Blue Fuel #16 | October 2012 | Vol. 5 | Issue 3

33

Alexander Medvedev: Gazprom's Strategy in Asia Gazprom Export Global Newsletter October 2012 | Vol. 5 | Issue 3 Page 16 Page 11 Page 5 Gazprom and Gail Deal on LNG Supply The Golden Age of Methane in Transport is Inevitable © Gazprom Export www.gazpromexport.com | [email protected] +7 (499) 503-61-61 | [email protected] BLUE FUEL

-

Upload

gazprom-export -

Category

Documents

-

view

214 -

download

0

description

Gazprom Export Global Newsletter

Transcript of Blue Fuel #16 | October 2012 | Vol. 5 | Issue 3

Alexander Medvedev: Gazprom's Strategy in Asia

Gazprom Export Global NewsletterOctober 2012 | Vol. 5 | Issue 3

Page 16

Page 11

Page 5

Gazprom and Gail Deal on LNG Supply

The Golden Age of Methane in Transport is Inevitable

© Gazprom Export

www.gazpromexport.com | [email protected] +7 (499) 503-61-61 | [email protected]

BLUE FUEL

Ý Ê Ñ Ï Î Ð Ò

BLUE FUELGazprom Export Global Newsletter

Publishers Contact Info:www.gazpromexport.com | [email protected] +7 (499) 503-61-61 | [email protected]

To Our Readers: The Risks of Politicizing Europe’s Gas Market ........................Pg. 4

Alexander Medvedev: Gazprom's Strategy in Asia ..................Pg. 5

Russia and Slovakia Celebrate 50 Years of Energy Cooperation ..............................................................Pg. 8 Macedonia: 20 Years of Partnership and Still Going Strong ...Pg. 8

Blue Corridor Through Europe: NGVs Demonstrate Advantages of Clean and Affordable Fuel ................................Pg. 9

The Golden Age of Methane in Transport is Inevitable .........Pg. 11

Gazprom and Summa Group to Develop Global LNG Market for Marine Fleet Bunker Fuel......................................Pg. 13

The Face of Gazprom in Asia .................................................Pg. 14

Gazprom and Gail Deal on LNG Supply .................................Pg. 16

Gazprom Energy Tops Customer Satisfaction Rankings for Large Gas Users ...............................................Pg. 17

Russia, Energy Dialogue with Europe and WTO: A Chance Not to Be Missed ...................................................Pg. 17

Natural Gas as the Fuel of Choice From the European Gas Forum Perspective ..........................................................Pg. 19

Energy and Leadership ..........................................................Pg. 21

Will Shale Gas Disrupt the European Gas Market? ...............Pg. 24

Energy Policy and the Hungarian Economy ..........................Pg. 25

Developing a Partnership Between Wind and Gas ................Pg. 27

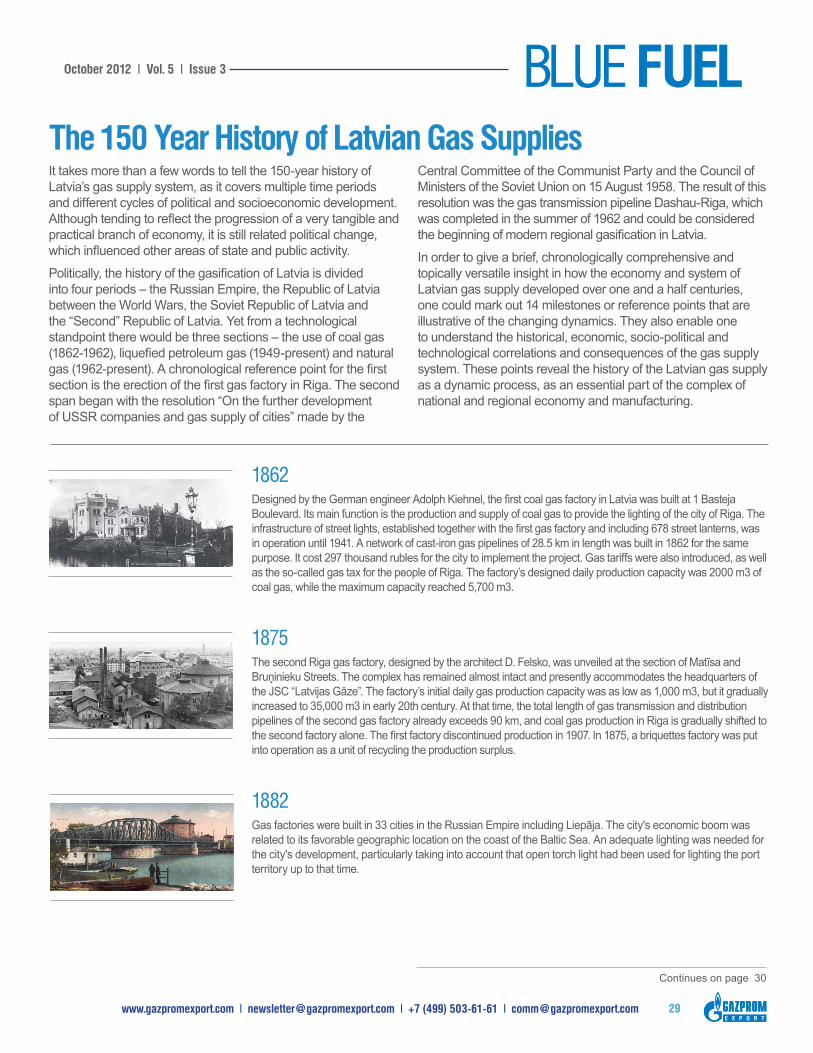

The 150 Year History of Latvian Gas Supplies ......................Pg. 29

Europa Park Hosts Russian Festival–2012 ...........................Pg. 32

“Energy for Life” and the Power of Art ..................................Pg. 32

In this issueOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

4

The recent launch of an antitrust investigation by the European Commission against Gazprom has triggered unwarranted media speculation and in some cases outright Schadenfreude. This obscures the real facts around the case.

Although this is not the first – and probably will not be the last – investigation of its kind undertaken by the EU against energy companies, this move cannot be regarded as standard procedure. Many have been surprised by the statement of the Commission that “unfair” gas prices might have been imposed “by linking the gas price to the oil price” – which gives the case an entirely different dimension way beyond Gazprom and could affect the whole gas industry.

Long-term gas supply contracts are standard business practice across all of Europe’s major natural gas suppliers, as is linking the gas price to a basket of oil products. The oil-peg provides price stability and predictability, and prevents any major supplier from manipulating the gas price. Enforcing gas-to-gas pricing would render Europe’s gas market entirely unattractive for investors. Plus, European hub prices are a mere derivative of oil-indexed gas prices; the tail cannot wag the dog.

Some have argued that the primary motive behind the EU’s investigation may not really be to establish a level-playing field and enforce competition in the region, as EU officials have argued, but rather to pressure Gazprom to lower its prices – which incidentally are the result of commercial negotiations among companies. This is the way the EU plans to get cheaper energy which already, in the form of shale gas, enviously serves as a stimulus for the recuperation of the US economy. If the end game is to dictate gas prices by EU decree, then the Commission should say so. Russians know from their own painful history that arbitrary administration of the economy brings about adverse results.

Regardless of whether the suspicion of political overtones in Brussels’ scrutiny is founded or unfounded, it remains a controversial issue in the context of relations between the EU and Russia, adversely affecting if not their substance, certainly the psychological climate in which they are conducted.

Gazprom’s business activities on EU markets are in full conformity with legal standards applied by other natural gas producers and exporters, also where price formation mechanisms are concerned. Gazprom duly noted the statement by the European Commission that the opening of proceedings does not imply that Gazprom has acted in breach of the EU competition rules.

The charges of alleged obstruction of competition on the European gas market on the part of Gazprom are strangely out of touch with reality. In fact, it may be argued that Gazprom virtually pioneered the liberalization of the European gas market. Back in the 1990s, the company made initial attempts to independently access end-users, but consistently faced resistance from local players who have continued to block access to transport capacities.

According to the decree signed by President Vladimir Putin in the wake of the EU’s announced investigation, “strategic companies” like Gazprom have the right to disclose information about their operations to foreign countries, companies and regulators only with prior consent of an authorized Russian federal body. This rule covers cases related to changes in long-term contracts with foreign counterparties, including clauses on pricing and other key terms and conditions. It does not preclude us from continuing our cooperation with the European Commission, however.

And, for the record: Gazprom has always been true to its commitment to cooperate in good faith with the European Commission and remains committed to proceed with this interaction for the sake of constructive dialogue.

TO OUR READERS: The Risks of Politicizing Europe’s Gas Market

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 5

As a native of Sakhalin, I am immensely pleased that the Gazprom Group has been tasked by the Russian Federation government to implement the Eastern Gas Program, which was adopted in September 2007. Our task is to create “a united system of gas production, transportation and gas supply with the possibility of gas exports to the markets of China and other Asia-Pacific countries” as well as in Eastern Siberia and the Russian Far East.

Progress is well underway. In eastern Russia, gas production centers have been established in Krasnoyarsk, Irkutsk, Yakutsk, Sakhalin and Kamchatka, and the first in the Far East interregional gas transmission network "Sakhalin-Khabarovsk-Vladivostok." Construction of major gas pipelines to China and possibly South Korea (via North Korea) are also planned. In the Far East, we are planning to increase production capacity for producing and exporting LNG, primarily to the Asia-Pacific Region (APR).

According to most projections, the average annual growth rate of consumption of natural gas in APR will be 3.3%, and will reach 660 bcm from 2012 to 2035. The main growth will come from China and India. The appetite for energy commodities could further increase with Japan's plan to phase out nuclear power generation.

Natural gas is expected to become the fuel of choice for Asia. It has a great future as a motor fuel, and as vehicle sales grow in the region, so too does the consumption of gasoline and diesel. We also see great prospects for natural gas in the form of LNG as a fuel for ships, especially with regard to the role of maritime transport in the region. This work in Asia, in essence, has not even begun.

India is another important market, as it has one of the most dynamic economies in the world and is home to one-sixth of the world's population! In early August of this year, a large part of its territory with a population of 600 million people, suffered a series of unprecedented power cuts – “blackouts.” This was caused by overloading of the grid in the face of ever-growing demand. Although the immediate crisis has subsided, organizations around the Indian capital still must work in an environment where, for 80% of the time, they have no energy. Companies are forced to keep large supplies of expensive oil and other fuel and electricity generators to maintain the health of their production. Gasification is the key to solving this problem. Gazprom recognizes the potential here and is working to develop closer fuel-relations with India. Gazprom recently signed a contract with GAIL, which provides for the delivery of 2.5 mt of LNG for 20 years in India via Gazprom Marketing and Trading Singapore.

There will come a time when Gazprom's export strategy will be equally split between the western and eastern vectors, with comparable profits received from Europe and Asia. Currently, however, Europe accounts for 65% of all Gazprom gas exports, and Asia is far behind. It is in the interests of Gazprom, to accelerate the development in Asia-Pacific based on the conditions of the regional gas markets.

What attracts us to the Asia-Pacific Region (or APR)? It already accounts for over 18% of global natural gas

Alexander Medvedev: Gazprom's Strategy in Asia Key notes from the speech at the Sakhalin Oil and Gas 2012 international conference (24 September 2012)

Continues on page 6

6

consumption. According to statistics, in 2011, the region used more than 600 bcm. Many countries in the APR are forced to satisfy their energy needs partially and sometimes completely, by imported raw materials. The focus group of profitable customers are South Korea, China, India, Taiwan, Thailand, Singapore and the largest importer of natural gas in the world (in the form of LNG), Japan. The total imports of these countries in 2011 amounted to 239 bcm.

Already, the APR is a premium market which is willing to pay more for gas than on the trading floors in the U.S. and Europe. Gas is a substance which, as Gazprom folklore says, moves from areas of higher pressure to areas of maximum profit.

JapanLast year's tragedy at the nuclear Fukushima power plant forced the Japanese government to reconsider the possible directions of energy development.

Apparently, the total cessation of nuclear generation in Japan is being considered.

This will have enormous implications for the market. Japan is the fourth largest country in the world in terms of energy consumption, while it has few of its own energy resources. Gas consumption in the country is about

80 bcm a year. Gas has a 14% share of the energy consumption in Japan. The country imports nearly 100% of its gas as LNG, ranking it first in the world for imports.

In 2011, Japan was supplied with 8.5 mt of LNG more than in 2010. For the 12 months between April 2011 to April 2012, the demand for LNG in Japan increased by 18% and will likely grow even more. The share of gas in the energy balance of Japan is also growing. Given the strong demand for LNG, Japanese partners are involved in the feasibility study on the construction of LNG plant near Vladivostok.

The Japanese market has considerable appeal for us because of both its geographical proximity, which reduces transportation costs, and the high solvency of its consumers. Here you can think and look beyond the current vectors of interaction.

ChinaChina has a special place in our Asian growth strategy. China’s need for natural gas is projected to exceed 300 bcm per year by 2020. There are ongoing negotiations between Gazprom and China regarding details of supplies and prices for Russian pipeline gas deliveries of up to 68 bcm through two corridors. The variants

Alexander Medvedev: Gazprom's Strategy in AsiaContinued from page 5

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 7

of enhanced cooperation, in particular in the field of building underground gas storage facilities in China, as well as the development of shale gas are being studied – although it is too early to make decisions on these issues.

What hinders the conclusion of an agreement on the supply of Russian pipeline gas to China? The issue is price. It should not be calculated to the detriment of the supplier. Some are urging Gazprom to quickly negotiate a deal under the concept of “charitable pricing” – yet this would mean that we would be essentially granting subsidies to the Chinese economy, the second largest economy in the world and the owner of the largest foreign exchange reserves. This strategy makes no sense.

China is counting on the future production of its own shale gas reserves. In our view, the active development of these reserves will allow the Chinese partners to evaluate the high cost of such production and, consequently, lead to the market reform of gas pricing. This can speed up agreement with Gazprom Group on supply price parameters. In general, the price increase should not affect the rate of inflation too much: in 2011, the share of natural gas amounted to only 5% of China's energy mix; by 2015 it is expected to be 7%.

The authors of a recent study by Bank of America Merrill Lynch expect an increase in gas prices in China by 80%, as the government encourages the production of shale gas. The bank predicts that by 2016 the price of gas will be up to $11.4 per mBtu, while the cost of shale gas to be produced in China will not fall below $8.5 per mBtu. Following a price adjustment in-line with the market, Gazprom will have an improved bargaining position, so the time for China to compromise is approaching.

The Korean PeninsulaAbout a year ago a "road map" that will deliver 10 bcm of natural gas to the Republic of Korea by pipeline through the territory of the DPRK was signed. The first deliveries are scheduled to begin in 2017. A joint working group established by Gazprom and KOGAS is working on the agreed route.

Consultations with technical experts are being held in order to determine the best solutions for the future union of gas transportation systems between Russia and South Korea.

The ideas behind the pipeline look very difficult to implement, especially given the complex political-military context continuing on the Korean peninsula, and the obvious political risks. However, if there is political will and a mutual commitment, this project could take place, strengthening not only energy, but also military and political security in this rather turbulent region.

Apart from the three named countries — China, Japan and South Korea — other Pacific Rim countries are already included in or are preparing to be included in the number of buyers of Gazprom gas. We consider as inevitable the increase in gas consumption in India, Pakistan, Bangladesh, Thailand, and Vietnam. As demand fluctuates in some regions, India and China take in the extra LNG volumes contracted for other markets. In particular, the volume of LNG from the Sakhalin-2 project contracted by Gazprom group for supply to the U.S., was delivered there.

We should also mention the use of LNG as motor fuel. Asian countries are actively involved in this process. In China in 2010, 150 thousand vehicles running on natural gas were launched. In China, the total number of vehicles using CNG and LNG in 2012 will reach 1.1 million units, and in 2015 it is expected to increase to 3 million units.

The natural gas vehicle revolution could also occur in the sea and in the future rail and even air transport. This course of development is both environmentally oriented and economically feasible.

The evaluation of the economic growth in Asia-Pacific countries, the structure of energy consumption, and the interest in the majority of countries in the reduction of CO2 emissions allow us to predict the steady growth in demand for natural gas. This means that there are opportunities to promote the exports of Gazprom Group on these markets, primarily, LNG and pipeline gas.

8

Russia and Slovakia Celebrate 50 Years of Energy Cooperation

Macedonia: 20 Years of Partnership and Still Going Strong

Bratislava recently hosted celebrations dedicated to several different occasions highlighting Gazprom’s positive and longstanding relationship with Slovakia. This includes the 50th anniversary of the launch of the Druzhba (Russian for “Friendship”) oil pipeline, the 45th anniversary of the first blue fuel shipment from the former-USSR to the former-Czechoslovakia and the 40th anniversary of the launch of the Eustream A.S. gas transit pipeline system.

The festivities were attended by the Deputy Chairman of the Gazprom Management Committee and Director General of Gazprom Export Alexander Medvedev, the Slovakian Minister of Economy Tomáš Malatinský, the Russian Ambassador to Slovakia Pavel Kuznetsov, the Vice-President of the European Commission Responsible for Inter-Institutional Relations and Administration Maroš Šefčovič, the Managing Director of the Slovak Oil and Gas Union Ján Klepáč, members of Parliament and CEOs of Slovak companies.

The events demonstrated how Gazprom values Slovakia as a major partner. Although gas volumes purchased by the country for domestic consumption are relatively small, it may surprise some to learn that Slovakia is the second largest transit operator of Russian gas after Ukraine.

In November 2008, a contract was signed stipulating the shipment of up to 6.5 bcmpa of Russian gas to Slovakia, as well as gas

transit westward of up to 50.0 bcmpa. In 2011, Gazprom provided Slovakia with 5.89 bcm for its own use and pumped exactly 47.38 bcm across its territory.

There was an understandable concern on the part of the Slovak partners regarding what would become of these contracts once Nord Stream begins running at full steam and later is complemented by South Stream’s delivery system. However Medvedev assured Slovakia: “All our contract commitments will be honored. Gas transit across Slovakia is protected by the ‘ship-or-pay’ clause. You can feel certain that you will not be left without the transit fees.”

The participants at the celebratory events noted with satisfaction that a mutually beneficial partnership between Gazprom and Slovakia was crucial for the security of gas supplies to European customers and also made an important contribution to the overall development of positive Russian-European relations.

“We observe the objective changes in the European gas market and are ready to deal with them. But at the same time we are confident that there are things and principles that must be preserved intact irrespective of price fluctuations or the emergence of new gas sources. These are principles of free competition, non-discriminatory approach, abidance by legal norms,” Medvedev emphasized.

Some 20 years have passed since Gazprom entered into a mutually beneficial partnership with Macedonia.

In 1982, we signed a long-term agreement on Russian natural gas deliveries with Makpetrol A.D. for a period of 15 years. After the construction of a gas pipeline was completed and it was officially opened in September 1997, the first blue fuel supplies started to flow into Macedonia.

“We place high importance on the cooperation with the countries of South East Europe

and in particular with Macedonia,” head of representative office of Gazprom Export in Skopje Sergei Ikonnikov said. He reminded the audience that in the time span of 20 years Macedonia received more than 1.0 bcm of Russian natural gas. The volumes of gas delivered to Macedonia are only set to increase as the local gas industry grows.

New vistas will be opened if a portion of the South Stream pipeline links to Macedonia.

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 9

Ý Ê Ñ Ï Î Ð Ò

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

9

Blue Corridor Through Europe: NGVs Demonstrate Advantages of Clean and Affordable FuelFrom 8 to 24 September, Gazprom and its German partner E.ON Ruhrgas joined forces to promote the sixth Blue Corridor NGV Rally, which featured natural gas vehicles (NGVs) driving across Europe in an effort to expose the public to the benefits of natural gas as motor fuel.

Some 15 cars, buses and trucks were parading across Europe, setting off from Moscow and making brief stays in the cities of Orsha, Minsk, Brest, Warsaw, Ostrava, Prague, Mannheim, Paris, Brussels, Essen, Berlin and Poznan. Along the 6,700 kilometer-long route, the rally organizers held a number of round table discussions, where rally participants and invited experts demonstrated to the public why methane is the most abundant, clean, safe and affordable transportation fuel.

The rally capitalized on the growing number of natural gas refueling stations, which increased dramatically in the last seven years – reaching some 4,000 in Europe, with 900 in Germany alone. The network has enabled more than 1.5 million vehicles to run on gas in Europe. Experts believe that from the existing 16 million vehicles on the road today, by 2020 up to 50 million NGVs will be consuming 200 bcm of natural gas annually worldwide.

The flagship event was held in Brussels on September 17 with European Union officials participating in an open and proactive discussion of the benefits of NGVs. The roundtable and the exhibition event held at Brussels’ iconic Autoworld museum hosted over 110 guests in attendance, including Gazprom and E.ON top management, representatives of the European Commission, and the leaders of Natural Gas Vehicles Association (NGVA) Europe and NGVA Russia.

Continues on page 10

10

All speakers pointed out the challenges for NGVs, such as the infrastructure deficit with not enough filling stations so far in EU. Heinrich Hick from the office of the European Energy Commissioner Oettinger pointed out that the benefits natural gas offers would help Europe meet the emissions targets set out in EU’s 2050 Energy Roadmap. Director from DG Move Olivier Onidi noted that natural gas is definitely among the future fuels for transport in Europe and that gas filling infrastructure will also be considered in the new call for proposals of EU energy infrastructure projects. Participants also noted that the perception is still that electricity (e-mobility) is a cleaner technology than gas — although that is mostly due to better PR spinning campaign.

Gazprom’s Board member, head of gas transportation, underground storage and utilization department Oleg Aksyutin, presenting the results of NGV development in Russia, stressed the importance of regulation that can serve as game-changer in the NGV development, illustrating it with the case of Russia. Gazprom is fully committed to continue supplying Europe with whatever gas amount is necessary

to further promote the use of gas both in transport and shipping, Aksyutin concluded.

The regulation issues were prominent on the agenda at each roundtable. In Warsaw, the need for Polish government support was defined as one of the key factors enabling the growth of the natural gas vehicles market in Poland. In Prague, the participants also called for clear rules of the game to be set: although it does not necessarily mitigate the tax burden, it still allows for the predictability and long-term planning.

In Berlin, Gazprom Germania’s hometown, the key message brought up by all panelists amounted to the following: framework conditions have to be improved. Existing tax reprieves for natural gas are

Blue Corridor Through Europe: NGVs Demonstrate Advantages of Clean and Affordable FuelContinued from page 9

How Many Kilometers Can You Drive On 10 Euro?

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 11

The Golden Age of Methane in Transport is InevitableBy Evgeny Pronin, Executive Director of the National Gas Vehicle Association

Global economic growth can be illustrated by the increase in a number of indicators. According to various international institutions, the world’s population will increase by 58% (from 6 to 9 billion people) between 2000 and 2050; automobilization (the number of cars per 1,000 inhabitants) will increase by

50%. Growth in energy consumption, including in the transport sector, could grow by 100%-130%.

This economic growth is associated with an increase in negative risk factors, with potential environmental and economic consequences that include the following:

• global emissions of CO2 could more than double by 2050 to about 60 GW;

• maintaining the 1% annual growth trend for the price of oil may lead to its increase to $145 to $150 per barrel.

Environmental and economic imperatives are forcing the global economy to engage in a constant search for new alternatives to conventional petroleum-based motor fuels.

Substituting petroleum products with alternative energy sources can reduce the share of oil in the global fuel mix from 32% in 2010 to 24% in 2050, while natural gas is expected to

due to end in 2018 but they should be prolonged until 2025 and be complemented by additional incentives to ensure the much needed investments. The further development of the European Energy Taxation Directive should also be considered.

Another regulatory solution that could make life easier could be the introduction of correct labeling: now, consumers buy natural gas vehicles because they are eco-friendly and natural gas is up to two times more affordable than diesel. But the price for natural gas at the pump station is dispensed on a cents-per-kilogram basis, which is confusing for consumers and needs to be changed for transparent and uniform labeling scheme for natural gas as a fuel (in liter-equivalent).

Nota bene: natural gas itself is the cheapest carburant it allows drivers to save about 30 percent of fuel costs compared to diesel and about 50 percent of petrol costs.

The synergy of natural gas with biomethane and other renewables as practical transportation fuel is not less worth emphasizing at all levels. Gas industry, for its part, should keep on pioneering the development of on- and off-grid natural gas filling infrastructure, and provide supportive policy to get positive response from businesses. And from the side of vehicle manufacturers, more positive engagement policy is expected. Expanding the range of factory-built NGVs in order to meet more stringent and extensive environmental regulations, granting them deserved promotion status, and

offering high-quality technical support to customers will bring additional impulse to the all industries involved.

Driving NGVs is good for the planet because natural gas-powered engines emit 25 percent less carbon dioxide compared to petrol, produce 95 percent less nitrogen oxide, generate almost no particular matter and do not produce any soot at all. Recent proposals will mandate manufacturers to reduce average CO2 emissions of their car fleets, providing an incentive for the adoption of low-carbon technology, including NGVs. Euro 6 vehicle standards, applicable from 2015 will also strictly cap emissions of nitrogen oxide, which will greatly favour natural gas over petrol and diesel and lead to improved air quality. On the other hand, this will contribute to attractiveness of NGVs, imposing higher standards on traditionally-fueled cars thus making them more expensive, while the price of NGVs remains the same.

Blue Corridor rally, hopefully, has inspired European industries and citizens, demonstrating that running on gas is convenient, cost effective and environmentally beneficial, and encouraging more and more NGV users to travel on the clean and cheap blue fuel throughout Europe.

Learn more about the Blue Corridor Rally: www.bluecorridor.org

Continues on page 12

12

increase from 22% in 2010 to 27% in 2050 – thereby helping to achieve both climate-based and economically-driven goals.

What kind of alternative fuels – specifically fuel alternatives – and technologies in the transport sector, can we speak of with confidence? They are known: hybrid schemes, biofuels, electricity, hydrogen, and gas fuel – LPG and methane. Of course, the list of fuel alternatives for transport is not limited to vehicles. However, this article considers only this type of use.

CH4 – methane (compressed and liquefied), regardless of source of origin: natural gas, shale gas, biomethane, coalbed methane, e-gas (synthetic methane), etc.;

Biomethane (compressed and liquefied), regardless of source of origin;

Petroleum products – diesel fuel, gasoline, jet and marine fuels

LPG – liquefied petroleum gas

Electricity – (batteries and contact wire)

Hybrid – hybrid schemes

H2 – hydrogen technologies

Each type of motor fuel has a completely different level of market readiness, scope of application, environmental cleanliness, pricing attractiveness, etc. Assessing selected commercial properties of each type of fuel enables their overall evaluation and ranking.

What are these properties, what do they imply, and how does natural gas compare?

Applicability – the possibility of using that fuel for vehicles of different categories and purposes: natural gas is used in all types and classes of vehicles.

Resources – security of resources for that fuel: natural gas reserves will meet the world's needs for another 250 years.

Cleanliness – compliance with increasingly stringent environmental requirements:

The Golden Age of Methane in Transport is Inevitable Continued from page 11

methanePetroleum products

LPG Electricity Hybrid H2CH

4Biomethane

Applicability 5 5 5 3 1 2 1

Resources 5 5 2 2 3 3 5

Cleanliness 5 4 3 4 3 3 5

Price 5 2 2 3 2 2 1

Readiness 5 3 5 5 5 3 1

Infrastructure 3 4 5 4 3 5 1

Sustainability 4 3 1 1 3 1 5

Independence 4 2 4 4 4 2 1

Integrated rating 1.0 0.97 0.94 0.92 0.92 0.81 0.75

1 32 4 5

Worse Better

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 13

natural gas is the most environmentally friendly of all motor fuels available for commercial sale; methane enables a 50% reduction in CO2 emissions and 80% in NOx.

Price – the average retail price of compressed natural gas is equal to half the price of petroleum products; natural gas is the cheapest of all motor fuels available for commercial sale.

Readiness – the degree and stage of productization; natural gas is available for commercial sale in more than 80 countries around the world.

Infrastructure – the level of development of filling stations: methane is available at nearly 21,000 filling stations.

Sustainability – the possibility of obtaining this type of fuel from other sources or synthetically at affordable prices: methane can be regarded as a renewable energy source since it can be produced from biomass or synthetically.

Independence – the ability to introduce the fuel into the market without government support; such support for natural gas is desirable but not a must, as is the case with other – political – alternatives.

The following table reflects a peer assessment of the commercial attractiveness of each alternative fuel for use in the global transportation segment.

The conclusion can be presented as follows: At present and in the future, the most optimal kind of motor fuel, from all points of view, is methane, the main source of which is and will remain natural gas.

Methane has the unique feature of combining all environmental, technical and commercial advantages simultaneously. No other fuel offers such a combination.

It can be argued that the golden age of methane intransport is inevitable. In 2011, world consumption of natural gas by vehicles was estimated at 35 to 40 billion cubic meters. According to various forecasts, by 2035 the global fleet of gas-cylinder cars will range from 30 to 190 million units – from 2% to 10% of the world’s total vehicle fleet – with natural gas consumption between 60 and 380 billion cubic meters per year.

This in turn allows for adding another criterion to those previously mentioned: investment attractiveness. In the coming years, it is likely that the market for methane in transport may grow 10 times (!). This is a very significant volume, considering this fuel’s consumption by water and rail transport. Simple arithmetic shows that, at May 2012 prices, the world gas engine market may reach up to 400 billion euros on the gas component alone.

The time is ripe for investment in the market for gas motor fuels.

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Gazprom and Summa Group to Develop Global LNG Market for Marine Fleet Bunker FuelIn September 2012, Deputy Head of the Gazprom Management Committee Alexander Medvedev and President of Summa Group Alexander Vinokurov signed a Memorandum of Understanding stipulating cooperation in the use of liquefied natural gas (LNG) as a bunker fuel for marine fleets, including those belonging to and operated by Summa Group.

Initially, Gazprom and Summa Group will study opportunities for cooperation in the region of the North and Baltic seas. Aside from supplying LNG for the needs of Summa Group, the parties will also consider the possibility of developing bunkering infrastructure in the basin of the Baltic and North seas, including LNG storage facilities.

Further, the parties will consider the possibility of expanding cooperation into the Black Sea, Mediterranean and Pacific, regions where Summa Group also operates its fleet and possesses well-developed harbor infrastructure.

“The strict mandatory emission limitations that will be imposed after 2015 for the vessels operating in the Baltic and North

Seas are a crucial factor in switching to alternative fuel. Only natural gas fully complies with the emission limits for marine motors without need for expensive filters and has price advantages over low-sulfur petrochemicals. The vessel, motor and storing technologies for the LNG-fueled fleet are available and proven. Cooperation with the Summa Group has a strong potential,” Alexander Medvedev noted.

“Due to the joint efforts of Summa Group as an infrastructure operator and Gazprom as the world’s biggest natural gas producer, a real breakthrough will be achieved. I am sure it will provide a long-term positive impact on the environmental effects of marine transport, not only in our country but also globally, and will provide a new standard for the whole industry,” Alexander Vinokurov said.

Summa Group is a Russian-based diversified private holding joining assets in port logistics, engineering, construction, telecommunications and the oil and gas sectors. Summa Group is active in almost 40 regions of Russia and abroad.

The Face of Gazprom in AsiaBy Serguei Edrenkine, General Director, Gazprom Marketing & Trading Singapore

In late 2009, when Gazprom Marketing & Trading decided to pursue a commercial opportunity in Asia by dispatching, almost overnight, one member of its staff to Singapore, no one anticipated that the bold move would result in a successful office in the city-state being established during a short span of three years.

From one staff member, to three, and now 64 employees of 16 nationalities, Gazprom Marketing & Trading Singapore (GM&TS) has not only grown its team, but has also developed a robust business and raised the profile and brand of its parent company in the short time it has had a presence in the region. GM&TS was originally envisioned as an office to market the liquefied natural gas (LNG) cargoes from Sakhalin in Asia Pacific. But it has expanded its initial operations as a platform for LNG trading and shipping to originating carbon reduction projects and trading in liquefied petroleum gas (LPG) and foreign exchange.

GM&TS closed its first full year of operations with a portfolio of 19 Master Trading Agreements, providing access to a large selection of Asian sellers and buyers. It executed the first direct sale of Russian gas to an Indian energy player, and completed the sale of a number of cargoes into Taiwan, again marking the first Russian gas sales into the country – contributing to the final count of 27 cargoes delivered by the team that year.

Being in the heart of the action, of course, has helped. Demand for LNG in Asia Pacific has increased steadily during recent years

and is forecasted to reach 400 million tonnes in the next 10 years. Having a physical office in the region, close to the sources of demand, means GM&TS can respond and optimize cargoes better and faster.

Today, GM&TS has 30 Matched Sale-Purchase Agreement (MSPAs) in place and has firmly established Gazprom’s marketing and trading presence in the premium LNG markets of the region. Some of its other achievements include building a diversified portfolio of carbon projects with 140 Clean Development Mechanism (CDM) projects worldwide, 80 percent of which are in Asia and more than half originated out of Singapore, as well as Shipping & Logistics being recognized as a center of operational excellence with ISO 9001:2008 accreditation.

More notable, however, is the fact that GM&TS has grown the capability of its team not just in the front office but across key support functions such as finance, risk and legal. This enables it to be a valuable part of a network – together with the London headquarters and other GM&T offices around the world – that offers global presence, 24/7 trading, and a comprehensive suite of products, from gas and electricity marketing, trading and supply to energy management solutions and carbon deals.

Much of GM&TS’ success has to be attributed to collaboration. It is fortunate to have key members from Gazprom’s management on its board of directors – Pavel Oderov, Head of International Business Department, OAO Gazprom; Elena Burmistrova, Deputy Director General for Oil, Petroleum and Petrochemicals, Gazprom Export; and Andrey Biryulin, Managing Director, Gazprom Germania – who provide direction and leadership and also facilitate connections within its Moscow headquarters and the wider Gazprom group.

Since its early days, GM&TS has fostered a relationship with Gazprom’s representative office in Beijing, which was instrumental in providing GM&TS introductions to counterparties in China.

14

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 15

In addition, its efforts to form mutually beneficial partnerships within the group was bolstered early this year with the establishment of LNG Working Groups to investigate and further opportunities for collaboration with Gazprom Exploration & Production International.

Singapore has proved to be a very advantageous location for GM&T’s first office in the region. With its dynamic business environment, highly supportive government, and a burgeoning LNG trading market – the country is constructing its first LNG terminal due to be completed in 2013 and its energy and business agencies are actively developing the country into an energy trading hub – GM&TS has found that its arrival as one of the nation’s earliest LNG traders has helped it carve a position as a leading LNG player in the region as well as allowed it to nurture excellent relationships with the government and energy agencies.

In October 2011, GM&TS moved from the serviced offices it had been operating out of since 2009 into permanent premises in a brand-new office building – another milestone in the office’s young history. With the availability of physical space for the company’s further expansion, GM&TS is greatly focused on the future and its continued growth.

Diversification will be very much the theme for GM&TS’ next goal. In addition to building security of LNG supply through a variety of sources, the management team is also concentrating its efforts on diversifying the scope of its business. While LNG will always be a major part of its portfolio, GM&TS is also concentrating on developing its other businesses such as

Clean Energy and moving into other areas of growth for the long term sustainability of the business.

At the heart of GM&TS’ approach is the recognition that its remit is to create value for the Gazprom group through innovative products and solutions for the energy markets, and to be the face of Gazprom in Asia Pacific.

This representation of Gazprom is not limited to the commercial realm only. In May this year, with support from Gazprom, GM&TS organized a concert featuring renowned Russian violist Yuri Bashmet and world famous chamber orchestra the Moscow Soloists in Singapore. The concert was part of the chamber orchestra’s 20th anniversary world tour, which was sponsored by Gazprom Export.

It was well attended by partners from the region’s major energy companies, representatives from government agencies and members of the Russian diplomatic community, marking a successful brand building and networking event. In line with Gazprom Export’s commitment to supporting social and charitable activities for cultural development, education and sport, partial proceeds from tickets sales were donated to a local charity that offers theatre experiences to underprivileged children.

The event – along with similar concerts in Shanghai, Beijing and Tokyo – generated considerable positive coverage in the local and regional media and emphasized Gazprom’s standing as a leading global energy company with a solid commitment to corporate social responsibility.

16

Gazprom Energy Tops Customer Satisfaction Rankings for Large Gas Users

In 2006, Gazprom Energy acquired Pennine Natural Gas Limited to start direct sales to commercial and industrial customers in the United Kingdom. Soon after it became the second largest supplier in terms of volume, listing some of the largest gas consumers in the UK as its customers. Gazprom Energy’s market share has grown rapidly, now accounting for more than 14 percent of gas volume sold to B2B customers. Now it has culminated its rise by topping the Datamonitor customer satisfaction rating.

Gazprom Marketing and Trading Singapore and Gail Sign 20-Year LNG Supply DealGazprom to supply GAIL 2.5 million tonnes of LNG per annum for 20 years

Gazprom Marketing and Trading Singapore (GM&TS), a 100% wholly-owned subsidiary of Gazprom Marketing & Trading, has signed a legally binding 20-year liquefied natural gas (LNG) sales and purchase agreement (SPA) with GAIL (India) Limited (GAIL), following the signing of an earlier Basic Framework Agreement (BFA) by the two companies on 18 May 2011.

Under the terms of the agreement, GAIL will receive 2.5 million tonnes of LNG per annum of LNG (equivalent to approximately 130 million MMBtu or 3.5 bcm or 122 bcf per annum) over a period of 20 years.

LNG will come from Gazprom’s production facilities, optimised and supplemented by GM&T’s global trading portfolio and capabilities. Under the contract, LNG will be sustainably priced with an oil-indexed formula and delivered to Dahej, Dabhol and Kochi terminals in India.

This agreement is a key milestone for both GAIL and Gazprom, reaffirming both their strong corporate partnership in developing India as one of the core markets for LNG business and the Indo-Russian trade relationship.

Vitaly Vasiliev, CEO of Gazprom Marketing & Trading, said: “We are delighted to have signed this agreement with GAIL, during a period of rising demand for LNG in India. We are looking forward to working together with GAIL to help meet India’s expanding gas demand whilst securing a long-term market for Russian gas.” He continued, “We recognise GAIL’s strength as the major gas player within India, enabling flexible access to a rapidly developing market and are confident that this SPA will further strengthen our already well-established LNG trading relationship.”

Commenting on the development, B. C. Tripathi, Chairman & Managing Director,

GAIL (India) Limited said, “This long-term LNG supply agreement with Gazprom, which holds the world’s largest gas reserves, is another milestone in Indian–Russian Energy Cooperation. The deal with Gazprom reinforces GAIL’s commitment to facilitate the development of the Indian market for which US$6 billion in investments are being made by GAIL in creating Natural Gas infrastructure. The deal also marks our efforts to create a well-diversified and secured supply portfolio to meet the ever growing energy requirements of the Indian economy and enable sustainable long-term growth for GAIL.”

About GAIL (India) LimitedGAIL (India) Ltd., is India's principal Natural Gas Company with activities ranging from Gas Transmission and Marketing to Processing (for fractionating LPG, Propane, SBP Solvent and Pentane); transmission of Liquefied Petroleum Gas (LPG); production and marketing of Petrochemicals like HDPE and LLDPE and leasing bandwidth in Telecom sector. GAIL has extended its presence in Power, Liquefied Natural Gas (LNG) re-gasification, City Gas Distribution and Exploration & Production areas through equity and joint venture participations. GAIL registered a turnover of US$7.9 billion and profit after tax of US$708 million for the year 2011-12.

GAIL owns and operates over 9,500 Km of high pressure cross country natural gas pipeline network and can handle 175 mmscmd. The company is in the process of significantly augmenting its pipeline network to reach every part of India. Within the next two to three years, GAIL will have a pan-India natural gas pipeline infrastructure spanning over 14,500 km and can handle volumes over 300 mmscmd. To secure import of LNG, GAIL is at an advance stage of commissioning 5 MMTPA LNG Terminal

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 17

Russia, Energy Dialogue with Europe and WTO: A Chance Not to Be MissedBy Dr. Rainer Seele, Chairman of the Board of Directors of Wintershall

The Russian parliament recently ratified an agreement on Russia’s accession to the World Trade Organization (WTO) and President Vladimir Putin has signed it into law. All the formalities

have now been completed, and on 22 August Russia became a full-fledged member of the WTO. This event may form the basis for growth in the Russian economy during the coming years. But first, Russia and the EU should use this opportunity to forge a closer relationship and achieve a higher level of trust in their challenging energy dialogue.

Russia and Europe already have a long history of cooperation and have reaped economic benefits from this relationship. The European Union is Russia's main trading partner, and European countries are investing significantly in the Russian economy. For more than 20 years, I have been observing the development of relations between Russian and German businesses, and trade between our countries continues to grow: in 2011, it reached a new peak, as German exports to Russia increased by 40%. Today, more than 6,000 German companies are active in Russia, and Germany is the largest foreign investor in Russia.

Businesses in Russia and the EU are well aware of each other's strengths and weaknesses. This is reflected in the successful

of RGPPL (a JV of GAIL) at Dabhol on the Western Coast of India. GAIL ’s Natural Gas Pipeline from Kochi is at an advanced stage of commissioning its phase-I which connects to Kochi LNG Terminal. Recently, GAIL has been authorised to lay 1550 km natural gas pipeline from Western to Eastern Coast – Surat to Paradip Pipeline project.

Besides, GAIL has also set up a wholly- owned subsidiary company GAIL Global (Singapore) Pte. Ltd. in Singapore for sourcing LNG, and petrochemicals.

For further information please visit: www.gailonline.com

Gazprom Energy Tops Customer Satisfaction Rankings for Large Gas UsersFor the first time, Gazprom Energy reached the top of the Datamonitor’s Energy Buyer Customer Satisfaction Survey, which is for large gas users.

Gazprom Energy, one of the “granddaughters” of Gazprom Export and a 100% subsidiary of Gazprom Marketing & Trading, keeps “dislodging” competitors, as Datamonitor phrased it.

Datamonitor noted that “independent suppliers in the energy market are performing extremely well in terms of growing market share and maintaining high levels of customer satisfaction.”

In 2006, Gazprom Energy acquired Pennine Natural Gas Limited to start direct sales to commercial and industrial customers in the United Kingdom. Soon after it became the second largest supplier in terms of volume, listing some of the largest gas consumers in the UK as its customers. Gazprom Energy’s market share has grown rapidly, now accounting for more than 14 percent of gas volume sold to B2B customers. Now it has culminated its rise by topping the Datamonitor customer satisfaction rating.

Continues on page 18

history of our joint projects in the fields of energy, engineering, construction, and other industries. But there are difficulties as well: a recent example can be cited from the natural gas industry: it has been announced that through 2015, the tax on mineral extraction in Russia will increase several fold, which automatically makes all planned gas projects less attractive to foreign investors. Therein lies the main problem that now faces business in Russia: the ever-changing "rules of the game." Each year it becomes increasingly difficult to plan long-term investments in Russia.

At the same time, the conditions for investment in Russia have never been more favorable. Russia is one of the top three countries in the world in terms of gold and currency reserves, and it is not burdened by significant debt, with external borrowings equivalent to just 10% of GDP. In the current climate, this is an extremely favorable fiscal situation. Russia also boasts significant intellectual resources: over 70% of young Russians have a college degree, and they not only understand the need for change but have the motivation to become the driving force behind it.

How Russia utilizes these opportunities depends in part on its new, but already very familiar government, from which real political and economic changes are expected. Accession to the WTO can play a very useful role here. By becoming a member of the WTO, Russia is undertaking a public commitment to carry through changes in the socio-political and economic life of the country. A reduction in customs duties would help counteract customs bureaucracy. Russia's integration into the international system of regulated trade will reduce the political risks for its foreign partners. And, generally speaking, Russia's WTO membership will improve the business climate and expand the planning horizon, which can only serve to attract more investment.

Russia’s accession to the WTO will create an organization whose member countries

produce around 85% of the world’s oil and gas. No other global industry club can boast this kind of resource base. A significant reinforcement of the energy component within the WTO should help create a better environment for the energy dialogue between Russia and the European Union. On the one hand, thanks to unique infrastructure projects such as Nord Stream and South Stream and the joint exploitation of huge fields like Yuzhno-Russkoe, Russia has a stable reputation as a reliable energy supplier. On the other hand, Europe is apprehensive about new energy transit crises and is demanding even more supply guarantees from Russia. Russia, for its part, is unhappy with restrictive directives such as the Third Energy Package. These have an impact on long-term contracts with energy suppliers and cast doubt on the economics of those very same infrastructure projects. However, these are the only solution to the transit problems and the sole means of ensuring energy security. Therefore, the WTO could become the formal structure within which Europe and Russia can synchronize their efforts to build an energy dialogue. Priority should be given to joint action in three main areas: creating a favorable investment climate, developing infrastructure and implementing joint modernization processes.

However, no partnership can be a one-way street. While counting on change in the business climate in Russia, the EU must be ready to reciprocate with measures to bring down the barriers on its side. As foreign investors, we rightly demand guarantees for our investments in Russia, but tend to forget that Russian companies are entitled to demand the same for their European investments. Europe must ensure equal conditions for all foreign investment partners. And what better way to begin than by reforming the visa regime, which would send a clear signal of openness and trust.

Hence, Russia's accession to the WTO is a chance for Europe to start negotiating a new agreement on cooperation between

18

Russia, Energy Dialogue with Europe and WTO: A Chance Not to Be MissedContinued from page 17

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 19

our countries, which will form the basis of discussion for new arrangements in respect to visas, free trade and partnerships, not only in the field of energy supplies, but also in the exchange of technology, expertise and project management experience.

Growing business cooperation must, in turn, be accompanied by a strengthening of ties between our societies. Ultimately, Russia and Europe are two parts of one whole: Politically, economically, and culturally.

Natural Gas as the Fuel of Choice From the European Gas Forum PerspectiveBy Philippe Miquel, Chief of Staff of GDF SUEZ, Global Gas & LNG

The European Gas Forum (EGaF) is an informal initiative of eight major energy companies including Centrica, E.On-Ruhrgas, Eni, Gazprom Export, GDF SUEZ, Qatar Petroleum, Shell and Statoil. The organization is designed to exchange views on the promotion of natural gas, with a focus on Europe. Participants do not reflect on any of their own points of view in particular, as the forum is intended to be a discussion about various global viewpoints, on the basis of economic analysis.

The forum is composed of major industry players from many countries, representing each part of the value chain, whilst keeping the group small enough to be efficient and effective. Since there was no pre-existing place or organization to foster the exchange of complementary perspectives, the EGaF focuses on specific topics of common interest, such as the promotion of natural gas, large gas producers (eg Gazprom, Qatar Petroleum and Statoil) and European energy suppliers,. Rather than establishing a permanent secretariat, with the associated bureaucracy and costs, our intention was to take pragmatic and focused actions. Company senior executives were to be directly involved to address the issues around natural gas targeted at the highest level of stakeholders.

The EGaF was initiated during the summer of 2010 to contribute to the on-going debate on the EU “Roadmap for a low carbon economy” going forward to the year 2050. Despite its inherent advantages, at the time natural gas was assessed as being unreasonably ignored in the debate, particularly with respect to the evolution of the energy mix until 2050, led by the European Commission.

In October 2009, the European Council set a clear target in terms of greenhouse gas emission reductions. The objective was to decarbonize the European economy by 80% to 95% by 2050 in comparison to 1990, aiming to limit global warming to 2°C. Although there was a political agreement on the objectives and on the need to control global warming, there was no consensus on how to get to this point. Yet, the choices that Europe was about to make with respect to the energy mix in the light of 2050 objectives, were to have a significant impact for years to come and also for the overall competitiveness of the European economy as a whole.

There was an abundance of alternatives presented at the time. While meeting the CO2 objectives, these alternatives varied in vastly different ways. Some of them promoted the sole use of renewable energy, others insisted on the benefits and reliance of nuclear energy, and a majority were geared a higher electrification of the energy mix.

Very few of these analyses addressed the issue of costs for the overall economy and for society as a whole. Furthermore, natural gas was seldom considered as a possible fuel of choice. The benefits of natural gas were largely ignored by policy makers and EU-leaders. The fact that natural gas is not only a sound environmental alternative but also cost-effective was clearly overlooked.

For the European Gas Forum, it was important to contribute to the discussions and ensure that the role of natural gas was correctly reflected or that its potential contribution to meeting the stated EU objectives was, at the least, adequately assessed. It was also important to demonstrate the potential role of natural gas in the construction of a

Continues on page 20

20

Natural Gas as the Fuel of Choice From the European Gas Forum PerspectiveContinued from page 19

balanced European energy mix, alongside other energy sources, and to highlight the issues of cost and moral hazard in ongoing debates.

As industrialized economies, we also needed to position gas more effectively as an intrinsic part of a longer term alternative.

As a first step, EGaF fielded a study titled “Making the Green Journey Work” that covers all sectors of the European economy. The main focus is on power generators but other sectors are also included, albeit covered in less detail. The study provides a technical analysis of the contribution that natural gas can make to meeting CO2 emission reductions as targeted by the EU. It builds on scenarios outlined in the European Climate Foundation (ECF) Roadmap 2050 and describes three potential ways to achieve the 80% emissions abatement targets by 2050.

The first conclusion of the study was that Europe should refrain from mandating specific technologies as part of setting CO2 emission targets for the period until 2050. The benefits of this strategy were outlined to lead to significant cost savings, maintaining European competitiveness, and hence put no restraint on economic growth. Two reasons fermented the aforementioned conclusion. First, there is considerable predictive uncertainty which new technologies will be readily available 30-40 years from now, and at what cost. Second, flexibility is needed to deliver a low carbon energy mix which will be cost efficient during the period in question. The other conclusion of the study was that Europe should rely on existing mature technologies at first and gradually move into new technologies (such as carbon capture & storage and others) at a later stage, once the feasibility and their performances were better established. This would allow new

technologies to come to maturity and have a lower impact on costs.

Compared to the reference scenario (i.e., 60% RES scenario of the ECF Roadmap 2050), the alternatives proposed by EGaF achieve significant cost savings to meet CO2 reduction targets, by using natural gas in a more balanced energy mix, that relies less on coal and less on higher cost renewable technologies. For the period 2010-2030, total costs savings in the power sector could be in the vicinity of €250-500 bn. This is about half the investment needed in this sector by 2030. Additional savings of a similar magnitude are also possible for the period between 2030 and 2050, although costs are much more uncertain given the uncertainties in terms of investment costs in that time frame.

Natural gas enjoys the lowest cost of capital compared to other power generation schemes that are capable of meeting emissions goals. Combined-cycle gas plants emit half as much CO2 per kilowatt-hour as modern supercritical coal plants and they are two-to-three times less capital intensive. While operating costs are low, renewables can be very expensive both in start-up capital costs and transmission grid impact costs. Nevertheless, we do see a significant role for lower cost renewables as part of a cost-efficient future energy generation mix. The study demonstrates that EU emission goals could be met by utilizing slightly less of the more expensive renewables, compared to the higher renewable utilization scenario, particularly with respect to the next 20 years. If adopted natural gas-fired generation will normally be the lowest cost source of back-up thermal generation required to complement intermittent renewables (such as wind power) and help maintain energy supply security.

Hence, adopting alternatives as outlined by the study between 2010-2030 would

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 21

Energy and LeadershipBy Eric Dam, president of the Energy Delta Institute

Energy plays a crucial role in supporting our modern way of life. In spite of significant progress in the efficiency of its use, energy consumption will continue to rise as income levels grow and increased access to energy is guaranteed to an ever growing population. In order to meet growing global energy demand, the energy sector has to work hard to overcome numerous challenges. Exploring the unknown area’s for new gas, energy transition, CO2 reduction, market liberalization, and the need for new and different infrastructure services are but a few of the challenges that lay ahead. It will be up to future executives and leaders of the energy industry to meet and resolve these issues. This will require skills, knowledge and expertise in an ever more complex industry.

To identify what skills and competences are needed to become a successful executive in the energy industry, the Energy Delta Institute (EDI) conducted a market survey

Continues on page 22

provide Europe with more time to select and fine-tune its carbon abatement plans by 2050. Policy support should be reasonably even-handed across a range of low carbon energy technologies (which include but are not limited to renewables) for providing additional “start-up” support for emerging technologies which promise a competitive cost of CO2 abatement in due course.

EGaF is exploring the residential and the transportation sectors in more detail with two additional studies. The residential study was made public on 19 July, while publication of the transportation study will soon follow. Both studies highlight the potential cost savings to meet the 2050 CO2 emissions targets through a higher reliance on natural gas technologies.

In the residential sector adopting a more diverse technology mix that include gas fuelled heat pumps, gas-fired District Heating and Combined Heat and Power (CHP) could lead to cost savings in the order of €100-120bn compared to a higher electrification pathway by 2030. In the transportation sector, an increased reliance on natural gas powered vehicles (particularly an increased use of LNG as a bunkering and heavy trucking fuel) could also lead to significant savings (in the order of €60-70bn, to 2030) while remaining on track to meet the EU Transport White Paper’s 2050 GHG reduction targets.

These two complementary approaches show how a lower-cost, lower-risk, and low-carbon energy mix for Europe can be achieved based on cost-effective and technology neutral CO2 mitigation solutions, combining necessary actions on climate change with secure and affordable access to energy.

EGaF has met on several occasions with EU Commissioner Oettinger and representatives of DG Energy to present its results. It also met with other stakeholders of other gas organizations such as Eurogas, IGU, Gas Naturally, or NGO’s such as ECF, Greenpeace, WWF. It has received very positive feedbacks and gained some significant momentum in the debate over the future of the energy mix in Europe.

In terms of perspectives for natural gas in Europe, it is fair to say that things have changed significantly over the last two years. The impact of Fukushima and the economic downturn have shed a new light on the energy future of Europe. Leaving options open, relying on a balanced energy mix and ensuring that we avoid unnecessary costs to the economy are now being addressed more prominently.

Natural gas now has a much brighter future perspective, although a lot remains to be done, particularly with respect to ensuring that natural gas remains a competitive energy source. In the light of abundant due to the unconventional gas revolution, increased diversity of supply and efficient technological solutions, we are confident in the tremendous opportunities of growth that natural gas offers in the short and long term.

At EGaF, we like to think that part of this effort is due to the extensive work done by our members. Yet, challenges remain and EGaF intends to continue to be part of the debate.

To learn more, please visit http://europeangasforum.eu/

22

Energy and LeadershipContinued from page 21

amongst a number of industry leaders.40 CEO’s and top managers from the industry, a.o. from BP, Chevron, Dong, EON, Eni, Essent, GasTerra, Gasunie, Gazprom, Qatar Gas, Shell, South Stream and Total, participated in this survey and shared their opinion. In this article, besides highlighting survey results, I will also shed some light on my own vision on strong leadership.

Leadership: A definitionIt is evident that we need strong leadership in order to overcome the challenges we are facing in the industry. But how do we define competent leadership? If we check the dictionary on leadership, it tells us that one of the meanings is ‘the capacity or ability to lead or give direction.’

Before I became president of the Energy Delta Institute, I was a member of the executive board of N.V. Nederlandse Gasunie, where I was also responsible for construction and maintenance. Being responsible for of one of the largest departments of Gasunie, I was ‘giving direction’ to a team of several hundreds of employees.

Golden rules in project management and leadershipFor all department activities both in the past and in the present, I always apply four ‘golden rules’. The first one is safety. In our business safety is priority number one. The second rule is budget equals budget. This means always sticking to the defined budget. Sticking to the budget instils confidence by external parties. Rule number three is scope control. It is of great importance to determine the scope, based on what you know today and expect to be true in the future. If and when situations change, you have to assess the effect of these changes on all aspects of the project, like time and budget. Delivering on time is the fourth golden rule I apply as a manager. In my work I also apply another, not so formal rule, which I think is very important for a great team atmosphere, which is: work hard and have fun.

Strong leadershipIn my opinion, giving direction to a large team of employees doesn’t automatically mean you are a skilled leader. You can’t judge yourself whether you are a good leader or not. This is something only others can say about you. Being a good leader means that you are able to let others excel in everything they do, and that others respect you for doing so.

Some people believe that a good leader should have the full package of sector knowledge – both of the entire energy value chain and in-dept knowledge – and possess excellent skills, competences and expertise. I disagree. In my opinion, good leadership means you are able to build a good team around you. With a fine sense of diversity, you are able to establish a team in which all knowledge and competences needed to get the job done are covered. When you are able to surround yourself with such a team, and know how to inspire them in order to let them excel, you have proven strong leadership. Of course you should have a sound fundamental knowledge of technology and sector developments, and also develop and experiment a broad view on different business processes during your career. But establishing a winning team also means being able to identify personal skills and interests, both internally and externally. It means mastering the art of stakeholder management.

‘A great person attracts great people and knows how to hold them together’

–Johann Wolfgang Von Goethe

During the 25th World Gas Conference in Kuala Lumpur, Malaysia, the first copy of our ‘leadership’ report, written by energy analyst Marius Popescu, was handed over to Dr. Datuk Abdul Rahim Hashim, President of the International Gas Union, on 4 June, 2012. The outcome of the report shall guide the further development of EDI’s educational portfolio.

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 23

Key findings report According to several interviewees, a successful executive in the energy industry will require a solid understanding of the energy industry as a whole, as well as the function it serves in society. A clear overview of the energy value chain and how different segments interact with one another is vital for the leaders of the industry. Besides understanding the energy business, being an executive requires a comprehensive knowledge of the technical aspects of the industry and also solid commercial skills. Thus, executives must not only understand the technical processes behind their products but also the commercial mechanisms involved in delivering their products to the market. Ultimately, most executives lead for-profit organizations and must concentrate on ensuring desirable financial results. Next to these ‘hard’ skills, an energy executive must demonstrate good vision and leadership in order to drive energy companies to success.

In order to succeed in today’s energy industry, executives require an international orientation. The industry is a global and multicultural industry, which means that leaders must be comfortable in multicultural environments, accept diversity and leverage on variety.

The development of skills and competenciesIn their own professional development, most executives regard practical experience as the most important factor. Rotating several jobs within different countries, potentially different companies and even among various stakeholders encourages the development of an open mind and a much needed overall perspective.

Formal education such as professional courses, together with mentoring, mainly had a role of complementing the experience gained on the job by the interviewees with relevant knowledge on how the energy industry’s mechanisms interact and how a company integrates into the overall perspective.

Future skills and competenciesThe skill that most interviewees expect to become of greater importance in the future is stakeholder management. As the industry becomes more central in public debate, society’s expectations towards energy companies regarding their social, health & safety and environmental responsibilities will increase significantly and future executives will be required to possess the necessary skills to manage tighter relationships with all stakeholders. As the energy industry is moving more and more towards open market conditions, commercial skills and an orientation that places customers at the center of organizations will become crucial for future energy executives. Future leaders will require increased flexibility to face the coming trials and rapidly capitalize on future opportunities.

Generalists vs. specialistsProfessionals can develop themselves as specialists or as pure generalists; both routes can lead to top executive positions. There is a ’preferred or natural’ path for professionals in the energy industry to develop into top level executives namely to first specialize for a couple of years and afterwards look to branching out. Several interviewees say that most of the executives they know personally in the energy industry are generalists with a specialization.

Visit our website to read more or contact us to get a copy of the report.

About EDIEnergy Delta Institute (EDI) is an international energy business school, with a primary focus on natural gas. EDI was founded in 2002 by Nederlandse Gasunie, GasTerra, Gazprom and the University of Groningen, later joined by Shell, Essent, Dong Energy, EBN, Eneco, Taqa, A.Hak and Tebodin. EDI’s main objective is to contribute to the professional development of current and future energy managers. EDI develops and organizes training programmes and network events with a focus on the economic, management, legal and geopolitical aspects of the energy business.

IGU President, Dr Datuk Abdul Rahim Hashim with the first copy of EDI’s report flanked by Eric Dam (left) and Marius Popescu (right).

24

Is shale gas a revolution?The supposed unconventional gas revolution – which includes shale, tight and coal-bed gas – has deeply altered the U.S. energy balance in the last five to seven years. This revolution, initiated by directional drilling and hydraulic fracturing, has helped the U.S. become the world’s largest gas producer, by volume. Gas prices have collapsed on the Henry Hub, replacing coal and nuclear energy in the U.S. For the moment, this directly affects the U.S. only, but indirect impacts can be observed on European and other gas markets. Remember that fossil energies still amount to more than 80% of global energy consumption, and their share will likely remain high through 2030.

Will American shale gas impact the European gas market?The spot market only plays a minor role in Asia and Europe, as long-term contracts provide Europe’s main source of gas supplies (more than 60% of Europe’s gas consumption, including 98% for France). These contracts are generally appreciated because they ensure the security of supplies for the purchaser. They include an oil-indexation, which was created when oil was

the main energy source. Oil indexation allows for balanced risks: the supplier runs the “price risk” as it does not know the price at which its gas will be sold, and the purchaser runs the “volume risk” since it may not exhaust the volumes purchased. This indexation can differ significantly from gas spot prices when they are too dissociated from oil prices, as is currently the case. Gas prices on the Henry Hub fluctuate around $2-3 per MBtu against $10-12 in Europe and $16-18 in Asia. As a result, the U.S. no longer needs to import LNG, contrary to expectations 5 years ago, and prices have decreased on the European spot market.

Can the U.S. become a shale gas exporter?Some wonder if the U.S. could become a shale gas exporter in the near future, potentially exporting it to Europe and competing with Europe’s usual suppliers, such as Norway, Russia and Algeria. This might be possible, but some obstacles should not be underestimated. Although existing U.S. LNG terminals can easily be converted into export units, liquefaction is more expensive than regasification. Because of the added expense, as well as the increasing cost of using LNG ships, the price of American LNG would probably rise to $7-8 per MBtu. It is also doubtful that the U.S. will be interested in supplying the rest of the world with cheap gas, especially as low hydrocarbons prices there have fostered the revival and development of many energy consuming industries.

Should shale gas be exploited in Europe, including in France?According to the International Energy Agency, shale gas reserves may amount to more than 25 Tcm in the U.S., 36 Tcm inChina and 22 Tcm in Argentina. Europe may contain 15 Tcm, including 5 Tcm in both France and Poland. In France, this

Will Shale Gas Disrupt the European Gas Market? By Jacques Percebois, Director, The Center for Research in Energy Economics and Law, The University of Montpellier

BLUE FUELOctober 2012 | Vol. 5 | Issue 3

Ý Ê Ñ Ï Î Ð Ò

www.gazpromexport.com | [email protected] | +7 (499) 503-61-61 | [email protected] 25

would provide 100 years’ worth of gas consumption at the current rate. Since France’s trade deficit was €70bn in 2011, and energy imports accounted for €61.4bn, the potential of exploiting a national energy resource should be explored.

How to look at shale gas in EuropeShale gas development is a sensitive political issue in Europe. Views are often built on perceptions of dependence on Russia, as well as visceral emotions, rather than on economics. There is substantial public support in Poland for shale gas exploration, while France has banned hydraulic fracturing because of its alleged negative environmental effects, especially involving groundwater. Citizen opposition is strong, particularly near Paris and Southeastern France.

However, emotions should not get in the way of sound judgment. We should answer several questions rationally:

1. Are hopes linked to the existence of shale gas reserves justified?

2. At what cost can shale gas be exploited?

3. How do current shale gas drilling techniques affect the environment?

Energy Policy and the Hungarian EconomyBy Judit Barta, GKI Energy Research and Consulting Ltd. (Hungary)