BMCE BANK · E-mail: [email protected] Website: BALANCE SHEET 2012 2011 ASSETS...

47

BMCE BANK CONSOLIDATED FINANCIAL STAT MENTS UNDER IAS/IFRS December 31, 2012 BMCE BANK

Transcript of BMCE BANK · E-mail: [email protected] Website: BALANCE SHEET 2012 2011 ASSETS...

BMCE BANK CONSOLIDATEDFINANCIAL STAT MENTS

UNDER IAS/IFRS

December 31, 2012

BMCE BANK

CONTENTFINANCIAL COMMUNICATION OF BMCE BANK GROUP 3

ACCOUNTING STANDARDS AND PRINCIPLES APPLIED BY THE GROUP 8

IFRS CONDSOLITATD FINANCIAL STATEMENTS AS OF DECEMBER 31, 2012 18

Balance Sheet 18 Income Statement 19 Statement of Changes in Shareholder’s Equity 20 Cash Flows Statement 21

2. NOTES TO CONSOLIDATED INCOME 22

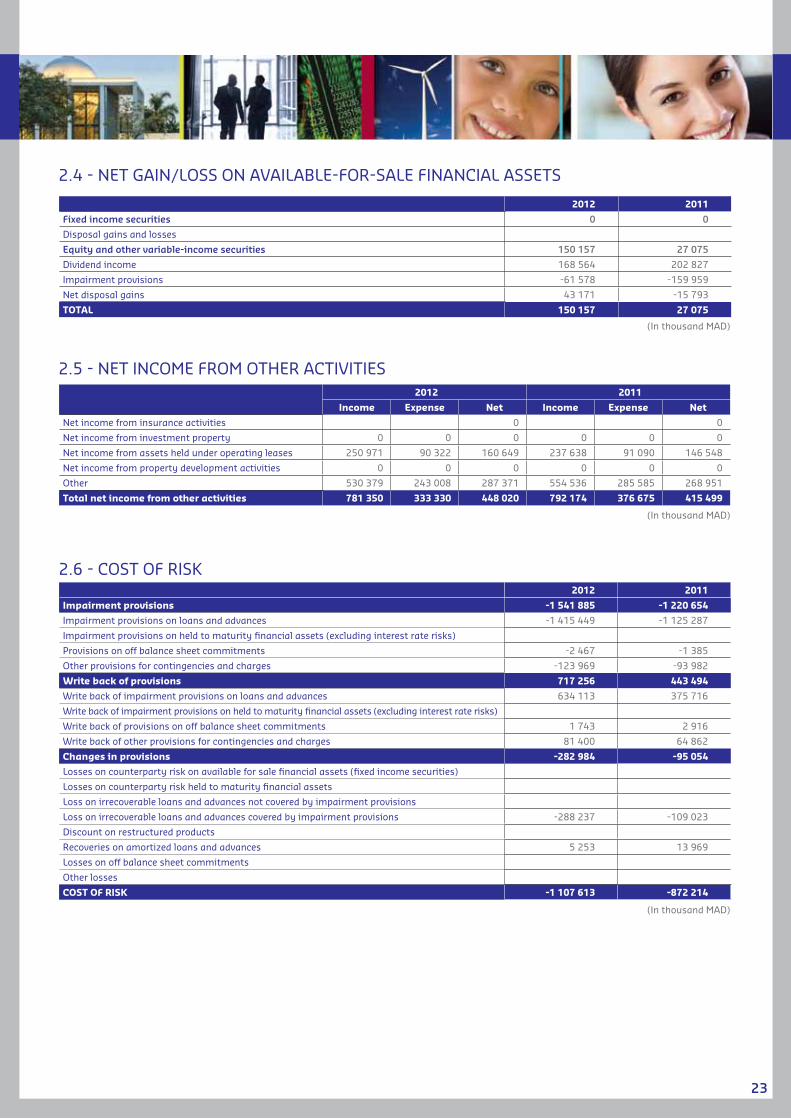

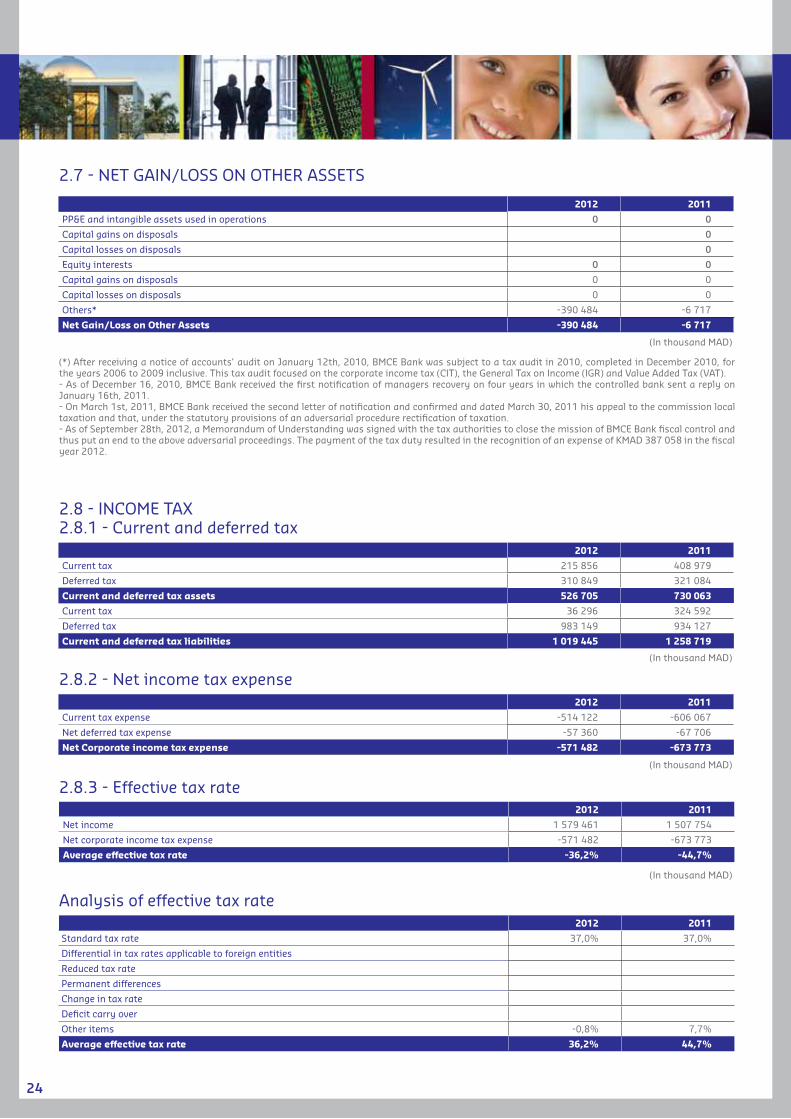

2.1 Net Interest Income 222.2 Net Fee Income 222.3 Net gain/loss on financial instruments at fair value through profit or loss 222.4 Net gain/loss on available for sale assets 232.5 Net income from other activities 232.6 Cost of risk 232.7 Net gain/loss on other assets 242.8 Income Tax 24

3. SEGMENT INFORMATION 25

4. RISK EXPOSURE AND HEDGING STRATEGIES 26

4.1 Risk Management System 264.2 Credit Risk 284.3 Market Risk 314.4 Operational Risk 334.5 Stress Testing 354.6 Capital Components and Capital Adequacy 364.7 Country Risk 364.8 Asset Liability Management 36

5. BALANCE SHEET NOTE 37

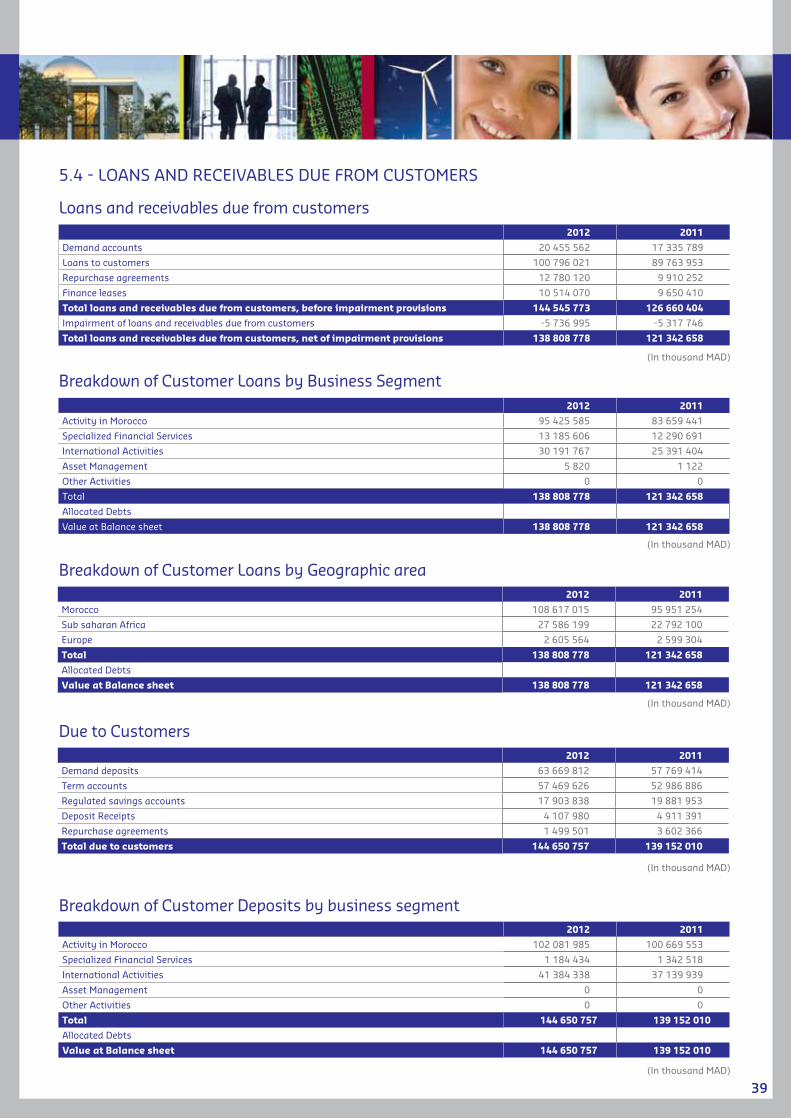

5.1 Financial assets, financial liabilities, and derivatives at fair value through profit or loss 375.2 Available for sale financial assets 385.3 Interbank and money-market items 385.4 Loans and receivables due from customers 395.5 Debt securities and subordinated debts 405.6 Held to maturity financial assets 405.7 Current and deferred taxes 405.8 Accrued income/expense and other assets/liabilities 415.9 Investments in companies consolidated under the equity method 415.10 Property, plant and equipment and intangible assets used in operations 415.11 Goodwill 425.12 Provisions for contingencies and charges 42

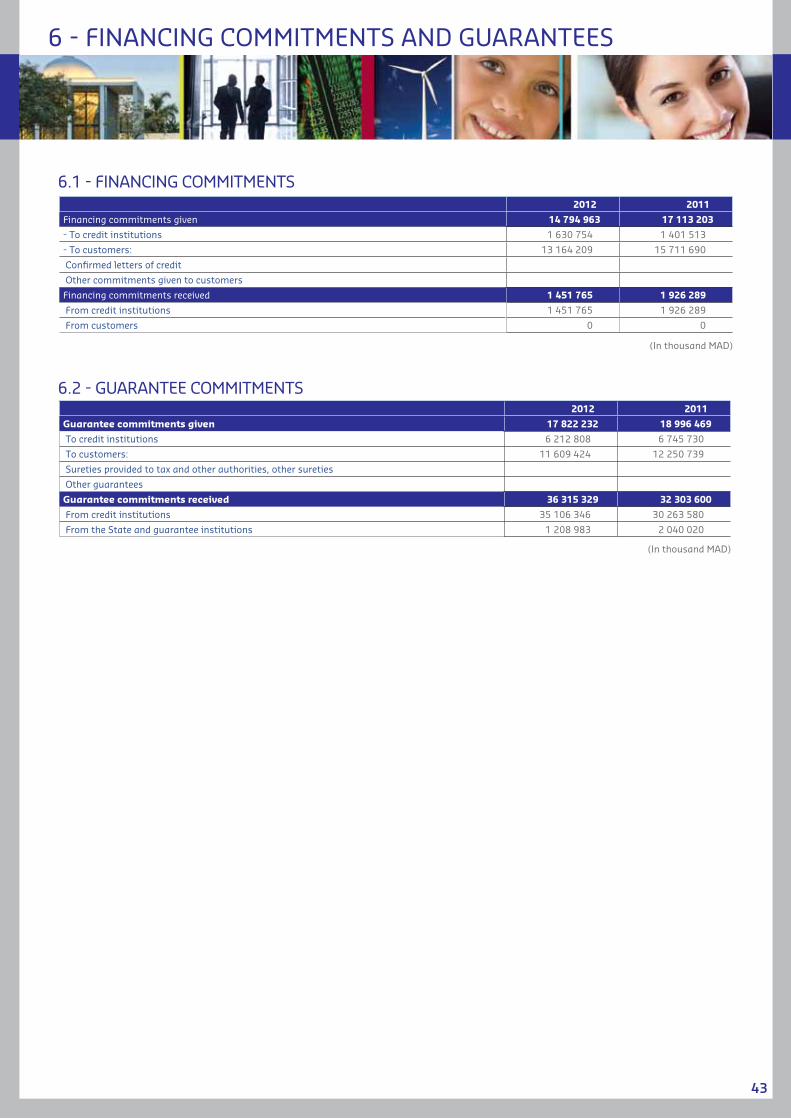

6. FINANCING COMMITMENTS AND GUARANTEE 43

6.1 Financing Commitments 436.2 Guarantee Commitments 43

7. SALARIES AND EMPLOYEE BENEFITS 44

7.1 Description of evaluation method 447.2 Summary of provisions and description of existing schemes 447.3 Cost of post- employment plans 447.4 Provision evolution included in the balance sheet 44

8. ADDITIONAL INFORMATION 45

8.1 Changes in share capital and earnings per share 458.2 Scope of consolidation 458.3 Related parties 45

FY

FiNANciAl coMMUNicATioN oF BMcE BANk GRoUP

A SOLID FINANCIAL PERFORMANCE IN 2012 IN LINE WITH OBJECTIVES

2012BMcE Bank’s Board of directors, chaired by Mr othman Benjelloun, met on Friday 22 March 2013 at the bank’s registered officein casablanca. it examined the business activity of the bank and of the Group for the financial year ended 31 december 2012and drew up the financial statements for the year in question.

The Board of directors will propose to the Annual General Meeting of Shareholders a dividend of 3.30 dirhams per share.

The 2012 financial statements under iAS/iFRS are published on the bank’s website www.bmcebank.ma.

cOnSOLIDATEDAcTIVITY

AGGREGATEDAcTIVITY

MAD 9 billion

MAD 1.2 billion

MAD 3.6 billion

+11%

Net banking income

+47%

Net Income Attributable to ParentExcluding exceptional items

+19%

Gross operating income

MAD 1.0 billion$148 m and €112m $119 m and €90m

MAD 4.6 billion$1bn and €809m $544 m and €412m

MAD 1.8 billion$425 m and €321m $218 m and €165m

+90%

Aggregated net incomeExcluding exceptional items

MAD 923 million+9%

Net Income Attributable to Parent

MAD 713 million$109 m and €83m $85 m and €64m

+31%

Aggregated net income

Net banking income

Gross operating income

+13%

+41%

Net earnings excluding exceptional items of more than MAd 1 billion –more than

$119 m and €90m

capital base strengthened with a 15% rise to MAd 14.3 billion -$1.7bn and €1.3 bn-

in shareholders’ equity attributable to Parent

BMcE Bank Group expands further in Africawith operations in 19 countries

FiNANciAl coMMUNicATioNTel: +212 522 49 80 03/04 - Fax: +212 522 26 49 65E-mail: [email protected]: www.bmcebank.ma

BALANCE SHEET 2012 2011

ASSETS EUR USd MAd % change MAd12-11

cash, central banks, treasury & giro accounts 890 1 176 9 922 55% 6 392

Financial assets at fair value through profit or loss 3 072 4 058 34 245 8% 31 732

Available for financial assets 251 331 2 796 20% 2 330

loans and receivables due from credit institutions 1 920 2 535 21 397 -10% 23 823

loans and receivables due from customers 12 453 16 449 138 809 14% 121 343

Held to maturity financial assets 944 1 246 10 519 10% 9 591

investment property 55 73 614 12% 547

Tangible fixed assets 460 608 5 131 1% 5 064

intangible fixed assets 67 89 751 16% 645

Goodwill 75 99 832 0% 832

other assets 527 696 5 873 3% 5 689

TOTAL ASSETS 20 714 27 360 230 889 11% 207 988

LIABILITIESdue to credit institutions 3 071 4 056 34 228 38% 24 849

due to customers 12 977 17 141 144 651 4% 139 152

debt securities 1 257 1 661 14 015 17% 12 009

Provisions for contigencies and charges 47 62 523 14% 457

Subordinated debts 427 564 4 760 -3% 4 904

Shareholders Equity 1 652 2 182 18 413 12% 16 385

Attributable to Parent 1 279 1 690 14 260 15% 12 428Non-controlling interests 373 492 4 153 5% 3 957

other liabilities 1 283 1 694 14 299 40% 10 232

TOTAL LIABILITIES & SHAREHOLDERS EQUITY 20 714 27 360 230 889 11% 207 988

2012 2011IncOME STATEMEnT EUR USd MAd % change MAd

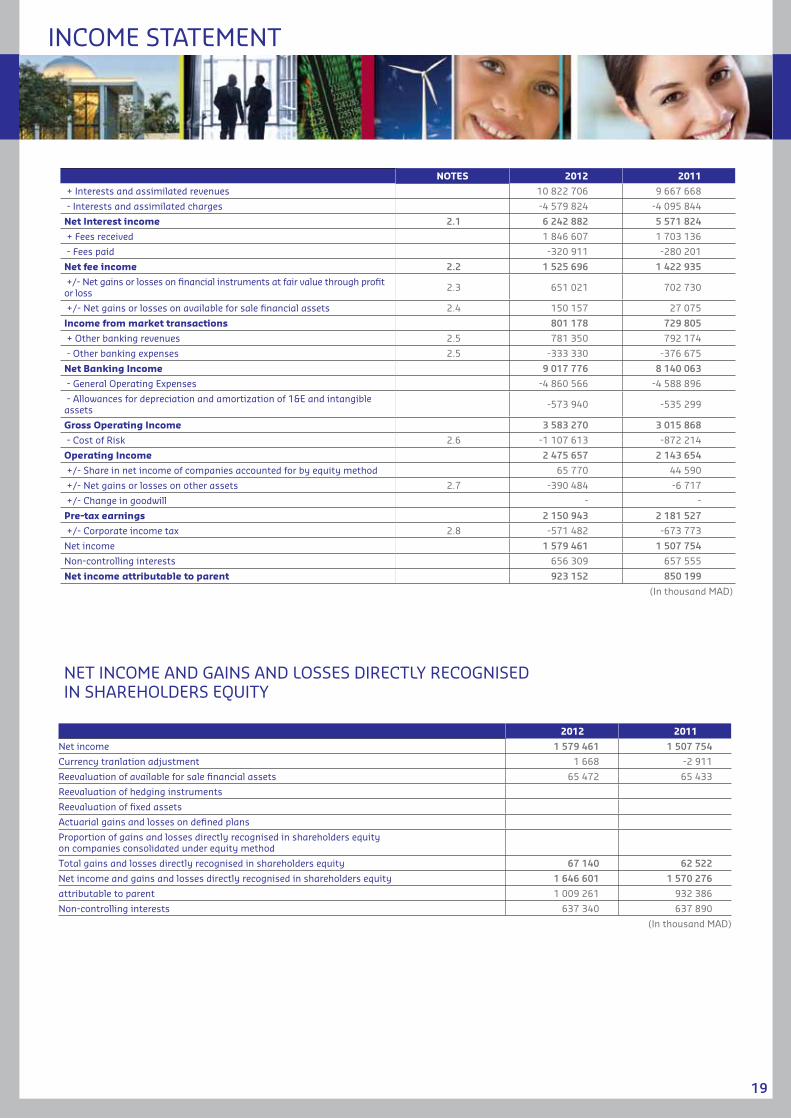

12-11 Net interest income 560 740 6 243 12% 5 572

Net fee income 137 181 1 526 7% 1 423

income from market transactions 72 95 801 10% 730

Net miscellaneous 40 53 448 8% 415

net Banking Income 809 1 069 9 018 11% 8 140

General operating expenses 436 576 4 861 6% 4 589

Provision for amortization and depreciation 51 68 574 7% 535

Gross Operating Income 321 425 3 583 19% 3 016

cost of risk 99 131 1 108 27% 872

operating income 222 293 2 476 15% 2 144

Pretax income 193 255 2 151 -1% 2 181

income tax 51 68 571 -15% 674

net Income 142 187 1 579 5% 1 508

Non-controlling interests 59 78 656 0% 657

nET IncOME ATTRIBUTABLE TO PAREnT 83 109 923 9% 850

in million

in million

in millionExchange rates as of december 31st, 2012EUR/MAD: 11.1465USD/MAD: 8.4390

coNSolidATEd AcTiviTy

IFRS SIMPLIFIED FINANCIAL STATEMENTS

Plaquette ANGLast.qxd:Mise en page 1 10/04/13 11:17 Page 1

SPECIALISED FINANCIAL SERVICES:RESILIENT PERFORMANCE DESPITE ANuNFAVOuRABLE ENVIRONMENT

MAGHREBAIL

6.3% growth in net outstandings versus 3% growthfor the sector resulting in a rise in market share from19.8% to 20.5%.

SALAFIn

6% rise in distributed loans against a fall in that of thesector with net income broadly unchanged at MAd 92 million -$11 m and €8.2 m - inclusive of a MAd 1.4 million -$170 k and €130 k - Social cohesioncontribution.

MAROc FAcTORInG

2012 was marked by a refocusing of activities on thecore business, full factoring, by outsourcing thecorporate client portfolio, reorganising sales andreducing costs in a highly competitive environment.

RM EXPERTS

Positive performance from BMcE Bank Group’s debtrecovery subsidiary with the volume of debt recoveredtotalling MAd 305 million -$36 m and €27.4 m - in2012 resulting in MAd 130 million -$15.4 m and €12 m - in provision write-backs.

SuB-SAHARAN AFRICAN ACTIVITIES:GROuP INCREASINGLY ANCHORED INAFRICA

BAnK OF AFRIcA

Solid consolidated results with 15% rise to € 291 million -$ 384 million- in net banking incomeand 13.6% increase to € 119 million -$ 157 million- ingross operating income.

Strong commercial performance with (i) 11% growthin customer deposits to € 3.2 billion -$ 4.2 bn- and20% increase to € 2.2 billion -$ 2.9 bn- in customerloans and (ii) 23% rise in customer portfolio to 1.4 million accounts.

BoA Group continues to grow organically with 32 newbranch openings taking the total distribution networkto 370 branches covering 15 countries.

Banking licence granted to Bank of Africa in Togo in2012,taking the total number of countries in whichthe Group has operations to 15.

LA cOnGOLAISE DE BAnQUE

Another positive financial performance in line withprevious years with a 17% rise to € 30 million -$ 39.7 million- in net banking income and a 16% riseto € 10.7 million -$ 14.1 million- in net income.

BAnQUE DE DEVELOPPEMEnT DU MALI

Significant growth of 21% to €12.7 million -$ 16.8 million- in net income at 31 december 2012.

EuROPEAN ACTIVITIES: RETuRN TOBREAk-EVEN

Recovery seen at BMcE Bank international Plc, theGroup’s london-based subsidiary, with net income of£ 1.2 billion, positive for the first time sinceestablishment, due to a major restructuringprogramme since 2011.

Satisfactory results from BMcE Bank internationalMadrid despite a difficult economic environment inSpain with net banking income stable at € 11 million-$ 14.5 million- and net income of € 3 million -$ 4 million-.

CSR AND SuSTAINABLE DEVELOPMENT:CONSOLIDATION OF SOCIALLY-RESPONSIBLE AND ENVIRONMENTALPRACTICES

BMcE Bank Foundation honoured by the awardsbestowed upon its President, dr leila MezianBenjelloun, in acknowledgment of her commitment topromoting Amazigh culture and human developmentincluding the Prix du Mérite de la culture Amazighe2011 from the Royal institute of Amazigh culture aswell as the Woman of the year 2012 prize from theAmerican chamber of commerce.

Expansion of the Medersat.com network to 174complexes, school and pre-school units following theopening of a school in imouzzer Marmoucha and thebuilding of an establishment in Bamako in Mali. Thistakes the total number of children educated and caredfor by the Foundation to 14,000.

Energico, Morocco’s first green product, introduced bythe corporate banking network, aimed primarily atSMEs to help them finance the purchase of energy-saving equipment.

Encouraging results which exceeded expectationsfollowing the implementation of iSo 14001 aimed atreducing water, electricity and paper consumption.

RETAIL BANkING: NEW MARkETSEGMENTS TARGETED

Significant growth of 29% in total bancassurancerevenue to MAd 1.7 billion -$198 m and €153 m -.

Enhanced services for Moroccans living abroad tosatisfy their changing needs such as E-transfert andcash to Account.

development strategy launched targeting the high-growth private client market segment.

BMcE direct, the bank’s remote banking serviceenhanced with the introduction of an onlinestockbroking service.

New services introduced dedicated to very smallenterprises such as Forfait TPE and crédit damaneExpress.

CORPORATE BANkING: A SuCCESSFuLSME STRATEGY GENERATING ADDTIONALVALuE

11.2% growth in corporate banking deposits to MAd 25 billion -$3 bn and €2.2 bn - and 4.3% growthin corporate loans to MAd 61.3 billion -$7.3 bn and €5.5 bn -.

coverage of SME banking market segment bolsteredthrough: (i) a more personalised products and servicesoffering and greater innovation e.g. Pack BusinessPME and club PME and (ii) closer relations with SMEcustomers by organising regional meetings.

Foreign trade business strengthened as can be seenin the 12% rise in import volumes and the 16% rise inexport volumes, registering a stronger pace of growththan the industry average (+7% and +4%respectively).

Market leadership in Project Finance consolidateddue to a number of large-scale deals in various sectors despite less than favourable businessconditions.

closer relations developed with corporate customerswith the opening of 3 new business centres in Nador,oujda and laâyoune.

INVESTMENT BANkING: MARkETCONDITIONS STILL uNFAVOuRABLE

BMcE capital Markets’ share of the private debt market rose to 53.2% due to aggressive sales approach and a differentiated product offering, resulting in the bank retaining its position as themarket leader.

Synergies derived between BMcE capital Bourse andcM-cic Securities as part of the African SecuritiesNetwork project with an agreement signed todistribute each other’s research products.

5% rise to MAd 33.5 billion -$4 bn and €3 bn - inBMcE capital Gestion’s assets under managementversus a 4.6% rise for the sector, resulting in increasedmarket share to 14%.

BMcE capital Titres’ volume of assets under custodystable and market share unchanged at 28% despite adecline in stock market volume in 2012.

PoSiTivE PERFoRMANcE By THE GRoUP’S iNdividUAl BUSiNESS liNESSTRoNG GRoWTH AcRoSS THE BoARd

CONSOLIDATED ACTIVITY: 47% RISE INNET INCOME ATTRIBuTABLE TO PARENTEXCLuDING EXCEPTIONAL ITEMS TO MAD 1.2 BILLION -$148 m and €112m-

9% rise in Net income Attributable to Parent to MAd 923 million -$109 m and €83m- despite morethan MAd 1 billion in provisions (MAd 1.1 billion;$131 m and €99m-).

47% rise in Net income Attributable to Parentexcluding exceptional items to MAd 1.2 billion -$148 m and €112m - exceptional net charge of MAd 323 million -related to taxation and the Socialcohesion contribution.

- A very strong performance by domesticactivities including (i) BMcE Bank SA whichsaw its contribution rise by 78% and (ii) theinvestment banking and assetmanagement division which registered a15% increase in its contribution to Netincome Attributable to Parent excludingexceptional items;

- Solid results from international activitieswith (i) a positive contribution fromEuropean subsidiaries, accounting for 4% ofNet income Attributable to Parent excludingexceptional items versus a negativecontribution the previous year and (ii) a30% rise in the contribution from sub-Sahara African activities.

11% rise in consolidated Net Banking income tomore than MAd 9 billion -$1bn and €809m- for thefirst time. This, together with a 6% rise in generaloperating expenses resulted in a 2.6 pointsimprovement in the cost-to-income ratio to 60.3%.

19% rise in gross operating income to almost MAd 3.6 billion -$425 m and €321m-in 2012 versusMAd 3 billion -$349 m and €270m-the previousyear due to a sustainable performance at theoperating level.

capital base strengthened with a 15% increase inshareholders’ equity attributable to parent fromMAd 12.4 billion -$1.4bn and €1.1 bn - in 2011 toMAd 14.3 billion -$1.7bn and €1.3 bn -in 2012following a MAd 1.5 billion -$180 m and €135 m -equity issue reserved for reference shareholders.The purpose was to provide adequate funds for theGroup’s strategic development domestically andoverseas and to meet new regulatory capitalrequirements.

Steady growth in the Group’s assets at 11% overthe past 4 years with total consolidated assets ofMAd 231 billion -$27bn and €21 bn -in 2012.

4% rise to MAd 144.6 billion - $17bn and €13 bn -in consolidated deposits and 14% increase toMAd 138.8 billion - $16bn and €12.5 bn -inconsolidated loans.

AGGREGATED ACTIVITY: DOuBLE-DIGITGROWTH IN THE MAIN INDICATORS

90% year-on-year rise in aggregated net income excluding exceptional items to more than MAd 1 billion -$119 m and €90m- and 31%rise from MAd 545 million -$65 m and €49m- in 2011 to MAd 713 million -$85 m and €64m - in 2012 after recognition of an exceptional tax expense.

13% rise to MAd 4.6 billion -$544 m and €412m-in aggregated net banking income due to a strongperformance by the bank’s core business as can beseen in an 11% increase in net interest income anda 9% rise in fee income.

contained growth in general operating expenses at5.5% resulting in a 4.3 points improvement in thecost-to-income ratio to 60.6%.

41% rise in gross operating income to MAd 1.8 billion -$209 m and €165m- due to asubstantial provisioning effort of almost MAd 712 million - $84 m and €64m - including aMAd 217 million -$26 m and €19.5m - sector-specific gross provision for general risks taking totalgross provisions for general risks to MAd 472 million -$56 m and €42.4m -.

Strong ability to attract savings with a 6% rise indeposits to MAd 107 billion -$12.7 bn and €9.6 bn- versus 2.7% growth in sector deposits resulting ina 43 basis point improvement in BMcE Bank’smarket share to 14.78%.

Strong momentum in lending with a 6% rise in totalloans to MAd 93.5 billion -$11 bn and €8.4 bn -,resulting in an 11 basis point improvement inmarket share.

IMPROVEMENT IN THE BANk’S SOLVENCYAND RISk PROFILE

core capital bolstered resulting in a Tier 1 capitalratio of more than 9% and a solvency ratio of morethan 12%.

40 basis point decline in the loan loss ratioto 4.53% which is below the sector average of 4.96%

improvement in the non-performing loan coverageratio from 67.4% in 2011 to 71.6% in 2012.

coNSolidATEd ANNUAl RESUlTS 2012

2012-2013 HIGHLIGHTS

Shareholding in Bank of Africa Groupincreased to 68%.

BoA granted banking licence in Togo.

BMcE Bank named “Best Trade Finance Bankin Morocco” by Global Trade Review as wellas “Socially Responsible Bank of the year”by African Banker Awards.

BMcE Bank international Plc awarded“African Project Finance – Transport deal ofthe year” by Euromoney.

MAd 1.5 billion -$180 m and €135 m - equity issue by BMcE Bank reserved formajor shareholders.

MAd 1 billion -$119 m and €90m-subordinated bond issue.

$75 million credit line obtained from theEuropean Bank for Reconstruction anddevelopment (EBRd) to refinance foreigntrade activities.

Spanish subsidiary BMcE Euroservicesestablished to take charge of the Moroccansliving Abroad business in partnership withthe domestic network in the context of theGroup reorganising its European platform.

BMCE BANk GROuP CONSOLIDATED ACTIVITY

231 MAd

208

+11%

20122011

Total Assets - In billion

1 246 MAd

850

+47%

20122011

Net Income Attributable to ParentExcluding exceptional items - In million

9 018 MAd

+11%

20122011

Net Banking Income - In million

3 583 MAd+19%

20122011

Gross Operating Income - In million

923 MAd850

+9%

20122011

Net Income Attributable to Parent - In million

3 016

8 140

2012 NET INCOME GROuP SHARE By GEoGRAPHic AREA

Morocco

Sub-Saharan Africa

Europe

51%

44%

5%

112€

148$

109$

1069$

425$

321€

20.7€

27.4$

83€

809€

Plaquette ANGLast.qxd:Mise en page 1 10/04/13 11:17 Page 2

SPECIALISED FINANCIAL SERVICES:RESILIENT PERFORMANCE DESPITE ANuNFAVOuRABLE ENVIRONMENT

MAGHREBAIL

6.3% growth in net outstandings versus 3% growthfor the sector resulting in a rise in market share from19.8% to 20.5%.

SALAFIn

6% rise in distributed loans against a fall in that of thesector with net income broadly unchanged at MAd 92 million -$11 m and €8.2 m - inclusive of a MAd 1.4 million -$170 k and €130 k - Social cohesioncontribution.

MAROc FAcTORInG

2012 was marked by a refocusing of activities on thecore business, full factoring, by outsourcing thecorporate client portfolio, reorganising sales andreducing costs in a highly competitive environment.

RM EXPERTS

Positive performance from BMcE Bank Group’s debtrecovery subsidiary with the volume of debt recoveredtotalling MAd 305 million -$36 m and €27.4 m - in2012 resulting in MAd 130 million -$15.4 m and €12 m - in provision write-backs.

SuB-SAHARAN AFRICAN ACTIVITIES:GROuP INCREASINGLY ANCHORED INAFRICA

BAnK OF AFRIcA

Solid consolidated results with 15% rise to € 291 million -$ 384 million- in net banking incomeand 13.6% increase to € 119 million -$ 157 million- ingross operating income.

Strong commercial performance with (i) 11% growthin customer deposits to € 3.2 billion -$ 4.2 bn- and20% increase to € 2.2 billion -$ 2.9 bn- in customerloans and (ii) 23% rise in customer portfolio to 1.4 million accounts.

BoA Group continues to grow organically with 32 newbranch openings taking the total distribution networkto 370 branches covering 15 countries.

Banking licence granted to Bank of Africa in Togo in2012,taking the total number of countries in whichthe Group has operations to 15.

LA cOnGOLAISE DE BAnQUE

Another positive financial performance in line withprevious years with a 17% rise to € 30 million -$ 39.7 million- in net banking income and a 16% riseto € 10.7 million -$ 14.1 million- in net income.

BAnQUE DE DEVELOPPEMEnT DU MALI

Significant growth of 21% to €12.7 million -$ 16.8 million- in net income at 31 december 2012.

EuROPEAN ACTIVITIES: RETuRN TOBREAk-EVEN

Recovery seen at BMcE Bank international Plc, theGroup’s london-based subsidiary, with net income of£ 1.2 billion, positive for the first time sinceestablishment, due to a major restructuringprogramme since 2011.

Satisfactory results from BMcE Bank internationalMadrid despite a difficult economic environment inSpain with net banking income stable at € 11 million-$ 14.5 million- and net income of € 3 million -$ 4 million-.

CSR AND SuSTAINABLE DEVELOPMENT:CONSOLIDATION OF SOCIALLY-RESPONSIBLE AND ENVIRONMENTALPRACTICES

BMcE Bank Foundation honoured by the awardsbestowed upon its President, dr leila MezianBenjelloun, in acknowledgment of her commitment topromoting Amazigh culture and human developmentincluding the Prix du Mérite de la culture Amazighe2011 from the Royal institute of Amazigh culture aswell as the Woman of the year 2012 prize from theAmerican chamber of commerce.

Expansion of the Medersat.com network to 174complexes, school and pre-school units following theopening of a school in imouzzer Marmoucha and thebuilding of an establishment in Bamako in Mali. Thistakes the total number of children educated and caredfor by the Foundation to 14,000.

Energico, Morocco’s first green product, introduced bythe corporate banking network, aimed primarily atSMEs to help them finance the purchase of energy-saving equipment.

Encouraging results which exceeded expectationsfollowing the implementation of iSo 14001 aimed atreducing water, electricity and paper consumption.

RETAIL BANkING: NEW MARkETSEGMENTS TARGETED

Significant growth of 29% in total bancassurancerevenue to MAd 1.7 billion -$198 m and €153 m -.

Enhanced services for Moroccans living abroad tosatisfy their changing needs such as E-transfert andcash to Account.

development strategy launched targeting the high-growth private client market segment.

BMcE direct, the bank’s remote banking serviceenhanced with the introduction of an onlinestockbroking service.

New services introduced dedicated to very smallenterprises such as Forfait TPE and crédit damaneExpress.

CORPORATE BANkING: A SuCCESSFuLSME STRATEGY GENERATING ADDTIONALVALuE

11.2% growth in corporate banking deposits to MAd 25 billion -$3 bn and €2.2 bn - and 4.3% growthin corporate loans to MAd 61.3 billion -$7.3 bn and €5.5 bn -.

coverage of SME banking market segment bolsteredthrough: (i) a more personalised products and servicesoffering and greater innovation e.g. Pack BusinessPME and club PME and (ii) closer relations with SMEcustomers by organising regional meetings.

Foreign trade business strengthened as can be seenin the 12% rise in import volumes and the 16% rise inexport volumes, registering a stronger pace of growththan the industry average (+7% and +4%respectively).

Market leadership in Project Finance consolidateddue to a number of large-scale deals in various sectors despite less than favourable businessconditions.

closer relations developed with corporate customerswith the opening of 3 new business centres in Nador,oujda and laâyoune.

INVESTMENT BANkING: MARkETCONDITIONS STILL uNFAVOuRABLE

BMcE capital Markets’ share of the private debt market rose to 53.2% due to aggressive sales approach and a differentiated product offering, resulting in the bank retaining its position as themarket leader.

Synergies derived between BMcE capital Bourse andcM-cic Securities as part of the African SecuritiesNetwork project with an agreement signed todistribute each other’s research products.

5% rise to MAd 33.5 billion -$4 bn and €3 bn - inBMcE capital Gestion’s assets under managementversus a 4.6% rise for the sector, resulting in increasedmarket share to 14%.

BMcE capital Titres’ volume of assets under custodystable and market share unchanged at 28% despite adecline in stock market volume in 2012.

PoSiTivE PERFoRMANcE By THE GRoUP’S iNdividUAl BUSiNESS liNESSTRoNG GRoWTH AcRoSS THE BoARd

CONSOLIDATED ACTIVITY: 47% RISE INNET INCOME ATTRIBuTABLE TO PARENTEXCLuDING EXCEPTIONAL ITEMS TO MAD 1.2 BILLION -$148 m and €112m-

9% rise in Net income Attributable to Parent to MAd 923 million -$109 m and €83m- despite morethan MAd 1 billion in provisions (MAd 1.1 billion;$131 m and €99m-).

47% rise in Net income Attributable to Parentexcluding exceptional items to MAd 1.2 billion -$148 m and €112m - exceptional net charge of MAd 323 million -related to taxation and the Socialcohesion contribution.

- A very strong performance by domesticactivities including (i) BMcE Bank SA whichsaw its contribution rise by 78% and (ii) theinvestment banking and assetmanagement division which registered a15% increase in its contribution to Netincome Attributable to Parent excludingexceptional items;

- Solid results from international activitieswith (i) a positive contribution fromEuropean subsidiaries, accounting for 4% ofNet income Attributable to Parent excludingexceptional items versus a negativecontribution the previous year and (ii) a30% rise in the contribution from sub-Sahara African activities.

11% rise in consolidated Net Banking income tomore than MAd 9 billion -$1bn and €809m- for thefirst time. This, together with a 6% rise in generaloperating expenses resulted in a 2.6 pointsimprovement in the cost-to-income ratio to 60.3%.

19% rise in gross operating income to almost MAd 3.6 billion -$425 m and €321m-in 2012 versusMAd 3 billion -$349 m and €270m-the previousyear due to a sustainable performance at theoperating level.

capital base strengthened with a 15% increase inshareholders’ equity attributable to parent fromMAd 12.4 billion -$1.4bn and €1.1 bn - in 2011 toMAd 14.3 billion -$1.7bn and €1.3 bn -in 2012following a MAd 1.5 billion -$180 m and €135 m -equity issue reserved for reference shareholders.The purpose was to provide adequate funds for theGroup’s strategic development domestically andoverseas and to meet new regulatory capitalrequirements.

Steady growth in the Group’s assets at 11% overthe past 4 years with total consolidated assets ofMAd 231 billion -$27bn and €21 bn -in 2012.

4% rise to MAd 144.6 billion - $17bn and €13 bn -in consolidated deposits and 14% increase toMAd 138.8 billion - $16bn and €12.5 bn -inconsolidated loans.

AGGREGATED ACTIVITY: DOuBLE-DIGITGROWTH IN THE MAIN INDICATORS

90% year-on-year rise in aggregated net income excluding exceptional items to more than MAd 1 billion -$119 m and €90m- and 31%rise from MAd 545 million -$65 m and €49m- in 2011 to MAd 713 million -$85 m and €64m - in 2012 after recognition of an exceptional tax expense.

13% rise to MAd 4.6 billion -$544 m and €412m-in aggregated net banking income due to a strongperformance by the bank’s core business as can beseen in an 11% increase in net interest income anda 9% rise in fee income.

contained growth in general operating expenses at5.5% resulting in a 4.3 points improvement in thecost-to-income ratio to 60.6%.

41% rise in gross operating income to MAd 1.8 billion -$209 m and €165m- due to asubstantial provisioning effort of almost MAd 712 million - $84 m and €64m - including aMAd 217 million -$26 m and €19.5m - sector-specific gross provision for general risks taking totalgross provisions for general risks to MAd 472 million -$56 m and €42.4m -.

Strong ability to attract savings with a 6% rise indeposits to MAd 107 billion -$12.7 bn and €9.6 bn- versus 2.7% growth in sector deposits resulting ina 43 basis point improvement in BMcE Bank’smarket share to 14.78%.

Strong momentum in lending with a 6% rise in totalloans to MAd 93.5 billion -$11 bn and €8.4 bn -,resulting in an 11 basis point improvement inmarket share.

IMPROVEMENT IN THE BANk’S SOLVENCYAND RISk PROFILE

core capital bolstered resulting in a Tier 1 capitalratio of more than 9% and a solvency ratio of morethan 12%.

40 basis point decline in the loan loss ratioto 4.53% which is below the sector average of 4.96%

improvement in the non-performing loan coverageratio from 67.4% in 2011 to 71.6% in 2012.

coNSolidATEd ANNUAl RESUlTS 2012

2012-2013 HIGHLIGHTS

Shareholding in Bank of Africa Groupincreased to 68%.

BoA granted banking licence in Togo.

BMcE Bank named “Best Trade Finance Bankin Morocco” by Global Trade Review as wellas “Socially Responsible Bank of the year”by African Banker Awards.

BMcE Bank international Plc awarded“African Project Finance – Transport deal ofthe year” by Euromoney.

MAd 1.5 billion -$180 m and €135 m - equity issue by BMcE Bank reserved formajor shareholders.

MAd 1 billion -$119 m and €90m-subordinated bond issue.

$75 million credit line obtained from theEuropean Bank for Reconstruction anddevelopment (EBRd) to refinance foreigntrade activities.

Spanish subsidiary BMcE Euroservicesestablished to take charge of the Moroccansliving Abroad business in partnership withthe domestic network in the context of theGroup reorganising its European platform.

BMCE BANk GROuP CONSOLIDATED ACTIVITY

231 MAd

208

+11%

20122011

Total Assets - In billion

1 246 MAd

850

+47%

20122011

Net Income Attributable to ParentExcluding exceptional items - In million

9 018 MAd

+11%

20122011

Net Banking Income - In million

3 583 MAd+19%

20122011

Gross Operating Income - In million

923 MAd850

+9%

20122011

Net Income Attributable to Parent - In million

3 016

8 140

2012 NET INCOME GROuP SHARE By GEoGRAPHic AREA

Morocco

Sub-Saharan Africa

Europe

51%

44%

5%

112€

148$

109$

1069$

425$

321€

20.7€

27.4$

83€

809€

Plaquette ANGLast.qxd:Mise en page 1 10/04/13 11:17 Page 2

5

SPECIALISED FINANCIAL SERVICES:RESILIENT PERFORMANCE DESPITE ANuNFAVOuRABLE ENVIRONMENT

MAGHREBAIL

6.3% growth in net outstandings versus 3% growthfor the sector resulting in a rise in market share from19.8% to 20.5%.

SALAFIn

6% rise in distributed loans against a fall in that of thesector with net income broadly unchanged at MAd 92 million -$11 m and €8.2 m - inclusive of a MAd 1.4 million -$170 k and €130 k - Social cohesioncontribution.

MAROc FAcTORInG

2012 was marked by a refocusing of activities on thecore business, full factoring, by outsourcing thecorporate client portfolio, reorganising sales andreducing costs in a highly competitive environment.

RM EXPERTS

Positive performance from BMcE Bank Group’s debtrecovery subsidiary with the volume of debt recoveredtotalling MAd 305 million -$36 m and €27.4 m - in2012 resulting in MAd 130 million -$15.4 m and €12 m - in provision write-backs.

SuB-SAHARAN AFRICAN ACTIVITIES:GROuP INCREASINGLY ANCHORED INAFRICA

BAnK OF AFRIcA

Solid consolidated results with 15% rise to € 291 million -$ 384 million- in net banking incomeand 13.6% increase to € 119 million -$ 157 million- ingross operating income.

Strong commercial performance with (i) 11% growthin customer deposits to € 3.2 billion -$ 4.2 bn- and20% increase to € 2.2 billion -$ 2.9 bn- in customerloans and (ii) 23% rise in customer portfolio to 1.4 million accounts.

BoA Group continues to grow organically with 32 newbranch openings taking the total distribution networkto 370 branches covering 15 countries.

Banking licence granted to Bank of Africa in Togo in2012,taking the total number of countries in whichthe Group has operations to 15.

LA cOnGOLAISE DE BAnQUE

Another positive financial performance in line withprevious years with a 17% rise to € 30 million -$ 39.7 million- in net banking income and a 16% riseto € 10.7 million -$ 14.1 million- in net income.

BAnQUE DE DEVELOPPEMEnT DU MALI

Significant growth of 21% to €12.7 million -$ 16.8 million- in net income at 31 december 2012.

EuROPEAN ACTIVITIES: RETuRN TOBREAk-EVEN

Recovery seen at BMcE Bank international Plc, theGroup’s london-based subsidiary, with net income of£ 1.2 billion, positive for the first time sinceestablishment, due to a major restructuringprogramme since 2011.

Satisfactory results from BMcE Bank internationalMadrid despite a difficult economic environment inSpain with net banking income stable at € 11 million-$ 14.5 million- and net income of € 3 million -$ 4 million-.

CSR AND SuSTAINABLE DEVELOPMENT:CONSOLIDATION OF SOCIALLY-RESPONSIBLE AND ENVIRONMENTALPRACTICES

BMcE Bank Foundation honoured by the awardsbestowed upon its President, dr leila MezianBenjelloun, in acknowledgment of her commitment topromoting Amazigh culture and human developmentincluding the Prix du Mérite de la culture Amazighe2011 from the Royal institute of Amazigh culture aswell as the Woman of the year 2012 prize from theAmerican chamber of commerce.

Expansion of the Medersat.com network to 174complexes, school and pre-school units following theopening of a school in imouzzer Marmoucha and thebuilding of an establishment in Bamako in Mali. Thistakes the total number of children educated and caredfor by the Foundation to 14,000.

Energico, Morocco’s first green product, introduced bythe corporate banking network, aimed primarily atSMEs to help them finance the purchase of energy-saving equipment.

Encouraging results which exceeded expectationsfollowing the implementation of iSo 14001 aimed atreducing water, electricity and paper consumption.

RETAIL BANkING: NEW MARkETSEGMENTS TARGETED

Significant growth of 29% in total bancassurancerevenue to MAd 1.7 billion -$198 m and €153 m -.

Enhanced services for Moroccans living abroad tosatisfy their changing needs such as E-transfert andcash to Account.

development strategy launched targeting the high-growth private client market segment.

BMcE direct, the bank’s remote banking serviceenhanced with the introduction of an onlinestockbroking service.

New services introduced dedicated to very smallenterprises such as Forfait TPE and crédit damaneExpress.

CORPORATE BANkING: A SuCCESSFuLSME STRATEGY GENERATING ADDTIONALVALuE

11.2% growth in corporate banking deposits to MAd 25 billion -$3 bn and €2.2 bn - and 4.3% growthin corporate loans to MAd 61.3 billion -$7.3 bn and €5.5 bn -.

coverage of SME banking market segment bolsteredthrough: (i) a more personalised products and servicesoffering and greater innovation e.g. Pack BusinessPME and club PME and (ii) closer relations with SMEcustomers by organising regional meetings.

Foreign trade business strengthened as can be seenin the 12% rise in import volumes and the 16% rise inexport volumes, registering a stronger pace of growththan the industry average (+7% and +4%respectively).

Market leadership in Project Finance consolidateddue to a number of large-scale deals in various sectors despite less than favourable businessconditions.

closer relations developed with corporate customerswith the opening of 3 new business centres in Nador,oujda and laâyoune.

INVESTMENT BANkING: MARkETCONDITIONS STILL uNFAVOuRABLE

BMcE capital Markets’ share of the private debt market rose to 53.2% due to aggressive sales approach and a differentiated product offering, resulting in the bank retaining its position as themarket leader.

Synergies derived between BMcE capital Bourse andcM-cic Securities as part of the African SecuritiesNetwork project with an agreement signed todistribute each other’s research products.

5% rise to MAd 33.5 billion -$4 bn and €3 bn - inBMcE capital Gestion’s assets under managementversus a 4.6% rise for the sector, resulting in increasedmarket share to 14%.

BMcE capital Titres’ volume of assets under custodystable and market share unchanged at 28% despite adecline in stock market volume in 2012.

PoSiTivE PERFoRMANcE By THE GRoUP’S iNdividUAl BUSiNESS liNESSTRoNG GRoWTH AcRoSS THE BoARd

CONSOLIDATED ACTIVITY: 47% RISE INNET INCOME ATTRIBuTABLE TO PARENTEXCLuDING EXCEPTIONAL ITEMS TO MAD 1.2 BILLION -$148 m and €112m-

9% rise in Net income Attributable to Parent to MAd 923 million -$109 m and €83m- despite morethan MAd 1 billion in provisions (MAd 1.1 billion;$131 m and €99m-).

47% rise in Net income Attributable to Parentexcluding exceptional items to MAd 1.2 billion -$148 m and €112m - exceptional net charge of MAd 323 million -related to taxation and the Socialcohesion contribution.

- A very strong performance by domesticactivities including (i) BMcE Bank SA whichsaw its contribution rise by 78% and (ii) theinvestment banking and assetmanagement division which registered a15% increase in its contribution to Netincome Attributable to Parent excludingexceptional items;

- Solid results from international activitieswith (i) a positive contribution fromEuropean subsidiaries, accounting for 4% ofNet income Attributable to Parent excludingexceptional items versus a negativecontribution the previous year and (ii) a30% rise in the contribution from sub-Sahara African activities.

11% rise in consolidated Net Banking income tomore than MAd 9 billion -$1bn and €809m- for thefirst time. This, together with a 6% rise in generaloperating expenses resulted in a 2.6 pointsimprovement in the cost-to-income ratio to 60.3%.

19% rise in gross operating income to almost MAd 3.6 billion -$425 m and €321m-in 2012 versusMAd 3 billion -$349 m and €270m-the previousyear due to a sustainable performance at theoperating level.

capital base strengthened with a 15% increase inshareholders’ equity attributable to parent fromMAd 12.4 billion -$1.4bn and €1.1 bn - in 2011 toMAd 14.3 billion -$1.7bn and €1.3 bn -in 2012following a MAd 1.5 billion -$180 m and €135 m -equity issue reserved for reference shareholders.The purpose was to provide adequate funds for theGroup’s strategic development domestically andoverseas and to meet new regulatory capitalrequirements.

Steady growth in the Group’s assets at 11% overthe past 4 years with total consolidated assets ofMAd 231 billion -$27bn and €21 bn -in 2012.

4% rise to MAd 144.6 billion - $17bn and €13 bn -in consolidated deposits and 14% increase toMAd 138.8 billion - $16bn and €12.5 bn -inconsolidated loans.

AGGREGATED ACTIVITY: DOuBLE-DIGITGROWTH IN THE MAIN INDICATORS

90% year-on-year rise in aggregated net income excluding exceptional items to more than MAd 1 billion -$119 m and €90m- and 31%rise from MAd 545 million -$65 m and €49m- in 2011 to MAd 713 million -$85 m and €64m - in 2012 after recognition of an exceptional tax expense.

13% rise to MAd 4.6 billion -$544 m and €412m-in aggregated net banking income due to a strongperformance by the bank’s core business as can beseen in an 11% increase in net interest income anda 9% rise in fee income.

contained growth in general operating expenses at5.5% resulting in a 4.3 points improvement in thecost-to-income ratio to 60.6%.

41% rise in gross operating income to MAd 1.8 billion -$209 m and €165m- due to asubstantial provisioning effort of almost MAd 712 million - $84 m and €64m - including aMAd 217 million -$26 m and €19.5m - sector-specific gross provision for general risks taking totalgross provisions for general risks to MAd 472 million -$56 m and €42.4m -.

Strong ability to attract savings with a 6% rise indeposits to MAd 107 billion -$12.7 bn and €9.6 bn- versus 2.7% growth in sector deposits resulting ina 43 basis point improvement in BMcE Bank’smarket share to 14.78%.

Strong momentum in lending with a 6% rise in totalloans to MAd 93.5 billion -$11 bn and €8.4 bn -,resulting in an 11 basis point improvement inmarket share.

IMPROVEMENT IN THE BANk’S SOLVENCYAND RISk PROFILE

core capital bolstered resulting in a Tier 1 capitalratio of more than 9% and a solvency ratio of morethan 12%.

40 basis point decline in the loan loss ratioto 4.53% which is below the sector average of 4.96%

improvement in the non-performing loan coverageratio from 67.4% in 2011 to 71.6% in 2012.

coNSolidATEd ANNUAl RESUlTS 2012

2012-2013 HIGHLIGHTS

Shareholding in Bank of Africa Groupincreased to 68%.

BoA granted banking licence in Togo.

BMcE Bank named “Best Trade Finance Bankin Morocco” by Global Trade Review as wellas “Socially Responsible Bank of the year”by African Banker Awards.

BMcE Bank international Plc awarded“African Project Finance – Transport deal ofthe year” by Euromoney.

MAd 1.5 billion -$180 m and €135 m - equity issue by BMcE Bank reserved formajor shareholders.

MAd 1 billion -$119 m and €90m-subordinated bond issue.

$75 million credit line obtained from theEuropean Bank for Reconstruction anddevelopment (EBRd) to refinance foreigntrade activities.

Spanish subsidiary BMcE Euroservicesestablished to take charge of the Moroccansliving Abroad business in partnership withthe domestic network in the context of theGroup reorganising its European platform.

BMCE BANk GROuP CONSOLIDATED ACTIVITY

231 MAd

208

+11%

20122011

Total Assets - In billion

1 246 MAd

850

+47%

20122011

Net Income Attributable to ParentExcluding exceptional items - In million

9 018 MAd

+11%

20122011

Net Banking Income - In million

3 583 MAd+19%

20122011

Gross Operating Income - In million

923 MAd850

+9%

20122011

Net Income Attributable to Parent - In million

3 016

8 140

2012 NET INCOME GROuP SHARE By GEoGRAPHic AREA

Morocco

Sub-Saharan Africa

Europe

51%

44%

5%

112€

148$

109$

1069$

425$

321€

20.7€

27.4$

83€

809€

Plaquette ANGLast.qxd:Mise en page 1 10/04/13 11:17 Page 2

SPECIALISED FINANCIAL SERVICES:RESILIENT PERFORMANCE DESPITE ANuNFAVOuRABLE ENVIRONMENT

MAGHREBAIL

6.3% growth in net outstandings versus 3% growthfor the sector resulting in a rise in market share from19.8% to 20.5%.

SALAFIn

6% rise in distributed loans against a fall in that of thesector with net income broadly unchanged at MAd 92 million -$11 m and €8.2 m - inclusive of a MAd 1.4 million -$170 k and €130 k - Social cohesioncontribution.

MAROc FAcTORInG

2012 was marked by a refocusing of activities on thecore business, full factoring, by outsourcing thecorporate client portfolio, reorganising sales andreducing costs in a highly competitive environment.

RM EXPERTS

Positive performance from BMcE Bank Group’s debtrecovery subsidiary with the volume of debt recoveredtotalling MAd 305 million -$36 m and €27.4 m - in2012 resulting in MAd 130 million -$15.4 m and €12 m - in provision write-backs.

SuB-SAHARAN AFRICAN ACTIVITIES:GROuP INCREASINGLY ANCHORED INAFRICA

BAnK OF AFRIcA

Solid consolidated results with 15% rise to € 291 million -$ 384 million- in net banking incomeand 13.6% increase to € 119 million -$ 157 million- ingross operating income.

Strong commercial performance with (i) 11% growthin customer deposits to € 3.2 billion -$ 4.2 bn- and20% increase to € 2.2 billion -$ 2.9 bn- in customerloans and (ii) 23% rise in customer portfolio to 1.4 million accounts.

BoA Group continues to grow organically with 32 newbranch openings taking the total distribution networkto 370 branches covering 15 countries.

Banking licence granted to Bank of Africa in Togo in2012,taking the total number of countries in whichthe Group has operations to 15.

LA cOnGOLAISE DE BAnQUE

Another positive financial performance in line withprevious years with a 17% rise to € 30 million -$ 39.7 million- in net banking income and a 16% riseto € 10.7 million -$ 14.1 million- in net income.

BAnQUE DE DEVELOPPEMEnT DU MALI

Significant growth of 21% to €12.7 million -$ 16.8 million- in net income at 31 december 2012.

EuROPEAN ACTIVITIES: RETuRN TOBREAk-EVEN

Recovery seen at BMcE Bank international Plc, theGroup’s london-based subsidiary, with net income of£ 1.2 billion, positive for the first time sinceestablishment, due to a major restructuringprogramme since 2011.

Satisfactory results from BMcE Bank internationalMadrid despite a difficult economic environment inSpain with net banking income stable at € 11 million-$ 14.5 million- and net income of € 3 million -$ 4 million-.

CSR AND SuSTAINABLE DEVELOPMENT:CONSOLIDATION OF SOCIALLY-RESPONSIBLE AND ENVIRONMENTALPRACTICES

BMcE Bank Foundation honoured by the awardsbestowed upon its President, dr leila MezianBenjelloun, in acknowledgment of her commitment topromoting Amazigh culture and human developmentincluding the Prix du Mérite de la culture Amazighe2011 from the Royal institute of Amazigh culture aswell as the Woman of the year 2012 prize from theAmerican chamber of commerce.

Expansion of the Medersat.com network to 174complexes, school and pre-school units following theopening of a school in imouzzer Marmoucha and thebuilding of an establishment in Bamako in Mali. Thistakes the total number of children educated and caredfor by the Foundation to 14,000.

Energico, Morocco’s first green product, introduced bythe corporate banking network, aimed primarily atSMEs to help them finance the purchase of energy-saving equipment.

Encouraging results which exceeded expectationsfollowing the implementation of iSo 14001 aimed atreducing water, electricity and paper consumption.

RETAIL BANkING: NEW MARkETSEGMENTS TARGETED

Significant growth of 29% in total bancassurancerevenue to MAd 1.7 billion -$198 m and €153 m -.

Enhanced services for Moroccans living abroad tosatisfy their changing needs such as E-transfert andcash to Account.

development strategy launched targeting the high-growth private client market segment.

BMcE direct, the bank’s remote banking serviceenhanced with the introduction of an onlinestockbroking service.

New services introduced dedicated to very smallenterprises such as Forfait TPE and crédit damaneExpress.

CORPORATE BANkING: A SuCCESSFuLSME STRATEGY GENERATING ADDTIONALVALuE

11.2% growth in corporate banking deposits to MAd 25 billion -$3 bn and €2.2 bn - and 4.3% growthin corporate loans to MAd 61.3 billion -$7.3 bn and €5.5 bn -.

coverage of SME banking market segment bolsteredthrough: (i) a more personalised products and servicesoffering and greater innovation e.g. Pack BusinessPME and club PME and (ii) closer relations with SMEcustomers by organising regional meetings.

Foreign trade business strengthened as can be seenin the 12% rise in import volumes and the 16% rise inexport volumes, registering a stronger pace of growththan the industry average (+7% and +4%respectively).

Market leadership in Project Finance consolidateddue to a number of large-scale deals in various sectors despite less than favourable businessconditions.

closer relations developed with corporate customerswith the opening of 3 new business centres in Nador,oujda and laâyoune.

INVESTMENT BANkING: MARkETCONDITIONS STILL uNFAVOuRABLE

BMcE capital Markets’ share of the private debt market rose to 53.2% due to aggressive sales approach and a differentiated product offering, resulting in the bank retaining its position as themarket leader.

Synergies derived between BMcE capital Bourse andcM-cic Securities as part of the African SecuritiesNetwork project with an agreement signed todistribute each other’s research products.

5% rise to MAd 33.5 billion -$4 bn and €3 bn - inBMcE capital Gestion’s assets under managementversus a 4.6% rise for the sector, resulting in increasedmarket share to 14%.

BMcE capital Titres’ volume of assets under custodystable and market share unchanged at 28% despite adecline in stock market volume in 2012.

PoSiTivE PERFoRMANcE By THE GRoUP’S iNdividUAl BUSiNESS liNESSTRoNG GRoWTH AcRoSS THE BoARd

CONSOLIDATED ACTIVITY: 47% RISE INNET INCOME ATTRIBuTABLE TO PARENTEXCLuDING EXCEPTIONAL ITEMS TO MAD 1.2 BILLION -$148 m and €112m-

9% rise in Net income Attributable to Parent to MAd 923 million -$109 m and €83m- despite morethan MAd 1 billion in provisions (MAd 1.1 billion;$131 m and €99m-).

47% rise in Net income Attributable to Parentexcluding exceptional items to MAd 1.2 billion -$148 m and €112m - exceptional net charge of MAd 323 million -related to taxation and the Socialcohesion contribution.

- A very strong performance by domesticactivities including (i) BMcE Bank SA whichsaw its contribution rise by 78% and (ii) theinvestment banking and assetmanagement division which registered a15% increase in its contribution to Netincome Attributable to Parent excludingexceptional items;

- Solid results from international activitieswith (i) a positive contribution fromEuropean subsidiaries, accounting for 4% ofNet income Attributable to Parent excludingexceptional items versus a negativecontribution the previous year and (ii) a30% rise in the contribution from sub-Sahara African activities.

11% rise in consolidated Net Banking income tomore than MAd 9 billion -$1bn and €809m- for thefirst time. This, together with a 6% rise in generaloperating expenses resulted in a 2.6 pointsimprovement in the cost-to-income ratio to 60.3%.

19% rise in gross operating income to almost MAd 3.6 billion -$425 m and €321m-in 2012 versusMAd 3 billion -$349 m and €270m-the previousyear due to a sustainable performance at theoperating level.

capital base strengthened with a 15% increase inshareholders’ equity attributable to parent fromMAd 12.4 billion -$1.4bn and €1.1 bn - in 2011 toMAd 14.3 billion -$1.7bn and €1.3 bn -in 2012following a MAd 1.5 billion -$180 m and €135 m -equity issue reserved for reference shareholders.The purpose was to provide adequate funds for theGroup’s strategic development domestically andoverseas and to meet new regulatory capitalrequirements.

Steady growth in the Group’s assets at 11% overthe past 4 years with total consolidated assets ofMAd 231 billion -$27bn and €21 bn -in 2012.

4% rise to MAd 144.6 billion - $17bn and €13 bn -in consolidated deposits and 14% increase toMAd 138.8 billion - $16bn and €12.5 bn -inconsolidated loans.

AGGREGATED ACTIVITY: DOuBLE-DIGITGROWTH IN THE MAIN INDICATORS

90% year-on-year rise in aggregated net income excluding exceptional items to more than MAd 1 billion -$119 m and €90m- and 31%rise from MAd 545 million -$65 m and €49m- in 2011 to MAd 713 million -$85 m and €64m - in 2012 after recognition of an exceptional tax expense.

13% rise to MAd 4.6 billion -$544 m and €412m-in aggregated net banking income due to a strongperformance by the bank’s core business as can beseen in an 11% increase in net interest income anda 9% rise in fee income.

contained growth in general operating expenses at5.5% resulting in a 4.3 points improvement in thecost-to-income ratio to 60.6%.

41% rise in gross operating income to MAd 1.8 billion -$209 m and €165m- due to asubstantial provisioning effort of almost MAd 712 million - $84 m and €64m - including aMAd 217 million -$26 m and €19.5m - sector-specific gross provision for general risks taking totalgross provisions for general risks to MAd 472 million -$56 m and €42.4m -.

Strong ability to attract savings with a 6% rise indeposits to MAd 107 billion -$12.7 bn and €9.6 bn- versus 2.7% growth in sector deposits resulting ina 43 basis point improvement in BMcE Bank’smarket share to 14.78%.

Strong momentum in lending with a 6% rise in totalloans to MAd 93.5 billion -$11 bn and €8.4 bn -,resulting in an 11 basis point improvement inmarket share.

IMPROVEMENT IN THE BANk’S SOLVENCYAND RISk PROFILE

core capital bolstered resulting in a Tier 1 capitalratio of more than 9% and a solvency ratio of morethan 12%.

40 basis point decline in the loan loss ratioto 4.53% which is below the sector average of 4.96%

improvement in the non-performing loan coverageratio from 67.4% in 2011 to 71.6% in 2012.

coNSolidATEd ANNUAl RESUlTS 2012

2012-2013 HIGHLIGHTS

Shareholding in Bank of Africa Groupincreased to 68%.

BoA granted banking licence in Togo.

BMcE Bank named “Best Trade Finance Bankin Morocco” by Global Trade Review as wellas “Socially Responsible Bank of the year”by African Banker Awards.

BMcE Bank international Plc awarded“African Project Finance – Transport deal ofthe year” by Euromoney.

MAd 1.5 billion -$180 m and €135 m - equity issue by BMcE Bank reserved formajor shareholders.

MAd 1 billion -$119 m and €90m-subordinated bond issue.

$75 million credit line obtained from theEuropean Bank for Reconstruction anddevelopment (EBRd) to refinance foreigntrade activities.

Spanish subsidiary BMcE Euroservicesestablished to take charge of the Moroccansliving Abroad business in partnership withthe domestic network in the context of theGroup reorganising its European platform.

BMCE BANk GROuP CONSOLIDATED ACTIVITY

231 MAd

208

+11%

20122011

Total Assets - In billion

1 246 MAd

850

+47%

20122011

Net Income Attributable to ParentExcluding exceptional items - In million

9 018 MAd

+11%

20122011

Net Banking Income - In million

3 583 MAd+19%

20122011

Gross Operating Income - In million

923 MAd850

+9%

20122011

Net Income Attributable to Parent - In million

3 016

8 140

2012 NET INCOME GROuP SHARE By GEoGRAPHic AREA

Morocco

Sub-Saharan Africa

Europe

51%

44%

5%

112€

148$

109$

1069$

425$

321€

20.7€

27.4$

83€

809€

Plaquette ANGLast.qxd:Mise en page 1 10/04/13 11:17 Page 2

STATUTORY AUDITORS STATEMENTIFRS CONSOLIDATED FINANCIALS

LIMITED REVIEW ATTESTATION OF THE CONSOLIDATED SITUATION AS OF DECEMBER 31st, 2012(This is a free translation of the original French text for information purposes only)

We have conducted a limited review of the consolidated situation of the Banque Marocaine du Commerce Extérieur and its subsidiaries (BMCE Bank Group) including the consolidated balance sheet, the consolidated income statement, the global income statement, the cash flow statement, the statement of changes in shareholders’ equity and a selection of explicative notes to the financial statements covering the period from January 1st to December 31th, 2012. This consolidated financial situation shows a consolidated shareholders’ equity of KMAD 18.413.529, including a consolidated net income of KMAD 1.579.754.

We conducted our limited review in accordance with the Moroccan Standards. Those standards require that we plan and perform the limited review in order to obtain a moderate assurance about whether that the consolidated financial statements mentioned above in the first paragraph are free from significant misstatement. A limited review consists essentially of interviews with the personnel of the company and the analytical review of the financial data; in thus provides a lower level of assurance than an audit. We did not carry out an audit and as a consequence, we do not express an opinion of audit.

Based on our limited review, subject to the impact of the situation described in the paragraph above, we did not identify any fact that makes us believe that the attached consolidated financial statements does not give a true and fair view of the results of the operations for the ended period, as well as the financial situation and assets of the BMCE Bank Group at December 31, 2012, in accordance with IAS/IFRS international accounting standards.

Without qualifying the conclusion expressed above, we draw your attention to note 2.7 which describes how the final outcome of tax audits of BMCE Bank which took as an effect the recognition in 2012 of a gross expense of KMAD 387.058.

Casablanca, March 22th, 2013

The Statutory Auditors

Faïçal MEKOUARPartner

Bachir TAZI Partner

8

1. CONTEXT

The application of IAS/IFRS is obligatory starting from the fiscal year 2008.

The paramount objective of the regulatory authorities is to provide credit institutions with an accounting framework in accordance with international standards in terms of disclosure and financial transparency.

BMCE Bank Group has adopted IFRS, approved by IASB to the consolidated accounts for the 2008 fiscal year compared to the 2007 fiscal year as well.

2. APPLICABLE ACCOUNTING STANDARDS

2.1. CONSOLIDATION

The scope of consolidation includes all domestic and foreign entities in which the Group has direct or indirect control. The consolidation method, i.e. full consolidation, proportional consolidation, and equity method, is respectively determined by whether the Group exercises exclusive control, joint control, or significant influence. However, joint ventures are consolidated using the proportional method or the equity method.

Options Adopted by BMCE Bank

Definition of the Consolidation Scope

BMCE Bank Group consolidates entities, regardless of their activity, in which it holds at least 20% of the voting power.

On the other hand, the Group consolidates entities meeting the following conditions :

• The subsidiary’s total assets is greater than 0,5% of the parent company’s ;

• The subsidiary’s net assets is greater than 0,5% of the parent company’s ;

• The subsidiary’s banking revenues are greater than 0,5% of the parent company’s ;

• Cumulated thresholds where the total of unconsolidated entities does not exceed 5% of the consolidated aggregate.

Exception

Any entity having a non significant contribution has to be consolidated if it holds stakes in subsidiaries which meet one of the conditions mentioned above.

2.2. TANGIBLE FIXED ASSETS

A tangible fixed asset is a long term asset held by the firm to be used for operations or lease.

Initial Recognition

Tangible fixed assets are initially recognised at purchase price plus directly attributable costs.

Subsequent Measurement

Subsequent to initial recognition, tangible fixed assets can be measured according to two methods :

• Cost method (recommended) : assets are measured at cost less cumulated depreciation and any impairment losses ;

• Reevaluation method (optional) : assets are measured

at fair value at the date of reevaluation less subsequent cumulated depreciation and any impairment losses. Fair value is the amount for which an asset could be exchanged, or liability settled, between knowledgeable, willing parties in an arm’s length transaction.

Reevaluation should be conducted on a sufficient regular basis so that the book value will not be significantly different from the fair value at the closing date.

Component-based Approach

Where an asset consists of a number of components that have different users or different patterns of consumption of economic benefits, each component is recognised separately and depreciated using an appropriate method to that component.

Depreciation rules

The depreciation of a tangible fixed asset is the cost of this asset less any residual value, which corresponds to the current value of the asset, taking into account its estimated age and condition over its useful life.

A tangible fixed asset is depreciated over its useful life, which corresponds to the period over which the entity expects to use this asset. The depreciation should reflect the consumption patterns of future economic benefits. The depreciation periods and methods have to be reviewed periodically by the firm, and hence the depreciation expenses for the current and future fiscal years must be readjusted.

Even if the fair value of the asset is greater than its book value, depreciation is recognised, as long as the residual value does not exceed the book value.

Impairment

The amount of impairment is the excess of the carrying value over the recoverable value, which corresponds to the highest value between the net disposal price and the value in use.

Impairment losses are recognised when there is an indication of impairment (internal or external), which has to be valued at the end of each fiscal year.

Options Adopted by BMCE Bank

Initial Recognition

The Group has chosen the cost method instead of the reevaluation method, as specified by IAS16. The entry cost of an asset includes borrowing costs incurred in compliance with IAS 23 (page 9).

Residual Value

Given the nature of BMCE Bank’s fixed assets, the Group did not retain any residual value, except for equipment transport of the subsidiary LOCASOM. Actually, there is no sufficiently active market or replacement policy over a period that is shorter than the asset’s useful life so that a residual value can be recognised.

Depreciation Period

The Group has adopted an identical depreciation scheme in the IAS/IFRS consolidated accounts.

accounting standards and principles applied by the group

9

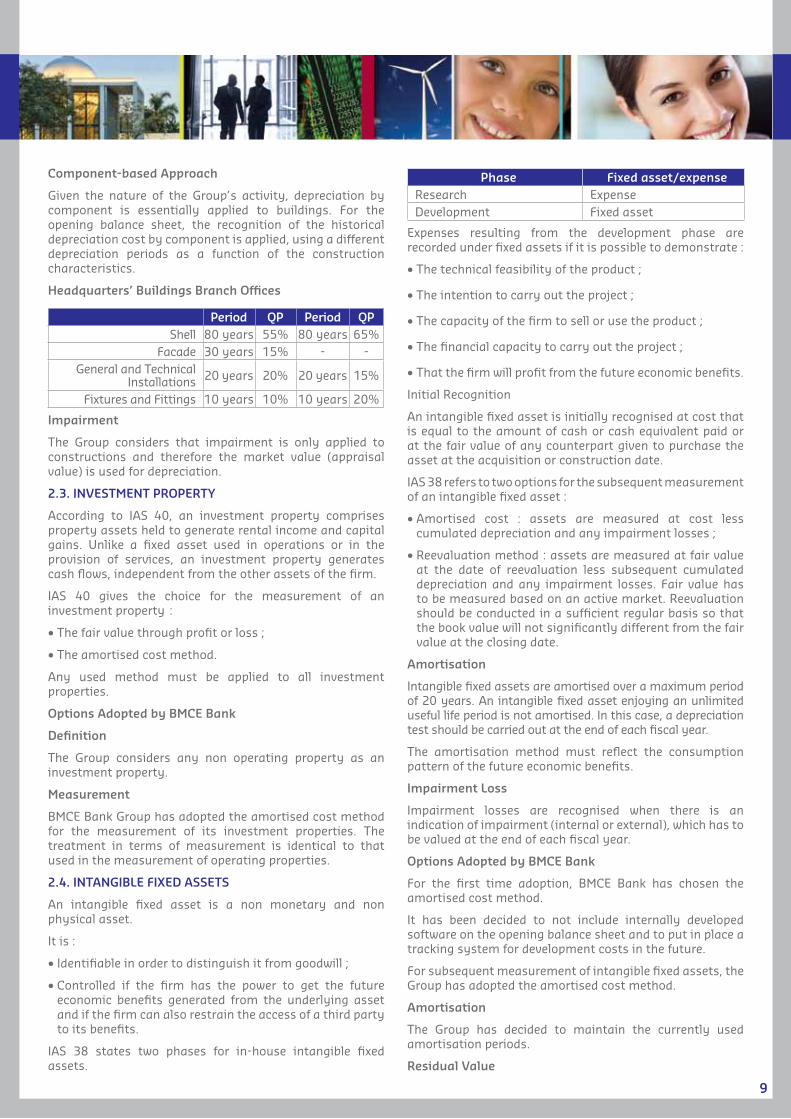

Component-based Approach

Given the nature of the Group’s activity, depreciation by component is essentially applied to buildings. For the opening balance sheet, the recognition of the historical depreciation cost by component is applied, using a different depreciation periods as a function of the construction characteristics.

Headquarters’ Buildings Branch Offices

Period QP Period QPShell 80 years 55% 80 years 65%

Facade 30 years 15% - -General and Technical

Installations 20 years 20% 20 years 15%

Fixtures and Fittings 10 years 10% 10 years 20%

Impairment

The Group considers that impairment is only applied to constructions and therefore the market value (appraisal value) is used for depreciation.

2.3. INVESTMENT PROPERTY

According to IAS 40, an investment property comprises property assets held to generate rental income and capital gains. Unlike a fixed asset used in operations or in the provision of services, an investment property generates cash flows, independent from the other assets of the firm.

IAS 40 gives the choice for the measurement of an investment property :

• The fair value through profit or loss ;

• The amortised cost method.

Any used method must be applied to all investment properties.

Options Adopted by BMCE Bank

Definition

The Group considers any non operating property as an investment property.

Measurement

BMCE Bank Group has adopted the amortised cost method for the measurement of its investment properties. The treatment in terms of measurement is identical to that used in the measurement of operating properties.

2.4. INTANGIBLE FIXED ASSETS

An intangible fixed asset is a non monetary and non physical asset.

It is :

• Identifiable in order to distinguish it from goodwill ;

• Controlled if the firm has the power to get the future economic benefits generated from the underlying asset and if the firm can also restrain the access of a third party to its benefits.

IAS 38 states two phases for in-house intangible fixed assets.

Phase Fixed asset/expenseResearch ExpenseDevelopment Fixed asset

Expenses resulting from the development phase are recorded under fixed assets if it is possible to demonstrate :

• The technical feasibility of the product ;

• The intention to carry out the project ;

• The capacity of the firm to sell or use the product ;

• The financial capacity to carry out the project ;

• That the firm will profit from the future economic benefits.

Initial Recognition

An intangible fixed asset is initially recognised at cost that is equal to the amount of cash or cash equivalent paid or at the fair value of any counterpart given to purchase the asset at the acquisition or construction date.

IAS 38 refers to two options for the subsequent measurement of an intangible fixed asset :

• Amortised cost : assets are measured at cost less cumulated depreciation and any impairment losses ;

• Reevaluation method : assets are measured at fair value at the date of reevaluation less subsequent cumulated depreciation and any impairment losses. Fair value has to be measured based on an active market. Reevaluation should be conducted in a sufficient regular basis so that the book value will not significantly different from the fair value at the closing date.

Amortisation

Intangible fixed assets are amortised over a maximum period of 20 years. An intangible fixed asset enjoying an unlimited useful life period is not amortised. In this case, a depreciation test should be carried out at the end of each fiscal year.

The amortisation method must reflect the consumption pattern of the future economic benefits.

Impairment Loss

Impairment losses are recognised when there is an indication of impairment (internal or external), which has to be valued at the end of each fiscal year.

Options Adopted by BMCE Bank

For the first time adoption, BMCE Bank has chosen the amortised cost method.

It has been decided to not include internally developed software on the opening balance sheet and to put in place a tracking system for development costs in the future.

For subsequent measurement of intangible fixed assets, the Group has adopted the amortised cost method.

Amortisation

The Group has decided to maintain the currently used amortisation periods.

Residual Value

10

Given the nature of BMCE Bank’s intangible fixed assets, the Group considers that the concept of residual value is not relevant and thus did not retain any.

2.5. SECURITIES

IAS 39 classifies financial assets into 4 categories, defined as a function of the management purpose.

Financial Assets at Fair Value Through Profit or Loss

It is classified under this category any financial asset meeting the following criteria .

It is considered a trading financial instrument because :

• It is acquired or contracted to be sold or purchased in the short term ;

• It is part of a portfolio made of distinct financial instruments, for which exists a recent effective pattern of retained earnings in the short term ;

• It is a derivative (except for hedging instruments) ;

• It is designated as so during its acquisition.

Financial instruments can be classified under financial assets or liabilities at fair value through profit or loss, except for equity investments for which an active market does not exist and thus the fair value cannot be precisely measured.

Derivatives are also classified as financial assets or liabilities at fair value through profit or loss, except for hedging instruments.

Accounting Principles

Initial Recognition

Financial assets at fair value through profit or loss must be initially recognised at acquisition price, excluding transaction costs directly attributable to the acquisition, and accrued interest on fixed income securities.

Subsequent Measurement

Securities in this category are measured at fair value. Changes in fair value are presented in the profit and loss account.

These securities are not subject to amortisation.

Held-to-maturity investments

Held-to-maturity investments are financial assets with fixed or determinable payments and fixed maturity that an entity has the intention and ability to hold until maturity. These securities do not include financial instruments initially designated as assets or liabilities at fair value through profit or loss or loans and receivables.

An entity cannot classify securities under held to maturity investments if it has, during the current fiscal year or during the two previous fiscal years, sold or reclassified before maturity a significant portion of these securities. This restriction is not applicable to disposals :

• Near maturity (less than three months) where a change in interest rates has no significant impact on the fair value of the securities;

• Occur after the accumulation of a substantial portion of the initial principal (about 90% of the asset’s carried amount);

• Attributable to an isolated and incontrollable event, which

could not be predicted ;

• Between the group entities (intra-group transactions).

An entity does not have the intention to hold a financial

asset until maturity if one of the following criteria is met :

• The entity intends to hold the financial asset for an

undetermined period ;

• The entity is willing to sell the asset as a response to

changes in interest rates or risks, to liquidity needs,

to changes in the availability and yield of alternative

investments, to changes in the funding base, and foreign

exchange risks ;

• The issuer has the right to pay for the financial asset an

amount that is well below its amortised cost.

Any entity does not have the ability to hold a financial asset

until maturity if one of the following two criteria is not met :

• It does not have adequate financial resources to continue

the financing of its held-to maturity investments ;

• It is subject to an existing legal constraint or other, which

could distrust its intention to hold the financial asset until

maturity.

Accounting Principles

Initial Recognition

Held to maturity investments must be initially accounted

for at acquisition price, plus transactions costs directly

attributable to the acquisition, and accrued interest on

fixed income securities (in a related receivables account).

Subsequent Measurement

Subsequent to initial recognition, held to maturity

investments are accounted for at amortised cost using the

effective interest method, which builds in amortisation of

premium or discount

11

Impairment loss

When there is objective evidence of measurable decrease in value, an impairment loss is recognised for the difference in the carrying amount and the estimated recoverable value.

The estimated recoverable value is measured through discounted future cash flows at the original effective interest rate.

Any subsequent decrease in the impairment loss is credited to the profit and loss account.

Loans and Receivables

Loans and receivables are assets rather than derivatives with fixed or determinable payments and which are not quoted in an active market. The following assets are not classified under this category :

• Assets that the entity has the intention to sell immediately or in the short term; these assets are classified under ‘‘assets held for trading purposes’’and financial assets at fair value through profit or loss ;

• Assets that the entity designates as available for sell ;

• Assets of which a significant portion of the investment could not be recovered for other reasons than the deterioration of the loan; these assets are classified under ‘‘available-for-sale financial assets’’.

Accounting Principles

Loans and receivables are recognised at amortised cost, net of provisions for impairment loss.

Impairment Loss

When there is objective evidence of measurable decrease in value, an impairment loss is recognised for the difference in the carrying amount and the estimated recoverable value.

Any subsequent decrease in the impairment loss is credited to the profit and loss account.

Available for Sale Financial Assets

These are financial assets other than derivatives, loans and receivables, held to maturity investments, or financial assets at fair value through profit or loss.

Accounting Principles

According to IAS 39, the accounting principles for ‘‘available for sale financial assets’’ are as follows :

Initial Recognition

Available for sale financial assets are initially recognised at the acquisition price plus transaction costs directly attributable to the acquisition, and accrued interest on fixed income securities (in a related receivables account).

Subsequent Measurement

The changes in the fair value of these securities are recognised in shareholders’ equity. On disposal or on recognition of an impairment loss, unrealised gains and losses on fixed income securities are taken to the profit or loss account, using effective interest method.

Impairment Loss

When there is objective evidence of measurable decrease in value for equity securities, or the occurring of credit risk for debt securities, unrealised capital losses are transferred from shareholders’ equity to the profit or loss account.

Any subsequent decrease in the impairment loss is credited to the profit and loss account for debt securities, but not for equity securities. Any positive change in the fair value of the latter will be recognised in the shareholders’ equity, whereas any negative change in the fair value will be accounted for in the profit or loss account.

Options Adopted by BMCE Bank

BMCE Bank Group has chosen a classification as a function of the intention of management and the nature of securities.

The portfolio is made of the following securities :

• Equity investments ;

• Trading securities ;

• Regulated securities

Securities

Classification

These securities are classified as available-for-sale financial assets, recognised at fair value.

Valuation

Listed securities : the reference value is the last stock price.

Unlisted securities : the fair value is measured according to internal models.

Impairment Loss

Listed securities : decrease by 20% in the stock price over the last 6 months ;

Unlisted securities : according to impairment indications for the monitoring of provisioning.

Trading Room

Classification

The purpose of management is defined in accordance with the future management of the Trading Room. At the opening balance sheet, the securities managed under the trading room were essentially for trading purposes.

Valuation

Listed Securities : the fair value corresponds to the market share.

Unlisted Securities : the fair value is measured according to an internal model.

Regulated Securities

These securities are classified as held-to-maturity financial assets.

2.6. IMPAIRMENT

Portfolio Impairment

If there is no objective evidence of impairment, whether it is

12

significant or not, the financial asset is included in a portfolio of securities having the same credit risk characteristics to be collectively assessed.

Indication of Impairment

In a portfolio assessment, an objective evidence of impairment can be reduced to observable events indicating a measurable decrease in the estimated future cash flows of a group of loans, since the initial recognition, although this decrease can be associated with the different loans making this portfolio :

• Adverse changes in the capacity of borrowers ;

• A national or local economic situation correlated to the default payment on the assets of the portfolio.

Individual Impairment

An impairment loss is recognised when there is objective evidence or several objective indications of a decrease in the value of loans, including:

• Significant financial difficulties of the issuer or the debtor ;

• A breach in the contract resulting from a default payment (interest or principal) ;

• The granting by the lender to the borrower, for economic or legal reasons related to financial difficulties, of a facility that the lender did not expect in other circumstances ;

• The increasing likelihood of bankruptcy or other restructuring of the borrower ;

• The disappearance of an active market for that financial asset following financial difficulties, or ;

• Observable events indicating a measurable decrease in the estimated future cash flows of a group of financial assets, since the initial recognition, although this decrease can be associated with every single asset in the portfolio :

- Adverse changes in the solvency of borrowers ;

- A national or local economic situation correlated to the default payment on the assets of the portfolio.

Impairment Method

IAS 39 does not distinguish different methodologies for the assessment of individually and collectively impaired assets.

Instead, the only principle is to provision the excess of the book value (carrying amount) on the recovered value.

The recoverable value is the present value, discounted at the effective interest rate, of the estimated future cash flows of the asset (or a group of assets).

An impairment loss is recognised when there is an evidence of a measurable decrease in the value (impact on the cash flows of the asset).

Given the valuation technique of recoverable values under IFRS, companies must be able to correlate the observed objective evidence of impairment and its impact on the expected cash flows of the portfolio.

Impairment Loss

Under IFRS, the amount of impairment is the difference between the carrying amount and the recoverable value, which corresponds to the present value of the estimated recoverable cash flows, discounted at the effective interest rate.

Options Adopted by BMCE Bank

Portfolio Impairment

Only an observable decrease in value is subject to impairment according to IAS 39. Expected losses are not subject to impairment.

As for portfolio impairment, BMCE Bank has identified a certain number of criteria for the analysis of the behavior of loans and receivables, and their categorisation in types of anomalies that will be used for the constitution of homogenous groups of assets.