BOC Pension Scheme Valuation Special · PDF fileBOC Pension Scheme . Valuation Special...

12

BOC Pension Scheme Valuation Special Newsletter. Your Scheme’s financial health check

Transcript of BOC Pension Scheme Valuation Special · PDF fileBOC Pension Scheme . Valuation Special...

BOC Pension Scheme Valuation Special Newsletter.

Your S

cheme’s

finan

cial

health ch

eck

Designed and produced by A

nthony Hodges C

onsulting Limited 2015_101951

2 Valuation Special Newsletter

Chairman’s WelcomeWelcome to the Valuation Special Newsletter for active, deferred and pensioner members of the BOC Pension Scheme (the Scheme).

In this special newsletter is a summary of the results of the most recent actuarial valuation, which was carried out as at 31 March 2014. An actuarial valuation is the Scheme’s regular financial health check. You can also find details of the recent review of the Scheme factors – see pages 10 and 11.

If you have any questions about the information provided in this newsletter, or the Scheme in general, please contact BOC Pension Services using the contact details shown on the back page.

John Hylands, Chairman of the Trustee Board.

3Valuation Special Newsletter

At 30 April 2015, the Pension Protection Fund reported that 78.74% of defined benefit pension schemes were in deficit*.

*Source: PPF 7800 Index – 30 April 2015

i

What is an actuarial valuation?

The actuarial valuation is normally carried out every three years by an actuary, a qualified professional who is independent from the pension scheme and the employer.

Pension schemes are required to meet the Statutory Funding Objective, which is to have enough assets to meet the expected cost of members’ benefits built up to the valuation date. If the assets are greater than the liabilities, the scheme is in surplus. If the liabilities are greater than the assets, the scheme is in deficit.

An actuarial valuation is a ‘snapshot’ of a pension scheme’s funding position at a set date.

It reviews:

Compared to:

The valuation is carried out on:

The value of a scheme’s assets (the money it has available).

Its liabilities (the money needed to pay benefits to members now and in the future, based on pensionable service to the valuation date).

• An ongoing basis, which assumes that the pension scheme will carry on as it is now; and

• A discontinuance basis, which assumes that the pension scheme is wound up at the valuation date.

4 Valuation Special Newsletter

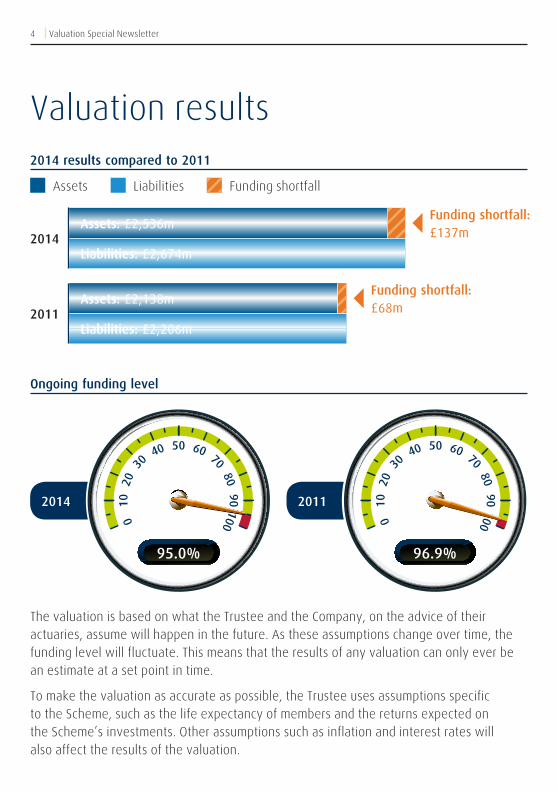

Valuation results

2014

2011

2014 results compared to 2011

Ongoing funding level

Assets Liabilities Funding shortfall

Funding shortfall: £137m

Funding shortfall: £68m

The valuation is based on what the Trustee and the Company, on the advice of their actuaries, assume will happen in the future. As these assumptions change over time, the funding level will fluctuate. This means that the results of any valuation can only ever be an estimate at a set point in time.

To make the valuation as accurate as possible, the Trustee uses assumptions specific to the Scheme, such as the life expectancy of members and the returns expected on the Scheme’s investments. Other assumptions such as inflation and interest rates will also affect the results of the valuation.

Liabilities: £2,674m

Assets: £2,536m

Assets: £2,138m

Liabilities: £2,206m

2014 2011

504030

2010

0

10090

80

7060

95.0%

504030

2010

0

10090

80

7060

96.9%

5Valuation Special Newsletter

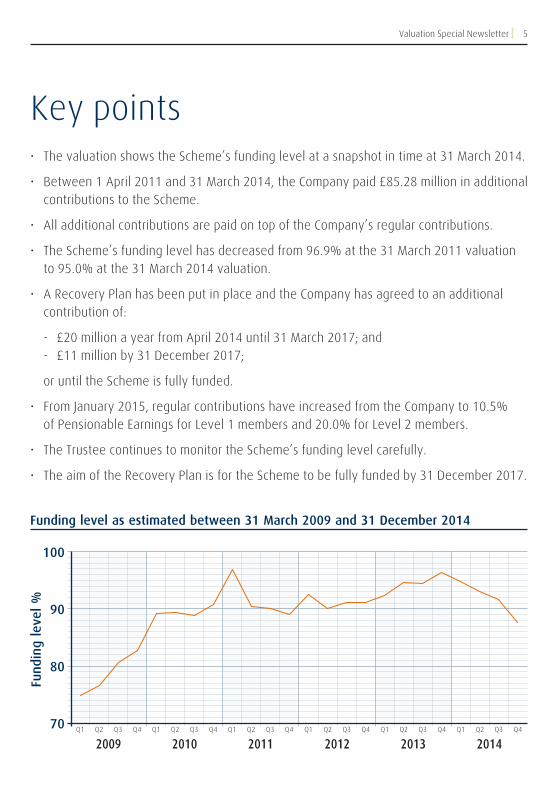

Key points• The valuation shows the Scheme’s funding level at a snapshot in time at 31 March 2014.

• Between 1 April 2011 and 31 March 2014, the Company paid £85.28 million in additional contributions to the Scheme.

• All additional contributions are paid on top of the Company’s regular contributions.

• The Scheme’s funding level has decreased from 96.9% at the 31 March 2011 valuation to 95.0% at the 31 March 2014 valuation.

• A Recovery Plan has been put in place and the Company has agreed to an additional contribution of:

- £20 million a year from April 2014 until 31 March 2017; and - £11 million by 31 December 2017;

or until the Scheme is fully funded.

• From January 2015, regular contributions have increased from the Company to 10.5% of Pensionable Earnings for Level 1 members and 20.0% for Level 2 members.

• The Trustee continues to monitor the Scheme’s funding level carefully.

• The aim of the Recovery Plan is for the Scheme to be fully funded by 31 December 2017.

Funding level as estimated between 31 March 2009 and 31 December 2014

20102009 20122011 20142013

80

70

90

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

6 Valuation Special Newsletter

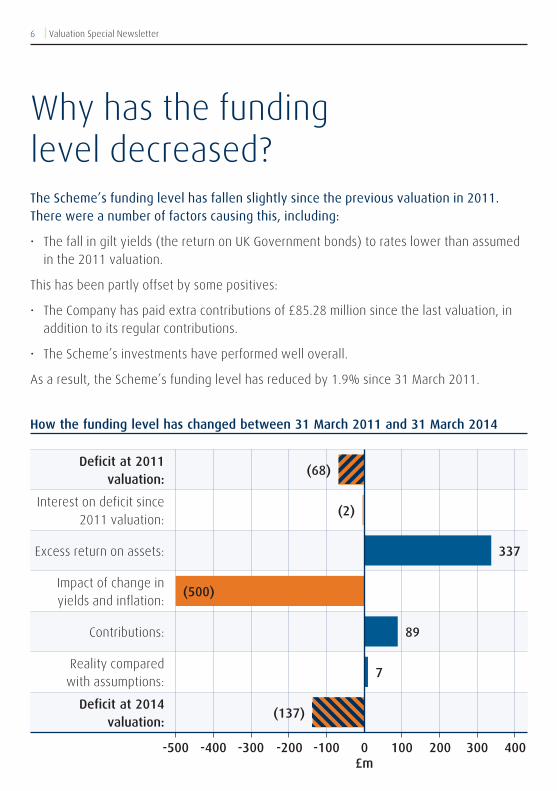

Why has the funding level decreased?The Scheme’s funding level has fallen slightly since the previous valuation in 2011. There were a number of factors causing this, including:

• The fall in gilt yields (the return on UK Government bonds) to rates lower than assumed in the 2011 valuation.

This has been partly offset by some positives:

• The Company has paid extra contributions of £85.28 million since the last valuation, in addition to its regular contributions.

• The Scheme’s investments have performed well overall.

As a result, the Scheme’s funding level has reduced by 1.9% since 31 March 2011.

How the funding level has changed between 31 March 2011 and 31 March 2014

Deficit at 2011 valuation:

Excess return on assets:

Interest on deficit since 2011 valuation:

Impact of change in yields and inflation:

Contributions:

Reality compared with assumptions:

Deficit at 2014 valuation:

0-500 -100

(137)

(2)

(68)

7

89

337

100-200 200-300 300 400-400£m

(500)

7Valuation Special Newsletter

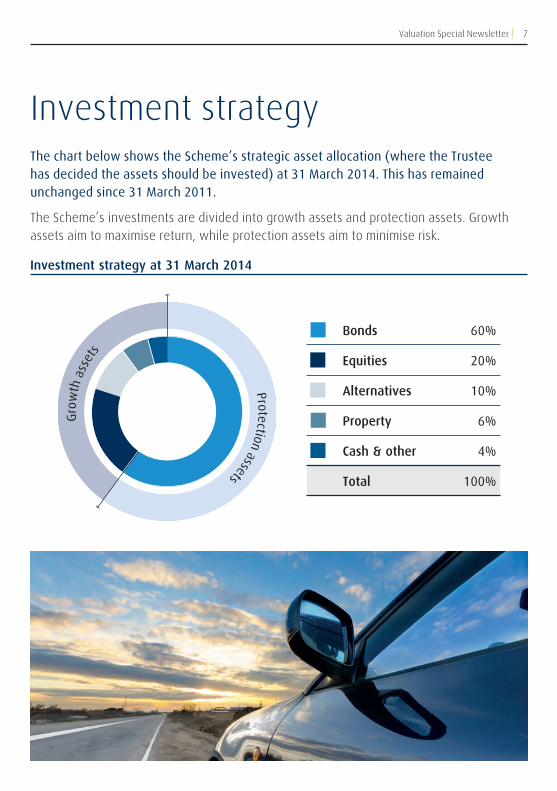

Investment strategy at 31 March 2014

Investment strategyThe chart below shows the Scheme’s strategic asset allocation (where the Trustee has decided the assets should be invested) at 31 March 2014. This has remained unchanged since 31 March 2011.

The Scheme’s investments are divided into growth assets and protection assets. Growth assets aim to maximise return, while protection assets aim to minimise risk.

Gro

wth

ass

ets

Protection assets

Bonds 60%

Alternatives 10%

Cash & other 4%

Equities 20%

Property 6%

Total 100%

8 Valuation Special Newsletter

What has been agreed following the Scheme’s 2014 valuation?As part of the valuation process, after taking advice from the Scheme Actuary, the Trustee has agreed the following with the Company:

Statement of Funding Principles

Schedule of Contributions

Recovery Plan

This is the Trustee’s policy for ensuring that the Statutory Funding Objective is met over a specific time period.

This details the regular contributions to be made by the Company to the Scheme to meet the cost of future benefits. From 1 April 2014, the Company contributions were 5.7% of Pensionable Earnings for Level 1 members and 12.3% of Pensionable Earnings for Level 2 members. From 1 January 2015, the Company contributions increased to 10.5% of Pensionable Earning for the Level 1 members and 20.0% of Pensionable Earnings for Level 2 members.

This sets out how the Company will address the Scheme’s funding shortfall.

• The new Recovery Plan, designed to ensure that the Scheme’s assets fully cover the liabilities, has been in place since 6 November 2014.

• The Company has agreed to make additional payments of: - £20 million a year for three years; and - £11 million by 31 December 2017;

or until the Scheme is fully funded.

• The Trustee monitors the Scheme’s funding position every quarter and the Recovery Plan can be revised if necessary.

9Valuation Special Newsletter

What is the funding level on a discontinuance basis?The discontinuance basis assumes that the Scheme is discontinued (‘wound up’) on the valuation date. Inclusion of this information is a legal requirement and does not mean that there is any intention to wind up the Scheme.

In the unlikely event that the Scheme was to wind up, the Company would have to pay enough into the Scheme to cover the cost of buying members’ benefits from an insurance company.

The discontinuance funding level, similarly to the ongoing funding level, has decreased compared to the 2011 valuation. The results of the 2014 valuation showed a discontinuance funding level of 67.0%, a reduction on the 2011 discontinuance funding level of 75.4%.

Have there been any payments from the Scheme to the Company?

The Trustee can confirm that there have been no payments to the Company out of the Scheme since the last Summary Funding Statement issued in 2013 (or indeed ever), other than to reimburse the Company for the costs of administering the Scheme.

10 Valuation Special Newsletter

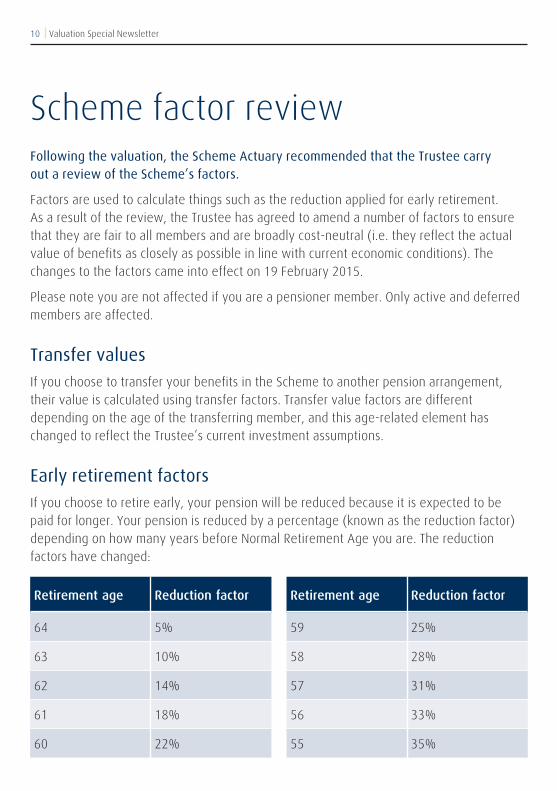

Scheme factor reviewFollowing the valuation, the Scheme Actuary recommended that the Trustee carry out a review of the Scheme’s factors.

Factors are used to calculate things such as the reduction applied for early retirement. As a result of the review, the Trustee has agreed to amend a number of factors to ensure that they are fair to all members and are broadly cost-neutral (i.e. they reflect the actual value of benefits as closely as possible in line with current economic conditions). The changes to the factors came into effect on 19 February 2015.

Please note you are not affected if you are a pensioner member. Only active and deferred members are affected.

Transfer values

If you choose to transfer your benefits in the Scheme to another pension arrangement, their value is calculated using transfer factors. Transfer value factors are different depending on the age of the transferring member, and this age-related element has changed to reflect the Trustee’s current investment assumptions.

Early retirement factors

If you choose to retire early, your pension will be reduced because it is expected to be paid for longer. Your pension is reduced by a percentage (known as the reduction factor) depending on how many years before Normal Retirement Age you are. The reduction factors have changed:

Retirement age

64

62

63

61

60

59

57

58

56

55

Retirement ageReduction factor

5%

14%

10%

18%

22%

25%

31%

28%

33%

35%

Reduction factor

11Valuation Special Newsletter

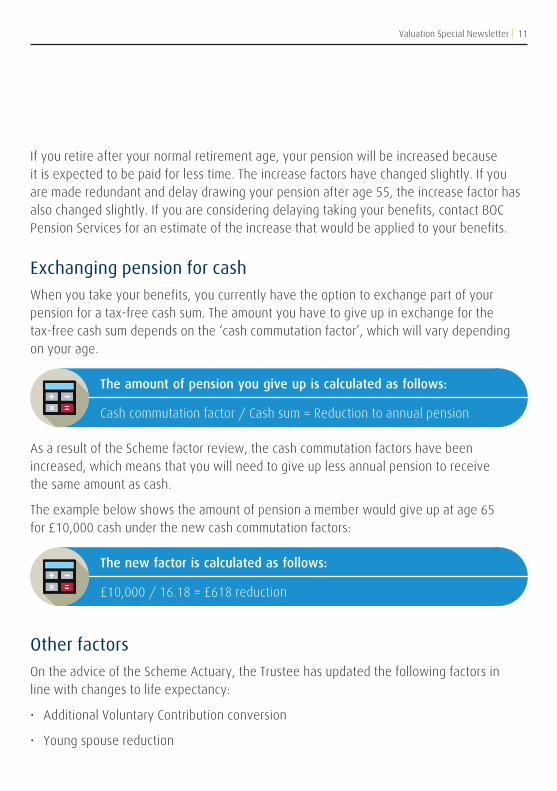

If you retire after your normal retirement age, your pension will be increased because it is expected to be paid for less time. The increase factors have changed slightly. If you are made redundant and delay drawing your pension after age 55, the increase factor has also changed slightly. If you are considering delaying taking your benefits, contact BOC Pension Services for an estimate of the increase that would be applied to your benefits.

Exchanging pension for cash

When you take your benefits, you currently have the option to exchange part of your pension for a tax-free cash sum. The amount you have to give up in exchange for the tax-free cash sum depends on the ‘cash commutation factor’, which will vary depending on your age.

As a result of the Scheme factor review, the cash commutation factors have been increased, which means that you will need to give up less annual pension to receive the same amount as cash.

The example below shows the amount of pension a member would give up at age 65 for £10,000 cash under the new cash commutation factors:

The amount of pension you give up is calculated as follows:

Cash commutation factor / Cash sum = Reduction to annual pension

The new factor is calculated as follows:

£10,000 / 16.18 = £618 reduction

Other factors

On the advice of the Scheme Actuary, the Trustee has updated the following factors in line with changes to life expectancy:

• Additional Voluntary Contribution conversion

• Young spouse reduction

Contact details

BOC Pension Services are on hand to help with any questions you have in relation to the Scheme. You can contact us at:

BOC Pension Services

The Priestley Centre

10 Priestley Road

The Surrey Research Park

Guildford

Surrey

GU2 7XY

Helpline: 0800 096 3214 (BOC TEL 750 4745)

Fax: 01483 244 739

Email: [email protected]

Website: www.bocpensions.co.uk

Smartphone users with a QR code app can

scan this code to visit our website.

Legal note

Please note that this newsletter is intended to outline the results of the actuarial valuation as at 31 March 2014 and the Scheme factor review and nothing in it grants any legal rights to benefits. Your entitlement to benefits is defined in the Trust Deed and Rules at the date you leave service (as amended from time to time). You can download a copy of the current Trust Deed and Rules from the website at www.bocpensions.co.uk or request one from BOC Pension Services. If you are a deferred member or pensioner you should ask for a copy of the edition which applied when you left service or retired.

July 2015

Where can I get further information?If you have any questions or would like further information, please contact BOC Pension Services. The Scheme documents, such as the full Valuation Report and the Schedule of Contributions, are available on request from BOC Pension Services.

Designed and produced by A

nthony Hodges C

onsulting Limited 2015_101951