Biomass Thermal Markets Outlook: 2012-2015€¦ · Biomass Thermal Markets Outlook: 2012-2015. ......

54

Biomass Thermal: Market Outlook 1 Biomass Thermal Markets Outlook: 2012-2015 This Webinar is brought to you by: Biomass Thermal Energy Council (BTEC) With the generous support of the U.S. Forest Service Wood Education Resource Center 2 PM ET, December 20, 2011 “The work upon which this publication is based was funded in whole or in part through a grant awarded by the Wood Education and Resource Center, Northeastern Area State and Private Forestry, U.S. Forest Service. This institution is an equal opportunity provider.”

Transcript of Biomass Thermal Markets Outlook: 2012-2015€¦ · Biomass Thermal Markets Outlook: 2012-2015. ......

Biomass Thermal: Market Outlook

1

Biomass Thermal Markets Outlook: 2012-2015

This Webinar is brought to you by:

Biomass Thermal Energy Council (BTEC)

With the generous support of the U.S. Forest Service

Wood Education Resource Center

2 PM ET, December 20, 2011

“The work upon which this publication is based was funded in whole or in part through a grant awarded by the Wood Education and Resource Center, Northeastern Area State and Private Forestry, U.S. Forest Service. This institution is an equal

opportunity provider.”

Biomass Thermal: Market Outlook

2

Joseph Seymour - Introductions

Executive Director - Biomass Thermal Energy Council (BTEC)

I. Introduction - Seymour

Biomass Thermal: Market Outlook

Quick notes

Two Audio Options: Streaming Audio and Dial-In.1. Streaming Audio/Computer

Speakers (Default)2. Dial-In: Use the Audio Panel

(right side of screen) to see dial- in instructions. Call-in separately from your telephone.

Ask questions using the Questions Panel on the right side of your screen.

The recording of the webinar and the slides will be available after the event. Registrants will be notified by email.

I. Introduction - Seymour

Biomass Thermal: Market Outlook

4

Speakers

Jeffrey Eppink, President, Enegis LLC Amanda Hamsley Lang, Operations Manager, Forisk ConsultingSeth Walker, Associate Economist, RISI Inc.; presenting for William Perritt, Senior Editor, RISI Inc.

Joseph Seymour, Executive Director, Biomass Thermal Energy Council

Moderator

I. Event Introduction - Seymour

Biomass Thermal: Market Outlook

5

Presentation OutlineI. Introduction – Joe SeymourII. Assessing Biomass Energy Supply – Jeffrey

EppinkIII. Technology and Markets – Amanda Hamsley LangIV. Market Drivers – Seth Walker for William PerrittV. Q&A – Joe SeymourVI. Resources and Future Events - Joe Seymour

[Full presentation will be available online, www.biomassthermal.org/resource/webinars.asp]

I. Event Introduction - Seymour

Biomass Thermal: Market Outlook

6

Introduction BTEC

Introduction to BTEC

The Biomass Thermal Energy Council (BTEC) is the industry trade association dedicated to advancing the use of biomass for heat and other thermal energy applications.

Why was BTEC established?1. To advocate for and promote the industry in the national energy policy debate2. To reach out to and educate the public and decision makers on the benefits

and advantages of using biomass for heat3. To develop biomass energy research and analysis that enables sound

investment and policy decisions

Biomass Thermal: Market Outlook

BTEC’s membership* * As of November 13, 2011

7

Introduction BTEC

Biomass Thermal: Market Outlook

8

BTEC Membership

I. Introducing BTEC - Seymour

Abundant Power Ernst Biomass Public Policy VirginiaACT Bioenergy Forest Energy Rainforest AllianceAFS Energy Systems FutureMetrics Ray AlbrightAlliance for Green Heat Green Clean Heat Recast EnergyAlternative Energy Solutions International Indeck Ladysmith Renewable Energy ResourcesAmerican Agriculture Movement Innovative Natural Resource Solutions Resource Professionals GroupAmerican Biomass Integrated Biomass Resources Richmond Energy AssociatesAmerican Wood Fibers International Renewable Energy Technology Institute Sandri CompaniesAPEX International WoodFuels Santa Energy CorporationBear Mountain Forest Products Jesse E. Lyman Pellets Sewall CompanyBiomass Combustion Systems Lignetics of Virginia Skanden EnergyBiomass Commodities Corporation Maine Energy Systems State University of New York ‐ Environmental Science and Forestry

Biomass Energy Resource Center Maine Pellet Fuels Association Tarm BiomassBiomass Energy Works Marth Twin Ports TestingBionera Resources Missouri Corn Merchandising Council University of British ColumbiaBiowood Energy Montana Community Development Corporation Vapor Locomotive CompanyChip Energy National Network of Forest Practitioners VecoplanClean Power Development New England Wood Pellet Vermont Sustainable Jobs FundComact Equipment New Horizon Vermont Wood PelletConfluence Energy Northeast Mill Services ViessmannContinental Biomass Industries PA Pellets West Oregon Wood ProductsControl Labs Pellet Technology USA Western Ag EnterprisesCorinth Wood Pellet Pelletco Westervelt Renewable EnergyCousineau Forest Products Piney Wood Pellets Wilson Engineering ServicesDejno's Plum Creek Wisconsin Energy Conservation CorporationEcostrat Pratt & Whitney Power Systems ‐ Turboden WoodmasterEnviva Materials Proe Power Systems Zilkha Biomass Energy

Biomass Thermal: Market Outlook

9

Project made possible by the USDA FS WERCBTEC awarded a grant from the USDA Forest Service’s Wood Education and Resource Center (WERC) in June 2010 to advance education and outreach on biomass thermal energy

The Center's mission is to work with the forest products industry toward sustainable forest products production for the eastern hardwood forest region.

Previous webinars available at: www.biomassthermal.org/resource.

All questions and attendee feedback will help form future activities.

Remember to answer the survey at the webinar’s conclusion!

I. Sponsoring Entity - Seymour

Biomass Thermal: Market Outlook

10

Jeffrey EppinkPresident, Enegis LLC

Assessing Biomass Energy Supply

II. Assessing Supply - Eppink

11

Biomass Energy Analytical Model

Assessing Biomass Energy SupplyPresented to the

Biomass Thermal Energy CouncilDecember 2011

Jeffrey Eppink, Enegis, LLC

Assessing Biomass Energy SupplyAssessing Biomass Energy SupplyPresented to the

Biomass Thermal Energy CouncilBiomass Thermal Energy CouncilDecember 2011

Jeffrey Eppink, Enegis, LLC

12

Biomass Energy Analytical Model

• BEAM was initially developed to support the Federal Energy Management Program

• Features– Assess biomass availability, transport options, and delivery cost– Models the biomass resource from field/forest, through

processing, to demand• Geographic resources quantification• Storage and densification options• Transportation costs

– Can be used for both site-specific, regional, or national-scale biomass assessments

• 30 m resolution for the lower 48 states• ~50 Species and commodities can be analyzed• Focuses on residual biomass, although dedicated energy crops can be

readily analyzed

– Costs, net energy and net carbon carried forward at all modeling steps

Biomass Energy Analytical ModelBBiomass iomass EEnergy nergy AAnalytical nalytical MModelodel

13

Biomass Energy Analytical Model

Species Data Source Species Data SourceAgriculture Residues: Agriculture Residues Cont:Hay All (Dry) USDA NASS Sweet Corn For Processing USDA NASSHay Alfalfa (Dry) USDA NASS Wheat Winter All USDA NASSRice All USDA NASSSorghum For Grain USDA NASSBarley All USDA NASS Woody Residues:Canola USDA NASS Logging Residue ‐ HardWood USDA FSCorn For Grain USDA NASS Logging Residue ‐ SoftWood USDA FSCotton Amer. Pima USDA NASS Forest Management Residue ‐ HardWood BAMF Hazardous FuelsCotton Upland USDA NASS Forest Management Residue ‐ SoftWood BAMF Hazardous FuelsBeans Dry Edible USDA NASS Coarse Wood Residue ‐ Hardwood BAMF Industrial Wood WasteWheat Durum USDA NASS Coarse Wood Residue ‐ Softwood BAMF Industrial Wood WasteFlaxseed USDA NASS Fine Wood Residue ‐ Hardwood BAMF Industrial Wood WastePeanuts for Nuts USDA NASS Fine Wood Residue ‐ Softwood BAMF Industrial Wood WastePotatoes All USDA NASS Urban Wood Waste ‐ Tree clippings Based on US Census Bureau PopulationHay Other (Dry) USDA NASSOats ‐ (Fall) USDA NASS Human Produced Wastes:Rye USDA NASS Wastewater Treatment Plants BAMF Anaerobic WWTPSafflower USDA NASS Landfills Producing Methane EPASoybeans USDA NASSSugarcane For Sugar USDA NASS Animal Manure:Sunflower All USDA NASS All Goats USDA NASS & HSIPSweet Potatoes USDA NASS Milk Cows USDA NASS & HSIPSugarbeets USDA NASS Beef USDA NASS & HSIPWheat Other Spring USDA NASS Hogs All USDA NASS & HSIPTobacco Air‐Cured Light Burley USDA NASS Sheep USDA NASS & HSIPTobacco Flue‐Cured Class 1 USDA NASS Layer USDA NASS & HSIPGreen Peas For Processing USDA NASS Broiler USDA NASS & HSIPSnap Beans For Processing USDA NASS Turkey USDA NASS & HSIP

Species Data Source Species Data SourceAgriculture Residues: Agriculture Residues Cont:Hay All (Dry) USDA NASS Sweet Corn For Processing USDA NASSHay Alfalfa (Dry) USDA NASS Wheat Winter All USDA NASSRice All USDA NASSSorghum For Grain USDA NASSBarley All USDA NASS Woody Residues:Canola USDA NASS Logging Residue ‐ HardWood USDA FSCorn For Grain USDA NASS Logging Residue ‐ SoftWood USDA FSCotton Amer. Pima USDA NASS Forest Management Residue ‐ HardWood BAMF Hazardous FuelsCotton Upland USDA NASS Forest Management Residue ‐ SoftWood BAMF Hazardous FuelsBeans Dry Edible USDA NASS Coarse Wood Residue ‐ Hardwood BAMF Industrial Wood WasteWheat Durum USDA NASS Coarse Wood Residue ‐ Softwood BAMF Industrial Wood WasteFlaxseed USDA NASS Fine Wood Residue ‐ Hardwood BAMF Industrial Wood WastePeanuts for Nuts USDA NASS Fine Wood Residue ‐ Softwood BAMF Industrial Wood WastePotatoes All USDA NASS Urban Wood Waste ‐ Tree clippings Based on US Census Bureau PopulationHay Other (Dry) USDA NASSOats ‐ (Fall) USDA NASS Human Produced Wastes:Rye USDA NASS Wastewater Treatment Plants BAMF Anaerobic WWTPSafflower USDA NASS Landfills Producing Methane EPASoybeans USDA NASSSugarcane For Sugar USDA NASS Animal Manure:Sunflower All USDA NASS All Goats USDA NASS & HSIPSweet Potatoes USDA NASS Milk Cows USDA NASS & HSIPSugarbeets USDA NASS Beef USDA NASS & HSIPWheat Other Spring USDA NASS Hogs All USDA NASS & HSIPTobacco Air‐Cured Light Burley USDA NASS Sheep USDA NASS & HSIPTobacco Flue‐Cured Class 1 USDA NASS Layer USDA NASS & HSIPGreen Peas For Processing USDA NASS Broiler USDA NASS & HSIPSnap Beans For Processing USDA NASS Turkey USDA NASS & HSIP

~50 Species/Commodities Incorporated~50 Species/Commodities Incorporated~50 Species/Commodities IncorporatedJan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Annual Total

Species: % % % % % % % % % % % % %Hay All (Dry) ‐ ‐ ‐ ‐ 10 20 30 20 10 10 ‐ ‐ 100Hay Alfalfa (Dry) ‐ ‐ ‐ ‐ 10 20 30 20 10 5 5 ‐ 100Rice All ‐ ‐ ‐ ‐ ‐ ‐ 10 20 40 30 ‐ ‐ 100Sorghum For Grain ‐ ‐ ‐ ‐ ‐ ‐ ‐ 10 15 45 30 ‐ 100Barley All ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Canola ‐ ‐ ‐ ‐ 20 30 30 20 ‐ ‐ ‐ ‐ 100Corn For Grain ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Cotton Amer. Pima ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 20 50 15 15 100Cotton Upland ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 20 50 15 15 100Beans Dry Edible ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ 100Wheat Durum ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Flaxseed ‐ ‐ ‐ ‐ ‐ ‐ 50 50 ‐ ‐ ‐ ‐ 100Peanuts for Nuts ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Potatoes All ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Hay Other (Dry) ‐ ‐ ‐ ‐ 10 20 30 20 10 10 ‐ ‐ 100Oats ‐ (Fall) ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Rye ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ ‐ ‐ 100Safflower ‐ ‐ ‐ ‐ ‐ ‐ ‐ 50 50 ‐ ‐ ‐ 100Soybeans ‐ ‐ ‐ ‐ ‐ ‐ ‐ 10 10 30 30 20 100Sugarcane For Sugar 15 15 10 5 ‐ ‐ ‐ ‐ ‐ 10 20 25 100Sunflower All ‐ ‐ ‐ ‐ ‐ ‐ ‐ 5 20 50 25 ‐ 100Sweet Potatoes ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ 100Sugarbeets ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Wheat Other Spring ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Tobacco Air‐Cured ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ 100Tobacco Flue‐Cured ‐ ‐ ‐ ‐ ‐ 20 30 30 20 ‐ ‐ ‐ 100Green Peas For Processing 2 3 5 10 11 15 20 11 10 8 3 2 100Snap Beans For Processing ‐ ‐ 2 5 7 20 30 20 10 3 2 1 100Sweet Corn For Processing ‐ ‐ ‐ ‐ 5 10 30 30 10 10 5 ‐ 100Wheat Winter All ‐ ‐ ‐ ‐ 10 25 30 25 10 ‐ ‐ ‐ 100

Seasonal AvailabilityJan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Annual Total

Species: % % % % % % % % % % % % %Hay All (Dry) ‐ ‐ ‐ ‐ 10 20 30 20 10 10 ‐ ‐ 100Hay Alfalfa (Dry) ‐ ‐ ‐ ‐ 10 20 30 20 10 5 5 ‐ 100Rice All ‐ ‐ ‐ ‐ ‐ ‐ 10 20 40 30 ‐ ‐ 100Sorghum For Grain ‐ ‐ ‐ ‐ ‐ ‐ ‐ 10 15 45 30 ‐ 100Barley All ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Canola ‐ ‐ ‐ ‐ 20 30 30 20 ‐ ‐ ‐ ‐ 100Corn For Grain ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Cotton Amer. Pima ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 20 50 15 15 100Cotton Upland ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 20 50 15 15 100Beans Dry Edible ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ 100Wheat Durum ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Flaxseed ‐ ‐ ‐ ‐ ‐ ‐ 50 50 ‐ ‐ ‐ ‐ 100Peanuts for Nuts ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Potatoes All ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Hay Other (Dry) ‐ ‐ ‐ ‐ 10 20 30 20 10 10 ‐ ‐ 100Oats ‐ (Fall) ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Rye ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ ‐ ‐ 100Safflower ‐ ‐ ‐ ‐ ‐ ‐ ‐ 50 50 ‐ ‐ ‐ 100Soybeans ‐ ‐ ‐ ‐ ‐ ‐ ‐ 10 10 30 30 20 100Sugarcane For Sugar 15 15 10 5 ‐ ‐ ‐ ‐ ‐ 10 20 25 100Sunflower All ‐ ‐ ‐ ‐ ‐ ‐ ‐ 5 20 50 25 ‐ 100Sweet Potatoes ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ 100Sugarbeets ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ 100Wheat Other Spring ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ ‐ 100Tobacco Air‐Cured ‐ ‐ ‐ ‐ ‐ ‐ ‐ 25 50 25 ‐ ‐ 100Tobacco Flue‐Cured ‐ ‐ ‐ ‐ ‐ 20 30 30 20 ‐ ‐ ‐ 100Green Peas For Processing 2 3 5 10 11 15 20 11 10 8 3 2 100Snap Beans For Processing ‐ ‐ 2 5 7 20 30 20 10 3 2 1 100Sweet Corn For Processing ‐ ‐ ‐ ‐ 5 10 30 30 10 10 5 ‐ 100Wheat Winter All ‐ ‐ ‐ ‐ 10 25 30 25 10 ‐ ‐ ‐ 100

Seasonal AvailabilitySeasonality ParametersSeasonality ParametersSeasonality Parameters

BtuHHV BtuLHV Ash Avg Ash Min Ash Max Moisture Potassium

(K ) Sodium (Na )

Chlorine (Cl )

Carbon (C )

Mercury (Hg)

Sulfur (S)

Species: MMBtu /Tonne

MMBtu /Tonne

% % % % g/kg (DAF)

g/kg (DAF)

weight % (DAF)

weight %

weight % (DAF)

weight % (DAF)

Logging Residue ‐ HardWood 18.8 17.4 0.9 0.2 2.6 11.3 1.20 0.01 0.0 49.7 0.0 0.1Logging Residue ‐ SoftWood 19.9 18.5 1.6 0.4 4.1 4.7 1.68 0.25 0.0 51.9 0.0 0.0Forest Mgmt. Residue ‐ HardWood 18.8 17.4 0.9 0.2 2.6 11.3 1.20 0.01 0.0 49.7 0.0 0.1Forest Mgmt. Residue ‐ SoftWood 19.9 18.5 1.6 0.4 4.1 4.7 1.68 0.25 0.0 51.9 0.0 0.0Coarse Wood Residue ‐ Hardwood 18.5 17.2 0.9 0.4 2.1 15.2 0.98 0.04 0.0 50.0 0.0 0.1Coarse Wood Residue ‐ Softwood 19.3 18.0 0.3 0.3 0.3 9.3 0.38 0.04 0.0 49.8 0.0 0.0Fine Wood Residue ‐ Hardwood 17.2 16.0 1.5 8.0 ‐ ‐ 50.8 0.0 0.0Fine Wood Residue ‐ Softwood 18.4 17.2 1.1 34.9 0.49 0.03 0.0 49.3 0.0 0.0Urban Wood Waste ‐ Tree clippings 19.5 18.4 15.6 1.4 39.4 35.4 4.15 2.05 0.1 51.1 0.0 0.1

Physical Parameters

BtuHHV BtuLHV Ash Avg Ash Min Ash Max Moisture Potassium

(K ) Sodium (Na )

Chlorine (Cl )

Carbon (C )

Mercury (Hg)

Sulfur (S)

Species: MMBtu /Tonne

MMBtu /Tonne

% % % % g/kg (DAF)

g/kg (DAF)

weight % (DAF)

weight %

weight % (DAF)

weight % (DAF)

Logging Residue ‐ HardWood 18.8 17.4 0.9 0.2 2.6 11.3 1.20 0.01 0.0 49.7 0.0 0.1Logging Residue ‐ SoftWood 19.9 18.5 1.6 0.4 4.1 4.7 1.68 0.25 0.0 51.9 0.0 0.0Forest Mgmt. Residue ‐ HardWood 18.8 17.4 0.9 0.2 2.6 11.3 1.20 0.01 0.0 49.7 0.0 0.1Forest Mgmt. Residue ‐ SoftWood 19.9 18.5 1.6 0.4 4.1 4.7 1.68 0.25 0.0 51.9 0.0 0.0Coarse Wood Residue ‐ Hardwood 18.5 17.2 0.9 0.4 2.1 15.2 0.98 0.04 0.0 50.0 0.0 0.1Coarse Wood Residue ‐ Softwood 19.3 18.0 0.3 0.3 0.3 9.3 0.38 0.04 0.0 49.8 0.0 0.0Fine Wood Residue ‐ Hardwood 17.2 16.0 1.5 8.0 ‐ ‐ 50.8 0.0 0.0Fine Wood Residue ‐ Softwood 18.4 17.2 1.1 34.9 0.49 0.03 0.0 49.3 0.0 0.0Urban Wood Waste ‐ Tree clippings 19.5 18.4 15.6 1.4 39.4 35.4 4.15 2.05 0.1 51.1 0.0 0.1

Physical Parameters

Detailed Physical ParametersDetailed Physical ParametersDetailed Physical Parameters

Species-Specific ParametersSpeciesSpecies--Specific ParametersSpecific Parameters

Biomass Residue ConversionsBiomass Residue ConversionsBiomass Residue Conversions

14

Biomass Energy Analytical Model

Densification and Processing OptionsDensification and Processing OptionsDensification and Processing OptionsCAPEX OPEX Energy

Balance Carbon

Footprint MBtu / tonne

kg CO2 / tonne

Wood Bundler 0.89 13.78 38.6 2.99Small Wood Chipper 0.51 10.38 79.5 6.15Large Wood Chipper 0.08 0.64 13 1.04Wood As is 0.00 0.00 0.00 0.00General Agricultural Bundler 1.64 8.6 52.9 4.09Grassy Agricultural Bundler 3.03 5.89 73.4 5.68Producer Payment 0.00 0.00 0.00 0.00

Activity$ / tonne

Farm

/For

est G

ate

CAPEX OPEXEnergy Balance

Carbon Footprint

Mbtu / tonne

kg CO2 / tonne

Pelletization with Chipper 12.31 36.16 3,800 358 Briquettization with Chipper 16.40 32.71 3,780 357 Torrefaction with Chipper 13.86 39.61 1,220 133 Pelletization 11.71 32.71 3,780 357 Briquettization 15.80 29.27 3,760 355 Torrefaction 13.27 36.06 1,200 132 Wood Chipper ‐ Large 0.08 0.64 13 1 Storage 6.91 2.20 31 2

$ / tonne

Post‐Den

sification

Activity

CAPEX OPEXEnergy Balance

Carbon Footprint

Mbtu / tonne

kg CO2 / tonne

Pelletization with Chipper 12.31 36.16 3,800 358 Briquettization with Chipper 16.40 32.71 3,780 357 Torrefaction with Chipper 13.86 39.61 1,220 133 Pelletization 11.71 32.71 3,780 357 Briquettization 15.80 29.27 3,760 355 Torrefaction 13.27 36.06 1,200 132 Wood Chipper ‐ Large 0.08 0.64 13 1 Storage 6.91 2.20 31 2

$ / tonne

Post‐Den

sification

Activity

15

Biomass Energy Analytical Model

BEAM: Coverage of Lower 48 StatesBEAM: Coverage of Lower 48 StatesBEAM: Coverage of Lower 48 States

16

Biomass Energy Analytical Model

BEAM—Grid Mode: Lower 48 StatesBEAMBEAM——Grid Mode: Lower 48 StatesGrid Mode: Lower 48 States

Agricultural Agricultural ResiduesResidues

Woody Woody ResiduesResidues

17

Biomass Energy Analytical Model

Land cover / useLand cover / useLand cover / use

BEAM: California ExampleBEAM: California ExampleBEAM: California Example

18

Biomass Energy Analytical Model

BEAM calculates transportation costs as function of time…. BEAM calculates transportation costs as function of time….

and functions of Distance.and functions of Distance.

Transportation CostsTransportation CostsTransportation Costs

19

Biomass Energy Analytical Model

Biomass costBiomass costBiomass cost

BEAM—Results: Pellets, Processed and StoredBEAMBEAM——Results: Pellets, Processed and StoredResults: Pellets, Processed and Stored

20

Biomass Energy Analytical Model

$62.04366.8 kg CO23.97 MMBtu

$62.04$62.04366.8 kg CO2366.8 kg CO23.97 3.97 MMBtuMMBtu

$63.72 366.2 kg CO23.97 MMBtu

$63.72 $63.72 366.2 kg CO2366.2 kg CO23.97 3.97 MMBtuMMBtu

$66.46370.7 kg CO24.02 MMBtu

$66.46$66.46370.7 kg CO2370.7 kg CO24.02 4.02 MMBtuMMBtu

$63.56366.0 kg CO23.96 MMBtu

$63.56$63.56366.0 kg CO2366.0 kg CO23.96 3.96 MMBtuMMBtu

$64.55367.6 kg CO23.98 MMBtu

$64.55$64.55367.6 kg CO2367.6 kg CO23.98 3.98 MMBtuMMBtu

$67.64372.6 kg CO24.05 MMBtu

$67.64$67.64372.6 kg CO2372.6 kg CO24.05 4.05 MMBtuMMBtu

$66.88371.4 kg CO24.03 MMBtu

$66.88$66.88371.4 kg CO2371.4 kg CO24.03 4.03 MMBtuMMBtu

$65.25368.7 kg CO24.00 MMBtu

$65.25$65.25368.7 kg CO2368.7 kg CO24.00 4.00 MMBtuMMBtu

$63.44365.8 kg CO23.96 MMBtu

$63.44$63.44365.8 kg CO2365.8 kg CO23.96 3.96 MMBtuMMBtu

$63.44365.8 kg CO23.96 MMBtu

$63.44$63.44365.8 kg CO2365.8 kg CO23.96 3.96 MMBtuMMBtu

All values per tonne of pelletsAll values per All values per tonnetonne of pelletsof pellets

BEAM—Results: Plant Gate Pellet CostBEAMBEAM——Results: Plant Gate Pellet CostResults: Plant Gate Pellet Cost

21

Biomass Energy Analytical Model

Cost-Supply Curve

22

Biomass Energy Analytical Model

BEAM: Northern Missouri SwitchgrassBEAM: Northern Missouri BEAM: Northern Missouri SwitchgrassSwitchgrass

• Scope: Single 30,000 bpd plant, 30% switchgrass, 70% Illinois #6 coal

• Decision: switchgrass land--mix of available land types (cultivated/hay-pasture) within 50-miles

• Plant location criteria– Northern Missouri– Rail transport of coal– Spur pipeline to major pipeline– Switchgrass feed rate: 4,240

short tons per day

23

Biomass Energy Analytical Model

Northern Missouri Switchgrass Exercise (cont)Northern Missouri Northern Missouri SwitchgrassSwitchgrass Exercise (cont)Exercise (cont)

24

Biomass Energy Analytical Model

Enegis, LLC

3959 Pender Dr. Suite 300

Fairfax, VA 22030

phone: (703) 861.4189

fax: (703) 738.7022

email: [email protected]

www.Enegis.com

This work was funded by the U.S. Department of Energy’s National Energy Technology Laboratory (U.S. DOE/NETL) under Contract No. DE-AC26- 05NT41816. The NETL sponsors for this project, Craig Hustwit and Tim Skone provided guidance and technical oversight for this study. The authors gratefully acknowledge the significant role played by U.S. DOE/NETL in providing the programmatic guidance and review of this study.

Biomass Thermal: Market Outlook

25

Amanda Hamsley LangOperations Manager, Forisk Inc.,Managing Editor, Wood Bioenergy US

Technology and Markets

III. Technology and Markets – Lang

About Forisk

Consulting

• Support investments in timberlands, timber REITs, and wood‐

using energy and manufacturing facilities.

• Conduct research of wood and stumpage markets.– Publish Wood Bioenergy

US

• Founded in 2004.

• Based in Athens, Georgia.

• Staff experience includes forest economics, wood

procurement, business strategy, finance, and equity research.

Bioenergy

Projects: Screen for Success

Bioenergy

Demand: US

• Projects: 456 Expected: 294 (64%)

• Wood demand: 130 MM Expected: 73 MM (56%)

Sources: Forisk

Consulting, as of December 2011

Bioenergy

Projects

• 456 projects announced or operating:– 159 electricity– 62 CHP– 20 thermal

– 39 liquid fuel– 176 pellet

Source: Forisk

Consulting, as of December 2011

Type North South West US

CHP 23 20 19 62Thermal 8 10 2 20Electricity 77 43 39 159

Number of Projects

CHP and Thermal Project Stats

Capacity of thermal projects varies from <1,000 pph

steam to 600,000 pph

steam

CHP Thermal

Avg.

Capacity

North South West US

CHP 29 35 23 29Electricity 122 119 43 101

Project Size (MW)

Source: Forisk

Consulting, as of December 2011

Why Forisk

separated CHP & thermal

• Previously grouped with electricity; separated in Sept. 2011

• Why we separated them:– Technologies– End markets

– Drivers

• Potential data improvements:– Size cut‐off– Commercial vs. industrial tracking

Bioenergy Trends

• Projects being put on hold until they obtain financing

or an

off‐take (PPA) agreements

• Lack of federal RES or state RPS is hindering the development

of stand‐alone bioelectricity plants

• Low price of natural gas is affecting the economics of biomass

power; biomass is more expensive by comparison.

• Combined heat and power (CHP or cogeneration) projects are

moving forward. Announcements at forest industry facilities

(i.e. Graphic Packaging in Macon) and government or

institutional use (i.e. Ameresco

at Savannah River Site).

Bioenergy Trends

• Liquid fuel projects remain speculative. Projects in

development rely heavily on government funding through

grants and loan guarantees. Future funding is uncertain.• Shift in federal funding preference to drop‐in fuels instead of

ethanol projects. – USDA, DOE, and Navy announced partnership to invest $510 MM in

next three years to produce drop‐in aviation and marine biofuels.

• Pellet mills targeting exports to Europe are moving forward

and continue to make announcements (Georgia Biomass,

Enviva)• Torrefied

biomass is still in development.

– A few announcements, but no commercial‐scale plants operating.

Recent CHP Activity / Announcements• Recast Energy is converting a coal‐fired power plant in

Louisville, KY to burn biomass.– The plant will supply steam and power to two

manufacturing plants.• Westervelt

Renewable Energy recently started operating a

power plant at its lumber mill in Moundville, AL.– The 7 MW of electricity generated will be sold to Alabama

Power. The plant began operating in December 2011.• WE Energies is building a 50 MW biomass power plant at the

Domtar Rothschild Paper mill in Wisconsin.– The steam will supply the Domtar paper mill and Domtar

will retire its fossil fuel boilers. The project is targeted to

be operating in Spring 2013.

Biomass Thermal: Market Outlook

36

Seth Walker

Associate Economist, RISI Inc.

Market Drivers

IV. Marker Drivers - Walker

William R. PerrittSenior Editor, Wood Biomass Market ReportBTEC Webinar

December 20, 2011

North American Wood Biomass Market Drivers

38

New Capacity: NA wood biomass project announcements, 2007-15 total ~100 million green

tons/year

5 1 3

5 1 3

Thousand green tons/year.Source: RISI Wood Biomass Project Database.www.risi.com/wbdb

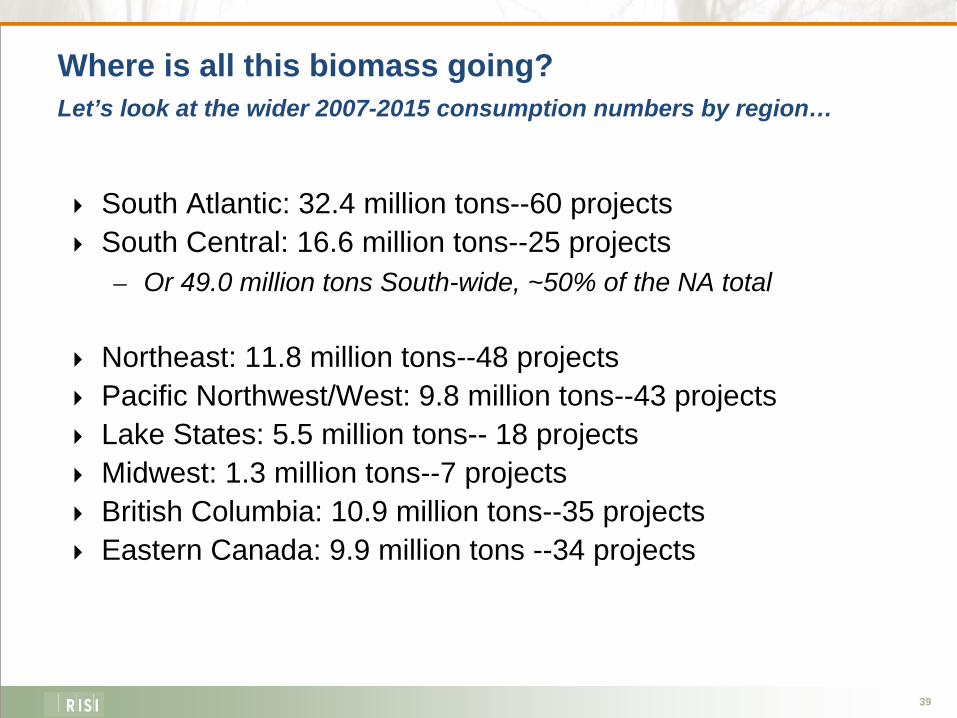

39

Where is all this biomass going? Let’s look at the wider 2007-2015 consumption numbers by region…

South Atlantic: 32.4 million tons--60 projectsSouth Central: 16.6 million tons--25 projects– Or 49.0 million tons South-wide, ~50% of the NA total

Northeast: 11.8 million tons--48 projectsPacific Northwest/West: 9.8 million tons--43 projectsLake States: 5.5 million tons-- 18 projectsMidwest: 1.3 million tons--7 projectsBritish Columbia: 10.9 million tons--35 projectsEastern Canada: 9.9 million tons --34 projects

40

Wood Pellet Production will continue to increase rapidly with the majority of new capacity coming from industrial export facilities

41

European Demand for Biomass

Policy Driven– “20/20/20” goals for 2020:

• 20% reduction in GHGs• 20% renewable• 20% efficiency gains

– BiomassReduction in GHGsRenewable Source

– European Renewable Energy Council• 61% of renewable - biomass • 50% of the growth

– AEBIOM (European Biomass Association):• Europe can supply just over 50% of the biomass

42

New Western European wood biomass demand, 2007-16, 72.1 mm green tons across top five countries

Top five countries represent 83% of potential new demand in Western Europe.Source: RISI European Wood Biomass Projects Database.www.risi.com/eurobiomassdatabase

43

New Demand for Biomass in the EU:

44

US South Delivered Woodfiber Prices 2006-2016

•The woodfiber supply will become progressively tighter based on growth in demand by OSB + bioenergy

•Fiber supply shortages are not expected to be a major issue in most regions

•Wood prices remain fairly low on an inflation-adjusted basis.

45

How does it all stack up? Low grade wood fiber demand across all industries.

46

Growth of Bioenergy Industries

•Woodfiber consumption by bioenergy industries is projected to more than double over the next five years

•RISI has reduced its forecasted capacity for biomass power generation by 22% compared to last year’s estimates

•Commercialization of cellulosic biofuels appears likely to occur within the next five years – still remains small

Biomass Thermal: Market Outlook

48

Q & A

V. Q & A - Seymour

Ask questions using the Questions Panel on the right side of your screen.

All questions and comments will be recorded and incorporated in the webinar summary report.

Also, please take a few moments to answer the survey questions after the conclusion of the webcast.

Biomass Thermal: Market Outlook

Interviews with key industry leaders (10+, also on iTunes Podcasts)

Factsheets (biomass background, job data, technology, etc.)

Presentation (comprehensive program information)

49

Other Resources

VI. Other Resources - Seymour

All Resources are available here: biomassthermal.org/resources

Biomass Thermal: Market Outlook

50

Upcoming Events

Biomass Research Institute Open House – February 1-2, 2012 in Wichita, Kansas

Join us for a two day open house celebrating the grand opening of our biomass energy demonstration facility!

Featuring guided tours and lessons from the experts

More information is available at: http://www.aesintl.net/bri/bri-open-house

VI. Upcoming Events - Seymour

Biomass Thermal: Market Outlook

51

Upcoming Events

Northeast Biomass Heating Expo –March 21 - 23, 2012 in Saratoga Springs, New York

Come see what Biomass Heat can do for your customers, your clients, and your community!

Increased space for exhibitors, registration open.

More information is available at: www.nebiomassheat.com

VI. Upcoming Events - Seymour

Biomass Thermal: Market Outlook

52

Upcoming Events

Building the Vision Conference and Expo –April 25-27, 2012 in Eau Claire, WI

Sponsored by Heating the Midwest with Renewable Biomass

More information is available at: www.heatingthemidwest.org

VI. Upcoming Events - Seymour

Biomass Thermal: Market Outlook

53

More Information

This Webinar will be available by Wednesday, Dec. 21.

Sign up to receive BTEC news at on our website.

Join BTEC for:

-- Frequent and timely regulatory, policy and market intelligence updates

-- Business Development opportunities and networking with other biomass leaders

-- Visibility as a supporter of the market’s growth

-- Discounts to nearly all major biomass industry events in the U.S.

For more info or to join, go to: www.biomassthermal.org/membership

VI. More Information - Seymour

Biomass Thermal: Market Outlook

54

Thank you!

BTEC Board of Directors

If you want to learn more about the biomass thermal industry, BTEC, or membership, visit

www.biomassthermal.org