Bloomberg)L.P. IFRS)9)Classification)and)Measurement

21

Bloomberg L.P. IFRS 9 Classification and Measurement Scott Coulter, CPA, CA, CFA Enterprise Accounting Products 1 Mar 2017

Transcript of Bloomberg)L.P. IFRS)9)Classification)and)Measurement

Bloomberg L.P.IFRS 9 Classification and Measurement

Scott Coulter, CPA, CA, CFAEnterprise Accounting Products1 Mar 2017

Agenda

§ Overview of IFRS 9 Classification & Measurement§ Implementation Challenges

§ Data§ Technical Expertise§ Audit Trail & Documentation

§ Bloomberg Solution Overview§ Case Study: Large European Bank & Insurer§ The Road to Implementation§ Q&A

BLOOMBERG REGULATORY SOLUTIONSRAAP<GO>

3

Capital & LiquidityTrading & Monitoring

Automated machine readable data feed

Accounting

Bloomberg’s Enterprise Regulatory Data solutions support firms’ regulatory compliance efforts while unlocking significant operational, capital and balance sheet efficiencies

Tax

Bloomberg Solutions

RiskFront office Treasury Finance

Functions

Daily re-‐assessment & quality controls

Compliance Audit

Bloomberg Accounting SolutionsBloomberg Accounting

Solutions

Fair Value Hierarchy Levelling IFRS 9 SPPI IFRS 9 ECL

• Assists clients in performing the contractual cash flows test required by IFRS 9’s updated classification and measurement model by automating the process of manually reviewing individual security prospectuses and legal documents

• Allows clients to create and store their own fair value leveling rules to generate unique, client-specific leveling results.

• These rules leverage over 70 data fields which provides a summary of the underlying, observable market data used to generate the Bloomberg’s price for a security

• Leverages our existing market-leading default risk models and incorporates new IFRS 9 requirements to deliver the an implementation-ready credit risk product specifically targeted for IFRS 9 purposes

Overview IFRS 9 Financial Instruments

5

§ On July 24, 2014 the IASB issued IFRS 9, Financial Instruments1, replacing IAS 39 ‘Financial Instruments

§ IFRS 9 is effective for annual periods beginning on or after 1 January 2018 with early adoption permitted

§ Regulatory bodies started conducting Quantitative Impact Studies (QIS) by mid-‐2016 to understand impact in more detail

A Single and Integrated Standard

1. http://www.ifrs.org/current-‐projects/iasb-‐projects/financial-‐instruments-‐a-‐replacement-‐of-‐ias-‐39-‐financial-‐instruments-‐recognitio/documents/ifrs-‐9-‐project-‐summary-‐july-‐2014.pdf

Classification and Measurement Impairment Hedge Accounting

6

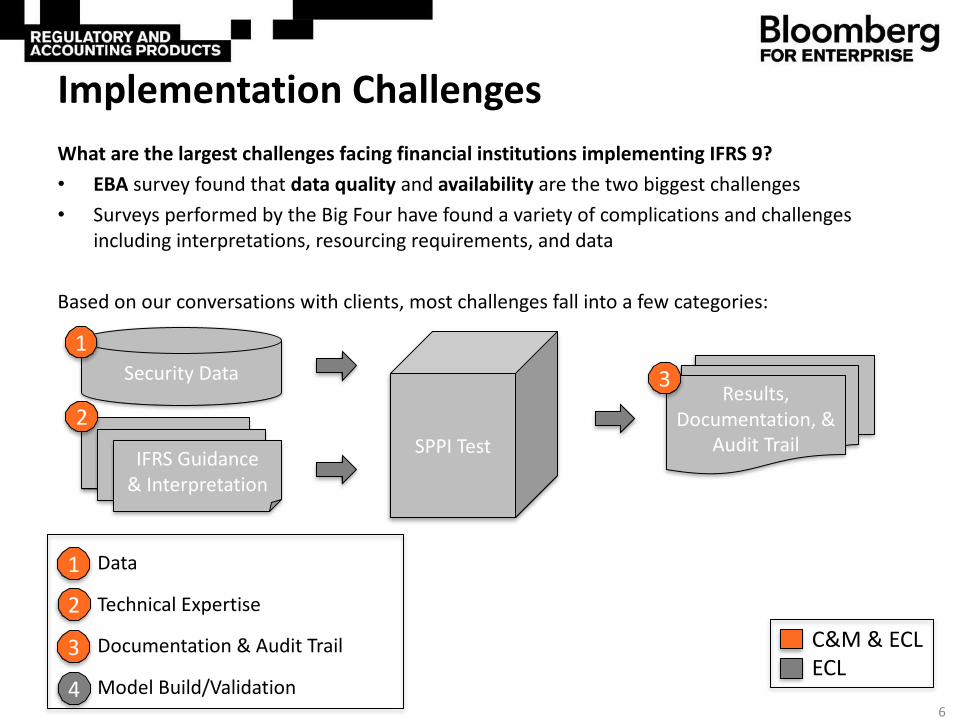

What are the largest challenges facing financial institutions implementing IFRS 9?• EBA survey found that data quality and availability are the two biggest challenges• Surveys performed by the Big Four have found a variety of complications and challenges

including interpretations, resourcing requirements, and data

Based on our conversations with clients, most challenges fall into a few categories:

Implementation Challenges

Security Data

SPPI Test

Results, Documentation, &

Audit TrailSecurity DocsSecurity DocsIFRS Guidance& Interpretation

1

23

1

2

3

Data

Technical Expertise

Documentation & Audit Trail

Model Build/Validation

C&M & ECLECL

4

7

• By Bloomberg’s count, more than 100 different individual security features need to be extracted from prospectuses and analyzed in order to comprehensively apply the SPPI test

• In many cases, financial institutions do not have the required security level data available or the manpower to mine this data themselves

• The data extraction process is arduous and time consuming; it reaches teams of people reviewing securities one-‐by-‐one

• However, without the underlying data, it is challenging if not impossible for these clients to accurately or efficiently reach conclusions or defend those conclusions to auditors/regulators

• Many firms have tried to short-‐cut the SPPI analysis using sample testing because of the huge data burden, but based on our interpretation and many of the Big 4, this is not allowed

Implementation Challenge #1: Data

Security DocsSecurity DocsSecurity Docs

Data Warehouse

Key Challenge Area: Contractually-‐Linked Instruments• Guidance requires looking through the securitization structure in assessing the SPPI test• Entities must have data not only on the instruments but on the underlying pools as well

Data Challenge Example -‐ Hybrid Bonds

8

• XS0304987042 is a hybrid bond issued by insurance company Munich Re. The bond initially has a fixed coupon, but subsequent to Jun 2017, the coupon switches to a variable coupon calculated as 3 month EURIBOR + 204 bps

Data Challenge Example -‐ Hybrid Bonds

9

• XS0304987042 is a hybrid bond issued by insurance company Munich Re. The bond initially has a fixed coupon, but subsequent to Jun 2017, the coupon switches to a variable coupon calculated as 3 month EURIBOR + 204 bps

• As is the case with many hybrid bonds, the Munich Re bond allows for the issuer to exercise an optional deferral of interest payments

Deferrable interest payment, cumulative

Data Challenge Example -‐ Hybrid Bonds

10

No interest on deferral

• XS0304987042 is a hybrid bond issued by insurance company Munich Re. The bond initially has a fixed coupon, but subsequent to Jun 2017, the coupon switches to a variable coupon calculated as 3 month EURIBOR + 204 bps

• As is the case with many hybrid bonds, the Munich Re bond allows for the issuer to exercise an optional deferral of interest payments

• Section 4(a) of the Munich Re prospectus states that if the optional interest deferral is exercised, the interest which is deferred does not accrue interest

Data Challenge Example -‐ Hybrid Bonds

11

No interest on deferral

• XS0304987042 is a hybrid bond issued by insurance company Munich Re. The bond initially has a fixed coupon, but subsequent to Jun 2017, the coupon switches to a variable coupon calculated as 3 month EURIBOR + 204 bps

• As is the case with many hybrid bonds, the Munich Re bond allows for the issuer to exercise an optional deferral of interest payments

• Section 4(a) of the Munich Re prospectus states that if the optional interest deferral is exercised, the interest which is deferred does not accrue interest

Fail

• Once the necessary data has been obtained, flowing this data through the SPPI test requires significant understanding of complex technical accounting concepts at a broad enterprise level. In many cases, this in-‐depth technical knowledge is scarce internally.

• Need to follow and keep up to date on guidance and interpretations from:– IASB– Large, global accounting firms– Peer firms (market consensus)– Industry groups

Implementation Challenge #2: Technical Expertise

12

• Proper implementation of IFRS 9 requires personnel to:1. Understand the guidelines and

interpretations of IFRS 92. Stay current on changes caused by new

standards, interpretations or industry consensus

3. Apply this guidance accurately and consistently throughout implementation and going forward

SPPI Methodology/ Rules Engine

Defensible SPPI Results

IASB

Industry Players Industry Groups

Accounting Firms

13

• The conclusions reached on the SPPI test and contractual cash flows test affect the classification and measurement of financial institutions’ investment portfolios in their audited financial statements.

• Therefore, the SPPI test conclusions fall within the scope of the financial institution’s external audit.

• It is imperative financial statement issuers are able to defend the logic and interpretations that they have applied in performing their SPPI test as well as the output and results of the test.

• It’s is important that any IFRS 9 Classification & Measurement Plan considers the following questions:– How will you document and audit your C&M results?– How will you present and defend your C&M results to your auditors?– How will you adjust your results with changes in guidance or interpretations?

Implementation Challenge #3: Audit Trail & Documentation

“If it’s not documented, it wasn’t done!”

How is Bloomberg Helping Clients with IFRS 9 C&M?

§ Considers on daily basis more than 100 security field characteristics for any features potentially creating cash flows inconsistent with the “solely payments of principal and interest” criterion

§ Provides comprehensive, global coverage of security attributes that would be time-‐consuming and costly for users to review manually on a security-‐by-‐security basis. Product covers approximately 2 million securities (350k fixed income, 1.6 million securitized/pools)

§ Bloomberg Global Data reviews each security’s prospectus in detail in order to evaluate 70 security attributes one-‐by one:§ Security descriptive data§ Coupon characteristics§ Optionalities§ Covenants§ Structured features§ Benchmark and reference rate characteristics

14

Bloomberg’s IFRS 9 SPPI Solution is an operational solution which combines Bloomberg’s extensive security data with an in-‐depth methodology.

Case Study: Large Global Bank & Insurer

Background• Global bank and insurer with significant investment portfolios on both their sell side (bank) and buy side (insurer)• Employed Big 4 consultants to help review and determine gaps• Needed a centralized process to ensure consistent results across buy/sell sides and geographies

15

DATA TECHNICAL INTERPRETATIONS

DOCUMENTATION & AUDIT TRAIL

Challenges

• Insufficient security attributeinformation

• Holes in coverage across instruments and geography

• Inconsistent methodology and application across buy/sell side and geographies

• Insufficient staff/resources to centralize process

• Need documentation to ensure consistent application and to defend results to auditors and regulators

• Need to be able to adjust results with changing guidance/interpretations

Perform initial assessment/gap

analysisObtain security data

Develop policies/assessment

methodology

Perform security-‐by-‐security assessment Document results

Implementation Timeline

ü

Implementation Challenges

Case Study: Large Global Bank & Insurer

Solution• After assessing their needs and options, the client selected Bloomberg’s IFRS 9 SPPI solution• Considers on daily basis more than 100 security field characteristics for any features potentially creating cash

flows inconsistent with the “solely payments of principal and interest” criterion• Provides global coverage of approx. 2 million securities (350k fixed income, 1.6 million securitized/pools)

16

DATA TECHNICAL INTERPRETATIONS

DOCUMENTATION & AUDIT TRAIL

Benefits

• Product leverages Bloomberg’s extensivesecurity data warehouse to product automated results

• Product considers over 100 security attributes in reaching an SPPI conclusion

• Worked with key industry players and auditors in developing the product methodology

• Test rules were built basedon the aggregate consensus of the market and the accounting firms

• Product provides security data to justify conclusions reached

• All interpretations are included in a 35 page methodology document available to clients/auditors

Perform initial assessment/gap

analysisObtain security data

Develop policies/assessment

methodology

Perform security-‐by-‐security assessment Document results

Implementation Timeline

ü

Benefits of Solution

ü ü ü ü

Bloomberg’s IFRS 9 SPPI Solution

2014 2015 2016 2017 2018

IFRS 9 Issued Today Implementation

17

The Road to Implementation: Jan 1, 2018 Looms

Benefits of automated solution include:• Reduced data requirements• Reduced resources requirements• Ensure consistent results across geography/product

• Ensures guidance is applied uniformly • Allows for flexibility to changes in guidance or interpretation• Automatically generates an audit trail of the reason for pass

or fail result

1 2 3

• How will you maintain the IFRS 9 C&M process after the adoption date?

• What sort of resources and team will this project have going forward?

• Have you designed or implemented an operational solution?

Where is your organization with

implementation of C&M?

What still needs to be done by Jan 1, 2018?

What about after Jan 1, 2018?

• Are there still data gaps that need to be solved?

• Are you prepared for possible changes in guidance/interpretation between now and 2018?

• How will you maintain the IFRS 9 C&M process after the adoption date?

• What sort of resources and team will this project have going forward?

• Have you designed or implemented an operational solution?

1 2 3

IFRS 9 Implementation Timeline

18

The Road to Implementation: Jan 1, 2018 Looms

The Case for Automation

Given that internal resources are scarce and the scope of IFRS 9 is wide, any efficiencies that can be gained in the initial assessment are valuable.

Benefits of automation include:• Reduced data requirements• Reduced resources requirements• Ensures guidance is applied uniformly (no variance in interpretations)• Ensure consistent results across geography and product type• Allows for flexibility to changes in guidance, interpretation, or market practice• Automatically generates an audit trail of the reason for pass or fail result

2014 2015 2016 2017 2018

IFRS 9 Issued Today Implementation1 2 3IFRS 9 Implementation Timeline

Q&A

Contact & Accounting Solutions

Bloomberg Accounting Solutions

Agnieszka SoltysikE: [email protected]: +44 20 35253217

Fair Value Hierarchy Levelling IFRS 9 SPPI IFRS 9 ECL

Please stop by our booth or reach out to any of our team members in order to discuss our portfolio of accounting products

Bloomberg Accounting Solutions

Scott Coulter, CFA, CPA, CAE: [email protected]: +1 646 324 2880

Bloomberg Accounting Solutions

Murat BozdemirE: [email protected]: +44 20 35258449

Accounting Product Team

DISCLAIMERThe BLOOMBERG PROFESSIONAL service, BVAL and BRAM (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly owned subsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-‐BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only to sophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of information in the Services. Nothing in the Services shall constitute or be construed as (a) a recommendation of fair value hierarchy classification rules or (b) investment advice or recommendations (i.e., recommendations as to whether or not to "buy", "sell", "hold", or to enter or not to enter into any other transaction involving any specific interest or interests) by BLP, BFLP or their affiliates under any circumstance. You and your firm should review the applicable rules and consult with your advisors to determine your firm's classification policies. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marks of BFLP, a Delaware limited partnership, or its subsidiaries.

© 2017 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.