Body & Ending

77

1 Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank” 1.1 Origin of the Report This report is based on an internship program. IBTRA arranges internship program to gather practical knowledge about banking activities followed by AIBL for University students as Universities conducted with different organization after the completion of theoretical courses of program of Bachelor of Business Administration (BBA). Each internee must carry out a specific report, which is assigned by the University. We select Al-Arafah Islami bank Limited (AIBL) for my internship & since then I have started my realistic orientation program in Foreign Exchange Department. But I have prepared my report on General Banking, Investment & Foreign Exchange as it is assigned by the University. Hence I was placed in Banani Branch of Al-Arafah Islami bank Limited from 19 th September to 19 th December , 2012. 1.2 Objective of the study The first objective of writing the report is fulfilling the partial requirements of the BBA program. In this report, I have attempted to give on overview of Al-Arafah Islami bank Limited in general. Following are the main objectives To familiar the history and operations of Islami Banking in Bangladesh. To show the investment mechanism and product offerings in different modes of AIBL. To show overall investment proposal, appraisal procedures, documentation system of AIBL and Conventional Banks.

description

Internship report

Transcript of Body & Ending

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

1.1 Origin of the Report

This report is based on an internship program. IBTRA arranges internship program to gather

practical knowledge about banking activities followed by AIBL for University students as

Universities conducted with different organization after the completion of theoretical courses

of program of Bachelor of Business Administration (BBA). Each internee must carry out a

specific report, which is assigned by the University. We select Al-Arafah Islami bank

Limited (AIBL) for my internship & since then I have started my realistic orientation

program in Foreign Exchange Department. But I have prepared my report on General

Banking, Investment & Foreign Exchange as it is assigned by the University.

Hence I was placed in Banani Branch of Al-Arafah Islami bank Limited from 19 th September

to 19th December , 2012.

1.2 Objective of the study

The first objective of writing the report is fulfilling the partial requirements of the BBA

program. In this report, I have attempted to give on overview of Al-Arafah Islami bank

Limited in general. Following are the main objectives

To familiar the history and operations of Islami Banking in Bangladesh.

To show the investment mechanism and product offerings in different modes of

AIBL.

To show overall investment proposal, appraisal procedures, documentation system of

AIBL and Conventional Banks.

To show the differences with conventional banking regarding investments aspects.

To identify strength and weakness of investments of AIBL.

To identify the problems related to investments faced by AIBL.

To recommend actions that may be necessary to redesign the investments of AIBL.

1.3 Justification of the study

In our economy, there are mainly three types of schedule commercial banks are in operation.

They are Nationalized Commercial Banks, Local Private Commercial Banks and Foreign

Private Commercial Banks. Islami Bank has discovered a new horizon in the field of banking

area, which offers different General Banking, Investments and Foreign Exchange banking

system. So I have decided to study on the topic “General Banking, Investment and Foreign

Exchange”. Because the Internship program of the university is an integral part of the BBA

program. So it is obligatory to undertake such task by the students who desirous to complete

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

and successfully end-up their BBA degree. This also provides an opportunity to the students

to minimize the gap between theoretical and practical knowledge. During the internship

program the teachers of the department are attached to actively and constantly guide the

students. A student are required to work on a specific topic based on their theoretical and

practical knowledge acquired during the period of the internship program and then submits it

to the teacher. That is why I have prepared this report.

1.4 Methodology of the study

For carrying out this project paper I had to study the actual banking operations of AIBL.

In order to carry out this study, two sources of data and information have been used:

a) Primary data

I discussed with the executives & officials of the AIBL and found the approximate data,

which has been presented in the report. I also discussed with the officials of conventional

Banks regarding the issue and found necessary information, which has been presented in the

report.

b) Secondary data

Annual Reports of 2011 of Al-Arafah Islami Bank Ltd.

Desk report of the related department

Manuals of Al-Arafah Islami Bank Ltd (Bai-Murabaha, Bai-Muajjal, Bai-Salam,

Musharaka)

Training sheets which are provided by Islami Bank Training and Research Academy

(IBTRA).

1.5 Scope of the report

The scope of this paper is limited to the organizational structure, background, and objectives,

functions, and investment performance of AIBL as a whole. The scope is also limited to

different investment schemes, modes, mechanism, investment proposal appraisal procedures,

monitoring and documentation of AIBL.

1.6 Limitations of the study

There are some limitations in our study. We faced some problems during the study which we

are mentioning them as below-

i) Lack of time

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

The time period of this study is very short. I had only 4 weeks in my hand to complete this

report, which was not enough. So I could not go in depth of the study. Most of the times the

officials were busy and were not able to give us much time.

ii) Insufficient data

Some desired information could not be collected due to confidentiality of business.

iii) Lack of monitory support

Few officers sometime felt disturbed, as they were busy in their job. Sometime they didn’t

want to supervise us out of their official work.

1.7 What is Islamic Banking?

Islamic bank is a financial Institution that operates with the objective to implement and

materialize the economic and financial principles of Islam in the banking area. The

organization of Islamic conference (OIC) defines an Islamic bank as “a financial institution

whose statutes, rules and procedures expressly state its commitment to the principals of

Islamic Shariah and to the banning of the receipt and payment of interest on any of its

operation.”

According Islamic banking Act 1983 of Malaysia Islamic bank is a “company, which carries

on Islamic banking business. Islamic banking business means banking business whose aims

and operations do not involve any element which is not approved by the religion of Islam.”

It appears from the above definitions that Islamic banking is system of financial

intermediation that avoids receipt and payment of interest in its transactions and conducts its

operations in a way that it helps achieve the objectives of an Islamic economy. Alternatively,

this is a banking system whose operation is based on Islamic principles of transactions of

which profit and loss sharing (PLS) is a major feature, ensuring justice and equity in the

economy. That is why Islamic banks are often known as PLS-banks.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

1.8 Why Islamic Bank?

The objective of Islamic banking is not only to earn profit, but also to do good and welfare to

the people. Islam upholds the concept that money, income and property belong to Allah and

this wealth is to be used for the good of the society.

Islamic banks operate on Islamic principals of profit and loss sharing, strictly avoid interest,

which is the root of exploitation and is responsible for large-scale information and

unemployment. An Islamic bank is committed to do away with disparity and establish justice

in the economy, trade, commerce and industry, build socio-economic infrastructure and

create employment opportunities.

1.9 RIBA and its basic features

The word used by the Quran concerning ‘interest’ is Riba. The literal meanings of Riba are

money increase, increase of anything or increment of anything from its original amount

(Maududi 1979, p.84). However, all increases are not considered as Riba in Islam. Money

may increase in business activities as well. This increase is not at all considered as Riba. The

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

increase, instead of being prohibited (Haram), is approved (Halal) in Islam. Islam prohibits

only those increases that are charged on the loan with a prefixed rate.

Muslim scholars equate interest with Riba. In the Shariah, Riba technically refers to the

premium that must be paid by the borrower to the lender along with the principal amount as

a condition for the loan or for an extension in its maturity (Chapra 1985, p.64). In other

words, Riba is the predetermined return on the use of money. In the past there has been

dispute about whether Riba refers to interest or usury, but there is now consensus among

Muslim scholars that the term covers all forms of interest and not only “excessive” interest

(Khan 1985, p.52).

Imam al Rajhi describes, “During the era of Jahiliah people invested their money and

charged Riba on a monthly basis, though the invested amount remained unchanged. Money

so invested was called back at the time of repayment. In case of the borrower being unable to

pay back, the lender extended the period of repayment enhancing the amount to be paid on

and above the principal amount.” Abu Bakr al Jasas writes, “During the period of Ignorance

the lender and borrower came to an agreement that the borrower would pay back within a

specified period the principal amount along with the agreed upon excess.” Ibne Hajar

Askalani says, “Excess goods or money charged on and above principal amount is Riba.”

The basic characteristics of Riba are -

Origin of riba is loan(Quard or Dayn)

Riba is excess over and above the principal loan

Riba is charged or paid only as a condition of loan or time and no other recompense,

price or exchange value is paid for the excess or Riba

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Riba is related with time and become double and redouble and multiple with passage

time

Riba is not related with the result of business.

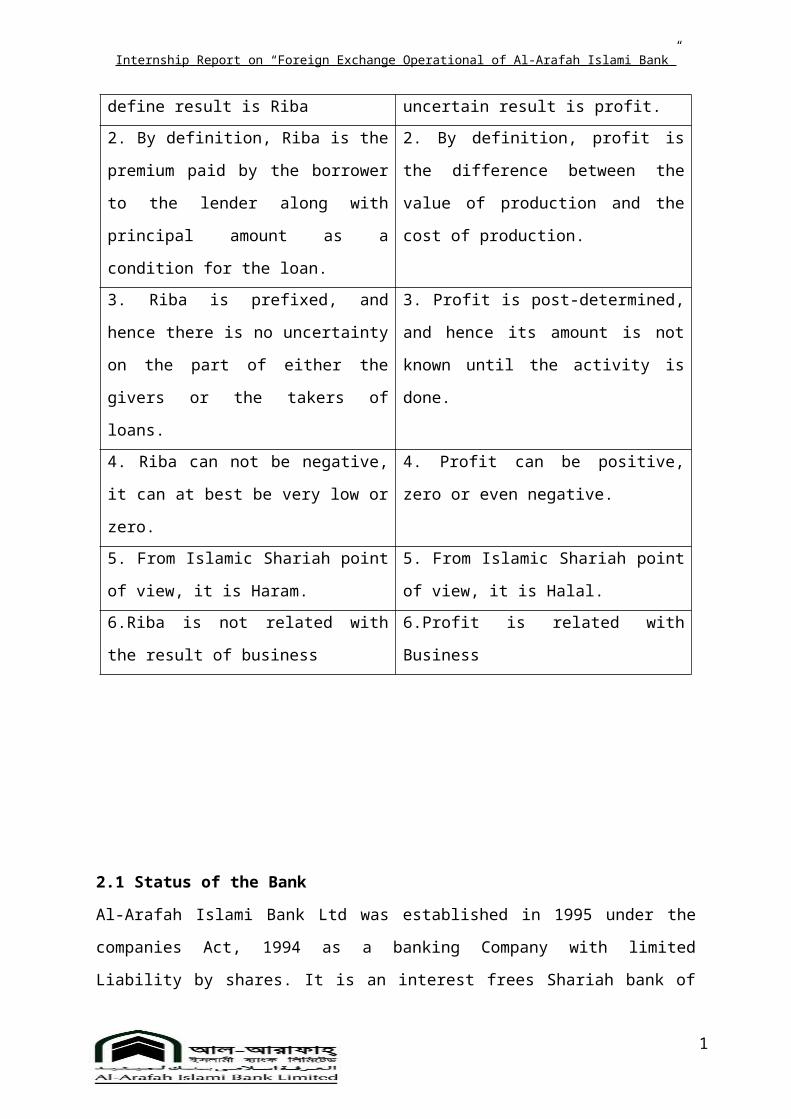

1.10 RIBA and Profit

Most of the persons are trying to connect Riba with profit. In effect, they are fundamentally

different from each other. These misunderstanding will be removed if we look at the

differences of the Riba and Profit. These differences are as follows:

Riba Profit

1. When money is “charged”, its imposed

positive and define result is Riba

1. When money is used in trading (for e.g.)

its uncertain result is profit.

2. By definition, Riba is the premium paid

by the borrower to the lender along with

principal amount as a condition for the

loan.

2. By definition, profit is the difference

between the value of production and the

cost of production.

3. Riba is prefixed, and hence there is no

uncertainty on the part of either the givers

or the takers of loans.

3. Profit is post-determined, and hence its

amount is not known until the activity is

done.

4. Riba can not be negative, it can at best be

very low or zero.

4. Profit can be positive, zero or even

negative.

5. From Islamic Shariah point of view, it is

Haram.

5. From Islamic Shariah point of view, it is

Halal.

6.Riba is not related with the result of

business

6.Profit is related with Business

2.1 Status of the Bank

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Al-Arafah Islami Bank Ltd was established in 1995 under the companies Act, 1994 as a

banking Company with limited Liability by shares. It is an interest frees Shariah bank of

Bangladesh rendering all types of commercial banking service under the regulation of Bank

Companies Act, 1991. The Bank conducts its business on the principles of Musaraka, Bai-

Murabaha, Bai-muazzal and Fire Purchase transactions approved by Bangladesh Bank.

Naturally its modes and operations are substantially different from those of other

conventional commercial banks. There is a Shariah Council in the bank who maintains

constant vigilance to ensure that the activities of the bank are being conducted on the precepts

of Islam. The Shariah Council consists of prominent Ulema, reputed Bankers, renowned

Lawyers and eminent Economist.

2.2 Vision of AIBL

To establish Islamic banking through the introduction of welfare oriented banking and also

ensure equity and justice in the field of all economic activities, achieve balanced growth and

equitable development through diversified investment operations particularly in the priority

sectors and less development areas of the country. Encourage social-economic boost and

financial services to the low -income community particularly in the rural areas.

2.3 Mission of AIBL

To conduct interest free banking.

To establish participatory banking instead of banking on debtor creditor relationship.

To invest through different modes permitted under Islamic Shariah.

To accept deposits on profit-loss sharing basis.

To establish a welfare-oriented banking system.

To extend co-operation to the poor, the helpless and the low-income group for their

economic uplift

To play a vital role in human development and employment generation

To contribute towards balanced growth and development of the country through

investment operations particularly in the less developed areas.

To contribute in achieving the ultimate goal of Islamic economic system

2.4 Aims and objectives

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

The motto of the Al-Arafah Islami Bank Ltd is to explore a new horizon of innovative

modern banking creating an automated and computerized environment providing one stop

service and prepare itself to face the new challenges of globalization and 12th century.

One of the main objectives of the bank is to be a provider of high products and services to

cater to the needs of its corporate clients and provides a comprehensive range of financial

services to national and multinational companies.

2.5 Organgram

Source - Service Rule of AIBL

2.6 Management System of AIBL

Managing Director

Executive Vice President

Senior Vice President

Vice President

Assistant Vice President

Senior Principle Officer Principle Officer

Senior Officer

Officer

Probationary Officer

Junior Officer

Assistant Officer

MCG

Tea Boy

Manpower Position of AIBL

DMD

FAVP

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

The management team of the Bank consists of high motivated, well educated and high skilled

and dynamic executives who have been contributing substantially in the continued growth

and progress of the bank. The management is ably supported and assisted by well motivated

and experienced officers and members of staff.

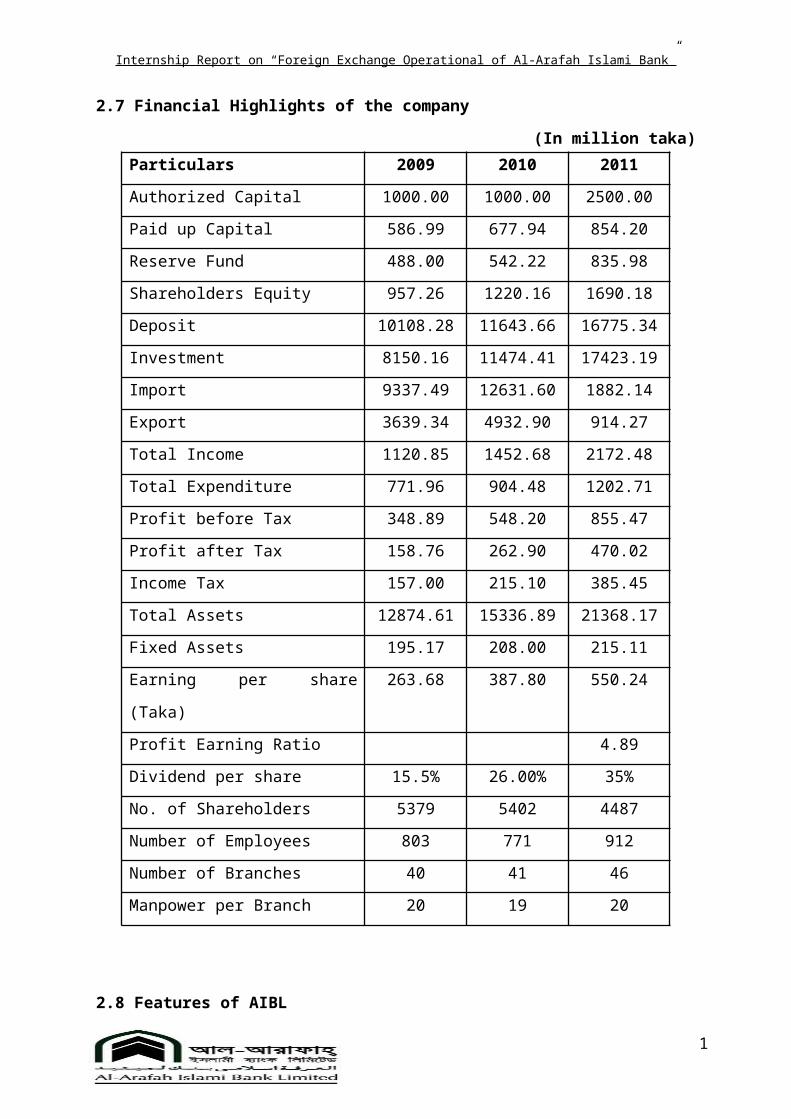

2.7 Financial Highlights of the company

(In million taka)

Particulars 2009 2010 2011

Authorized Capital 1000.00 1000.00 2500.00

Paid up Capital 586.99 677.94 854.20

Reserve Fund 488.00 542.22 835.98

Shareholders Equity 957.26 1220.16 1690.18

Deposit 10108.28 11643.66 16775.34

Investment 8150.16 11474.41 17423.19

Import 9337.49 12631.60 1882.14

Export 3639.34 4932.90 914.27

Total Income 1120.85 1452.68 2172.48

Total Expenditure 771.96 904.48 1202.71

Profit before Tax 348.89 548.20 855.47

Profit after Tax 158.76 262.90 470.02

Income Tax 157.00 215.10 385.45

Total Assets 12874.61 15336.89 21368.17

Fixed Assets 195.17 208.00 215.11

Earning per share (Taka) 263.68 387.80 550.24

Profit Earning Ratio 4.89

Dividend per share 15.5% 26.00% 35%

No. of Shareholders 5379 5402 4487

Number of Employees 803 771 912

Number of Branches 40 41 46

Manpower per Branch 20 19 20

2.8 Features of AIBL

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

All activities of the bank are conducted according to Islamic shariah.

The banks investment policy follows different modes approved by Islamic shareah

based on Quaran & Sunnah.

The bank is committed towards establishing welfare oriented banking system,

economic upliftment of the law- income group of people, create employment

opportunities.

According to the needs and demands of the society and the country as a whole the

bank invests money to different halal business.

The bank participates in different activities aiming at creating jobs, implementing

development projects taken by the government and developing infrastructure.

The bank is committed to establish an economic system through social justice and

equal distribution of wealth.

It is also committed to bring about changes in the underdeveloped rural areas for

ensuring balanced socio economic development of the country through micro credit

program, according to mudaraba system

The bank is contributing to economic and philanthropic activities side by side. Al-

Arafah English Medium Madrasah and AIBL Library are among mention worthy.

2.9 International Trade

At the year of 2010, the bank experienced satisfactory growth in the International trade. At

the end of 2009, the total amount of International Trade (export, import and Remittance) was

13268.83 million taka; which has increased at 35.81% to reach 18020.10 million taka in

2010. The total export of the bank was 3639.34 million taka in 2009, which has increased at

35.54 % growth rate to reach 4932.90 million taka in 2010, whereas the national growth was

15.70% during the same period. Similarly the amount of import has increased from 9337.49

million taka of 2009 to 12631.60 million taka in 2010, experiencing a growth rate of 35.27%.

Last year the amount of remittance through the bank was 292.00 million taka, which grows to

455.60 million taka in the current year.

2.10 Correspondent Banking Relationship

The main aim of Al-Arafah Islami Bank Ltd is to increase its foreign exchange business and

in this connection we are doing international banking with all major banks of the world. At

present we are maintaining correspondent banking relationship with 20 major reputed banks

of the world.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

2.11 Foreign exchange risk Management

Foreign exchange risk is defined as the potential change in earnings arising due to change in

market prices. International Division independently conducts the transactions and passing of

their entries in books of accounts. All foreign exchange transactions are revalued at Mark-to

Market rate as determined by Bangladesh Bank at the month-end. All Nostrum accounts are

reconciled on monthly basis and outstanding entry beyond 30 days is reviewed by the

Management for its settlement.

2.12 Nature of Business

All kinds of commercial banking services are provided by the bank to the customers

following the provisions of Banking Companies Act, 1991, Bangladesh bank’s directives and

the principles of Islamic Shariah.

2.13 Capital Adequacy

The Bangladesh Bank has fixed the ratio of capital adequacy against Risk-Weighted Assets at

9.00% in place of 8% in the month of September 2007. In 2007, the amount of total equity of

the bank was 41.57 Crore taka, which stood at TK.85.56 Crore in the year 2008 and Taka

104.27 Crore in the year 2009. This year it stood at taka 130.56 Crore. At 31 December 2010,

the capital adequacy ratio of the bank is 12.16 % against 14.56% at the same period of 2009.

3.1 Types of Accounts in Al-Arafah Islami Bank

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

A bank is essentially an intermediary of short-term investment/funds. It can carry out

extensive lending/investment operations only when it can effectively mobilize the savings of

the community. A good banker is one who effectively mobilizes the savings of the

community as well as makes such use of savings by making it available to productive and

priority sectors of the economy thereby fostering the growth and development of the nations’

economy.

Accounts are opened under the following two modes -

1. Al-Wadeeah ( Current Account)

2. Al-Mudaraba (Deposit Account)

1. Al-Wadeeah (Current Account): The word ‘Al-Wadeeah’ has been derived from the

Arabic word ‘Wada’yn which means to keep/to deposit/to give up/Amanat. As per Shariah ,

Amanat means to keep something (goods/money/others) to any reliable person/institution for

safe and secured preservation of the same keeping its ownership unchanged and which will

be returned to the owner of the fund on demand as it is/in original shape. In case of Amanat

Bank/any other institution cannot use, invest and amalgamate the funds without the prior

permission of the owner of the Amanat.

The depositor can deposit any amount in this account

The depositor can withdraw any amount by cheque

No profit is allowed in this account

The depositor shall also not bear any loss

Cheques, bills etc collected in this account against commission

Govt. excise and incidental charge realize from this a/c as per rule.

2. Al-Mudaraba (Deposit Account): The word Mudaraba derived from the Arabic word

‘Darb/Darabun’. Literally it means movement to earn profit (munafa). It is a form of

partnership where one of the parties called the ‘Shahib-al-mal’ provides a specified amount

of capital and acts like a sleeping or dormant partner, while the other party called the

Mudarib (entrepreneur), provides the entrepreneurship and management for carrying on any

venture, trade, industry or service with the objective of earning profit. The Mudarib is

required to work with honesty and sincerity and to exert the maximum possible care and

precaution in the exercise of the functions.

3.2 Mudaraba Deposit Products

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Mudaraba Short Notice Account (MSNA)

Mudaraba Savings Account (MSA)

Mudaraba Term Deposit Receipt (MTDR)

Mudaraba Savings Bond (MSB)

Mudaraba Special Scheme (MSS)

Mudaraba Monthly Profit Distribution Scheme (MMPDS)

Mudaraba Muhor Savings Account (MMS)

Mudaraba Waqf Cash Account (MWCA)

Mudaraba Hajj Savings Account (MHSA)

Mudaraba Foreign Currency Deposit

3.3 Different Types of Account Holders

Anyone can open an account with the banker if he is not incapable of entering into a valid

contract and the banker is satisfied of his bonafide and is willing to enter into the business

relations with him. There are certain types of accounts in regard to which the banker should

take note of the relative laws and exercise pre-cautions in order to safeguard its interest.

Some types are:

A/c opened by minors

Joint (two or more persons)

Firms

Co-operative societies

Government

Public bodies

Agents

Executors

Administrators

Trustees

Liquidators

Receivers

Non-Res

3.4 Account opening

This section opens account. It receives account opening application from the interested

applicants, examines and scrutinizes the applications and then selects final customers.

Selection of customers is very much important as the success and failure of the bank is

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

largely dependent on the valued customers. If the customer is found to be fraudulent or

create some sort of forgery, it will ultimately destroy the goodwill of the company.

The following formalities must be maintained by the customer for opening of different types

of account.

3.5 Individual

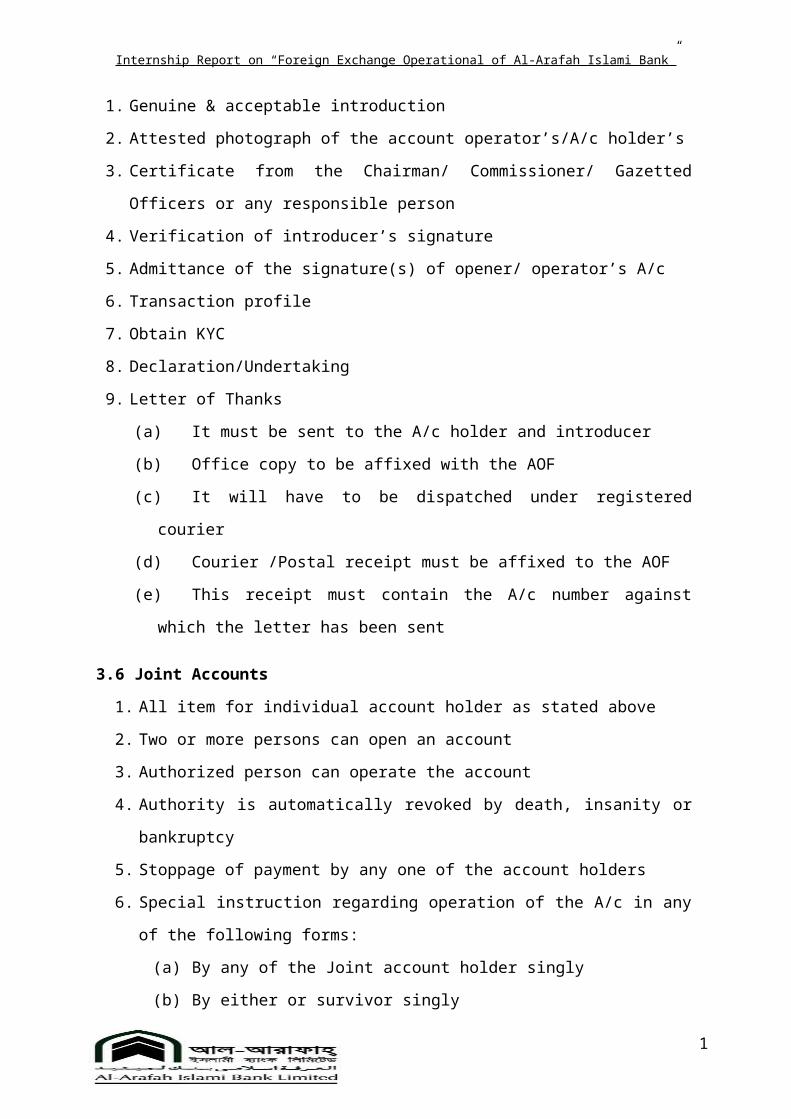

1. Genuine & acceptable introduction

2. Attested photograph of the account operator’s/A/c holder’s

3. Certificate from the Chairman/ Commissioner/ Gazetted Officers or any responsible

person

4. Verification of introducer’s signature

5. Admittance of the signature(s) of opener/ operator’s A/c

6. Transaction profile

7. Obtain KYC

8. Declaration/Undertaking

9. Letter of Thanks

(a) It must be sent to the A/c holder and introducer

(b) Office copy to be affixed with the AOF

(c) It will have to be dispatched under registered courier

(d) Courier /Postal receipt must be affixed to the AOF

(e) This receipt must contain the A/c number against which the letter has been sent

3.6 Joint Accounts

1. All item for individual account holder as stated above

2. Two or more persons can open an account

3. Authorized person can operate the account

4. Authority is automatically revoked by death, insanity or bankruptcy

5. Stoppage of payment by any one of the account holders

6. Special instruction regarding operation of the A/c in any of the following forms:

(a) By any of the Joint account holder singly

(b) By either or survivor singly

(c) By either singly

(d) By any two or more joint account holding jointly

(e) By all the survivors jointly

3.7 Sole Proprietorship

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

In case of opening an account by a sole-proprietor of a firm, he/she should sign the account

opening form and furnish his specimen signature showing his representative character.

1. All items for individual account holder as stated above.

2. Valid trade license or attested photocopy thereof issued by the competent authority

3. Membership certificate from local business association/Chamber of Commerce

3.8 Partnership Firm

A banker should not open an account in the name of a partnership unless one or more of the

partners apply to him to do so. Except where the partner, making an application for the

opening of an account in the firm’s name, is deprived of the power, which fact is known to

the banker, there can be no legal objection to a banker opening an account in the name of the

firm at request. Failure, however, to make proper enquiries by referring to the partnership

agreement or any other record in writing which maybe available before opening of account

on behalf of a firm in a partner’s name may lead a banker in trouble.

1. All items for individual account holder as stated above.

2. Valid trade license or attested photocopy thereof issued by the competent authority

3. Two or more person can form a partnership firm by partnership deed. (Registered

notarized)

4. Clear mandate for operating the a/c from the partners regarding name of the persons to

draw cheques and borrow money, to overdraw, to mortgage or to sell properties owned

by the firm

5. In case of insolvency of the firm: Operation should be stopped after receiving notice of

insolvency of the firm

3.9 Private Limited Company

A company registered under the Companies Act, 1913 has a legal entity apart from its

shareholder. Private Company means a company which by its articles:

Restricts the right to transfer the shares if any;

Limits the number of its members 2 to 50

Prohibits any invitation to the public to subscribe for the shares, if any or debentures

of the company.

When a current account is to be opened for a private limited company the banker will have to

obtain the following requirements:

1. All terms for individual account holder as stated above

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

2. Copy of memorandum and articles of association duly certified by the

Secretary/Director of the company

3. Certificate of incorporation

3.10 Mudaraba Savings A/c (MSA A/c)

1. Nationality certificate from Ward Commissioner/ UP Chairman or Passport

(photocopy) of every signatories of the A/c

2. KYC form for individual

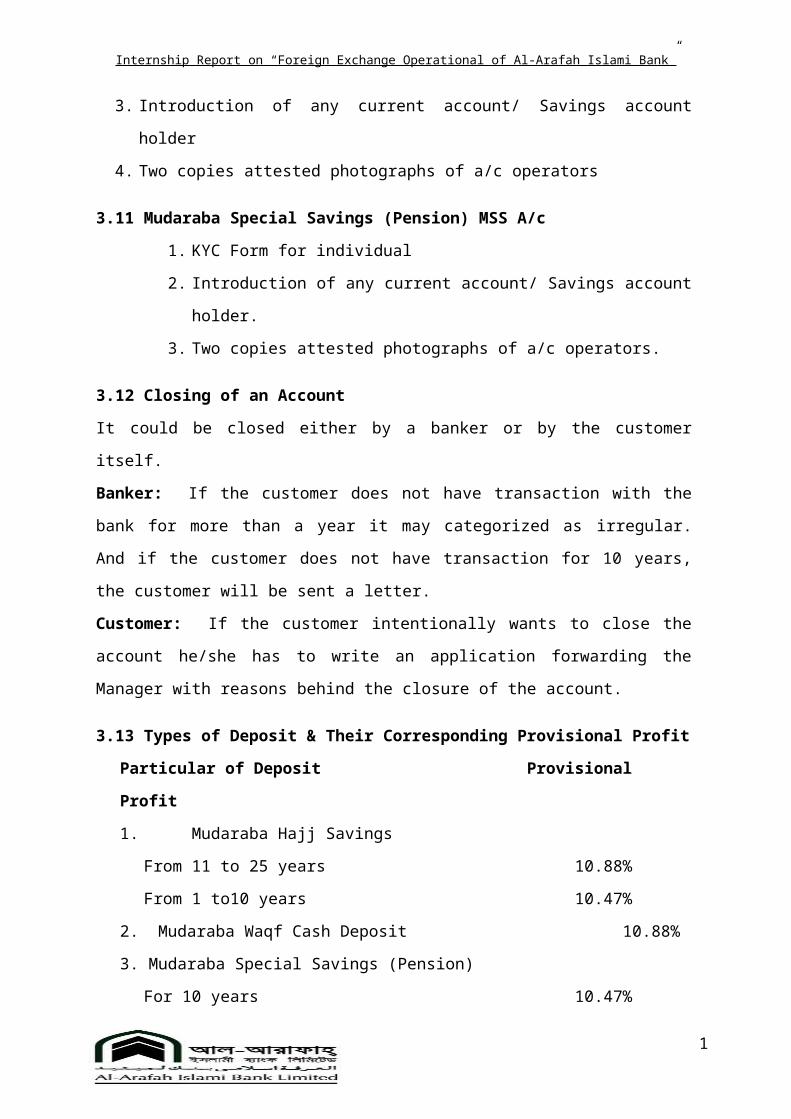

3. Introduction of any current account/ Savings account holder

4. Two copies attested photographs of a/c operators

3.11 Mudaraba Special Savings (Pension) MSS A/c

1. KYC Form for individual

2. Introduction of any current account/ Savings account holder.

3. Two copies attested photographs of a/c operators.

3.12 Closing of an Account

It could be closed either by a banker or by the customer itself.

Banker: If the customer does not have transaction with the bank for more than a year it may

categorized as irregular. And if the customer does not have transaction for 10 years, the

customer will be sent a letter.

Customer: If the customer intentionally wants to close the account he/she has to write an

application forwarding the Manager with reasons behind the closure of the account.

3.13 Types of Deposit & Their Corresponding Provisional Profit

Particular of Deposit Provisional Profit

1. Mudaraba Hajj Savings

From 11 to 25 years 10.88%

From 1 to10 years 10.47%

2. Mudaraba Waqf Cash Deposit 10.88%

3. Mudaraba Special Savings (Pension)

For 10 years 10.47%

For 5 years 10.10%

4. Mudaraba Muhor Savings A/c

For 10 years 10.47%

For 5 years 10.10%

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

5. Mudaraba Saving Bond

For 8 years 10.25%

For 5 years 10.10%

6. Mudaraba Monthly Profit Deposit Scheme 10.20%

7. Mudaraba Term Deposit

36 months 10.00%

24 months 9.52%

12 months 9.37%

06 months 7.41%

03 months 7.09%

8. Mudaraba Savings Account 6.35%

3.14 Cash Section

A banker’s transactions are mainly of three types. They include –

Cash

Transfer &

Clearing

The cash section of any bank plays very significant role in general banking department

because, it deals with most liquid assets. Basically cash department is the most vital and

sensitive department of the branch which deals with all kinds of transaction in cash. All cash

receipts and payments are made through this department. The Al-Arafah Islami bank is

equipped with electronic machinery with fully computerized system which delivers quick

service to its valued customers. This section receives cash from depositors and pay cash

against cheques, draft, Pay order (PO), etc over the counter. This section accepts cheques

from the depositors for payment in cash. The drawer who wants to receive money against

cheque comes to the payment counter and presents the cheque to the officer. He verifies the

following information:

1. Date of the cheque

2. Signature of the account holder

3. Material alteration

4. Whether the cheque is crossed or not

5. Whether the cheque is endorsed or not

6. Whether the amount in figure and in word corresponds with each one

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Then the officer checks the cheque from the computer for further verification. Here is the

following information that is checked.

1. Whether there is sufficient balance or not

2. Whether there is stop payment instruction or not

3. Whether there is any legal obstruction or not

The cash section deals with all type of negotiable instruments. It also includes the Vault

which is used as the store of the cash instruments. The vault is insured up to a certain

amount, which is called the vault limit; the excess cash is then transferred to Bangladesh

Bank. The AIBL, Banani Branch Vault limit is 1.5 crore. When the excess cash is

transferred, the cash officer issues IBDA. The vault counter is around 35 lacs. Any client

who wants to deposit money will fill up the deposit slip and give the form along with the

money to the cash officer over the counter. The cash officer counts the cash and compares

with the figure written in the deposit slip. He then puts his signature on the slip along with

the ‘cash received’ seal and records in the cash receive register and also in the computer

against the account holder.

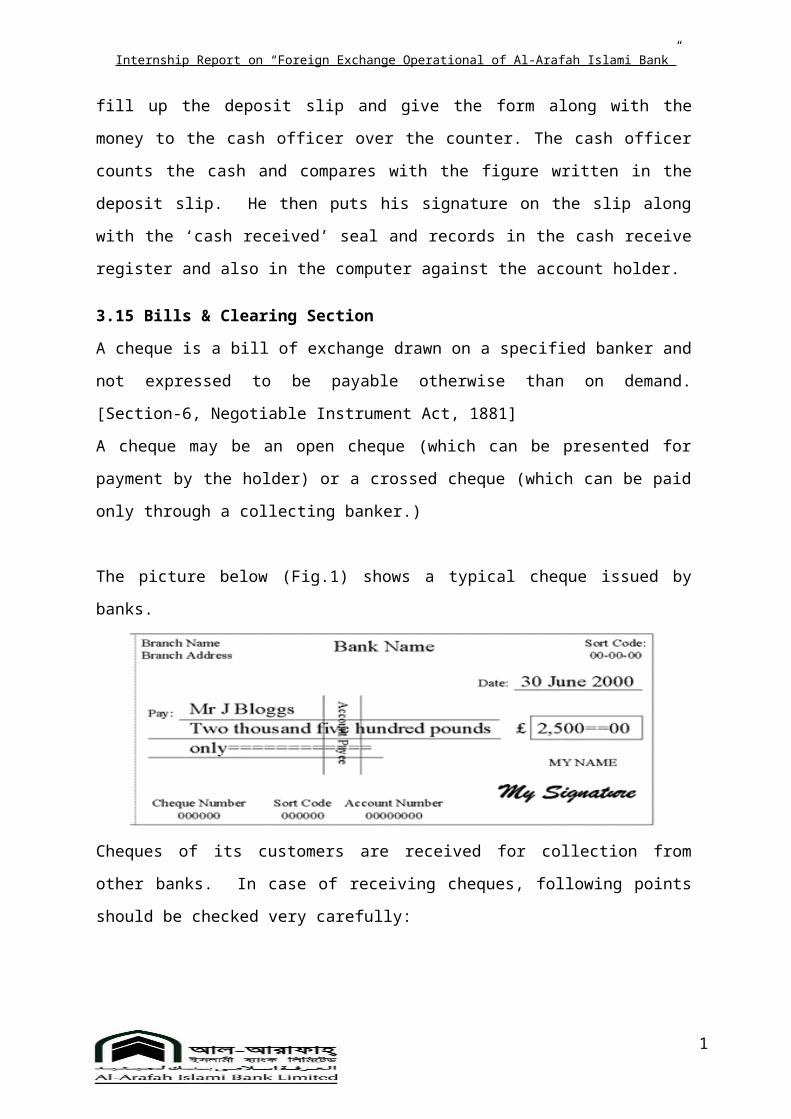

3.15 Bills & Clearing Section

A cheque is a bill of exchange drawn on a specified banker and not expressed to be payable

otherwise than on demand. [Section-6, Negotiable Instrument Act, 1881]

A cheque may be an open cheque (which can be presented for payment by the holder) or a

crossed cheque (which can be paid only through a collecting banker.)

The picture below (Fig.1) shows a typical cheque issued by banks.

Cheques of its customers are received for collection from other banks. In case of receiving

cheques, following points should be checked very carefully:

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

The cheques should not carry a date older than the receiving date for more than 1

months. In that case it will be a stale cheque and it will not be allowed for

collection.

The amount in figure and words in both sides of the pay-in-slip should be same.

The name mentioned in the cheque should be same in both side of the pay-in-slip

and it should be the same with the name mentioned in the cheque

The cheque must be crossed

3.16 Types of cheque

Inward clearing cheques: Inward cheques are those ones drawn on the respective branch

which have been presented on other banks and will be cleared/honored through the clearing

house. For example, the cheque drawn on AIBL, Head Office.

Outward Cheques: These cheques are received on the counter from other banks. There are 3

types:

1. Drawn on another branch of AIBL. These are called Outward Bills for Collection

(OBC).

2. Drawn on another bank, which is situated in the clearing house area. This cheques

are called clearing cheque.

3. Drawn on another bank, which is situated outside the clearing area. These cheques

are also called as OBC.

3.17 Outward Bills for Collection (OBC)

OBC are those cheques drawn on other banks which are not within the same clearing house.

An officer gives OBC seal on this type of cheques and later sends a letter to the manager of

the branch of the same bank located in the branch on which cheque has been drawn. After

collection of that bill, branch advice the concerned branch in which cheque has been

presented to credit the customer account through IBCA. In absence of the branch, officer

sends a letter to the manager of the bank on which the cheque is drawn. That bank will send

pay order in the name of the branch. This is the procedure of OBC mechanism.

3.18 Inward Bills for Collection (IBC)

All clearing cheques are not received on the counter. Some cheques are received from other

source for collection. These cheques are received from other branch of Al-Arafah Islami

Bank. These cheques are settled by sending IBCA.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

3.19 Remittance

Remittance means transmission/transfer of money from one place to another. Local

remittance represents remittance that takes place within the territory of a country.

Virtually there are three types of remittances as under:

DD- Demand Draft

TT – Telegraphic Transfer

PO - Payment Order

3.20 Demand Draft

According to Section 85 (A) of the negotiable instruments Act, a demand draft is “an order

to pay money drawn by one office of the bank upon other office of the same bank for a sum

of money payable to order on demand.”

The followings are essential features of a demand draft issued by the bank:

1. It is a negotiable instrument

2. It is drawn by one office of a bank upon another office of the same bank

3. It is payable on demand.

3.21 Issuance of DD

1. A prescribed Application Form bearing No (F20). The following columns should be

filled in properly.

(a) Name & address of the applicant

(b) Telephone No

(c) Date

(d) Signature of the applicant

(e) Name of the payee

2. Commission to be realized/charged as per Head Office circular, at present @0.1 %

but min TK.40/-

3. Total amount should be deposited by the party in cash or cheque as per arrangement.

4. Printed DD block/leaf to be filled in by a bank official as per request of the purchase

(a) Name of the issuing branch

(b) Date

(c) A/c payee rubber stamp

(d) Payee’s name

(e) Amount in words and figure

(f) Drawee branch

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

4.1 INVESTMENT OF AIBL

Investment is the action of deploying funds with the intention and expectation that they will

earn a positive return for the owner (Brokington 1986, p.68). Funds may be invested in either

real assets or financial assets. When resources are used for purchasing fixed and current

assets in a production process or for a trading purpose, then it can be termed as real

investment. The establishment of a factory or the purchase of raw materials and machinery

for production purposes are examples in point. On the other hand, the purchase of a legal

right to receive income in the form of capital gains or dividends would be indicative of

financial investments. Specific examples of financial investments are: deposits of money in a

bank account, the purchase of Mudaraba Savings Bonds or stock in a company.

4.2 Investment Objectives of Al-Arafah Islami Bank

The objectives and principles of investment operations of the Banks are -

The investment fund strictly in accordance with the principles of Islamic Shariah.

To diversifies its portfolio by size of investment, by sectors (public and private), by

economic purpose, by securities and by geographical area including industrial,

commercial and agricultural.

To ensure mutual benefit both for the Bank and the investment client by professional

appraisal of investment proposals, judicious sanction of investment, close and

constant supervision and monitoring therefore.

To make investment keeping the socio-economic requirement of the country in view.

To increase the number of potential investors by making participatory and productive

investment.

To finance various developments schemes for poverty alleviation, income and

employment generation with a view to accelerating sustainable socio-economic

growth and upliftment of the society.

4.3 Strategies

Risk in the investments and return thereon are interrelated. An investment policy that

emphasizes a high return must accept relatively high risk. Conversely, an investment policy

that will tolerate only small amount of risk must be prepared to accept a relatively low return.

As such, it is really difficult whether to select a high return port-folio on high risk or low risk

port-folio with a low return.

1

a) Bai-Murabahab) Bai-Muajjalc) Bai-Salamd) Istishna’a

a) Mudarabab) Musharaka

a) Hire Purchaseb) Hire Purchase Under shirkatul Melk

Bai- Mechanism Share Mechanism

Ijara Mechanism

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Nevertheless, considering all aspects following guidelines shall be followed as strategy for

banks investments.

i. If two port-folios have the same risk but different returns, the port-folio having

higher return shall be preferred.

ii. If the two port-folios have the same expected returns, but different degrees of risk,

the port-folio with lower risk shall get preference.

iii. If one port-folio has both a higher return and a lower risk than another, the first

port-folio shall be preferred.

iv. Keeping in view the risk factor, the bank shall maintain flexibility in

determination of rate of return on investments on case to case basis in

consideration of the risk element involved in the respective investment.

v. Emphasis is given for expansion and strengthening cottage and small industries

sector and rural industries. This immensely potential industrial sub-sector shall

create employment opportunities to rural and semi-urban population and shall

have positive contribution in employment and income generation and poverty

alleviation of the low-income group.

vi. Investment facilities shall be extended for establishment and expansion of export

oriented forward / back ward linkage and import substitute industries.

4.4 Investment Mechanism of Al-Arafah Islami Bank

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

4.5 Bai-Murabaha

Bai-Murabaha may be defined as contract between a buyer and a seller under which the seller

sells certain specific goods (permissible under Islamic Shariah and the Law of the land), to

the buyer at a cost plus agreed profit payable in cash or on any fixed future date in lump-sum

or by installments. The profit marked –up may be fixed in lump-sum or in percentage of the

cost price of the goods.

4.6 Types of Murabaha

In respect of dealing parties Bai-Murabaha may be of two types.

Ordinary Bai-Murabaha

If there are only two parties, the seller and the buyer, where the seller as an ordinary trader

purchases the goods from the market without depending on any order and promise to buy the

same from him and sells those to a buyer for cost plus profit, then the sale is called Ordinary

Bai-Murabaha.

Bai-Murabaha on Order and Promise

If there are three parties, the buyer, the seller and the Bank as an intermediary trader between

the buyer and the seller, where the bank upon receipt of order from the buyer with

specification and a prior outstanding promise to buy the goods from the Bank, purchases the

ordered goods and sells those to the ordering buyer at a cost plus agreed profit, the sale is

called “Bai-Murabaha on Order or Promise”, generally known as Murabaha.

In this Bank, Bai-Murabaha is treated as a contract between the Bank and the Client under

which the Bank purchases the specified goods as per order and specification of the client and

sells those to the ordering client at a cost plus agreed upon profit payable within a fixed

future date in lump-sum or by fixed installments. Thus it is a sale of goods on profit by

which ownership of the goods is transferred by the Bank to the Client, but the payment of the

sale price (cost plus profit) by the Client is deferred for a fixed period.

4.7 Operational Procedures of Investment of AIBL

The Bank shall sell the goods at a higher price (Cost + Profit) to earn profit. The cost of

goods sold and profit mark-up therewith shall separately and clearly be mentioned in the Bai-

Murabaha Agreement. The profit mark-up may be mentioned in lump sum or in percentage of

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

the purchase/cost price of goods. But, under no circumstances, the percentage of the profit

shall have any relation with time or expressed in relation with time, such as per month, per

annum etc. The price once fixed as per agreement and deferred cannot be further increased. It

is permissible for the Bank to authorize any third party to buy and receive the goods on

Bank’s behalf. The authorization must be in a separate contract.

Induction of client

Application

Categorization

Processing and appraisal

Sanction

Documentation

Purchase of goods by the Bank

Taking delivery of goods by the Bank

Sales and delivery of goods to the client

4.8 Application

Obtain application in triplicate from the client of F-167A and record the same in the

Investment Proposal Received and Disposal Register (B-53).

Obtain and affix attested photograph(s) of the Proprietor /Partner/Directors/

Trustee/ Administrator on the top right hand corner of the application.

Scrutinize the application of the Client to see that-

(a) All columns are properly field in;

(b) Particulars and information given therein are complete and correct in all

respects;

(c)All required Documents/papers as listed in the footnote for the application is submitted;

4.9 Special Schemes under Investment Modes

Household Durable Scheme

Al-Arafah Islami Bank has introduced Household Durables Investment Scheme which has

already created great enthusiasm among the people and received tremendous response from

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

them. Objectives are to assist the service holders with limited income in purchasing

household articles such as Furniture, Electric and Electronic equipments like Television,

Refrigerator, Gas cooker etc.

Investment Scheme for Doctors

A good number or newly graduated doctors from Medical Colleges are unemployed. Many of

the medical graduates are waiting for job because the opportunity for Government service is

limited. If these young doctors could be self-employed by extending investment facilities,

they could make modern facilities available at the door-steps of rural people. In view of the

above facts, Al-Arafah Islami bank has taken the initiative an introduced the " Doctors

Investment Scheme" to ensure modern treatment and medical facilities available to the people

through extension of Bank’s investment facilities for self-employment of newly graduated

doctors and at the same time extending investment facilities to the established medical

practitioners to procure modern and sophisticated medical equipment.

Rural Development Scheme of Al-Arfah Islami Bank

Al-Arafah Islami Bank envisages an economic system based on equity and justice. Taking

into consideration that majority of the population below poverty line lives in rural

Bangladesh, the Bank has devised a Rural Development Scheme (RDS) with a view to

creating employment opportunity for them and alleviates their poverty through income

generation activities.

The Al-Arafah Islami Bank through its RDS project has been implementing integrated

programs for the landless poor, wage laborers and marginal farmers aimed at meeting their

basic needs and promoting their comprehensive development. Consciousness among the poor

needs should be enhanced so that they can lift their position in the socio-economic structure

of the country. In order to consolidate their economic base, invested money should be used in

income generating activities so the poorer section of the population can become self-reliant.

RSD works for the realization of that objective.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Agricultural Implements

Investment Scheme

Bangladesh is predominantly an agricultural country with vast majority of people living in

rural areas. Most of our people for their living are dependent on agriculture. Agriculture still

contributes the lion share of the gross domestic product. But we could not as yet become self-

sufficient in food production. We still import a bulk quantity of food grains from abroad to

meet the deficit. We must modernize our agriculture and establish more and more industries

in order to minimize imports. The Bank has introduced “Agriculture Implements Investment

Scheme" to provide power tillers, power pumps, shallow tube wells, thrasher machine etc. On

easy terms unemployed youths for self-employment and to the farmers help augment

production in agricultural sector.

Micro Industries Investment Scheme

Al-Arafah Islami Bank has been appreciably participating in this direction by financing

industrial sector. With a view to creating

wider base for industries, the Bank

has decided to launch "Micro Industries

Investment Scheme" through its Branches.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

4.10 Data Analysis of the Investment of Al-Arafah Islami Bank

Mode 2007 2008 2009 2010 2011

Bai-

Murabaha

12,003.92 17,112.56 23,522.94 31,138.88 41,731.48

HPSM 8,496.87 10,664.08 14,131.48 18,065.10 23,344.46

Bai-Muajjal 4,478.34 4,753.54 4,965.74 5,512.13 5,735.19

Purchase &

Negotiation

1,337.05 1,386.14 1,865.26 1,801.33 2,416.84

Quard 640.23 923.16 1,298.19 1,765.65 1,694.32

Bai-Salam - - 407.98 610.27 807.14

Mudaraba 52.00 52.00 52.00 102.00 102.00

Musharaka 428.91 346.28 37.02 12.13 27.13

Total 27,437.32 35,237.76 46,280.61 59,007.49 75,858.56

Table: 4.10 Mode-wise Investment

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Chart – Industrial Investment

Chart - Commercial Investment

Chart - Investment in Real State

Chart - Investment in Agriculture

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Chart - Investment in Other Sectors

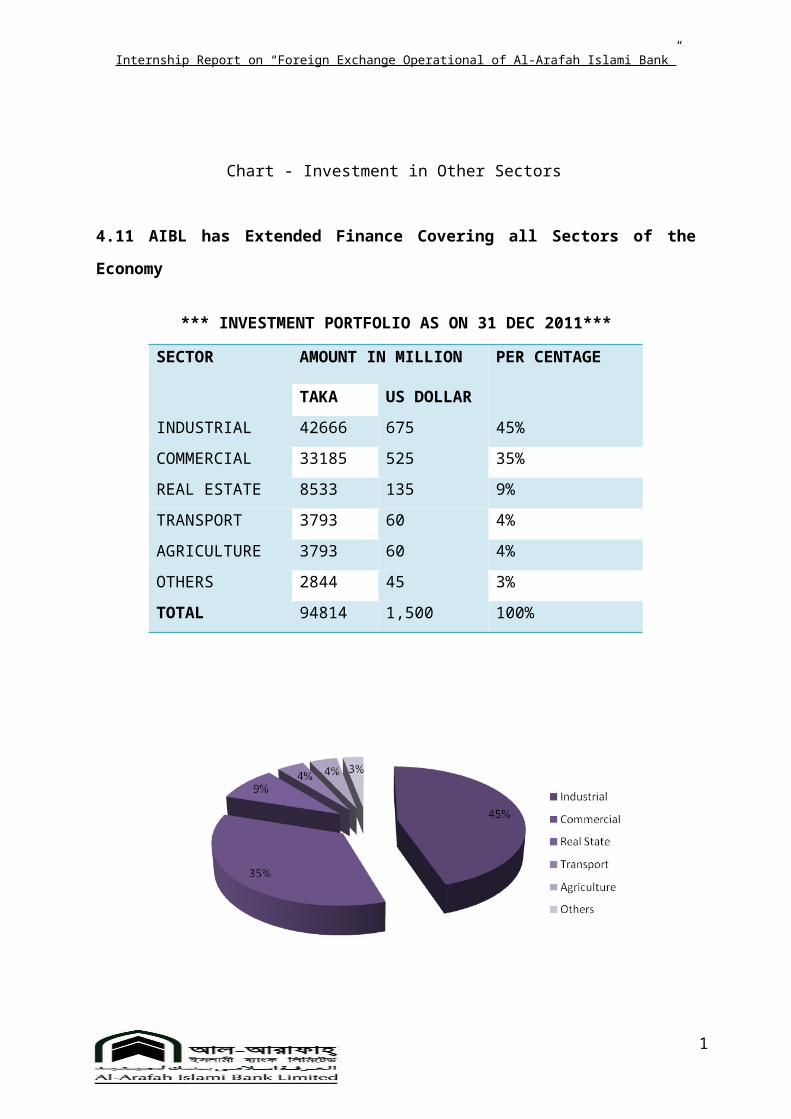

4.11 AIBL has Extended Finance Covering all Sectors of the Economy

*** INVESTMENT PORTFOLIO AS ON 31 DEC 2011***

SECTOR AMOUNT IN MILLION PER CENTAGE

TAKA US DOLLAR

INDUSTRIAL 42666 675 45%

COMMERCIAL 33185 525 35%

REAL ESTATE 8533 135 9%

TRANSPORT 3793 60 4%

AGRICULTURE 3793 60 4%

OTHERS 2844 45 3%

TOTAL 94814 1,500 100%

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Chart - Investment Portfolio 2011

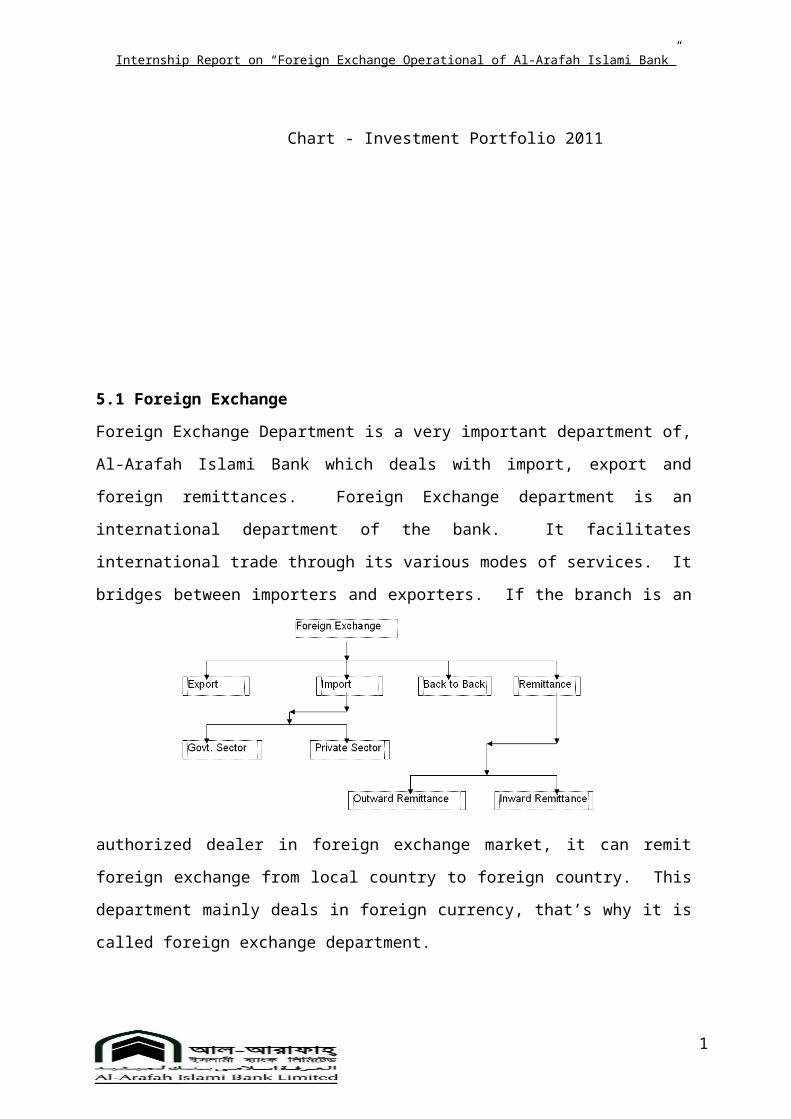

5.1 Foreign Exchange

Foreign Exchange Department is a very important department of, Al-Arafah Islami Bank

which deals with import, export and foreign remittances. Foreign Exchange department is an

international department of the bank. It facilitates international trade through its various

modes of services. It bridges between importers and exporters. If the branch is an

authorized dealer in foreign exchange market, it can remit foreign exchange from local

country to foreign country. This department mainly deals in foreign currency, that’s why it

is called foreign exchange department.

Bank branch should be authorized dealer, with due approval from Bangladesh Bank to run

foreign exchange transactions. According to the Bangladesh Law, the payment must be

received within 120 days.

Foreign Exchange Department is dividend in to 3 sections

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Import Export Remittance

5.2 Mode of Foreign Exchange Business

1. Import

2. Export

3. Remittance

A. Inward Remittance

B. Outward Remittance

5.2.1 Meaning of ImportImport means lawfully carrying out of anything from one country to county for Buying. It

will be occurred according to the Government law.

5.2.2 Classification of Importer

Importers are those who are authorized by the import Trade Control Authority that is CCI& E

for import of goods essential for consumption or for production purposes.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

There are mainly three types of Importer

1. Commercial Importer

2. Industrial Importer.

3. Importer under Wage Earner Scheme - WES

(1) Commercial Importer

It means an importer registered under the importers, exporters and indenture registration

order 1981 who import goods for sale.

(2) Industrial Importers

When issued to an industrial consumer, gives the items of import as raw materials and

packing materials and spare parts, the value of entitlement and ITC classification.

(3) Importers under - WES

It means registered importers who import only under the WES. WES importers can be

importing all permissible items as declared by the import policy and notification. Besides all

registered commercial and industrial importer also can import under WES.

Other Importers are as follows

Lease Financing Import.

Govt. Sector Importer.

Import under Bonded Ware-House System.

Import by Actual Users.

Import by E.P.Z.

5.2.3 Import Policy OrderEarlier import policy has been formulated the five years. But present import policy order has

been formulated for 3 (three) years, Effect from the 14 th June 2003 to 30th June 2006 and

valid till announce of new import policy order. If require Government can revise the policy in

each every years.

5.2.4 General Rules in connection with importRestriction of Import

a) Negative list of Merchandises.

b) Restricted list.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

c) Footnote under Restricted List

d) Freely importable items.

ITC number is compulsory (H.S code 6 digit) to be mentioned in the L/C and LCAF to

identification the item to be imported.

1. Requirement Right of Refusal (ROR) for public sector agency from Ministry of

Industry or respective Ministry/department of both to Import item under Restricted

List.

2. Import cannot be Israel.

3. Pre-shipment inspection (PSI) for private sector normally PSI is not mandatory.

4. Shipment to be made through Bangladeshi ship some exemption

5.2.5 The Documentary Letter of Credit

Letter of Credit is a credit contract where the Opening/Issuing Bank is committed to place an

agreed amount of money at the beneficiary’s disposal under some agreed conditions. In other

words letters of credit is a letter form the importer Bankers to the exporter that the bills if

drawn as per terms & conditions complied with will be honored on presentation.

Definition of L/C

A letter of Credit is a conditional bank undertaking of payment. In other words letters of

credit is a letter form the importer bankers to the exporter that the bills if drawn as per terms

and conditions are compiled with will be honored on presentation

As per UCPDC 500 a credit may be either:

i) Revocable.

ii) Irrevocable.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

The Credit, therefore, should clearly indicate whether it is revocable or irrevocable. In the

absence or such indication the credit shall be deemed to be irrevocable.

Types of L/C

1. Revocable Credit: As per Article no. 8 (a) A revocable credit is a credit which can

be amended or canceled by the issuing bank at any time without prior notification to the seller

since to offers little security to the seller.

2. Irrevocable Credit: As per Article no 9 an irrevocable credit constitutes a definite

undertaking of the issuing Bank. A credit cannot be amended or cancelled without the

agreement of all parties. It gives the seller grater assurance of payment. An irrevocable credit

can be either confirms or unconfirmed dependant on the desire of the seller.

Other types of Letter of Credit are as follows -

1. Confirmed L/C.

2. Transferable L/C.

3. Divisible L/C.

4. Back to Back L/C.

5. Revolving L/C.

6. Restricted L/C

7. Red clause L/C.

8. Green Clause L/C

9. With Recourse

10. Without Recourse

5.2.6 Registration of Importer

As per import & Export control Act. 1950 no person can indent, import or export any goods

into Bangladesh except kin case of exemption issued by the Government of the peoples

Republic of Bangladesh. Violation of this order is punishable with fine under the provisions

of Sea Customs Act 1878 as applied by sub section (3) of Section 3 of this Act.

Procedure for obtaining, IRC ( Import Registration Certificate )

Through public notice or import policy the chief controller of imports & Exports invites

applications usually for registration of importers. The following papers/ documents are

required for submission to CCI&E or area office of CCI & for import registration certificate:

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

1. Application form.

2. Nationality Certificate.

3. Income Tax registration Certificate with GIR.

4. Trade License from the municipal or local Authority.

5. Membership Certificate.

6. Partnership deed (for partnership firm)

7. Certificate of Registration with the register of joint Stock Co. & Articles and

Memorandum of Association in case of Limited Co.

8. Bank Certificate.

9. Documentary evidence for business existence.

10. Original copy of Treasury Chalan being payment of registration fees.

11. Original copy Chaplin for passbook.

12. Other documents if any required by the CCI & E.

13. Ownership’s documents or Rent receipts of the place of Business.

14. Survey clearance from the relevant Authority.

The nominated bank of the application will examine the papers/documents s& verity the

signature of the applicant and forward the same to the concerned office of the CCI & E with

forwarding schedule in duplicate through bank’s representative. The duplicate copy of the

same bearing the acknowledgement of CCI & E office of the receipt of the documents is back

by the bank and is preserved. If the documents are found in order and the CCI & E is satisfied

the IRC is issued to the applicant and sent direct to the nominated bank. The passbook is also

issued by the CCI & E simultaneously to the importer and sent direct to the nominated bank.

Parties to Letter of Credit

1. Importer (Buyer)/Applicant

2. The Issuing Bank (Opening Bank)

3. The Advising Bank (Notifying Bank)

4. Exporter/Seller (Beneficiary)

5. Confirming Bank

6. Negotiating Bank

7. The Paying/Reimbursing/Accepting/Remitting

Bank

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Applicant: The person/body who requests the bank (opening bank) to issue letter of credit.

As per instruction and on behalf of the applicant, the bank opens L/C in line with the terms

and conditions of the seller contract between the buyer and the seller.

Opening bank/Issuing Bank: The bank which open/issue letter of credit on behalf of the

applicant/ importer. Issuing bank’s obligation is to make payment against presentation of

documents drawn strictly as per terms of the L/C.

Advising/Notifying Bank: The bank through which the L/C is advised/forward to the

beneficiary (exporter). The responsibility of advising bank is to communicate the L.C to the

beneficiary after checking the authenticity of the credit. It acts as an agent of the issuing

bank without having any engagement on their part.

Beneficiary: Beneficiary of the L/C is the party in whose favor the letter of credit is issued.

Usually they are the seller or exporter.

Confirming Bank: The bank which under instruction in the letter of credit adds

confirmation of making payment in addition to the issuing bank. It is done at the request of

the issuing bank having arrangement with them. This confirmation constitutes a definite

undertaking on the part of confirming bank in addition to that of issuing bank.

Reimbursing/Paying Bank: the bank nominated in the letter of credit by the issuing bank to

make payments stipulated in the document, complying with reimbursing bank.

SELLER BUYER

2. Doc .CreditApplication

ISSUING BANKADVISING BANK

4. Advise of Doc .Credit

3. Documentary Credit

1. Contract ApplicantBeneficiary

The Canadian Advising Bank The Bangladeshi Issuing Bank

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Figure: The Documentary Credit Cycle

Documents submitted by the importer before opening of the L/C

a. Trade License (Valid).

b. Import Registration certificate (Must be kept in the bank custody).

c. Passbook import.

d. Income Tax declaration.

e. Membership certificate.

f. Memorandum of Articles (In case of Ltd. Co.)

g. Registrar deed (In case of partnership firm)

h. Resolution.

i. Photo one copy.

Bank will supply the following papers/documents before opening of the L/C

a) L/C application form.

b) LCAF Form.

c) IMP Form

d) Murabaha agreement.

e) Charge documents paper.

The above paper must be completed duly filled and signed by the party and verified the

signature.

5.2.7 Import Procedure under Al-Arafah Islami Bank

1. Selection of Clients On the basis of

a. Credit Report.

b. Credibility.

c. CIB Report.

(To association of liability if any with other bank.)

2. Induction of client as Importer.

3. L/C

a. Conditional Undertakings of bank payments.

b. .Processing to open

c. Permissibility and marketability of the item.

d. Price competitiveness.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

e. Credit report of the supplier.

f. Fixation of the cash security.

g. Documentation.

h. Preparation of vouchers.

i. Realizations of the cash security, commission and other charge.

4. Througing of L/C

a. SWIFT is a worldwide community. It has over 7500 financial institution over 199

Countries as its member.

b. Air mail/Telex through advising Bank.

5. Lodgment

a. Checking of import documents upon receipt from negotiating banks.

b. Entry the bills register.

c. Passing the voucher.

d. Purchase of FC. Fund for payment of the bills.

6. Retirement

a. Preparation of cost memo.

b. Intimation to importer regarding arrival of shipping document.

c. Asking the bill paying bank’s dues showing in the cost memo.

d. Delivery of the documents against receipt of payment

7. Post Import Finance

a. At the request of importer bank undertakes clearing of the imported goods paying duty.

VAT and other relevant charges stores the same under control

b. Delivers to importer against payment as per prior arrangement.

8. Enlistment of C&F agent

a. For C&F purpose. C&F agents are enlisted under different categories.

9. Reporting

a. To Bangladesh Bank

b. Monthly returns statement to the Head office.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Figure : Summary of the Plan of Payments

5.3 Export5.3.1 Meaning of ExportExport means lawful carrying out of anything from one country to another country for sale.

5.3.2 Definition of Exporter

The importers and exports trade of the

country is regulated by the Imports Exports Control Act 1950. No person /firm is allowed to

export any thing from Bangladesh unless he is registered with CCI and E under the

registration order (Importer and Exporter) 1952. To become an exporter an ERC (export

Registration Certificate) must be obtained from the office of CCI & E.

5.3.3 Procedure for obtaining Export Registration Certificate (ERC)

For obtaining Export Registration Certificate (ERC), intending Bangladesh Exporters are

required to apply to the CCI & E authority in the prescribed from along with the following

documents:

a) Nationality Certificate.

b) Copy of valid Trade License.

c) Income Tax Certificate.

d) Bank Certificate.

e) Copy of rent receipt of the business firm.

f) Registered Partnership Deed in case of partnership concerns.

g) Memorandum of Articles & Association and Incorporation certificate in

Case of Limited Company.

On satisfaction of the CCI & E the potential exporter is advised to deposit export registration

fee of Tk. 1,000/- through Treasury Chelan to Bangladesh Bank/ Sonali Bank for enabling

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

them to issue ERC. The ERC may be renewed every year on payment of renewal fee of Tk.

1,000/- through Treasury Chelan as started.

5.3.4 Different types of Exporta. Export under L/C

Exporters are allowed to export the commodity under irrevocable letter of credit. Under this

type of export, exporter will ship the goods as pr terms of the credit and will get payment as

per arrangement of the credit.

b. Consignment basis export

Exports are allowed against firm contract. As per contract, importer will ship the goods and

the buyer will make payment after selling the consignment.

c. Export against advancement payment

Sometimes exporter receives payment in advance. In that case Authorized Dealer should

obtain a declaration from the exporter on the “Advance receipt voucher” certifying the

purpose of the remittance. Then the exporter will export the goods against the advance

payment.

5.3.5 General Rules for ExportThere are some rules, which are mandatory for export of any goods form Bangladesh. The

rules are as under:

(1) No Person can export any goods from Bangladesh, unless he is duly registered as an

exporter with the CCI & E.

(2) All export must be declared on the EXP form, which is consisting of 4 copies.

(3) Export mush is against any of the following:

a) Export L/C.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

b) Firm Contract.

c) Advance Payment.

(4) Transport documents related to land route or sea and any other Author8ized Dealer. The

Airway Bill and any other documents of title to car4go may be drawn to the order of a Bank

in the country of import. However in case of advance payment, transport document may be

drawn to the order of Foreign Importer Bank endorsement of transport documents is

prohibited. Directions under Sl. No. shall not apply in the following cases:

a) Export of Trade sample.

b) Personal Effects.

c) Goods shipped under the order of Govt.

d) Export of fresh fish, vegetable and fruits.

5.3.6 Export Documents CheckingAfter submissions of export documents by the exporter, Bank must check, whether the entire

required document submitted or not. Bank must examine all documents stipulated in the

credit with reasonable care to ascertain

whether or not they appear, on their face to

be in compliance with the terms and

conditions of the credit. The Banks will not

examine documents not stipulated in the

credit. To examine documents Bank must

follow the L.C terms and international

standard banking practice. Automated or

computerized carbon copies to be treated as original documents if it is marked ‘original’

Copy documents need not be signed. Multiple documents means one original and remaining

copies, Signature, Mark, Stamp or label is sufficient for authentication of document. Bank

will accept a prohibited in the L/C.

5.3.7 Export FinancingTo meet up the cost of the goods to be exported, the exporter, the exporter may require Bank

finance. Besides, he may require finance for go down rent, freight etc. Event after shipment

of the goods, exporter may require Bank finance to meet-up his current expenditure up to

repatriation of the export proceeds.

There are two types of export finance:

(I) Pre-shipment finance.

(ii) Post shipment finance.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

5.3.8 Pre-shipment finance

Pre-shipment investment is finance, allowed by a Bank to an exporter, to meet the cost up to

the shipment of the goods t overseas buyer. The purpose of the investment is to purchase raw

materials or finished goods or manufacturing processing, packing and transporting the goods.

5.3.9 Post shipment finance

There is a time gap between export of the goods and realization of the proceeds. So exporter

may require finance in that period to continue his business. So Bank may finance against

export documents ensuring the following:

1) Export documents comply the credit terms.

2) Buyer is bona-fide.

3) Party’s past performance is satisfactory.

4) Any other security in case of export under contract.

5.3.10 Aa. Security of Pre-shipment Investment

1) Bank will mark loin on the related export L/C.

2) Bank will finance against a L/C having sufficient time to procure the goods for export.

3) Finance to be done after arrival of the imported raw materials under back-to-back L/C.

4) Bank will supervise the production from time to time to ensure export of the goods in time.

5) If finance is applied for a particular purpose Bank will ensure the proper use of the money

for the purpose only.

6) Change documents to be signed by the exporter before disbursement of the PSI.

7) In case of Quota finance, Quota allocation letters to be kept lien with the Bank.

8) Bank will adjust the liability proportionately from related export documents.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

5.4 Remitance5.4.1 Meaning of RemittanceThe word “Remittance” originates from the word “remit” which means to transmit money/

fund. In banking terminology the word “remittance means transfer of fund one place to

another. When money transferred from one country to another is called “Foreign Remittance”

5.4.2 Types of RemittanceForeign remittance may be classified into.

Inward Foreign Remittance.

Outward Foreign Remittance.

5.4.3 Inward Foreign Remittance

Inward Foreign Remittance means Remittance received from foreign countries from abroad.

In other words remittance coming into our country from other countries by the remitter by

way of permissible banking channel through freely convertible Foreign Currencies is called

‘Inward Foreign Remittance’ i.e. payless point of view it is inward foreign remittance. On the

other hand remitter’s point of view it is called outward Foreign Remittance. During The year

1995-1996 Bangladesh received and amount of US$ 1217.062 Mil as Foreign remittance. The

above process of Remittance may be presented diagrammatically as under:

5.4.4 Outward Remittance

Outward remittance of funds be made by means of T.T., D.D.T.T. etc. the remitter has to

deposit money along with the application contains name and address of the payee name of the

currency etc. All outward remittances must cover the transactions approved by the

Bangladesh Bank. Which are usually for importers travel & educational expenses.

5.4.5 Direct/ Indirect Remitter

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

Wage Earners: Bangladeshi citizens are working abroad both in private sector & in Govt.

Sector.

Indenture: Indenting commission & Agency commission received from suppliers from

abroad. Bangladeshi citizens are working in Bangladesh Embassy abroad.

Donors: Foreign Donors can only remit to Bangladesh through the Govt. Register

Organization & institution etc.

Exporters: Export proceeds also remitted to Bangladesh against exporting of goods.

Instruments of Foreign Remittances Cash for : Dollar, Pound, France Fr. Riyal or any other currency.

T.C : Travelers Cheque.

F.D.D : Foreign Demand Draft.

T.T : Telegraphic Transfer, Cable transfer or swift transfer.

M.T : Mail Transfer.

I.M.O : International Money Order.

Cheque : By any person & institution..

P.O : Payment Order.

5.5 Foreign Exchange Performance of AL-ARAFAH ISLAMI BANK

AL-ARAFAH ISLAMI BANK has glorious history in mobilizing Foreign Exchange

Business. Over the years the bank’s Foreign Exchange Business was a record high amount

among all banks in Bangladesh.

The Bank has a wide Network of Authorized Dealers throughout the year. Well- equipped

and international network with skilled manpower, the bank is confident of running Foreign

Exchange business efficiently to the satisfactory of importers, exporters and Bangladeshi

Expatriates working abroad.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

From the coefficient table, we can see that the beta coefficient of XI which is customer

satisfaction of Al-Arafah Islami Bank is .931 which shows a positive relationship between

overall performance of Al-Arafah Islami Bank and satisfaction of customers towards the

bank.

6.1 SWOT Analysis

Like other organizations, AIBL also have its strength, weakness, opportunities and threats.

The following stated the SWOT analysis of the bank.

Strengths

AIBL provides its customer excellent & consistent quality in every service.

AIBL is a financially sound company.

AIBL utilize state of the art technology to ensure consistent quality & operation.

AIBL provides its works force an excellent place to work.

AIBL has already achieved goodwill among the clients.

AIBL has a research division.

Weakness

They have a very few number of branches and foreign exchange department. This is a

great weakness. If they cannot recover this weakness, they will not increase earnings

from foreign exchange sector.

They cannot open sufficient number of L/C in a month. Because they have not enough

exporter and importer. This is another great weakness for foreign exchange

department.

Risk Management system is not strong. The bank has already exposed to a variety of

risks the most important of which are credit risk, market risk and liquidity risk.

1

Internship Report on “Foreign Exchange Operational of Al-Arafah Islami Bank”

IT Division is not strong because bank put due importance to utilization of technology-

based service to the customers.

Opportunities

Emergence of E-banking will open more scope for AIBL.

AIBL can introduce more innovative and modern customer service.

Many branches can be open in remote location.

Threats

The world wide trend of mergers and acquisition in financial institutions is causing

problem.

Frequent taka devaluation and foreign exchange rate fluctuation is causing problem.

Lots of new banks are coming in the scenario with new service.

Local competitors can capture huge market share by offering similar products.

Recommendations

It goes without saying that AIBL has turned over a new leaf of general people through the

invention of new products, which are easily introduced and accepted by the general people on

account of its reliability and flexibility.

Overall my observation we can say that customer service quality AIBL is good and

continuously meets the challenges of developing new product and service.

AIBL is a well-known private bank in Bangladesh. It is high time to improve the performance

to provide the international flavored service by a Local bank. A set of recommendation is set

forth below to improve the banking service:

AIBL can diffuse its scope of investment through focusing Shariah concept regarding

investments among the Bank officers; employer and the Clients by strong training,

workshops and Clients get - together.

The authority of AIBL should exert pressure on Government bodies to run proper and

sufficient application of Islamic banking laws in Bangladesh.

Practice amount of doubtful income declined substantially during the year as

compared to the past few years, indicating more carefulness of the Management in