BIG Call - May 2012

21

400 W. Wilson Bridge Road, Suite 200, Worthington, OH, 43085 614-846-0146 [email protected] PAMELA GOODFELLOW CONSUMER INSIGHTS DIRECTOR, BIGINSIGHT™ DIANNE KREMER SENIOR ANALYST, BIGINSIGHT™ The BIG Call May 2012

-

Upload

prosper-business-development -

Category

Education

-

view

450 -

download

1

Transcript of BIG Call - May 2012

400 W. Wilson Bridge Road, Suite 200, Worthington, OH, 43085 614-846-0146 [email protected]

PAM E L A G O O D F E L L O W

C O N S U M E R I N S I G H T S D I R E C T O R , B I G I N S I G H T ™

D I AN N E K R E M E R

S E N I O R AN ALY S T, B I G I N S I G H T ™

The BIG Call

May 2012

© 2012, Prosper®

May 2012 Consumer Survey

Disclaimer: BIGinsight™ is a trademark of Prosper Business Development Corp. Services are delivered by Prosper and/or a Prosper affiliated company (“Prosper”).

Prosper makes no warranties, either expressed or implied, concerning: data gathered or obtained from any source; the present or future methodology employed in

producing the statistics; or the data and estimates represent only the opinion of Prosper and reliance thereon and use thereof shall be at the user’s own risk.

This report is derived from the following studies:

• BIGinsight™ Monthly Consumer Survey, May 2012 (N = 8789, respondents surveyed 5/2 – 5/8/12)

• BIGinsight™ Monthly Consumer Survey Trends, May 2007 – May 2012

May 2012 Results • Consumer Confidence

• Practical Purchasing

• Financial Forecast

Personal Financial Situation

• Women’s Clothing

Department Store Domination?

• 90 Day Outlook: Future Purchase

Plans

Hispanic InsightCenter™

• Key Insights on Hispanic

Consumers for May 2012

© 2012, Prosper®

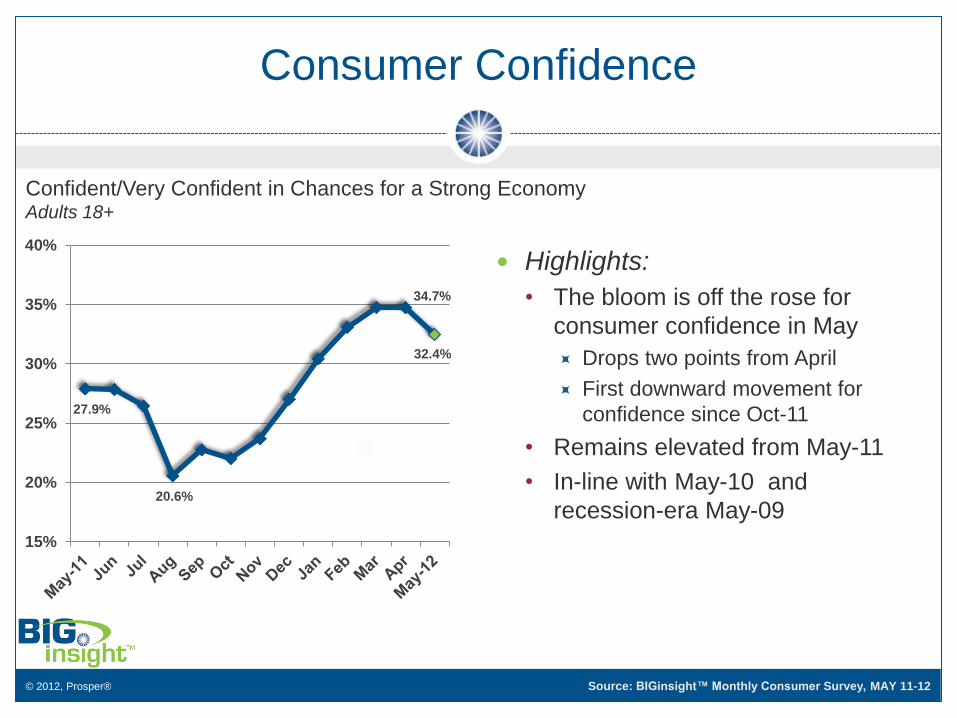

Confident/Very Confident in Chances for a Strong Economy Adults 18+

Consumer Confidence

Source: BIGinsight™ Monthly Consumer Survey, MAY 11-12

Highlights:

• The bloom is off the rose for

consumer confidence in May

Drops two points from April

First downward movement for

confidence since Oct-11

• Remains elevated from May-11

• In-line with May-10 and

recession-era May-09

27.9%

20.6%

34.7%

32.4%

15%

20%

25%

30%

35%

40%

© 2012, Prosper®

Confident/Very Confident in Chances for a Strong Economy Adults 18+

Consumer Confidence

Source: BIGinsight™ Monthly Consumer Survey, MAY 07-12

27.9%

20.6%

34.7%

32.4%

15%

20%

25%

30%

35%

40%

44

.7%

19

.5%

31

.2%

31

.5%

27

.9%

34

.7%

32

.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

May-07 May-08 May-09 May-10 May-11 Apr-12 May-12

25%+

decline

from

May-07

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAY 11-12

Practical Purchasing

In the last 6 months, have you made any of the following changes? Adults 18+

Highlights:

• Confidence declined, but

practicality didn’t increase in

kind

Nearly half pragmatic in

spending (46.6%)

Remains elevated from

May-11, May-10

• 55.0% are focused on

necessities

On par with May-11, but

inflated compared to

May-10 (51.5%)

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

I have become more practical and realistic in my purchases

I focus more on what I NEED rather than what I WANT

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAY 11-12

Financial Forecast

Which of the following financial steps are you planning to take in the next 3 months? Adults 18+

Highlights:

• Decreasing overall spending

lowered from the extreme we

saw in April

Still the highest May

reading since May-04

• Nearly as many plan to pay

down debt, increasing from

last year

• Increasing savings slips from

April, but up from May-11

0% 10% 20% 30% 40% 50%

Pay down debt

Increase savings

Pay with cash more often

Decrease overall spending

May-11 Apr-12 May-12

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAY 07-12

Personal Financial Situation

Regarding your personal financial situation, compared to this time last year, are you... Adults 18+

Highlights:

• One-third (32.3%) feels “worse

off” about personal financial

situation compared to one year

ago

20% decline from those

who felt this way in May-11

33% decrease from May-09

• Largest proportion (49.4%)

feels like they are in the

“same” boat

• Minority (18.3%) is “better off,”

increasing 20% from May-11

(15.2%)

18.3%

49.4% 48.5%

32.3%

10%

20%

30%

40%

50%

May-07 May-08 May-09 May-10 May-11 May-12

Better off Same Worse off

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAY 03-12

Women’s Clothing

Store Shopped Most Often for Women’s Clothing – Top 2 [write-in] Adults 18+

0%

5%

10%

15%

20%

25%Walmart

Kohl's

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, APR 11-12

Department Store Domination?

Consumer Equity Index™ (CEI) for Women’s Clothing Females

Macy's

Kohl's

Ross Target

Marshalls

TJ Maxx

Old Navy Kmart

JC Penney Walmart

80

100

120

140

= 100+ = <100 April 2011 v. April 2012

Details:

• CEI is available exclusively in

our monthly Retail Ratings

Reports.

• Shows year-over-year growth

[or decline] of Consumer

Preference Share

• Key:

CEI > 100 = GROWTH

CEI < 100 = DECLINE

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, APR 11-12

Department Store Domination?

Consumer Equity Index™ (CEI) for Women’s Clothing Females

Macy's

Kohl's

Ross Target

Marshalls

TJ Maxx

Old Navy Kmart

JC Penney Walmart

80

100

120

140

= 100+ = <100 April 2011 v. April 2012

43% growth

14% growth

Highlights:

• Walmart is losing share in a

key Women’s Clothing Shopper

segment: Women

Meanwhile, Kohl’s and

Macy’s are growing

• Not only is Kohl’s contesting

Walmart’s lead, but Macy’s

may enter the mix

Among shoppers overall,

Macy’s share increased

60%+ from Jan-12 to Apr-12

5% decline

NEW Blog

FYU: Department Store

Domination? CLICK to Read

© 2012, Prosper®

Category: Apr-12 May-11 May-10 Category: Apr-12 May-11 May-10

Children’s up up up Toys/Games up up up

Women’s Dress up up up CDs/DVDs/Videos/Books up up up

Women’s Casual up up up Electronics up up up

Men’s Dress up up up Groceries up up up

Men’s Casual flat up up Home Improvement up up up

Shoes up up up Lawn & Garden up up up

HBC up up up Home Furniture up up up

Dining Out up up up Home Décor up up up

Sporting Goods up up up Linens/Bedding/Draperies up up up

Retail Merchandise Categories - 90 Day Outlook (May-12 compared to Apr-12, May-11, and May-10)

Note: “Up,” Down,” “Flat” refers to the direction of the Diffusion Index compared to the previous month (Apr-12) or years (May-11, May-10). Diffusion Index = %

Spending More - % Spending Less.

BIG Forward Look: 90 Day Spending

Source: BIGinsight™ Monthly Consumer Survey, MAY 10-12

Over the next 90 days (May, June and July), do you plan on spending more, the same or less

on the following items than you would normally spend at this time of the year? Adults 18+

© 2012, Prosper®

Category: Apr-12 May-11 May-10 Category: Apr-12 May-11 May-10

Children’s up up up Toys/Games up up up

Women’s Dress up up up CDs/DVDs/Videos/Books up up up

Women’s Casual up up up Electronics up up up

Men’s Dress up up up Groceries up up up

Men’s Casual flat up up Home Improvement up up up

Shoes up up up Lawn & Garden up up up

HBC up up up Home Furniture up up up

Dining Out up up up Home Décor up up up

Sporting Goods up up up Linens/Bedding/Draperies up up up

Retail Merchandise Categories - 90 Day Outlook (May-12 compared to Apr-12, May-11, and May-10)

Note: “Up,” Down,” “Flat” refers to the direction of the Diffusion Index compared to the previous month (Apr-12) or years (May-11, May-10). Diffusion Index = %

Spending More - % Spending Less.

BIG Forward Look: 90 Day Spending

Source: BIGinsight™ Monthly Consumer Survey, MAY 10-12

Over the next 90 days (May, June and July), do you plan on spending more, the same or less

on the following items than you would normally spend at this time of the year? Adults 18+

All categories

remain

DOWN

from

pre-downturn

May 2007

© 2012, Prosper®

Sp

ec

ial

Ins

igh

t:

His

pan

ic C

on

su

mers

Key Insights for May 2012:

1. Higher Confidence; Lower Expectations

2. More Positive Personal Financial Situation

3. Practical, But Willing to Spend

4. Word of Mouth is Key

Visit http://www.hispanicinsightcenter.com/hicinfo/

Free App for Android

& Apple® iPad

© 2012, Prosper®

Hispanic Consumer Confidence

Confidence in Chances for a Strong Economy Confident or Very Confident

0%

10%

20%

30%

40%

50%

60%

Hispanics 18+

Adults 18+

Highlights:

• Though declining in May, Hispanic Consumer confidence remains higher than recession-era

May 2009 levels and well above that of consumers in general.

Source: BIGinsight™ Monthly Consumer Survey, MAY 09-12

© 2012, Prosper®

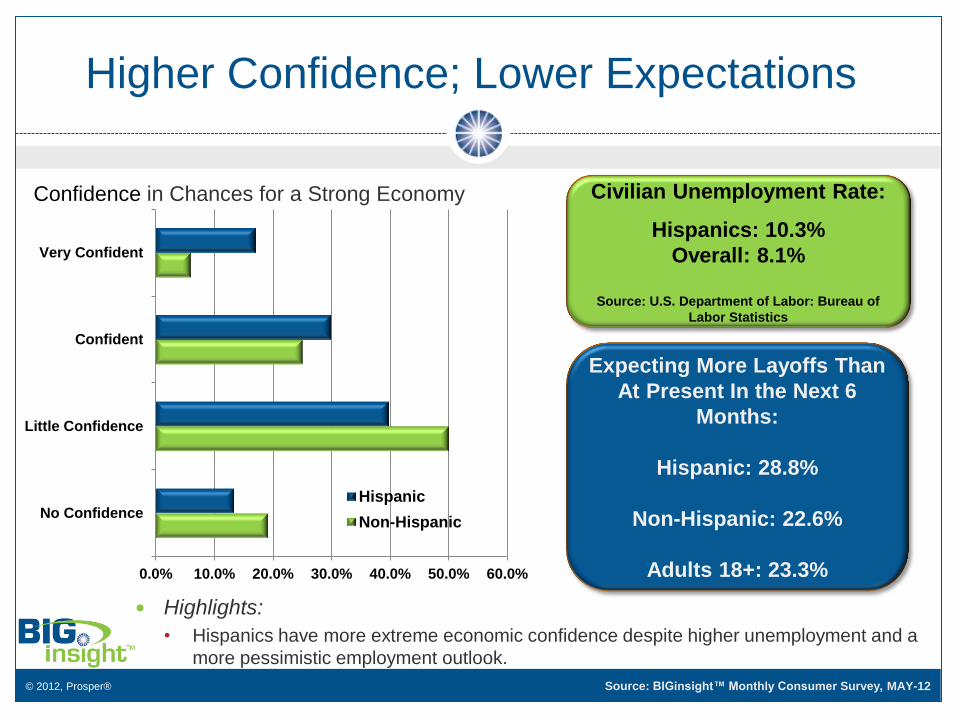

Higher Confidence; Lower Expectations

Confidence in Chances for a Strong Economy

Highlights:

• Hispanics have more extreme economic confidence despite higher unemployment and a

more pessimistic employment outlook.

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

No Confidence

Little Confidence

Confident

Very Confident

Hispanic

Non-Hispanic

Expecting More Layoffs Than

At Present In the Next 6

Months:

Hispanic: 28.8%

Non-Hispanic: 22.6%

Adults 18+: 23.3%

Civilian Unemployment Rate:

Hispanics: 10.3%

Overall: 8.1%

Source: U.S. Department of Labor: Bureau of

Labor Statistics

Source: BIGinsight™ Monthly Consumer Survey, MAY-12

© 2012, Prosper®

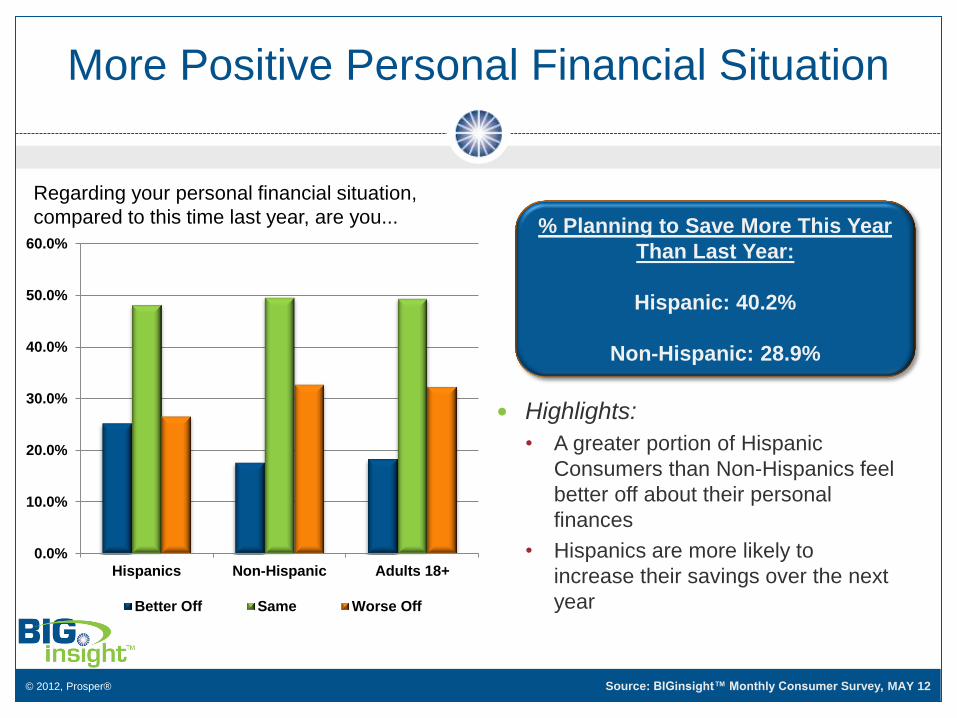

More Positive Personal Financial Situation

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Hispanics Non-Hispanic Adults 18+

Better Off Same Worse Off

Regarding your personal financial situation,

compared to this time last year, are you...

Highlights:

• A greater portion of Hispanic

Consumers than Non-Hispanics feel

better off about their personal

finances

• Hispanics are more likely to

increase their savings over the next

year

% Planning to Save More This Year

Than Last Year:

Hispanic: 40.2%

Non-Hispanic: 28.9%

Source: BIGinsight™ Monthly Consumer Survey, MAY 12

© 2012, Prosper®

Hispanic Consumer Practicality

In the last six months, have you made any of the following changes? Hispanic Adults 18+

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

I focus more on what I NEED rather than what I WANT

I have become more practical and realistic in my purchases

I have become more budget conscious

Highlights:

• Practicality, Focus on

Needs, Budget

Consciousness down

from April

• Practicality remains

elevated from May

2011

Source: BIGinsight™ Monthly Consumer Survey, MAY 11-12

© 2012, Prosper®

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Vacation Travel

Digital Camera

TV

Mobile Device

Computer

Jewelry/Watch

Major Home Improvement

Home Appliances

Furniture

House

Car/Truck

Hispanic

Non-Hispanic

Practical, But Willing to Spend

Major Purchase Plans – Next Six Months

Source: BIGinsight™ Monthly Consumer Survey, MAY 12

© 2012, Prosper®

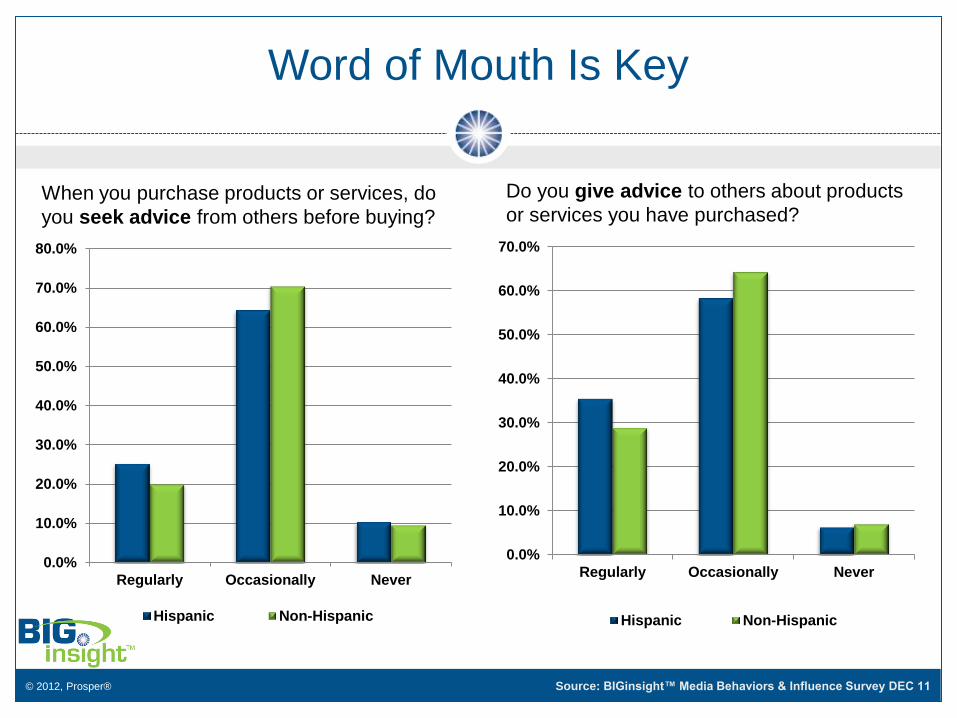

Word of Mouth Is Key

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Regularly Occasionally Never

Hispanic Non-Hispanic

When you purchase products or services, do

you seek advice from others before buying?

Do you give advice to others about products

or services you have purchased?

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Regularly Occasionally Never

Hispanic Non-Hispanic

Source: BIGinsight™ Media Behaviors & Influence Survey DEC 11

© 2012, Prosper®

BIG

Co

ns

um

er

Blo

g

Have You Been Briefed for May? view

Gen Y’s Financial Lessons from Forrest Gump view

FYU: Department Store Domination? view

A Mom Blog view

Generation Gap: Time to Chow Down on New Data view

A Fashion Fixation view

Two-Thirds of Trader Joe’s, Whole Foods Shoppers

Express Health Happiness view

Consumer Buzz: Touring the Autobahn view

Pain at the Pump Blog Series view

© 2012, Prosper®

Co

nta

ct

400 W. Wilson Bridge Road

Suite 200

Worthington, OH 43085

Ph: 614-846-0146

for complimentary insights, visit:

www.BIGinsight.com

![[Music Score] Big Band - Call Me Claus](https://static.fdocuments.net/doc/165x107/577cdc1a1a28ab9e78a9df38/music-score-big-band-call-me-claus.jpg)