Bloomberg BNA Daily Tax Report_Mike Starr

20

HIGHLIGHTS Audit Regime Opt-Out Thinking Shifts for Small Partnerships Partnerships with 100 or fewer partners might be able to opt out of the new audit regime for passthrough entities, but they may want to wait to see how the final regulations look before deciding the rules aren’t for them, a practitio- ner says. ‘‘The initial thought was that if you’re eligible to opt out you were going to opt out,’’ Jonathan Horn, a senior technical manager at the American Institute of CPAs, tells Bloomberg BNA at an IRS Nationwide Forum. ‘‘How- ever, as people look at it more and more, we’re not sure. Until we see what the rules really look like, it may or may not make sense.’’ G-4 Foundation Returns Drop Sharply in Continuing ‘Tough Period’ Private and community foundations saw dramatically lower investment re- turns in fiscal year 2015, the second consecutive year of a decline, new data shows. Participating private foundations saw an average annual return of zero percent, down from 6.1 percent in fiscal 2014, according to an investment re- port by the Council on Foundations and Commonfund Institute. Community foundations reported an average annual return of -1.8 percent in fiscal 2015, a decline from 4.8 percent the previous fiscal year, according to the report. The returns reflect the challenge of the environment for private and commu- nity foundations. G-2 Online Tax Bills Still in Limbo Despite New Goodlatte Draft Rep. Goodlatte may soon introduce his long-proposed online sales tax legisla- tion, congressional watchers tell Bloomberg BNA. But when that might hap- pen, and whether it would pass, remains unclear. The House Judiciary Com- mittee releases Chairman Goodlatte’s new discussion draft. The draft bill would require states to look at a vendor’s location when assessing sales tax obligations, but tax rates would be determined by where the sales are des- tined. Some say this approach, which modifies an earlier draft that proposed a purely origin-based tax rate, doesn’t capture all taxable revenue. G-6 Puerto Rico’s ‘Wal-Mart’ Tax Invalid, Appeals Court Holds Puerto Rico’s alternative minimum tax is unconstitutional on its face, a fed- eral appeals court rules, affirming a lower court’s injunction that bars enforce- ment of the tax against Wal-Mart Puerto Rico Inc. The U.S. Court of Appeals for the First Circuit says it is ‘‘indisputable’’ that the AMT unfairly targets cross-border transactions. The tax applies only to transactions between a Puerto Rican corporate taxpayer and a home office or related entity outside of Puerto Rico and imposes its highest rate of 6.5 percent on only one taxpayer, Wal-Mart. K-2 Court Questions Consultant’s Virgin Islands Residency A purported consultant who stayed on a yacht docked in St. Thomas may not have established his residency in the Virgin Islands and, thus, an exemption from U.S. taxes. A federal appeals court rules in Commissioner v. Estate of TEXT EXEMPT ORGANIZATIONS: IRS news release (IR-2016-114) on applications for Advisory Com- mittee on Tax Exempt and Gov- ernment Entities (ACT). TaxCore TAXCORE: For a complete listing of today’s full text documents, look in the contents section. ALSO IN THE NEWS IRS: House conservatives are set to relaunch their effort to impeach IRS Commissioner Koskinen, with or without Speaker Ryan’s go-ahead. G-1 BNA EVENTS R&D: Bloomberg BNA will host a Sept. 19 conference in Washing- ton on new developments impacting the research and development tax credit under tax code Section 41. FOREIGN EARNINGS: Bloomberg BNA will host a conference Sept. 26-27 in Washington on the details of calculating and plan- ning with the earnings and prof- its of foreign subsidiaries. ESTATE TAXES: Bloomberg BNA will host an Oct. 18 webinar on ways to evaluate a trio of estate tax planning structures, and how the IRS might scrutinize and challenge them. A full list of BNA events is at www.bna.com. NUMBER 166 FRIDAY, AUGUST 26, 2016 COPYRIGHT 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. ISSN 0092-6884 Daily Tax Report ®

-

Upload

marissa-confredo -

Category

Documents

-

view

28 -

download

1

Transcript of Bloomberg BNA Daily Tax Report_Mike Starr

H I G H L I G H T S

Audit Regime Opt-Out Thinking Shifts for Small PartnershipsPartnerships with 100 or fewer partners might be able to opt out of the newaudit regime for passthrough entities, but they may want to wait to see howthe final regulations look before deciding the rules aren’t for them, a practitio-ner says. ‘‘The initial thought was that if you’re eligible to opt out you weregoing to opt out,’’ Jonathan Horn, a senior technical manager at the AmericanInstitute of CPAs, tells Bloomberg BNA at an IRS Nationwide Forum. ‘‘How-ever, as people look at it more and more, we’re not sure. Until we see what therules really look like, it may or may not make sense.’’ G-4

Foundation Returns Drop Sharply in Continuing ‘Tough Period’Private and community foundations saw dramatically lower investment re-turns in fiscal year 2015, the second consecutive year of a decline, new datashows. Participating private foundations saw an average annual return of zeropercent, down from 6.1 percent in fiscal 2014, according to an investment re-port by the Council on Foundations and Commonfund Institute. Communityfoundations reported an average annual return of -1.8 percent in fiscal 2015,a decline from 4.8 percent the previous fiscal year, according to the report.The returns reflect the challenge of the environment for private and commu-nity foundations. G-2

Online Tax Bills Still in Limbo Despite New Goodlatte DraftRep. Goodlatte may soon introduce his long-proposed online sales tax legisla-tion, congressional watchers tell Bloomberg BNA. But when that might hap-pen, and whether it would pass, remains unclear. The House Judiciary Com-mittee releases Chairman Goodlatte’s new discussion draft. The draft billwould require states to look at a vendor’s location when assessing sales taxobligations, but tax rates would be determined by where the sales are des-tined. Some say this approach, which modifies an earlier draft that proposeda purely origin-based tax rate, doesn’t capture all taxable revenue. G-6

Puerto Rico’s ‘Wal-Mart’ Tax Invalid, Appeals Court HoldsPuerto Rico’s alternative minimum tax is unconstitutional on its face, a fed-eral appeals court rules, affirming a lower court’s injunction that bars enforce-ment of the tax against Wal-Mart Puerto Rico Inc. The U.S. Court of Appealsfor the First Circuit says it is ‘‘indisputable’’ that the AMT unfairly targetscross-border transactions. The tax applies only to transactions between aPuerto Rican corporate taxpayer and a home office or related entity outside ofPuerto Rico and imposes its highest rate of 6.5 percent on only one taxpayer,Wal-Mart. K-2

Court Questions Consultant’s Virgin Islands ResidencyA purported consultant who stayed on a yacht docked in St. Thomas may nothave established his residency in the Virgin Islands and, thus, an exemptionfrom U.S. taxes. A federal appeals court rules in Commissioner v. Estate of

T E X T

EXEMPT ORGANIZATIONS: IRSnews release (IR-2016-114) onapplications for Advisory Com-mittee on Tax Exempt and Gov-ernment Entities (ACT). TaxCore

TAXCORE: For a complete listingof today’s full text documents,look in the contents section.

A L S O I N T H E N E W S

IRS: House conservatives are setto relaunch their effort toimpeach IRS CommissionerKoskinen, with or withoutSpeaker Ryan’s go-ahead. G-1

B N A E V E N T S

R&D: Bloomberg BNA will host aSept. 19 conference in Washing-ton on new developmentsimpacting the research anddevelopment tax credit undertax code Section 41.

FOREIGN EARNINGS: BloombergBNA will host a conference Sept.26-27 in Washington on thedetails of calculating and plan-ning with the earnings and prof-its of foreign subsidiaries.

ESTATE TAXES: Bloomberg BNAwill host an Oct. 18 webinar onways to evaluate a trio of estatetax planning structures, and howthe IRS might scrutinize andchallenge them.

A full list of BNA events is atwww.bna.com.

NUMBER 166 FRIDAY, AUGUST 26, 2016

COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. ISSN 0092-6884

Daily Tax Report®

H I G H L I G H T S

Continued from previous page

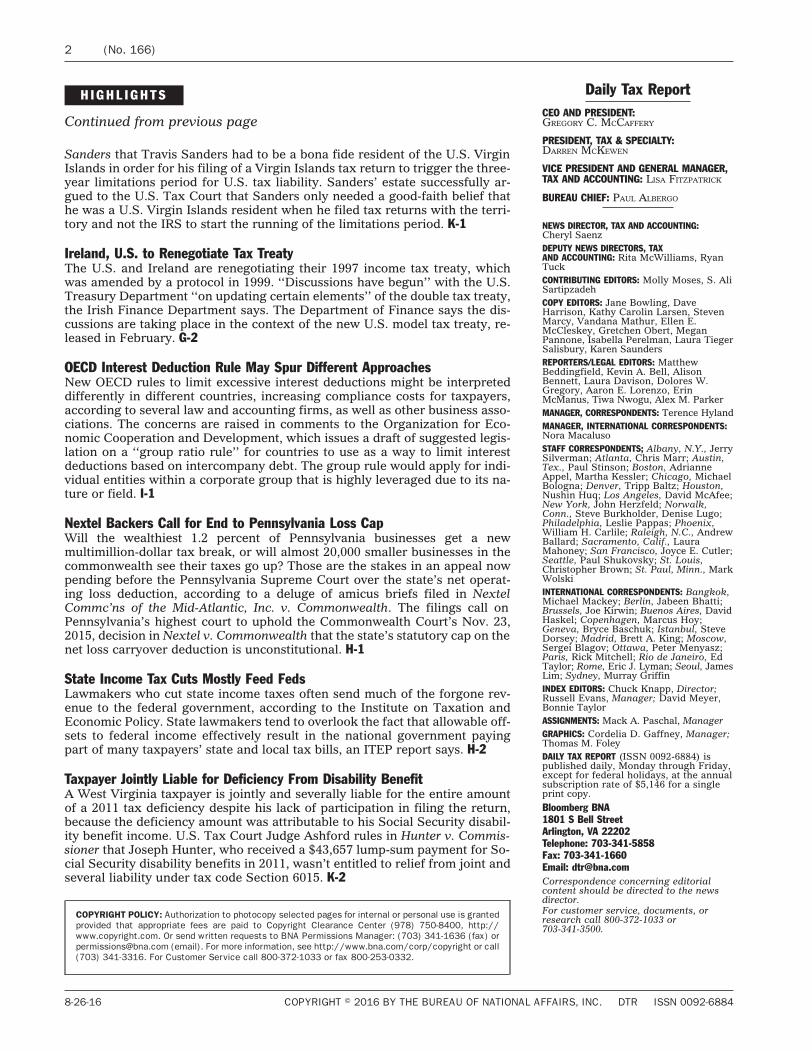

Sanders that Travis Sanders had to be a bona fide resident of the U.S. VirginIslands in order for his filing of a Virgin Islands tax return to trigger the three-year limitations period for U.S. tax liability. Sanders’ estate successfully ar-gued to the U.S. Tax Court that Sanders only needed a good-faith belief thathe was a U.S. Virgin Islands resident when he filed tax returns with the terri-tory and not the IRS to start the running of the limitations period. K-1

Ireland, U.S. to Renegotiate Tax TreatyThe U.S. and Ireland are renegotiating their 1997 income tax treaty, whichwas amended by a protocol in 1999. ‘‘Discussions have begun’’ with the U.S.Treasury Department ‘‘on updating certain elements’’ of the double tax treaty,the Irish Finance Department says. The Department of Finance says the dis-cussions are taking place in the context of the new U.S. model tax treaty, re-leased in February. G-2

OECD Interest Deduction Rule May Spur Different ApproachesNew OECD rules to limit excessive interest deductions might be interpreteddifferently in different countries, increasing compliance costs for taxpayers,according to several law and accounting firms, as well as other business asso-ciations. The concerns are raised in comments to the Organization for Eco-nomic Cooperation and Development, which issues a draft of suggested legis-lation on a ‘‘group ratio rule’’ for countries to use as a way to limit interestdeductions based on intercompany debt. The group rule would apply for indi-vidual entities within a corporate group that is highly leveraged due to its na-ture or field. I-1

Nextel Backers Call for End to Pennsylvania Loss CapWill the wealthiest 1.2 percent of Pennsylvania businesses get a newmultimillion-dollar tax break, or will almost 20,000 smaller businesses in thecommonwealth see their taxes go up? Those are the stakes in an appeal nowpending before the Pennsylvania Supreme Court over the state’s net operat-ing loss deduction, according to a deluge of amicus briefs filed in NextelCommc’ns of the Mid-Atlantic, Inc. v. Commonwealth. The filings call onPennsylvania’s highest court to uphold the Commonwealth Court’s Nov. 23,2015, decision in Nextel v. Commonwealth that the state’s statutory cap on thenet loss carryover deduction is unconstitutional. H-1

State Income Tax Cuts Mostly Feed FedsLawmakers who cut state income taxes often send much of the forgone rev-enue to the federal government, according to the Institute on Taxation andEconomic Policy. State lawmakers tend to overlook the fact that allowable off-sets to federal income effectively result in the national government payingpart of many taxpayers’ state and local tax bills, an ITEP report says. H-2

Taxpayer Jointly Liable for Deficiency From Disability BenefitA West Virginia taxpayer is jointly and severally liable for the entire amountof a 2011 tax deficiency despite his lack of participation in filing the return,because the deficiency amount was attributable to his Social Security disabil-ity benefit income. U.S. Tax Court Judge Ashford rules in Hunter v. Commis-sioner that Joseph Hunter, who received a $43,657 lump-sum payment for So-cial Security disability benefits in 2011, wasn’t entitled to relief from joint andseveral liability under tax code Section 6015. K-2

2 (No. 166)

8-26-16 COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. DTR ISSN 0092-6884

COPYRIGHT POLICY: Authorization to photocopy selected pages for internal or personal use is grantedprovided that appropriate fees are paid to Copyright Clearance Center (978) 750-8400, http://www.copyright.com. Or send written requests to BNA Permissions Manager: (703) 341-1636 (fax) [email protected] (email). For more information, see http://www.bna.com/corp/copyright or call(703) 341-3316. For Customer Service call 800-372-1033 or fax 800-253-0332.

Daily Tax ReportCEO AND PRESIDENT:GREGORY C. MCCAFFERY

PRESIDENT, TAX & SPECIALTY:DARREN MCKEWEN

VICE PRESIDENT AND GENERAL MANAGER,TAX AND ACCOUNTING: LISA FITZPATRICK

BUREAU CHIEF: PAUL ALBERGO

NEWS DIRECTOR, TAX AND ACCOUNTING:Cheryl SaenzDEPUTY NEWS DIRECTORS, TAXAND ACCOUNTING: Rita McWilliams, RyanTuckCONTRIBUTING EDITORS: Molly Moses, S. AliSartipzadehCOPY EDITORS: Jane Bowling, DaveHarrison, Kathy Carolin Larsen, StevenMarcy, Vandana Mathur, Ellen E.McCleskey, Gretchen Obert, MeganPannone, Isabella Perelman, Laura TiegerSalisbury, Karen SaundersREPORTERS/LEGAL EDITORS: MatthewBeddingfield, Kevin A. Bell, AlisonBennett, Laura Davison, Dolores W.Gregory, Aaron E. Lorenzo, ErinMcManus, Tiwa Nwogu, Alex M. ParkerMANAGER, CORRESPONDENTS: Terence HylandMANAGER, INTERNATIONAL CORRESPONDENTS:Nora MacalusoSTAFF CORRESPONDENTS; Albany, N.Y., JerrySilverman; Atlanta, Chris Marr; Austin,Tex., Paul Stinson; Boston, AdrianneAppel, Martha Kessler; Chicago, MichaelBologna; Denver, Tripp Baltz; Houston,Nushin Huq; Los Angeles, David McAfee;New York, John Herzfeld; Norwalk,Conn., Steve Burkholder, Denise Lugo;Philadelphia, Leslie Pappas; Phoenix,William H. Carlile; Raleigh, N.C., AndrewBallard; Sacramento, Calif., LauraMahoney; San Francisco, Joyce E. Cutler;Seattle, Paul Shukovsky; St. Louis,Christopher Brown; St. Paul, Minn., MarkWolskiINTERNATIONAL CORRESPONDENTS: Bangkok,Michael Mackey; Berlin, Jabeen Bhatti;Brussels, Joe Kirwin; Buenos Aires, DavidHaskel; Copenhagen, Marcus Hoy;Geneva, Bryce Baschuk; Istanbul, SteveDorsey; Madrid, Brett A. King; Moscow,Sergei Blagov; Ottawa, Peter Menyasz;Paris, Rick Mitchell; Rio de Janeiro, EdTaylor; Rome, Eric J. Lyman; Seoul, JamesLim; Sydney, Murray GriffinINDEX EDITORS: Chuck Knapp, Director;Russell Evans, Manager; David Meyer,Bonnie TaylorASSIGNMENTS: Mack A. Paschal, ManagerGRAPHICS: Cordelia D. Gaffney, Manager;Thomas M. FoleyDAILY TAX REPORT (ISSN 0092-6884) ispublished daily, Monday through Friday,except for federal holidays, at the annualsubscription rate of $5,146 for a singleprint copy.

Bloomberg BNA1801 S Bell StreetArlington, VA 22202Telephone: 703-341-5858Fax: 703-341-1660Email: [email protected] concerning editorialcontent should be directed to the newsdirector.For customer service, documents, orresearch call 800-372-1033 or703-341-3500.

Federal Tax & Accounting / Page G-1

State Tax & Accounting / Page H-1

International Tax & Accounting / Page I-1

Tax Decisions & Rulings / Page K-1

F E D E R A L TA X & A C C O U N T I N G

ACCOUNTING Push underway to require U.S.regulatory filings in XBRL ..................................... G-4

ELECTRONIC COMMERCE Online tax bills still inlimbo despite new Goodlatte draft ........................... G-6

EXEMPT ORGANIZATIONS Foundation returns dropsharply in continuing ‘tough period’ ........................ G-2

IRS taking applications for exempt-issues advisorypanel .................................................................. G-2

IRS IRS chief faces likely House impeachment votein September ....................................................... G-1

PASSTHROUGH ENTITIES Audit regime opt-outthinking shifts for small partnerships ....................... G-4

TAX ADMINISTRATION IRS wants comments on newcustomer survey ................................................... G-1

TAX TREATIES Ireland, U.S. to renegotiate tax treaty... G-2

S TAT E TA X & A C C O U N T I N G

PENNSYLVANIA Nextel backers call for end toPennsylvania loss cap ........................................... H-1

STATE TAXES State income tax cuts mostly feed feds .. H-2

I N T E R N AT I O N A L TA X & A C C O U N T I N G

PROFIT SHIFTING OECD interest deduction rule mayspur different approaches ....................................... I-1

TA X D E C I S I O N S & R U L I N G S

AMT Puerto Rico’s ‘Wal-Mart’ tax invalid, appealscourt holds .......................................................... K-2

CORPORATE TAXES Comcast, California end briefingin unitary business appeal ...................................... K-1

FILING REQUIREMENTS Court questions consultant’sVirgin Islands residency ......................................... K-1

INCOME Tax protester couldn’t escape liability forwages, gambling ................................................... K-3

INNOCENT SPOUSE RELIEF Taxpayer jointly liablefor deficiency from disability benefit ........................ K-2

TA X C O R E T E X T

AMT Wal-Mart P.R., Inc. v. Zaragoza-Gomez ..... TaxCore

ELECTRONIC COMMERCE Discussion draft for‘Online Sales Simplification Act,’ byRep. Goodlatte .............................................. TaxCore

EXEMPT ORGANIZATIONS IRS news release (IR-2016-114) on applications for Advisory Committee onTax Exempt and Government Entities (ACT) ...... TaxCore

FILING REQUIREMENTS Commissioner v. Estate ofSanders ........................................................ TaxCore

INCOME Canzoni v. Commissioner ................... TaxCore

INNOCENT SPOUSE RELIEF Hunter v.Commissioner ............................................... TaxCore

TA B L E O F C A S E S

Canzoni v. Commissioner (T.C.) ............................ K-3

ComCon Prod. Servs. I, Inc. v. Cal. Franchise TaxBd. (Cal. Ct. App.).............................................. K-1

Commissioner v. Estate of Sanders (11th Cir.) ......... K-1

Hunter v. Commissioner (T.C.) .............................. K-2

Wal-Mart P.R., Inc. v. Zaragoza-Gomez (1st Cir.) ..... K-2

C O D E S E C T I O N I N D E X

SECTION 61 Canzoni v. Commissioner ........ K-3, TaxCore

SECTION 932 Commissioner v.Estate of Sanders .................................... K-1, TaxCore

SECTION 6015 Hunter v. Commissioner ...... K-2, TaxCore

TA X C O R E

For full-text tax documents and IRS hearingtranscripts refer to: http://news.bna.com/tcln/. Toregister for TaxCore, contact BNA CustomerRelations at 800-372-1033.

(No. 166) 3

InThis Issue

DAILY TAX REPORT ISSN 0092-6884 BNA 8-26-16

Federal TAX&ACCOUNTING

Tax Administration

IRS Wants Comments on NewCustomer-Experience Survey

T he IRS’s Wage and Investment Division is develop-ing a customer survey to help the agency identifyand implement service improvements, and is look-

ing for comments on the effort.In an Aug. 26 Federal Register notice, the Internal

Revenue Service said the ‘‘feedback will provide in-sights into customer or stakeholder perceptions, expe-riences and expectations, provide an early warning ofissues with service, or focus attention on areas wherecommunication, training or changes in operationsmight improve delivery of products or services.’’

The title of the information collection is ‘‘Wage andInvestment Behavioral Laboratory Customer Surveysand Support,’’ with an Office of Management and Bud-get number of 1545-NEW.

More information is available from R. Joseph Dur-bala at [email protected].

Comments are due by Oct. 25 to Tuawana Pinkston,IRS, Room 6526, 1111 Constitution Ave. N.W., Wash-ington, DC 20224.

IRS

IRS Chief Faces Likely HouseImpeachment Vote in September

H ouse conservatives are set to relaunch their effortto impeach IRS Commissioner John Koskinen,with or without Speaker Paul Ryan (R-Wis.)’s go-

ahead.Rep. John Fleming (R-La.) says he and other conser-

vatives are prepared to unilaterally force an impeach-ment vote within days after Congress returns to sessionon Sept. 6. ‘‘The only thing up in the air is whether itwill be the first or second week we’re back,’’ Flemingsaid in an Aug. 24 interview.

Any action would be largely symbolic, because the ef-fort would get blocked in the Senate if it passes theHouse. But Republicans remain angry at Koskinen, whothey accuse of impeding an investigation into whetherthe tax agency improperly targeted conservative non-profits. Their allegations include failing to prevent theInternal Revenue Service from destroying evidence andproviding false and misleading information to Con-gress.

A rogue impeachment effort on the House floor byconservatives dissolved in July as time ran out beforeCongress broke for the seven-week summer break (136DTR G-4, 7/15/16).

Ryan has neither threatened to block this re-do ‘‘norgiven us any lecture or reason not to do it,’’ Flemingsaid in an interview. But the House speaker, while him-self critical of Koskinen, has shown reluctance to theidea of setting a modern-day precedent on impeachingcabinet officials.

Legislation pushed by conservatives to remove Koski-nen hasn’t advanced to the House floor under the nor-mal committee process, which Ryan says he prefers.And Ryan in July emphasized that the entire House Re-publican conference must first settle on an ‘‘appropriatepath’’ to addressing concerns about Koskinen whenlawmakers return from break (135 DTR G-12, 7/14/16).

New Precedent. The House hasn’t impeached a cabi-net official since the mid-1870s. Rep. John Conyers Jr.(Mich.), the top Democrat on the House Judiciary Com-mittee, is among those who say that even if the Housevotes to impeach, the Senate wouldn’t provide a two-thirds votes to convict him at trial.

But the delay in House action has led conservatives,led by Fleming and other members of the House Free-dom Caucus, to want to push ahead with their ownplan, even without the backing of Ryan.

In the interview, Fleming said that plan would involverefiling a privileged resolution of impeachment on be-half of the conservative House Freedom Caucus. Thatmeans lawmakers would have two legislative days tovote on either impeaching Koskinen or tabling the mea-sure.

That is the same parliamentary maneuver he andRep. Tim Huelskamp (R-Kan.) launched a day beforeCongress left for summer break, but didn’t have time tosee through before the House broke for summer.

Four Articles. That resolution contained four separatearticles of impeachment, one of which accused Koski-nen of ‘‘engaging in a pattern of conduct showing he isunfit,’’ including false statements to Congress. The con-servatives have accused the IRS under Koskinen’swatch of destroying 422 backup tapes containing poten-tially 24,000 e-mails relevant to the IRS targeting ofconservative organizations. It all adds up to gross neg-ligence, dereliction of duty and violating the publictrust, they say.

The Treasury Department, which oversees the IRS,responded to the July impeachment resolution with astatement calling the effort baseless and a distraction,adding that Treasury Secretary Jacob J. Lew continuesto have full confidence in Koskinen.

Fleming, in the Aug. 24 interview, said such state-ments from the administration make it clear that it isbeing left to Congress to deal with Koskinen.

‘‘And this is not happening under the regular commit-tee process,’’ he said.

BY BILLY HOUSE

(No. 166) G-1

DAILY TAX REPORT ISSN 0092-6884 BNA 8-26-16

To contact the reporter on this story: Billy House inWashington at [email protected]

To contact the editor responsible for this story: KevinWhitelaw at [email protected]

�2016 Bloomberg L.P. All rights reserved. Used withpermission

Exempt Organizations

IRS Taking Applications ForExempt-Issues Advisory Panel

P eople who want to serve on the IRS’s AdvisoryCommittee on Tax Exempt and Government Enti-ties can apply by Sept. 26.

The Internal Revenue Service is seeking members forvacancies expected to occur in June 2017 in sectors rep-resenting federal, state and local governments; Indiantribal governments; and expertise in employment taxwithin areas that include employee plans, exempt orga-nizations, tax-exempt bonds and various levels of gov-ernment.

Applications and nominations should be sent by fax,according to an Aug. 25 news release (IR-2016-114).

In a Federal Register notice scheduled for publicationAug. 26, the IRS said committee members aren’t paid,but are reimbursed for travel expenses related to work-ing sessions and public meetings.

Text of IR-2016-114 is in TaxCore.

Tax Treaties

Ireland, U.S. to Renegotiate Tax TreatyIn Wake of New U.S. Model Treaty

T he U.S. and Ireland are renegotiating their 1997 in-come tax treaty, which was amended by a protocolin 1999.

‘‘Discussions have begun’’ with the U.S. Treasury De-partment ‘‘on updating certain elements’’ of the doubletax treaty, the Irish Finance Department said in an Aug.25 announcement.

The Department of Finance said the discussions aretaking place in the context of the new U.S. model taxtreaty, released in February.

Practitioners said in February that the new U.S.model tax treaty may face an uncertain reception inother countries, despite Treasury’s work to narrowsome of its anti-tax evasion provisions in ways wel-comed by the business community (33 DTR G-8,2/19/16).

Ireland is the globe’s largest recipient of corporate in-versions by value, according to a 2015 study, and theU.S. government has recently used regulations to crackdown on the transactions.

Apple Inc., for instance, has made use of existinggaps in the U.S. tax system to shift its U.S. taxable earn-ings to Ireland. Proposed Internal Revenue Serviceregulations (REG-135734-14) are aimed at curbing so-called earnings stripping, and European tax regulators

are examining the company’s tax practices (65 DTRGG-1, 4/5/16).

BEPS Recommendations. Announcing the treaty nego-tiations Aug. 25, the Irish government pointed out thatthe OECD base erosion and profit shifting final reportslast October made a number of recommendations forupdating tax treaties globally.

The government said countries, including Ireland,‘‘are now actively engaged in implementing the BEPSrecommendations both domestically and through inter-national agreements.’’

The Irish revenue commissioners are asking for com-ments through Oct. 14 on how to update the U.S. modeltax treaty ‘‘from an Irish perspective,’’ and also for com-ments ‘‘on specific aspects’’ of the current Ireland-U.S.income tax treaty.

BY KEVIN A. BELL

To contact the reporter on this story: Kevin A. Bell inWashington at [email protected]

To contact the editor responsible for this story: MollyMoses at [email protected]

Exempt Organizations

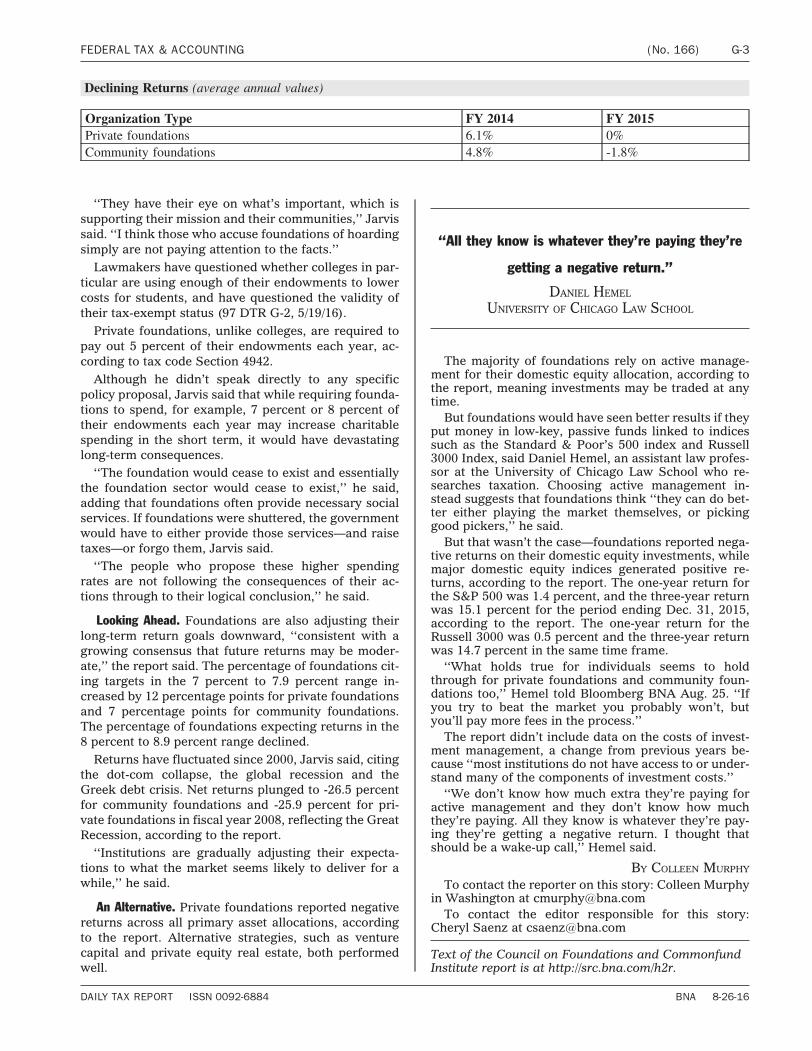

Foundation Returns Drop SharplyIn Continuing ‘Tough Period’

P rivate and community foundations saw dramati-cally lower investment returns in fiscal year 2015,the second consecutive year of a decline, new data

shows.

Participating private foundations saw an average an-nual return of zero percent, down from 6.1 percent infiscal 2014, according to an investment report releasedAug. 23 by the Council on Foundations and Common-fund Institute. Community foundations reported an av-erage annual return of -1.8 percent in fiscal 2015, a de-cline from 4.8 percent the previous fiscal year, accord-ing to the report.

The returns reflect ‘‘the challenge of the environ-ment’’ for private and community foundations, whichstrive to maintain or increase annual distributions whilemaintaining the funds’ purchasing power and nominalvalue, William Jarvis, executive director of the Com-monfund Institute, told Bloomberg BNA Aug. 25.

‘‘This is going to be a very tough period that we’re inright now, is the conclusion,’’ he said.

The report surveyed 228 foundations with combinedassets of $100.6 billion.

Not Hoarders. The effective spending rate—the dol-lars spent in a given year divided by the endowment’svalue at the beginning of the year—for all participatingfoundations held steady at an average of 5.1 percent,according to the report.

G-2 (No. 166) FEDERAL TAX & ACCOUNTING

8-26-16 COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. DTR ISSN 0092-6884

Declining Returns (average annual values)

Organization Type FY 2014 FY 2015Private foundations 6.1% 0%Community foundations 4.8% -1.8%

‘‘They have their eye on what’s important, which issupporting their mission and their communities,’’ Jarvissaid. ‘‘I think those who accuse foundations of hoardingsimply are not paying attention to the facts.’’

Lawmakers have questioned whether colleges in par-ticular are using enough of their endowments to lowercosts for students, and have questioned the validity oftheir tax-exempt status (97 DTR G-2, 5/19/16).

Private foundations, unlike colleges, are required topay out 5 percent of their endowments each year, ac-cording to tax code Section 4942.

Although he didn’t speak directly to any specificpolicy proposal, Jarvis said that while requiring founda-tions to spend, for example, 7 percent or 8 percent oftheir endowments each year may increase charitablespending in the short term, it would have devastatinglong-term consequences.

‘‘The foundation would cease to exist and essentiallythe foundation sector would cease to exist,’’ he said,adding that foundations often provide necessary socialservices. If foundations were shuttered, the governmentwould have to either provide those services—and raisetaxes—or forgo them, Jarvis said.

‘‘The people who propose these higher spendingrates are not following the consequences of their ac-tions through to their logical conclusion,’’ he said.

Looking Ahead. Foundations are also adjusting theirlong-term return goals downward, ‘‘consistent with agrowing consensus that future returns may be moder-ate,’’ the report said. The percentage of foundations cit-ing targets in the 7 percent to 7.9 percent range in-creased by 12 percentage points for private foundationsand 7 percentage points for community foundations.The percentage of foundations expecting returns in the8 percent to 8.9 percent range declined.

Returns have fluctuated since 2000, Jarvis said, citingthe dot-com collapse, the global recession and theGreek debt crisis. Net returns plunged to -26.5 percentfor community foundations and -25.9 percent for pri-vate foundations in fiscal year 2008, reflecting the GreatRecession, according to the report.

‘‘Institutions are gradually adjusting their expecta-tions to what the market seems likely to deliver for awhile,’’ he said.

An Alternative. Private foundations reported negativereturns across all primary asset allocations, accordingto the report. Alternative strategies, such as venturecapital and private equity real estate, both performedwell.

‘‘All they know is whatever they’re paying they’re

getting a negative return.’’

DANIEL HEMEL

UNIVERSITY OF CHICAGO LAW SCHOOL

The majority of foundations rely on active manage-ment for their domestic equity allocation, according tothe report, meaning investments may be traded at anytime.

But foundations would have seen better results if theyput money in low-key, passive funds linked to indicessuch as the Standard & Poor’s 500 index and Russell3000 Index, said Daniel Hemel, an assistant law profes-sor at the University of Chicago Law School who re-searches taxation. Choosing active management in-stead suggests that foundations think ‘‘they can do bet-ter either playing the market themselves, or pickinggood pickers,’’ he said.

But that wasn’t the case—foundations reported nega-tive returns on their domestic equity investments, whilemajor domestic equity indices generated positive re-turns, according to the report. The one-year return forthe S&P 500 was 1.4 percent, and the three-year returnwas 15.1 percent for the period ending Dec. 31, 2015,according to the report. The one-year return for theRussell 3000 was 0.5 percent and the three-year returnwas 14.7 percent in the same time frame.

‘‘What holds true for individuals seems to holdthrough for private foundations and community foun-dations too,’’ Hemel told Bloomberg BNA Aug. 25. ‘‘Ifyou try to beat the market you probably won’t, butyou’ll pay more fees in the process.’’

The report didn’t include data on the costs of invest-ment management, a change from previous years be-cause ‘‘most institutions do not have access to or under-stand many of the components of investment costs.’’

‘‘We don’t know how much extra they’re paying foractive management and they don’t know how muchthey’re paying. All they know is whatever they’re pay-ing they’re getting a negative return. I thought thatshould be a wake-up call,’’ Hemel said.

BY COLLEEN MURPHY

To contact the reporter on this story: Colleen Murphyin Washington at [email protected]

To contact the editor responsible for this story:Cheryl Saenz at [email protected]

Text of the Council on Foundations and CommonfundInstitute report is at http://src.bna.com/h2r.

FEDERAL TAX & ACCOUNTING (No. 166) G-3

DAILY TAX REPORT ISSN 0092-6884 BNA 8-26-16

Passthrough Entities

Audit Regime Opt-Out ThinkingShifts for Small Partnerships

P artnerships with 100 or fewer partners might beable to opt out of the new audit regime for pass-through entities, but they may want to wait to see

how the final regulations look before deciding the rulesaren’t for them, a practitioner said.

‘‘The initial thought was that if you’re eligible to optout you were going to opt out,’’ Jonathan Horn, a seniortechnical manager at the American Institute of CPAs,told Bloomberg BNA at an IRS Nationwide Forum Aug.25. ‘‘However, as people look at it more and more,we’re not sure. Until we see what the rules really looklike, it may or may not make sense.’’

The new audit procedure, required by the BipartisanBudget Act of 2015 (Pub. L. No. 114-74), seeks tostreamline the process for the Internal Revenue Serviceand allows it to conduct examinations and collect ad-justments at the entity level, rather than dealing with in-dividual partners. The law allows single-tier partner-ships with no more than 100 partners to opt out of thelaw as long as all the partners are individuals, C corpo-rations, S corporations or estates of deceased partners.

Under the previous audit regime, known as the TaxEquity and Fiscal Responsibility Act (TEFRA), onlypartnerships with 10 or fewer partners could opt out.The law change launches significantly more and sizablylarger partnerships into pre-TEFRA rules, somethingIRS Chief Counsel William J. Wilkins has called ‘‘un-charted waters.’’

Wilkins and others at the IRS don’t want partnershipsto opt out of the new regime, because that would makeit more difficult for the IRS to track down unpaid taxrevenue. However, many partners are hesitant to em-brace the new regulations because many say the rulesstill have too many problems and cede too much powerto one representative during an audit. Groups includingthe National Association of Manufacturers and the Na-tional Association of Real Estate Investment Trustshave asked the IRS to expand the opt-out rules (74 DTRG-5, 4/18/16).

Saga of a Small Partnership. For small partnershipswhere the partners aren’t changing, it is likely to berelatively simple to coordinate on filing amended re-turns, and having one audit with one final answer mightbe preferable to three audits with potentially three dif-ferent answers, Horn said. In cases like this, the part-nership might be better off inside the regime than out-side.

IRS officials are in the process of writing regulations,which will be released in a proposed form before theyare made final. They will go into effect in 2018, but part-nerships can choose to opt in early. Most partnershipswon’t elect to be audited under the new rules until theysee the regulations, because there are so many ambigui-ties in how the rules will work, Horn said.

Horn said partnerships that opt in before the 2018 of-ficial start date could receive favorable treatment be-cause the IRS has yet to fully flesh out the issues in thelaw.

A partnership might think, ‘‘Yeah, I want the newrules to apply because then you don’t know what to dowith me,’’ Horn said.

Wilkins has warned against opting into the new rulesearly because some features of the law, including theadministrative adjustment request mechanism and theability to push out the adjustment to the partners, aren’tavailable until the general effective date (20 DTR G-6,2/1/16).

BY LAURA DAVISON

To contact the reporter on this story: Laura Davisonin Washington at [email protected]

To contact the editor responsible for this story:Cheryl Saenz at [email protected]

Accounting

Push Underway to RequireU.S. Regulatory Filings in XBRL

A massive lobbying campaign is being waged to re-quire U.S. financial regulatory agencies to collectfinancial regulatory filings electronically, using

only standardized data: eXtensible Business ReportingLanguage (XBRL).

If successful, it would be a major step in the way in-formation is distributed and shared by and among fi-nancial agencies. It could mark a historic turning pointin U.S. financial reporting.

The movement comes on top of what federal agenciesmust do as of 2017 under the Digital Accountability andTransparency Act (DATA) of 2014, the nation’s firstopen-data law. The act requires the federal governmentto transform all spending information into open data.

Washington-based advocacy group Data Coalition,which represents the technology industry, and some inCongress say they would like to see all regulatory bod-ies completely replace document-based reporting withopen standardized data. A bill is being floated, the Fi-nancial Transparency Act of 2015 (H.R. 2477), to ac-complish that goal.

Standardized data like XBRL will save companiesand regulators billions of dollars while also bringingtransparency, consistency and accountability to themarketplace, according to lobbyists. ‘‘We think that ifthe government replaces documents with standardizeddata, that’s great news for investors,’’ Data CoalitionExecutive Director Hudson Hollister told BloombergBNA Aug. 15.

‘‘It’s great news for the agencies doing their own jobsand it’s good news for the companies themselves andthe regulated entities, because when standardized datais reported, then it can be automated with and throughsoftware,’’ he said.

Data Law Already Passed. The topic has taken wings.DATA passed in part through the efforts of the Data Co-alition. The law requires the Treasury Department andthe White House Office of Management and Budget byMay 9, 2017, ‘‘to establish government-wide data stan-dards for the spending information that agencies al-ready report to Treasury, OMB and the General Ser-vices Administration.’’

By May 9, 2018, the Treasury and OMB are requiredto publish all of this spending information for free ac-

G-4 (No. 166) FEDERAL TAX & ACCOUNTING

8-26-16 COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. DTR ISSN 0092-6884

cess and download it on the government’s USASpend-ing.gov website.

Bill Proposed to Mandate. Just as DATA transformsfederal spending information from documents intoopen data, the Financial Transparency Act seeks to en-act the same transformation for financial regulatory fil-ings.

According to the main tenets of the bill, it would re-quire the eight major U.S. financial regulatory agenciesto adopt consistent data fields and formats for informa-tion they already collect from the industry under exist-ing securities, commodities and banking laws.

Rep. Darrell Issa (R-Calif.) introduced the bill with 11bipartisan original co-sponsors May 20, 2015. The DataCoalition is working to build support for its passage andfull implementation.

Worldwide Movement. Rep. Randy Hultgren (R-Ill.),member of the Subcommittee on Oversight and Investi-gations, is one of the co-sponsors.

Hultgren and others say modern electronic reportingwould prevent financial wrongdoing like the years-longPonzi scheme of Bernie Madoff’s, because it would im-prove communication among agencies.

Open, searchable data would allow investors to easilyand accurately research new investment opportunities,according to proponents of this view.

‘‘We believe providing machine-readable data im-proves transparency and accountability in the capitalmarkets, both on the part of those who are regulatedand the regulator,’’ Mike Starr, vice president of gov-ernmental and regulatory affairs at Ames, Iowa,-basedsoftware company Workiva, told Bloomberg BNA Aug.17.

‘‘We also think that the transformation from staticdocuments that are not searchable to a non-proprietarydata format that is searchable is inevitable—it’s not if itwill happen, it’s just a matter of when,’’ said Starr, a for-mer deputy chief accountant for policy at the Securitiesand Exchange Commission.

Starr, who also sits on the board of Data Coalition,said the move would bring tremendous efficiency andeffectiveness to the regulatory process and to those whohave to report to the federal government across a broadspectrum of bodies.

‘‘Whether it’s federal contractors and grantees underthe Data Act, or it’s the eight federal financial regula-tory agencies under the proposed Transparency Act, orit’s the banks that report quarterly to the FDIC, or it’sthe public companies that report to the SEC, and this isa movement that’s worldwide,’’ he said.

Changing Mentality. Lobbyists say they haven’t par-ticularly advocated for a specific type of reporting pro-gram, but XBRL is the only choice on the marketplaceright now for standardized data.

XBRL took to the U.S. capital markets almost two de-cades ago after the Federal Deposit Insurance Corpora-tion and the SEC decided it was a good tool for report-ing data.

There was some reluctance about XBRL initially fromsome firms, but most of it has abated because enoughtime has passed since its inception to generate compari-sons and trends, practitioners said.

‘‘In the last year or two we started to see a bit

more traction on the consumption of XBRL data

outside the SEC market space.’’

EMILY HUANG, IDACITI INC.

‘‘In the last year or two we started to see a bit moretraction on the consumption of XBRL data outside theSEC market space,’’ Emily Huang, chief executive offi-cer and co-founder of Denver, Colo.-based data plat-form company Idaciti, told Bloomberg BNA Aug. 16.

‘‘In the last year or two I’ve started to gradually seepeople’s mentality change, because the quality is goodand every company is filing it,’’ she said.

Huang said XBRL data now has a five-to-seven-yearhistory, which eliminates one of the earliest complaintsby practitioners with its initial enactment: ‘‘ ‘how do wedo comparisons; we need the trending data and there isnot enough data.’ ’’

As to how fast this new traction on XBRL use willgrow, said Huang, ‘‘time will tell.’’

Old Clashing with New. So far, the FDIC requiresbanks to file Call Reports using XBRL. The SEC also re-quires companies to file Forms 10-Q and 10-K usingXBRL. But it also requires them to continue to reportusing PDF document.

Data Coalition’s Hollister says the SEC’s dualapproach—requiring both data and document—hasn’tbeen successful or as effective as it should and could be.‘‘What this has led to is that both the SEC staff and theDivision of Corporation Finance and the companiesthemselves still regard the document as the official ver-sion,’’ said Hollister.

‘‘And they see the XBRL version as this bolted oncompliance requirement—this means that the quality ofthe XBRL data has been much poorer than it should be.In turn that has made it more difficult for informationintermediaries to use the data,’’ Hollister said.

Both the SEC and the Federal Reserve also have hun-dreds of different forms that public companies, finan-cial firms and banking institutions must file, whichhaven’t been transformed from document filings intodata filings, he said.

Reasons for Lobbying. Those advocating mandatingstandardized data say they are passionate about thecause because it will save billions of dollars a year forcompanies and would also provide opportunities withinthe technology space.

Other benefits they point to include accountability,greater workforce efficiency and the usefulness of theinformation to investors.

‘‘Taking all these information flows and making themcheaper, whether it’s in federal spending, with the DataAct or regulatory reporting with the SEC, that saves somuch time and money it means that resources—ifyou’re a company—can be redirected to building thecompany,’’ Hollister said. ‘‘If you’re in government itmeans resources can be redirected to doing whateveryour agency’s job is. That means economic growth; thatmeans people lifted out of poverty,’’ he said.

DENISE LUGO

FEDERAL TAX & ACCOUNTING (No. 166) G-5

DAILY TAX REPORT ISSN 0092-6884 BNA 8-26-16

To contact the reporter on this story: Denise Lugo inNew York, at [email protected]

To contact the editor responsible for this story: AliSartipzadeh at [email protected]

The USA Spending.gov website is at https://www.usaspending.gov/Pages/Default.aspx.

Multistate DevelopmentsElectronic Commerce

Rep. Goodlatte Disseminates NewDiscussion Draft of Online Sales Tax Bill

R ep. Robert W. Goodlatte (R-Va.) may soon intro-duce his long-proposed online sales tax legisla-tion, congressional watchers told Bloomberg BNA.

But when that might happen, and whether it wouldpass, remains unclear.

The House Judiciary Committee released ChairmanGoodlatte’s new discussion draft on Aug. 25. The draftbill would require states to look at a vendor’s locationwhen assessing sales tax obligations, but tax rateswould be determined by where the sales are destined.Some states claim this approach, which modifies anearlier draft that proposed a purely origin-based taxrate, doesn’t capture all taxable revenue.

According to a House Judiciary aide, the bill levelsthe playing field for traditional retailers and ensuresstates can collect sales taxes due.

Destination Tax Rates. The chairman’s measure,which proponents say prohibits taxation without repre-sentation and offers a simpler approach to competingbills already pending in Congress, would allow taxationof remote sales if ‘‘the tax is applied using the originState’s tax base applicable to non-remote sales.’’ Butthe applicable tax rate would be determined by the con-sumer’s state.

The earlier discussion draft simply proposed an ori-gin tax rate.

‘‘The largest change in this compromise was to re-quire sellers to use a single rate per state based onwhere the purchaser lives,’’ Steve DelBianco, executivedirector of NetChoice, told Bloomberg BNA. ‘‘This wasin response to criticism that low tax states would some-how attract catalog and online retailers from higher taxstates.’’

DelBianco noted that the risk of sales tax rates en-couraging businesses to relocate isn’t a real risk, be-cause businesses choose their location on a host of fac-tors. However, the Judiciary Committee felt the com-promise would address critics’ concerns, which hehopes will be the case.

‘‘It isn’t a significant burden to look up 45 additionaltax rates before you apply the rate to your own taxbase,’’ he said. ‘‘I felt like that was acceptable from astandpoint of computer systems modifications. Espe-cially since those rates can only change once a year.’’

Goodlatte released the measure in draft form earlylast year.

Moving Forward. As for future action, the House Judi-ciary aide said that the committee is awaiting stake-holders’ feedback before announcing next steps.

‘‘We are glad to see this bill take center stage as wemove into the annual ritual of lame duck considerationof internet sales tax,’’ DelBianco said. He believes thebill will be introduced this session, but stakeholder re-action will dictate the timing. He doesn’t expect salestax collectors will favor the bill, ‘‘since what they trulywant is unprecedented powers to audit any businessanywhere in the country.’’

Because the Judiciary Committee would be the com-mittee of jurisdiction once the proposal is introduced,the bill could move quickly, at least through the House.

Obstructing Other Bills? The Aug. 25 release followsthe release of an earlier discussion draft and talkingpoints on the Online Sales Simplification Act. Manylawmakers and practitioners have suggested that Good-latte has obstructed competing online sales tax billsfrom moving to the House floor (128 DTR J-1, 7/5/16).

The Marketplace Fairness Act (S. 698) and the Re-mote Transactions Parity Act (H.R. 2775) are structuredaround the customer’s location, but neither have ad-vanced out of committee this session.

All the bills address states’ authority to collect salestax from remote sales, with the MFA and RTPA movingaway from the U.S. Supreme Court’s decision in QuillCorp. v. North Dakota, 504 U.S. 298, which prohibitsstates from taxing retailers without an in-state physicalpresence.

Alabama and South Dakota are leading a flurry of ac-tivity from states to capture more e-retailer tax dollarsand to overturn Quill (158 DTR H-1, 8/16/16).

‘Breath of Fresh Air.’ Many retailer organizations wel-come Goodlatte’s latest proposal, with several reiterat-ing their view that the plan is simple and fair.

‘‘Unlike the MFA and the RTPA, which would subjectsellers to 10,000 to 12,000 rates, the remote seller wouldonly be subject to 45 rates, a significant improvement interms of simplification,’’ Mark E. Nebergall, presidentof the Software Finance and Tax Executives Council,told Bloomberg BNA. However, while characterizingthe one-rate-per-state approach as ‘‘a breath of fresh airin terms of simplification,’’ he noted that the new struc-ture is a ‘‘bit more complex than the single ‘origin’ ratefrom the older draft.’’

Likewise, the National Retail Federation, AmericanCatalog Mailers Association and Electronic RetailingAssociation said they back the bill.

Silencing States? As they await a congressional solu-tion, states and retailers have increasingly wrangledover the taxation of cross-border sales.

Litigation is continuing in Alabama and South Da-kota over their recently enacted e-retailer regimes,which require sales tax collection if a remote vendor’ssales meet a monetary or volume threshold—notwithstanding the lack of a physical presence. Sev-eral other states have enacted legislation that toes theQuill line, with some considering more aggressive tac-tics modeled after Alabama and South Dakota.

This collective effort may have been the impetus be-hind the release of Goodlatte’s latest discussion draft.

‘‘In 2016, the states mounted a campaign of harassingonline and catalog retailers all over the country withnew laws designed to expand nexus and even somelaws that were direct challenges to Quill,’’ DelBiancosaid.

G-6 (No. 166) FEDERAL TAX & ACCOUNTING

8-26-16 COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. DTR ISSN 0092-6884

He explained that this strategy has worked, urgingbusinesses to call on Congress for an end to the states’crusade. And, in particular, he explained that a touch-stone of Goodlatte’s proposal is ensuring there is notaxation without representation.

‘‘The Judiciary Committee bill has an explicit pre-emption of state efforts to define sales tax nexus byanything other than physical presence,’’ he said. ‘‘Andit goes so far as to define physical presence, so there isno question about it.’’

BY JENNIFER MCLOUGHLIN

To contact the reporter on this story: JenniferMcLoughlin in Washington at [email protected]

To contact the editor responsible for this story: RyanTuck at [email protected]

Text of the discussion draft is in TaxCore..

FEDERAL TAX & ACCOUNTING (No. 166) G-7

DAILY TAX REPORT ISSN 0092-6884 s BNA 8-26-16

State TAX&ACCOUNTING

Pennsylvania

Chorus of Nextel Backers CallFor End to Pennsylvania Cap on Losses

W ill the wealthiest 1.2 percent of Pennsylvaniabusinesses get a new multimillion-dollar taxbreak, or will almost 20,000 smaller businesses

in the commonwealth see their taxes go up?Those are the stakes in an appeal now pending before

the Pennsylvania Supreme Court over the state’s netoperating loss (NOL) deduction, according to a delugeof amicus briefs filed in the case (Nextel Commc’ns ofthe Mid-Atlantic, Inc. v. Commonwealth, Pa., No. 6 EAP2016).

The filings call on Pennsylvania’s highest court to up-hold the Commonwealth Court’s Nov. 23, 2015, deci-sion in Nextel v. Commonwealth that the state’s statu-tory cap on the net loss carryover deduction is uncon-stitutional. Most of the briefs call for elimination of thecap entirely, arguing that it is unfair, anti-business, andthat any other remedy could burden tens of thousandsof Pennsylvania taxpayers.

‘‘Pennsylvania is an outlier’’ in terms of capping netoperating losses, Jonathan Liss, a senior director forstate and local tax in accounting firm BDO USA LLP’sPhiladelphia office, told Bloomberg BNA. ‘‘There’s noother state that has anything like it.’’

The Commonwealth Court’s en banc panel ruled 7-0that the state discriminated against Nextel Communica-tions of the Mid-Atlantic, Inc. in 2007 by imposing a $3million carryover cap on operating losses, because thecap prevented Nextel from reducing its taxable incometo zero as thousands of other Pennsylvania taxpayerswith prior-year losses were able to do.

Since 2006, Pennsylvania has capped the amount ofnet operating losses that businesses may apply to theirtaxable income to either a flat dollar amount or a per-centage of income. In 2007, Pennsylvania’s law limitedthe amount of net losses a company could carry over to$3 million or 12.5 percent of income, whichever waslarger. The current cap is the larger of $5 million or 30percent of taxable income.

‘Bad Tax Policy.’ Capping the NOL deduction is sim-ply ‘‘bad tax policy,’’ the Council On State Taxation(COST) argued in its June 24 amicus brief. ‘‘By limitingthe NOL deduction only for taxpayers with large tax-able income, those taxpayers with more income are dis-couraged from locating or expanding their operationsin the Commonwealth,’’ according to the Washington,D.C., trade association. ‘‘In the long run, this will re-duce jobs and harm the Commonwealth’s economy aswell as reduce the state’s overall tax revenues.’’

Nextel argued that Pennsylvania’s statute only affectscorporations with large amounts of income, and thelarger the income, the greater the effect. In 2007, a to-tal of 19,537 corporations in Pennsylvania had net loss

carryovers in excess of their 2007 income, Nextel saidin its appellate brief.

The record shows that 19,303 of them had income of$3 million or less, and were thus able to reduce theirtaxable income to zero. The other 234 corporations—about 1.2 percent of the total—had incomes of morethan $3 million, and were therefore restricted to the12.5 percent limitation.

The higher the income, the greater the cost: For Nex-tel, 87.5 percent of its net loss deduction was disal-lowed.

‘‘There’s an innate unfairness in that,’’ Catie Oryl,staff attorney for COST, told Bloomberg BNA after theCOST brief was filed June 24. ‘‘There’s a lot of otherstates that have NOL deductions, but none of them capit like Pennsylvania does.’’

Cap Since 2006. There hasn’t always been a cap inPennsylvania, the Institute for Professionals in Taxa-tion, pointed out in its June 23 filing with the court.

Pennsylvania enacted a NOL deduction in 1980 andinitially provided for an uncapped deduction, the IPT’sbrief said. ‘‘Not until tax years beginning after Decem-ber 31, 2006 did a percentage-based ‘cap’ on net operat-ing losses become a feature of Pennsylvania’s Corpo-rate Net Income Tax.’’

Pennsylvania and New Hampshire were the onlystates in 2007 to have caps on net operating loss carry-forwards, the institute said. Federal law allows taxpay-ers to carry net operating losses forward to 20 years,without limitation on amount.

‘‘Far from being a ‘loophole,’ the ability to carry for-ward net operating losses is essential to a fair and equi-table income tax system,’’ the institute argued. ‘‘With-out the net loss carryover allowance, investment wouldbe discouraged, research and development would bestymied, and businesses would be less apt to takerisks.’’

What Remedy? In its November decision, the Com-monwealth Court unanimously agreed that the $3 mil-lion cap violated the state constitution’s uniformityclause because it taxed similarly situated taxpayers dif-ferently. The court split 5-2, however, on what to doabout it.

The majority ruled that Nextel should be able to ig-nore the cap, reduce its taxable income to zero in 2007,and get a $3.9 million tax refund. It then called on thestate’s General Assembly to take action without speci-fying what the action should be. Two dissenting judgesargued that to make things uniform for all taxpayers,Pennsylvania should eliminate the flat dollar cap whilekeeping the percentage cap.

Pennsylvania continues to maintain that neither capviolates the uniformity clause and the lower court’s de-cision should be reversed. Should the court disagree,the commonwealth wrote in its May 26 brief, ‘‘the rem-edy for any constitutional disparity should be the sever-ing of the dollar cap on the net loss deduction leavingthe percentage cap in place.’’

(No. 166) H-1

DAILY TAX REPORT ISSN 0092-6884 BNA 8-26-16

‘Draconian’ Result. Such a remedy would be ‘‘draco-nian,’’ the Pennsylvania Chamber of Business and In-dustry wrote in its June 23 brief, which argued that allcaps should be removed. ‘‘This would result in a broadbased tax increase for all of the PA Chamber’s membersthat currently utilize the flat cap net operating loss de-duction and will result in the assessment of thousandsof taxpayers.’’

In 2007, all of the 19,303 corporations with an incomeof $3 million or less were able to deduct 100 percent oftheir loses, without limitation, the chamber argued.‘‘Therefore, the Commonwealth is advocating thisCourt essentially disallow 87.5 percent of the losses de-ducted by the almost twenty thousand corporations thatrelied on the statute.’’

Pennsylvania is advocating ‘‘that in order to solve theuniformity violation against one taxpayer (Nextel), theCourt should order the assessment of thousands of dol-lars against 19,303 corporate taxpayers,’’ the brief con-tinued. ‘‘The Court should reject that remedy.’’

Wider Impact. The chamber implored the court tothink carefully about how to remedy to the problem, es-pecially given the impact that the case would have onothers.

Despite the court’s attempt to limit the remedy onlyto Nextel and only for the year 2007, the Nextel case isalready being applied in other cases, the brief noted.

In RB Alden Corp. v. Commonwealth, the court refer-enced the Nextel decision to find that the $2 million netoperating loss cap in 2016 was also unconstitutional(116 DTR H-1, 6/16/16).

Getting the remedy correct is essential to improvingthe business climate in Pennsylvania, Sam Denisco,vice president of government affairs for the chamber,told Bloomberg BNA Aug. 23.

‘‘The issue of the net operating loss has been at thetop of our tax advocacy platform forever,’’ said Denisco,who favors elimination of all caps. ‘‘If the Common-wealth were to uncap this, we would be sending a mes-sage that Pennsylvania is a business-friendly state.’’

The Pennsylvania Business Council, the GreaterPhiladelphia Chamber of Commerce and the GreaterPittsburgh Chamber of Commerce also filed amicusbriefs in the case. The Republican Caucus of the Penn-sylvania House of Representatives applied Aug. 22 tofile an amicus brief and is awaiting the court’s decision.

Kyle O. Sollie of Reed Smith, who represents Nextel,told Bloomberg BNA that the earliest the court will hearoral arguments in the case will be November.

BY LESLIE A. PAPPAS

To contact the reporter on this story: Leslie A. Pappasin Philadelphia at [email protected]

To contact the editor responsible for this story: RyanTuck at [email protected]

Text of Nextel’s brief is at http://src.bna.com/h11.

Text of COST’s amicus brief is at http://src.bna.com/h1Y.

Text of the Institute for Professionals in Taxation’samicus brief is at http://src.bna.com/h12.Text of the Pennsylvania Chamber of Business andIndustry’s amicus brief is at http://src.bna.com/hXM.

State Taxes

States Send Money to FedsVia Income Tax Cuts, ITEP Says

L awmakers who cut state income taxes often sendmuch of the forgone revenue to the federal govern-ment, according to the Institute on Taxation and

Economic Policy.State lawmakers tend to overlook the fact that allow-

able offsets to federal income effectively result in thenational government paying part of many taxpayers’state and local tax bills, according to an ITEP report re-leased Aug. 22.

Income tax cuts affecting the wealthy result in agreater proportion of the tax cut being given to the fed-eral government, the Washington-based nonpartisanthink tank said in its report.

‘Federal Offset.’ According to ITEP, federal incometax rules allow taxpayers to itemize certain expenses,and many state and local tax payments are deductibleas well. Due to that ‘‘federal offset,’’ the national gov-ernment pays a portion of itemizing taxpayers’ stateand local tax obligations, the group said.

The impact is greater for higher-income taxpayersand is related to whether they itemize and the appli-cable federal tax rate, according to ITEP.

‘‘Tax deductions, including those for state and localtaxes, are often regressive because being able to shielda dollar from tax is more valuable to wealthier taxpay-ers who would see that dollar taxed at a higher rate inthe absence of such a deduction,’’ the institute said.

Tied to Wealth. Such a deduction doesn’t really im-pact lower-income taxpayers because they generallydon’t itemize. The impact from sales and property taxchanges also are relatively minor, as the federal offsetfrom those items is fairly small, the institute said.

Therefore, state income tax changes have the poten-tial to produce the largest offset effects, and cuts tar-geted to the wealthy give a larger percentage of thosecuts to the federal government, ITEP said. Conversely,raising revenue through progressive income taxes willexport much of the cost to the feds, it said.

‘‘Greater awareness of the federal offset can helpstate policymakers design better targeted tax policies,’’the institute said.

BY ANDREW M. BALLARD

To contact the reporter on this story: Andrew M. Bal-lard in Raleigh, N.C., at [email protected]

To contact the editor responsible for this story: RyanTuck at [email protected]

Text of the report is at http://src.bna.com/h2W.

H-2 (No. 166) STATE TAX & ACCOUNTING

8-26-16 s COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. DTR ISSN 0092-6884

International TAX&ACCOUNTING

Profit Shifting

Taxpayers Fear Inconsistent ApproachesTo OECD Guidance on Limiting Deductions

N ew OECD rules to limit excessive interest deduc-tions might be interpreted differently in differentcountries, increasing compliance costs for taxpay-

ers, according to several law and accounting firms, aswell as other business associations.

The concerns were raised in comments to the Orga-nization for Economic Cooperation and Development,which issued a draft of suggested legislation on a‘‘group ratio rule’’ for countries to use as a way to limitinterest deductions based on intercompany debt. Thegroup rule would apply for individual entities within acorporate group that is highly leveraged due to its na-ture or field (133 DTR I-2, 7/12/16).

The group ratio rule is part of the guidance under theOECD’s Action Plan on Base Erosion and Profit Shift-ing, which aims to tweak the international corporate taxsystem to prevent perceived tax avoidance. Most of thefinal recommendations were released in October 2015(193 DTR GG-1, 10/6/15).

Rules in Practice. In comments on the group ratiodraft, which the OECD accepted until Aug. 16, taxpayerrepresentatives supported the overall goal—but raisedconcerns that the rules, in practice, could be inconsis-tently applied.

‘‘We would encourage the OECD to suggest only oneapproach that can be applied by all countries,’’ said acomment letter from Grant Thornton U.K. LLP. ‘‘Thiswill reduce the compliance burden for multinationalgroups and also ensure that the results are applied con-sistently.’’

Others submitting comments agreed.‘‘Although we found many aspects of the discussion

draft welcome, we would still suggest more concreteand prescriptive recommendations in certain areas,’’wrote the Business Industry Advisory Group (BIAC).‘‘The worst situation would be if different countrieswere able to choose different approaches to calculate agroup’s net third party interest expense on a country bycountry basis. The application of any global rule inevi-tably requires some local work on the part of taxpayers.However, if the group ratio rule were to be imple-mented differently in different jurisdictions the admin-istrative cost of compliance would mean that some mul-tinational entities will simply lack the resource to applythe rule at all.’’

PricewaterhouseCoopers International Ltd. argued,conversely, that variations in jurisdictions—including‘‘the accounting standards applied by a group of com-panies’’ and the ‘‘tax law of the territory in question’’could lead to inconsistent application of a single rule,‘‘which means that a fully harmonized approach maynot be optimal.’’

‘‘We would therefore suggest that it is more appropri-ate for territories to determine their rules for computinga group ratio in a manner which is consistent with theirdomestic rules for the taxation of interest and deriva-tives,’’ PwC continued.

Transfer Pricing Changes. The OECD also releasedcomments on its proposed changes to Chapter IX of theTransfer Pricing Guidelines, relating to business re-structurings, as part of the BEPS project.

Will Morris, chair of BIAC, said that in some casesthe recommendations went beyond what was necessaryto incorporate new BEPS standards—in particular, withtweaks to the arm’s-length standard.

‘‘It is important to maintain a focus on what thearm’s-length principle is attempting to achieve: namely,a reflection of the realities of third party arrangementsin transactions between controlled parties,’’ Morriswrote. ‘‘We are disappointed that some elements of thediscussion draft seem to impose approaches that do notfully conform with this principle.’’

He included as examples language in the draft to con-sider the business purpose of a restructuring, and look-ing at the effect of pre-tax profits when determiningwhether an arm’s-length payment is needed.

New Signatories. The OECD also announced that withthe signatures of five new nations, more than 100 coun-tries have signed onto the Multilateral Convention onMutual Administrative Assistance in Tax Matters. Bur-kina Faso, Malaysia, Saint Kitts and Nevis, Saint Vin-cent and the Grenadines, and Samoa signed onto theglobal anti-tax evasion and avoidance protocol, bring-ing the total number of participating nations to 103.

BY ALEX M. PARKER

To contact the reporter on this story: Alex M. Parkerin Washington at [email protected]

To contact the editor responsible for this story: MollyMoses at [email protected]

Comments on the OECD group ratio rule are at http://src.bna.com/h4b; comments on the proposed changesto Chapter 9 are at http://src.bna.com/h4n.

(No. 166) I-1

DAILY TAX REPORT ISSN 0092-6884 s BNA 8-26-16

Tax DECISIONS&RULINGS

Filing Requirements

Court Questions Consultant’sVirgin Islands Residency

A purported consultant who stayed on a yachtdocked in St. Thomas may not have establishedhis residency in the Virgin Islands and, thus, an

exemption from U.S. taxes (Commissioner v. Estate ofSanders, 2016 BL 275035, 11th Cir., No. 15-12582,8/24/16).

A federal appeals court ruled Aug. 24 that TravisSanders had to be a bona fide resident of the U.S. Vir-gin Islands in order for his filing of a Virgin Islands taxreturn to trigger the three-year limitations period forU.S. tax liability.

Sanders’ estate successfully argued to the U.S. TaxCourt that Sanders only needed a good-faith belief thathe was a U.S. Virgin Islands resident when he filed taxreturns with the territory and not the Internal RevenueService to start the running of the limitations period (20DTR K-2, 1/30/15).

Remanded. The U.S. Court of Appeals for the Elev-enth Circuit disagreed and sent the case back to the TaxCourt to determine whether Sanders, who died in 2012,was a bona fide resident of the Virgin Islands for the2002 through 2004 tax years.

Judge R. Lanier Anderson, writing for the court, said‘‘Congress did not intend to create an exception to thefiling requirement for persons who file with’’ the VirginIslands Bureau of Internal Revenue merely subjectivelybelieving themselves to be U.S. Virgin Islands residents.

The Eleventh Circuit adopted the ‘‘four broad catego-ries’’ of factors for determining Virgin Islands residencyset forth by the U.S. Court of Appeals for the Third Cir-cuit in Vento v. Dir. of Virgin Islands Bureau of InternalRevenue (76 DTR K-1, 4/19/13).

Anderson added that those factors aren’t exclusive,and ‘‘the appropriate analysis is one based on the total-ity of circumstances relevant to the residency issue.’’

Hotel Condo, Yacht. In 2002, Sanders became a limitedpartner in a Virgin Islands-based consulting firm thatthe IRS claimed was actually a tax shelter. For the 18days he spent in the Virgin Islands during 2002, hestayed in a condominium at the Ritz Carlton St. Thomasowned by the consulting firm or another unit if thefirm’s unit wasn’t available.

In 2003 and 2004, Sanders stayed in a yacht dockedwith utility connections at St. Thomas. Sanders ownedthe yacht with a friend through a limited liability com-pany. Sanders spent between 49 and 78 days in the Vir-gin Islands in 2003 and between 74 and 109 days therein 2004.

Circuit Judge Adalberto Jordan and Judge Roy B.Dalton Jr. of the U.S. District Court for the Middle Dis-

trict of Florida, sitting by designation, joined Andersonin the opinion.

BY ERIN MCMANUS

To contact the reporter on this story: Erin McManusin Washington at [email protected]

To contact the editor responsible for this story:Cheryl Saenz at [email protected]

Text of the decision is in TaxCore.

Corporate Taxes

Comcast, California FTB Finalize BriefsIn Unitary Business Appeal, Await Argument

C omcast and the California Franchise Tax Boardhave completed a year-long round of briefing indueling appeals over the cable provider’s unitary

relationships and taxable business income (ComConProd. Servs. I, Inc. v. Cal. Franchise Tax Bd., Cal. Ct.App., No. B259619, reply brief 8/24/16).

The pending cross-appeals before the CaliforniaCourt of Appeal, Second Appellate District, arise from aSuperior Court decision adopting Comcast’s positionthat there was no unitary relationship between thecable provider and its former QVC Inc. subsidiary.However, the lower court favored the FTB by character-izing Comcast’s $1.5 billion termination fee from afailed merger as apportionable business income

Comcast filed a reply brief Aug. 24 wrapping up itsopposition to branding the termination fee as taxablebusiness income. The FTB finalized its arguments in aMay 4 brief seeking reversal of the ruling on the unityissue.

The court of appeal hasn’t scheduled oral arguments.

Not Taxable. After a fall-out from merger discussionswith MediaOne, Comcast received $1.5 billion as a con-tractual termination fee. After failing to report the feeas taxable income, Comcast has maintained that themonies aren’t business income under the transactionalor functional tests (46 DTR K-4, 3/10/14).

According to Comcast, taxation of the termination feeexceeds limitations under the U.S. and California con-stitutions, fighting any finding of a ‘‘minimum connec-tion.’’

‘‘The failed merger agreement did not improve, as-sist, benefit, or deter in any way Comcast’s cable opera-tions in California—and thus, there was no connectionbetween the merger agreement and California whatso-ever,’’ according to the Aug. 24 reply brief. ‘‘FTB’s ar-gument that it is constitutionally permissible to tax in-come that ‘would have been earned’ by Comcast flies inthe face of the United States Supreme Court’s admoni-tion against state taxation of multistate income basedon future—or potential—events.’’

In the alternative, if the termination fee constitutesbusiness income, Comcast has contended that the pro-

(No. 166) K-1

DAILY TAX REPORT ISSN 0092-6884 BNA 8-26-16

ceeds must be incorporated within the company’s salesfactor denominator.

Proof of Unity. The FTB reply brief recapped severalreasons for finding unity between Comcast and QVC,refuting Comcast’s reasoning to affirm the lower’s courtruling.

Among several arguments, the FTB reasserted thatthe lower court failed to address a regulatory presump-tion that ‘‘commonly owned businesses engaged in‘steps in a vertical process’ are strongly presumed to beunitary,’’ highlighting several facts to show a vertical in-tegration between Comcast and QVC. Likewise, theFTB emphasized that the trial court failed to apply thestate’s dependency or contribution test for unity.

FTB also circled back to its rationale supporting thetreatment of the termination fee as taxable business in-come.

BY JENNIFER MCLOUGHLIN

To contact the reporter on this story: JenniferMcLoughlin in Washington at [email protected]

To contact the editor responsible for this story: RyanTuck at [email protected]

Text of Comcast’s brief is at http://src.bna.com/h2t.

Text of the FTB’s brief is at http://src.bna.com/h2u.

Innocent Spouse Relief

Taxpayer Jointly Liable ForDeficiency From Disability Benefit

A West Virginia taxpayer is jointly and severally li-able for the entire amount of a 2011 tax deficiencydespite his lack of participation in filing the return,

because the deficiency amount was attributable to hisSocial Security disability benefit income (Hunter v.Commissioner, T.C., No. 16465-14, T.C. Memo. 2016-164, 8/25/16).

U.S. Tax Court Judge Tamara W. Ashford ruled Aug.25 that Joseph Hunter, who received a $43,657 lump-sum payment for Social Security disability benefits in2011, wasn’t entitled to relief from joint and several li-ability under tax code Section 6015.

In 2007, Hunter was working as a mechanic for atransportation company when he was forced to leavehis job after suffering a workplace injury, which led tothe benefits payment.

Hunter’s ex-wife, whom he was married to during theyear at issue, handled the family financial affairs, in-cluding the preparation of tax returns. For 2011, shefiled a joint income tax return for herself and Hunter,and signed it without his having reviewed it. In July2013, the Internal Revenue Service issued the couple adeficiency notice for $4,364, plus a $1,673 penalty, fortheir failure to properly report the benefits payment re-ceived.

Failure to Report. The deficiency also related to a fail-ure to report certain interest income from HuntingtonNational Bank and rental income from Charleston-Kanawha Housing Authority. Hunter filed a petition forinnocent spouse relief in August 2013, arguing that hedidn’t know his ex-wife had filed a tax return with re-spect to 2011, and that before preparing the return she

had withdrawn all the money from their bank accountwithout his knowledge.

In May 2014, the IRS issued a final determination toHunter denying relief from joint and several liability be-cause ‘‘relief is not allowed on tax you owe on your ownincome.’’

At the Tax Court, Hunter presented ‘‘no evidencewhatsoever to corroborate his assertions regarding thejoint return,’’ Ashford said.

Knowledge of Filing. According to the opinion, ‘‘it isclear that petitioner had already agreed to file jointlywith Mrs. Hunter when the joint return was timelyfiled,’’ and that Hunter had admitted that he and his ex-wife had always filed joint tax returns, and that henever made any attempt to file a separate income taxreturn for 2011.

‘‘Relief under section 6015 hinges on attributing theincome tax liability which, in this case, as petitioner ad-mits, is entirely attributable to him,’’ Ashford said.

Ashford ruled that Hunter wasn’t entitled to relief be-cause he couldn’t satisfy the requirement that he showthe understatement of tax was attributable to erroneousitems of the other spouse.

BY MATTHEW BEDDINGFIELD

To contact the reporter on this story: Matthew Bed-dingfield in Washington at [email protected]

To contact the editor responsible for this story:Cheryl Saenz at [email protected]

Text of the decision is in TaxCore.

AMT

Puerto Rico’s ‘Wal-Mart’ TaxUnconstitutional, Appeals Court Holds

P uerto Rico’s alternative minimum tax is unconsti-tutional on its face, a federal appeals court ruled,affirming a lower court’s injunction that bars en-

forcement of the tax against Wal-Mart Puerto Rico Inc.(Wal-Mart P.R., Inc. v. Zaragoza-Gomez, 1st Cir., No.16-01370, 8/24/16).

The U.S. Court of Appeals for the First Circuit saidAug. 24 that it is ‘‘indisputable’’ that the AMT unfairlytargets cross-border transactions. The tax applies onlyto transactions between a Puerto Rican corporate tax-payer and a home office or related entity outside ofPuerto Rico and imposes its highest rate of 6.5 percenton only one taxpayer, Wal-Mart.

Wal-Mart Puerto Rico is the largest private employeron the island, with 48 stores and 14,300 employees. Inany given year, it spends about $1.6 billion on inventoryin Puerto Rico and buys about $700 million in goodsfrom its U.S. parent, Wal-Mart Stores Inc. and other re-lated parties on the mainland, the court said.

Taxes in Excess of Income. In an Aug. 15 letter to theFirst Circuit, Wal-Mart said it booked net taxable in-come of $35 million and regular income taxes of $13.7million before credits for the tax year ended Jan. 31,2016. Had the AMT been in place, Wal-Mart would havefaced an additional $32.9 million in taxes, the companysaid, resulting in a tax liability of more than $46 million,or 132 percent of its income (160 DTR K-1, 8/18/16).

K-2 (No. 166) TAX DECISIONS & RULINGS

8-26-16 COPYRIGHT � 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC. DTR ISSN 0092-6884

Wal-Mart challenged the constitutionality of the AMTin the U.S. District Court for the District of Puerto Rico.On March 28, the district court agreed that the AMTviolates the dormant commerce clause, the Federal Re-lations Act and the equal protection clause.