Bookkeeping Controls Integrated Workbook

130

Bookkeeping Controls Integrated Workbook AAT Foundation Certificate in Accounting

Transcript of Bookkeeping Controls Integrated Workbook

Bookkeeping Controls

Integrated Workbook

AAT Foundation Certificate in Accounting

Bookkeeping Controls

P.2

© Kaplan Financial Limited, 2016

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any firm or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of Kaplan Publishing.

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

P.3

CONTENTS

Page

Chapter 1 Re-cap: Accounting for sales 1

Chapter 2 Re-cap: Accounting for purchases 15

Chapter 3 Re-cap: Ledger accounts and the trial balance 21

Chapter 4 Errors and suspense accounts 31

Chapter 5 Control accounts and reconciliations 55

Chapter 6 Payroll procedures 83

Chapter 7 Bank reconciliations 99

Chapter 8 The banking system 115

Bookkeeping Controls

P.4

INTEGRATED WORKBOOK ICONS

Definition

Important Calculation

Key Point

Question

Quality and accuracy are of the utmost importance to us so if you spot an error in any of our products, please send an email to [email protected] with full details.

Our Quality Co-ordinator will work with our technical team to verify the error and take action to ensure it is corrected in future editions.

1

By the end of this session you should be able to:

define the key concepts of dual effect, separate entity and the accountingequation

distinguish between assets, liabilities, capital, drawings, income and expenses

prepare journal entries relating to sales in the business

record entries in ledger accounts and balance the ledger accounts

identify whether items are debit or credit balances in a trial balance

and answer questions relating to these areas.

Chapter 1 Re-cap: Accounting for sales

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 1 of your Study Text

Bookkeeping Controls

2

Overview

Overview

Accounting principles

Re-cap: Accounting for sales

Definitions

Accounting for sales

Ledger accounting

Re-cap: Accounting for sales : Chapter 1

3

It is essential that you have studied the Bookkeeping Transactions unit prior toBookkeeping Controls.

Many of the tasks in the assessment require double entries, so the knowledgefrom Bookkeeping Transactions is a fundamental part of passing the exam.

The assessment will last for 2 hours.

Re-cap of Bookkeeping Transactions

This unit builds on knowledge from Bookkeeping Transactions which is required to study the following areas:

types of errors and journal adjustments

the suspense account

control account reconciliations

VAT control account

payroll

bank reconciliations

banking procedures and services.

Introduction

Basic principles of accounting

Bookkeeping Controls

4

These accounting principles form the basis for double entry bookkeeping:

1 Dual effect

For every transaction that a business encounters there are two effects.

2 Separate entity

The business and the owner of the business are seen as two separate entities for accounting purposes. Transactions are viewed in the perspective of the business.

3 Accounting equation

As long as the above two principles have been correctly adhered to, the accounting equation should always balance:

Assets – Liabilities = Capital + Profit – Drawings

Accounting principles

Re-cap: Accounting for sales : Chapter 1

5

Statement of financial position – definitions

Asset

Something owned by the business, available for use by the business

Examples:

Buildings, Vehicles, Inventory, Receivables, Bank, Cash

Assets can be categorised as being either ‘non-current’ or ‘current’:

Non-current asset

An asset which is to be used for the long term and not resold as part of trading activities.

Examples:

Buildings, Vehicles, Plant & Machinery

Current asset

A short term asset which is either cash or will soon be converted into cash.

Examples:

Inventory, Receivables, Bank, Cash

Receivable – Someone owing the business money following a credit sale. Receivables may also be referred to as the sales ledger control account (SLCA)

Key definitions

Bookkeeping Controls

6

Liability

An amount owed by the business. It is an obligation to pay money at a future date.

Examples: Loans, Mortgages, Payables, Bank Overdraft.

Liabilities can be categorised as being either ‘current’ or ‘non-current’:

Current liability

An amount owed and due to be paid by the business in the short term (less than 12 months).

Examples:

Trade payables, bank overdraft, VAT payable

A payable is someone the business owes money to. A payable is created when the business buys goods on credit from a supplier. The balance of payables may also be referred to as the purchases ledger control account (PLCA)

Non-current liability

An amount owed by the business and due to be paid in the longer term (after 12 months).

Examples:

Loans, Mortgages

Re-cap: Accounting for sales : Chapter 1

7

Capital

The amount which the owner has invested in the business; this is owed back to the owner and is therefore considered to be a special liability of the business.

Drawings

Amounts withdrawn from the business by the owner for the owner’s personal use. Drawings can either be cash or inventory.

Statement of profit or loss – definitions

Sales revenue – Income generated from trading activities i.e. selling your goods

Cost of sales – This is the cost of buying the goods for resale

The cost of sales equation:

Opening inventory + Purchases – Closing inventory

Gross profit – The profit remaining, after the cost of sales have been deducted from sales revenue

Expenses – The day to day running costs of the business

Examples: Stationery, wages, rent and rates, heat and light

Net profit or (loss) – The profit or (loss) remaining after expenses have been deducted

Bookkeeping Controls

8

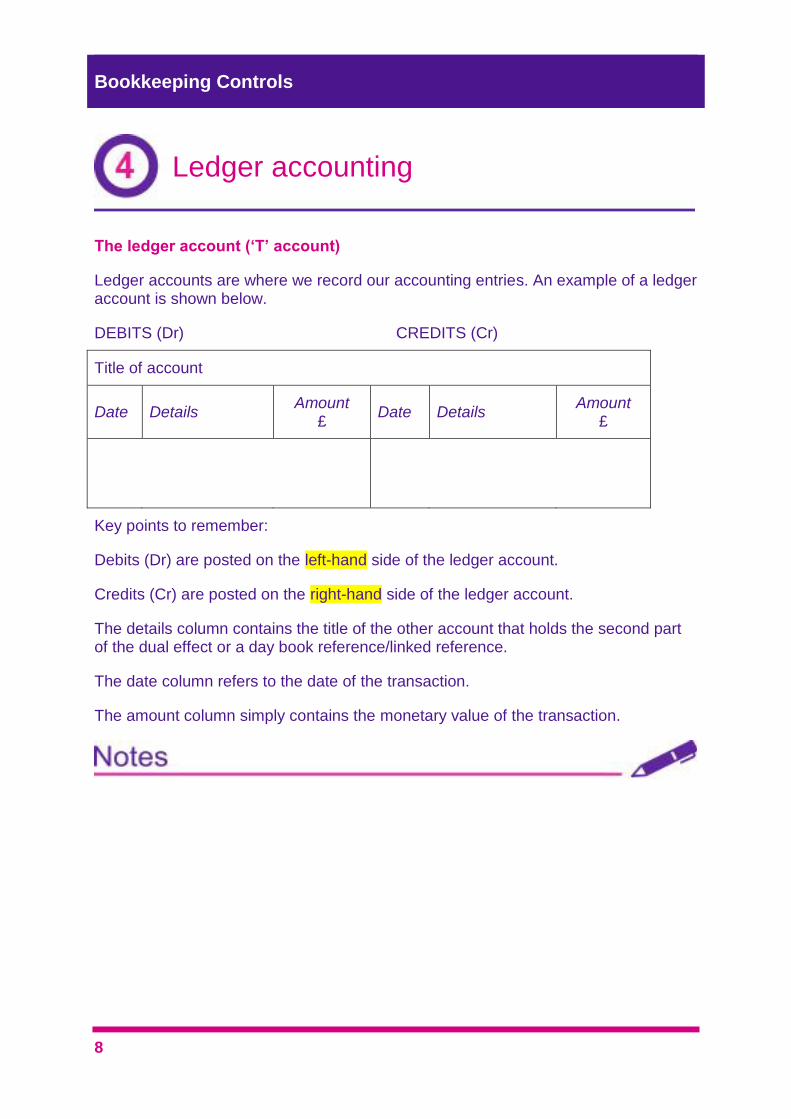

The ledger account (‘T’ account)

Ledger accounts are where we record our accounting entries. An example of a ledger account is shown below.

DEBITS (Dr) CREDITS (Cr)

Title of account

Date Details Amount

£ Date Details

Amount £

Key points to remember:

Debits (Dr) are posted on the left-hand side of the ledger account.

Credits (Cr) are posted on the right-hand side of the ledger account.

The details column contains the title of the other account that holds the second part of the dual effect or a day book reference/linked reference.

The date column refers to the date of the transaction.

The amount column simply contains the monetary value of the transaction.

Ledger accounting

Re-cap: Accounting for sales : Chapter 1

9

The golden rule

The golden rule is that every debit has an equal and opposite credit.

Ledger account

A debit entry represents:

An increase to an asset

A decrease to a liability

An increase to an item of expense

A decrease to an item of income

A credit entry represents:

An increase to a liability

A decrease to an asset

An increase to an item of income

A decrease to an item of expense

The mnemonic DEAD CLIC may help you to remember these effects:

Debit Cash Credit

Cash in

Debits increase:

Expenses

Assets

Drawings

Cash out

Credits increase:

Liabilities

Income

Capital

Bookkeeping Controls

10

There are some fundamental double entries relating to sales and it is essential that you are able to process these. Common sales items are outlined below.

Credit sale:

Dr Trade receivables (SLCA) (Gross amount)

Cr Sales revenue (Net amount)

Cr VAT (VAT amount)

Cash is received from a credit customer:

Dr Cash

Cr Trade receivables (SLCA)

Goods returned by a credit customer:

Dr Sales returns (Net amount)

Dr VAT (VAT amount)

Cr Trade receivables (SLCA) (Gross amount)

Settlement discount given to a credit customer:

Dr Discounts allowed (Net amount)

Dr VAT (VAT amount)

Cr Trade receivables (SLCA)

Accounting for sales

Re-cap: Accounting for sales : Chapter 1

11

Bookkeeping Controls

12

Accounting principles

Dual effect

Accounting equation

Separate entity

Definitions

Assets

Liabilities

Capital

Drawings

Income

Expenditure

Ledger accounting

Every entry has two sides

Accounting for sales

Credit sales

Sales returns

Discounts given

Summary

Re-cap: Accounting for sales : Chapter 1

13

Further reading

For more detailed explanation, analysis and illustration of this topic please read Chapter 1 of the Bookkeeping Controls Study Text. Please complete any TYU that have not been completed in class.

Less detailed summaries can be found in Chapter 1 of the BKCL Pocket Notes.

We recommend the following additional material for the topics covered in this chapter:

Study Text (for teaching throughout the Chapter)

Re-cap: Accounting for sales (Chapter 1)

Additional tutor guidance

Illustrations and further practice

Bookkeeping Controls

14

15

By the end of this chapter you should be able to:

prepare journal entries relating to purchases in the business

and answer questions relating to these areas.

Chapter 2 Re-cap: Accounting for purchases

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 2 of your Study Text

Bookkeeping Controls

16

Similar to accounting for sales, there are a number of entries which need to be considered in accounting for purchases.

Credit purchase:

Dr Purchases (Net amount)

Dr VAT (VAT amount)

Cr Trade payables (PLCA) (Gross amount)

Goods are returned by the business to a credit supplier:

Dr Trade payables (PLCA) (Gross amount)

Cr Purchase returns (Net amount)

Cr VAT (VAT amount)

Cash is paid to a credit supplier:

Dr Trade payables (PLCA)

Cr Cash

Prompt payment discount received from suppliers

Dr Trade payables (PLCA)

Cr Discounts received (Net amount)

Cr VAT (VAT amount)

Accounting for purchases

Basic principles of accounting

Re-cap: Accounting for purchases : Chapter 2

17

Example 1

Identify whether the items below will represent debits or credits, and give the reason why (assets, liabilities, income, expenses, capital, drawings)

Details Debit/Credit Why

Cash in hand Debit Asset

Bank overdraft Credit Liability

Sales Credit Income

Motor vehicles Debit Asset

Money withdrawn by owner Debit Drawings

Rent Debit Expense

Loan from bank Credit Liability

VAT payable Credit Liability

Trade receivables Debit Asset

Capital invested by owner Credit Capital

Bookkeeping Controls

18

Accounting for purchases

Credit purchases

Purchases returns

Prompt payment discounts

Summary

Re-cap: Accounting for purchases : Chapter 2

19

Further reading

For more detailed explanation, analysis and illustration of this topic please read Chapter 2 of the Bookkeeping Controls Study Text. Please complete any TYU that have not been completed in class.

Less detailed summaries can be found in Chapter 2 of the BKCL Pocket Notes.

We recommend the following additional material for the topics covered in this chapter:

Study Text (for teaching throughout the Chapter)

Re-cap: Accounting for purchases (Chapter 2)

Illustrations and further practice

Additional tutor guidance

Bookkeeping Controls

20

21

By the end of this session you should be able to:

understand the purpose of the trial balance

balance off ledger accounts

use ledger accounts to create a trial balance

and answer questions relating to these areas.

Chapter 3 Re-cap: Ledger accounts and the trial

balance

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 3 of your Study Text

Bookkeeping Controls

22

Overview

Overview

Balancing off

Ledger accounts

Creating the trial

balance

Re-cap: Ledger accounts and trial balance : Chapter 3

23

The trial balance is a list showing the balance brought down on each ledger account. It acts as a control. It shows us that our debits and credits balance, prior to us preparing the financial statements.

Although preparing the final financial statements isn’t examined within this unit, we do still have to be able to prepare a trial balance in preparation for this.

To be able to get our ‘balance b/d’ which is the balance to go into our TB, we have to first of all ‘balance off’ the ledger accounts.

The trial balance

Basic principles of accounting

Bookkeeping Controls

24

Procedure for balancing a ledger account:

Step 1 Total both the debit and the credit side of the ledger account and make a note of each total.

Step 2 Insert the higher of the two totals as the total on both sides of the ledger account leaving a line beneath the final entry on each side of the account.

Step 3 On the side with the smaller total insert the figure needed to make this column add up to the total. Refer to this figure as the ‘balance carried down’ (or ‘Bal c/d’ as an abbreviation).

Step 4 On the opposite side of the ledger account, below the total insert this same figure and refer to it as the ‘balance brought down’ (or ‘Bal b/d’ as an abbreviation).

Balancing ledger accounts

Re-cap: Ledger accounts and trial balance : Chapter 3

25

Step 1: Total up each side (to find the highest valued side)

Bank

Date Detail £ Date Detail £

16.02 Capital 20,000 16.02 Machinery 5,000

16.02 SLCA 500 16.02 PLCA 200

Dr side totals £20,500, CR side totals £5,200 – higher total is Dr side.

Step 2: Put the highest total to the bottom of both sides.

Bank

Date Detail £ Date Detail £

16.02 Capital 20,000 16.02 Machinery 5,000

16.02 SLCA 500 16.02 PLCA 200

20,500 20,500

Step 3: In the lower valued side, insert the ‘balance carried down’ (balance c/d) to make it up to the total.

Bank

Date Detail £ Date Detail £

16.02 Capital 20,000 16.02 Machinery 5,000

16.02 SLCA 500 16.02 PLCA 200

16.02 Balance c/d 15,300

20,500 20,500

Step 4: Bring the same balance as the balance c/d to the opposite side below the total and refer to as ‘balance brought down’ (balance b/d).

Bank

Date Detail £ Date Detail £

16.02 Capital 20,000 16.02 Machinery 5,000

16.02 SLCA 500 16.02 PLCA 200

16.02 Balance c/d 15,300

20,500 20,500

17.02 Balance b/d 15,300

Bookkeeping Controls

26

Re-cap: Ledger accounts and trial balance : Chapter 3

27

The balance brought down is transferred to the Trial Balance. These balances appear in the Trial Balance on the same side as they are brought down on.

After all the accounts have been balanced off, the brought down figures can be listed in a trial balance on the same side as the brought down figure.

Example of a trial balance:

£ £

Dr Cr

Bank 9,730

Capital 10,000

Drawings 500

Van (non-current asset) 2,000

Gas 70

Loan 2,000

PLCA 3,200

Purchases 5,600

Rent 500

Sales 8,900

SLCA 2,200

Wages 3,500

Total 24,100 24,100

The debit and the credit column totals should agree. However there may be occasions that this does not happen due to errors or omissions. We will look at what can cause this to happen and how to correct this in a later chapter.

In the assessment, tasks may involve preparing journals for opening entries. This would mean that a trial balance, or extracts of a trial balance, will be given. Students would then be required to state whether each balance is a debit or credit.

Many other tasks will involve journal entries where it is essential that you are comfortable with making double entries.

Bookkeeping Controls

28

Ledger accounts

Balancing off ledger accounts

Being able to successfully construct a trial balance

The trial balance

Using the b/d balance

Common double entries

Summary

Re-cap: Ledger accounts and trial balance : Chapter 3

29

Further reading

For more detailed explanation, analysis and illustration of this topic please read Chapter 3 of the Bookkeeping Controls Study Text. Please complete any TYU that have not been completed in class.

More challenging TYUs in this chapter are TYU 5, 6, 7.

Less detailed summaries can be found in Chapter 3 of the BKCL Pocket Notes.

You should now be able to answer these questions from the Exam Kit:

Question 1 – Intrepid Interiors

Question 2 – Bedroom Bits

If you are attending a revision course, please do not attempt the Exam Kit questions until your tutor instructs you to do so.

Illustrations and further practice

Exam Kit questions

Bookkeeping Controls

30

Tutor’s question bank

Support Questions

Q1 is a simpler question for students who may be struggling

Q13 is a trickier question to challenge more able students

These questions and answers may be printed off separately and distributed to students as necessary, to supplement the material listed above.

We recommend the following additional questions for the topics covered in this chapter:

Study Text (for teaching throughout the Chapter)

Re-cap: Ledger accounts and the trial balance (Chapter 3): TYU 2, 3, 6, 7

Additional tutor resources Additional tutor resources

Additional tutor guidance

31

By the end of this session you should be able to:

identify which errors are detected by the trial balance, and which errors are not

understand how the journal works, and use the journal to make corrections

make adjustments for irrecoverable debts and contras

understand how the suspense account works

create a suspense account

produce journals to clear the suspense account

and answer questions relating to these areas.

Chapter 4 Errors and suspense accounts

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 4 of your Study Text

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 4 of your Study Text

Bookkeeping Controls

32

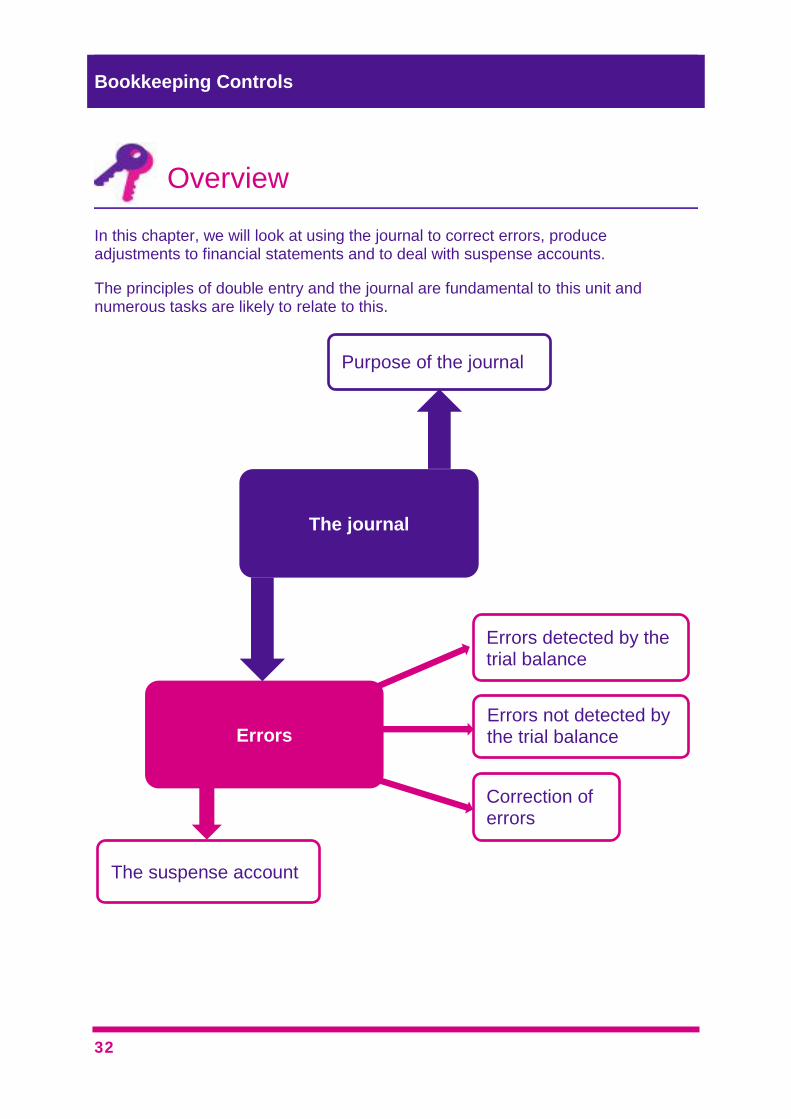

In this chapter, we will look at using the journal to correct errors, produce adjustments to financial statements and to deal with suspense accounts.

The principles of double entry and the journal are fundamental to this unit and numerous tasks are likely to relate to this.

Overview

Overview

Purpose of the journal

The journal

Errors

Errors detected by the trial balance

Errors not detected by the trial balance

Correction of errors

The suspense account

Errors and suspense accounts : Chapter 4

33

A journal is a written instruction to record an item by double entry in the general ledger accounts.

Journals are generally made when adjustments are made to the ledgers and should have narratives accompanying them to explain the reason for the adjustment.

Reasons you may have to write up a journal:

Correction of errors

Other year-end adjustments (i.e. writing off of an irrecoverable debt or contra)

Firstly, we will look at journal entries for year-end adjustments, and then we will look at how the journal is used to correct errors.

(a) Irrecoverable debts

A debt which is highly unlikely to be received is known as an irrecoverable debt: it is not prudent for the business to consider this debt as an asset and therefore the debt is written off.

Reasons for irrecoverable debts

Customer in liquidation

Customer having difficulty paying

Customer disputes all/part of debt.

The journal

Basic principles of accounting

Bookkeeping Controls

34

How do we account for irrecoverable debts – if not considering VAT?

Dr Irrecoverable debt expense

Cr SLCA (and subsidiary sales ledger)

How do we account for irrecoverable debts – if considering VAT?

If the debt is over 6 months overdue, you can reclaim the VAT that you would have paid over to HMRC.

Dr Irrecoverable debt expense

Dr VAT

Cr SLCA (and subsidiary sales ledger)

Example 1

Simpson and King, a credit customer of Cars R Us, has ceased trading. The amount owing in the account is an 8 month old debt of £720 inclusive of VAT at 20%. Today’s date is 30 June 2012.

Dr Irrecoverable debt expense £600

Dr VAT £120

Cr SLCA (and subsidiary sales ledger) £720

Errors and suspense accounts : Chapter 4

35

(b) Contra entries

A business will be both a receivable and a payable of another business if it both buys from the other business and sells to it.

If this is the case, then there will be money owed to the business and money owing from it. Under the condition of both businesses agreeing, we net these amounts off against each other to show the net position.

The amount netted off will be the lowest common figure owed by both parties.

For a contra entry, we are always reducing both the payables and the receivables.

The double entry for this is always:

Dr PLCA (and subsidiary purchases ledger)

Cr SLCA (and subsidiary sales ledger)

This has the effect of reducing the liability to the payable and reducing the receivable’s debt.

Bookkeeping Controls

36

For example: Company ‘A’ owes Company ‘B’ £500 and Company ‘B’ owes Company ‘A’ £200. You work for Company ‘A’.

Company ‘A’ General ledger

PLCA

C’B 500

SLCA

C’B 200

The contra entry for Company ‘A’ would be:

Dr PLCA 200

Cr SLCA 200

Company ‘A’ General ledger

PLCA

SLCA 200 C’ B 500

c/d 300

SLCA

C’B 200 PLCA 200

The net effect of this would be that:

Company ‘A’ would owe Company ‘B’ £300.

Errors and suspense accounts : Chapter 4

37

If the TB doesn’t balance this indicates that an error or a number of errors have occurred. Errors of this type are referred to as errors that can be detected by the TB.

If errors cause the TB to not balance, a suspense account is opened. The useof a suspense account is reviewed later on in this chapter.

As well as errors causing the TB to not balance, there will also be errors wherethe TB still balances.

Errors detected by the trial balance

Errors detected by the trial balance

Basic principles of accounting

Single entry

Casting error

Transposition error

Extraction error

Omission

Two entries on one side

Errors detected

by the trial

balance

Bookkeeping Controls

38

Errors that cause a difference to occur between the debit and credit column totals in the TB:

Single entry Only one side of the entry being made

e.g. if only the credit entry for payments to payables has been made, the credit total on the trial balance will exceed the debit total.

Casting (addition) error

If a ledger account has not been balanced correctly due to a casting error then this will mean that the trial balance will not balance.

Transposition error If an amount in a ledger account or a balance on a ledger account has been transposed and incorrectly recorded

e.g. a debit entry was recorded correctly as £5,291 but the related credit entry was entered as £5,219.

Extraction error If a ledger account balance is incorrectly recorded on the TB either by recording the wrong figure or putting the balance on the wrong side of the TB.

Omission (of one ledger balance)

If a ledger account balance is inadvertently omitted from the TB.

Two entries on one side

A debit in two accounts, or credit in two accounts, rather than a corresponding debit and credit.

Errors and suspense accounts : Chapter 4

39

Errors not detected by the trial balance

Basic principles of accounting

Error of original entry

Compensating error

Error of omission

Error of commission

Error of principle

Reversal of entries

Errors not detected

by the trial

balance

Bookkeeping Controls

40

The errors that have appeared in the diagram above are those which do not cause the debit and credit columns of the trial balance to be different:

Error of original entry

This is where the wrong figure is entered as both the debit and credit entry, meaning the figure is wrong on both sides.

Compensating error This is where two separate errors of the exact same amount are made, one on the debit side and the other on the credit side.

Error of omission This is where an entire double entry is omitted from the ledger accounts.

Error of commission

With this type of error a debit entry and an equal credit entry have been made but one of the entries has been to the wrong account

e.g. if the heat and light expense was debited to the rent account but the credit entry was correctly made in the bank account.

Error of principle This is similar to an error of commission but the entry has been made in the wrong type of account

e.g. if the electricity expense was debited to a non-current asset account

Reversal of entries Debit and credit entries have been made in the correct accounts but have been made to the wrong sides of the accounts

e.g. a cash payment for electricity was debited to the cash account and credited to the electricity account.

Errors and suspense accounts : Chapter 4

41

In the assessment, you may have to write a journal to correct errors.

For each error, it may be helpful to consider the following questions:

1 What journal entry did we make?

2 What journal entry should we have made?

3 How do we correct this?

Correcting errors

Basic principlesof accounting

Bookkeeping Controls

42

Example 2

The following errors have been made in Night Night Beds Ltd.

Error 1

£170 has been debited to the insurance account instead of the motor tax account

This error has been caused by £170 being debited to insurance instead of motor tax. We have to assume that the other side to the journal was posted correctly; let us assume that the other side was a credit to the bank account.

1 What journal did we make?

Dr Insurance £170

Cr Bank £170

2 What journal entry should we have made?

Dr Motor tax £170

Cr Bank £170

3 How do we correct this?

Dr Motor tax £170

Cr Insurance £170

Errors and suspense accounts : Chapter 4

43

The following errors have been made in Night Night Beds Ltd.

Error 2

Purchases valued at £9,000 have been credited to the purchases account and debited to the payables ledger control account (ignore VAT)

1 What journal did we make?

Dr PLCA £9,000

Cr Purchases £9,000

2 What journal entry should we have made?

Dr Purchases £9,000

Cr PLCA £9,000

3 How do we correct this?

We need to reverse these entries. This can be done by doing the correct entry by double the amount, the first amount of £9,000 eliminates the reversed postings, the second £9,000 posts the correct entry.

Dr Purchases £18,000

Cr PLCA £18,000

Showing it as two entries:

Dr Purchases £9,000

Cr PLCA £9,000

Dr Purchases £9,000

Cr PLCA £9,000

Bookkeeping Controls

44

A suspense account is used in two circumstances.

To hold a difference in a TB prior to its correction

When the correct posting for an item is uncertain – the suspense account is just used as a temporary holding account until the correct account to post to has been decided.

Only those errors which cause a difference on the TB need to be adjusted by means of an entry in the suspense account.

Example 3

Mr Plum’s trial balance was extracted and did not balance. The debit column of the TB totalled £109,798 and the credit column totalled £219,666.

What entry would be made in the suspense account to balance the trial balance?

Account name Amount £

Debit

Credit

Suspense 109,868

The suspense account

Basic principles of accounting

Errors and suspense accounts : Chapter 4

45

Example 4

The trial balance didn’t balance, so a suspense account of £60 was created. The following two errors have been discovered.

Error 1: A payment of £900 has been recorded as £1,000 in the heat and light account.

Error 2: An amount of £40 has been omitted from the discounts allowed account (ignore VAT).

Error 1

For the first error, the heat and light expense has been overstated at £1,000 instead of £900 as recorded in the bank (if assuming it is a bank payment).

As the two sides of the accounting entry were for differing amounts, a suspense balance of £100 would have been created. See below:

Dr Heat & Light expense £1,000

Cr Bank £900

Cr Suspense £100

When correcting this entry we need to bring the heat and light expense down to £900 and also eliminate the suspense balance of £100.

Dr Suspense £100

Cr Heat and light expense £100

Bookkeeping Controls

46

As well as knowing how to correct errors, it is also important that you are able to identify from a list of transactions which will be disclosed by the trial balance and which will not.

Error 2

The second error has been an omission to the discounts allowed account of £40. The entry to record a discount allowed is:

Dr Discounts allowed £40

Cr SLCA £40

As the debit entry to the discounts allowed was omitted, in replacement of this to make the entry balance, the debit would have been posted to the suspense account instead:

Dr Suspense £40

Cr SLCA £40

To correct this error we need to post £40 as a debit to discounts allowed and eliminate the debit that is in the suspense account for this amount.

Solution

Dr Discounts allowed £40

Cr Suspense £40

We can now see how these entries have cleared the original suspense balance of £60. The suspense account is cleared when both sides balance to the same amount.

SUSPENSE

Date Detail £ Date Detail £

Heat and light 100 Opening balance 60

Discounts allowed

40

100 100

Errors and suspense accounts : Chapter 4

47

Bookkeeping Controls

48

Example 5

Which of the errors below are disclosed by the trial balance?

Details Disclosed by trial

balance?

Recording a receipt from a receivable in the bank account only.

Yes – single entry

Recording bank payment of £56 for motor expenses as £65 in the expense account.

Yes – transposition error

Recording a credit purchase on the debit side of the purchases ledger control account and the credit side of the purchases account.

No – compensating error (reversal of entries)

Recording a payment for electricity in the insurance account.

No – error of commission

Recording a bank receipt for cash sales on the credit side of both the bank and the sales account.

Yes – Two entries on one side

Incorrectly calculating the balance on the motor vehicles account.

Yes – Casting error

Writing off an irrecoverable debt in the irrecoverable debt expense and sales ledger control accounts only.

No – Double entry is correct, subsidiary ledger

isn’t

An account with a ledger balance of £3,500 was recorded on the trial balance as £350.

Yes – extraction error

Errors and suspense accounts : Chapter 4

49

Bookkeeping Controls

50

Example 6

Identify the type of error described in each situation below.

Details Type of error

Recording a gas bill paid in the bank account but nowhere else.

Single entry

Recording a bill for electricity expense as an asset rather than an expense.

Error of principle

Recording a credit purchase on the debit side of the purchases ledger control account and the credit side of the purchases account.

Reversal of entries

Copying the total from the SLCA into the trial balance incorrectly.

Extraction error

Errors and suspense accounts : Chapter 4

51

Errors

Errors detected by the trial balance

Errors not detected by the trial balance

Types of error

Correcting errors

What journal entry did we make?

What journal entry should we have made?

How do we correct this?

Further adjustments

Irrecoverable debt expense

Contra

Suspense account

Creating a suspense account

Producing journal entries to clear the suspense account

Summary

Basic principles of accounting

Bookkeeping Controls

52

Further reading

For more detailed explanation, analysis and illustration of this topic please read Chapter 4 of the Bookkeeping Controls Study Text. Please complete any TYU that have not been completed in class.

Less detailed summaries can be found in Chapter 4 of the BCKL Pocket Notes.

You should now be able to answer these questions from the Exam Kit:

Question 38 – Pat’s Cafe

Question 14 – Chestnut

Question 22 – Principles

If you are attending a revision course, please do not attempt the Exam Kit questions until your tutor instructs you to do so.

Illustrations and further practice

Exam Kit questions

Errors and suspense accounts : Chapter 4

53

Tutor’s question bank

Support Questions

Question 2 and 3

Challenging questions

Question 14 and 15

These questions and answers may be printed off separately and distributed to students as necessary, to supplement the material listed above.

We recommend the following additional questions for the topics covered in this chapter:

Study Text (for teaching throughout the Chapter)

Errors and suspense accounts (Chapter 4): TYU 3, 4

Exam Kit

Questions 16, 17, 23, 39

Additional tutor resources Additional tutor resources

Additional tutor guidance

Bookkeeping Controls

54

55

By the end of this session you should be able to:

record entries into the sales ledger control account, purchases ledger controlaccount and VAT control account.

perform reconciliations between the sales/purchases ledger control accountsand the subsidiary ledger.

complete the VAT control account, identifying whether the balance represents aliability or an asset.

and answer questions relating to these areas.

Chapter 5 Control accounts and reconciliations

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 5 of your Study Text

Bookkeeping Controls

56

Control accounts are likely to feature in one or more tasks in the assessment.

Overview

Overview

Sales ledger control account

reconciliations

Control accounts and reconciliations

VAT control account

Purchases ledger control account reconciliations

Controls accounts and reconciliations : Chapter 5

57

To increase the balance on the SLCA it has to be debited (increase of an asset)– this shows us that the amounts owed by receivables are increasing.

To decrease the balance on the SLCA it has to be credited (decrease of anasset) – this shows us that the amounts owed by receivables are decreasing.

The standard entries in a sales ledger control account are:

Sales ledger control account

£ £

Balance b/d x Returns per sales returns day book x

Sales per sales day book x Cash from receivables x

Discounts allowed x

Irrecoverable debt written off x

Contra entry x

Balance c/d x

–– ––

x x

–– ––

Balance b/d x

Sales ledger control account (SLCA)

Outcome

Bookkeeping Controls

58

Comparing the control account balance with the total of the subsidiary ledger accounts is a form of internal control.

Ensuring that the total on the control account agrees with the total of the subsidiary accounts is referred to as CONTROL ACCOUNT RECONCILIATION.

If the total of the balances on the subsidiary ledgers do not equal the balance on the control account, then an error, has been made in either the general or the subsidiary ledger.

Reconciliations should be done regularly so that any discrepancies are highlighted and investigated in a timely manner. If this is not done, this could lead to potential fraud or errors going unnoticed.

In addition to regular reconciliations, an aged receivables ledger should be kept. This contains a list of how old each receivables balance is, enabling a business to chase up older debts.

Controls accounts and reconciliations : Chapter 5

59

Errors can occur due to the following:

Casting errors in a day book, which will only affect the control account.

Casting errors in the subsidiary ledger either within an individual account orwhen adding the subsidiary ledger balances together.

Posting individual entries twice, affecting the subsidiary ledger.

Omitted items; showing an incorrect balance for either the control account orsubsidiary ledger.

Transactions recorded in the control account, but omitted from the subsidiaryledger.

Transactions recorded in the subsidiary ledger, but omitted from the controlaccount.

Bookkeeping Controls

60

Example 1

The balance on the sales ledger control account for a business at 31 March 2012 is £14,378.37. The total of the list of subsidiary ledger balances for receivables is £13,935.37.

The difference has been investigated and the following errors identified:

The sales day book was overcast by £1,000.

A credit note for £150 was entered into the individual receivable's account as an invoice.

Discounts allowed of £143 were correctly accounted for in the subsidiary ledger but were not entered into the general ledger accounts.

A credit balance on one receivable’s account of £200 was mistakenly listed as a debit balance when totalling the individual receivable accounts in the subsidiary ledger.

Correct any errors in the sales ledger control account and prepare the reconciliation between the balance on that account and the total of the individual balances on the subsidiary ledger accounts.

Step 1

Open up a SLCA and amend this for any errors that have been made.

The adjusted SLCA can be seen below.

Sales ledger control account

£ £

Balance b/d 14,378.37 SDB overcast (1) 1,000.00

Discounts allowed (3) 143.00

Amended balance c/d 13,235.37

–––––––– ––––––––

14,378.37 14,378.37

–––––––– ––––––––

Amended balance b/d 13,235.37

Controls accounts and reconciliations : Chapter 5

61

Step 2

Draw up the list of balances on the subsidiary ledger, and amend this for any errors.

In this example, the first thing to be done will be to copy in the opening balance of £13,935.37

From the list of errors, there are 2 that will affect the list of balances on the subsidiary ledger.

Item 2 will mean that the list of balances on the subsidiary ledger is overstated by £300 due to the credit note of £150 being incorrectly added rather than deducted.

Therefore £300 must be DEDUCTED from the list of balances.

Item 4 will also mean that the list of balances on the subsidiary ledger is overstated, as the recording of a credit incorrectly as a debit would have led to the balances being overstated by £400.

Therefore £400 must be DEDUCTED from the list of balances.

£

Original total 13,935.37

Less: Credit note entered as invoice (2) (2 × 150) (300.00)

Credit balance entered as debit balance (4) (2 × 200) (400.00)

––––––––

13,235.37

From here, it can be seen that the revised SLCA balance of £13,235.37 agrees to the revised list of balances on the subsidiary ledger, and therefore the reconciliation has been performed accurately.

Bookkeeping Controls

62

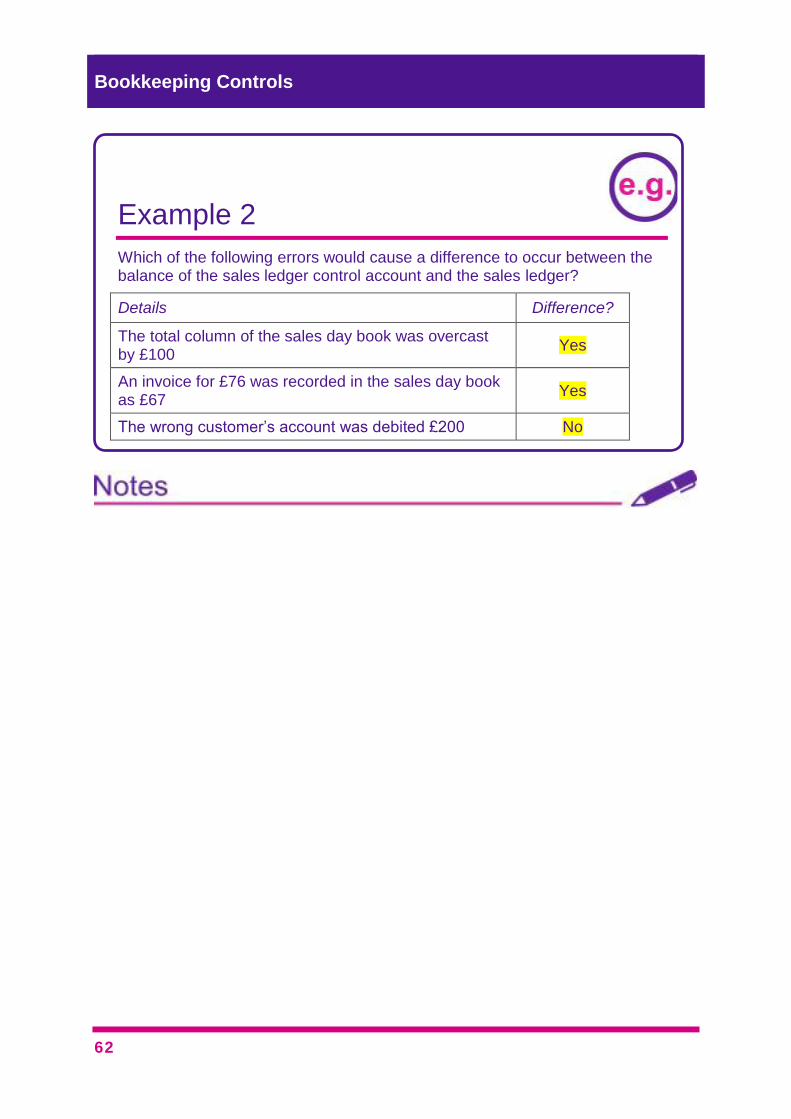

Example 2

Which of the following errors would cause a difference to occur between the balance of the sales ledger control account and the sales ledger?

Details Difference?

The total column of the sales day book was overcast by £100

Yes

An invoice for £76 was recorded in the sales day book as £67

Yes

The wrong customer’s account was debited £200 No

Controls accounts and reconciliations : Chapter 5

63

To increase the balance on the PLCA it has to be credited (increase of a liability)

To decrease the balance on the PLCA it has to be debited (decrease of a liability)

The standard entries in the purchases ledger control account are:

Purchases ledger control account

£ £

Balance b/d x

Purchases per purchases day book

x

Cash paid x

Discount received x

Purchase returns x

Contra entry x

Balance c/d x

–– ––

x x

–– ––

Balance b/d x

If the total of the balances on the subsidiary ledgers do not equal the balance on the control account, then an error has been made.

The purchases ledger control account

Outcome

Bookkeeping Controls

64

Example 3

The balance on the purchases ledger control account for a business at 30 June 2012 was £12,159. The total of the balances on the individual payables’ accounts in the subsidiary ledger was £19,200.

The following errors were also found:

the cash payments book had been undercast by £70

an invoice from Thomas Ltd, a credit supplier, for £2,400 was correctly entered in the subsidiary ledger but had been missed out of the addition of the total in the purchases day book

an invoice from Fred Singleton for £2,000 plus VAT (20%) was included in his individual account in the subsidiary ledger at the net amount

an invoice from Horace Shades for £6,000 was entered into the individual account in the subsidiary ledger twice

the same invoice is for £6,000 plus VAT (20%) but the VAT had not been included in the subsidiary ledger

returns to Horace Shades of £311 had been omitted from the subsidiary ledger.

You are required to correct any errors in the purchases ledger control account and prepare the reconciliation between the balance on that account with the total of the individual balances on the subsidiary ledger accounts at 30 June.

Controls accounts and reconciliations : Chapter 5

65

Step 1

Open up a purchases ledger control account, and amend this for any errors that have been made.

In this example, the first thing to be done will be to copy in the opening balance of £12,159.

From the list of errors, there are 2 that will affect the control account.

Item 1 will mean that the control account is overstated by £70 due to the cash payments book being undercast. Therefore a DEBIT is needed to the PLCA to correct this.

Item 2 will mean that the control account is understated, as an invoice has been omitted. Therefore a CREDIT is required to record this.

The adjusted PLCA can be seen below:

Purchases ledger control account

£ £

Undercast of CPB (1) 70 Balance b/d 12,159

Invoice omitted (2) 2,400

Balance c/d 14,489

–––––– ––––––

14,559 14,559

–––––– ––––––

Amended balance b/d 14,489

Bookkeeping Controls

66

Step 2

Draw up the list of balances on the subsidiary ledger, and amend this for any errors. In this example, the first thing to be done will be to copy in the opening balance of £19,200.

From the list of errors, there are 4 that will affect the list of balances on the subsidiary ledger.

Item 3 will mean that the list of balances on the subsidiary ledger is understated by £400, as Fred will owe the gross amount, not the net amount. Therefore £400 must be ADDED to the list of balances.

Item 4 will mean that the list of balances on the subsidiary ledger is overstated, as £6,000 has been added to the subsidiary ledger twice. Therefore £6,000 must be DEDUCTED from the list of balances.

Item 5 is the same as item 3. The list of balances will be understated, as the gross amount will be owed, not the net amount. Therefore the VAT of £1,200 (£6,000 × 20%) should be ADDED to the list of balances.

Item 6 means the list of balances is overstated, as the returns have not been recorded. Therefore £311 must be DEDUCTED from the list of balances.

£

Original total 19,200

Add: Fred Singleton VAT (3) 400

Less: Credit balance entered twice (4) (6,000)

Add: Horace Shades VAT (5) 1,200

Less: Horace Shades returns (6) (311)

––––––

14,489

The revised PLCA balance of £14,489 now agrees with the revised total of the list of balances on the subsidiary ledgers. Therefore the reconciliation is accurate.

Controls accounts and reconciliations : Chapter 5

67

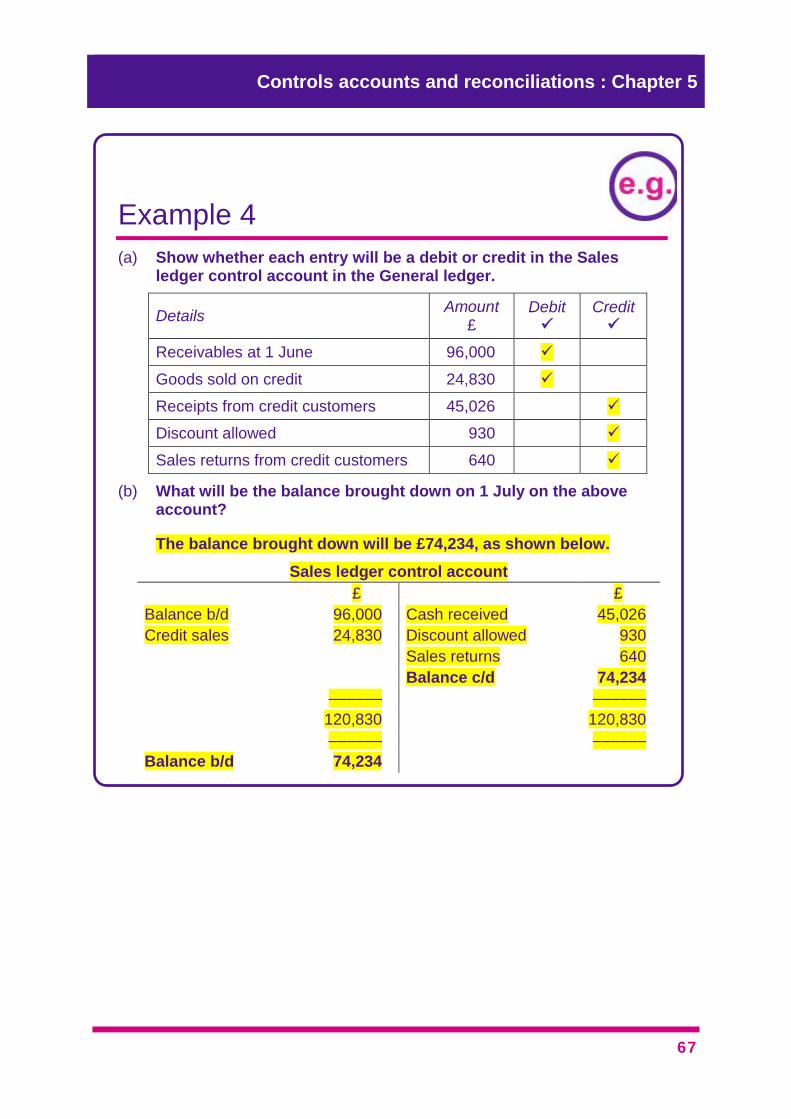

Example 4

(a) Show whether each entry will be a debit or credit in the Salesledger control account in the General ledger.

Details Amount

£ Debit

Credit

Receivables at 1 June 96,000

Goods sold on credit 24,830

Receipts from credit customers 45,026

Discount allowed 930

Sales returns from credit customers 640

(b) What will be the balance brought down on 1 July on the aboveaccount?

The balance brought down will be £74,234, as shown below.

Sales ledger control account

£ £

Balance b/d 96,000 Cash received 45,026

Credit sales 24,830 Discount allowed 930

Sales returns 640

Balance c/d 74,234

–––––– ––––––

120,830 120,830

–––––– ––––––

Balance b/d 74,234

Bookkeeping Controls

68

The following debit balances were in the subsidiary (sales) ledger on 1 July.

£

ATD Ltd 42,600

ARD Ltd 10,752

CC Ltd 10,984

SI Ltd 9,258

(c) Reconcile the balances shown above with the sales ledger control account balance you have calculated in part (a).

£

Sales ledger control account balance as at 30 June 74,234

Total of subsidiary (sales) ledger accounts as at 30 June 73,954

Difference 640

(d) What may have caused the difference you calculated in part (c)?

The difference is likely to have been caused by the sales returns being omitted from the SLCA, or the sales returns being included in the subsidiary accounts twice in error.

Controls accounts and reconciliations : Chapter 5

69

VAT

VAT is charged on the taxable supply of goods and services by a taxable person in the course of a business carried on by them. VAT is an indirect tax borne (suffered) by the ultimate consumer. In the UK, it is administered by HM Revenue & Customs (HMRC) which we may refer to as the tax authorities.

VAT is charged on purchases (input tax) and sales (output tax).

Businesses that are VAT registered must charge VAT on top of their sales price and collect the VAT from their customers on behalf of the tax authorities.

The VAT collected from their customers is then owed to the tax authorities (HMRC) and must be shown as a liability within the accounts, until the liability is paid.

When VAT is charged on invoices for purchases and expenses, a business pays the full amount including VAT to that supplier. If the business is VAT registered the VAT that has been paid can be reclaimed from the tax authorities. This reduces the VAT liability within the VAT control account.

VAT

Outcome

Bookkeeping Controls

70

If output tax exceeds input tax, the business has a VAT liability of the excess to the tax authorities. This would be represented by a balance brought down on the credit side of the VAT control account.

If input tax exceeds output tax, the business has a VAT asset of the excess from the tax authorities. This would be represented by a balance brought down on the debit side of the VAT control account.

Re-cap from Bookkeeping Transactions: Understanding and calculating the VAT figures

The standard rate of VAT in the UK is currently 20%.

Let’s review how the figures work:

Cost structure:

Net 100%

+ VAT VAT %

––––– –––––

= Gross 100% + VAT%

With a VAT rate at 20%, the cost structure is as follows:

Net 100%

+ VAT 20%

––––– –––––

= Gross 120%

How to manipulate VAT

The amount known × % of what you want to know

% what you do know

There is also a specific rounding rule to remember with VAT:

VAT should always be rounded down to the nearest penny e.g. VAT of £21.5677 will be rounded down to £21.56.

Controls accounts and reconciliations : Chapter 5

71

Illustration

VAT from Net

Say we want to find out the VAT from a net amount of £120,000.

Using the equation above, the amount we know is the net amount of £120,000, the percentage of what we want to know is 20% (i.e. the VAT), and the percentage of what we do know is the net percentage which is 100%.

£120,000 × 20

100

= £24,000

VAT from Gross

Say we want to find out the VAT from a gross amount of £288,000.

Using the same equation, the amount we know is the gross amount of £288,000, the percentage of what we want to know is 20% (i.e. the VAT) and the percentage of what we do know is the gross percentage which is 120% (the net 100% + VAT rate 20%).

£288,000 ×20

120

= £48,000

Bookkeeping Controls

72

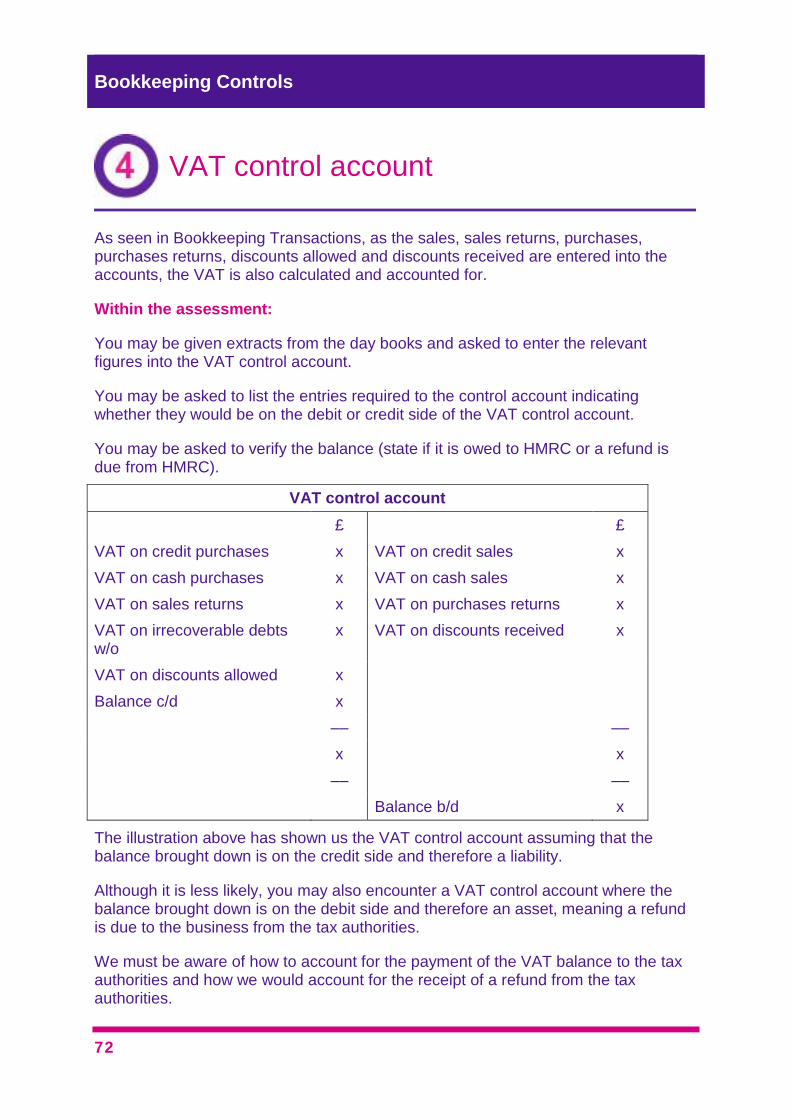

As seen in Bookkeeping Transactions, as the sales, sales returns, purchases, purchases returns, discounts allowed and discounts received are entered into the accounts, the VAT is also calculated and accounted for.

Within the assessment:

You may be given extracts from the day books and asked to enter the relevant figures into the VAT control account.

You may be asked to list the entries required to the control account indicating whether they would be on the debit or credit side of the VAT control account.

You may be asked to verify the balance (state if it is owed to HMRC or a refund is due from HMRC).

VAT control account

£ £

VAT on credit purchases x VAT on credit sales x

VAT on cash purchases x VAT on cash sales x

VAT on sales returns x VAT on purchases returns x

VAT on irrecoverable debts w/o

x VAT on discounts received x

VAT on discounts allowed x

Balance c/d x

–– ––

x x

–– ––

Balance b/d x

The illustration above has shown us the VAT control account assuming that the balance brought down is on the credit side and therefore a liability.

Although it is less likely, you may also encounter a VAT control account where the balance brought down is on the debit side and therefore an asset, meaning a refund is due to the business from the tax authorities.

We must be aware of how to account for the payment of the VAT balance to the tax authorities and how we would account for the receipt of a refund from the tax authorities.

VAT control account

Outcome

Controls accounts and reconciliations : Chapter 5

73

Bookkeeping Controls

74

Example 5

This quarter, Company A had sales of £250,000 exclusive of VAT, made purchases of £90,000 net and made some returns to suppliers amounting to £5,000 plus VAT. Complete the VAT control account for Company A for this quarter.

Solution

Firstly, the VAT amounts must be calculated, as these are not given. The information provided means that VAT will have to be calculated from the net amounts, as all figures have been given without VAT included. The VAT amounts are calculated as a percentage of the amounts given, shown below:

VAT on sales (Output tax): £50,000 (£250,000 × 20%)

VAT on purchases (Input tax): £18,000 (£90,000 × 20%)

VAT on purchases returns: £1,000 (£5,000 × 20%)

The tax on sales will be a CREDIT, as this will increase the amount owed.

The tax on purchases will be a DEBIT, as this could be reclaimed from HMRC, therefore reducing the liability.

The tax on purchases returns will be a CREDIT. Tax on purchases can be reclaimed, so is included initially as a debit balance. However, some of these goods have now been returned to the supplier. As these goods are being returned, then the company cannot reclaim any of the tax. Therefore this is credited to reduce the amount that can be reclaimed.

VAT control account

Detail £ Detail £

Purchases 18,000 Sales 50,000

Balance c/d 33,000 Purchase returns 1,000

Total 51,000 Total 51,000

Balance b/d 33,000

The balance of £33,000 should be PAID to HMRC as it is a LIABILITY.

Controls accounts and reconciliations : Chapter 5

75

Bookkeeping Controls

76

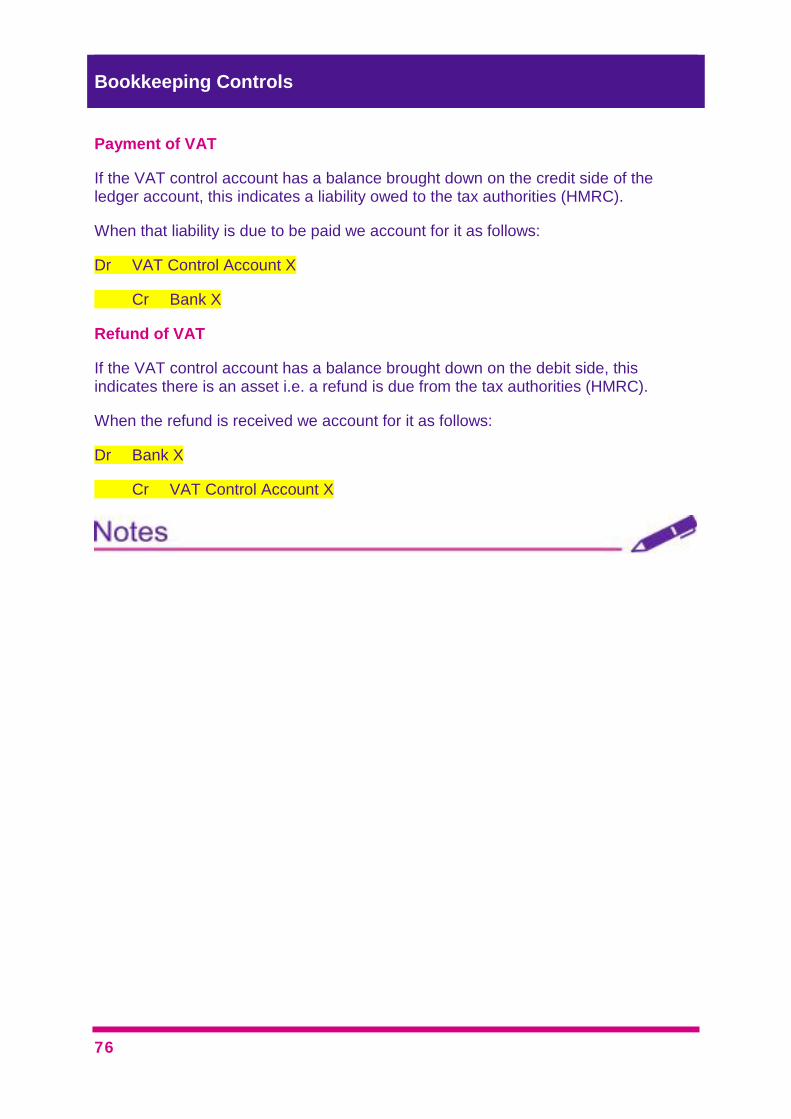

Payment of VAT

If the VAT control account has a balance brought down on the credit side of the ledger account, this indicates a liability owed to the tax authorities (HMRC).

When that liability is due to be paid we account for it as follows:

Dr VAT Control Account X

Cr Bank X

Refund of VAT

If the VAT control account has a balance brought down on the debit side, this indicates there is an asset i.e. a refund is due from the tax authorities (HMRC).

When the refund is received we account for it as follows:

Dr Bank X

Cr VAT Control Account X

Controls accounts and reconciliations : Chapter 5

77

Example 6

Which of the following items would be debit balances in the VAT control account?

VAT total in sales day book No – owed to HMRC

VAT total in purchases day book Yes – Reclaimable from HMRC

VAT on petty cash payments made Yes – Reclaimable from HMRC

VAT refund received from HMRC No – this is the business receiving the cash from HMRC that was owed. The double entry will be Dr Cash, Cr VAT Control

VAT on cash sales No – owed to HMRC

VAT in purchase returns day book No – Can no longer reclaim

VAT total in sales returns day book Yes – As these sales have been returned, the VAT is no longer owed to HMRC

VAT on irrecoverable debts written off

Yes – Reclaimable from HMRC as long as debts more than 6 months old

VAT total in discounts allowed day book

This is reclaimable from HMRC, as the amount of VAT recorded on sales would have initially been on the amount invoiced

VAT total in discounts received day book

No – payable to HMRC, as the amount of VAT recorded as initially reclaimable would have been on the full purchase price, which we have not paid

Bookkeeping Controls

78

Controls accounts and reconciliations : Chapter 5

79

Example 7

The following VAT figures have been extracted from the books of prime entry:

£

Sales day book 24,530

Sales returns day book 1,270

Purchases day book 11,250

Cash payments book 2,430

Show the entries in the VAT control account.

VAT control account

Detail £ Detail £

Sales returns 1,270 Sales 24,530

Purchases 11,250

Cash payments 2,430

Balance c/d 9,580

Total 24,530 Total 24,530

Balance b/d 9,580

Bookkeeping Controls

80

Sales ledger control account

Control account entries

Types of error

Reconciling sales ledger control account to the subsidiary ledger

Purchases ledger control account

Control account entries

Types of error

Reconciling purchases ledger control account to the subsidiary ledger

VAT

Purpose of VAT

Calculation of VAT

VAT control account

Control account entries

Verify the balance on the control account

Make entries for payment/receipt

Summary

Outcome

Controls accounts and reconciliations : Chapter 5

81

Further reading

For more detailed explanation, analysis and illustration of this topic please read Chapter 5 of the Bookkeeping Controls Study Text. Please complete any TYU that have not been completed in class.

Less detailed summaries can be found in Chapter 5 of the BKCL Pocket Notes.

You should now be able to answer these questions from the Exam Kit:

Question 61 – Monster Munchies

Question 65 – Zhang

Question 70 – Disley

If you are attending a revision course, please do not attempt the Exam Kit questions until your tutor instructs you to do so.

Illustrations and further practice

Exam Kit questions

Bookkeeping Controls

82

Tutor’s question bank

Support Questions

Question 5 and 6

More challenging questions:

Questions 16 and 17

These questions and answers may be printed off separately and distributed to students as necessary, to supplement the material listed above.

We recommend the following additional questions for the topics covered in this chapter:

Study Text (for teaching throughout the Chapter)

Control Accounts and Reconciliations (Chapter 5): TYU 1, 2, 6, 7

Exam Kit

Questions 64, 66, 71

Additional tutor resources Additional tutor resources

Additional tutor guidance

83

By the end of this session you should be able to:

give examples of the types of transactions that might be entered into thebookkeeping system by using the journal

prepare and enter the journal entries in the general ledger to process payrolltransactions, including gross pay, income tax, employer’s and employees’ NIC,employer’s and employee’s pension and voluntary deductions

and answer questions relating to these areas.

Chapter 6 Payroll procedures

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 6 of your Study Text

Bookkeeping Controls

84

Employer’s NI Employer’s pension

Gross pay

Payroll

Net pay

Tax/pension liabilities

Overview

Overview

Payroll procedures : Chapter 6

85

Gross pay This is the total payable to the employee before deductions.

This could consist of wages or salary; overtime; shift payments; bonus; commission; holiday pay.

Income tax (PAYE) This is the tax owed by the employee on their gross pay.

The employer collects it on the employee’s behalf by deducting it from wages and paying it to the tax authorities (HMRC).

Employee’s NIC The national insurance contributions owed by the employee on their gross pay.

The employer collects it on the employee’s behalf by deducting it from wages and paying it to the tax authorities (HMRC).

Employer’s NIC This is NOT deducted from the employee’s gross pay.

This is an additional expense to the company for employing individuals. This is paid by the company to the tax authorities (HMRC).

Employer’s pension This is an additional expense to the company for employing individuals. This is paid by the company into a pension fund.

Other deductions These may be contributions to items such as employee contribution to pension schemes, charitable donations or trade unions. These reduce the amount the employee receives and are paid over to the respective parties.

Overview of the payroll function

Overview

Bookkeeping Controls

86

There are 3 different elements to payroll calculations which will be examined here:

(a) calculating net pay

(b) calculating total wages expense for the employer

(c) working out the liabilities due to various parties.

Net pay

In order to calculate net pay, begin with the figure for gross pay, and then deduct items that relate to the employee. This will mean that PAYE, employee’s NIC and any other employee deductions (such as pension contributions) are taken off.

Note: Employer’s NIC are not deducted here.

£

Gross pay X

PAYE (X)

Employee’s NIC (X)

Other deductions (X)

–––

Net pay X

Payroll calculations

Overview

Payroll procedures : Chapter 6

87

Total wages expense

The total cost to the employer is the employee’s gross pay plus the employer’s national insurance contributions.

Wages expense = Gross pay + Employer’s NIC + Employer’s pension contributions

Liabilities

Once the employee has been paid, the company will be left with other liabilities:

PAYE/NIC – The total of the PAYE and both sets of NIC will be owed to the tax authorities

Items payable to other organisations, such as the amount owed to the pension fund or trade unions based on the monthly deductions.

Bookkeeping Controls

88

Example 1

John earns £12,000 per annum. His deductions for the month of May are:

£

PAYE 125

Employee’s NIC 80

Employer contribution to pension 50

Employee contribution to pension 50

Employer’s NIC 85

Calculate John’s net pay

£

Gross pay (12,000/12) 1,000

PAYE (125)

Employee’s NIC (80)

Other deductions (50)

–––

Net pay 745

The total cost to the employer of employing John will be the total of John’s gross pay, employer’s NIC and the employer’s pension contributions.

Total expense = 1,000 + 85 + 50 = £1,135

Finally, after paying John, the company will have the following liabilities:

Tax authorities (HMRC): £

PAYE 125

Employee’s NIC 80

Employer’s NIC 85

–––

Total owed 290

Pension liability (50 + 50) 100

Payroll procedures : Chapter 6

89

Bookkeeping Controls

90

The accounting for wages and salaries is based upon two fundamental principles.

The accounts must reflect the full cost to the employer of employing someone.

The accounts must show the liability payable to HMRC for PAYE and NIC.

We need accounts to record the wages expense and liabilities to external parties such as HMRC.

As part of the double entries, we will also use a third account, which is the wages control account.

Accounting for payroll

Overview

Payroll procedures : Chapter 6

91

The T accounts used will therefore be as follows:

1 The wages expense account

This shows the total expense to the business (Gross pay plus employer’s NIC). This is the expense account shown in the trial balance.

2 The liability accounts

The liability account to HMRC shows all the liabilities due to the tax authorities (namely PAYE and all NIC).

There could also be other liability accounts such as a pension liability if there are pension deductions.

3 The wages and salaries control account

One side of each double entry is put through the control account.

This account is cleared out each payroll run and there is never a balance brought down to take to the trial balance.

Bookkeeping Controls

92

The entries to be posted into the ledgers are as follows:

Firstly, record the TOTAL expense to the business (gross pay, employer’s NIC, employer pension contributions).

Dr Wages expense X

Cr Wages control X

Next, from the total expense, record the amount paid to the employee (net pay).

Dr Wages control X

Cr Bank X

Of the remaining amounts, record them in the appropriate liability accounts.

Dr Wages control X

Cr HMRC X (The total of PAYE and all NIC)

Dr Wages control X

Cr Pension liability/Trade union X

Payroll procedures : Chapter 6

93

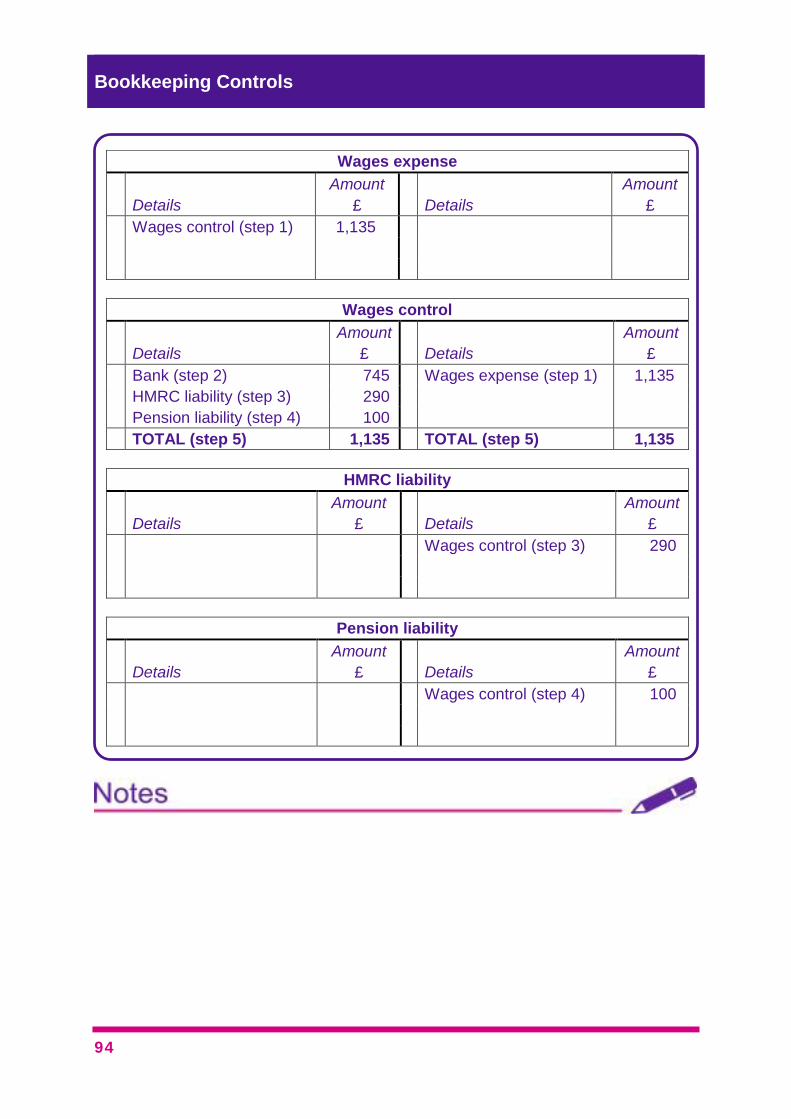

Illustration 1

Using the figures calculated for John’s pay earlier, the accounting entries will now be shown.

Step 1: Firstly, record total wage expense (Dr Wages expense, Cr Wages control).

Step 2: Next, record the amount paid to the employee in wages control (net pay of £745). Note: the bank T account is not given here as we are just looking at the payroll accounts.

Step 3: Now, split out the liabilities. Firstly, record the liability due to HMRC (the total of PAYE and all NIC, which is £290).

Step 4: Finally, record the pension liability of £50 (Dr Wages control, Cr Pension liability).

Step 5: Once all entries have been made, the wages control account can be balanced off to ensure there is no remaining balance. If there is a remaining balance carried down, an error has been made somewhere.

Bookkeeping Controls

94

Wages expense

Details

Amount

£

Details

Amount

£

Wages control (step 1) 1,135

Wages control

Details

Amount

£

Details

Amount

£

Bank (step 2) 745 Wages expense (step 1) 1,135

HMRC liability (step 3) 290

Pension liability (step 4) 100

TOTAL (step 5) 1,135 TOTAL (step 5) 1,135

HMRC liability

Details

Amount

£

Details

Amount

£

Wages control (step 3) 290

Pension liability

Details

Amount

£

Details

Amount

£

Wages control (step 4) 100

Payroll procedures : Chapter 6

95

Elements of payroll

Gross pay

Net pay

PAYE

Employee’s NIC

Employer’s NIC

Other deductions

Calculations

Net pay = Gross pay less employee’s deductions

Total expense = Gross pay plus Employer’s NIC

HMRC payable = PAYE plus all NIC

Accounting for payroll

1 Record total expense

2 Record payment to employee

3 Record HMRC liability

4 Record other liabilities

All entries go through the wages control account. Ensure that the wages controlaccount has no balance carried down at the end

Summary

Overview

Bookkeeping Controls

96

Further reading

For more detailed explanation, analysis and illustration of this topic please read Chapter 6 of the Bookkeeping Controls Study Text. Please complete any TYU that have not been completed in class.

Less detailed summaries can be found in Chapter 6 of the BKCL Pocket Notes.

You should now be able to answer these questions from the Exam Kit:

Question 4 – Ivano

Question 9 – Rhyme Time

Question 10 – Down and out

If you are attending a revision course, please do not attempt the Exam Kit questions until your tutor instructs you to do so.

Illustrations and further practice

Exam Kit questions

Payroll procedures : Chapter 6

97

Tutor’s question bank

Support Questions

Question 7 and question 8

More challenging questions:

Question 18 and question 19

These questions and answers may be printed off separately and distributed to students as necessary, to supplement the material listed above.

We recommend the following additional questions for the topics covered in this chapter:

Study Text (for teaching throughout the Chapter)

Payroll procedures (Chapter 6): TYU 4, TYU 5

Exam Kit

Questions 5, 7, 11

Additional tutor resources Additional tutor resources

Additional tutor guidance

Bookkeeping Controls

98

99

By the end of this session you should be able to:

understand the different items that can be included within a bank reconciliation

update the cash book and prepare a bank reconciliation

and answer questions relating to these areas.

Chapter 7 Bank reconciliations

Outcome

Outcome

The underpinning detail for this Chapter in your Workbook can be found in

Chapter 7 of your Study Text

Bookkeeping Controls

100

Updating the cash book

Bank reconciliation

Preparing bank

reconciliation

Overview

Overview

Bank reconciliations : Chapter 7

101

Bank reconciliations compare the balance per the bank statement to the balance per the cash book recorded by the business. The difference between the two is then explained.

At regular intervals the cashier must check that the cash book is correct by comparing the cash book with the bank statement.

However, at a particular date the balance as per the cash book and the balance as per the bank statement might not agree due to a number of reasons.

Items on the bank statement but not in the cash book

There may be some items that are accounted for on the bank statement but which have not been updated in the cash book.

These include bank charges, interest and other automated payments.

The cash book needs to be updated for these items. This will give a revised cash book balance.

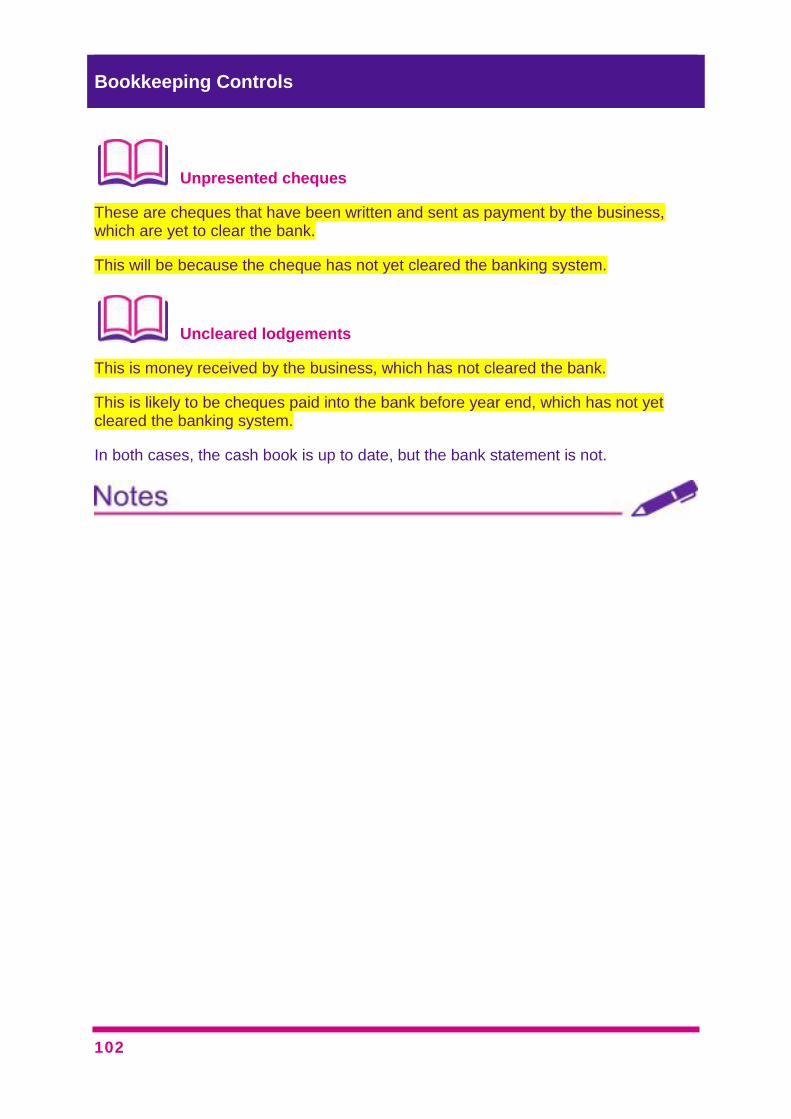

Items in the cash book but not on the bank statement

There are 2 major items that are recorded in the cash book but which have not yet been accounted for on the bank statement. These are:

unpresented cheques

uncleared lodgements.

Within a bank reconciliation question, it is likely that you will have to deal with both of these, so it is essential that you understand each one.

Understanding bank reconciliations

Basic principles of accounting

Bookkeeping Controls

102

Unpresented cheques

These are cheques that have been written and sent as payment by the business, which are yet to clear the bank.

This will be because the cheque has not yet cleared the banking system.

Uncleared lodgements

This is money received by the business, which has not cleared the bank.

This is likely to be cheques paid into the bank before year end, which has not yet cleared the banking system.

In both cases, the cash book is up to date, but the bank statement is not.

Bank reconciliations : Chapter 7

103

The bank reconciliation process

1 Agree the opening balance on the bank statement and in the cash book.

If the balance does not agree tick off any prior period reconciling itemswhich have caused the opening balances to disagree.

These items that have been crossed off the bank statement should thenbe ignored.

2 Agree that items on the bank statement appear in the cash book (tick off).

Use the amounts for this, as the descriptions may not match. Often thebanks statement will simply show a cheque number, while the cash bookwill have the details of the customer or supplier name.

If there are items on the bank statement that do not appear in the cashbook, update the cash book for these (these items now updated should beticked off).

3 Any un-ticked items in cash book (i.e. they have not appeared on the bank statement) are reconciling items, i.e. unpresented cheques or uncleared lodgements.

These will appear in the bank reconciliation statement.

To prove that the cash book and the bank statement closing balances agree through reconciliation, we must update the bank statement balance to reflect the entries that have been made to the cash book already.

We add any receipts to the bank amount that we have already added to thecash book balance.

We take away any payments from the bank amount that we have alreadydeducted from the cash book balance.

Producing bank reconciliations

Overview

Bookkeeping Controls

104

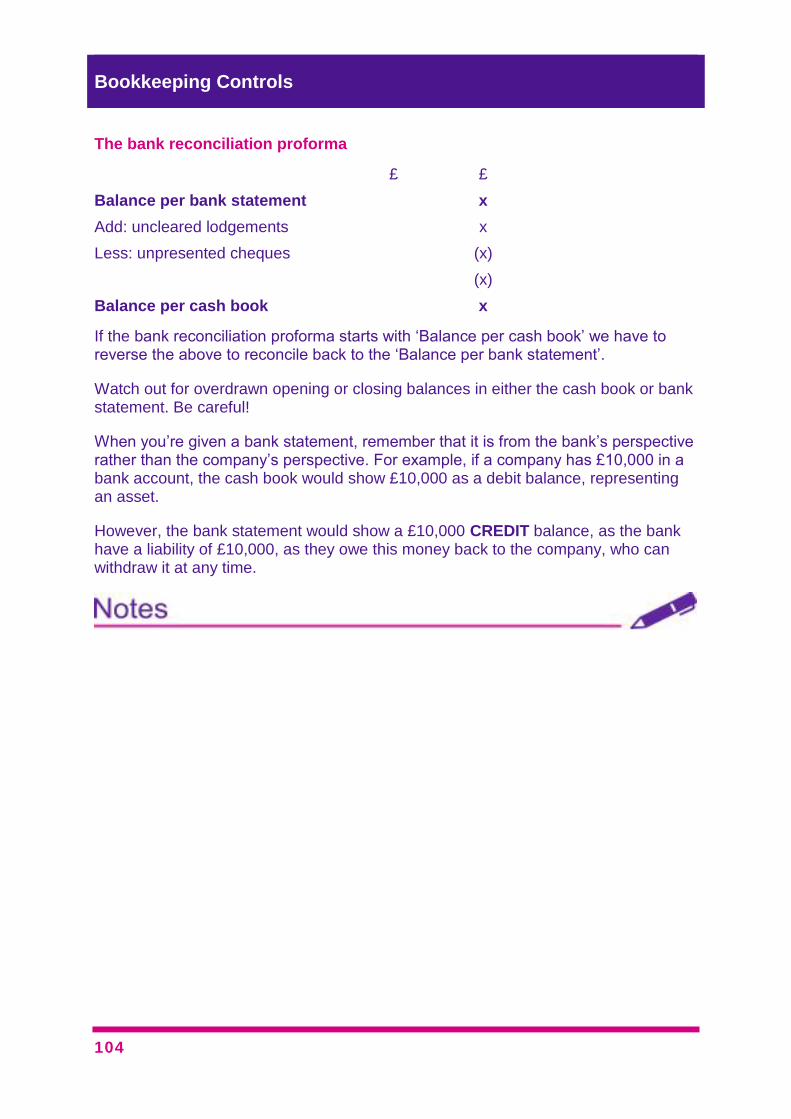

The bank reconciliation proforma

£ £

Balance per bank statement x

Add: uncleared lodgements x

Less: unpresented cheques (x)

(x)

Balance per cash book x

If the bank reconciliation proforma starts with ‘Balance per cash book’ we have to reverse the above to reconcile back to the ‘Balance per bank statement’.

Watch out for overdrawn opening or closing balances in either the cash book or bank statement. Be careful!

When you’re given a bank statement, remember that it is from the bank’s perspective rather than the company’s perspective. For example, if a company has £10,000 in a bank account, the cash book would show £10,000 as a debit balance, representing an asset.

However, the bank statement would show a £10,000 CREDIT balance, as the bank have a liability of £10,000, as they owe this money back to the company, who can withdraw it at any time.

Bank reconciliations : Chapter 7

105

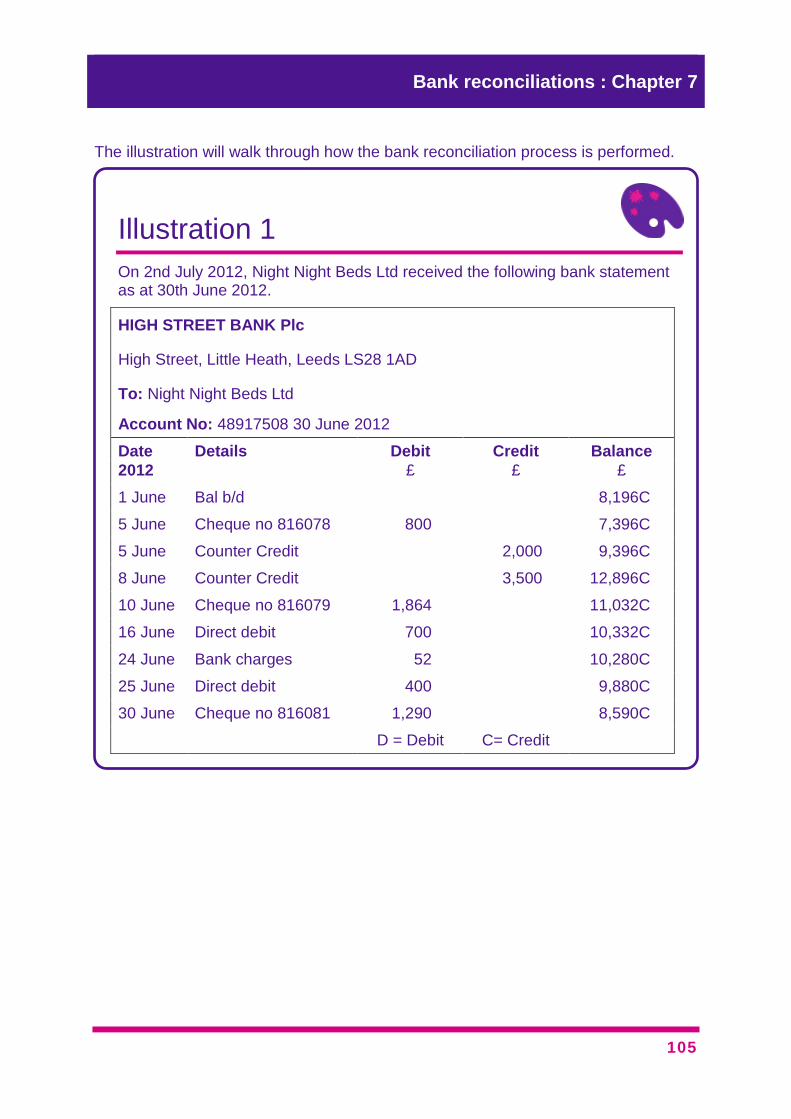

The illustration will walk through how the bank reconciliation process is performed.

Illustration 1

On 2nd July 2012, Night Night Beds Ltd received the following bank statement as at 30th June 2012.

HIGH STREET BANK Plc

High Street, Little Heath, Leeds LS28 1AD

To: Night Night Beds Ltd

Account No: 48917508 30 June 2012

Date Details Debit Credit Balance

2012 £ £ £

1 June Bal b/d 8,196C

5 June Cheque no 816078 800 7,396C

5 June Counter Credit 2,000 9,396C

8 June Counter Credit 3,500 12,896C

10 June Cheque no 816079 1,864 11,032C

16 June Direct debit 700 10,332C

24 June Bank charges 52 10,280C

25 June Direct debit 400 9,880C

30 June Cheque no 816081 1,290 8,590C

D = Debit C= Credit

Bookkeeping Controls

106

Night Night Beds Ltd's cash account for June 2012 was as follows.

Date 2012

Details Bank £

Date 2012

Cheque number

Details Bank £

1 June Balance b/d 7,396 1 June 816079 SpringRite 1,864

5 June Barbara’s Beds

2,000 5 June 816080 Fabric House 2,120

29 June JRB Ltd 5,120 22 June 816081 Heads Up 1,290

29 June 816082 John Joiner 7,400

29 June 816083 Foamies 200

Firstly, we need to agree the opening balances.

The opening balance on the bank statement doesn’t agree with the opening cash book balance, but this is due to the £800 cheque clearing the bank on 5 June, which would have been included in the previous month’s cash book.

Therefore the opening balance of £7,396 can be agreed. The £800 cheque on the bank statement is now dealt with, so can be ticked off.

Secondly, items on the bank statement should be agreed to the cash book and ticked off. Identify from the bank statement the items which have not been entered into the cash book. These are:

8 June – Counter credit of £3,500

16 June – Direct debit of £700

24 June – Bank charges of £52

25 June – Direct debit of £400.

Bank reconciliations : Chapter 7

107

These must be updated in the cash book. This is seen below.

Date 2012

Details Bank £

Date 2012

Cheque number

Details Bank £

1 June Balance b/d 7,396 1 June 816079 SpringRite 1,864

5 June Barbara’s Beds

2,000 5 June 816080 Fabric House 2,120

29 June JRB Ltd 5,120 22 June 816081 Heads Up 1,290

8 June Counter Credit

3,500 29 June 816082 John Joiner 7,400

29 June 816083 Foamies 200

16 June Direct debit 700

24 June Bank charges 52

25 June Direct debit 400

30 June Balance c/d 3,990

18,016 18,016

1 July Balance b/d 3,990

After entering these items into the cash book:

The closing bank balance per the bank statement is £8,590.

The closing balance per the cash book is £3,990.

This leaves a difference of £4,600.

Bookkeeping Controls

108

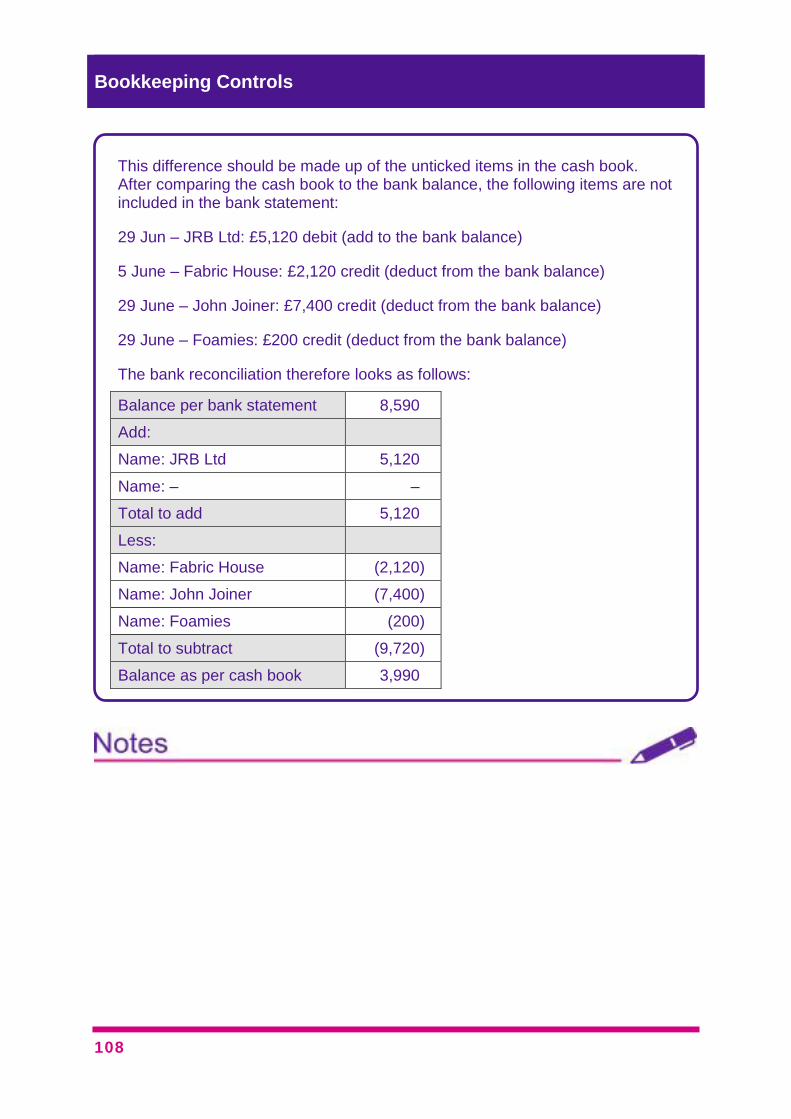

This difference should be made up of the unticked items in the cash book. After comparing the cash book to the bank balance, the following items are not included in the bank statement:

29 Jun – JRB Ltd: £5,120 debit (add to the bank balance)

5 June – Fabric House: £2,120 credit (deduct from the bank balance)

29 June – John Joiner: £7,400 credit (deduct from the bank balance)

29 June – Foamies: £200 credit (deduct from the bank balance)

The bank reconciliation therefore looks as follows:

Balance per bank statement 8,590

Add:

Name: JRB Ltd 5,120

Name: – –

Total to add 5,120

Less:

Name: Fabric House (2,120)

Name: John Joiner (7,400)

Name: Foamies (200)

Total to subtract (9,720)

Balance as per cash book 3,990

Bank reconciliations : Chapter 7

109

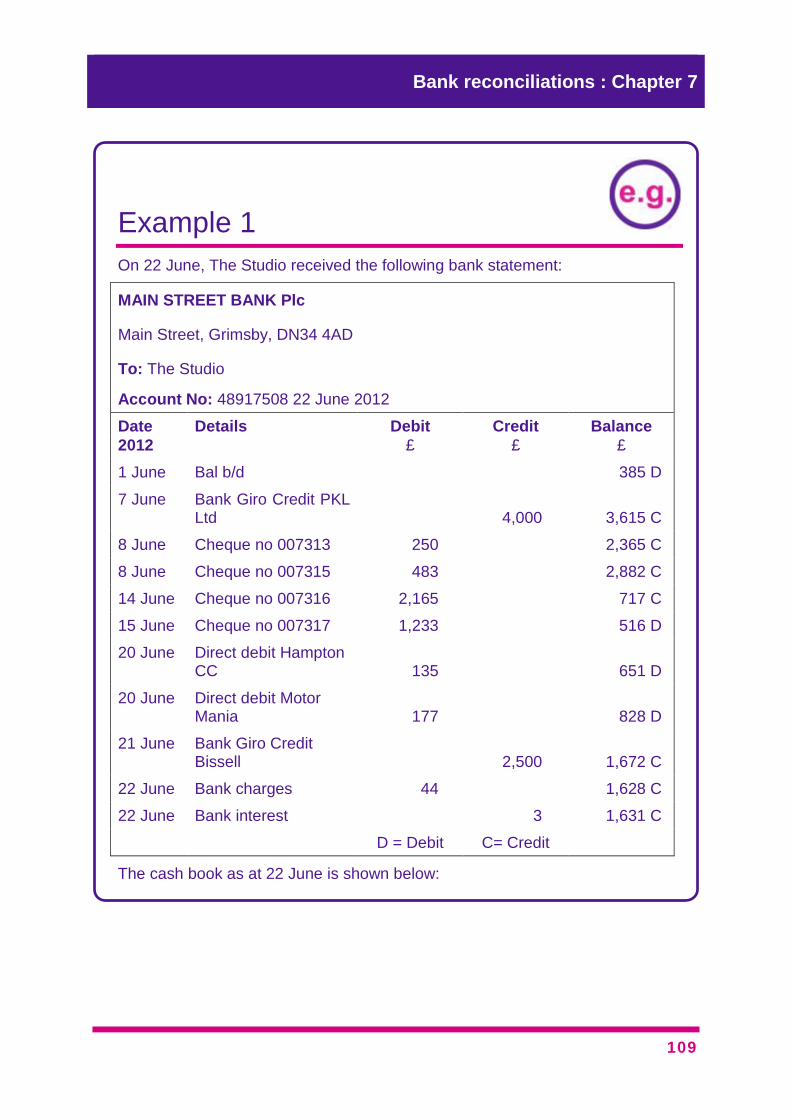

Example 1

On 22 June, The Studio received the following bank statement:

MAIN STREET BANK Plc

Main Street, Grimsby, DN34 4AD

To: The Studio

Account No: 48917508 22 June 2012

Date Details Debit Credit Balance

2012 £ £ £

1 June Bal b/d 385 D

7 June Bank Giro Credit PKL Ltd

4,000

3,615 C

8 June Cheque no 007313 250 2,365 C

8 June Cheque no 007315 483 2,882 C