Best Practices & Considerations for Accelerated Underwriting · Best Practices & Considerations for...

25

Session 161 PD - Best Practices & Considerations for Accelerated Underwriting Moderator: Donna Christine Megregian, FSA, MAAA Presenters: Gregory A. Brandner, FSA, MAAA Lisa Hollenbeck Renetzky, FSA, MAAA SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer

Transcript of Best Practices & Considerations for Accelerated Underwriting · Best Practices & Considerations for...

Session 161 PD - Best Practices & Considerations for Accelerated Underwriting

Moderator:

Donna Christine Megregian, FSA, MAAA

Presenters: Gregory A. Brandner, FSA, MAAA

Lisa Hollenbeck Renetzky, FSA, MAAA

SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer

2017 SOA Annual Meeting & ExhibitMODERATOR: DONNA MEGREGIAN, FSA, MAAA

PRESENTERS:

GREGORY BRANDNER, FSA, MAAA

LISA RENETZKY, FSA, MAAASession 161 , Best Practices & Considerations for Accelerated UnderwritingDate

SOCIETY OF ACTUARIESAntitrust Compliance Guidelines

Active participation in the Society of Actuaries is an important aspect of membership. While the positive contributions of professional societies and associations are well-recognized and encouraged, association activities are vulnerable to close antitrust scrutiny. By their very nature, associations bring together industry competitors and other market participants.

The United States antitrust laws aim to protect consumers by preserving the free economy and prohibiting anti-competitive business practices; they promote competition. There are both state and federal antitrust laws, although state antitrust laws closely follow federal law. The Sherman Act, is the primary U.S. antitrust law pertaining to association activities. The Sherman Act prohibits every contract, combination or conspiracy that places an unreasonable restraint on trade. There are, however, some activities that are illegal under all circumstances, such as price fixing, market allocation and collusive bidding.

There is no safe harbor under the antitrust law for professional association activities. Therefore, association meeting participants should refrain from discussing any activity that could potentially be construed as having an anti-competitive effect. Discussions relating to product or service pricing, market allocations, membership restrictions, product standardization or other conditions on trade could arguably be perceived as a restraint on trade and may expose the SOA and its members to antitrust enforcement procedures.

While participating in all SOA in person meetings, webinars, teleconferences or side discussions, you should avoid discussing competitively sensitive information with competitors and follow these guidelines:

• Do not discuss prices for services or products or anything else that might affect prices• Do not discuss what you or other entities plan to do in a particular geographic or product markets or with particular customers.• Do not speak on behalf of the SOA or any of its committees unless specifically authorized to do so.

• Do leave a meeting where any anticompetitive pricing or market allocation discussion occurs.• Do alert SOA staff and/or legal counsel to any concerning discussions• Do consult with legal counsel before raising any matter or making a statement that may involve competitively sensitive information.

Adherence to these guidelines involves not only avoidance of antitrust violations, but avoidance of behavior which might be so construed. These guidelines only provide an overview of prohibited activities. SOA legal counsel reviews meeting agenda and materials as deemed appropriate and any discussion that departs from the formal agenda should be scrutinized carefully. Antitrust compliance is everyone’s responsibility; however, please seek legal counsel if you have any questions or concerns.

2

Presentation Disclaimer

Presentations are intended for educational purposes only and do not replace independent professional judgment. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of the Society of Actuaries, its cosponsors or its committees. The Society of Actuaries does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented. Attendees should note that the sessions are audio-recorded and may be published in various media, including print, audio and video formats without further notice.

3

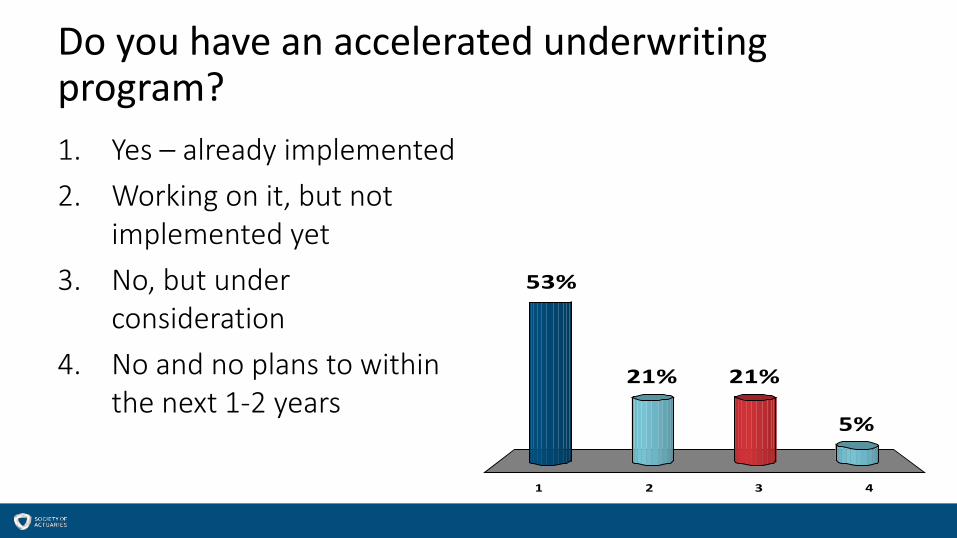

Do you have an accelerated underwriting program?

1 2 3 4

53%

5%

21%21%

1. Yes – already implemented2. Working on it, but not

implemented yet3. No, but under

consideration4. No and no plans to within

the next 1-2 years

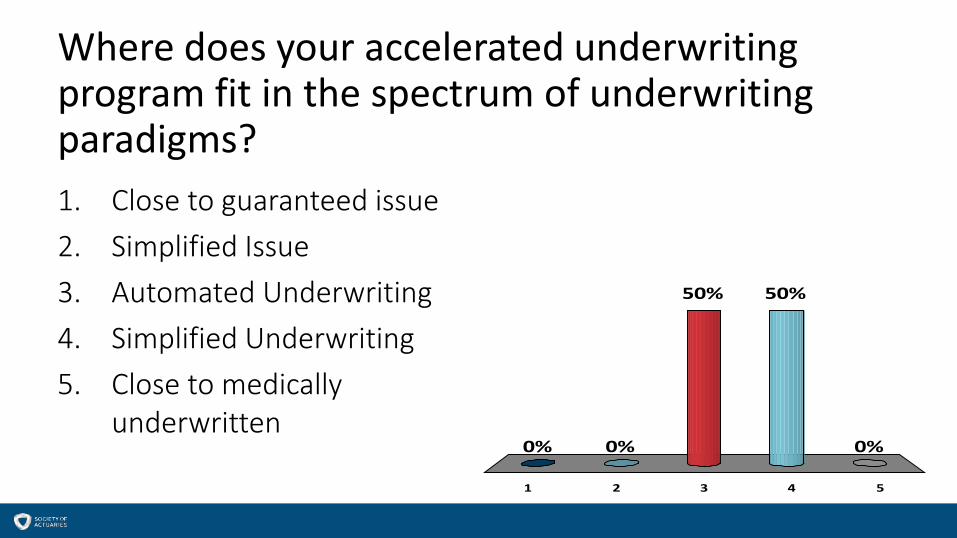

Where does your accelerated underwriting program fit in the spectrum of underwriting paradigms?

1 2 3 4 5

0% 0% 0%

50%50%

1. Close to guaranteed issue2. Simplified Issue3. Automated Underwriting4. Simplified Underwriting5. Close to medically

underwritten

6

Q/A• How do you define accelerated underwriting?

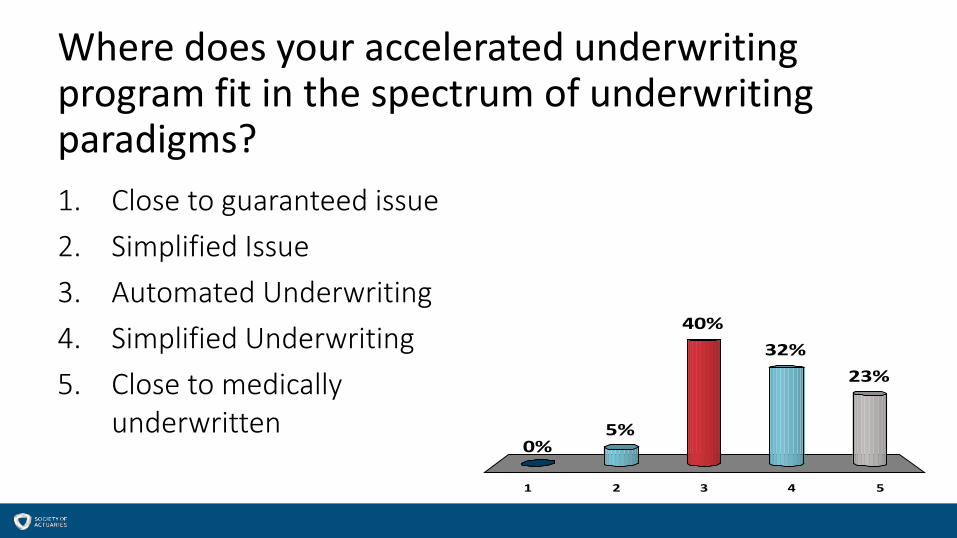

Where does your accelerated underwriting program fit in the spectrum of underwriting paradigms?

1 2 3 4 5

0%5%

23%32%

40%

1. Close to guaranteed issue2. Simplified Issue3. Automated Underwriting4. Simplified Underwriting5. Close to medically

underwritten

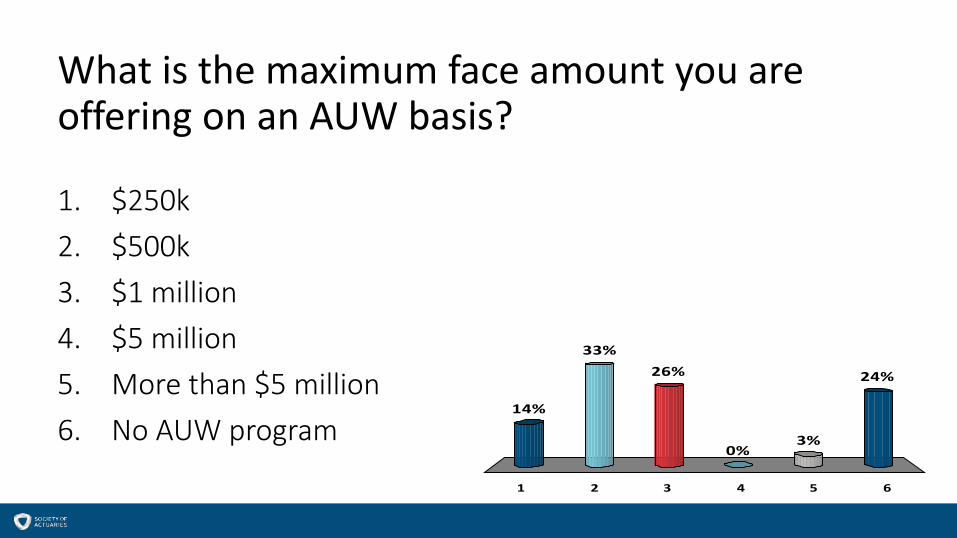

What is the maximum face amount you are offering on an AUW basis?

1 2 3 4 5 6

14%

33%

24%

3%0%

26%

1. $250k2. $500k3. $1 million4. $5 million5. More than $5 million6. No AUW program

9

Q/A• What is/are the reason(s) to move to develop an

accelerated underwriting program?

10

Q/A• How does accelerated underwriting interact with

other underwriting paradigms? Why is it important?

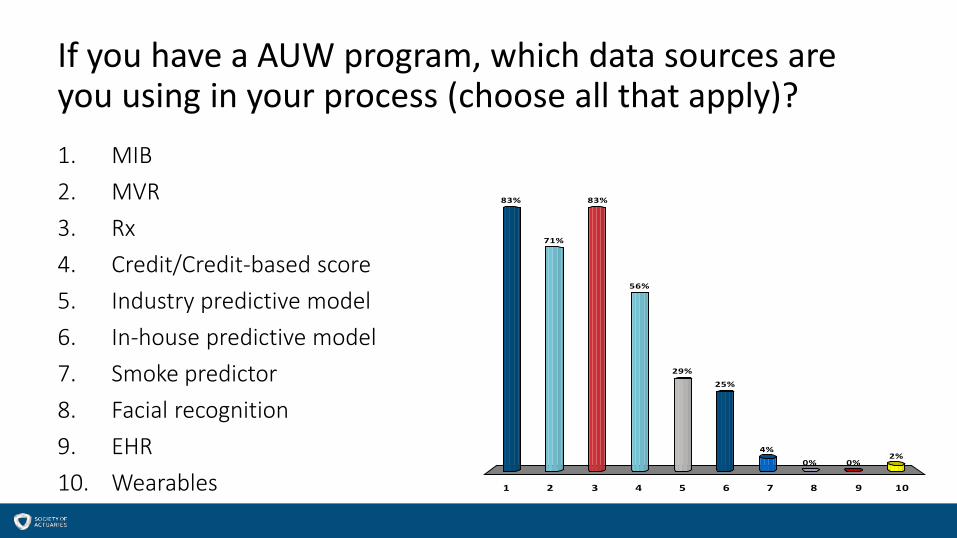

If you have a AUW program, which data sources are you using in your process (choose all that apply)?

1 2 3 4 5 6 7 8 9 10

83%

71%

83%

56%

2%0%0%

4%

25%

29%

1. MIB2. MVR3. Rx4. Credit/Credit-based score5. Industry predictive model6. In-house predictive model7. Smoke predictor8. Facial recognition9. EHR10. Wearables

12

Q/A• What tools are useful and/or necessary in your

opinion to develop a program and why? • What roles do the new tools play in changing the

underwriting process?

13

Q/A• Where would you suggest a company start when

looking at AUW?

What area of your company is leading the AUW movement/exploration?

1. Marketing2. Pricing3. Underwriting4. Distribution5. Senior Management6. IT7. Legal8. Other

15

Q/A• Who needs to be involved in the conversation as it

pertains to AUW program development?

16

Q/A• What area(s) of the company are leading the

implementation effort?• Is this useful and how would you suggest improving

that implementation effort?

17

Q/A• Your marketing area wants a new AUW program. They

say that other companies are getting 80%-90% of people through their programs and want that as well. How do you respond to this…politely.”

• What are the balancing factors when developing an AUW program?

• Where do you begin when developing assumptions for AUW?• What data is available or how do you make it available?

18

Q/A• Many carriers are introducing AUW programs at the

same retail premium rates and same risk classes as their current medically underwritten products. Does this mean those carriers are expecting the same mortality results as for their fully underwritten business?

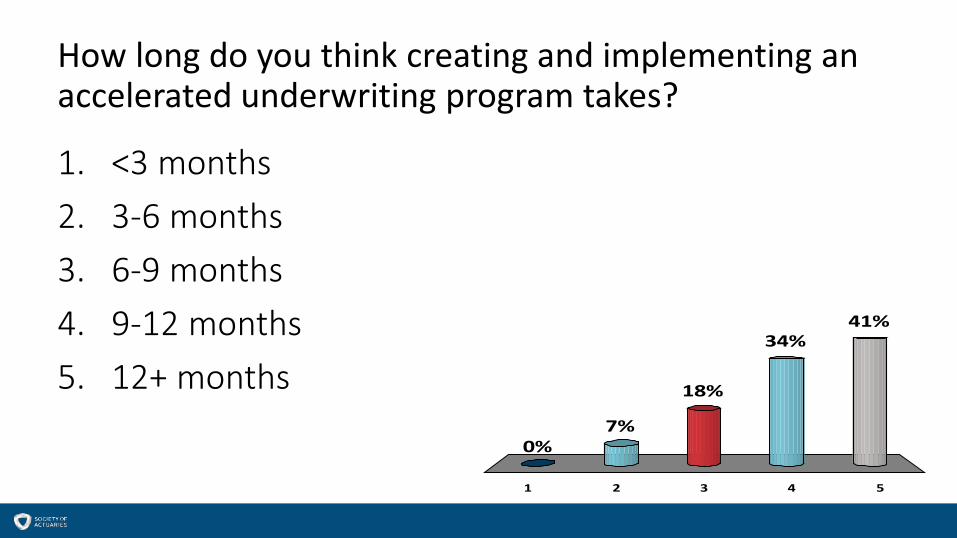

How long do you think creating and implementing an accelerated underwriting program takes?

1 2 3 4 5

0%7%

41%34%

18%

1. <3 months2. 3-6 months3. 6-9 months4. 9-12 months5. 12+ months

20

Q/A• What are some difficult issues during development,

then during implementation of an AUW program?• Development being the idea/concept of the program,

implementation meaning execution of the program.

21

Q/A• Pros and cons of hold outs?

• What have you heard about how hold out programs are working?

• What other kind of monitoring should be done?

22

Q/A• Do you have any suggestions on how to help train

underwriters when AUW may be allowing basic training cases to be sent through without an underwriter looking at the case?

23

Q/A• How does AUW fit in the changing PBR world?• What do companies need to consider and work

through?