BOETrends in Lending July09

12

Trends in Lending July 2009

Transcript of BOETrends in Lending July09

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 1/12

Trends in Lending

July 2009

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 2/12

BANK OF ENGLAND

Trends in Lending July 2009

This publication presents the Bank of England’s assessment of the latest trends in lending to the

UK economy. It draws mainly on long-established official data sources, such as the existing

monetary and financial statistics collected by the Bank. These data are supplemented by the

results of a new data set, established by the Bank in late 2008, to provide more timely data

covering aspects of lending to the UK corporate and household sectors.(1) The Bank collects

these data on behalf of the Lending Panel,(2) which was established by the Chancellor in

November 2008 to monitor lending to the UK economy and to promote best practice across theindustry in dealing with borrowers facing financial difficulties.

The new data set — referred to as ‘Lending Panel data’ — covers the major UK lenders:(3) Banco

Santander, Barclays, HSBC, Lloyds Banking Group, Nationwide and Royal Bank of Scotland.

Together they accounted for around 65% of the stock of lending to businesses, 50% of the stock

of consumer credit, and 70% of the stock of mortgage lending at the end of 2008. These data

have provided a useful input to discussions between the major lenders and Bank staff, giving

staff a better understanding of the business developments driving the figures and this

intelligence is reflected in the report. The report also draws on intelligence gathered by the

Bank’s regional Agents and from market contacts, as well as the results of other surveys. The

focus of the report is on lending, but broader credit market developments, such as those relating

to trade credit or capital market issuance, may be discussed where relevant.

The report covers official data up to May 2009, supplemented by Lending Panel data and

intelligence gathered up to end June 2009. Unless stated otherwise, the data reported cover

lending in both sterling and foreign currency, are expressed in sterling terms, and are not

seasonally adjusted. Lending Panel data are provided to the Bank on a ‘best endeavours’ basis.

This, together with their relative timeliness, means that they may not be as accurate as

established data sets. As a result, care is needed in interpreting the Lending Panel data

presented in this report.

(1) For a fuller background please refer to the first edition of Trends in Lending available at:www.bankofengland.co.uk/publications/other/monetary/TrendsApril09.pdf.

(2) The Lending Panel comprises Government, lenders, consumer, debt advice and trade bodies, regulators and the Bank of England. Seewww.hm-treasury.gov.uk/press_126_08.htm.

(3) Membership of the group of major UK lenders is based on the provision of credit to UK-resident companies and individuals, regardlessof the country of ownership.

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 3/12

Executive summary 3

1 Lending to UK businesses 4

2 Mortgage lending 7

3 Consumer credit 10

Glossary and other information 11

Contents

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 4/12

Executive summary 3

The flow of net lending to UK businesses remained negative in May. Some UK businesses repaid bank debt using funds raised on

the capital markets. But, taken together, funds raised by businesses from banks and capital markets remained weak. Spreads and

fees are reported to have risen in recent months, which the major UK lenders have attributed to higher longer-term funding costs

and credit risk, though some of them thought that spreads may now be close to reaching a plateau. And, for some major UK

lenders, a stabilisation in the economic outlook, as well as slightly more plentiful and cheaper funding, was expected to help them

make credit more available over the next three months. Lenders reported little actual or expected increase in demand for credit,

except for balance sheet restructuring.

Official data for May showed the lowest flow of total net mortgage lending since the monthly series began in April 1993, but the

major UK lenders reported that in June their flow of net mortgage lending rose a little. The major UK lenders reported a furtherrise in approvals for house purchase in June, suggesting that mortgage lending for house purchase may continue to strengthen in

coming months. Fixed mortgage rates rose in June, in part reflecting increases in swap rates. Some major UK lenders have

reported that signs of stabilisation in housing market activity and prices, and the margins prevailing on higher LTV products, have

slightly increased their appetite to lend at higher LTVs.

Net flows of consumer credit remained weak in May. Within the total, net consumer credit excluding credit cards remained

subdued, but was positive for the first time since December 2008. Spreads on credit card lending have continued to rise, reflecting

higher actual and expected default rates. None of the major UK lenders reported any plans to expand the availability of consumer

credit, and they had yet to detect any significant signs of an increase in demand.

Executive summary

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 5/12

4 Trends in Lending July 2009

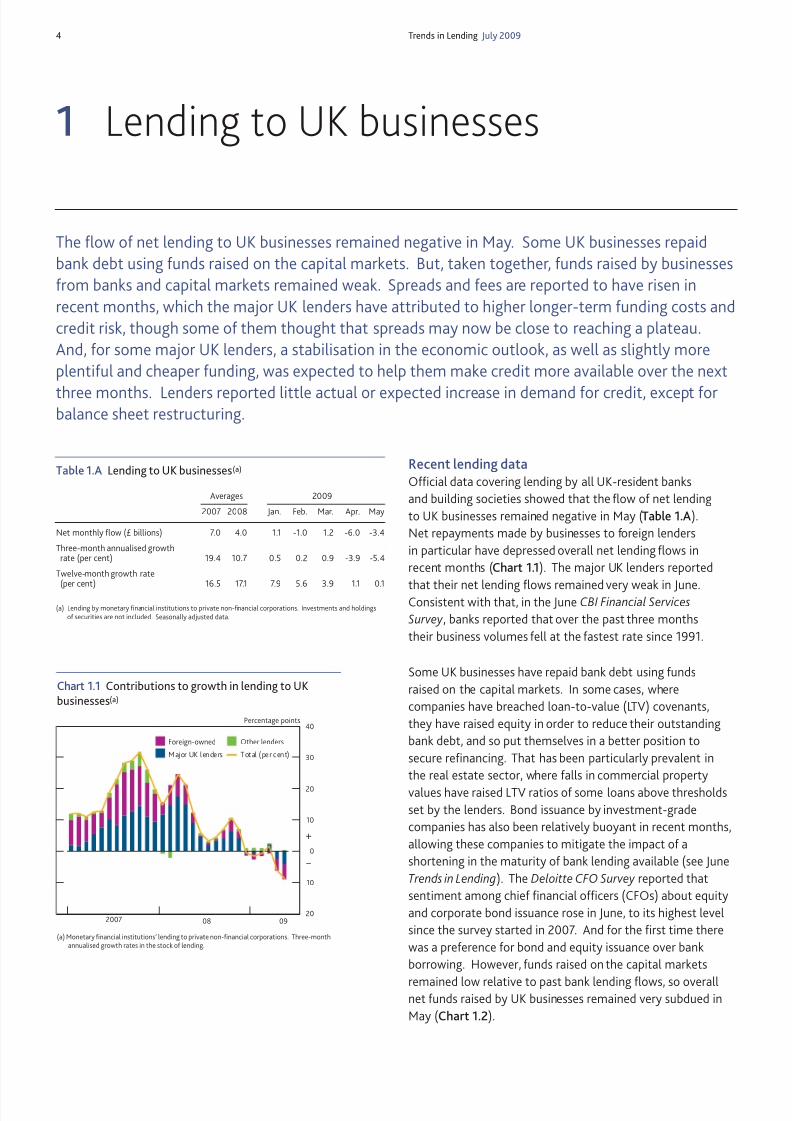

Recent lending dataOfficial data covering lending by all UK-resident banks

and building societies showed that the flow of net lending

to UK businesses remained negative in May (Table 1.A).

Net repayments made by businesses to foreign lenders

in particular have depressed overall net lending flows in

recent months (Chart 1.1). The major UK lenders reported

that their net lending flows remained very weak in June.Consistent with that, in the June CBI Financial Services

Survey , banks reported that over the past three months

their business volumes fell at the fastest rate since 1991.

Some UK businesses have repaid bank debt using funds

raised on the capital markets. In some cases, where

companies have breached loan-to-value (LTV) covenants,

they have raised equity in order to reduce their outstanding

bank debt, and so put themselves in a better position to

secure refinancing. That has been particularly prevalent in

the real estate sector, where falls in commercial property

values have raised LTV ratios of some loans above thresholds

set by the lenders. Bond issuance by investment-grade

companies has also been relatively buoyant in recent months,

allowing these companies to mitigate the impact of a

shortening in the maturity of bank lending available (see June

Trends in Lending). The Deloitte CFO Survey reported that

sentiment among chief financial officers (CFOs) about equity

and corporate bond issuance rose in June, to its highest level

since the survey started in 2007. And for the first time there

was a preference for bond and equity issuance over bank

borrowing. However, funds raised on the capital markets

remained low relative to past bank lending flows, so overallnet funds raised by UK businesses remained very subdued in

May (Chart 1.2).

1 Lending to UK businesses

The flow of net lending to UK businesses remained negative in May. Some UK businesses repaidbank debt using funds raised on the capital markets. But, taken together, funds raised by businessesfrom banks and capital markets remained weak. Spreads and fees are reported to have risen inrecent months, which the major UK lenders have attributed to higher longer-term funding costs andcredit risk, though some of them thought that spreads may now be close to reaching a plateau.And, for some major UK lenders, a stabilisation in the economic outlook, as well as slightly moreplentiful and cheaper funding, was expected to help them make credit more available over the next

three months. Lenders reported little actual or expected increase in demand for credit, except forbalance sheet restructuring.

20

10

0

10

20

30

40

2007 08 09

Percentage points

Other lendersForeign-owned

Major UK lenders Total (per cent)

+

–

(a) Monetary financial institutions’ lending to private non-financial corporations. Three-monthannualised growth rates in the stock of lending.

Chart 1.1 Contributions to growth in lending to UKbusinesses(a)

Table 1.A Lending to UK businesses(a)

Averages 2009

2007 2008 Jan. Feb. Mar. Apr. May

Net monthly flow (£ billions) 7.0 4.0 1.1 -1.0 1.2 -6.0 -3.4

Three-month annualised growthrate (per cent) 19.4 10.7 0.5 0.2 0.9 -3.9 -5.4

Twelve-month growth rate(per cent) 16.5 17.1 7.9 5.6 3.9 1.1 0.1

(a) Lending by monetary financial institutions to private non-financial corporations. Investments and holdingsof securities are not included. Seasonally adjusted data.

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 6/12

Section 1 Lending to UK businesses 5

10

5

0

5

10

15

20

2007 08 09

£ billions

Loans Bonds

Equity Total

+

–

(a) Private non-financial corporations. Loans are seasonally adjusted, but bond and equityissuance is not, as it has been found not to be significantly seasonal. Commercial paper isincluded within bonds.

Chart 1.2 Net funds raised by UK businesses(a) Corporate loan pricingThe total cost of bank finance to a company can be

decomposed into the fees charged by the bank to provide

facilities, the spread over a given reference rate (Libor or Bank

Rate) at which loans are offered, and the prevailing level of

that reference rate in the financial markets. In the Bank ofEngland’s 2009 Q2 Credit Conditions Survey a net balance of

lenders reported that spreads and fees had risen over the three

months to mid-June, though the net balance was much

smaller than in previous quarters (Chart 1.3). Contacts of the

Bank’s regional Agents have also continued to report paying

higher spreads and fees on renewed or extended facilities.

One factor that lenders have cited for the upward pressure on

spreads over Libor or Bank Rate has been the difficulty and

expense of raising longer-term funding. Funding conditions for

lenders have eased slightly over the past three months,moderating somewhat that influence on spreads. On the

other hand, in the Credit Conditions Survey lenders continued

to report that defaults and losses on loans to companies had

increased and were expected to rise further. This deterioration

in the credit quality of borrowers has caused lenders to widen

spreads to cover the higher expected cost of default. Looking

forward, in recent discussions with the Bank some major UK

lenders thought that spreads may be close to reaching a

plateau. Indeed, several reported recent instances where

renewed competition to grant loans had led to some

compression of spreads. Some lenders reported that a further

easing in longer-term funding conditions might also allow

them to reduce spreads over Libor or Bank Rate.

Supply and demandThe amount of lending and its price depend on the interaction

of demand and supply factors. Disentangling the separate

influences of changes in the supply of and demand for credit is

extremely difficult, though surveys can help. In the Credit

Conditions Survey a net balance of lenders reported that they

had increased the availability of credit over the past three

months, albeit by less than they had expected (Chart 1.4).

Some contacts of the Bank’s regional Agents felt that banks’appetite for lending had increased in June, but others

continued to report difficulties in accessing finance, notably in

the property and construction sectors and some retail sectors.

The flow of gross new facilities granted by the major UK

lenders has not changed significantly since the beginning of

the year (Chart 1.5). Those new facilities are reported to

continue to reflect mainly the refinancing of existing

customers’ facilities, and so have not flowed through into

additional (or net) lending.

A net balance of lenders in the Credit Conditions Survey

expected to increase further the availability of credit in

2009 Q3, particularly those lenders who have made lending

commitments under the Government’s Asset Protection

Scheme (APS). A stabilisation in the economic outlook, as well

80

70

60

50

40

30

20

10

0

10

20

Q2 Q4 Q2 Q4 Q2 Q2 Q4 Q2 Q4 Q2

2007 08 09 2007 08 09

Spread on loans Fees/commissions on loans

Net percentage balances

Increase in spreads and fees

+

–

(a) Net percentages are calculated by weighting together the responses of those lenders whoanswered the questions. The blue bars show the responses over the previous three months.The red diamonds show the expectations over the next three months. Expectations balanceshave been moved forward a quarter so that they can be compared with the actual outturns inthe following quarter.

(b) A negative balance indicates an increase in spreads and fees. Covers lending to medium-sizedcompanies only.

Chart 1.3 Credit Conditions Survey : spreads and fees onloans(a)(b)

60

50

40

30

20

10

0

10

20

30

40

50

Q2 Q4 Q2 Q4 Q2 Q2 Q4 Q2 Q4 Q2 Q2 Q4 Q2 Q4 Q2

2007 08 09 2007 08 09 2007 08 09

Availability of credit Demand frommedium PNFCs(c)

Demand fromlarge PNFCs(c)

Net percentage balances

+

–

(a) See footnote to Chart 1.3.(b) A positive balance indicates that more credit is available or there is greater demand.(c) Private non-financial corporations.

Chart 1.4 Credit Conditions Survey : corporate creditavailability and demand for credit(a)(b)

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 7/12

6 Trends in Lending July 2009

6

5

4

3

2

1

0

1

2

3

4

1988 91 94 97 2000 03 06 09

Per cent of nominal GDP

+–

Sources: ONS and Bank calculations.

(a) Private non-financial corporations. Four-quarter moving average is shown. Financial surplusis measured as the difference between total income and outgoings.

Chart 1.6 Financial surplus of UK businesses(a)

as slightly more plentiful and cheaper funding, was expected

to help increase credit availability.

In the Credit Conditions Survey , and in discussions with the

Bank, lenders have continued to report subdued demand for

new loans, in particular for capital investment. Contacts of theBank’s regional Agents have reported very weak investment

intentions and a preference for preserving cash — as their

normal tendency to hoard cash at a time of uncertain demand

is being exacerbated by concerns over the availability of

working capital. Since the beginning of 2008, the Deloitte CFO

Survey has reported that a net balance of companies think that

UK corporate balance sheets are overleveraged. Lower

spending on capital equipment and inventories by businesses

has allowed them to maintain a historically high financial

surplus (defined as total income net of outgoings) in the face

of lower profits (Chart 1.6). This financial surplus has beenused in part to repay bank debt and so reduce leverage.

Looking forward, in the Credit Conditions Survey lenders

expected some increase in loan demand from small and

medium-sized companies in 2009 Q3. Demand from large

companies was expected to be unchanged (Chart 1.4). The

divergence perhaps reflects the greater ability of large

companies to access the capital markets. Demand for lending

was still mainly expected to be for balance sheet restructuring

— the refinancing of existing loans, sometimes also requiring

the borrower to inject more equity. Weaker spending on

capital equipment and inventories was expected to continue toreduce demand for credit. In the June Deloitte CFO Survey

there was a big increase in the percentage of companies

expecting mergers and acquisitions (M&A) activity to increase

over the next year. But in the Credit Conditions Survey , and in

discussions with the Bank, lenders reported only very tentative

expectations of greater loan demand for that purpose.

0

2

4

6

8

10

12

Dec. Jan. Feb. Mar. Apr. May June

£ billionsOther

Construction

Renting andother business activities

Hotels and restaurants

Wholesale and retail trade

Manufacturing

Real estate

2008 09

(a) Lending Panel data, available from December 2008 only. Lending Panel data are generally oflower quality than existing data sources and have a short history. As a result, less weightshould be attached to this chart than to those using existing data sources.

Chart 1.5 Gross new loan facilities granted by the majorUK lenders(a)

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 8/12

Section 2 Mortgage lending 7

Recent lending dataOfficial data covering all lenders showed that total net

mortgage lending fell in May (Table 2.A), the weakest flow

since the monthly series began in April 1993. But the major

UK lenders reported that in June their flow of net mortgage

lending rose a little (Chart 2.1). Data collected from the major

UK lenders for the Lending Panel provide a split of gross

lending (lending before repayments are deducted) between

house purchase and the refinancing of existing mortgages

(remortgaging). Chart 2.1 shows that since the beginning of

the year gross mortgage lending for house purchase by the

major UK lenders has been rising. Until May that had been

more than offset by weaker remortgaging activity, but in June

remortgaging activity also edged higher, leading to the first

increase in total gross mortgage lending by the major UK

lenders since April 2008.

The increase in gross mortgage lending for house purchase by

the major UK lenders reflects the increase in approvals for

house purchase since the beginning of the year. Approvals rose

further in June in the Lending Panel data (Chart 2.2),suggesting that mortgage lending for house purchase may

continue to strengthen in coming months.

Mortgage pricingIn May, the Bank’s measure of the overall effective mortgage

rate paid by individuals was little changed. But in June many

lenders announced increases in their fixed mortgage rates, and

the Bank’s measure of quoted two-year fixed mortgage rates

rose (Chart 2.3). Fixed rates increased by more than

comparable two-year swap rates, leading to a further widening

in the spread between them. This spread has risen significantly

since the onset of the financial crisis, which lenders have

attributed to higher longer-term funding costs and greater

credit risk. But discussions with the major UK lenders

indicated that, for some, the most recent increase in spreads

2 Mortgage lending

Official data for May showed the lowest flow of total net mortgage lending since the monthly seriesbegan in April 1993, but the major UK lenders reported that in June their flow of net mortgagelending rose a little. The major UK lenders reported a further rise in approvals for house purchase in June, suggesting that mortgage lending for house purchase may continue to strengthen in comingmonths. Fixed mortgage rates rose in June, in part reflecting increases in swap rates. Some majorUK lenders have reported that signs of stabilisation in housing market activity and prices, and themargins prevailing on higher LTV products, have slightly increased their appetite to lend at higher

LTVs.

0

5

10

15

20

25

Jan July Jan.

House purchase

Other

Remortgaging

Gross lending

Net lending

Net lending

£ billions

Lending Panel data

2008 09

(a) The split in 2008 is estimated using gross lending data and the split of loan approval valuesbetween house purchase, remortgaging and other advances. The split using Lending Paneldata in 2009 is reported, rather than estimated, data. Seasonally adjusted data.

(b) Lending Panel data are generally of lower quality than existing data sources.

Chart 2.1 Gross mortgage lending by the major UKlenders(a)(b)

Table 2.A Secured lending to individuals(a)

Averages 2009

2007 2008 Jan. Feb. Mar. Apr. May

Net monthly flow (£ billions) 9.0 3.4 0.9 1.4 0.6 0.9 0.3

Three-month annualised growthrate (per cent) 10.4 4.0 1.2 1.4 0.9 0.9 0.6

Twelve-month growth rate(per cent) 11.0 6.9 2.9 2.4 1.9 1.5 1.3

(a) Lending by monetary financial institutions and other lenders to UK individuals. Seasonally adjusted data.

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 9/12

8 Trends in Lending July 2009

may also have reflected the strength of demand for fixed-rate

mortgages relative to their capacity to fund them. Since the

beginning of the year, borrowers have increasingly chosen to

take out fixed-rate mortgages, which accounted for around

70% of new mortgages in May.

Supply and demandAs with corporate lending, it is difficult to identify precisely the

separate influences on overall mortgage lending of changes in

the supply of and demand for mortgages. On the supply side,

in the Credit Conditions Survey a net balance of lenders

reported that there had been an increase in the availability of

secured credit to households over the three months to

mid-June, the first significantly positive balance since the

survey began in 2007 Q2 (Chart 2.4). As with lending to

businesses, that partly reflects the impact of the lending

commitments made under the Government’s APS. The majorUK lenders have reported that approval rates for mortgages

have edged higher in recent months.

Over the past few months contacts of the Banks’ regional

Agents have reported an increase in the range of mortgage

products available. And according to Moneyfacts Group, the

number of 90%-plus LTV mortgages available increased

slightly in both May and June, though remains only around one

tenth of the number on offer a year ago. Moreover, the extra

cost of borrowing at 90% LTV relative to 75% LTV is much

higher than prior to the onset of the financial crisis (Chart 2.3).

Some major UK lenders have reported that signs of

stabilisation in housing market activity and prices, and the

margins prevailing on higher LTV products, have made them a

little more inclined to lend at higher LTV ratios. Consistent

with that, a net balance of lenders in the Credit Conditions

Survey expected to increase the availability of mortgages to

higher (>75%) LTV borrowers in 2009 Q3, alongside a slight

easing in credit scoring criteria (Chart 2.4). The slight increase

in risk appetite may have been supported by lower than

expected increases in default rates on secured lending over the

past three months. In discussions with the Bank, most lenderssaid they had become less pessimistic about defaults since the

beginning of the year. And in June the Council of Mortgage

Lenders revised down its projections for arrears and

repossessions in 2009, citing the beneficial effects of low

interest rates and increased forbearance by the lenders.

In the Credit Conditions Survey , demand for mortgages for

house purchase was reported to have increased in the three

months to mid-June. The Royal Institution of Chartered

Surveyors’ (RICS) new buyer enquiries balance has continued

to rise in recent months, indicating that demand for mortgages

for house purchase may rise further. And the major UK lenders

have reported rising applications for house purchase

mortgages. But lenders and the Bank’s regional Agents have

said that difficulties in valuing properties in present market

0

2

4

6

8

2007 08 09

Per cent

95% loan-to-value(b) 90% loan-to-value(c)

75% loan-to-value

Two-year swap rate(d)

(a) The Bank’s quoted interest rates series comprise data from up to 31 monetary financialinstitutions.

(b) Series finishes in April 2008, as thereafter only two or fewer products are offered.(c) Series is only available on a consistent basis back to May 2008, as earlier periods require a

greater degree of estimation, and is not published for March-May 2009 as only two or fewerproducts were offered in that period. The Ju ne observation is marked with the diamond.

(d) End-month rate.

Chart 2.3 Quoted interest rates on two-year fixed-ratemortgages(a)

80

60

40

20

0

20

40

60

Q2 Q4 Q2 Q4 Q2 Q2 Q4 Q2 Q4 Q2 Q2 Q4 Q2 Q4 Q2

2007 08 09

Overall creditavailability

Availability toborrowers withmore than 75%loan to value

Changes in creditscore criteria

Net percentage balances

n.a.

Tighter criteria

2007 08 09 2007 08 09

+

–

(a) See footnote to Chart 1.3.(b) A positive balance indicates that more credit is available or credit score criteria are less strict.

The balance for overall credit availability in 2007 Q3 was 0.1 but is not visible on the chart.

Chart 2.4 Credit Conditions Survey : mortgage credit

availability(a)(b)

0

20

40

60

80

100

120

140

2007 08 09

Major UK lenders(b)

Major UK lenders (Lending Panel data)(b)

Total(c)

Thousands

(a) Seasonally adjusted.(b) Gross approvals data.(c) Monetary financial institutions and other lenders. These data are net of cancellations and

hence the total can fall below the gross approvals data shown for the major UK lenders.

Chart 2.2 Approvals for mortgages for house purchase(a)

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 10/12

Section 2 Mortgage lending 9

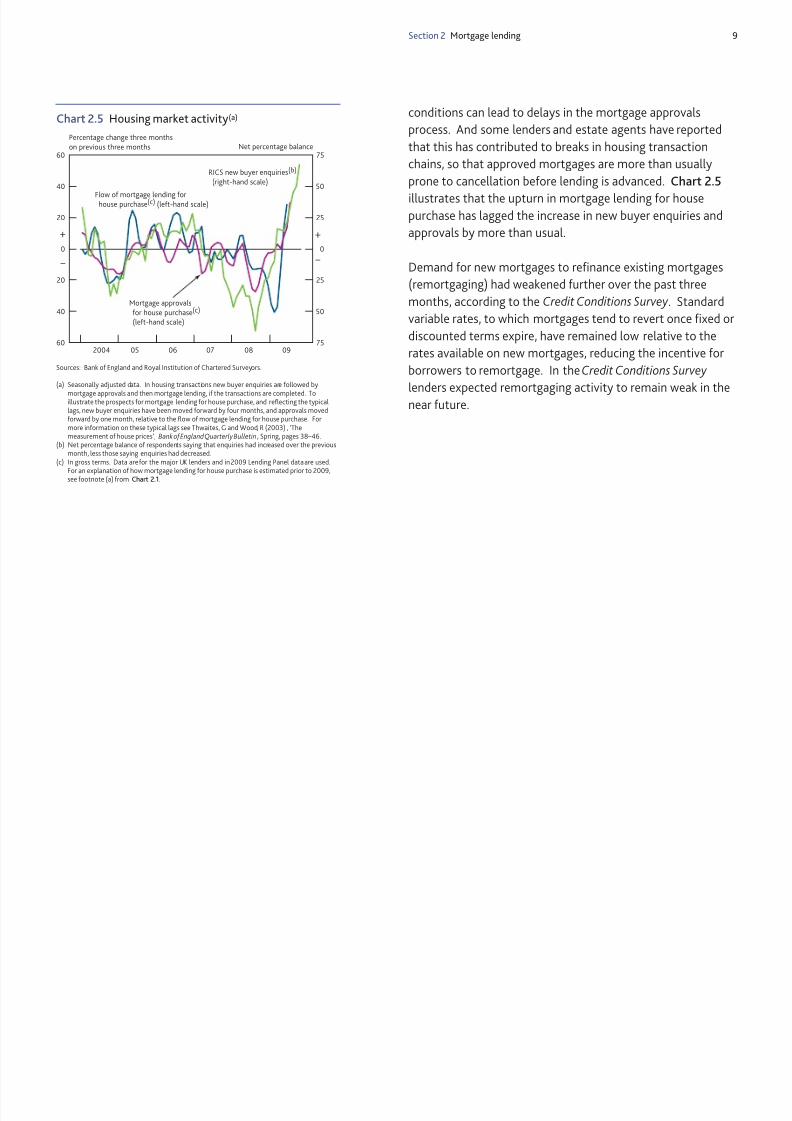

conditions can lead to delays in the mortgage approvals

process. And some lenders and estate agents have reported

that this has contributed to breaks in housing transaction

chains, so that approved mortgages are more than usually

prone to cancellation before lending is advanced. Chart 2.5

illustrates that the upturn in mortgage lending for housepurchase has lagged the increase in new buyer enquiries and

approvals by more than usual.

Demand for new mortgages to refinance existing mortgages

(remortgaging) had weakened further over the past three

months, according to the Credit Conditions Survey . Standard

variable rates, to which mortgages tend to revert once fixed or

discounted terms expire, have remained low relative to the

rates available on new mortgages, reducing the incentive for

borrowers to remortgage. In the Credit Conditions Survey

lenders expected remortgaging activity to remain weak in thenear future.

60

40

20

0

20

40

60

2004 05 06 07 08 0975

50

25

0

25

50

75Net percentage balance

Percentage change three monthson previous three months

RICS new buyer enquiries(b)

(right-hand scale)

Flow of mortgage lending forhouse purchase(c) (left-hand scale)

Mortgage approvalsfor house purchase(c)

(left-hand scale)

+

–

+

–

Chart 2.5 Housing market activity(a)

Sources: Bank of England and Royal Institution of Chartered Surveyors.

(a) Seasonally adjusted data. In housing transactions new buyer enquiries are followed by

mortgage approvals and then mortgage lending, if the transactions are completed. Toillustrate the prospects for mortgage lending for house purchase, and reflecting the typicallags, new buyer enquiries have been moved forward by four months, and approvals movedforward by one month, relative to the flow of mortgage lending for house purchase. Formore information on these typical lags see Thwaites, G and Wood, R (2003) , ‘Themeasurement of house prices’, Bank of England Quarterly Bulletin, Spring, pages 38–46.

(b) Net percentage balance of respondents saying that enquiries had increased over the previousmonth, less those saying enquiries had decreased.

(c) In gross terms. Data are for the major UK lenders and in 2009 Lending Panel data are used.For an explanation of how mortgage lending for house purchase is estimated prior to 2009,see footnote (a) from Chart 2.1.

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 11/12

10 Trends in Lending July 2009

Recent lending data

Total net consumer credit flows remained weak in May(Table 3.A), so the twelve-month growth rate in the stock of

consumer credit continued to drift down. Within the total, net

consumer credit excluding credit cards remained subdued, but

was positive for the first time since December 2008 (Chart 3.1).

The major UK lenders in aggregate also reported a very slight

improvement in net lending via personal loans in June.

Consumer credit pricingEffective interest rates on overdrafts and personal loans have

fallen in recent months, though by much less than Bank Rate

and Libor. By contrast, rates on credit cards have remained

broadly unchanged. This widening in spreads is reported toreflect in part lenders’ perceptions of heightened credit risk on

consumer credit. In the 2009 Q2 Credit Conditions Survey

default rates and losses on consumer credit were reported to

have risen over the past three months, and further increases

were anticipated. Chart 3.2 shows how, for credit cards, this

has coincided with the sharp increase in spreads.

Supply and demandA net balance of lenders in the Credit Conditions Survey

reported that they had reduced the availability of consumer

credit over the past three months, and by more than they hadanticipated. Over the next three months, lenders expected

credit limits to be reduced and credit scoring criteria to be

tightened further. In discussions with the Bank, none of the

major UK lenders indicated any plans to expand the availability

of consumer credit.

The tentative recovery in net consumer credit excluding credit

cards might be consistent with the recent pick-up in private car

sales, some of which is likely to have been financed by personal

loans. According to the Society of Motor Manufacturers and

Traders, new private car registrations in June were 4% higher

than a year ago, the first positive annual growth rate since

November 2007. But in discussions with the Bank, the major

UK lenders had yet to detect any significant signs of an

increase in demand for personal loans.

3 Consumer credit

Net flows of consumer credit remained weak in May. Within the total, net consumer creditexcluding credit cards remained subdued, but was positive for the first time since December 2008.Spreads on credit card lending have continued to rise, reflecting higher actual and expected defaultrates. None of the major UK lenders reported any plans to expand the availability of consumercredit, and they had yet to detect any significant signs of an increase in demand.

0.5

0.0

0.5

1.0

1.5

2.0

2.5

2007 08 09

£ billions

Other consumer credit

Credit cardTotal

+

–

(a) Flow of net unsecured lending by monetary financial institutions and other lenders to UKindividuals. Seasonally adjusted data. Sterling lending only.

Chart 3.1 Consumer credit(a)

30

20

10

0

10

20

30

40

50

60

70

2007 08 09

7

8

9

10

11

12

13

14

15

16

17

Spread of quoted credit card ratesover three-month Libor(c)

(right-hand scale)

Percentage pointsNet percentage balances

+

–

June Dec. June Dec. June

(a) See footnote to Chart 1.3.(b) A positive balance indicates an increase in default rates.(c) The Bank’s quoted interest rates series comprise data from up to 31 monetary financial institutions.

Chart 3.2 Credit Conditions Survey : change in default rateson credit cards(a)(b)

Table 3.A Consumer credit(a)

Averages 2009

2007 2008 Jan. Feb. Mar. Apr. May

Net monthly flow (£ billions) 1.1 1.0 0.1 0.1 0.0 0.2 0.3

Three-month annualised growthrate (per cent) 6.4 5.3 2.1 0.9 0.4 0.6 0.9

Twelve-month growth rate(per cent) 6.1 6.3 4.7 3.6 3.1 2.8 2.3

(a) Unsecured lending by monetary financial institutions and other lenders to UK individuals. Seasonallyadjusted data. Sterling lending only.

8/14/2019 BOETrends in Lending July09

http://slidepdf.com/reader/full/boetrends-in-lending-july09 12/12

Glossary and other information 11

AbbreviationsAPS – Asset Protection Scheme (see below).

CBI – Confederation of British Industry.

CFO – chief financial officer.

Libor – London interbank offered rate (see below).

LTV – loan to value ratio (see below).M&A – mergers and acquisitions.

ONS – Office for National Statistics.

PNFCs – private non-financial corporations (see below).

RICS – Royal Institution of Chartered Surveyors.

GlossaryAsset Protection A Government scheme that provides

Scheme lenders with partial protection, in return

for a fee, against credit losses on

portfolios of assets.Bank Rate The official rate paid on commercial bank

reserves by the Bank of England.

Businesses Private non-financial corporations (see

below).

Consumer credit Borrowing by UK individuals to finance

expenditure on goods and/or services.

Consumer credit is split into two

components: credit card lending

and ‘other’ lending (mainly overdrafts

and other loans/advances).

Effective interest The weighted average of calculated

rates interest rates on various types of deposit

and loan accounts. The calculated

annual rate is derived from the deposit or

loan interest flow during the period,

divided by the average stock of deposit or

loan during the period.

Facility An agreement in which a lender sets out

the conditions on which it is prepared to

commit to advance a specified amount

to a borrower within a defined period.

Gross lending The total value of loans advanced by an

institution in a given period.Loan approvals Lenders’ firm offers to advance credit.

Loan to value ratio Ratio of outstanding loan amount to the

(LTV) market value of the asset against which

the loan is secured (normally residential

or commercial property).

London interbank The rate of interest at which banks

offered rate (Libor) borrow funds from each other, in

marketable size, in the London interbank

market.

Major UK lenders Banco Santander, Barclays, HSBC,

Lloyds Banking Group, Nationwide and

Royal Bank of Scotland.

Monetary financial A statistical grouping comprising banks

institutions and building societies.

Mortgage lending Lending to households, secured against

the value of their dwellings.

Net lending The difference between gross lending and

gross repayments of debt in a givenperiod.

Private All corporations whose primary activity is

non-financial non-financial, and that are not controlled

corporations by central or local government.

Quoted interest The weighted average of a sample of

rates advertised deposit and loan rates:

weights calculated from Bank of England

statistical collections.

Reference rate The rate on which loans to businesses are

set, with an agreed margin over the

reference rate (typically these will beBank Rate or Libor).

Remortgaging A process whereby borrowers repay

their current mortgage in favour of a new

one secured on the same property.

Swap rate The fixed rate of interest in a swap

contract in which floating-rate interest

payments are exchanged for fixed-rate

interest payments. Swap rates are a key

factor in the setting of fixed mortgage

rates.

Symbols and conventionsExcept where otherwise stated, data are not seasonally

adjusted and the source of data in charts and tables is the

Bank of England.

On the horizontal axes of graphs, larger ticks denote the first

observation within the relevant period, eg data for the first

quarter of the year.

© Bank of England 2009

ISSN: 2040-4042 (online)