BMO Metals & Mining Conference - March 2021

17

The Australian Gold Miner - For Global Investors BMO Metals & Mining Conference - March 2021

Transcript of BMO Metals & Mining Conference - March 2021

The Australian Gold Miner - For Global Investors

BMO Metals & Mining Conference - March 2021

2

Forward Looking Statements, Reserves and ResourcesForward Looking Statements

Northern Star Resources Limited has prepared this announcement based on information available to it. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this announcement. To the maximum extent permitted by law, none of Northern Star Resources Limited, its directors, employees or agents, advisers, nor any other person accepts any liability, including, without limitation, any liability arising from fault or negligence on the part of any of them or any other person, for any loss arising from the use of this announcement or its contents or otherwise arising in connection with it.

This announcement is not an offer, invitation, solicitation or other recommendation with respect to the subscription for, purchase or sale of any security, and neither this announcement nor anything in it shall form the basis of any contract or commitment whatsoever. This announcement may contain forward looking statements that are subject to risk factors associated with gold exploration, mining and production businesses. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a variety of variables and changes in underlying assumptions which could cause actual results or trends to differ materially, including but not limited to price fluctuations, actual demand, currency fluctuations, drilling and production results, Resource or Reserve estimations, loss of market, industry competition, environmental risks, physical risks, legislative, fiscal and regulatory changes, economic and financial market conditions in various countries and regions, political risks, project delay or advancement, approvals and cost estimates.

ASX Listing Rules Disclosures

The Scheme of Arrangement in relation to the merger of Northern Star and Saracen Mineral Holdings Limited (Saracen) was implemented on 12 February 2021, As a result, both Saracen and Kalgoorlie Consolidated Gold Mines Pty Ltd (KCGM) became wholly owned subsidiaries of Northern Star on 12 February 2021. Until such time as Northern Star reports ore reserves, mineral resources, and production targets of the Northern Star group of companies on a consolidated basis, this announcement contains estimates of Northern Star's and Saracen's respective ore reserves and mineral resources, as well as estimates of KCGM’s ore reserves and mineral resources and also production targets that are a product of these estimates. Northern Star and Saracen collectively own 100% of the assets and operations of KCGM (including the Super Pit). The information in this announcement that relates to the ore reserves and mineral resources, and production targets of:

(a) Northern Star has been extracted from the following: the ASX release by Northern Star entitled “Resources and Reserves, Production and Cost Guidance Update (ex-KCGM)” dated 13 August 2020, available at www.nsrltd.com and www.asx.com (Northern Star Announcement);

(b) Saracen has been extracted from the following: the ASX release by Saracen entitled “Carosue Dam and Thunderbox only – Reserves rise to 3.7Moz” dated 4 August 2020, available at www.saracen.com.au and www.asx.com (Saracen Announcement); and

(c) KCGM has been extracted from the following: Northern Star's and Saracen's joint ASX announcement entitled “KCGM Reserves, Resources and Guidance Update” dated 18 August 2020, available at www.nsrltd.com and www.asx.com (KCGM Announcement).

Northern Star confirms that it is not aware of any new information or data that materially affects the information included in the Northern Star Announcement and, in relation to the estimates of Northern Star's ore reserves and mineral resources, that all material assumptions and technical parameters underpinning the estimates in the Northern Star Announcement continue to apply and have not materially changed. Northern Star confirms that the form and context in which the Competent Person's findings are presented have not been materially modified from that announcement.

Saracen confirms that it is not aware of any new information or data that materially affects the information included in the Saracen Announcement and, in relation to the estimates of Saracen's ore reserves and mineral resources, that all material assumptions and technical parameters underpinning the estimates in the Saracen Announcement continue to apply and have not materially changed. Saracen confirms that the form and context in which the Competent Person's findings are presented have not been materially modified from that announcement.

Both Northern Star and Saracen confirm that they are not aware of any new information or data that materially affects the information included in the KCGM Announcement and, in relation to the estimates of KCGM's ore reserves and mineral resources, that all material assumptions and technical parameters underpinning the estimates in the KCGM Announcement continue to apply and have not materially changed. Northern Star and Saracen confirms that the form and context in which the Competent Person's findings are presented have not been materially modified from that announcement.

*All currency conversions in this document were converted at a spot conversion rate of AUD/USD of $0.78.

Authorised to release to the ASX by Raleigh Finlayson, Managing Director.

3

Tier-1 assets in Tier-1 locations

Australia

US(Alaska)

Perth

Yandal

10.2Moz Resource

4.6Moz Reserve

Kalgoorlie

30.5Moz Resource

13.3Moz Reserve

▪ Simple, growth business; Targeting the best

2Mozpa from three Tier-1 production centres

▪ Post-merger integration running ahead of

schedule

▪ On track to achieve FY21 production guidance

1.5-1.7Moz at an AISC A$1,390-A$1,520/oz

(US$1,080-US$1,190/oz)

▪ >10 years mine life underpinned by Reserves

▪ Further growth from aggressive exploration;

FY21 exploration budget A$150M (US$117M)

▪ Robust balance sheet; Net cash A$180M

(US$140M) (31 Dec-20)

▪ Surface stockpiles 3.2Moz (31 Dec-20)

▪ >10 year track record of paying dividends to

Shareholders, targeting 6% of revenue

Pogo

6.7Moz Resource

1.5Moz Reserve

Top 10, ASX-listed global gold miner

4

Progressive ESGOur Sustainability Vision

“Delivering responsible environmental and social business practices that lead to the creation of strong economic returns for our Shareholders, and shared value for our Stakeholders.”

Our Sustainability Framework Ecosystem

Completed Stage Two of our

TCFD Recommendation

adoption

Aligning business actions with

global sustainable

development needs as

defined by the United Nations

Strengthening our ESG

disclosures by adopting the

SASB materiality framework

for CY2020 reporting

Progressive corporate governance

▪ Recent Board decision to transition from an Executive Chair to an Independent Non-Executive Chair; Global search imminent

▪ Positive Shareholder feedback

Health and safety

▪ The health and safety of our workforce is our number one priority; sector leading safety performance; Exited CY20 with a 1.13 LTIFR*

▪ Swift proactive management mitigated COVID-19 impacts over the last ~12 months

Stakeholder ESG engagement

▪ Annual ESG investor roadshow and continuous stakeholder engagement on priority ESG areas

▪ Allows us to progress our sustainability strategy

CY2020 sustainability highlights

▪ Zero significant environmental, heritage or regulator infringements under NST ownership of current portfolio of operating assets

▪ Total water use intensity per ounce reduced by 7%

▪ Scenario analysis completed and target setting action plan created as part of TCFD alignment

* Number of recordable injuries per million hours worked, calculated on 12 month rolling average

5

Pathway to the best 2Moz per annum

▪ 100% in Reserves at 30 June 2020

▪ 30% production growth in next 3 years alone

1,000

1,250

1,500

1,750

2,000

FY20A FY21 FY22 FY23 FY24 FY25 FY26 FY27

+30%

Production profile (koz)

A growth business, with falling costs and margin expansion

▪ A$1.5-2.0B NPV (pre-tax, net of stamp duty) to be unlocked over the next 10 years

▪ Opportunities include:

▪ Optimisation work well advanced to produce the best 2Mozpa from the three production centres

▪ Annual Strategy Day September quarter 2021

Procurement Savings

Corporate & Net Tax savings

Milling Optimisation of Ore

KCGM JV Savings

Operational Efficiency Upside

6

“Through-the-Cycle” gold stockSignificant levers to adjust to changes in gold prices

3.2Moz in surface stockpiles

Attributes

“Future-proofing” strategy flex

Hedging ~15% of production next 3yrs

De-risked production growth,

earnings and cash flow

Merger synergies / optimisation

Robust balance sheet – Net cash

Structurally lower costs

Resilience to gold price cycle /

“black swan” shocks

Higher trading multiples to reflect

consistency

100% Tier-1 assets

THE PREFERRED

“THROUGH-THE-

CYCLE” GOLD

STOCK

Goal

Benefits

7

Kalgoorlie Operations:

Production target 1.1Mozpa

Yandal Operations:

Production target 600kozpa

North American Operations:

Production target 300kozpa

Kalgoorlie

Operations

Carosue

KB

South Kalgoorlie

Fimiston

Kundana

Carbine

Acra

Yandal

Operations

Thunderbox

Bronzewing

Jundee

NST tenure NST mill

Reserves: 287Mt @ 1.4g/t for 13.3Moz

Resources: 516Mt @ 1.8g/t for 30.5Moz

Processing capacity: 18.6Mtpa

Reserves: 66Mt @ 2.2g/t for 4.6Moz

Resources: 139Mt @ 2.3g/t for 10.2Moz

Processing capacity: 5.5Mtpa

Reserves: 5.9Mt @ 8.0g/t for 1.5Moz

Resources: 22Mt @ 9.8g/t for 6.7Moz

Processing capacity: 1.3Mtpa from mid 2021

Nth American

Operations

Pogo

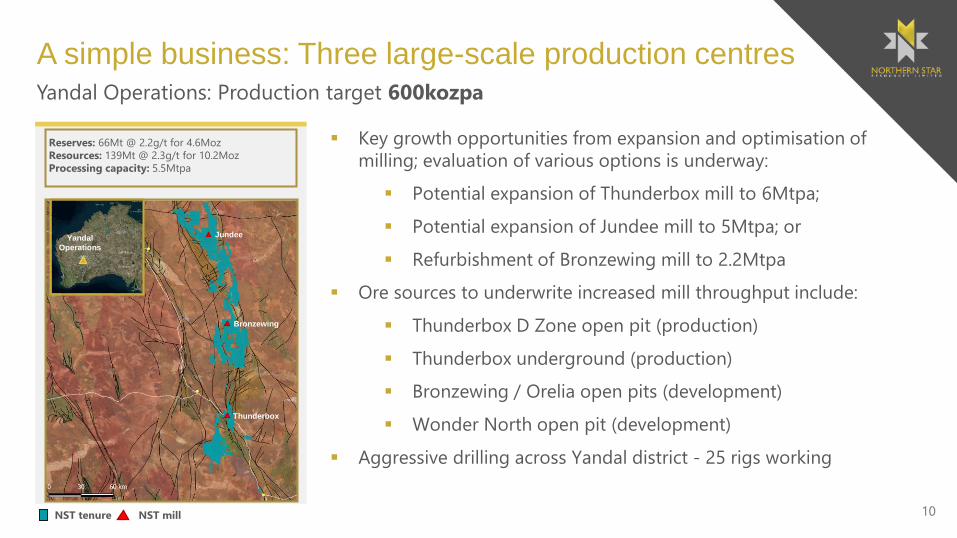

A simple business: Three large-scale production centres

8

0.0

0.5

1.0

1.5

2.0

2.5

0

10

20

30

40

50

60

70

FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30 FY31 FY32 FY33 FY34

Gra

de (

g/t

)

Str

ip R

ati

o (

w:o

)

Strip ratio Grade

Kalgoorlie

Operations

Carosue

KB

South Kalgoorlie

Fimiston

Kundana

Carbine

Acra

Yandal

Operations

Reserves: 287Mt @ 1.4g/t for 13.3Moz

Resources: 516Mt @ 1.8g/t for 30.5Moz

Processing capacity: 18.6Mtpa

Pogo

▪ Before climbing to +675kozpa by FY28

▪ Aggressive drilling across Kalgoorlie District – 28 rigs working

▪ Key growth area at Fimiston (KCGM) - Production rising to +500kozpa by

FY24 as access to high grade Golden Pike North is restored (post wall

remediation) and Fimiston South becomes the dominant ore source

Fimiston South – Gets better every day… over a decade

A simple business: Three large-scale production centres

NST tenure NST mill

Kalgoorlie Operations: Production target 1.1Mozpa

9

▪ Growth supported by vast quantity

of significant drill results at KCGM…

▪ …outside Reserves including:

▪ Fimiston South open pit (includes

23m @ 66g/t in the “saddle”)

▪ OBH North open pit

▪ Fimiston South underground

▪ Mt Charlotte underground (Mt

Ferrum, Kal East, Little Wonder)

▪ Resource averages a globally leading

45,000oz per vertical metre

▪ Significant Fimiston Underground

potential (starting 2.2Moz Resource)

A simple business: Three large-scale production centresKalgoorlie Operations: Production target 1.1Mozpa

10

Yandal

Operations

Thunderbox

Bronzewing

Jundee

Reserves: 66Mt @ 2.2g/t for 4.6Moz

Resources: 139Mt @ 2.3g/t for 10.2Moz

Processing capacity: 5.5Mtpa

Yandal Operations: Production target 600kozpa

▪ Key growth opportunities from expansion and optimisation of

milling; evaluation of various options is underway:

▪ Potential expansion of Thunderbox mill to 6Mtpa;

▪ Potential expansion of Jundee mill to 5Mtpa; or

▪ Refurbishment of Bronzewing mill to 2.2Mtpa

▪ Ore sources to underwrite increased mill throughput include:

▪ Thunderbox D Zone open pit (production)

▪ Thunderbox underground (production)

▪ Bronzewing / Orelia open pits (development)

▪ Wonder North open pit (development)

▪ Aggressive drilling across Yandal district - 25 rigs working

NST tenure NST mill

A simple business: Three large-scale production centres

11

Reserves: 5.9Mt @ 8.0g/t for 1.5Moz

Resources: 22Mt @ 9.8g/t for 6.7Moz

Processing capacity: 1.3Mtpa from mid 2021

Pogo

North American Operations: Production target 300kozpa

Nth American

Operations

▪ Production growing to 300kozpa by FY23 through an expanded

1.3Mtpa processing plant (mid-2021 completion)

▪ Outstanding high grades – December half 9.0g/t head grade

▪ Development advance ramping up (current ~1,000m per month,

target 1,500m per month)…

▪ …to increase stoping volumes once five long-hole open stoping

areas are brought online

▪ Aggressive drilling across Pogo - 13 rigs working after COVID-19

hiatus:

▪ Excellent hits in the main production lodes

▪ Upside from multiple un-modelled structures across mine area

▪ Goodpaster discovery highlights the “camp-scale” opportunity

▪ Other key prospects include Hill 4021, Burn, Cholla, Stone Boy

(excludes Monte Cristo)

A simple business: Three large-scale production centres

NST tenure NST mill

12

FY21 guidance 1.5–1.7Moz at AISC of US$1,080-$1,190/oz

FY21 guidance based on previously announced market disclosures – Refer to page 2 of this presentation

OperationProduction

(koz)

AISC

(US$/oz)

Growth capex

(US$M)

KCGM 440 - 480 1,147 - 1,225 154

Kalgoorlie 270 - 300 1,287 - 1,365 9

Carosue Dam 240 - 250 1,014 - 1,092 109

Kalgoorlie Operations 950 - 1,030 273

Jundee and Bronzewing 270 - 300 936 - 995 29

Thunderbox 140 - 150 780 - 858 148

Yandal Operations 410 - 450 177

Pogo 180 - 220 1,200 - 1,400 35

North American Operations 180 - 220 35

GROUP 1.5-1.7Moz 1,080 - 1,190 485

13

Increasing dividends

1.0 1.0 2.0 3.0 3.0 4.5

6.0 7.5

9.5

2.5 2.5 2.5

3.0

4.0 6.0

5.0

7.5

9.5

3.0

10.0

11 25

46 76

118

190

249

336

536

647

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 HY21

Interim (cps) Final (cps) Special (cps) Cumulative Dividend

▪ Long track record of paying dividends to owners

▪ Dividend payout targeted at 6% of revenue

▪ December Half FY21 interim dividend up 27% to A9.5cps fully franked (A$110.5M (US$86M) on the expanded post-merger capital base)

▪ Record date 9 March 2021; Payment date 30 March 2021

▪ Shareholder returns anticipated to increase further in the coming years due to significant production growth

14

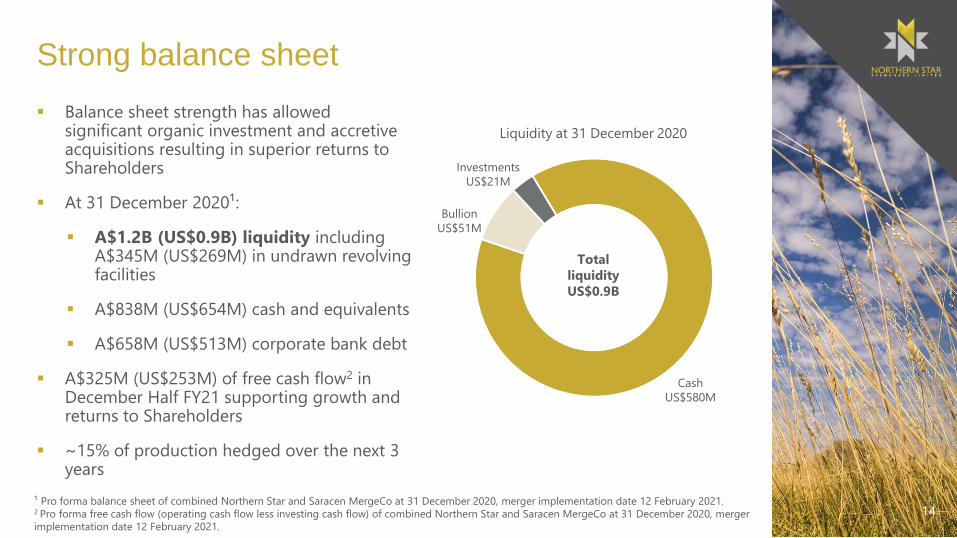

Strong balance sheet

▪ Balance sheet strength has allowed significant organic investment and accretive acquisitions resulting in superior returns to Shareholders

▪ At 31 December 2020¹:

▪ A$1.2B (US$0.9B) liquidity including A$345M (US$269M) in undrawn revolving facilities

▪ A$838M (US$654M) cash and equivalents

▪ A$658M (US$513M) corporate bank debt

▪ A$325M (US$253M) of free cash flow2 in December Half FY21 supporting growth and returns to Shareholders

▪ ~15% of production hedged over the next 3 years

Total

liquidity

US$0.9B

Cash

US$580M

Bullion

US$51M

Investments

US$21M

Liquidity at 31 December 2020

¹ Pro forma balance sheet of combined Northern Star and Saracen MergeCo at 31 December 2020, merger implementation date 12 February 2021.2 Pro forma free cash flow (operating cash flow less investing cash flow) of combined Northern Star and Saracen MergeCo at 31 December 2020, merger

implementation date 12 February 2021.

15

Advantage Northern StarUnrivalled exposure to Tier-1 assets

(Market capitalisation at 24/2/21)

100%

47%

41%

33%29%

20%14%

7%2% 0%

Northern Star

(US$9B)

D

(US$14B)

B

(US$34B)

A

(US$44B)

I

(US$4B)

G

(US$8B)

H

(US$8B)

F

(US$8B)

C

(US$15B)

E

(US$9B)

Tier-1 jurisdictions = Top 10 jurisdictions as per Fraser Institute Annual Survey of Mining Companies 2020

Reserve data sourced from Company Reserve and Resource Reports at Feb 2021

Leading gold producers - Reserves (%) in Tier-1 jurisdictions

16

Unrivalled exposure to production growth

Advantage Northern Star

Tier-1 jurisdictions = Top 10 jurisdictions as per Fraser Institute Annual Survey of Mining Companies 2020

Production growth (FY20-23) sourced from BMO Capital Markets “The GoldPages” February 2021

Leading gold producers - Growth (3-year CAGR)

(Market capitalisation at 24/2/21)

12%

9% 9%

5%4%

3% 2%

0%

-3%-4%

Northern Star

(US$9B)

D

(US$14B)

G

(US$8B)

H

(US$8B)

I

(US$4B)

A

(US$44B)

E

(US$9B)

B

(US$34B)

F

(US$8B)

C

(US$15B)

17

Northern Star Resources LimitedASX Code: NST

The Australian gold miner – for global investors

Investor Enquiries:

Troy Irvin

Level 1, 388 Hay Street, Subiaco 6008 Western Australia

T: +61 8 6188 2100

W: www.nsrltd.com

Inventum 3D Page Links click here