B.Grimm Power: Q2’2021

77

1 September 2021 B.Grimm Power: Q2’2021 Opportunity Day

Transcript of B.Grimm Power: Q2’2021

1

September 2021

B.Grimm Power:

Q2’2021

Opportunity Day

2

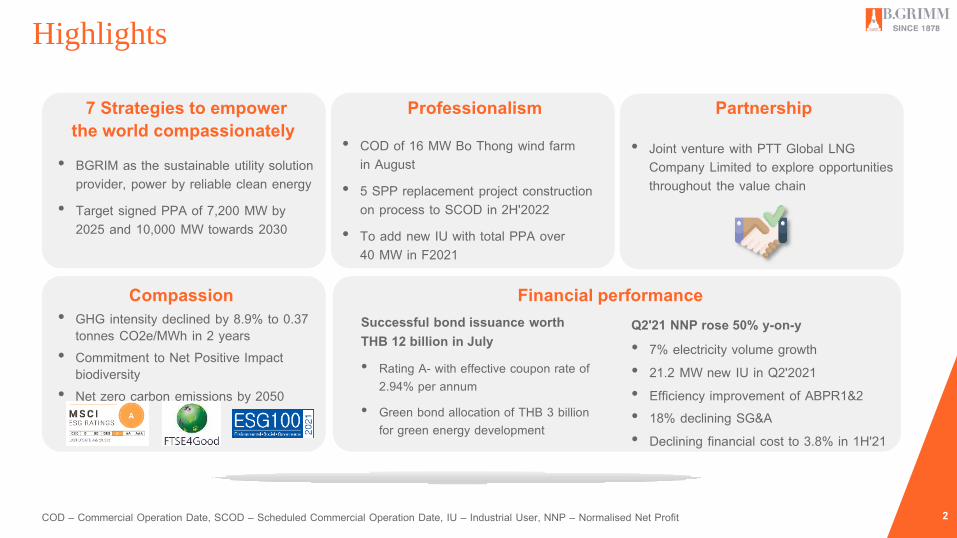

7 Strategies to empower Professionalism Partnershipthe world compassionately

• BGRIM as the sustainable utility solution provider, power by reliable clean energy

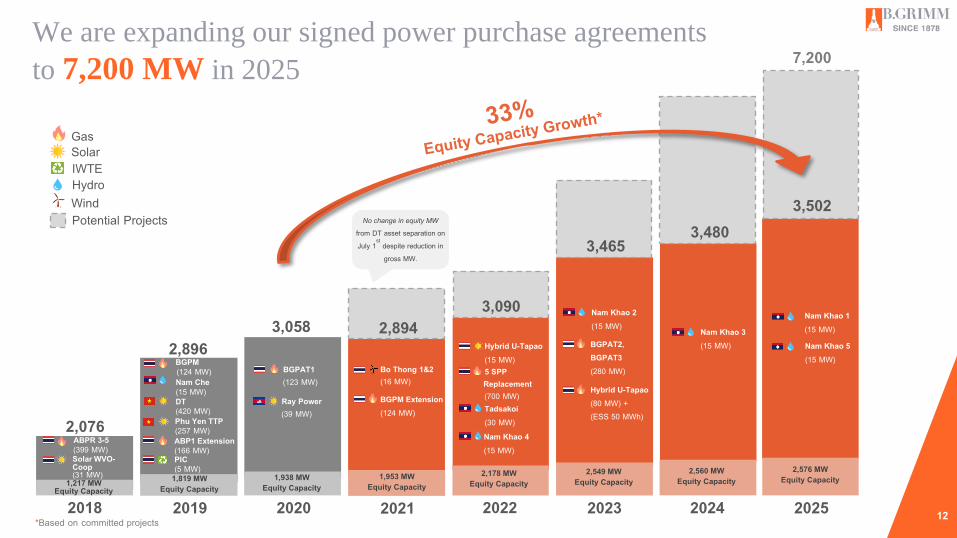

• Target signed PPA of 7,200 MW by 2025 and 10,000 MW towards 2030

Successful bond issuance worth THB 12 billion in July• Rating A- with effective coupon rate of

2.94% per annum• Green bond allocation of THB 3 billion

for green energy development

• GHG intensity declined by 8.9% to 0.37 tonnes CO2e/MWh in 2 years

• Commitment to Net Positive Impact biodiversity

• Net zero carbon emissions by 2050

Highlights

COD – Commercial Operation Date, SCOD – Scheduled Commercial Operation Date, IU – Industrial User, NNP – Normalised Net Profit

Compassion Financial performanceQ2'21 NNP rose 50% y-on-y • 7% electricity volume growth• 21.2 MW new IU in Q2'2021• Efficiency improvement of ABPR1&2• 18% declining SG&A• Declining financial cost to 3.8% in 1H'21

• COD of 16 MW Bo Thong wind farm in August

• 5 SPP replacement project construction on process to SCOD in 2H'2022

• To add new IU with total PPA over 40 MW in F2021

• Joint venture with PTT Global LNG Company Limited to explore opportunities throughout the value chain

3

Agenda

02 Professionalism

01 7 Strategies to Empower the world compassionately

03 Partnership

04 Compassion

05 Financial Performance

4

Our strategy is guided by our vision:

Empowering the world compassionately

That means empowering great people and partners to be a force for good in the societies and the environment where we operate.

EMPOWER

● Build human capabilities● Power industries, businesses

and communities

THE WORLD

● Find trusted partners and great opportunities in attractive countries

● Grow our footprint all over the world

COMPASSIONATELY

● Cultivate a culture of mindfulness and compassion among everyone at B.Grimm

5

As compassionate professionals, we believe we can achieve success by adhering to our four core values

PositivityTo continue at a world-class level, we work with positivity, demonstrate a strong can-do-attitude and stay flexible and tolerant in the face of difficulties.

PartnershipWe work together as a team, among each other, with our customers, with our partners and communities. We constantly build, maintain and value trustworthy relationships to bring well being, prosperity, and happiness to others.

Pioneering SpiritWe aim to be a leader in the power business, since the beginning of the company. To accomplish that, we have to actively always seek out new opportunities in both investment and development.

ProfessionalismWe strive for excellence and world-class standards on all levels: be it in developing or operating power plants.

6

Our five key success factorsgovern our long-term strategic success

Our capability to find attractive opportunities

Our capability to be an attractive partner of choice to others

Our capability to build, operate, and maintainstarting from greenfield

Our capability tofinance our growth at attractive rates

%

Our capability to embrace Digital Transformation

7

We will focus on 7 strategic initiatives to (em)power our future

Market Opportunities

Needs for lower cost of electricity and resources

Needs for reliable power in industrial estate

Needs for power transmission in other countries Energy trading

Implement wide ranging digital technologies

Significantly expand our gas and renewable generating capacity in the region (B2G)

7 StrategicInitiatives

1

Become a significant player in the LNG business and clean fuel supply

2

Grow our B2B solution offerings to industrialcustomers

3

Supply commercial building complexes with reliable utilities

4

Become a significant player in private transmission & distribution

5

Maximize reliability and viability in energy trading

6

Champion global best practices in digital transformation

7

Increasingelectricity demand in Asia Pacific (B2G)

Needs for end-to-end total solution for buildings

8

To be the Sustainable Utility Solution Provider, Powerby Reliable Clean Energy

Reliability Sustainability Affordability

Utility Solution Provider

9

SIGNIFICANTLY EXPAND OUR GAS AND RENEWABLE GENERATING

CAPACITY IN THE REGION (B2G)1

10

Many opportunities for government power purchase agreements (PPA) across the world with the biggest global power demand in Asia Pacific

Re-powering markets: Market design and regulation during the transition to low-carbon power

Gas turbines in the thermal power market, Growth rate by region 2020-2025

Growth trend: Low Medium HighSource: Mordor Intelligence report 2018, Team analysisSource: IEA (2016a), Team analysis

1

11

We will focus on expanding our power generation business regionally and internationally to empower the world compassionately

Offer cleaner energy globally through long term concessions

Cost leadership in project development, financing, fuel supply, and operational excellence

Become a local company to support community, society and economy wherever we go

1

12*Based on committed projects2018 2019

ABPR 3-5(399 MW)Solar WVO-Coop

2,076

2,896

1,217 MWEquity Capacity

1,819 MWEquity Capacity

BGPM(124 MW)Nam Che(15 MW)

(31 MW)

DT (420 MW)Phu Yen TTP(257 MW)ABP1 Extension(166 MW)PIC (5 MW)

7,200

HydroWind

GasSolarIWTE

Potential Projects

2020 2021 2022 2023 2024 2025

3,058

BGPAT1(123 MW)

Ray Power(39 MW)

Bo Thong 1&2 (16 MW)

BGPM Extension(124 MW)

Hybrid U-Tapao(15 MW)

2,894

1,938 MWEquity Capacity

3,090

5 SPPReplacement(700 MW)

Nam Khao 4(15 MW)

Tadsakoi(30 MW)

3,4653,480

3,502

1,953 MWEquity Capacity

2,178 MWEquity Capacity

2,549 MWEquity Capacity

2,560 MWEquity Capacity

2,576 MWEquity Capacity

No change in equity MW from DT asset separation on July 1

stdespite reduction in gross MW.

Nam Khao 2(15 MW)

BGPAT2, BGPAT3(280 MW)

Hybrid U-Tapao(80 MW) + (ESS 50 MWh)

Nam Khao 3(15 MW)

Nam Khao 1(15 MW)Nam Khao 5(15 MW)

We are expanding our signed power purchase agreements

to 7,200 MW in 2025

13

.. and 10,000 MW towards 2030

Hydro

GasSolar

Hybrid

Transmission and Distribution System (T&D)

Wind

LNGSolar Rooftop

LAOS

PHILIPPINES

THAILAND

MALAYSIA

VIETNAM

CAMBODIA

KOREA

MYANMAR

INDONESIA

NORTH AMERICA

EUROPE

14

BECOME A SIGNIFICANT PLAYER IN THE LNG BUSINESS AND CLEAN

FUEL SUPPLY2

15

The growth is in our backyard: Growing gas demand, declining domestic supply makes Southeast Asia one of the largest global markets for LNG

Myanmar

2020 2030 2040

Thailand

Philippines

Indonesia

Vietnam

Malaysia

Singapore15

60

114+660%

Source: Wood MacKenzie, BNEF, Team analysis

Demand for LNG (liquified natural gas) in Asia Pacific, 2020-2040, MMTPA

2

16

LNG is our most significant cost item: Going forward, we want to turn LNG into a strategic advantage and revenue generator

LNG shipper license, for 1.2 million tons in Thailand

Collaboration with key stakeholders, including power plants, industrial estate developers, and logistic providers

Establish strong team capabilities, in both commercial and technical, to best serve our partners

2

17

GROW OUR B2B SOLUTION OFFERING TO INDUSTRIAL CUSTOMERS3

18

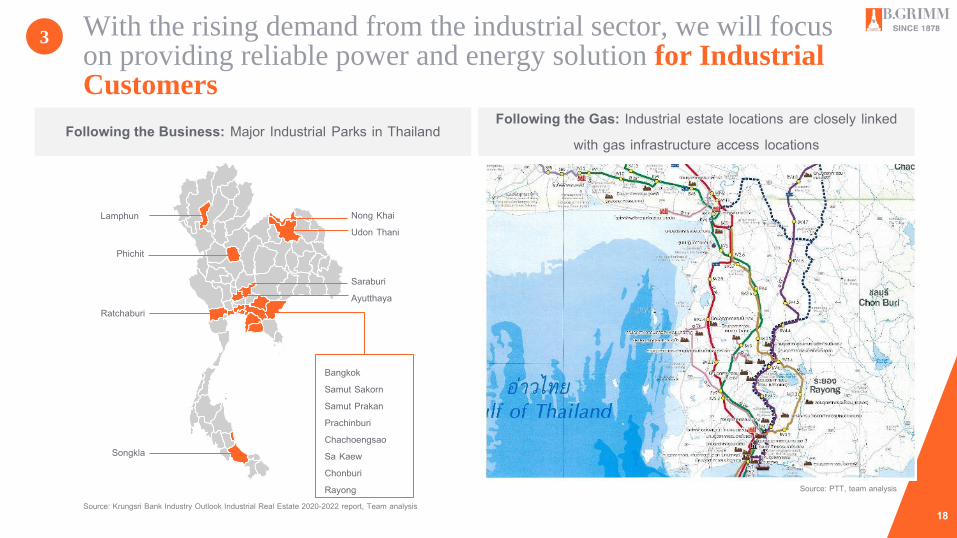

3

Following the Business: Major Industrial Parks in Thailand Following the Gas: Industrial estate locations are closely linked

with gas infrastructure access locations

Source: PTT, team analysis

Source: Krungsri Bank Industry Outlook Industrial Real Estate 2020-2022 report, Team analysis

Nong KhaiUdon Thani

Lamphun

Phichit

Ratchaburi

Songkla

SaraburiAyutthaya

BangkokSamut SakornSamut PrakanPrachinburiChachoengsaoSa KaewChonburiRayong

With the rising demand from the industrial sector, we will focus on providing reliable power and energy solution for Industrial Customers

19

Our industrial customer base is continuously expanding over 300 companies

Energy storage

Solar Power

Combined cycleco-generation power plant

Energy trading platform &Renewable energy certificate

We have been trusted by hundreds of our industrial partnerslocally and internationally to supply electricity and utilities solutions

3

20

3

New potential markets to come from Data Centers, EV manufacture, frozen warehouses, healthcare, modern warehouses

Create value for customers through reliability, smart energy, smart factories

Cost leadership from LNG import and operational excellence

Strategic partnership with industrial estate developers, MEA, PEA and industrial customers

We will focus on growing beyond industrial estates in the region, to provide extremely reliable electricity and additional services

21

BUILD A FOOTHOLD IN THE COMMERCIAL AND BUILDING SEGMENTS4

22

B.Grimm able to provide energy efficiency & healthy building solution by

• Captive power (Gas-Fired)• Solar panels and Inverters• Air-conditioning and controlling • Energy storage systems• Building management systems• Electric vehicle charging stations • Lighting sensors• Entry and exit controls• Power distribution boards

4Together with a variety of businesses under B.Grimm, we have the unique ability to be a total solutions provider to commercial and building end-users

23

4

Energy Businesses

Industrial Businesses

Energy Equipment Cooling TransportationBuildingMaterials

B.Grimm Power● Co-generation● LNG● Hydro● Solar● Wind● Hybrid● Backup for Power

Trading● Waste to energy● Distribution Systems

Hamon B.Grimm● Environmental- friendly

cooling towerB.Grimm Babcock Power● Energy-efficient HRSG

& heat exchanger

B.Grimm Carrier● Energy-saving &

healthy residential AC Carrier Thailand● Complete HVAC

solutionBeijer B.Grimm● AC parts and

refrigerationB.Grimm Aircon● AC factory with

customization

PCM ● Train equipment &

spare partsPanrail● Railway development

& maintenance

B.Grimm Trading ● Energy-efficient building

solutionMBM Metalworks● Bespoke & heat-

insulated FacadesChubb● Safety & Security

SolutionKSB Pumps● Pump & valves. ● SupremeServ Smart

services

We can provide something other groups cannot: A total solution for building and commercial clients

24

BECOME A SIGNIFICANT PLAYER IN PRIVATE TRANSMISSION AND

DISTRIBUTION5

25

Amata City Long Thanh

1 2

3

4 5

Amata City Chonburi

1

3

2

x Remote Substation

x ABP 1-5

From more than 25 years of experience in transmission and distribution systems, we can help improve power infrastructure globally

5

Amata City Halong

26

5

The largest private transmission and distribution network in the region with 9 strategic locations

Strong networking with regulator to ensure we end up in the right geography and space in the value chain

To be the leader in developing smart grids and smart cities

We will be the first mover in the market to focus on transmission and distribution beyond industrial estate.

27

MAXIMIZE VIABILITY AND RELIABILITY IN ENERGY TRADING6

28

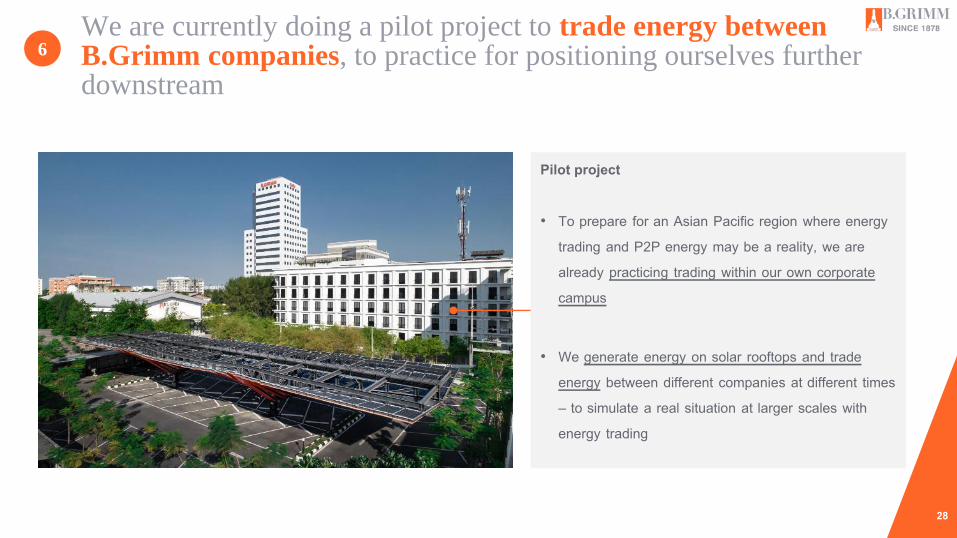

Pilot project

• To prepare for an Asian Pacific region where energy trading and P2P energy may be a reality, we are already practicing trading within our own corporate campus

• We generate energy on solar rooftops and trade energy between different companies at different times – to simulate a real situation at larger scales with energy trading

We are currently doing a pilot project to trade energy between B.Grimm companies, to practice for positioning ourselves further downstream

6

29

As distributed generation and renewables scale up, we seek to provide expertise and leadership in energy trading 6

30

CHAMPION GLOBAL BEST PRACTICES IN DIGITAL TRANSFORMATION7

31

7

Done right at scale, digital transformation will materially affect competitiveness and profitability

32

FINANCIAL STRATEGY & SUSTAINABILITY

33

Our corporate financial strategy to support 10-year growth consists

of 3 pillars

Installed Capacity

10,000 MW

10-yearCAPEX

250-300 billionTHB

2030 Revenue over 100 billion

THB

$

DEBTPrudent Capital Structure

Through budget forecasting and controlling system to monitor key financial ratio within target i.e.● Consolidated Net Debt to Equity

Ratio at 2.0 times ● Project level Debt to Equity Ratio

at 3.0 times

Fundraising Initiatives● Non-recourse/limited recourse

project loan● EPC financing● Green loan/debenture● Perpetual debenture● Asset recycling● Infrastructure fund● Vietnam IPO

Risk Mitigation

manage foreign exchange rate, interest rate risk through natural hedge and hedging instrument

34

PEOPLE

PLANET PROFIT

PEOPLE

PROFIT

PLANETAim to achieve carbon neutral by 2050

Students joined tiger conservation education6,704

Total Areas of Reforestation (sq.m.)

711,199

11Years of supportingDual Vocation Education Programs

11Years of supportingThe Little Scientists’ House

18Years of supporting Equestrian Sports in Thailand

16Years of supporting Royal Bangkok Symphony Orchestra

Generating Capacity in 2030Revenue (THB)in 2030

10,000 MW

> 100 Billion

With compassion, business can exist in harmony with nature

35

We have been continuously awarded various sustainability recognitions after IPO in 2017

FTSE4GOOD Emerging IndexFTSE4GOOD ASEAN 5 Index

MSCI ESG Rating: A

Thailand Sustainability Investment by SET3 consecutive years (2018-2020)

ESG 100 company by Thaipat Institute4 consecutive years (2018-2021)

Thai CAC certifiedby Thailand’s Private Sector Collective Action 2 consecutive terms

CGR Score: EXCELLENTby Thai Institute of Directors Association

2018 The first green bond certified by Climate Bond Initiative in Thailand

2020 The first green loan certified by Climate Bond Initiative in CLMVT

36

Empowering the world compassionately as a Utility Solution

Provider with net zero carbon emission in 2050

Reliability Sustainability Affordability

Utility Solution ProviderSignificantly expand gas and renewable generating capacity to the areas where electricity is insufficient1Become a significant player in the LNG business and clean fuel supply2Grow our B2B solution offerings to industrial customers3Build a foothold in commercial and buildingsegments4Become a significant player in private transmission & distribution5Maximize reliability and viability in energy trading6Champion global best practices in digital transformation7

37

Agenda

02 Professionalism

01 7 Strategies to Empower the world compassionately

03 Partnership

04 Compassion

05 Financial Performance

38

81.9%

15.6%1.9%

0.6%Waste to Energy

(IWTE) 5 MW

GAS – FIRED POWER PLANT (INDUSTRIAL POWER PLANTS) RENEWABLE GROUP

TRANSMISSION & DISTRIBUTION

25.6%

24.5%10.6%

4.7%

8.7%

8.7%

7.4%4.9%3.0%

Solar Group696 MW

(15 MW UnderDevelopment)

Total 849 MWIn Operation 737 MW*Total 2,640 MW

In Operation 2,144 MW*

Amata City (Chonburi)675 MW

(Including ABP1&2 Replacement of 140 MW each)

Amata City (Rayong) 647 MW

Bangkadi229 MW

Laem Chabang196 MW

(Including BPLC1 Replacement of 140 MW)

WHA Chonburi 1130 MW

World Food Valley280 MW

(Under Development)

Hydro Group133 MW

(98 MW Under Development)

Poi Pet PPSEZ 14 MW**

*As of August 2021**Transmission & distribution and solar rooftop are not included in total installed capacity

SOLAR ROOFTOP

Solar rooftop for industrial users and commercial buildings with up to 100 MW opportunity**

WHA (Map Ta Phut)280 MW

(Including BGPM Replacement of 140 MW each)

Angthong Province123 MW

Type of EnergyInstalled MW Equity MW

Total Capacity % In Operation Total Capacity % In OperationGas fired 2,560 MW 73.1 2,144 MW 1,769 MW 68.7 1,311 MWSolar 681 MW 19.4 681 MW 596 MW 23.1 596 MWHydro 133 MW 3.8 35 MW 95 MW 3.6 25 MWHybrid 95 MW 2.7 95 MW 3.7Wind 16 MW 0.5 16 MW 15 MW 0.6 15 MWIWTE 5 MW 0.1 5 MW 2 MW 0.1 2 MWBackup for power

trading 13 MW 0.4 13 MW 4 MW 0.2 4 MW

Total 3,502 MW 100 2,894 MW* 2,576 MW 100 1,953 MW*

U-Tapao Area (Hybrid)80 MW

(Under Development)

Wind Group16 MW

Well-diversified portfolio with expertise in green-field development

Bien Hoa 90 MW (with 13 MW back up for power trading)

39

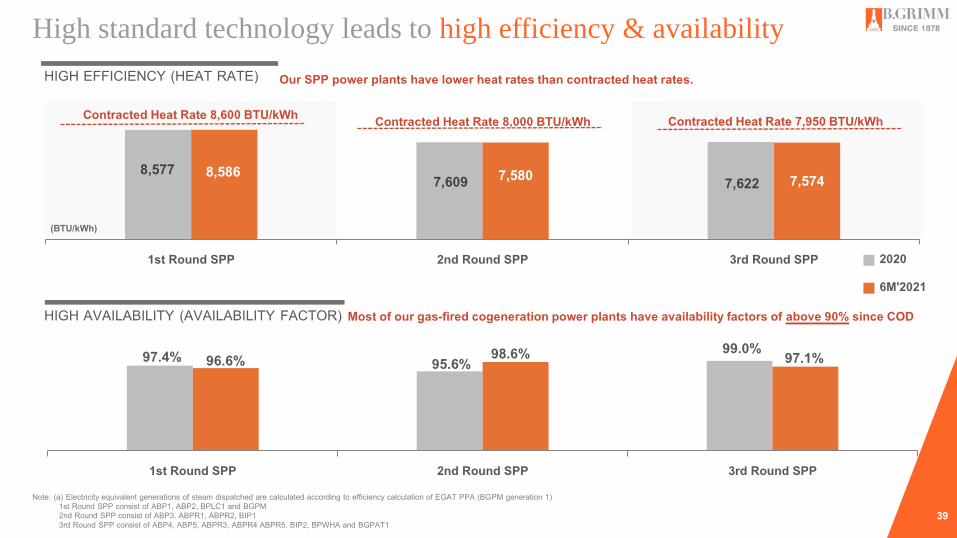

8,5777,609 7,6228,586 7,580 7,574

1st Round SPP 2nd Round SPP 3rd Round SPP 2020

6M'2021

97.4% 95.6%99.0%

96.6% 98.6% 97.1%

1st Round SPP 2nd Round SPP 3rd Round SPP

HIGH AVAILABILITY (AVAILABILITY FACTOR)

HIGH EFFICIENCY (HEAT RATE) Our SPP power plants have lower heat rates than contracted heat rates.

Contracted Heat Rate 8,600 BTU/kWh Contracted Heat Rate 8,000 BTU/kWh Contracted Heat Rate 7,950 BTU/kWh

(BTU/kWh)

Note: (a) Electricity equivalent generations of steam dispatched are calculated according to efficiency calculation of EGAT PPA (BGPM generation 1)1st Round SPP consist of ABP1, ABP2, BPLC1 and BGPM2nd Round SPP consist of ABP3, ABPR1, ABPR2, BIP1 3rd Round SPP consist of ABP4, ABP5, ABPR3, ABPR4 ABPR5, BIP2, BPWHA and BGPAT1

Most of our gas-fired cogeneration power plants have availability factors of above 90% since COD

High standard technology leads to high efficiency & availability

40

5 Under ConstructionReplacement In OperationABP1, ABP2, BPLC1, BGPM1, BGPM2

(SCOD in 2022)

ABP3, ABP4, ABP5, BPWHA, ABPR1, ABPR2, ABPR3, ABPR4, ABPR5, BIP1, BIP2,

BPLC2, BGPAT1

BGPAT2, BGPAT3(SCOD in 2023)

New Technology

MW increase by 135 MW

IUs portion

Gas consumption by 10-15%

Wastewater treatment capacity

MW increase by 280 MW

Food and beverage customer's base

Upgrading gas turbine of 6 projects under LTSA with Siemens during 2019-2023

LNG import for fuel-cost flexibility

7 MW / plant available for IU

SPP Portfolio

218

Maintenance period

Gas consumption by 1%

New Technology

Improve efficiency continually

41

Benefits from the LTSA with SiemensEnhance Availability To increase availability or reduce the number of

maintenance days from 18-20 days to 10-15 days

To predict the degradation of a machine more accurateMoving towards Digitalization

Enhance Efficiency To enhance heat rate of gas turbine after performingmajor overhaul and doing design improvement

More operating days

More MW for IUs

Lower gas consumption by 1%

2019Plants 2018 2020

Nov Jan

Jul

Feb Nov

Jun-Jul

Aug-Oct

Feb

Jan

2 Gas Turbines 1 Gas Turbine2021 2022

LTSA Upgrade Schedule

BPWHA

ABPR2

ABPR1

ABP5

ABP3

ABP4

1

2

3

4

5

6

Asian Power Award 2020: “Power Plant Upgrade of

the Year-Thailand”by Asian Power Magazine

2023

Enhancing performance of operating projects

42

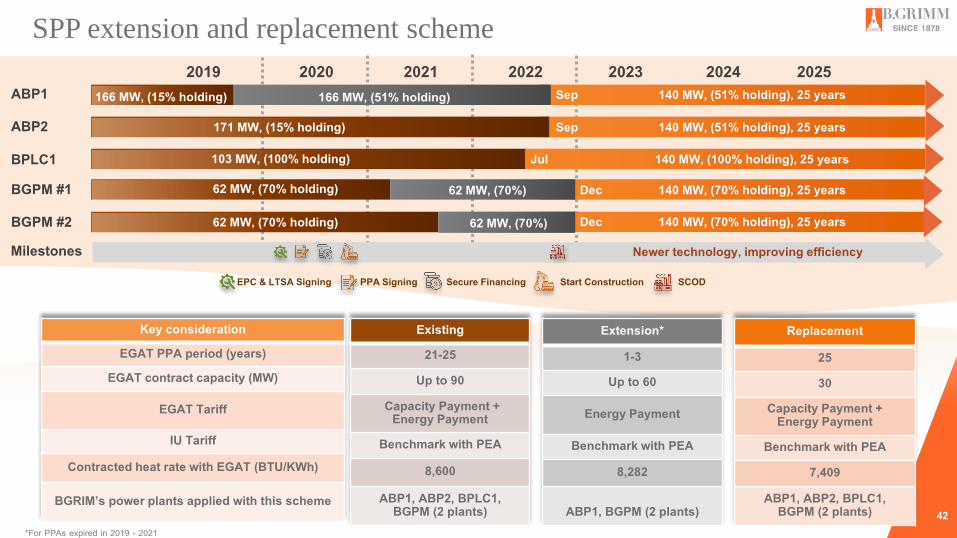

ABP12019 2020 2021 2022 2023 2024 2025

ABP2

BPLC1BGPM #1

BGPM #2

166 MW, (15% holding) 140 MW, (51% holding), 25 years

140 MW, (51% holding), 25 years

140 MW, (100% holding), 25 years

171 MW, (15% holding)

103 MW, (100% holding)

62 MW, (70% holding)

62 MW, (70% holding)

62 MW, (70%)

62 MW, (70%)

140 MW, (70% holding), 25 years

140 MW, (70% holding), 25 years

166 MW, (51% holding)

Milestones

Sep

Sep

Jul

Dec

Dec

EPC & LTSA Signing PPA Signing Secure Financing Start Construction SCOD

Key considerationEGAT PPA period (years)

EGAT contract capacity (MW)

EGAT Tariff

IU Tariff

Contracted heat rate with EGAT (BTU/KWh)

BGRIM’s power plants applied with this scheme

Replacement

2530

Capacity Payment + Energy Payment

Benchmark with PEA7,409

ABP1, ABP2, BPLC1, BGPM (2 plants)

Extension*1-3

Up to 60

Energy Payment

Benchmark with PEA8,282

ABP1, BGPM (2 plants)

Existing 21-25

Up to 90Capacity Payment +

Energy PaymentBenchmark with PEA

8,600

ABP1, ABP2, BPLC1, BGPM (2 plants)

*For PPAs expired in 2019 - 2021

SPP extension and replacement scheme

Newer technology, improving efficiency

43

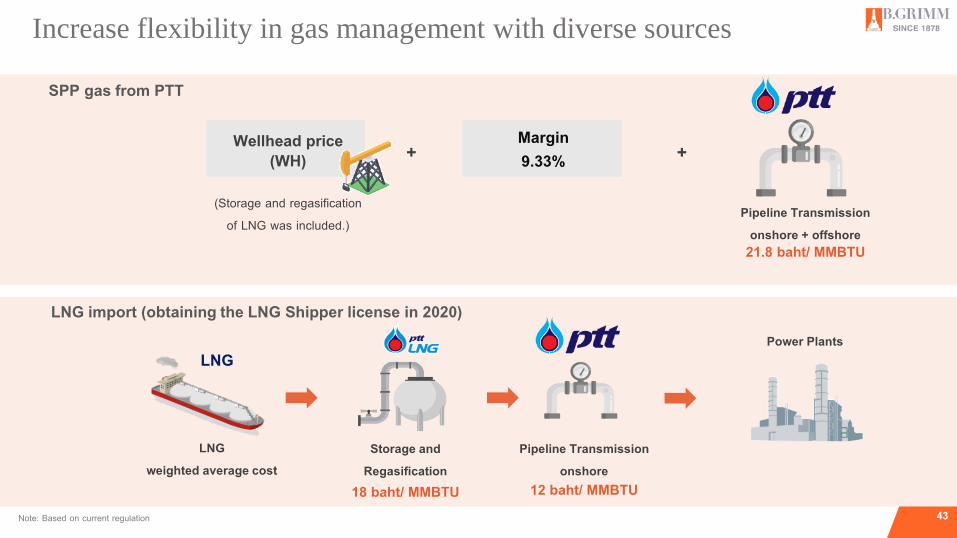

Lower gas consumption by 1%

LNG weighted average cost

Storage and Regasification

Pipeline Transmissiononshore

Note: Based on current regulation

Power PlantsLNG

LNG import (obtaining the LNG Shipper license in 2020)

SPP gas from PTT

21.8 baht/ MMBTU

+ +

Pipeline Transmissiononshore + offshore

18 baht/ MMBTU 12 baht/ MMBTU

(Storage and regasification of LNG was included.)

Wellhead price(WH)

Margin9.33%

Increase flexibility in gas management with diverse sources

44

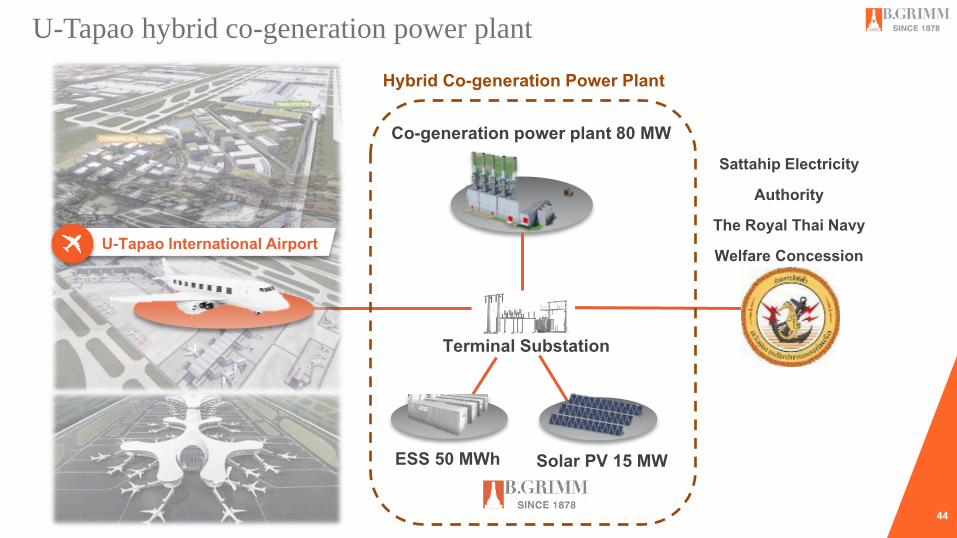

Solar PV 15 MWESS 50 MWh

Co-generation power plant 80 MW

Hybrid Co-generation Power Plant

U-Tapao International Airport

Terminal Substation

Sattahip Electricity Authority

The Royal Thai Navy Welfare Concession

U-Tapao hybrid co-generation power plant

45

Agenda

02 Professionalism

01 7 Strategies to Empower the world compassionately

03 Partnership

04 Compassion

05 Financial Performance

46

B.Grimm Power PCLIndustrial Power Plant

HydroSolar

Wind

Hybrid

Waste to Energy

Distribution Systems

B.Grimm Trading CorporationHamon – B.GrimmB.Grimm Babcock Power

Energy Equipment

CoolingB.Grimm. AirconditioningB.Grimm Carrier (Thailand) Carrier (Thailand) Beijer B.Grimm (Thailand) TransportPCM Transport and Panrail (Thailand)B.Grimm Maritime Building MaterialsB. Grimm Trading CorporationKSB PumpsChubb (Thailand)MBM Metalworks

Merck ThailandGetinge Group ThailandZeiss ThailandBiomonde (Thailand) Primo Care Clinic

Energy Industrial Healthcare Lifestyle & Real Estate

B.Grimm Real EstateB.Grimm Country ClubThe MET Store ThailandNymphenburg PorcelainParis SpaProvence Restaurant

Strong partnership - Synergy under B.Grimm umbrella

47

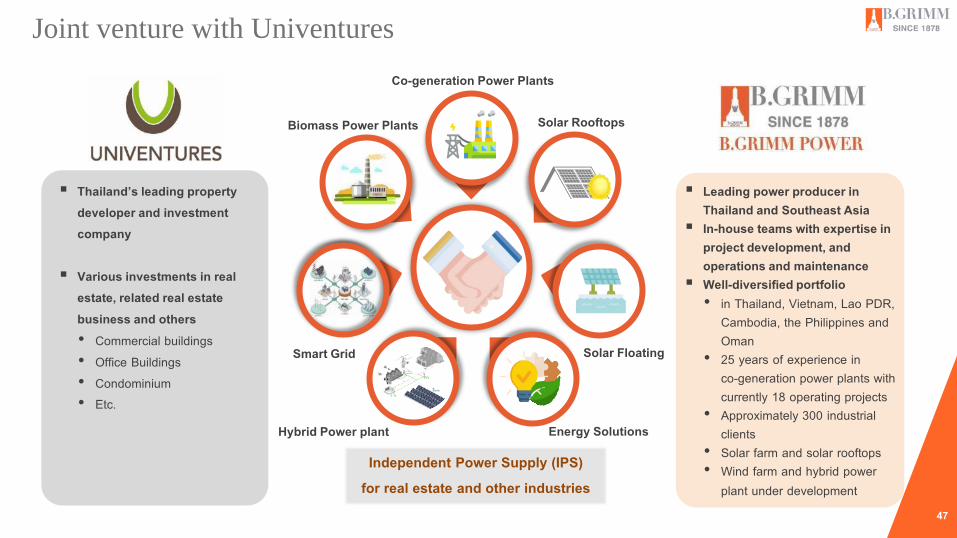

▪ Leading power producer in Thailand and Southeast Asia

▪ In-house teams with expertise in project development, and operations and maintenance

▪ Well-diversified portfolio• in Thailand, Vietnam, Lao PDR,

Cambodia, the Philippines and Oman

• 25 years of experience in co-generation power plants with currently 18 operating projects

• Approximately 300 industrial clients

• Solar farm and solar rooftops• Wind farm and hybrid power

plant under development

▪ Thailand’s leading property developer and investment company

▪ Various investments in real estate, related real estate business and others • Commercial buildings • Office Buildings• Condominium• Etc.

Solar RooftopsBiomass Power Plants

Co-generation Power Plants

Solar FloatingSmart Grid

Independent Power Supply (IPS) for real estate and other industries

Joint venture with Univentures

Hybrid Power plant Energy Solutions

48

Joint venture with PTT Global LNG company limited

Cooperation with PTTGL to procure and supply LNG and explore other business opportunities related to LNG value chainboth domestically and internationally together

49

Exploring business opportunities with MEA, PEA and PEA ENCOM

• Independent Power Supply (IPS) • Service coverage expansion• Microgrid and Smart Microgrid

System• Renewable project expansion

Partner with MEA, PEA and PEA ENCOM

50

FOOTHOLD IN TOP INDUSTRIAL ESTATES WITHMULTIPLE OF GENERATING UNITS IN EACH LOCATION

SELECTED TOP IU FOR ELECTRICITY AND STEAM

THAILAND

CAMBODIA

LAOS

VIETNAM▪ 1 power plant▪ 130 MW▪ 3 generating units

▪ 2 power plants▪ 229 MW ▪ 6 generating units

▪ 2 power plants▪ 280 MW▪ 6 generating units

▪ 5 power plants ▪ 647 MW▪ 15 generating units

▪ 5 power plants ▪ 732 MW▪ 17 generating units

▪ 2 power plants ▪ 159 MW▪ 5 generating units

WHA Chonburi 1

Bangkadi

BGPAT2&3

Amata CityRayong

Amata City Bien Hoa

Gas-fired cogeneration power plants Transmission and Distribution

▪ 2 power plants ▪ 124 MW▪ 4 generating units

WHA Eastern (Map Ta Phut)

Amata CityChonburi

Laem Chabung

Poi Pet PP SEZ

▪ 1 power plant▪ 123 MW ▪ 3 generating units

World Food Valley

Long-term relationship with industrial estates and customers

51

Agenda

02 Professionalism

01 7 Strategies to Empower the world compassionately

03 Partnership

04 Compassion

05 Financial Performance

52

Solar power plants

Hydro power plants

Waste to energy power plantWind power plant

THAILAND

CAMBODIA

LAOS

VIETNAM

▪ 8 power plants▪ 60 MW

▪ 1 power plant ▪ 8 MW

▪ 1 power plant ▪ 8 MW

BGYSP

Solar WVO-Coop

Nam Khao▪ 5 power plants▪ 67.5 MW

BGPSK

TPS Com.

DT▪ 1 power plant▪ 240 MW

Phu Yen TTP▪ 1 power plant▪ 257 MW

Nam Che 1▪ 1 power plant▪ 15 MW

▪ 7 power plants▪ 31 MW

Solarwa▪ 5 power plants▪ 39 MW

▪ 1 power plant▪ 5 MW

PIC

XXHP▪ 1 power plant▪ 20 MW

Tadsakoi▪ 1 power plant▪ 30 MW

▪ 2 power plants▪ 16 MW

Bo Thong

▪ 1 power plant ▪ 39 MW

Ray Power

Expanding renewable power continually

53

100% of SPP projects implemented• ISO 14001 Environmental

Management Systems• OHSAS 18001 / ISO 45001

Occupational Health and Safety Management System

Commit to Net Positive Impact (NPI) on biodiversity

11.9% reducing in netwater consumption in 2020 (vs 2019)

GHG intensity declined by 8.9% from 2018 to 0.37 tonnes CO2e/MWh in 2020

0% Fatality

Board Diversity• Independent directors 60% • Female directors 50%

CGR score of “Excellent”

ZERO case of corruption and non-complianceRenewable capacity rose to 29%

in 2020 from 8% in 2018

More than 60% of total water consumption was from mixed wastewater

Sustainability highlights

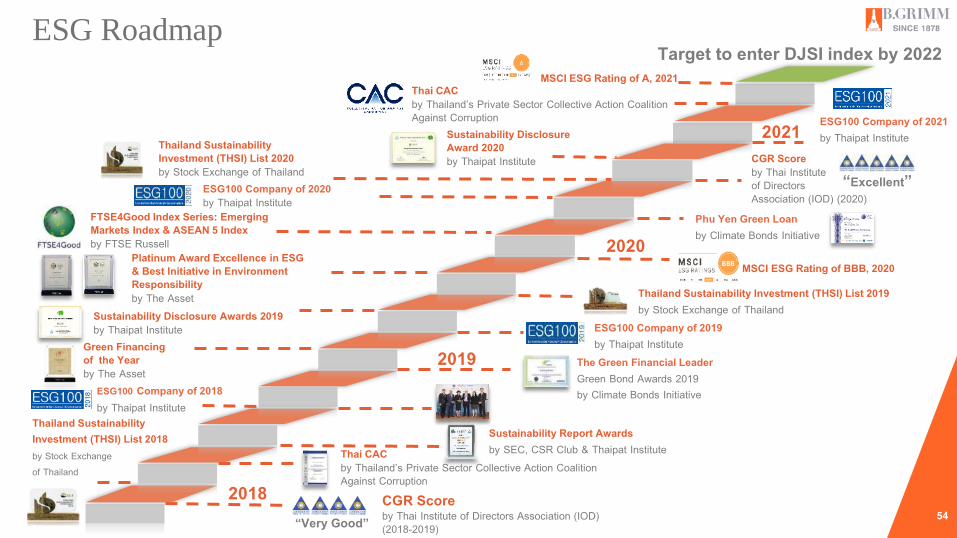

54

Target to enter DJSI index by 2022MSCI ESG Rating of A, 2021

Thailand Sustainability Investment (THSI) List 2019by Stock Exchange of Thailand

Green Financing of the Yearby The Asset

Sustainability Report Awardsby SEC, CSR Club & Thaipat Institute

Thailand Sustainability Investment (THSI) List 2018by Stock Exchange of Thailand

ESG100 Company of 2018by Thaipat Institute

2018 CGR Scoreby Thai Institute of Directors Association (IOD)(2018-2019)

Thai CACby Thailand’s Private Sector Collective Action Coalition Against Corruption

2019 The Green Financial LeaderGreen Bond Awards 2019by Climate Bonds Initiative

ESG100 Company of 2019by Thaipat Institute

Sustainability Disclosure Awards 2019by Thaipat Institute

Platinum Award Excellence in ESG & Best Initiative in Environment Responsibility by The Asset

FTSE4Good Index Series: Emerging Markets Index & ASEAN 5 Indexby FTSE Russell

Phu Yen Green Loanby Climate Bonds Initiative

“Very Good”

2020

ESG100 Company of 2020by Thaipat Institute

Thailand Sustainability Investment (THSI) List 2020by Stock Exchange of Thailand

CGR Scoreby Thai Institute of Directors Association (IOD) (2020)

“Excellent”

Sustainability Disclosure Award 2020by Thaipat Institute

2021

Thai CACby Thailand’s Private Sector Collective Action Coalition Against Corruption ESG100 Company of 2021

by Thaipat Institute

MSCI ESG Rating of BBB, 2020

ESG Roadmap

55

Agenda

02 Professionalism

01 7 Strategies to Empower the world compassionately

03 Partnership

04 Compassion

05 Financial Performance

56

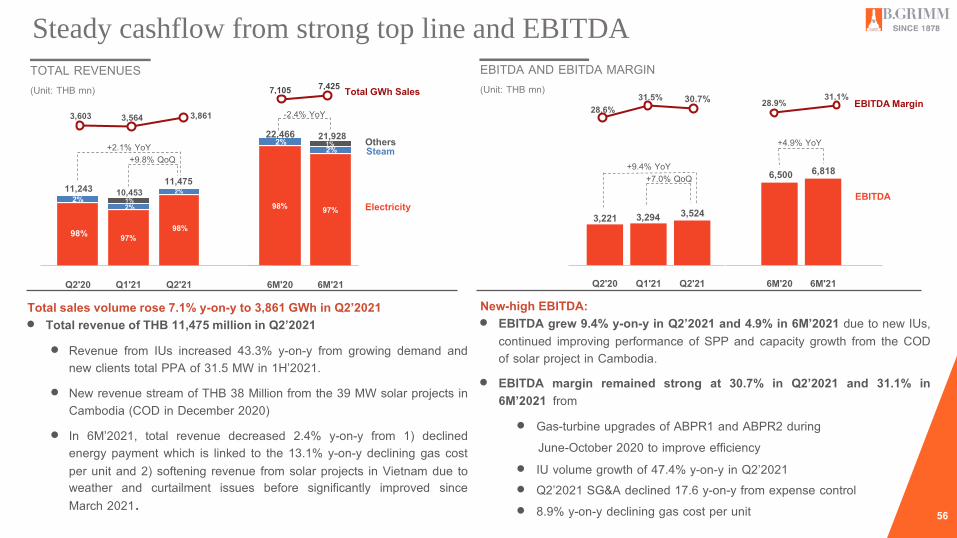

EBITDA AND EBITDA MARGIN (Unit: THB mn)

28.9% 31.1%

3,221 3,294 3,524

6,500 6,818

Q2'20 Q1'21 Q2'21 6M'20 6M'21

New-high EBITDA:• EBITDA grew 9.4% y-on-y in Q2’2021 and 4.9% in 6M’2021 due to new IUs,

continued improving performance of SPP and capacity growth from the CODof solar project in Cambodia.

• EBITDA margin remained strong at 30.7% in Q2’2021 and 31.1% in6M’2021 from• Gas-turbine upgrades of ABPR1 and ABPR2 during

June-October 2020 to improve efficiency• IU volume growth of 47.4% y-on-y in Q2’2021• Q2’2021 SG&A declined 17.6 y-on-y from expense control• 8.9% y-on-y declining gas cost per unit

EBITDA Margin

EBITDA+7.0% QoQ

+9.4% YoY

28.6%31.5% 30.7%

+4.9% YoY

TOTAL REVENUES (Unit: THB mn) 7,105 7,425

98% 97%98%

98% 97%2%

2%

2%1%

2%2%

11,243 10,45311,475

Q2'20 Q1'21 Q2'21 6M'20 6M'21

3,603 3,564 3,861

Total sales volume rose 7.1% y-on-y to 3,861 GWh in Q2’2021• Total revenue of THB 11,475 million in Q2’2021

• Revenue from IUs increased 43.3% y-on-y from growing demand andnew clients total PPA of 31.5 MW in 1H’2021.

• New revenue stream of THB 38 Million from the 39 MW solar projects inCambodia (COD in December 2020)

• In 6M’2021, total revenue decreased 2.4% y-on-y from 1) declinedenergy payment which is linked to the 13.1% y-on-y declining gas costper unit and 2) softening revenue from solar projects in Vietnam due toweather and curtailment issues before significantly improved sinceMarch 2021.

Electricity

SteamOthers+2.1% YoY

+9.8% QoQ

Total GWh Sales

1%22,466 21,928

-2.4% YoY

Steady cashflow from strong top line and EBITDA

57

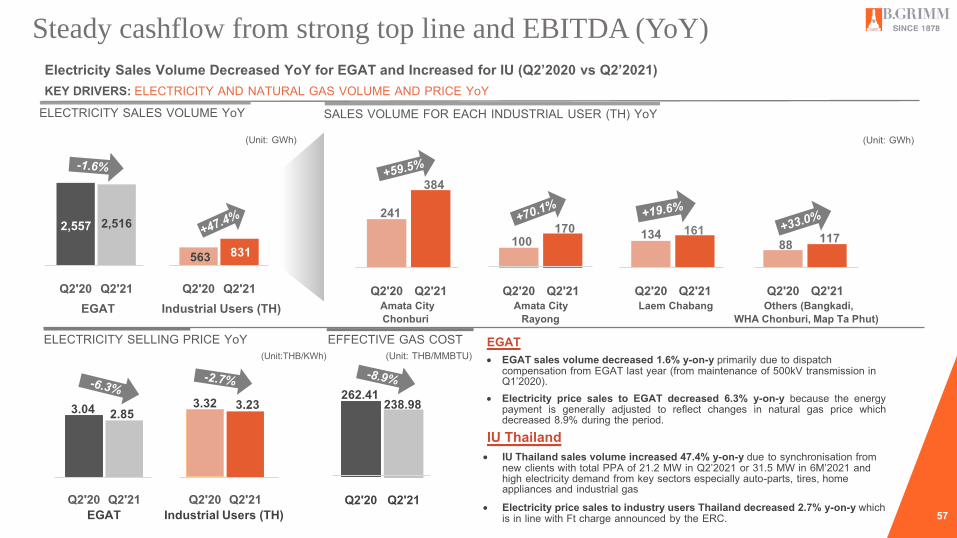

ELECTRICITY SALES VOLUME YoY SALES VOLUME FOR EACH INDUSTRIAL USER (TH) YoY

241

384

100170 134 161

88 117

Q2'20 Q2'21 Q2'20 Q2'21 Q2'20 Q2'21 Q2'20 Q2'21Amata City Amata City Laem Chabang Others (Bangkadi, Chonburi Rayong WHA Chonburi, Map Ta Phut)

2,557

563

2,516

831 -

500

1,000

1,500

2,000

2,500

3,000

Q2'20 Q2'21 Q2'20 Q2'21

3.04 2.853.32 3.23

Q2'20 Q2'21 Q2'20 Q2'21EGAT Industrial Users (TH)

EFFECTIVE GAS COST

Q2'20 Q2'21

ELECTRICITY SELLING PRICE YoY

262.41 238.98

EGAT• EGAT sales volume decreased 1.6% y-on-y primarily due to dispatch

compensation from EGAT last year (from maintenance of 500kV transmission in Q1’2020).

• Electricity price sales to EGAT decreased 6.3% y-on-y because the energypayment is generally adjusted to reflect changes in natural gas price whichdecreased 8.9% during the period.

IU Thailand• IU Thailand sales volume increased 47.4% y-on-y due to synchronisation from

new clients with total PPA of 21.2 MW in Q2’2021 or 31.5 MW in 6M’2021 and high electricity demand from key sectors especially auto-parts, tires, home appliances and industrial gas

• Electricity price sales to industry users Thailand decreased 2.7% y-on-y which is in line with Ft charge announced by the ERC.

(Unit: GWh) (Unit: GWh)

EGAT Industrial Users (TH)

KEY DRIVERS: ELECTRICITY AND NATURAL GAS VOLUME AND PRICE YoY Electricity Sales Volume Decreased YoY for EGAT and Increased for IU (Q2’2020 vs Q2’2021)

Steady cashflow from strong top line and EBITDA (YoY)

(Unit:THB/KWh) (Unit: THB/MMBTU)

58

ELECTRICITY SELLING PRICE QoQ

2,300 814

2,516

831 -

500

1,000

1,500

2,000

2,500

Q1'21 Q2'21 Q1'21 Q2'21

2.72 2.853.23 3.23

Q1'21 Q2'21 Q1'21 Q2'21EGAT Industrial Users (TH)

EGAT Industrial Users (TH)

Q1'21 Q2'21

387 384

152 170 168 161 108 117 -

100

200

300

400

500

Q1'21 Q2'21 Q1'21 Q2'21 Q1'21 Q2'21 Q1'21 Q2'21Amata City Amata City Laem Chabang Others (Bangkadi, Chonburi Rayong WHA Chonburi, Map Ta Phut)

SALES VOLUME FOR EACH INDUSTRIAL USER (TH) QoQELECTRICITY SALES VOLUME QoQ

EFFECTIVE GAS COST

220.64 238.980.0%

Steady cashflow from strong top line and EBITDA (QoQ)

KEY DRIVERS: ELECTRICITY AND NATURAL GAS VOLUME AND PRICE QoQElectricity Sales Volume Increased QoQ for EGAT and Increased for IU (Q1’2021 vs Q2’2021)

(Unit:THB/KWh)

(Unit: GWh) (Unit: GWh)

(Unit: THB/MMBTU) EGAT• EGAT sales volume increased 9.4% q-on-q primarily due to more scheduled

maintenance during Q1’2021.• Electricity price sales to EGAT increased 4.8% q-on-q because the energy

payment is generally adjusted to reflect changes in natural gas price which increased in Q2’2021.

IU Thailand• IU Thailand sales volume increased 2.0% q-on-q primarily due to growth from

auto-parts, tires, home appliances and industrial gas and new clients with total PPA of 21.2 MW in Q2’2021.

• Electricity price sales to industry users Thailand remain unchanged which is in line with Ft charge announced by the ERC.

59

Auto part42%

Tire17%

Industrial Gas10%

Home Appliance 9%

Packaging6%

Consumer3%

Others13%

Q2’2021 IU VOLUME BREAKDOWN BY SECTOR

EGAT63%

IU-TH23%

EVN7% IU-VN

3%PEA, MEA, EDC2%

Steam2%

EDL1%

THB 11,476 mnQ2’2021

Sales and Service Income

Q2’2021 REVENUE BREAKDOWN BY CUSTOMER

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019 2020 2021

New-high IU volume of 831 GWh in Q2’2021

(Thai new year)

Revenue breakdown

IU Volume

60

261.56 269.57 271.02 266.33 261.09 256.80 241.30 236.01 228.35 211.94212.48 217.68 220.16 219.52 220.83 231.95 239.19 244.53

265.43 259.38 255.92270.13 265.53 265.29

SPP Gas Price (THB/MMBTU)Ft (THB/kWh)

Source: ERC and PTT

Based on 2019 figures;

◼ THB 0.01 change in IU tariff would impact earnings by THB 18 million per annum.

◼ THB 1/MMBTU change in gas cost would impact earnings by THB 15 million per annum.

-0.1160 -0.1160 -0.1160 -0.1160 -0.1160 -0.1160 -0.1160 -0.1160 -0.1243 -0.1243 -0.1243 -0.1243-0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532 -0.1532

Ft charge and gas price

61

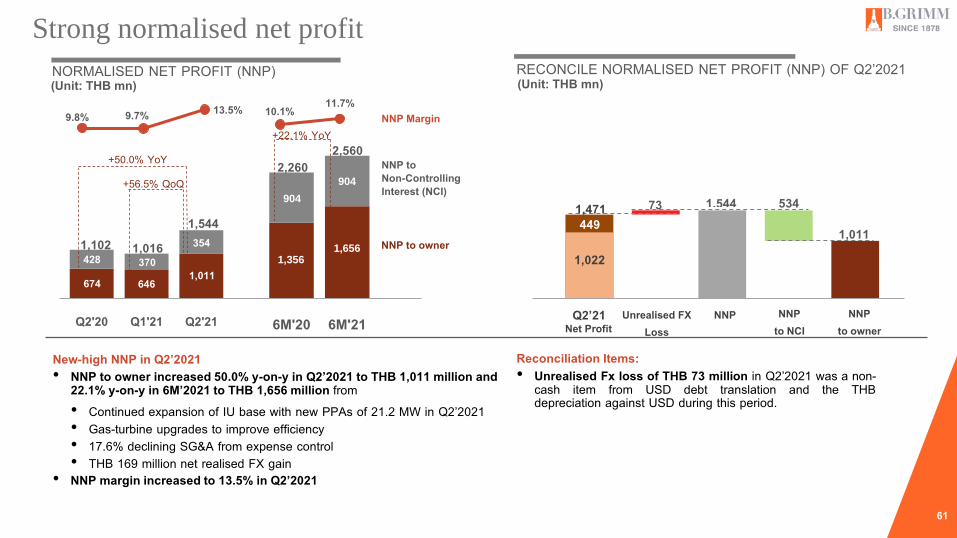

RECONCILE NORMALISED NET PROFIT (NNP) OF Q2’2021

1,3561,656

904

904

6M'20 6M'21

9.8% 9.7% 13.5%

674 646 1,011428 370

3541,102 1,016 1,544

0

500

1000

1500

2000

Q2'20 Q1'21 Q2'21

+56.5% QoQ

+50.0% YoY

NNP Margin

NNP to owner

NNP to Non-Controlling Interest (NCI)

10.1% 11.7%

2,2602,560

+22.1% YoY

New-high NNP in Q2’2021• NNP to owner increased 50.0% y-on-y in Q2’2021 to THB 1,011 million and

22.1% y-on-y in 6M’2021 to THB 1,656 million from• Continued expansion of IU base with new PPAs of 21.2 MW in Q2’2021• Gas-turbine upgrades to improve efficiency• 17.6% declining SG&A from expense control• THB 169 million net realised FX gain

• NNP margin increased to 13.5% in Q2’2021

(Unit: THB mn)NORMALISED NET PROFIT (NNP)(Unit: THB mn)

1,011

73 5341,544

Net Profit

1,022

1,471

449

664

Q2’21 Unrealised FX Loss

NNP NNP to NCI

NNP to owner

Reconciliation Items:• Unrealised Fx loss of THB 73 million in Q2’2021 was a non-

cash item from USD debt translation and the THBdepreciation against USD during this period.

449

Strong normalised net profit

62

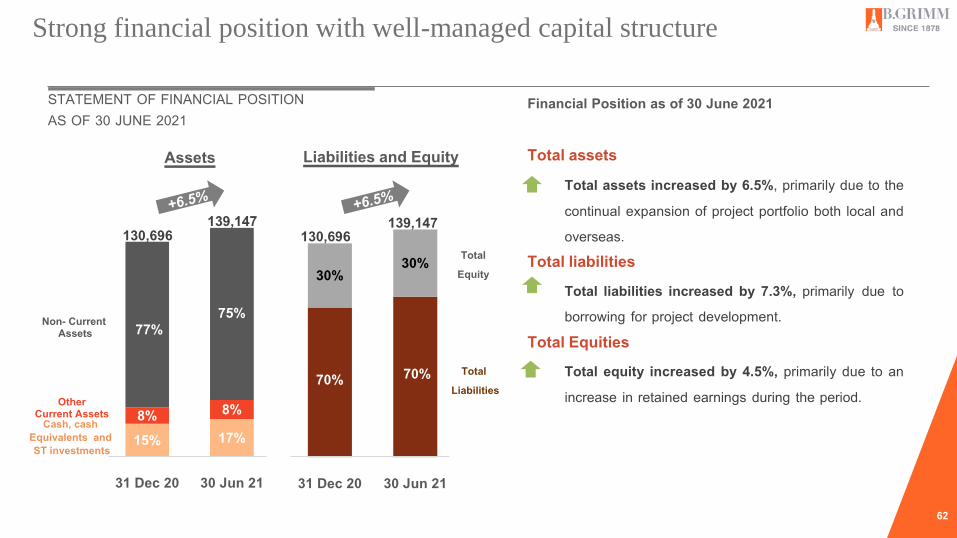

STATEMENT OF FINANCIAL POSITION AS OF 30 JUNE 2021

Assets Liabilities and Equity

Financial Position as of 30 June 2021

Total assets • Total assets increased by 6.5%, primarily due to the

continual expansion of project portfolio both local andoverseas.

Total liabilities• Total liabilities increased by 7.3%, primarily due to

borrowing for project development.Total Equities• Total equity increased by 4.5%, primarily due to an

increase in retained earnings during the period.70% 70%

30%30%

31 Dec 20 30 Jun 21

15% 17%8% 8%

77%75%

31 Dec 20 30 Jun 21

130,696139,147

Cash, cash Equivalents and ST investments

OtherCurrent Assets

Total Liabilities

TotalEquity

Non- Current Assets

130,696139,147

Strong financial position with well-managed capital structure

63

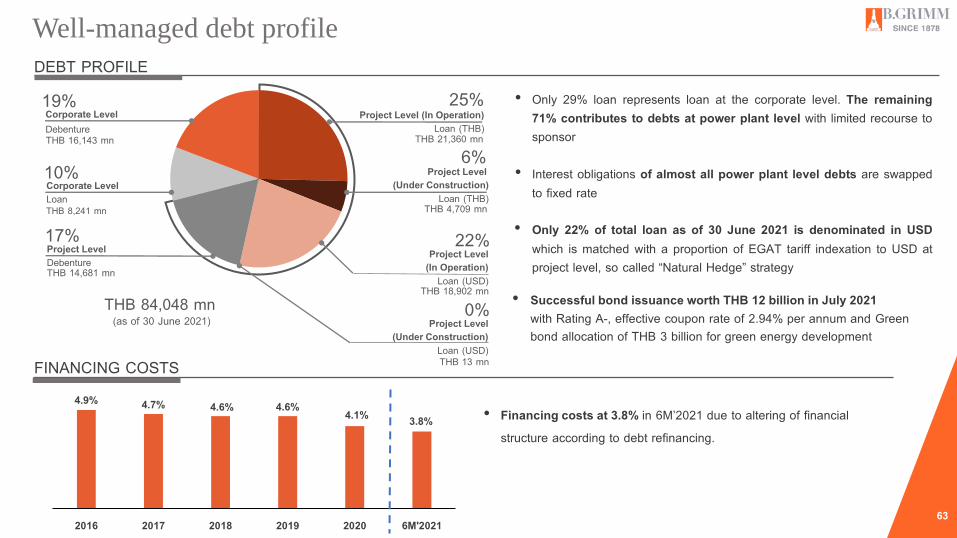

Well-managed debt profile

DEBT PROFILE

4.9% 4.7% 4.6% 4.6% 4.1% 3.8%

0.00

0.01

0.02

0.03

0.04

0.05

0.06

2016 2017 2018 2019 2020 6M'2021

• Financing costs at 3.8% in 6M’2021 due to altering of financial structure according to debt refinancing.

25%19%

Project Level (Under Construction)

Loan (THB)

0%Project Level

(Under Construction)Loan (USD)

THB 84,048 mn(as of 30 June 2021)

Project Level (In Operation)Loan (THB)

THB 21,360 mn

THB 18,902 mn

Project LevelDebenture

THB 8,241 mn

Corporate LevelLoan

THB 16,143 mn

Corporate LevelDebenture

THB 14,681 mnProject Level

(In Operation)Loan (USD)

22%THB 4,709 mn

6%

THB 13 mn

10%

17%

• Only 29% loan represents loan at the corporate level. The remaining71% contributes to debts at power plant level with limited recourse tosponsor

• Interest obligations of almost all power plant level debts are swappedto fixed rate

• Only 22% of total loan as of 30 June 2021 is denominated in USDwhich is matched with a proportion of EGAT tariff indexation to USD atproject level, so called “Natural Hedge” strategy

FINANCING COSTS

• Successful bond issuance worth THB 12 billion in July 2021 with Rating A-, effective coupon rate of 2.94% per annum and Green bond allocation of THB 3 billion for green energy development

64

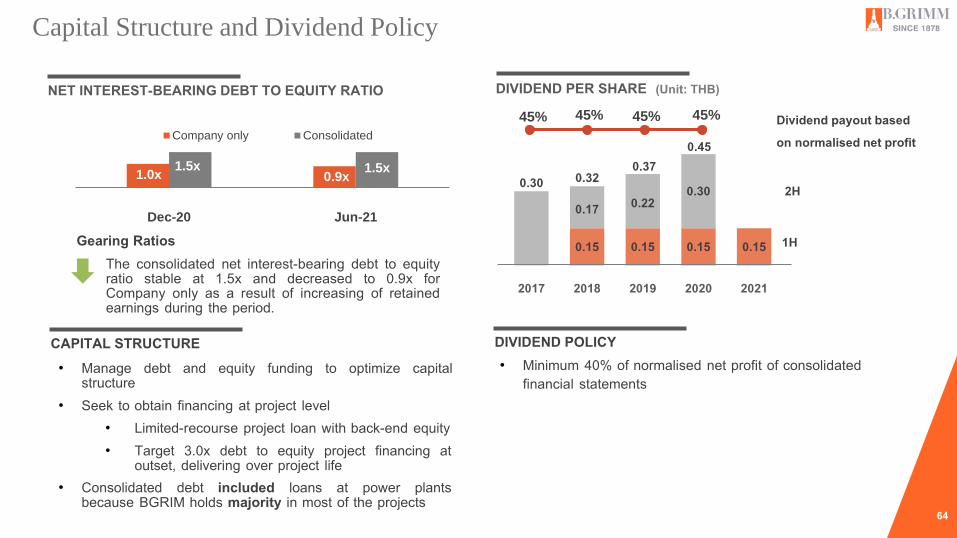

1.0x 0.9x1.5x 1.5x

(1.50) (1.40) (1.30) (1.20) (1.10) (1.00) (0.90) (0.80) (0.70) (0.60) (0.50) (0.40) (0.30) (0.20) (0.10)

- 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90 1.00 1.10 1.20 1.30 1.40 1.50 1.60 1.70 1.80 1.90 2.00 2.10 2.20 2.30 2.40 2.50

Dec-20 Jun-21

Company only Consolidated

Capital Structure and Dividend Policy

0.15 0.15 0.15 0.15

0.17 0.220.30

00.050.1

0.150.2

0.250.3

0.350.4

0.450.5

2017 2018 2019 2020 2021

45% 45% 45% 45%

• Manage debt and equity funding to optimize capital structure

• Seek to obtain financing at project level• Limited-recourse project loan with back-end equity• Target 3.0x debt to equity project financing at

outset, delivering over project life• Consolidated debt included loans at power plants

because BGRIM holds majority in most of the projects

NET INTEREST-BEARING DEBT TO EQUITY RATIO

• Minimum 40% of normalised net profit of consolidated financial statements

DIVIDEND POLICYCAPITAL STRUCTURE

(Unit: THB)DIVIDEND PER SHARE

2H

1H

Dividend payout based on normalised net profit

0.30 0.320.37

0.45

Gearing Ratios• The consolidated net interest-bearing debt to equity

ratio stable at 1.5x and decreased to 0.9x forCompany only as a result of increasing of retainedearnings during the period.

65

Appendix

66

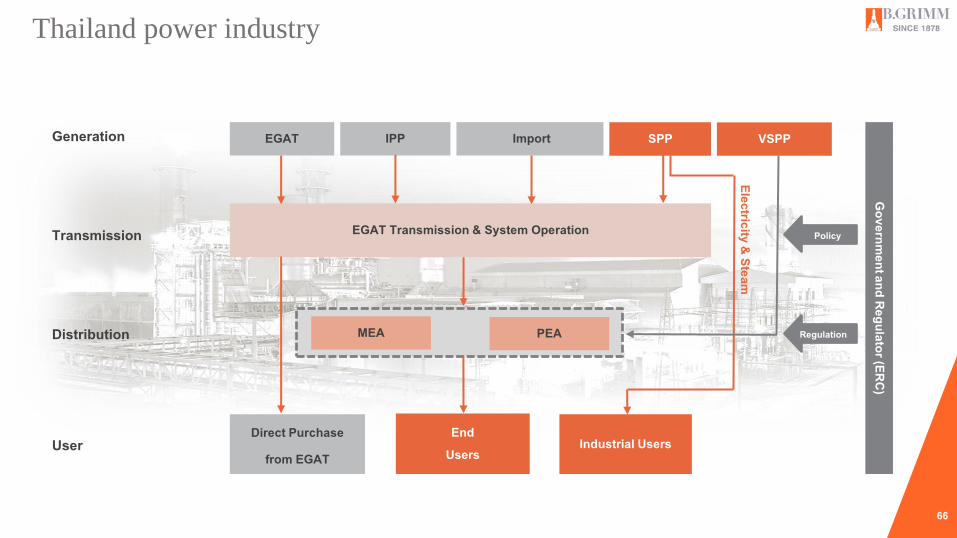

Governmentand Regulator (ERC)

Generation EGAT IPP Import SPP VSPP

Transmission EGAT Transmission & System Operation

Distribution

Direct Purchase

from EGAT

EndUsers

Industrial UsersUser

Electricity & Steam

MEA PEA

Policy

Regulation

Thailand power industry

67

1) Located in strategic industrial estates, near users2) IU tariff is linked to market price while EGAT tariff

is based on a cost-plus model3) Provide both electricity and stream to IUs

Contracted Capacity 30-90 MW The rest All (> 90 MW)

Off-taker EGAT Industrial Users EGAT

Tenors 20-25 10-15 20-25Product and Service Electricity Electricity, Stream,

Demin Water Electricity

Tariff Structure CP+EP+FS Base Tariff + Ft AP+EP

Minimum CP Base Tariff APFuel cost pass-through mechanism EP Ft EPIncentive from the government FS* - None

IPPSPP

*Fuel saving payment is made to cogeneration when the plant achieves a certain degree of cogeneration efficiency = 0.36 Baht /kWh

SPP

Round 1: 1992Round 2: 2007Round 3: 2010Replacement: 2018

CP = Capacity PaymentEP = Energy PaymentFS = Fuel SavingAP = Availability PaymentFS = Fuel Saving

Small Power Producer (SPP) scheme

68

Track Record of Extensions

23.1 Years 20.6

Years19.5

Years17.9

Years17.2

Years

8.4 Years

EDL PEA / MEA EDC EVN EGAT Industrial users -electricity (Thailand)

15.0Years

WEIGHTED AVERAGE REMAINING PPA LIFE

LONG-TERM PPA STRUCTURE• EGAT : 21 to 25 years tenor with take-or-pay structure• PEA / MEA : up to 25 years tenor (VSPP of solar, wind, waste to energy)• EDC : 20 years tenor (solar)• EDL : 25 years tenor (hydro)• EVN : 20 years tenor (solar)• Industrial Users : up to 15-year tenor with track record of extensionsSecured Gas Supply with PTT covering respective PPA tenorsGas price pass-through at contracted heat rate under EGAT PPANote: Weighted Average Remaining PPA life is calculated as the average remaining contractual term remaining from 31 June 2021 to expiry weighted by the aggregate contracted capacity under the relevant agreement

Longt-term PPA and well-established contracts

69BGRIM’s electricity tariff for IU is normally benchmarked with PEA (base tariff+Ft) which generally moves in the same direction with gas price.

Ft (Fuel Adjustment Charge) is a component of electricity market tariff, announced by Energy Regulatory Commission (ERC) every 4 months toreflect EGAT’s overall cost electricity which includes EGAT’s power generations, its purchase from private sector and the import from neighboringcountries

➢ In general, natural gas contributes approximately 70% of total fuel used to produce electricity in Thailand. Thus, change in gas price has highcorrelation with change in Ft.

➢ In addition, the gap between these two indexes is widen since 2011 – when renewable business started commencement in Thailand.

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Jan-

18

Jul-1

8

Jan-

19

Jul-1

9

Jan-

20

Jul-2

0

Jan-

21

Jul-2

1

Change in Ft vs Gas Price in 2005-2021Introduction of

renewable energy

Adjusted Ft Index

Gas Price Index

High correlation between gas price and Ft charge

70

Core subsidiaries and associates only

Corporate structure

71Note: As of August 2021

(a) Based on B.Grimm Power’s direct and/or indirect interest in the project company owning the power plant(b) Amata B.Grimm Power owned 30.0% of ABPIF’s units and consequently, our economic ownership of Amata B.Grimm Power 2 Limited was 15.3%(c) ABP1, ABP2, BPCL1 and BGPM got the approval to build new replacement projects under the 25-year PPA with the scheduled commercial operation in 2022(d) Acquired from Sime Darby Energy on 30 June 2014(e) We instead purchase power directly from a subsidiary of EVN which we then on-sell to industrial users in Amata City Bien Hoa Estate

Company Abbreviation Fuel Type COD EconomicOwnership %(a) Installed Equity Offtaker / PPA Expiry EGAT Contracted

Capacity (MW)IU Electricity Contracted

Capacity (MW)Steam Contracted

Capacity(MW) (MW) Program (t/h)

Amata Nakorn Industrial Estate, ThailandAmata B.Grimm Power 1 ABP1 Gas-Fired Cogen Sep-98 50.69% 166.4 84.3 EGAT (SPP) Sep-22(c) 60.0 104.3 6.0Amata B.Grimm Power 2 ABP2 Gas-Fired Cogen Sep-01 15.3%(b) 171.2 26.2 EGAT (SPP) Sep-22(c) 90.0 101.0 19.0Amata B.Grimm Power 3 ABP3 Gas-Fired Cogen Oct-12 60.70% 132.5 80.4 EGAT (SPP) Oct-37 90.0 43.1 13.0Amata B.Grimm Power 4 ABP4 Gas-Fired Cogen Nov-15 55.50% 131.1 72.8 EGAT (SPP) Nov-40 90.0 30.9 -Amata B.Grimm Power 5 ABP5 Gas-Fired Cogen Jun-16 55.50% 131.1 72.8 EGAT (SPP) Jun-41 90.0 32.7 13.0Subtotal 732.3 336.5 420.0 312.0 51.0Amata City Industrial Estate, ThailandAmata B.Grimm Power (Rayong) 1 ABPR1 Gas-Fired Cogen Nov-13 61.70% 123.3 76.1 EGAT (SPP) Nov-38 90.0 33.0 14.0Amata B.Grimm Power (Rayong) 2 ABPR2 Gas-Fired Cogen Jun-13 61.70% 124.4 76.8 EGAT (SPP) Jun-38 90.0 24.0 14.0Amata B.Grimm Power (Rayong) 3 ABPR3 Gas-Fired Cogen Feb-18 55.50% 133.0 73.8 EGAT (SPP) Feb-43 90.0 18.0 -Amata B.Grimm Power (Rayong) 4 ABPR4 Gas-Fired Cogen Jun-18 55.50% 133.0 73.8 EGAT (SPP) Jun-43 90.0 33.5 -Amata B.Grimm Power (Rayong) 5 ABPR5 Gas-Fired Cogen Oct-18 55.50% 133.0 73.8 EGAT (SPP) Oct-43 90.0 34.5 -Subtotal 646.7 374.3 450.0 143.0 28.0Laem Chabang Industrial Estate, ThailandB.Grimm Power (Laem Chabang) 1 BPLC1 Gas-Fired Cogen Jul-01(d) 100.00% 103.0 103.0 EGAT (SPP) Jul-22(c) 60.0 54.3 46.2B.Grimm Power (Laem Chabang) 2 BPLC2 Gas-Fired Cogen Feb-09(d) 100.00% 56.1 56.1 – – – 61.3 18.5Subtotal 159.1 159.1 60.0 115.6 64.7Bangkadi Industrial Park, ThailandB.Grimm BIP Power 1 BIP1 Gas-Fired Cogen Apr-15 74.00% 114.6 84.8 EGAT (SPP) Apr-40 90.0 14.0 –B.Grimm BIP Power 2 BIP2 Gas-Fired Cogen Jan-16 74.00% 114.6 84.8 EGAT (SPP) Jan-41 90.0 24.3 –Subtotal 229.2 169.6 180 38.3 –WHA Chonburi1 Industrial Estate, ThailandB.Grimm Power (WHA) 1 BPWHA1 Gas-Fired Cogen Nov-16 70.00% 130.2 97.7 EGAT (SPP) Nov-41 90.0 31.7 –WHA Eastern (Map Ta Phut) Industrial Estate, Thailand

B.Grimm Power (AIE-MTP) BGPM Gas-Fired CogenFeb &Dec-98

70.00% 124.0 86.8 EGAT (SPP) Feb & Dec-21(c) 110.0 4.6 48.0

B.Grimm Power (Angthong) 1 BGPAT1 Gas-Fired Cogen May -16 70.00% 123.0 86.1 EGAT (SPP) May-41 90.0 3.0 5.0Gas-Fired Cogen Total 2,144.5 1,310.1 1,400.0 648.2 196.7Amata City (Bien Hoa) Industrial Estate, VietnamAmata Power (Bien Hoa)(e) APB Diesel Generator Apr-99 30.70% 13.0 4.0 – – – 441.4 –Conventional Total 2,157.5 1,314.1 1,400.0 1,089.6 196.7

Operational power plants: conventional

72

Operational power plants: solarCompany / Project Abbreviation Location COD

EconomicOwnership %(a)

Capacity Main PPA(s)Installed

(MW)Equity (MW)

Offtaker /Program PPA Expiry

B.Grimm Yanhee Solar Power BGYSP 100.0% 59.7 59.7

Sai Luang 2

Pathumthani province, Thailand Dec-15

8.0 8.0

PEA (FiT) Dec-40

8.0 8.0Sai Luang 3

Sai Luang 9 7.2 7.2

Sai Luang 10 7.5 7.5

Sai Yai Nha 8.0 8.0

Sai Manow 8.0 8.0

Sai Putsa 8.0 8.0

Sai Sena 2 Ayutthaya province, Thailand 5.0 5.0Solarwa Solarwa 47.5% 38.5 18.3

Sai Lui Rim Num

Nakhon Pathom province, Thailand

Dec-15

8.0 3.8

PEA (FiT) Dec-40

Sai Chalouw 1 8.0 3.8

8.0 3.8Sai Sab

BGTTRE2

Saraburi province, ThailandBGTTRE3 8.0 3.8

6.5 3.1

TPS Commercial TPS Saraburi province, Thailand Dec-15 47.5% 8.0 3.8 PEA (FiT) Dec-40B.Grimm Solar Power (Sakaeo) 1 BGPSK Sakaeo province, Thailand Apr-16 100.0% 8.0 8.0 PEA (FiT) Apr-41Solar WVO-Cooperatives Solar WVO-Coop Dec-18 100.0% 30.8 30.8

BSPCD Sakaeo province, Thailand 2.3 2.3PEA (FiT)

Dec-43

BGPCCS Chachoengsao province, Thailand 3.6 3.6BSPCB Surat Thani province, Thailand 5.0 5.0

BGSP1WN Bangkok province, Thailand 5.0 5.0

MEA (FiT)BGPLKB Bangkok province, Thailand 5.0 5.0BGPBBO Samut Prakan province, Thailand 5.0 5.0BGPSAI Nonthaburi province, Thailand 5.0 5.0

Dau Tieng Tay Ninh Energy DT Tay Ninh province, Vietnam Jun-19 96.25% 240.0 231.0 EVN (FiT) Jun-39Phu Yen TTP (Phu Yen) Phu Yen TTP Phu Yen province, Vietnam Jun-19 80.0% 257.0 205.6 EVN (FiT) Jun-39Ray Power Ray Power Banteay Meanchey Province, Cambodia Dec-20 100.0% 39.0 39.0 EDC (FiT) Dec-40Total 681.0 596.2

Note: As of August 2021(a) Based on B.Grimm Power’s direct and/or indirect interest in the project company owning the power plant.

73

SPP Gas-fired Cogeneration Solar PV Solar (Vietnam) Wind Hydro iWTE Solar

(Cambodia)

EGATIndustrial Users PEA/MEA

(FiT) EVN PEA (Adder) EDL PEA EDCElectricity Steam

Term (years) 21 – 25 years 5 – 15 years(a) 5 – 15 years(a) 25 years 20 years 5 years 25 years 20 years 20 years

Extension option ✓ ✓ ✓ – – 5 years auto extension Up to 10 years – –

Contracted capacity

90 MW (except for

BPLC1 which is 60MW)

Depends on each contract 2.25-8 MW 677 MW dc564 MW ac

8 MW (each) 6.7 – 15 MW(b) 4 MW 30 MW

Secured fuel supply ✓ ✓ ✓ N/A N/A N/A N/A N/A N/A

Natural gas cost pass-through✓

(at contracted heat rate)

Partially through Ft

Depends on contract N/A N/A N/A N/A N/A N/A

FX pass-through ✓Partially through

Ft – – – – – – –

Inflation indexation – – ✓ – – – – – –

Tariff See next page 5.66 THB/kWh4.12 THB/kWh

9.35 Cents/kWh

PEA wholesale + 10-year adder at 3.50 THB/kWh

6.50 Cents/kWhFiTF + FiTV + 8-year adder

at 0.7 THB/kWh7.60 Cents/kWh

Applicable power plants ABP1-5, ABPR1-5, BPLC1, BIP1-2, BPWHA1, BGPAT1-3, BGPM

BGYSP (8 projects),Solarwa (5

projects), TPS, BGPSK,

Solar WVO-Coop

DT1&2, Phu Yen TTP

Bo Thong(2 projects)

XXHP(2 projects),

Nam Che, Nam Khao 1-5(5 projects)

PIC Ray Power

Source: 56-1, EGAT, PEASome contract terms are year-on-year basisAccording to concession agreements

Contractual overview: commercial features

74

Electricity Tariff = Capacity Payment + Energy Payment + Fuel Saving Payment + VAT

Capacity Payment Rate (THB/kW/month) = 𝐶𝑃0 × (𝑥 ×𝐹𝑋𝑡

𝐹𝑋0)+(1− 𝑥)

Energy Payment Rate (THB/kWh) = 𝐸𝑃0 +𝑃𝑡−𝑃0

106× contracted Heat Rate

Fuel Saving Payment Rate (THB/kWh) = 𝐹𝑆0 ×𝑃𝐸𝑆𝑡

10%

𝐹𝑋𝑡 = THB/ US$ Exchange Rate

𝑃𝑡 = Price for natural gas PTT sells to SPPs in a month (THB/MMBTU)

𝑃𝐸𝑆𝑡 = primary energy saving (“PES”) statistic measuring the efficiency rate of our gas-fired cogeneration power plant in consuming natural gas in the generation of electricity and thermal energy

SPP Regulation 1992, 2005 2007 2010

Applicable power plantsABP1-2, BPLC1,BGPM

ABP3, ABPR1-2,

BIP1

ABP4-5,ABPR3-5,

BIP2, BPWHA, BGPAT1

Base Capacity Payment Rate (𝐶𝑃0) (THB/kW)

302.00 383.66 420.00

Base Exchange Rate (𝐹𝑋0) (THB/US$)

27 37 34

US$THB FX indexation (𝑥) 0.8 0.5 0.5

Base Energy Payment Rate (𝐸𝑃0) (THB/kWh)

0.85 1.70 1.85

Base Price for Natural Gas PTT sells to SPPs (𝑃0) (THB/MMBTU)

77.0812 209.4531 232.6116

Contracted Heat Rate (BTU/kWh)

8,600 8,000 7,950

Fuel Saving Payment - ✓ ✓

Base Fuel Saving Payment (𝐹𝑆0) (THB/kWh)

- 0.36 0.36

TARIFF STRUCTURE

Contractual overview: EGAT PPA under SPP program

75

ProjectsInstalled Capacity

(MW)Steam Capacity

(ton/hr)Type of maintenance

Duration(days)

2021Q1 Q2 Q3 Q4

Amata City (Chonburi)

ABP4 131.1 30.0 Major Overhaul 27

ABP5 131.1 30.0 Major Overhaul 15

Amata City (Rayong)

ABPR3 133.0 30.0 Major Inspection 24

ABPR4 133.0 30.0 Major Inspection 24

ABPR5 133.0 30.0 Major Inspection 24

Bangkadi

BIP1 114.6 20.0 Major Inspection 10

Laem Chabang

BPLC2 56.1 20.0 Major Inspection 11

WHA Eastern (Map Ta Phut)

BGPM 124.0 90.0 Major Overhaul 22

ProjectsInstalled Capacity

(MW)Steam Capacity

(ton/hr)Type of maintenance

Duration(days)

2020

Q1 Q2 Q3 Q4Amata City (Rayong)

ABPR1 123.3 30.0 Major Overhaul 40

ABPR2 124.4 30.0 Major Overhaul 40

WHA Chonburi 1

BPWHA 130.0 30.0 Major Inspection 15

Major maintenance schedule in 2020 to 2021

76

ABBREVIATIONADB Asian Development Bank

COD Commercial Operation Date

EBITDA Earnings before Interest, Taxes, Depreciation and Amortization

EDC Electricite Du Cambodge

EDL Electricite Du Laos

EGAT Electricity Generating Authority of Thailand

ERC Energy Regulatory Commission

EPC Engineering, Procurement and Construction

EVN Electricity of Vietnam

FiT Feed-in Tariff

kWh / GWh Kilowatt / Gigawatt-hour

MEA Metropolitan Electricity Authority

MMBTU Million Btu (unit of gas consumption)

NNP Normalised net profit

OUR PROJECTSABPIF Amata B.Grimm Power Plant Infrastructure Fund

ABP1 Amata B.Grimm Power 1

ABP2 Amata B.Grimm Power 2

ABP3 Amata B.Grimm Power 3

ABP4 Amata B.Grimm Power 4

ABP5 Amata B.Grimm Power 5

ABPR1 Amata B.Grimm Power (Rayong) 1

ABPR2 Amata B.Grimm Power (Rayong) 2

ABPR3 Amata B.Grimm Power (Rayong) 3

ABPR4 Amata B.Grimm Power (Rayong) 4

ABPR5 Amata B.Grimm Power (Rayong) 5

BGPAT1 B.Grimm Power (Angthong) 1

BIP1 B.Grimm BIP Power 1

BIP2 B.Grimm BIP Power 2

BGPM B.Grimm Power (AIE-MTP) (SPP1)

BPLC1 B.Grimm Power (Laem Chabang) 1

BPLC2 B.Grimm Power (Laem Chabang) 2

BPWHA1 B.Grimm Power (WHA) 1

DT Dau Tieng Tay Ninh Energy Solar Project

Nam Che 1 Nam Che 1 Hydro Power Project

PIC Progress Interchem

FX Foreign exchange

IPO Initial public offering

IU Industrial user

IWTE Industrial Waste to Energy

JV Joint venture

P.A. Per annum

PEA Provincial Electricity Authority (Thailand)

PPA Power purchase agreement

PTT PTT public Company Limited

ROA Return on assets

ROE Return on equity

SG&A Selling, general & administrative expense

YE Year End

YoY Year-on-Year

O&M Operations and maintenance

BGPSK B.Grimm Solar Power (Sakaeo) 1

BGSENA B.Grimm Sena Solar Power Limited

BGYSP B.Grimm Yanhee Solar Power

Phu Yen TTP Phu Yen TTP Solar Project (Phu Yen)

Solar WVO Solar WVO-Cooperatives Projects

Ray Power Ray Power Supply Company Limited

XXHP Xenamnoy 2 and Xekatam 1 Hydro Power Project

BSPCD The Chon Daen agricultural cooperatives project

BGPCCS The WVO project, namely the Veteran Support Office of Chonburi

BSPCB The Ban Na Doem agricultural cooperatives project

BGSP1WNThe WVO project, namely Office of Agriculture, Industry and Services Affairs

BGPLKB The WVO project, namely the Veterans General Hospital

BGPBBOThe WVO project, namely the WVO Office of Terminal Production Workshop

BGPSAI The WVO project, namely the WVO Office of Security Services

Abbreviation & our projects

77

DisclaimerNone of the Company makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained in thisdocument or otherwise made available nor as to the reasonableness of any assumption contained herein or therein, and any liability therein (including in respectof any direct, indirect or consequential loss or damage) is expressly disclaimed. Nothing contained herein or therein is, or shall be relied upon as, a promise orrepresentation, whether as to the past or the future and no reliance, in whole or in part, should be placed on the fairness, accuracy, completeness or correctnessof the information contained herein. Further, nothing in this document should be construed as constituting legal, business, tax or financial advice.This document is a summary only and does not purport to contain all of the information that may be required to evaluate any potential transaction and anyrecipient hereof should conduct its own independent analysis of the Company, including the consulting of independent legal, business, tax and financial advisers.The information in these materials is provided as at the date of this document and is subject to change without notice..

INVESTOR RELATIONSEmail: [email protected]

Tel: +66 (0) 2710 3528

Solaya Na Songkhla

Email: [email protected]

Pornratchanee Sethakaset

Email: [email protected]

Gunnlapat Wichutarat

Email: [email protected]

Thunruethai Makaraphan

Email: [email protected]

Contact Us:Dr. Gerhard Link Building,

5 Krungthepkreetha Road, Huamark, Bangkapi, Bangkok 10240, Thailand

Tel: +66 (0) 2710 3400Fax: +66 (0) 2379 4245