Bisk Chapter 8 – Leases. Definitions Lessor - lease payment are made by lessee to Lessor –Lessor...

29

Bisk Chapter 8 – Leases

-

Upload

alban-briggs -

Category

Documents

-

view

230 -

download

1

Transcript of Bisk Chapter 8 – Leases. Definitions Lessor - lease payment are made by lessee to Lessor –Lessor...

Bisk Chapter 8 – Leases

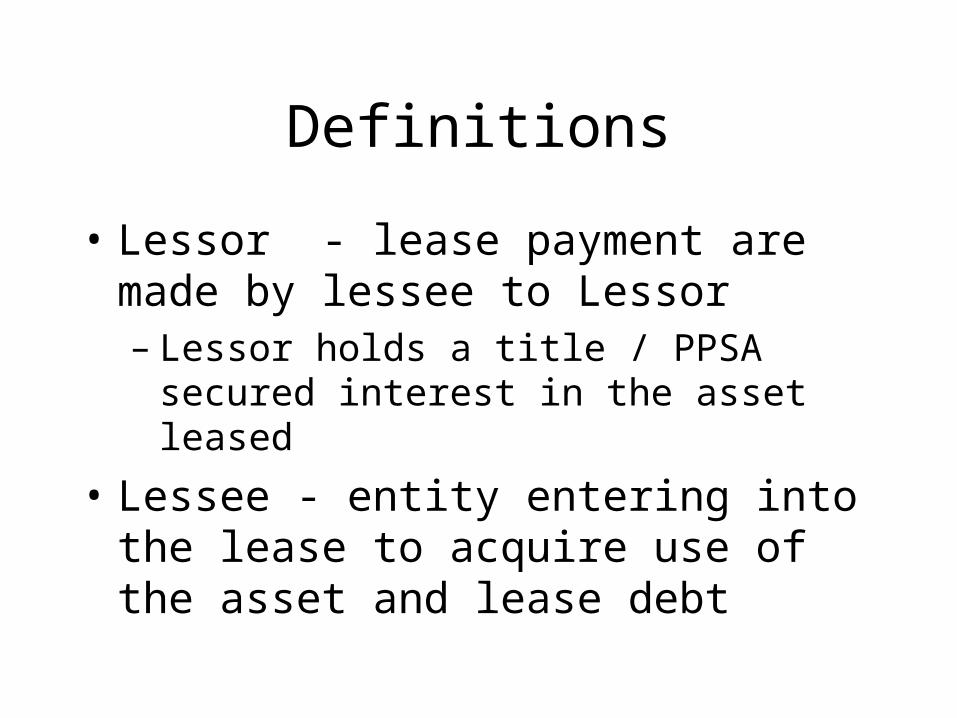

Definitions

• Lessor - lease payment are made by lessee to Lessor – Lessor holds a title / PPSA secured interest in

the asset leased

• Lessee - entity entering into the lease to acquire use of the asset and lease debt

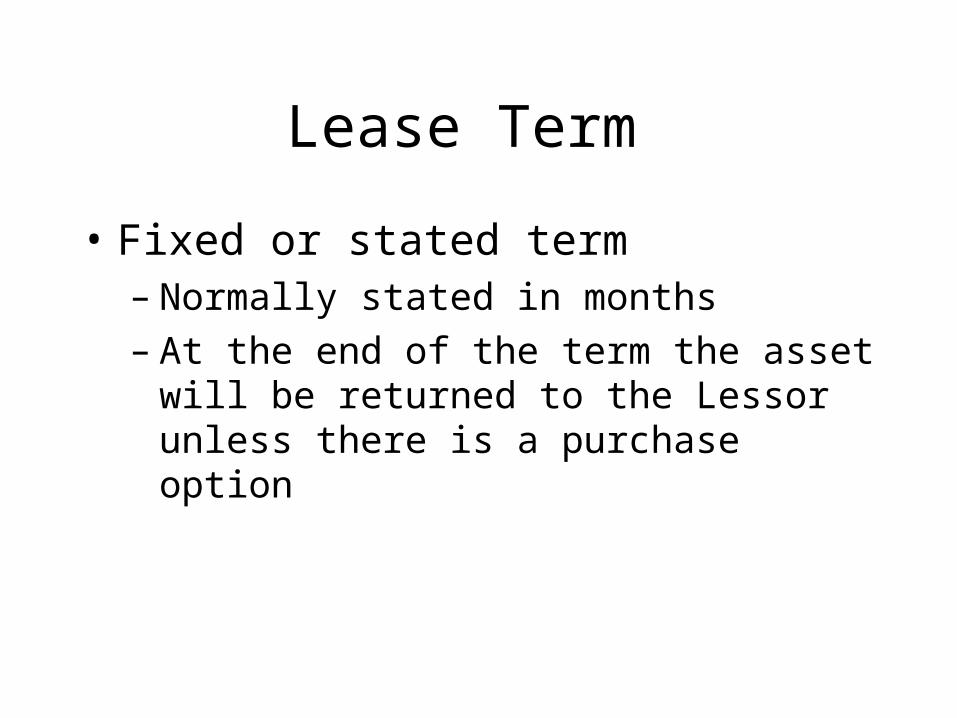

Lease Term

• Fixed or stated term– Normally stated in months– At the end of the term the asset will be returned

to the Lessor unless there is a purchase option

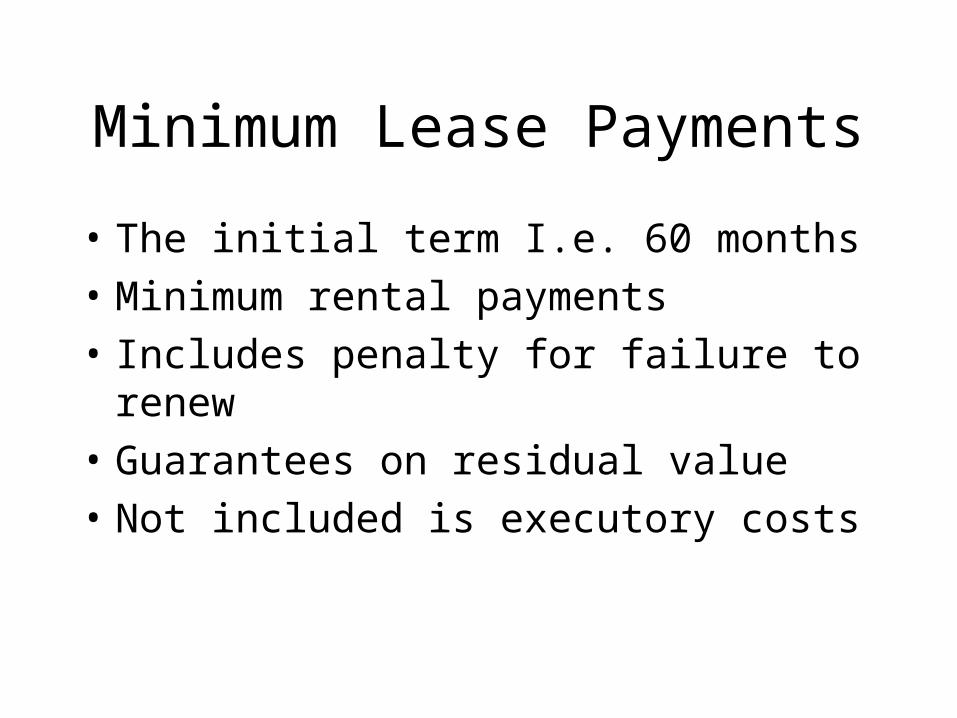

Minimum Lease Payments

• The initial term I.e. 60 months

• Minimum rental payments

• Includes penalty for failure to renew

• Guarantees on residual value

• Not included is executory costs

Executory costs

• Insurance

• R & M

• Taxes

• Required to be paid during term of the lease.

• Failure to pay executory cost is a breech of contract.

Present Values

• Incremental borrowing rate • Implicit interest rate during terms of lease

remains constant• Discount rate that would result in the

transfer of title at the end of the lease = implicit interest rate

• Must know cash price of asset to determine implicit interest rate.

Residual Value

• Estimate FMV at the end of the lease

• To be profitable for Lessor – residual values must be certain.

• If residual values are uncertain – the Lessor will loose money, i.e. GM / Ford out of lease business now

• Guaranteed (option) and unguaranteed

Cont…

• Unguaranteed residual values are not part of minimum lease payments

• Guaranteed RV is included in MLP (if – then scenario - deficiencies)

Termination

• Exit or disposal plan

• SFAS requires recognition of lease termination costs in period when obligations to others exist, not necessarily commencing in the period of commitment to a plan.

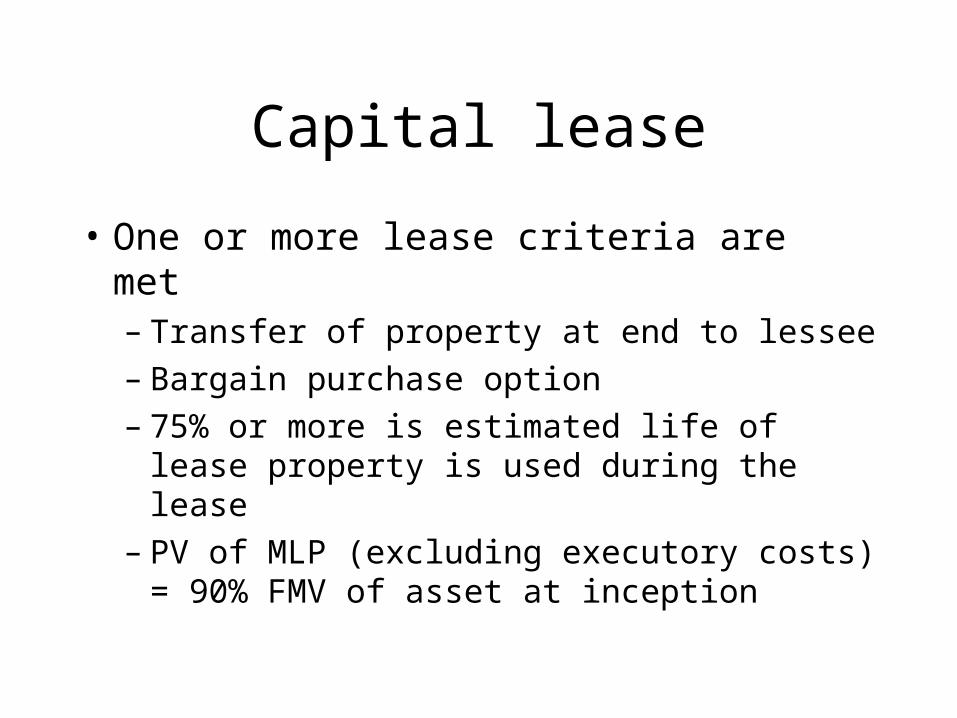

Capital lease

• One or more lease criteria are met– Transfer of property at end to lessee– Bargain purchase option– 75% or more is estimated life of lease property

is used during the lease– PV of MLP (excluding executory costs) = 90%

FMV of asset at inception

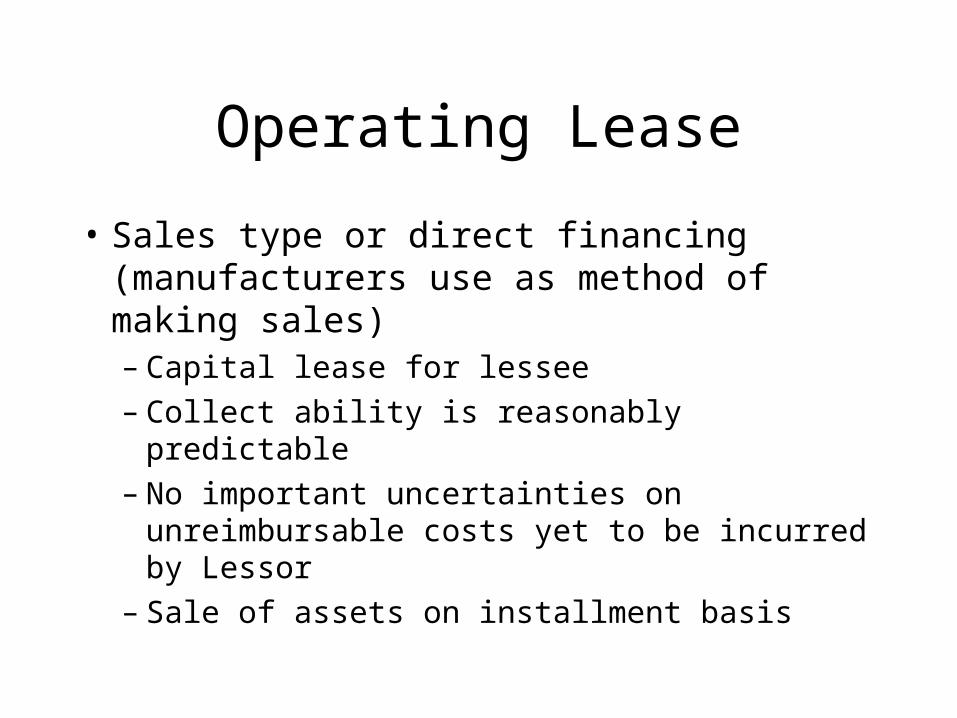

Operating Lease

• Sales type or direct financing (manufacturers use as method of making sales)– Capital lease for lessee– Collect ability is reasonably predictable– No important uncertainties on unreimbursable

costs yet to be incurred by Lessor– Sale of assets on installment basis

Exhibit 2

• Capital Lease Criteria page 6-5

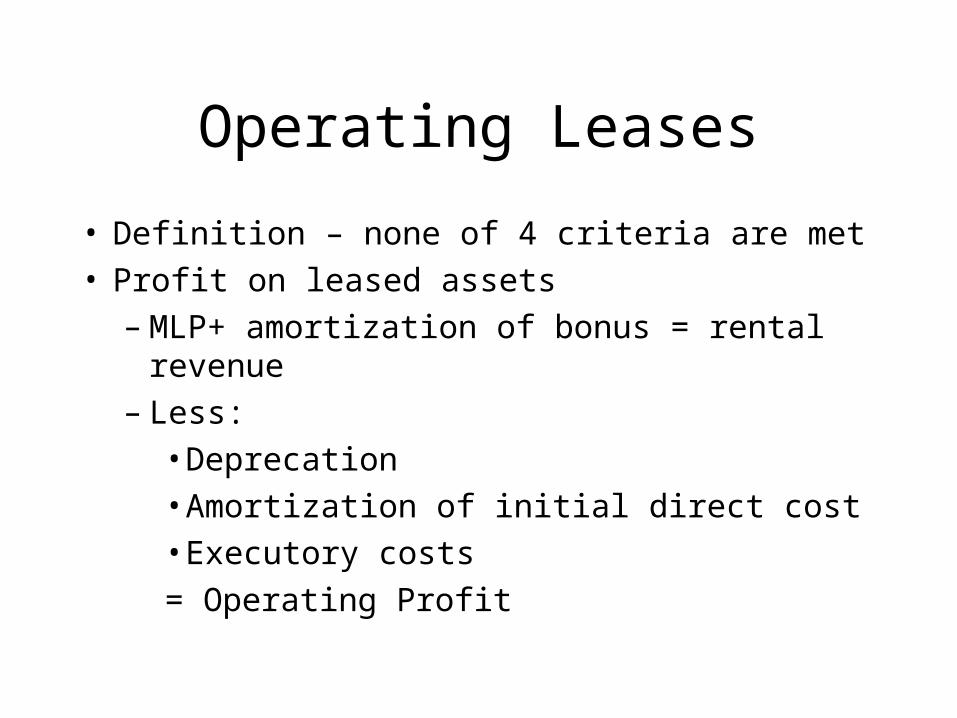

Operating Leases

• Definition – none of 4 criteria are met• Profit on leased assets

– MLP+ amortization of bonus = rental revenue– Less:

• Deprecation• Amortization of initial direct cost• Executory costs

= Operating Profit

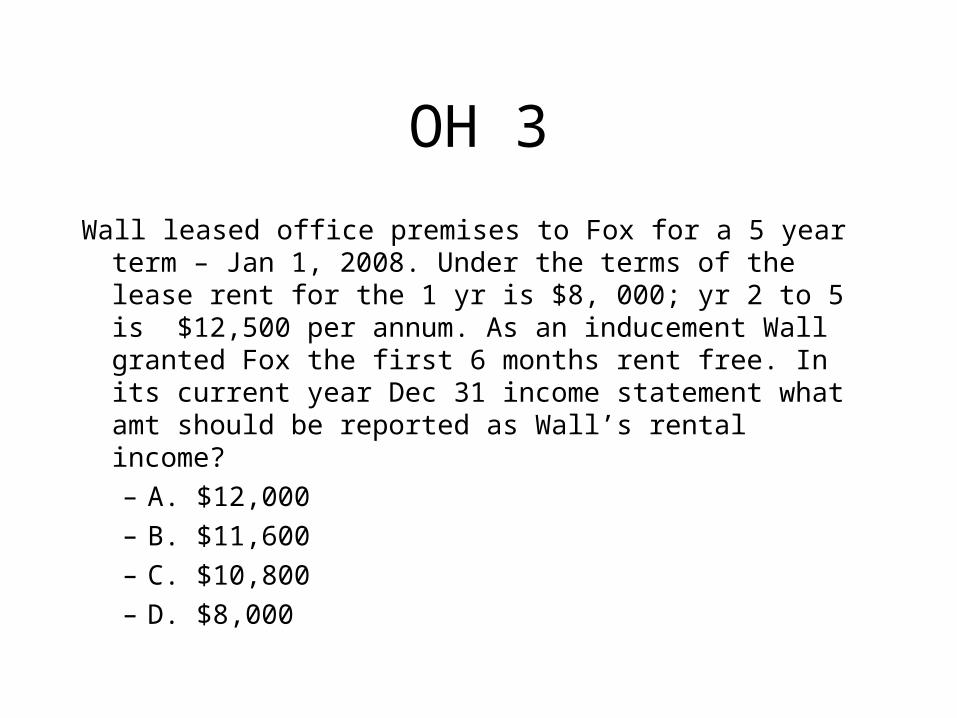

OH 3

Wall leased office premises to Fox for a 5 year term – Jan 1, 2008. Under the terms of the lease rent for the 1 yr is $8, 000; yr 2 to 5 is $12,500 per annum. As an inducement Wall granted Fox the first 6 months rent free. In its current year Dec 31 income statement what amt should be reported as Wall’s rental income?

– A. $12,000

– B. $11,600

– C. $10,800

– D. $8,000

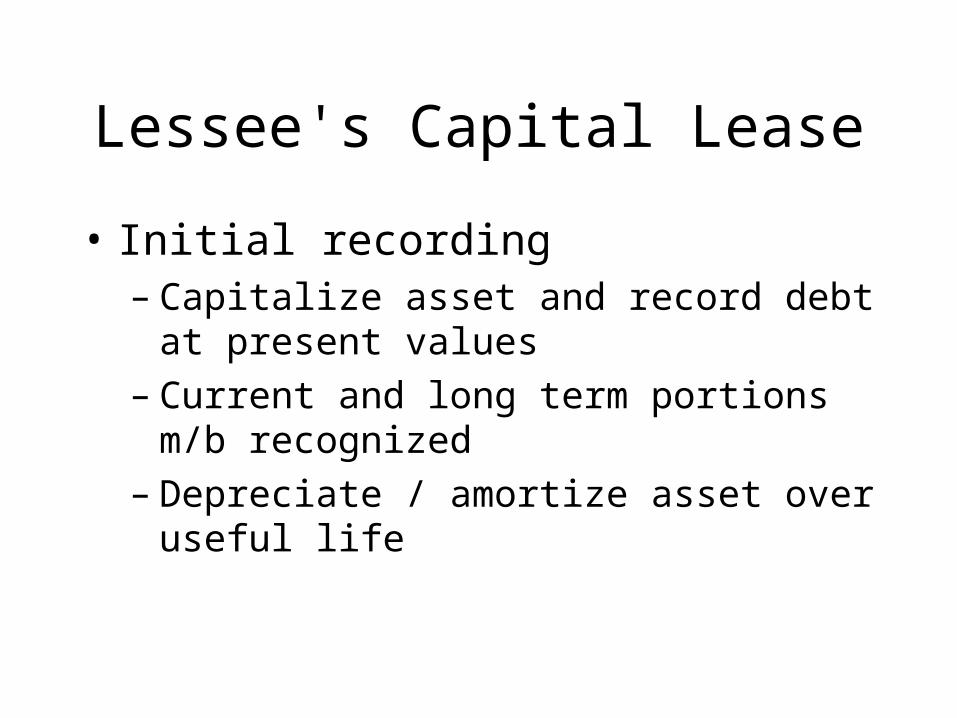

Lessee's Capital Lease

• Initial recording– Capitalize asset and record debt at present

values– Current and long term portions m/b recognized– Depreciate / amortize asset over useful life

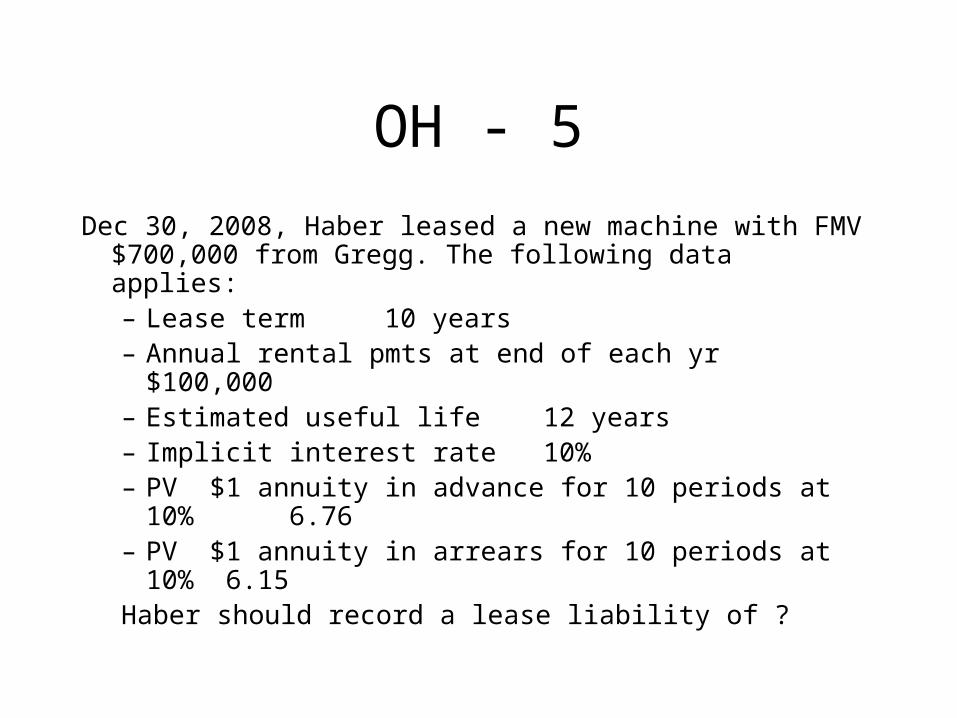

OH - 5

Dec 30, 2008, Haber leased a new machine with FMV $700,000 from Gregg. The following data applies:– Lease term 10 years– Annual rental pmts at end of each yr $100,000– Estimated useful life 12 years– Implicit interest rate 10%– PV $1 annuity in advance for 10 periods at 10%

6.76– PV $1 annuity in arrears for 10 periods at 10% 6.15

Haber should record a lease liability of ?

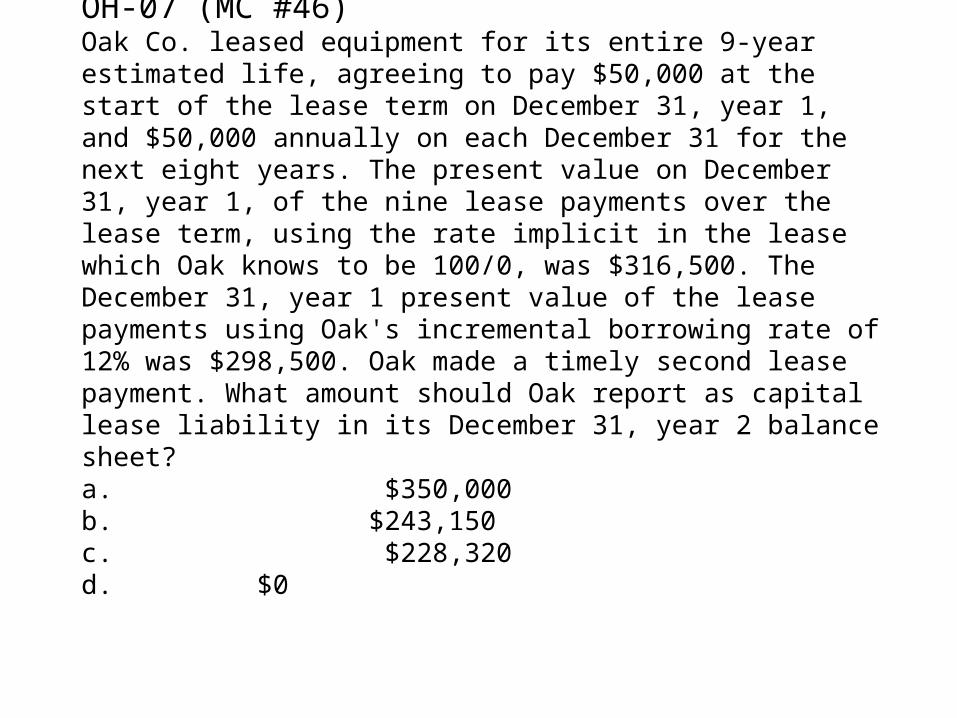

OH-07 (MC #46) Oak Co. leased equipment for its entire 9-year estimated life, agreeing to pay $50,000 at the start of the lease term on December 31, year 1, and $50,000 annually on each December 31 for the next eight years. The present value on December 31, year 1, of the nine lease payments over the lease term, using the rate implicit in the lease which Oak knows to be 100/0, was $316,500. The December 31, year 1 present value of the lease payments using Oak's incremental borrowing rate of 12% was $298,500. Oak made a timely second lease payment. What amount should Oak report as capital lease liability in its December 31, year 2 balance sheet? a. $350,000 b. $243,150 c. $228,320 d. $0

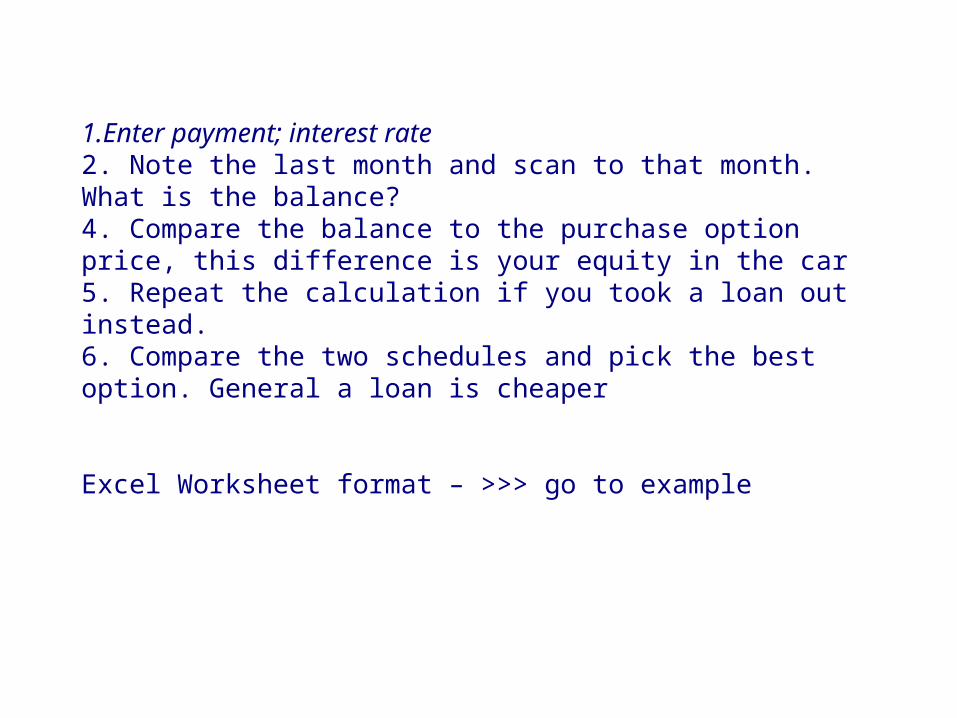

1.Enter payment; interest rate2. Note the last month and scan to that month. What is the balance?4. Compare the balance to the purchase option price, this difference is your equity in the car5. Repeat the calculation if you took a loan out instead.6. Compare the two schedules and pick the best option. General a loan is cheaper

Excel Worksheet format – >>> go to example

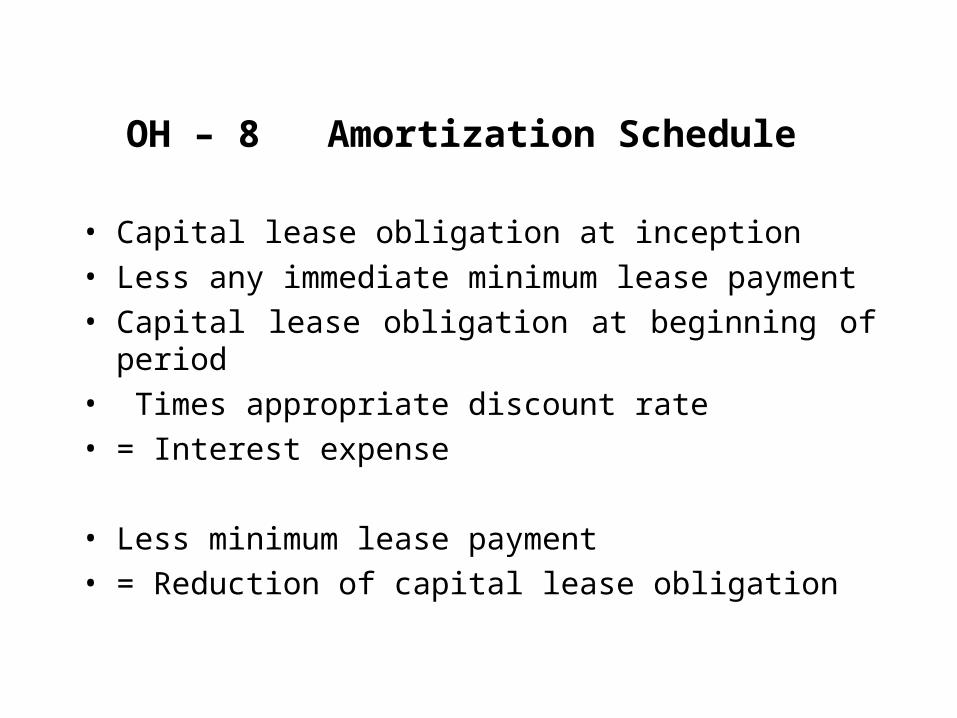

OH – 8 Amortization Schedule

• Capital lease obligation at inception • Less any immediate minimum lease payment • Capital lease obligation at beginning of period• Times appropriate discount rate • = Interest expense

• Less minimum lease payment

• = Reduction of capital lease obligation

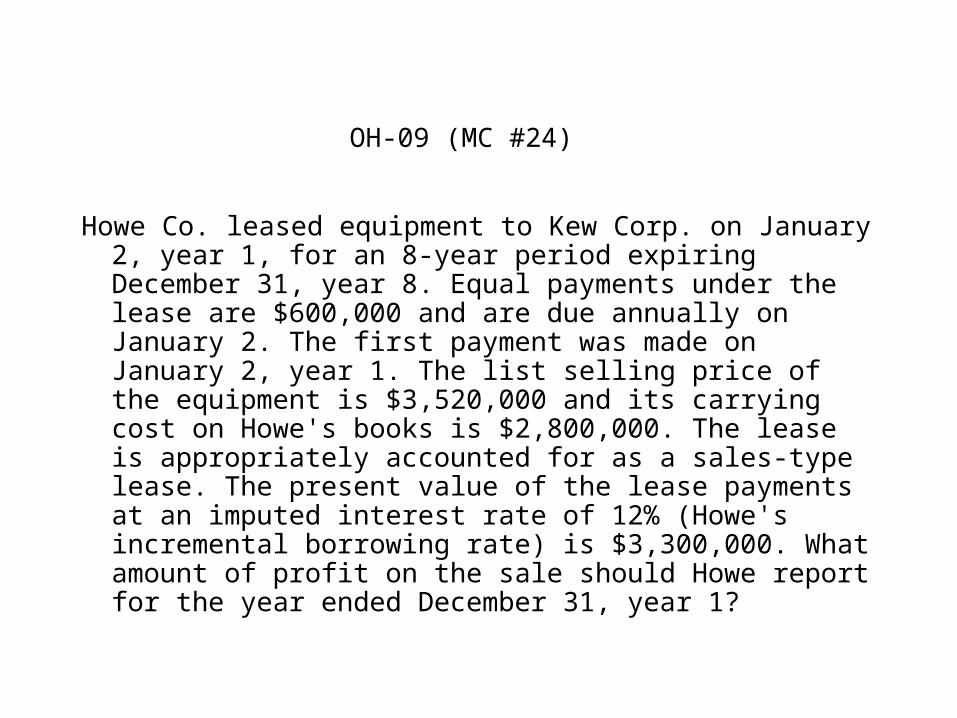

OH-09 (MC #24)

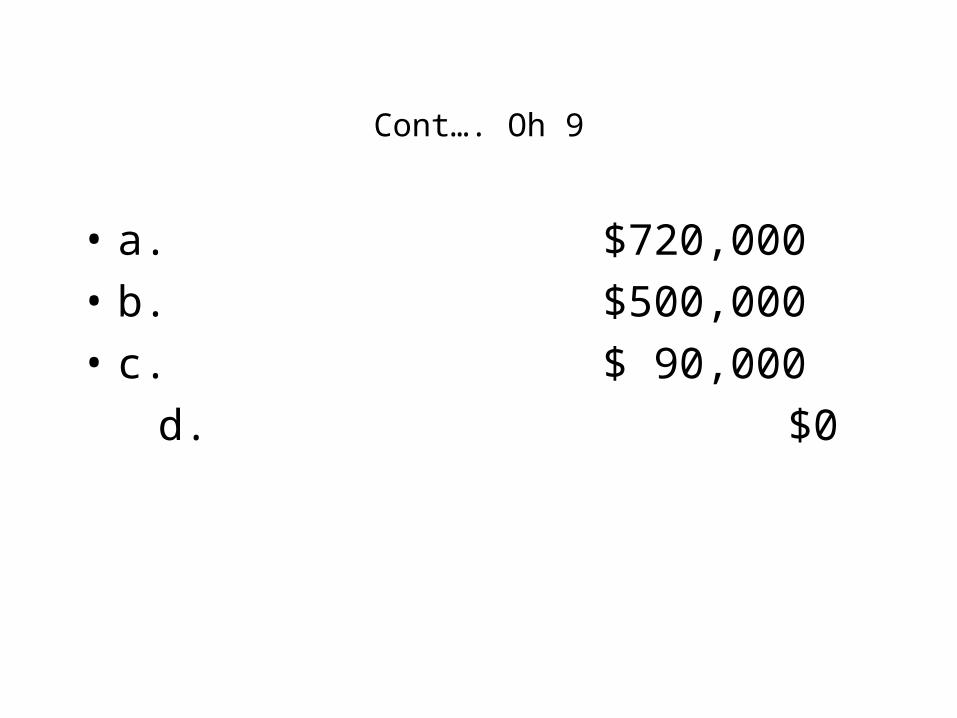

Howe Co. leased equipment to Kew Corp. on January 2, year 1, for an 8-year period expiring December 31, year 8. Equal payments under the lease are $600,000 and are due annually on January 2. The first payment was made on January 2, year 1. The list selling price of the equipment is $3,520,000 and its carrying cost on Howe's books is $2,800,000. The lease is appropriately accounted for as a sales-type lease. The present value of the lease payments at an imputed interest rate of 12% (Howe's incremental borrowing rate) is $3,300,000. What amount of profit on the sale should Howe report for the year ended December 31, year 1?

Cont…. Oh 9

• a. $720,000 • b. $500,000 • c. $ 90,000

d. $0

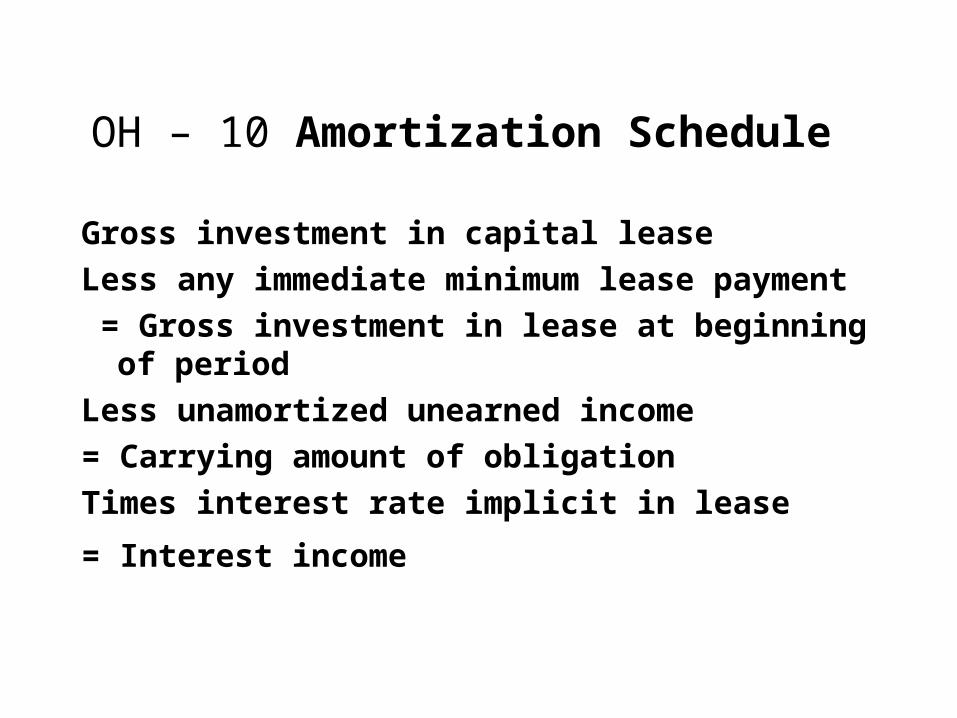

OH – 10 Amortization Schedule

Gross investment in capital lease

Less any immediate minimum lease payment

= Gross investment in lease at beginning of period

Less unamortized unearned income

= Carrying amount of obligation

Times interest rate implicit in lease

= Interest income

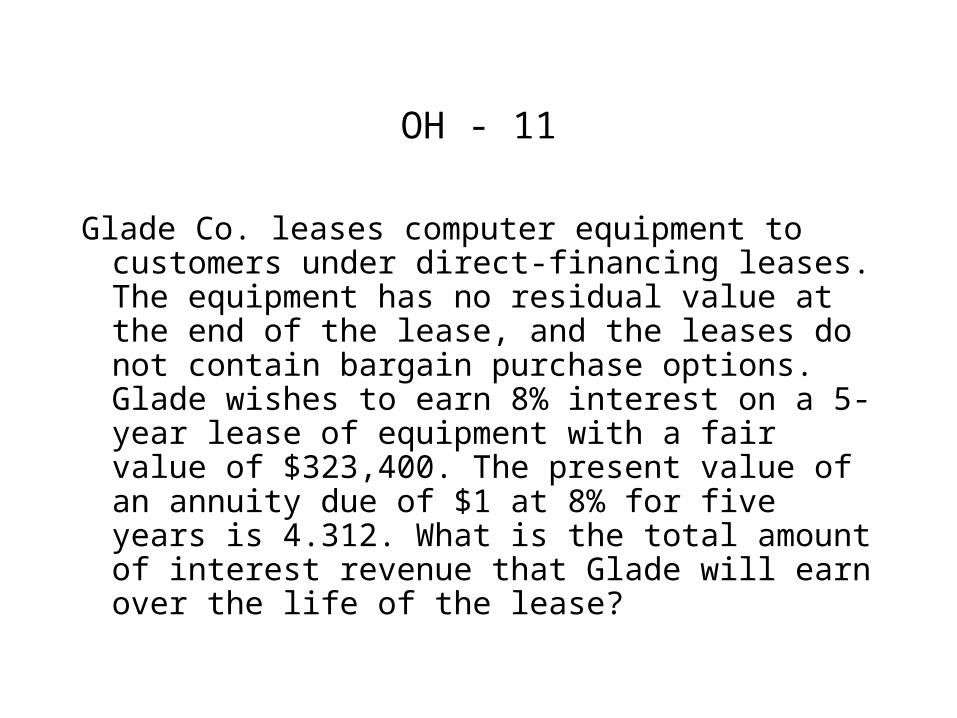

OH - 11

Glade Co. leases computer equipment to customers under direct-financing leases. The equipment has no residual value at the end of the lease, and the leases do not contain bargain purchase options. Glade wishes to earn 8% interest on a 5-year lease of equipment with a fair value of $323,400. The present value of an annuity due of $1 at 8% for five years is 4.312. What is the total amount of interest revenue that Glade will earn over the life of the lease?

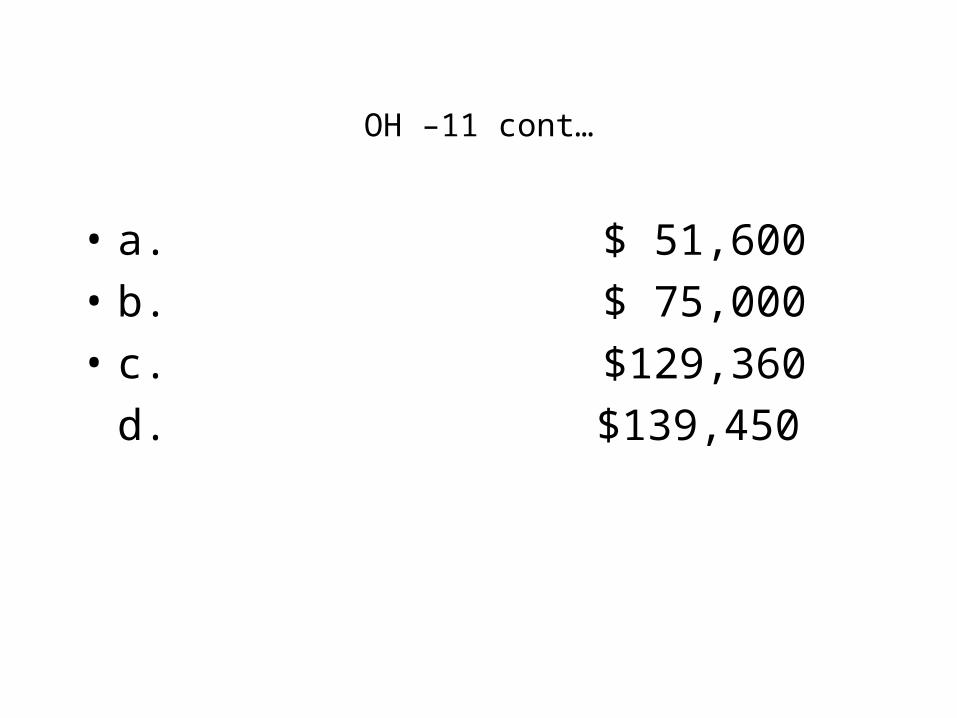

OH –11 cont…

• a. $ 51,600 • b. $ 75,000 • c. $129,360

d. $139,450

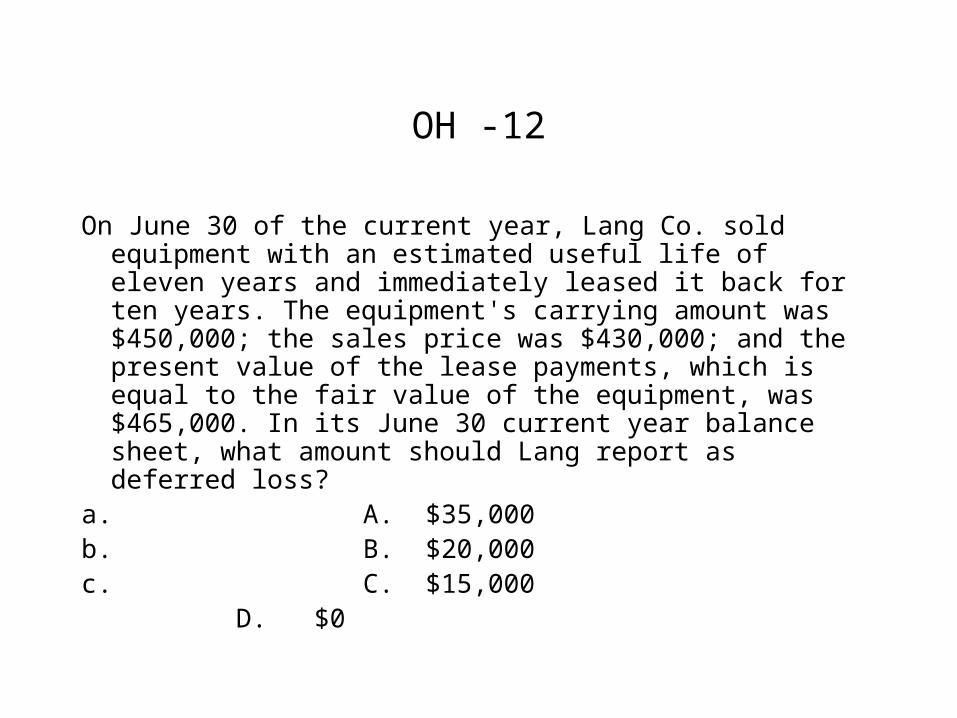

OH -12

On June 30 of the current year, Lang Co. sold equipment with an estimated useful life of eleven years and immediately leased it back for ten years. The equipment's carrying amount was $450,000; the sales price was $430,000; and the present value of the lease payments, which is equal to the fair value of the equipment, was $465,000. In its June 30 current year balance sheet, what amount should Lang report as deferred loss?

a. A. $35,000 b. B. $20,000 c. C. $15,000

D. $0

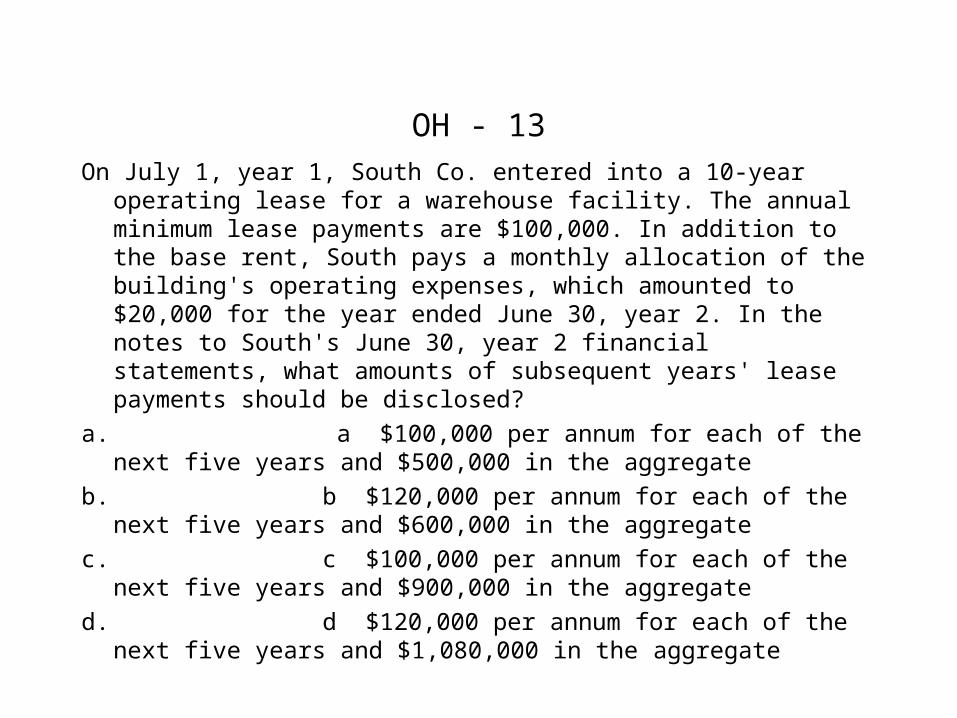

OH - 13

On July 1, year 1, South Co. entered into a 10-year operating lease for a ware house facility. The annual minimum lease payments are $100,000. In addition to the base rent, South pays a monthly allocation of the building's operating expenses, which amounted to $20,000 for the year ended June 30, year 2. In the notes to South's June 30, year 2 financial statements, what amounts of subsequent years' lease payments should be disclosed?

a. a $100,000 per annum for each of the next five years and $500,000 in the aggregate

b. b $120,000 per annum for each of the next five years and $600,000 in the aggregate

c. c $100,000 per annum for each of the next five years and $900,000 in the aggregate

d. d $120,000 per annum for each of the next five years and $1,080,000 in the aggregate

The end ch 8