%

• No compromising safety or integrity

• Capital allocation based on investment hurdles

• Driving efficiency

• Capturing market rates

• Flexible short-cycle investments

• Future growth remains intact

2017 Upstream

capital expenditure

(1) Licence to operate

$bn

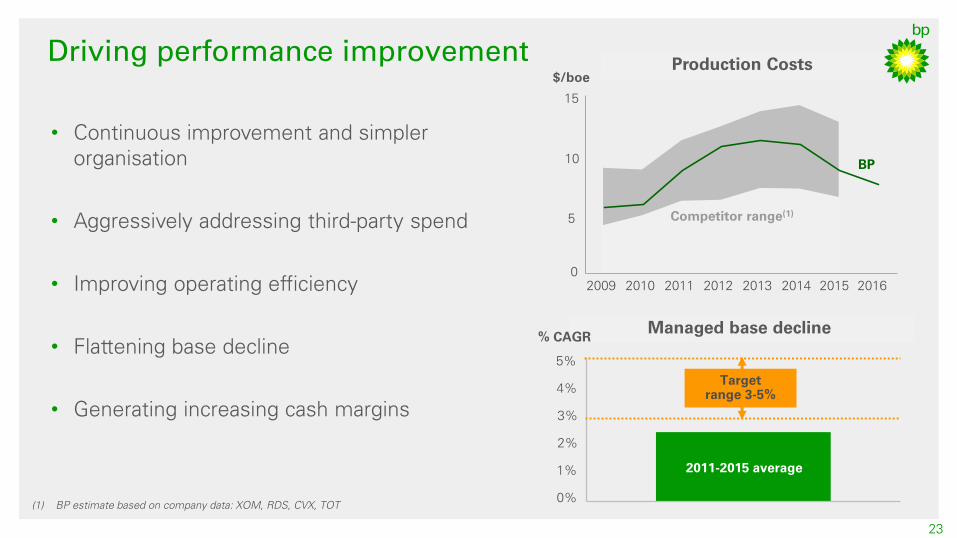

Driving performance improvement

• Continuous improvement and simpler

organisation

• Aggressively addressing third-party spend

• Improving operating efficiency

• Flattening base decline

• Generating increasing cash margins

Competitor range(1)

0

2016 2015 2014 2009 2010 2011 2012 2013

10

15

5

Production Costs

BP

$/boe

5%

4%

3%

2%

1%

0%

2011-2015 average

Managed base decline

Target

range 3-5%

% CAGR

23

(1) BP estimate based on company data: XOM, RDS, CVX, TOT

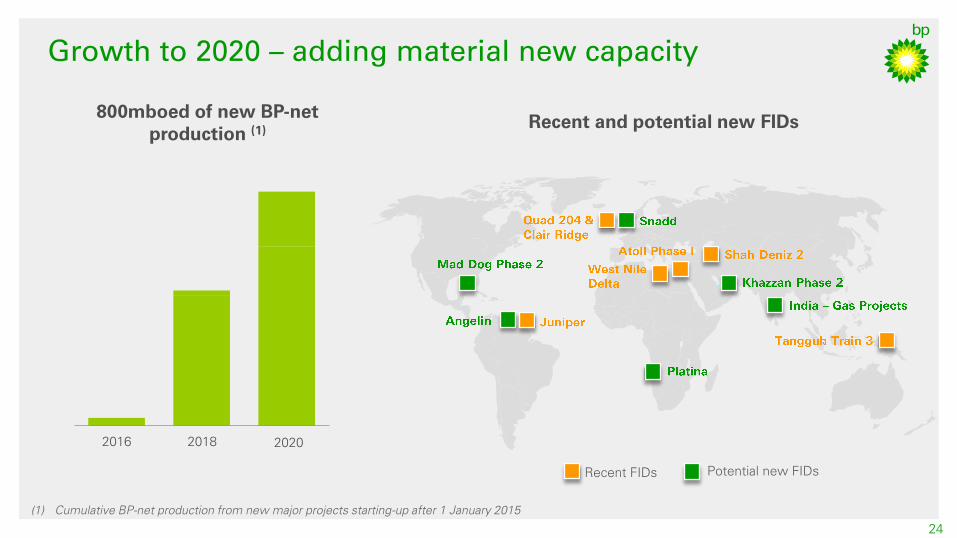

Growth to 2020 – adding material new capacity

24

2020 2018 2016

800mboed of new BP-net

production (1)

Recent and potential new FIDs

Potential new FIDs Recent FIDs

(1) Cumulative BP-net production from new major projects starting-up after 1 January 2015

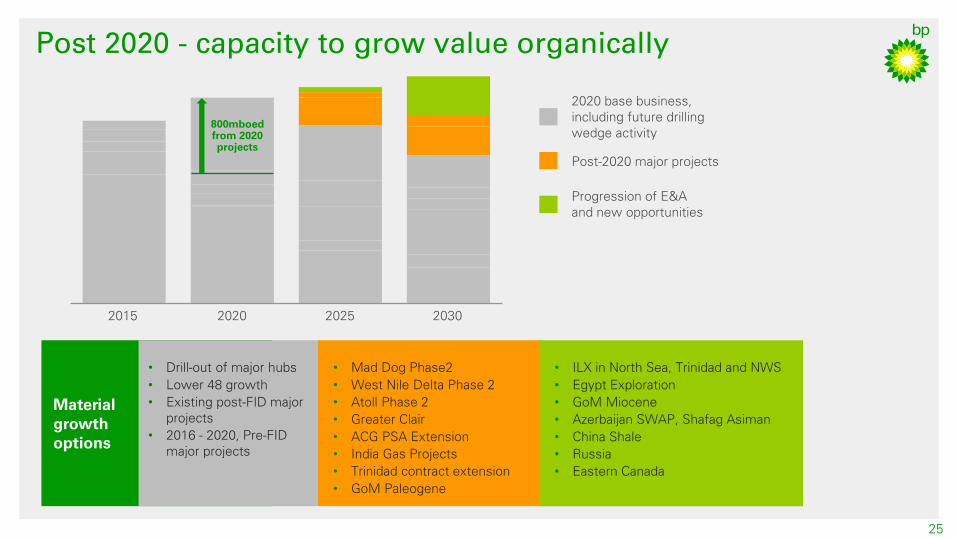

Post 2020 - capacity to grow value organically

25

2020 2030 2025 2015

Progression of E&A

and new opportunities

Post-2020 major projects

2020 base business,

including future drilling

wedge activity

Material

growth

options

• Mad Dog Phase2

• West Nile Delta Phase 2

• Atoll Phase 2

• Greater Clair

• ACG PSA Extension

• India Gas Projects

• Trinidad contract extension

• GoM Paleogene

• Drill-out of major hubs

• Lower 48 growth

• Existing post-FID major

projects

• 2016 - 2020, Pre-FID

major projects

• ILX in North Sea, Trinidad and NWS

• Egypt Exploration

• GoM Miocene

• Azerbaijan SWAP, Shafag Asiman

• China Shale

• Russia

• Eastern Canada

800mboed

from 2020

projects

0

3

6

9

2013 2014 2015 2Q16

$/bbl

Competitor range(3)

0

10

20

2013 2014 2015 2Q16

%

Actual returns

Margin

adjusted(2)

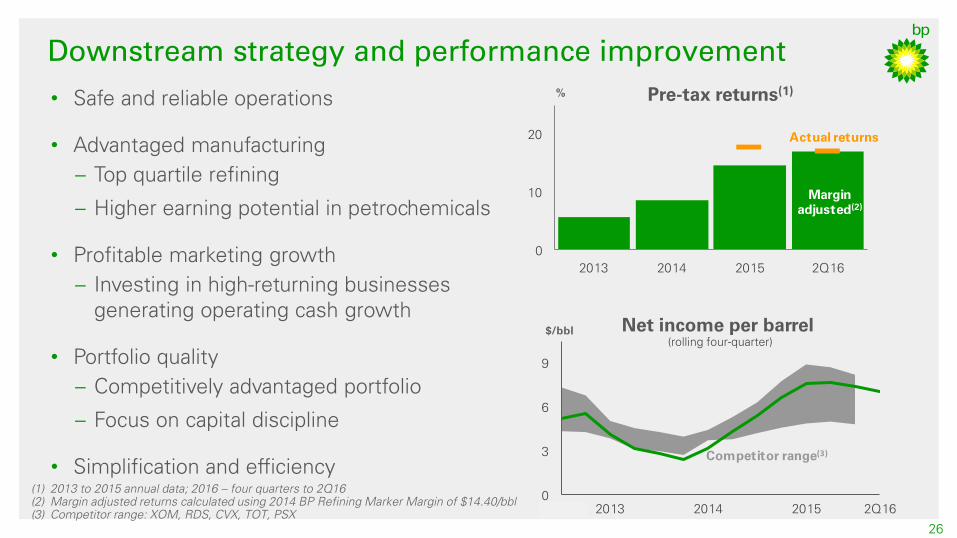

Downstream strategy and performance improvement

26

Net income per barrel

(rolling four-quarter)

(1) 2013 to 2015 annual data; 2016 – four quarters to 2Q16

(2) Margin adjusted returns calculated using 2014 BP Refining Marker Margin of $14.40/bbl

(3) Competitor range: XOM, RDS, CVX, TOT, PSX

• Safe and reliable operations

• Advantaged manufacturing

– Top quartile refining

– Higher earning potential in petrochemicals

• Profitable marketing growth

– Investing in high-returning businesses

generating operating cash growth

• Portfolio quality

– Competitively advantaged portfolio

– Focus on capital discipline

• Simplification and efficiency

Pre-tax returns(1)

10

15

20

25

Rolling four quarters

RMM required to generate

15% pre-tax returns

2014 2015

2011 - 2015

RMM range

RMM

$/bbl

10

15

20

25

0

4

8

2014 Four quarters

to 2Q16

RMM

RMM(1)

$/bbl

Pre-tax

earnings

$bn

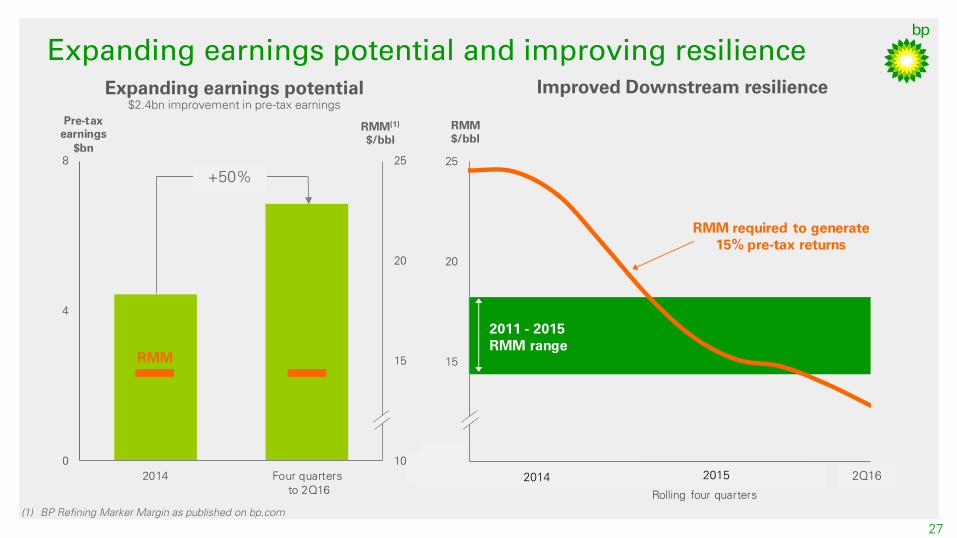

Expanding earnings potential and improving resilience

27

Improved Downstream resilience

(1) BP Refining Marker Margin as published on bp.com

Expanding earnings potential

$2.4bn improvement in pre-tax earnings

2014 2015 2Q16

+50%

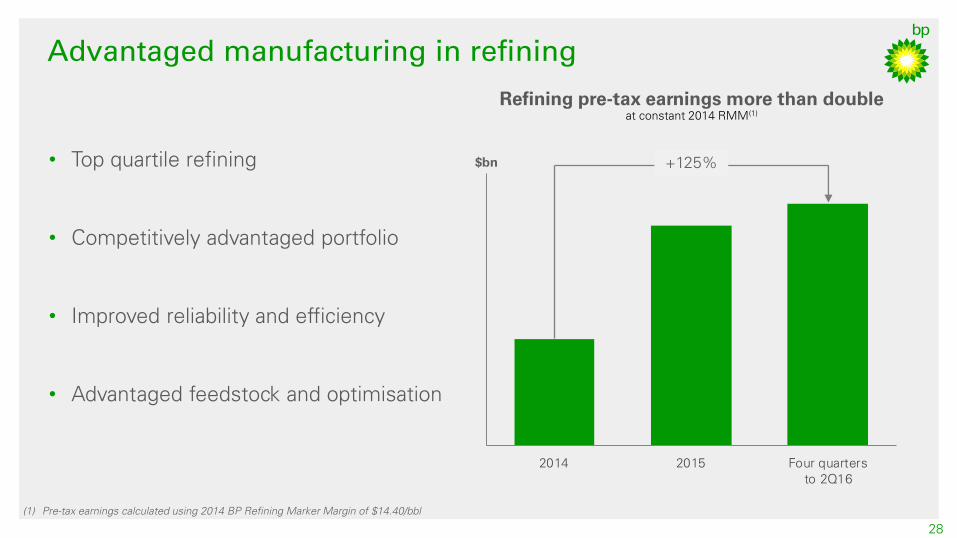

Advantaged manufacturing in refining

28

• Top quartile refining

• Competitively advantaged portfolio

• Improved reliability and efficiency

• Advantaged feedstock and optimisation

(1) Pre-tax earnings calculated using 2014 BP Refining Marker Margin of $14.40/bbl

Refining pre-tax earnings more than double

at constant 2014 RMM(1)

2014 2015 Four quarters

to 2Q16

$bn +125%

0

1

2

2013 2014 2015 Four quarters

to 2Q16

Lubricants

Pre-tax

earnings

$bn

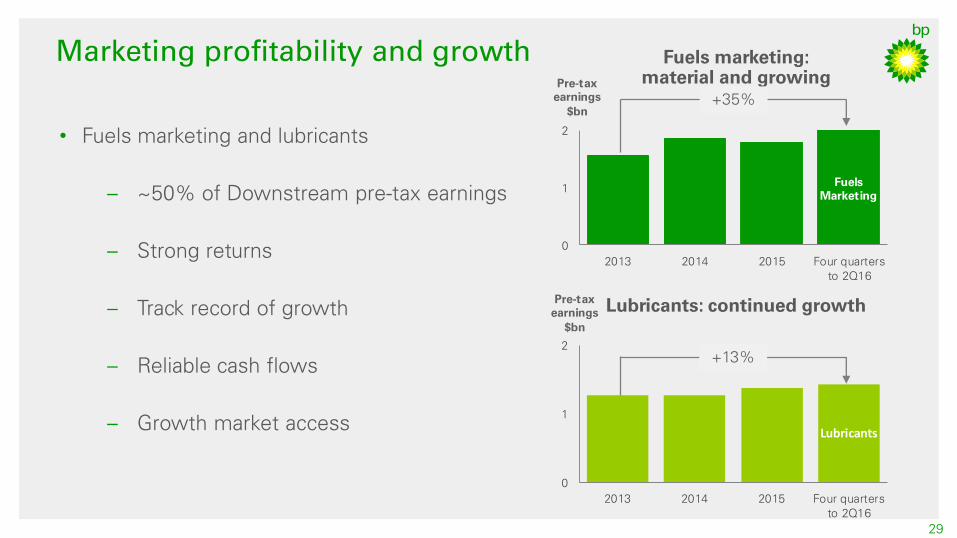

Marketing profitability and growth

29

(1) Primarily markets excluding North America and Western Europe

(2) Pre tax underlying replacement cost profit re-stated to constant foreign exchange rates

• Fuels marketing and lubricants

– ~50% of Downstream pre-tax earnings

– Strong returns

– Track record of growth

– Reliable cash flows

– Growth market access

Fuels marketing:

material and growing

Lubricants: continued growth

0

1

2

2013 2014 2015 Four quarters

to 2Q16

Fuels

Marketing

Pre-tax

earnings

$bn

+35%

+13%

0

10

20

30

40

2014 2015 2Q16 2017

'000

Employees

Agency

2014 2015 2016

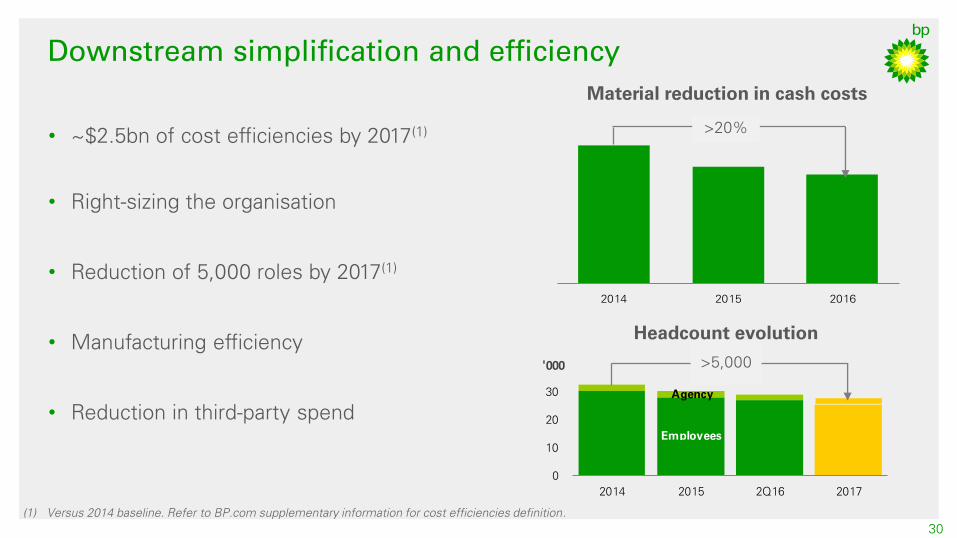

Downstream simplification and efficiency

30

• ~$2.5bn of cost efficiencies by 2017(1)

• Right-sizing the organisation

• Reduction of 5,000 roles by 2017(1)

• Manufacturing efficiency

• Reduction in third-party spend

(1) Versus 2014 baseline. Refer to BP.com supplementary information for cost efficiencies definition.

Material reduction in cash costs

>20%

Headcount evolution

>5,000

• Relentless focus on safety and

reliability

• A balanced portfolio with distinctive

capabilities

• Portfolio actively managed for value

over volume

• Continued capital and cost discipline

Growing sustainable free cash flow

and distributions over the long term

• Capex: below $17bn for 2016; $15-17bn in

2017

• Cash costs reduced by $7bn for 2017 versus

2014

• Balance organic sources and uses of cash(1)

at $50-55/bbl by 2017; organic free cash

flow(2)

growth thereafter

• Divestments of $3-5bn in 2016; $2-3bn 2017+

• Gearing in a re-established 20-30% band

Sustaining the dividend

Our future

A clear set of enduring principles A medium-term financial frame

(1) Based on: $2.5 mmbtu Henry Hub gas (real) and $14/bbl Refining Marker Margin Excludes Gulf of Mexico oil spill payments. Based on current portfolio

(2) Organic free cashflow = Operating cash flow excluding Gulf of Mexico oil spill payments less organic capex. Based on current portfolio

Q&A

32

Tufan Erginbilgic

Chief Executive, Downstream

Jess Mitchell

Head of Group Investor Relations

Bob Dudley

Group Chief Executive

Bernard Looney

Chief Executive, Upstream