Bham Uni M Sc V2 Larner January 2008

62

Cooperative Public Purchasing Dr Andrew Larner Regional Director South East Improvement & Efficiency Partnership

-

Upload

andrewlarner -

Category

Documents

-

view

131 -

download

0

Transcript of Bham Uni M Sc V2 Larner January 2008

Cooperative Public Purchasing

Dr Andrew Larner

Regional Director

South East Improvement & Efficiency Partnership

Overview

• RCE History• How South East Centre (SECE) works• Priorities and prioritisation

• Key projects

• Joining up with the Improvement Partnerships• Where have we got to and where next• National Leads

RCE History

RCE History

• Formation– National Procurement Strategy– Regional Centre’s of Procurement Excellence– Formation July 2004 to March 2005

• Coordination– Regional Directors Group– Assistant Directors Group– Programme Management Team– National Leads

How the South East Centre (SECE) Works

The South East Region

• 55 Districts

• 12 Unitaries• 7 Counties• 5 Police Authorities

• 8 Fire Authorities

• SHA’s and PCT’s

How SECE Works

• Formed Late 2004, Programme Started April 2005• Efficiency and Procurement from the start• Governance

– Host authority Kent County Council– Board made up of Senior officer from around the region

• Mix of authority types• Representation from the 8 County areas

• Ways of working– Leadership of Workstreams spread around the region– Small core team seconded from Kent CC– Secondments from around the region– Virtual working– Admin support from one District in the regions centre

• Strong emphasis on business management– Project Management– Monitoring and Reporting

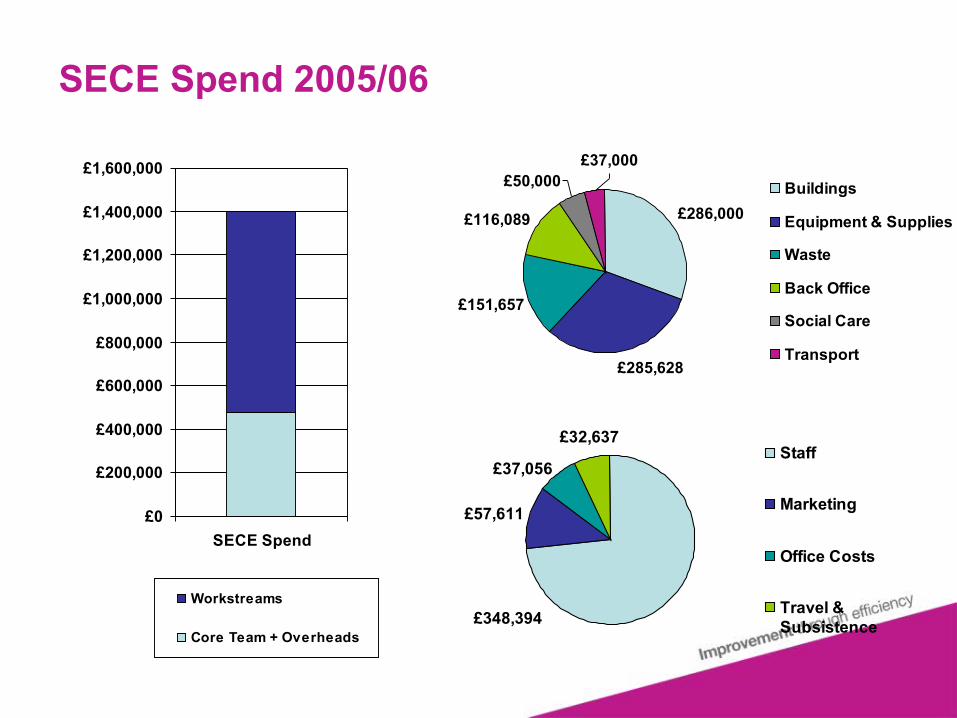

SECE Spend 2005/06

£57,611

£348,394

£37,056

£32,637Staff

Marketing

Office Costs

Travel &Subsistence

£286,000

£285,628

£151,657

£37,000

£116,089

£50,000 Buildings

Equipment & Supplies

Waste

Back Office

Social Care

Transport

£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000

£1,400,000

£1,600,000

SECE Spend

Workstreams

Core Team + Overheads

Priorities and Prioritisation

Finding the right levers

Prioritisation

• South East Context– Grant floor– Net contribution of tax– Net decrease in government funding– Unable to raise local taxation

• Financial impact– For all authorities– Maximising return on investment– Threats (Opportunities)– Legislative drivers

• Used a Number of Methods– Evolving these– Give value in their own right as well as identifying

priorities for improvement

Supplier Spend Analysis

• 167 of 388 councils in England (43%)

• Relative amount of data gathered by Regional Centre of Excellence and by Authority Type

Sample Data by Regional Centre of Excellence

0

10

20

30

40

50

60

70

80

ECE EMCE LCE NECE NWCE SECE SWCE WMCE Y&HCE

Regional Centre of Excellence

Nu

mb

er

Total number of local authorities No. of local authorities with aggregate spend data

No. of local authorities with spend data by supplier

Sample Data by Authority Type

0

50

100

150

200

250

CC DC LBC MDC UA

Authority Type

Nu

mb

er

Total number of local authorities No. of local authorities with aggregate spend data

No. of local authorities with spend data by supplier

Master Category Spend Breakdown

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Constr

uctio

n

Social

care

Facilit

ies

Profes

siona

l ser

vices

Enviro

nmen

tal se

rvice

s IT

Public

bod

ies

Financ

ial se

rvice

sTra

vel

Office s

ervic

es

Energ

y and

utilie

s

Logis

tics

Marke

ting a

nd m

edia

Miscell

aneo

us

Events

and l

eisur

e

Medica

l car

eFue

ls

Common

categ

ory

Master Category

Sp

end

(£

mill

ion

)

extrapolated aggregate spend by Master Category across all local authority councils in England. The extrapolated total spend is c£45 billion.

Level 2 Supplier Spend Analysis

Buildings

Waste Management

Commodities appear throughout

Social Care

Value from top suppliers

Value from top transactions

From Thompson to Gershon

External Spend – National Overview

Construction Spend: £14.3 Billion35% of total external spend

Corporate Services Spend: £14.2 Billion35% of total spend

Social Care Spend: £7.8 Billion19% of total spend

Waste Spend: £2.9 Billion7% of total spend

Commodity, Goods and Services. Spend in top 4 areas £11.3 billion, 30% of total spend

These four areas cover £96% billion of the total external spend

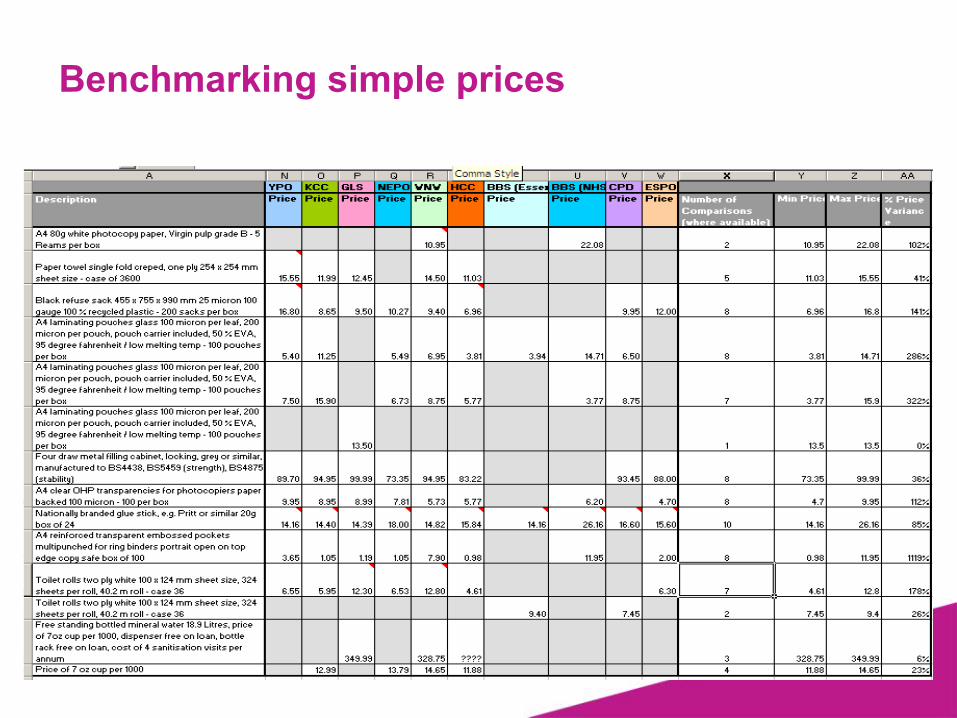

Benchmarking simple prices

Benchmarking Complex prices

Average gross weekly expenditure per looked after child in foster care or in a children's home (incl respite and short term placements and placed for adoption)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Hampshire

Isle

of W

ight U

AKen

t

Med

way T

owns

UA

South

ampt

on U

A

East S

ussex

West

Berks

hire

UA

Slough

UA

Wind

sor a

nd M

aiden

head

UA

Portsm

outh

UA

Brack

nell F

ores

t UA

Wokin

gham

UA

Reading

UA

Milto

n Key

nes U

A

Oxford

shire

Surre

y

Bright

on an

d Hov

e UA

Buckin

gham

shire

West

Susse

x

£ 10

00 Saving - Upper Quartile

Unit Cost

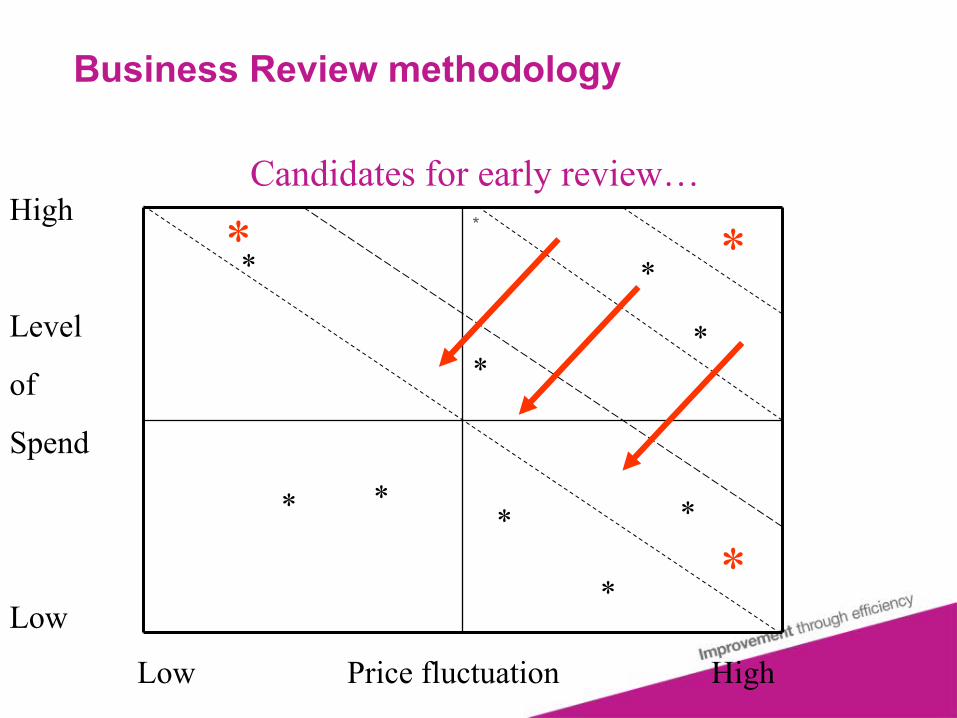

Business Review methodology

*

Low Price fluctuation High

High

Level

of

Spend

Low

*

* *

*

*

*

*

*

* **

*

Candidates for early review…

Comprehensive Gap Analysis

• What we do / buy? • From whom do we buy? • What we pay / cost?

• What contractual arrangements exist?

• Rate pay / outcome?

Business Review methodology

*

Low Price fluctuation High

High

Level

of

Spend

Low

*

* *

*

*

*

*

*

* **

*

Candidates for early review…Level of Spend (Cost)

•Actual Calculation

•Internal Costs (of service delivery)

•External Spend(of service delivery)

•On-Cost

•Service Management Costs

•Corporate

Result = Total/Unit cost

Business Review methodology

*

Low Price fluctuation High

High

Level

of

Spend

Low

*

* *

*

*

*

*

*

* **

*

Candidates for early review…Level of Spend (rate)

•Total Spend (now)

•No of Units of service delivery

•Rate per Unit

•Ratio of Management Costs:Service Costs

Result = Total/Unit cost

Take 5 yr projected position where service demands are dynamic

Business Review methodology

*

Low Price fluctuation High

High

Level

of

Spend

Low

*

* *

*

*

*

*

*

* **

*

Candidates for early review…Benchmark Information

(Price Fluctuation)

•Returns (PSS EX1, E51, BVPI’s CCPR etc etc)

•Contracts Portal

•External Spend Analysis

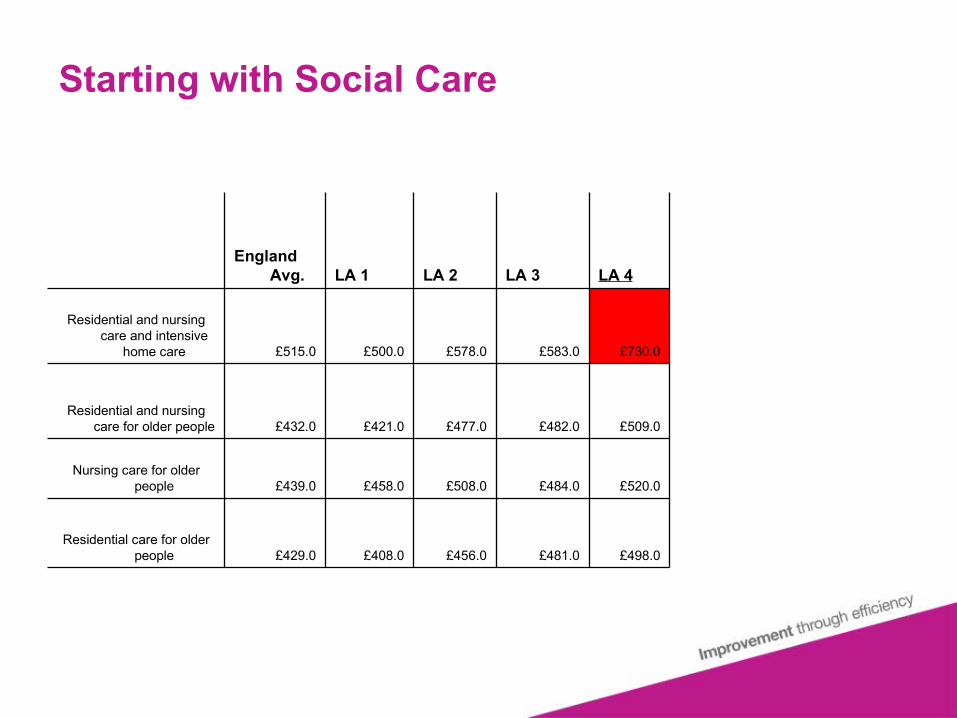

Starting with Social Care

England Avg. LA 1 LA 2 LA 3 LA 4

Residential and nursing care and intensive

home care £515.0 £500.0 £578.0 £583.0 £730.0

Residential and nursing care for older people £432.0 £421.0 £477.0 £482.0 £509.0

Nursing care for older people £439.0 £458.0 £508.0 £484.0 £520.0

Residential care for older people £429.0 £408.0 £456.0 £481.0 £498.0

Key Projects

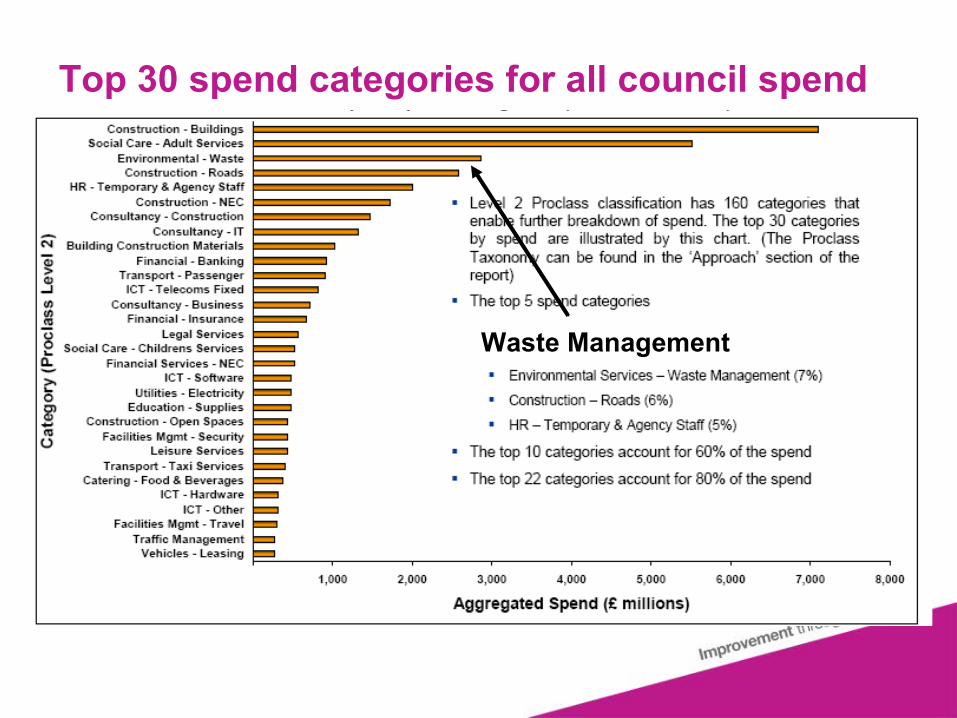

Top 30 spend categories for all council spend

Buildings

Buildings

Partnership / Non Framework £43,000,000Strategic Frameworks £71,000,000Traditional procurement £393,000,000

Based on responses from 5 County Councils and 10 Unitary Councils in 2005

Pulling the levers: Buildings Construction Frameworks

• South East Regional Framework– No limit on the number of members– Savings 5% spot, 12% groups of blgs, 20%

programmes?

• Regional framework is well established and projects with commitment approaching £1.3 Billion in the first year

– Cost overruns are being reduced from an average of 10% to less than 1%

– Each project is saving more that £150K in procurement costs and savings on construction costs look likely to exceed 10%

– Participation now includes Police, Fire, NHS, Further Education (LSC)

– The first Hospital is being procured through the framework and the construction of the first project, Alfred Sutton School, is completed

Sub regional activity

• Sub Regional Frameworks– Intermediate projects, more local firms– Surrey, Berkshire, Hampshire

• Commodities - later• Client capacity

– Sharing professional resource– Supporting improvement– Consultancy framework

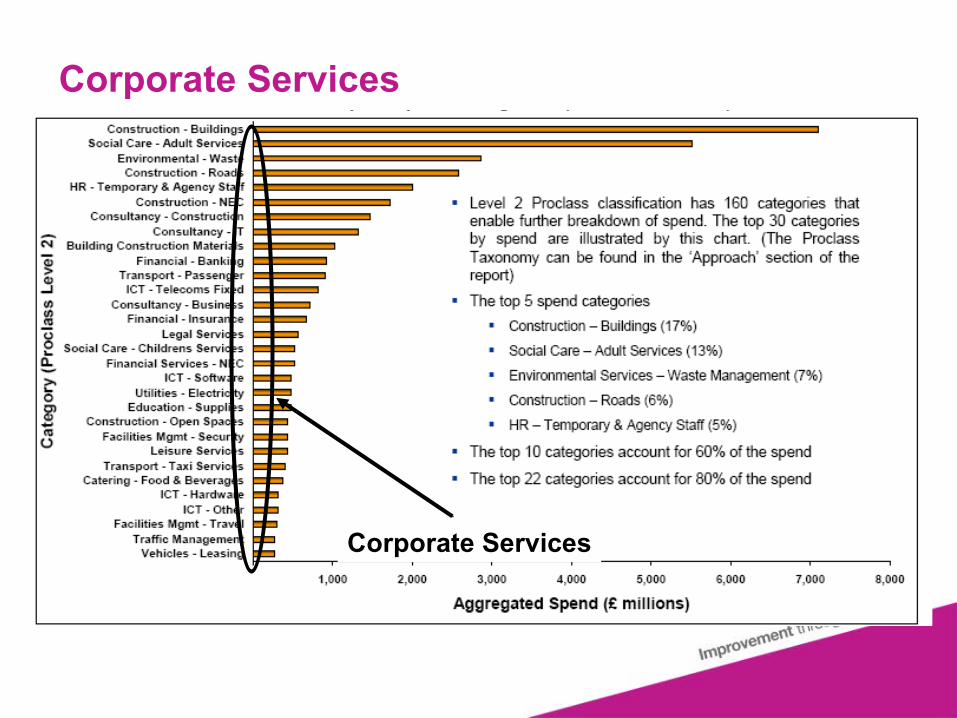

Corporate Services

Corporate Services

Corporate and Transactional Services

• South East Market– Individual business cases but no global business case– High expectations from government– No critical mass

• Significant local authority collaboration– Adur and Worthing merged officer structure– Adur, Mid Sussex and Horsham partnership– South Oxfordshire / Vale of White Horse– Berkshire Procurement and Shared Service Unit

• Service specific collaborations– Pan regional joint library management system contract signed

with £1m savings• Cross sector collaboration

– Police, Fire, Health, Local Authority• Isle of White• Brighton and Hove

• Corporate procurement– Legal services– Banking services

Commodity Goods and Services

Commodity Goods and Services

Extrapolated NationalCommodity Spend

Category CGS Spend

Temporary and Agency Staff £1,995,649,352

Building Construction Materials £1,016,584,553

Telecoms - Fixed £810,416,180

Insurance £675,133,872

Legal Services £558,092,496

Software £480,843,065

Electricity £475,761,198

Catering Food and Beverages £369,354,629

Hardware £319,213,999

Leasing £271,598,118

Commercial £236,517,481

Water £227,565,571

Mail Services £225,737,404

Furniture £212,980,958

Travel £208,160,545

ICT Other (NEC) £206,009,684

Accountancy £193,425,692

Print £190,622,913

Catering Services £184,057,186

Heavy Construction Equipment £183,413,585

Training and conferences £179,801,085

Gas £169,381,986

Stationary £155,082,049

Sports and Playground £144,315,463

Advertising £138,626,225

Social Care - Supplies £137,204,844

Extrapolated national spend of £10.6 billion

Commodity Goods and Services

• 30% of external spend is commodity spend (Directly identifiable)• From stationary to agency staff• Top 20 commodities account for 81% of the commodity spend• A saving of 10% would be 1.5% of an authorities total spend• Authorities can have off contract spend of 40% to 60%, although it may be as low

as 5%• Overpayment on 40% off contract spend equates to 0.6% of total budget• 3 levels of procurement

– Market knowledge and management– Aggregating buying power– Ensuring take up

• Tried to do all in every local authority – NPS wrong direction?• Initial views of consortia

– Little take up– Variation in performance for buy and sell price

– Lack of transparency and trust

Commodity activities

• Market intelligence• Business Portal

– Sharing contract information– One stop shop for suppliers– Identify opportunities to collaborate and save

• Best Deals – more later

• Commodity reverse auctions• Procurement Hubs

– Sharing procurement resource across local authorities

Example: Best deals service

• Compare over 3000 commodities– Over 2000% variation between price of a single

commodity is relatively common

• Market study to supplement the commodity comparison

• OJEU watch of local authority notices• Portal of local authority contract information, register

of contracts

• Bring together in pro-active and re-active service– Working with clusters of authorities to migrate to lowest

price– Advising authorities going to procurement of existing

opportunities– Creating procurement hubs to aggregate local authority

spend

Example: Commodity Reverse Auction

• Procurements in Y&H, NE.• Savings of 25% to 40%• SME friendly

– Increasing efficiency of SME usage– Reducing costs of the SME supply chain– Allowing SME’s to compete fairly

Social Care

Social Care

A complex set of areas

• A number of services– Some generic like needs assessment– Many specific

• A number of age ranges of customers

45%

39%

14%

2%

0%

0% Residential Care Homes

Nursing Homes

Home Care Services

Rest & Retirement Homes

Mental Health Centres

Home Help Services -Private

42%

41%

10%

4% 3%Adoption & Fostering

Children's Homes

Childcare Services

Children's Activity Centres

other

Social Care

• South East Market– Regional adult social care spend c. £673– Big area of cost overrun– Big variation in unit costs

• Low hanging fruit – e.g. Taxi services– C. £10 m per County area– Saving 40% with quality improvement

• Learning Difficulty Placements– high cost specialist residential care average 12% saving– Cost model

• Frameworks for specialist services– live-in domiciliary care and nursing dementia care up to 10%

• Centralised buying of temporary worker time 10% to 20%• Roll out of the Kent Purchase Card

– Savings and transparency of costs

Example: National Roll out of Learning Difficulty Toolkit

National toolkit pilots

All regions taking part in pilot

Total 71

6

11

6

9

2

18

76

6

Timeline

Phase Completion Date

• Establish team including recruitment of necessary resources Completed

• Property expert to develop a formula for property prices to be included in the tool

Completed

• Develop toolkit Completed

• Develop guidelines for use of model Completed

• Train pilot authorities • Pilot authorities use on at least 20 cases each

Completed Ongoing

• Pilot authorities feed back results of pilots End January 2008

• Model and guidelines updated • Estimate of savings achieved in pilot sites • Agree plan for ensuring continuing updates of national cost

assumptions

End February 2008

• Launch in Regions • Regional training programmes established

End March 2008

Top 30 spend categories for all council spend

Waste Management

The Municipal Waste Flow Diagram

Reprocessing and Market

Tre

atm

ent

Fina

l D

ispos

al a

nd

Mar

ketin

g

Energy RecoveryDispoal to Land

Material Recycling/Recovery Facility (MRF)

Mechanical Biological Treatment (MBT)

Composting

Civic AmenintyBring Banks

Col

lect

ion

Kerbside Collection

Hom

e se

pera

tion

Home Composting

Food Digestion

Re-Use

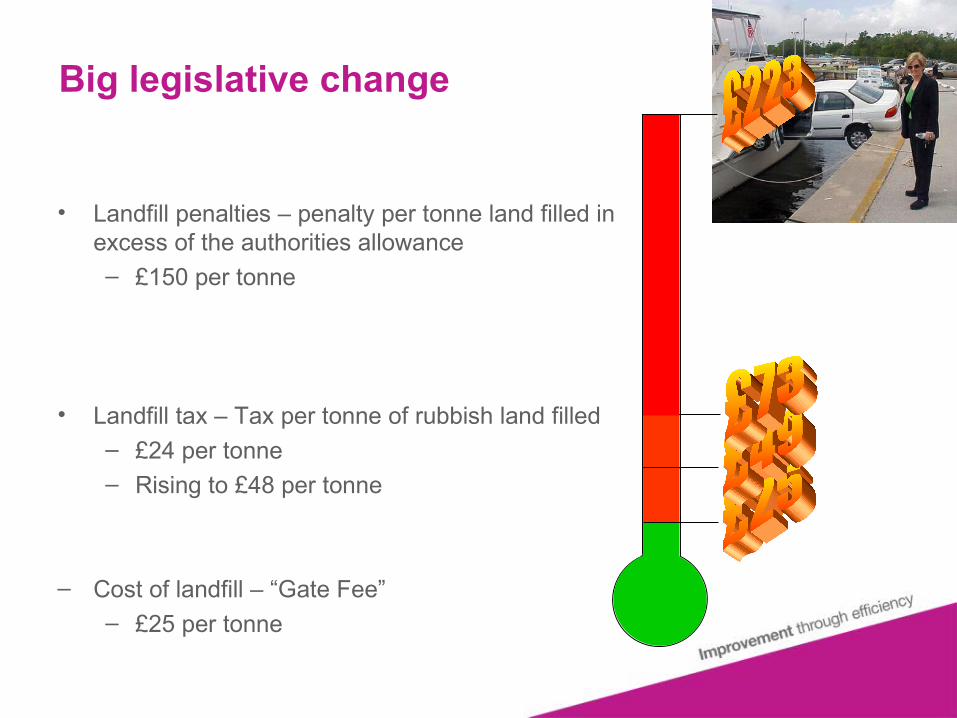

Big legislative change

• Landfill penalties – penalty per tonne land filled in excess of the authorities allowance– £150 per tonne

• Landfill tax – Tax per tonne of rubbish land filled– £24 per tonne– Rising to £48 per tonne

– Cost of landfill – “Gate Fee”– £25 per tonne

Waste Management

• South East Market– Regional waste management services spend c. £427 million– England

• Potential LATS fines of £2 billion to £3 billion - England• >60%% of collection contracts coming to market within 3 yr period

• Reduce disposal costs– WDA collaboration: Northants / MK, Bucks / RBWM– Use of new technology to reduce disposal required– Standardisation of collection methods

• Reduce the costs of collection– Collaborative procurement of commodities / reverse auctions– Use of e-tendering– Collaborative collection contracts

• Reduce the costs of procurement– Use of e-tendering

Joining up with the Improvement Partnerships

“when two elephants compete it is the grass that suffers.”

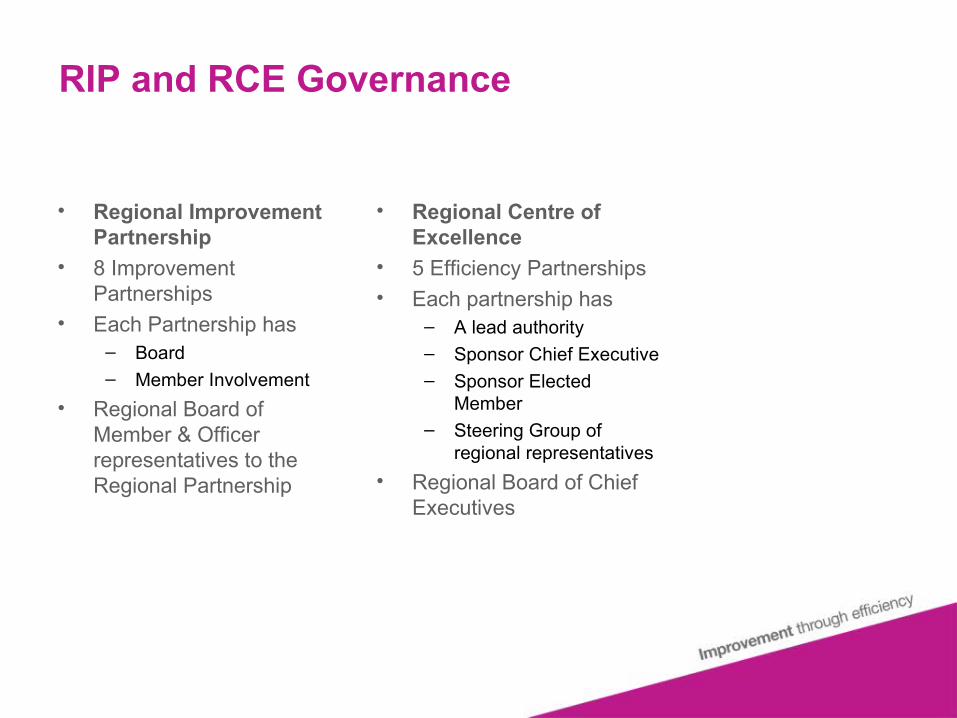

RIP and RCE Governance

• Regional Improvement Partnership

• 8 Improvement Partnerships

• Each Partnership has – Board– Member Involvement

• Regional Board of Member & Officer representatives to the Regional Partnership

• Regional Centre of Excellence

• 5 Efficiency Partnerships• Each partnership has

– A lead authority– Sponsor Chief Executive– Sponsor Elected

Member– Steering Group of

regional representatives

• Regional Board of Chief Executives

SOUTH EAST IMPROVEMENT AND EFFICIENCY PARTNERSHIP

Progress Through Partnership(LSP’s)

GEOGRAPHICAL

PARTNERSHIPS

Fire Improvement Partnership

Berkshire

Hampshire/Isle of Wight

Surrey

Kent & Medway

Sussex (East & West Sussex/Brighton & Hove)

Milton Keynes, Oxfordshire & Bucks

THEMED

PARTNERSHIPS

Waste(Led by East Sussex)

Social Care(Led by West Sussex)

Buildings Construction(Led by Hampshire)

Commodity Goods & Services(Led by Wealden)

Corporate & Transactional Services(Led by Aylesbury)

SEIEP Partnership Structure

Developing the SE CSR07 Regional Strategy

June AugJuly

SEIEP Board Approval by email

Develop PID

• Timescales

• Resources

• Roles

• Approval route

• Dependencies on CLG

• Formats and detailed plans for consultation

• Acceptance criteria for plan

• Evidence based template for proposals

31st

Subregional Strategies & Phase 1 Bids

10th?

NIS Published

Draft High LevelBusiness Plan

(compile component bids)

30th24th

Sept Oct Nov JanDec

RIPNetwork

19th

SECE Workstream Strategies & Phase 1 Bids

SEIEPConference

SEIEP Board sign-off

Draft Detailed Business Plan

Bid Review & Approval

(to include RIP Boards and SECE Board approval of local plans)

Final Draft Business

Plan

Rebuild of Evidence Base

• SECE spend analysis

• Audit Commission & IDeA views

• Summarise draft NIS etc.

SEIEP Member Panel

30th

Feb

RIPNetwork

19th

SEIEP

Member/Of

ficer Board

8th

Where have we got to and where next

South East Return on Investment

£0

£5,000,000

£10,000,000

£15,000,000

£20,000,000

£25,000,000

£30,000,000

EastMidlands

East ofEngland

London NorthEast

NorthWest

SouthEast

SouthWest

WestMidlands

Yorkshire& the

HumberRCE

Exp

ecte

d S

avin

gs

Reasonable

Analysis carried out by external consultants at end 2006

SECE Figures – Jan 07

Return on £1 Social Care Corp Proc Buildings Waste CTS

SECE £32 £42 £58 £40 £11

Total £26 £42 £58 £32 £3

SECE Budget Position

£0

£500,000

£1,000,000

£1,500,000

£2,000,000

£2,500,000

£3,000,000

Budget 07/08 Spend atend August

Core Team

Comms

Buildings

Waste

Social Care

CTS

CGS

• Budget includes variances to original budget agreed in July

• Spend running behind the curve due to resources only recently coming on board

• All workstreams forecasting to spend budgets

• £700k surplus predicted from original 3 yr funding of £6.8m – required to cover 08/09 contract commitments

• £10.7m evidenced savings to date• Expected savings over 5 years

– High confidence £38 million– Medium confidence £120 million

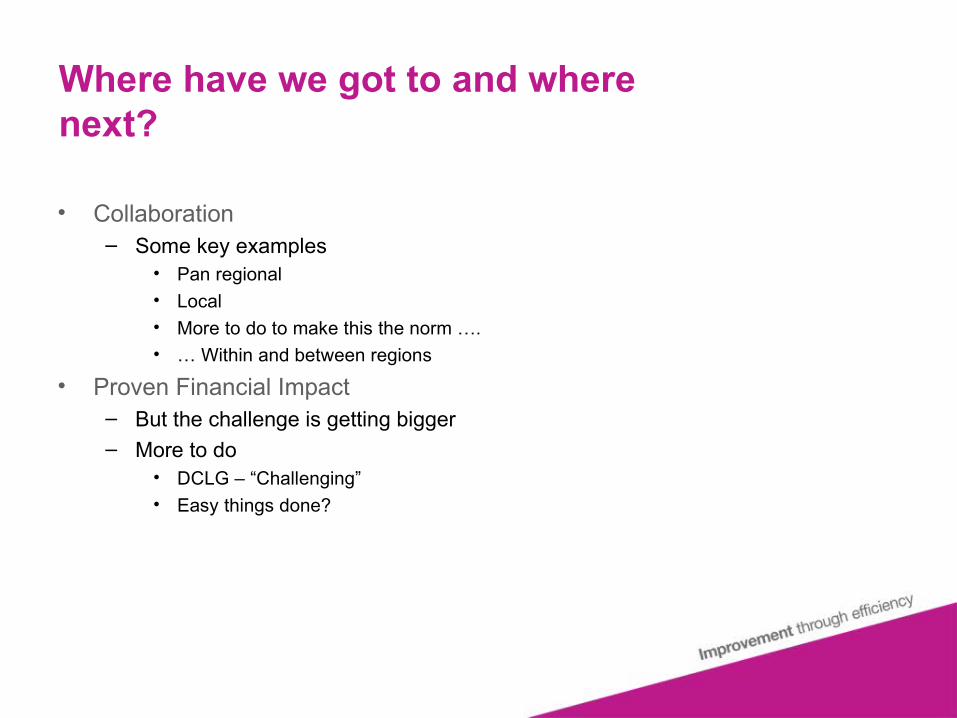

Where have we got to and where next?

• Collaboration– Some key examples

• Pan regional• Local• More to do to make this the norm ….• … Within and between regions

• Proven Financial Impact– But the challenge is getting bigger– More to do

• DCLG – “Challenging”• Easy things done?

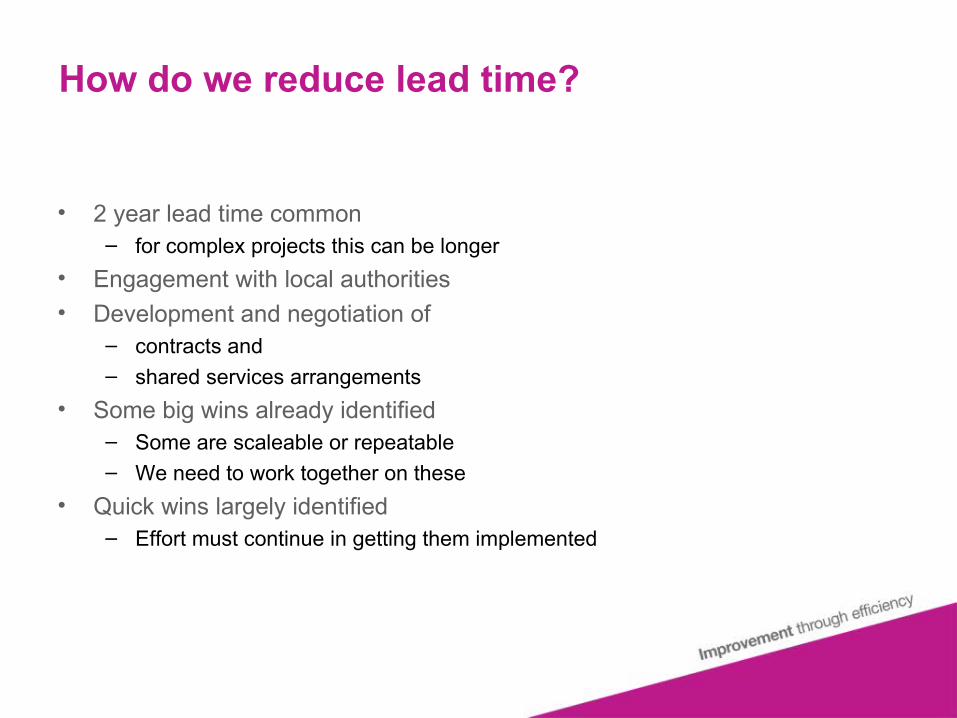

How do we reduce lead time?

• 2 year lead time common– for complex projects this can be longer

• Engagement with local authorities

• Development and negotiation of– contracts and– shared services arrangements

• Some big wins already identified– Some are scaleable or repeatable– We need to work together on these

• Quick wins largely identified– Effort must continue in getting them implemented

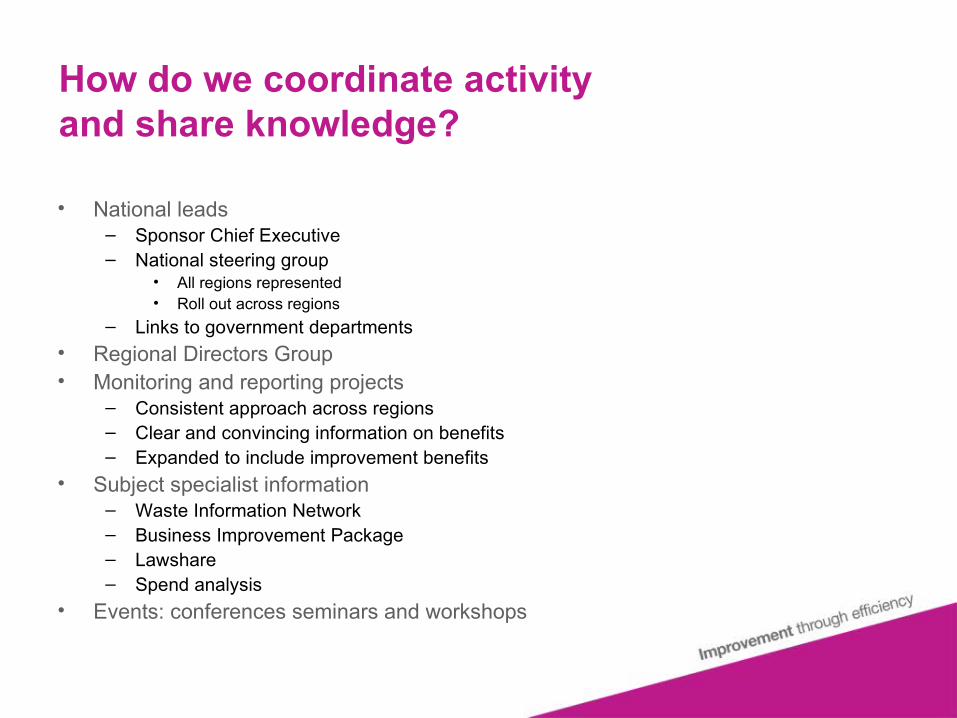

How do we coordinate activity and share knowledge?

• National leads– Sponsor Chief Executive– National steering group

• All regions represented• Roll out across regions

– Links to government departments

• Regional Directors Group• Monitoring and reporting projects

– Consistent approach across regions– Clear and convincing information on benefits– Expanded to include improvement benefits

• Subject specialist information– Waste Information Network– Business Improvement Package– Lawshare– Spend analysis

• Events: conferences seminars and workshops

How do we coordinate with Government?

• Nationally, DEFRA has identified six key priorities to support delivery of efficiency targets for waste management:

Priority Best Placed Lead

1.Effective and efficient procurement of goods and services that provide value for money by WCA’s

RCE’s

2. Effective Regional Procurement of large scale waste recycling, treatment and disposal infrastructure projects

DEFRA

3.Promoting and supporting Local Authorities in recycling infrastructure projects and initiatives

WRAP

4.Improving skills, knowledge and awareness RCE’s/ CIWM/ WRAP

5. Streamlined efficient systems and processes RCE’s

6. Service improvement programmes delivering “best in class” performance

RCE’s / WRAP

How do we ensure we transplant success?

• Framework procurement process in parallel with the first procurements across South East

– Kent, Oxfordshire, Buckinghamshire• What variation would be possible?

– A number of standard options under the framework

– Some variables would be settled when the authorities contract is let e.g. cost of back door collection. But against a standard pricing calculator

– Costs of what we are asking for would be transparent• How would a partnership of collection authorities work?

– A contract is let which has a variable start date– For each authority the new contract would start as their existing contract

ended

– The contract as a whole would come into effect as the first authority entered into it

How do we capitalise on big wins?

• Where are the big wins?– Large Buildings Framework– Insurance Municipal– Care Placements Pricing Tool– Regional shared procurement– LawShare Project– Business Process Improvement ….

• What sort of expertise do we need?– Procurement and project management– Process improvement and service redesign– Market understanding and domain expertise

• Can we also impact improvement?– Expertise used to manage collective arrangements– Add to this capacity to support activity in struggling

authorities– Essential to ensure a minimum standard

Cooperative Public Purchasing

Dr Andrew Larner

Regional Director

South East Improvement & Efficiency Partnership

www.sece.gov.uk