Benetton Full costing and direct costing lezione e …...1. the variable costing method; 2. the...

15

ATTIVITÀ DIDATTICHE 1 RiViSTA online CLIL: FULL COSTING AND DIRECT COSTING METHOD di Sonia BENETTON MATERIE: ECONOMIA AZIENDALE (Classe quinta IT AFM, RIM, SIA) Il materiale didattico proposto, da utilizzare nelle lezioni con la meto- dologia CLIL, si compone di tre parti: un testo destinato agli studenti che consente di apprendere in lingua inglese, anche con il supporto di esempi applicativi, i metodi di calcolo dei costi (full costing e direct co- sting); una serie di diapositive che l’insegnante può utilizzare in aula con la LIM per la spiegazione degli argomenti; una prova strutturata, da somministrare al termine delle lezioni, per verificare il livello di co- noscenze e abilità acquisite dagli studenti. INTRODUCTION. A central task of managers is cost management, a term to describe the actions managers undertake in the short-run and long-run planning and control costs which strategically increase the value chain and lower the costs and prices of products and services. Understanding costs is useful in many contexts for determing ways of containing costs, for replacing a product with another, for evaluating stocks etc. Generally speaking a cost is a resource forgone to achieve a specific objective, an amount paid to acquire goods and services while a cost object is anything for which a separate measurement is required, for example a product, a service, a project, a brand category, a department, a production line etc. Cost allocation is the process of identifying, aggregating and assigning costs to cost objects and it plays a strategic role in every organization. Cost usually are divided in : 1. variable cost: is a cost that changes in proportion to changes in the related level of total activity or volume; 2. fixed cost: is a cost that does not change in total when changes the related level of activity or volume; 3. direct cost: is any cost that is related to the cost object and can be traced to that cost in an economically feasible way; 4. indirect cost: is a cost that is related to the cost object but cannot be traced to it in an economically feasible way and is allocated to the cost object using a cost-allocation method (one base; multiple base, cost centre). Costs may be simultaneously: 1. direct and variable (materials for a product); 2. direct and fixed (equipment depreciation for a department); 3. indirect and variable (indirect manufacturing labour); 4. indirect and fixed (distribution overheads, administrative costs). There are two commonly methods distinguished for their different approach to the cost and which help companies take decisions: 1. the variable costing method; 2. the absorption (full) costing method. The former is the most frequently used for decision making and performance evaluation purpose, while the latter is used for external reporting because of its accepted accounting principles. 1. VARIABLE COSTING METHOD. This method collects to a cost object only costs that are related to this particular cost object (variable costs and fixed costs) and can be traced to it in an economically feasible way. For example: take a bag as a cost object, the cost of the leather used to make the bag is a direct and, in this case, a variable cost too. The amount of materials used in making the bag can easily be traced to the bag. Variable costing method highlights :

Transcript of Benetton Full costing and direct costing lezione e …...1. the variable costing method; 2. the...

ATTIVITÀ DIDATTICHE 1

RiViSTA online

CLIL: FULL COSTING AND DIRECT COSTING METHOD

di Sonia BENETTON

MATERIE: ECONOMIA AZIENDALE (Classe quinta IT AFM, RIM, SIA) Il materiale didattico proposto, da utilizzare nelle lezioni con la meto-dologia CLIL, si compone di tre parti: un testo destinato agli studenti che consente di apprendere in lingua inglese, anche con il supporto di esempi applicativi, i metodi di calcolo dei costi (full costing e direct co-sting); una serie di diapositive che l’insegnante può utilizzare in aula con la LIM per la spiegazione degli argomenti; una prova strutturata, da somministrare al termine delle lezioni, per verificare il livello di co-noscenze e abilità acquisite dagli studenti.

INTRODUCTION. A central task of managers is cost management, a term to describe the actions managers undertake in the short-run and long-run planning and control costs which strategically increase the value chain and lower the costs and prices of products and services. Understanding costs is useful in many contexts for determing ways of containing costs, for replacing a product with another, for evaluating stocks etc. Generally speaking a cost is a resource forgone to achieve a specific objective, an amount paid to acquire goods and services while a cost object is anything for which a separate measurement is required, for example a product, a service, a project, a brand category, a department, a production line etc.

Cost allocation is the process of identifying, aggregating and assigning costs to cost objects and it plays a strategic role in every organization. Cost usually are divided in : 1. variable cost: is a cost that changes in proportion to changes in the related level of total activity or

volume;2. fixed cost: is a cost that does not change in total when changes the related level of activity or volume;3. direct cost: is any cost that is related to the cost object and can be traced to that cost in an economically

feasible way;4. indirect cost: is a cost that is related to the cost object but cannot be traced to it in an economically

feasible way and is allocated to the cost object using a cost-allocation method (one base; multiple base,cost centre).

Costs may be simultaneously: 1. direct and variable (materials for a product);2. direct and fixed (equipment depreciation for a department);3. indirect and variable (indirect manufacturing labour);4. indirect and fixed (distribution overheads, administrative costs).

There are two commonly methods distinguished for their different approach to the cost and which help companies take decisions: 1. the variable costing method;2. the absorption (full) costing method.

The former is the most frequently used for decision making and performance evaluation purpose, while the latter is used for external reporting because of its accepted accounting principles.

1. VARIABLE COSTING METHOD. This method collects to a cost object only costs that are related tothis particular cost object (variable costs and fixed costs) and can be traced to it in an economically feasibleway.For example: take a bag as a cost object, the cost of the leather used to make the bag is a direct and, in thiscase, a variable cost too. The amount of materials used in making the bag can easily be traced to the bag.Variable costing method highlights :

ATTIVITÀ DIDATTICHE 2

RiViSTA online

1. the first level contribution margin that is the difference between revenues and all variable direct costs;2. the second level contribution margin that is the difference between the first level margin and the

specific fixed cost.

The contribution margin can be expressed as total, as an amount per unit or as percentages. The first contribution margin help managers understand how a product covers fixed costs and what product should be preferred to increase company's profit. Planning decisions about production include an analysis of the first contribution margin as total and the first contribution margin per unit.

Example 1 Alpha company manufactures two products: product X and product Y. Data regarding these products are as follows:

Product X Product Y Units produced 500 600 Selling price per unit € 45 € 60 Variable cost per unit € 20 € 50 Fixed cost € 12.000 € 900

Solution Product X Total Product Y Total

Selling price € 45 € 22.500 € 60 € 36.000 Variable cost € 20 € 10.000 € 50 € 30.000 First level contribution margin € 25 € 12.500 € 10 € 6.000 Fixed cost € 12.000 € 900 Second level contribution margin € 500 € 5.100

Assume that company has the opportunity to produce other 100 products. Evaluate whether Alpha made the correct decision manufacturing product X .

Solution New profit 25 x 100 € 2.500 10 x 100 € 1.000

The first level contribution margin of product X is higher than product Y and gives more profit for the same number of units. Alpha company made the correct decision.

ATTIVITÀ DIDATTICHE 3

RiViSTA online

Example 2 Now suppose markets demand 100 units of product at the same selling price. Product X needs additional fixed costs of 4.000 euros while product Y an amount of 800 euros. Alpha company decided to produce product X because of its first level margin (25>10). Evaluate whether Alpha made the correct decision producing 100 units of product X . Consider the following figures:

Product X Product Y Units produced 100 100 Selling price per unit € 45 € 60 Variable cost per unit € 20 € 50 Fixed cost € 4.000 € 800

In this case the answer is as follow: Product X Total Product Y Total

Selling price € 45 € 4.500 € 60 € 6.000 Variable cost € 20 € 2.000 € 50 € 5.000 First level contribution margin € 25 € 2.500 € 10 € 1.000 Fixed cost € 4.000 € 800 Second level contribution margin -€ 1.500 € 200

Alpha company considered the first level contribution margin of product X (€ 25) rather than the second level contribution margin of product X (-€ 1.500). In this case it did not consider the added fixed costs which were strategic to take the correct choice.

Conclusion: first level margin is vital to take decisions about the right product to promote because first level contribution margin shows how the product covers fixed costs, but at the same time it is important to remember the general context and the second level contribution margin to understand the impact of the fixed costs, especially for the production of a new order.

2. FULL (ABSORPTION) COSTING METHOD. This method collects to a cost object all direct andindirect costs. While direct costs are related and traced to it in a cost-effective way, indirect costs are allocatedto the cost object using a cost-allocation method that could be based on a single cost-allocation base, or on amultiple cost- allocation base or on the cost centres method.A single cost allocation base supposes that only a factor is the parameter to allocate a group of indirect coststo a cost object; while multiple cost allocation base uses more factors as a common denominator for linking anindirect cost or group of costs to a cost object.The cost centres method adds indirect costs to different cost centres that are business organizational entitywhich a specific function.

They may be: 1. real centres: organizational material units such as purchasing division, sale departments, etc ;2. non-real centres: organizational non-material units such as buildings management centre which collects

all costs for rent, maintenance and heating expenses.

ATTIVITÀ DIDATTICHE 4

RiViSTA online

They may be: 1. production centres: in which all products are manufactured or processed;2. auxiliary centres: they provide measurable services to other centres (for example the maintenance

centre),3. production overhead services centres: they provide non-measurable services to production centres (for

example research and development department);4. functional centres: they include all administrative, commercial and personnel areas.

The main phases to calculate the cost of a product are: 1. to divide direct and indirect costs;2. to allocate direct cost to products, production, auxiliary and functional centres;3. to overturn the costs of production overhead services centres to other cost centres;4. to overturn the costs of auxiliary centres to the centres which use their services;5. to overturn the costs of functional centres to the cost object,6. to overturn the costs of production centres to the cost object.

Example 1 Consider Beta company using data contained in the following table :

Product A 500 units

Product B 600 units

Total 1.100 units

Direct materials € 1.750 € 2.160 € 3.910 Direct manufacturing labour € 800 € 720 € 1.520 Indirect manufacturing labour (variable costs) € 950 Depreciation (fixed cost) € 2.200 Production overheads € 4.000 Total manufacturing costs € 12.580

The following table shows how the total cost changes as indirect production costs are allocated under a single cost-allocation base, or on a multiple cost- allocation base or on the cost centres method.

1. Single cost-allocation base (indirect manufacturing labour under units sold )Table 1 Product A

500 units Product B 600 units

Total 1.100 units

Direct materials € 1.750 € 2.160 € 3.910 Direct manufacturing labour € 800 € 720 € 1.520 Prime cost € 2.550 € 2.880 € 5.430 Overhead costs € 3.250 € 3.900 € 7.150 Total manufacturing cost € 5.800 € 6.780 € 12.580 Cost per unit 5.800/500 = 11,60 6.780/600 = 11,30 (950+2.200+4.000)= 7.150 overhead costs 7.150: (500+600) = 6,5 allocation coefficient 6,5 x 500 = 3.250 euros for product A 6,5x 600 = 3.900 euros for product B

In this case the cost-allocation shows that manufacturing cost per unit of product A is higher than product B (11,60>11,30).

ATTIVITÀ DIDATTICHE 5

RiViSTA online

2. Multiple cost-allocation base:• indirect manufacturing labour costs are allocated under direct labour costs;• depreciation costs are allocated under machine-hours (500 for A; 1.700 for B);• production overheads are allocated under direct material costs.

Table 2 Product A 500 units

Product B 600 units

Total 1.100 units

Direct materials € 1.750 € 2.160 € 3.910 Direct manufacturing labour € 800 € 720 € 1.520 Prime cost € 2.550 € 2.880 € 5.430 Indirect manufacturing labour € 500 € 450 € 950 Depreciation € 500 € 1.700 € 2.200 Production overheads € 1.790,29 € 2.209,71 € 4.000 Total manufacturing cost € 5.340,29 € 7.239,71 € 12.580 Cost per unit 5.340,29/500 = 10,68 7.239,71/600 = 12,07

950 : (800 + 720) = 0,625 allocation coefficient for indirect manufacturing labour 0,625 x 800 = 500 euros for product A 0,625 x 720 = 450 euro for product B

2.200 : (500 + 1.700) = 1 allocation coefficient for depreciation 1 x 500 = 500 euros for product A 1 x 1.700 = 1.700 euros for product B

4.000 : (1.750 + 2.160) = 1,02301 allocation coefficient for production overheads 1,02302 x 1.750 = 1.790,29 euros for product A 1,02302 x 2.160 = 2.209,71 euros for product B

In this case the multiple cost-allocation base shows that the manufacturing cost of product A is cheaper than the manufacturing cost of product B (10,68<12,07).

COST CENTRES METHOD. Suppose that Beta compay has two auxiliary centres :maintenance centre and quality control centre. • Maintenance centre: where workers focus their efforts in supervising the production line and general

troubleshooting .• Quality control centre: where workers pay attention to the speed of the production and to the quality of

goods and services.• Product A is processed in two departments (X,Y) while product B needs to be manufactured in three

departments. (X,Y,Z) . Departments costs are allocated on the base of units produced and sold.• X , Y and Z departments need services from maintenance and quality control centres , but with different

percentages.

ATTIVITÀ DIDATTICHE 6

RiViSTA online

Table 3.1 Product A - 500 units

Product B - 600 units

Total 1.100 units

Direct materials € 2.160 € 3.910

Direct manufacturing labour € 800 € 720 € 1.520 Indirect manufacturing labour (variable cost) € 950 Depreciation (fixed cost) € 2.200 Production overheads € 4.000 Maintenance centre 60% of indirect manufacturing labour;

40% depreciation costs 30% production overheads

Quality control centre 40% of indirect manufacturing labour; 60% depreciation costs 70% production overheads

X DEPARTMENT Y DEPARTMENT Z DEPARTMENT TOTAL 30% maintenance centre 40% quality control center

50% maintenance centre 20% quality control centre

20% maintenance centre 40% quality control center

100%

100% PRODUCT A, B PRODUCT A, B PRODUCT B

Solution Table 3.2 Maintenance Quality control Total Indirect manufactoring labour € 570 (950x60%) € 380 (950x40%) € 950 Depreciation costs € 880 (2200x40%) € 1.320 (2200x60%) € 2.200 Production overheads € 1.200 (4000x30%) € 2.800 (4000x70%) € 4.000 Total cost € 2.650 € 4.500 € 7.150

Tab. 3.3 X department

Y department

Z department

Total Auxiliary centres Maintenance € 795 (2650x30%) € 1.325 (2650x50%) € 530 (2650x20%) € 2.650 Quality control € 1.800 (4500x40%) € 900 (4500x20%) € 1.800(4500x40%) € 4.500 Total cost € 2.595 € 2.225 € 2.330 € 7.150

ATTIVITÀ DIDATTICHE 7

RiViSTA online

Tab 3.4 Product A Product B Total Costs X department € 1.179,55 € 1.415,45 € 2.595,00 Y department € 1.011,37 € 1.213,63 € 2.225,00 Z department € 2.330,00 € 2.330,00 Total overhead costs € 2.190,92 € 4.959,08 € 7.150,00

2.595/(500+600) = 2,35909 allocation coefficient 2,35909 x 500 = 1.179,55 euros for product A 2,35909 x 600 = 1.415,45 euros for product B 2.225/(500+600) = 2,02273 allocation coefficient 2,02273 x 500 =1.011,37 euros for product A 2,02273 x 600 = 1.213,63 euros for product B

Table 3.5 Product A 500 units

Product B 600 units

Total 1.100 units

Direct materials € 1.750,00 € 2.160,00 € 3.910,00 Direct manufacturing labour € 800,00 € 720,00 € 1.520,00 Prime cost € 2.550,00 € 2.880,00 € 5.430,00 Overhead costs € 2.190,92 € 4.959,08 € 7.150,00 Total manufacturing cost € 4.740,92 € 7.839,08 € 12.580,00 Cost per unit 4.740,92/500 = 9,48 7.839,08/600 = 13,07

Cost centres method shows that manufacturing cost of product A is cheaper than manufacturing cost of product B (9,48 < 13,07) and the difference between the two costs per unit is very important for decision making. Cost figures play a key role in many important decisions. The use of an inappropriate cost-allocation base can cause products to be manufactured less efficiently or managers may take solutions that conflict with a correct vision of the economic context, and finally products can be mispriced in the market place.

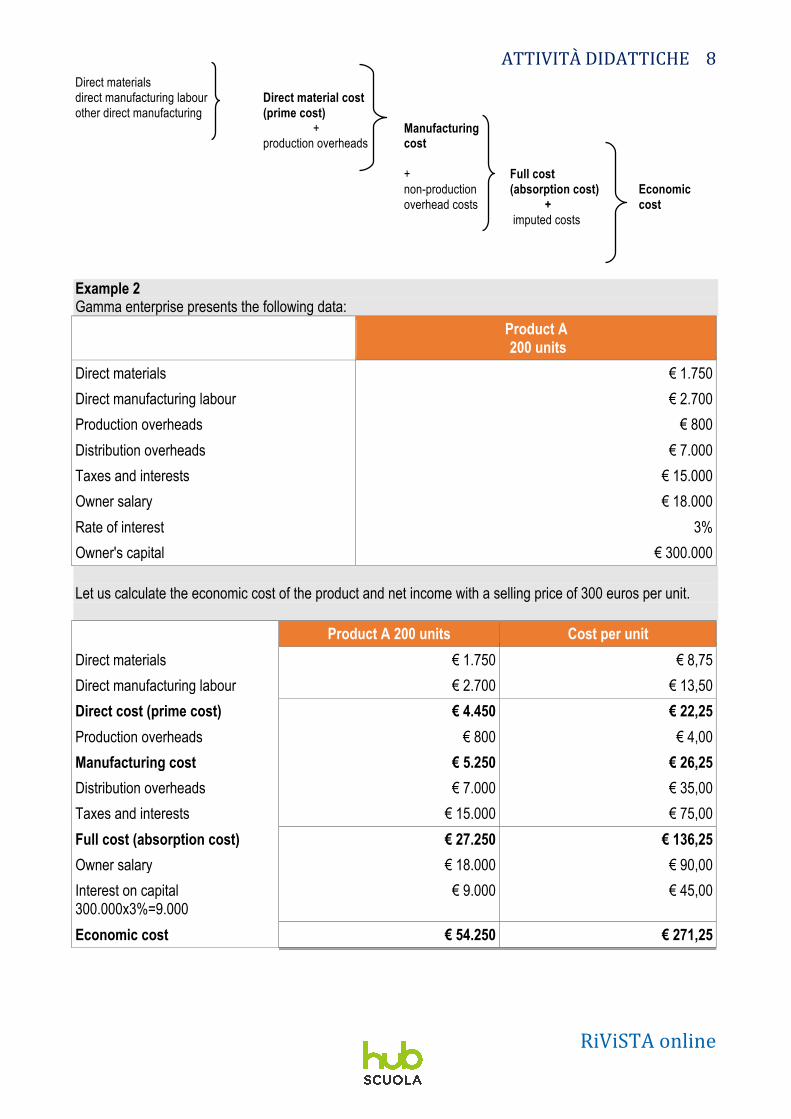

COST FRAME. Now consider all costs allocated to a cost object (not only manufacturing costs); the cost frame would be: 1. direct material cost (prime cost): the sum of direct materials/labour costs;2. manufacturing cost: the sum of direct materials/labour costs and production overheads;3. full (absorption) cost: the sum of manufacturing cost and non-production overhead costs (selling

overheads, taxes, interests, etc);4. economic cost: the sum of full cost and imputed costs (lost interest in a different business investment and

owner's annual salary).

ATTIVITÀ DIDATTICHE 8

RiViSTA online

Direct materials direct manufacturing labour Direct material cost other direct manufacturing (prime cost)

+ Manufacturingproduction overheads cost

+ Full costnon-production (absorption cost) Economic overhead costs + cost

imputed costs

Example 2 Gamma enterprise presents the following data:

Product A 200 units

Direct materials € 1.750 Direct manufacturing labour € 2.700 Production overheads € 800 Distribution overheads € 7.000 Taxes and interests € 15.000 Owner salary € 18.000 Rate of interest 3% Owner's capital € 300.000

Let us calculate the economic cost of the product and net income with a selling price of 300 euros per unit.

Product A 200 units Cost per unit Direct materials € 1.750 € 8,75 Direct manufacturing labour € 2.700 € 13,50 Direct cost (prime cost) € 4.450 € 22,25 Production overheads € 800 € 4,00 Manufacturing cost € 5.250 € 26,25 Distribution overheads € 7.000 € 35,00 Taxes and interests € 15.000 € 75,00 Full cost (absorption cost) € 27.250 € 136,25 Owner salary € 18.000 € 90,00 Interest on capital 300.000x3%=9.000

€ 9.000 € 45,00

Economic cost € 54.250 € 271,25

ATTIVITÀ DIDATTICHE 9

RiViSTA online

Product A Per unit Total Selling price € 300,00 € 60.000,00 Full cost € 136,25 € 27.250,00 Net income € 163,75 € 32.750,00

Product A Per unit Total Selling price € 300,00 € 60.000,00 Economic cost € 271,25 € 54.250,00 Profit € 28,75 € 5.750,00

TEST

EXERCISE 1 Tick the statement which are true of false and in case of false write the correct phrase.

1 Cost allocation is the process of identifying, aggregating and assigning costs to cost objects and it plays a strategic role in every organization. ……………………………………………………………………………………..

T F

2 Variable cost : is a cost that does not change in proportion to changes in the related level of total activity or volume. ……………………………………………………………………………………..

T F

3 Fixed cost: is a cost that does not change in total when changes the related level of activity or volume. ……………………………………………………………………………………..

T F

4 Direct cost: is any cost that is not related to the cost object and can not be traced to that cost in an economically feasible way. ……………………………………………………………………………………..

T F

5 Variable costing method is the most frequently used for decision making and performance evaluation purpose. ……………………………………………………………………………………..

T F

6 The first level contribution margin is the difference between revenues and all variable direct costs. ……………………………………………………………………………………..

T F

7 The second level contribution margin that is the difference between the first level margin and the specific fixed cost. ……………………………………………………………………………………..

T F

8 Real centres : organizational non-material units such as purchasing division , sale departments, etc . ……………………………………………………………………………………..

T F

9 Production centres: they provide measurable services to other centres (for example the maintenance centre). ……………………………………………………………………………………..

T F

10 Manufacturing cost: the sum of indirect materials/labour costs and production overheads. ……………………………………………………………………………………..

T F

ATTIVITÀ DIDATTICHE 10

RiViSTA online

EXERCISE 2 Complete the sentences using the words listed below.

allocation, production line, traced, revenues, imputed , fixed, real, measurable, the sum, maintenance, units, cost objects, overheads, management, feasible, lost ,workers, increase, first level margin ,difference.

1. Cost …........... describes the actions managers undertake in the short-run and long-run planning and control costs which strategically …...... the value chain and lower the costs and prices of products and services.

2. Cost …...... is the process of identifying, aggregating and assigning costs to ….. ….... and it plays a strategic role in every organization.

3. Direct cost: is any cost that is related to the cost object and can be …..... to that cost in an economically …....... way.

4. The first level contribution margin that is the …....... between ….... and all variable direct costs. 5. The second level contribution margin that is the difference between the........ ......... ........and the

specific …..... cost. 6. …...... centres : organizational material …...... such as purchasing division , sale departments, etc . 7. Auxiliary centres: they provide …....... services to other centres ( for example the …...... centre). 8. Manufacturing cost: …......of direct materials/labour costs and production …........ 9. Economic cost :...... ....... of full cost and imputed costs ( ….... interest in a different business

investment and owner's annual salary). 10. Maintenance centre: where …..... focus their efforts in supervising the …...... …..... and general

troubleshooting .

EXERCISE 3 Alpha company manufactures two products: product A and product B . Data regarding these products are as follows:

Product A Product B Units produced 200 300 Selling price per unit € 50 € 40 Variable cost per unit € 30 € 10 Fixed cost € 5.000 € 4.500

A) Calculate the first level contribution margin and the second level contribution marginProduct A Total Product B Total

Selling price € ….. € ….... € …. € …...... Variable cost € ….. €....... € ….. € …...... First level contribution margin € …... € …...... €...... € …...... Fixed cost € 5.000 € ….... Second level contribution margin € ….... € 4.500

Now assume that company has the opportunity to produce other 200 products.

B) Evaluate whether Alpha made the correct decision manufacturing product B .

ATTIVITÀ DIDATTICHE 11

RiViSTA online

New profit …...x 200 € ….... …...x 200 € …......

The first level contribution margin of product A/B is higher than product A/B and gives more profit for the same number of units . Alpha company made the right/wrong decision.

EXERCISE 4 Consider Beta company using data contained in the following table:

Product A 250 units

Product B 300 units

Total 550 units

Direct materials € …....... € 2.800 € 4.800 Direct manufacturing labour € 1.000 € 1.200 € 2.200 Indirect manufacturing labour (variable costs) € 700 Depreciation (fixed cost) € 800 Production overheads € 2.000 Total manufacturing costs € 10.500

Assume Beta company allocate overhead costs under a single cost-allocation base (units sold) 1. calculate the total manufacturing cost2. calculate the manufacturing cost per unit

Product A 250 units

Product B 300 units

Total …....units

Direct materials € 2.000 € ….... € 4.800 Direct manufacturing labour € …....... € 1.200 € 2.200 Prime cost € …..... € …........ € …..... Overhead costs € …...... € 1.909,09 € …..... Total manufacturing cost € …...... € …........... € …........ Cost per unit …......./250 =....... 5.909,09/...... = 19,70

(700 + ...... + 2.000)= 3.500 overhead costs 3.500 : (…. + 300) = 6,363636 allocation coefficient …........ x ….. = 1.590,91 euros for product A …......... x ….. = …........ euros for product B

ATTIVITÀ DIDATTICHE 12

RiViSTA online

EXERCISE 5 Gamma enterprise presents the following data:

Product A 500 units Direct materials € 5.000 Direct manufacturing labour € 8.000 Production overheads € 12.000 Distribution overheads € 3.500 Taxes and interests € 4.000 Owner salary € 20.000 Rate of interest 2% Owner's capital € 200.000

Calculate: 1. the economic cost of the product as total and per unit2. the net income with a selling price of 120 euros as total and per unit3. the profit of product A as total and per unit

Product A 500 units

Cost per unit

Direct materials € ….... € ….... Direct manufacturing labour € ….... € 16,00 Direct cost (prime cost) € 13.000 € ….... Production overheads € …..... € 24,00 Manufacturing cost € ….... € ….... Distribution overheads € ….... € ….... Taxes and interests € 4.000 …..... Full cost (absorption cost) ….......... € 65,00 Owner salary € …...... € …...... Interest on capital 200000 x 2% …......... …....... Economic cost € 56.500 ….............

Product A Per unit Total Selling price € 120,00 …............. Full cost € 65,00 …............. Net income …........ € 27.500,00

Product A Per unit Total Selling price € 120,00 € 60.000,00 Economic cost …............ …............ Profit € 7,00 ….............

ATTIVITÀ DIDATTICHE 13

RiViSTA online

CORRECTION

CLIL: FULL COSTING AND DIRECT COSTING METHOD

EXERCISE 1 1. T; 2. F. Variable cost: is a cost that changes in proportion to changes in the related level of total activity orvolume; 3. T; 4. F. Direct cost: is any cost that is related to the cost object and can be traced to that cost inan economically feasible way; 5. T; 6. T; 7. T; 8. F. Real centres: organizational material units such aspurchasing division, sale departments, etc; 9. F Production centres: in which all products are manufacturedor processed; 10. F. Manufacturing cost: the sum of direct materials/labour costs and production overheads.

EXERCISE 2 1. management, increase2. allocation, cost objects3. traced, feasible4. difference, revenues5. first level margin, fixed6. real, units7. measurable, maintenance8. the sum, overheads9. imputed, lost10. workers, production line

EXERCISE 3 A).

Product A Total Product B Total Selling price € 50 € 10.000 € 40 € 12.000 Variable cost € 30 € 6.000 € 10 € 3.000 First level contribution margin € 20 € 4.000 € 30 € 9.000

Fixed cost € 5.000 € 4.500 Second level contribution margin -€ 1.000 € 4.500

B) New profit 20 x 200 € 4.000 30 x 200 € 6.000

The first level contribution margin of product B is higher than product A and gives more profit for the same number of units. Alpha company made the right decision.

The new order could cover fixed costs of product A . The net income could be 9.500 euros ( -1.000+4.500+6.000).

ATTIVITÀ DIDATTICHE 14

RiViSTA online

EXERCISE 4 Product A 250 units

Product B 300 units

Total 550 units

Direct materials € 2.000 € 2.800 € 4.800 Direct manufacturing labour € 1.000 € 1.200 € 2.200 Prime cost € 3.000 € 4.000,00 € 7.000 Overhead costs € 1.590,91 € 1.909,09 € 3.500 Total manufacturing cost € 4.590,91 € 5.909,09 € 10.500 Cost per unit 4.590,91/250 =18,36 5.909,09/300 = 19,70

(700 + 800 + 2.000) = 3.500 overhead costs 3.500: (250 + 300) = 6,363636 allocation coefficient 6,363636 x 250 = 1.590,91 euros for product A 6,363636 x 300= 1.909,09 euros for product B

EXERCISE 5 Product A 500 units

Cost per unit

Direct materials € 5.000 € 10,00 Direct manufacturing labour € 8.000 € 16,00 Direct cost (prime cost) € 13.000 € 26,00 Production overheads € 12.000 € 24,00 Manufacturing cost € 25.000 € 50,00 Distribution overheads € 3.500 € 7,00 Taxes and interests € 4.000 € 8,00 Full cost (absorption cost) € 32.500 € 65,00 Owner salary € 20.000 € 40,00 Interest on capital 200.000 x 2% € 4.000 € 8,00 Economic cost € 56.500,00 € 113,00

Product A Per unit Total Selling price € 120,00 € 60.000,00 Full cost € 65,00 € 32.500,00 Net income € 55,00 € 27.500,00

Product A Per unit Total Selling price € 120,00 € 60.000,00 Economic cost € 113,00 € 56.500,00 Profit € 7,00 € 3.500

ATTIVITÀ DIDATTICHE 15

RiViSTA online

TABELLA VALUTAZIONE ESERCIZIO PUNTEGGIO PUNTEGGIO MASSIMO

1. Vero falso 1 punto per ogni risposta esatta 1 punto con esatta formulazione

15

2. Completamento 2,5 punti per ogni frase completata 25 3. Esercizio guidato 20 punti per lo svolgimento corretto 20 4. Esercizio guidato 20 punti per lo svolgimento corretto 20 5. Esercizio guidato 20 punti per lo svolgimento corretto 20 Punteggio totale 100

PROVA COMPLESSIVA PUNTEGGIO GIUDIZIO

0-49 Gravemente insufficiente (1-4) 50-59 Insufficiente (5) 60-69 Sufficiente (6) 70-79 Discreto (7) 80-89 Buono (8)

90-100 Ottimo (9-10)