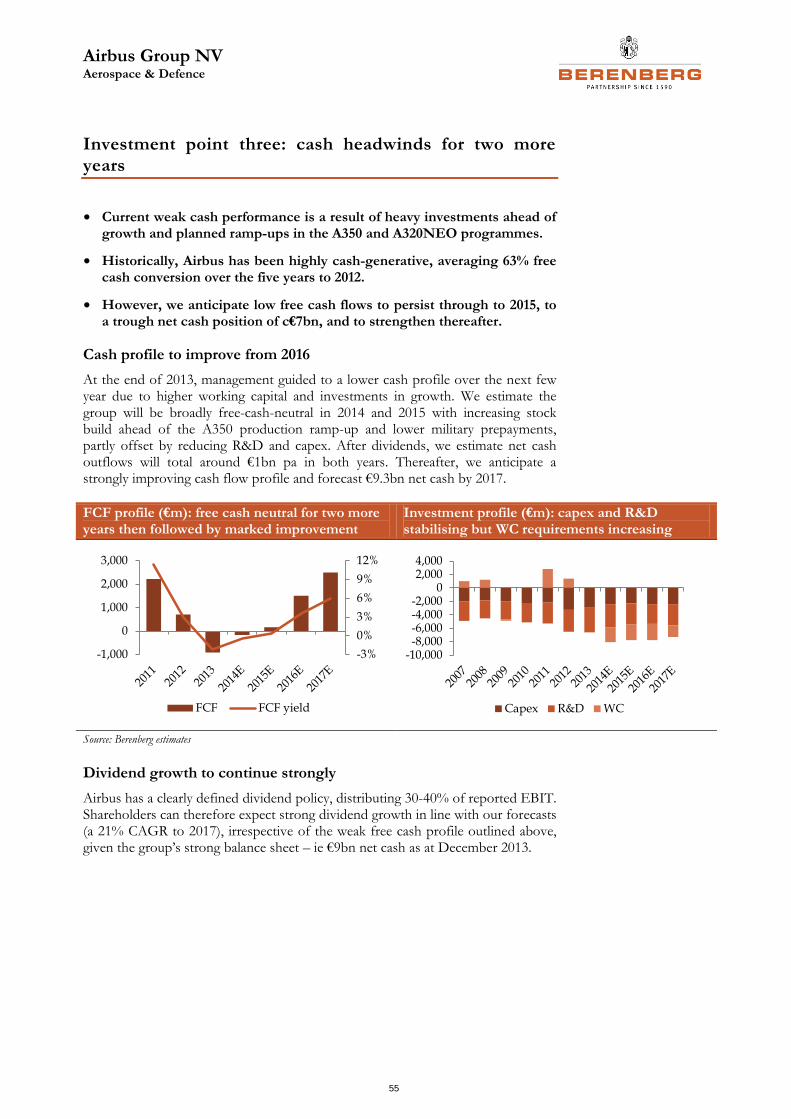

Berenberg European AerospaceDefence sector report Jun 17 2014 330pgs (Initiations)

330

BERENBERG EQUITY RESEARCH Aerospace & Defence Flying through the turbulence Andrew Gollan Analyst +44 20 3207 7891 [email protected] Chris Armstrong Specialist Sales +44 20 3207 7809 [email protected] 16 June 2014 Aerospace & Defence

-

Upload

angadsawhney -

Category

Documents

-

view

79 -

download

8

description

Berenberg European AerospaceDefence sector report Jun 17 2014 330pgs .

Transcript of Berenberg European AerospaceDefence sector report Jun 17 2014 330pgs (Initiations)

BERENBERG EQUITY RESEARCH BERENBERG EQUITY RESEARCH

Aerospace & Defence

Flying through the turbulence

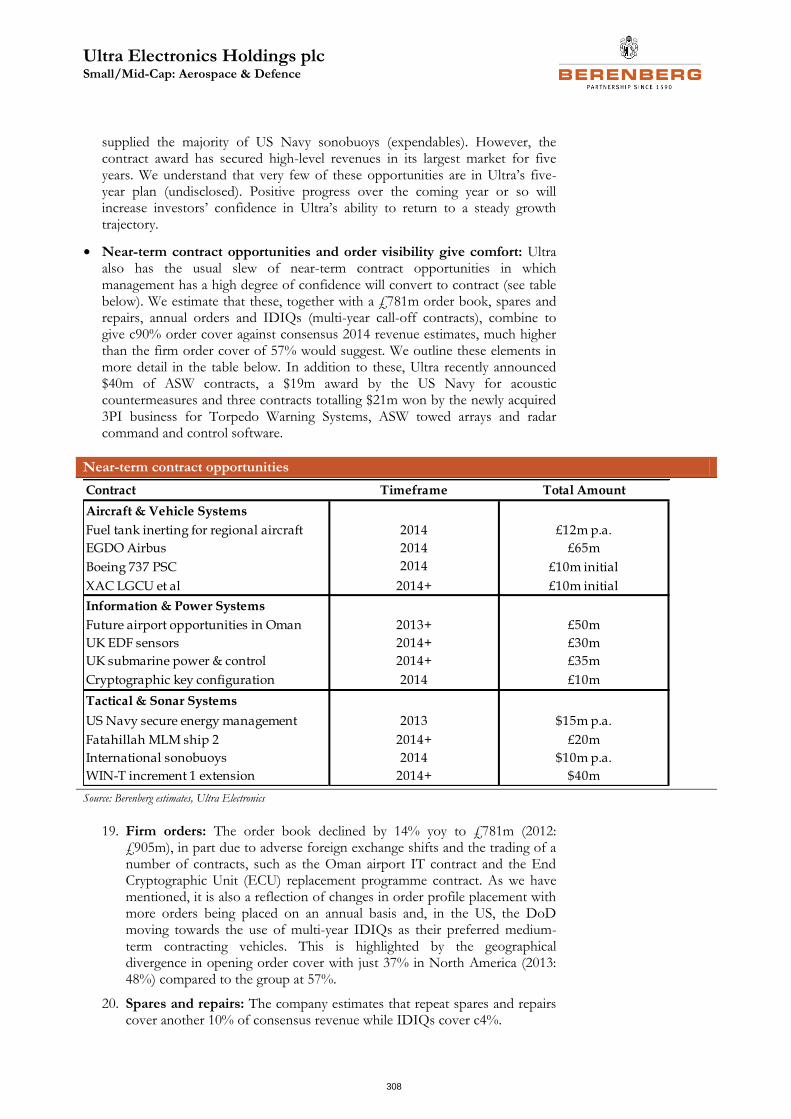

Andrew Gollan

Analyst

+44 20 3207 7891

Chris Armstrong

Specialist Sales

+44 20 3207 7809

16 June 2014

Aerospace & Defence

What is Berenberg THOUGHT LEADERSHIP?

Berenberg's analysts are recognised by investors and by corporates for their in-depth research into the industries they cover.

Our THOUGHT LEADERSHIP brand will highlight the deep-dive fundamental industry research that we feel is most important to informing our forecasts and ratings.

For our disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) and our disclaimer please see the end of this document. Please note that the use of this research report is subject to the conditions and restrictions set forth in the disclosures and the disclaimer at the end of this document.

Aerospace & Defence

Table of contents Flying through the turbulence 1

Sector overview 2

Aerospace and defence – 10 charts to bring us up to speed 6

Stock summary – five key picks 8

Stock summary – the rest 11

UK and European aerospace and defence valuation table 14

US aerospace and defence valuation table 15

Share price performance 16

Valuation charts 18

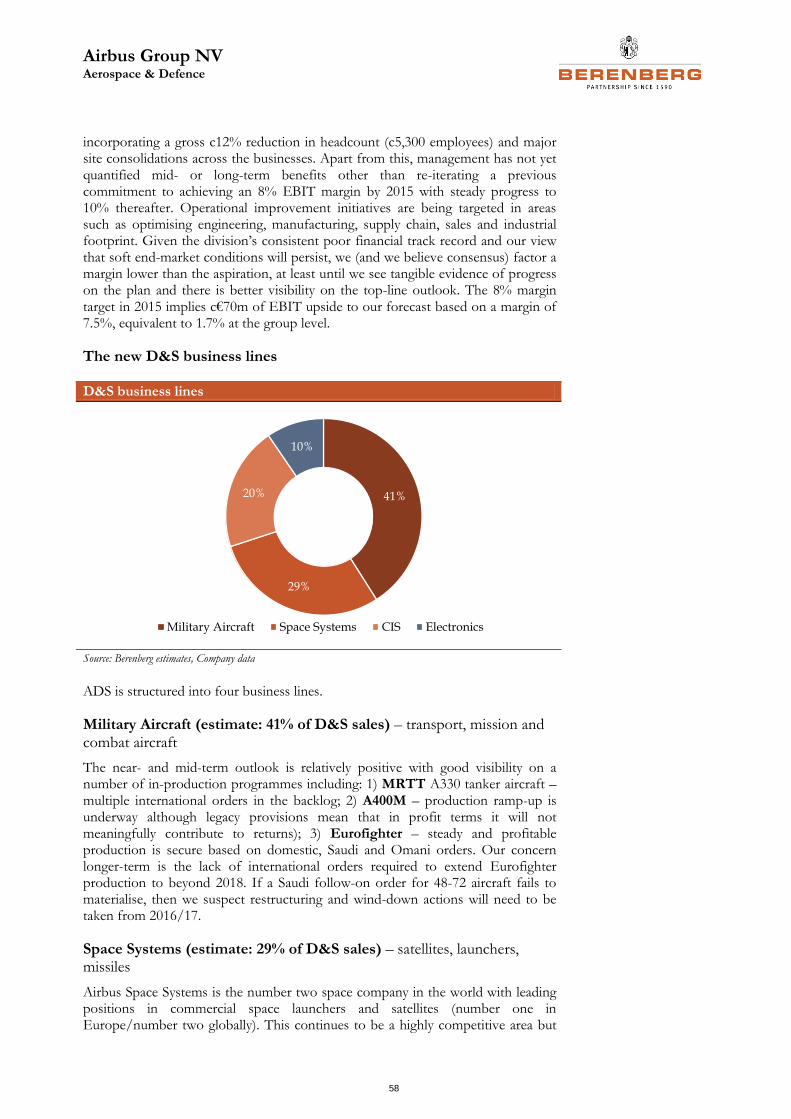

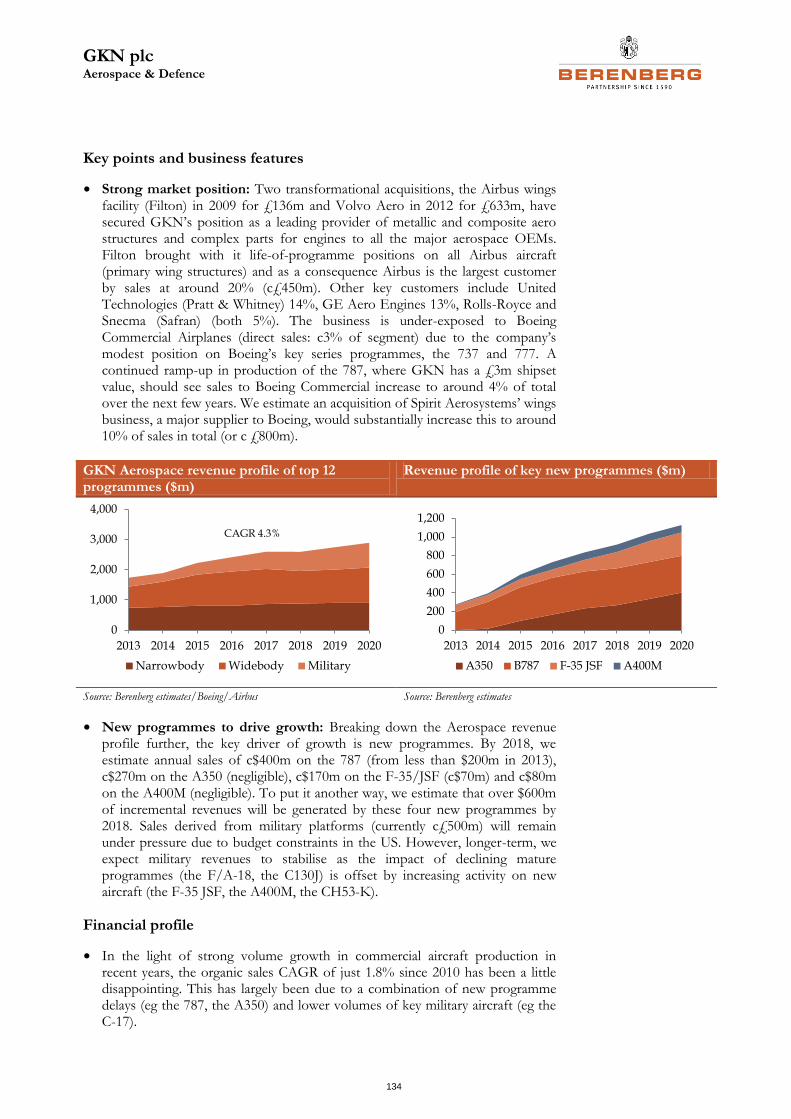

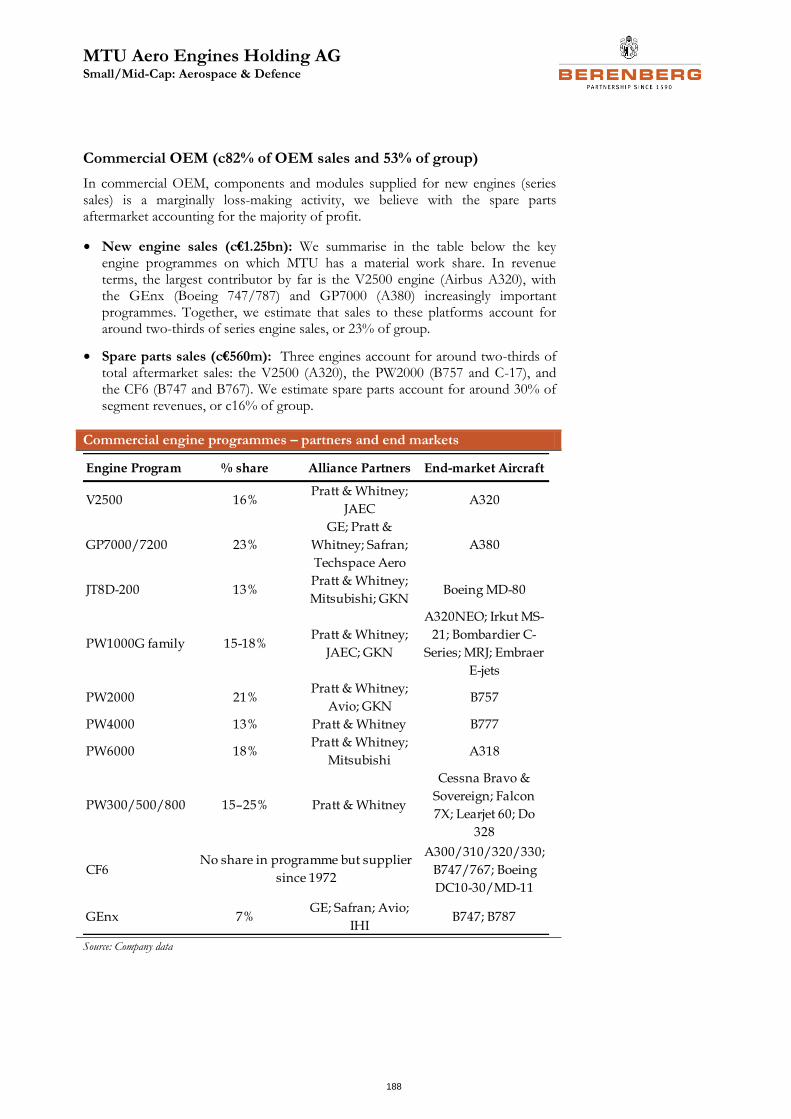

Civil aerospace – OE 20

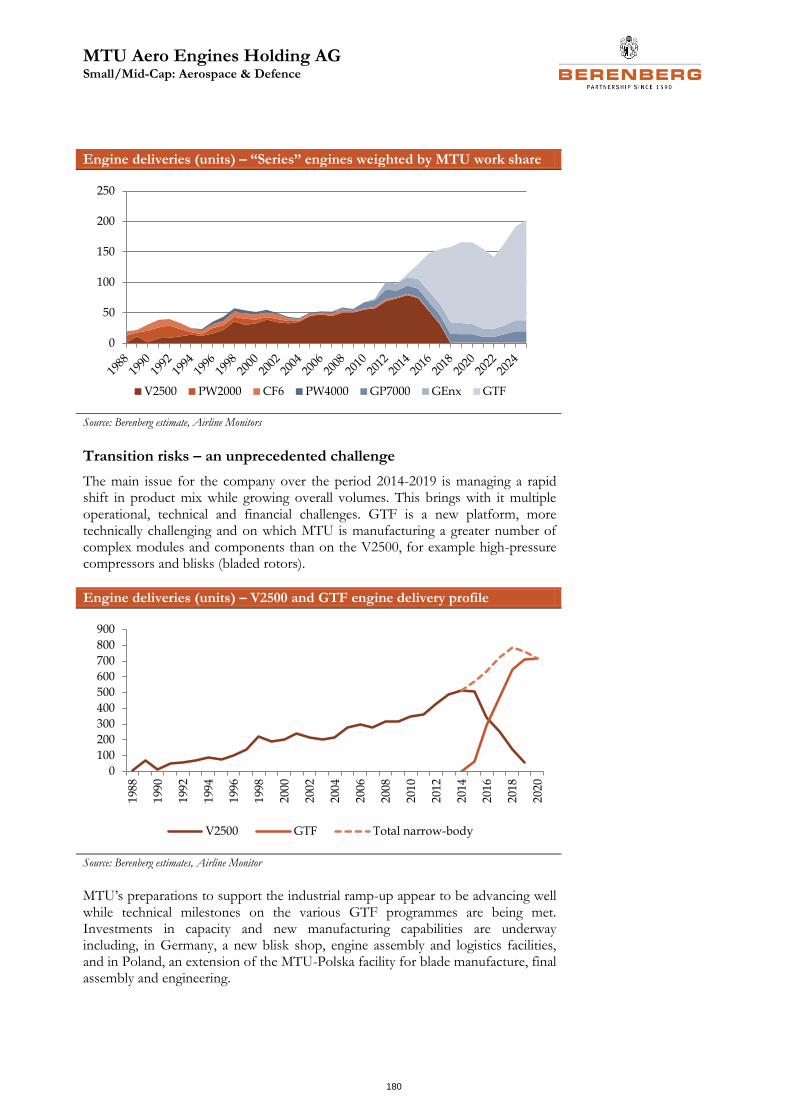

Commercial jets delivery profile 25

Civil aerospace – aftermarket 26

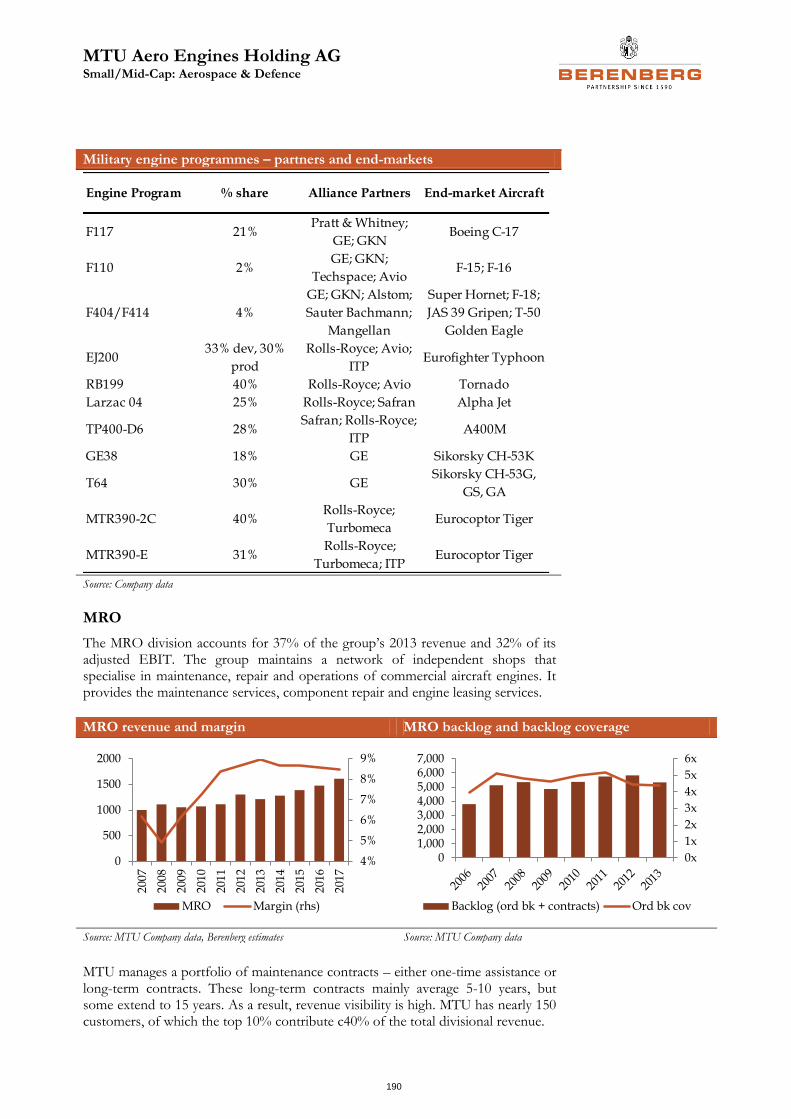

Defence – market outlook 28

Global trends 28

US defence – a stabilising situation 29

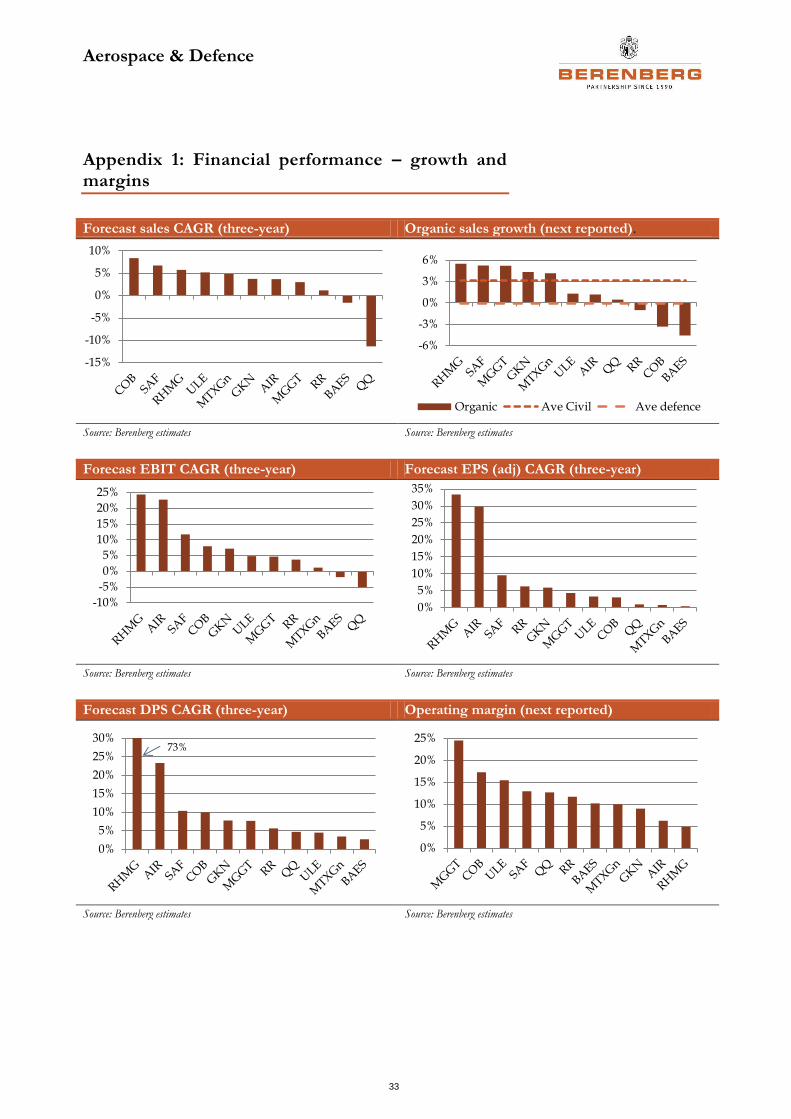

Appendix 1: Financial performance – growth and margins 33

Appendix 2: Financial performance – returns, cash, balance sheet 34

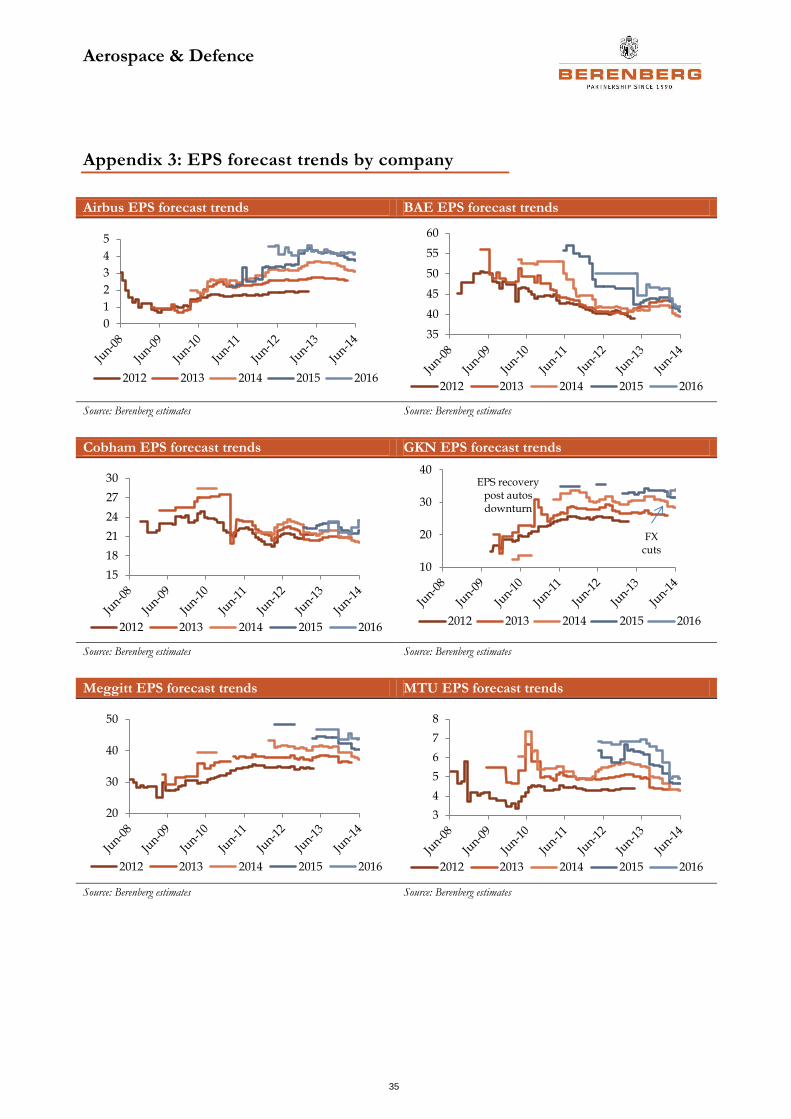

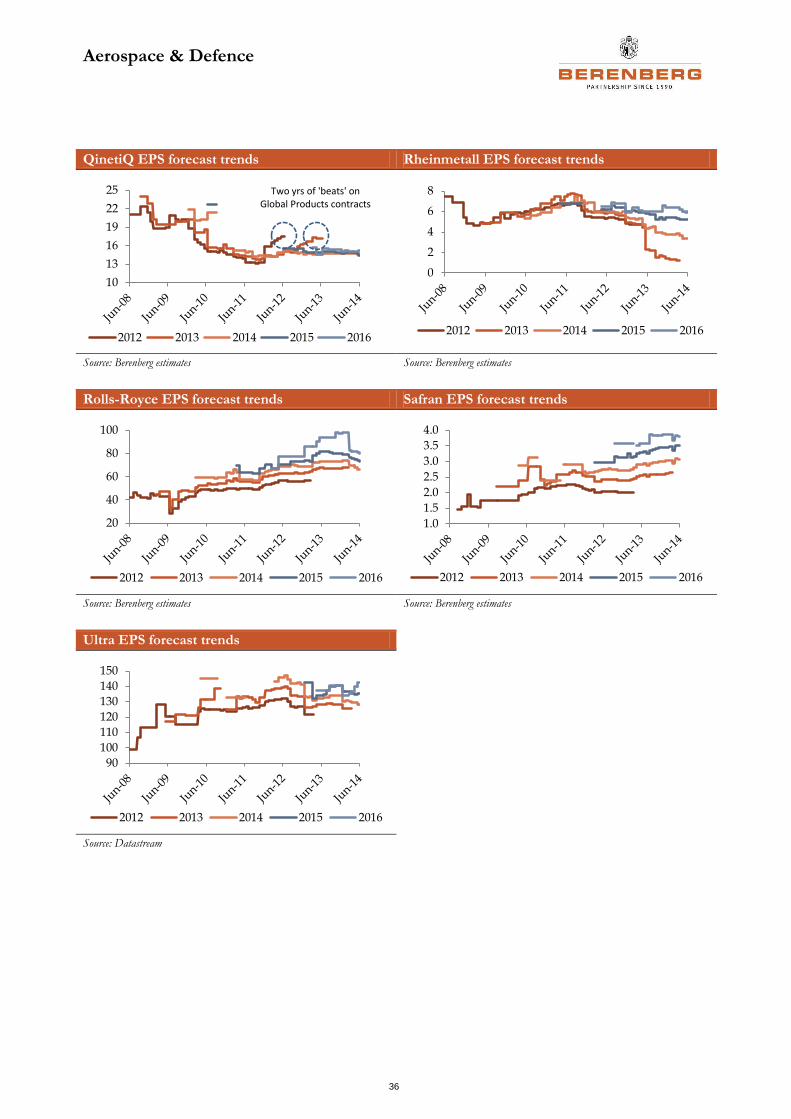

Appendix 3: EPS forecast trends by company 35

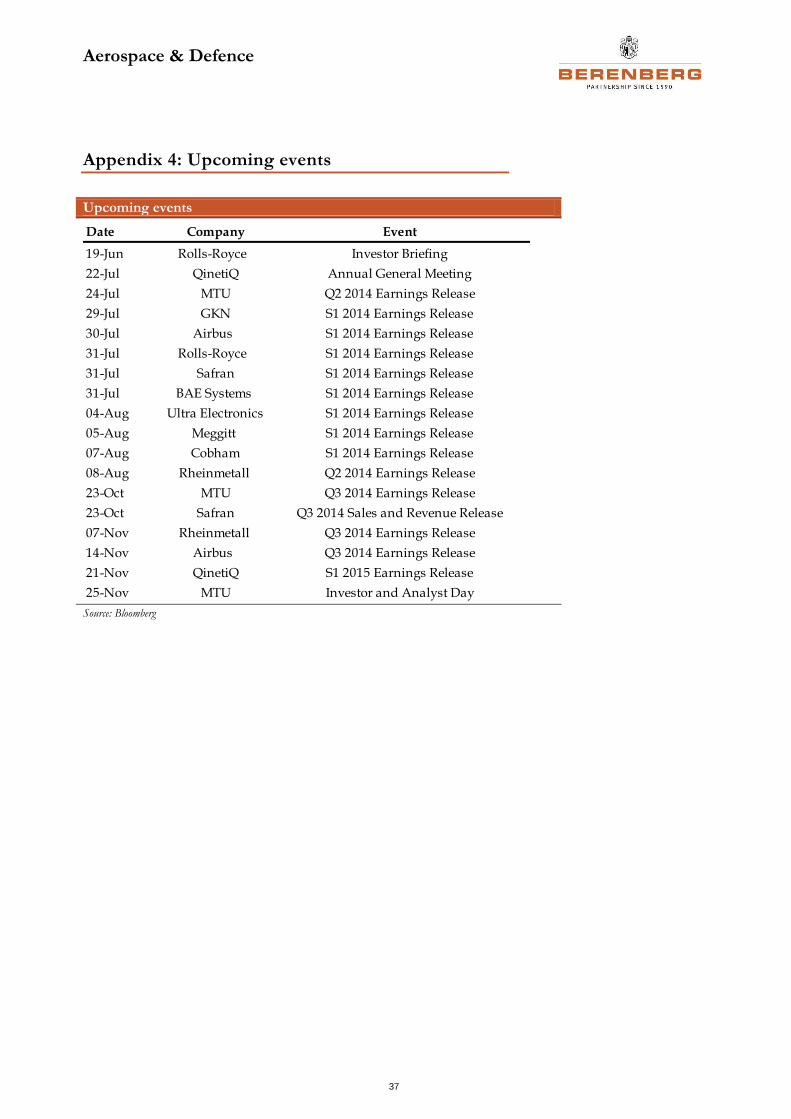

Appendix 4: Upcoming events 37

Companies

Airbus Group 38

BAE Systems 65

Cobham 89

GKN 112

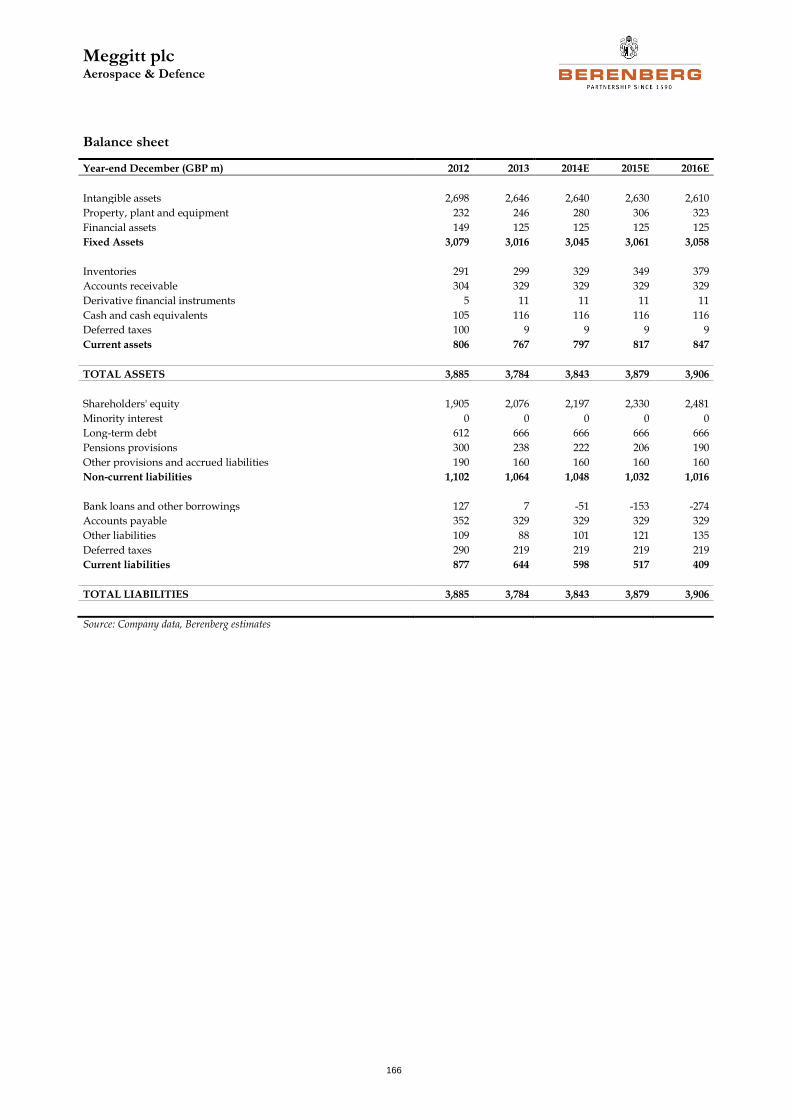

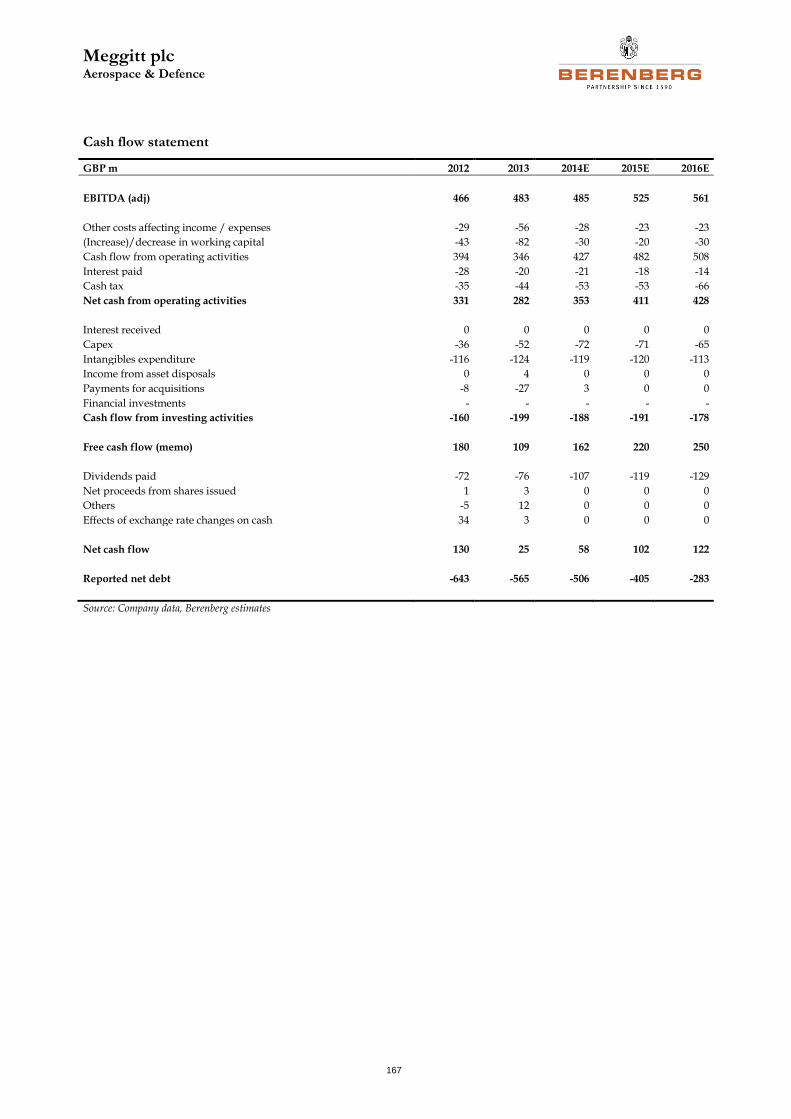

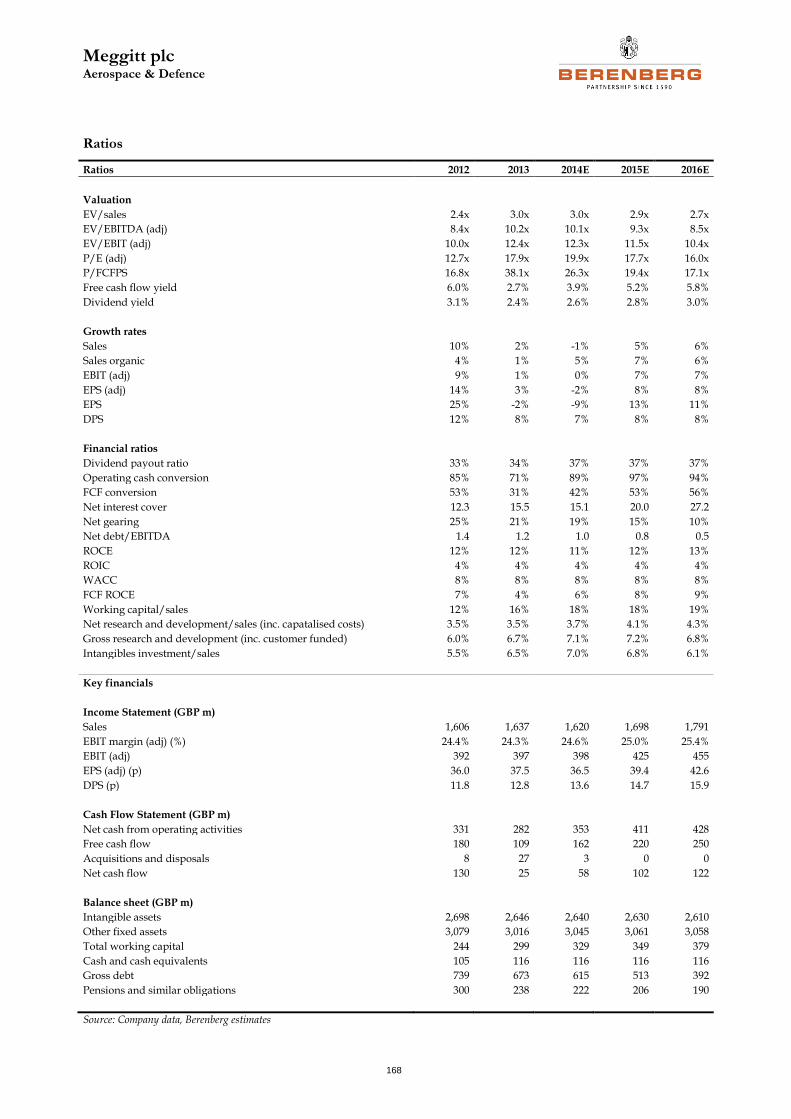

Meggitt 142

MTU Aero Engines 169

QinetiQ 196

Aerospace & Defence

Rheinmetall 219

Rolls-Royce 244

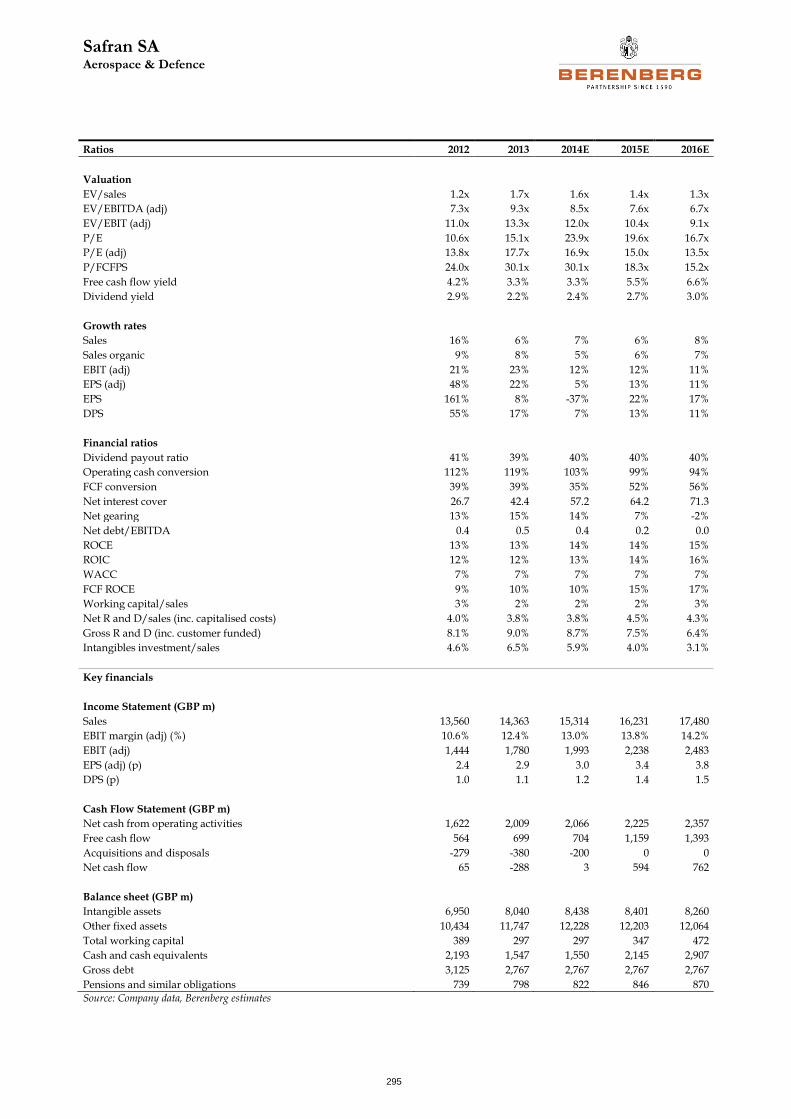

Safran 269

Ultra Electronics 296

Contacts: Investment Banking 321

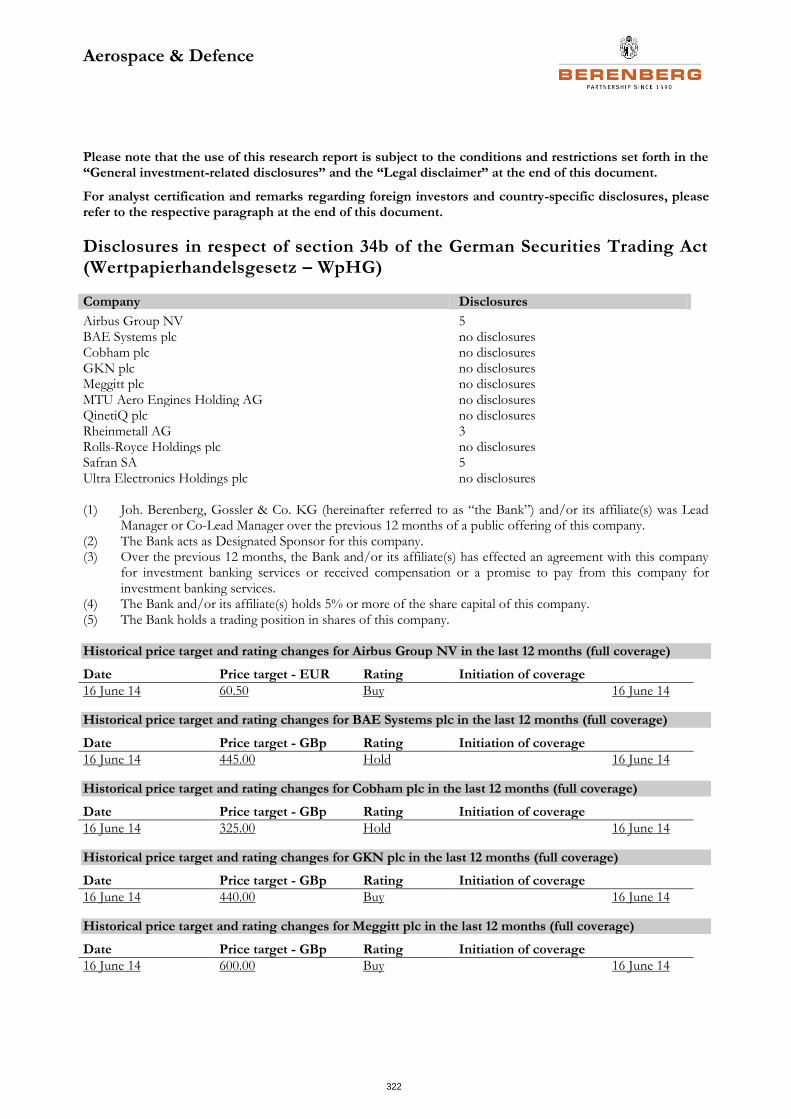

Disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) 322

Aerospace & Defence

1

Flying through the turbulence

● We initiate coverage on nine companies in the pan-European aerospace and defence sector. We also include analysis of two further companies in this report following a change of analyst.

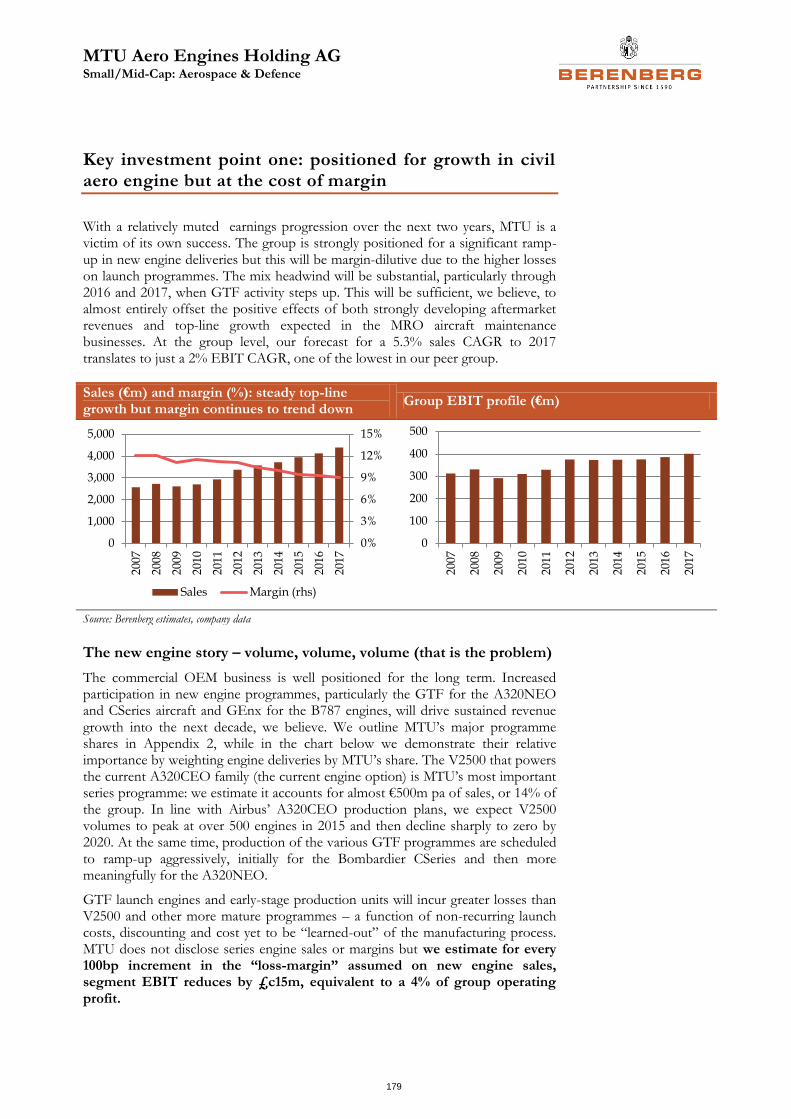

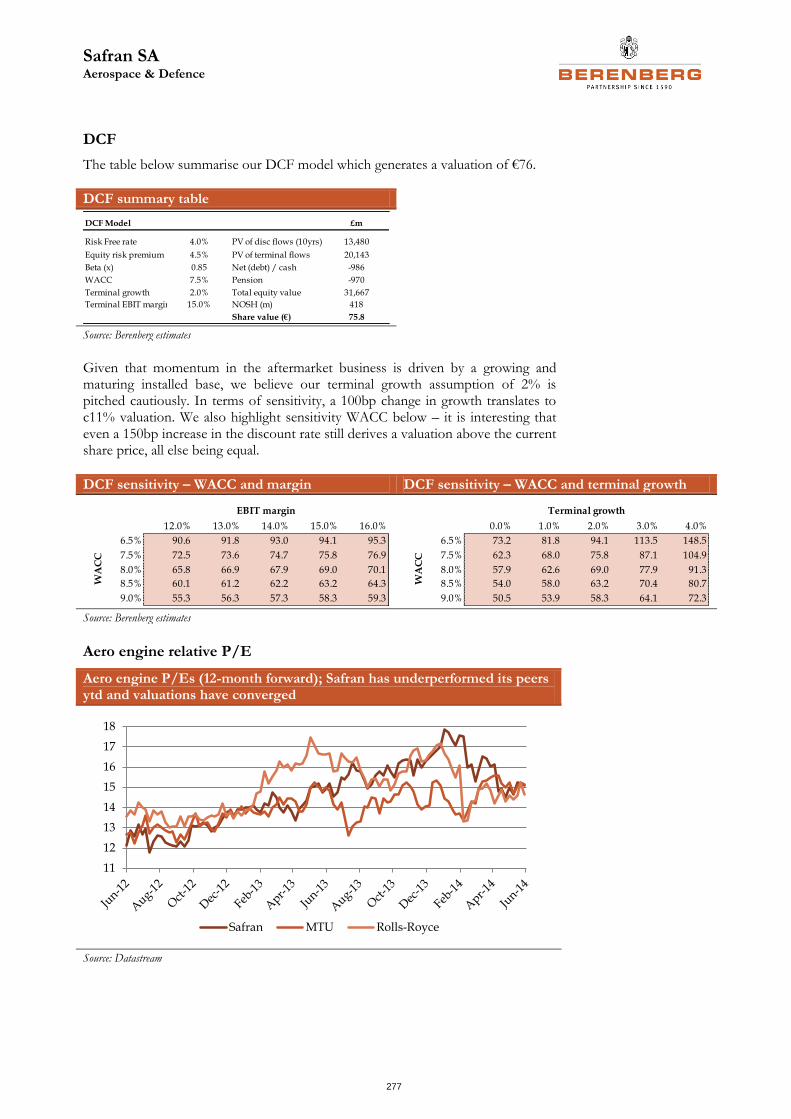

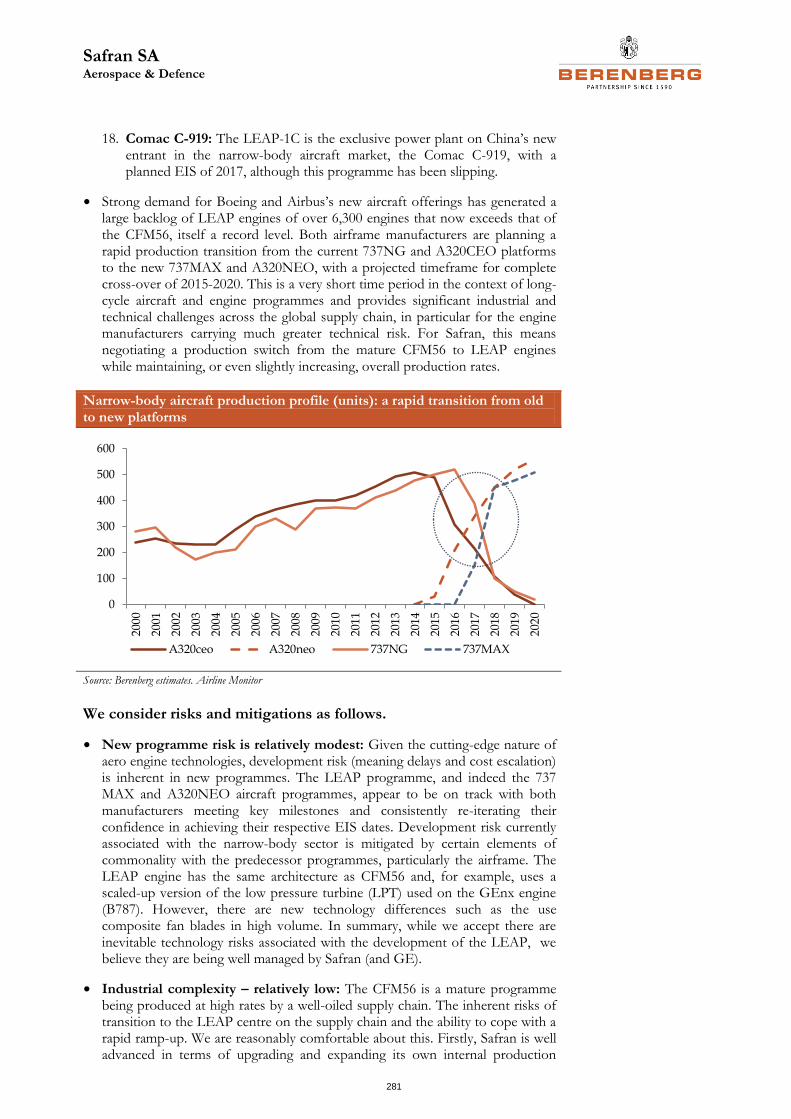

● Sector stance: We have six Buy and five Hold recommendations (no Sells) with a preference for civil-aerospace-exposed stocks. Over the last 12 months, civil and defence valuations have converged as defence headwinds have moderated and civil profit momentum have faltered. We look to the civil names to at least deliver against growth expectations as the industry continues to increase production and as aftermarket activity recovers. If they do, then current valuations look attractive. There are risks, not least programme execution (and macro-related, as discussed below), hence stock selection is key.

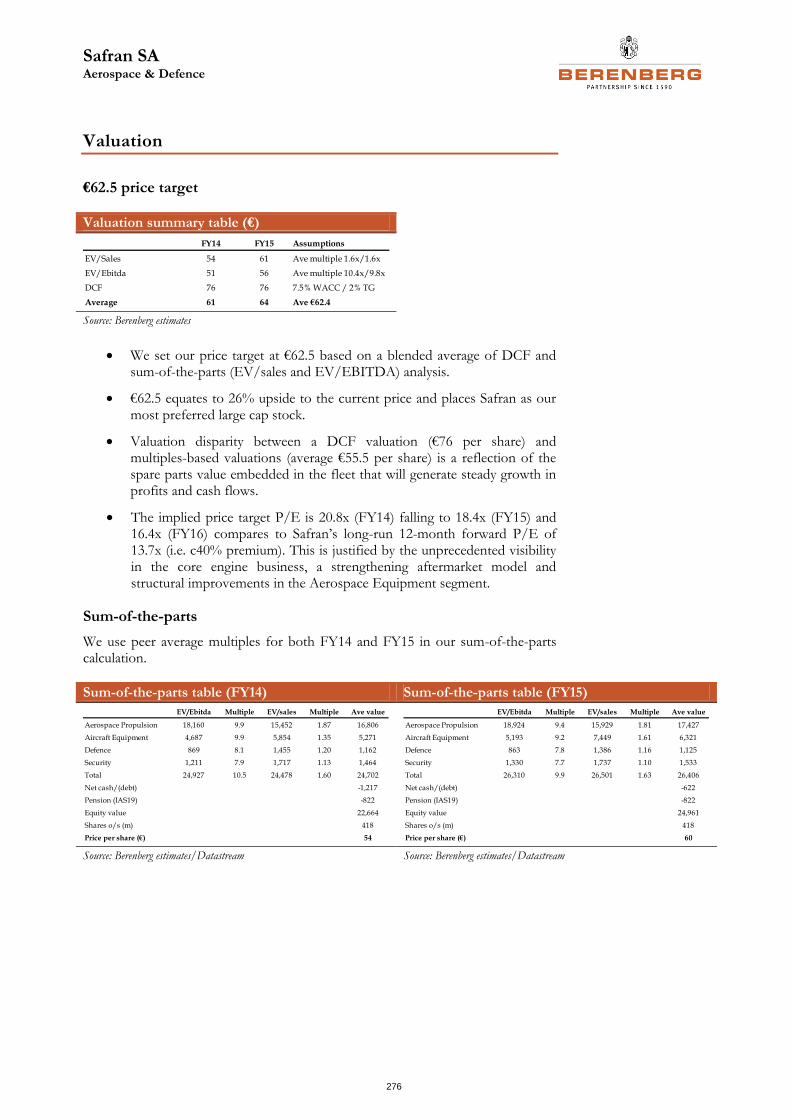

● Stock picks: Our large and mid-cap stocks with the most upside are respectively Safran (Buy, PT €62.5, upside 25%) and Rheinmetall (Buy, PT €62.5, upside 22%). We are also Buyers of Airbus PT €60.5), Rolls-Royce (PT 1,216p), Meggitt (PT 600p) and GKN (PT 440p).

● Preferred large cap: Safran (PT €62.5) – the optimal play on the dual trends of the commercial aftermarket and original equipment cycles. Safran’s engine fleet has a relative structural advantage over its peers that will drive continuous growth in high-margin spares.

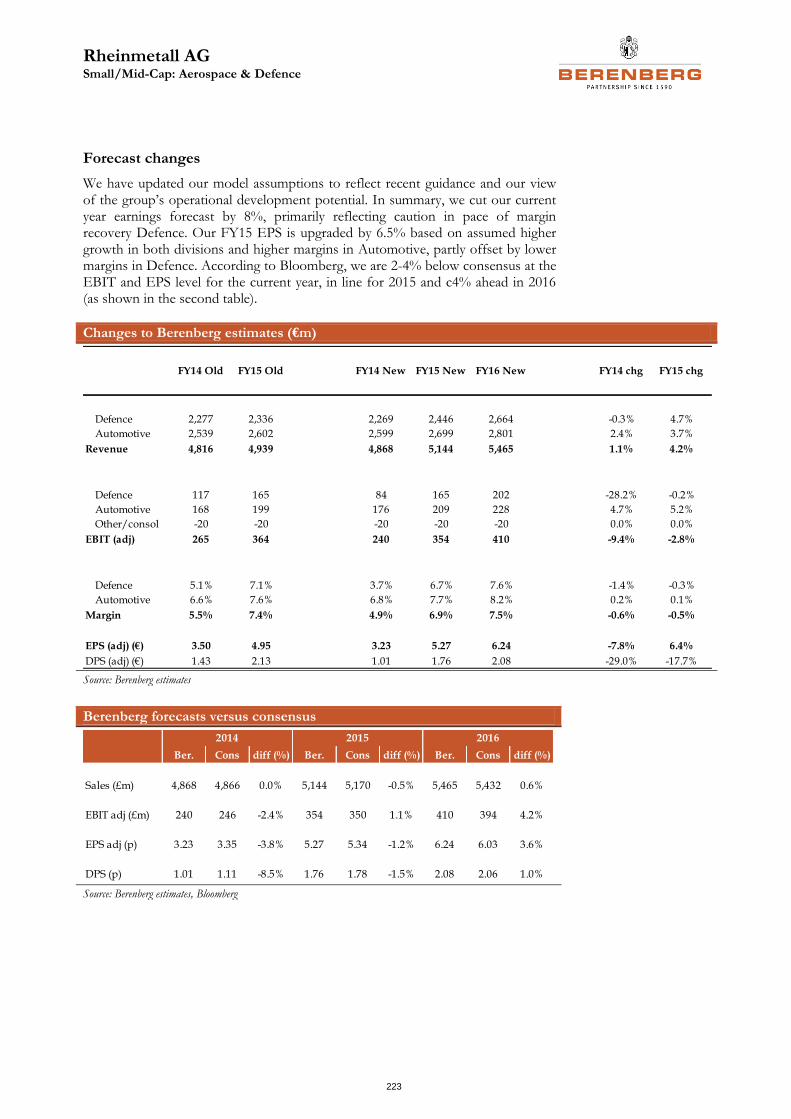

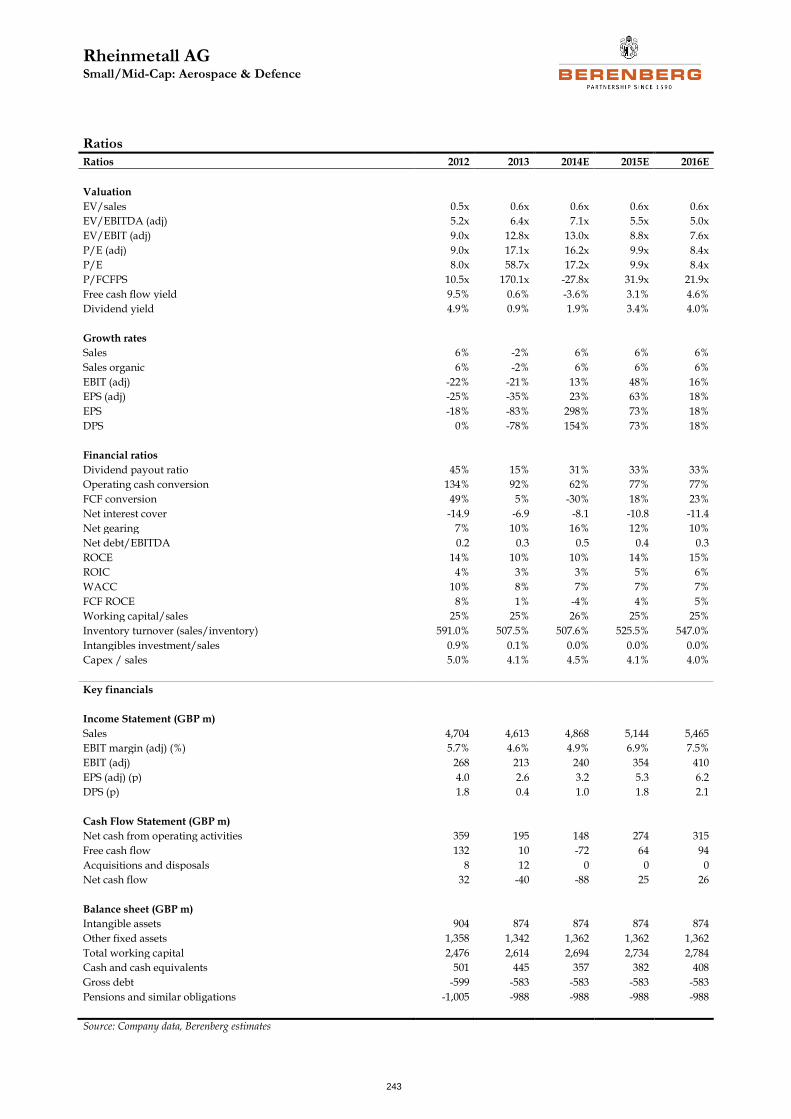

● Preferred mid-cap: Rheinmetall (PT €62.5) – with the potential to deliver a strong recovery in profits with both divisions back in growth mode. Valuation metrics are low suggesting only modest upside is priced in.

● Defence headwinds moderating: The US finally has an executable budget and top-line declines are moderating. Companies naturally remain cautious but most expect to return to organic growth by 2015.

● Commercial aerospace is all about execution: The fundamental outlook for both the original equipment (OE) and aftermarket remains positive but we caution that the industry is embarking on a ramp-up of activity on an unprecedented number of new aircraft and engine programmes, bringing with it execution risk and margin dilution.

● Growth: Excluding earnings recovery at Airbus and Rheinmetall, weak underlying sector EPS growth in 2014 (average: -2.4%) is due to FX impacts and certain one-off charges. Thereafter, we anticipate an improving earnings profile (three-year CAGR: 4.0%).

● Performance: The sector is down by 5% ytd (or by 1% unweighted), an 11% and 7% underperformance of the SXXP and the FTSE All-Share respectively. We believe this has been driven by sector rotation (after a strong 2013) and company-specific downgrades/de-ratings. Best and worst performers: Cobham +18%, Rolls-Royce -19%.

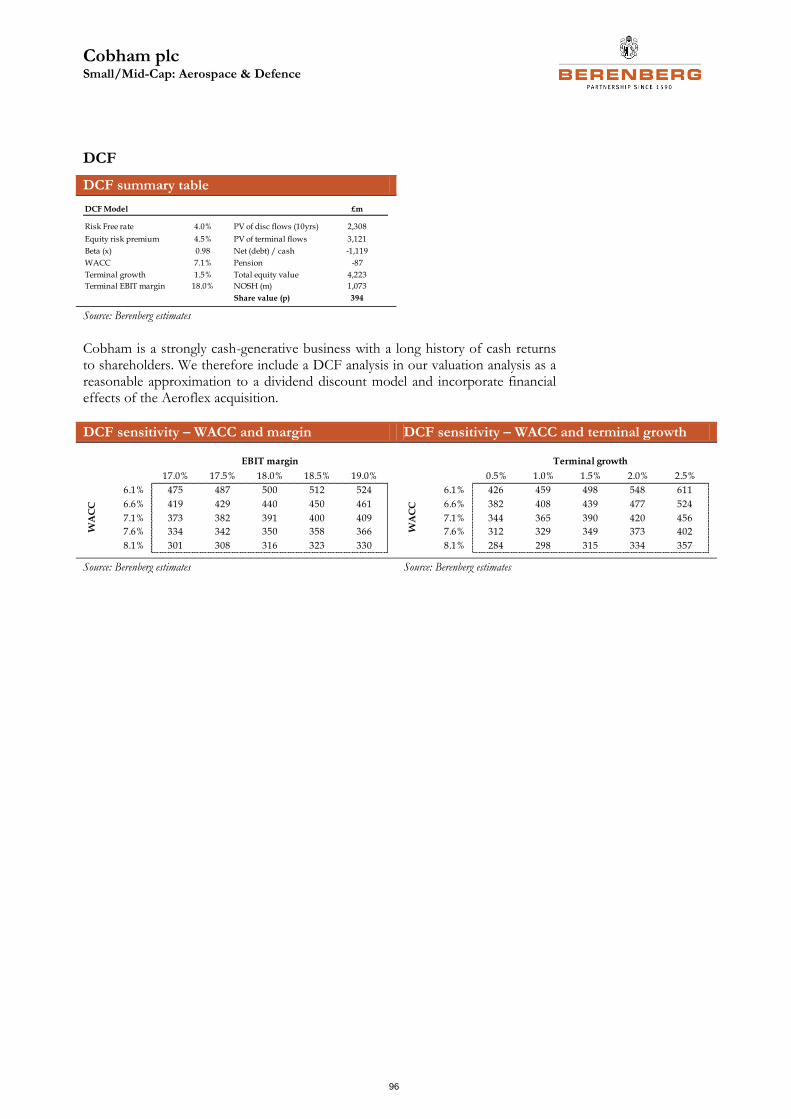

● Sector valuations have converged: The defence stocks re-rated over the past year and now trade on multiples only slightly below the civil aerospace average, except for the defence prime contractors (BAE and Rheinmetall) that continue to trade at their historical 20-30% discount. Based on our FY15 forecasts, the sector average P/E is 13.3x (ranging from Rolls-Royce on 15.4x to Rheinmetall on 9.9x), and adjusted EV/EBITDA is 8.1x (ranging from Cobham on 10.0x since the Aeroflex acquisition, and Airbus and Rolls-Royce on 7.5x).

● Macro risks: As we go to print, the evolving geopolitical situation in Iraq and other recent developments such as the Emirates order cancellation are disproportionately affecting sentiment. Clearly, sector valuations could be at risk if the macro situation deteriorates.

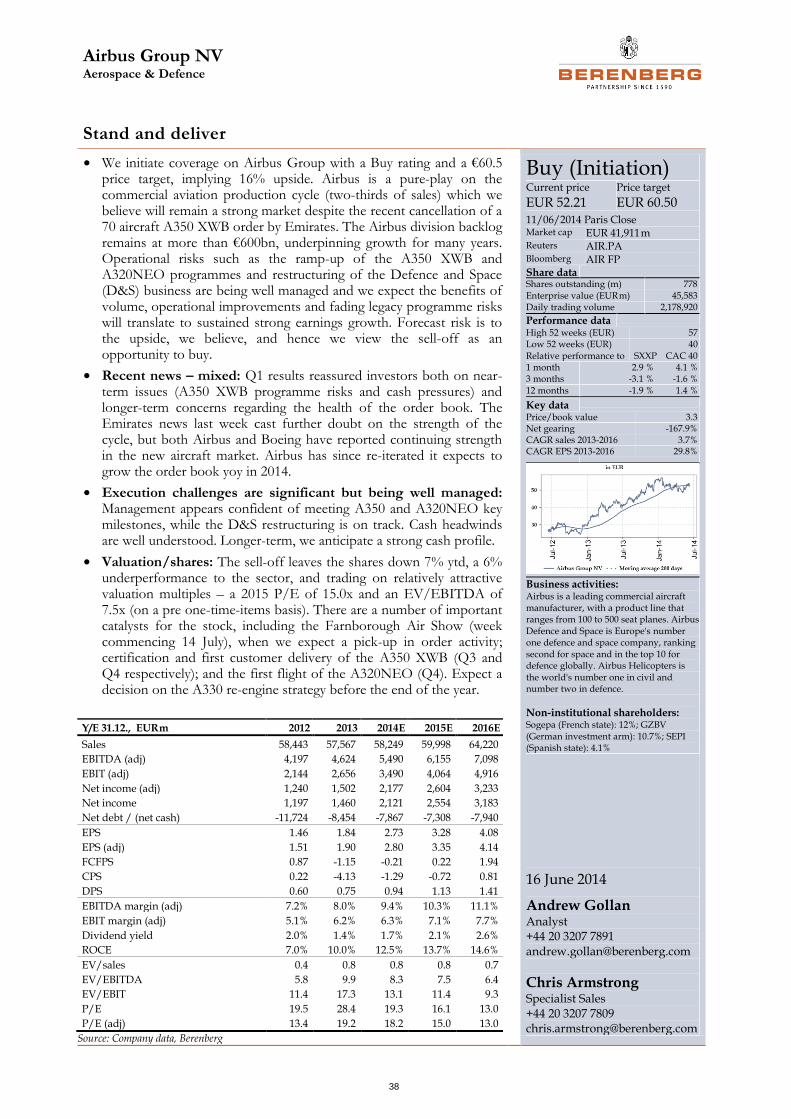

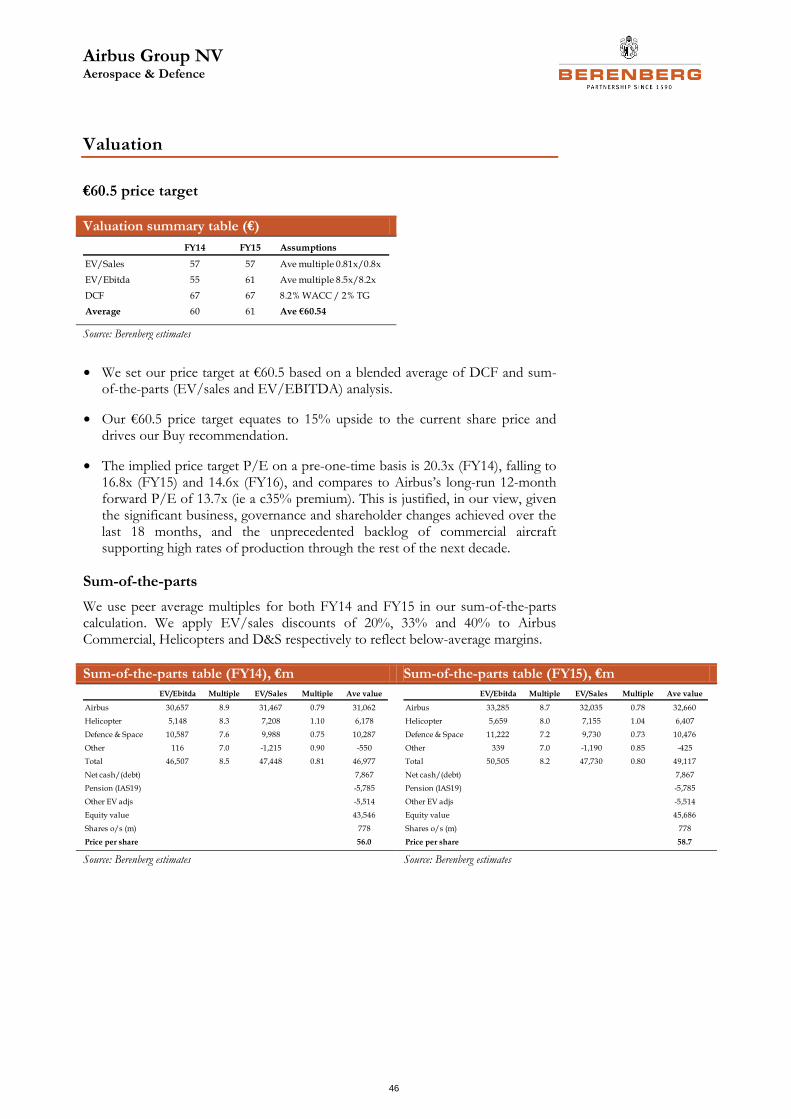

Airbus Group NV (Initiation) Buy Current Price EUR 52.21

Price Target EUR 60.50

11/06/2014 Paris Close

BAE Systems plc (Initiation) Hold Current Price GBp 426

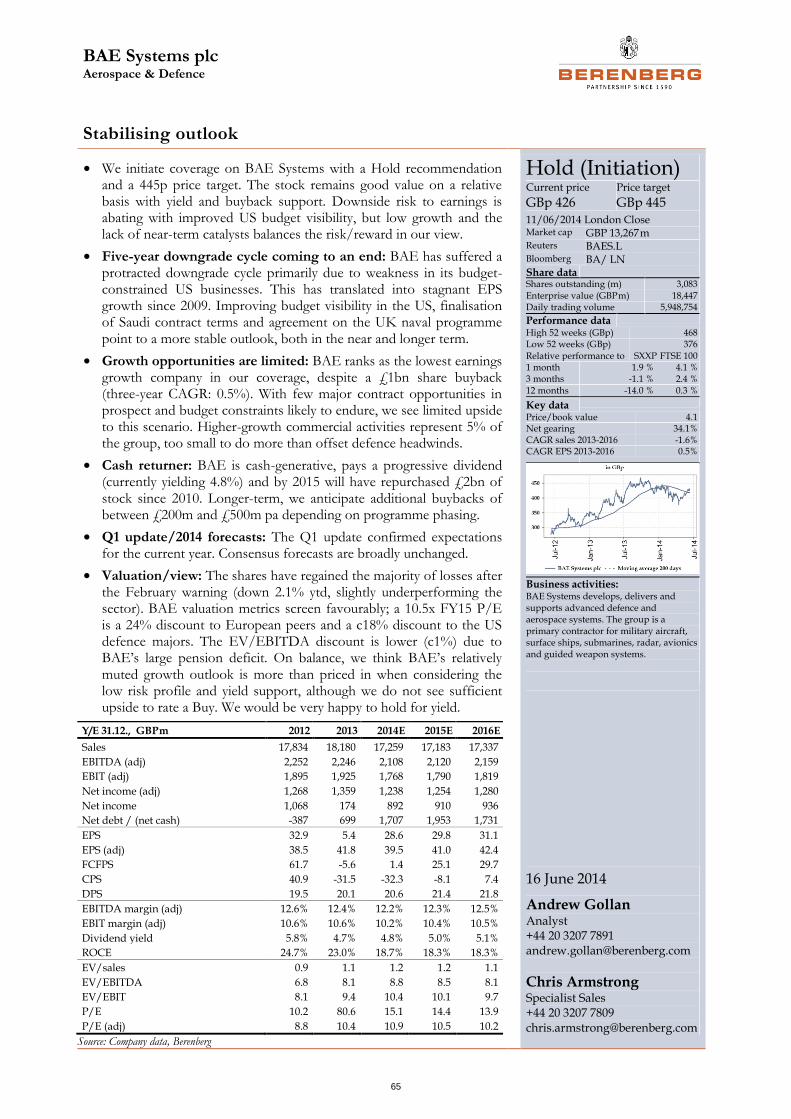

Price Target GBp 445

11/06/2014 London Close

Cobham plc (Initiation) Hold Current Price GBp 324

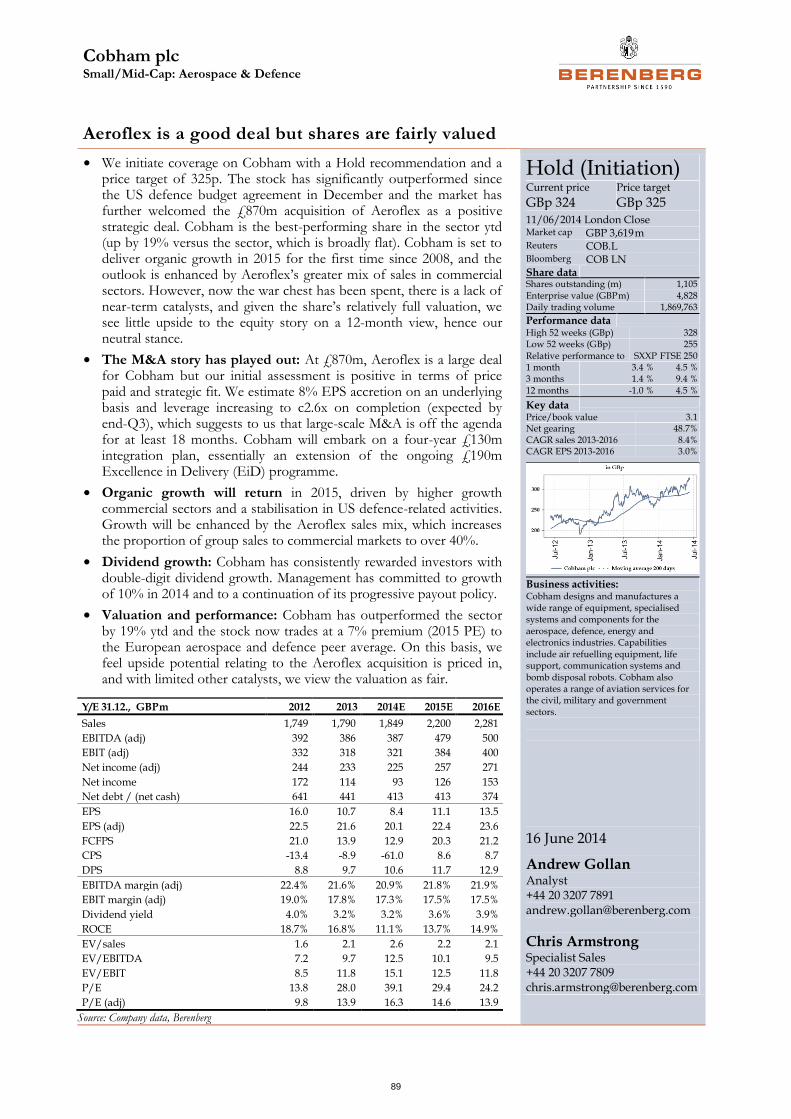

Price Target GBp 325

11/06/2014 London Close

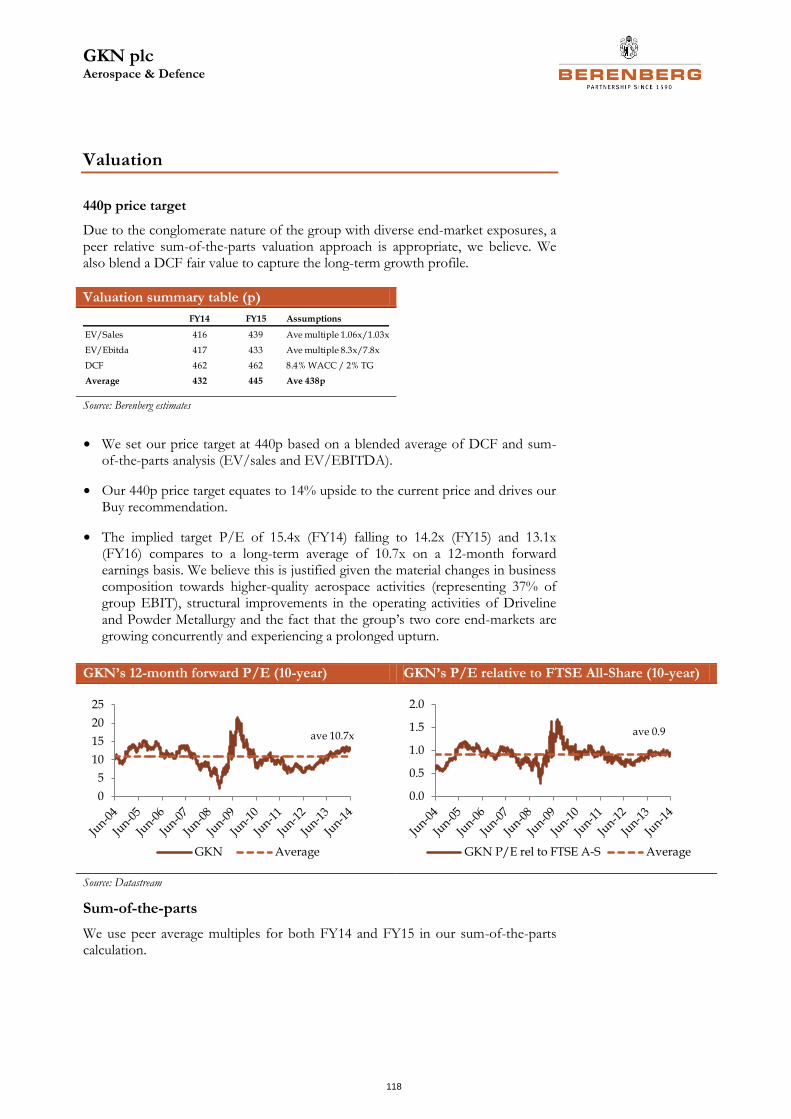

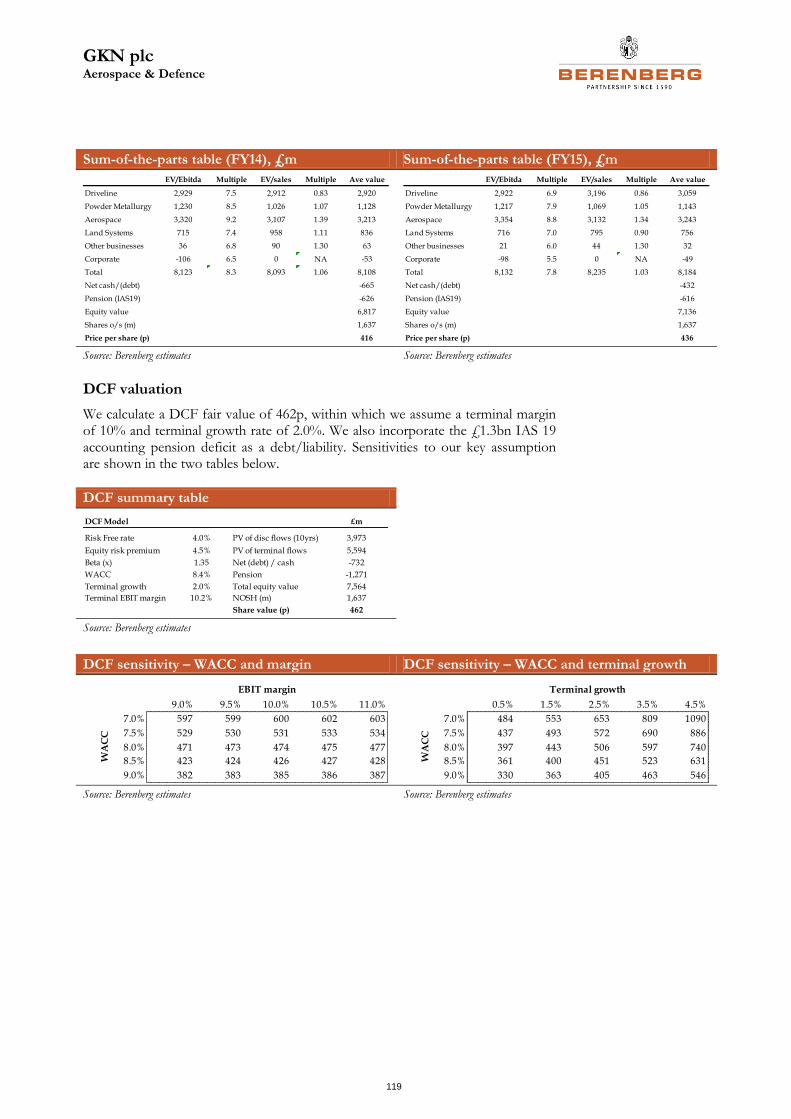

GKN plc (Initiation) Buy Current Price GBp 385

Price Target GBp 440

11/06/2014 London Close

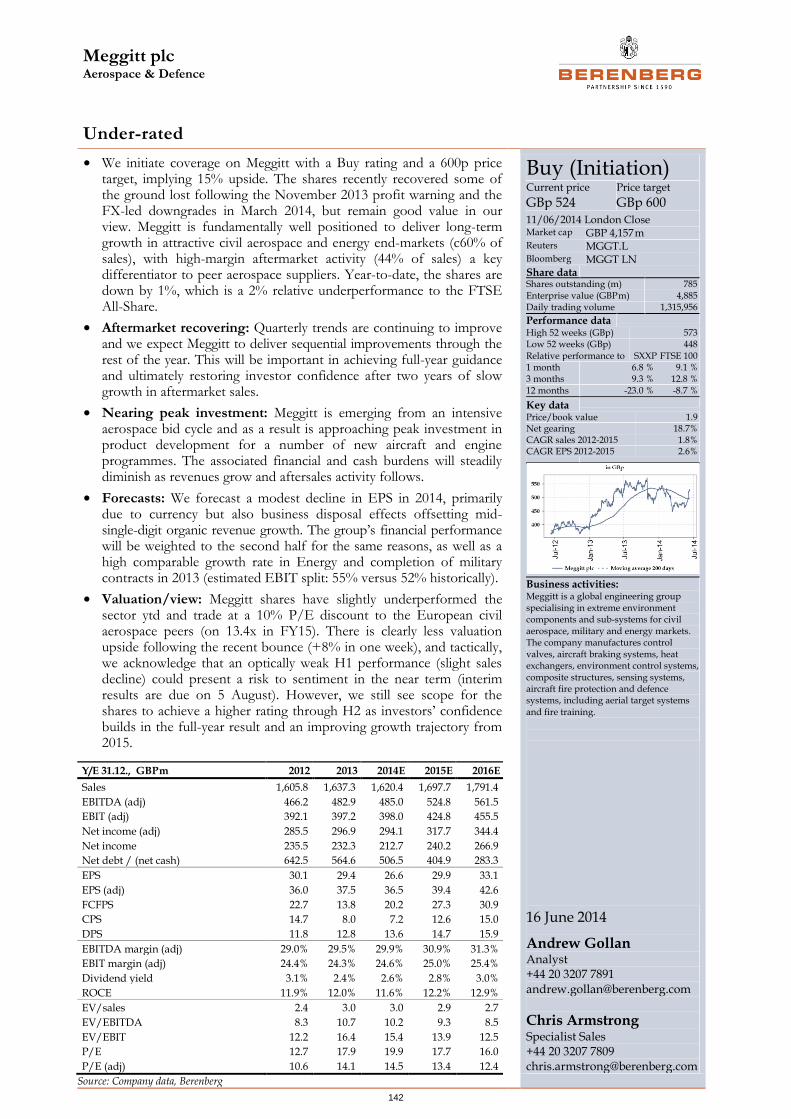

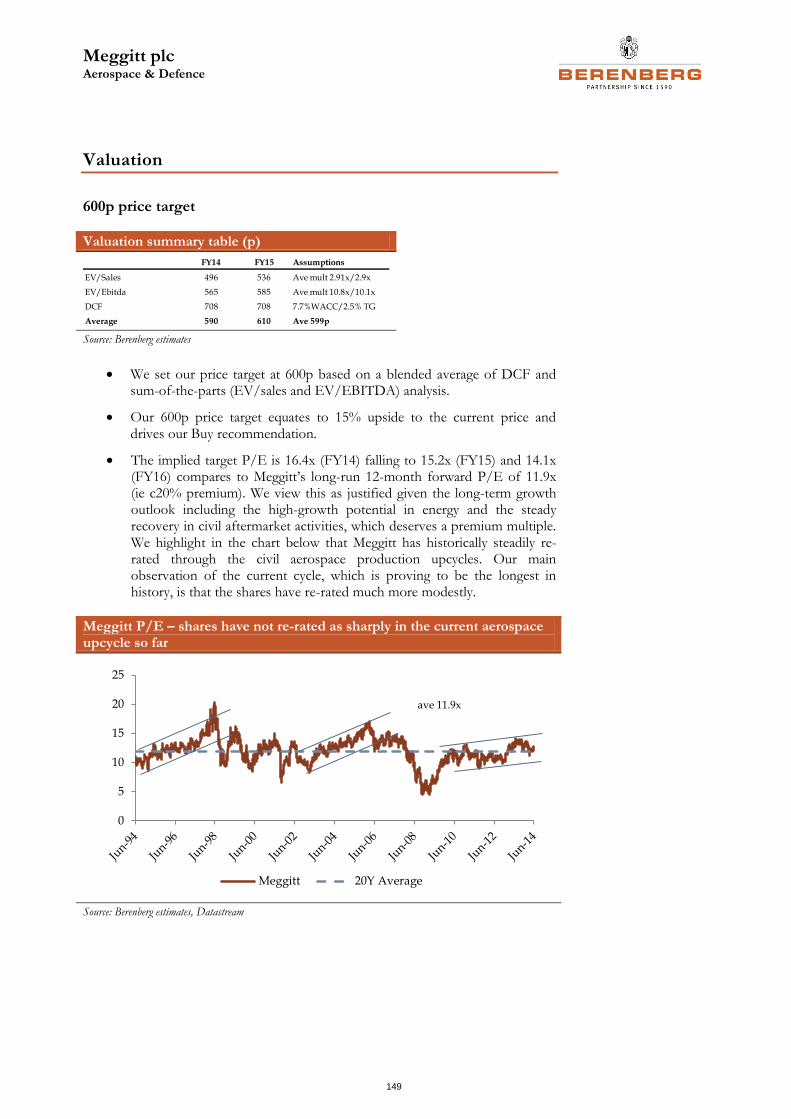

Meggitt plc (Initiation) Buy Current Price GBp 524

Price Target GBp 600

11/06/2014 London Close

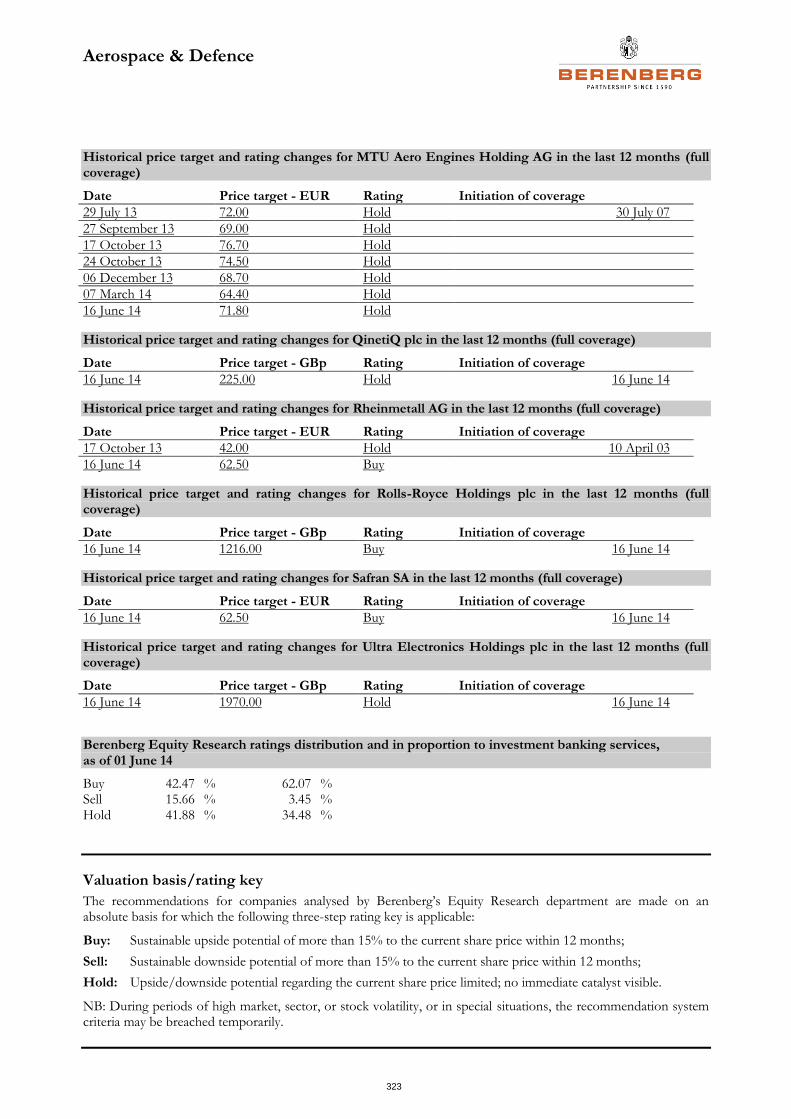

MTU Aero Engines Holding AG Hold Current Price EUR 68.33

Price Target EUR 71.80 (64.40)

11/06/2014 XETRA Close

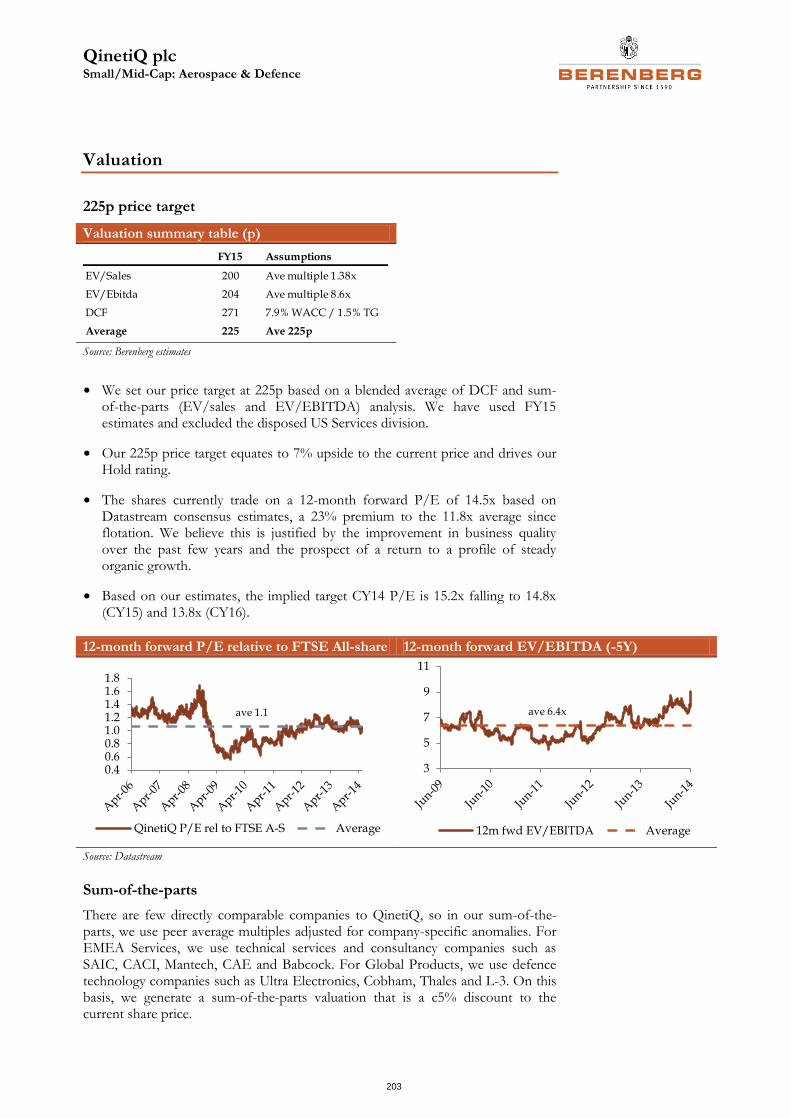

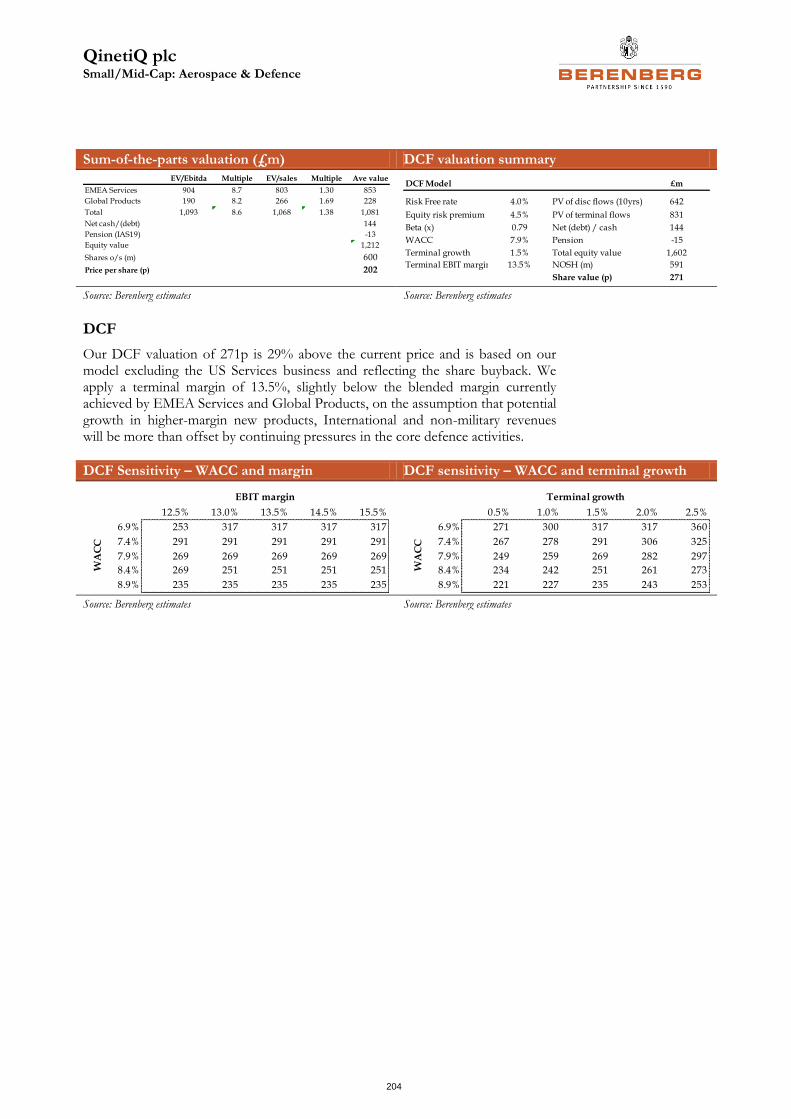

QinetiQ plc (Initiation) Hold Current Price GBp 210

Price Target GBp 225

11/06/2014 London Close

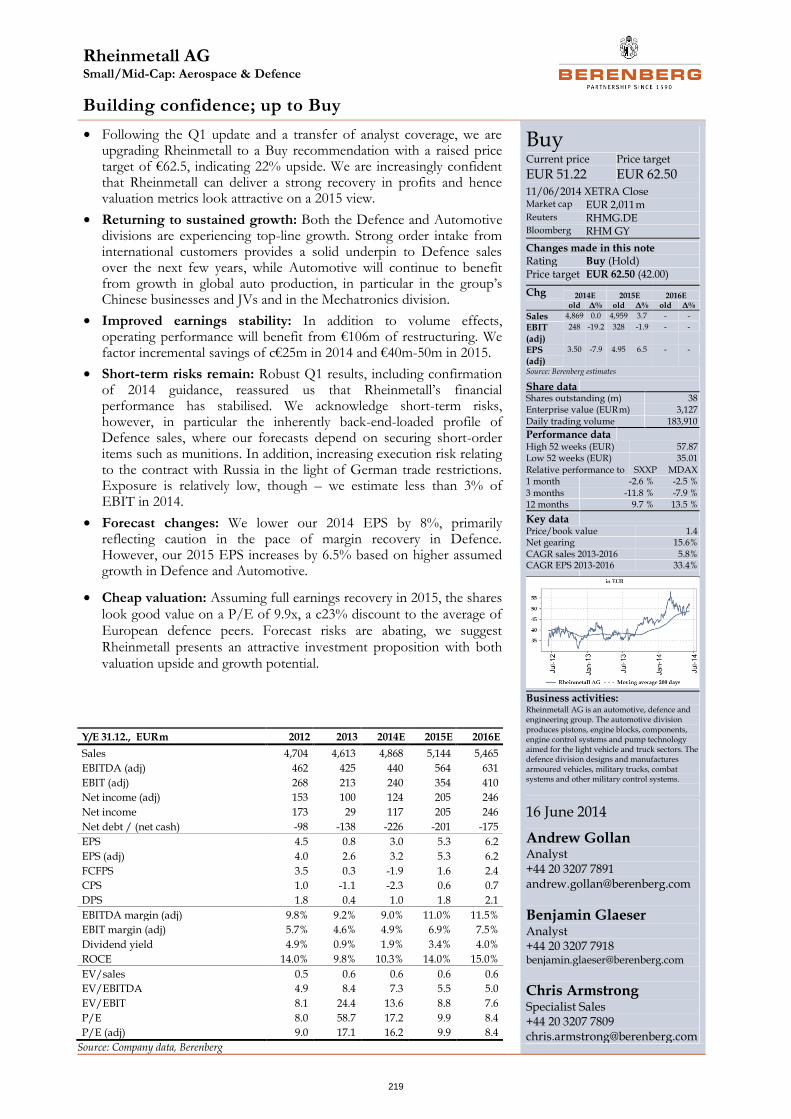

Rheinmetall AG Buy (Hold) Current Price EUR 51.22

Price Target EUR 62.50 (42.00)

11/06/2014 XETRA Close

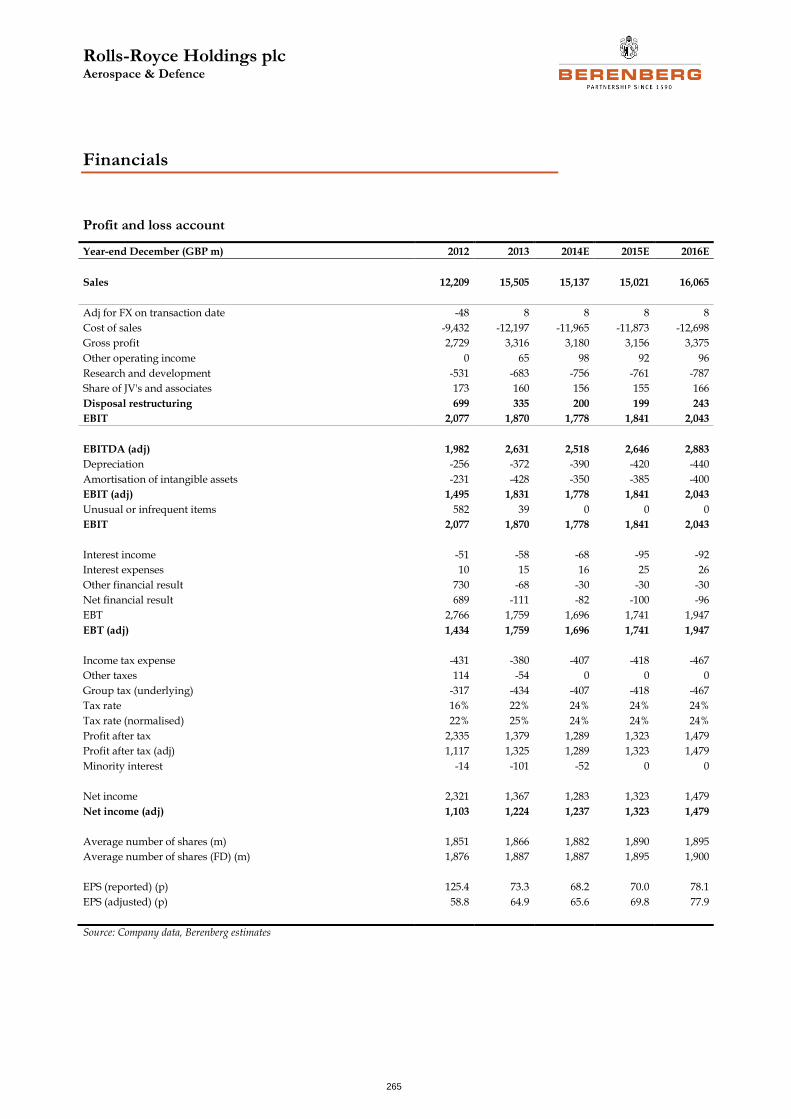

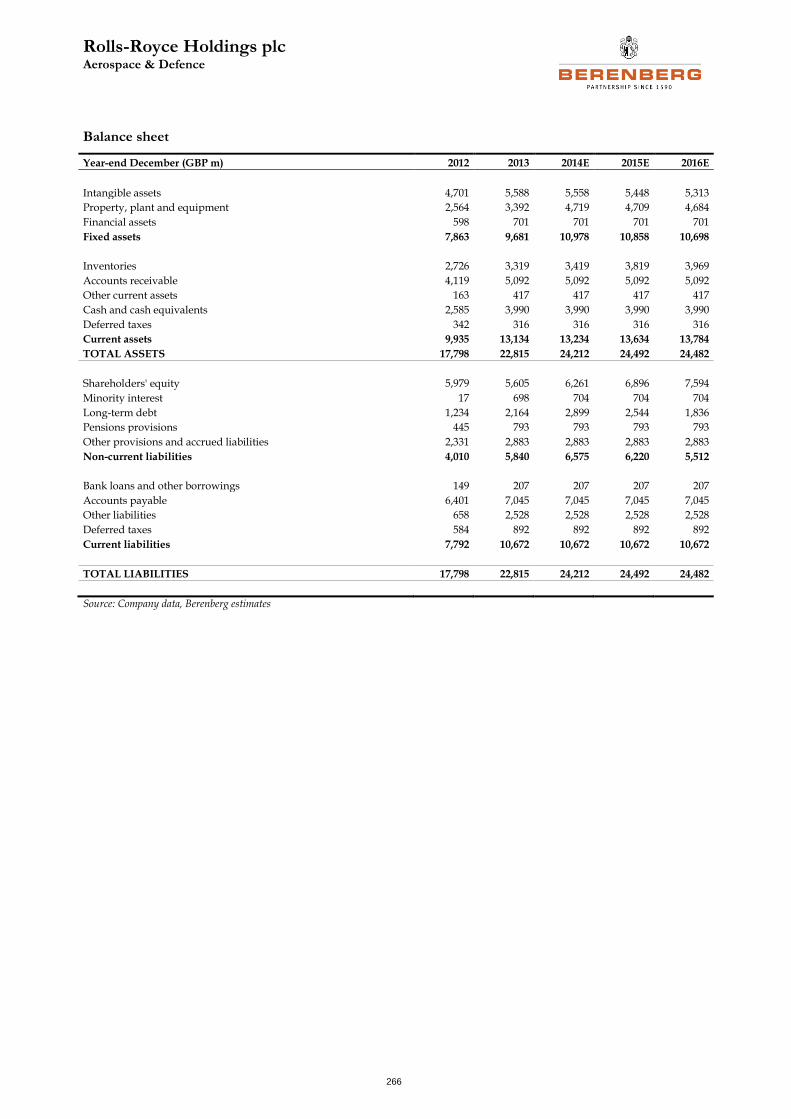

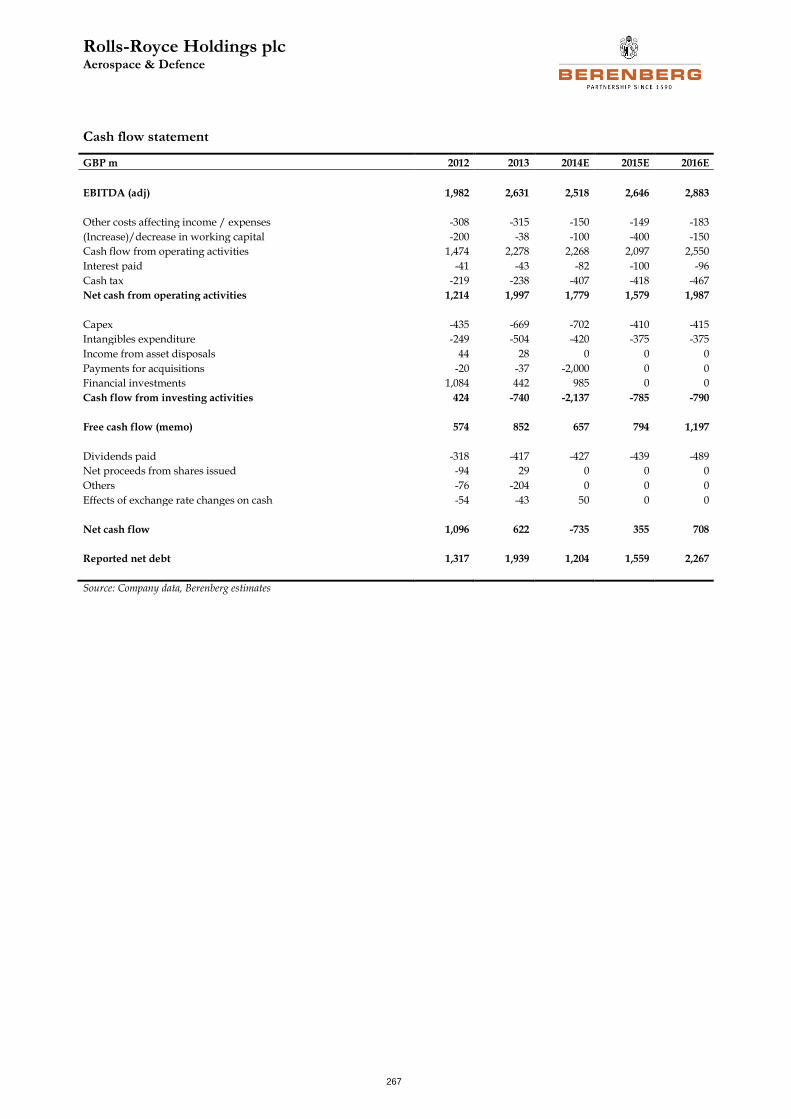

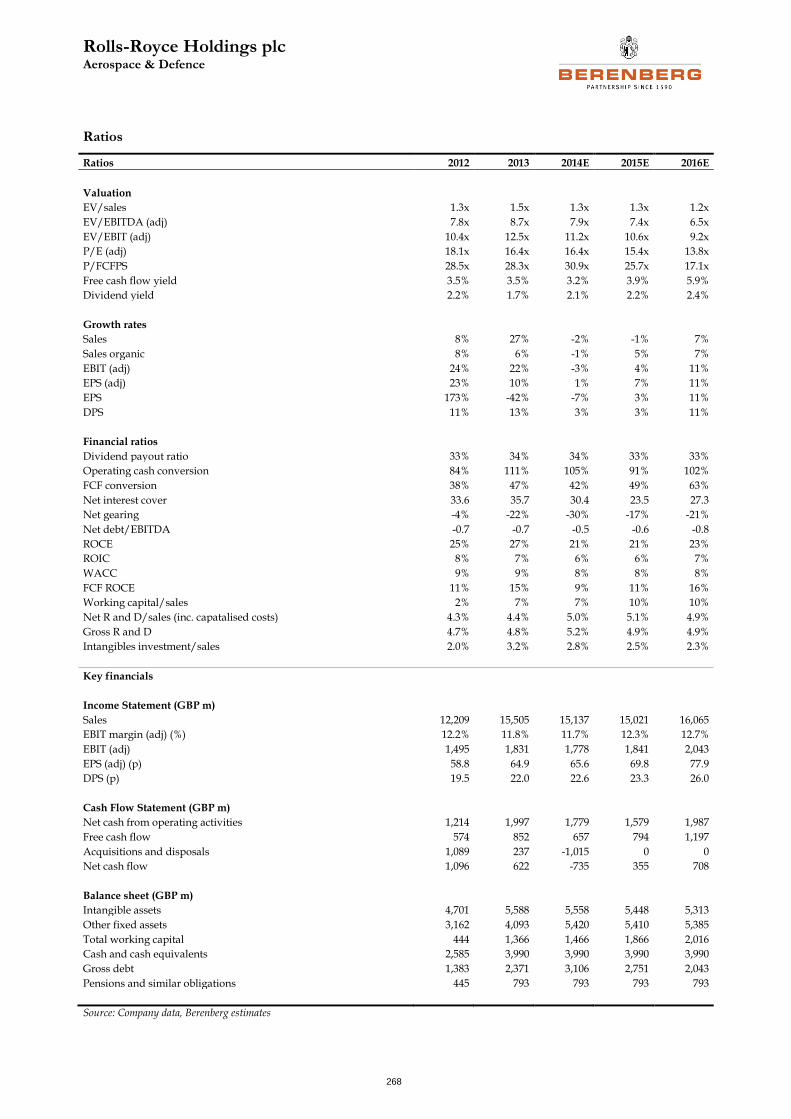

Rolls-Royce Holdings plc (Initiation) Buy Current Price GBp 1,017

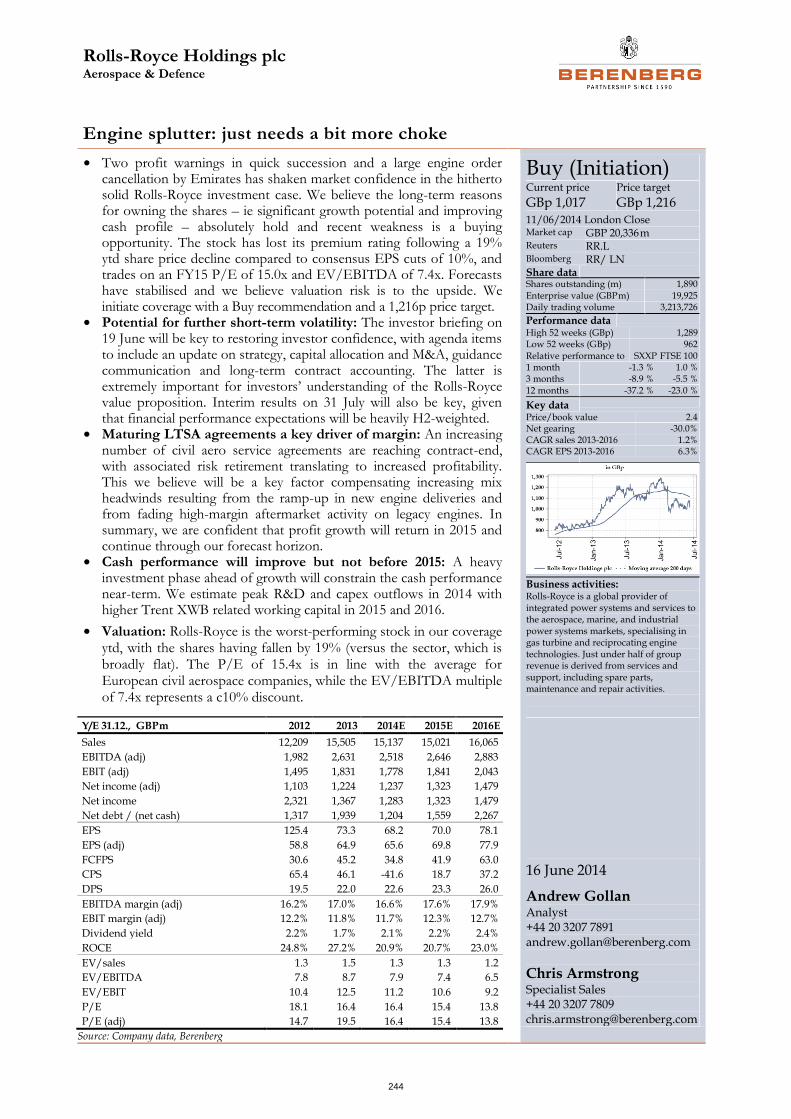

Price Target GBp 1,216

11/06/2014 London Close

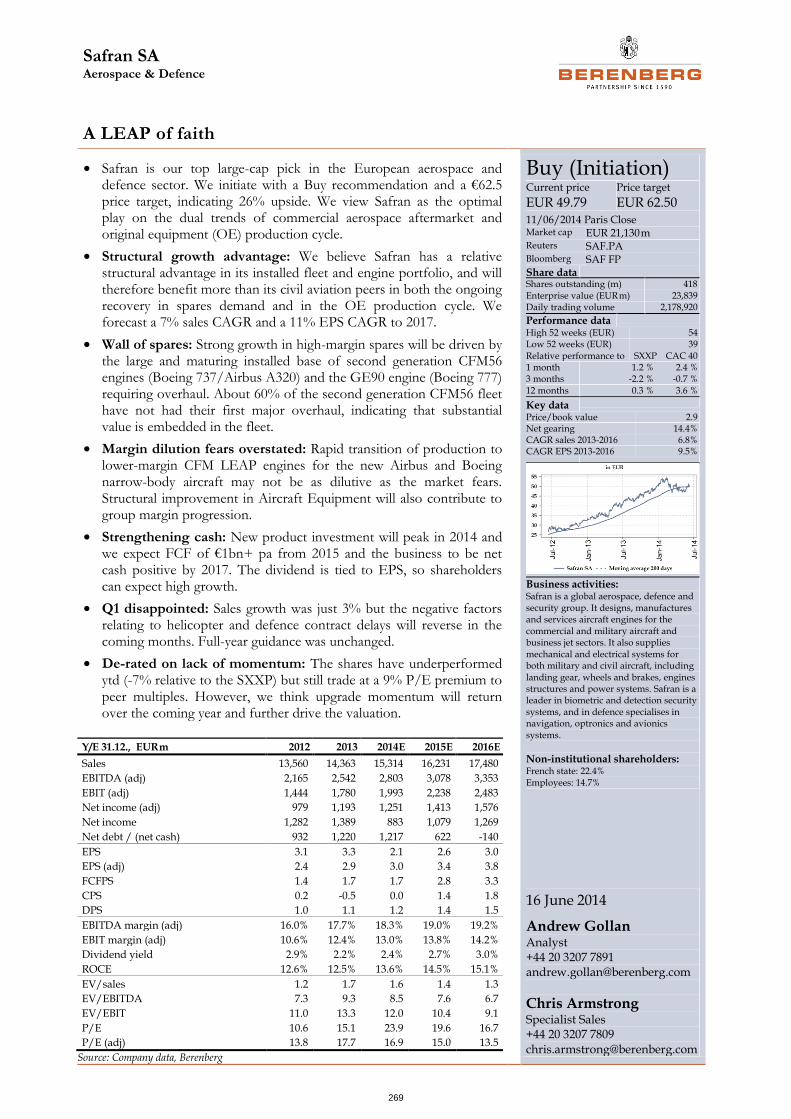

Safran SA (Initiation) Buy Current Price EUR 49.79

Price Target EUR 62.50

11/06/2014 Paris Close

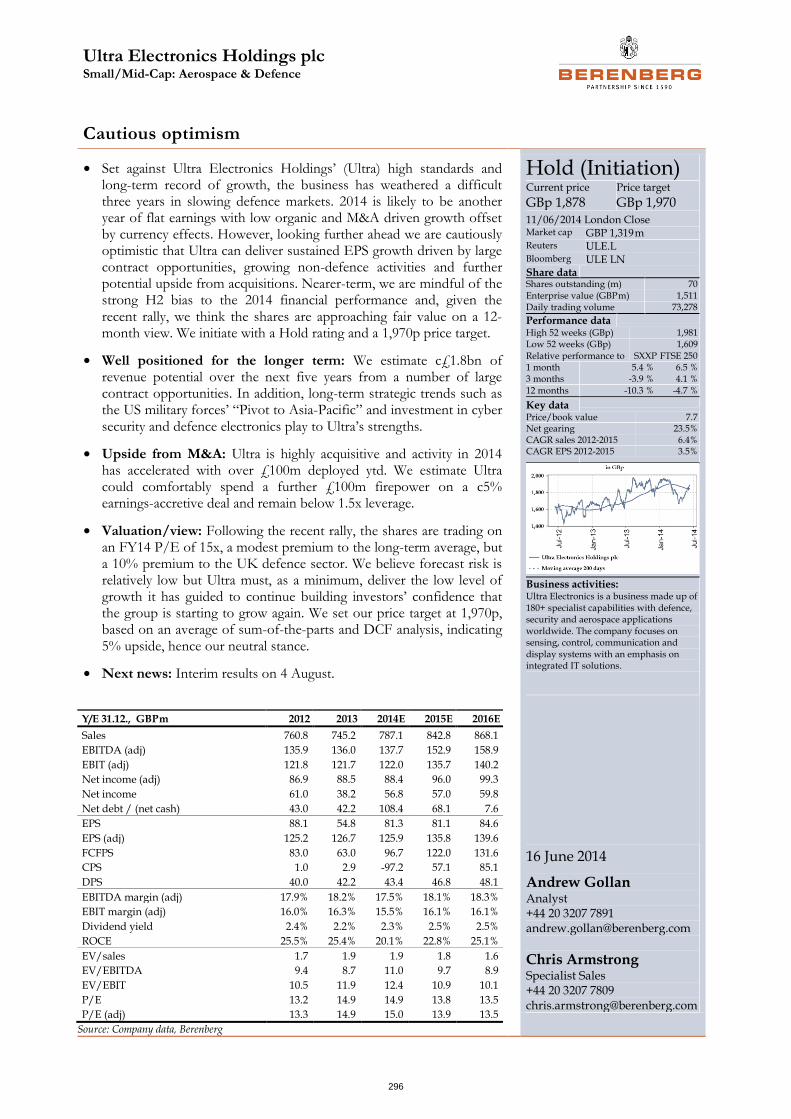

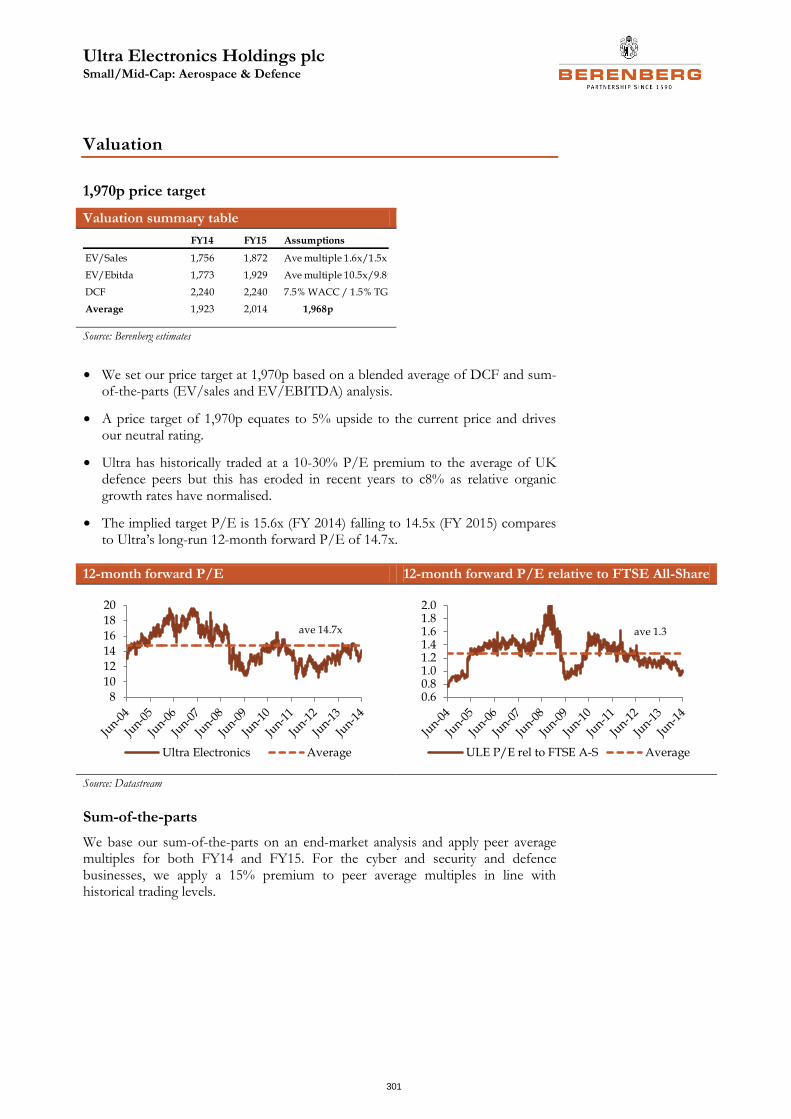

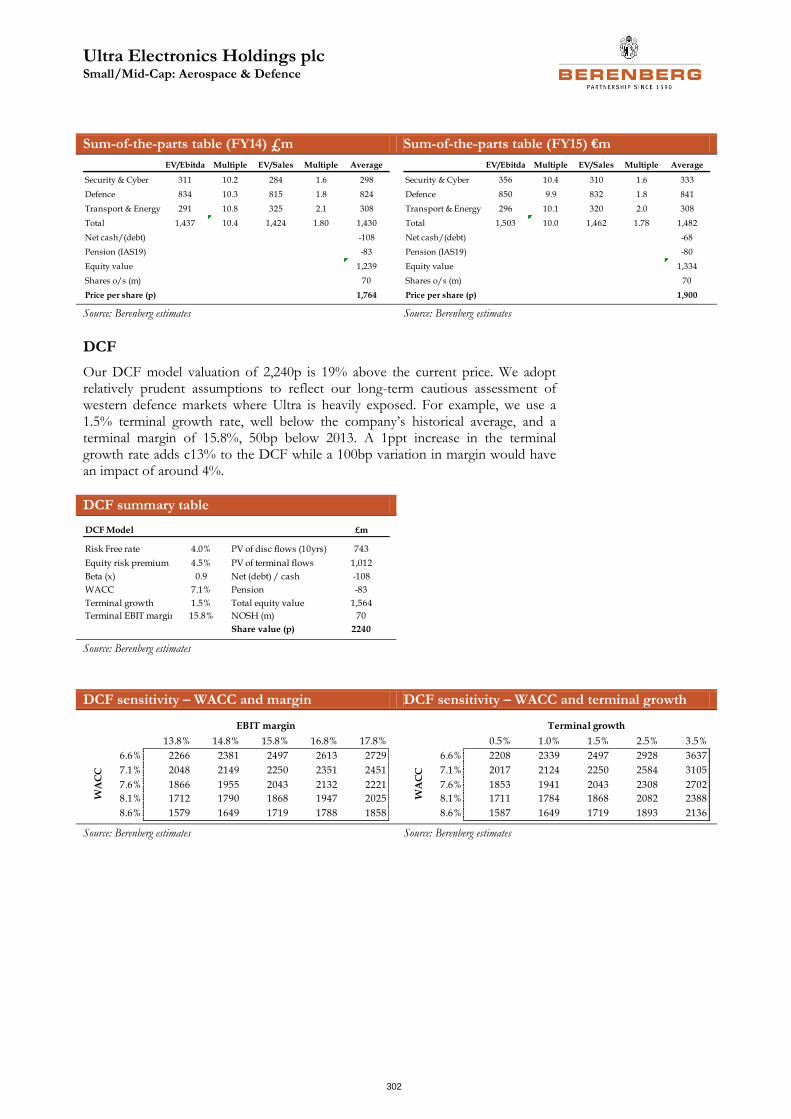

Ultra Electronics Holdings plc (Initiation) Hold

Current Price GBp 1,878

Price Target GBp 1,970

11/06/2014 London Close

16 June 2014

Andrew Gollan Analyst +44 20 3207 7891 [email protected]

Chris Armstrong

Specialist Sales +44 20 3207 7809 [email protected]

Aerospace & Defence

2

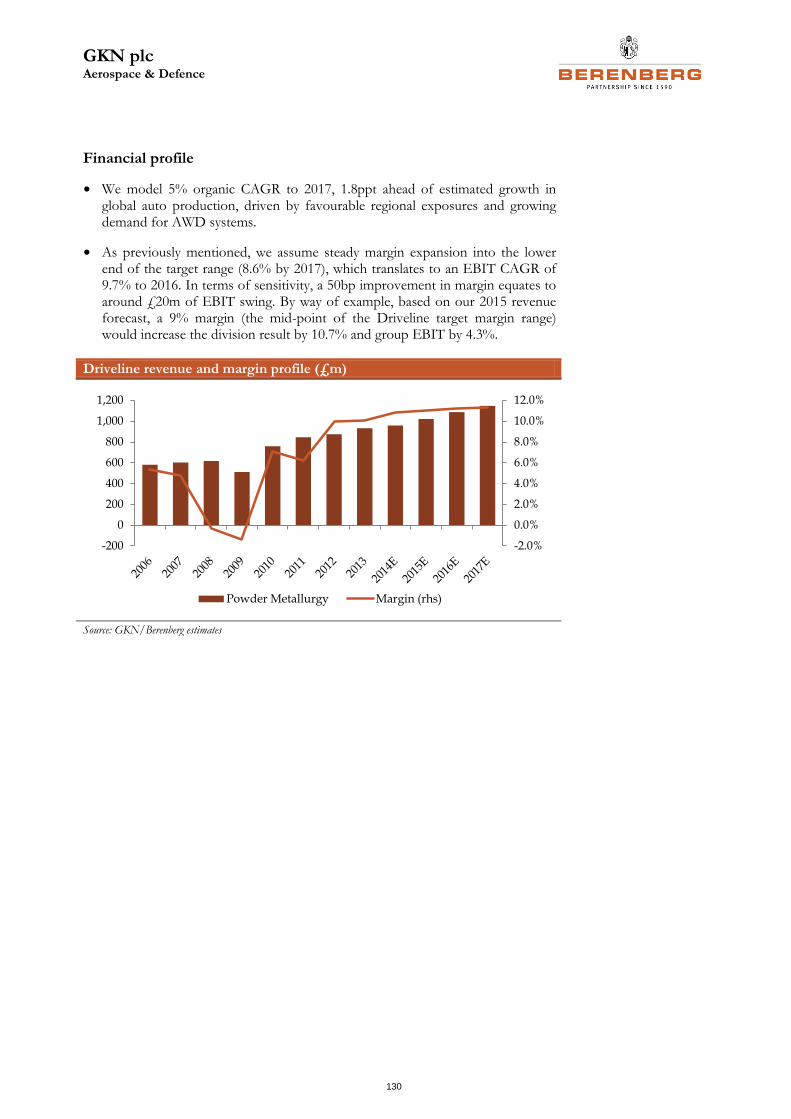

Sector overview

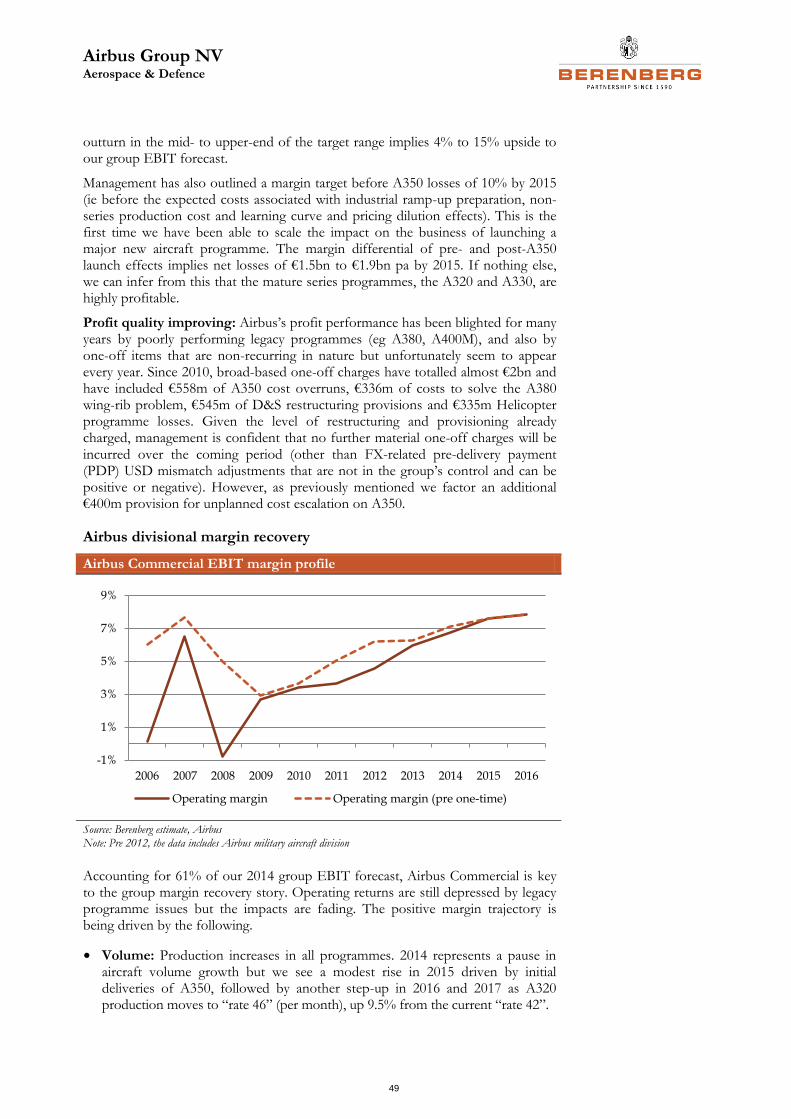

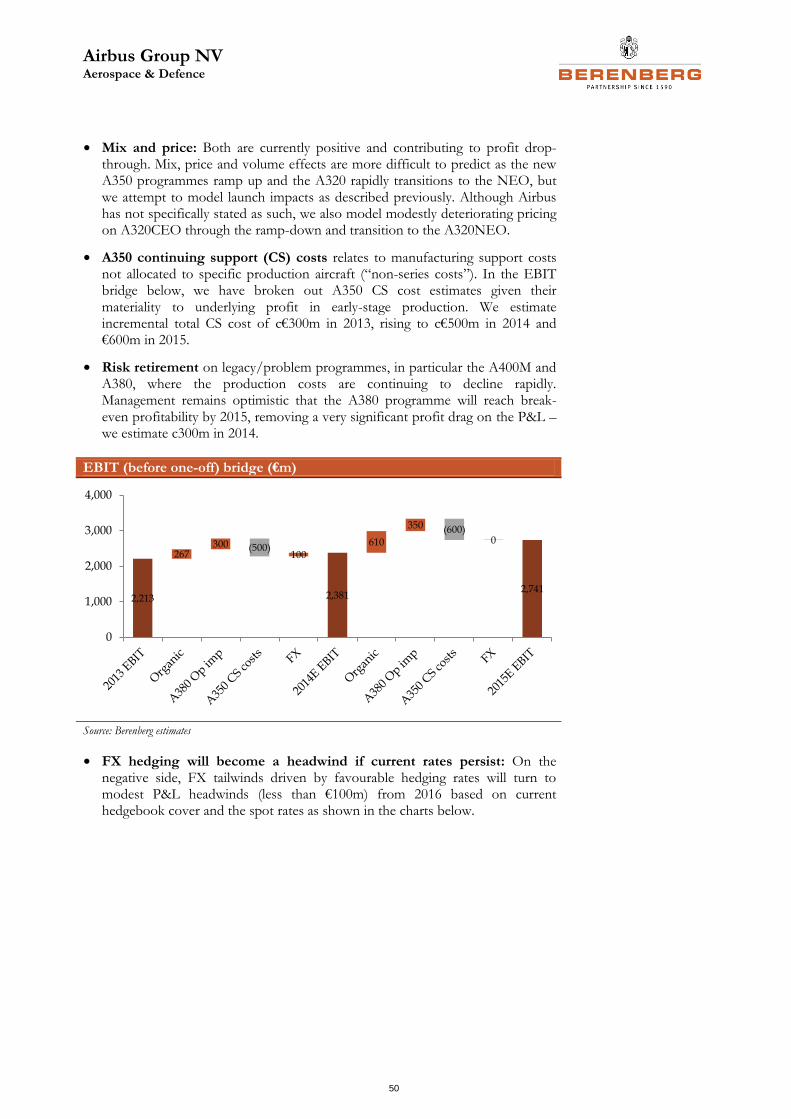

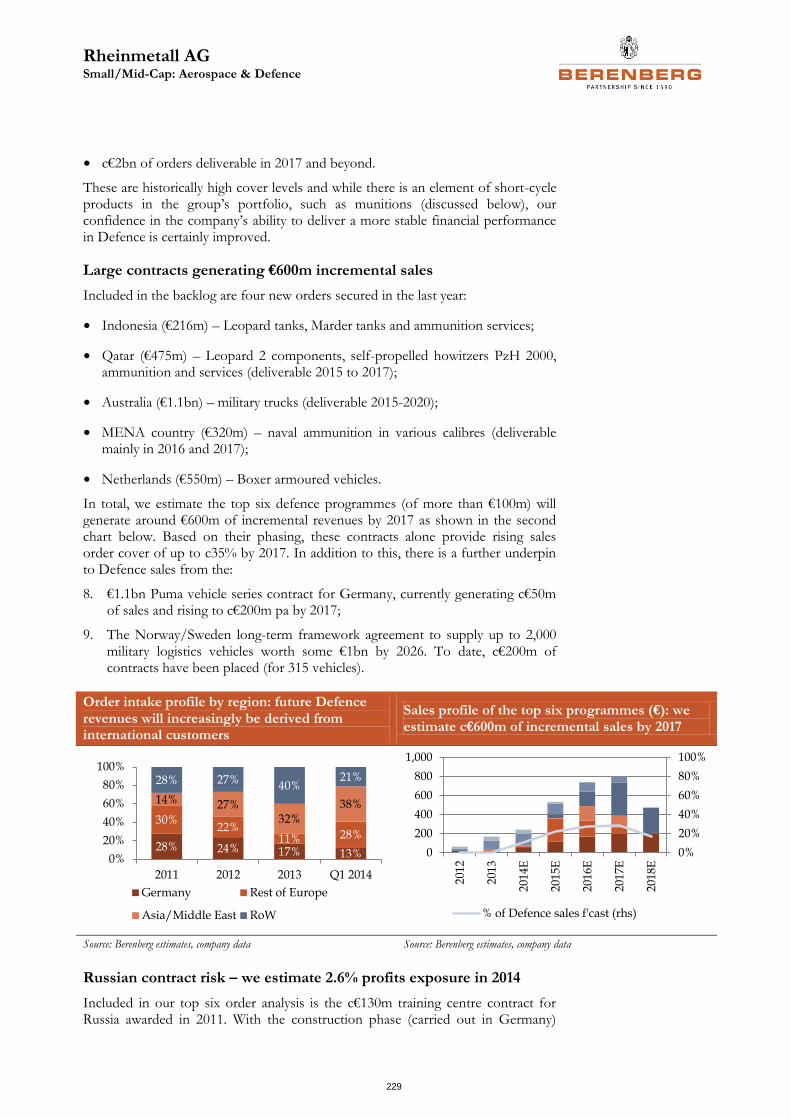

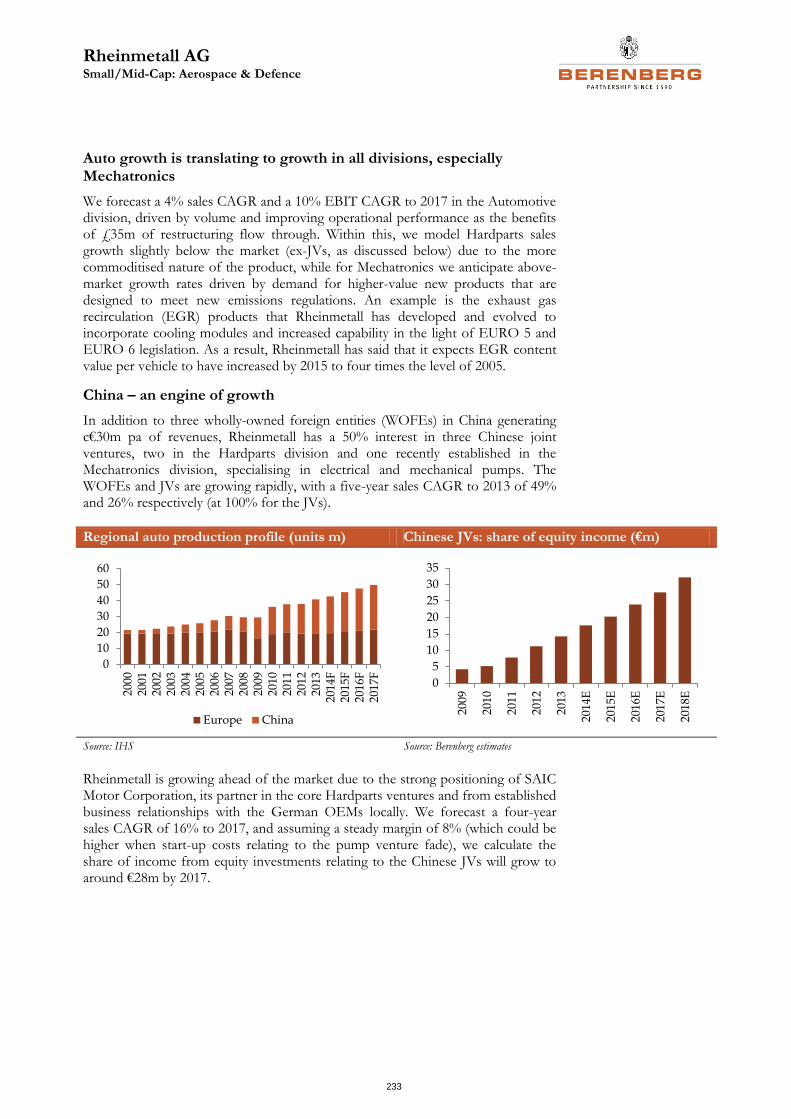

Initiating coverage on the European aerospace and defence sector

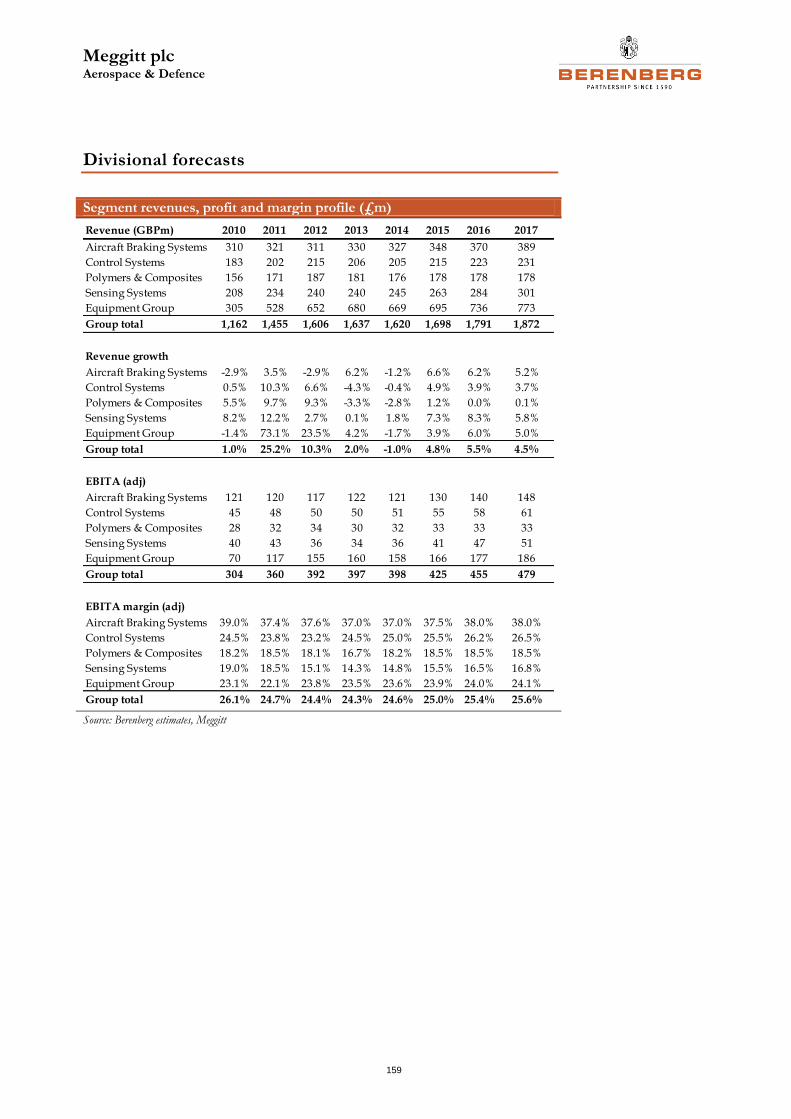

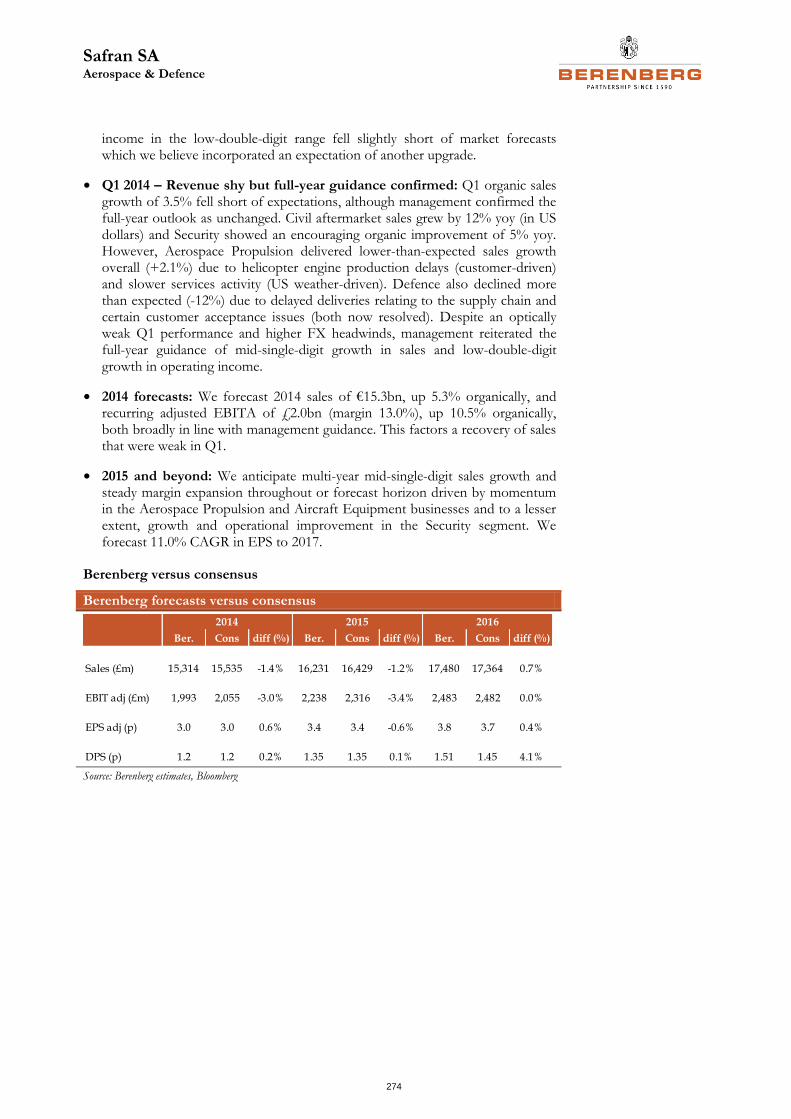

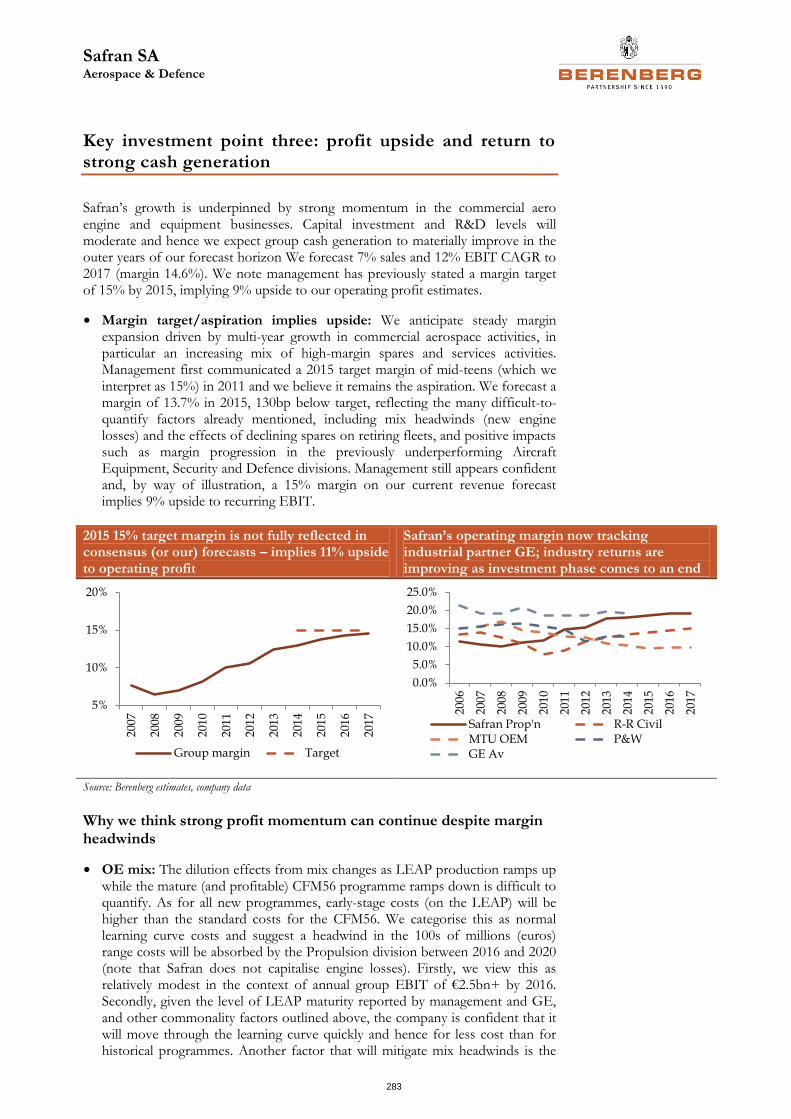

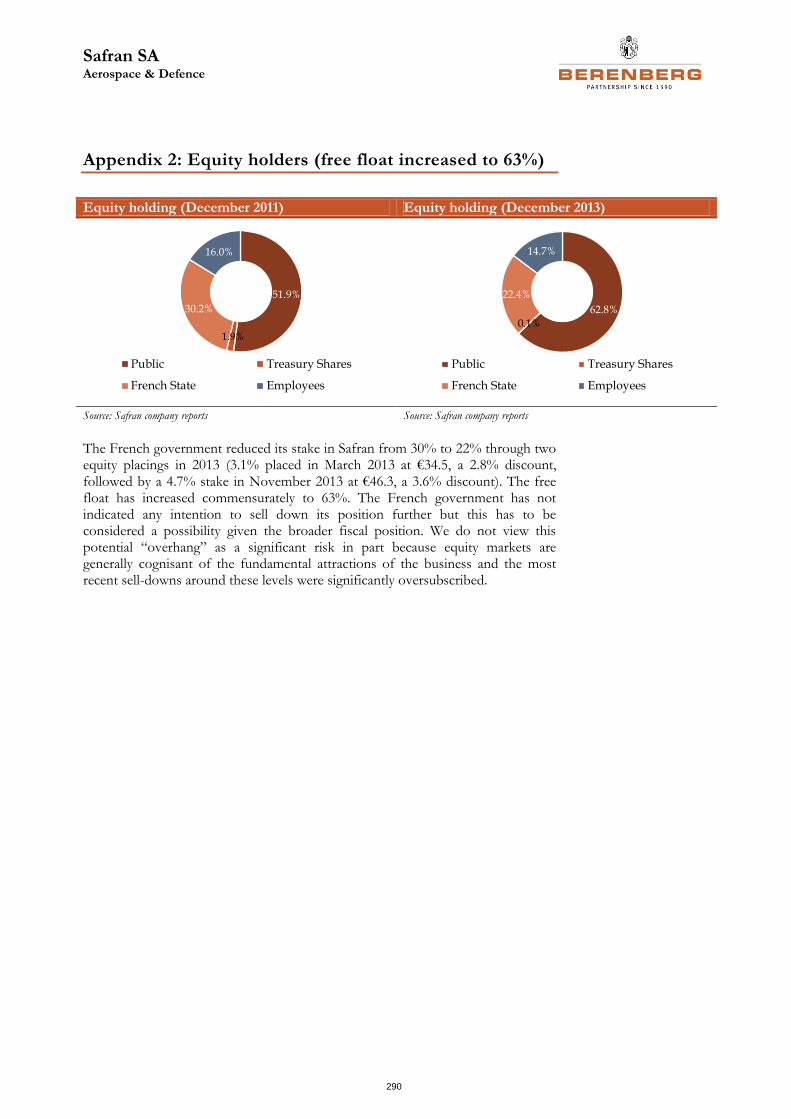

We initiate coverage on nine companies in the European aerospace and defence sector. We also include analysis of two further companies in this report, MTU Aero Engines and Rheinmetall, following a change of analyst coverage. Our key picks are Safran, Rheinmetall, Rolls-Royce, Airbus and Meggitt. We also have a Buy recommendation on GKN.

Recommendation table

Source: Berenberg estimates

Sector stance – stock selection is key

Given the diversity of the companies under coverage, we make our recommendations on an individual stock selection basis. However, if we assess our initiations based purely on the number of Buy recommendations our sector stance is positive with a slight bias towards civil aerospace facing companies. The civil growth story is well understood, but central to our Buy calls is an assumption that companies (and the industry) will execute profitably on various new aircraft and engine programmes entering production. Defence stocks have universally re-rated over the past 12 months, linked mainly to the improving US budget environment. We have no Sell recommendations because we believe both earnings and valuation risk is low given the relatively supportive macro environments.

We summarise our key picks below.

● Safran, price target €62.5 – the optimal play on the dual trends of the commercial aerospace aftermarket recovery and the aircraft production cycle: Safran’s engine fleet profile has a relative structural advantage compared to its peers that will drive continuous growth in high-margin spares. Temporary shortfalls compared to Q1 expectations masked strong underlying momentum that will become apparent in H2 and beyond.

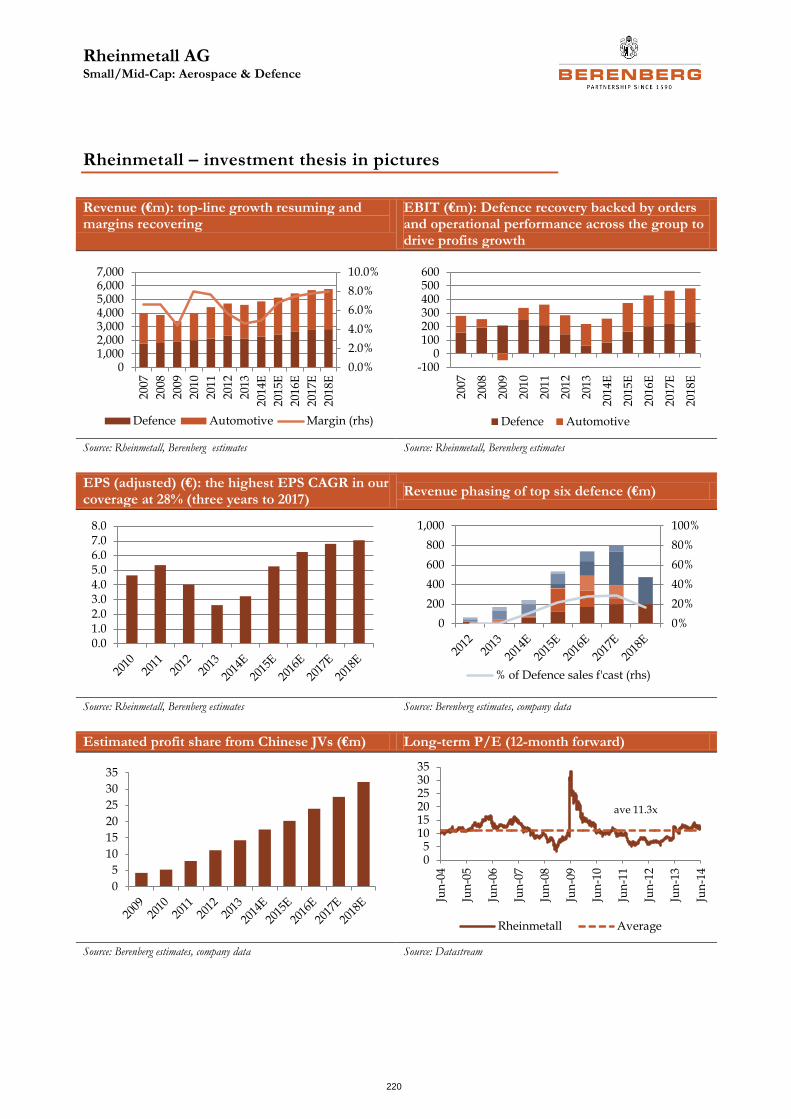

● Rheinmetall, price target €62.5 – on a strong recovery path: Both divisions are in growth mode with high revenue visibility in the Defence segment from large multi-year international orders, while the Automotive segment is benefiting from favourable end-market demand. Assuming management

Company Curr. RatingPrice

Target

Current

Price

Upside /

(Downside)P/E (CY15)

EPS CAGR

(3yr)

Airbus Group EUR Buy 60.5 52.2 15.9% 15.0 29.8%

BAE Systems GBp Hold 445.0 425.8 4.5% 10.5 0.5%

Cobham GBp Hold 325.0 323.9 0.3% 14.6 3.0%

GKN GBp Buy 440.0 384.9 14.3% 12.6 5.9%

Meggitt GBp Buy 600.0 524.0 14.5% 13.4 4.3%

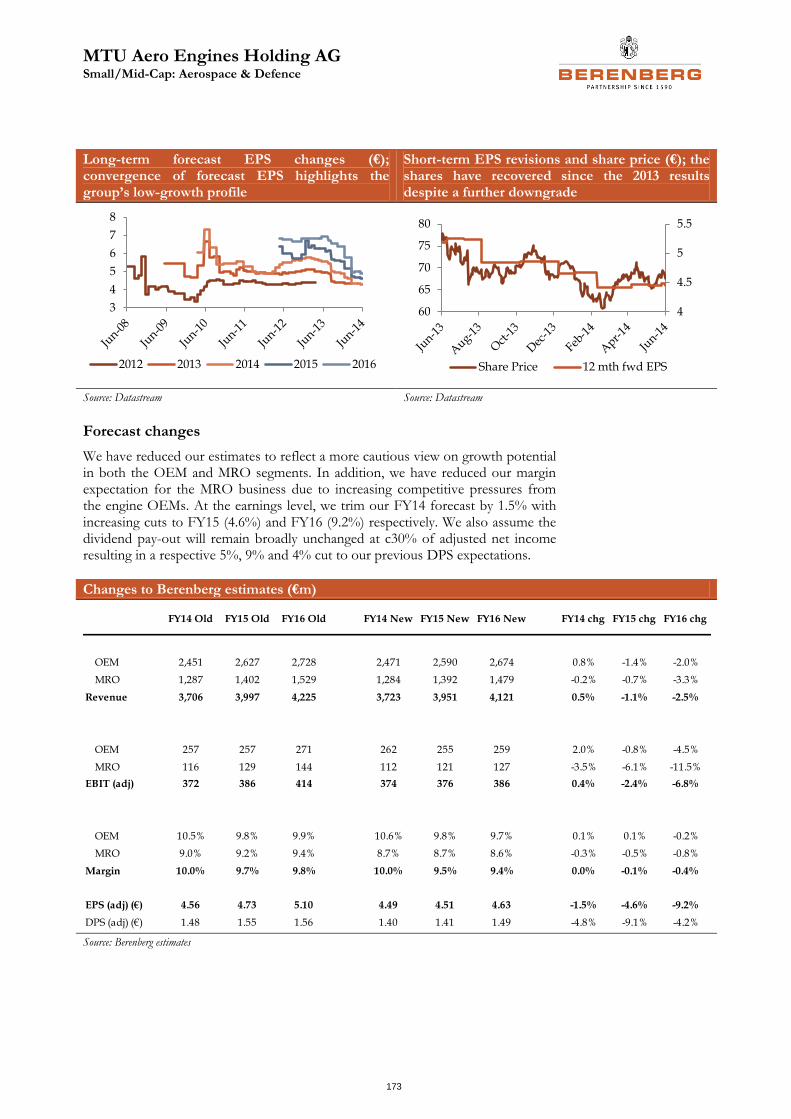

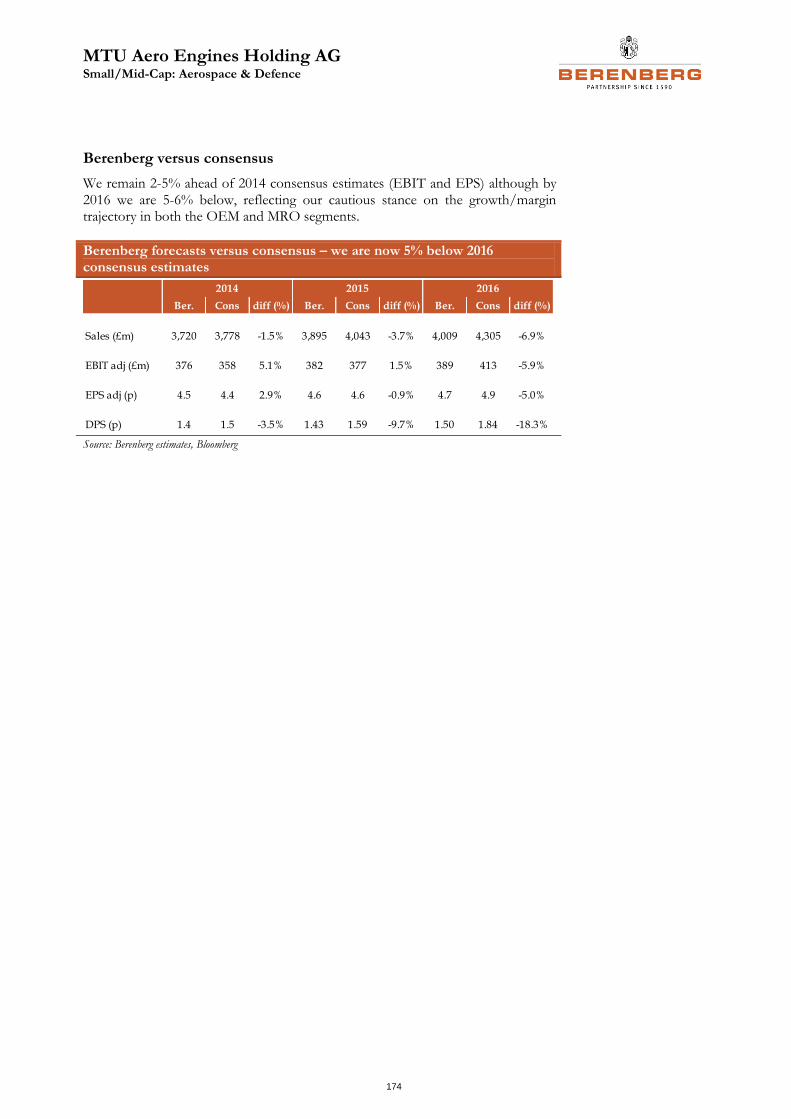

MTU Aero Engines EUR Hold 71.8 68.3 5.1% 15.2 0.8%

QinetiQ GBp Hold 225.0 210.0 7.1% 13.8 1.0%

Rheinmetall EUR Buy 62.5 51.2 22.0% 9.9 33.4%

Rolls-Royce GBp Buy 1216.0 1017.0 19.6% 15.4 6.3%

Safran EUR Buy 62.5 49.8 25.5% 15.0 9.5%

Ultra Electronics GBp Hold 1970.0 1878.0 4.9% 13.9 3.3%

Aerospace & Defence

3

continues to deliver against its mid-term “Two-Pillar” strategy, Rheinmetall ranks as the highest EPS growth and lowest P/E stock in our coverage.

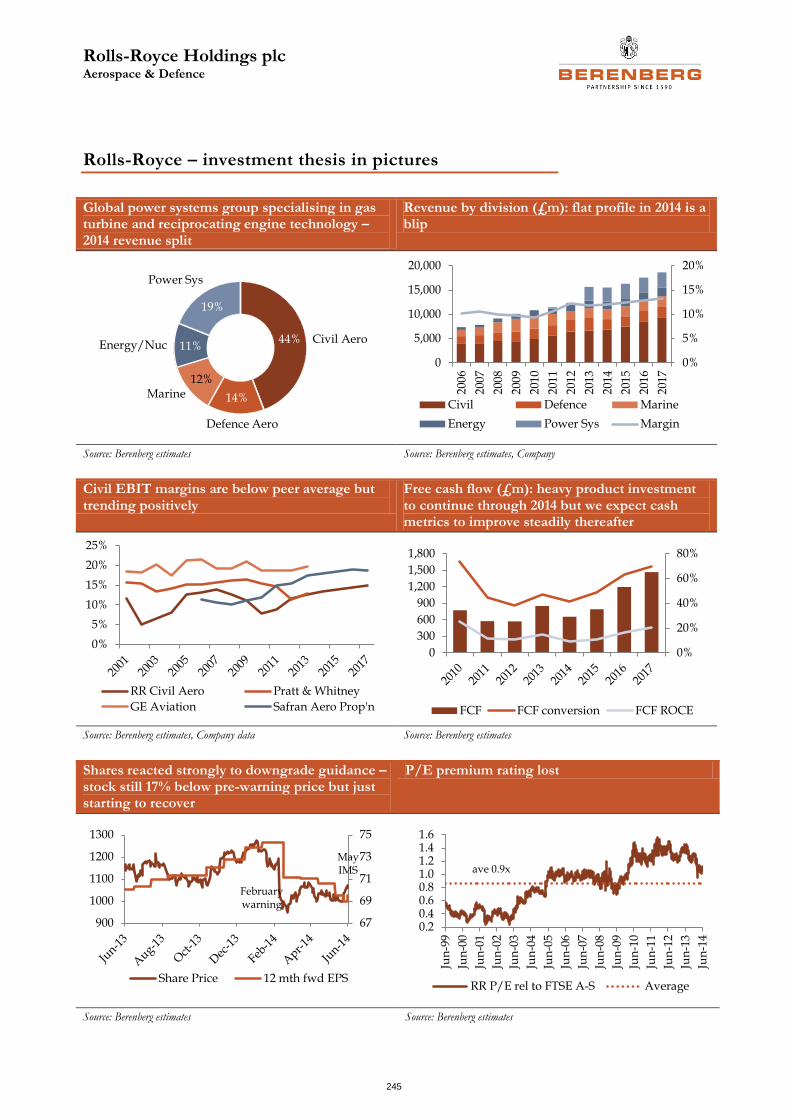

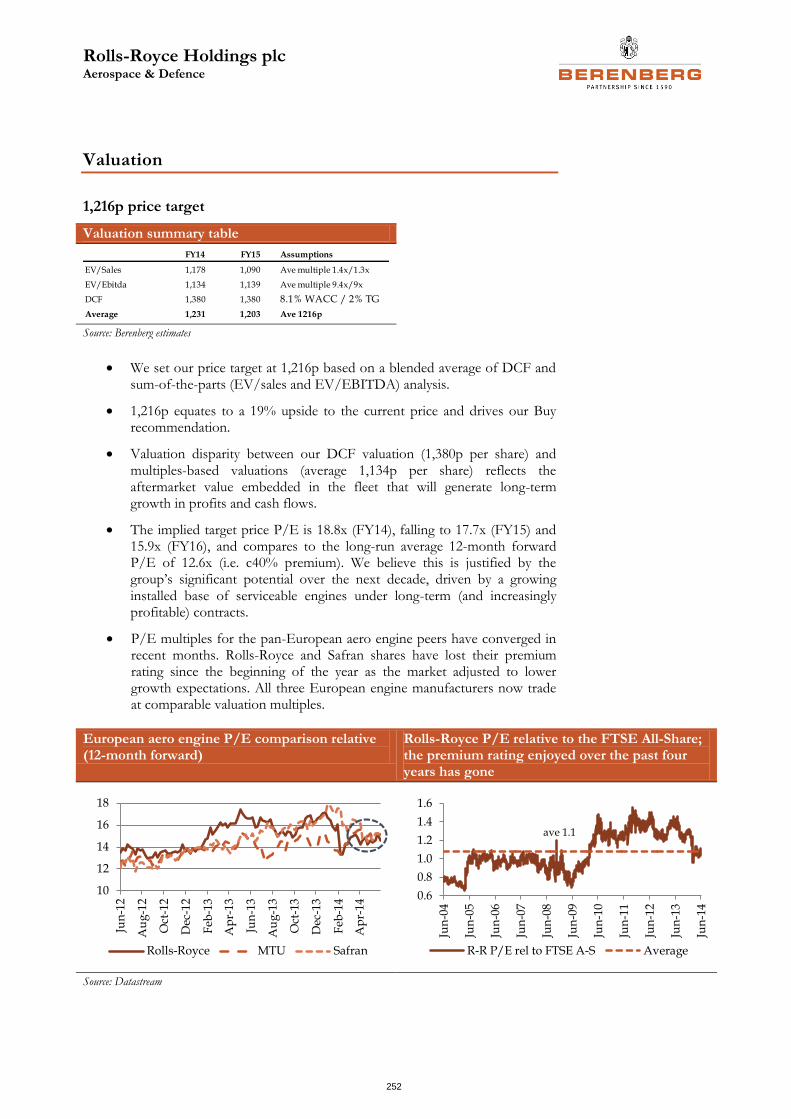

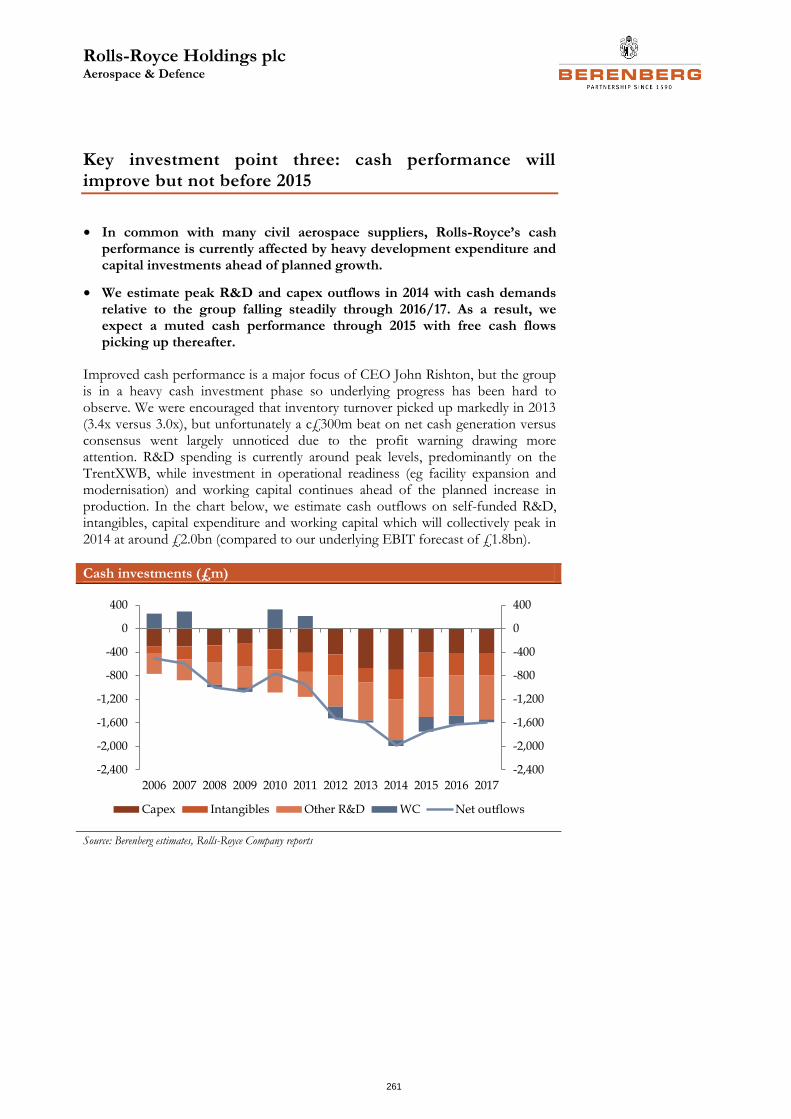

● Rolls-Royce, price target 1,216p – out of favour following two profit warnings and the Emirates order cancellation: The shares are down by 19% ytd compared to 11% consensus earnings downgrades. We see no structural issues to detract from the long-term growth and margin expansion story, and we expect investor confidence to steadily rebuild through the year. A crucial investor briefing event is to be held on 19 June.

● Airbus, price target €60.5 – strong earnings growth driven by margin expansion as legacy headwinds fade and programme risks diminish: The market has over-reacted to the Emirates order cancellation; the shares have underperformed the SXXP by 12% ytd. There is potential for progressively positive newsflow through H2, such as A350 XWB certification and first customer delivery (in Q3 and Q4 respectively), and order announcements at the Farnborough Air Show (week commencing 14 July).

● Meggitt, price target 600p – well positioned in attractive end-markets (civil aerospace and energy) translating to sustained earnings growth in the mid- to high single-digit range: 48% of sales are derived from high-margin aftermarket activity, which is a key differentiator. Investor interest is starting to return after the November 2013 profit warning, which was caused largely by one-off events. We see scope for valuation multiples to expand if positive aftermarket trends continue.

A few sector observations

The (really) big picture

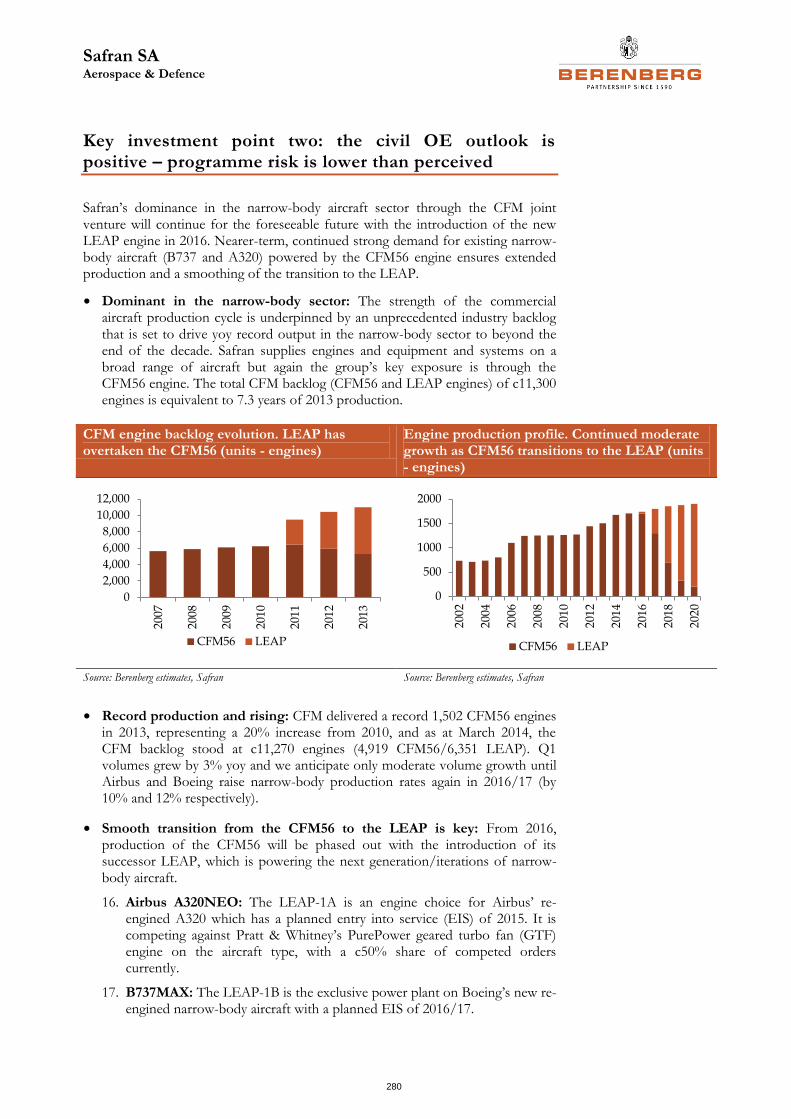

● Civil aerospace: We estimate the commercial jet liner market will increase by almost 50% by 2020 to c$130bn, equivalent to a revenue CAGR of 5.7%, driven by planned production increases by Boeing and Airbus in both their narrow-body programmes and a continued ramp-up in new wide-body programmes such as the 787 and the A350 XWB. The launch and ramp-up of a multitude of new aircraft and aero engine programmes increases risk. Execution is key. We examine the outlook for the commercial aerospace sector in detail on pages 20 to 27.

● Defence: Global defence spending is flat-lining with higher growth regions such as Asia and the Middle East offset by declines in the budgets of Western/developed nations. The outlook for the defence industry is much improved, however, now that the US budget environment has stabilised (representing c34% of the global market). Headwinds are moderating in this, the most important defence market for the industry, and for the first time in several years the manufacturers are looking tentatively towards organic growth scenarios. We examine the outlook for the defence sector in detail on pages 28 to 32.

Aerospace & Defence

4

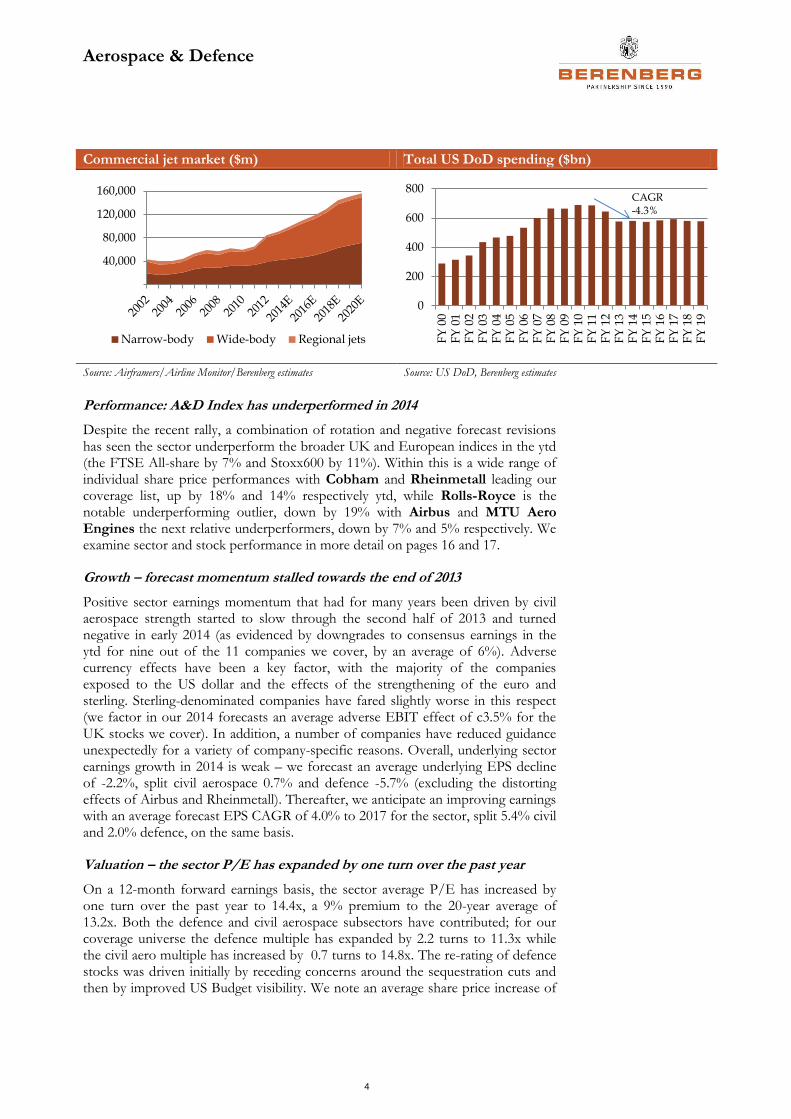

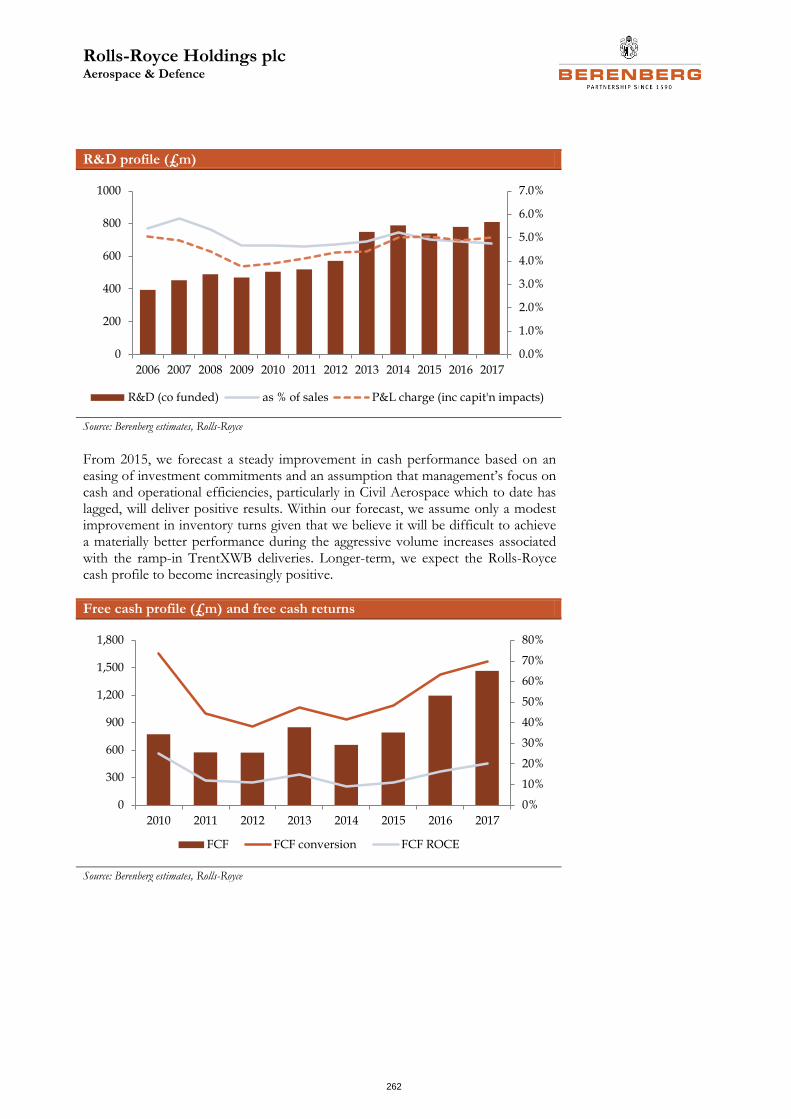

Commercial jet market ($m) Total US DoD spending ($bn)

Source: Airframers/Airline Monitor/Berenberg estimates Source: US DoD, Berenberg estimates

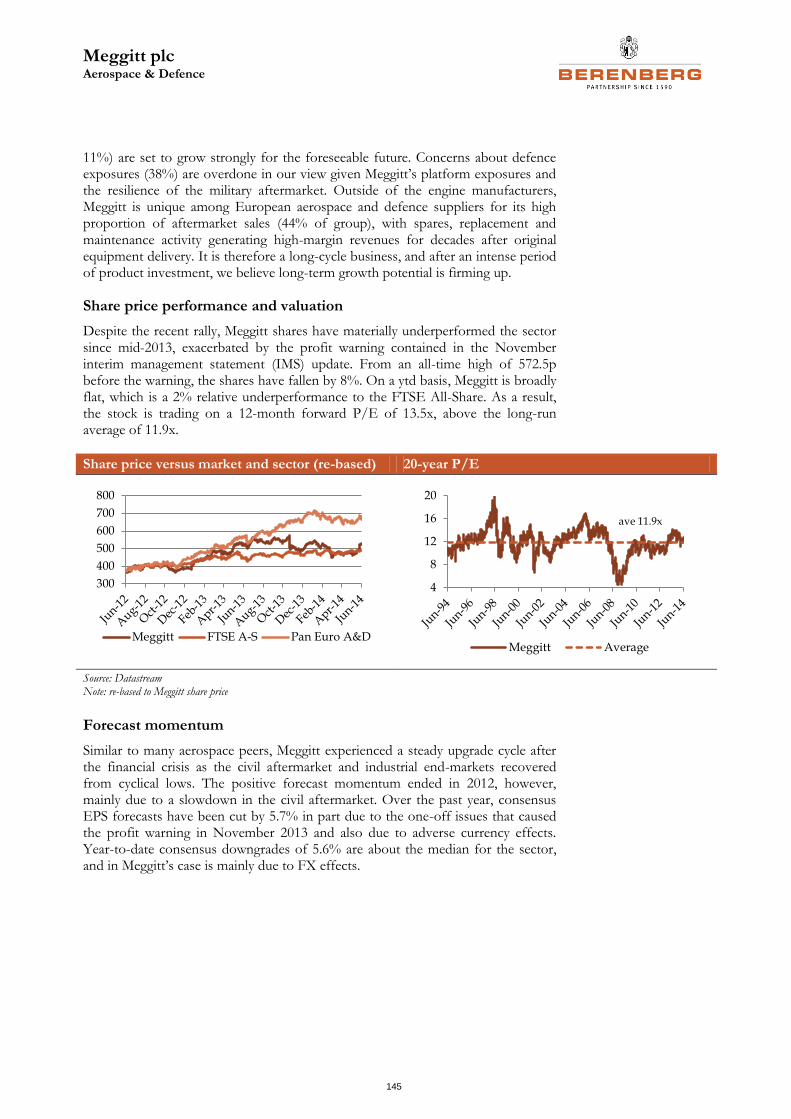

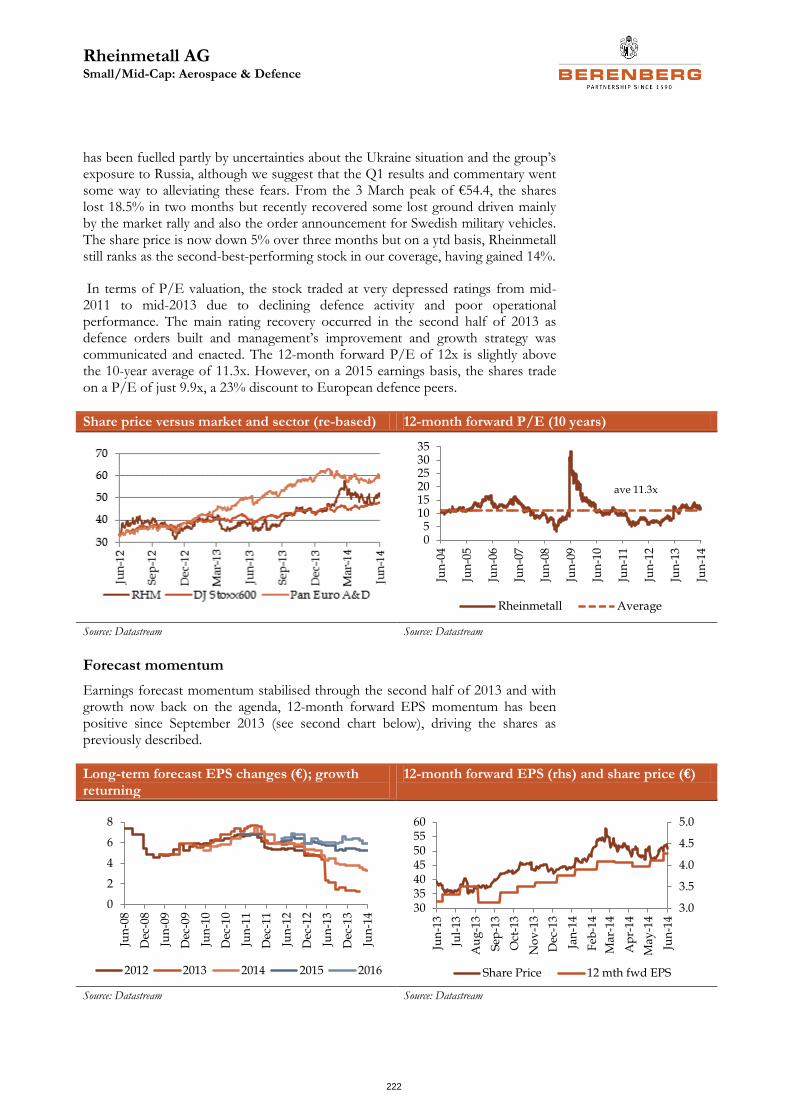

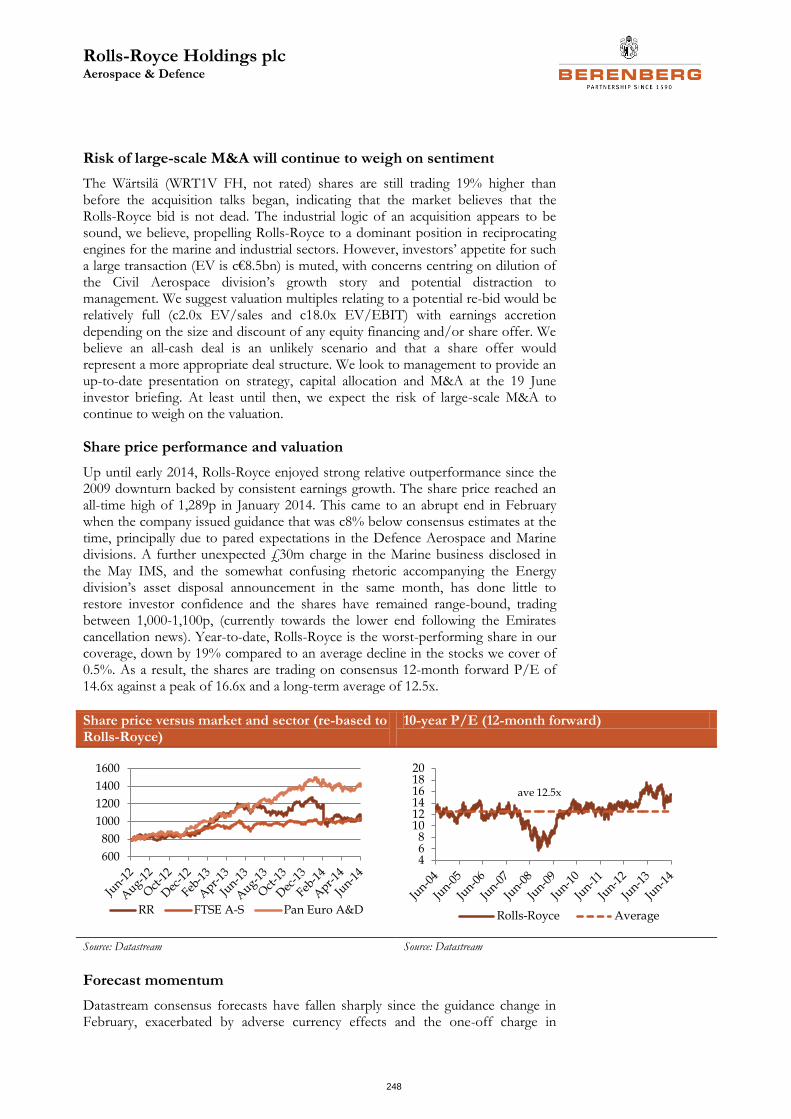

Performance: A&D Index has underperformed in 2014

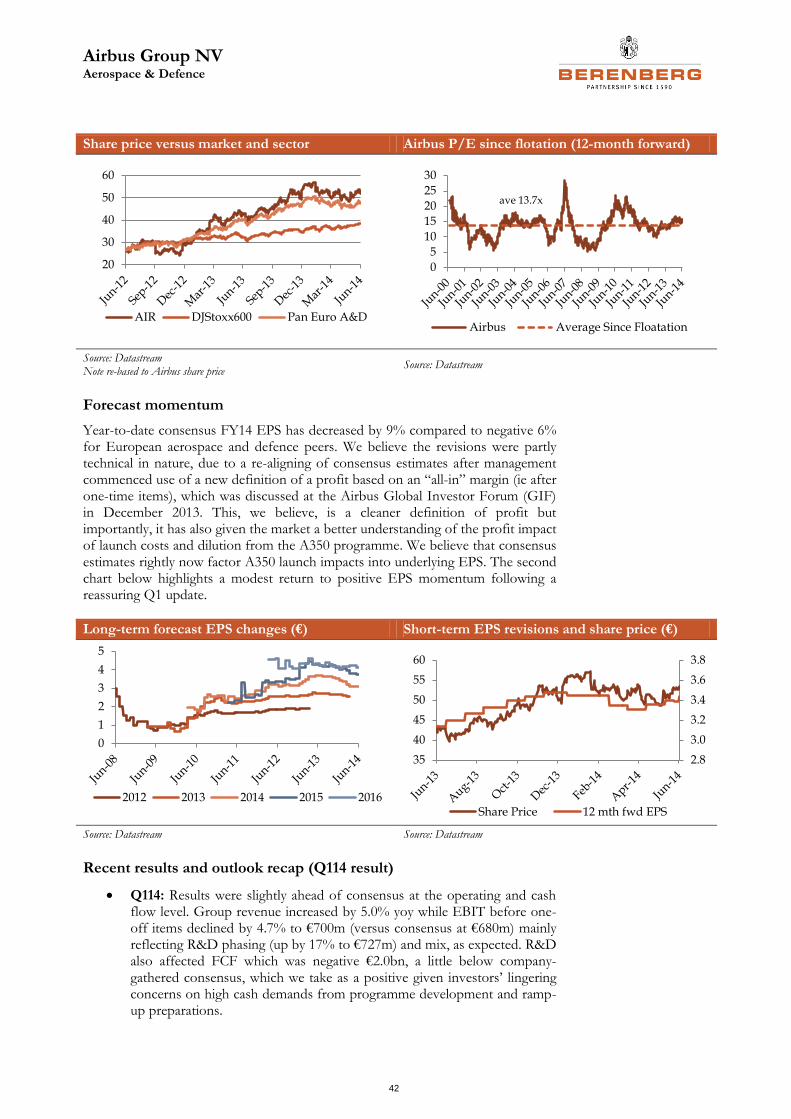

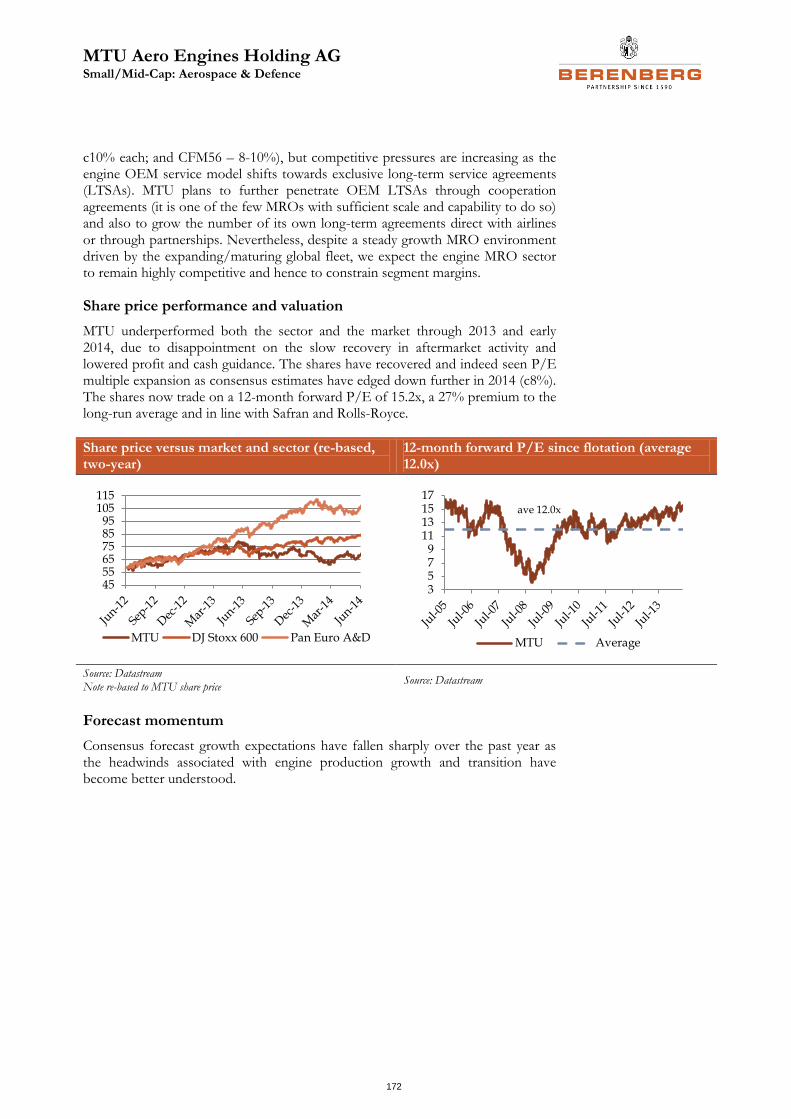

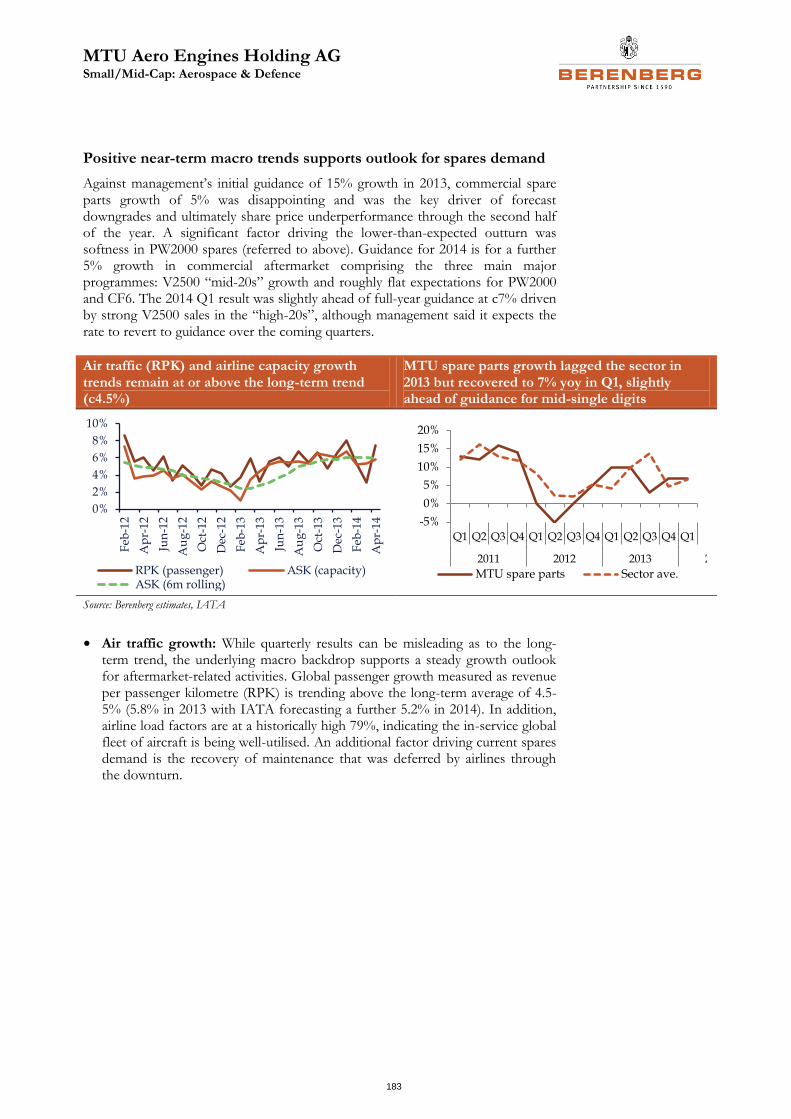

Despite the recent rally, a combination of rotation and negative forecast revisions has seen the sector underperform the broader UK and European indices in the ytd (the FTSE All-share by 7% and Stoxx600 by 11%). Within this is a wide range of individual share price performances with Cobham and Rheinmetall leading our coverage list, up by 18% and 14% respectively ytd, while Rolls-Royce is the notable underperforming outlier, down by 19% with Airbus and MTU Aero Engines the next relative underperformers, down by 7% and 5% respectively. We examine sector and stock performance in more detail on pages 16 and 17.

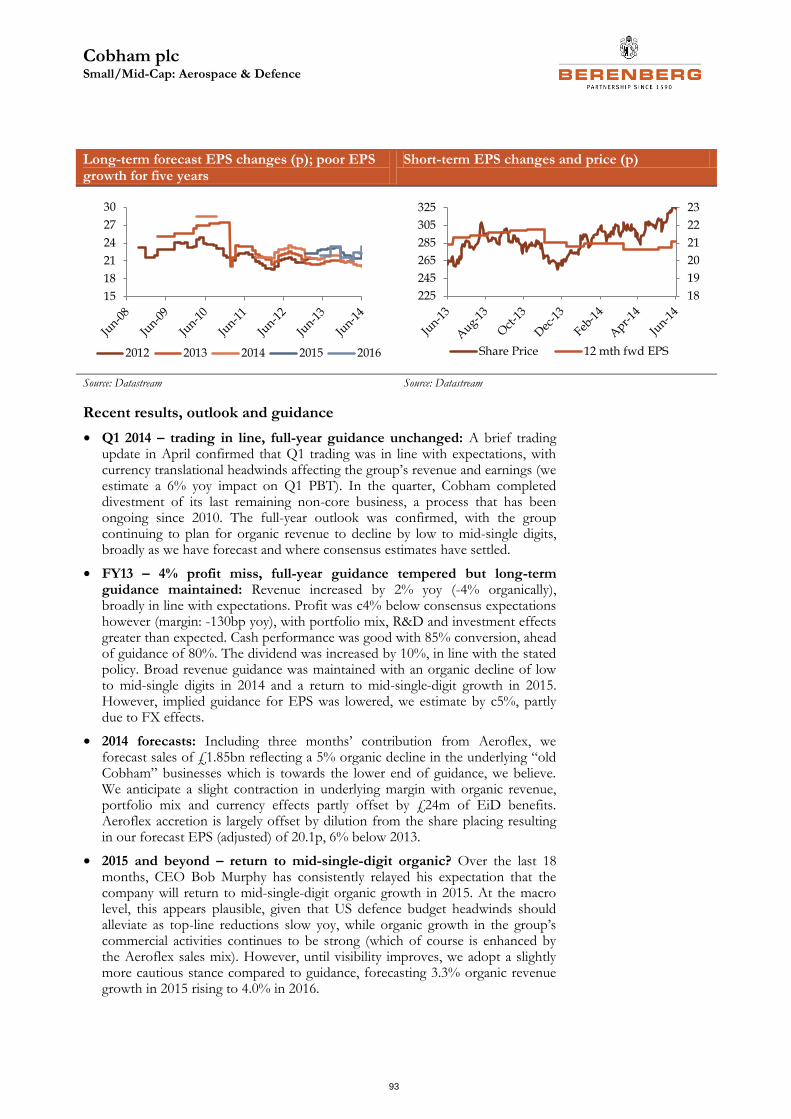

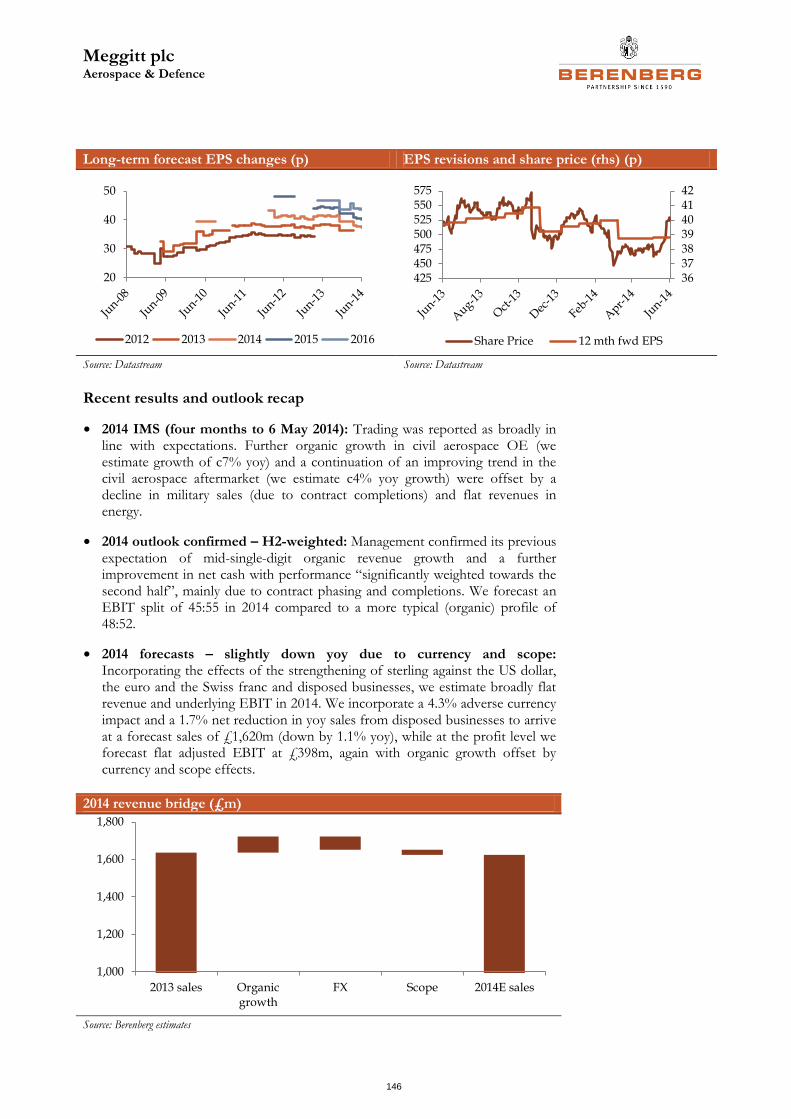

Growth – forecast momentum stalled towards the end of 2013

Positive sector earnings momentum that had for many years been driven by civil aerospace strength started to slow through the second half of 2013 and turned negative in early 2014 (as evidenced by downgrades to consensus earnings in the ytd for nine out of the 11 companies we cover, by an average of 6%). Adverse currency effects have been a key factor, with the majority of the companies exposed to the US dollar and the effects of the strengthening of the euro and sterling. Sterling-denominated companies have fared slightly worse in this respect (we factor in our 2014 forecasts an average adverse EBIT effect of c3.5% for the UK stocks we cover). In addition, a number of companies have reduced guidance unexpectedly for a variety of company-specific reasons. Overall, underlying sector earnings growth in 2014 is weak – we forecast an average underlying EPS decline of -2.2%, split civil aerospace 0.7% and defence -5.7% (excluding the distorting effects of Airbus and Rheinmetall). Thereafter, we anticipate an improving earnings with an average forecast EPS CAGR of 4.0% to 2017 for the sector, split 5.4% civil and 2.0% defence, on the same basis.

Valuation – the sector P/E has expanded by one turn over the past year

On a 12-month forward earnings basis, the sector average P/E has increased by one turn over the past year to 14.4x, a 9% premium to the 20-year average of 13.2x. Both the defence and civil aerospace subsectors have contributed; for our coverage universe the defence multiple has expanded by 2.2 turns to 11.3x while the civil aero multiple has increased by 0.7 turns to 14.8x. The re-rating of defence stocks was driven initially by receding concerns around the sequestration cuts and then by improved US Budget visibility. We note an average share price increase of

40,000

80,000

120,000

160,000

Narrow-body Wide-body Regional jets

0

200

400

600

800

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

CAGR -4.3%

Aerospace & Defence

5

18% for our defence stocks over the last year. Expansion of the civil aero P/E is the combined effect of an average 4% increase in share prices and modest earnings cuts over the same period. As a result of these re-ratings, the valuation differential between the civil aerospace and defence subsectors has narrowed to just 1.6 turns with civil stocks trading on an average P/E multiple of 14.4x with defence stocks on 12.8x (based on our FY15 forecasts). We examine sector and stock performance in more detail on pages 18 and 19.

Aerospace & Defence

6

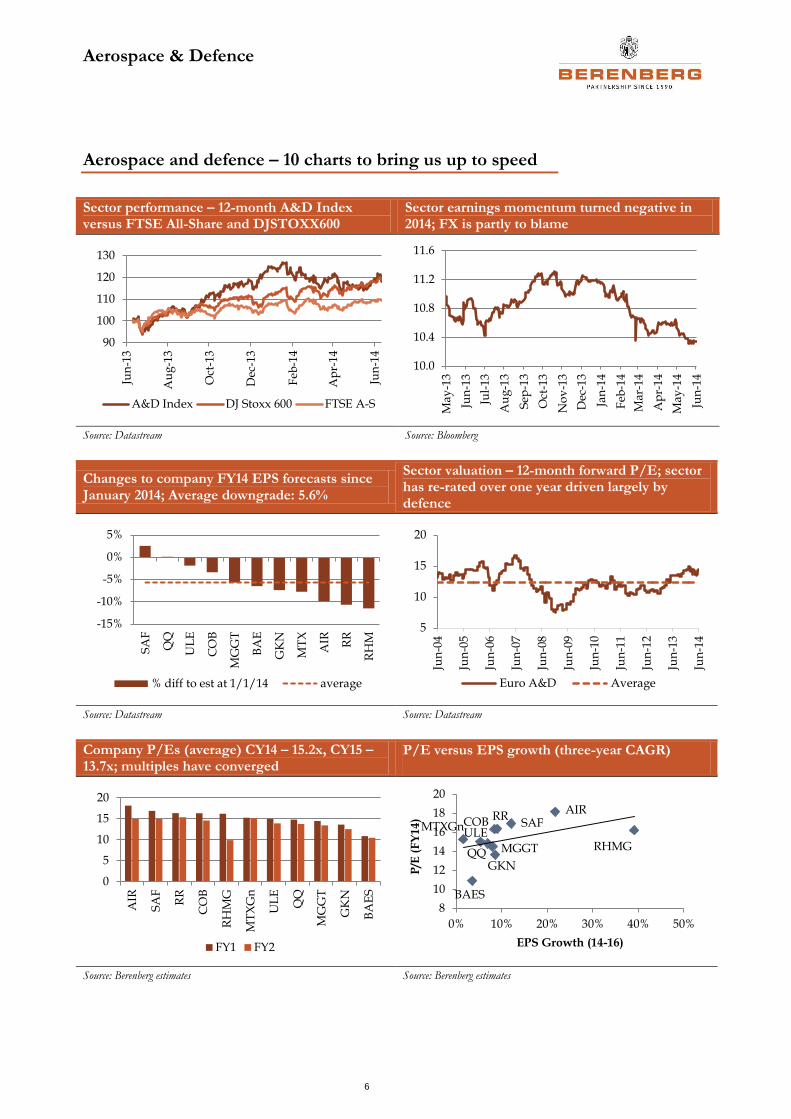

Aerospace and defence – 10 charts to bring us up to speed

Sector performance – 12-month A&D Index versus FTSE All-Share and DJSTOXX600

Sector earnings momentum turned negative in 2014; FX is partly to blame

Source: Datastream Source: Bloomberg

Changes to company FY14 EPS forecasts since January 2014; Average downgrade: 5.6%

Sector valuation – 12-month forward P/E; sector has re-rated over one year driven largely by defence

Source: Datastream Source: Datastream

Company P/Es (average) CY14 – 15.2x, CY15 – 13.7x; multiples have converged

P/E versus EPS growth (three-year CAGR)

Source: Berenberg estimates Source: Berenberg estimates

90

100

110

120

130

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb

-14

Ap

r-14

Jun

-14

A&D Index DJ Stoxx 600 FTSE A-S

10.0

10.4

10.8

11.2

11.6

May

-13

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

Oct

-13

No

v-1

3

Dec

-13

Jan

-14

Feb

-14

Mar

-14

Ap

r-14

May

-14

Jun

-14

-15%

-10%

-5%

0%

5%

SA

F

UL

E

CO

B

MG

GT

BA

E

GK

N

MT

X

AIR RR

RH

M

% diff to est at 1/1/14 average

5

10

15

20

Jun

-04

Jun

-05

Jun

-06

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

Jun

-13

Jun

-14

Euro A&D Average

0

5

10

15

20

AIR

SA

F

RR

CO

B

RH

MG

MT

XG

n

UL

E

MG

GT

GK

N

BA

ES

FY1 FY2

AIR

BAES

COB

GKN

MGGT

MTXGn

QQRHMG

RRSAF

ULE

8

10

12

14

16

18

20

0% 10% 20% 30% 40% 50%

P/E

(F

Y1

4)

EPS Growth (14-16)

Aerospace & Defence

7

Organic sales growth (three-year CAGR) Company end-market exposures

Source: Berenberg estimates Source: Berenberg estimates / Company data

Commercial aircraft deliveries: good growth but new programme* execution is key

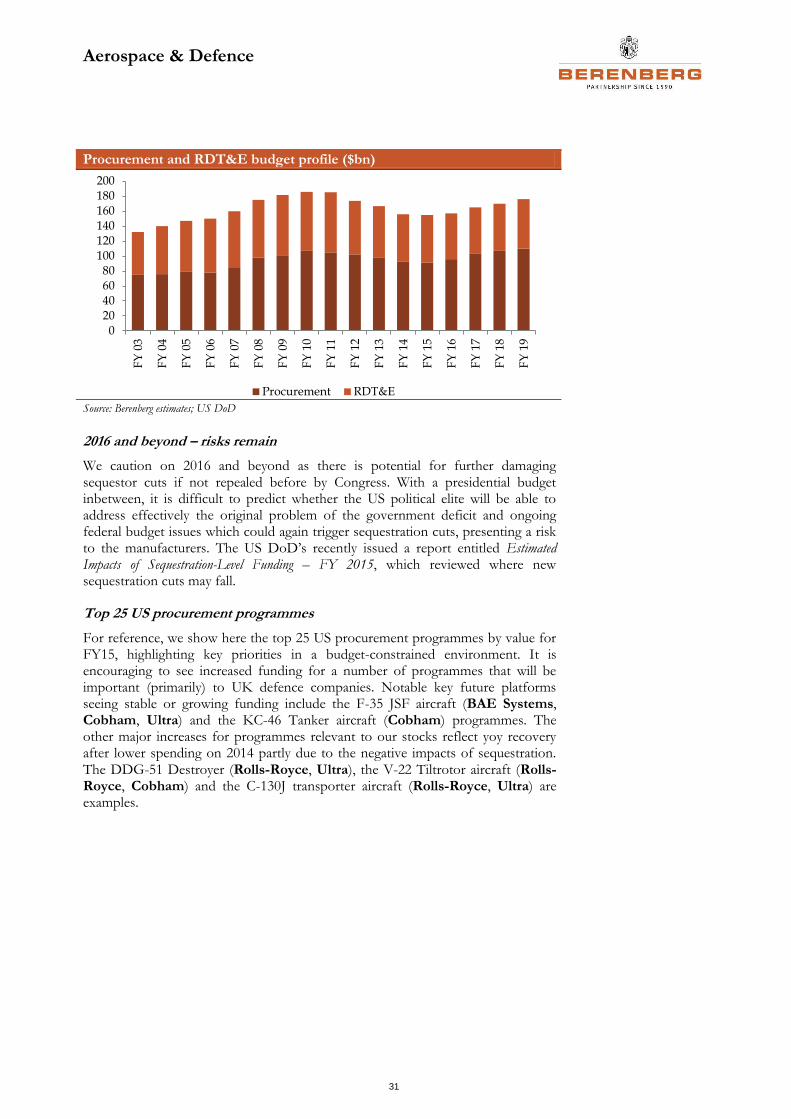

US defence procurement and RDT&E budgets ($bn): through the worst?

Source: Berenberg estimates/company data * New programmes include A320NEO, A350, 737MAX, 787

Source: US DoD

-10%

-5%

0%

5%

10%

SA

F

RH

MG

MG

GT

GK

N

MT

XG

n

AIR RR

UL

E

CO

B

BA

ES

3yr Historical 3yr Forecast

0%

20%

40%

60%

80%

100%

Civil OE Civil Aftermarket Defence Other

500

1,000

1,500

2,000

Series aircraft New narrow-body

New wide-body

0

50

100

150

200

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

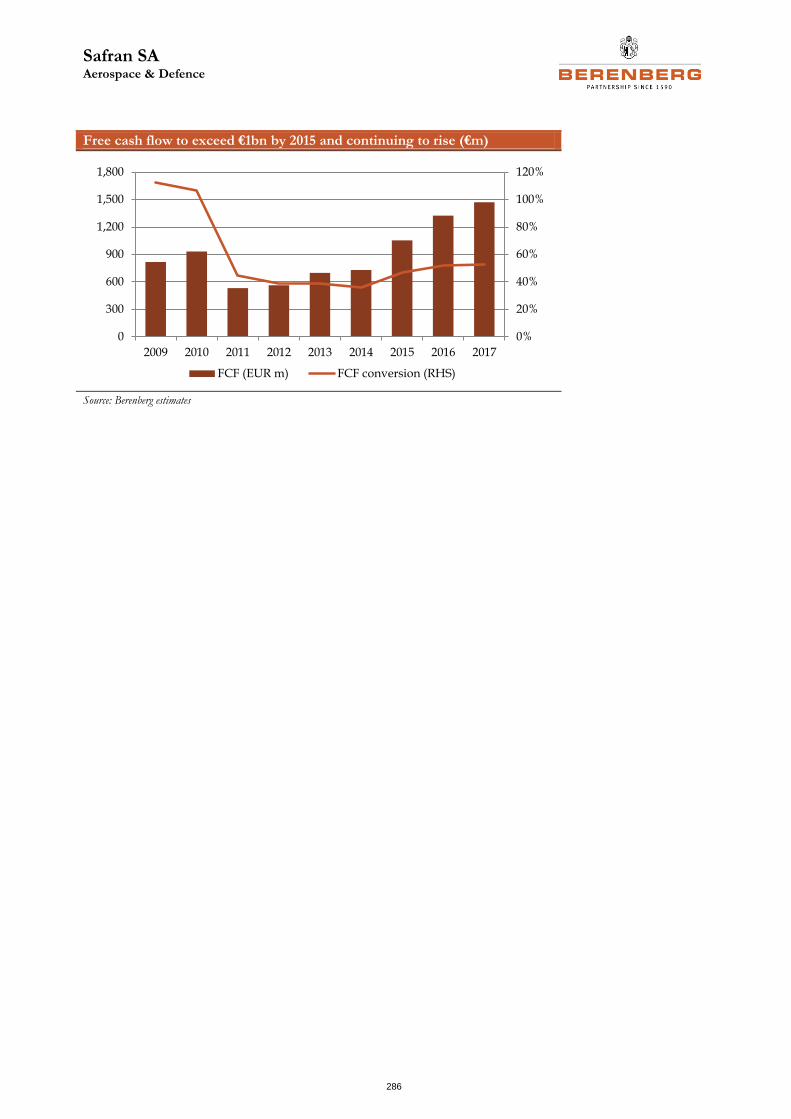

Procurement RDT&E

Aerospace & Defence

8

Stock summary – five key picks

Safran: LEAP of faith (Buy, PT €62.5 – 25% upside)

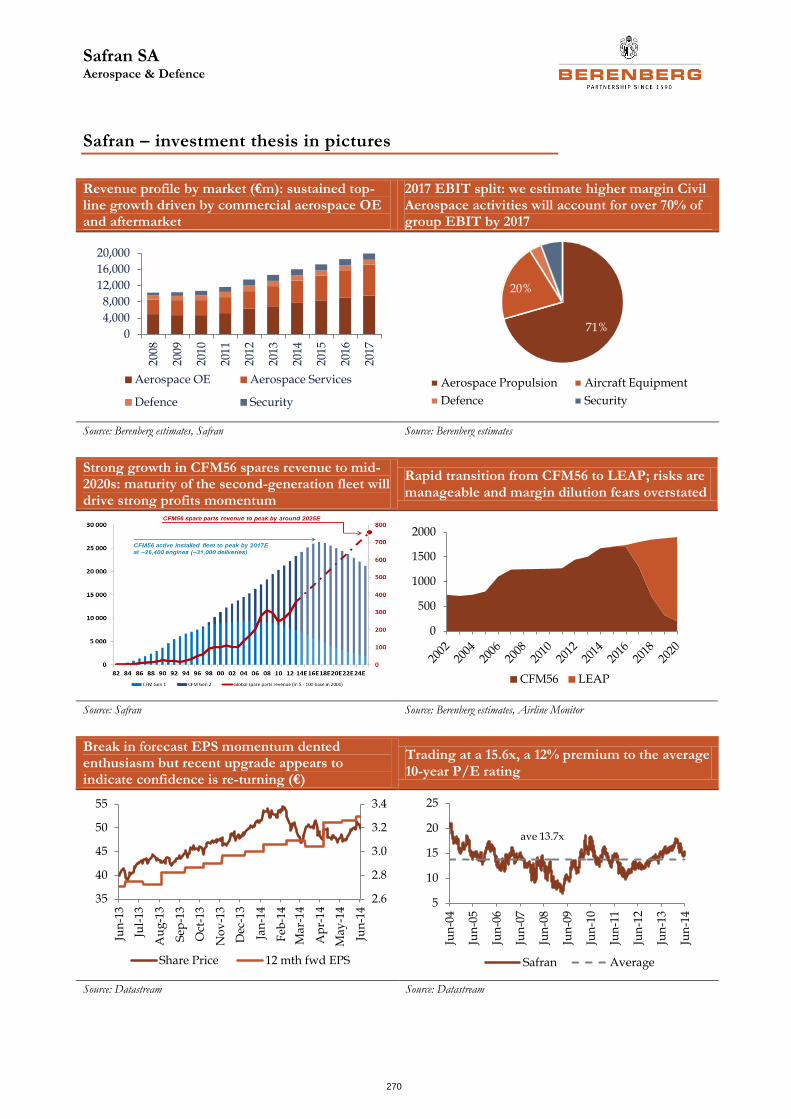

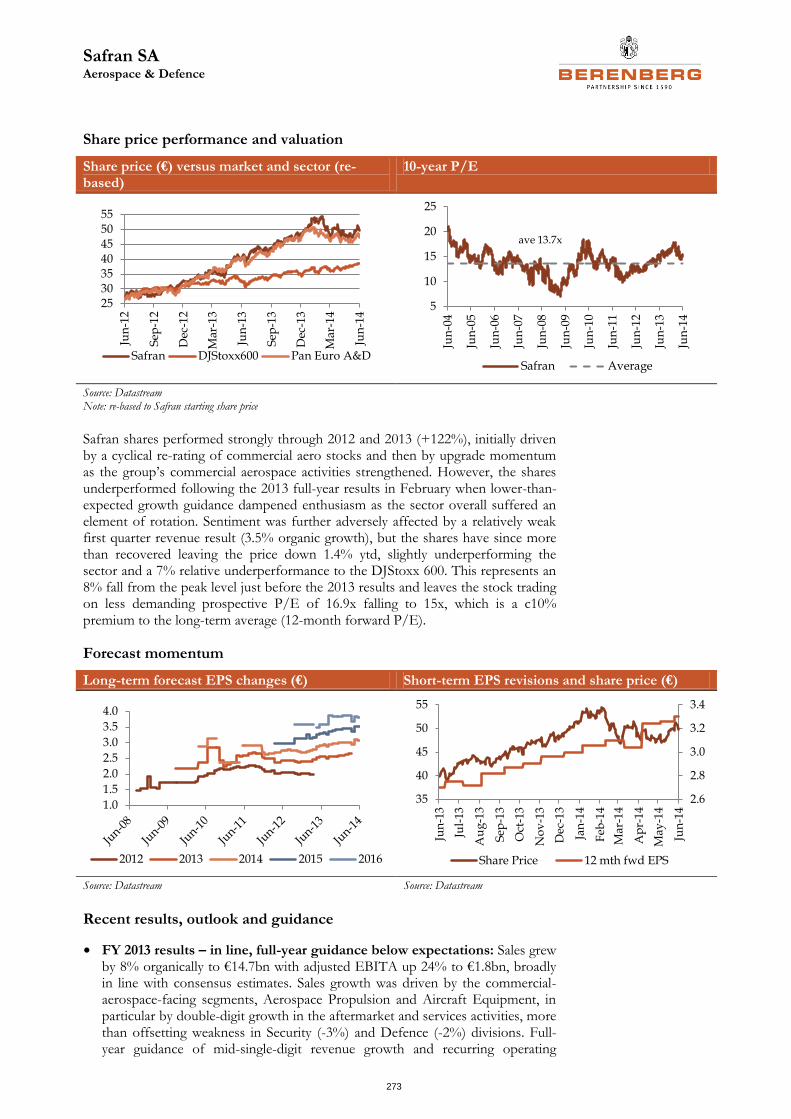

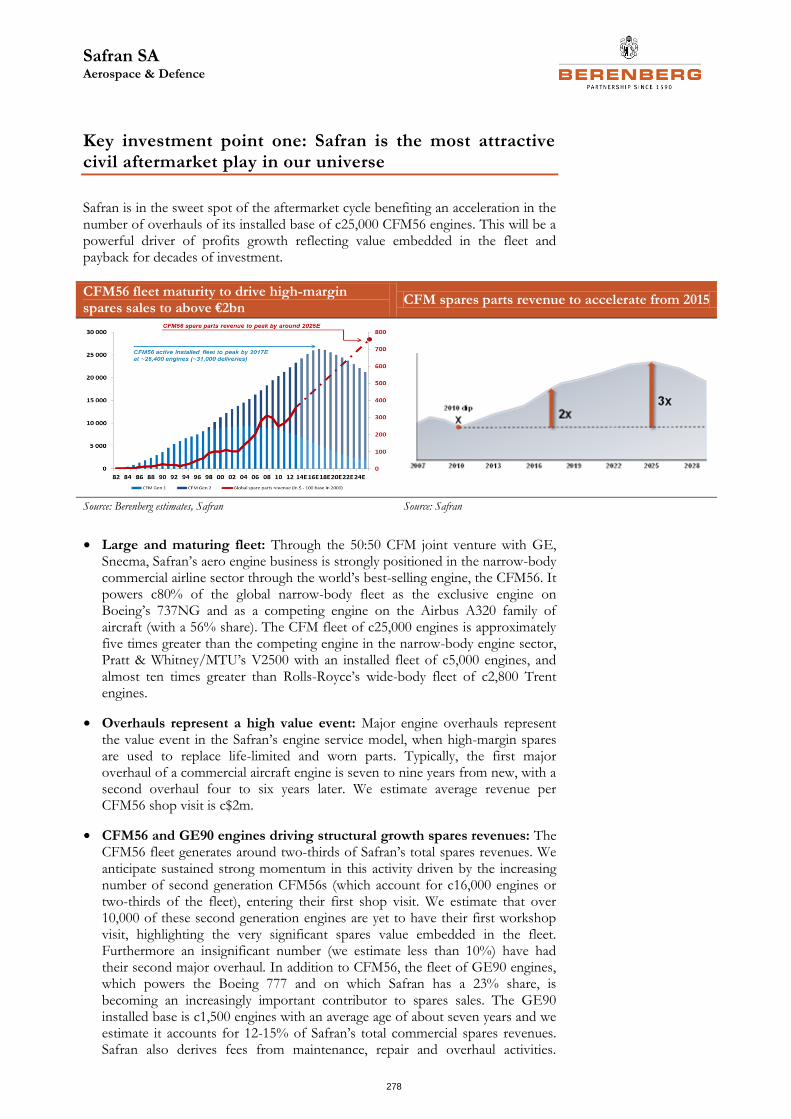

Safran is our top large-cap pick in the European aerospace and defence sector. We believe Safran is the optimal play on dual trends of the commercial aerospace aftermarket recovery and the original equipment (OE) production cycle. Safran’s very large and relatively young engine fleet profile has a relative structural advantage compared to its peers that will drive continuous strong growth in high-margin spares parts. This will more than offset dilution from the launch and ramp-up in production of the new CFM LEAP engine (for the B737MAX and A320 aircraft).

Sentiment for the stock waned through the early part of 2014 as a long run of positive earnings momentum stalled (mainly currency-related) followed by lacklustre Q1 results (organic growth: 3.5%) due to unforeseen delays in helicopter and defence programmes. We believe this masked strong underlying performances in the Propulsion (services), Aircraft Equipment and Security divisions. Management has assured the market that the effects of delays are temporary and confirmed full-year guidance.

Safran shares are down by 1.4% ytd, which is a slight underperformance relative to the stocks we cover. Business momentum is strong in the key civil aviation businesses and we expect Safran will at least deliver to expectations. With the shares trading on EV/EBITDA (FY15) of just 7.6x, we believe valuation risk is to the upside.

Rheinmetall: building confidence; up to Buy (Buy, PT €62.5 – upside 22%)

After a few years of poor financial performance and declining earnings, Rheinmetall is on a strong growth recovery path with both divisions, Defence and Automotive, experiencing top-line growth on a restructured cost base. The outlook for Defence has been much improved by a number of large-scale, multi-year international orders swelling the order book to a record €6.7bn and providing a high level of sales cover compared to history. Growth in the Automotive division is being driven by rising global auto production, including a strengthening presence in China through its joint ventures and rising demand for its emission systems products.

From the depressed level in 2013, the rate of profit growth over the next couple of years is difficult to predict given a number of near-term risks such as the strong second-half skew to the Defence division’s business that partly depends on securing orders in the shorter cycle munitions businesses. Even if the company delivers to our forecasts, which are pitched at the lower end of the 2015 margin guidance range of 7-9% in Defence and 8% in Automotive (we forecast 6.7% and 7.7% respectively), then this stock is too cheap on just 8.8x P/E (FY15E).

Rolls-Royce: engine splutter: just needs a bit more choke (Buy, PT 1,216p – upside 20%)

Investor confidence has been shaken by an uncharacteristic brace of warnings on profit due to a sharper-than-expected reduction in defence aerospace activity and a

Aerospace & Defence

9

one-off charge in the Marine division. In effect, this translates to a lost year of growth in 2014, the first time in over a decade that operating profits have declined yoy. In reaction, the stock has significantly underperformed ytd, down by 19% against an average decline of the sector of 1%. In our view, there are no structural issues to de-rail the long-term growth story, backed by a c£70bn orderbook and the planned ramp-up in civil engine (Trent XWB) production. The high profile Emirates cancellation of its 70 aircraft A350 XWB order last week is clearly a disappointment but does not affect the programme, which still has a seven-year backlog.

The key debate is around margin progression – in particular, the net impact of dilution from the A350 XWB launch and declining high-margin services revenues on legacy programmes, offset by growth in the revenues derived from long-term service agreements (LTSAs) and the benefits of restructuring and efficiency initiatives. Our view is that the maturing LTSA model will prevail driving a return to continuing profits growth from 2015.

We acknowledge the possibility of further share price volatility in the short term with an investor briefing on 19 June when agenda items include an update on strategy and long-term contract accounting. Long-term contract accounting will be extremely important for investors’ understanding of the LTSA value proposition. Provided management can communicate this effectively, it should allay concerns about the quality and pace of the growth story and drive the rating higher, we believe. Failure to do so will delay the sentiment recovery. Regardless, in 12 months’ time, we believe the market will be feeling more confident about the Rolls-Royce story as the A350 XWB and LTSA effects become clearer and are better understood.

Separately, investor appetite for large-scale M&A appears muted after the approach to Wärtsilä (market cap: €8bn) was rejected earlier this year. This threat of a potential re-bid is weighing on the stock. Again, the 19 June investor briefing will be key, given that the company has said it will address the subject of capital allocation at the event.

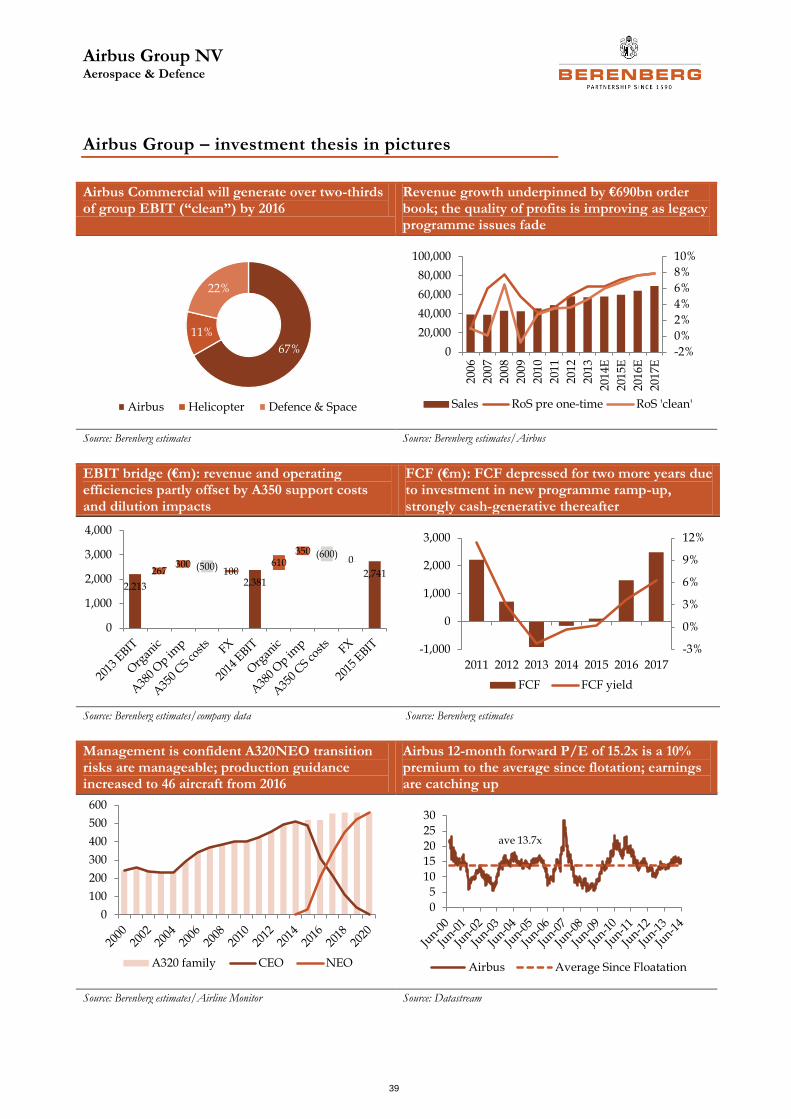

Airbus: stand and deliver (Buy, PT €60.5 – upside 16%)

Major programme risk continues to reduce as legacy issues fade (the A380 is progressing towards achieving the 2015 breakeven objective and production of the A400M is steadily ramping up) and new programmes mature (the A350 XWB is nearing entry into service and the A320NEO development programme is advancing). This together with operational improvements across the group is resulting in steady margin expansion and improving profits quality, despite growing losses related to launch of the A350 XWB.

As ever, Airbus faces a multitude of business challenges including the production ramp-up of the A350 XWB, the launch of the A320NEO and the navigation of a complex, multi-year restructuring of the Defence and Space business. We believe that these risks are being well managed and the market’s confidence will build as further milestones are passed, which in turn could drive upgrades to consensus forecasts. Flight certification of the A350 XWB is expected in Q3, with first customer delivery (to Qatar Airways) to follow in Q4. Other significant news before the year is out could include a decision on whether to re-engine the A330 and/or the A380 which, if pursued, would commit more development dollars, not a major concern for us because R&D spend is trending down and it would extend

Aerospace & Defence

10

the life of existing platforms, deferring the need for more expensive all-new aircraft developments.

Emirates’ cancellation of its order for 70 A350 XWB aircraft, while large, has little bearing on the financial performance of the group in the near term or the success of the overall programme (there is still c7 years of A350 XWB backlog to execute). However, it raises the broader question of whether the aircraft order cycle is softening and hence the risk of further cancellations. In the context of the group’s c5,500 aircraft backlog, we are not concerned but we recognise sentiment towards Airbus (and the sector generally) will be adversely affected by this development. Airbus continues to talk of a healthy order environment and has confirmed it still expects to achieve a book-to-bill greater than 1x in 2014. We expect positive order activity during the Farnborough Air Show (14 July).

Year-to-date, Airbus shares have underperformed the European peer group by 6% and Boeing by 8%, and in our view look good value if the company delivers continued profit growth at the current trajectory.

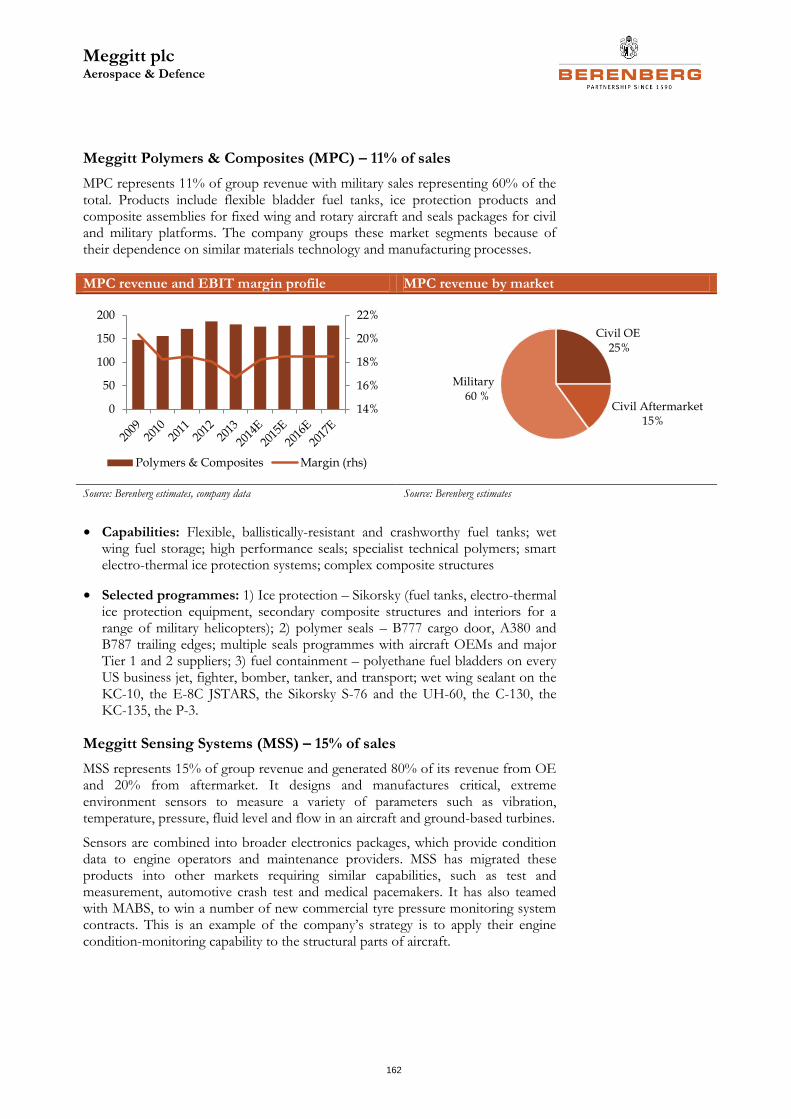

Meggitt: under-rated (Buy, PT 600p – upside 15%)

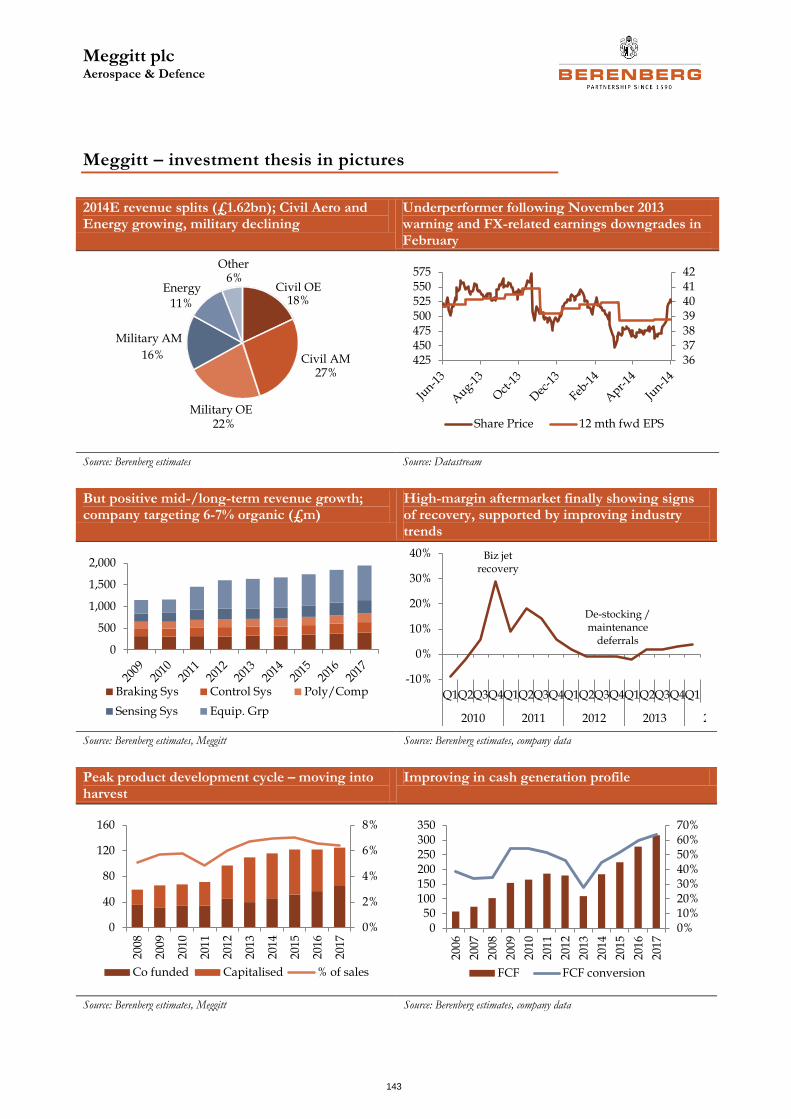

Meggitt is nearing the peak of an intensive product investment cycle and we believe it is fundamentally well positioned in attractive end-markets (civil aerospace and energy) to deliver long-term growth. High-margin aftersales activity is a key differentiator to peer aerospace suppliers, accounting for almost half of group sales and providing resilience in the military aerospace business.

The shares have rallied in recent weeks, indicating investors’ confidence is returning following the November 2013 profit warning and the FX-led downgrades in March 2014. Continued recovery of high-margin civil aftermarket activity (27% of sales) is key to sustaining this confidence, particularly through the interims which are expected to indicate a greater-than-normal H2 bias to financial performance. Assuming it does, and management is able to confirm full-year guidance, we see scope for valuation multiples to expand further (the shares currently trade at an 10% FY15 P/E discount to civil aerospace peers on our forecasts). Over the longer term, we expect Meggitt to deliver sustained earnings growth (we forecast an EPS CAGR of 7% to 2017), which should continue to drive the shares.

Aerospace & Defence

11

Stock summary – the rest

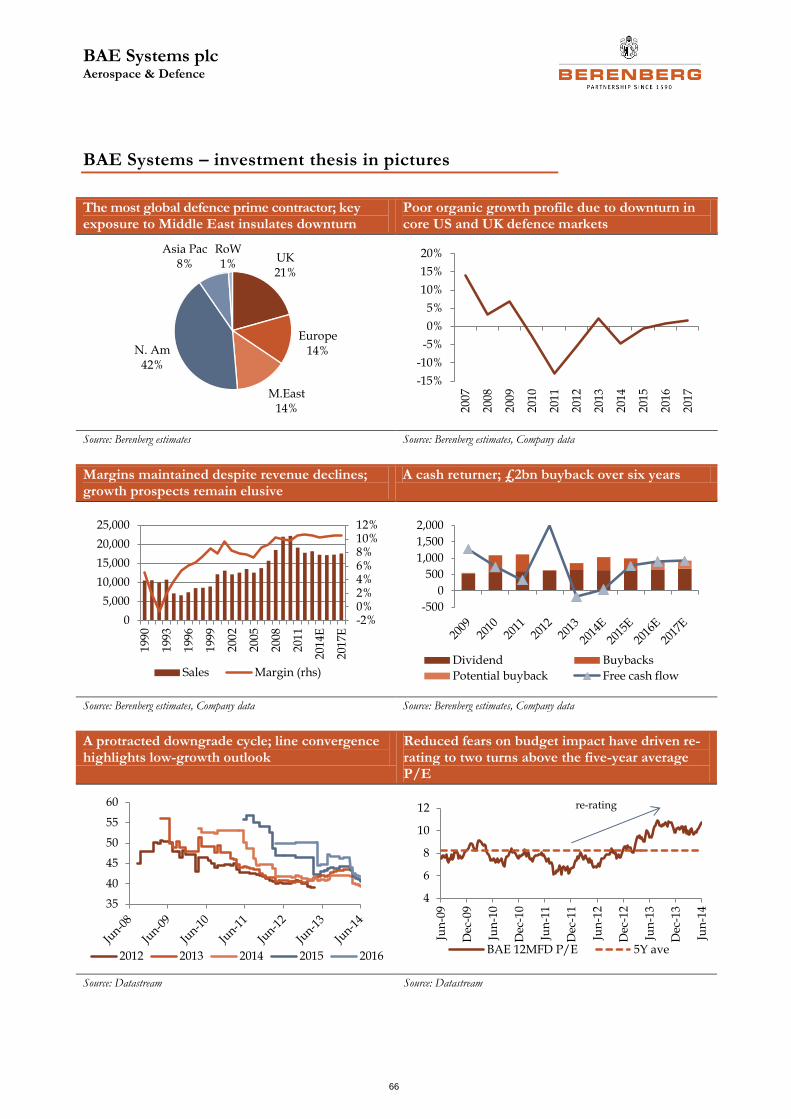

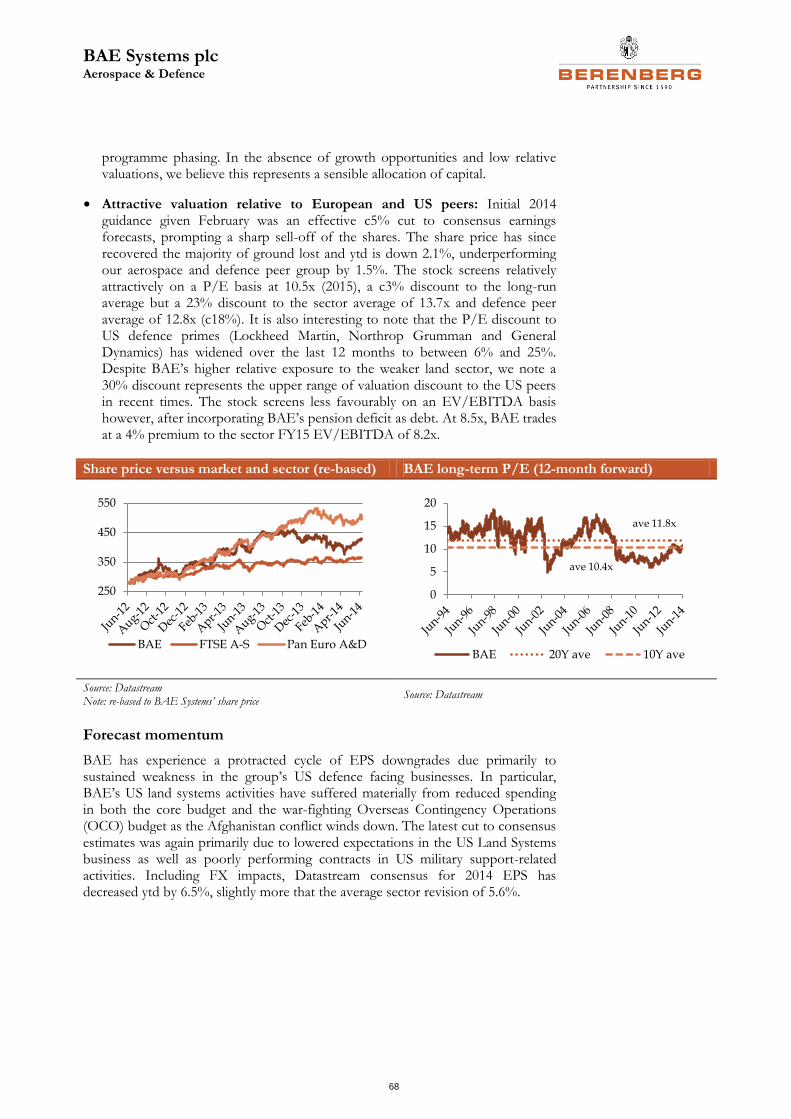

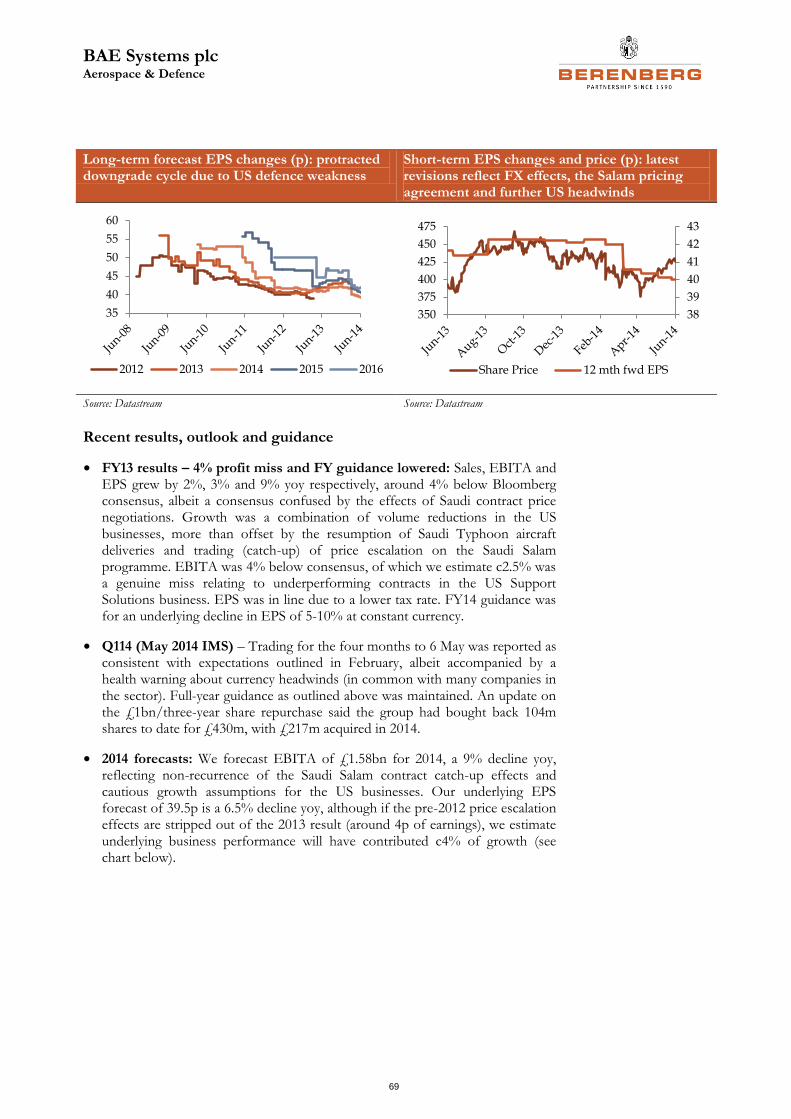

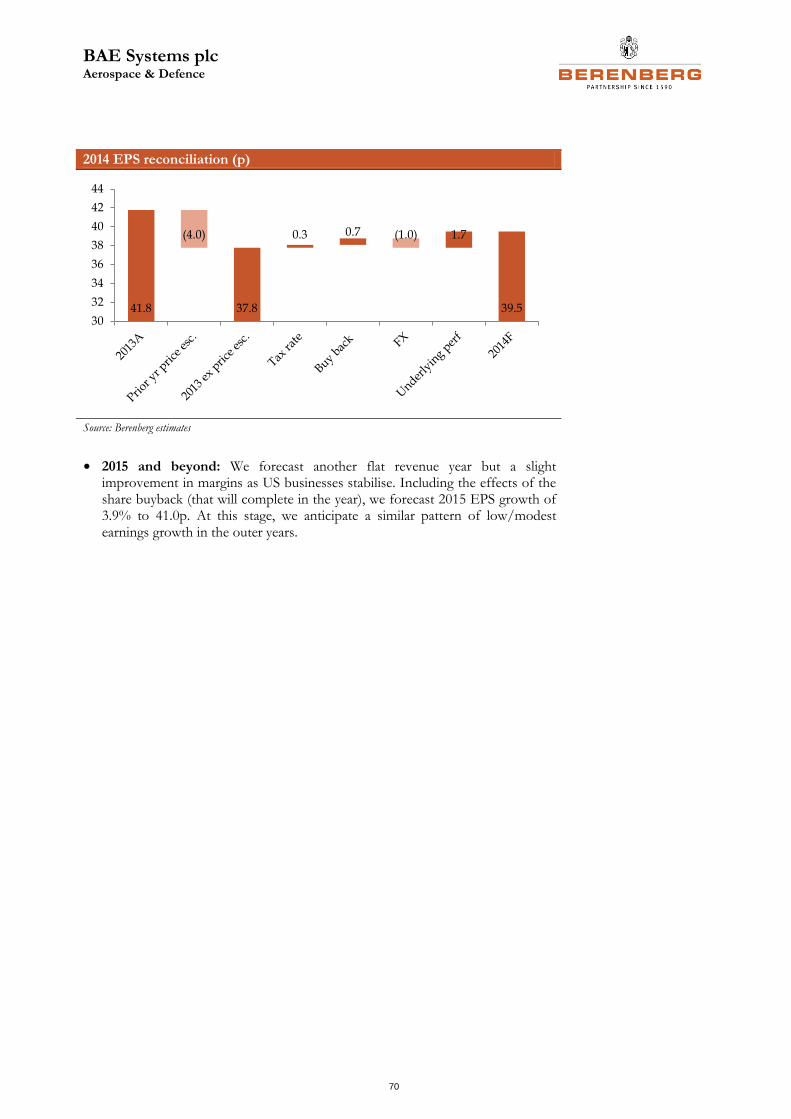

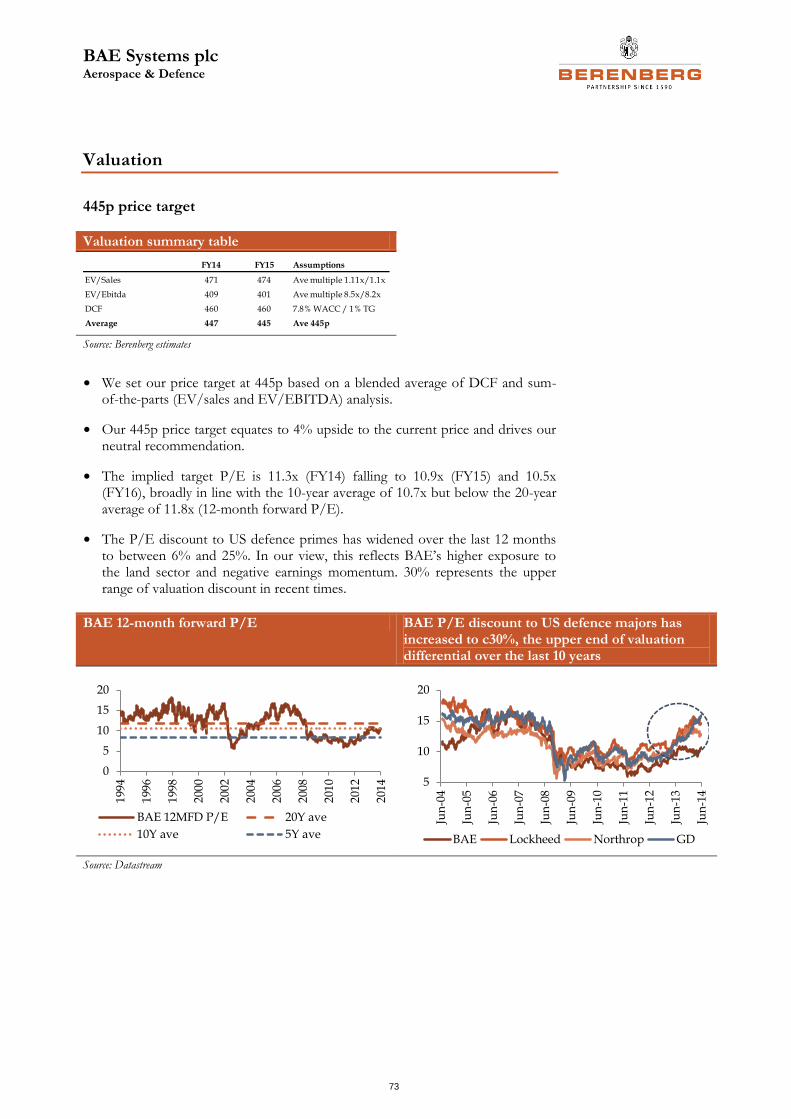

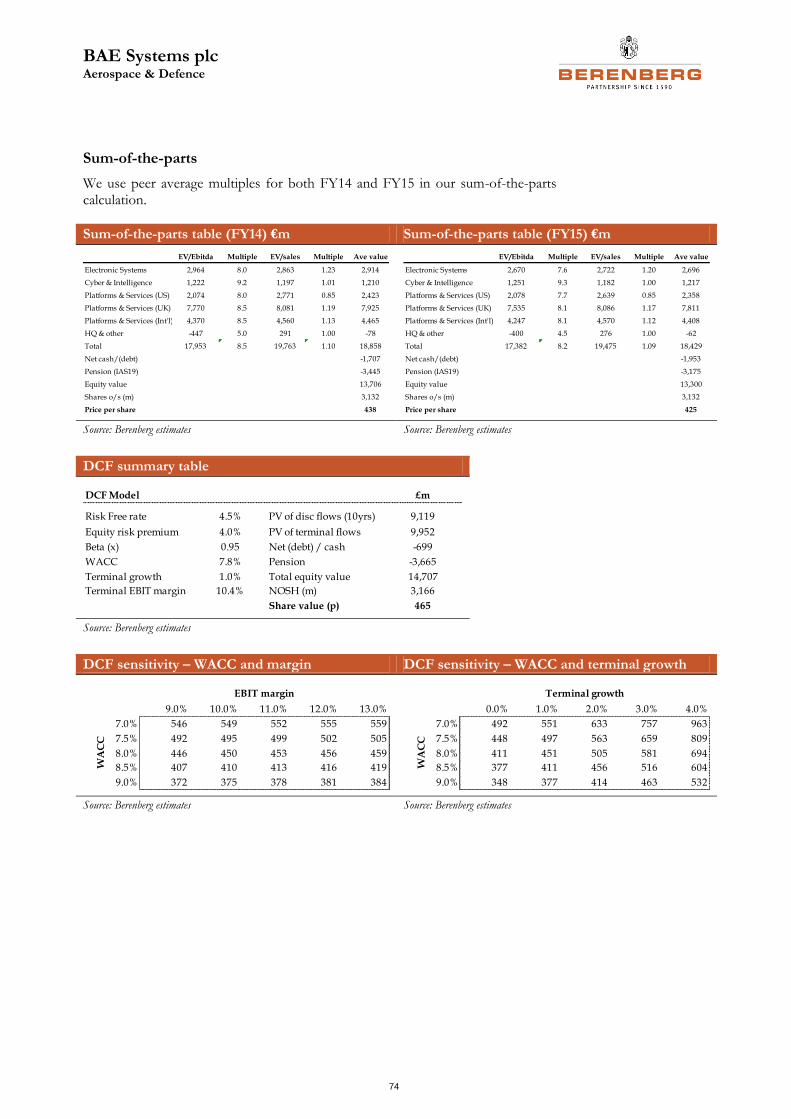

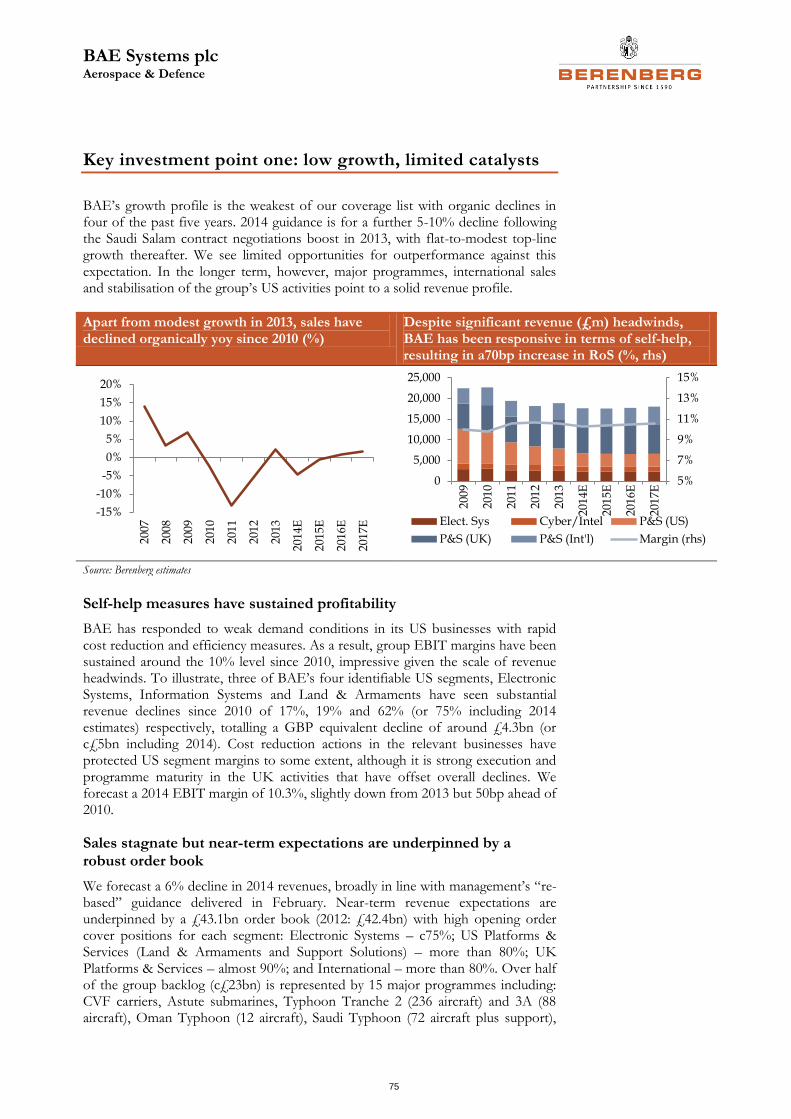

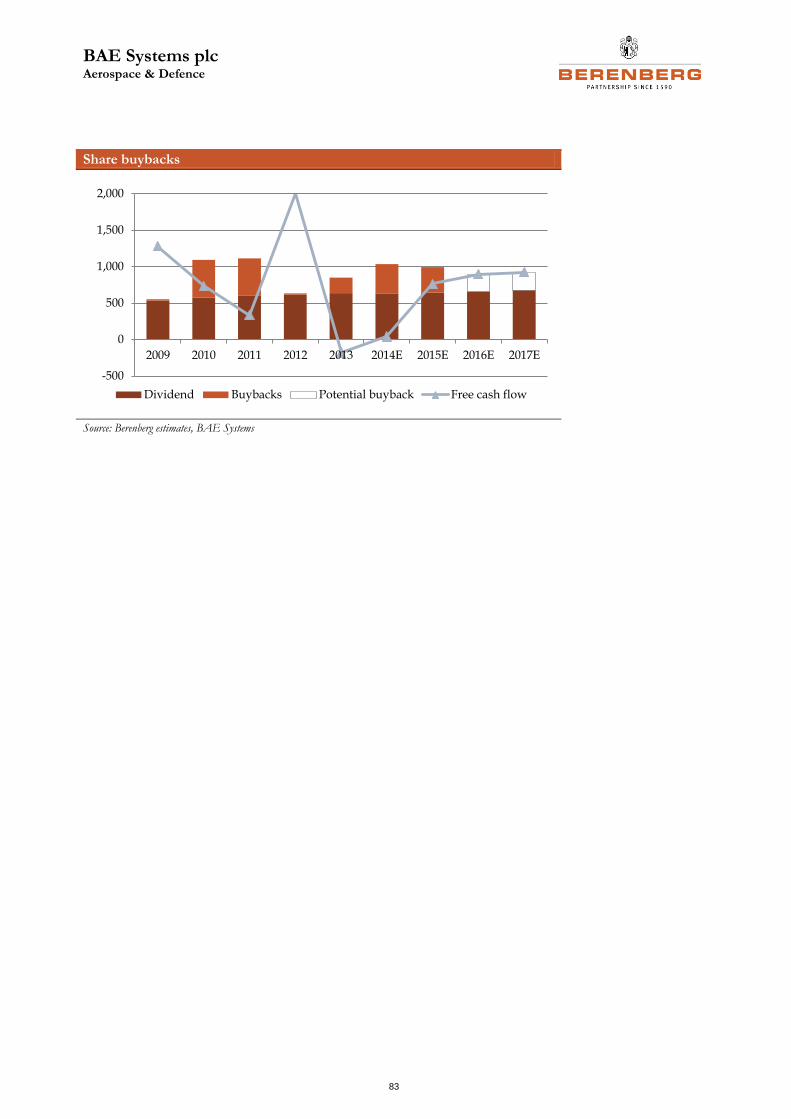

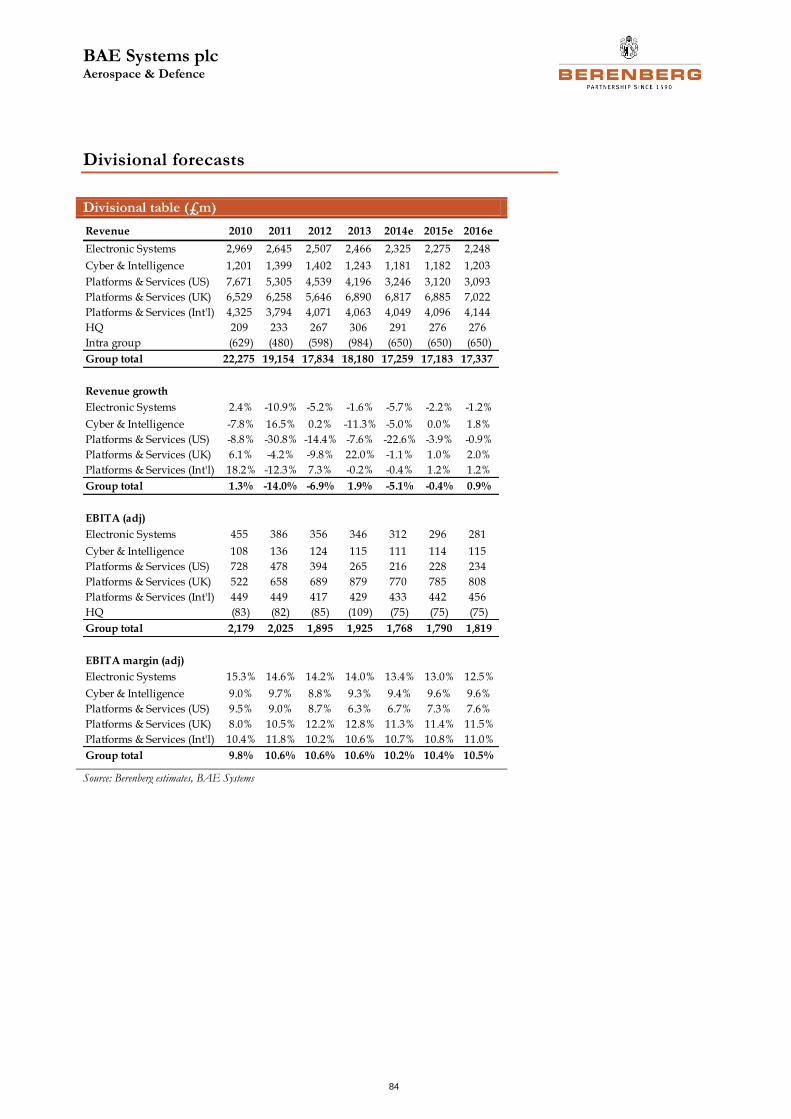

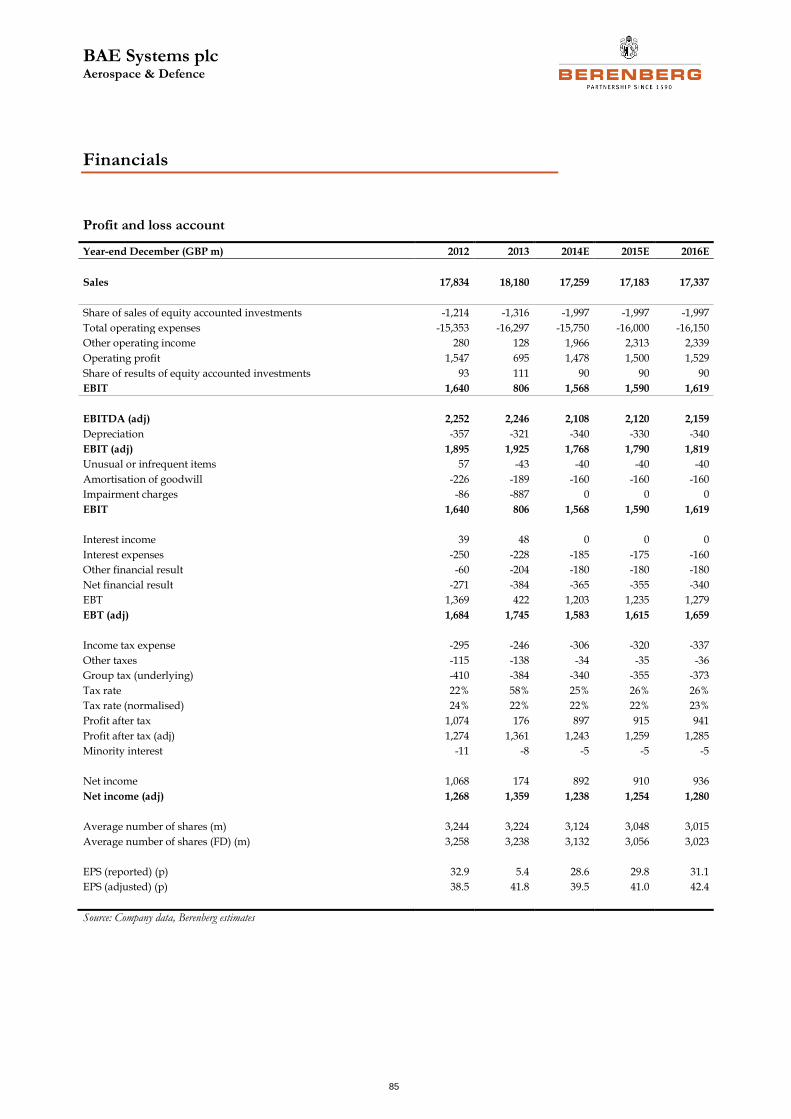

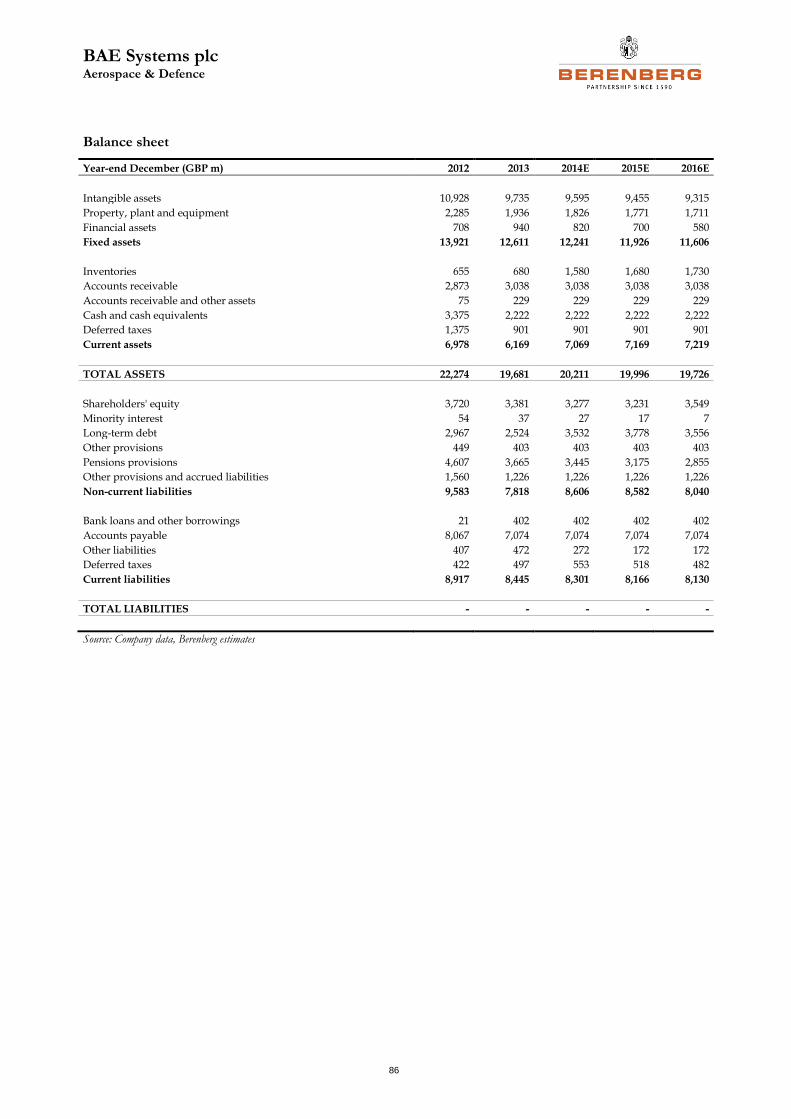

BAE Systems: stabilising outlook (Hold, PT 445p – upside 5%)

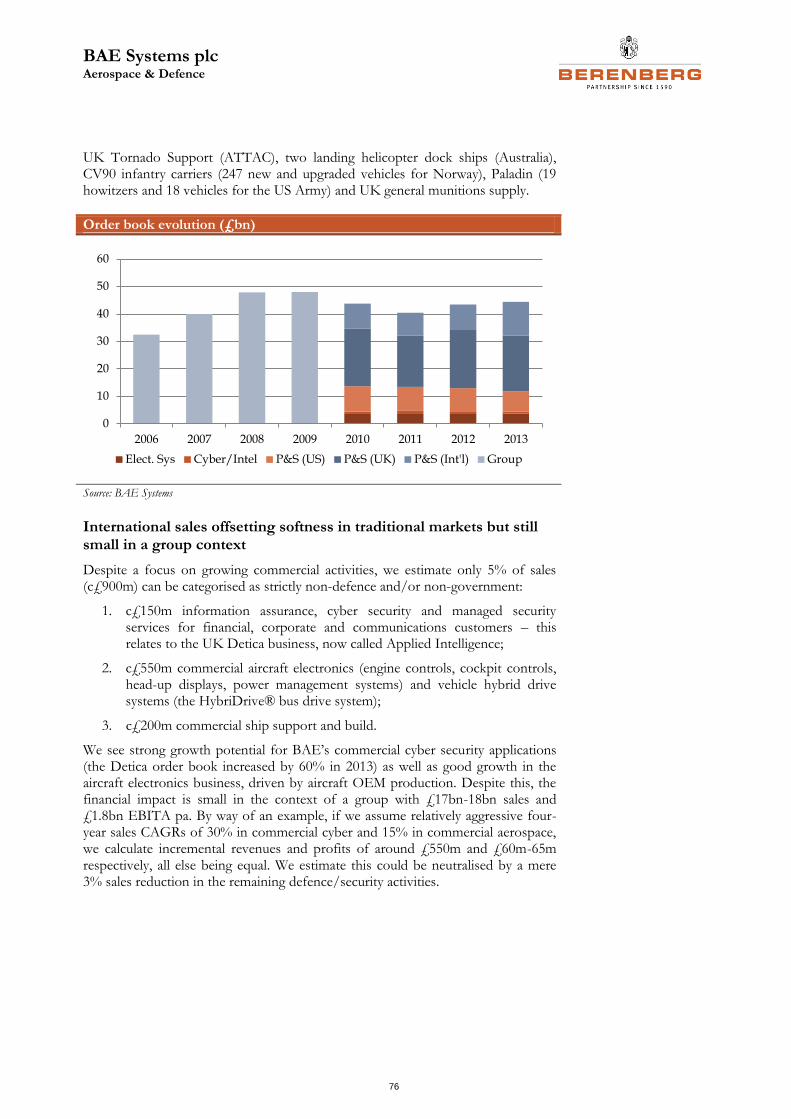

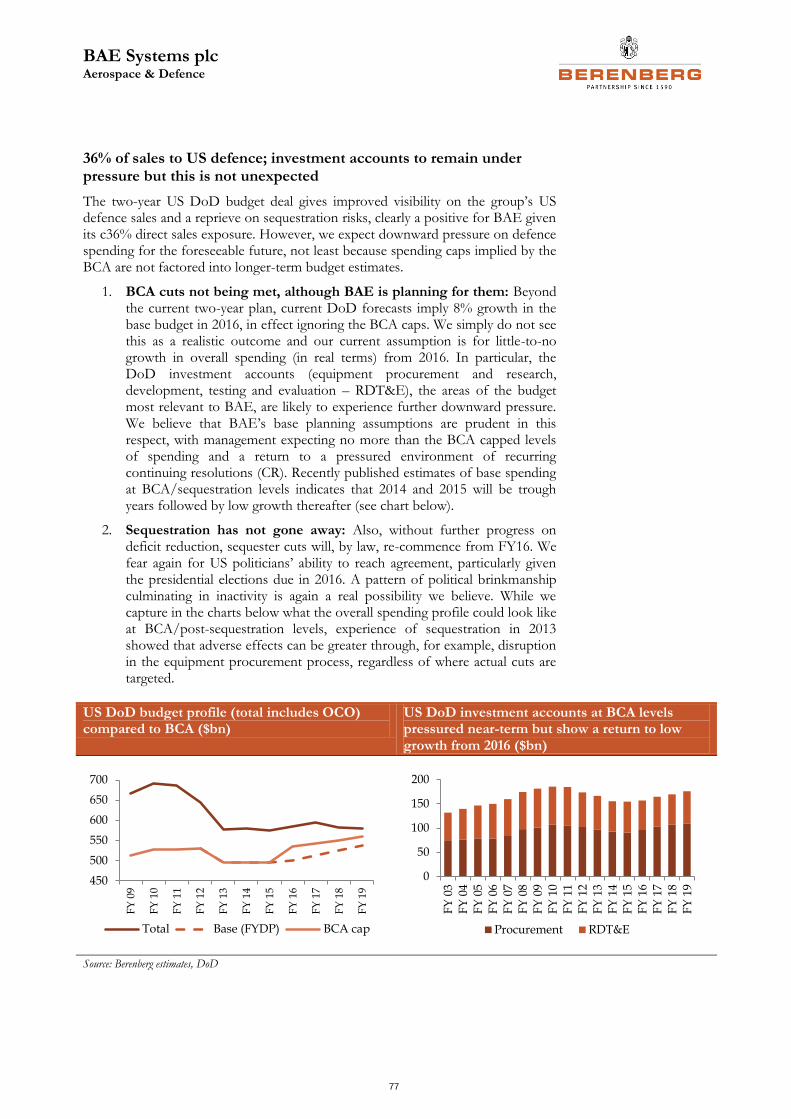

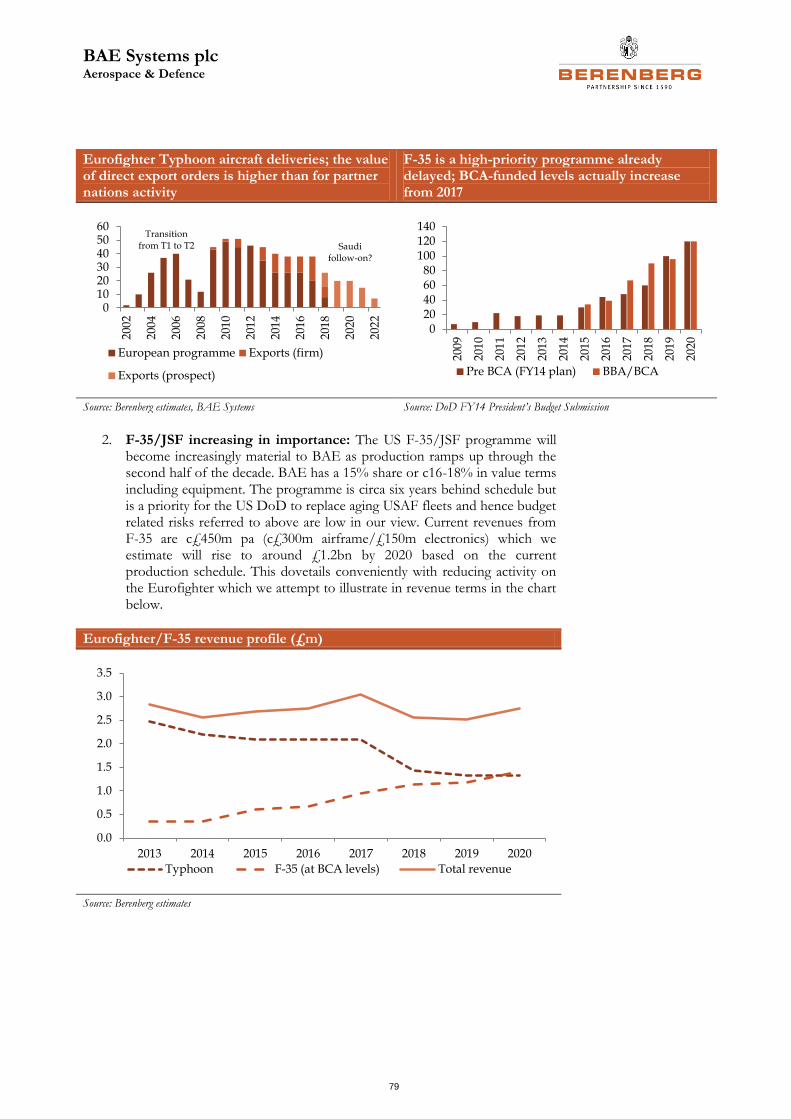

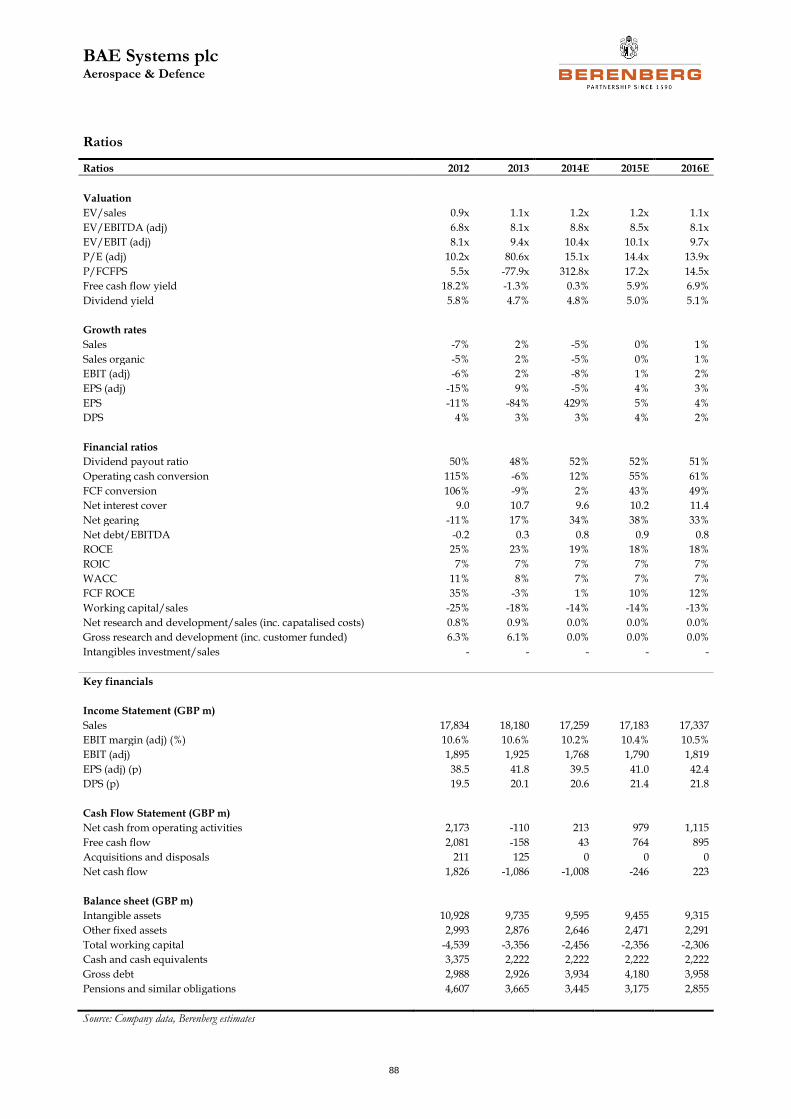

BAE has suffered a protracted downgrade cycle primarily due to weakness in its budget-constrained US businesses which has translated into stagnant earnings since 2009. Improving budget visibility in the US, finalisation of Saudi contract terms and agreement on the UK naval programme point to a more stable outlook, both in the near and longer term. However, BAE is still the lowest earnings growth company in our coverage, despite a £1bn share buyback (we forecast a three-year EPS CAGR of 0.5%) and with few major contract opportunities in prospect and budget constraints likely to endure, we see limited upside to this scenario. Higher-growth commercial activities represent 5% of the group, too small to do more than offset defence headwind.

The key investment attraction for us is the rock solid dividend, yielding 4.8% and providing strong support to already depressed valuation multiples. The main risk to our neutral stance is multiple expansion. We are just not sure of a meaningful catalyst in the short term.

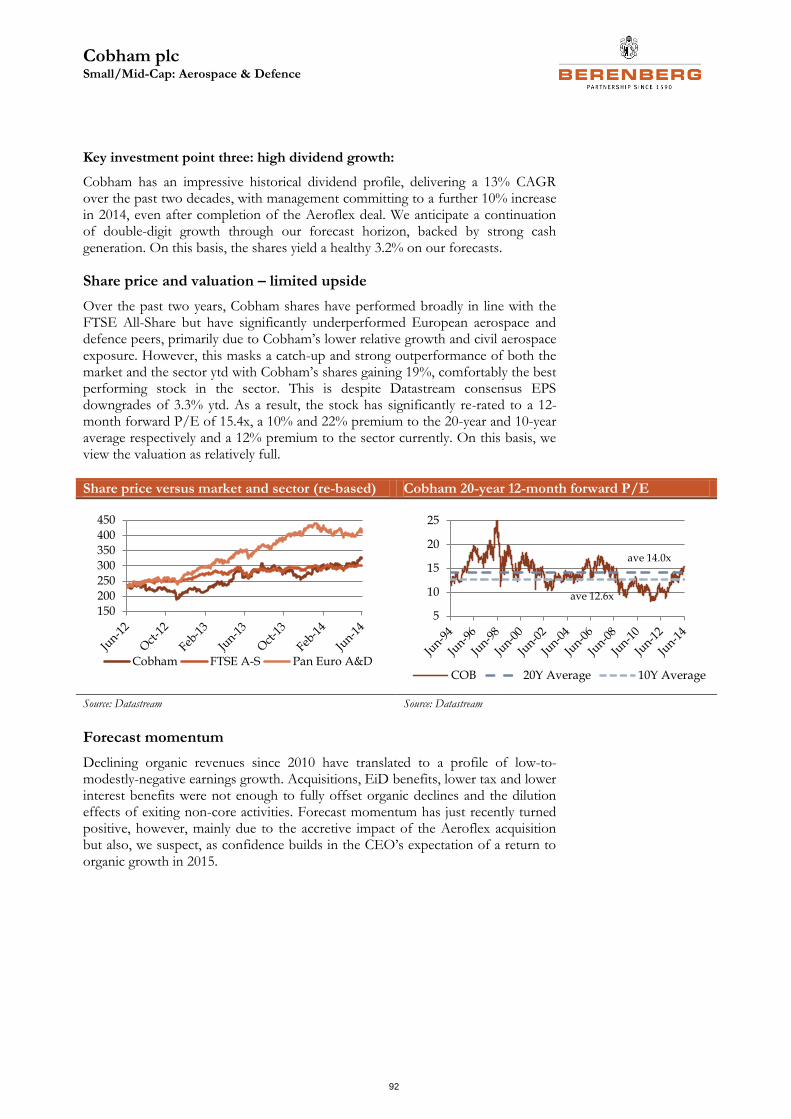

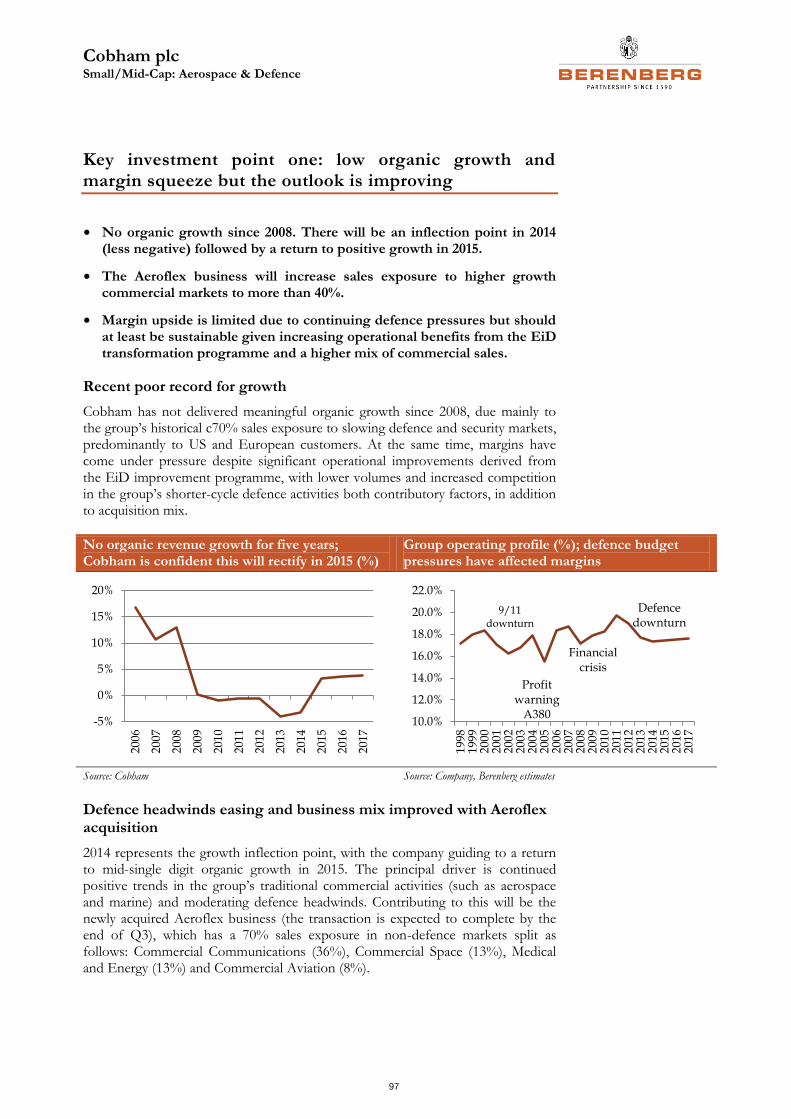

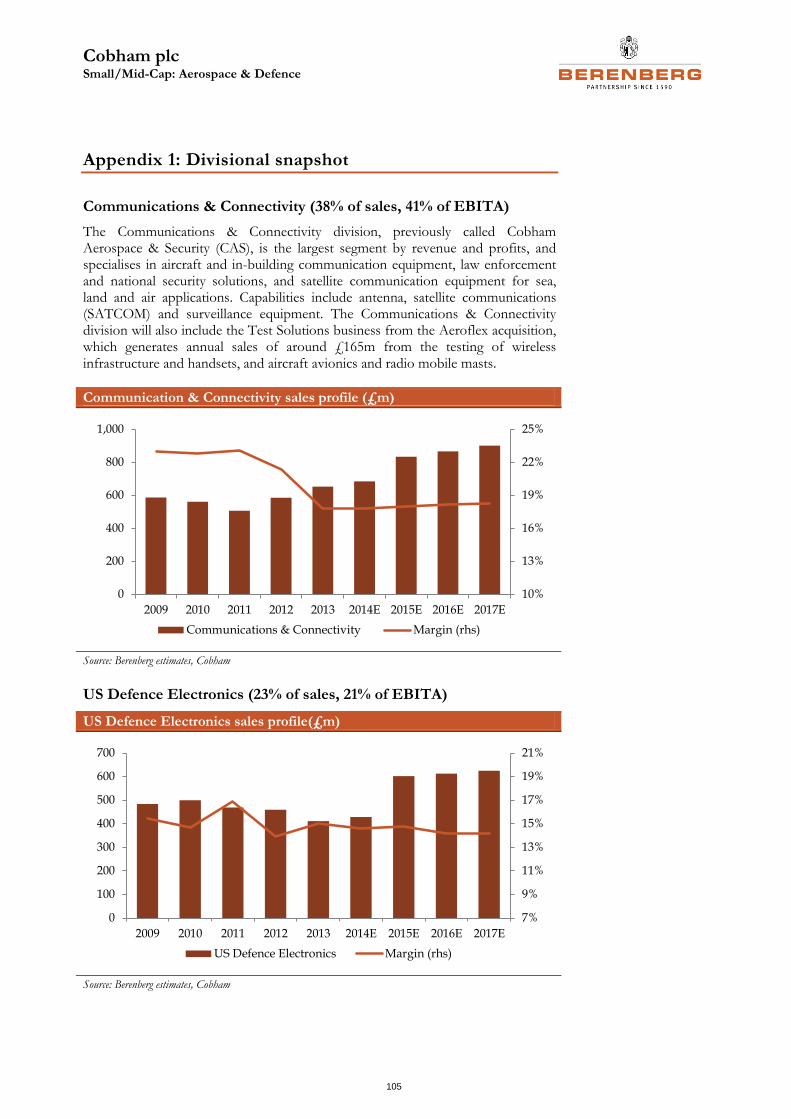

Cobham: Aeroflex is a good deal but shares are fairly valued (Hold, PT 325p – upside/downside 0%)

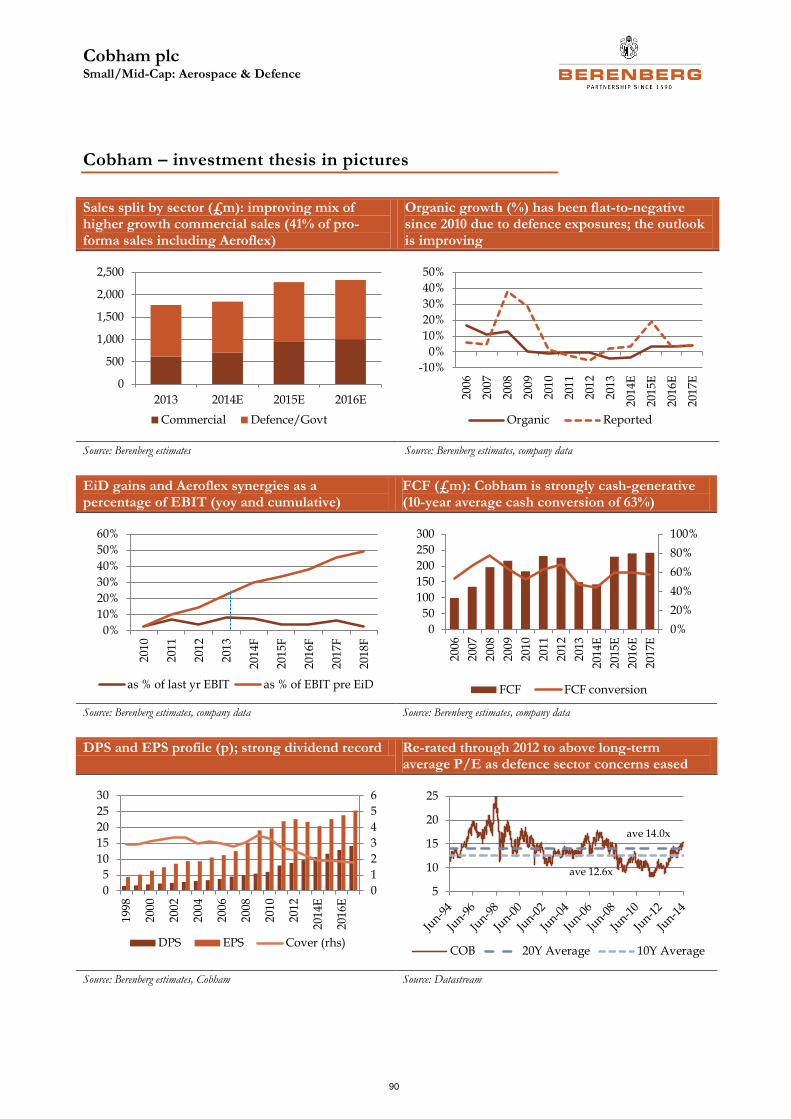

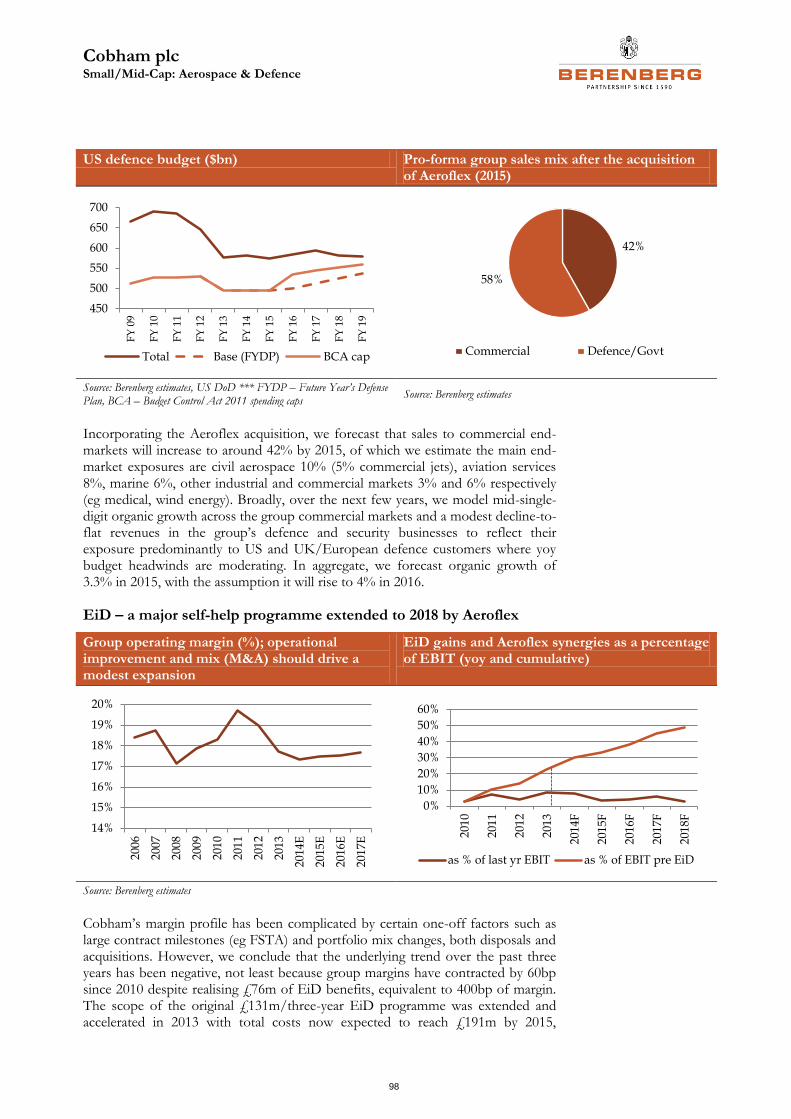

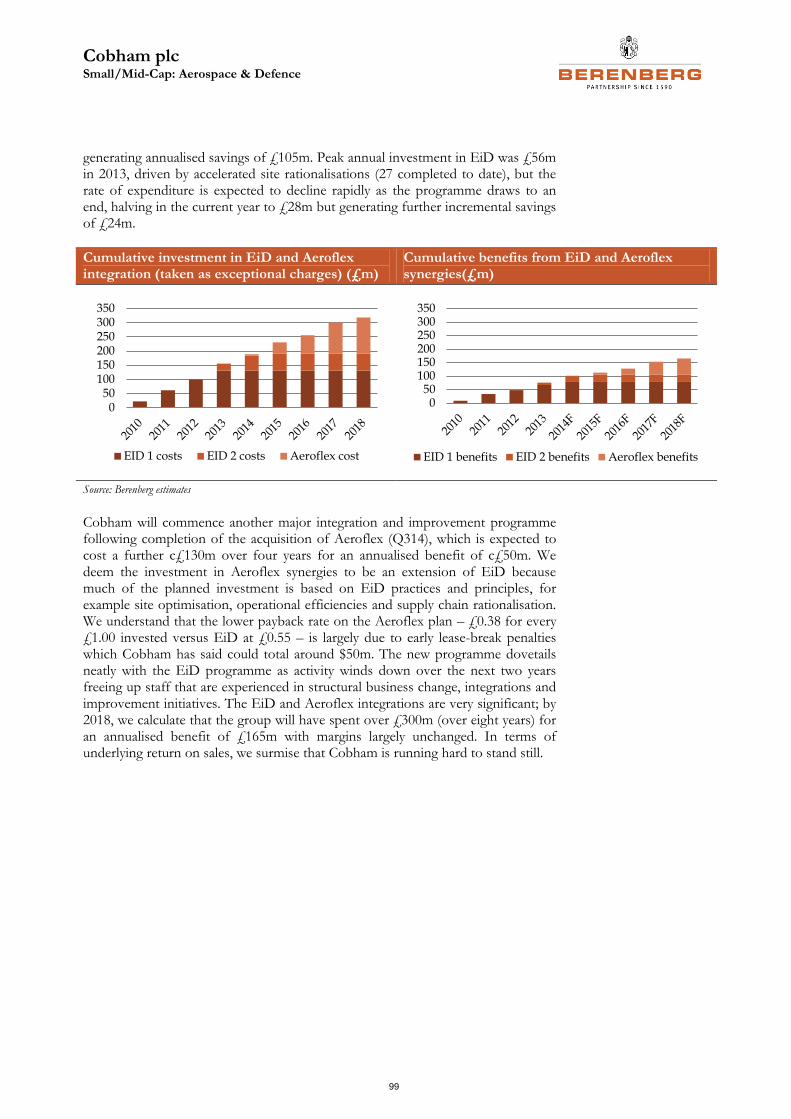

The stock has significantly outperformed since the US defence budget agreement in December and the market further welcomed the announcement in May of Cobham’s largest-ever acquisition, Aeroflex, for £870m. We agree that Aeroflex appears to be an excellent strategic and technological fit, and in raw earnings terms we estimate the transaction is c8% earnings-accretive in 2015 on an underlying basis. Integration costs are high, however, at c£130m over 3-4 years for an annualised benefit of c£50m.

Management has been consistent in longer-term guidance of delivering organic growth in 2015 (for the first time since 2008) and the outlook is enhanced by Aeroflex’s greater mix of sales in commercial sectors. As a result, Cobham has been the best-performing share in the sector ytd, up by 19% versus the sector (which is itself up by 1%) and valuation metrics are relatively full (a c14% premium to the sector on a 2015 P/E basis). Now the war chest has been spent, there is a lack of near-term catalysts and we see little upside to the equity story, hence our neutral stance.

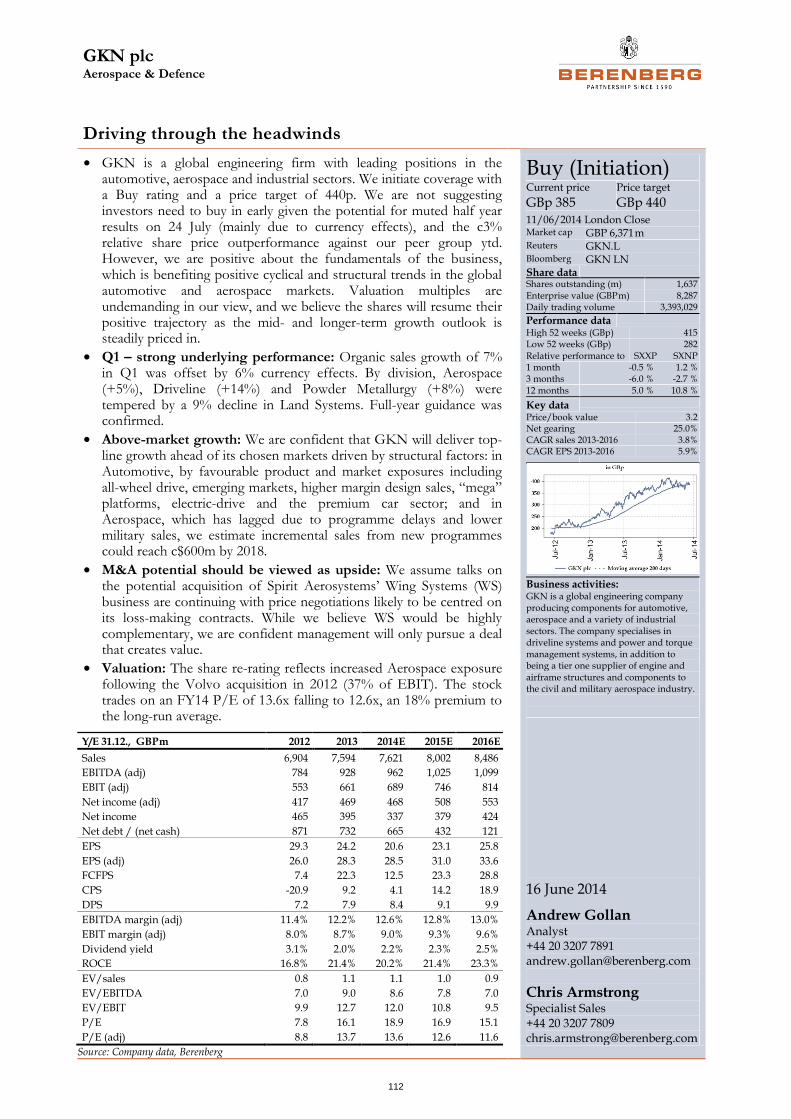

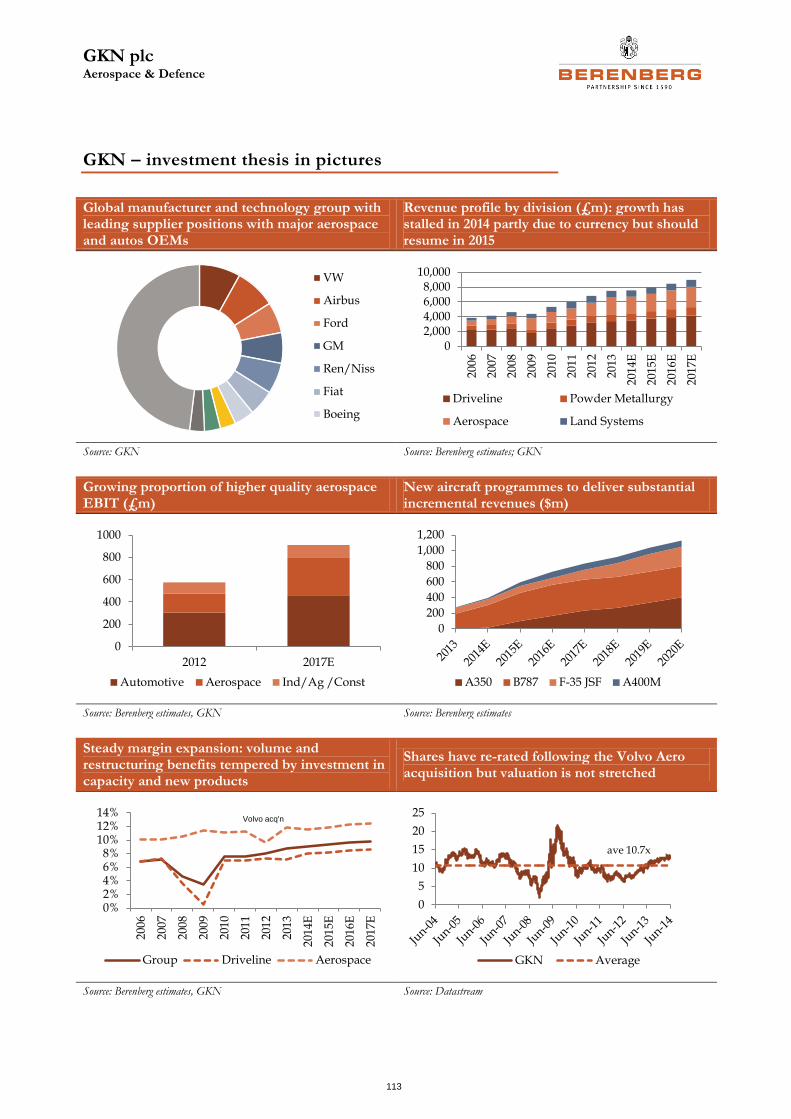

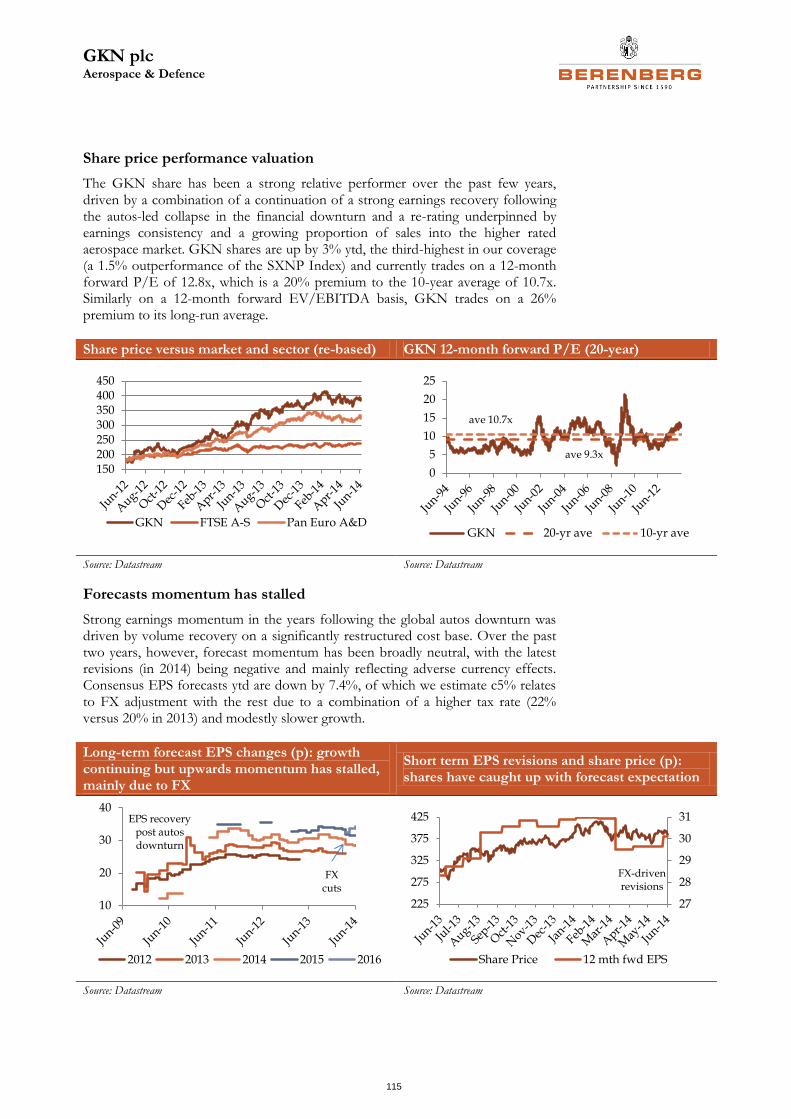

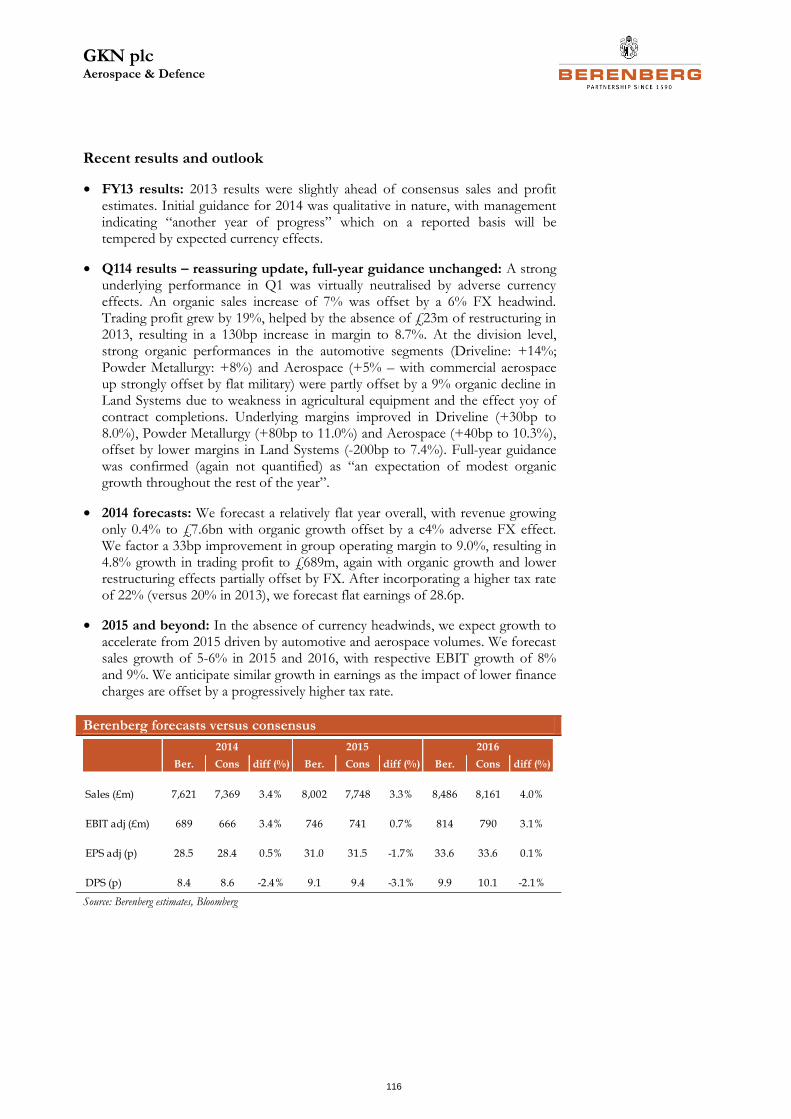

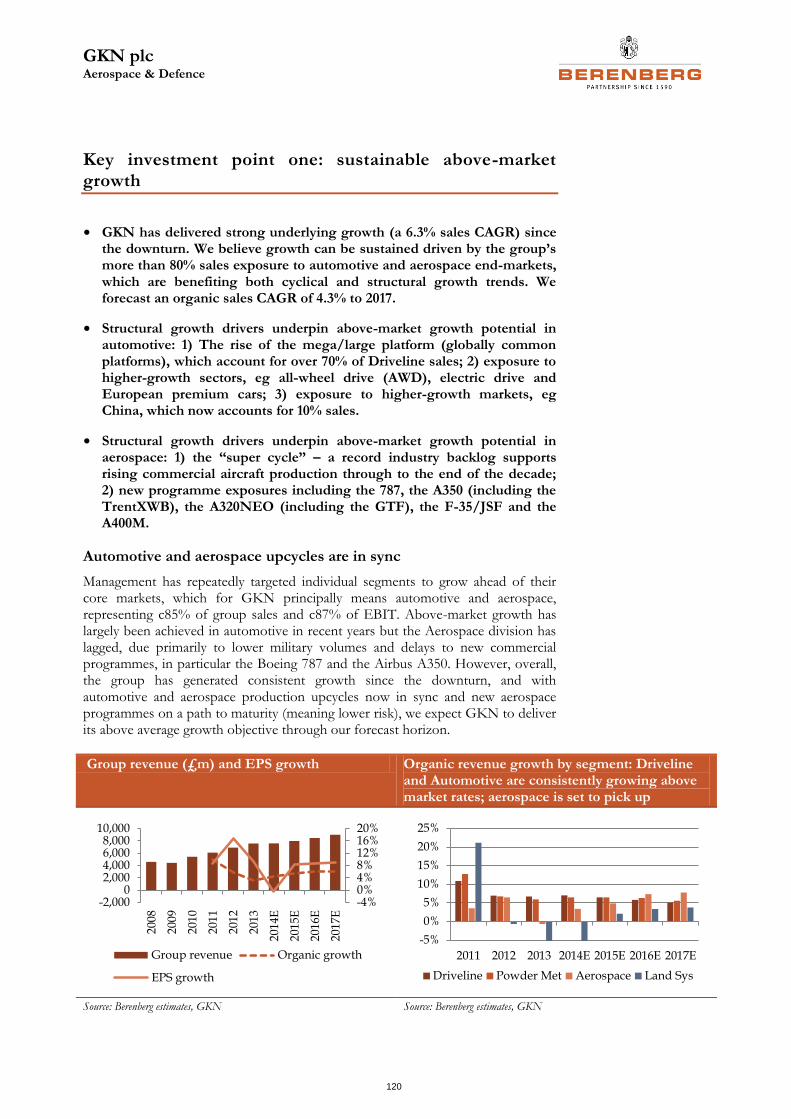

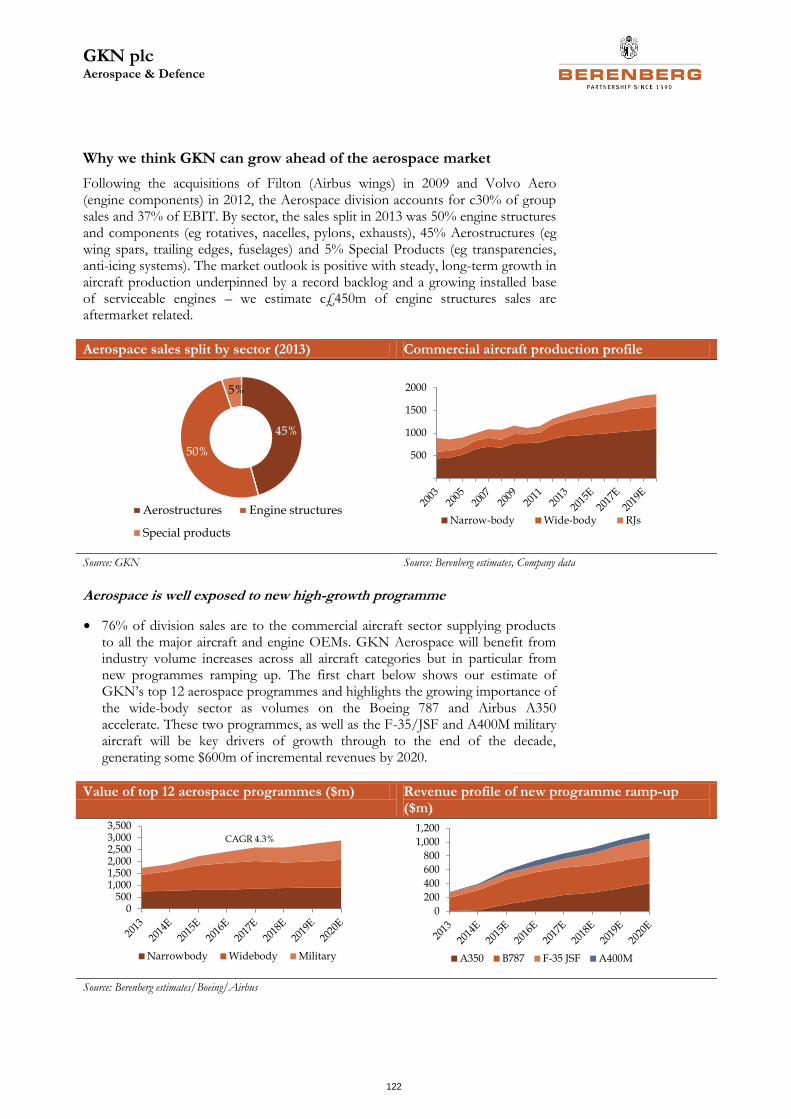

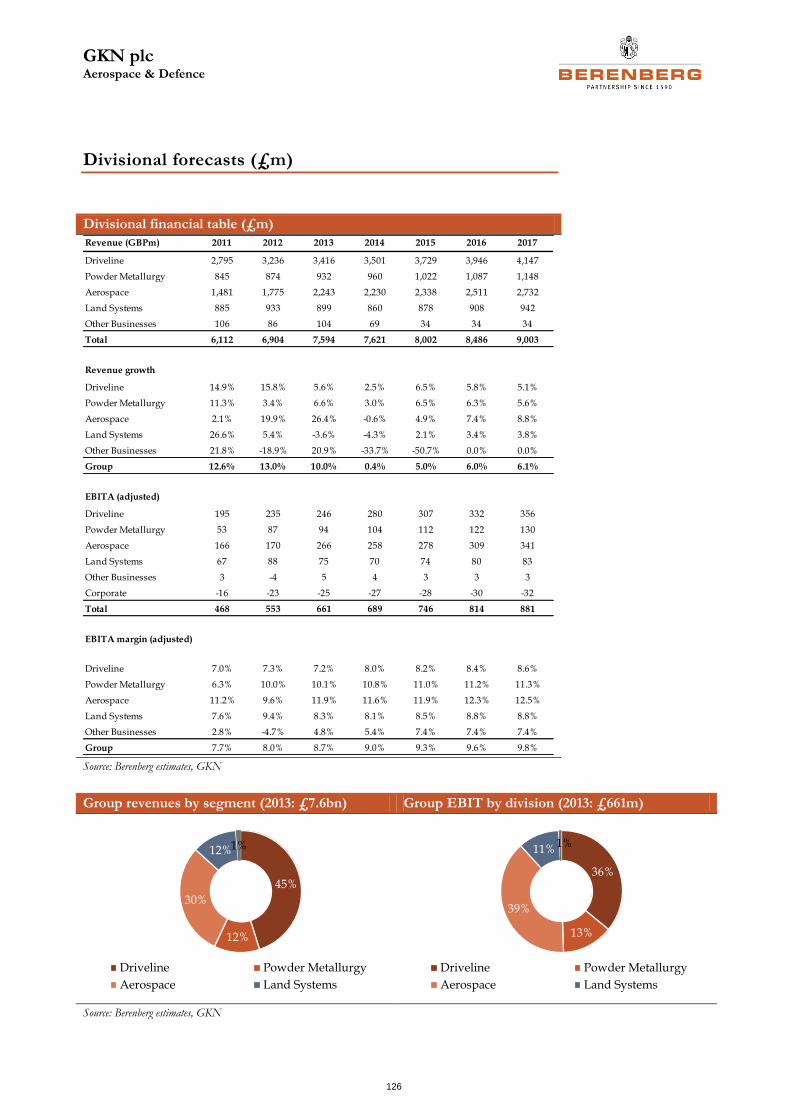

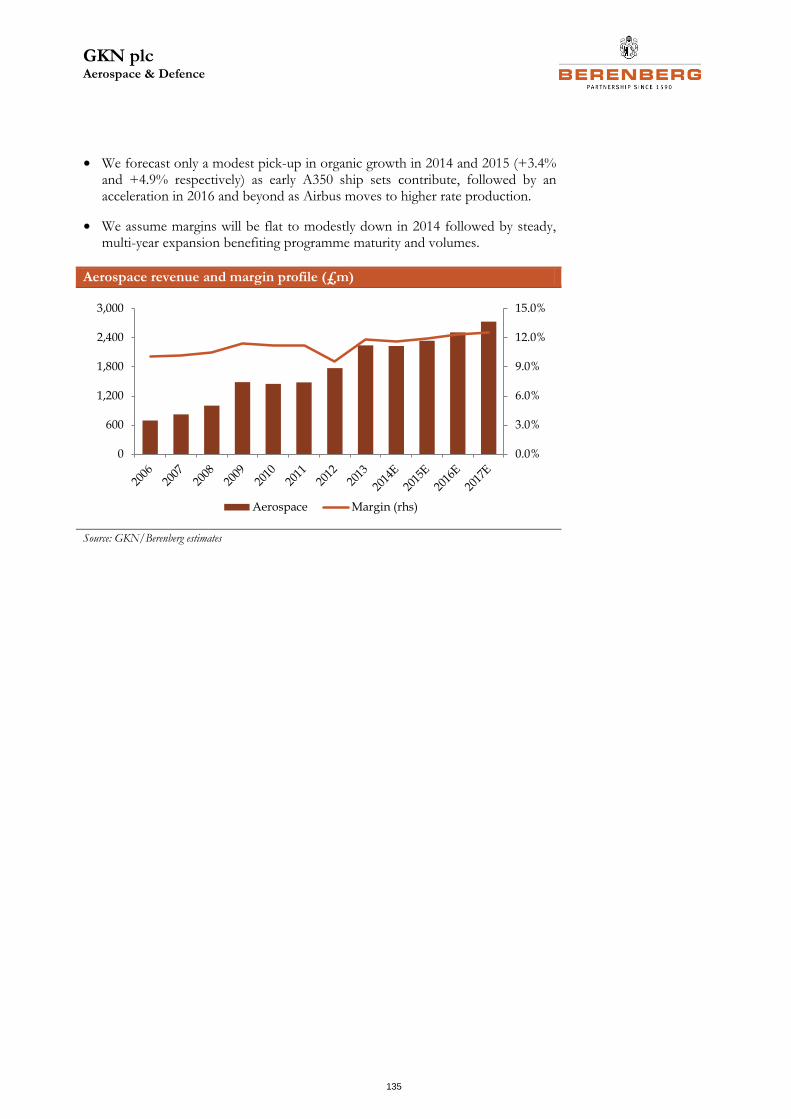

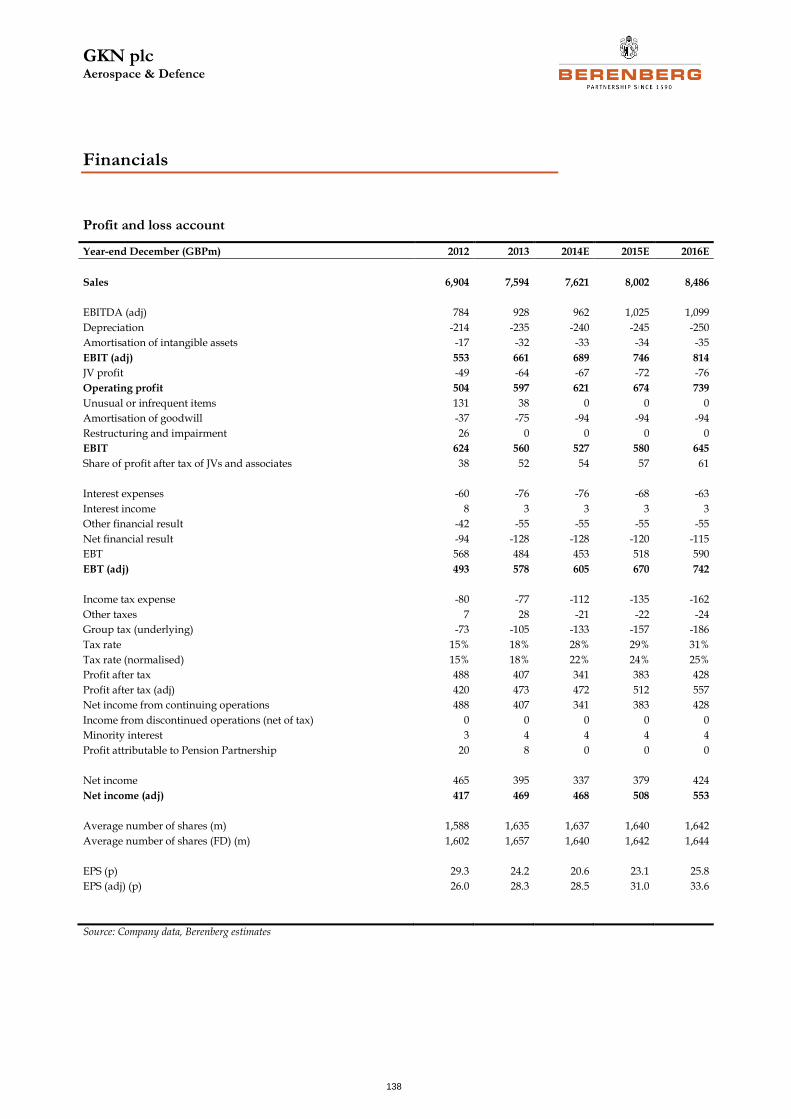

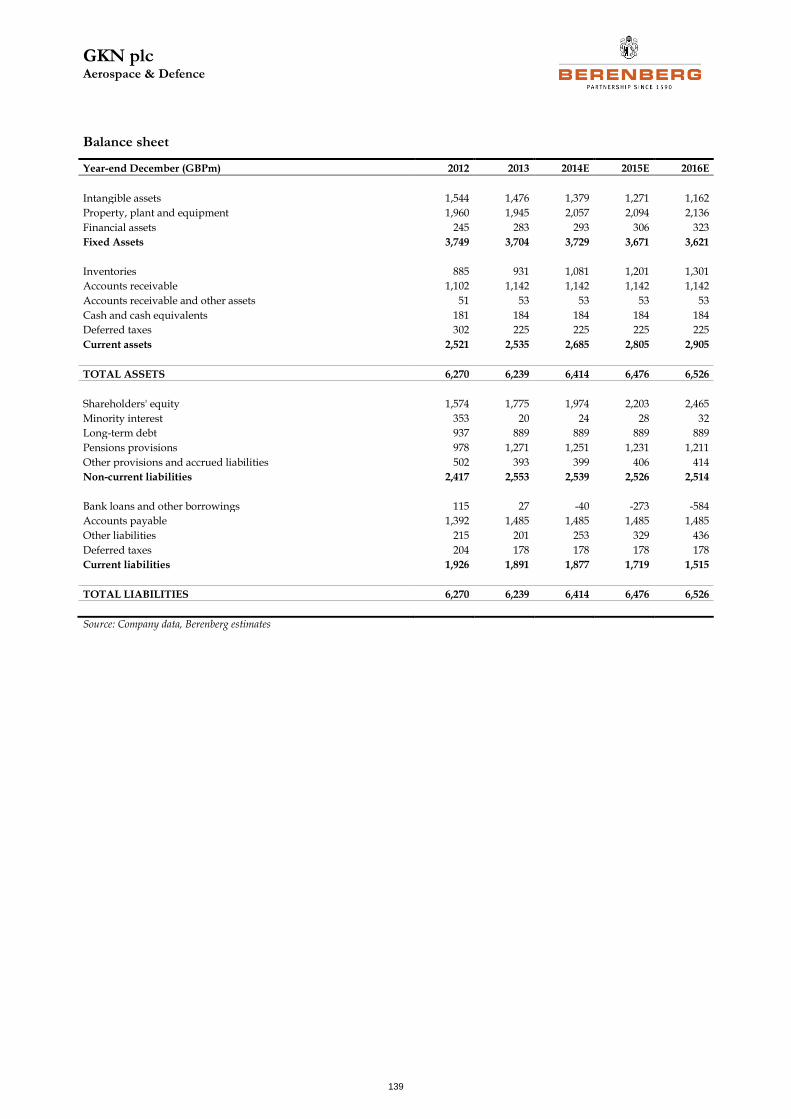

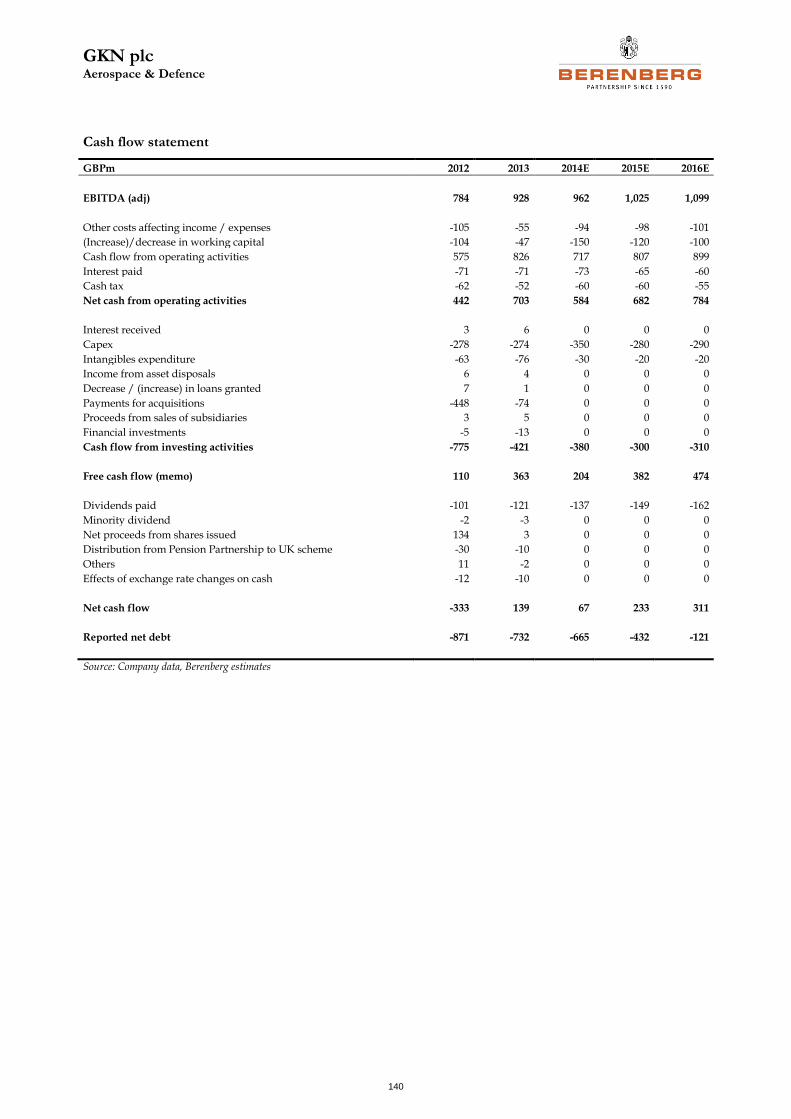

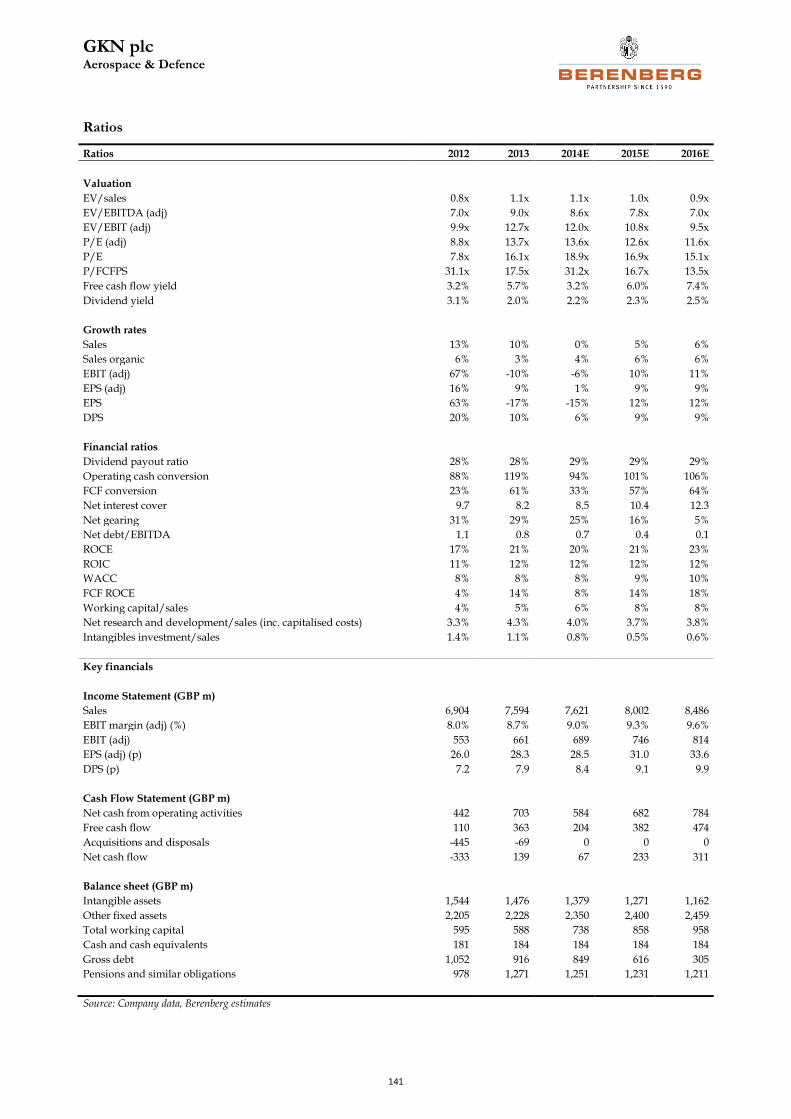

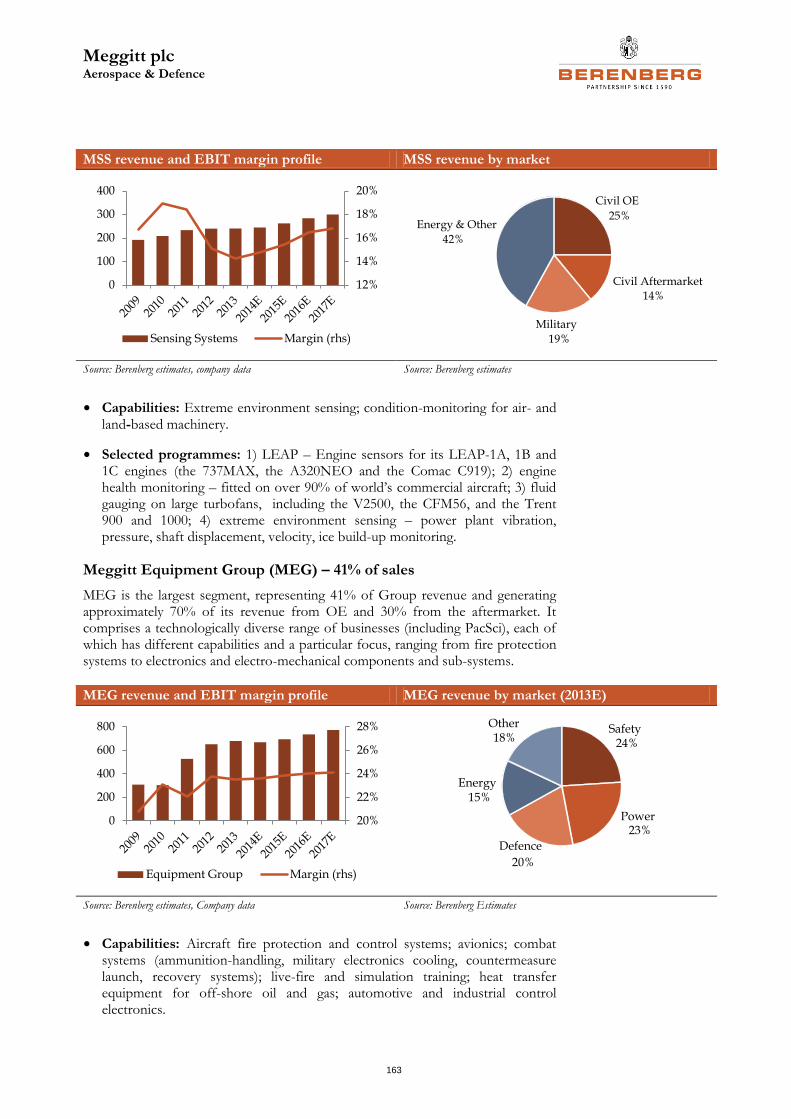

GKN: driving through the headwinds (Buy, PT 440p – upside 14%)

The fundamentals of the business are positive with the group’s two core end-markets, global automotive and aerospace, representing c85% of sales, growing concurrently. This, we believe, will translate to management’s stated ambition of sustaining revenue growth ahead of end-markets over the mid- to long term (we forecasts a sales CAGR of 4.5% and an EBIT CAGR of 7.2% to 2017). In the short term, we recognise that performance and earnings growth will be tempered by a combination of currency headwinds, the phasing of aerospace programmes (a slow ramp-up in commercial and wind-down of profitable military activity) and higher tax, which we believe will translate to a muted H1 result and flat earnings for the year.

Aerospace & Defence

12

Uncertainty about potential large-scale M&A may also affect sentiment, with discussions ongoing (we believe) with Spirit Aerosystems to acquire its underperforming Wing Systems (WS) business. WS would be highly complementary to GKN’s existing Airbus wing structures business, significantly increasing the group’s exposure to Boeing and other airframers. Management has a good M&A track record and hence we are confident it will not overpay if a transaction progresses. We believe the market is price-neutral on a potential deal and hence we think it should be viewed as upside should it progress. In summary, while we see potential for some share price volatility over the shorter term, the fundamental outlook for GKN is positive. The rating is not particularly demanding and we expect the shares price to steadily advance as the growth trend resumes.

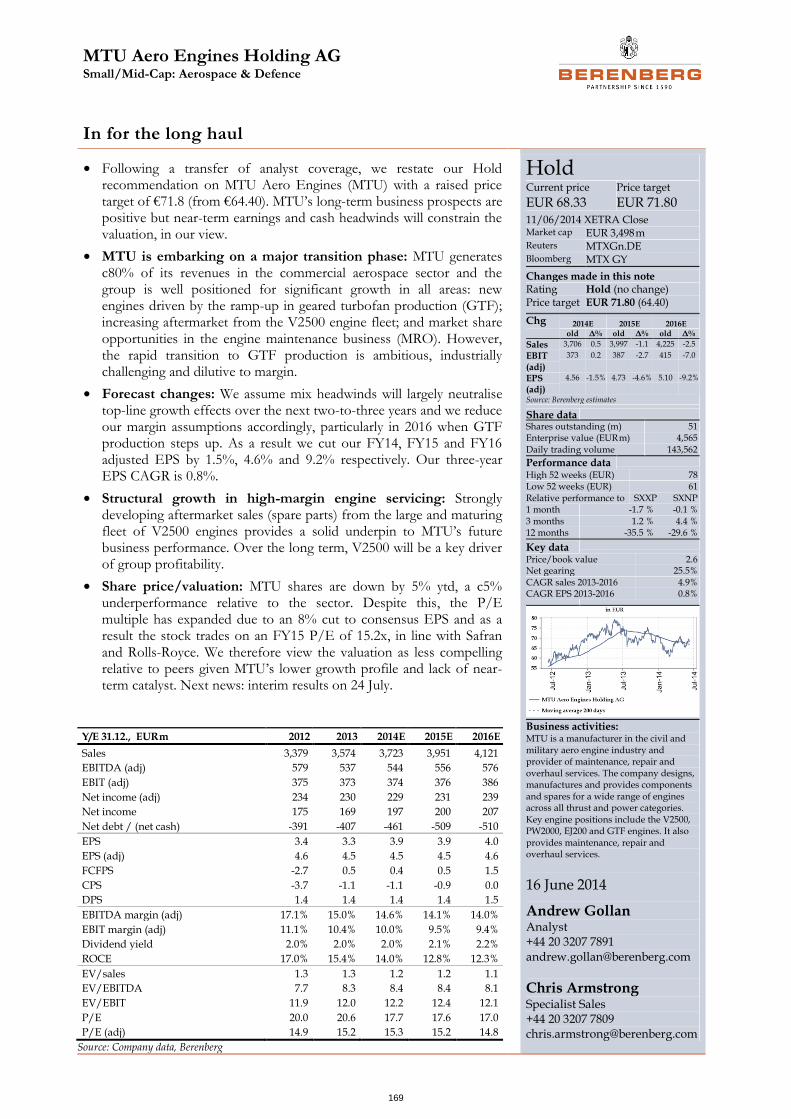

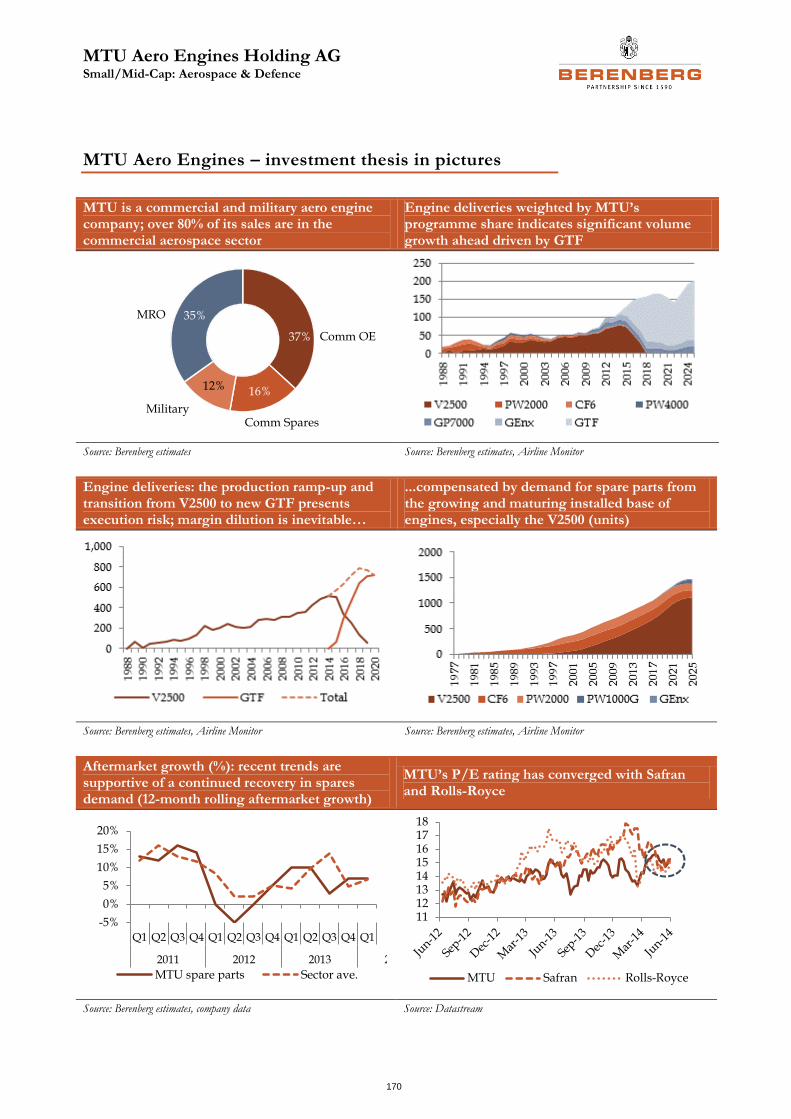

MTU Aero Engines: in for the long haul (Hold, PT €71.8 – upside 5%)

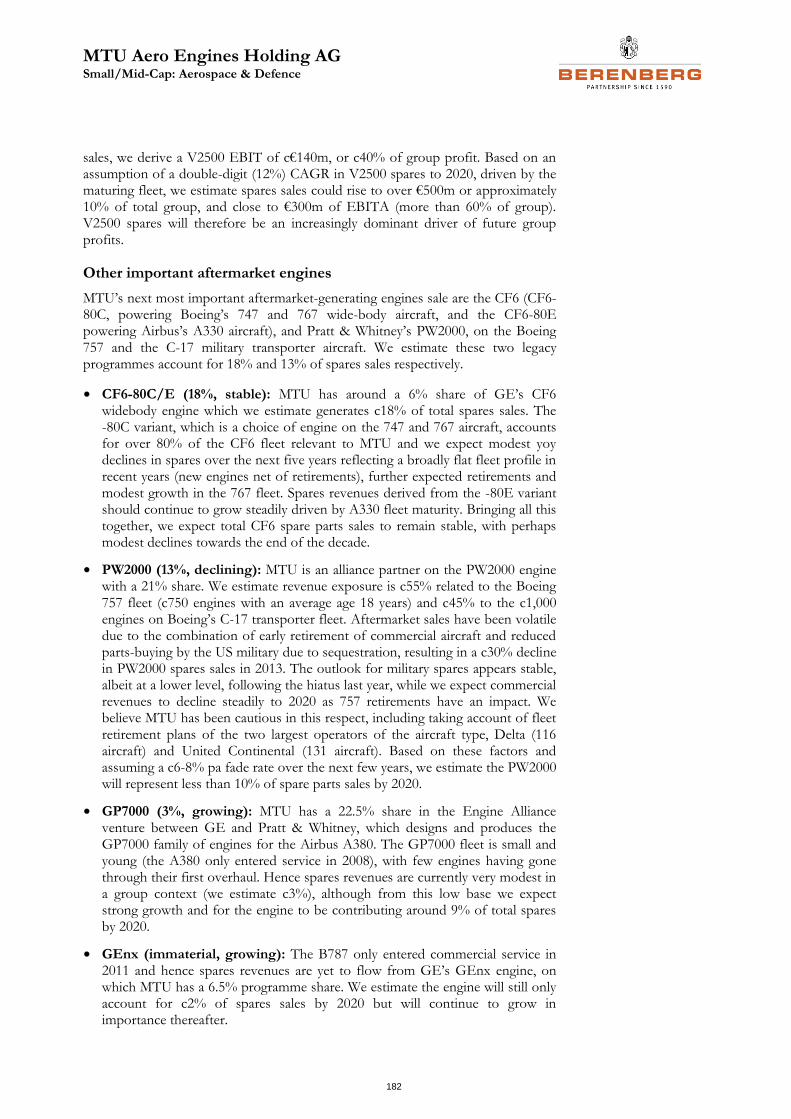

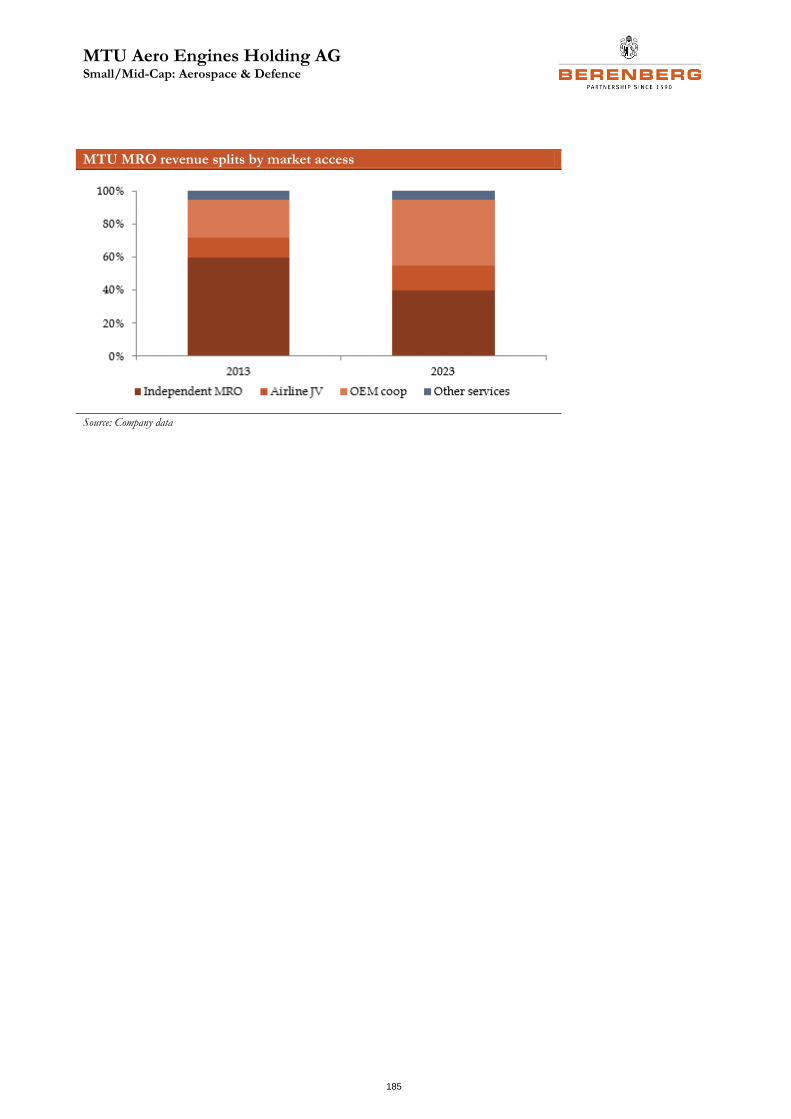

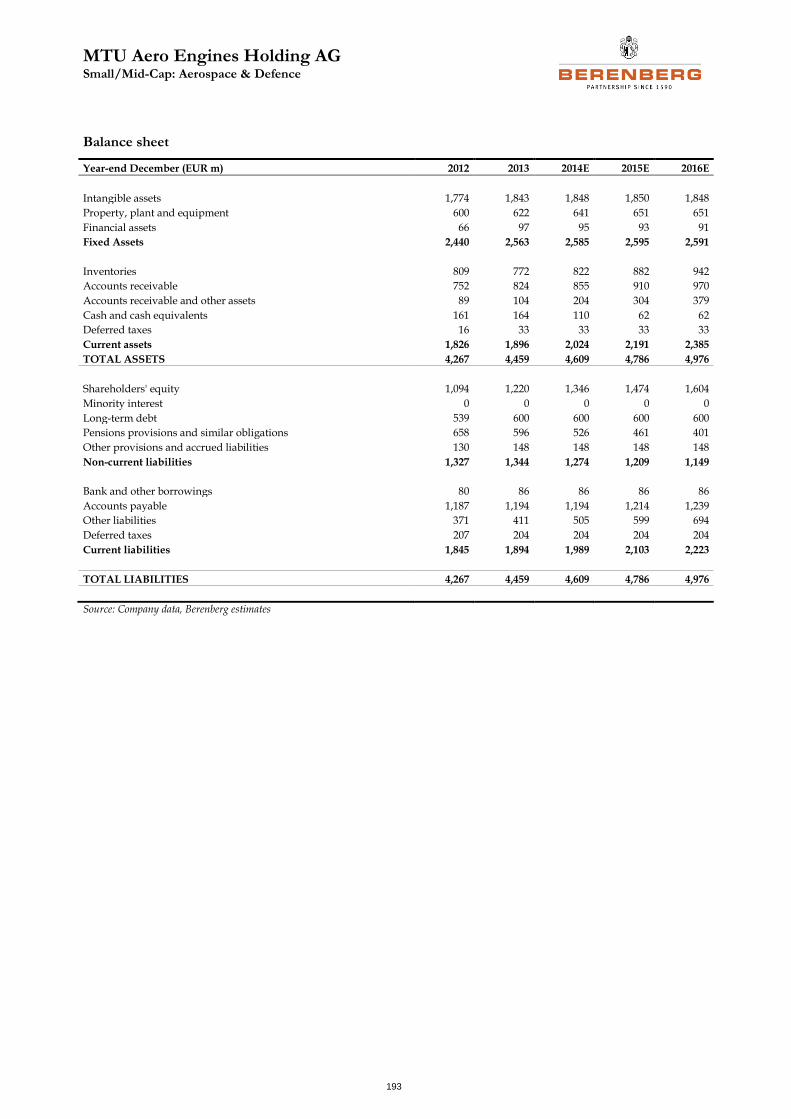

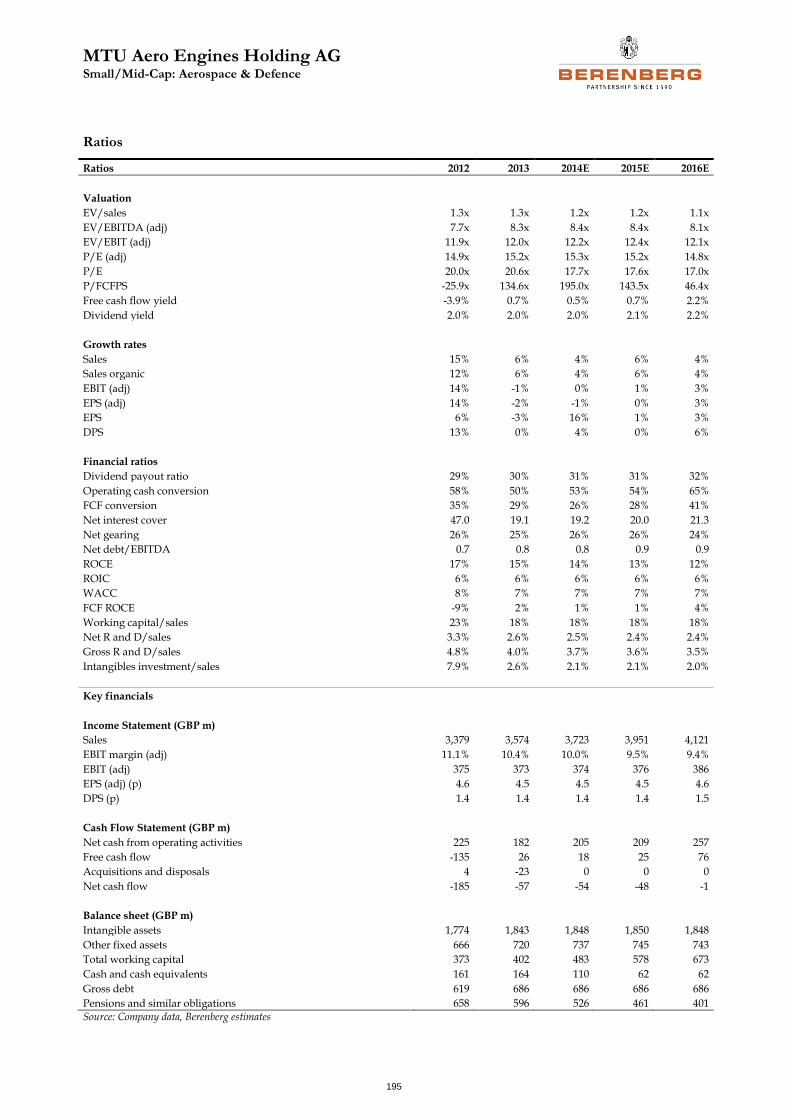

MTU generates c80% of its revenues in the commercial aerospace sector and the group is well positioned for significant top-line growth in all areas: new engines driven by the ramp-up in geared turbofan production (GTF); increasing aftermarket from the V2500 engine fleet; and market share opportunities in the engine maintenance business (MRO).

However, the rapid transition to GTF production over the next three to four years is ambitious, industrially challenging and dilutive to margin due to losses on new engine sales. We believe mix headwinds from the GTF will largely neutralise the positive impacts of volume growth and continuous strong momentum in the high margin V2500 spare parts business, as the expanding fleet of engines mature. The ramp-up of activity on the GTF will also lead to cash challenges over the next few years which, although well understood by the market, will combine with low profits growth to constrain the valuation in the near term. We think MTU remains a great long-term growth story once GTF production matures and the V2500 aftermarket story develops further, and we are comfortable that investors with long-term horizons will enjoy positive long-term returns. However, following the recent rally in the share price, MTU’s valuation metrics have converged with Safran and Rolls-Royce and hence we see limited upside in the near term on both an absolute and relative basis.

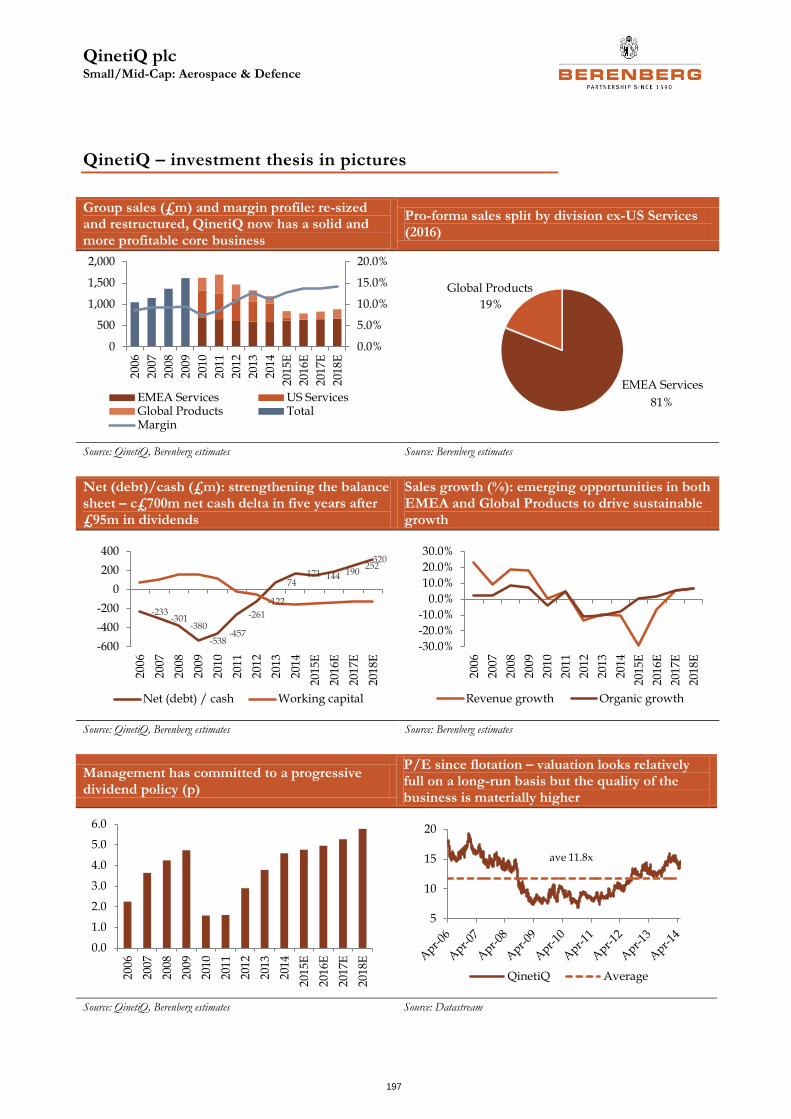

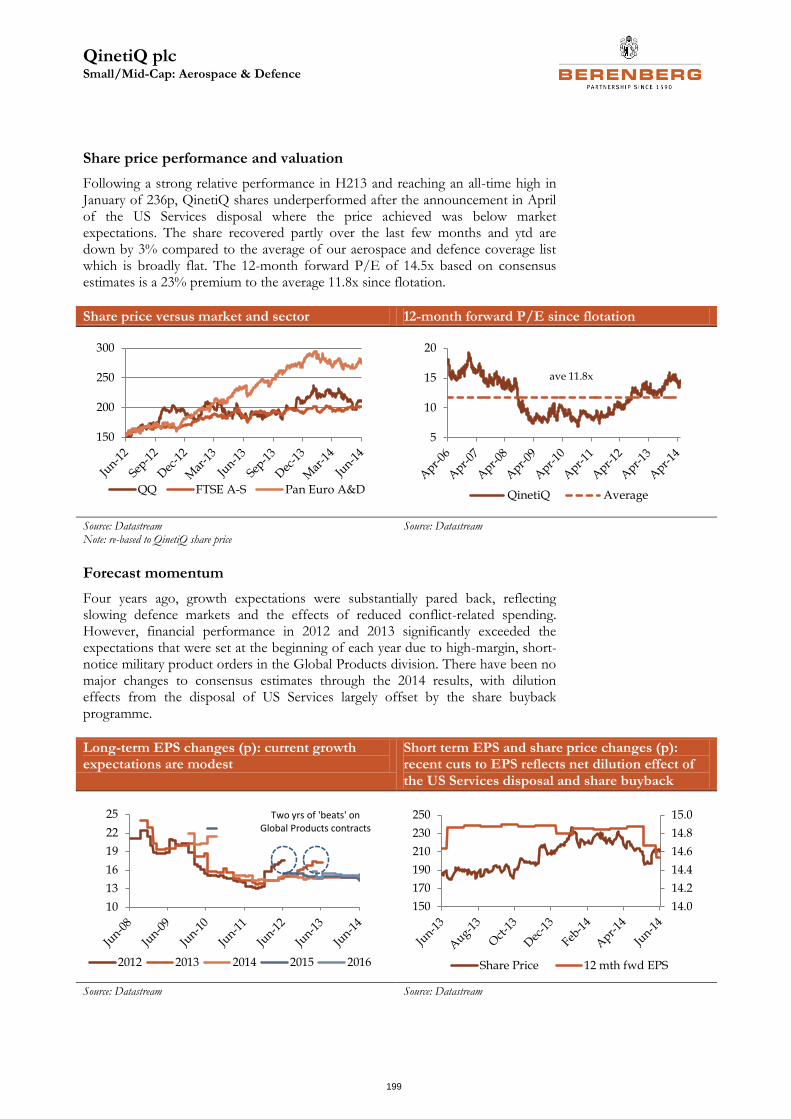

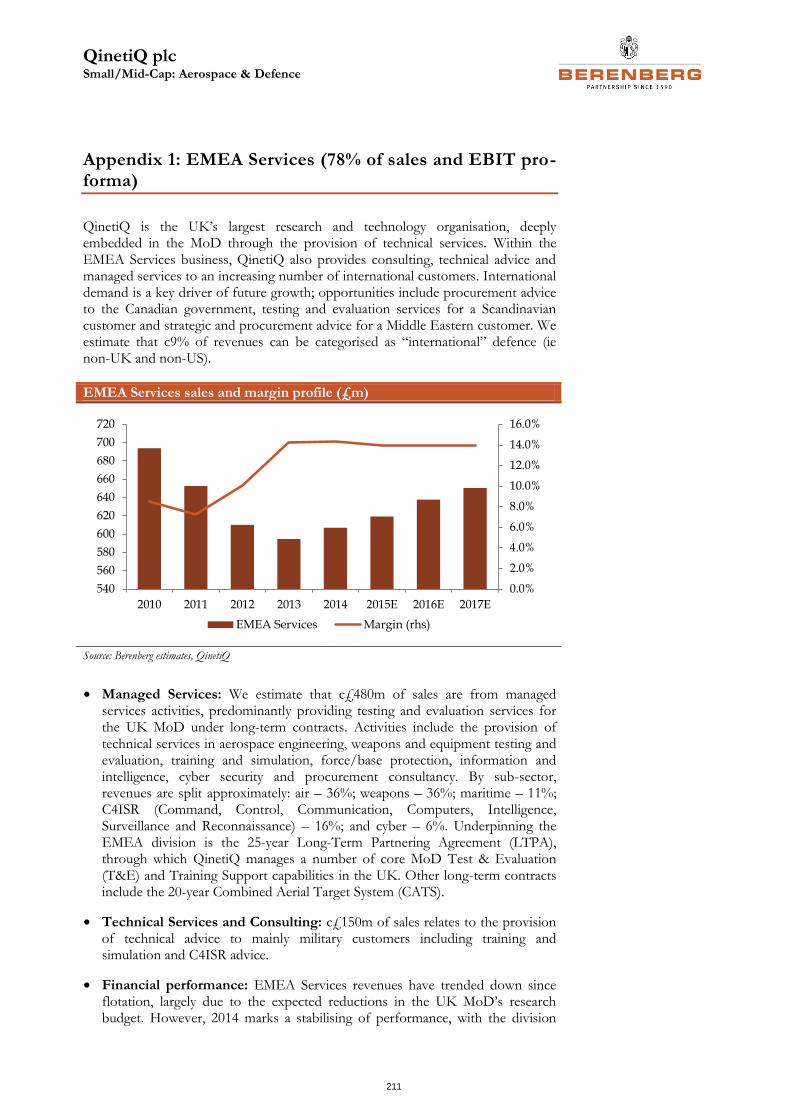

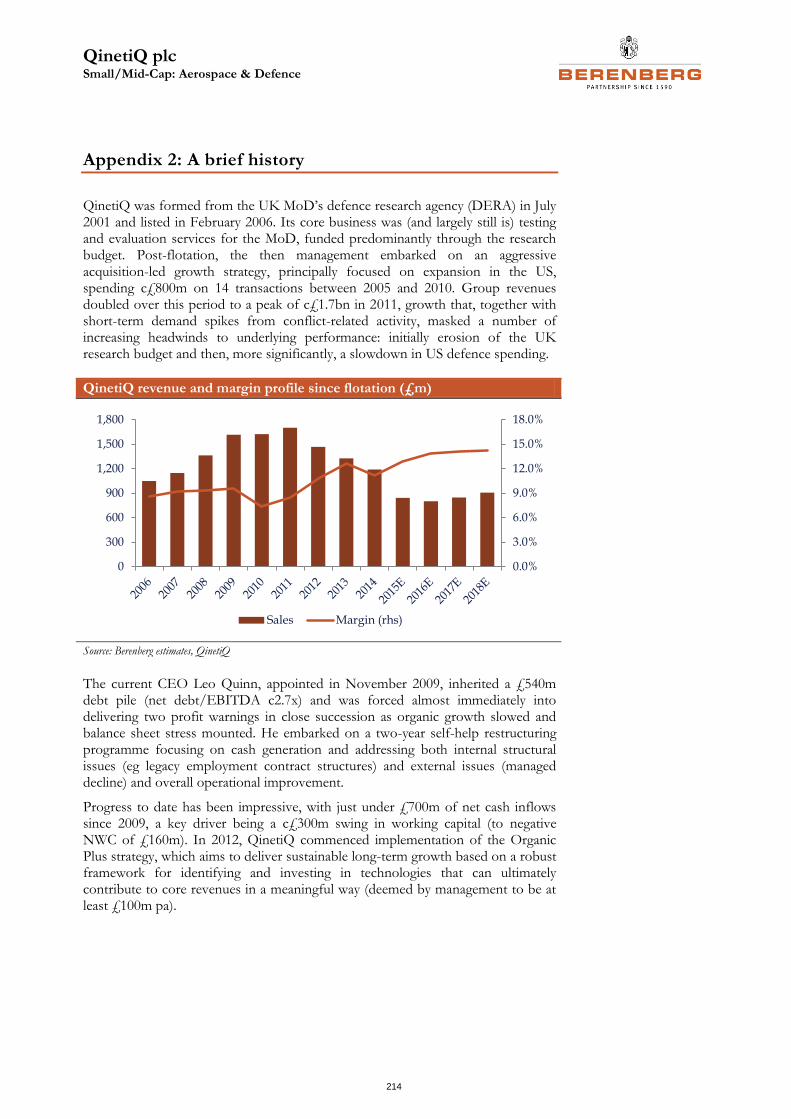

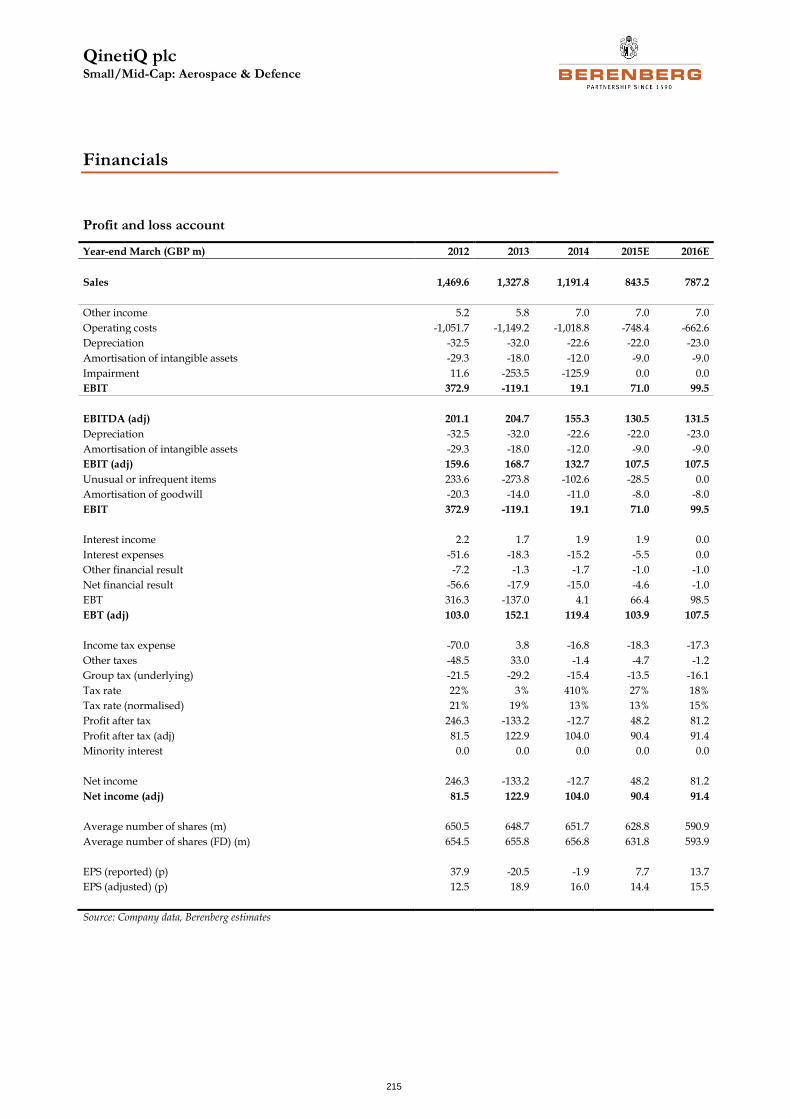

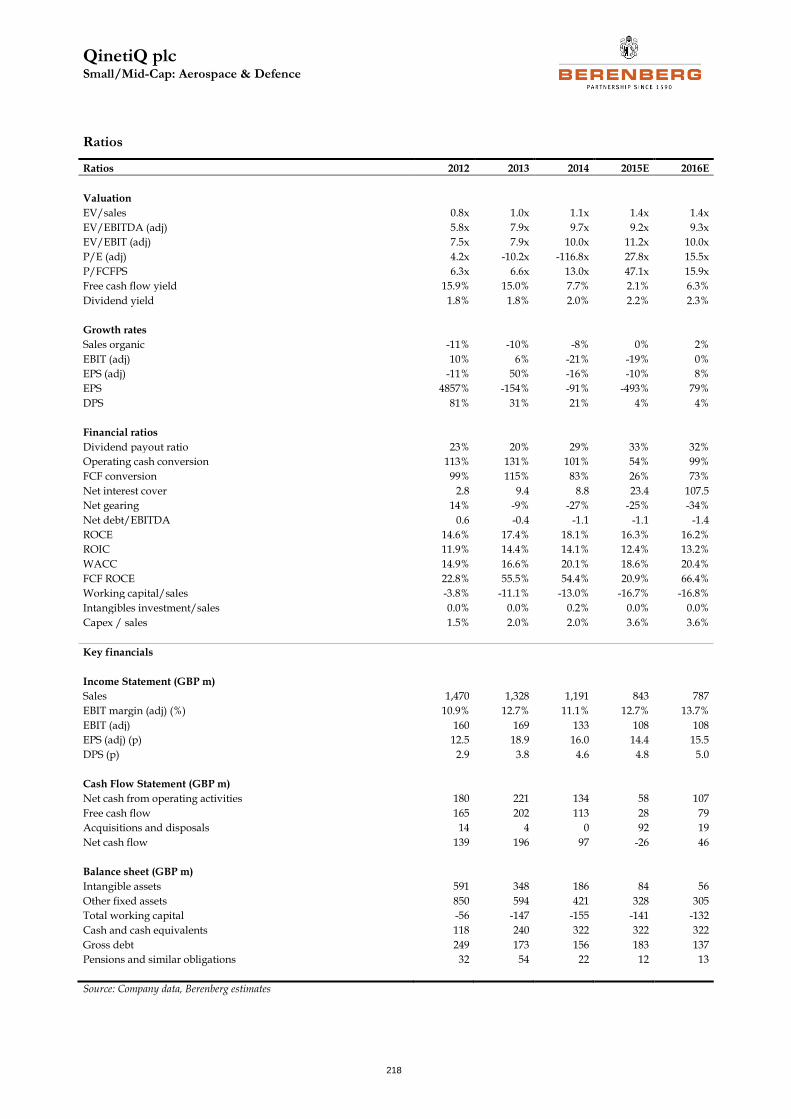

QinetiQ: looking ahead again (Hold, PT 225p – upside 7%)

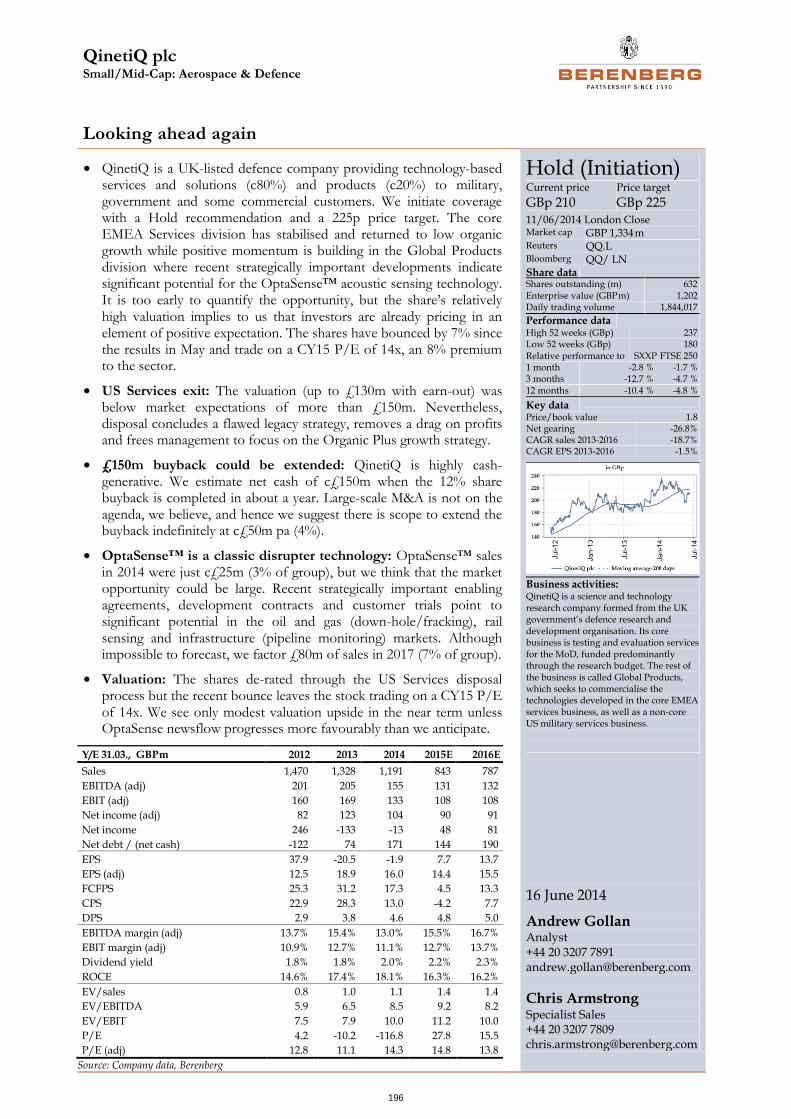

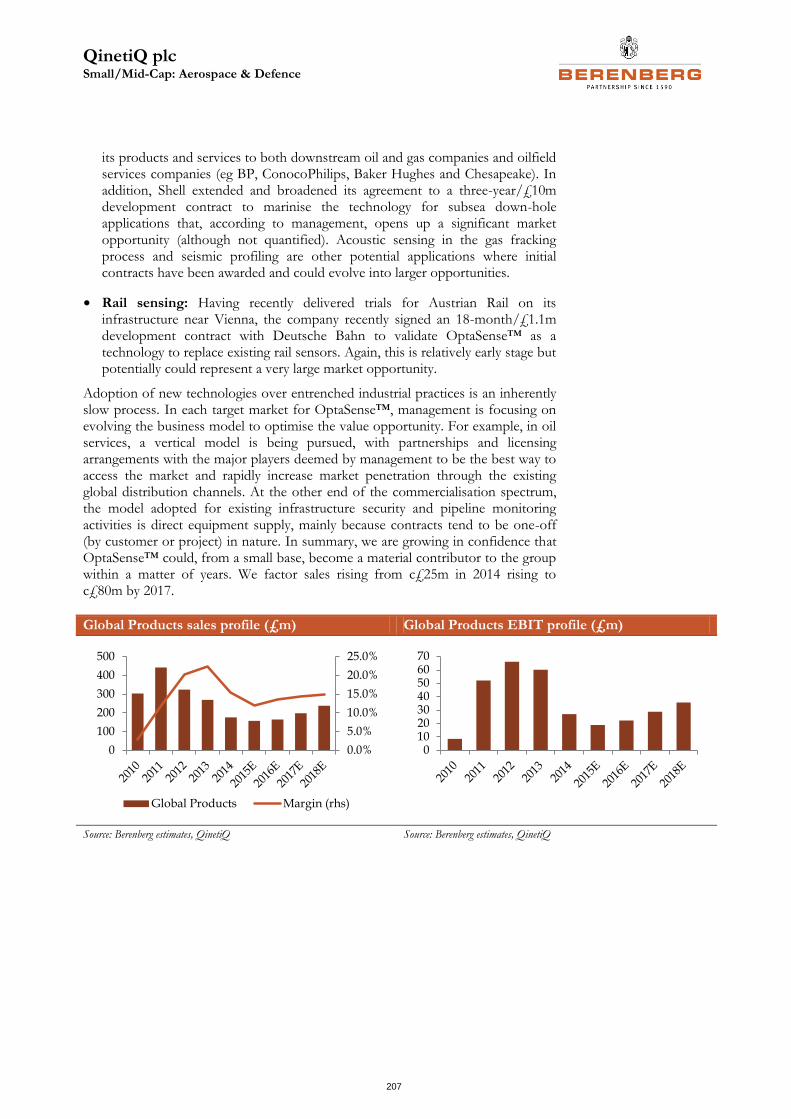

The valuation achieved on disposal of the US Services business (up to £130m) was below market expectations but it concludes a flawed strategy of the previous management and removes a drag on profit. QinetiQ has commenced returning excess cash through a £150m buyback (equivalent to 12% of the current market cap) and we suggest there is scope to extend this indefinitely at c£50m pa based on continued strong cash generation. After years of top-line decline, it is encouraging that the group’s core EMEA Services division has stabilised and returned to low organic growth with the emergence of new opportunities, for example in international markets. However, the main value hook for investors is the momentum building in the Global Products (GP) division. While the strategy to broaden the GP product range has been slow, recent strategically important developments indicate significant potential for the OptaSense™ acoustic sensing technology. It is still too early to quantify the opportunity and we monitor developments closely but given the share’s relatively high valuation, it implies to us that investors are already pricing in an element of positive

Aerospace & Defence

13

expectation. The shares have bounced by 8% since the results in May and trade on a CY15 P/E of 13.8x, a 15% premium to the sector.

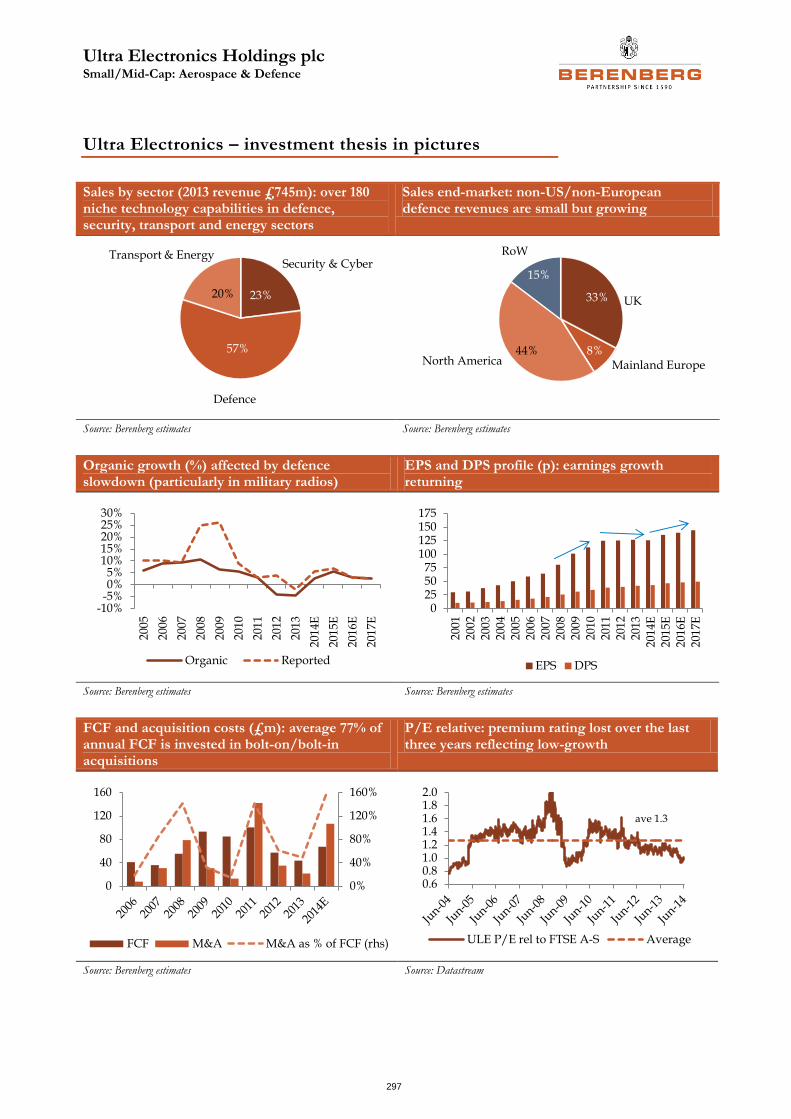

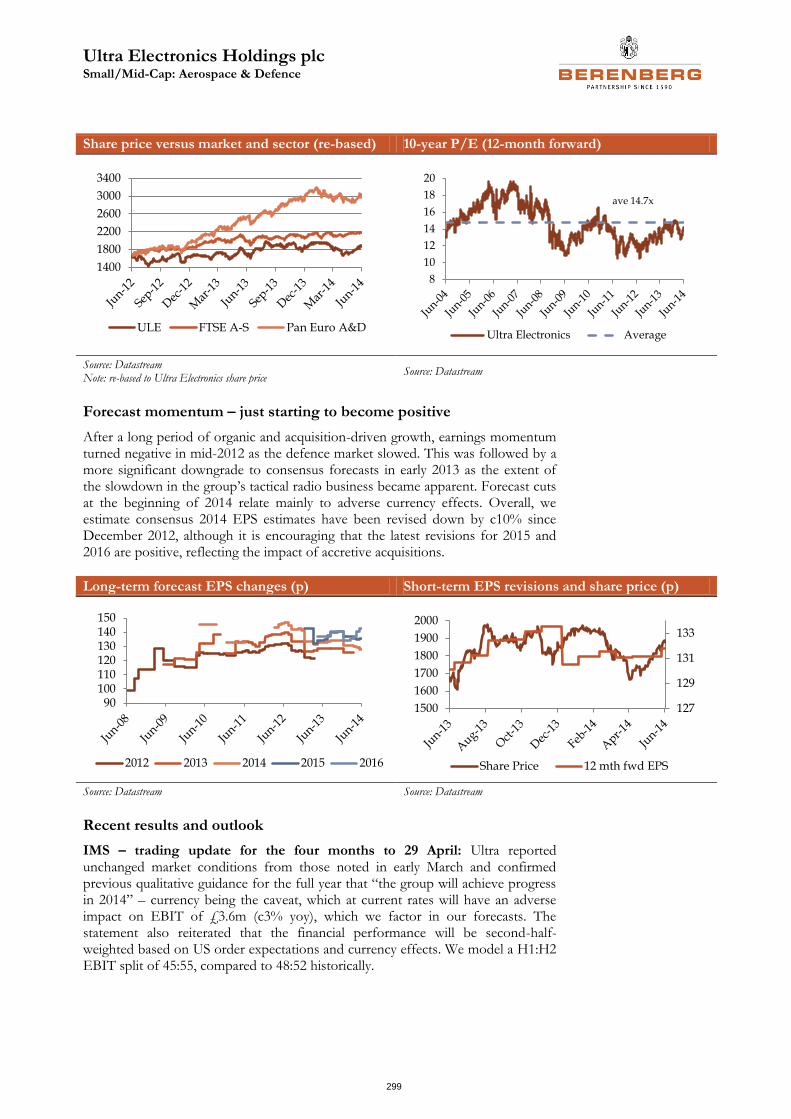

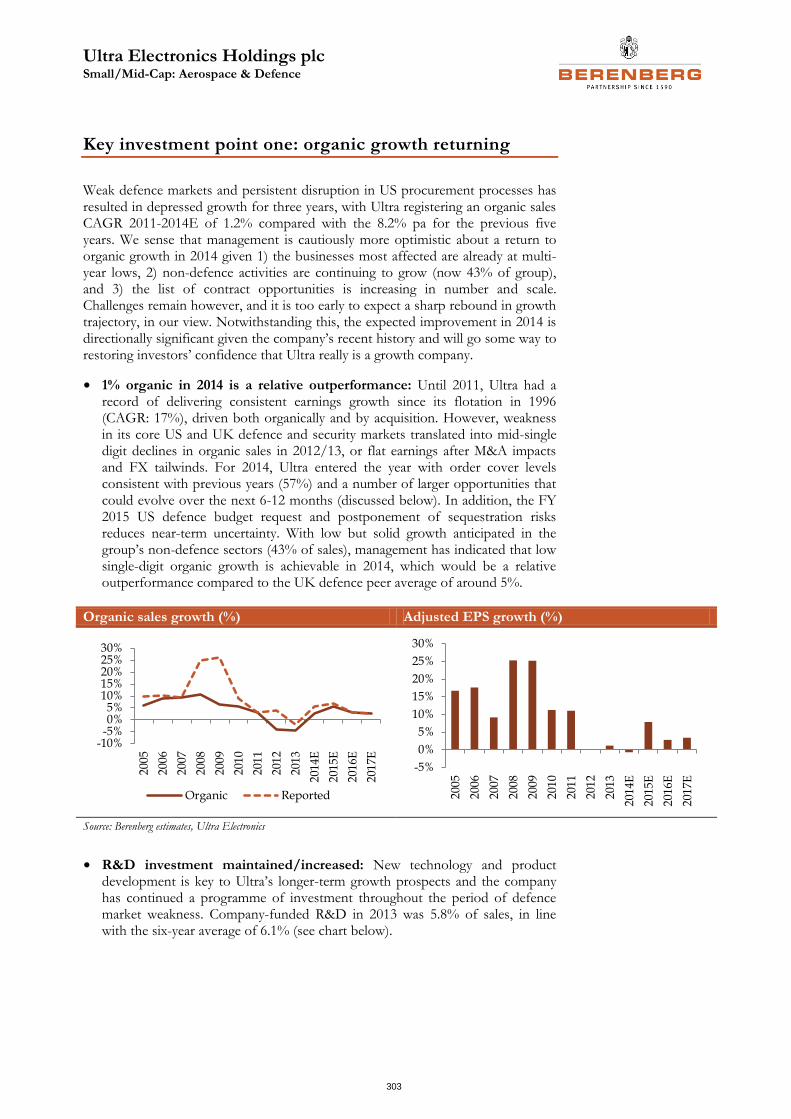

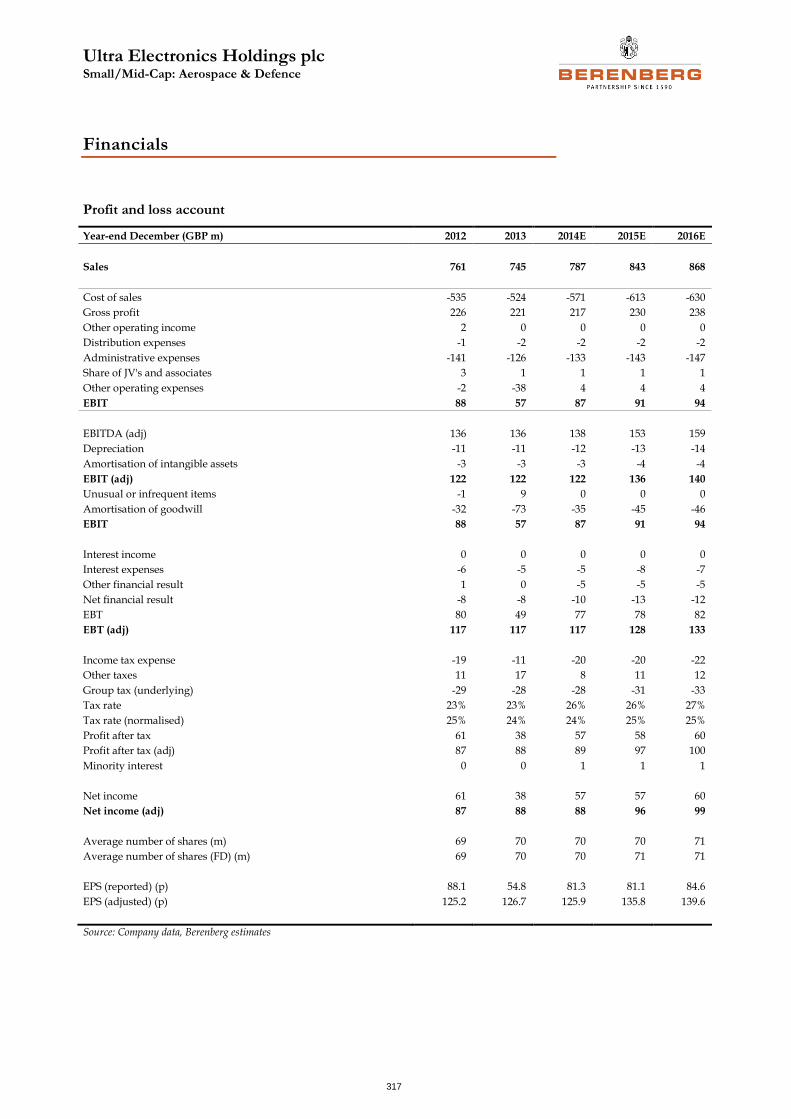

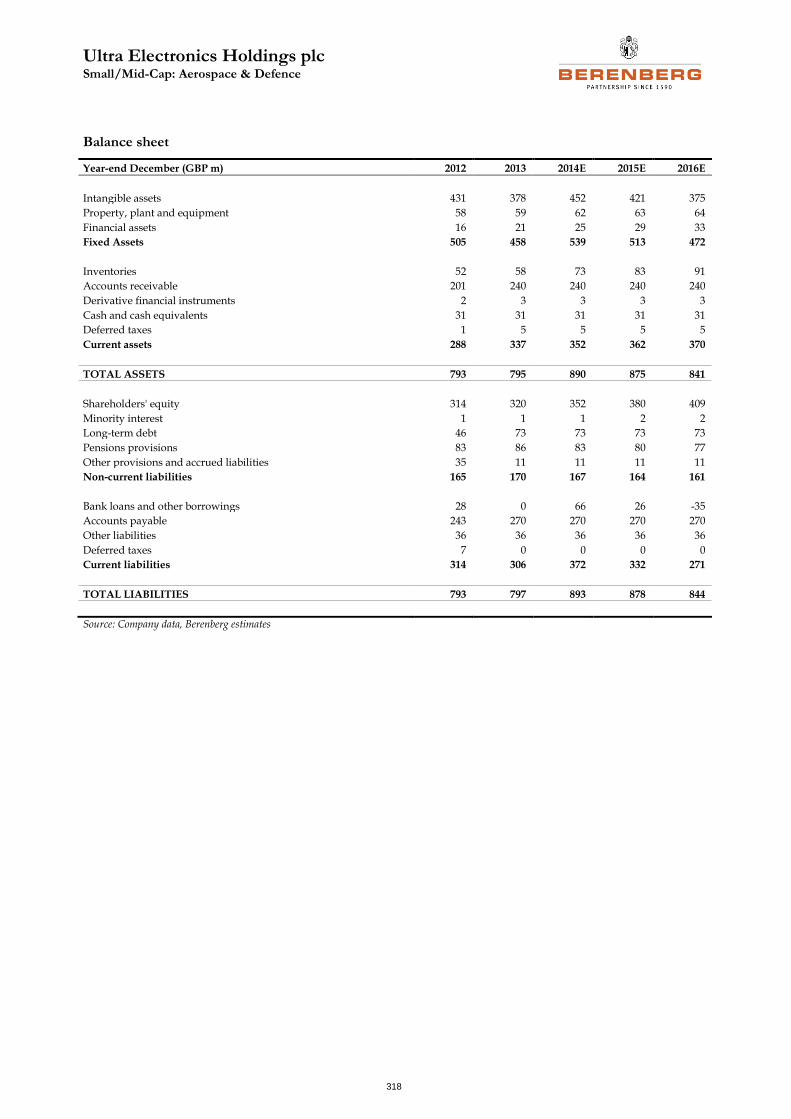

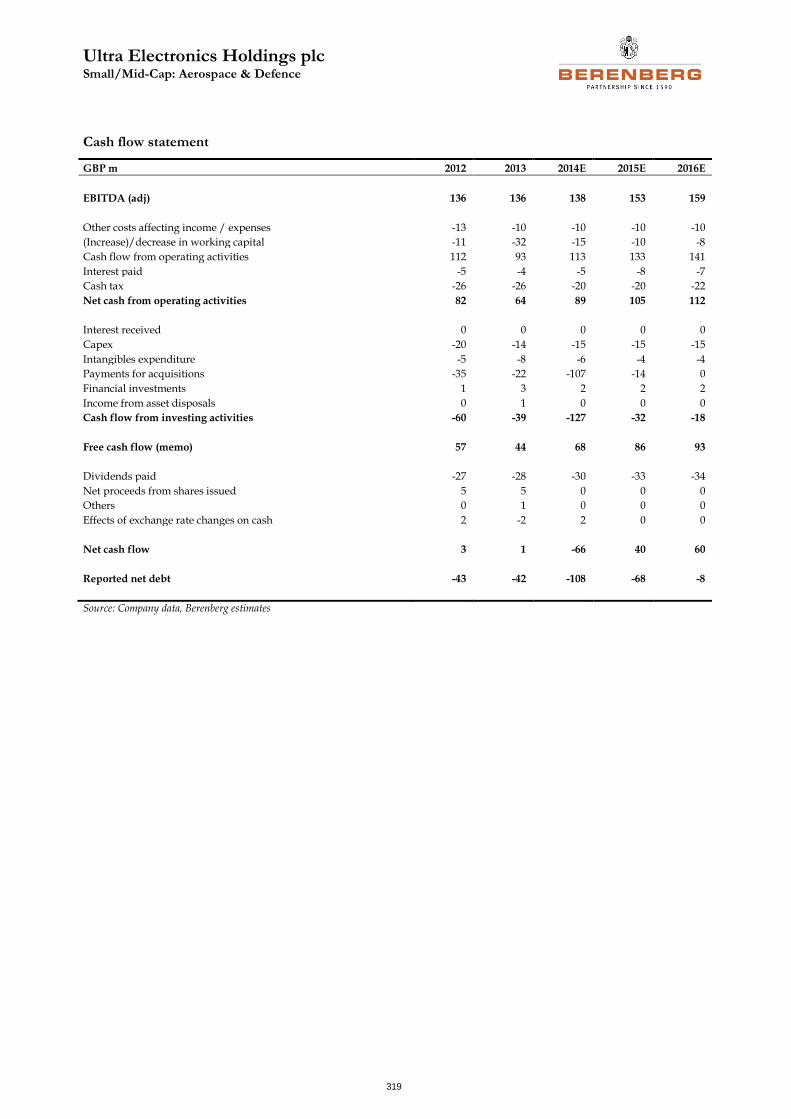

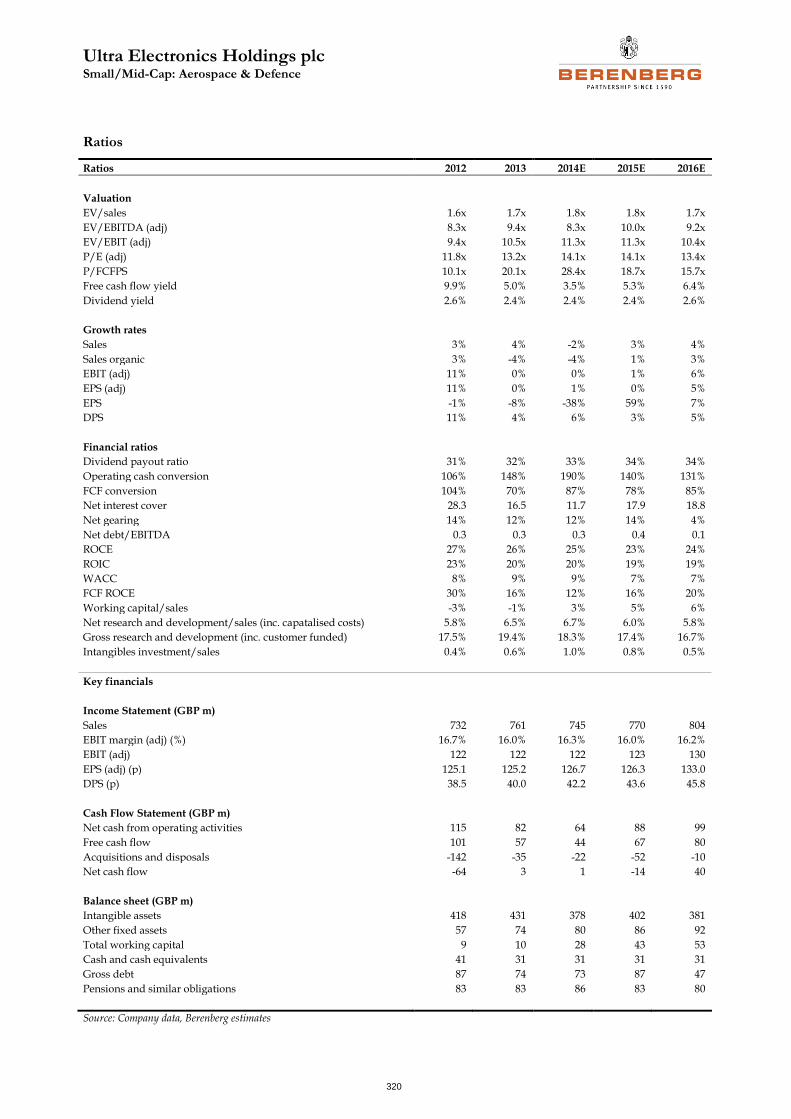

Ultra Electronics: cautious optimism (Hold, PT 1,970p – 5% upside)

Ultra is a high-quality, technology-rich electronics company with a broad range of specialist capabilities in the defence, security, transport and energy sectors. Set against the group’s high standards and long-term record of growth, the business has weathered a difficult three years in slowing defence markets which in 2014 is likely to culminate in another year of flat earnings with low organic and M&A-driven growth offset by currency effects. However, we are cautiously optimistic that Ultra can return to sustained EPS growth driven by large contract opportunities, growing non-defence activities and further potential upside from acquisitions. Indeed, M&A activity has already picked up, with over £100m of transactions announced ytd. In addition, Ultra has recently announced a number of sizable new contracts supporting our view that the company can deliver steady earnings growth over the next few years. The shares oversold following the March prelims but have since rallied on the back of the contract newsflow and acquisitions. In summary, notwithstanding the potential for some volatility through the interim results (due to a strong weighting to H2), we view Ultra as a high-quality, low-risk investment proposition, but now with insufficient valuation upside on a 12-month view to Buy.

Aerospace & Defence

14

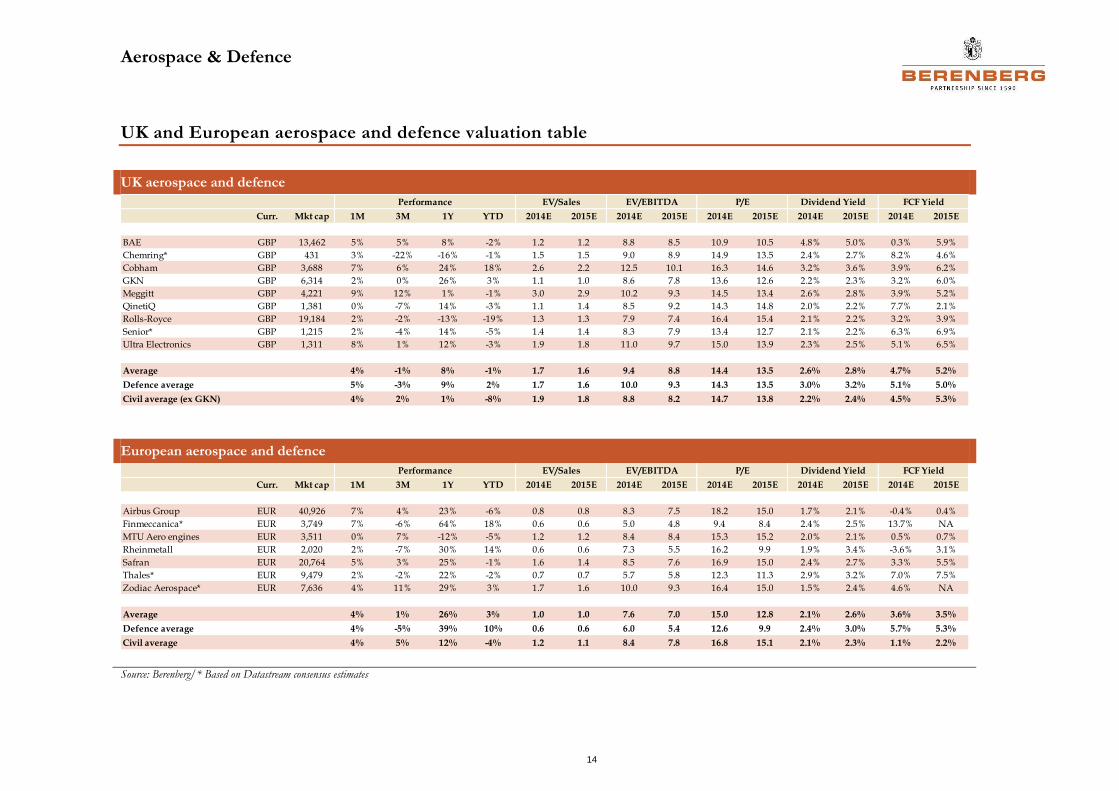

UK and European aerospace and defence valuation table

UK aerospace and defence

European aerospace and defence

Source: Berenberg/* Based on Datastream consensus estimates

Curr. Mkt cap 1M 3M 1Y YTD 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E

BAE GBP 13,462 5% 5% 8% -2% 1.2 1.2 8.8 8.5 10.9 10.5 4.8% 5.0% 0.3% 5.9%

Chemring* GBP 431 3% -22% -16% -1% 1.5 1.5 9.0 8.9 14.9 13.5 2.4% 2.7% 8.2% 4.6%

Cobham GBP 3,688 7% 6% 24% 18% 2.6 2.2 12.5 10.1 16.3 14.6 3.2% 3.6% 3.9% 6.2%

GKN GBP 6,314 2% 0% 26% 3% 1.1 1.0 8.6 7.8 13.6 12.6 2.2% 2.3% 3.2% 6.0%

Meggitt GBP 4,221 9% 12% 1% -1% 3.0 2.9 10.2 9.3 14.5 13.4 2.6% 2.8% 3.9% 5.2%

QinetiQ GBP 1,381 0% -7% 14% -3% 1.1 1.4 8.5 9.2 14.3 14.8 2.0% 2.2% 7.7% 2.1%

Rolls-Royce GBP 19,184 2% -2% -13% -19% 1.3 1.3 7.9 7.4 16.4 15.4 2.1% 2.2% 3.2% 3.9%

Senior* GBP 1,215 2% -4% 14% -5% 1.4 1.4 8.3 7.9 13.4 12.7 2.1% 2.2% 6.3% 6.9%

Ultra Electronics GBP 1,311 8% 1% 12% -3% 1.9 1.8 11.0 9.7 15.0 13.9 2.3% 2.5% 5.1% 6.5%

Average 4% -1% 8% -1% 1.7 1.6 9.4 8.8 14.4 13.5 2.6% 2.8% 4.7% 5.2%

Defence average 5% -3% 9% 2% 1.7 1.6 10.0 9.3 14.3 13.5 3.0% 3.2% 5.1% 5.0%

Civil average (ex GKN) 4% 2% 1% -8% 1.9 1.8 8.8 8.2 14.7 13.8 2.2% 2.4% 4.5% 5.3%

FCF YieldPerformance EV/Sales EV/EBITDA P/E Dividend Yield

Curr. Mkt cap 1M 3M 1Y YTD 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E

Airbus Group EUR 40,926 7% 4% 23% -6% 0.8 0.8 8.3 7.5 18.2 15.0 1.7% 2.1% -0.4% 0.4%

Finmeccanica* EUR 3,749 7% -6% 64% 18% 0.6 0.6 5.0 4.8 9.4 8.4 2.4% 2.5% 13.7% NA

MTU Aero engines EUR 3,511 0% 7% -12% -5% 1.2 1.2 8.4 8.4 15.3 15.2 2.0% 2.1% 0.5% 0.7%

Rheinmetall EUR 2,020 2% -7% 30% 14% 0.6 0.6 7.3 5.5 16.2 9.9 1.9% 3.4% -3.6% 3.1%

Safran EUR 20,764 5% 3% 25% -1% 1.6 1.4 8.5 7.6 16.9 15.0 2.4% 2.7% 3.3% 5.5%

Thales* EUR 9,479 2% -2% 22% -2% 0.7 0.7 5.7 5.8 12.3 11.3 2.9% 3.2% 7.0% 7.5%

Zodiac Aerospace* EUR 7,636 4% 11% 29% 3% 1.7 1.6 10.0 9.3 16.4 15.0 1.5% 2.4% 4.6% NA

Average 4% 1% 26% 3% 1.0 1.0 7.6 7.0 15.0 12.8 2.1% 2.6% 3.6% 3.5%

Defence average 4% -5% 39% 10% 0.6 0.6 6.0 5.4 12.6 9.9 2.4% 3.0% 5.7% 5.3%

Civil average 4% 5% 12% -4% 1.2 1.1 8.4 7.8 16.8 15.1 2.1% 2.3% 1.1% 2.2%

Performance EV/Sales EV/EBITDA P/E Dividend Yield FCF Yield

Aerospace & Defence

15

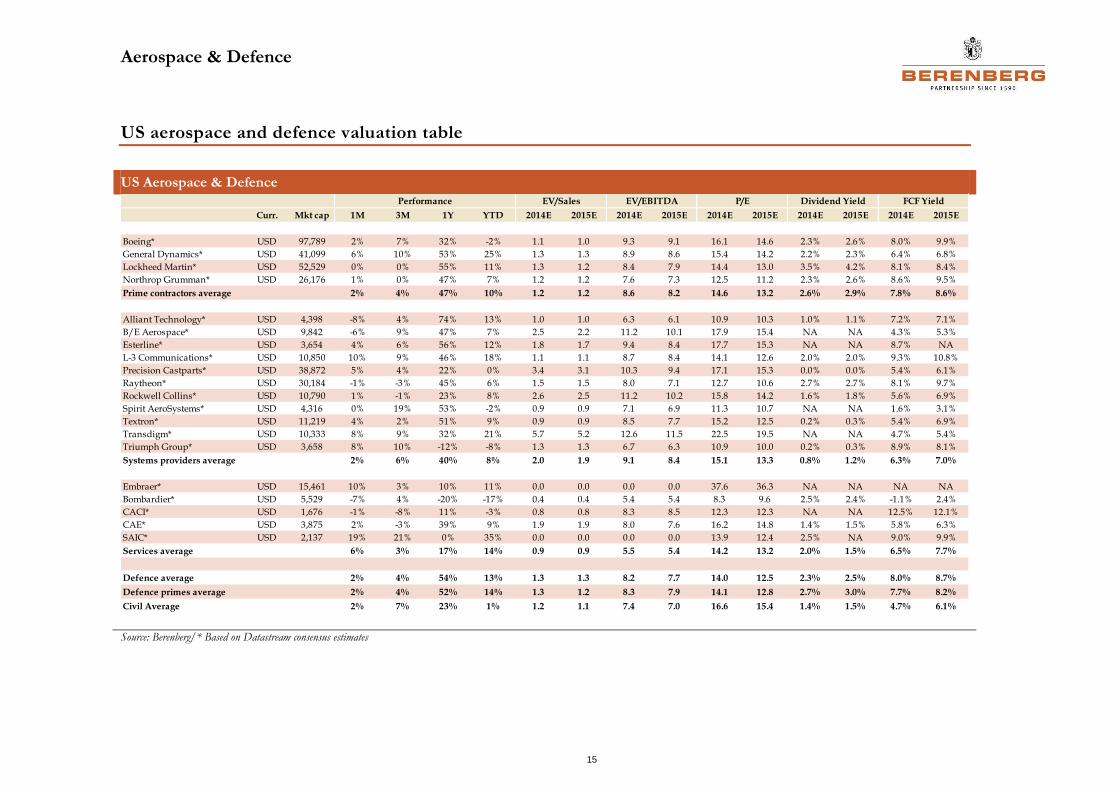

US aerospace and defence valuation table

US Aerospace & Defence

Source: Berenberg/* Based on Datastream consensus estimates

Curr. Mkt cap 1M 3M 1Y YTD 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E

Boeing* USD 97,789 2% 7% 32% -2% 1.1 1.0 9.3 9.1 16.1 14.6 2.3% 2.6% 8.0% 9.9%

General Dynamics* USD 41,099 6% 10% 53% 25% 1.3 1.3 8.9 8.6 15.4 14.2 2.2% 2.3% 6.4% 6.8%

Lockheed Martin* USD 52,529 0% 0% 55% 11% 1.3 1.2 8.4 7.9 14.4 13.0 3.5% 4.2% 8.1% 8.4%

Northrop Grumman* USD 26,176 1% 0% 47% 7% 1.2 1.2 7.6 7.3 12.5 11.2 2.3% 2.6% 8.6% 9.5%

Prime contractors average 2% 4% 47% 10% 1.2 1.2 8.6 8.2 14.6 13.2 2.6% 2.9% 7.8% 8.6%

Alliant Technology* USD 4,398 -8% 4% 74% 13% 1.0 1.0 6.3 6.1 10.9 10.3 1.0% 1.1% 7.2% 7.1%

B/E Aerospace* USD 9,842 -6% 9% 47% 7% 2.5 2.2 11.2 10.1 17.9 15.4 NA NA 4.3% 5.3%

Esterline* USD 3,654 4% 6% 56% 12% 1.8 1.7 9.4 8.4 17.7 15.3 NA NA 8.7% NA

L-3 Communications* USD 10,850 10% 9% 46% 18% 1.1 1.1 8.7 8.4 14.1 12.6 2.0% 2.0% 9.3% 10.8%

Precision Castparts* USD 38,872 5% 4% 22% 0% 3.4 3.1 10.3 9.4 17.1 15.3 0.0% 0.0% 5.4% 6.1%

Raytheon* USD 30,184 -1% -3% 45% 6% 1.5 1.5 8.0 7.1 12.7 10.6 2.7% 2.7% 8.1% 9.7%

Rockwell Collins* USD 10,790 1% -1% 23% 8% 2.6 2.5 11.2 10.2 15.8 14.2 1.6% 1.8% 5.6% 6.9%

Spirit AeroSystems* USD 4,316 0% 19% 53% -2% 0.9 0.9 7.1 6.9 11.3 10.7 NA NA 1.6% 3.1%

Textron* USD 11,219 4% 2% 51% 9% 0.9 0.9 8.5 7.7 15.2 12.5 0.2% 0.3% 5.4% 6.9%

Transdigm* USD 10,333 8% 9% 32% 21% 5.7 5.2 12.6 11.5 22.5 19.5 NA NA 4.7% 5.4%

Triumph Group* USD 3,658 8% 10% -12% -8% 1.3 1.3 6.7 6.3 10.9 10.0 0.2% 0.3% 8.9% 8.1%

Systems providers average 2% 6% 40% 8% 2.0 1.9 9.1 8.4 15.1 13.3 0.8% 1.2% 6.3% 7.0%

Embraer* USD 15,461 10% 3% 10% 11% 0.0 0.0 0.0 0.0 37.6 36.3 NA NA NA NA

Bombardier* USD 5,529 -7% 4% -20% -17% 0.4 0.4 5.4 5.4 8.3 9.6 2.5% 2.4% -1.1% 2.4%

CACI* USD 1,676 -1% -8% 11% -3% 0.8 0.8 8.3 8.5 12.3 12.3 NA NA 12.5% 12.1%

CAE* USD 3,875 2% -3% 39% 9% 1.9 1.9 8.0 7.6 16.2 14.8 1.4% 1.5% 5.8% 6.3%

SAIC* USD 2,137 19% 21% 0% 35% 0.0 0.0 0.0 0.0 13.9 12.4 2.5% NA 9.0% 9.9%

Services average 6% 3% 17% 14% 0.9 0.9 5.5 5.4 14.2 13.2 2.0% 1.5% 6.5% 7.7%

Defence average 2% 4% 54% 13% 1.3 1.3 8.2 7.7 14.0 12.5 2.3% 2.5% 8.0% 8.7%

Defence primes average 2% 4% 52% 14% 1.3 1.2 8.3 7.9 14.1 12.8 2.7% 3.0% 7.7% 8.2%

Civil Average 2% 7% 23% 1% 1.2 1.1 7.4 7.0 16.6 15.4 1.4% 1.5% 4.7% 6.1%

FCF YieldPerformance EV/Sales EV/EBITDA P/E Dividend Yield

Aerospace & Defence

16

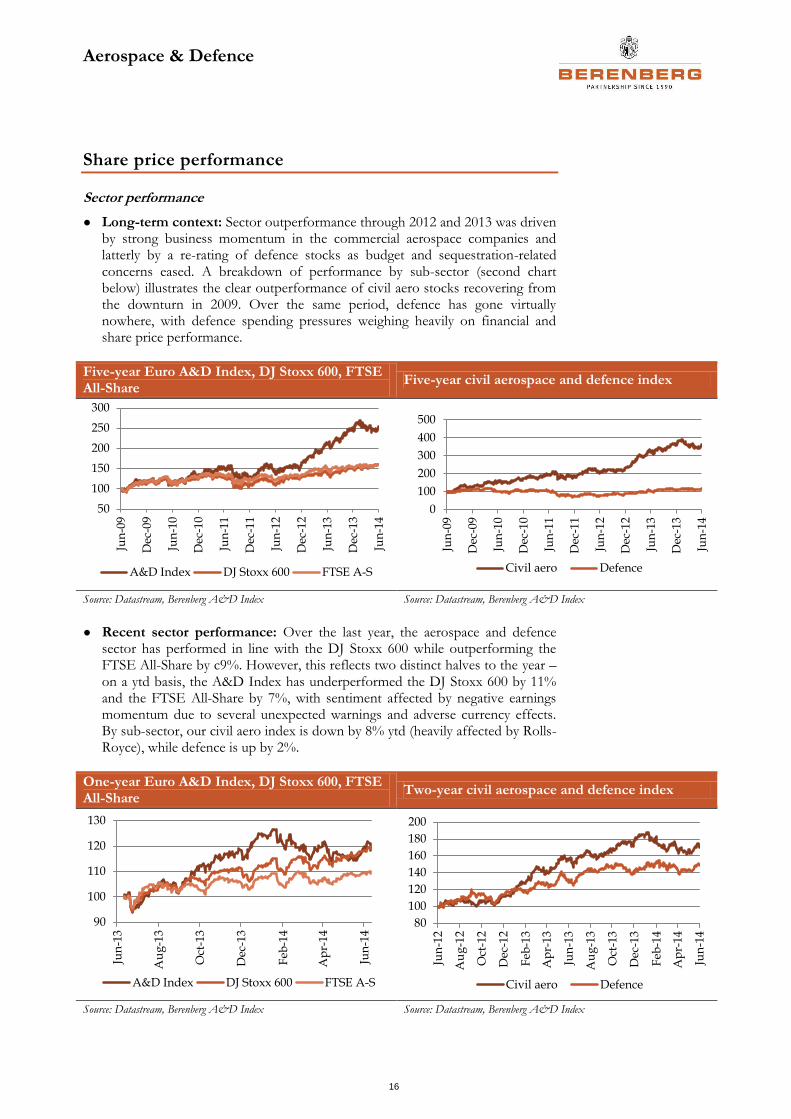

Share price performance

Sector performance

● Long-term context: Sector outperformance through 2012 and 2013 was driven by strong business momentum in the commercial aerospace companies and latterly by a re-rating of defence stocks as budget and sequestration-related concerns eased. A breakdown of performance by sub-sector (second chart below) illustrates the clear outperformance of civil aero stocks recovering from the downturn in 2009. Over the same period, defence has gone virtually nowhere, with defence spending pressures weighing heavily on financial and share price performance.

Five-year Euro A&D Index, DJ Stoxx 600, FTSE All-Share

Five-year civil aerospace and defence index

Source: Datastream, Berenberg A&D Index Source: Datastream, Berenberg A&D Index

● Recent sector performance: Over the last year, the aerospace and defence sector has performed in line with the DJ Stoxx 600 while outperforming the FTSE All-Share by c9%. However, this reflects two distinct halves to the year – on a ytd basis, the A&D Index has underperformed the DJ Stoxx 600 by 11% and the FTSE All-Share by 7%, with sentiment affected by negative earnings momentum due to several unexpected warnings and adverse currency effects. By sub-sector, our civil aero index is down by 8% ytd (heavily affected by Rolls-Royce), while defence is up by 2%.

One-year Euro A&D Index, DJ Stoxx 600, FTSE All-Share

Two-year civil aerospace and defence index

Source: Datastream, Berenberg A&D Index Source: Datastream, Berenberg A&D Index

50

100

150

200

250

300

Jun

-09

Dec

-09

Jun

-10

Dec

-10

Jun

-11

Dec

-11

Jun

-12

Dec

-12

Jun

-13

Dec

-13

Jun

-14

A&D Index DJ Stoxx 600 FTSE A-S

0

100

200

300

400

500

Jun

-09

Dec

-09

Jun

-10

Dec

-10

Jun

-11

Dec

-11

Jun

-12

Dec

-12

Jun

-13

Dec

-13

Jun

-14

Civil aero Defence

90

100

110

120

130

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

A&D Index DJ Stoxx 600 FTSE A-S

80

100

120

140

160

180

200

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

Civil aero Defence

Aerospace & Defence

17

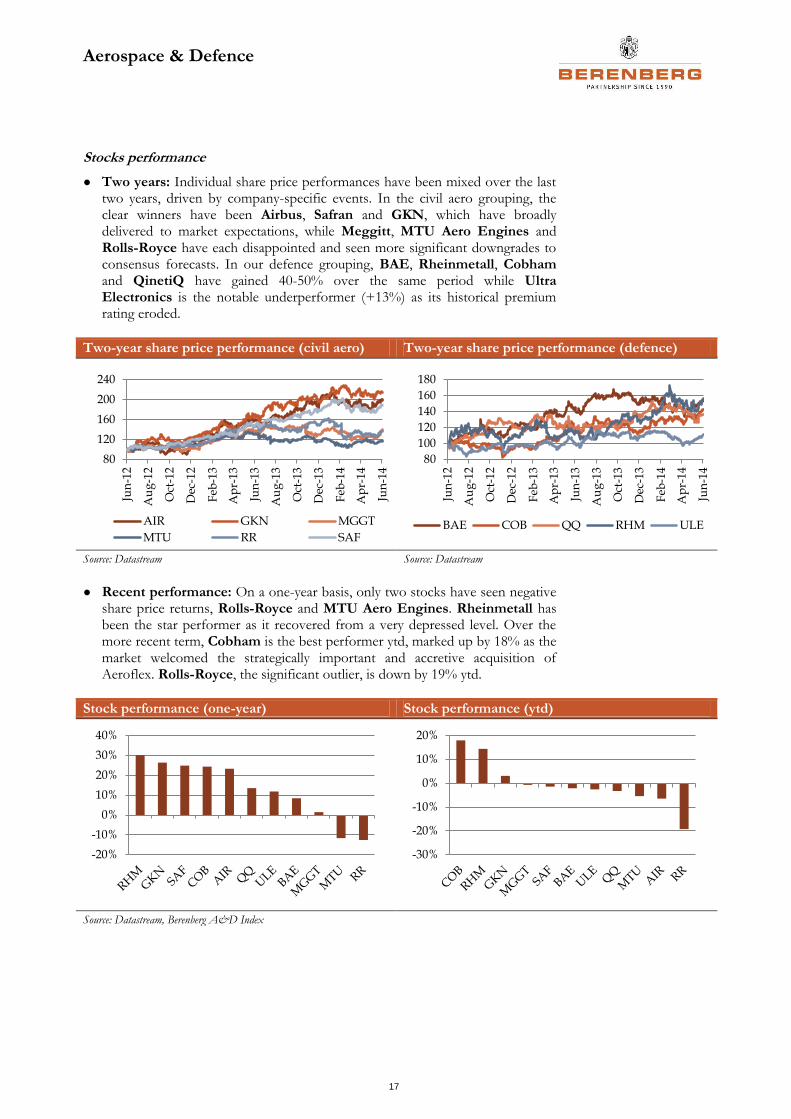

Stocks performance

● Two years: Individual share price performances have been mixed over the last two years, driven by company-specific events. In the civil aero grouping, the clear winners have been Airbus, Safran and GKN, which have broadly delivered to market expectations, while Meggitt, MTU Aero Engines and Rolls-Royce have each disappointed and seen more significant downgrades to consensus forecasts. In our defence grouping, BAE, Rheinmetall, Cobham and QinetiQ have gained 40-50% over the same period while Ultra Electronics is the notable underperformer (+13%) as its historical premium rating eroded.

Two-year share price performance (civil aero) Two-year share price performance (defence)

Source: Datastream Source: Datastream

● Recent performance: On a one-year basis, only two stocks have seen negative share price returns, Rolls-Royce and MTU Aero Engines. Rheinmetall has been the star performer as it recovered from a very depressed level. Over the more recent term, Cobham is the best performer ytd, marked up by 18% as the market welcomed the strategically important and accretive acquisition of Aeroflex. Rolls-Royce, the significant outlier, is down by 19% ytd.

Stock performance (one-year) Stock performance (ytd)

Source: Datastream, Berenberg A&D Index

80

120

160

200

240

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-13

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb

-14

Ap

r-14

Jun

-14

AIR GKN MGGT

MTU RR SAF

80

100

120

140

160

180

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

BAE COB QQ RHM ULE

-20%

-10%

0%

10%

20%

30%

40%

-30%

-20%

-10%

0%

10%

20%

Aerospace & Defence

18

Valuation charts

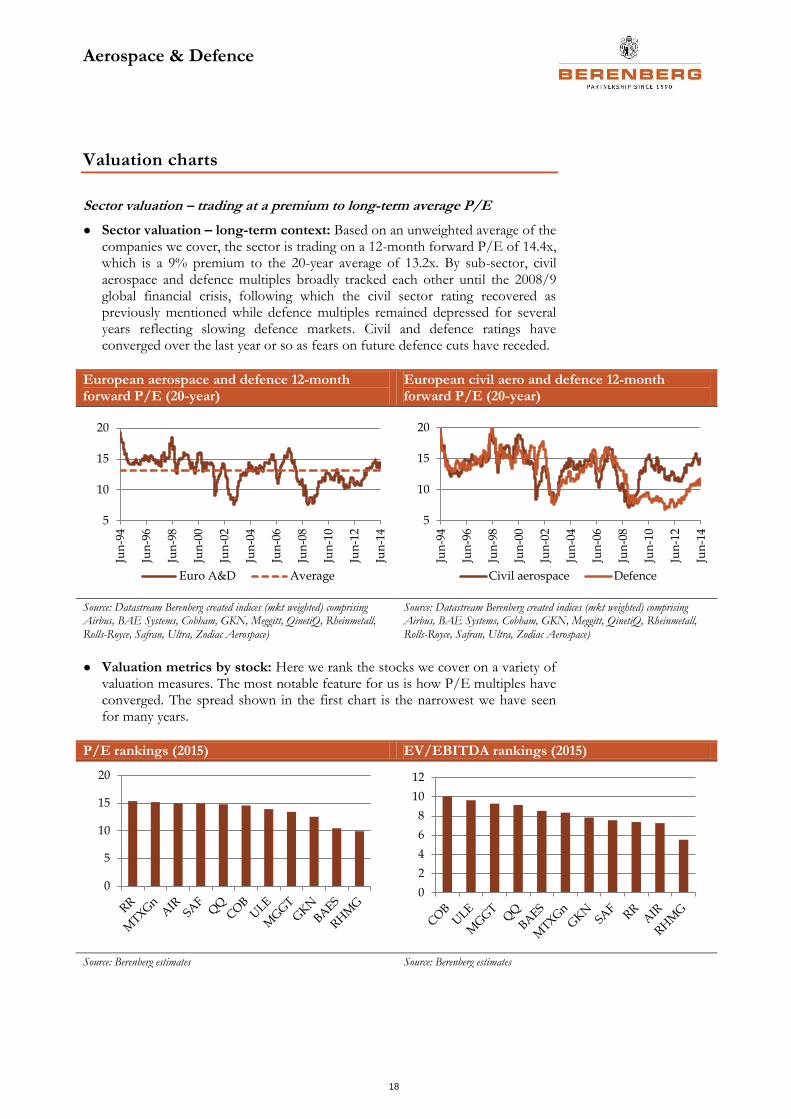

Sector valuation – trading at a premium to long-term average P/E

● Sector valuation – long-term context: Based on an unweighted average of the companies we cover, the sector is trading on a 12-month forward P/E of 14.4x, which is a 9% premium to the 20-year average of 13.2x. By sub-sector, civil aerospace and defence multiples broadly tracked each other until the 2008/9 global financial crisis, following which the civil sector rating recovered as previously mentioned while defence multiples remained depressed for several years reflecting slowing defence markets. Civil and defence ratings have converged over the last year or so as fears on future defence cuts have receded.

European aerospace and defence 12-month forward P/E (20-year)

European civil aero and defence 12-month forward P/E (20-year)

Source: Datastream Berenberg created indices (mkt weighted) comprising Airbus, BAE Systems, Cobham, GKN, Meggitt, QinetiQ, Rheinmetall, Rolls-Royce, Safran, Ultra, Zodiac Aerospace)

Source: Datastream Berenberg created indices (mkt weighted) comprising Airbus, BAE Systems, Cobham, GKN, Meggitt, QinetiQ, Rheinmetall, Rolls-Royce, Safran, Ultra, Zodiac Aerospace)

● Valuation metrics by stock: Here we rank the stocks we cover on a variety of valuation measures. The most notable feature for us is how P/E multiples have converged. The spread shown in the first chart is the narrowest we have seen for many years.

P/E rankings (2015) EV/EBITDA rankings (2015)

Source: Berenberg estimates Source: Berenberg estimates

5

10

15

20

Jun

-94

Jun

-96

Jun

-98

Jun

-00

Jun

-02

Jun

-04

Jun

-06

Jun

-08

Jun

-10

Jun

-12

Jun

-14

Euro A&D Average

5

10

15

20Ju

n-9

4

Jun

-96

Jun

-98

Jun

-00

Jun

-02

Jun

-04

Jun

-06

Jun

-08

Jun

-10

Jun

-12

Jun

-14

Civil aerospace Defence

0

5

10

15

20

0

2

4

6

8

10

12

Aerospace & Defence

19

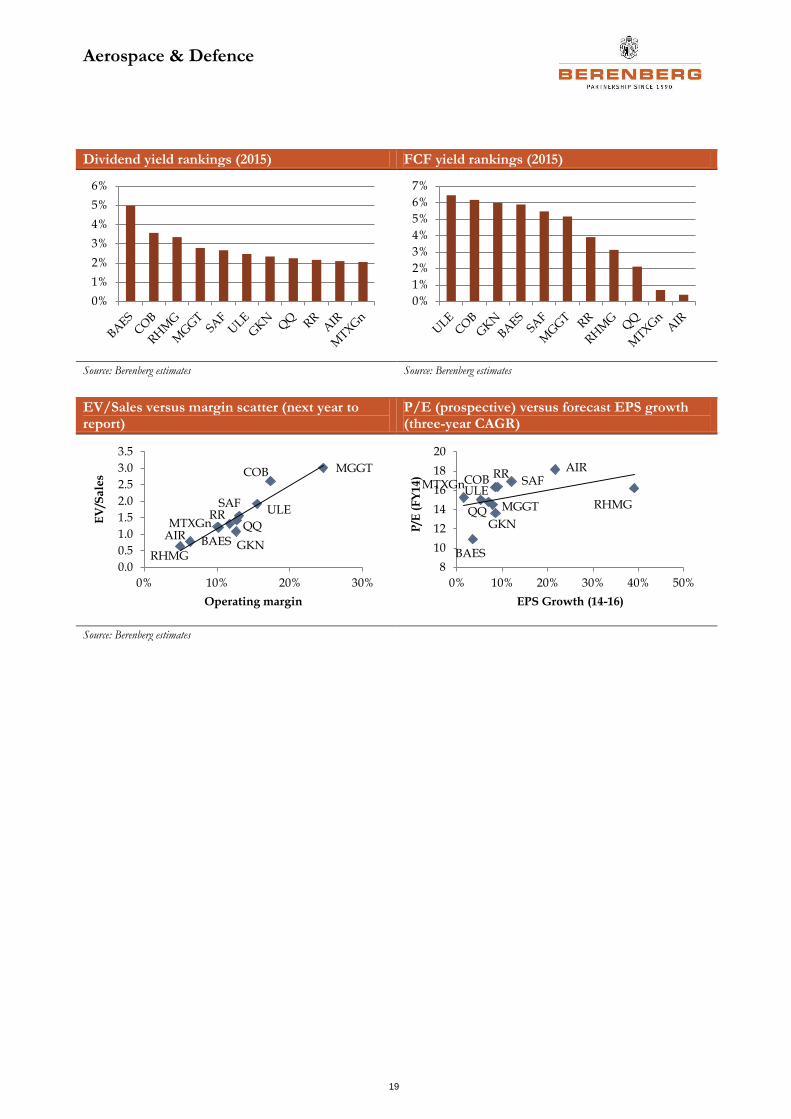

Dividend yield rankings (2015) FCF yield rankings (2015)

Source: Berenberg estimates Source: Berenberg estimates

EV/Sales versus margin scatter (next year to report)

P/E (prospective) versus forecast EPS growth (three-year CAGR)

Source: Berenberg estimates

0%

1%

2%

3%

4%

5%

6%

0%

1%

2%

3%

4%

5%

6%

7%

AIR BAES

COB

GKN

MGGT

MTXGn QQ

RHMG

RRSAF

ULE

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0% 10% 20% 30%

EV

/Sa

les

Operating margin

AIR

BAES

COB

GKN

MGGT

MTXGn

QQRHMG

RRSAF

ULE

8

10

12

14

16

18

20

0% 10% 20% 30% 40% 50%

P/E

(F

Y1

4)

EPS Growth (14-16)

Aerospace & Defence

20

Civil aerospace – OE

The commercial aerospace sector is in the middle of an extended production up-cycle, with the order backlog in the large commercial jet sector, which accounts for over 85% of the civil aircraft market by value, covering an average eight years production. A combination of structural factors is driving demand for new aircraft pointing to sustained high production.

● Replacement demand: The aging global fleet of first and second generation airliners is increasingly being retired. According to Ascend, the replacement rate has averaged 48% of aircraft deliveries during the past five years. Over time, we expect this to increase both in absolute (unit) terms and as a proportion because, by definition, the trend will increase in line with the historical fleet profile.

● Fuel efficiency: Aviation fuel represents 40-50% of airline operating cost compared to 15-25% a decade ago when the oil price was 80% below where it is today. Thus, the economic pressure to replace inefficient fleets remains a significant demand driver and we suggest it will continue to do so at even a materially lower oil price. We note the recent tensions relating to the situation in Iraq has driven the price of oil up by another 6%. The same applies to other environmental factors such as emissions and noise regulations driving the need for new aircraft.

● Economic growth: Commercial Aerospace is ultimately driven by economic growth and can be surmised as a “GDP plus” sector, growing by 1.5-2.0% above global GDP over the long term. While there are always short-term cycle and regional variations, powerful structural trends such as emerging market growth and low-cost travel have transformed the demand picture over the past 10-20 years. We note non-US and non-European markets account for over 50% of the total backlog (higher excluding leasing companies) compared to 22% in 2000.

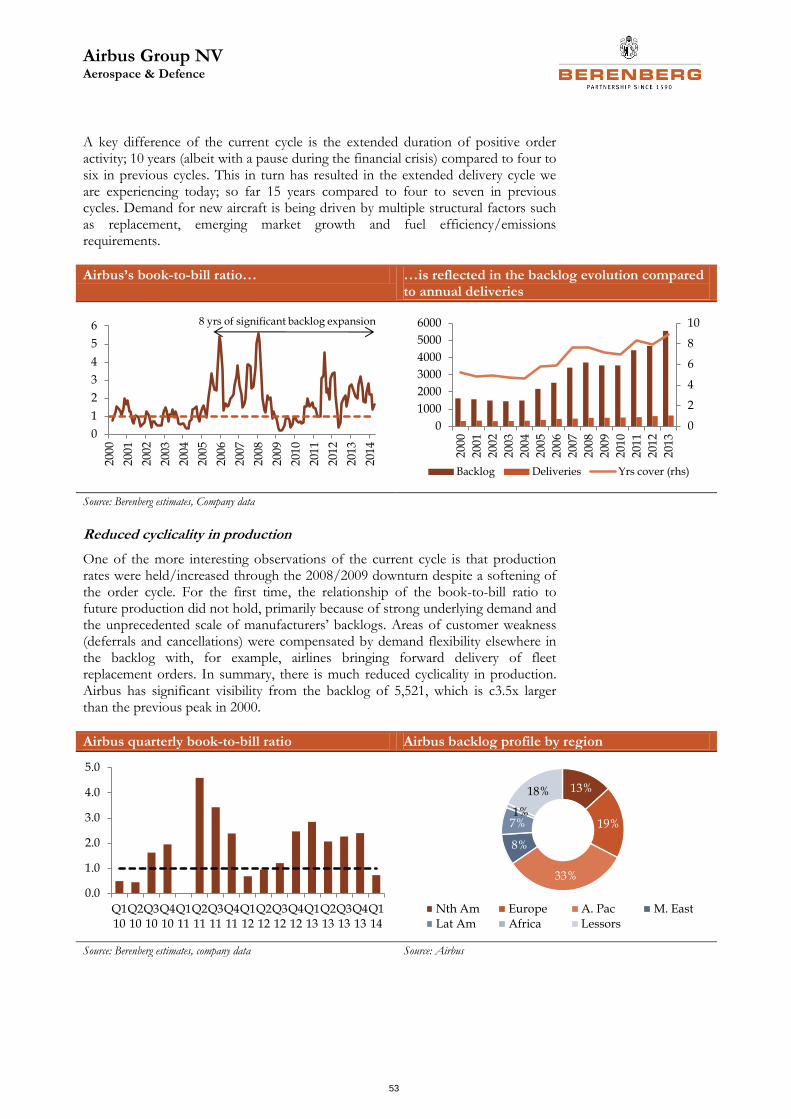

Backlog growth

The commercial large jet backlog has grown by a factor of four since 2004 to almost 10,700 aircraft (11,500 including regional jets), representing around 55% of the in-service fleet and dwarfs the previous cycle peak of 3,900 in 2000. Over this period, more than 18,000 new aircraft orders have been placed (approximately equivalent in number to the entire global fleet in 2004) despite spanning a severe global financial crisis and aviation downturn,.

Aerospace & Defence

21

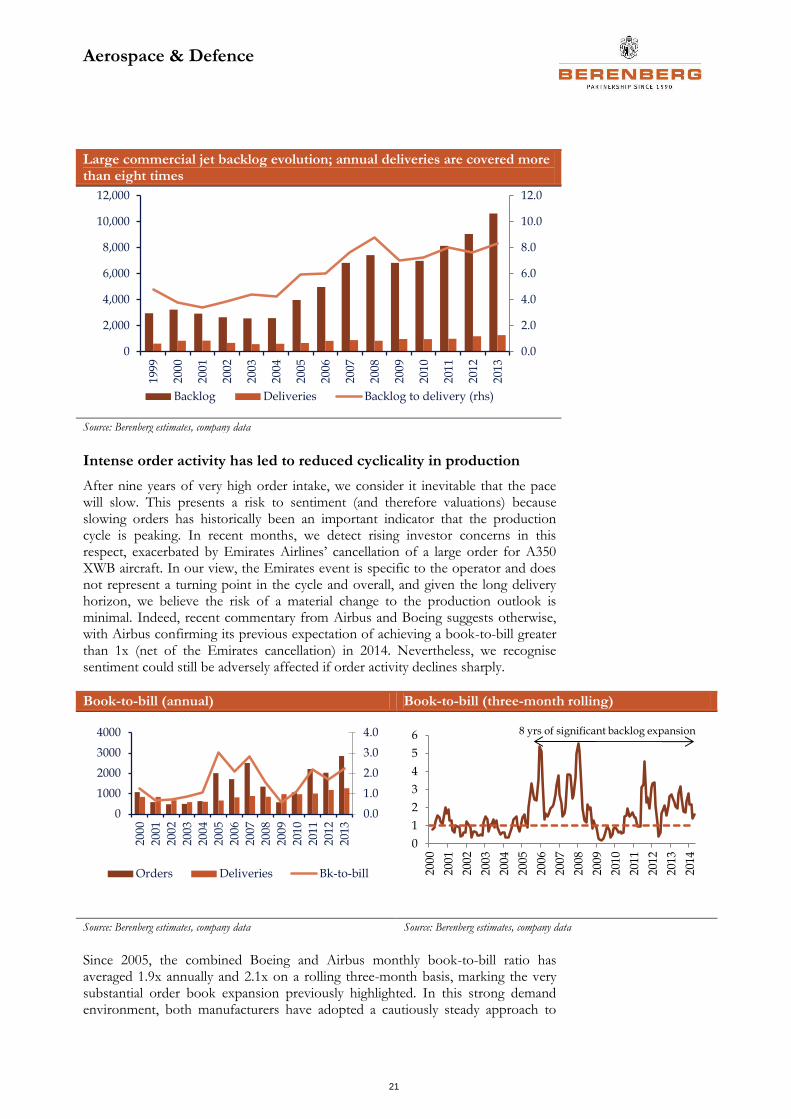

Large commercial jet backlog evolution; annual deliveries are covered more than eight times

Source: Berenberg estimates, company data

Intense order activity has led to reduced cyclicality in production

After nine years of very high order intake, we consider it inevitable that the pace will slow. This presents a risk to sentiment (and therefore valuations) because slowing orders has historically been an important indicator that the production cycle is peaking. In recent months, we detect rising investor concerns in this respect, exacerbated by Emirates Airlines’ cancellation of a large order for A350 XWB aircraft. In our view, the Emirates event is specific to the operator and does not represent a turning point in the cycle and overall, and given the long delivery horizon, we believe the risk of a material change to the production outlook is minimal. Indeed, recent commentary from Airbus and Boeing suggests otherwise, with Airbus confirming its previous expectation of achieving a book-to-bill greater than 1x (net of the Emirates cancellation) in 2014. Nevertheless, we recognise sentiment could still be adversely affected if order activity declines sharply.

Book-to-bill (annual) Book-to-bill (three-month rolling)

Source: Berenberg estimates, company data Source: Berenberg estimates, company data

Since 2005, the combined Boeing and Airbus monthly book-to-bill ratio has averaged 1.9x annually and 2.1x on a rolling three-month basis, marking the very substantial order book expansion previously highlighted. In this strong demand environment, both manufacturers have adopted a cautiously steady approach to

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0

2,000

4,000

6,000

8,000

10,000

12,000

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

Backlog Deliveries Backlog to delivery (rhs)

0.0

1.0

2.0

3.0

4.0

0

1000

2000

3000

4000

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

Orders Deliveries Bk-to-bill

0

1

2

3

4

5

6

200

0

200

1

200

2

200

3

2004

200

5

200

6

200

7

200

8

200

9

201

0

2011

201

2

201

3

2014

8 yrs of significant backlog expansion

Aerospace & Defence

22

production increases. By way of illustration, annual aircraft deliveries have more than doubled from the trough in 2003 at a CAGR of 8%, which compares to previous cycles when the average trough-to-peak increase of c50% over three to four years, implied a CAGR of c12%. The result is lower volatility in the production cycle as evidenced by the fact there were no production cuts through the 2008/9 downturn, despite a sharp drop in air travel and a temporary period of depressed order activity.

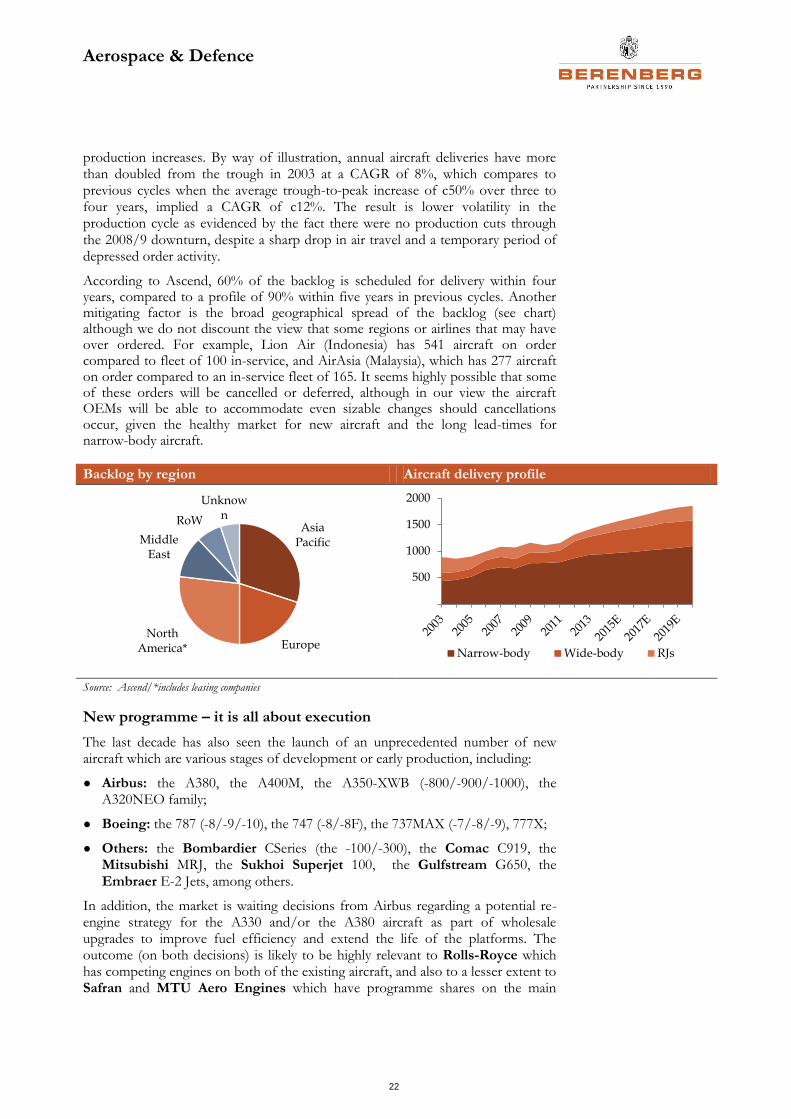

According to Ascend, 60% of the backlog is scheduled for delivery within four years, compared to a profile of 90% within five years in previous cycles. Another mitigating factor is the broad geographical spread of the backlog (see chart) although we do not discount the view that some regions or airlines that may have over ordered. For example, Lion Air (Indonesia) has 541 aircraft on order compared to fleet of 100 in-service, and AirAsia (Malaysia), which has 277 aircraft on order compared to an in-service fleet of 165. It seems highly possible that some of these orders will be cancelled or deferred, although in our view the aircraft OEMs will be able to accommodate even sizable changes should cancellations occur, given the healthy market for new aircraft and the long lead-times for narrow-body aircraft.

Backlog by region Aircraft delivery profile

Source: Ascend/*includes leasing companies

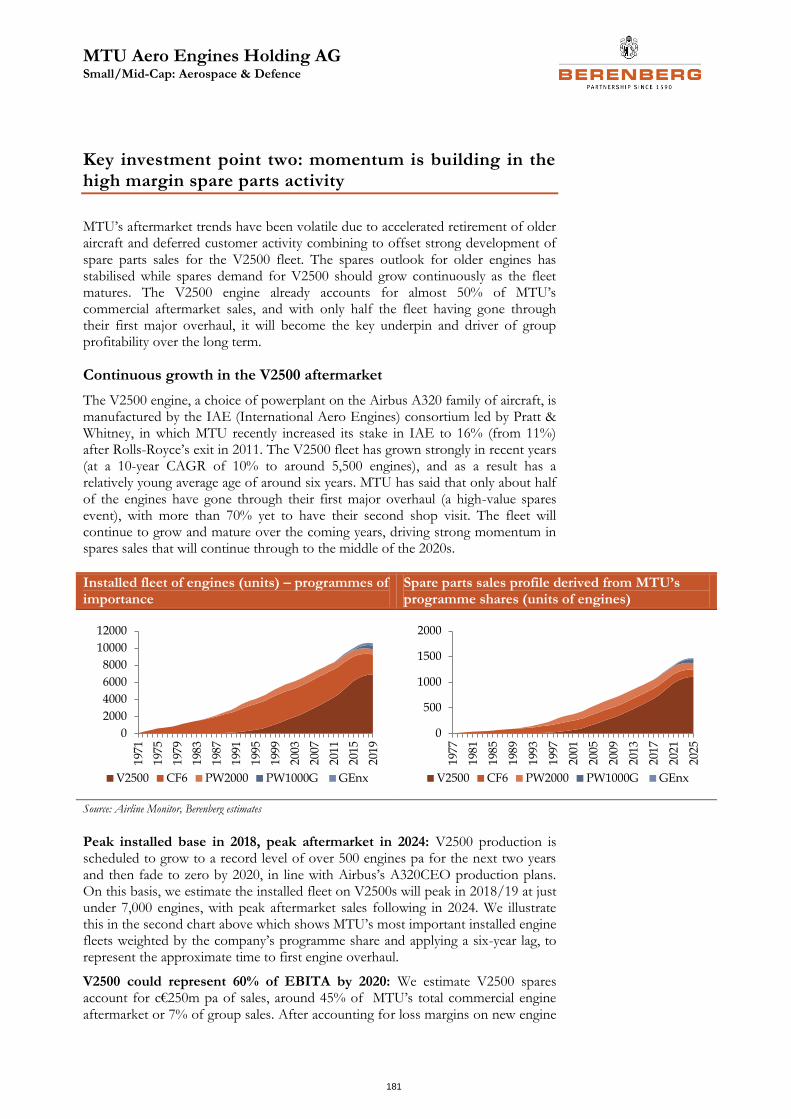

New programme – it is all about execution

The last decade has also seen the launch of an unprecedented number of new aircraft which are various stages of development or early production, including:

● Airbus: the A380, the A400M, the A350-XWB (-800/-900/-1000), the A320NEO family;

● Boeing: the 787 (-8/-9/-10), the 747 (-8/-8F), the 737MAX (-7/-8/-9), 777X;

● Others: the Bombardier CSeries (the -100/-300), the Comac C919, the Mitsubishi MRJ, the Sukhoi Superjet 100, the Gulfstream G650, the Embraer E-2 Jets, among others.

In addition, the market is waiting decisions from Airbus regarding a potential re-engine strategy for the A330 and/or the A380 aircraft as part of wholesale upgrades to improve fuel efficiency and extend the life of the platforms. The outcome (on both decisions) is likely to be highly relevant to Rolls-Royce which has competing engines on both of the existing aircraft, and also to a lesser extent to Safran and MTU Aero Engines which have programme shares on the main

Asia Pacific

EuropeNorth

America*

Middle East

RoW

Unknown

500

1000

1500

2000

Narrow-body Wide-body RJs

Aerospace & Defence

23

competing engines from GE and Engine Alliance, the 50:50 joint venture between GE and Pratt and Whitney.

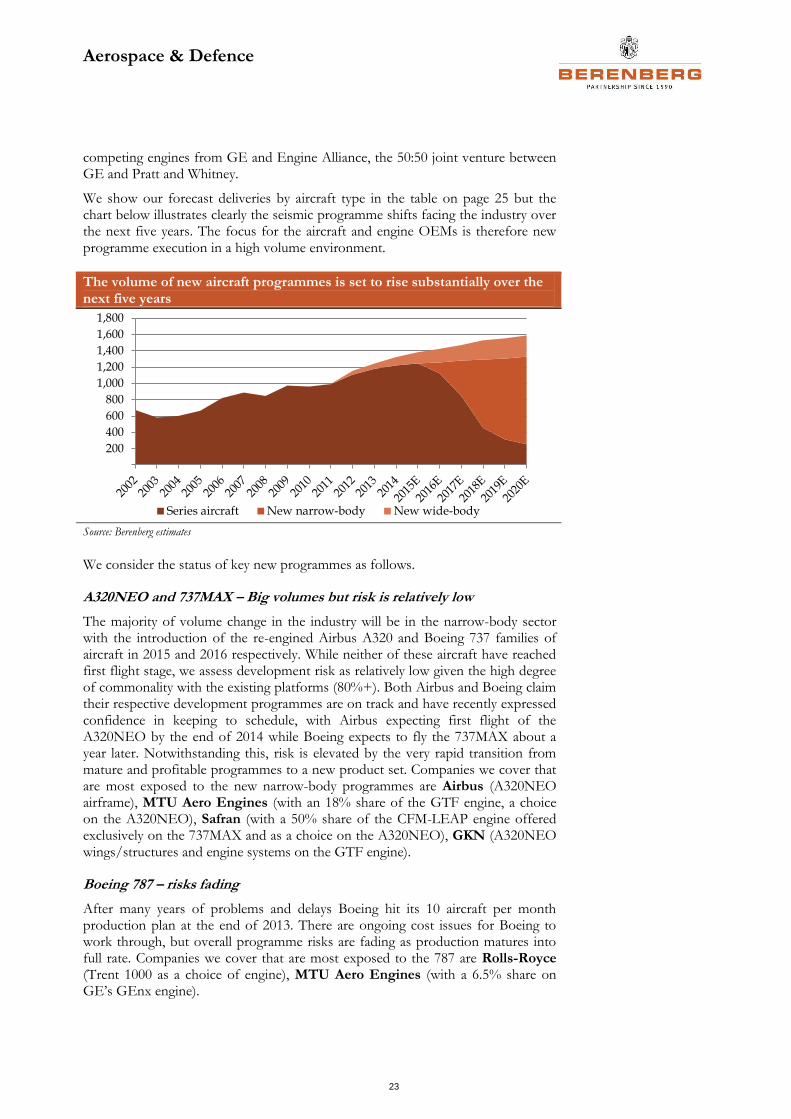

We show our forecast deliveries by aircraft type in the table on page 25 but the chart below illustrates clearly the seismic programme shifts facing the industry over the next five years. The focus for the aircraft and engine OEMs is therefore new programme execution in a high volume environment.

The volume of new aircraft programmes is set to rise substantially over the next five years

Source: Berenberg estimates

We consider the status of key new programmes as follows.

A320NEO and 737MAX – Big volumes but risk is relatively low

The majority of volume change in the industry will be in the narrow-body sector with the introduction of the re-engined Airbus A320 and Boeing 737 families of aircraft in 2015 and 2016 respectively. While neither of these aircraft have reached first flight stage, we assess development risk as relatively low given the high degree of commonality with the existing platforms (80%+). Both Airbus and Boeing claim their respective development programmes are on track and have recently expressed confidence in keeping to schedule, with Airbus expecting first flight of the A320NEO by the end of 2014 while Boeing expects to fly the 737MAX about a year later. Notwithstanding this, risk is elevated by the very rapid transition from mature and profitable programmes to a new product set. Companies we cover that are most exposed to the new narrow-body programmes are Airbus (A320NEO airframe), MTU Aero Engines (with an 18% share of the GTF engine, a choice on the A320NEO), Safran (with a 50% share of the CFM-LEAP engine offered exclusively on the 737MAX and as a choice on the A320NEO), GKN (A320NEO wings/structures and engine systems on the GTF engine).

Boeing 787 – risks fading

After many years of problems and delays Boeing hit its 10 aircraft per month production plan at the end of 2013. There are ongoing cost issues for Boeing to work through, but overall programme risks are fading as production matures into full rate. Companies we cover that are most exposed to the 787 are Rolls-Royce (Trent 1000 as a choice of engine), MTU Aero Engines (with a 6.5% share on GE’s GEnx engine).

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Series aircraft New narrow-body New wide-body

Aerospace & Defence

24

A350 XWB – the next big all-new programme; ramp-up from 2016

Flight testing of the first variant of the A350-XWB (extra wide-body), the A350-900, is nearing completion, with Airbus confident of achieving aircraft certification in Q3 before first customer delivery to Qatar Airways in Q4. Early rate production commences in 2015 with a sharp increase planned thereafter. Two more variants, the smaller A350-800 and the larger A350-1000, are in early development but there is speculation that: 1) Airbus may not proceed with the -800, especially if the A330 is re-engined, on which a decision is expected by the year-end, 2) a stretched -1000 variant may be a future option to compete more effectively with Boeing’s new 777X. Companies that we cover that are most exposed to the A350 XWB programme are Airbus (airframe), Rolls-Royce (Trent XWB engines – currently sole source) and GKN (wing structures and engine systems on the Trent 1000).

B777X – A long way out

Production of the recently launched successor to Boeing’s 777 aircraft is set to begin in 2017 with first delivery targeted for late 2019/early 2020. The 777X will compete at a seating capacity level at, and just above the A350-1000. Development of the 777X is at an early stage and suppliers are still being selected. Both Safran and MTU Aero Engines are bidding for a share on GE’s GE9X engine which has been selected as the sole power plant for the 777X with decisions likely to be announced before the end of the year.

CSeries – A troubled upstart

Bombardier’s CSeries is a new family of narrow-body aircraft designed to compete at the smaller end of the Boeing 737 and Airbus A320 ranges. The programme, which is in the late stages of testing and early production, has been beset by problems and entry-in-to-service of the smaller 110-seat variant (C100) has again been delayed to the second half of 2015. The CSeries is the first aircraft to be powered by Pratt & Whitney’s PurePower GTF engine (the PW1500G), on which MTU Aero Engines has a 17% share. In late May, Bombardier reported an engine incident during ground testing which caused significant damaged and the flight testing programme remains temporarily halted. Recent comments from Pratt & Whitney suggest the problem can be fixed rapidly and flight testing is expected to resume in the next few weeks. It therefore appears this latest issue does not represent a fundamental or structural problem that could de-rail the GTF or whole CSeries programme. In volume terms, the A320NEO is a far more important programme for the GTF engine where deliveries are expected to commence in late 2015 and ramp up aggressively thereafter.

Aerospace & Defence

25

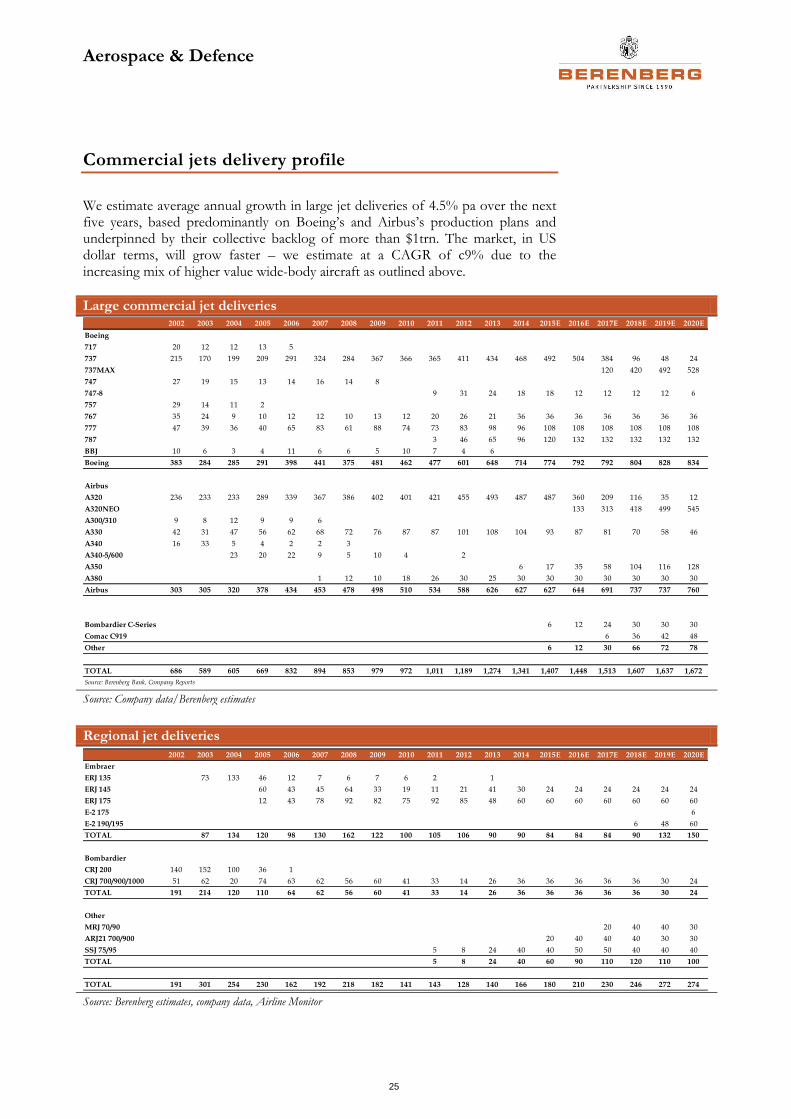

Commercial jets delivery profile

We estimate average annual growth in large jet deliveries of 4.5% pa over the next five years, based predominantly on Boeing’s and Airbus’s production plans and underpinned by their collective backlog of more than $1trn. The market, in US dollar terms, will grow faster – we estimate at a CAGR of c9% due to the increasing mix of higher value wide-body aircraft as outlined above.

Large commercial jet deliveries

Source: Company data/Berenberg estimates

Regional jet deliveries

Source: Berenberg estimates, company data, Airline Monitor

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

Boeing

717 20 12 12 13 5

737 215 170 199 209 291 324 284 367 366 365 411 434 468 492 504 384 96 48 24

737MAX 120 420 492 528

747 27 19 15 13 14 16 14 8

747-8 9 31 24 18 18 12 12 12 12 6

757 29 14 11 2

767 35 24 9 10 12 12 10 13 12 20 26 21 36 36 36 36 36 36 36

777 47 39 36 40 65 83 61 88 74 73 83 98 96 108 108 108 108 108 108

787 3 46 65 96 120 132 132 132 132 132

BBJ 10 6 3 4 11 6 6 5 10 7 4 6

Boeing 383 284 285 291 398 441 375 481 462 477 601 648 714 774 792 792 804 828 834

Airbus

A320 236 233 233 289 339 367 386 402 401 421 455 493 487 487 360 209 116 35 12

A320NEO 133 313 418 499 545

A300/310 9 8 12 9 9 6

A330 42 31 47 56 62 68 72 76 87 87 101 108 104 93 87 81 70 58 46

A340 16 33 5 4 2 2 3

A340-5/600 23 20 22 9 5 10 4 2

A350 6 17 35 58 104 116 128

A380 1 12 10 18 26 30 25 30 30 30 30 30 30 30

Airbus 303 305 320 378 434 453 478 498 510 534 588 626 627 627 644 691 737 737 760

Bombardier C-Series 6 12 24 30 30 30

Comac C919 6 36 42 48

Other 6 12 30 66 72 78

TOTAL 686 589 605 669 832 894 853 979 972 1,011 1,189 1,274 1,341 1,407 1,448 1,513 1,607 1,637 1,672

Source: Berenberg Bank, Company Reports

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

Embraer

ERJ 135 73 133 46 12 7 6 7 6 2 1

ERJ 145 60 43 45 64 33 19 11 21 41 30 24 24 24 24 24 24

ERJ 175 12 43 78 92 82 75 92 85 48 60 60 60 60 60 60 60

E-2 175 6

E-2 190/195 6 48 60

TOTAL 87 134 120 98 130 162 122 100 105 106 90 90 84 84 84 90 132 150

Bombardier

CRJ 200 140 152 100 36 1

CRJ 700/900/1000 51 62 20 74 63 62 56 60 41 33 14 26 36 36 36 36 36 30 24

TOTAL 191 214 120 110 64 62 56 60 41 33 14 26 36 36 36 36 36 30 24

Other

MRJ 70/90 20 40 40 30

ARJ21 700/900 20 40 40 40 30 30

SSJ 75/95 5 8 24 40 40 50 50 40 40 40

TOTAL 5 8 24 40 60 90 110 120 110 100

TOTAL 191 301 254 230 162 192 218 182 141 143 128 140 166 180 210 230 246 272 274

Aerospace & Defence

26

Civil aerospace – aftermarket

Attractive sector

Given the very long lifecycle of aircraft, we view the civil aftermarket as an attractive sector, typically characterised by high margins, strong pricing and high barriers to entry and long-term structural growth (driven by growing and aging fleets). The civil aero aftermarket, incorporating spare parts, maintenance, overhaul and repair (MRO) is inherently more cyclical than aircraft production because demand is closely linked to growth in air traffic and fleet utilisation trends.

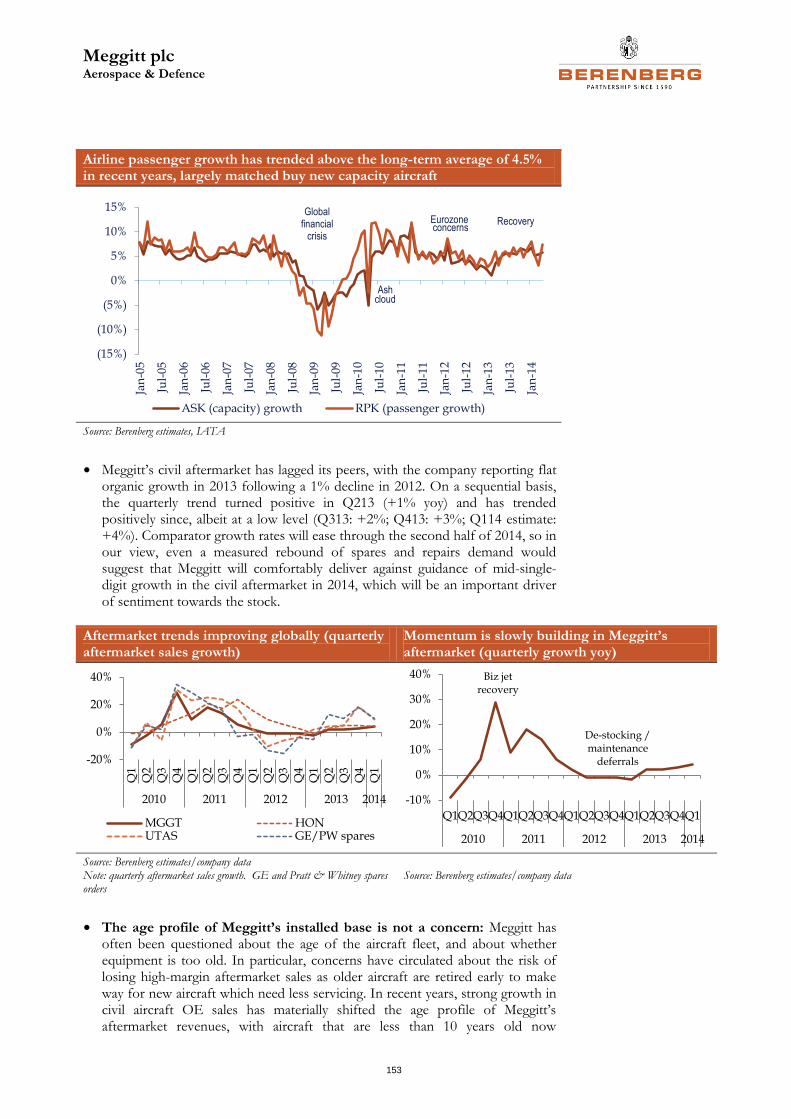

Industry aftermarket growth was below trend growth through 2013

Over the past two years, industry aftermarket growth rates have dipped below long-term trends (which are typically around 1.5% to 2.0% points above global GDP), despite airlines’ improved financial health and steady growth in passenger demand. This is partly due to careful fleet management and cash conservation by the airlines, for example in response to slowing air traffic growth and economic concerns about the eurozone through the second half on 2012. As a result, passenger growth and airline capacity decelerated through 2012 into 2013 which in turn led to a slowdown in aftermarket, exacerbated by airlines deferring and/or reducing maintenance content and working down parts inventory.

Passenger growth (RPKs) and airline capacity growth (ASKs)

Source: IATA

Macro backdrop is supportive of a return to growth

Aviation industry trends are improving with airline profitability increasing and global passenger growth sustaining above the long-term trend of around 4.5%. International Air Transport Association (IATA) traffic data shows sequentially improving half-yearly growth in passenger demand, measured in revenue passenger kilometres (RPKs) as follows: H113: +4.5%; H213: +5.9%; 2014 ytd: 6.0%. Airline capacity trends, measured in available seat kilometres (ASKs), which are a good proxy for the aftermarket, have followed: H113: +3.7%, H213: +5.9%; 2014 ytd: 5.8%. IATA predicts further above trend growth in ASKs for the full year of 5.4% (versus 5.2% in 2013 and 3.9% in 2012).

(25%)

(15%)

(5%)

5%

15%

25%

35%

45%

Ap

r-0

1

Ap

r-0

2

Ap

r-0

3

Ap

r-0

4

Ap

r-0

5

Ap

r-0

6

Ap

r-0

7

Ap

r-0

8

Ap

r-0

9

Ap

r-1

0

Ap

r-1

1

Ap

r-1

2

Ap

r-1

3

Ap

r-1

4

ASKs (Capacity) RPK (passenger growth)

9/11 attacks

Gulf War II and SARS Global

financial crisis

Ash cloud

Eurozone concerns

Aerospace & Defence

27

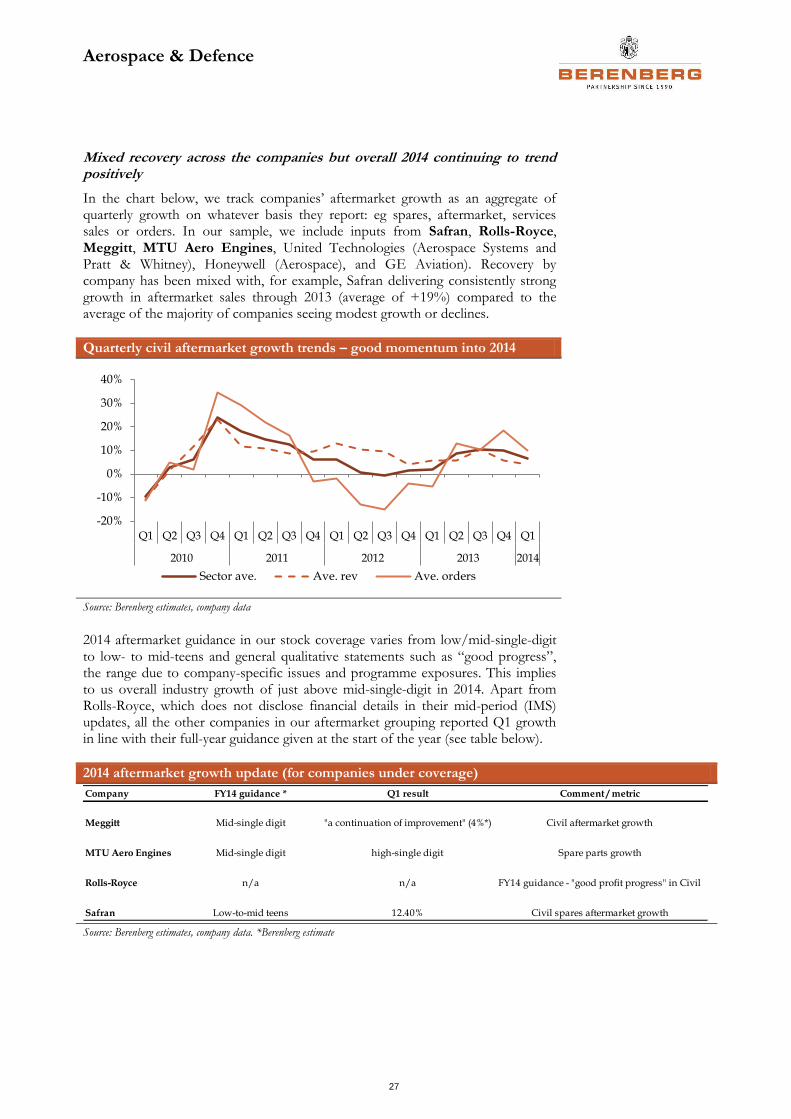

Mixed recovery across the companies but overall 2014 continuing to trend positively

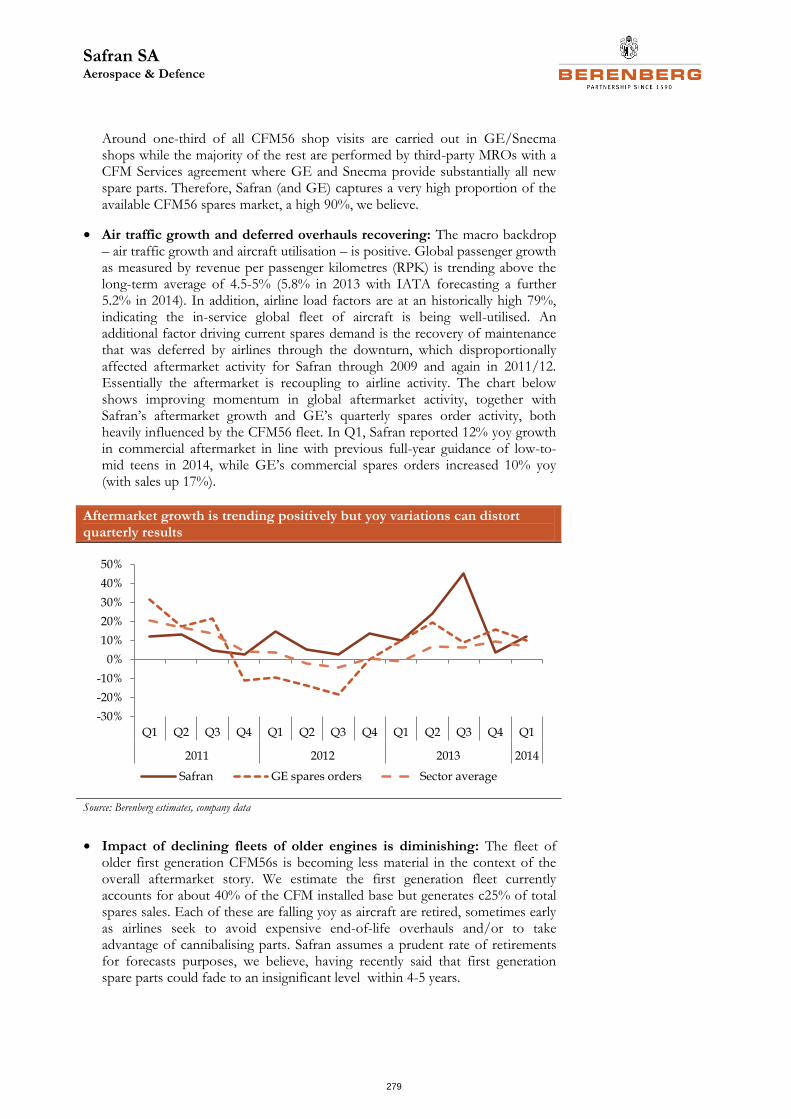

In the chart below, we track companies’ aftermarket growth as an aggregate of quarterly growth on whatever basis they report: eg spares, aftermarket, services sales or orders. In our sample, we include inputs from Safran, Rolls-Royce, Meggitt, MTU Aero Engines, United Technologies (Aerospace Systems and Pratt & Whitney), Honeywell (Aerospace), and GE Aviation). Recovery by company has been mixed with, for example, Safran delivering consistently strong growth in aftermarket sales through 2013 (average of +19%) compared to the average of the majority of companies seeing modest growth or declines.

Quarterly civil aftermarket growth trends – good momentum into 2014

Source: Berenberg estimates, company data

2014 aftermarket guidance in our stock coverage varies from low/mid-single-digit to low- to mid-teens and general qualitative statements such as “good progress”, the range due to company-specific issues and programme exposures. This implies to us overall industry growth of just above mid-single-digit in 2014. Apart from Rolls-Royce, which does not disclose financial details in their mid-period (IMS) updates, all the other companies in our aftermarket grouping reported Q1 growth in line with their full-year guidance given at the start of the year (see table below).

2014 aftermarket growth update (for companies under coverage)

Source: Berenberg estimates, company data. *Berenberg estimate

-20%

-10%

0%

10%

20%

30%

40%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2010 2011 2012 2013 2014

Sector ave. Ave. rev Ave. orders

Company FY14 guidance * Q1 result Comment / metric

Meggitt Mid-single digit "a continuation of improvement" (4%*) Civil aftermarket growth

MTU Aero Engines Mid-single digit high-single digit Spare parts growth

Rolls-Royce n/a n/a FY14 guidance - "good profit progress" in Civil

Safran Low-to-mid teens 12.40% Civil spares aftermarket growth

Aerospace & Defence

28

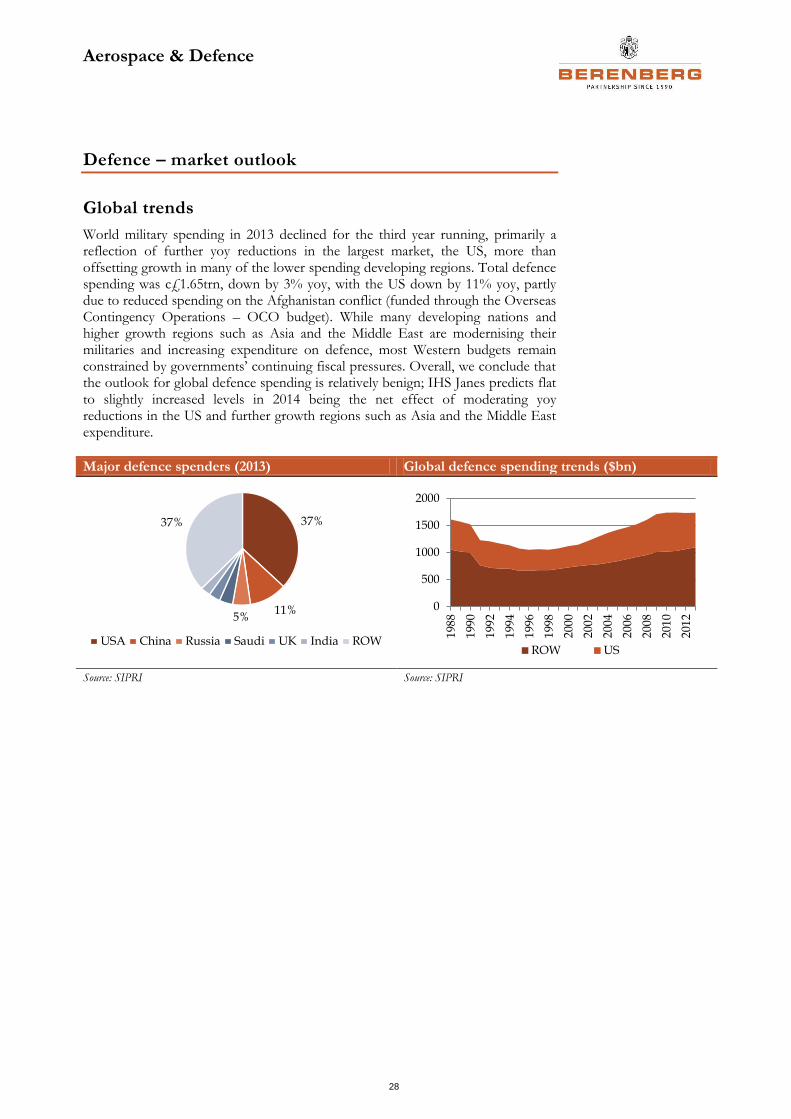

Defence – market outlook

Global trends

World military spending in 2013 declined for the third year running, primarily a reflection of further yoy reductions in the largest market, the US, more than offsetting growth in many of the lower spending developing regions. Total defence spending was c£1.65trn, down by 3% yoy, with the US down by 11% yoy, partly due to reduced spending on the Afghanistan conflict (funded through the Overseas Contingency Operations – OCO budget). While many developing nations and higher growth regions such as Asia and the Middle East are modernising their militaries and increasing expenditure on defence, most Western budgets remain constrained by governments’ continuing fiscal pressures. Overall, we conclude that the outlook for global defence spending is relatively benign; IHS Janes predicts flat to slightly increased levels in 2014 being the net effect of moderating yoy reductions in the US and further growth regions such as Asia and the Middle East expenditure.

Major defence spenders (2013) Global defence spending trends ($bn)

Source: SIPRI Source: SIPRI

37%

11%5%

37%

USA China Russia Saudi UK India ROW

0

500

1000

1500

2000

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

2010

201

2

ROW US

Aerospace & Defence

29

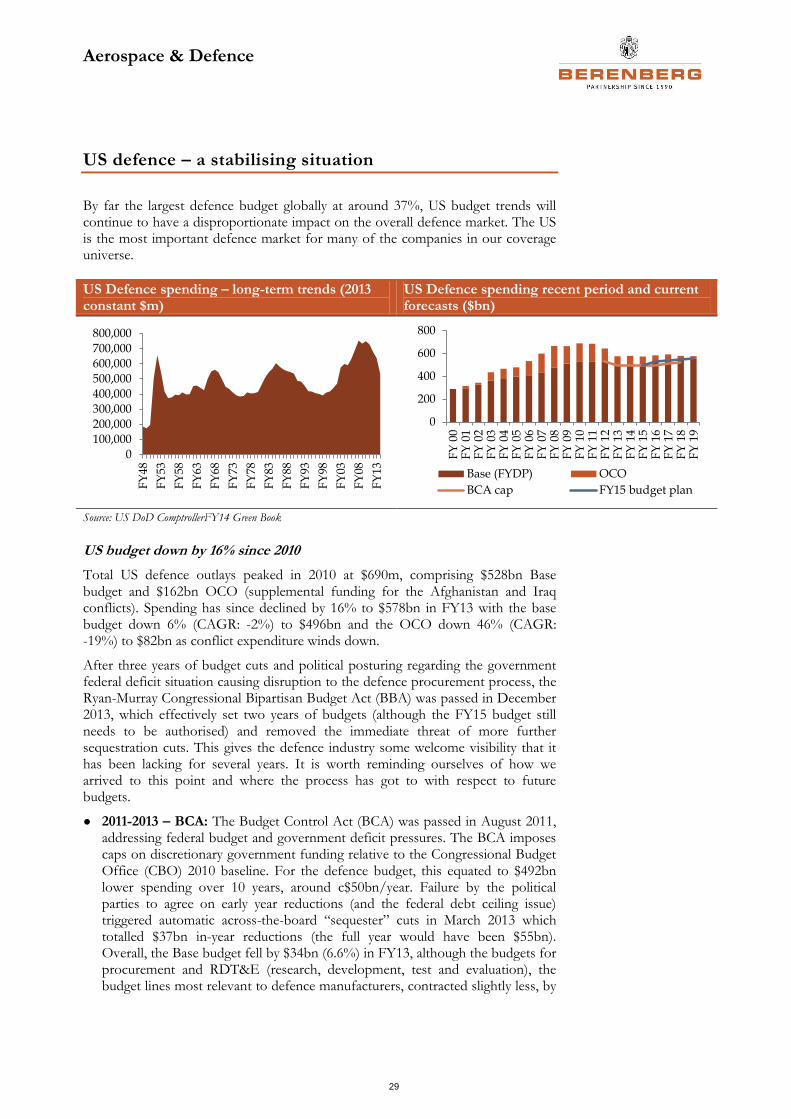

US defence – a stabilising situation

By far the largest defence budget globally at around 37%, US budget trends will continue to have a disproportionate impact on the overall defence market. The US is the most important defence market for many of the companies in our coverage universe.

US Defence spending – long-term trends (2013 constant $m)

US Defence spending recent period and current forecasts ($bn)

Source: US DoD ComptrollerFY14 Green Book

US budget down by 16% since 2010

Total US defence outlays peaked in 2010 at $690m, comprising $528bn Base budget and $162bn OCO (supplemental funding for the Afghanistan and Iraq conflicts). Spending has since declined by 16% to $578bn in FY13 with the base budget down 6% (CAGR: -2%) to $496bn and the OCO down 46% (CAGR: -19%) to $82bn as conflict expenditure winds down.

After three years of budget cuts and political posturing regarding the government federal deficit situation causing disruption to the defence procurement process, the Ryan-Murray Congressional Bipartisan Budget Act (BBA) was passed in December 2013, which effectively set two years of budgets (although the FY15 budget still needs to be authorised) and removed the immediate threat of more further sequestration cuts. This gives the defence industry some welcome visibility that it has been lacking for several years. It is worth reminding ourselves of how we arrived to this point and where the process has got to with respect to future budgets.

● 2011-2013 – BCA: The Budget Control Act (BCA) was passed in August 2011, addressing federal budget and government deficit pressures. The BCA imposes caps on discretionary government funding relative to the Congressional Budget Office (CBO) 2010 baseline. For the defence budget, this equated to $492bn lower spending over 10 years, around c$50bn/year. Failure by the political parties to agree on early year reductions (and the federal debt ceiling issue) triggered automatic across-the-board “sequester” cuts in March 2013 which totalled $37bn in-year reductions (the full year would have been $55bn). Overall, the Base budget fell by $34bn (6.6%) in FY13, although the budgets for procurement and RDT&E (research, development, test and evaluation), the budget lines most relevant to defence manufacturers, contracted slightly less, by

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

FY

48

FY

53

FY

58

FY

63

FY

68

FY

73

FY

78

FY

83

FY

88

FY

93

FY

98

FY

03

FY

08

FY

13

0

200

400

600

800

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

Base (FYDP) OCO

BCA cap FY15 budget plan

Aerospace & Defence

30

4.1% to £155bn. Through this period there was significant uncertainty around the exact nature of cuts and risks to future funding lines, which was exacerbated by late annual budget agreements (forcing prolonged periods of budgeting under multi- part-year Continuing Resolutions) and resulted in a dislocated procurement environment. As a result, order and contract approval delays have been commonplace.

● December 2013 – January 2014: The BBA was passed in December 2013. This is a two-year budget agreement which avoids a further government shut down and replaces sequester spending cuts with savings from future-year cuts. In January, the “Omnibus Appropriations Bill” was passed containing the FY14 Defense Appropriations Bill and outline of the FY15 request.

● May 2015: In the route to finalising the FY15 Defense budget, the Senate Armed Services Committee passed its version of the 2015 National Defense Authorisation Act (NDAA) on 22 May at levels consistent with spending caps for FY15 set out in the BBA; namely authorisations of $496bn (flat yoy) for the Base budget including $91bn for procurement (-2.1% yoy) and $64bn for RDT&E (+1.2% yoy)

● OCO: The OCO is separate from Base defence spending and indeed exempt from BCA spending caps. OCO spending peaked in 2008 at $187bn falling to $82bn in 2013. The FY14 budget actually increased 3.9% yoy to $85bn but reduces by 6.8% in FY15 to $79bn. As troop drawdown continues, we expect annual OCO spending will decline for foreseeable future. We expect a reduction to a much lower number when troop drawdown is complete, and when remaining in-country commitments are defined.

Longer-term budget outlook is flat although sequestration risks remain