bne chairman list 010614

67

This is bne's Russia chairman’s newsletter, a selection of forward looking stories on development in eastern Europe and the region. Feel free to request topics or ask questions: [email protected] Contents: Top Story Ukraine crisis has been an economic train wreck for Russia Putin lays out action plan for technological modernisation of Russia in St Petersburg Russia oil addiction myth Politics – the good State Duma could bring back imprisonment for corruption Russia ramps up fines for obtaining and revealing commercial secrets Russian upper house passes bill on fines for hiding dual citizenship Number of economic crimes in Russia down by 20% About 23,000 convicts released under presidential amnesty in Russia Five convicted of killing Russian journalist Politkovskaya Russian government slashes red tape to unleash housing construction Government bans trust funds for officials Politics – the bad Putin celebrates being Presidents for 10 years Russian government and companies spend 2% of GDP on compliance checks Putin tightens curbs on protesters Moscow denies gay pride parade for ninth time in a row Politics – the ugly Fraud probe launched against leading Russian journalist Rosneft President Sechin sues media over excessive salary claims Russian State Project Helped Fund 'Putin's Palace' Arrest order upheld against former Deputy Agriculture Minister Ex-senator detained in Moscow on suspicion of $50m embezzlement Military prosecutors uphold amnesty for Russia’s ex-defence minister Polls, mood, sociology Russia's consumer confidence index dropped drastically in May Putin, Medvedev popularity hits all-time highs Russians pour spare cash into real estate to protect it Less Russians fear growing old

description

Hard core wrap of the main economic, business and finance news in Russia for the last month

Transcript of bne chairman list 010614

This is bne's Russia chairman’s newsletter, a selection of forward looking stories on development in eastern Europe and the region. Feel free to request topics or ask

questions: [email protected]

Contents: Top Story

Ukraine crisis has been an economic train wreck for Russia Putin lays out action plan for technological modernisation of Russia in St Petersburg Russia oil addiction myth

Politics – the good

State Duma could bring back imprisonment for corruption Russia ramps up fines for obtaining and revealing commercial secrets Russian upper house passes bill on fines for hiding dual citizenship Number of economic crimes in Russia down by 20% About 23,000 convicts released under presidential amnesty in Russia Five convicted of killing Russian journalist Politkovskaya Russian government slashes red tape to unleash housing construction Government bans trust funds for officials

Politics – the bad

Putin celebrates being Presidents for 10 years

Russian government and companies spend 2% of GDP on compliance checks Putin tightens curbs on protesters Moscow denies gay pride parade for ninth time in a row

Politics – the ugly

Fraud probe launched against leading Russian journalist Rosneft President Sechin sues media over excessive salary claims Russian State Project Helped Fund 'Putin's Palace' Arrest order upheld against former Deputy Agriculture Minister Ex-senator detained in Moscow on suspicion of $50m embezzlement Military prosecutors uphold amnesty for Russia’s ex-defence minister

Polls, mood, sociology

Russia's consumer confidence index dropped drastically in May Putin, Medvedev popularity hits all-time highs Russians pour spare cash into real estate to protect it Less Russians fear growing old

Only 52% of Russians identify with any political party Opposition leader Navalny's popularity in the polls is falling Russians Prefer Direct Mayoral Elections, Poll Says Russians satisfied with quality of life Public's desire to protest hits record low Russia is worst place for foreign investment Moscow, St. Petersburg Near Bottom in Regional Investment Rating Only 8% of top-managers of international companies think that the business environment in Russia is favourable Third of European companies will increase Russian investment, half to keep on same level 94% of Russians Depend on State TV for Ukraine Coverage Enthusiasm for ties with the west of fading in Russia Russians are world's 2nd highest spenders on alcohol Russians are increasingly nostalgic for the Soviet era

Banks and Finance

Russian Banking sector profitability falls further behind asset growth BRICS emerging nations to launching bank for 2016 Every seventh Russian retail loan is in arrears (NPLs)

NPLs in Russia are rising but not as much as in other countries Japan's payment system JCB to enter Russia VTB results were hammered in the first quarter, state to boost state bank capital Corporate loans were up by 18% year-on-year in April Government subordinated lending up as government props up sector Visa, MasterCard ready to continue operations in Russia Share of dollars in domestic retail deposits soars Russian government sends financial ombudsman bill to Duma Russian state sets up a RUB50 SME loan guarantee agency Russian banks to help exporters bill contracts in rubles

Economics Crisis in Ukraine cripples Russia's foreign trade… … but Russia's trade balance improves dramatically Russia's regions threaten to become an Achilles' heel Russian retail trade growth slowed to 2.6% year-on-year in April Domestic goods boost Russian April industrial output Just over third of Russian firms loss-making in January-March Investments declined but not as sharply as expected

Russia's CBR sees capital outflow at $85-$90bn in 2014 Inflation stabilizes at 7.4% year-on-year, could rise to 8% Value of the ruble remains volatile, but stabilizing recently Russians rush to ditch ruble on devaluation, political fears Government implements only half of Putin's "May decrees" Russian budget runs surplus over 4m14, on track for flat or small surplus this year Russian federal budget would likely remain intact under stricter sanctions Russian spring amendments to 2014 budget law - to spend or not to spend is NOT the question Russian PMI down, waning orders block growth New real estate tax may triple Russians' tax burden Demographic crisis declining in Russia

ECM

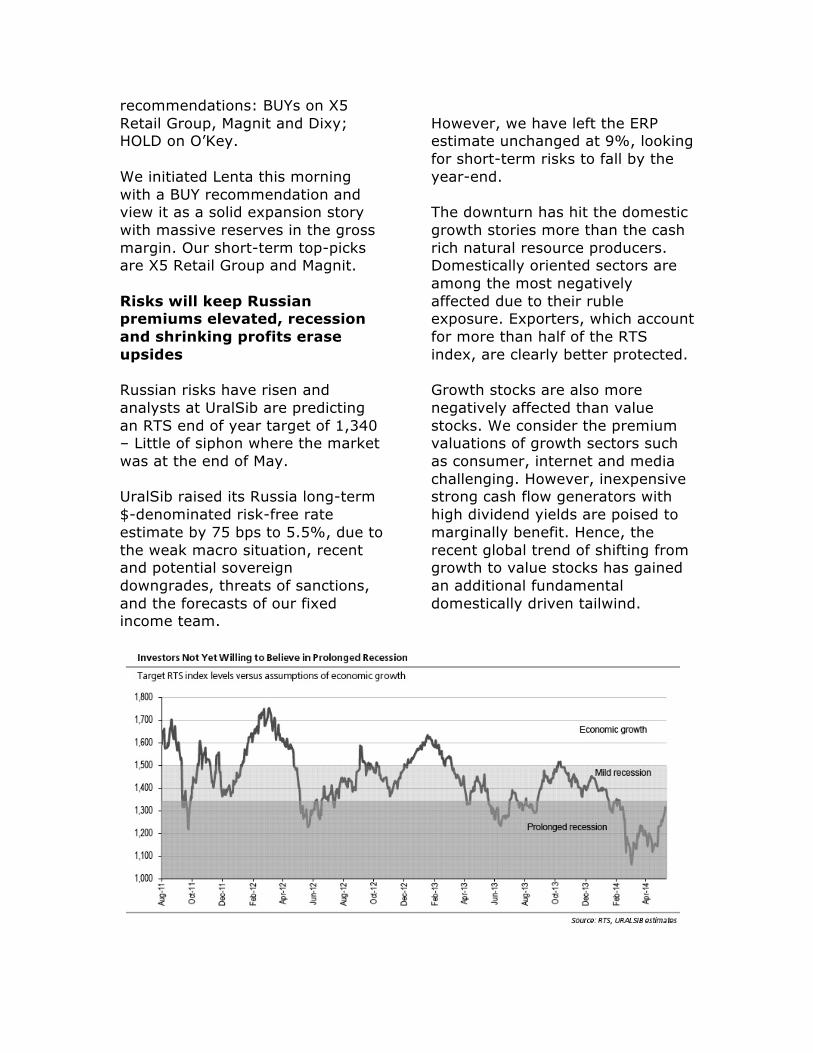

Is a party about to start in Russian stocks? Russian Consumer companies sell off heavily and harder than overall market Risks will keep Russian premiums elevated, recession and shrinking profits erase upsides MinFin says pension age may increase ETF inflows more than matched by our flows from Russian specialist funds

Russia not popular amongst international portfolio investors

DCM

Russian firms finding it harder to get international financing Russian government cuts 2014 domestic borrowing plan to RUB135bn, cancels international borrowing Russia's foreign debt falls 1.6% to $55bn in the first quarter Crisis has put pressure on Russian bonds yields US sanctions threaten freeze on Russian bonds

Sectors

Austria South Stream gas pipeline deal undermines wests attempt to punish Russia over Ukraine Russia's Rosneft to boost hydrocarbon output 30% by 2020 Russia's Industry and Trade Ministry does not plan to resume the automotive bailout program Supermarket chain Dixy Group revenue growth accelerates in April Russia's No. 1 Military Producer Reports Growing Revenues Russian advertisement market shows reasonable growth in 1Q14 Russian mobile TV market to reach RUB16bn by 2015 State-owned telco giant Rostelecom launches the Sputnik search engine Russian online stores' sales up 25% to RUB520bn in 2013

Top Story Ukraine crisis has been an economic train wreck for Russia The Ukraine crisis has been an economic train wreck for Russia. The outlook for this year was never good, but on April 30 the International Monetary Fund (IMF) argued the Russian economy is already in recession and a growing number of analysts believe the economy will shrink this year. That's bad news for Russian President Vladimir Putin. Last year's slowdown came as a surprise, but this was supposed to be the year of recovery. However, predictions about the economy have been steadily worsening as the months wore on: analysts began the year predicting 1.5% growth for the year, but that fell to 0.3% growth more recently. Now the IMF has slashed its growth forecast for Russia for the second time in less than a month after the economy contracted by 0.5% in the first three months of this year, saying that international sanctions and the fear of more threaten to prolong the recession. "If you understand by recession two quarters of negative economic growth, then Russia is experiencing recession now," IMF mission chief Antonio Spilimbergo told reporters on April 30.

The IMF said Russia’s economy is on track to grow by just 0.2% this year, rather than the 1.3% it forecast earlier, warning that further downgrades were likely unless the Ukrainian crisis abated. Christopher Hartwell, head of Global Markets and Institutional Research at Skolkovo Institute for Emerging Market Studies (SIEMS), is just as pessimistic. "I think Russia is already in recession and the economy will contract this year," he says in an interview with bne. There seems little doubt now that despite more optimistic government forecasts, the Russia’s economy will dive below zero in the second quarter of this year thanks partly to massive capital outflows

and lack of investment. At the same time, capital flight surged to $20bn-25bn in March, which implies GDP growth for March may have already gone negative. No way out The problem for the Kremlin is there is little it can do to stop the slowdown. While other governments around the world have slashed interest rates close to zero that is not an option for Russia. "Money stimulus is suicide," said Hartwell. "Russia has got as far as it can go with the capital account or using money from the National Reserve Fund. If the central bank cuts rates, all that will happen is you'll send inflation soaring and will see the money used to buy more imports." Capital flight is also putting pressure on Russia's banking sector, which should be one of the main sources for the badly needed investment money. The outflows have made cash scarce, so banks instead of lending are struggling to avoid a liquidity-driven crisis. "There is no investment because there is a small pool of capital and therefore the cost of the capital is high," says Hartwell. "The high interest rates represents concern, but there is also a high risk premium in Russia. The central bank can't cut interest rates, as that would just lead to inflation and growing imports." The tanking ruble, which has lost 9% of its value since the start of the year, forced the central bank to spendbns of dollars to prop up its value. That has only reduced the

pool of capital further and adds further the pressure on the banks. Banks have turned to the Central Bank of Russia (CBR) in droves. In March Russian banks borrowed a record post-crisis amount of RUB735bn ($21bn) via repurchase agreement, or repo, transactions, as well as credits under non-market assets (bank-bills, rights of claims on credit agreements, other banks guarantee) from the CBR. Now banks owe an all-time high of RUB4.7 trillion ($134bn) to the central bank as of April 1, 2014 – amounts comparable to what banks borrowed from the CBR during the onset of the global crisis in 2008, according to Alfa Bank research. Policy vacuum Russia's cash pile will buy it some time, but clearly drastic action is needed to turn the situation around. With no fiscal tools to hand and the diminishing returns associated with state-funded megaprojects, the only real solution is to make deep structural reforms. "Previously, Russia was growing so fast it didn't matter how bad the government was. But now with the economic slowdown bad government makes all the difference," says Hartwell. And here the situation doesn't look good. A fight broke out in April between Russia's finance and economy ministries. The Ministry of Economic Development wanted to increase spending in the hope of boosting growth, but the finance ministry wanted to stick to the so-called "budget rule," which limits

the amount that the government can spend. So far the finance ministry has the upper hand: Putin threw his support behind sticking to the budget rule in remarks to the press in April. The government cut federal expenditure growth to just 4% in 2013, after increasing it by 18% in 2012 thanks to unusually high revenue receipts in Russia's regions and a reduction in social payments. This year the government may tap the National Welfare Fund to meet its obligations, however the $85bn in the fund will not last forever. "Putin admitted that the problems are internal not external," says Hartwell. "Today there is strong leadership in Russia and people love that, but how beholden is Putin to the bureaucracy? The economics ministry has no coherence policy plan. Different parts of the government are working against each other. There is no comprehensive economic programme or coordination amongst the different branches of government."

The one bright light in the Russian economy is the Russian regions. Some of the more progressive are making just the reforms that the country as a whole needs to see. The most successful – like Tatarstan and Kaluga – are easily outperforming the rest of the economy as a result. "Russia's regions have become the laboratory of innovation. They are creating laws and processes needed at a federal level. But it takes time for those policy ideas to work their way up to the national level. A big part of Russia's problems is that it's still a top-down mentality," says Hartwell. "It's the janitor effect: the opinion of a PhD in the field is worth less than that of the janitor in the head office." Hartwell says that this crisis should be put to use to make painful changes. There was a missed opportunity in 2005 and the WTO accession was another opportunity that was missed. "I am cautiously optimistic, trending towards optimistic, but it's going to be hard work," says Hartwell.

Putin lays out action plan for technological modernisation of Russia in St Petersburg In his keynote speech at the St Petersburg International Economic Forum (SPIEF), President Vladimir Putin shared his views on geopolitics, Russia-Ukraine relations, the China gas deal and related investments. The president also talked through the recent achievements in the economy, summarised what progress there had been on the path to improving the business climate and presented an updated action plan to spur growth and foster a technological revolution/modernisation. In what follows, we summarise the key points of the action plan, as well as the relevant macro and sector implications. 1. Cheap long-term funding. President Putin suggested extending access to cheap funding for investments via project financing, particularly in manufacturing. The final borrowing cost on such project financing facilities is to be capped at CPI+1%. The government and the CBR are to present the plan soon and comprehensive legislation is to be finalised by EY14. The implications are unclear at this stage, as the government is yet to elaborate on specific measures. There are potentially three ways to ensure low borrowing costs: i) an interest rate subsidy from the budget; ii) pressure on banks’ margins; and

iii) subsidised back-to-back funding from the CBR. Given the recent introduction of the new three-year refinancing facility from the CBR, with an interest rate lower than the key policy rate, the government might be inclined to contemplate the third option. Whatever the final choice (or mix), we note that the shift towards non-market based pricing for loans, while admittedly helpful for growth/investment in the short term, might ultimately result in the suboptimal allocation of capital (similar to what happened in Brazil). Subsidised borrowing costs for government-sponsored/approved projects would have to be offset by higher interest rates for the private sector. Thus, the equilibrium macro-wide interest rate remains the same, but more (subsidised) capital is allocated to the state sector. 2. Improve conditions for greenfield projects. In particular, the president proposed granting tax benefits for greenfield projects. To make it neutral from the fiscal standpoint, tax benefits need to be capped at the value of the project’s initial investment. The idea of tax incentives for new businesses is not new. In particular, the government is considering allowing regions to introduce tax holidays for new SMEs, while the new initiative would extend it to large businesses as well.

Also of note, in April the government submitted the draft law on ‘Territories that are a Development Priority’, which envisages a comprehensive set of tax and other benefits for new businesses in the Russian Far East. Overall. Analysts welcomed this initiative as if properly structured, tax incentives have a higher long-term fiscal multiplier than budget spending. 3. Recapitalisation of systemically important banks. One of the mechanisms mentioned was converting previously granted (in 2008-09) NWF-sponsored subordinated loans into preferred shares. From the credit perspective, this measure would likely be positive for both sentiment on and the ratings of state-controlled banks, as an indication of the state’s willingness to support banks, even if there is no full clarity on the exact recapitalisation mechanisms. Converting the subordinated loans provided by VEB in 2008-09 and back-financed by NWF (based on the ‘anti-crisis’ law #173-FZ) into Tier I equity or hybrids is one of the likeliest solutions. The total amount is RUB400bn, with VTB, Gazprombank and Russian Agricultural Bank as the major recipients. While the immediate effect of such a conversion on a bank’s overall capital base is rather neutral, it would strengthen the core component of capital, offsetting the amortisation effects of sub debt.

The government is also demonstrating its willingness to provide fresh capital to systemically-important banks “if needed” (paid in cash or OFZs). Analysts think this must be viewed as a contingent mechanism i.e. also without any immediate implications for most banks other than improving market sentiment. 4. Easier access to government guarantees. Putin highlighted that access to the state guarantee mechanism and related formalities must be eased significantly. Coming on top of the first point of the action plan (cheap long-term funding), this fits well with the shift back towards a state-led growth model, whereby more capital is allocated to government-sponsored/approved projects. It is probably not a coincidence that the recently introduced three-year refinancing facility (with a lowered interest rate) allows large banks to pledge only those investment loans that are backed by state guarantees. Hence, the initiative to ease access to guarantees might be an indication that the authorities want to ramp up this facility. The medium-term implication is higher interest rates for the private sector, as the CBR would be reluctant to cut its (non-subsidised) key policy rate in order to achieve the same equilibrium macro-wide interest rate. 5. Import substitution. The president highlighted the importance of modernising and localising industry for import substitution (particularly in

software, electronics and power engineering, the textile industry and agriculture) which is now seen as one of the priorities for economic policy. He stressed that no trade restrictions should be contemplated, and pointed out that the term ‘local producer’ also relates to foreign-owned subsidiaries. Among specific policy measures, Putin mentioned support (interest rate subsidies or loans) from special state fund and restrictions on certain imported goods (which have competitive, locally produced substitutes) for government procurement programmes. 6-7. Industrial modernisation. The president pointed to a two-pronged policy approach. On the one hand, the government needs to work out an incentive mechanism (tax breaks, etc.) for companies implementing modern technologies. On the other hand, the cost of running out-dated and 'dirty' technologies must be increased. On the latter point, an audit of production capacities is to be carried out in 2015-16 and then a higher tax levied on those using dirty and hazardous technologies. 8. Budget funding. The government is to assess the fiscal commitments required to fund the aforementioned policy measures (technological refitting) and make appropriate provisions in the budget law for 2015-17. 9. Infrastructure investment. The construction of the two NWF-funded projects (Central Ring Road around Moscow and the expansion of the Trans-Siberian railway link)

is to start this summer. President Putin also reiterated the goal to double the construction of roads and mentioned PPP as one of the mechanisms to attract the required financing from the private sector. Although no new projects were mentioned, the Ministry for the Economy is looking to expand the list. Seven new projects with total investments of RUB 920bn (RUB 470bn to be sourced from NWF) were mentioned recently as the most likely candidates. Should all the projects go through the approval procedures, the government would need to lift the self-imposed maximum cap on domestic investment from the NWF (currently 40%). On a general note, we think that as the impact of infrastructure investments funded by the NWF, RDIF and state companies increases, investment activity is likely to recover in late 2014 and further into 2015.

Russia oil addiction myth

Russia's addiction to oil revenues is a myth. The former head of research at Alfa Bank and economic consultant Peter Szopo came up with an interesting charge in his weekly email. "What I found interesting though is [a chart in a paper from two IMF economists] shows the share of resource-based taxes in total government revenues. The surprising thing (to me at least) is that Russia stands much lower in this ranking than I would have thought. The figure for Russia seems to be in the mid-30s, while countries like Mexico, Malaysia, Kazakhstan and Venezuela have higher shares," Spozo wrote. Actually this should be a lot less surprising that it is. The rest of the world is fixated on the myth of Russia's addiction to oil and gas. However as bne pointed out in <a href="http://www.bne.eu/content/

moscow-blog-economist-takes-biscuit-worst-coverage-russia">an article earlier this year</a>, a study from respected bank of Finland's Institute for Economies in Transition into Russia's dependence on oil and gas is GDP concluded: "When adjusted to reflect the oil and gas sector's actual contribution to GDP, Russia is on par with Norway. This is much less than traditional oil states such as Saudi Arabia, which generates about half of its GDP directly from the oil and gas sector." Read the IMF paper <a href="http://www.voxeu.org/article/tax-policies-resource-rich-economies">here</a> Read the Bank of Finland paper<a href="http://www.suomenpankki.fi/bofit_en/tutkimus/tutkimusjulkaisut/policy_brief/Documents/2013/bon0313.pdf">here</a>

Politics – the good State Duma could bring back imprisonment for corruption Russia's Duma is debating bringing back prison sentences for corruption-related crimes instead of large fines. Several years ago, as a measure to liberalize criminal punishments, a law was adopted that replaced imprisonment with fines for corruption. The problem is that most officials don't pay the fines if the caught. The move is part of Putin's on going crackdown on corruption. The fines had brought no change in the level of corruption, said State Duma deputies. Russia ramps up fines for obtaining and revealing commercial secrets The Duma has passed a law that makes corporate spying illegal. Those caught could face fines of up to RUB1.5m ($43,500) or even a spell in jail of at least one year. The relevant amendments to the Criminal Code have been published on the website of planned legislation. The Finance Ministry proposed increasing the fines for these offences to match the fines approved for business fraud under Article 159.4.

Russian upper house passes bill on fines for hiding dual citizenship Russia's upper house of parliament, the Federation Council, passed a bill in May to increase the penalties for those concealing dual citizenship. Russian citizens must now notify the Federal Migration Service within two months of acquiring foreign citizenship. Failure to do so would result in a fine of up to RUB200,000 ($5,838) or up to 400 hours of compulsory community service. Number of economic crimes in Russia down by 20% The number of economic crimes has fallen by 20% after the adoption of a federal law, which restricts powers of law enforcement authorities, business ombudsman Boris Titov told President Vladimir Putin during the St Petersburg Economic Forum. The Interior Ministry was deprived of the right to initiate criminal cases on charges of tax evasion in 2011, after it became clear that officials were using the powers to extort money from businessmen. The resolution releases from criminal liability, regardless of the designated prison term, individuals convicted or held liable under 27

articles of the Criminal Code related to business activities. For the amnesty to take effect, a suspect or a convict has to return the property or compensate the damages to the complainants. About 23,000 convicts released under presidential amnesty in Russia Around 23,000 convicts have been released in Russia in accordance with the presidential amnesty, which has been arranged to coincide with the 20th anniversary of the Constitution of the Russian Federation, Russia’s Federal Penitentiary Service announced Tuesday. The State Duma in December unanimously adopted an amnesty bill submitted by Russian President Vladimir Putin. Five convicted of killing Russian journalist Politkovskaya Five men were convicted in May of murdering the investigative journalist and Kremlin critic Anna Politkovskaya in 2006, including three defendants who had been acquitted in a previous trial. Politkovskaya's killing drew attention to the risks faced by Russians who challenge the authorities and deepened Western concerns for the rule of law under President Vladimir Putin, who was then serving his second term. The family welcomed the result, but added: "The murder will only be solved when the name of the

person who ordered it is known," a lawyer for Politkovskaya's family, Anna Stavitskaya, was quoted as saying by RIA news agency. Russian government slashes red tape to unleash housing construction The government is slashing red tape in residential construction by 40% within the year, promising much-needed relief to a sector hobbled by excessive bureaucracy. Better access to construction permit was at the top of Putin's reform programme after he took office in 2012. It is also one of the eight factors in the World Bank's Doing Business ranking, where Russia does especially badly compared to the other countries in the survey. However despite Putin's orders to do something about the problem two years ago almost no progress has been made. The governments renewed effort shows both how seriously the Kremlin takes reforms but at the same time how difficult those reforms are to put in place. The list of administrative procedures faced by builders before construction will be cut to 134 from 220, according to an order signed in May by Prime Minister Dmitry Medvedev and published on the government's website. Construction companies currently have to cope with a list of 220 procedures set by the federal government and a proliferation of additional requirements specific to separate regions. While this

hampers all real estate developers, it causes particular problems for foreign investors, who have had to learn their way around regional as well as federal legislation, a spokesman for the Construction, Housing and Utilities Ministry said. Government bans trust funds for officials The Kremlin continued its crackdown on corruption in the government by introducing a band for officials on the use of trust funds. These have been widely used by members of the government because they effectively hide who the beneficial owner of the funds are. The band follows earlier laws that forbid government officials and employees of state and companies from holding either foreign assets or foreign bank accounts. Trust funds would have been an effective way to dodge these bans. The new law is intended to increase transparency and identify the beneficiaries of domestic

businesses. That means trust funds will have to declare their beneficial owners are in order to be allowed. The central bank of Russia introduced similar rules several years ago, refusing to grant licenses to banks where the beneficiary owner is not identified. Likewise last year the government introduced a new rule that state-owned companies could not hire subcontractors unless the beneficiary owners of the subcontractor was identified. State-owned companies ended up cancelling between 40% and 60% of their contracts as a result. Vedomosti reported that the plan is supposed to be submitted for Parliamentary approval by December this year. The draft law will create a mechanism for gathering information about domestic companies and a ban on doing state business unless the beneficial owners are declared.

Politics – the bad Putin celebrates being Presidents for 10 years On May 6 Russian President Vladimir Putin celebrated the 10th anniversary of his presidency and the second anniversary of his third term in office.

Putin’s career at the helm of the Russian government kicked off in 2000 when he served as acting President following the surprise resignation of Boris Yeltsin. The same year, Putin was inaugurated as president and four years later he was re-elected for a second term. He temporarily served as prime minister

from 2008 to 2012, before returning to the presidency on May 7, 2012. Although Putin saw the first street protests during his time in office in December 2011 and the birth of a real liberal grassroots opposition following a dodgy parliamentary election, more recently his rating has soared to all time highs on the back of the annexation of Crimea and the surgeon national pride. In theory putting can serve until 2018 and then has another six years after that two 2024. There are rumours in Moscow that he may step down at the end of this term, however bne believes that's just wishful thinking. Putin's entire reform program is built around a deadline of 2020 and it is highly unlikely that he will step down before the deadline passes. Russian government and companies spend 2% of GDP on compliance checks Russian government and domestic companies have to spend the equivalent of 1.8% of GDP on compliance assessments, Boris Titov, the country's business ombudsman, said in May complaining about Russia's legendary red tape. According to Titov, country's authorities conduct RUB2.7m compliance assessments annually, and their results do not pay for the investments. Putin tightens curbs on protesters President Vladimir Putin has quietly enacted laws, which continue the Kremlin's tightening of the screws

over the opposition movements in May. Putin signed laws in the middle of May that bring in tougher punishments for people involved in riots and imposing life sentences for various "terrorist" crimes that have been used by the authorities against political opponents and demonstrators. He also approved tighter controls on bloggers, some of whom have emerged as opposition leaders and have used the Internet to criticize Putin and arrange protests. Moscow denies gay pride parade for ninth time in a row Gay pride activists had their application to hold the gay pride march in 2014 in Moscow denied by the authorities again – for the ninth year in a row. Well-known LGBT activist and parade organizer Nikolai Alexeyev submitted the application for an event that would've been held on May 31. Article 31 of the Russian Constitution guarantees the right to public meetings. If a court denies an application at the chosen venue is obliged to offer an alternative venue according to the constitution. Most of the opposition protests have applied to demonstrate in the centre of the city, but courts routinely refused, offering instead venues on the edge of the capital. However in the case of the gay pride movement no alternatives have ever been offered, which is in contradiction to the Constitution.

Politics – the ugly Fraud probe launched against leading Russian journalist Legendary Russian journalist Aleksei Venediktov, the former editor-in-chief of liberal minded Ekho Moskvy radio station, has been named in a multi-million dollar media deal embezzlement investigation.

Police are investigating a $20m deal where state-owned Sberbank bankrolled the creation of a new web portal called PublicPost in 2011. The now-defunct venture was a partnership between Venediktov, Sberbank, and the state-owned Interfax news agency. The investigation was requested by Oleg Mitvol, the leader of the Green Alliance-People's Party, former chairman of newspaper Novaya Izvesitya and one time head of the State agency responsible for the environment.

Mitvol became notorious in the last decade for very publicly announcing investigations into the licenses of various large Russian natural resource producers, threatening to call their licenses on environmental grounds. Almost none of these cases came to court and none of the producers lost their licenses. Some businessman speculated that the stock market reaction to these announcements was the real motivation. PublicPost, which offered a mix of original reporting and user-submitted posts, abruptly shut down in July 2013. Rosneft President Sechin sues media over excessive salary claims President of state-owned oil major Rosneft and close personal friend of Putin Igor Sechin filed a lawsuit in May against the Russian version of Forbes and Komsomolskaya Pradva, demanding a retraction of an article that claims he is the highest-paid manager in Russia. Magazine estimated Sechin's income at $50m in 2012. Earlier this year bne reported that Sechin bought just over $25m worth of Rosneft's shares, which raised eyebrows at the time. The rather red faced company issued a statement later claiming that Sechin had used his "bonus" to buy the stares. Confusingly Sechin

himself told the press he had borrowed the money from Gazprombank. Russian State Project Helped Fund 'Putin's Palace' A luxury villa on the black sea, allegedly builds for Putin, was partly funded by taxpayers money, by diverting cash from a $1bn hospital project, Reuters said in an investigation. While the existence of the property is well known, this trail of funding has not been revealed before. Two allies of the Russian leader profited from state contracts worth about $200m, according to customs documents and banking transactions examined by Reuters. Nikolai Shamalov and Dmitry Gorelov owned a company that supplied medical equipment to a federal hospital project — initiated by Putin — at prices some medical specialists say were inflated. Sergei Kolesnikov, a former business colleague of Shamalov and Gorelov, said in 2010 the estate was built on behalf of Putin. The Kremlin has denied that Putin has any connection to the property. Arrest order upheld against former Deputy Agriculture Minister The Moscow City Court has upheld the decision to arrest former Deputy Agriculture Minister Alexei Bazhanov in absentia who is charged with having embezzled a RUB1.15bn ($33m) loan issued by

the Russian Agricultural Bank to the Masloproduct group of companies, which produce vegetable oil. The group was established by Bazhanov and controls about 6% of the Russian sunflower oil market. Ex-senator detained in Moscow on suspicion of $50m embezzlement Businessman Alexander Sabadash, a former member of the Russian parliament’s Federation Council, has been detained in Moscow for the alleged embezzlement of nearly RUB2bn ($50m) in the form of VAT refund, Kommersant reported. Military prosecutors uphold amnesty for Russia’s ex-defence minister The Main Military Prosecutor Office has upheld the decision to pardon former Russian defence minister Anatoly Serdyukov, Kommersant newspaper reported. According to the newspaper, a committee of experts found Serdyukov’s release justified. Former Russian defence minister Anatoly Serdyukov was pardoned earlier this year, but the information was deliberately kept secret under the terms of an agreement reached between the minister’s attorneys and the investigators. According to Padva, the agreement was reached in an effort to avoid “agitating the public.”

Polls, mood, sociology Russia's consumer confidence index dropped drastically in May Economic growth for the last two years has been driven by strong consumer demand on the back of ever increasing wages. However now that wage rises are beginning to slow confidence is evaporating. The Russian State Statistical Service Rosstat reported the confidence had fallen by a whole% age point in May to 3%. The index was growing mainly in response to the improved expectations of demand and sales. However, findings of opinion polls conducted by Rosstat among 5,500 industrial companies and by the Institute of Economic Policy (IEP) among 1,700 companies point to a marked difference in the estimates of inventory stocks and employment in May. Large industrial companies are typically more confident of the future, particularly in iron and steel manufacturers. Putin, Medvedev popularity hits all-time highs A total of 83% of Russian citizens approve of the activities of Vladimir Putin as president in May, Levada Center sociologists found at the end of May, up from 72% in early March and 65% in April.

A separate poll from the all Russia Public Opinion Research Centre (VTsIOM) put the number even higher at 85.9% in early May. The share of Russians discontent with Putin's work dropped 50% in January-May, sociologists said citing a poll held on May 23-26 among 1,600 respondents over 18 years old in 130 cities, towns and villages in 45 Russian regions. According to the poll, if the presidential election was held today, Putin would easily win at least 70% of the vote, while United Russia — the ruling party that not long ago seemed to have exhausted its popularity — could count on 60%, four times more than its closest rival, the Communist Party. The new State Duma would include only one more party in addition to those two, the Liberal Democratic Party, and United Russia would once again secure a constitutional majority — this time without any need to falsify election results. Meanwhile, 65% of respondents (48% in January and 60% in April) approve of the activities of Russian Prime Minister Dmitry Medvedev and 34% (51%, 38% respectively) disapprove, Levada Center said. Currently 60% of respondents (against 43% in January) say that things in the country are going in the right direction, while 23%

(41% in January) have the opposite stance. At the same time, polls show that the level of support of the United Russia party grew considerably in the past months - from 41.7% in January to 60.4% in early May. Thus, the rating of the ruling party, which was 46.5% on average in the past two years and six months, has reached a six-year maximum (2008-2014), sociologists said. Russians pour spare cash into real estate to protect it In times of crisis – and Russians are very familiar with crises – the population has a sure fire strategy to protect their savings: buy something expensive that is easy to sell. In the 1990s and the years of hyperinflation the favourite item was a washing machine. Washing machines was still not widespread but highly desirable. When the ruble finally stopped plummeting it was easy to sell the washing machine and get your money back – hopefully in dollars, but if the currency was stable enough then the ruble would do. After the ruble lost nearly 10% of its value in the first quarter of this year Russians have been adopting the same strategy – but with some changes. The sale of premium cars has soared in the last months and the volume of transactions on the secondary housing market has spiked. Obviously in the last decade Russians are a lot better off than they used to be.

Slightly more than half of all Russians think that real estate is the most reliable form of investment, according to a recent survey conducted by the polling center VTsIOM. A third of those surveyed, however, also considered opening accounts with state-owned Sberbank to be a useful way of investing money, marking an increase from the last time the question was asked in the fourth quarter of 2013, when only 25% of Russians chose this option. Asked to name their three favourite investments to protect a household's wealth, about 20% identified gold or jewels as the most reliable form of investment; 16% said rubles were a good option for saving; while 11% said that they preferred to keep their cash offshore in foreign banks. As a whole respondents were uninterested in investment strategies common in the West. Only 4% of respondents were interested in pensions and 3% interested in mutual funds. About 7% of respondents said that opening commercial bank accounts made for a good investment, while a mere 6% would opt for purchasing shares in companies. Less Russians fear growing old The number of Russians who regard old age positively has grown over the past 10 years, a poll released in May shows.

This is an important change. Since the fall of the Soviet union in 1991 people's personal horizons have been stretching out into the future. In the 90s the horizon didn't stretch more than a few months distance. However now the personal horizon is reaching almost towards the end of the average Russian life. Only a few years ago another poll found that 80% of Russians intended to remain in their jobs until they dropped down dead. The concept of retirement and pensions simply did not exist, or at least the people had no confidence in the State's ability to take care of them in their old age. This poll, conducted by the Public Opinion Foundation, showed 45% of respondents said they believed there were distinct advantages to old age, compared to 20% a decade ago. A large majority, 64%, said they were not afraid of aging and the share of Russians who do not see any benefits to old age has shrunk from 70% in 2005 to 40%. Of those questioned, a majority of respondents, 56%, said they were not concerned with taking steps to prepare for old age — such as saving money, looking after their health and improving their living conditions — compared to 15% who said they were. Only 52% of Russians identify with any political party Only 52% of Russians think their interests are adequately represented by one of Russia's existing political parties, according

to a survey conducted by state pollster VTsIOM. That said, the ruling United Russia party has been hit with a surge of support recently, the same poll found. 80% of respondents remained optimistic that a suitable party could be formed in the next year, while another 27% rejected the possibility. Still respondents were hard-pressed to name specific alternatives to the present mix of party platforms. Opposition leader Navalny's popularity in the polls is falling Once the rising star of the opposition movement and de facto opposition presidential candidate, Alexei Navalny's star has begun to fade following Putin's highly popular invasion and annexation of Crimea. Navalny's ratings fell to 34% in April, down from 20% in October. Russians Prefer Direct Mayoral Elections, Poll Says Russians want to vote in their mayors, a poll from the Levada Centre found, just as the Kremlin it thinking about nixing the gubernatorial: 77% voiced support for the continuation of direct mayoral elections in Russia's cities in the poll. Russians satisfied with quality of life Russians have become more satisfied with their quality of life, while their desire to protest has

decreased, according to polls by the Levada Center and the All-Russian Public Opinion Research Center (VTsIOM) in May. In April 46% of Russians said they were generally satisfied with their quality of life, compared to 43% of respondents in March and 40% in February, according to VTsIOM. About 11% of the respondents were "mostly not satisfied" with their life conditions in April, 12% in March and 14% in February. Only 2% of Russian were "absolutely not satisfied" with their lives, and 39% were "somewhat satisfied, somewhat not," VTsIOM reported. Those most satisfied with their quality of life were respondents aged 18-24 (57%) and respondents with above-average incomes (56%). The numbers are a bit lower among the elderly (40%) and people with low incomes (38%). The opinion poll was conducted by VTsIOM April 26-27 among 1,600 people across Russia. The statistical error was 3.4% . According to the poll by Levada Center, the protest activity of Russians is decreasing. In April, 74% of Russians said that mass demonstrations in their locality are unlikely versus 66% in February. If mass demonstrations were still held, 80% of the respondents said they would not participate in them (versus 39% in February). Public's desire to protest hits record low Russians desire to participate in political protests hit an all time low

in April, the Levada Center found in a poll. A record high 85% of Russians would likely not take part in political protests, if they were called, the poll found and 95% of Russians had not participated in protests in the past year. The same poll conducted in late April after President Vladimir Putin’s approval rating soared to 82% showed that 79% of Russians think political protests were “unlikely” to take place in their community. This figure, which carries a 3.4% margin of error, has increased by 34% since 1999. Russia is worst place for foreign investment Of foreign companies poll on the attractiveness of Russia as an investment destination, nearly 56% of respondents said that Russia was a poor place to invest, mostly due to the conflict in Ukraine, according to foreign investors polled by Bloomberg in their quarterly Global Market Investor's Poll. This is the second worse result for a negative attitude to a particular market in the whole history of the poll, which has been held since 2009 and relies on the attitudes of worlds's financial elite — traders, bank officials and asset managers. About 45% of the respondents think that now it is the best time to sell Russian assets due to tensions with Ukraine and the financial sanctions EU and the have imposed on Russia. Moreover, 75%

expressed pessimism about the way President Vladimir Putin's policies will affect the investment climate. The Association of European Businesses (AEB) found that European companies feel less optimistic about doing business in Russia due to the slowdown of economic growth in the country and the unrest in Ukraine. The integrated AEB-GfK Index this year dropped to 115 points out of 200, a 29 point decrease on 2013, the AEB said in a statement. The shift signals a sharp decline in the optimism of top level managers in their Russian operations "regarding both the macroeconomic development of the country and the growth of their own business," the statement said. Moscow, St. Petersburg Near Bottom in Regional Investment Rating Kaluga region has been rated Russia's best region for investment out of 21 regions evaluated by Kremlin-aligned think tank Agency for Strategic Initiatives, while the country's economic centers, Moscow and St. Petersburg, trailed at number 17 and 20 respectively. The pilot study, published on the agency's website, gauged the investment climate in 21 of the Russia's 83 federal districts, issuing ratings according to four sets of criteria — regulatory

environment, institutions for business, infrastructure, and support for small and medium businesses — on a scale of 1 to 5. These ratings were then averaged out and regions were then assigned tiers from I to V, with V being the lowest on the scale. Kaluga — a special economic zone that has a long-standing reputation for being friendly for investment — was the only region surveyed to score top marks in all four categories. Meanwhile, Moscow and St. Petersburg trailed the pack. Moscow, designated a tier IV region, placed 17 on the overall rankings. St. Petersburg — Peter the Great's "window to the West" — fared even worse and was designated a tier V region, placing 20 overall, besting only Primorye region on the Pacific coast. Only 8% of top-managers of international companies think that the business environment in Russia is favourable Amid the crisis in Ukraine, top-managers became more concerned over political risks, according to a survey "Global Business Barometer" conducted by FT and The Economist. 41% of respondents feel the most serious concerns over the political factor versus 35.5% in the fourth quarter of 2013 and 30.2% a year ago The key risks mentioned by the top-managers are economic and market risks (50.5%), which had been decreasing almost unceasingly over the past three

years (69.9% in 2Q 2011). The political risk is of the greatest concern to top-managers in

Eastern Europe (58%): the reason is the situation in Ukraine and sanctions against Russia.

Third of European companies will increase Russian investment, half to keep on same level Just under a third of European companies (30%) intend to step up investment in Russia in 2014 and half (50%) will not change their investment policies: they will keep investment at the former level and proceed with the projects which

have already been launched, according to a survey "Strategies and Prospects of European Companies in Russia" conducted by the Association of European Business (AEB) together with GfK-Rus. About 60% of companies dealing with projects in Russia increased their turnover last year. 10% of companies saw their turnover

falling in 2013. 52% of companies operating both in Moscow and in regions think that the economic environment in Russia is worse than they expected. 6% of companies said that the situation is better than they expected. 69% of respondents think that Russia's economy will grow steadily in 6-10 years. 94% of Russians Depend on State TV for Ukraine Coverage A huge majority of Russians rely on the state-owned TV stations as their main source of news, the Levada Center found in a poll in May: 94% of the population relies on domestic television networks to follow developments in Ukraine and Crimea. State-owned networks account for the first five of Russia's six leading TV stations. The exception is CTC TV, Russia's sixth largest TV station, a pure entertainment channel and carries no news whatsoever. The Levada Center found that 44% of respondents think foreign media outlets are "not very objective" about the situation in Ukraine, while 50% consider Russia's state media outlets to be "generally objective." According to Levada center 58% of Russians believe Russia has the right to annex territories if "Russians are being threatened" and 59% of Russians believe Russia should provide weapons to pro-Russian forces in southeast Ukraine.

Enthusiasm for ties with the west of fading in Russia In 2013, over 70% Russians wanted closer ties with West; now it's 41%. While 39% want to distance themselves from West, according to a poll from the Levada Centre. Polls show that the mutual mistrust of Americans and Russians is

growing and alarming over the last 15 years. However the trends took off as could be expected at the end of last year.

Russians are world's 2nd highest spenders on alcohol Russian consumers ranked second only to Estonians in terms of the amount of money they spent on alcoholic beverages last year, Euromonitor International said in a report in May. Estonian consumers spent 6.5% of their cash on beer, wine or

spirits in 2013. Russians spent 5.8%, or $61.5m, on alcohol. Vodka has long been losing ground to beer and wine; beer accounted for $27.5m of Russian spending, whereas $21.9mm was spent on spirits and $12m on wine, Lenta.ru reported.

Russians are increasingly nostalgic for the Soviet era Russians are becoming increasingly nostalgic for the certainties of the Soviet era, a poll by the Pew Research Centre found. When asked: "is it a great misfortune of the Soviet union no longer exists?" some 27% of respondents agree completely and another 28% of respondents mostly agree. That's more than half of Russians who think the Soviet Union was a good thing. Russians are uncomfortable with the annexation of Crimea but earn for a return of the Soviet Union. Most Russians (58%) are concerned enough about discrimination against their fellow Russians to want their government to take action, but not enough to advocate forcible annexation (only 15% were in favour). Regarding Ukraine, 66% believe Russian language rights are restricted, and that there is also psychological discrimination (38%) and crude physical pressure (32%) against Russians and Russian-speakers in Ukraine. A significant number of Russians do not seem willing to translate these concerns into military actions; 41% say “economic sanctions” should be put in place. Only 43% are prepared to vote for a Customs Union of Ukraine, Belarus and Kazakhstan now. Russians polled ranked the countries where they had the most concerns about the rights of

Russians and Russian speakers as follows: Ukraine 62% Latvia 53% Lithuania 48% Estonia 46% Georgia 25% Kazakhstan 12% Moldova 12% Azerbaijan 11% Tajikistan 11% Uzbekistan 10%

Banks and Finance Russian Banking sector profitability falls further behind asset growth Another month of relatively strong lending growth. Corporate loans (including sub-federal loans) continued to grow in the Russian banking sector in April, expanding 1.7% month-on-month and 19.2% year-on-year, or 15.4% year-on-year net of ruble depreciation (both figures are slightly lower than in March). Retail lending growth of 1.8% was strongest month-on-month this year, but it slowed to 24.6% year-on-year from 26.3% in March. Overdue loans grew even faster, resulting in the corporate NPL ratio

adding 8 bps month-on-month to 4.15% and the retail ratio increasing 16 bps. Retail deposits also rose the fastest month-on-month this year (up 1.7%), but year-on-year expansion decelerated to 10.8% from 12.4% in March; thus, the sector is still down 0.6% YtD. Corporate deposits remained practically flat month-on-month and year-on-year growth slowed to 20%. ROAE increasingly unimpressive ... The sector earned RUB292bn ($8.3bn) in 4M14 and RUB58.2bn ($1.6bn) in April, reflecting contraction of 10% year-on-year and 8% month-on-month.

BRICS emerging nations to launching bank for 2016 The five BRICS nations will likely agree to fund their $100bn development bank equally, giving them the same rights in a new multilateral bank that could start lending in two years, following a meeting of the foudners in May. Capitalization of the bank was one of the main sticking points in the sometimes tortuous negotiations among the emerging powers to create a joint lender to finance infrastructure projects in developing nations. Every seventh Russian retail loan is in arrears (NPLs) Every seventh retail loan granted in Russia falls in arrears, an average amount owed is RUB59,600 ($1702), United Credit Bureau (UCB) reports. The growth of retail lending has fallen to the record low over the past four years, Collection Agency Sequoia Credit Consolidation says in a survey. The market has increased 3.5% since January 1, 2014 versus 8.4% over the same period in 2013 and 10% over the same period in 2012. Loan arrears keep rising at a record pace - they reached RUB514.8bn as of May 1, up by 17% since beginning of this year UCB keeps information about 53.6m borrowers of which 36.3m have outstanding loans. One borrower in Russia accounts for 1.7 loans on average, according to

UCB's data. According to UCB today 9% of applicants have more than four outstanding loans. And that number has increased nearly three times since 2012. There is also a marked increase in the number of customers who have a credit history with four banks and more. The number of customers with loans from four banks was 8% as of the end of 2012 and increased to 12.5% in the first quarter of 2014: only 3% of customers had a credit history with five banks in 2012 and 6.5% in the first quarter of 2014. The number of customers with over 6 loans rose from 1.7% to 5.5%. The reason for using multiple banks is that the banks are becoming increasingly aggressive in winning new business and so it has become simpler to take loans from any bank. The highest level of debt burden on the population and competition among banks is seen in the segment of loans limited to RUB50,000. Such loans account for 62% of all loans granted." The analysis made by UCB shows that an average amount of a loan granted by a bank is RUB165,100 (auto and mortgage loans included). And average auto loan is RUB535,400, and an average mortgage loan is RUB1.4m. The average approved limit on credit cards is RUB55,400. However following an increase in

prudential regulations by the central bank of Russia the average loans size has been falling since the beginning of this year: the amount was RUB170,800 in January, RUB167,900 in February, RUB169,200 in March and, according to the most recent figures, decreased to RUB165,100. Loan arrears increased 14% in the first four months of 2013 and 4.3% in the same period of 2012. According to the Bank of Russia, arrears of retail loans were 4.9% as of April 1, 2014 (their share in the total loan portfolio is lower - 3.6%). Thus, the proportion of bad debts has come close to the level which is considered critical (5%). Collectors explain the deterioration of the loan portfolio by the fall in individuals' income, a high debt burden, and macroeconomic changes, including rising inflation and a high level of unemployment, Sequoia Credit Consolidation says. Defaults on bank loans in Russia reached a record high level,

according to the Central Bank of Russia: loan arrears increased nearly 1% in March to reach 13.5%. The rising risks of lending have meant that many small and medium-size banks to quit the fast loan market on a large scale, after making most of their profits from these types of loans in the last couple of years. The situation today is very similar to that in the 2009-2010 crisis say bankers. Retailers continue to cause the most problems and had lead leading retail lender Russian Standard Bank to cut the staff by 10% and close part of the offices. Russian Standard Bank refused to disclose precise figures. However, they have already suspended granting cash loans. Such loans are now available only to "proven" customers. Others may only have access to a credit card overdraft. Home Credit Bank intends to close about 200 offices (8% of the network).

Ranking of Banks by Overdue Retail Loans (for the period January-April 2014) Bank Arrears, % Sberbank of Russia +15.52 VTB24 +17.34 Russian Standard +26.55 Home Credit Bank -1.87 Alfa-Bank +15.18 OTP Bank +3.01 Rosbank +5.34 Renaissance Credit +2.55 NB Trust +23.67 Bank of Moscow +13.46 Source: Bankir

NPLs Russia are rising but not as much as in other countries

Japan's payment system JCB to enter Russia Japan's payment system JCB is about to enter the Russian market. Alfa-Bank may act as a settlement bank. Experts think that the Japanese system has few chances to gain a significant share on the Russian market after Visa and MasterCard decided to continue their business in Russia The potential target audience of JCB cards will be individuals who often travel to China, Japan and South Korea where Visa and MasterCard are not represented well.

To enter the Russian market and formalize Alfa-Bank's status as a settlement bank, JCB needs to obtain an authorization from the Bank of Russia to work in Russia as a payment system. The Japanese bank is expected to file these documents soon. The payment system is also interesting as it offers an alternative to the western backed Visa and MasterCard systems. On May 5 Putin signed a law to create a Russian payment system as a third option. The point is to try and create a payment system that avoids dollar base systems and so is not vulnerable to sanctions.

VTB results were hammered in the first quarter, state to boost state bank capital State-owned banking giant VTB was symptomatic of the problems in the banking sector after its results got one at in the first quarter of this year. The first quarter net profit under I FRS was onlyRUB400m, 39-times last year, RUB15.7bn. Much of the pain was inflicted by its Ukrainian operations. Net interest income increased 21.8% year on year to RUB89.9bn. Net fee and commission income increased 24.3% to RUB14.3bn. The lender's assets amounted to RUB9,402.3bn as of March 31, 2014, up by 7.2% during the quarter. The increase is driven by the growth of the loan portfolio, the growth of investment in debt instruments of Russian corporations, the increase in cash and short-term assets amid the decline in liquidity on the Russian market. However a combination of the economic slowdown, capital flight and general nervousness hurt the bottom line. Putin said the St Petersburg conference that he thought the major Russian banks were all need of recapitalisation after that the squeezing they have suffering for the last couple of years. The government intends to increase the capitalization of banks by converting subordinated loans into Tier-1 capital, Putin said. He

hopes that it will allow banks to step up lending to the economy and make credits cheaper. The debt could be converted into pref shares in order to avoid shareholder dilution. The conversion could add 2.6ppt to VTB’s Tier 1, increasing it to 13.5% at YE13; while Sberbank could add 1.6ppt to 12.3% at YE13. A decision on each bank will be taken individually. Another measure discussed to recapitalize banks was reducing the dividend policy to less than 25% of RAS. Sberbank and VTB each currently pay up to 20% of IFRS income to shareholders, in compliance with their respective dividend policies. Corporate loans were up by 18% year-on-year in April A good result for Russian banks in the first quarter of this year: corporate lending has started to rise again, up 18% year-on-year and well ahead fo the slow rise in retail loans. The outstripping growth of corporate loans is a non-typical trend for Russia. However, the corporate loan portfolio was growing faster than the retail one (5.2% versus 2.8%) in the first quarter of 2014 and in March in particular. In December 2013, loans to nonfinancial organizations decreased 0.7%, but loans to private customers added 1.9%. Early this year, the Bank of Russia forecasted that corporate loans would increase more than 10% and retail loans less than 25% in 2014.

If the forecast comes true, the growth of corporate lending will be the record low since the crisis times. In 2009, corporate loans increased 0.3% and retail loans decreased 11%. In 2013, the corporate loan portfolio increased 12.7%, same as in 2012. Annual rates of loan growth have stabilized at last year's level having demonstrated the best

performance over last two years. Demand for banking loans could have proved that companies are improving their investment programs if banking deposits of non-financial organizations in April did not grow by 20%. For a month volume of corporate credits rose by RUB323bn, their deposits - by RUB511bn amid comparable reduction of funds on corresponding accounts.

Government subordinated lending up as government props up sector The government spent about RUB900bn on subordinated loans to banks: Sberbank received RUB500bn from the Bank of Russia until the year 2018 (RUB200bn was repaid ahead of schedule), RUB404bn was granted by VEB to 17 other banks at 6.5% annual. The largest recipients were VTB Bank (RUB200bn), Russian Agricultural Bank (RUB25bn), Gazprombank (RUB90bn), and Alfa-Bank (RUB40bn).

It will be decided this year whether these loans remain in their current form or assume another legal form. Conversion into preferred shares is not the only option, and making subordinated loans equal to perpetual ones is being considered. However, the latter demands changes in the legislation and approvals from the Basel Committee. The mending is aimed at solving to problems that the banking sector is facing: providing liquidity and increasing capital.

The Ministry for Economic Development offers three main forms of support to banks: easing requirements in respect of dividends for state banks which would allow them to transfer more profit to capital, conversion of subordinated loans granted over the period 2008-2009 into bank capital, and contributing federal loan bonds to bank capital in exchange for preferred shares. The issue of such bonds at RUB200-300bn. Visa, MasterCard ready to continue operations in Russia After nearly being forced out of Russia following their refusal to service Russian banks on the US and European sanctions list, Visa and MasterCard struck a deal with the Kremlin to allow them to stay in Russia and maintain their $3bn-plus businesses. The first of the Prime Minister Igor Siluanov said that Visa and MasterCard had decided to establish an operator in Russia before the end of 2015. Siluanov said that the government will continue on this project to build a Russian payment system and the international ones will have to find a middle ground where they can co-exist. Russian affiliates of Visa and MasterCard will be integrated into the Russian national payment system, which will be created on the basis of the central bank's clearing house, Siluanov said.

Siluanov also said that Visa and MasterCard want to create "two separate subsidiaries" in Russia to operate with the national system, rather than a joint one. The trick is that both Visa and MasterCard will set up a Russian entities. The Kremlin had threatened to force foreign entities to pay massive deposits to guarantee their payments, equivalent to the entire year's turnover. Share of dollars in domestic retail deposits soars Russians have lost their newly-found faith in the domestic currency and have been swapping their rubles for dollars at an increasing pace, on the back of the sinking value of the national currency. The proportion of individuals' deposits in foreign currency increased from 17.4% to 20.3% in 1Q 2014 to RUB3.4 trillion, the Deposit Insurance Agency reports. The trend is driven by the depreciation of the ruble and expectations of further devaluation. In March and April, many depositors were withdrawing their ruble-denominated deposits in panic and buying dollars and euro at the peak of their value. Now when the ruble is recovering its positions, the ruble value of foreign currency savings is falling.

Russian government sends financial ombudsman bill to Duma The Russian government has sent a bill to create the institution of a financial ombudsman for financial organizations' consumers to the State Duma lower house on May 10. The ombudsman will consult a client before he goes to court if a bank illegally raises interest rates or demands an early debt repayment, or if an insurance company refuses to pay without serious reasons. The ombudsman may consider arguments between individuals and micro financial organizations, pawnshops, and professional securities traders. Russian state sets up a RUB50 SME loan guarantee agency As part of the Russian state's on-going efforts to boost small and medium-sized enterprises in Russia the government has announced it will launch is SME loan guarantee agency funded with RUB50bn. The agency will provide loan guarantees for smaller enterprises trying to setup. Small and medium size companies are typically penalised when going to banks and charged higher interest rates. The government estimates that SMEs need between RUB490bn and RUB900bn, reports Prime. The agency will provide at least RUB439.9bn of guarantees for RUB824.9-879.9bn of loans in 2014-2020.

Russian banks to help exporters bill contracts in rubles Putin’s order to bill export contracts in rubles is likely to be implemented formally. Russian banks may play the role of intermediaries that receive forex payments from international companies and convert the receipts into rubles in order to show clearly that export revenues are paid in rubles. Alfa Banks sees this news as negative. Should this initiative be implemented, it may reduce forex market liquidity, as companies, instead of operating through the market directly, may be restricted to converting export revenues through those banks where they hold accounts. Thus, the idea of billing contracts in rubles could likely end up causing additional economic costs by reducing forex market flexibility.

Economics Crisis in Ukraine cripples Russia's foreign trade… Russia's trade flows have been depressed by the Ukrainian crisis. This is hardly shocking. But the magnitude of this harm, however, is surprising. Rosstat showed that Russia suffered an 11.4% decline in foreign trade comparison to March 2013 (to be precise, exports shrank by 12.7% and imports declined by 9.4%). Now a more than 10% decline in foreign trade, on its own, a pretty big deal. Trade flows are variable,

but not to such a dramatic extent. But while the decline is noteworthy on its own, when you compare it to the trajectory that Russia was on it become even more stark and glaring. In the span of just a few months, Russia went from experiencing extremely rapid growth in foreign trade to suffering an absolute decline. That is just one data point among dozens showing that what's happening in Ukraine is a major break with past experience and that Russia, in many ways, is currently in uncharted economic waters.

… but Russia's trade balance improves dramatically The fall in the value of the ruble has made imports more expensive

and Russians have turned to but domestic product instead, which has been a major contribution to a $19.7 billion trade surplus in March. However it was the

unexpectedly strong export of oil products that was the biggest contribution to the number. The first-quarter contraction in the value of imports of 7% year-on-year reflects Russia’s current economic slowdown and the ruble’s slide. The value of goods imports from CIS countries dropped 20% in the first quarter while the volume of these imports fell as much as over 40% in January-February only. CIS countries, however, accounted for just over 10% of Russian imports. EU countries supplied over 40% of imports and Asian countries nearly 30%. Foodstuffs were the only major import category to show growth in value terms in the first quarter. The value of imports in other major categories, i.e. machinery & equipment and chemical products declined sharply. The value of goods exports contracted 2% year-on-year in the first quarter. The export prices of nearly all Russia’s major export commodities (crude oil, petroleum products, natural gas and metals) were slightly lower than a year earlier. Export volumes of crude oil and aluminium contracted sharply. Export volumes of natural gas and raw timber increased. Over half of Russian goods exports go to the

EU. Asia’s share is just under 20% and CIS countries’ a bit over 10%. The value of exports was nearly double that of imports, driving the goods trade surplus to over $50bn in the first quarter. Russia’s services trade increased slightly in January-March from a year earlier. Services represent nearly 30% of total imports and just over 10% of total exports. Russia’s services trade deficit was $10bn. The EU accounts for over 40% of Russia’s trade in services. Turkey is Russia’s largest single services trade partner. Analysts speculate that this setup is becoming a major trend that will persist in the near term. That's good news for the budget, which was facing a deficit due to the economic slowdown. Now analysts are speculating that the government will end the year flats or even run a slight surplus. As for April, faster and broad based drop in imports with even food imports started to decline (on imposed ban on EU meat imports) alongside with a spike in gas exports (according to MinEnergy, +17.4% year-on-year; partly owing to beneficial base effect), despite normalized exports of oil products, might have supported external trade surplus near elevated levels.

Russia's regions threaten to become an Achilles' heel Russia's economy is slowing dramatically, but the pain is not evenly spread. While a few Russian regions are making rapid progress and modernising, the bulk are getting into deep financial trouble. Between 2010 and 2014 regional indebtedness more than doubled from $35bn to $78bn, according to the rating agency Standard & Poor's. And the size of this debt is now beginning to threaten the health of the Russian economy.

If Russia was brought low during the 2008 crisis by over-borrowing amongst a few key large companies, the next crisis looks increasingly like it will be caused by the collapse of a regional debt bubble: the collective level of debt owed by Russia's far-flung regions has risen from just until 4% of GDP in 2010 to just under 8% now, and will top 10% next year according to estimates – a far faster growth rate than the federal government's borrowing growth. Russia's total sovereign debt is currently about $300bn, or 14% of GDP.

The consolidated deficit of Russian regions' budgets will stand at RUB700-RUB800bn in 2014-2015, Deputy Economic Development Minister Andrei Klepach said in May. After 2015, the regional budgets' deficit will decrease but it

will still be higher than the federal budget deficit, he said. Under the budget plan for 2014-2016, the federal budget deficit will stand at 0.5% of the GDP in 2014, 1% in 2015 and 0.6% in 2016.

The economic performance of Russia's 83 regions is very mixed. Only about a dozen regions are actually net contributors to the federal budget. The rest live day-to-day on handouts from the central government. The combination of a slowing economy exacerbated by the political turmoil in Ukraine has caused debt levels to rise alarmingly in a few regions and some are now starting to look default in the eye. Putin has set regional governments ambitious development goals – laid

out in the so-called May decrees in 2012 – but most are struggling to meet them. Local governments have been hoping the targets will be reduced, the deadlines extended or the central government will come up with more cash. "So far, it does not look like these hopes will materialize," says Uralsib. And raising money is going to be hard. Each region has to get federal approval to issue bonds, because regional bonds create more market competition for the federal and business bonds. Most

of the banking loans to the regions carry high interest rates and are short term (mostly between two and five years). The federal loans come with much lower rates and longer repayment schedules (mostly between five and 20 years), so naturally federal credits and loans are more attractive for the local governments, though unprofitable for the federal government. The City of Moscow is by far the biggest Russian user of international bond markets. It raised approximately $4.8bn in 2013, but has only issued $2.4bn this year due to restrictions on its own budget. The bottom line is that Russia's regions are becoming yet another mouth to feed from the slowly dwindling pot of hard currency reserves. Russian retail trade growth slowed to 2.6% year-on-year in April Nominal wages continue to increase however real disposable incomes in Russia contracted by 6.8% year-on-year in March after growing slightly in February.

However the March number seems to be an aberration because in April real disposable incomes were up again. That said everybody agrees that consumption is slowing, the main economic driver of the Russian economy at the moment. This is starting to be reflected in the retail trade, which slowed somewhat in April. Another drag on consumption is the right growing level of debt amongst Russian consumers. The central bank moved last year to cool lending to consumers and banks have responded by making it more difficult to get a loan. At the same time those who are still borrowing are using the fresh money to refinance old loans. Consumer credit borrowing is not showing up in the retail numbers any more. Retail trade growth was 2.6% year-on-year only versus 3.7%-3.8% year-on-year consensus, which is a material slowdown compared to 4% year-on-year growth in the previous two months.

Domestic goods boost Russian April industrial output Russia's industrial output rose by 2.4% in April, nearly triple the expected rate, surprising analysts after signs that Western sanctions imposed over the annexation of Crimea were weighing on the economy. The rise was spurred mainly by production of goods usually targeted at the domestic market, such as foodstuffs and textiles. Output of Russia's main exports, such as oil and gas, was weaker, with oil production rising 1.3% and gas production falling 6.7% , compared to a year ago, data released by the State Statistics Service showed. Overall extraction of natural resources rose 1.1% , however, improving from 0.6% growth in March. Manufacturing output was up 3.9% and utilities down 1.9% . Production of some foods, such as butter, rose by nearly a third, while output of jackets was up by nearly two-thirds Just over third of Russian firms loss-making in January-March Just over a third (37%) of Russian companies were losing money over

the first three months of this year, up 0.2% on the year to 36.7% in January-March, the Federal State Statistic Service said. The net profit of all organizations (except banks, small enterprises, insurance companies and public services firms) amounted to RUB1.274 trillion. Land transport industry (not including railroads) had the biggest share of loss-making companies: 63.3%, the share of companies having a net loss in the power, gas and water production and distribution stood at 49.3%. Pipeline operators had the smallest share of loss-makers - 16.4%; only 24.2% agricultural firms and 25.7% of car repair companies had losses. Investments declined but not as sharply as expected While the market was very skeptical about investment trend expecting a 5.0% y/y decline, in reality investments dropped by only 2.7% y/y which is positive. This figure is in line with acceleration of industrial output growth to 2.4% y/y in April and may suggest favorable effect of Crimea accession on investment growth at least in the short term.