Bk khare budget2015

62

Will the 2015 budget usher in Achche din BUDGET SPECIAL

-

Upload

shailesh-chheda -

Category

Business

-

view

96 -

download

2

Transcript of Bk khare budget2015

Will the2015 budgetusher in

Achche dinHead O�ce:706/708 Sharda Chambers,New Marine Lines, Mumbai 400020T: +91 22 22007318/0607/6360

PuneHotel Swaroop, 4th Floor,Lane No.10, Prabhat Road,Erandwane, Pune 411 004T: +91 020 25666932/64019743/32926341

Bengaluru101, Money Chambers,1st Floor, #6 K.H. Road,Shanthinagar, Bengaluru 560027T: +91 080 41105357

Delhi107, Siddharth Chambers,Near IIT Gate, Kalu Sarai,Hauz Khas, New Delhi 110 016 T: +91 11 4182 8360

www.bkkhareco.com

BUDGET SPECIAL

vaki

ls

1 B. K. Khare & Co.

INDIA’S UNION BUDGET

B. K. Khare & Co. Chartered Accountants

BUDGET ANALYSIS 2015

This publication is a service to our clients based on a quick appreciation of the budget proposals and must not be regarded as professional advice, authoritative opinion or the sole basis for your decisions. This publication does not constitute an offer or solicitation. For Private Circulation only.

INDIA’S UNION BUDGET

B. K. Khare & Co. 2

3 B. K. Khare & Co.

INDIA’S UNION BUDGET

CONTENTSPoem 4

Editorial 6

Union Budget 2015 10

India at cross roads 10

Biting the Bullet 11

Economic Survey 2015 – Highlights 14

Challenges Ahead 17

Key Features 18

Direct Tax 21

Indirect Taxes 47

Highlights 47

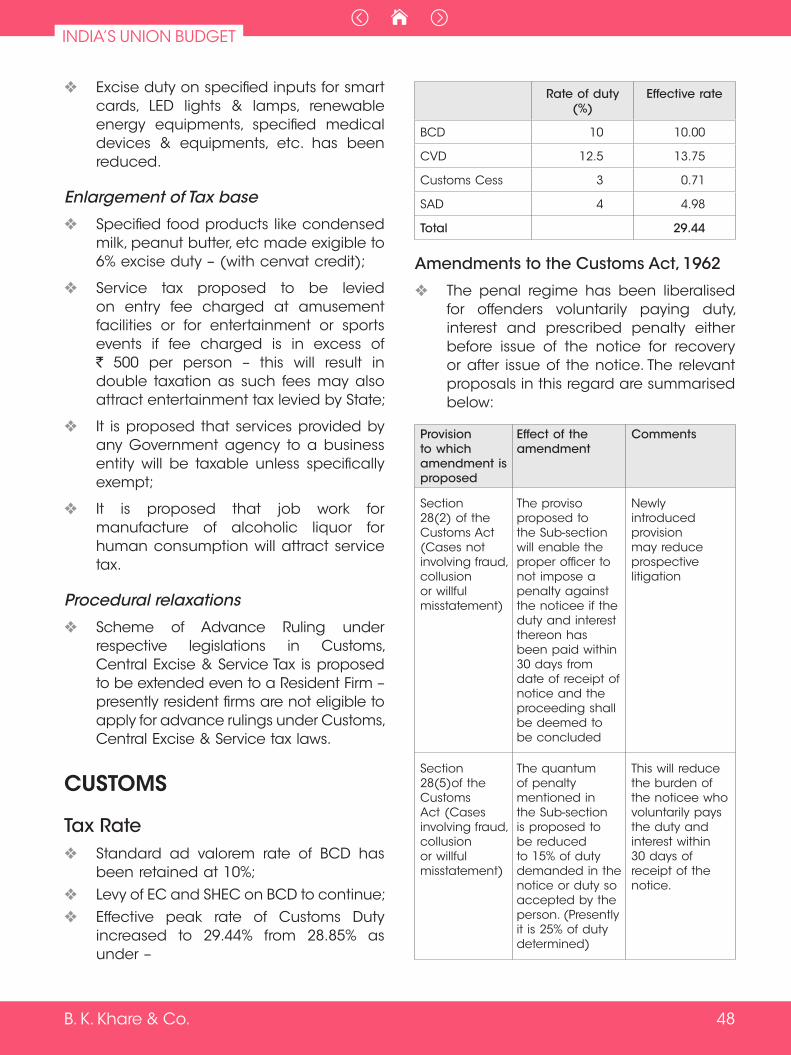

Customs 48

Tax Rate 48

Central Excise 51

Service Tax 55

INDIA’S UNION BUDGET

B. K. Khare & Co. 4

Nani Palkhivala famously saidWhen the United States sneezesThe world catches pneumonia.

Now we can sayMore modestlyWith the growing strength of India’s economyThat when India sneezesThe world shiversAnd reaches for a sweater.

India and ChinaThe oldest civilizationsAre the newest kids on the Economic Block!

The Indian economy is heating upAnd there might be a supernova explosionWith GST and business friendly policiesMr Modi has vowed our business leadersImpressed home and abroad with his preciseRousing oratoryEliciting rousing applauseRather than stifled yawnsPlaying to packed galleriesFrom Madison Square to Melbourne.

In New York at the turn of the last centuryFortunes were made by Rockerfellers and the likeIn the period when America emerged as an economic superpowerAnd was forging its Swayambhu identityBuilding cities and infrastructure that createdThe New Guilded American Age.

But thereafter prosperity did spreadAnd for a whileThe American Middle Class was the envy of one and allThrough the 1950’s, 1960’s and 1970’s.

We hope that this will happen in India as wellAnd with the growth of fortunes of the 1 per centThe rest of the 99 per cent will benefit from the BoomAnd the economic wave will lift millionsOut of aeons of poverty.Happiness shared is happiness multiplied!

5 B. K. Khare & Co.

INDIA’S UNION BUDGET

Meanwhile the able Mr Raghuram RajanFights against the Hydra of InflationGrowth too has its downsideLike anything else.

We are now the Boom and Bust generationBlase about the axiomThat wherever there is a BoomThere will be a BustNewton’s Third Law of Econometrics.

Science gives us the idea of scale and proportionAnd how certain quantities are conservedThings like Angular MomentumIf you draw your arms in when spinningYou spin faster and faster.

So one might askDoes the balance of smiles and tears always remain the same?Is the joke always at someone’s expense?We can hope against hopeThat Happiness and WealthRather than being conserved quantitiesWill subtly shift upwardsTowards greater and greaterAll round contentment in theEvolving Universe.

As Sant Dnyaneshwar foretold in his PasayadanWe live in an interconnected worldHe Vishwachee Mazhe Ghar“The world is my oyster”I pray for an Economic Boom timeWhich is inclusiveAnd Leaves No Citizen Behind.

St. Dnyaneshwar at the end of his writing ‘Dnyaneshwari’ he prayed for the whole human beingTo find Happiness for themselves without wishing anything for himself !In the same manner, we B.K. Khare & Co. wish our clients alround peace and indeed material prosperity ! Let me sign off by wishing all of youAcche DinJo Aane Wale TheAur Ab Aur Bhi Kareeb Aa Gaye.

— B. K. Khare

INDIA’S UNION BUDGET

B. K. Khare & Co. 6

Dear Esteemed Reader,

The Finance Minister’s Budget has been universally hailed as a Budget for Business and Growth. It seems to have something for everybody although not much for the middle class. The Finance Minister honoured the true spirit of federalism by taking the unprecedented step of increasing the share of States in the divisible pool of taxes to 42% (` 5.24 lakh crore in 2015-16). This has undoubtedly squeezed the Centre’s resources considerably. But as indicated by him that would not deter him from adhering to the challenging fiscal deficit target of 4.1% of GDP and committing to achieve the medium term target of 3% of GDP in the next three years.

Infrastructure which is the crying need of the hour could be a roadblock in the growth story. This has been an area of focus of the present Government and has received attention in this Budget. We certainly hope to see more action in the times to come. There is an additional earmarking of ` 70,000 crores from the Centre’s Funds; capital expenditure of the public sector units is expected to increase by ` 80,844 crores. The Finance Minister has also announced his intention of setting up a National Investment and Infrastructure Fund to which an annual flow of ` 20,000 crores is promised.

The most noticed announcement in the pro business measures of the Budget 2015 is of course the commitment to reduce Corporate tax to 25% from the present rate of 30% over the next four years. This conforms to the international benchmark and should in its own way make corporate India more globally competitive. During the 35 years that our firm has been commenting on Budget

proposals, this is the first time that such a commitment for the future has been made (although Mr. V. P. Singh in his own way also committed the Government to a more predictable tax regime). This reduction in rate, we are informed, will also be accompanied by a phasing out over the same period of various incentives and tax holidays that are currently available to companies. As a class of tax payers they effectively pay tax at 23% and therefore the proposed rate of 25% will not translate into a revenue loss. This then raises the question whether the proposed reduction is an optical illusion? Is it really a relief? In fact for the ensuing financial year 2015-16, a surcharge of 2% (discussed later) is proposed to be levied which will increase the tax rate for domestic companies to 34.61% It is of course a step in the right direction in terms of simple, predictable and certain tax regime, since the various incentives had led to a plethora of litigation, constituting a large part of tax litigation. Reduction in such litigation would reduce the burden of the Courts and hopefully lead to speedier justice for all.

There are a few incentives in the tax proposals for furthering the ‘Make in India’ mantra in the form of additional depreciation for capital expenditure in the form of plant and machinery and investment allowance for new units in backward areas of Andhra Pradesh and Telangana. Section 6 has been amended for defining residence of a company which is not an Indian company to provide that if the effective control and management of the company is at any time of the year in India then it would in some circumstances be resident in India. Although this is in keeping with OECD guidelines and DTAs and is ostensibly to take care of

7 B. K. Khare & Co.

INDIA’S UNION BUDGET

shell companies, such a step would widen the test of residence. Again by including ownership etc. in right of management or control through an associated enterprise as defined in Section 92A, the net is cast very wide and would attract the provisions of Explanation 5 to Section 9(1)(i). Both these amendments would in our view receive negative attention from MNCs seeking to do business in India and once again obstruct the ‘ease of doing business’ in the country. Special tax regime for Alternative Investment Funds has been introduced to cover trust, company, limited liability partnership or any other body corporate and they have been provided pass through status. The said proposed amendments have been brought in to boost the infrastructure and improve the investment climate in the country. The requirement of tax withholding @ 10% from distribution of non-business income by such funds however appears harsh as refunds of tax in the hands of unit holders are not easy to get.

On the indirect tax front one of the most eagerly awaited rationalization measure of introduction of GST did not see much light thrown except a re-assertion of the commitment to introduce GST from 1 April 2016. After revealing the broad contours of GST in the Constitution Amendment Bill (122nd Amendment) recently introduced in the Indian Parliament, it was widely anticipated, as a build up to the budget, that the draft GST legislation will be put in the public domain for comments and views of all the stakeholders. This was necessary, given that we have just about a year to prepare for the transition to the new GST regime. However to pave the way for GST the FM has raised tax rates in the current Budget – excise duty

to 12.5% (earlier 12.36%) and service tax to 14% (earlier 12.36%). The increase in tax rates on services is even more severe, given the impending 2% additional levy in the guise of ‘Swachh Bharat Cess’ in addition to the 2% increase in the rate of service tax. This is bound to make services more expensive for the end consumer. It is well known that GST will bring down compliance costs and significantly eliminate tax cascading; hence, higher tax rates may still not impact the lower cost of goods & services in the new regime. This however cannot be said of the present scheme of taxation where cross credits between central indirect taxes and state levies are not available.

Penal provisions have been liberalized under Customs, Excise & Service Tax laws to afford an opportunity to tax evaders who want to come clean by paying off the amount demanded alongwith interest.

On Job Creation, it was expected that the Small & Medium sector will get a boost by way of increase in threshold for payment of excise duty or service tax; however, there is no measure in this direction to encourage entrepreneurship. Turnover thresholds for small scale sector have been left untouched.

On Minimum Government and Maximum Governance, one expected the CENVAT credit regime and mechanism for SAD refunds and service tax refunds to be liberalized to an audit based regime (grant refund first and audit books subsequently) but again apart from increasing the expiry date for taking credit on invoices upto 1 year (earlier 6 months) and facilitating electronic registration within two working days in excise & service tax, not much action has been witnessed at the ground level.

INDIA’S UNION BUDGET

B. K. Khare & Co. 8

So far as maximising benefits to the economy is concerned, levy of service tax on lottery agents and chit fund operators is certainly a move in the right direction and so is the levy of tax on sin goods (higher excise on cigarettes and service tax on job work for alcoholic drinks) but increasing customs duty on imported commercial vehicles and metallurgical coke (an important input for the steel and engineering industry) is not a welcome step. And now even entry to entertainment events and amusement parks will bear a service tax in addition to entertainment tax.

Wealth Tax has been abolished and this is one further step taken by the present Government in keeping with its theme ‘Minimum Government and Maximum Governance’. Keeping in mind the practical considerations of revenue loss a surcharge of 2% is proposed to be imposed on high income tax payers (taxable income of over 1 crore). Going by the math which the Finance Minister himself mentioned, this has again become a source of revenue garnering; for against the revenue sacrifice of INR 1,000 crores, the Government hopes to get wealthier by collecting about INR 9,000 crores from the 2% additional surcharge. However, the draconian provisions sought to be introduced in a separate legislation to curb tax evasion and arrest the menace of Black Money is neither in keeping with minimum governance nor will it make the tax administration less adversarial. The provisions in the existing tax legislations and FEMA are sufficient for the purpose of achieving this objective. As an economist was heard commenting in the media, the tax payers’ experience today is that discretion is never used judiciously; thus, even an honest tax

payer would be alarmed by this measure. Tax administration continues to be the biggest challenge both to foreign investors and the Indian tax payer. Not much has been achieved in bringing in a tax payer friendly approach.

Finally there is clarity on the fate of the Direct Tax Code. It has now been officially announced as buried and the provisions of GAAR have also been deferred for another two years. The Finance Minister clarified that most of the provision of DTC have been incorporated in the existing legislation which is now well settled and well challenged.

The Finance Minister has introduced a ‘Gold Monetisation Scheme’, whereby depositors of gold with the Banks and other dealers, would be able to earn interest on their gold. The scheme would also allow jewelers to obtain loans on their gold, held as stock in trade. This scheme as its name suggests intends to monetise gold which is otherwise an idle asset. Sovereign Gold Bonds are also proposed to develop an alternate financial assets based on gold. Such bonds will carry fixed rate of interest. Buyers of such bonds would be getting bonds issued by the Government instead of physical gold. On maturity, bonds can be redeemed with equal value of gold and interest thereon.

Both the above schemes would help to reduce the demand of overseas gold and black money as well as help in building infrastructure out of money kept in the Sovereign Gold Bonds.

Certain key Financial Market Reforms were announced in the Budget for promoting investment in India; Setting up a Public Debt Management Agency (PDMA) to stream

9 B. K. Khare & Co.

INDIA’S UNION BUDGET

line government debt structure and enable deepening of the bond market; proposed merger of Forward Market Commission with SEBI to strengthen regulation of commodity forward markets and reduce wild speculation; and creation of Task Force to establish a sector-neutral Financial Redressal Agency that will address grievances against all financial service providers.

The present Government has already made visible progress and stands further committed to the cause of financial inclusion. The program to enable a bank account for each household under the Financial Inclusion Mission has turned out to be a significant achievement, with over 12.5 crore families brought into the financial mainstream. Establishment of the Micro Units Development Refinance Agency (MUDRA) Bank, proposal to utilize the vast Indian postal network for financial access, financing the trade receivables of MSMEs, launching the schemes to expand coverage of natural and accidental death risk and provision of pension to the needy are steps in the right direction in the current Budget. In view of the huge economic disparity between the various sections of society and the large

number of people below the poverty line it is incumbent on the Government to provide necessary support and not merely depend on the trickle-down effect of economic progress. The Finance Minister has quoted the Upanishads in the context of the Government’s commitment to the have nots which finds an echo in the poem penned by Mr. B. K. Khare quoting Saint Gyaneshwar, one of the greatest sages of Maharashtra.

Our detailed analysis of the Direct and Indirect tax proposals is preceded by an overview of the Indian Economy which we hope you will find interesting reading

We look forward to your response.

Sincerely,

Padmini Khare Kaicker

Managing Partner

B. K. Khare & Co.Chartered Accountants

Date: 1 March 2015

INDIA’S UNION BUDGET

B. K. Khare & Co. 10

UnIon BUDgET 2015

1. IndIA At CRoss RoAds: demogRAPHIC dIvIdend oR nIgHtmARe?

India is today the world’s fourth largest economy1. This has been one of the most significant achievements of our times. Only fifty years ago, very much within the living memory of many people, the country was chronically and helplessly dependent upon import of food grains from the U.S. Today, despite the fast increasing population, it is a powerhouse of agriculture and a net exporter of food: life expectancy has doubled and literacy rates quadrupled. India will soon have the largest and youngest workforce the world has ever known. It is also witnessing one of the fastest waves of urbanization ever recorded in history. In the coming decade its workforce is slowly poised to increase from 58% to 68% of the population. As that of the rest of the developed world ages and slowly diminishes during the same time horizon, the burgeoning working population in India is capable of producing an unprecedented bonanza in terms of GDP growth. More and more young people, at the rate of nearly ten million per annum, would be entering the job market. If the economy can grow, create enough jobs for them under the “Make in India” program, and make sure that skilled young men and women take advantage of them, unprecedented creative and entrepreneurial energies will unleash. But, if the country fails to get its act together, new investments do not materialize, or youth are not skilled enough to take advantage of the new opportunities that arise, the

1 Measuring GDP by the method of purchasing power parity (PPP)

same demographic dividend will soon convert into an unmitigated demographic disaster, generating considerable social and political stress.

The country thus stands at crossroads with possibilities both of an unprecedented boon as well as a slide into an economic quagmire of unimaginable proportions. If there is any certainty, it is only of huge expectations: if unfulfilled, it would be a sordid tale of wasted potential. The recent elections in Delhi during the past year or so have shown how volatile and impatient people have become.

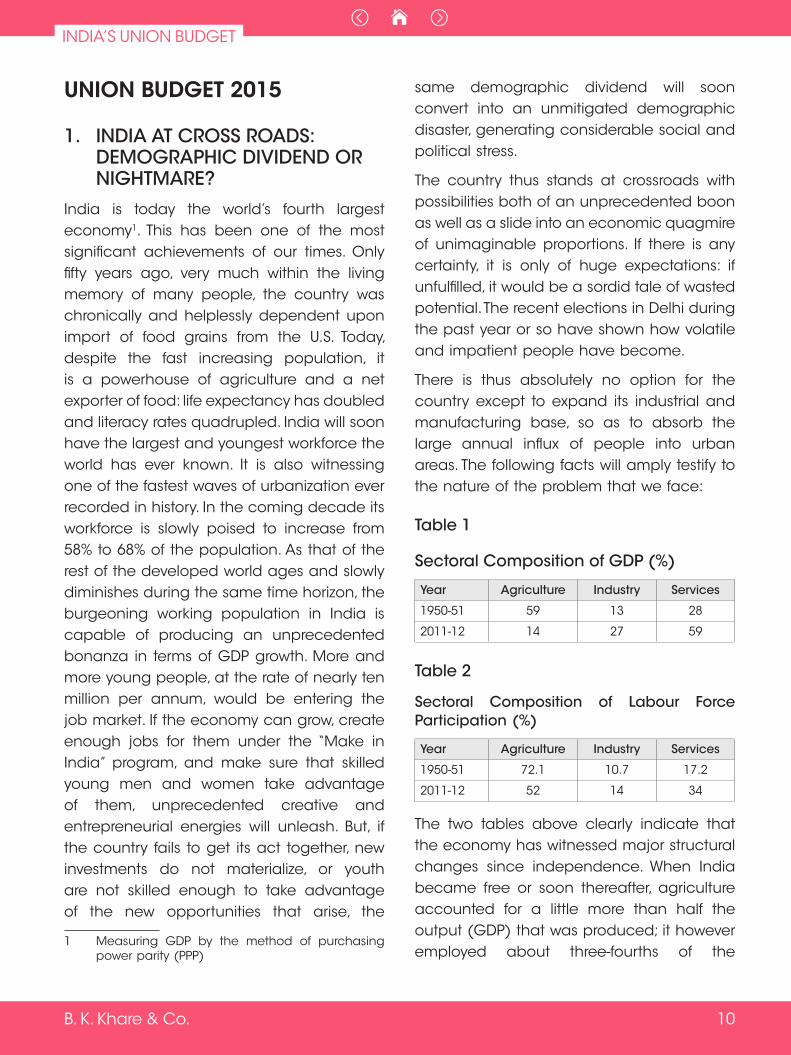

There is thus absolutely no option for the country except to expand its industrial and manufacturing base, so as to absorb the large annual influx of people into urban areas. The following facts will amply testify to the nature of the problem that we face:

table 1

sectoral Composition of gdP (%)

Year Agriculture Industry services

1950-51 59 13 28

2011-12 14 27 59

table 2

sectoral Composition of Labour Force Participation (%)

Year Agriculture Industry services

1950-51 72.1 10.7 17.2

2011-12 52 14 34

The two tables above clearly indicate that the economy has witnessed major structural changes since independence. When India became free or soon thereafter, agriculture accounted for a little more than half the output (GDP) that was produced; it however employed about three-fourths of the

11 B. K. Khare & Co.

INDIA’S UNION BUDGET

country’s labour force; now, it employs 50% of the labour force but produces less than 14% of the nation’s output or GDP. This structural shift in the composition of the GDP has been accompanied by a movement towards urban areas. In 1951, 82.7% of the population lived in rural areas; by 2011, about 15% of this population had migrated to urban areas in search of new jobs. Today, 14% of the population, mostly engaged in industry in urban areas, produces 27% of the GDP and another 34% of the population involved in providing services, contributes 59% of the GDP. It is in fact the industrial or manufacturing sector that offers the maximum hope for absorbing the large expected increase in the work force, simply because the services sector cannot create employment to the same extent, even though the two sectors are quite complementary to each other.

The trends we have witnessed in India are very similar to what other advanced countries witnessed while they were still developing. Today barely 2% the population of the U.S. is engaged in agriculture; this is simply because unless farmers reap economies of scale, it is just not a profitable activity and can provide meaningful livelihoods to very few people; most people have thus to migrate to urban areas in manufacturing and service sectors of the economy for their survival.

Reforms in the nineteen nineties focused mostly on freeing product markets, and inevitably produced a boon. The next generation of reforms which we have been waiting for a long time now must focus on freeing the factor markets- namely, land, labour and capital- so that poor people can find livelihoods and with luck, in the words of Mao Zedong, a thousand flowers can bloom.

2. BItIng tHe BuLLet

It is in this context that the current state of the economy has to be appraised: the year started with the economy still in the throes of a slowdown, caused partly by a policy paralysis and partly by six years of double digit inflation and high interest rates. When the year began, industrial activity was stagnant and infrastructural growth in disarray. Earlier still, during the year 2013 the economy had suffered a mini balance of payment crisis, but was fortunately able to recover from that without much pain.

Three developments occurring during the current year have proved beneficial medicine for nursing the economy back to health: first, the fall in oil and other commodity prices in the international market helped stabilize both the fiscal and current account deficits as well the rate of headline inflation in the economy. High rate of food inflation, in certain parts of the country, however, still remains a matter of concern, but this did not prevent the RBI from reducing the repo rate, thus signalling an easy monetary policy.

Second, the decisive mandate given to the new Government in the recent national elections and the political stability that followed fulfilled an important desire of many well-wishers of the country. The new Government was slow in its efforts to introduce economic reforms, but was quick in energizing the civil service, cutting red tape and introducing administrative reforms.

As a consequence, (and this is the third major trend to emerge), slow optimism began to replace the pessimism that had grounded the economy during the latter half of the UPA-II regime. Sentiment improved although it has still to result in actual hard investment on

INDIA’S UNION BUDGET

B. K. Khare & Co. 12

the ground. With an overall expected growth rate of 5.3%, the economy out-performed not only the emerging economies of India’s class, but other economies of the world as well. As Japan continues to stagnate, China slows down, Europe struggles with legacy problems, and the U.S. slowly recovers from a recession, India, with an expected growth rate of 5.3%, continued to be one beacon of hope in the world. Even so, in January this year the Government revised the method of computing GDP from factor cost to market price- supposedly to conform to international norms. As a result, we were informed that the economy had grown by 6.9% in 2013-14, a year of severe policy paralysis and economic slowdown! Currently, when agriculture has suffered because of a bad monsoon and industrial production is more or less stagnant, we are slated to be growing at 7.3% and have already overtaken the Chinese! The new rates just do not appear credible.

Even so, future growth is critically dependent upon the Government’s willingness and ability to persist with the next generation of reforms that free up labour, capital and land markets. Can the Government accept this challenge?

If the Economic Survey 2015, is to be believed, it already has. The Government is now aiming for a growth rate of 8.1% to 8.5% in the year 2015-16 and about 10% in the medium term. Simultaneously, it introduced a slew of ordinances directed inter alia at making it easier to acquire land for projects, raising the ceiling for FDI in insurance from 26% to 49% etc. These ordinances, particularly the two indicated above, are being hotly contested both inside and outside Parliament. So far the Government has stayed the course. It

has signaled a similar intent with regard to maintaining fiscal discipline.

great expectations

To put things in perspective, the Government did start in right earnest, with a slew of initiatives, to fulfil the great expectations that had been placed upon it. Some of the key initiatives it took were:

YY Swachh Bharat Abhiyan aiming to ensure provision of clean defecation facilities to all;

YY ‘Make in India’ to promote and encourage domestic manufacturing sector;

YY Deen Dayal Upadhyaya Grameen Kaushal Yojana and Deen Dayal Upadhyaya Antyodaya Yojana towards skill development especially amongst the youth;

YY National Policy for Skill Development and Entrepreneurship” to align skilling initiatives with global standards;

YY Liberalization of FDI policy for real estate sector, enhancing the corpus of the National Housing Bank and increasing the income-tax incentives for housing loans, all these towards fulfilling the mission titled “Housing for All”;

YY National Optical Fibre Network aiming to transform India into a digitally empowered society and knowledge economy;

YY Deendayal Upadhyaya Gram Jyoti Yojana to improve rural electrification;

YY Beti Bachao, Beti Padhao Abhiyaan to change mindsets to celebrate the girl child;

YY Apprentice Protsahan Yojana to promote apprentices in MSMEs;

YY Pradhan Mantri Jan Dhan Yojana for greater financial inclusion;

13 B. K. Khare & Co.

INDIA’S UNION BUDGET

YY NITI Aayog to foster cooperative federalism;

YY Namami Gange for River Ganga conservation;

YY Diamond Quadrilateral Project of high speed trains connecting the 4 metros

Note: Some of the schemes mentioned above are rechristened avatars of earlier schemes and in some cases, initiatives have now been taken up for pan-India implementation.

Since assuming office in May 2014, the new Government has undertaken a number of new reform measures whose cumulative impact could be substantial. These include:

YY Deregulating diesel prices, paving the way for new investments in this sector;

YY Raising gas prices from US$ 4.2 per million British thermal unit to US$ 5.6, and linking pricing, transparently and automatically, to international prices so as to provide incentives for greater gas supply and thereby relieving the power sector bottlenecks;

YY Taxing energy products by taking advantage of declining oil prices, resulting in additional tax collections;

YY Replacing the cooking gas subsidy by direct transfers on a national scale;

YY Instituting the Expenditure Management Commission, which has submitted its interim report for rationalizing expenditures;

YY Passing an ordinance to reform the coal sector via auctions;

YY Securing the political agreement on the goods and services tax (GST) that will allow legislative passage of the constitutional amendment bill;

YY Instituting a major program for financial inclusion—the Pradhan Mantri Jan Dhan Yojana;

YY Continuing the push to extending coverage under the Aadhaar program, targeting enrollment for 1 billion Indians;

YY Increasing FDI caps in defence;

YY Eliminating the quantitative restrictions on gold;

YY Passing an ordinance to make land acquisition less onerous, thereby easing the cost of doing business, while ensuring that farmers get fair compensation;

YY Facilitating Presidential assent for labour reforms in Rajasthan, setting an example for further reform initiatives by the states; and consolidating and making transparent a number of labour laws;

YY Passing an ordinance increasing the FDI cap in insurance to 49%;

YY Disinvestment of 10% of the government’s stake in Coal India; and

YY Passing the Mines and Minerals (Development and Regulation) (MMDR) Amendment Ordinance, 2015 to revive the hitherto stagnant mining sector in the country and usher in greater transparency and boost revenues for the States.

Overall, the Government made the right noises and sent out right signals to create trust and a business-friendly atmosphere inter-alia by not pursuing appeals in some high profile tax cases, trying to make it easy to do business in India and reforming labour laws. To indicate political intent, it even took the controversial ordinance route for some key reforms such as land acquisition and FDI in insurance. To be sure, it wanted to shed past baggage in order to reposition India on an 8-10% growth path.

INDIA’S UNION BUDGET

B. K. Khare & Co. 14

emerging “green shoots”

According to a recent poll by FICCI, measures announced by the Government over the past seven-eight months revealed a positive impact on the sentiment of the business community. To the Government’s credit, it has not played to the galleries by rushing in ill-thought measures or resorting to ad-hocism. The successful coal and spectrum auctions are a case in point. Given the weight of the colossal expectations, it was easy for the Government to cave in to such temptations to demonstrate quick results. As the Economic Survey puts it, what was required was “a persistent, encompassing, and creative incrementalism”. The potential impact of the reform initiatives of this Government will in on all likelihood yield results only over time. The Government is correctly focusing on strengthening fundamentals and is resolved to calibrate and walk the difficult path of fiscal consolidation.

It has also yet to figure out a way of getting its legislative and reformist agenda passed through the Rajya Sabha where it does not enjoy a majority. And this may very well turn out to be its Achilles heel.

3 eConomIC suRveY 2015 - HIgHLIgHts

The Economic Survey suggests that India has reached a ‘sweet spot’ in its economic history; as a consequence it may now finally launch itself on a sustained double-digit growth trajectory. The economic consequences of such a development are enormous. A growth trajectory of that order will in time “lift all boats” and allow millions to escape from a life of poverty.

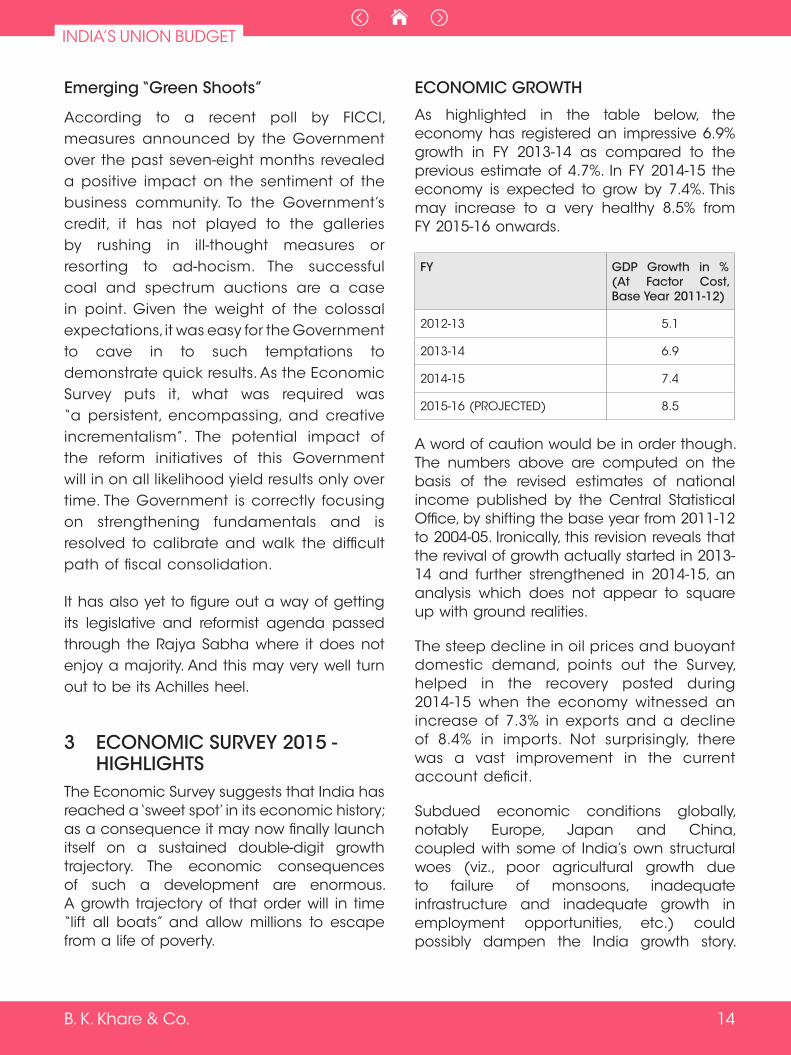

eConomIC gRoWtH

As highlighted in the table below, the economy has registered an impressive 6.9% growth in FY 2013-14 as compared to the previous estimate of 4.7%. In FY 2014-15 the economy is expected to grow by 7.4%. This may increase to a very healthy 8.5% from FY 2015-16 onwards.

FY gdP growth in % (At Factor Cost, Base Year 2011-12)

2012-13 5.1

2013-14 6.9

2014-15 7.4

2015-16 (PROJECTED) 8.5

A word of caution would be in order though. The numbers above are computed on the basis of the revised estimates of national income published by the Central Statistical Office, by shifting the base year from 2011-12 to 2004-05. Ironically, this revision reveals that the revival of growth actually started in 2013-14 and further strengthened in 2014-15, an analysis which does not appear to square up with ground realities.

The steep decline in oil prices and buoyant domestic demand, points out the Survey, helped in the recovery posted during 2014-15 when the economy witnessed an increase of 7.3% in exports and a decline of 8.4% in imports. Not surprisingly, there was a vast improvement in the current account deficit.

Subdued economic conditions globally, notably Europe, Japan and China, coupled with some of India’s own structural woes (viz., poor agricultural growth due to failure of monsoons, inadequate infrastructure and inadequate growth in employment opportunities, etc.) could possibly dampen the India growth story.

15 B. K. Khare & Co.

INDIA’S UNION BUDGET

However, the survey is optimistic of a strong domestic demand to keep the growth momentum going.

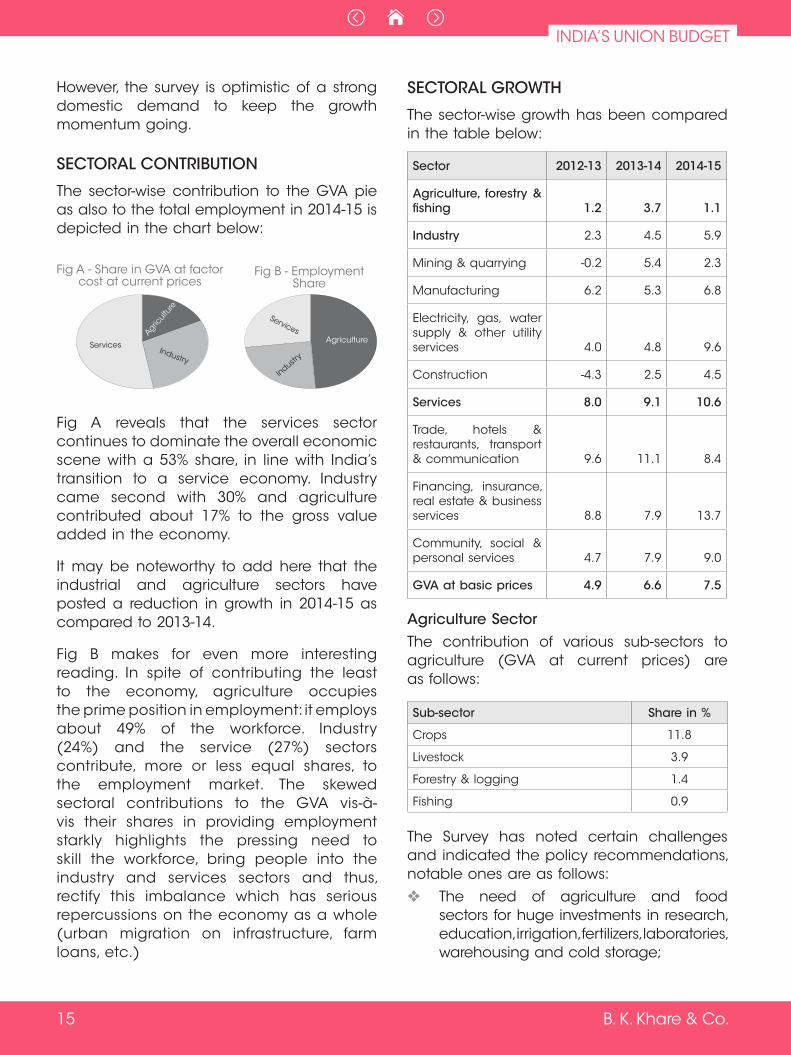

seCtoRAL ContRIButIon

The sector-wise contribution to the GVA pie as also to the total employment in 2014-15 is depicted in the chart below:

Fig A reveals that the services sector continues to dominate the overall economic scene with a 53% share, in line with India’s transition to a service economy. Industry came second with 30% and agriculture contributed about 17% to the gross value added in the economy.

It may be noteworthy to add here that the industrial and agriculture sectors have posted a reduction in growth in 2014-15 as compared to 2013-14.

Fig B makes for even more interesting reading. In spite of contributing the least to the economy, agriculture occupies the prime position in employment: it employs about 49% of the workforce. Industry (24%) and the service (27%) sectors contribute, more or less equal shares, to the employment market. The skewed sectoral contributions to the GVA vis-à-vis their shares in providing employment starkly highlights the pressing need to skill the workforce, bring people into the industry and services sectors and thus, rectify this imbalance which has serious repercussions on the economy as a whole (urban migration on infrastructure, farm loans, etc.)

seCtoRAL gRoWtH

The sector-wise growth has been compared in the table below:

sector 2012-13 2013-14 2014-15

Agriculture, forestry & fishing 1.2 3.7 1.1

Industry 2.3 4.5 5.9

Mining & quarrying -0.2 5.4 2.3

Manufacturing 6.2 5.3 6.8

Electricity, gas, water supply & other utility services 4.0 4.8 9.6

Construction -4.3 2.5 4.5

services 8.0 9.1 10.6

Trade, hotels & restaurants, transport & communication 9.6 11.1 8.4

Financing, insurance, real estate & business services 8.8 7.9 13.7

Community, social & personal services 4.7 7.9 9.0

gvA at basic prices 4.9 6.6 7.5

Agriculture sectorThe contribution of various sub-sectors to agriculture (GVA at current prices) are as follows:

sub-sector share in %

Crops 11.8

Livestock 3.9

Forestry & logging 1.4

Fishing 0.9

The Survey has noted certain challenges and indicated the policy recommendations, notable ones are as follows:YY The need of agriculture and food

sectors for huge investments in research, education, irrigation, fertilizers, laboratories, warehousing and cold storage;

INDIA’S UNION BUDGET

B. K. Khare & Co. 16

YY Poor yields in different crops as compared to the better ones across the world;

YY Creation of national common market for agricultural commodities;

YY Strengthening of Forward Markets Commission.

Overall, the Survey estimates sustainable future agricultural growth at about 4% per annum.

Industry sectorThe Prime Minister has made the revival of Indian manufacturing a top priority as reflected in the ‘Make in India’ campaign. The Survey highlights that only registered or formal manufacturing has the capacity to emerge as a transformational sector in terms of productivity and rapid growth. Accordingly, it has identified this sector apart from financial services, insurance and real estate services as requiring significant skill profile improvements to match underlying endowments.

If the Economic Survey truly reflects Government’s thinking, it could perhaps be inferred that the Government will not hesitate to adopt ‘protectionist’ responses (shielding domestic manufacturing from foreign competition via tariffs and local content requirements) to boost domestic industrial growth.

services sectorThe YoY growth in the services sector (as a % to GDP growth) has been depicted in the table below:

FY % to gdP

2012-13 8

2013-14 9.1

2014-15 10.6

It thus becomes evident that it was the services sector which provided the basic impetus for the growth during 2013-14. Trade and repair services, rail transport, communication and broadcasting services achieved close to double digit growth in 2013-14. Growth in financial, real estate and

professional services increased from 7.9% to 13.7% and public administration, defence and other services from 7.9% to 9.0% (yoy).

otHeR KeY mACRo eConomIC IndICAtoRs

Fiscal deficitThe fiscal deficit as a percentage of the GDP over the past few years has been tabulated in the table below:

% of gdP

2011-12 5.7

2012-13 4.8

2013-14 4.5

2014-15 4.1

2015-16 3.9

The budget documents reveal that the Government stood by its commitment of bringing down the fiscal deficit target for 2014-15 to 4.1% of GDP. However, the deadline to reduce it to 3% of GDP by 2016-17 has now been pushed back by another year.

InFLAtIon

Both the measures of inflation viz., the headline inflation measured in terms of Wholesale Price Index (WPI) and the Retail inflation as measured by the Consumer Price Index (CPI), have continued to show a downward trend.

2011-12 2012-13 2013-14 2014-15

W h o l e s a l e Price Index 8.9 7.4 6.0 3.4

C o n s u m e r Price Index 8.4 10.4 9.7 6.2

As fuel has larger weight in the WPI, the decline in oil prices led to sharper reduction in the WPI as compared to the CPI. The Finance Minister has indicated in the budget that the Government will maintain CPI inflation at around 5% in the immediate future.

17 B. K. Khare & Co.

INDIA’S UNION BUDGET

eXteRnAL seCtoR

The key macro-economic indicators in the external sector are compiled in the table below:

Indicator 2011-12 2012-13 2013-14 2014-15

Export Growth % 21.8 -1.8 4.7 4.0

Import Growth % 32.3 0.3 -8.3 3.6

Forex Reserves USD Billion 294.4 292 304.2 328.7

Net FDI USD Billion 22.06 19.82 21.56 16.18

Overall the the current account now stands at 1.3 % of the GDP, thanks mostly to the reduction in international price of oil.

tAX CoLLeCtIons

The detailed break-up of the gross tax revenue (GTR) is provided in the table below:

(` In crores)

tax Head 2013-14 2014-15 2015-16

(1) Direct Taxes

a) On Income & Expenditure

Corporate Income-tax 394,678 426,079 470,628

Income-tax (other than corporate income-tax) 237,817 272,607 320,836

Hotel Receipts tax 1 – –

Interest tax 8 – –

FBT 5 – –

Others 9 – –

b) On Property and Capital transactions

Estate duty 0 – –

Wealth tax 1,007 950 –

Gift tax 1 – –

STT 5,018 5,992 6,531

BCTT 0 – –

total direct taxes (a+b) 638,543 705,628 797,995

(2) Indirect Taxes

Customs 172,085 188,713 208,336

Excise duties 169,455 184,731 229,054

Service tax 154,779 168,132 209,774

Others 1,004 975 1,005

Taxes collected by Union Territories without legislature

3,130 3,438 3,577

total Indirect taxes 500,453 545,988 651,746

gross tax Revenue (gtR) (1+2) 1,138,995 1,251,616 1,449,741

% of direct taxes to gtR 56% 56% 55%

% of indirect taxes to gtR 44% 44% 45%

The proportion of direct taxes and indirect taxes to the GTR over the past few years has remained more or less constant but the current statistics do now reflect much greater reliance by the Central Government on direct as opposed to indirect taxes for meeting the country’s revenue needs. This is in sharp contrast to the position that prevailed in the past.

4 CHALLenges AHeAd

The Finance Minister has listed five major challenges in the Union Budget, viz. stress on agricultural incomes; the need for increasing investment in infrastructure; decline in manufacturing witnessed in the recent past; the emerging resource crunch, as higher tax revenues devolve on states; and finally the urgent requirement of maintaining fiscal discipline. In order to meet these challenges, the public sector needs to step in to catalyze investment.

Arvind Panagriya observed recently that “green shoots” of recovery were emerging in the Indian economy. These shoots, however, need, to be carefully and artfully nurtured, and be provided with the right environment to grow; otherwise they will disappear.

On the whole, the Union Budget 2015, is a step in the right direction even though it travels “on a road less taken”. The policy makers need to realize that ultimately the key to the success of various proposals will lie in effective implementation. We have had good budgets in the past as well, but they failed to leave a mark because policy was poorly implemented. It is thus very important therefore that those called upon to deliver should not lose focus.

INDIA’S UNION BUDGET

B. K. Khare & Co. 18

Key Features of Budget 2015-2016 presented on 28 February 2015

1 KeY ACHIevements

Credibility of Indian economy has been re-established in the last nine months.

After inheriting an economy with sentiments of “doom and gloom” with adverse macroeconomic indicators, nine months have seen at turn around, making India fastest growing large economy in the World with a real GDP growth expected to be 7.4% (New Series).

Three key achievements: 1) Financial Inclusion - 12.5 crores families financially mainstreamed in 100 days; 2) Transparent Coal Block auctions to augment resources of the States & 3) Swachh Bharat Abhiyaan to improve hygiene and cleanliness.

2 stAte oF tHe eConomYCPI inflation projected at 5% by the end of the year, consequently, easing of monetary policy.

GDP growth in 2015-16, projected to be between 8 to 8.5%.

The fiscal deficit targets are 3.9%, 3.5% and 3.0% in FY 2015-16, 2016-17 & 2017-18 respectively.

3 mAJoR CHALLenges AHeAd Five major challenges: Agricultural income under stress, increasing investment in infrastructure, decline in manufacturing, resource crunch in view of higher devolution in taxes to states, maintaining fiscal discipline.

4 KeY HIgHLIgHtsDirect Transfer of Benefits to be extended further with a view to increase the number of beneficiaries from 1 crore to 10.3 crore.

Target of ` 8.5 lakh crore of agricultural credit during the year 2015-16.

Government to work with the States, in NITI, for the creation of a Unified National Agriculture Market.

Micro Units Development Refinance Agency (MUDRA) Bank, with a corpus of ` 20,000 crores, and credit guarantee corpus of ` 3,000 crores to be created.

A Trade Receivables discounting System (TReDS) which will be an electronic platform for facilitating financing of trade receivables of MSMEs to be established.

Comprehensive Bankruptcy Code of global standards to be brought in fiscal 2015-16 towards ease of doing business.

Postal network with 1,54,000 points of presence spread across villages to be used for increasing access of the people to the formal financial system.

Pradhan Mantri Suraksha Bima Yojna to cover accidental death risk of ` 2 Lakh for a premium of just ` 12 per year.

Atal Pension Yojana to provide a defined pension, depending on the contribution and the period of contribution. Government to contribute 50% of the beneficiaries’ premium limited to ` 1,000 each year, for five years, in the new accounts opened before 31 December 2015.

Pradhan Mantri Jeevan Jyoti Bima Yojana to cover both natural and accidental death risk of ` 2 lakh at premium of ` 330 per year for the age group of 18-50.

National Investment and Infrastructure Fund (NIIF), to be established with an annual flow of ` 20,000 crores to it.

Tax free infrastructure bonds for the projects in the rail, road and irrigation sectors.

(SETU) Self-Employment and Talent Utilization) to be established as Techno-financial, incubation and facilitation program to support all aspects of start-up business.

19 B. K. Khare & Co.

INDIA’S UNION BUDGET

An expert committee to examine the possibility and prepare a draft legislation where the need for multiple prior permission can be replaced by a pre-existing regulatory mechanism.

5 new Ultra Mega Power Projects, each of 4000 MW, in the Plug-and-Play mode.

Public Debt Management Agency (PDMA) bringing both external and domestic borrowings under one roof to be set up this year.

Forward Markets commission to be merged with SEBI.

Section 6 of FEMA to be amended through Finance Bill to provide control on capital flows as equity will be exercised by Government in consultation with RBI.

India Financial Code to be introduced soon in Parliament for consideration

Gold monetisation scheme to allow the depositors of gold to earn interest in their metal accounts and the jewellers to obtain loans in their metal account to be introduced.

Foreign investments in Alternate Investment Funds to be allowed.

Distinction between different types of foreign investments, especially between foreign portfolio investments and foreign direct investments to be done away with. Replacement with composite caps.

Visas on arrival to be increased to 150 countries in stages.

Proposal to introduce a public Contracts (resolution of disputes) Bill to streamline the institutional arrangements for resolution of such disputes.

An autonomous Bank Board Bureau to be set up to improve the governance of public sector bank.

The first phase of GIFT to become a reality very soon. Appropriate regulations to be issued in March.

direct tax Proposals

No change in rate of personal income tax.

Proposal to reduce corporate tax from 30% to 25% over the next four years, starting from next financial year.

Bill for a comprehensive new law to deal with black money parked abroad to be introduced in the current session.

Benami Transactions (Prohibition) Bill to curb domestic black money to be introduced in the current session of Parliament.

Tax “pass through” to be allowed to both category I and category II alternative investment funds.

Permanent Establishment (PE) norm to be modified to encourage fund managers to relocate to India.

General Anti Avoidance Rule (GAAR) to be deferred by two years.

Additional investment allowance (@ 15%) and additional depreciation (@35%) to new manufacturing units set up during the period 01 April 2015 to 31 March 2020 in notified backward areas of Andhra Pradesh and Telangana.

Rate of Income-tax on royalty and fees for technical services reduced from 25% to 10% to facilitate technology inflow.

Benefit of deduction for employment of new regular workmen to all business entities and eligibility threshold reduced.

Monetary limit for a case to be heard by a single member bench of ITAT increase from ` 5 lakh to ` 15 lakh.

Wealth-tax replaced with additional surcharge of 2 per cent on super rich with a taxable income of over ` 1 crore annually.

Applicability of indirect transfer provisions to dividends paid by foreign companies to their shareholders to be addressed through a clarificatory circular.

INDIA’S UNION BUDGET

B. K. Khare & Co. 20

Domestic transfer pricing threshold limit increased from ` 5 crore to ` 20 crore.

MAT rationalised for FIIs and members of an AOP.

Limit of deduction of health insurance premium increased from ` 15,000 to ` 25,000, for senior citizens limit increased from ` 20,000 to ` 30,000.

Senior citizens above the age of 80 years, who are not covered by health insurance, to be allowed deduction of ` 30,000 towards medical expenditures.

To mitigate the problem being faced by many genuine charitable institutions, it is proposed to modify the ceiling on receipts from activities in the nature of trade, commerce or business to 20% of the total receipts from the existing ceiling of ` 25 lakh.

Direct Tax Code not being pursued.

Indirect tax Proposals

Basic Custom duty on certain inputs, raw materials, inter mediates and components in 22 items, reduced to minimise the impact of duty inversion.

All goods, except populated printed circuit boards for use in manufacture of ITA bound items, exempted from SAD.

Time limit for taking CENVAT credit on inputs and input services increased from 6 months to 1 year.

Service-tax plus education cesses increased from 12.36% to 14% to facilitate transition to GST.

Education cess and the Secondary and Higher education cess to be subsumed in Central Excise Duty.

21 B. K. Khare & Co.

INDIA’S UNION BUDGET

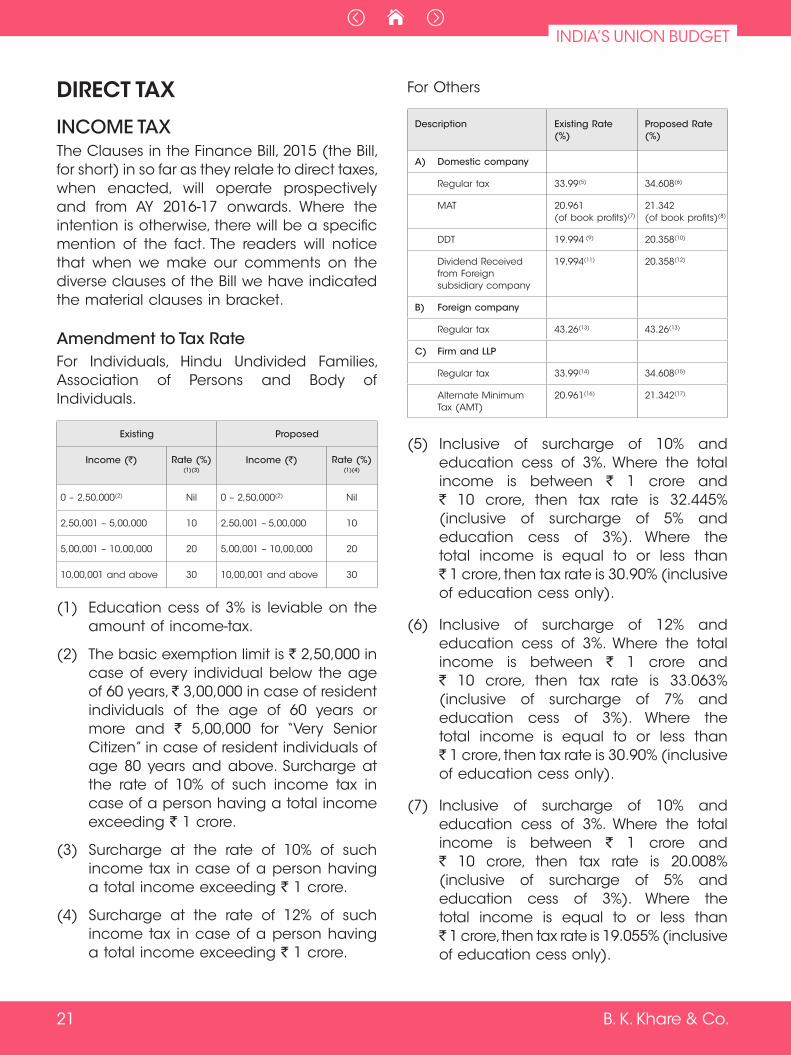

DIRECT TAX

INCOME TAXThe Clauses in the Finance Bill, 2015 (the Bill, for short) in so far as they relate to direct taxes, when enacted, will operate prospectively and from AY 2016-17 onwards. Where the intention is otherwise, there will be a specific mention of the fact. The readers will notice that when we make our comments on the diverse clauses of the Bill we have indicated the material clauses in bracket.

Amendment to Tax RateFor Individuals, Hindu Undivided Families, Association of Persons and Body of Individuals.

Existing Proposed

Income (`) Rate (%)

(1)(3)

Income (`) Rate (%) (1)(4)

0 – 2,50,000(2) Nil 0 – 2,50,000(2) Nil

2,50,001 – 5,00,000 10 2,50,001 – 5,00,000 10

5,00,001 – 10,00,000 20 5,00,001 – 10,00,000 20

10,00,001 and above 30 10,00,001 and above 30

(1) Education cess of 3% is leviable on the amount of income-tax.

(2) The basic exemption limit is ` 2,50,000 in case of every individual below the age of 60 years, ` 3,00,000 in case of resident individuals of the age of 60 years or more and ` 5,00,000 for “Very Senior Citizen” in case of resident individuals of age 80 years and above. Surcharge at the rate of 10% of such income tax in case of a person having a total income exceeding ` 1 crore.

(3) Surcharge at the rate of 10% of such income tax in case of a person having a total income exceeding ` 1 crore.

(4) Surcharge at the rate of 12% of such income tax in case of a person having a total income exceeding ` 1 crore.

For Others

Description Existing Rate (%)

Proposed Rate (%)

A) Domestic company

Regular tax 33.99(5) 34.608(6)

MAT 20.961 (of book profits)(7)

21.342 (of book profits)(8)

DDT 19.994 (9) 20.358(10)

Dividend Received from Foreign subsidiary company

19.994(11) 20.358(12)

B) Foreign company

Regular tax 43.26(13) 43.26(13)

C) Firm and LLP

Regular tax 33.99(14) 34.608(15)

Alternate Minimum Tax (AMT)

20.961(16) 21.342(17)

(5) Inclusive of surcharge of 10% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 32.445% (inclusive of surcharge of 5% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 30.90% (inclusive of education cess only).

(6) Inclusive of surcharge of 12% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 33.063% (inclusive of surcharge of 7% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 30.90% (inclusive of education cess only).

(7) Inclusive of surcharge of 10% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 20.008% (inclusive of surcharge of 5% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 19.055% (inclusive of education cess only).

INDIA’S UNION BUDGET

B. K. Khare & Co. 22

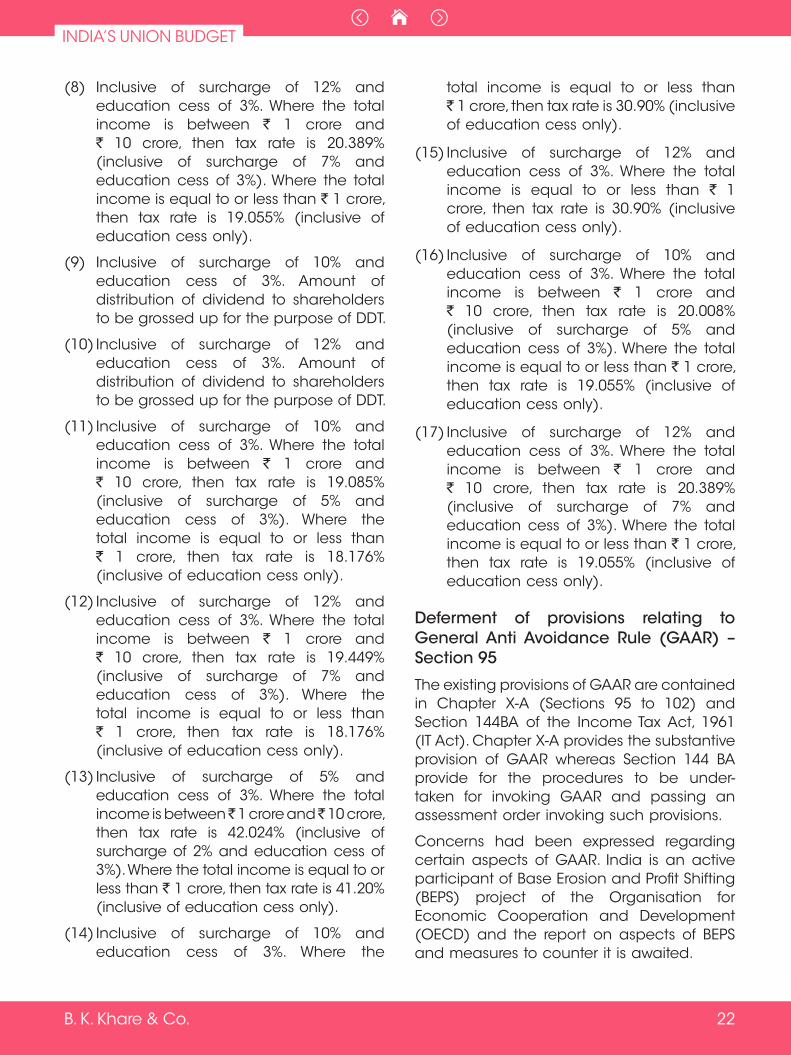

(8) Inclusive of surcharge of 12% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 20.389% (inclusive of surcharge of 7% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 19.055% (inclusive of education cess only).

(9) Inclusive of surcharge of 10% and education cess of 3%. Amount of distribution of dividend to shareholders to be grossed up for the purpose of DDT.

(10) Inclusive of surcharge of 12% and education cess of 3%. Amount of distribution of dividend to shareholders to be grossed up for the purpose of DDT.

(11) Inclusive of surcharge of 10% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 19.085% (inclusive of surcharge of 5% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 18.176% (inclusive of education cess only).

(12) Inclusive of surcharge of 12% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 19.449% (inclusive of surcharge of 7% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 18.176% (inclusive of education cess only).

(13) Inclusive of surcharge of 5% and education cess of 3%. Where the total income is between ̀ 1 crore and ̀ 10 crore, then tax rate is 42.024% (inclusive of surcharge of 2% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 41.20% (inclusive of education cess only).

(14) Inclusive of surcharge of 10% and education cess of 3%. Where the

total income is equal to or less than ` 1 crore, then tax rate is 30.90% (inclusive of education cess only).

(15) Inclusive of surcharge of 12% and education cess of 3%. Where the total income is equal to or less than ` 1 crore, then tax rate is 30.90% (inclusive of education cess only).

(16) Inclusive of surcharge of 10% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 20.008% (inclusive of surcharge of 5% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 19.055% (inclusive of education cess only).

(17) Inclusive of surcharge of 12% and education cess of 3%. Where the total income is between ` 1 crore and ` 10 crore, then tax rate is 20.389% (inclusive of surcharge of 7% and education cess of 3%). Where the total income is equal to or less than ` 1 crore, then tax rate is 19.055% (inclusive of education cess only).

Deferment of provisions relating to General Anti Avoidance Rule (GAAR) – Section 95

The existing provisions of GAAR are contained in Chapter X-A (Sections 95 to 102) and Section 144BA of the Income Tax Act, 1961 (IT Act). Chapter X-A provides the substantive provision of GAAR whereas Section 144 BA provide for the procedures to be under-taken for invoking GAAR and passing an assessment order invoking such provisions.

Concerns had been expressed regarding certain aspects of GAAR. India is an active participant of Base Erosion and Profit Shifting (BEPS) project of the Organisation for Economic Cooperation and Development (OECD) and the report on aspects of BEPS and measures to counter it is awaited.

23 B. K. Khare & Co.

INDIA’S UNION BUDGET

In the light of the said circumstances the implementation of GAAR has been deferred by two years and made applicable to income of the FY 2017-18 (AY 2018-19), as a measure to promote domestic industry and improve investment climate.

The amendment is proposed to effective from 1 April 2015.

[Clause 25]

Abolition of Wealth Tax

Currently wealth tax is levied on Individual, HUF or Company if net wealth of the person exceeds ` 30 lakhs on the last date of the previous year. Only few specified assets are taken into account for the purpose of computing net wealth.

The collection of wealth tax has not shown any buoyancy and has cast a disproportionately high compliance burden on the assessee and administrative burden on the department.

It is therefore proposed to abolish levy of wealth tax with effect from 1 April 2016 (AY 2016-17) onwards and an enhanced surcharge is proposed on taxpayers earning higher income. The details of levy of enhanced surcharge are given under rates of taxes.

[Clause 79]

Special Tax regime for Category I and Category II Alternative Investment Funds – Sections 115U and 115UA

Existing Section 10(23FB) of the Income Tax Act exempts from taxation any income of a Venture Capital Company (VCC) or a Venture Capital Fund (VCF) from investments in a Venture Capital Undertaking (VCU).

Section 115U of the Act provides that income accruing or arising to or received by a person out of investment made in a VCC or VCF shall be taxable in the same manner on a current year basis as if the person had made a direct investment in a VCU.

Theses sections provide a tax pass through (i.e. income is taxable in the hands of the investors instead of VCF/VCC) only to the funds, being set up as a company or trust, which are registered under SEBI Regulations as VCF before 21 May 2012 or Category I Alternative Investment Fund (AIF) regulated by SEBI (AIF) Regulations w.e.f. 21 May 2012.

Under the AIF Regulations various types of AIFs have been classified under three categories I, II and III AIFs. These AIFs can be set up as a trust, company limited liability partnership or any other body corporate. Category I AIFs invest in start up or early stage ventures or social ventures or SMEs or infrastructure or other sectors or in areas which the Government or Regulators consider as socially or economically desirable. Category II AIFs are funds including Private Equity Funds or Debt Funds which do not fall in Category I and III AIFs and which do not undertake leverage or borrowings other than for meeting day to day operational requirements. Category III AIFs are funds which employ diverse or complex trading strategies and may employ leverage.

It is proposed to provide a special tax regime to rationalise the taxation of Category I and II AIFs.

The salient features of tax regime are:

i. Income of the unit holder of investment fund shall be chargeable to tax in the same manner as if it were income accruing or arising had the investment been made directly by him.

ii. Income in the hands of investment fund other than profits and gains of business shall be exempt from tax. Income of the investment fund in the nature of Profits and gains shall be taxable in its hands.

iii. Income of the same nature as Profits and gains at the Investment Fund level

INDIA’S UNION BUDGET

B. K. Khare & Co. 24

would be exempt in the hands of the investor.

iv. Any income other than income taxable at the Investment fund level and which is payable to a unit holder by an Investment fund shall attract tax deduction at source (TDS) at the rate of ten percent and the fund is obligated to deduct tax at source.

v. Income paid or credited by the Investment fund shall be deemed to be of the same nature and in the same proportion in the hands of the unit holder as if it had been received by or had accrued or arisen to the Investment fund.

vi. If there is a loss at the fund level which is either current or which has remained to be set off then the loss would be carried over at the fund level for set off against income of the succeeding year in accordance with the provisions of Chapter VI of Income Tax Act. The loss shall not allowed pass through to the investors.

vii. Provisions of Chapter XII-D (Dividend Distribution Tax) or Chapter XII-E (Tax on distributed income) shall not apply to income paid by an Investment fund to its unit holders.

viii. Income received by an Investment fund is to be exempt from TDS requirement. An appropriate notification under Section 197A(1F) is proposed to be issued subsequently for the said purpose.

ix. The Investment fund will be mandatorily required to file its return of income. The fund is required to provide the prescribed income tax authority and the investors the details of various components of its income.

x. The existing pass through regime is proposed to continue to apply to a

VCF/VCC registered under SEBI VCF Regulations 1996. Other VCFs viz. Categories I and II AIFs would be subject to the new pass through regime.

xi. In Section 115UA, reference to Clause (23 FCA) Section 10 is proposed to be inserted after reference to Clause (23FC) of Section 10.

[Clauses 30, 31 & 32]

Residence in India – Section 6

Section 6 lays down the conditions to be satisfied for a person to be treated as a ‘resident’ in India.

Explanation to Section 6(1), among others, defines the residential status of an Indian citizen, being a member of the crew of an Indian ship, who leaves India in any previous year.

It is now proposed to amend the section to also deal with the situation of an Indian citizen being a member of the crew of a foreign bound ship (as opposed to foreign bound Indian ship) leaving India.

It is proposed that in this case the period or periods of stay in India shall, in respect of such voyage, be determined in the manner and subject to such conditions as may be prescribed.

This amendment will take retrospective effect from 1 April 2015 and will apply to AY 2015-16 and subsequent years.

Section 6(3) deals with the residential status of a company.

At present, to be categorised as a ‘resident in India, one basic condition is that the company should be an Indian company. Alternatively, during that year the control and management of its affairs should be situated wholly in India.

Thus, if the control and management was shown to be either not wholly in India or not in India during the whole of the year,

25 B. K. Khare & Co.

INDIA’S UNION BUDGET

residence could be shifted outside India thereby affecting the ambit of taxation of the income of such companies.

It is proposed that a company will be a resident in India if its place of effective management, at any time in that year, is in India.

“Place of effective management” is defined to mean a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance, made.

With this amendment provisions of the IT Act would be aligned with those of the DTAA entered into by India with other countries and would also be line with the principles recognised and accepted by OECD.

The aim of this amendment is stated to be to deal with cases of creation of shell companies incorporated outside India but effectively controlled from India. This amendment could have far reaching consequences.

[Clause 4]

Income deemed to accrue or arise in India – Section 9

Indirect Transfers This is one of amendments which has been categorised under ‘Ease of doing business/Dispute resolution’ and is stated to be based on the recommendations of the Expert Committee headed by Dr. Parthasarathi Shome.

The Finance Act, 2012 inserted Explanation 5 in Section 9(1)(i) which deals with income deemed to accrue or arise in India. The said explanation, inserted with retrospective effect from 1 April 1962, clarified that an asset or capital asset, being any share or interest in a company or entity registered or incorporated outside India shall be deemed to be situated in India if the value of share or interest is derived directly or indirectly substantially from the assets located in India.

The explanation was inserted with retrospective effect to overcome the decision in the case of Vodafone (341 ITR 1) wherein Honourable Supreme Court had held that transfer of shares of a foreign company which has an Indian Company as its subsidiary does not amount to transfer of any capital asset situated in India within meaning of fourth limb of Section 9(1)(i).

Subsequently the issue and applicability of said Explanation 5 came up for consideration before the Hon’ble Delhi High Court in the case of Copal Research Ltd., Mauritius 226 Taxman 226. The Delhi High Court referred to the substance of what the Explanation sought to achieve viz. charge of tax on the transfer of an asset where “in substance the assets in India are transacted by transacting in shares of overseas holding companies”. The Hon’ble Court expressed its view that a transfer of shares of foreign companies would not in substance be held to be a transfer of underlying Indian assets unless at least 50% of the value of such shares is derived from assets held in India. The Delhi High Court inter alia referred to the OECD Model Tax Convention on Income and on Capital to add a persuasive and not conclusive value and it was mentioned that the taxation rights in case of sale of shares are ceded to the country where the underlying assets are situated only if more than 50% of the value of such shares is derived from such property. The High Court also made a reference to the Shome Committee Report and the Direct Tax Code, 2010, wherein the term ‘substantially’ was considered to mean a threshold of 50% of the total value derived from assets of the entity. Based on the aforesaid reference, the Court concluded that the term ‘substantially’ has been used to define the threshold of attracting indirect transfer provisions and the term was synonymous to ‘principally’, ‘mainly’ or at least ‘majority’. Therefore, the Court held that gains arising from transfer of shares of an overseas company, which derives its

INDIA’S UNION BUDGET

B. K. Khare & Co. 26

value less than 50% of assets situated in India would not be taxable in India under Section 9(1)(i) of the Income Tax Act.

In order to give effect to the recommendations of expert committee under Chairmanship of Dr. Parthasarathy Shome amendments have been proposed in Section 9(1)(i) and Sections 47, 49 and 271GA, 273B and 285A.

The Finance Act, 2012 inserted certain clarificatory amendments in the provisions of Section 9 one of which was insertion of Explanation 5 in Section 9(1)(i), with retrospective effect from 1 April 1962.

This Explanation clarified that an asset or capital asset, being any share or interest in a company or entity registered or incorporated outside India shall be deemed to be situated in India if the share or interest derives, directly or indirectly, its value substantially from assets located in India.

It is now proposed that the share or interest of a foreign company or entity shall be deemed to derive its value substantially from the assets (whether tangible or intangible) located in India, if on the specified date, the value of Indian assets (a) exceeds the amount of ten crore rupees and (b) represents at least fifty per cent of the value of all the assets owned by the company or entity.

Value of an asset would be the gross value (without reduction of liabilities in respect of such assets) to be determined in the manner prescribed in the Rules.

Specified date is proposed to means (i) date on which the accounting period of the company or, as the case may be, the entity ends preceding the date of transfer of a share or an interest; or (ii) date of transfer, if the book value of the assets of the company or, as the case may be, the entity on the date of transfer exceeds the book value of the assets as on the date referred to in Sub-clause (i), by fifteen per cent.

The expression “Accounting period” is defined to cater to different situations.

The rigors of Explanation 5 are further proposed to be reduced by providing that the said deeming provision of indirect transfer will not apply in the case of a non-resident from transfer, outside India, of any share of, or interest in, a company or an entity, registered or incorporated outside India:

(i) if such company or entity directly owns the assets situated in India;

(ii) the transferor [whether individually or along with its associated enterprises (as defined in Section 92A)], at any time in the twelve months preceding the date of transfer, neither holds the right of management or control in relation to such company or entity, nor holds voting power or share capital or interest exceeding five per cent of the total voting power or total share capital or total interest, as the case may be, of such company or entity;

OR

a. if such company or entity indirectly owns the assets situated in India, and,

b. the transferor (whether individually or along with its associated enterprises), at any time in the twelve months preceding the date of transfer, neither holds the right of management or control in relation to such company or entity, nor holds any right in, or in relation to, such company or entity which would entitle him to the right of management or control in the company or entity that directly owns the assets situated in India,

c. nor holds such percentage of voting power or share capital or interest in such company or entity which results in holding of (either individually or along with associated enterprises) a voting power or share capital or interest exceeding five per cent of the total

27 B. K. Khare & Co.

INDIA’S UNION BUDGET

voting power or total share capital or total interest, as the case may be, of the company or entity that directly owns the assets situated in India.

It is further proposed that in a case where all the assets owned, directly or indirectly, by a company or, as the case may be, an entity referred to in the Explanation 5, are not located in India, the income of the non-resident transferor, from transfer outside India of a share of, or interest in, such company or entity, deemed to accrue or arise in India under this clause, shall be only such part of the income as is reasonably attributable to assets located in India and determined in such manner as may be prescribed.

By including ownership etc. of right of management or control through an associated enterprise as defined in Section 92A, the net is cast very wide to attract the provisions of Explanation 5 to Section 9(1)(i).

[Clause 5]

Allied to above certain amendments have been proposed in the regime of taxation of capital gains.

Following clauses are proposed to be inserted in Section 47 which deals with transactions not regarded as transfer of capital assets.

Clause (viab) – Any transfer of shares referred to in Explanation 5 to Section 9(1)(i) whose value is derived substantially directly or indirectly from shares of an Indian company, in a scheme of amalgamation by the amalgamating foreign company to the amalgamated foreign company would not be regarded as transfer if:

(A) at least twenty five per cent of the shareholders of the amalgamating foreign company continue to remain shareholders of amalgamated foreign company.

(B) such transfer of share does not attract capital gains in the country in which the amalgamating company is incorporated.

Clause (vicc) – Any transfer of share referred to in Explanation 5 to Section 9(1)(i) whose value is derived substantially directly or indirectly from shares of an Indian company, in a demerger by a demerged foreign company to the resulting foreign company would not be regarded as transfer if:

(a) the shareholders holding not less than three fourths in value of the shares of the demerged foreign company continue to remain shareholders of the resulting foreign company.

(b) such transfer of share does not attract capital gains in the country in which the resulting company is incorporated.

(c) Provisions of Sections 391 to 394 of the Companies Act, 1956 shall not apply in case of demerger referred to in this Clause.

[Clause 13]

Section 9(1)(v) deals with deemed accrual in India of Interest

It is proposed to provide that in the case of a non-resident, being a person engaged in the business of banking, any interest payable by the permanent establishment (as defined in Section 92F(iiia) in India of such non-resident to the head office or any permanent establishment or any other part of such non-resident outside India, shall be deemed to accrue or arise in India and shall be chargeable to tax in addition to any income attributable to the permanent establishment in India.

It is also proposed that the permanent establishment in India shall be deemed

INDIA’S UNION BUDGET

B. K. Khare & Co. 28

to be a person separate and independent of the non-resident person of which it is a permanent establishment and the provisions of the Act relating to computation of total income, determination of tax and collection and recovery shall apply accordingly;

Such interest would however be entitled to be deducted as expenditure in computing the income of the permanent establishment in India.

[Clause 5]

Permanent Establishment – eligible investment fund – Section 9A

A new Section 9A – is proposed to be inserted to provide that in the case of an ‘eligible investment fund’ fund management activity carried out through an eligible fund manager acting on behalf of such fund would not constitute business connection in India.

It is further proposed that an eligible investment fund shall not be said to be resident in India for the purpose of Section 6 merely because the eligible fund manager, undertaking fund management activities on its behalf, is situated in India.

An eligible investment fund has been defined to mean a fund established or incorporated or registered outside India, which collects funds from its members for investing it for their benefit and fulfils several stringent conditions (including that it is not a person resident in India; it is a resident of a country with whom India has entered into DTAA; it does not carry on or control and manage, directly or indirectly, any business in India or from India etc.)

Similarly, an eligible fund manager has been defined to mean any person who is engaged in the activity of fund management and fulfils certain conditions (including that he should be acting in the ordinary course of his business as a fund manager etc.)

The Fund would be required to file an annual statement in respect of its activities in a financial year non furnishing of which would attract penalty of ` 5 lacs.

This amendment would of course not affect the taxability of the income of the Fund earned or accrued in India de hors the business connection in India constituted by the fund manager. Similarly, the scope of total income of the eligible fund manager or its determination would not be affected by this amendment.

This provision will help off shore funds in that tax liability in respect of income arising to the Fund would not be affected by the existence of a fund manager in India for making investments. Similarly, income of the Fund from investments outside India would not be taxable in India simply by reason of the fact fund management activity in respect of such investments has been undertaken through a fund manager located in India.

It is further proposed that these exclusions shall apply to income of the eligible investment fund, which would have been so included irrespective of whether the activity of the eligible fund manager constituted the business connection in India of such fund or not.

It is similarly provided that nothing contained in the proposed section shall have any effect on the scope of total income or determination of total income in the case of the eligible fund manager.

[Clause 6]

Allowance of balance 50% additional depreciation where assets used for less than 180 days – Section 32(1)(ii)

The assessee, engaged in manufacture/ production of articles or things or in the business of generation and distribution of power is currently entitled to additional depreciation of 20% on purchase and

29 B. K. Khare & Co.

INDIA’S UNION BUDGET

installation of new plant & machinery, subject to compliance of specified conditions. Where the asset was put to use for less than 180 days in a year, the said additional depreciation was allowed at 50% of such depreciation.

The existing provision was silent on the assessee’s claim for depreciation of balance 50% in the succeeding year. The view that an assessee is entitled to claim the deduction for the balance 50% depreciation in the succeeding year was upheld by the Cochin Tribunal, the Mumbai Tribunal and the Delhi Tribunal. The Chennai Tribunal however held otherwise.

An amendment is proposed to allow the balance 50% of the additional depreciation on new plant or machinery acquired and used for less than 180 days which has not been allowed in the year of acquisition and installation shall be allowed in the immediately succeeding previous year. This provision will take effect from the assessment year 2016-17.

[Clause 10]

Additional depreciation at the rate of 35% for setting up of manufacturing units in the notified backward area in Andhra Pradesh or Telangana – Section 32(1)(iia)

In order to incentivise acquisition and installation of plant and machinery for setting up of manufacturing units in the notified backward area in Andhra Pradesh or Telangana, it is proposed to allow higher additional depreciation at the rate of 35% (instead of 20%) in respect of the actual cost of new machinery or plant (other than a ship and aircraft) acquired and installed by a manufacturing undertaking or enterprise which is set up in the notified backward area on or after the 1 April 2015. This higher additional depreciation shall be available in respect of new plant or machinery acquired and installed during the period beginning on 1 April 2015 and ending before 1 April 2020.

[Clause 10]

Additional investment allowance for setting up of manufacturing units in the notified backward area of Andhra Pradesh or Telangana – Section 32AD

Section 32AC was inserted by the Finance Act, 2013 in order to encourage substantial investment in plant and machinery by companies engaged in the business of manufacture or production of any article or thing. Deduction allowable under Section 32AC is 15% of actual cost of new plant and machinery, subject to compliance of certain specified conditions.

A new Section 32AD is proposed to be inserted in order to encourage the setting up of industrial undertaking in the backward areas of Andhra Pradesh and Telangana. The additional investment allowance would be 15% of the cost of new asset acquired and installed by an assessee, if:

YY The undertaking or enterprise engaged in manufacture or production of any article or thing is set up after 1 April 2015 in the notified backward areas of Andhra Pradesh and Telangana, and.

YY the new assets are acquired and installed during the period between 1 April 2015 and 31 March 2020.