Biofuels Industry: Minus Incentives 22 nd Annual EPAC Conference June 24-26, 2012 Billings, MT John...

18

Biofuels Industry: Minus Incentives 22 nd Annual EPAC Conference June 24-26, 2012 Billings, MT John M. Urbanchuk Technical Director - Environmental Economics Cardno ENTRIX [email protected]

-

Upload

belen-hewes -

Category

Documents

-

view

214 -

download

1

Transcript of Biofuels Industry: Minus Incentives 22 nd Annual EPAC Conference June 24-26, 2012 Billings, MT John...

Biofuels Industry: Minus Incentives22nd Annual EPAC ConferenceJune 24-26, 2012Billings, MT

John M. UrbanchukTechnical Director - Environmental EconomicsCardno [email protected]

Who we are

Cardno ENTRIX is a professional environmental consulting company specializing in water resources management, environmental risk management, natural resource economics, natural resources management, and facility permitting & compliance.

Our staff of more than 1,600 includes biologists, chemists, geologists, oceanographers, toxicologists, meteorologists, economists, and environmental, chemical, and civil engineers.

Headquartered in Houston, we have more than 40 offices in the U.S., Canada, Ecuador, Colombia and Peru.

Why Biofuels?

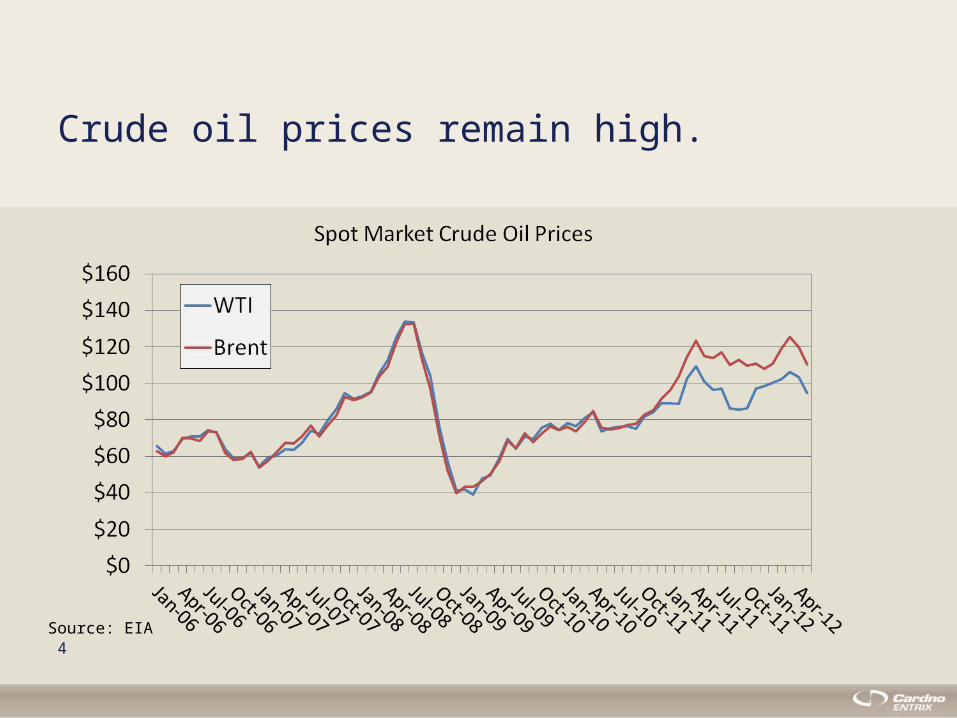

Crude oil prices remain high.

4Source: EIA

Gasoline and ethanol prices are diverging. As a result price margins continue to favor blending ethanol.

Source: Nebraska Ethanol Board. Updated 6/19/12

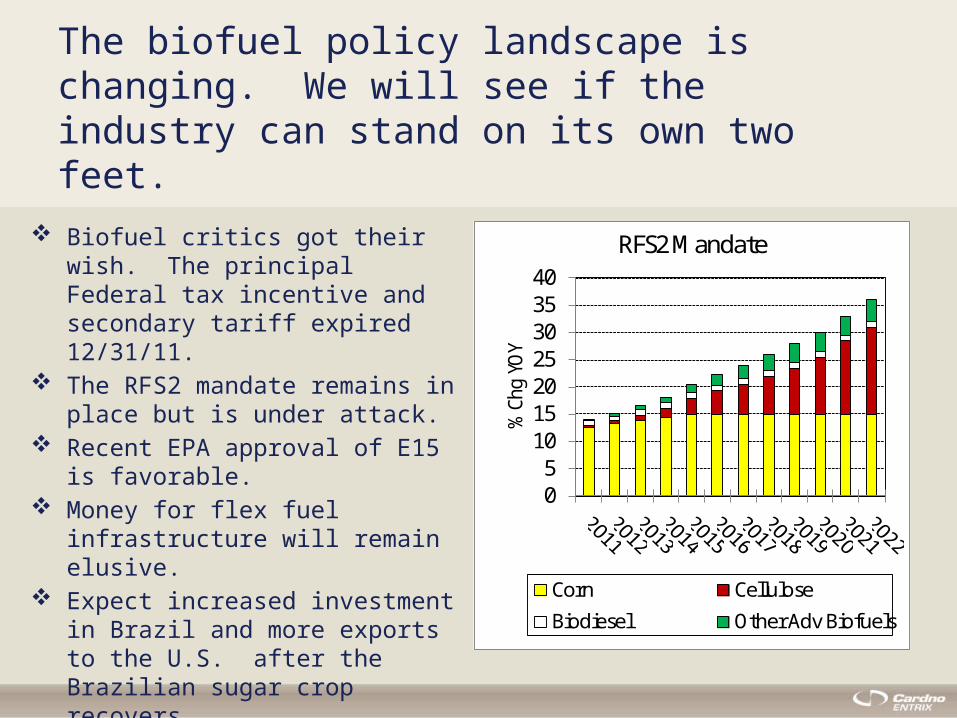

The biofuel policy landscape is changing. We will see if the industry can stand on its own two feet.

Biofuel critics got their wish. The principal Federal tax incentive and secondary tariff expired 12/31/11.

The RFS2 mandate remains in place but is under attack.

Recent EPA approval of E15 is favorable.

Money for flex fuel infrastructure will remain elusive.

Expect increased investment in Brazil and more exports to the U.S. after the Brazilian sugar crop recovers.

05

10152025303540

% C

hg Y

OY

RFS2 Mandate

Corn Cellulose

Biodiesel Other Adv Biofuels

Fundamentals for global petroleum growth favor biofuels. Will support expansion of export market.

Brazil Russia India China

Cur Pop (Mil) 201 139 1,157 1,330

2000 Pop (Mil) 223 132 1,326 1,384

GDP Per Cap $9,217 $14,907 $2,966 $6,237

Vehicle Stock (Mil)

28 38 20 51

Per 1,000 192 319 25 48

New Vehicle Sales (5-yr)

15% 3% 16% 25%

BRIC Characteristics

Biggest challenge facing ethanol industry will be demand! Approval for higher blends (than E15)will be necessary to meet RFS2 mandates.

Source: EIA 2012 Annual Energy Outlook

Biofuel feedstock prices continue to be a challenge. High sugar prices have made Brazilian ethanol unprofitable and oilseed prices are challenging biodiesel.

Source: IMF Primary Commodities Database. Updated April 2012

Industry profitability has declined sharply reflecting loss of VEETC and large supplies.

Ag Marketing Resource Center Iowa State Univ. May 2012; USDA/AMS

Production is outpacing domestic use. Exports are a bright area but stocks continue to build.

Year Production ImportsDomestic

Use ExportsEndingStocks

1995 1,358 168 1,501 34 92

2000 1,622 165 1,749 54 136

2005 3,904 212 4,072 62 234

2010 13,289 16 12,865 397 753

2011 13,948 132 12,874 1,193 767

11

U.S. Ethanol Supply & Utilization(Million Gallons)

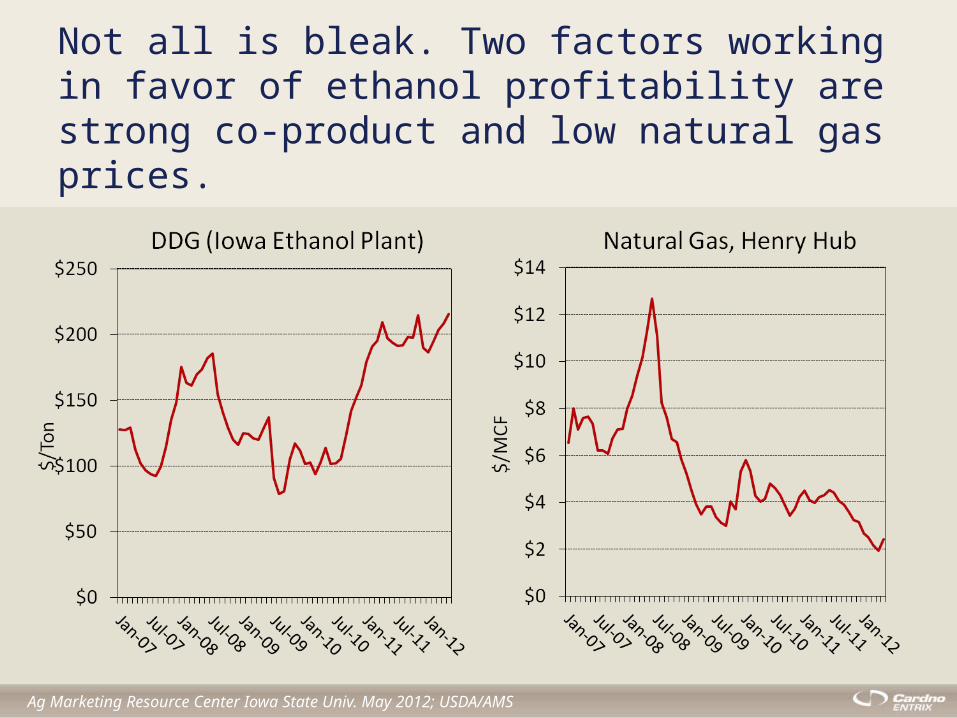

Not all is bleak. Two factors working in favor of ethanol profitability are strong co-product and low natural gas prices.

Ag Marketing Resource Center Iowa State Univ. May 2012; USDA/AMS

Profitability will remain a challenge. Expect profitability to remain under pressure until RIN values increase as inventories are drawn down.

20052006

20072008

20092010

20112012

20132014

20152016

2017

$0.00$0.25$0.50$0.75$1.00$1.25$1.50$1.75

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

Ethanol Profitability

Returns over Var Cost Ethanol, FOB Nebraska

$/G

al

$/G

al

J.M. Urbanchuk projection Jan 2012

How will we produce the 21 billion gallons of non-corn starch biofuels needed to meet RFS2 targets by 2022?

Biofuels policy is uncertain; budget pressures are likely to continue trumping energy needs.

RFS2 is under attack in the courts and Congress

VEETC and biodiesel tax credit are gone and will not return.

Cellulosic tax credit expires on 12/31/2012.

Feedstock diversity will provide both challenges and opportunities.

Another major challenge will be the required rate of expansion and availability of construction infrastructure

Producing 15 billion gallons of corn starch ethanol is no problem.

– Currently 212 refineries have nameplate capacity of 14.8 billion gallons with an average capacity of 70 MGY.

Capacity is in place to produce more than1 billion gallons of biomass biodiesel.

Assuming a 50 MGY capacity, as many as 400 new plants will be needed to be built by 2022 to meet RFS2 target at a capital cost of nearly $90 billion!

More challenges ...

Commercially successful conversion technology is uncertain and will require consistent R&D investments. Options include:

Biochemical (enzyme fermentation)Chemical (acid hydrolysis)Thermochemical gassification or pyrolysisAlgae

Capital availability and financing are uncertain. Money is available but lending standards have tightened significantly.

Permitting and sustainability will be issues for new biorefineries

In conclusion …

Biofuels production will expand both in the U.S. and globally but significant challenges remain.Threats to RFS2Feedstock and technology choicesFinancing and capital availabilityPermitting and sustainabilityRate of expansion and availability of resources

Biofuels are a shining star within a declining U.S. manufacturing sector and will continue to provide significant economic, environmental, and energy security benefits.

Questions?