A Study of the Challenges Facing the Devolved Governments ...

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor. | ©2016 CliftonLarsonAllen LLP

Best of Accounting Complexities Facing Local Governments –Capital Assets Focus2017 FGFOA Gulf Coast Chapter Fall ConferenceBy Andrew Laflin, CPAPrincipal, CliftonLarsonAllen LLP

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Learning Objectives

• This session will provide answers to a series of questions that present complex and often overlooked accounting and financial reporting issues. Examples include the following:– Net Position Classification – Net Investment In Capital

Assets– Capital Asset Transfer Between Funds– Restricted Net Position & Fund Balance– Capital Outlay & Capital Asset Additions– Revenue Recognition for Property Taxes

2

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #1

• The following information pertains to Pinellas County’s assets and liabilities in order to determine its classification of net position, specifically Net Investment in Capital Assets:– ASSETS:

◊ Investments = $189,133,213, which includes an investment account containing unspent bond proceeds totaling $80,572,327

◊ Prepaid Expenses = $2,214,698, which includes $1,533,228 of prepaid debt insurance costs (County determined that 0.8% of outstanding debt related to payment of issuance costs)

◊ Inventories = $4,344,525◊ Deferred Outflow of Resources (Deferred Amount on Refunding) =

$2,826,721◊ Total Capital Assets, Net of Depreciation = $1,149,445,769

3

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #1

– LIABILITIES:◊ Accounts Payable = $15,177,666, which includes $7,345,266 of

construction related A/P◊ Accrued Liabilities = $12,863,145, which includes $3,311,120 of

retainage payable◊ Bonds and Notes Payable, Current Portion = $75,449,400◊ Bonds and Notes Payable, Noncurrent Portion = $527,213,853◊ Interfund Advance = $2,227,983◊ Deferred Inflow of Resources (Deferred Amount on Refunding) =

$2,449,240

• What should the County report as Net Investment in Capital Assets?

4

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• What about cash and investments?• 7.23.2. Q—A government issues bonds late in the year to

purchase capital assets. The proceeds are received, but no capital assets have been purchased as of the balance sheet date. Which component of net position should include the debt?

• A—If there are significant unspent related debt proceeds at year-end, the portion of the debt attributable to the unspent proceeds should not be included in the calculation of the net investment in capital assets component of net position. Rather, that portion of the debt should be included in the same net position component as the unspent proceeds—for example, restricted for capital projects.

5

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• What about prepaids and inventories?• 7.23.3. Q—Which component(s) of net position do prepaid

bond insurance costs, premiums and discounts, and deferred outflows of resources or deferred inflows of resources from refundings affect—net investment in capital assets, restricted, or unrestricted?

• A—Prepaid bond insurance costs should be included in the unrestricted component of net position because those outlays do not acquire, construct, or improve capital assets. If the prepaid bond insurance costs were paid from bond proceeds, the portion of outstanding debt attributable to those insurance costs also should be included in the unrestricted component of net position.

6

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• One more thought on debt issuance costs:• 7.23.5. Q—Often, debt is issued for capital purposes, but

some of the proceeds are spent for assets that are not capitalized. Should some of the debt be removed from the net investment in capital assets component of net position?

• A—Governments are not expected to categorize all uses of bond proceeds to determine how much of the debt actually relates to assets that have been capitalized. Unless a significant portion of the debt proceeds is spent for non-capitalizable purposes, the entire amount could be considered "capital-related."

7

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• What about deferred inflows and outflows of resources?• 7.23.3. Q—Which component(s) of net position do prepaid

bond insurance costs, premiums and discounts, and deferred outflows of resources or deferred inflows of resources from refundings affect—net investment in capital assets, restricted, or unrestricted?

• A—Premiums, discounts, and deferred outflows of resources or deferred inflows of resources from refundings “follow the debt” in calculating the components of net position. That is, if debt is capital related, those amounts would be included in the calculation of the net investment in capital assetscomponent of net position.

8

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

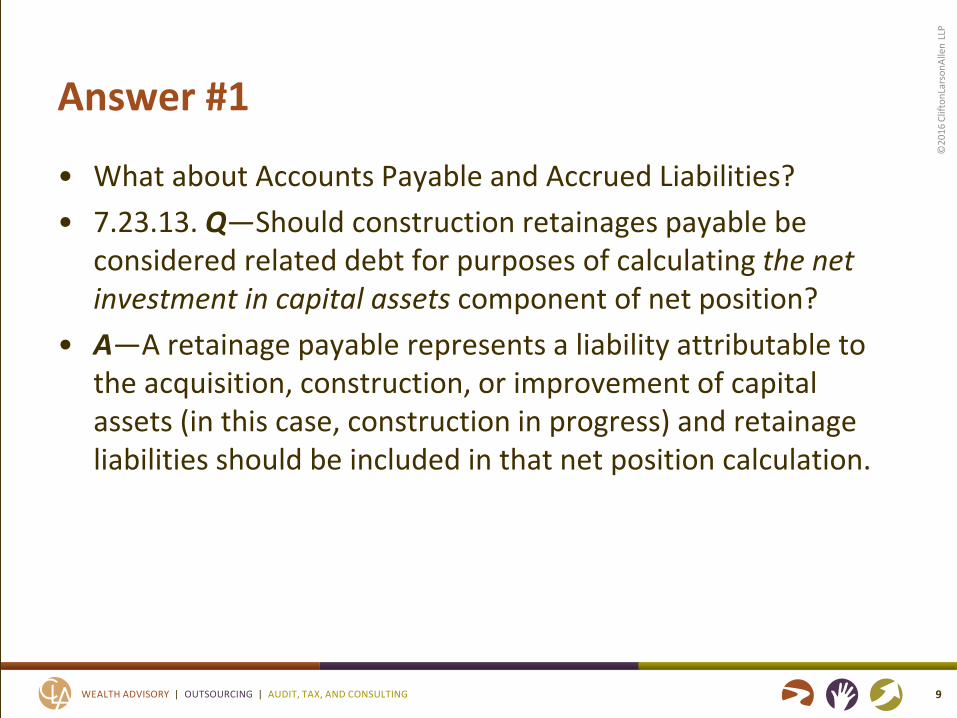

Answer #1

• What about Accounts Payable and Accrued Liabilities?• 7.23.13. Q—Should construction retainages payable be

considered related debt for purposes of calculating the net investment in capital assets component of net position?

• A—A retainage payable represents a liability attributable to the acquisition, construction, or improvement of capital assets (in this case, construction in progress) and retainage liabilities should be included in that net position calculation.

9

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• So that’s a yes on Retainage Payable, but what about Accounts Payable?

• 7.23.14. Q—Is the answer to Question 7.23.13 the same if the construction project is financed with bond proceeds?

• A—Yes. If the project is financed with bond proceeds, the amount of the retainage is attributed to the construction in progress, and would be included in the net investment in capital assets component of net position. Thus, “capital-related debt” in this situation includes the portion of the bonds payable that has been spent on the capital construction, plus retainages and accounts payable attributable to that construction.

10

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• What about interfund debt?• 7.23.11. Q—A government made an interfund loan from its

general fund to an enterprise fund for the purpose of purchasing capital assets. Does the advance due to the general fund constitute capital-related debt in the enterprise fund?

• A—No. Interfund advances are not considered debt or other borrowing for purposes of calculating the net position components. Interfund balances are included in the computation of unrestricted net position.

11

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #1

• Total Capital Assets, net of Depreciation: $1,149,445,769• Plus Outstanding Debt - Issuance Costs (if material): 4,821,306• Plus Deferred Outflow: 2,826,721• Less Deferred Inflow: (2,449,240)• Less Retainage & Construction A/P: (10,656,386)• Less Bonds and Notes Payable: (602,663,253)• Plus Unspent Bond Proceeds: 80,572,327

• Net Investment In Capital Assets = $621,897,244

12

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Additional Question & Answer #1

• Question: For smaller cities, towns, and other special districts that have capital assets but no related debt, should the caption still be “Net Investment in Capital Assets”?

• Answer: Should be titled “Investment in Capital Assets” (7.23.7)

• Question: If debt was issued simply to refund existing capital-related debt, should this also be considered capital-related?

• Answer: Yes (7.23.6)

13

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #2 – Capital Asset Transfer

• Pasco County is transferring vehicles and equipment out of one fund and into another. The assets have an original cost of $340,265 and accumulated depreciation of $166,244.

• What would be the entries to record this transfer from…– One enterprise fund to another enterprise fund?– An internal service fund to an enterprise fund?– A governmental fund to an enterprise fund?

14

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #2 – Capital Asset Transfer

• 7.74.4. Q—How should the reassignment of a capital asset between an enterprise fund and governmental activities be reported?

• A—If the assets reassigned from governmental activities to an enterprise fund are capital assets, the transaction is not “interfund” because it involves only one fund; consequently, the enterprise fund would report the receipt of the capital assets as a capital contribution from governmental activities (in the last section of the statement of revenues, expenses, and changes in net position). In the reverse situation, in which a capital asset is reassigned from an enterprise fund to governmental activities, the disposal of the capital asset would be reported by the enterprise fund as a nonoperating expense. In either case, governmental funds would not report the event because there has been no flow of current financial resources. In the statement of activities, the reassignment of the capital asset between governmental and business-type activities would be reported as a transfer, requiring a reconciling item in the governmental funds' reconciliation because a difference is created between the change in fund balances and the change in total net position.

15

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #2 – Capital Asset Transfer• Water & Sewer Fund to Solid Waste Fund:

– Transfer In (Solid Waste Fund) and Transfer Out (Water & Sewer Fund) for $174,021, offset by capital assets ($340,265) and A/D ($166,244)

• Water & Sewer Fund to General Fund:– Debit non-operating expense in Water & Sewer Fund for

$174,021, offset by credit to capital assets ($340,265) and debit to A/D ($166,244); no entry in General Fund

• General Fund to Water & Sewer Fund:– Credit non-operating revenue (capital contribution) in Water &

Sewer Fund for $174,021, offset by debit to capital assets ($340,265) and credit to A/D ($166,244); no entry in General Fund

16

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #2 – Capital Asset Transfer• Water & Sewer Fund to Governmental Activities:

– Transfer In (Governmental Activities) and Transfer Out (Water & Sewer Fund) for $174,021, offset by capital assets ($340,265) and A/D ($166,244)

17

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #3

• The City of Clearwater recently installed a new HR module within its enterprise resource planning (ERP) system. Which of the following costs would be capitalized versus expensed associated with this installation?– Staff time putting out an RFP and evaluating proposals to

select the most qualified consultant to assist with the implementation

– Staff time associated with determining the systems requirements for the module and whether the technology needed to achieve those requirements exists

18

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #3 - Continued

• Capitalized versus expensed, continued:– No expenses capitalized since the ERP system as a whole

has been largely developed at the City(all other modules completed and operational)

– Staff and consultant time relating to HR data conversion activities (processing of payroll transactions is dependent on the transfer of this information)

– Staff and consultant time relating to HR data conversion activities (processing of payroll transactions is not dependent on the transfer of this information)

– Employee training costs associated with developing & implementing the HR module

19

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #3 - Continued

• Capitalized versus expensed, continued:– Maintenance contract with its software vendor under

which the County pays an annual fixed fee that covers all required maintenance and any minor unspecified upgrades issued during the year by the vendor (more significant upgrades to the software, such as an upgrade to a new version of the software, are not covered under the contract)

– Should the utility billing module within this ERP system be subject to interest cost capitalization in accordance with GASBS 62, assuming the City has debt outstanding in its water & sewer fund?

20

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3

• Costs associated with modifying computer software already in use should be capitalized if the modification results in one or more of the following:– An increase in functionality of the software– An increase in efficiency of the software– An extension of the estimated useful life of the software

• Any modifications outside of these three situations are considered maintenance, and the related costs should be expensed as incurred

21

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• Developing and installing internally generated computer software consists of three stages:– Preliminary Project Stage– Application Development Stage– Post-implementation/Operation Stage

• Costs related to activities in the application development stage should be capitalized; costs in preliminary project and post-implementation/operation stage should be expensed as incurred

22

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• Specific tasks within preliminary project stage:– Making strategic decisions to allocate resources between alternative

projects at a given point in time– Determining the performance requirements for the computer software

project—for example, through a user needs analysis– Determining the systems requirements for the computer software project

and that the technology needed to achieve performance requirements exists

– Exploring alternative means of achieving the specified performance requirements—for example, evaluating internal development of the computer software against procurement and modification of commercially available software

– Selecting a vendor if commercially available software is to be acquired– Selecting a consultant to assist in the development or installation of the

computer software.

23

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• GASB Comprehensive Implementation Guide Question Z.51.12 asks if a government developing an ERP system with multiple modules should apply the guidance of GASBS 51 to each individual module within the system or to the ERP system as a whole.

• Answer: Since each module will have its own development cycle, particularly as it relates to application development-stage and post-implementation/operation-stage activities, guidance should be applied for each individual module.

24

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• GASB Comprehensive Implementation Guide Question Z.51.14 states data conversion activities should be considered activities of the application development stage of developing internally generated computer software only to the extent they are determined to be necessary to make the computer software operational

• Example of not necessary: “a database system containing vendor information and performance feedback may be less reliant on converted legacy data to be considered operational because the data provided by such a system may be more informational in nature and not essential to undertaking current procurement transactions”

25

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• Question Z.51.23 states that the outlays of the maintenance contract should be allocated between upgrades that result in an increase in functionality or efficiency of the computer software or an extension of the estimated useful life of the software (capitalizable) and all other upgrades and maintenance provided by the vendor (expensed as incurred). However, depending on the materiality of the outlays related to the unspecified upgrades, as a practical matter, a government may choose to establish a policy that all unspecified upgrades should be considered maintenance and, accordingly, expense the associated outlays as incurred

26

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• Question Z.51.15 regarding training of employees on developing internally generated computer software: although the skills obtained by the employees through the training may facilitate the development of the computer software, the training itself does not further the development of the software and does not otherwise contribute to putting the software in condition for use; therefore, expense, not capitalize

27

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #3, continued

• Question Z.51.11: Paragraph 8a of Statement 62 states that the interest capitalization requirements apply to assets that are constructed or otherwise produced for a government’s own use. Internally generated intangible assets meet this description. Therefore, the interest capitalization requirements should be applied, as appropriate, for internally generated intangible assets of business-type activities and enterprise funds

28

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #4 – Capital Outlay

• The City of St. Petersburg had the following capital-related activity in its governmental funds (capitalization threshold is $5,000):– Land purchase in general fund - $350,000– Purchase of signage in CRA fund - $75,325– Donated infrastructure in general fund - $673,522– Acquisition of street sweeper through a noncancelable lease in street

improvement fund - $130,565– Purchase of 15 Microsoft tablets in general fund at $400 each - $6,000– Street resurfacing project in progress in street improvement fund -

$256,852

• What is the City’s capital outlay balance in its governmental funds? What is the total amount of capital asset additions?

29

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #4 – Capital Outlay

• What about the lease on the street sweeper?– Lessor’s implicit rate on the lease is 6%– Requires no down payment and five equal annual

payments of $26,113– Street sweepers are considered to have a 7 year life– Title passes to the County at the end of the lease– The County’s incremental borrowing rate for similar

financing arrangements is 4%

30

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• GASBS 62, para 213: If at its inception a lease meets one or more of the following four criteria, the lease should be classified as a capital lease by the lessee. Otherwise, it should be classified as an operating lease.

a. The lease transfers ownership of the property to the lessee by the end of the lease term

b. The lease contains a bargain purchase optionc. The lease term is equal to 75 percent or more of the estimated

economic life of the leased propertyd. The present value at the beginning of the lease term of the minimum

lease payments, excluding that portion of the payments representing executory costs such as insurance and maintenance to be paid by the lessor, including any gain thereon, equals or exceeds 90 percent of the excess of the fair value of the leased property to the lessor at the inception of the lease

31

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• GASBS 62, para 213: A lessee should compute the present value of the minimum lease payments using its incremental borrowing rate, unless (1) it is practicable to obtain the implicit rate computed by the lessor and (2) the implicit rate computed by the lessor is less than the lessee's incremental borrowing rate. If both of those conditions are met, the lessee should use the implicit rate.

32

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• GASB 62, para 213: A lessee should compute the present value of the minimum lease payments using its incremental borrowing rate, unless (1) it is practicable to obtain the implicit rate computed by the lessor and (2) the implicit rate computed by the lessor is less than the lessee's incremental borrowing rate. If both of those conditions are met, the lessee should use the implicit rate.

33

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• GASBS 62, para 217: The asset recorded under a capital lease should be amortized as follows:– If the lease meets the criterion of either paragraph 213a or

213b, the asset should be amortized in a manner consistent with the lessee's normal depreciation policy for owned assets

– If the lease does not meet either criterion 213a or 213b, the asset should be amortized in a manner consistent with the lessee's normal depreciation policy except that the period of amortization should be the lease term. The asset should be amortized to its expected value, if any, to the lessee at the end of the lease term.

34

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• To summarize, at the inception of a capital lease, the capital asset and lease liability recorded by the lessee are the same. A two-part computation is required: – The present value of minimum lease payments scheduled

during the lease term is computed using the lower of the lessee's incremental borrowing rate or, if known, the implicit rate computed by the lessor. • The present value of minimum lease payments is compared with the fair value of the leased asset at the inception of the lease, and the lower amount is used to record the asset and liability.

35

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Leases Background Info

• Effective Date: For reporting periods beginning after December 15, 2019 (for December 31, 2020 and June 30, 2020). Early adoption encouraged.

• Summary: GASB No. 87 now requires the recognition of certain lease assets and liabilities for leases that were previously classified as operating leases, and establishes a single model for lease accounting.

• Adoption Methods: Retroactive, if practical for all periods presented (i.e. restate opening net position). If impractical (NOT inconvenient), must disclose reasons.

36

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Leases Background Info

• Lease Definition: Contract that conveys control of a non-financial asset for a period of time in an exchange or exchange-like transaction.

• Lease Term: Period during which lessee has a non-cancelable right to use the asset, plus:– Options to extent if reasonably certain– Unexercised options to terminate if reasonably certain– Fiscal funding or cancellation clause – should only affect

the lease term when it is reasonably certain that the clause will be exercised

37

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Leases Background Info

• Short‐term leases: Maximum possible term of 12 months or less.– Recognized as outflows of resources or expense (lessee) or

inflows of resources or revenue (lessor)

• Exclusions:– Intangible assets (oil/gas/mineral rights, licensing contracts)– Biological assets (timber, living plans, animals)– Inventory– Service Concession Arrangements– Leases financed with outstanding conduit debt (unless

supported by Lessor)– Supply contracts

38

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Lessee Initial Recognition

• Intangible right to use lease asset: Lease liability + lease payments made to lessor before commencement of lease + costs to place asset into service (excluding debt issuance costs)

• Lease liability: Present value of contractual lease payments (fixed) using implicit or incremental borrowing rate

39

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Lessee Subsequent Recognition

• Intangible right to use lease asset: Amortize/depreciate over the shorter of the useful life or lease term

• Lease liability: Difference between lease payment and interest expense reduces the liability

• Interest expense: Amortize the discount using an effective interest model

• Amortization/depreciation expense: Amortize in systematic and rational manner over shorter of lease term or useful life.

40

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Lessee Reporting & Disclosure

• Governmental funds: Expenditure and other financing source in the year of commencement, subsequent lease payments reported consistent with the debt service payments for long term debt

• • Disclosures:– General description– Total amount of lease assets (by major class) and related accumulated

amortization– Amount of outflows related to variable and other payments– Principal and interest requirements to maturity– Commitments under leases before commencement of the lease term– Components of any loss associated with an impairment.

41

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Lessor Initial Recognition

• Lease Receivable: Present value of contractual lease payments (fixed) using rate implicit in the lease, reduced by any amounts determined to be uncollectible

• Deferred inflow of resources: Lease receivable + lease payments received at or before commencement –incentives

42

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Lessor Subsequent Recognition

• Lease Receivable: Difference between lease payment and interest income reduces the receivable

• Deferred inflow of resources: Reduced by amount amortized to lease revenue

• Interest income: Amortize using effective interest model

• Lease revenue: Systematic and rational amortization of the deferred inflow of resources

43

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

GASB 87 – Lessor Reporting & Disclosure

• Governmental funds: Recognize lease receivable and deferred inflow of resources. Should NOT derecognize underlying asset, but continue to depreciate/evaluate for impairment

• Disclosures:– General description– Total amount of revenues (if not obvious from face of

statements)– Total amount of revenues from variable payments– Existence, terms and conditions of options by lessee to

terminate the lease of abate payments, when the lessor has issued debt secured by lease payments

44

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• 7.9.8. Q—Should a government's capitalization policy be applied only to individual assets or can it be applied to a group of assets acquired together? Consider a government that has established a capitalization threshold of $5,000 for equipment. If the government purchases 100 computers costing $1,500 each, should the computers be capitalized?

• A—Authoritative pronouncements do not address the manner in which a capitalization policy should be established and applied. Capitalization policies adopted by governments include many considerations such as finding an appropriate balance between ensuring that all significant capital assets, collectively, are capitalized and minimizing the cost of record keeping for capital assets. It may be appropriate for a government to establish a capitalization policy that would require capitalization of certain types of assets whose individual acquisition costs are less than the threshold for an individual asset. Computers, classroom furniture, and library books are assets that may not meet the capitalization policy on an individual basis, yet might be considered material collectively.

45

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

46

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• Entry in general fund (or in debt service fund, if required by legal or contractual mandate):– DR: Capital outlay $116,250– CR: Other financing sources $116,250– DR: Expenditure – debt service principal $21,463– DR: Expenditure – debt service interest $4,650– CR: Cash $26,113

• Entry in general capital assets ledger:– DR: Vehicle – street sweeper $116,250– CR: Capital lease obligation $116,250

47

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

48

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

49

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

50

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

51

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #4 – Capital Outlay

• Capital outlay computation:• Gov’t Activities Capital Asset Additions = $350,000

land purchase + $75,325 signage purchase + $673,522 donated infrastructure + $116,250 street sweeper capital lease + $0 Microsoft tablets + $256,852 CIP project

• Less: Reconciling Item– (673,522) donated infrastructure

• Total Capital Outlay – Governmental Funds $798,427

52

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #5

• The City of New Port Richey is implementing a new HR system. This is a commercially available software product that captures and stores all pertinent information pertaining to each employee and interfaces with the City’s payroll system to update any relevant wage and benefit changes to each employee on a bi-weekly basis. There were no upfront costs associated with acquiring this product. Rather, the City entered into a 5 year licensing agreement with the software provider.

53

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Question #5

• Over the 5 year agreement, the software company invoices the City on a quarterly basis. Details of each quarterly invoice include the following:– Right to use = $22,500– Training and support services = $4,000– Ongoing system maintenance and upgrades = $5,700

• The City is expensing the full amount when paid each quarter. Is this correct? If not, how should the City record the acquisition of the HR system and subsequent quarterly payments?

54

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #5

• Upon acquisition:– DR: Computer software $450,000– CR: Liability $450,000(Amortize over useful life of software)

• Upon invoice payment:– DR: Liability $22,500– DR: Expense (training & support) $4,000– DR: Expense (maintenance) $5,700– CR: Cash $32,200

55

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #5

• Z.51.16. Q—A government enters into a licensing agreement for computer software that will be considered internally generated. The payments made by the government to the vendor under the agreement are for multiple components, including the use of the software, development of modifications to meet the government’s requirements prior to being put into operation, training for users of the software, routine systems maintenance, and rights to future upgrades and modifications. How should this agreement be accounted for?

• A—In this circumstance, the outlays associated with the agreement should be allocated among all of the individual elements, and those elements should be accounted for based on the applicable guidance in Statement 51. For example, the outlays associated with the use of the software generally should be capitalized as part of the application development stage, and outlays associated with the training for users of the software and routine systems maintenance should be expensed as part of the postimplementation/operation stage of development.

56

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #5

• Z.51.1. Q—Should commercially available computer software that is purchased or licensed by the government and placed into operation without modification requiring more than minimal incremental effort (that is, the computer software is not considered internally generated) be considered an intangible asset as described in Statement 51?

• A—Yes. Commercially available computer software that is not considered internally generated computer software, whether purchased or licensed, generally will meet the description of an intangible asset in paragraph 2 of Statement 51.

57

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #5

• Z.51.21. Q—A government acquires commercially available computer software through a fiveyear licensing agreement. Under the terms of the agreement, the government is required to make annual installment payments to the software vendor for the right to use the software over the life of the agreement. How should this transaction be reported?

• A—As discussed in Question Z.51.1, in such circumstances, the government should report the licensed software as an intangible asset. A long-term liability representing the government’s obligation to make the annual payments over the life of the contract also should be reported. The provisions of Statement 62, paragraphs 211–271, as amended, should not be applied to determine the financial reporting for such a licensing agreement, even if the agreement is referred to as a lease, because the provisions of Statement 62 do not apply to licensing agreements.

58

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

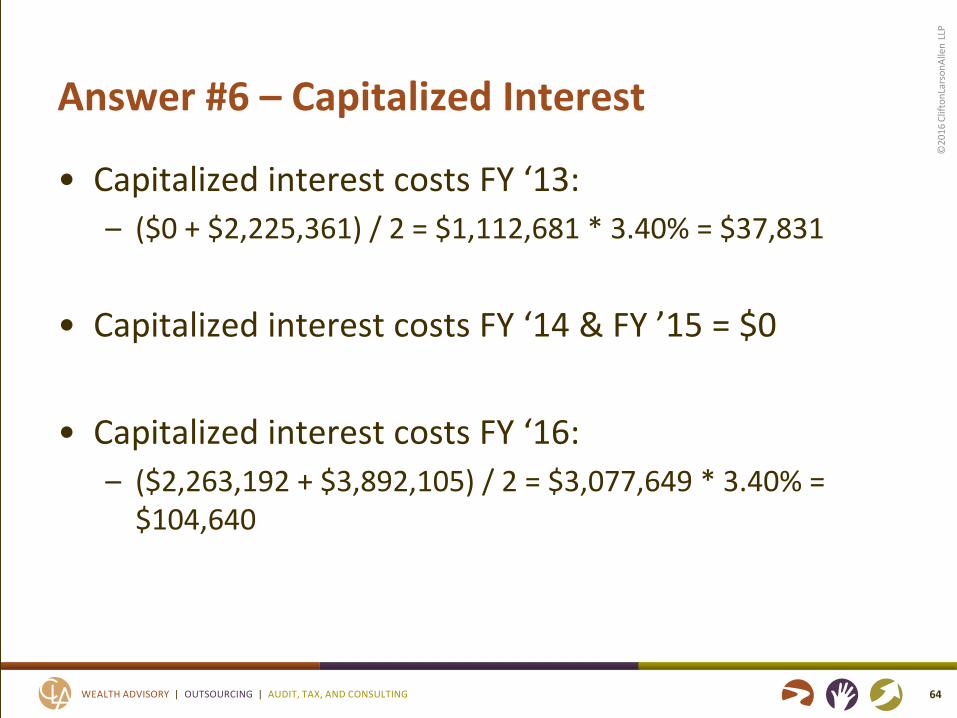

Question #6 – Capitalized Interest

• Pinellas County began a utility expansion project within its Water & Sewer fund that was entirely funded with $12m of BABS bonds (interest rate of 3.4%) The project began in October ‘12 and $2,225,361 was spent. Then, for various reasons the project took a two year hiatus, and project expenditures resumed in October ‘15. For FY ‘16, $3,892,105 was spent. How much interest, if any, should the County capitalize associated with this project?

59

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #6 - Capitalized Interest

• The County needs to capitalize interest if it’s material to that fund. See GASB 62 para 5-22.

• GASB 62, para 11 provides guidance for capitalization of interest on qualifying assets whenever an entity has outstanding debt.

• GASB 62, para 9f prohibits the capitalization of interest for assets acquired by contributions and grants that restrictively specify the type of asset that may be purchased or constructed.

• GASB 62, para 19 & 20 provides different guidance in situations in which a government issues tax-exempt debt that is externally restricted by the bond indenture to finance specific capital assets.

60

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #6 - Capitalized Interest

• GASB 37, para. 6, clarifies that these standards do not apply to general capital assets.

• GASB Implementation Guide Question Z.51.11: GASB 62, para 8a, states interest capitalization requirements apply to assets that are constructed or otherwise produced for a government's own use. Internally generated intangible assets meet this description (i.e. ERP implementations)

• Build America Bonds (BABS) not considered tax-exempt borrowing and should not follow para 19 & 20 of GASB 62, per Question 7.10.7 of the Guide

61

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #6 - Capitalized Interest

• What to do if the project is temporarily put on hold?• Per GASB 62, para 16: “If the government suspends

substantially all activities related to acquisition of the asset, interest capitalization should cease until activities are resumed. However, brief interruptions in activities, interruptions that are externally imposed, and delays that are inherent in the asset acquisition process should not require cessation of interest capitalization”

62

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #6 - Capitalized Interest

• Disclosure requirements per GASB 62, para 22:– For an accounting period in which no interest cost is

capitalized, the amount of interest cost incurred and charged to expense during the period

– For an accounting period in which some interest cost is capitalized, the total amount of interest cost incurred during the period and the amount thereof that has been capitalized

63

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Answer #6 – Capitalized Interest

• Capitalized interest costs FY ‘13:– ($0 + $2,225,361) / 2 = $1,112,681 * 3.40% = $37,831

• Capitalized interest costs FY ‘14 & FY ’15 = $0

• Capitalized interest costs FY ‘16:– ($2,263,192 + $3,892,105) / 2 = $3,077,649 * 3.40% =

$104,640

64

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Internal Control Considerations

• Monitoring Controls:– How well are capital asset records maintained, including

how such records are integrated into the accounting system? Are subsidiary ledger and/or tag system used containing information such as description, location, cost, tag #, useful life, etc. for each capital asset?

– Are individual(s) responsible for processing invoices knowledgeable of your entity’s capitalization policy? What is the risk that a capital asset addition could get improperly expensed? Or only partially recorded (i.e. not including any ancillary costs associated with getting the asset in place, such as shipping and installation)

65

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Internal Control Considerations

• Reconciliation Controls:– Ensure that the detailed listing of capital asset schedule

reconciles to the general ledger (for proprietary funds) and rollforward schedule (for governmental and proprietary funds).

– Ensure that capital asset additions related to governmental funds are reconciled to the capital outlay expenditure accounts.

66

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Internal Control Considerations

• Physical Inventory Controls:– Are periodic physical counts/comparisons made to ensure

that all capital assets included on the depreciation schedule are in existence? Does the nature and frequency of the counts meet regulatory requirements?

– If an asset is damaged or can no longer be used, does your entity have a written policy in place governing the treatment of those assets that are to be disposed of or sold? What controls are in place to ensure such policy is followed?

67

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Internal Control Considerations

• Recording Capital Asset Acquisitions – Requisition: Is procurement policy followed? Purchase

order always generated? Or can a capital item be purchased via check request or purchasing card?

– Payment: What layers of review take place before an invoice for a capital acquisition is paid?

– Segregation of Duties: Does the person(s) approving capital asset purchases have the ability to initiate purchases and create the documents supporting purchase initiation? If yes, who reviews and approves such purchases?

68

©20

16 C

lifto

nLar

sonA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Internal Control Considerations

• Cutoff– What does your entity do in order to ensure that all capital

asset acquisitions are recorded in the proper period (including construction-related costs and retainage)?

– Are capital projects closed out and depreciated timely? What controls are in place to verify this?

69

©20

16 C

lifto

nLar

sonA

llen

LLP

70

QUESTIONS?

I hope you enjoyed another rendition of Best of Accounting Complexities for the FGFOA Gulf Coast Chapter

twitter.com/CLAconnectfacebook.com/cliftonlarsonallen

linkedin.com/company/cliftonlarsonallen

©20

16 C

lifto

nLar

sonA

llen

LLP

CLAconnect.com

Andrew Laflin, [email protected]

71