Bookkeeping Foundations The art of using simple reporting so YOU know the source and solution of...

23

-

date post

19-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Bookkeeping Foundations The art of using simple reporting so YOU know the source and solution of...

Bookkeeping Bookkeeping FoundationsFoundations

The art of using simple reporting so YOU know The art of using simple reporting so YOU know the source and solution of EVERY challenge in the source and solution of EVERY challenge in your business …EVERY TIME!your business …EVERY TIME!

Tony McAliece& Associates

Personal, Business & Executive CoachingLeadership & Team Training

Team Services DirectorFirst Class Accounts (Central Victoria)

Email : [email protected] Mobile : 0409701055

Tony McAliece& Associates

Personal, Business & Executive CoachingLeadership & Team Training

Team Services DirectorFirst Class Accounts (Central Victoria)

Email : [email protected] Mobile : 0409701055

Why do MOST businesses look like Why do MOST businesses look like this?this?

…because owners think that knowing the Technical work of the business is the same as knowing how to manage a

business that does that Technical Work!

80% of small businesses FAIL because they fail to manage their profits and cash flow.

MarketingMarketingMarketing

Operations

MarketingMarketing

Operations

FinancialsFinancials

Operations

FinancialsFinancials

Operations

1. Lack of Money The business doesn’t generate the turnover & profits the business owner desires or believes possible from their business.

2. Lack of Time The owner works too many hours in the business therefore missing out on time with family & friends and developing interests outside the business.

3. Lack of Information The information necessary to properly manage the business is either not captured or not able to be utilized/found when and where required.

The 3 most common frustrations The 3 most common frustrations of business owners…of business owners…

Your SINGLE solution!Your SINGLE solution!Better Financial reporting Better Financial reporting

and and understandingunderstanding of of those reports. those reports.

It’s It’s YOURYOUR responsibility… responsibility… not YOUR Accountant’s!not YOUR Accountant’s!

““The typical financials provided to most business The typical financials provided to most business owners are for TAX purposes rather than management owners are for TAX purposes rather than management

use”…use”… Sue Hirst, My Business Magazine Sue Hirst, My Business Magazine (July 2007)(July 2007)

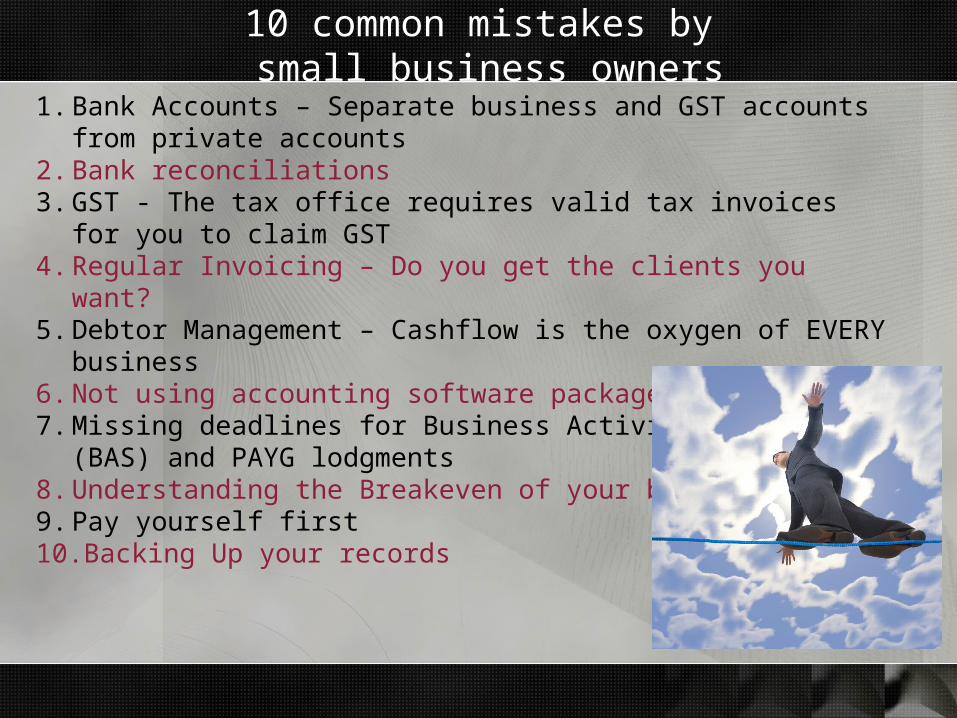

10 common mistakes by small business owners

1. Bank Accounts – Separate business and GST accounts from private accounts

2. Bank reconciliations3. GST - The tax office requires valid tax invoices for you to claim GST4. Regular Invoicing – Do you get the clients you want?5. Debtor Management – Cashflow is the oxygen of EVERY business6. Not using accounting software packages correctly7. Missing deadlines for Business Activity Statement (BAS) and PAYG

lodgments 8. Understanding the Breakeven of your business9. Pay yourself first10.Backing Up your records

How good bookkeeping can benefit your business

You enjoy real benefits:o Be free to concentrate on income-generating

activities o Improve your cashflow with efficient billing

and debt collection o Know the financial position of the business

each day o Have the financial management information

necessary to make informed decisions o Have the information your accountant

needs to accurately advise you ono Your banker will have accurate

information from which they can examine your performance

What bookkeeping systemdo I use?

There are a number of options available which include

o A manual system using spreadsheet and the ‘shoebox’ system

o Accounting software such as MYOB or Quickbooks

o Employing a bookkeeper to produce accounts and provide financial reports to effectively run the business.

o Using your Accountant.

First Class Services

o Set up of bookkeeping and office systems.o Training & support in MYOB & QuickBooks.o Regular weekly, monthly or quarterly bookkeeping

maintenance services.o Regular management reporting and analysis.o Regular management of cash flow.o Regular debt management.o Bank reconciliations.o Payroll & PAYG.o BAS/GST.o Preparation of Books for Accountant.

EQUITYOwners’ $$ to fund the start-up and buy assets

ASSETSThings bought so the business can run- Current (cash, stock, debtors)- Non-current (land, buildings, plant, equipment)

LIABILITIESOwners’ $$ that help fund the business and buy assets- Current (overdraft, creditors)- Non current (loans, debt)

SALES- PURCHASES/C.O.G.S.= GROSS PROFIT- OPERATING EXPENSES= NET PROFIT

Retained earnings, dividends to owners

Buy more assets

Repay loans, pay tax

THE BALANCE SHEET

CASH FLOW CYCLE

GET PAID(cash, accounts)

CASH(working capital)

BUY STOCK(C.O.G.S., purchases, inventory)ADD VALUE

(people, processes)

SELL(products, services)

PROFIT AND LOSS

What to get from your Balance SheetWhat to get from your Balance Sheet

o Debtor level & average collection daysDebtor level & average collection days o monitor amount and AGE of debt & days vs revenue growth.monitor amount and AGE of debt & days vs revenue growth.o install a consistent DEBTOR process & responsible person.install a consistent DEBTOR process & responsible person.o apply split pricing principles for A,B,C & D grade clientsapply split pricing principles for A,B,C & D grade clientso give incentives for early payments including ‘upgrading’give incentives for early payments including ‘upgrading’

o Creditor level & average payment daysCreditor level & average payment dayso monitor amount and maintain maximum payment terms.monitor amount and maintain maximum payment terms.o run payments to a system and negotiate increased terms.run payments to a system and negotiate increased terms.

o Stock turn & Inventory daysStock turn & Inventory dayso Know and apply the 80/20 rule of stock. More 80s, less 20sKnow and apply the 80/20 rule of stock. More 80s, less 20so Reduce/eliminate underperformers. Reduce/eliminate underperformers.

o Work In Progress (service based business)Work In Progress (service based business) o Invoice consistently and set WIP limitsInvoice consistently and set WIP limits

The Cash GapThe Cash Gap

The COST of CASH GAPThe COST of CASH GAPCash Gap Calculator

Average monthly debtors $ 50,000

Credit sales $400,000

Average monthly creditors $ 25,000

Total purchases $300,000

Average Inventory Days 30.0 Days

Collection Period 45.6 Days

Payment Period 30.4 Days

Cash Gap 45.2 Days

Interest rate on overdraft 9%

Cost of Cash Gap $ 4,459

Cash Gap Strategies Cash Gap Strategies (Shorten your Cash Gap)(Shorten your Cash Gap)

o Partial or full deposit to be paid up frontPartial or full deposit to be paid up fronto Finish projects so that they can be billed/invoicedFinish projects so that they can be billed/invoicedo Bill/invoice immediately on completion of jobBill/invoice immediately on completion of jobo Systematize billing/invoicing processSystematize billing/invoicing processo Complete the billing/invoicing process on a weekly Complete the billing/invoicing process on a weekly

basisbasiso Give 15 day terms instead of 30 daysGive 15 day terms instead of 30 dayso Send multiple bills/invoices with increasingly Send multiple bills/invoices with increasingly

demanding tone at 15, 30, 45 daysdemanding tone at 15, 30, 45 dayso Give 1 to 2% discount for early paying of invoicesGive 1 to 2% discount for early paying of invoiceso Add and collect interest on overdue accountsAdd and collect interest on overdue accountso Outsource the entire billing/invoicing & collection Outsource the entire billing/invoicing & collection

process to speed up cash to bank.process to speed up cash to bank.o Reduce inventory by using low inventory trigger Reduce inventory by using low inventory trigger

pointspointso Negotiate longer terms from vendorsNegotiate longer terms from vendors

What to get from your Profit & Loss What to get from your Profit & Loss StatementStatement

SalesSales

- COGS- COGS

=Gross =Gross ProfitProfit

- Fixed - Fixed CostsCosts

=Net Profit=Net Profit

Monitor % (not numbers) and you will identify changes

$20,000

$5,000

$15,000

$10,000

$5,000

25%

75%

50%

25%

Get to know your Industry’s and YOUR benchmarks!

Profit & Loss StatementProfit & Loss Statement

Product Profit Calculator

Total Business

Product 1Client 1 Team 1

Product 2Client 2Team 2

Product 3Client 3 Team 3

Sales $20,000 $12,000 $3,000 $5,000

CoGs $5,000 $4,000 $200 $800

Gross Profit $15,000 $8,000 $2,800 $4,200

Gross Profit % 75.00% 66.67% 93.33% 84.00%

Fixed Overheads $10,000 $6,000 $500 $3,500

Net Profit $5,000 $2,000 $2,300 $700

Net Profit % 25.00% 16.67% 76.67% 14.00%

What to do NEXTWhat to do NEXT

o Apply the 80/20 rule (The Paretto Principle)Apply the 80/20 rule (The Paretto Principle)o 20% of products provide 80% profits. 20% of products provide 80% profits.

o Sell more 80%, eliminate the 20% and Sell more 80%, eliminate the 20% and reinvestreinvest

o 20% of clients provide 80% profits. 20% of clients provide 80% profits. o Develop your marketing to attract more of Develop your marketing to attract more of

thesetheseo 20% team provide 80% profits. 20% team provide 80% profits.

o Reward and target more like membersReward and target more like memberso 80% hassles come from 20% clients. 80% hassles come from 20% clients.

o Tighten their terms, increase prices or Tighten their terms, increase prices or SACK!SACK!

o 80% hassles come from 20% team. 80% hassles come from 20% team. o Reposition, re-train or sack!Reposition, re-train or sack!

Know your BreakevenKnow your Breakeven

The value of Sales The value of Sales required to produce required to produce

neither profit nor lossneither profit nor loss

WhenWhen does that occur in your business? does that occur in your business?

Formula; Fixed CostsFixed Costs

Gross MarginGross Margin

Using your Break-evenUsing your Break-even

Total Sales/Revenues $240,000

Cost of Sales/Goods Sold/Variable Costs

$60,000

Gross Profit $ $180,000

Gross Margin % 75.0%

Yearly Monthly Weekly Daily

Fixed Costs $120,000 $10,000 $2,308 $476

Net Profit $ $60,000

Net Profit % 25.0%

Average $ Sale $50 (Value of average order/sale)

Break-Even Sales$160,000.

00$13,333 $3,077 $635

Break-Even Transactions 3,200 267 62 12.7

If you think the cost of Education is High

…try Ignorance!

AUSTRALIA’S LARGEST BOOKKEEPING FRANCHISE

““WHY GO SECOND CLASS WHY GO SECOND CLASS WHEN YOU CAN GO... WHEN YOU CAN GO...

FIRST CLASSFIRST CLASS””