Belarusian Economy: macroeconomic trends.

18

PRESENTATION OF THE REPUBLIC OF B E L A R U S OF B E L A R U S February 2013 1

-

Upload

ambasciata-bielorussa-in-italia -

Category

Documents

-

view

241 -

download

0

description

Presentazione della situazione macroeconomica in Bielorussia.

Transcript of Belarusian Economy: macroeconomic trends.

PRESENTATION OF THE REPUBLIC OF BELARUSOF BELARUS

February 2013

1

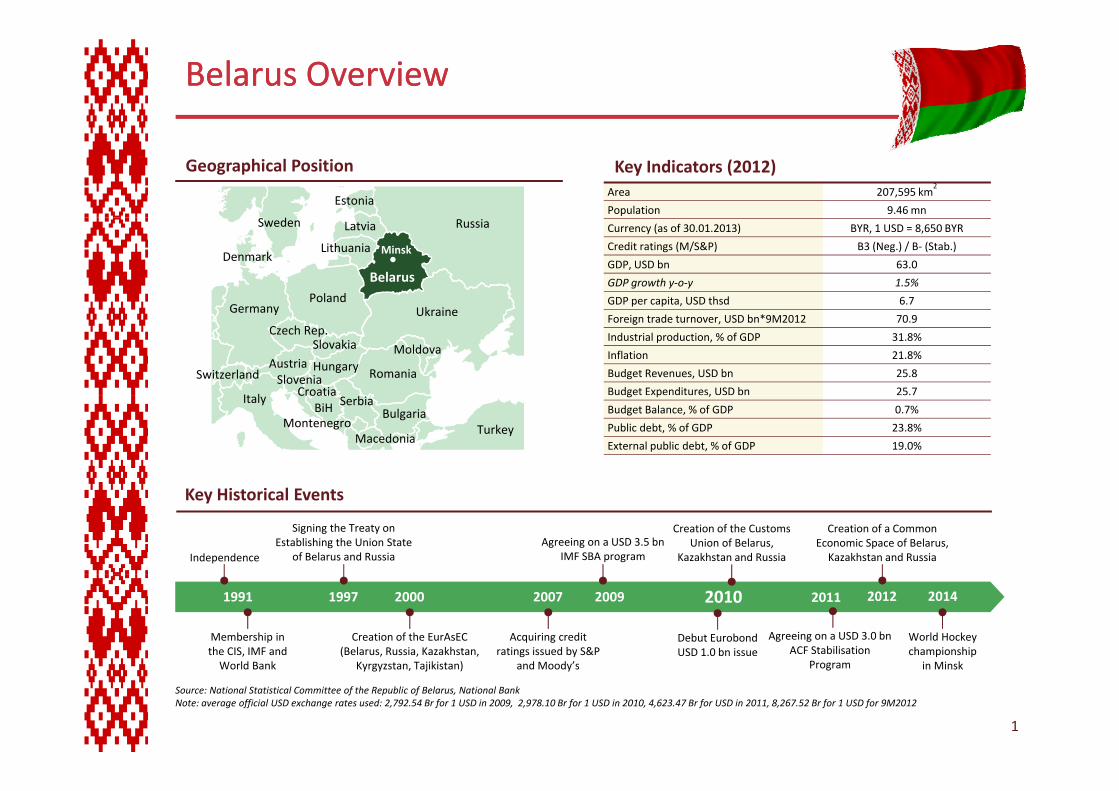

Belarus OverviewBelarus Overview

Geographical Position Key Indicators (2012)Area 207,595 km

2

Population 9.46 mnEstonia

Currency (as of 30.01.2013) BYR, 1 USD = 8,650 BYR

Credit ratings (M/S&P) B3 (Neg.) / B‐ (Stab.)

GDP, USD bn 63.0

GDP growth y‐o‐y 1.5%

GDP per capita, USD thsd 6.7Poland

Russia

Lithuania

Latvia

G

Sweden

Denmark

Belarus

Minsk

p p ,

Foreign trade turnover, USD bn*9M2012 70.9

Industrial production, % of GDP 31.8%

Inflation 21.8%

Budget Revenues, USD bn 25.8

Budget Expenditures, USD bn 25.7

Moldova

Germany

RomaniaHungary

SlovakiaCzech Rep.

Austria

It l

Switzerland

Ukraine

SloveniaCroatia g p ,

Budget Balance, % of GDP 0.7%

Public debt, % of GDP 23.8%

External public debt, % of GDP 19.0%

SerbiaBulgaria

Italy

Turkey

CroatiaBiH

MontenegroMacedonia

Key Historical Events

Creation of the Customs Union of Belarus,

Kazakhstan and Russia

Creation of a Common Economic Space of Belarus, Kazakhstan and Russia

Agreeing on a USD 3.5 bnIMF SBA program

Signing the Treaty on Establishing the Union State

of Belarus and RussiaIndependence

1991 20122010

Membership in the CIS, IMF and World Bank

2000

Creation of the EurAsEC(Belarus, Russia, Kazakhstan,

Kyrgyzstan Tajikistan)

2007

Acquiring credit ratings issued by S&P

and Moody’s

World Hockey championship

in Minsk

20091997 2014

Debut Eurobond USD 1.0 bn issue

2011

Agreeing on a USD 3.0 bnACF Stabilisation

Program

Source: National Statistical Committee of the Republic of Belarus, National Bank Note: average official USD exchange rates used: 2,792.54 Br for 1 USD in 2009, 2,978.10 Br for 1 USD in 2010, 4,623.47 Br for USD in 2011, 8,267.52 Br for 1 USD for 9M2012

World Bank Kyrgyzstan, Tajikistan) and Moody s in Minsk

1

Program

Investment HighlightsInvestment Highlights

Well‐diversified economy with focus on industrial productionfocus on industrial production

Improving businessImproving business environment and increasing competitiveness

One of the most qualified labor force in Eastern Europe

Active foreign trade playerEffective macroeconomicand budgetary policies

Ability to absorb external turbulence:y

Managed floating exchange rate mechanism

International reserves increase

2

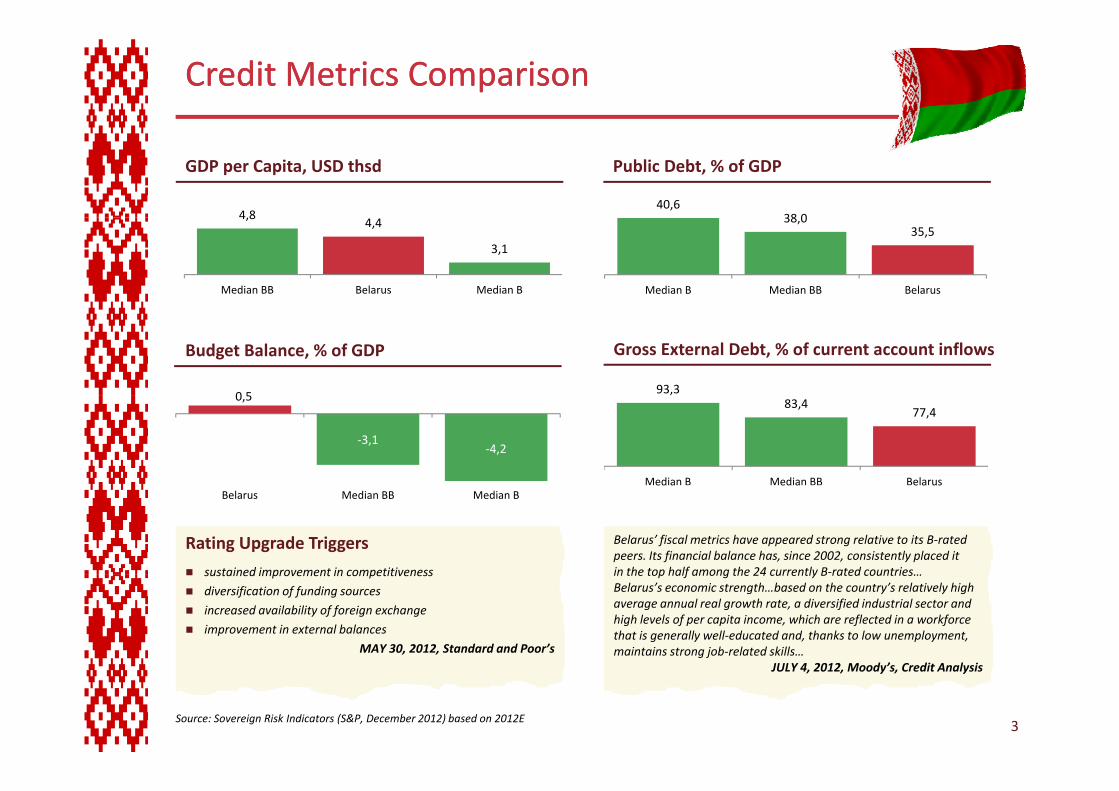

Credit Metrics ComparisonCredit Metrics Comparison

GDP per Capita, USD thsd

4 8

Public Debt, % of GDP

40,638 04,8

4,4

3,1

Median BB Belarus Median B

38,035,5

Median B Median BB Belarus

Budget Balance, % of GDP

0 5

Gross External Debt, % of current account inflows

93,30,5

‐3,1‐4,2

83,477,4

Median B Median BB BelarusBelarus Median BB Median B

ed a ed a e a us

Belarus’ fiscal metrics have appeared strong relative to its B‐rated peers. Its financial balance has, since 2002, consistently placed it in the top half among the 24 currently B‐rated countries…

Belarus’ fiscal metrics have appeared strong relative to its B‐rated peers. Its financial balance has, since 2002, consistently placed it in the top half among the 24 currently B‐rated countries…

Rating Upgrade Triggers

sustained improvement in competitiveness

Rating Upgrade Triggers

sustained improvement in competitiveness in the top half among the 24 currently B rated countries…Belarus’s economic strength…based on the country’s relatively high average annual real growth rate, a diversified industrial sector and high levels of per capita income, which are reflected in a workforce that is generally well‐educated and, thanks to low unemployment, maintains strong job‐related skills…

JULY 4 2012 M d ’ C dit A l i

in the top half among the 24 currently B rated countries…Belarus’s economic strength…based on the country’s relatively high average annual real growth rate, a diversified industrial sector and high levels of per capita income, which are reflected in a workforce that is generally well‐educated and, thanks to low unemployment, maintains strong job‐related skills…

JULY 4 2012 M d ’ C dit A l i

sustained improvement in competitiveness

diversification of funding sources

increased availability of foreign exchange

improvement in external balances

MAY 30, 2012, Standard and Poor’s

sustained improvement in competitiveness

diversification of funding sources

increased availability of foreign exchange

improvement in external balances

MAY 30, 2012, Standard and Poor’s

3

JULY 4, 2012, Moody’s, Credit AnalysisJULY 4, 2012, Moody’s, Credit Analysis

Source: Sovereign Risk Indicators (S&P, December 2012) based on 2012E

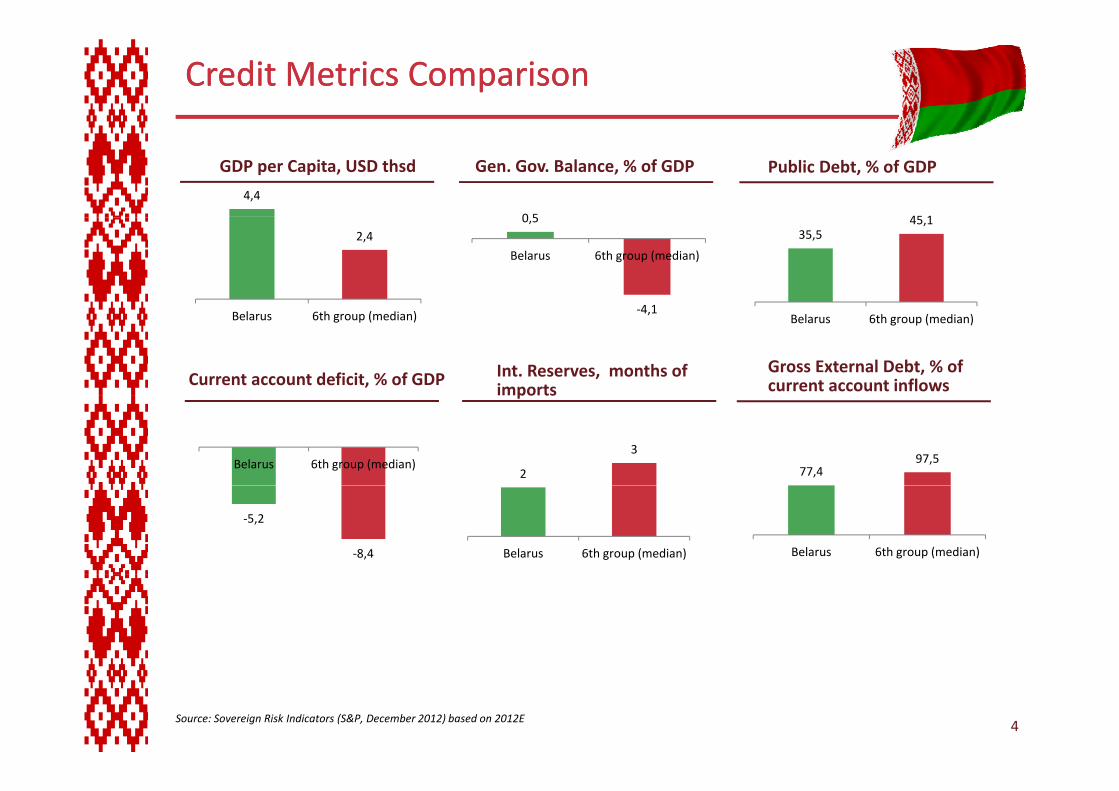

Credit Metrics ComparisonCredit Metrics Comparison

Gen. Gov. Balance, % of GDPGDP per Capita, USD thsd Public Debt, % of GDP

4,4

0 5 45 12,4

0,5

4 1

Belarus 6th group (median)

35,545,1

Gross External Debt, % of current account inflows

Belarus 6th group (median) ‐4,1Belarus 6th group (median)

Current account deficit, % of GDP Int. Reserves, months of imports

Belarus 6th group (median)

po ts

2

3

77,497,5

‐5,2

‐8,4 Belarus 6th group (median) Belarus 6th group (median)

4Source: Sovereign Risk Indicators (S&P, December 2012) based on 2012E

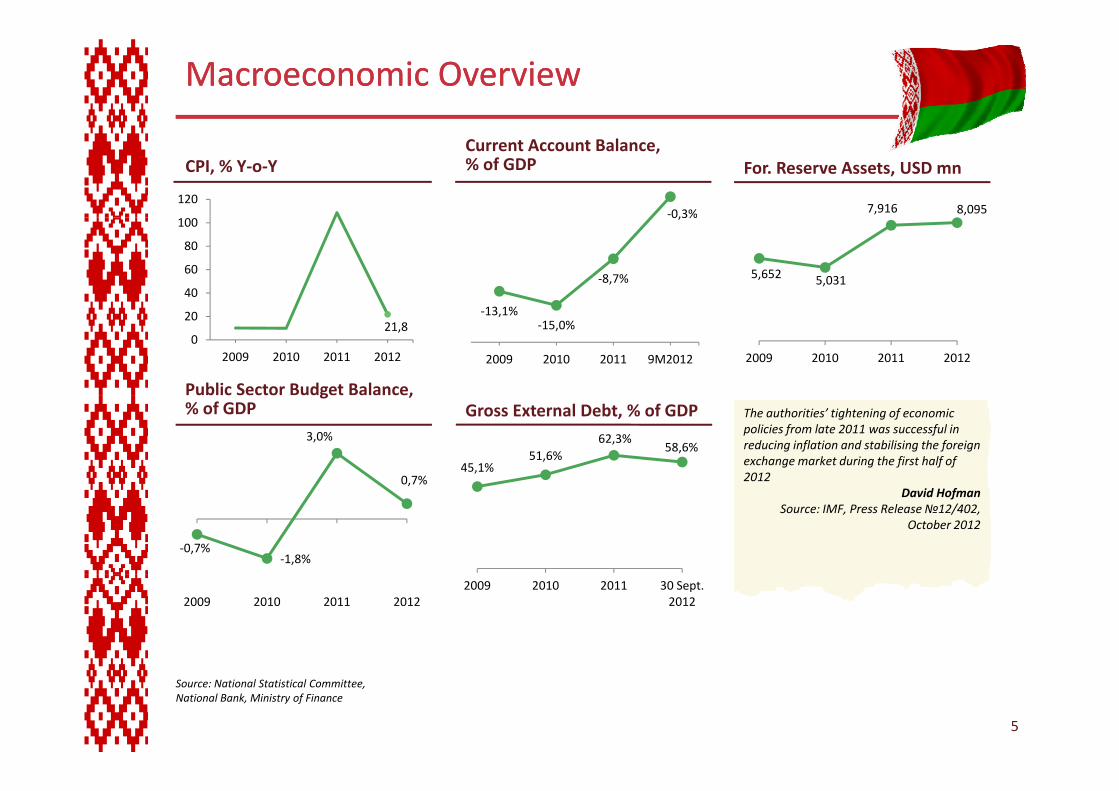

Macroeconomic OverviewMacroeconomic Overview

120

For. Reserve Assets, USD mn

‐0 3%

CPI, % Y‐o‐YCurrent Account Balance, % of GDP

7,916 8,095

40

60

80

100

‐8,7%

0,3%

5,652 5,031

21,80

20

2009 2010 2011 2012

‐13,1%‐15,0%

2009 2010 2011 9M2012 2009 2010 2011 2012

Public Sector Budget Balance, Gross External Debt, % of GDP

45,1%51,6%

62,3%58,6%

g ,% of GDP

3,0%

0,7%

The authorities’ tightening of economic policies from late 2011 was successful in reducing inflation and stabilising the foreign exchange market during the first half of 2012

The authorities’ tightening of economic policies from late 2011 was successful in reducing inflation and stabilising the foreign exchange market during the first half of 2012

‐0,7%‐1,8%

,David Hofman

Source: IMF, Press Release№12/402, October 2012

David HofmanSource: IMF, Press Release№12/402,

October 2012

2009 2010 2011 30 Sept. 20122009 2010 2011 2012

5

Source: National Statistical Committee, National Bank, Ministry of Finance

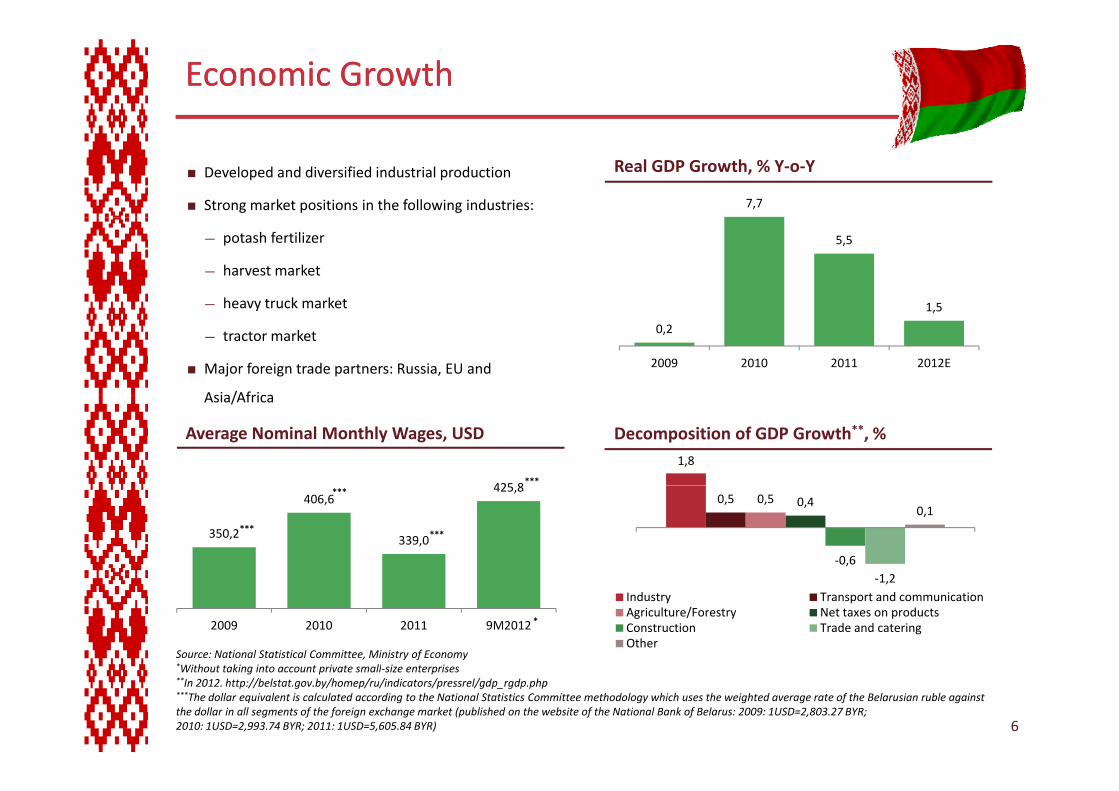

Economic GrowthEconomic Growth

7,7

Real GDP Growth, % Y‐o‐YDeveloped and diversified industrial production

Strong market positions in the following industries:

5,5

1 5

— potash fertilizer

— harvest market

— heavy truck market

0,2

1,5

2009 2010 2011 2012E

heavy truck market

— tractor market

Major foreign trade partners: Russia, EU and

Asia/Africa

Decomposition of GDP Growth**, %1,8

Asia/Africa

425 8

Average Nominal Monthly Wages, USD

***

0,5 0,5 0,4

‐0,61 2

0,1

350,2

406,6

339,0

425,8

***

***

***

‐1,2Industry Transport and communicationAgriculture/Forestry Net taxes on productsConstruction Trade and cateringOther

Source: National Statistical Committee, Ministry of Economy*Wi h ki i i ll i i

2009 2010 2011 9M2012 *

6

*Without taking into account private small‐size enterprises**In 2012. http://belstat.gov.by/homep/ru/indicators/pressrel/gdp_rgdp.php***The dollar equivalent is calculated according to the National Statistics Committee methodology which uses the weighted average rate of the Belarusian ruble against the dollar in all segments of the foreign exchange market (published on the website of the National Bank of Belarus: 2009: 1USD=2,803.27 BYR; 2010: 1USD=2,993.74 BYR; 2011: 1USD=5,605.84 BYR)

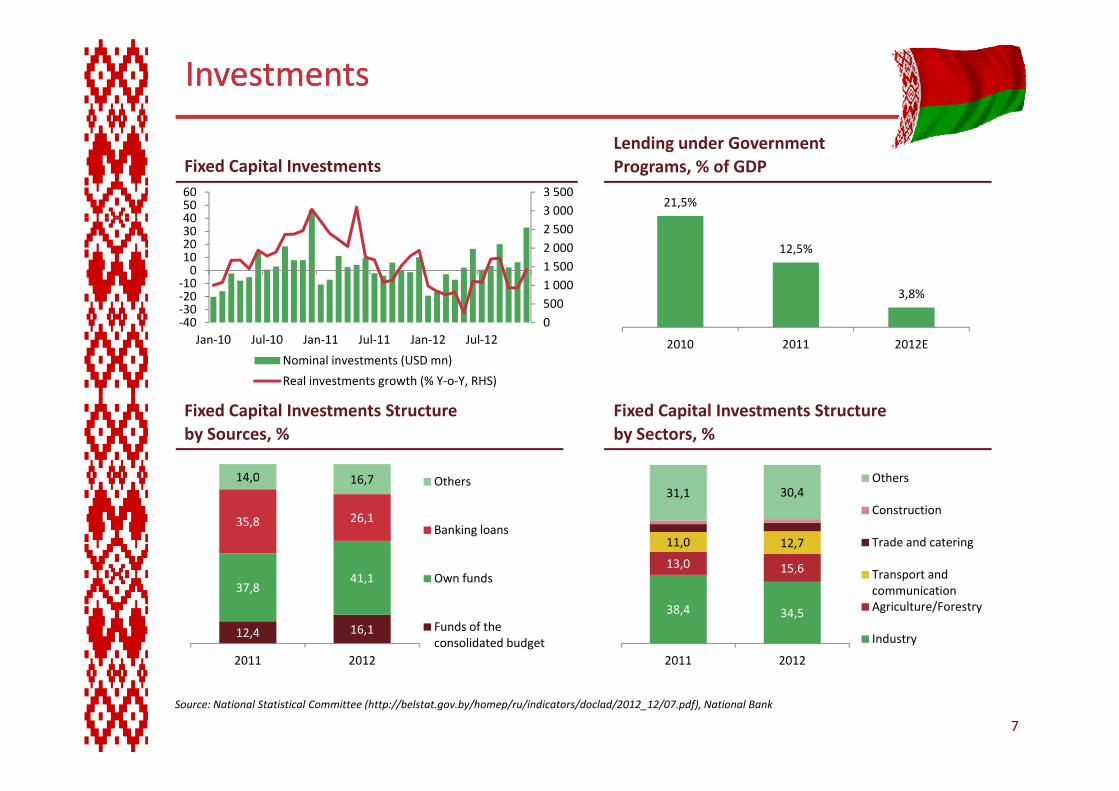

InvestmentsInvestments

3 0003 500

405060

Fixed Capital InvestmentsLending under Government Programs, % of GDP

21,5%

5001 0001 5002 0002 500

30‐20‐100

10203040

12,5%

3,8%

0500

‐40‐30

Jan‐10 Jul‐10 Jan‐11 Jul‐11 Jan‐12 Jul‐12

Nominal investments (USD mn)

Real investments growth (% Y‐o‐Y, RHS)

2010 2011 2012E

Fixed Capital Investments Structure by Sources, %

Fixed Capital Investments Structure by Sectors, %

14,0 16,7 Others Others

41 1

35,8 26,1

, Others

Banking loans

O f d13,0 15,6

11,0 12,7

31,1 30,4Construction

Trade and catering

Transport and

12,4 16,1

37,841,1

2011 2012

Own funds

Funds of the consolidated budget

38,4 34,5

2011 2012

Transport and communicationAgriculture/Forestry

Industry

7

Source: National Statistical Committee (http://belstat.gov.by/homep/ru/indicators/doclad/2012_12/07.pdf), National Bank

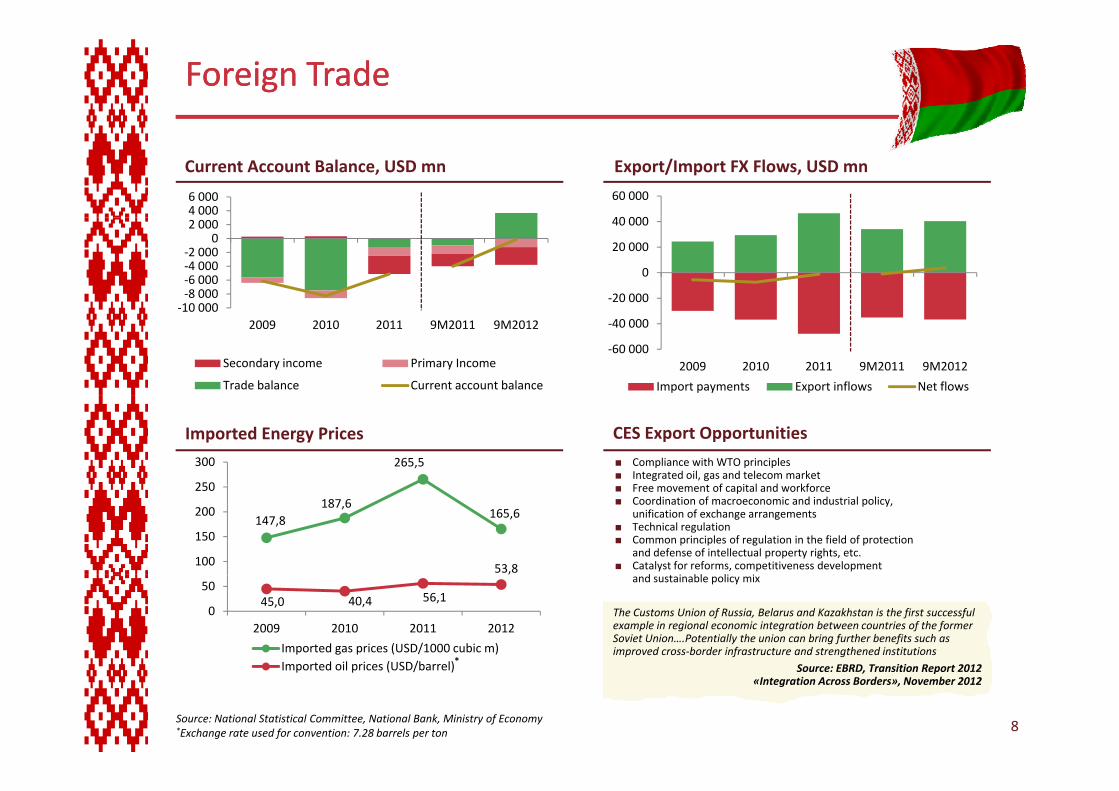

Foreign Foreign TradeTrade

4 0006 000

Current Account Balance, USD mn Export/Import FX Flows, USD mn

60 000

10 000‐8 000‐6 000‐4 000‐2 000

02 000

‐20 000

0

20 000

40 000

‐10 0002009 2010 2011 9M2011 9M2012

Secondary income Primary Income

Trade balance Current account balance

‐60 000

‐40 000

2009 2010 2011 9M2011 9M2012

Import payments Export inflows Net flows

Imported Energy Prices

265,5

250

300 Compliance with WTO principlesIntegrated oil, gas and telecom marketF t f it l d kf

CES Export Opportunities

147,8187,6

165,6

53,8100

150

200

250 Free movement of capital and workforceCoordination of macroeconomic and industrial policy, unification of exchange arrangementsTechnical regulationCommon principles of regulation in the field of protection and defense of intellectual property rights, etc.Catalyst for reforms, competitiveness development d i bl li i

45,0 40,4 56,10

50

2009 2010 2011 2012

Imported gas prices (USD/1000 cubic m)Imported oil prices (USD/barrel)

and sustainable policy mix

The Customs Union of Russia, Belarus and Kazakhstan is the first successful example in regional economic integration between countries of the former Soviet Union….Potentially the union can bring further benefits such as improved cross‐border infrastructure and strengthened institutions

S EBRD T iti R t 2012

The Customs Union of Russia, Belarus and Kazakhstan is the first successful example in regional economic integration between countries of the former Soviet Union….Potentially the union can bring further benefits such as improved cross‐border infrastructure and strengthened institutions

S EBRD T iti R t 2012*

8

Imported oil prices (USD/barrel)

Source: National Statistical Committee, National Bank, Ministry of Economy*Exchange rate used for convention: 7.28 barrels per ton

Source: EBRD, Transition Report 2012 «Integration Across Borders», November 2012

Source: EBRD, Transition Report 2012 «Integration Across Borders», November 2012

External Capital FlowsExternal Capital Flows

2 000

4 000

Capital Account, USD mn FDI Inflow

3 9

6 000

‐4 000

‐2 000

0

2 000

4,02,7

3,92,6 6,6

‐8 000

‐6 000

2009 2010 2011 9M2011 9M2012

Portfolio investments DerivativesOther investments Direct investments

1,9 1,41,1 0,7

,

2009 2010 2011

FDI (USD bn) Privatization receipts (USD bn) FDI/GDP (%)

FDI Inflow by Countries, % as of 9M2012 Investor Protection Ranking*

Country Rank 20132013/2011

Rank Changeg

New Zealand #1 (#1)

Singapore #2 (#2)

Hong Kong #3 (#3)

Kazakhstan #10 34 (#44)

Russia 48.0%

USA 1.2%

Other 13.6%

Kazakhstan #10 34 (#44)

Belarus #82 27 (#109)Russian Federation #117 24 (#93)

Ukraine #117 6 (#109)

Cyprus 4.4%

UK 32.8%

9

Source: National Statistical Committee, National Bank, The World Bank reports “Doing business” for 2013 and 2011 *Ranking is based on investor protection index which is calculated in accordance with the World Bank methodology taking into account quality of information disclosure, degree of management responsibilities and rights of minority shareholders. The index ranges from 0 to 10, with higher values indicating more investor protection

Economic Economic Policy PrioritiesPolicy Priorities

Macroeconomic stabilisation/inflation decrease

Consistency and predictability of macroeconomic policy

Preservation of sustainable long‐term growth:productivity increasecompetitiveness gains CES t t ti lCES export potential FDI attractioneconomy modernizationindustrial innovative developmentp

Lowering dependence on external financing and external debt reduction

Rising productivity efficiency

10

Preserving social achievements and human capital development

Monetary Monetary Policy ObjectivesPolicy Objectives

GuidelinesLatest Achievements

Inflation rate decrease1 Inflation rate decrease1 Inflation reduction

Flexible exchange rate mechanism based on market supply and demand with limited participation of the National Bank

Inflation rate decrease1 Inflation rate decrease1

Economic imbalances reduction2 Economic imbalances reduction2

Financial institutions’ refinancing on market conditions

Maintenance of inflation‐adjusted positive real interest rates

Exchange rate stabilisation3 Exchange rate stabilisation3

Financial stability preservation4 Financial stability preservation4

Inflation Rate Decrease

real interest ratesy py p

Inflation and Refinance Rate Dynamics in 2012

106109 110107106 101

45,0 44,0

38 0

3344

48

61

80

92101

8169 66

56

39

38,0 36,0 35,0 33,3 31,6 30,7 30,2 30,0

11 13 14 18

33 3123 22

Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12 Jul‐12 Oct‐12Inflation % YoY

22,818,0 18,0 20,4 19,2 21,6

15,6

27,6

15,621.6 20,4 16,8

Jan‐12 Mar‐12 May‐12 Jul‐12 Sep‐12 Nov‐12Inflation % MoM Refinance rate %*

Source: National Statistical Committee (http://belstat.gov.by/homep/ru/indicators/doclad/2012_12/12.pdf), National Bank (http://www.nbrb.by/statistics/Dynamic/)*Annualized inflation calculated as monthly rate multiplied by 12 11

Inflation, % YoY Inflation, % MoM Refinance rate, %

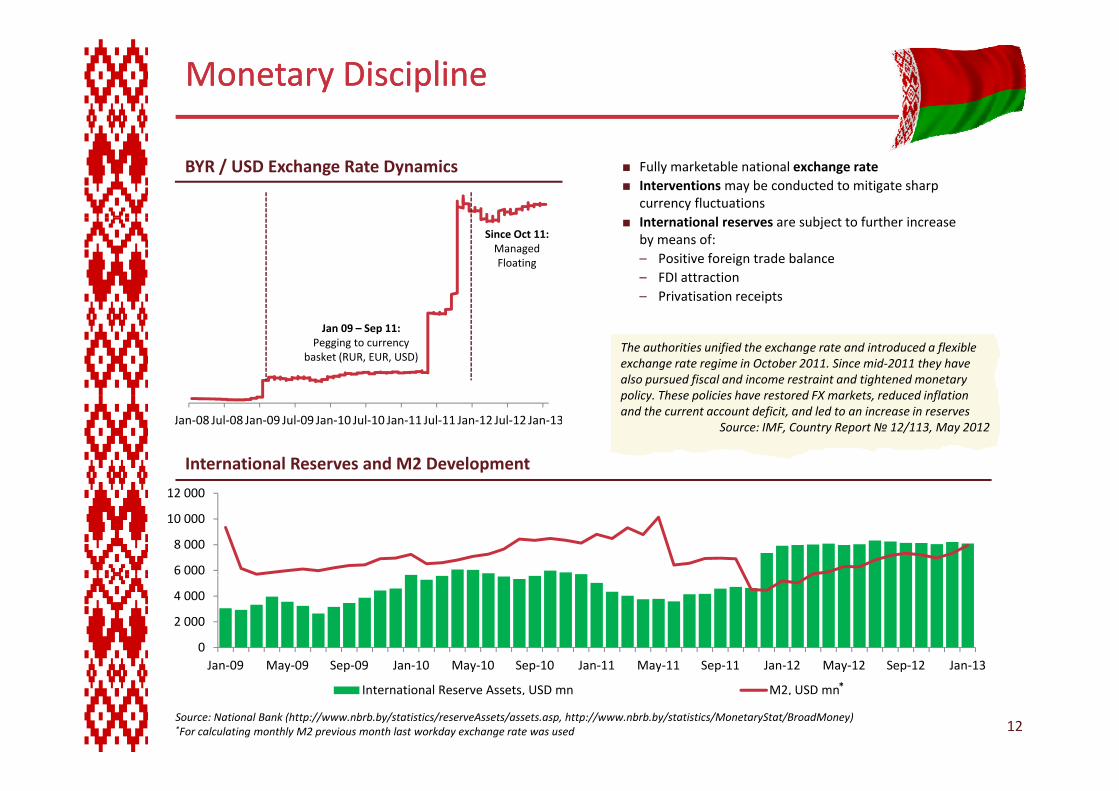

Monetary DisciplineMonetary Discipline

BYR / USD Exchange Rate Dynamics Fully marketable national exchange rate Interventionsmay be conducted to mitigate sharp currency fluctuations

Since Oct 11: ManagedFloating

International reserves are subject to further increase by means of:– Positive foreign trade balance– FDI attraction– Privatisation receipts

Jan 09 – Sep 11:Pegging to currency

basket (RUR, EUR, USD)The authorities unified the exchange rate and introduced a flexible exchange rate regime in October 2011. Since mid‐2011 they have also pursued fiscal and income restraint and tightened monetary policy These policies have restored FX markets reduced inflation

The authorities unified the exchange rate and introduced a flexible exchange rate regime in October 2011. Since mid‐2011 they have also pursued fiscal and income restraint and tightened monetary policy These policies have restored FX markets reduced inflation

Jan‐08 Jul‐08 Jan‐09 Jul‐09 Jan‐10 Jul‐10 Jan‐11 Jul‐11 Jan‐12 Jul‐12 Jan‐13

International Reserves and M2 Development

policy. These policies have restored FX markets, reduced inflation and the current account deficit, and led to an increase in reserves

Source: IMF, Country Report № 12/113, May 2012

policy. These policies have restored FX markets, reduced inflation and the current account deficit, and led to an increase in reserves

Source: IMF, Country Report № 12/113, May 2012

6 000

8 000

10 000

12 000

0

2 000

4 000

Jan 09 May 09 Sep 09 Jan 10 May 10 Sep 10 Jan 11 May 11 Sep 11 Jan 12 May 12 Sep 12 Jan 13

Source: National Bank (http://www.nbrb.by/statistics/reserveAssets/assets.asp, http://www.nbrb.by/statistics/MonetaryStat/BroadMoney) *For calculating monthly M2 previous month last workday exchange rate was used 12

Jan‐09 May‐09 Sep‐09 Jan‐10 May‐10 Sep‐10 Jan‐11 May‐11 Sep‐11 Jan‐12 May‐12 Sep‐12 Jan‐13

International Reserve Assets, USD mn M2, USD mn*

Banking SectorBanking Sector

Deposits by customer type*

Banking Sector highlights*:

– # of banks – 32 (27 with foreign capital participation)

t USD 37 5 b (60 9% f GDP)

Loansby borrower type*

5% 1%– assets – USD 37.5 bn (60.9% of GDP)

– loans– USD 23.6 bn (38.3% of GDP)

– deposits – USD 16.9 bn (27.4% of GDP)

– capital – USD 5.4 bn (8.9% of GDP)

12%

29%54%

%

46%

33%

20%

1%

capital USD 5.4 bn (8.9% of GDP)

– CAR – 20.8% vs. 8% regulatory floor

– ROA – 1.82% public sectorprivate sectorindividuals

33%

public sectorprivate sectorindividuals

Capital Adequacy Ratio and NPL Ratio*

4 2% 3 5%4,2%

5,5%

Banking Sector Rates

80%

non‐bank institutions non‐bank institutions

4,2% 3,5%,

36,2%

30,0%

40%

60%

19,8% 20,5% 24,7% 20,8%

Dec‐09 Dec‐10 Dec‐11 Dec‐12

Capital adequacy NPL Ratio

0%

20%

Jan‐11Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12 Jul‐12 Oct‐12 Jan‐13

Interbank market interest rate Refinancing rate p q y

Source: National Statistical Committee, National Bank (http://www.nbrb.by/statistics/Dynamic, http://www.nbrb.by/statistics/PrStavkiN)*As of 31 Dec. 2012

Interbank market interest rate Refinancing rate

13

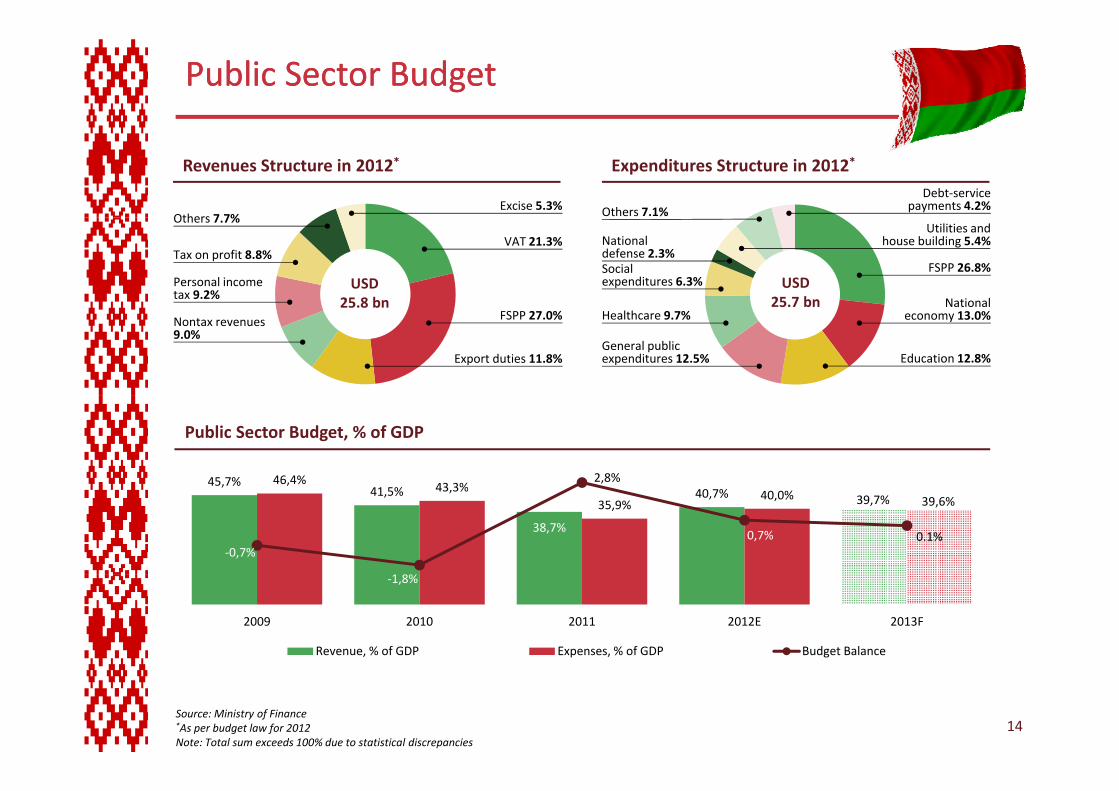

Public Sector BudgetPublic Sector Budget

Revenues Structure in 2012* Expenditures Structure in 2012*

Excise 5.3%Oth 7 7%

Debt‐service payments 4.2%Others 7.1%

USD25.7 bn

Others 7.7%

VAT 21.3%Tax on profit 8.8%

Personal income tax 9.2%

Ot e s . %

FSPP 26.8%

National defense 2.3%

Utilities and house building 5.4%

Social expenditures 6.3%

NationalUSD

25.8 bn 25.7 bnNontax revenues 9.0%

FSPP 27.0%

Export duties 11.8%

Healthcare 9.7%

General public expenditures 12.5%

National economy 13.0%

Education 12.8%

25.8 bn

Public Sector Budget, % of GDP

45,7% 46,4% 43 3%2,8%45,7%

41,5%

38,7%

40,7% 39,7%

, 43,3%35,9%

40,0% 39,6%

‐0,7%

1 8%

0,7% 0.1%

‐1,8%

2009 2010 2011 2012E 2013F

Revenue, % of GDP Expenses, % of GDP Budget Balance

Source: Ministry of Finance*As per budget law for 2012Note: Total sum exceeds 100% due to statistical discrepancies

14

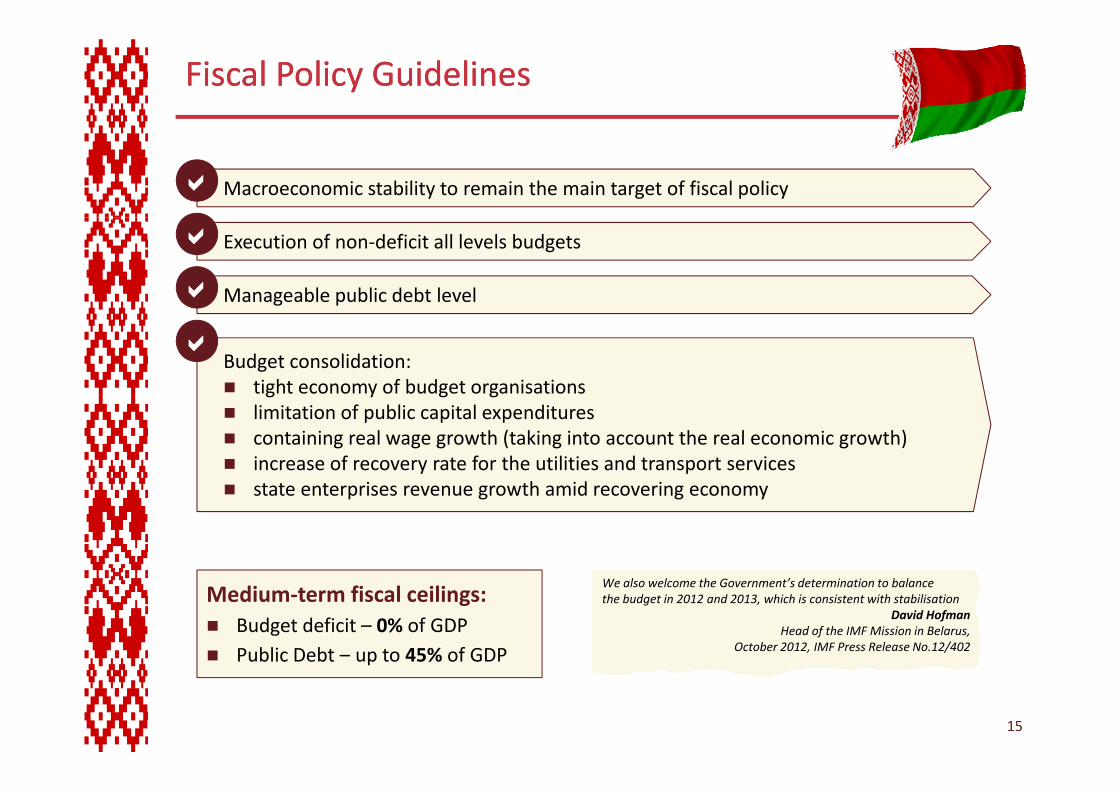

Fiscal Fiscal Policy Policy GuidelinesGuidelines

Macroeconomic stability to remain the main target of fiscal policy

Execution of non‐deficit all levels budgets

Manageable public debt level

Budget consolidation:tight economy of budget organisationsg y g glimitation of public capital expenditurescontaining real wage growth (taking into account the real economic growth)increase of recovery rate for the utilities and transport servicest t t i th id istate enterprises revenue growth amid recovering economy

Medium‐term fiscal ceilings:Budget deficit – 0% of GDPPublic Debt – up to 45% of GDP

We also welcome the Government’s determination to balance the budget in 2012 and 2013, which is consistent with stabilisation

David Hofman Head of the IMF Mission in Belarus,

October 2012, IMF Press Release No.12/402

We also welcome the Government’s determination to balance the budget in 2012 and 2013, which is consistent with stabilisation

David Hofman Head of the IMF Mission in Belarus,

October 2012, IMF Press Release No.12/402p

15

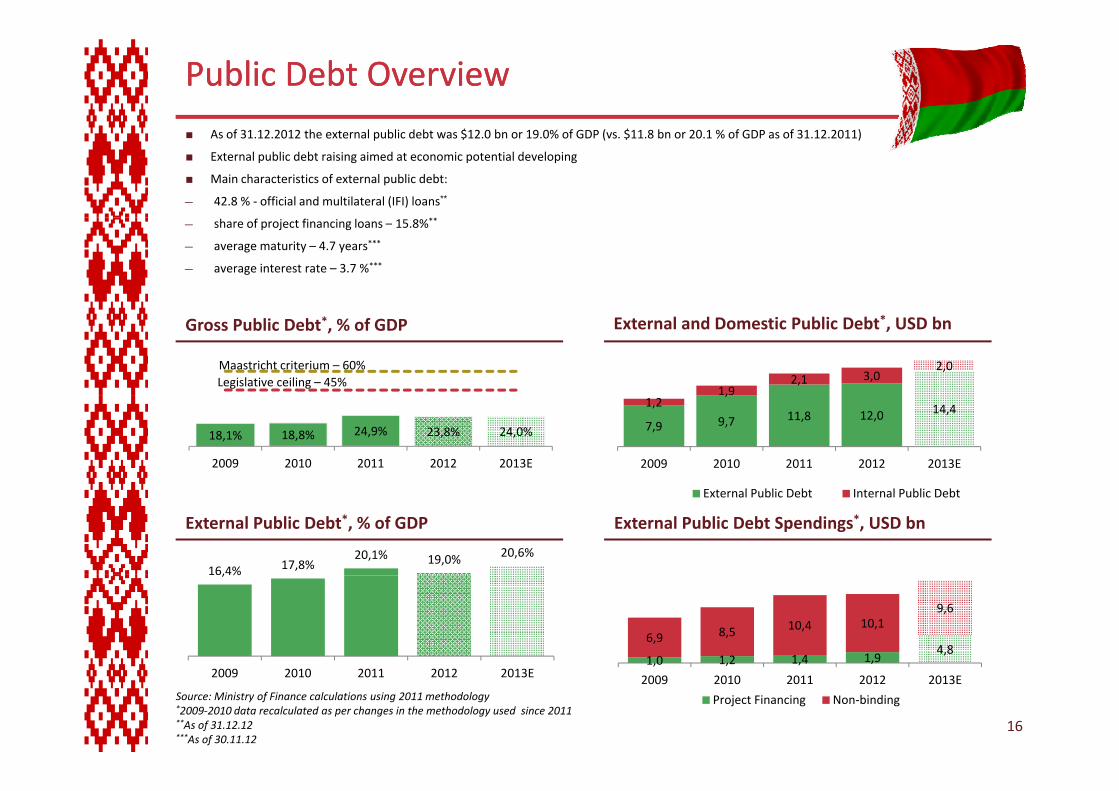

Public Public DebtDebt OverviewOverviewAs of 31.12.2012 the external public debt was $12.0 bn or 19.0% of GDP (vs. $11.8 bn or 20.1 % of GDP as of 31.12.2011)

External public debt raising aimed at economic potential developing

Main characteristics of external public debt:

— 42.8 % ‐ official and multilateral (IFI) loans**

— share of project financing loans – 15.8%**

— average maturity – 4.7 years***

— average interest rate – 3.7 %***

Gross Public Debt*, % of GDP

Legislative ceiling – 45%Maastricht criterium – 60%

External and Domestic Public Debt*, USD bn

1,92,1 3,0

2,0

18,1% 18,8% 24,9% 23,8% 24,0%

2009 2010 2011 2012 2013E

7,9 9,7 11,8 12,0 14,41,2,

2009 2010 2011 2012 2013E

External Public Debt*, % of GDP

External Public Debt Internal Public Debt

External Public Debt Spendings*, USD bn

16,4% 17,8%20,1% 19,0% 20,6%

, %

1,0 1,2 1,4 1,94,8

6,9 8,5 10,4 10,19,6

2009 2010 2011 2012 2013E

Source: Ministry of Finance calculations using 2011 methodology *2009‐2010 data recalculated as per changes in the methodology used since 2011**As of 31.12.12***As of 30.11.12

, , ,

2009 2010 2011 2012 2013E

Project Financing Non‐binding

16

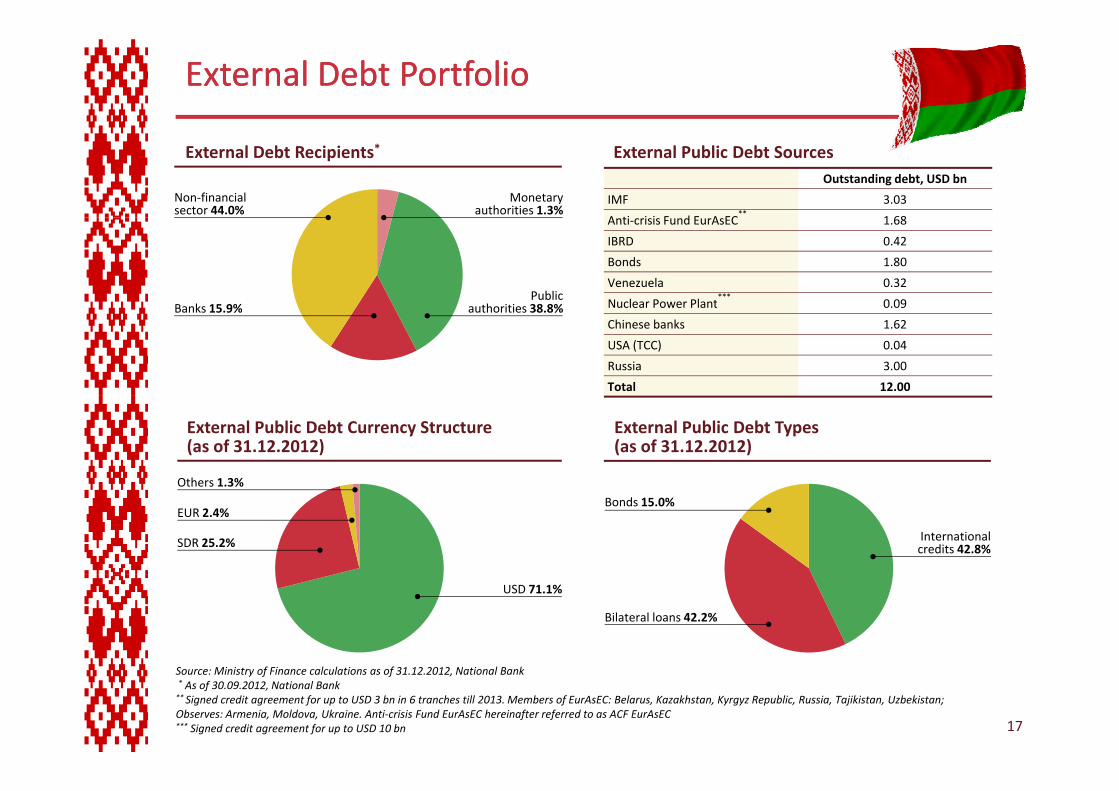

External Debt External Debt PortfolioPortfolio

Outstanding debt, USD bn

IMF 3.03

A i i i d A C**

1 68

External Public Debt SourcesExternal Debt Recipients*

Monetary authorities 1.3%

Non‐financial sector 44.0%

Anti‐crisis Fund EurAsEC 1.68

IBRD 0.42

Bonds 1.80

Venezuela 0.32

Nuclear Power Plant***

0 09Public

th iti 38 8%B k 15 9% Nuclear Power Plant 0.09

Chinese banks 1.62

USA (TCC) 0.04

Russia 3.00

Total 12.00

authorities 38.8%Banks 15.9%

External Public Debt Currency Structure (as of 31.12.2012)

External Public Debt Types (as of 31.12.2012)

Others 1.3%Others 1.3%

SDR 25.2%

EUR 2.4%

International credits 42.8%

Bonds 15.0%

USD 71.1%

Bilateral loans 42.2%

Source: Ministry of Finance calculations as of 31.12.2012, National Bank* As of 30.09.2012, National Bank** Signed credit agreement for up to USD 3 bn in 6 tranches till 2013. Members of EurAsEC: Belarus, Kazakhstan, Kyrgyz Republic, Russia, Tajikistan, Uzbekistan; Observes: Armenia, Moldova, Ukraine. Anti‐crisis Fund EurAsEC hereinafter referred to as ACF EurAsEC*** Signed credit agreement for up to USD 10 bn 17