BEECHWOOD INDEPENDENT SCHOOL DISTRICT have audited the accompanying financial statements of the...

61

BEECHWOOD INDEPENDENT SCHOOL DISTRICT June 30, 2016 FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS’ REPORT INCLUDING SUPPLEMENTARY INFORMATION

Transcript of BEECHWOOD INDEPENDENT SCHOOL DISTRICT have audited the accompanying financial statements of the...

BEECHWOOD INDEPENDENT SCHOOL DISTRICT June 30, 2016 FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS’ REPORT INCLUDING SUPPLEMENTARY INFORMATION

BEECHWOOD INDEPENDENT SCHOOL DISTRICT TABLE OF CONTENTS

PAGE Independent Auditors' Report Management’s Discussion and Analysis (MD&A) ............................................................................. 1 Basic Financial Statements District-Wide Financial Statements Statement of Net Position .................................................................................................... 6 Statement of Activities .......................................................................................................... 7 Fund Financial Statements Balance Sheet – Governmental Funds ................................................................................ 8 Reconciliation of the Balance Sheet – Governmental Funds to the Statement of Net Position .................................................... 9 Statement of Revenues, Expenditures and Changes in Fund Balance – Governmental Funds ....................................................................................................... 10 Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balance – Governmental Funds to the Statement of Activities ..................................................................................................... 11 Statement of Net Position – Proprietary Funds .................................................................. 12 Statement of Revenues, Expenses and Changes in Net Position – Proprietary Funds ............................................................................................................ 13 Statement of Cash Flows – Proprietary Funds ................................................................... 14 Statement of Fiduciary Net Position – Fiduciary Funds ...................................................... 15 Notes to the Financial Statements ............................................................................................. 16

BEECHWOOD INDEPENDENT SCHOOL DISTRICT TABLE OF CONTENTS

(Continued) PAGE

Required Supplementary Information Statement of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual – General Fund ..................................................................................... 38 Statement of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual – Debt Service Fund ............................................................................. 39 Statement of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual – Construction Fund ............................................................................. 40 Schedule of the District’s Proportionate Share of the Net Pension Liability .............................. 41 Schedule of the District’s Contributions ..................................................................................... 42 Other Supplementary Information Combining Balance Sheet – Non-Major Governmental Funds ................................................. 43 Combining Statement of Revenues, Expenditures and Changes in Fund Balance – Non-Major Governmental Funds ........................................... 44 Statement of Receipts, Disbursements and Fund Balance Beechwood Independent Board of Education – School Activity Fund ........................................................................................................................ 45 Independent Auditors’ Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards ......................................................... 46

Management Letter Comments ................................................................................................. 48

INDEPENDENT AUDITORS' REPORT Kentucky State Committee for School District Audits and Members of the Board of Education Beechwood Independent School District Fort Mitchell, Kentucky Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Beechwood Independent School District (the District) as of and for the year ended June 30, 2016, and the related notes to the financial statements, which collectively comprise the District’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States of America, Audits of States, Local Governments, and Non-Profit Organizations, and the audit requirements prescribed by the Kentucky State Committee for School District Audits in the Independent Auditor’s Contract – General Audit Requirements, State Compliance Requirements, Appendix I to the Independent Auditor’s Contract – Audit Extension Request and Appendix II to the Independent Auditor’s Contract – Instructions for Submission of the Audit Report, Audit Acceptance Statement, AFR and Balance Sheet, Statement of Certification, and Audit Report. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

Kentucky State Committee for School District Audits and Members of the Board of Education Beechwood Independent School District

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Beechwood Independent School District as of June 30, 2016, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter As discussed in the Note 14 to the financial statements, the previously issued financial statements for the year ended June 30, 2015 have been restated for the correction of a material misstatement. Our opinion is not modified with respect to that matter. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 1 - 5, budgetary comparison information on pages 41 – 43, and the pension schedules on pages 44 - 45 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Beechwood Independent School District’s basic financial statements. The combining and individual nonmajor fund financial statements and other supplementary information are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual nonmajor fund financial statements and other supplementary information are the responsibility of management and were derived from, and relate directly to, the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual nonmajor fund financial statements and other supplementary information are fairly stated, in all material respects, in relation to the basic financial statements as a whole.

Kentucky State Committee for School District Audits and Members of the Board of Education Beechwood Independent School District

Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report, dated November 1, 2016, on our consideration of the Beechwood Independent School District’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Beechwood Independent School District’s internal control over financial reporting and compliance.

VonLehman & Company Inc.

Fort Mitchell, Kentucky November 1, 2016 (except for Note 14, as to which the date is February 23, 2017)

1

BEECHWOOD INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (MD&A)

FOR THE FISCAL YEAR ENDED JUNE 30, 2016 UNAUDITED

As management of the Beechwood Independent School District (the District), we offer readers of the District's financial statements this narrative overview and analysis of the financial activities of the District for the fiscal year ended June 30, 2016. We encourage readers to consider the information presented here in conjunction with additional information found within the body of the audit. Financial Highlights Beechwood Independent Schools served 1,338 enrolled students in a unique K-12 public school district located in Ft. Mitchell, Kentucky. Throughout history, Beechwood schools have been noted for their sense of tradition and academic excellence. The General Fund had $11,500,013 in revenue, which primarily consisted of local real estate and property taxes, the state program (SEEK), on-behalf payments, local out-of-district tuition, utilities tax and motor vehicle taxes. Excluding inter-fund transfers, there was $11,328,743 in General Fund expenditures. In September 2015, the auxiliary gymnasium and renovated school kitchen were completed. Construction began in April of 2016 to renovate the athletic fields, create a new high school office and upgrade the HVAC system. Overview of Financial Statements This discussion and analysis is intended to serve as an introduction to the District's basic financial statements. The District's basic financial statements comprise three components: 1) district-wide financial statements; 2) fund financial statements; and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. The district-wide financial statements are designed to provide readers with a broad overview of the District's finances in a manner similar to a private-sector business. The statement of net position presents information on all of the District's assets and liabilities, with the difference between the two reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the District is improving or deteriorating. The statement of activities presents information showing how the District's net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods. The district-wide financial statements outline functions of the District that are principally supported by property taxes and intergovernmental revenues (governmental activities). The governmental activities of the District include instruction, support services, operation and maintenance of plant, student transportation and operation of non-instructional services. Fixed assets and related debt are also supported by taxes and intergovernmental revenues. The district-wide financial statements can be found on pages 6 and 7 of this report.

2

BEECHWOOD INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (MD&A)

FOR THE FISCAL YEAR ENDED JUNE 30, 2016 UNAUDITED (Continued)

Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. This is a state mandated uniform system and chart of accounts for all Kentucky public school districts utilizing the MUNIS administrative software. The District uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the District can be divided into three categories: governmental funds, proprietary funds and fiduciary funds. Fiduciary funds are trust funds established by benefactors to aid in student education, welfare and teacher support. The proprietary funds of the District include its food service operations. All other activities of the District are included in the governmental funds. The basic governmental fund financial statements can be found on pages 8 through 11 of this report. Notes to the financial statements. The notes to the financial statements provide additional information that is essential to a full understanding of the data provided in the district-wide and fund financial statements. The notes to the financial statements can be found on pages 16 through 40 of this report. District-Wide Financial Analysis Net position may serve over time as a useful indicator of a government's financial position. In the case of the District, assets and deferred outflows exceeded liabilities and deferred inflows by approximately $7.3 million as of June 30, 2016. A large portion of the District's net position reflects its investment in capital assets (e.g., land and improvements, buildings and improvements, vehicles, furniture and equipment and construction in progress) less any related debt used to acquire those assets that are still outstanding. The District uses these capital assets to provide services to its students; consequently, these assets are not available for future spending. Although the District's investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. The District's financial position is the product of several financial transactions including the net results of activities, the acquisition and payment of debt, the acquisition and disposal of capital assets and the depreciation of capital assets. The table on the following page provides a summary of the District’s net position for 2016 compared to 2015 (2015 does not include the effect of the prior period adjustment).

3

BEECHWOOD INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (MD&A)

FOR THE FISCAL YEAR ENDED JUNE 30, 2016 UNAUDITED (Continued)

Net Position for the Periods Ending June 30, 2016 and 2015

2016 2015

Current Assets $ 7,841,399 $ 8,376,380 Noncurrent Assets 27,376,900 22,996,373

Total Assets 35,218,299 31,372,753

Deferred Outflows of Resources 424,924 495,727

Total Assets and Deferred Outflows of Resources 35,643,223 31,868,480

Current Liabilities 3,128,388 1,279,697 Noncurrent Liabilities 25,146,431 23,312,967

Total Liabilities 28,274,819 24,592,664

Deferred Inflows of Resources 111,000 148,000

Total Liabilities and Deferred Inflows of Resources 28,385,819 24,740,664

Investment in Capital Assets (Net of Related Debt) 3,365,379 1,310,028 Restricted 3,153,359 4,128,299 Unrestricted 738,666 1,689,489

Total Net Position $ 7,257,404 $ 7,127,816

June 30,

Comments on Budget Comparisons

• The District's total general fund revenues for the fiscal year ended June 30, 2016, excluding inter-fund transfers, were $11,500,013.

• General Fund budget compared to actual revenue varied slightly from line item to line item with the ending actual balance being $383,150 in excess of budget, or approximately 3.4%. This is partially a result of the District recording more "on behalf" payments made by the state than expected.

• The total cost of all programs and services, excluding inter-fund transfers, in the General Fund, was $11,328,743.

• General fund actual expenditures were less than budgeted expenditures by $1,838,120. This is mainly a result of the District not spending as much in student transportation as expected as well as not using the contingency.

• The District recorded On-Behalf payments as revenues and expenditures during the fiscal year. The On-Behalf revenues and expenditures were included in the budget.

4

BEECHWOOD INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (MD&A)

FOR THE FISCAL YEAR ENDED JUNE 30, 2016 UNAUDITED (Continued)

The following table presents a summary of revenue and expense for the fiscal years ended June 30, 2016 and 2015 (2015 does not include the effect of the prior period adjustment):

2016 2015Revenues

Program RevenuesCharges for Services $ 705,520 $ 686,058 Operating Grants and Contributions 1,375,327 1,266,192 Capital Grants and Contributions 491,789 542,016

Total Program Revenues 2,572,636 2,494,266

General RevenuesTaxes 5,588,830 5,572,284 Federal and State Aid not Restricted to Specific Purposes 6,120,596 7,478,198 Investment Earnings 45,444 29,299 Miscellaneous 192,376 209,335

Total General Revenues 11,947,246 13,289,116

Total Revenues 14,519,882 15,783,382

ExpensesInstructional 8,134,740 7,626,170 Student Support Services 550,590 592,371 Instructional Staff Support Services 464,416 518,343 District Administration 491,764 477,257 School Administration 663,456 727,250 Business Support Services 570,784 602,068 Plant Operation and Maintenance 1,186,951 1,332,482 Student Transportation 90,810 126,180 Food Service Operations 391,049 401,196 Depreciation Expense 687,021 622,526 Pension Expense 320,583 151,590 Interest on Long-Term Debt 790,239 777,060

Total Expenses 14,342,403 13,954,493

Change in Net Position $ 177,479 $ 1,828,889

June 30,

5

BEECHWOOD INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (MD&A)

FOR THE FISCAL YEAR ENDED JUNE 30, 2016 UNAUDITED (Continued)

Capital Assets At the end of fiscal year 2016, the District had a total of approximately $27.4 million in capital assets net of accumulated depreciation, including approximately $26.5 million for governmental activities and approximately $877,000 for business type activities. Current year capital asset additions totaled approximately $5.0 million. Debt At June 30, 2016, the District had approximately $24.0 million in outstanding bonds. There was one new bond issuance in May, 2016 for $3,240,000. Budgetary Implications In Kentucky, the public school fiscal year is July 1-June 30; other programs, i.e. some federal, operate on a different fiscal calendar, but are reflected in the District’s overall budget. By law, the budget must have a minimum 2% contingency. The Board adopted a budget for 2016-2017 with $2.2 million in contingency (16%). The beginning cash balance in the general fund for the fiscal year is $2,183,423. Significant Board action that impacts the finances include step increase for all classified employees and all certified employees, facility repairs, and equipment purchases. Contacting the District's Financial Management Questions regarding this report should be directed to the Superintendent, Dr. Mike Stacy (859) 331-3250 or to Rae Wise, Director of Financial Services (859) 331-3250 or by mail at 50 Beechwood Road, Ft. Mitchell, Kentucky, 41017.

DISTRICT-WIDE FINANCIAL STATEMENTS

See accompanying notes.

6

Business-Governmental Type

Activities Activities TotalAssets and Deferred Outflows of Resources Current Assets Cash and Cash Equivalents $ 6,061,830 $ 68,140 $ 6,129,970 Escrow Funds 1,344,221 - 1,344,221 Accounts Receivable 238,696 - 238,696 Inventories - 4,390 4,390 Prepaid Expenses 124,122 - 124,122

Total Current Assets 7,768,869 72,530 7,841,399

Noncurrent Assets Nondepreciable Capital Assets Land 769,584 - 769,584 Construction in Progress 1,784,802 - 1,784,802 Depreciable Capital Assets Land Improvements 1,346,257 - 1,346,257 Buildings and Improvements 28,360,767 497,211 28,857,978 Vehicles 420,252 - 420,252 Technology Equipment 437,472 - 437,472 General Equipment 378,401 651,367 1,029,768 Less Accumulated Depreciation (6,998,022) (271,191) (7,269,213)

Total Noncurrent Assets 26,499,513 877,387 27,376,900

Total Assets 34,268,382 949,917 35,218,299

Deferred Outflows of Resources Deferred Loss on Refunding, Net 64,594 - 64,594 Difference Between Expected and Actual Experience 13,154 1,756 14,910 Net Difference Between Projected and Actual Investment Earnings 14,189 1,894 16,083 Changes of Assumptions 159,618 21,307 180,925 Changes in Proportion and Difference Between Employer Contributions and Proportionate Share 17,002 2,270 19,272 Contributions After Measurement Date 113,933 15,207 129,140

Total Deferred Outflows of Resources 382,490 42,434 424,924

Total Assets and Deferred Outflows of Resources 34,650,872 992,351 35,643,223

Liabilities and Deferred Inflows of Resources Current Liabilities Current Portion of Bonds Payable 712,769 - 712,769 Current Portion of Accrued Sick Leave 30,111 - 30,111 Accounts Payable 1,017,230 40 1,017,270 Accrued Interest 63,734 - 63,734 Funds Received in Excess of Revenues Earned 1,304,504 - 1,304,504

Total Current Liabilities 3,128,348 40 3,128,388

Noncurrent Liabilities Noncurrent Portion of Accrued Sick Leave 53,487 - 53,487 Noncurrent Portion of Bonds Payable 23,298,752 - 23,298,752 Net Pension Liability 1,582,895 211,297 1,794,192

Total Noncurrent Liabilities 24,935,134 211,297 25,146,431

Total Liabilities 28,063,482 211,337 28,274,819

Deferred Inflows of Resources Net Difference Between Projected and Actual Investment Earnings 97,927 13,073 111,000

Total Liabilities and Deferred Inflows of Resources 28,161,409 224,410 28,385,819

Net Position Invested in Capital Assets, Net of Related Debt 2,487,992 877,387 3,365,379 Restricted for Debt Service Fund 76,981 - 76,981 Construction Fund 2,855,732 - 2,855,732 Special Revenue Fund 120,646 - 120,646 Unrestricted 948,112 (109,446) 838,666

Total Net Position $ 6,489,463 $ 767,941 $ 7,257,404

BEECHWOOD INDEPENDENT SCHOOL DISTRICTSTATEMENT OF NET POSITION

JUNE 30, 2016

See accompanying notes.

7

Operating Capital Business -Charges for Grants and Grants and Governmental Type

Function/Programs Expenses Services Contributions Contributions Activities Activities Total

Governmental Activities Instructional $ 8,134,740 $ 411,483 $ 1,220,869 $ 100,413 $ (6,401,975) $ - $ (6,401,975) Support Services Student 550,590 - - - (550,590) - (550,590) Instructional Staff 464,416 - - - (464,416) - (464,416) District Administration 491,764 - - - (491,764) - (491,764) School Administration 663,456 - - - (663,456) - (663,456) Business Support Services 570,784 - - - (570,784) - (570,784) Plant Operation and Maintenance 1,186,951 - - - (1,186,951) - (1,186,951) Student Transportation 90,810 10,993 - - (79,817) - (79,817) Depreciation Expense 631,304 - - - (631,304) - (631,304) Building Improvements - - - - - - - Pension Expense 282,828 - - - (282,828) - (282,828) Interest on Long-Term Debt 790,239 - - 391,376 (398,863) - (398,863)

Total Governmental Activities 13,857,882 422,476 1,220,869 491,789 (11,722,748) - (11,722,748)

Business-Type Activities Food Service Operations 391,049 283,044 154,458 - - 46,453 46,453 Depreciation Expense 55,717 - - - - (55,717) (55,717) Pension Expense 37,755 - - - - (37,755) (37,755)

Total Business-Type Activities 484,521 283,044 154,458 - - (47,019) (47,019)

Total School District $ 14,342,403 $ 705,520 $ 1,375,327 $ 491,789 $ (11,722,748) $ (47,019) $ (11,769,767)

General Revenues Taxes $ 5,588,830 $ - $ 5,588,830 Federal and State Aid not Restricted to Specific Purposes 6,120,596 - 6,120,596 Operating Transfers (Out) In (850,000) 850,000 - Investment Earnings 45,248 196 45,444 Miscellaneous 192,236 140 192,376

Total General Revenues 11,096,910 850,336 11,947,246

Change in Net Position (625,838) 803,317 177,479

Net Position July 1, 2015 (As Restated) 7,115,301 (35,376) 7,079,925

Net Position June 30, 2016 $ 6,489,463 $ 767,941 $ 7,257,404

BEECHWOOD INDEPENDENT SCHOOL DISTRICTSTATEMENT OF ACTIVITIESYEAR ENDED JUNE 30, 2016

and Changes in Net PositionNet (Expense) Revenue

Program Revenues

FUND FINANCIAL STATEMENTS

See accompanying notes.

8

Debt Other TotalGeneral Service Construction Governmental Governmental

Fund Fund Fund Funds FundsAssets Cash and Cash Equivalents $ 2,183,423 $ - $ 3,814,038 $ 64,369 $ 6,061,830 Escrow Funds - 1,344,221 - - 1,344,221 Accounts Receivable 59,665 - - 179,031 238,696 Due from (to) Other Funds 100,000 (100,000) - Prepaid Expenses 124,122 - - - 124,122

Total Assets $ 2,467,210 $ 1,344,221 $ 3,814,038 $ 143,400 $ 7,768,869

Liabilities Accounts Payable $ 58,874 $ - $ 958,306 $ 50 $ 1,017,230 Unearned Revenues 14,560 1,267,240 - 22,704 1,304,504

Total Liabilities 73,434 1,267,240 958,306 22,754 2,321,734

Fund Balances Nonspendable 124,122 - - - 124,122 Restricted Debt Service Fund - 76,981 - - 76,981 Construction Fund - - 2,855,732 - 2,855,732 Special Revenue Fund - - - 120,646 120,646 Committed Accumulated Sick Leave 48,052 - - - 48,052 Future Construction 200,000 - - - 200,000 Future Bus Acquisition 70,000 - - - 70,000 Unassigned 1,951,602 - - - 1,951,602

Total Fund Balances 2,393,776 76,981 2,855,732 120,646 5,447,135

Total Liabilities and Fund Balances $ 2,467,210 $ 1,344,221 $ 3,814,038 $ 143,400 $ 7,768,869

BEECHWOOD INDEPENDENT SCHOOL DISTRICTBALANCE SHEET

GOVERNMENTAL FUNDSJUNE 30, 2016

See accompanying notes.

9

Amounts reported for governmental activities in the statement of net position are different because:

Total Governmental Funds Balance $ 5,447,135

Capital assets used in governmental activities are not financial resources and; therefore, are not reported as assets in governmental funds. Cost of Capital Assets $ 33,497,535 Accumulated Depreciation (6,998,022)

26,499,513

Deferred loss on refunding, net is not a financial resource and therefore are not reported as assets in governmental funds 64,594

Deferred outflows and inflows of resources related to pensions are applicable to future periods and, therefore, are not reported in the funds:

Difference Between Expected and Actual Experience 13,154 Net Difference Between Projected and Actual Investment Earnings 14,189 Changes of Assumptions 159,618 Changes in Proportion and Difference Between Employer Contributions and Proportionate Share 17,002 Contributions After Measurement Date 113,933 Net Difference Between Projected and Actual Investment Earnings on Pension Plan Investments (97,927)

Long-term liabilities, including bonds payable, are not due and payable in the current period and; therefore, are not reported as liabilities in the funds. Long-term liabilities at year end consist of: Bonds Payable 24,185,000 Bond Premiums 5,274 Bond Discounts (178,753) Accrued Interest on Bonds 63,734 Accumulated Sick Leave 83,598 Net Pension Liability 1,582,895

(25,741,748)

Total Net Position - Governmental Activities $ 6,489,463

BEECHWOOD INDEPENDENT SCHOOL DISTRICTRECONCILIATION OF THE BALANCE SHEET - GOVERNMENTAL FUNDS TO

THE STATEMENT OF NET POSITIONJUNE 30, 2016

See accompanying notes.

10

Debt Other TotalGeneral Service Construction Governmental Governmental

Fund Fund Fund Funds FundsRevenues Taxes $ 4,952,436 $ - $ - $ 636,394 $ 5,588,830 Tuition and Fees 411,483 - - - 411,483 Earnings on Investments 12,578 32,437 184 49 45,248 State Sources 6,051,528 174,979 - 796,349 7,022,856 Federal Sources - 392,466 - 409,326 801,792 Other Sources 71,988 - 2,884 136,963 211,835

Total Revenues 11,500,013 599,882 3,068 1,979,081 14,082,044

Expenditures Instructional 7,223,759 - - 894,561 8,118,320 Support Services Student 549,980 - - 610 550,590 Instructional Staff 448,534 - - 18,022 466,556 District Administration 495,633 - - - 495,633 School Administration 678,361 - - - 678,361 Business 591,561 - - - 591,561 Plant Operation and Maintenance 1,246,849 - - - 1,246,849 Student Transportation 94,066 - - - 94,066 Building Improvements - - 4,184,949 - 4,184,949 Debt Service Principal - 680,000 - - 680,000 Interest - 781,025 - - 781,025

Total Expenditures 11,328,743 1,461,025 4,184,949 913,193 17,887,910

Excess (Deficit) of Revenues Over Expenditures 171,270 (861,143) (4,181,881) 1,065,888 (3,805,866)

Other Financing Sources (Uses) Proceeds from Bond Issuance - - 3,240,000 - 3,240,000 Bond Issuance Costs - - (32,393) - (32,393) Operating Transfers In - 893,580 1,432,882 77,304 2,403,766 Operating Transfers Out (152,304) - (1,143,227) (1,958,235) (3,253,766)

Total Other Financing (Uses) Sources (152,304) 893,580 3,497,262 (1,880,931) 2,357,607

Net Change in Fund Balance 18,966 32,437 (684,619) (815,043) (1,448,259)

Fund Balance July 1, 2015, As Restated 2,374,810 44,544 3,540,351 935,689 6,895,394

Fund Balance June 30, 2016 $ 2,393,776 $ 76,981 $ 2,855,732 $ 120,646 $ 5,447,135

BEECHWOOD INDEPENDENT SCHOOL DISTRICTSTATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE

GOVERNMENTAL FUNDSYEAR ENDED JUNE 30, 2016

See accompanying notes.

11

Net Changes in Total Fund Balances Per Fund Financial Statements $ (1,448,259)

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures because they usecurrent financial resources. However, in the statement of activities, the costof those assets is allocated over their estimated useful lives and reported asdepreciation expense. This is the amount by which capital outlays exceeddepreciation expense for the year.

Depreciation Expense $ (631,304) Capital Outlays 4,216,849

3,585,545

The proceeds from bonds provide current financial resources and are reported inthe fund financial statements but they are presented as liabilities in the statementof net position. (3,240,000)

Deferred losses on refunding are reported in the governmental funds as an otherfinancing source. However, for governmental activities those items are show in the statement of net position and allocated over the term of the bond in the statementof activities. This is the amount of current year amortization of the deferred losses. (5,365)

Premiums on bonds are reported in the governmental funds as an other financingsource. However, for governmental activities those items are shown in thestatement of net position and allocated over the term of the bond in the statement

of activities. This is the amount of premium received net of current year amortization. (5,274)

Discounts on bonds are reported in the governmental funds as an other financingsource. However, for governmental activities those items are shown in thestatement of net position and allocated over the term of the bond in the statementof activities. This is the amount of current year amortization of the discount. (12,497)

Repayment of bond principal is an expenditure in the governmental funds but, itreduces long-term liabilities in the statement of net position and does not affectthe statement of activities. 680,000

In the statement of activities, compensated absences (sick leave) are measuredby the amounts earned during the year. In the governmental funds, however,expenditures for these amounts are measured by the amount of financialresources used (essentially, the amounts actually paid.) The difference in expensesreported in the statement of activities is as a result of the change in accumulatedsick leave. (57,406)

Governmental funds report District pension contributions as expenditures. However,in the statement of activities, the cost of pension benefits earned net of employeecontributions is reported as pension expense.

District Pension Contributions - June 30, 2015 (109,909) District Pension Contributions - June 30, 2016 113,932 Amortization of Deferred Outflows and Inflows of Resources 32,643 Cost of Benefits Earned Net of Employee Contributions (205,564)

(168,898)

Interest on long-term debt in the statement of activities differs from the amountreported in the governmental funds because interest is recorded as an expenditurein the funds when it is due and thus requires the use of current financial resources.In the statement of activities, however, interest expense is recognized as theinterest accrues, regardless of when it is due. The difference in interest expensereported in the statement of activities is as a result of (1) the change in accruedinterest on bonds and (2) refunding losses and gains not expended within the fund statements. 46,316

Change in Net Position of Governmental Activities $ (625,838)

BEECHWOOD INDEPENDENT SCHOOL DISTRICTRECONCILIATION OF THE STATEMENT OF REVENUES,EXPENDITURES AND CHANGES IN FUND BALANCES

GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIESYEAR ENDED JUNE 30, 2016

See accompanying notes.

12

FoodServiceFund

Assets and Deferred Outflows of Resources Current Assets Cash and Cash Equivalents $ 68,140 Inventories for Consumption 4,390

Total Current Assets 72,530

Noncurrent Assets Buildings and Improvements 497,211 Furniture and Equipment 651,367 Less Accumulated Depreciation (271,191)

Total Noncurrent Assets 877,387

Total Assets 949,917

Deferred Outflows of Resources Difference Between Expected and Actual Experience 1,756 Net Difference Between Projected and Actual Investment Earnings 1,894 Changes of Assumptions 21,307 Changes in Proportion and Difference Between Employer Contributions and Proportionate Share 2,270 Contributions After Measurement Date 15,207

Total Deferred Outflows of Resources 42,434

Total Assets and Deferred Outflows of Resources $ 992,351

Liabilities and Deferred Inflows of Resources Current Liabilities Accounts Payable $ 40

Noncurrent Liabilities Net Pension Liability 211,297

Total Liabilities 211,337

Deferred Inflows of Resources Net Difference Between Projected and Actual Investment Earnings 13,073

Total Liabilities and Deferred Inflows of Resources 224,410

Net Position Invested in Capital Assets, Net of Debt 877,387 Unrestricted (109,446)

Total Net Position 767,941

Total Liabilities, Deferred Inflows of Resources and Net Position $ 992,351

BEECHWOOD INDEPENDENT SCHOOL DISTRICTSTATEMENT OF NET POSITION

PROPRIETARY FUNDSJUNE 30, 2016

See accompanying notes.

13

FoodServiceFund

Operating Revenues Lunchroom Sales $ 283,044 Miscellaneous 140

Total Operating Revenues 283,184 Operating Expenses Salaries and Benefits 184,488 Contract Services 2,412 Materials and Supplies 204,149 Depreciation 55,717 Pension Expense 37,755

Total Operating Expenses 484,521

Loss Before Non-Operating Revenues (201,337) Non-Operating Revenues Federal Grants 111,646 State Grants 26,353 Donated Commodities and Other Donations 16,459 Interest Income 196

Total Non-Operating Revenues 154,654

Loss Before Other Financing Sources (46,683)

Other Financing Sources Operating Transfers In 850,000

Change in Net Position 803,317

Net Position July 1, 2015 (As Restated) (35,376)

Net Position June 30, 2016 $ 767,941

BEECHWOOD INDEPENDENT SCHOOL DISTRICTSTATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET POSITION

PROPRIETARY FUNDSYEAR ENDED JUNE 30, 2016

See accompanying notes.

14

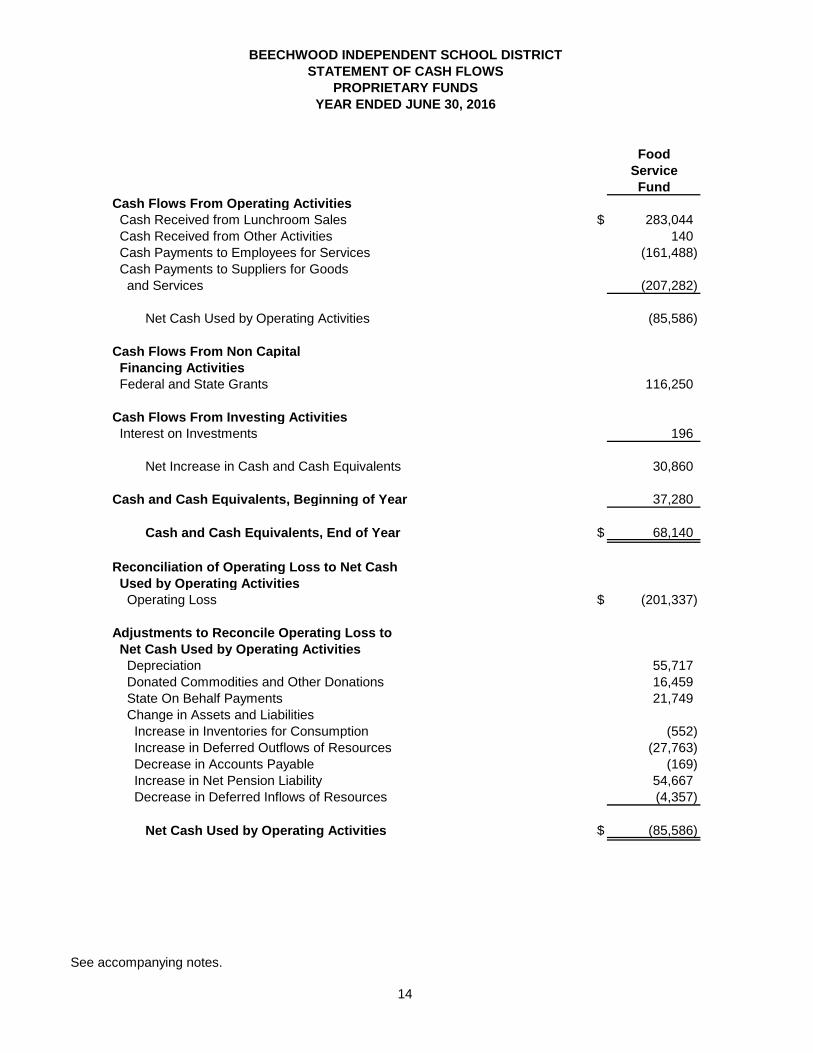

FoodServiceFund

Cash Flows From Operating Activities Cash Received from Lunchroom Sales $ 283,044 Cash Received from Other Activities 140 Cash Payments to Employees for Services (161,488) Cash Payments to Suppliers for Goods and Services (207,282)

Net Cash Used by Operating Activities (85,586)

Cash Flows From Non Capital Financing Activities Federal and State Grants 116,250

Cash Flows From Investing Activities Interest on Investments 196

Net Increase in Cash and Cash Equivalents 30,860 Cash and Cash Equivalents, Beginning of Year 37,280

Cash and Cash Equivalents, End of Year $ 68,140

Reconciliation of Operating Loss to Net Cash Used by Operating Activities Operating Loss $ (201,337)

Adjustments to Reconcile Operating Loss to Net Cash Used by Operating Activities Depreciation 55,717 Donated Commodities and Other Donations 16,459 State On Behalf Payments 21,749 Change in Assets and Liabilities Increase in Inventories for Consumption (552) Increase in Deferred Outflows of Resources (27,763) Decrease in Accounts Payable (169) Increase in Net Pension Liability 54,667 Decrease in Deferred Inflows of Resources (4,357)

Net Cash Used by Operating Activities $ (85,586)

BEECHWOOD INDEPENDENT SCHOOL DISTRICTSTATEMENT OF CASH FLOWS

PROPRIETARY FUNDSYEAR ENDED JUNE 30, 2016

See accompanying notes.

15

SchoolActivityFunds

Assets Cash and Cash Equivalents $ 244,512

LiabilitiesDue to Student Groups $ 244,512

JUNE 30, 2016FIDUCIARY FUNDS

STATEMENT OF FIDUCIARY NET POSITIONBEECHWOOD INDEPENDENT SCHOOL DISTRICT

16

BEECHWOOD INDEPENDENT SCHOOL DISTRICT NOTES TO THE FINANCIAL STATEMENTS

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reporting Entity The Beechwood Independent Board of Education (the Board), a five member group, is the level of government which has oversight responsibilities over all activities related to public elementary and secondary school education within the jurisdiction of the Beechwood Independent School District (the District). The District receives funding from local, state and federal government sources and must comply with the commitment requirements of these funding source entities. However, the District is not included in any other governmental "reporting entity" as defined in Section 2100, Codification of Governmental Accounting and Financial Reporting Standards. Board members are elected by the public and have decision making authority, the power to designate management, the responsibility to develop policies which may influence operations, and primary accountability for fiscal matters. The Board, for financial purposes, includes all of the funds and account groups relevant to the operation of the Beechwood Independent School District. The financial statements presented herein do not include funds of groups and organizations which, although associated with the school system, have not originated within the Board itself such as Band Boosters, Parent-Teacher Associations, etc. The financial statements of the District include those of separately administered organizations that are controlled by, or dependent on the Board. Control or dependence is determined on the basis of budget adoption, funding and appointment of the respective governing board. Based on the foregoing criteria, the financial statements of the following organization are included in the accompanying financial statements:

Beechwood Independent School Board Finance Corporation – In 1990 the Board resolved to authorize the establishment of the Beechwood Independent School Board Finance Corporation (a non-profit, non-stock, public and charitable corporation organized under the School Bond Act and KRS 273 and KRS 58.180) (the “Corporation”) as an agency of the Board for financing the costs of school building facilities. The members of the Board also comprise the Corporation’s Board of Directors.

Basis of Presentation District-Wide Financial Statements - The statement of net position and the statement of activities display information about the District as a whole. These statements include the financial activities of the primary government, except for fiduciary funds. The statements distinguish between those activities of the District that are governmental and those that are considered business-type activities. The district-wide statements are prepared using the economic resources measurement focus. This is the same approach used in the preparation of the proprietary fund financial statements, but differs from the manner in which governmental fund financial statements are prepared. Governmental fund financial statements; therefore, include reconciliations with brief explanations to better identify the relationship between the district-wide statements and the statements for governmental funds.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

17

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) The district-wide statement of activities presents a comparison between direct expenses and program revenues for each segment of the business-type activities of the District and for each function, or program of the District's governmental activities. Direct expenses are those that are specifically associated with a service, program or department and are; therefore, clearly identifiable to a particular function. Program revenues include charges paid by the recipient of the goods or services offered by the program and grants, and contributions that are restricted to meeting the operational or capital requirements of a particular program. Revenues that are not classified as program revenues are presented as general revenues of the District, with certain limited exceptions. The comparison of direct expenses with program revenues identifies the extent to which each business segment or governmental function is self-financing, or draws from the general revenues of the District. Fund Financial Statements - Fund financial statements report detailed information about the District. The focus of governmental and enterprise fund financial statements is on major funds rather than reporting funds by type. Each major fund is presented in a separate column. Non-major funds are aggregated and presented in a single column. Fiduciary funds are reported by fund type. The accounting and reporting treatment applied to a fund is determined by its measurement focus. All governmental fund types are accounted for using a flow of current financial resources measurement focus. The financial statements for governmental funds are a balance sheet, which generally includes only current assets and current liabilities, and a statement of revenues, expenditures and changes in fund balance, which reports on the changes in net total assets. Proprietary funds and fiduciary funds are reported using the economic resources measurement focus. The District has the following funds: I. Governmental Fund Types

(A) The General Fund is the primary operating fund of the District. It accounts for financial

resources used for general types of operations. This is a budgeted fund and any unrestricted fund balances are considered as resources available for use. This is a major fund of the District.

(B) The Debt Service Fund is used to account for the accumulation of resources for, and the payment of, general long-term debt principal and interest and related cost; and, for the payment of interest on general obligation notes payable, as required by Kentucky law. This is a major fund of the District.

(C) The Construction Fund accounts for proceeds from sales of bonds and other revenues to

be used for authorized construction. This is a major fund of the District.

(D) The Special Revenue Fund accounts for proceeds of specific revenue sources (other than expendable trusts or major capital projects) that are legally restricted to disbursements for specified purposes. It includes federal financial programs where unused balances are returned to the grantor at the close of specified project periods, as well as the state grant programs. Project accounting is employed to maintain integrity for the various sources of funds. This is not a major fund of the District.

(E) The Capital Outlay Fund is used to account for financial resources to be used for the acquisition of capital assets. This is not a major fund of the District.

(F) The Building Fund is used to account for financial resources to be used for the acquisition

or construction of major capital facilities and equipment. This is not a major fund of the District.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

18

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

II. Proprietary Fund Types (Enterprise Funds)

(A) The School Food Service Fund is used to account for school food service activities, including the National School Lunch Program, which is conducted in cooperation with the U.S. Department of Agriculture (USDA). Amounts have been recorded for in-kind contribution of commodities from the USDA. The Food Service Fund is a major fund of the District.

III. Fiduciary Fund Type (Agency Funds)

(A) The Activity Funds account for activities of student groups and other types of activities

requiring clearing accounts. These funds are accounted for in accordance with the Uniform Program of Accounting for School Activity Funds.

Basis of Accounting The basis of accounting determines when transactions are recorded in the financial records and reported on the financial statements. District-wide financial statements are prepared using the accrual basis of accounting. Governmental Funds use the modified accrual basis of accounting. Proprietary and Fiduciary Funds also use the accrual basis of accounting. Revenues Exchange and Non-Exchange Transactions - Revenues resulting from exchange transactions, in which each party receives essentially equal value, is recorded on the accrual basis when the exchange takes place. On a modified accrual basis, revenues are recorded in the fiscal year in which the resources are measurable and available. Available means that the resources will be collected within the current fiscal year, or are expected to be collected soon enough thereafter to be used to pay liabilities of the current fiscal year. For the District, available means expected to be received within sixty days of the fiscal year end. Non-exchange transactions, in which the District receives value without directly giving equal value in return, include property taxes, grants, entitlements and donations. On an accrual basis, revenue from property taxes is recognized in the fiscal year for which the taxes are levied. Revenue from grants, entitlements and donations is recognized in the fiscal year in which all eligibility requirements have been satisfied. Eligibility requirements include timing requirements, which specify the year when the resources are required to be used or the fiscal year when use is first permitted, matching requirements, in which the District must provide local resources to be used for a specified purpose, and expenditure requirements, in which the resources are provided to the District on a reimbursement basis. On a modified accrual basis, revenues from non-exchange transactions must also be available before they can be recognized. Funds Received in Excess of Revenues Earned - Funds received exceeds revenues earned when assets are recognized before revenue recognition criteria have been satisfied. Grants and entitlements received before the eligibility requirements are met are recorded as deferred revenue. Restricted and Unrestricted Resources – When both restricted and unrestricted resources are available for use, it is the District’s policy to use restricted resources first, then unrestricted resources as needed. Expenses/Expenditures - On the accrual basis of accounting, expenses are recognized at the time they are incurred. The fair value of donated commodities used during the year is reported as an expense with a like amount reported as donated commodities revenue.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

19

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) The measurement focus of governmental fund accounting is on decreases in net financial resources (expenditures) rather than expenses. Expenditures are generally recognized in the accounting period in which the related fund liability is incurred, if measurable. Allocations of cost, such as depreciation, are not recognized in Governmental Funds. Taxes Property Tax Revenues - Property taxes are levied each September on the assessed value listed as of the prior January 1, for all real and personal property in the District. The billings are considered due upon receipt by the taxpayer; however, the actual date is based on a period ending 30 days after the tax bill mailing. Property taxes collected are recorded as revenues in the fiscal year for which they were levied. All taxes collected are initially deposited into the General Fund and then transferred to the appropriate fund. Budgetary Process The District’s budget is prepared according to Kentucky law and is based on accounting for certain transactions on a basis of cash receipts, disbursements, and encumbrances. In Kentucky, the public school fiscal year is July 1 through June 30. Some programs relating to federal and state grants operate on a different fiscal year but are nevertheless reflected in the overall budget. Cash and Cash Equivalents The District considers demand deposits, money market funds, and other investments with an original maturity of 90 days or less, to be cash equivalents. Inventories Supplies and materials are charged to expenditures when purchased, except for inventories in the Proprietary Fund, which are capitalized at the lower of cost or market. Capital Assets General capital assets are those assets not specifically related to activities reported in the Proprietary Funds. These assets generally result from expenditures in the Governmental Funds. These assets are reported in the governmental activities column of the district-wide statement of net position, but are not reported in the Fund financial statements. Capital assets utilized by the Proprietary Funds are reported both in the business-type activities column of the district-wide statement of net position and in the respective funds. All capital assets are capitalized at cost (or estimated historical cost) and updated for additions and retirements during the year. Donated fixed assets are recorded at their fair market values as of the date received. The District maintains a capitalization threshold of $1,000 for food services equipment, $5,000 for technology equipment and general equipment, and $10,000 for land and building improvements. Improvements are capitalized; the cost of normal maintenance and repairs that do not add to the value of the asset or materially extend an asset's life are not.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

20

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) All reported capital assets are depreciated. Improvements are depreciated over the remaining useful lives of the related capital assets. Depreciation is computed using the straight-line method over the following useful lives for both general capital assets and proprietary fund assets: Buildings and Improvements 25 - 50 Years Land Improvements 20 Years Technology Equipment 5 Years Vehicles 5 - 10 Years Food Service Equipment 10 - 12 Years General Equipment 15 Years Accumulated Unpaid Sick Leave Benefits Upon retirement from the school system, an employee will receive from the District, an amount equal to 30% of the value of accumulated sick leave. Sick leave benefits are accrued as a liability using the termination payment method. An accrual for earned sick leave is made to the extent that it is probable that the benefits will result in termination payments. The liability is based on the District's experience of making termination payments. The entire compensated absence liability is reported on the district-wide financial statements. lnterfund Balances On the Fund financial statements, receivables and payables resulting from short-term interfund loans are classified as "interfund receivables/payables". These amounts are eliminated in the governmental and business-type activities columns of the statement of net position, except for the net residual amounts due between governmental and business-type activities, which are presented as internal balances. Accrued Liabilities and Long-Term Obligations All payables, accrued liabilities and long-term obligations are reported in the district-wide financial statements, and all payables, accrued liabilities and long-term obligations payable from Proprietary Funds are reported on the proprietary fund financial statements. In general, payables and accrued liabilities that will be paid from Governmental Funds are reported on the governmental fund financial statements regardless of whether they will be liquidated with current resources. However, claims and judgments, accumulated sick leave, contractually required pension contributions and special termination benefits that will be paid from Governmental Funds are reported as a liability in the Fund financial statements, only to the extent that they will be paid with current, expendable, available financial resources. In general, payments made within sixty days after year end are considered to have been made with current available financial resources. Bonds and other long-term obligations that will be paid from Governmental Funds are not recognized as a liability in the Fund financial statements until due.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

21

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Fund Balance Reserves The following classifications describe the relative strength of the spending constraints placed on the purposes for which resources can be used: • Non-spendable fund balance - amounts that are not in a spendable form (such as inventory) or

are required to be maintained intact.

• Restricted fund balance - amounts constrained to specific purposes by their providers (such as grantors, bondholders and higher levels of government), through constitutional provisions, or by enabling legislation.

• Committed fund balance - amounts constrained to specific purposes by the District itself, using its

decision making authority; to be reported as committed, amounts cannot be used for any other purpose unless the District takes the action to remove or change the constraint.

• Assigned fund balance - amounts the District intends to use for specific purpose (such as

encumbrances); intent can be expressed by the District, or by an official or body, to which the District delegates the authority.

• Unassigned fund balance - amounts that are available for purpose; positive amounts are reported only in the General Fund.

It is the District's practice to liquidate funds when conditions have been met releasing these funds from legal, contractual, District or managerial obligations, using restricted funds first, followed by committed funds, assigned funds, then unassigned funds. Encumbrances Encumbrances are not liabilities and are not recorded as expenditures until receipt of material or service. Encumbrances remaining open at the end of the fiscal year are automatically re-budgeted in the following fiscal year. Encumbrances are considered a managerial assignment of fund balance in the governmental funds balance sheet. Pensions For purposes of measuring the net pension liability, deferred outflows of resources and deferred inflows of resources related to pensions, and pension expense, information about the fiduciary net position of the County Employees Retirement System (CERS) and additions to/deductions from CERS’ fiduciary net position have been determined on the same basis as they are reported by CERS. For this purpose, benefit payments (including refunds of employee contributions) are recognized when due and payable in accordance with the benefit terms. Investments are reported at fair value. Net Position Net position represents the difference between assets and liabilities. Net position invested in capital assets, net of related debt, consists of capital assets, net of accumulated depreciation, reduced by the outstanding balances of any borrowings used for the acquisition, construction or improvement of those assets. Net position is reported as restricted when there are limitations imposed on its use either through the enabling legislation adopted by the District, or through external restrictions imposed by creditors, grantors or laws or regulations of other governments.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

22

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Operating Revenues and Expenses Operating revenues are those revenues that are generated directly from the primary activity of the Proprietary Funds. For the District, those revenues are primarily charges for meals provided by the various schools. Expenses are primarily payroll, food costs, and supply purchases. lnterfund Activity

Exchange transactions between funds are reported as revenues in the seller funds, and as expenditures/expenses in the purchaser funds. Flows of cash, or goods from one fund to another without a requirement for repayment, are reported as interfund transfers. lnterfund transfers are reported as other financing sources/uses in Governmental Funds and as non-operating revenues/expenses in Proprietary Funds. Repayments from funds responsible for particular expenditures/expenses to the funds that initially paid for them are not presented on the financial statements. Use of Estimates The process of preparing financial statements in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP) requires the use of estimates and assumptions regarding certain types of assets, deferred outflows of resources, liabilities, deferred inflows of resources, revenues, and expenses. Certain estimates relate to unsettled transactions and events as of the date of the financial statements. Other estimates relate to assumptions about the ongoing operations and may impact future periods. Accordingly, upon settlement, actual results may differ from estimated amounts.

NOTE 2 - CASH AND CASH EQUIVALENTS

At year end, the District had on deposit, cash and cash equivalents totaling $9,256,630. Of the total cash balance, $250,000 was covered by the Federal Depository Insurance Corporation (FDIC), with the remainder that needs to be covered by a collateral agreement held by the pledging banks' trust departments in the District's name. Cash and cash equivalents at June 30, 2016, consist of the following:

June 30,2016

Bank Balance $ 7,912,409

Book Balance $ 6,374,482

Funds held in escrow for future debt payments were $1,344,221 and $994,974 for the years ended June 30, 2016 and 2015, respectively. Allocation per financial statements:

Governmental Funds $ 6,061,830 Proprietary Funds 68,140 Fiduciary Funds 244,512

$ 6,374,482

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

23

NOTE 2 - CASH AND CASH EQUIVALENTS (Continued) The District had the following non-cash transactions for the proprietary funds:

June 30,2016

Transfer of Capital Assets $ 850,000

Donated Commodities $ 16,459

On-Behalf Payments $ 21,749

NOTE 3 - CAPITAL ASSETS Capital asset activity for the fiscal year ended June 30, 2016 was as follows:

Beginning Additions / Deductions / EndingBalance Transfers Transfers Balance

Governmental Activities Land $ 769,584 $ - $ - $ 769,584 Construction In Progress 1,143,466 1,784,803 (1,143,467) 1,784,802 Land Improvements 1,362,057 - (15,800) 1,346,257 Buildings & Improvements 24,828,645 3,543,613 (11,491) 28,360,767 Technology Equipment 449,974 - (12,502) 437,472 Vehicles 420,252 - - 420,252 General Equipment 371,697 31,900 (25,196) 378,401

Total at Historical Cost 29,345,675 5,360,316 (1,208,456) 33,497,535

Less Accumulated Depreciation Land Improvements 942,549 29,969 (15,800) 956,718 Buildings & Improvements 4,463,207 545,519 (11,491) 4,997,235 Technology Equipment 424,692 11,404 (12,502) 423,594 Vehicles 336,505 22,184 - 358,689 General Equipment 264,754 22,228 (25,196) 261,786

Total Accumulated Depreciation 6,431,707 631,304 (64,989) 6,998,022

Governmental Activities Capital Assets, Net $ 22,913,968 $ 4,729,012 $ (1,143,467) $ 26,499,513

Business-Type Activities Buildings & Improvements $ 117,211 $ 380,000 $ - $ 497,211 General Equipment 202,629 470,000 (21,262) 651,367

Total at Historic Cost 319,840 850,000 (21,262) 1,148,578

Less Accumulated Depreciation Buildings & Improvements 103,866 15,031 - 118,897 General Equipment 132,870 40,686 (21,262) 152,294

Total Accumulated Depreciation 236,736 55,717 (21,262) 271,191

Business-Type Activities Capital Assets, Net $ 83,104 $ 794,283 $ - $ 877,387

Depreciation expense was not allocated to governmental functions. It appears on the statement of activities as unallocated.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

24

NOTE 4 - DEBT AND LEASE OBLIGATIONS The amount shown in the accompanying financial statements as bond obligations represents the District's future obligations to make payments relating to the bonds issued by the Beechwood Independent School District Finance Corporation. The following is a summary of the District’s long-term debt transactions for the year ended June 30, 2016.

Amount of AmountsDebt Debt Expected

Outstanding Outstanding to be PaidJuly 1, June 30, Within2015 Additions Reductions 2016 One Year

Governmental Activities General Obligation Bonds $ 21,625,000 $ 3,240,000 $ 680,000 $ 24,185,000 $ 725,000 Unamortized Premium - 5,318 (44) 5,274 266 Unamortized Discount (191,251) - 12,498 (178,753) (12,497)

$ 21,433,749 $ 3,245,318 $ 692,454 $ 24,011,521 $ 712,769

The repayment of general obligation bonds includes the following:

Paid by the District $ 579,587 Paid by the Kentucky School Facility Construction Commission 100,413

$ 680,000

Bonds The District, through the General Fund, (including Facility Support Program of Kentucky Fund (FSPK) and the Support Education Excellence in Kentucky (SEEK) Capital Outlay Fund) is obligated to make payments in amounts sufficient to satisfy debt service requirements on bonds issued by the sponsoring governmental entity to construct school facilities. The District entered into "participation agreements" with the School Facility Construction Commission (the Commission). The Commission was created by the Kentucky General Assembly for the purpose of assisting local school districts in meeting school construction needs. The table below sets forth the amount to be paid by the District and the Commission for each year until maturity of all bond issues. The liability for the total bond amount remains with the District and, as such, the total principal outstanding has been recorded in the financial statements.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

25

NOTE 4 - DEBT AND LEASE OBLIGATIONS (Continued) The original amount of each outstanding issue, the issue date, interest rates and outstanding balances at June 30, 2016 are summarized below:

OutstandingOriginal Balance at

Issue Date Amount Interest June 30, 2016

November, 2007 $ 2,125,000 3.30 - 5.65 % $ 890,000 September, 2010 3,860,000 1.00 - 5.00 3,040,000 December, 2011 7,560,000 5.00 7,560,000 July, 2014 5,315,000 1.65 - 3.25 5,095,000 April, 2015 4,475,000 2.00 - 3.10 4,360,000 May, 2016 3,240,000 2.00 - 3.00 3,240,000

Plus: Unamortized Bond Premium 5,274 Less: Unamortized Bond Discounts (178,753)

$ 24,011,521

All issues may be called prior to maturity at dates and redemption premiums specified in each issue. Assuming no bonds are called prior to scheduled maturity, the minimum obligations of the District, including amounts to be paid by the Commission, at June 30, 2016 for debt service (principal and interest) are as follows:

FederalPrincipal Interest Principal Interest Rebate Total

$ 626,357 $ 818,512 $ 98,643 $ 93,197 $ (420,021) $ 1,216,688 639,558 802,043 100,442 89,974 (418,597) 1,213,420 657,726 784,403 102,274 86,513 (416,969) 1,213,947 675,859 766,200 104,141 82,755 (415,077) 1,213,878 693,959 743,686 106,041 78,564 (412,786) 1,209,464 707,024 727,219 107,976 73,949 (410,107) 1,206,061 720,053 710,023 109,947 69,089 (407,218) 1,201,894 737,648 689,401 112,352 63,542 (404,075) 1,198,868 759,656 665,031 115,344 57,203 (400,729) 1,196,505 781,514 639,158 118,486 49,980 (396,648) 1,192,490 803,284 613,940 121,716 42,663 (392,560) 1,189,043 824,893 587,654 125,107 35,823 (389,112) 1,184,365 851,332 559,921 128,668 28,679 (385,529) 1,183,071 876,107 530,098 113,893 21,277 (381,770) 1,159,605 854,390 316,613 7,625,610 13,481 (189,922) 8,620,172 724,437 105,228 65,563 8,322 - 903,550 746,463 83,495 68,537 6,355 - 904,850 769,407 61,101 70,593 4,299 - 905,400 787,289 38,019 72,711 2,181 - 900,200 480,000 14,400 - - - 494,400

$ 14,716,956 $ 10,256,145 $ 9,468,044 $ 907,846 $ (5,841,120) $ 29,507,871

KY School FacilitiesBeechwood Independent School District Construction Commission

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

26

NOTE 5 - ACCUMULATED UNPAID SICK LEAVE BENEFITS

Upon providing proof of qualification as an annuitant from the Kentucky Teachers’ Retirement System, certified and classified employees will receive from the District, an amount equal to 30% of the value of accumulated sick leave. At June 30, 2016, this amount totaled approximately $83,598 for those employees with twenty-seven or more years of experience. Changes in the District’s compensated absences during fiscal year 2016 were as follows:

AmountsExpected

Balance Balance to be PaidJune 30, June 30, Within

2015 Additions Reductions 2016 One Year

Governmental Activities Accumulated Sick Leave $ 26,192 $ 57,406 $ - $ 83,598 $ 30,111

The accumulated sick leave liability will be liquidated by the General Fund.

NOTE 6 - COMMITMENTS UNDER NON-CAPITALIZED LEASES

The District has operating leases for four copiers for sixty to sixty-three months that expire at various dates through December, 2020. Expenditures for the equipment under these operating leases totaled $28,891 for the year ended June 30, 2016. Future minimum rental lease payments under the leases are as follows:

Years EndingJune 30,

2017 $ 30,420 2018 25,610 2019 7,332 2020 6,320 2021 2,123

$ 71,805

The District’s total payroll for the year was $7,508,065. The payroll for employees covered under the following plans totaled $7,283,216.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

27

NOTE 7 - PENSION PLANS Kentucky Teachers' Retirement System Certified employees participate in the Kentucky Teachers' Retirement System (KTRS), which is a cost sharing, multiple-employer retirement system created by, and operating under, Kentucky law. The Kentucky Teachers' Retirement System covers all regular certified full-time employees of each school district. The plan provides for retirement, disability and death benefits. KTRS issues a publicly available financial report that includes financial statements and required supplementary information. The report may be obtained in writing from the Kentucky Teachers' Retirement System, 479 Versailles Road, Frankfort, Kentucky 40601-3800. Participating employees contribute 12.855% of creditable compensation. Matching contributions are made by the state. These on behalf payments are reflected in the District’s financial records and amounted to $930,864 for 2016. The matching contributions are paid by the federal program for any salaries paid by that program. Such contribution rates are determined by the District of Trustees of Kentucky Retirement Systems. The District contributed 16.105% of the employee's compensation paid by federal programs for the fiscal year ended June 30, 2016. In addition, the District contributed 3.00% of the employee’s compensation to the retiree medical insurance fund for employees who are not in federally funded positions. The District’s required contributions for pension obligations to KTRS for the fiscal years ended June 30, 2016, 2015, and 2014 were $1,018,924 (composed of $216,050 from the District and $802,874 from the employees), $866,241, and $708,916, respectively; 100% has been contributed for fiscal years 2016, 2015, and 2014. County Employees Retirement System General Information about the Pension Plan Plan description: County Employees Retirement System (CERS) consists of two plans, Nonhazardous and Hazardous. Each plan is a cost-sharing multiple-employer defined benefit pension plan administered by the Kentucky Retirement Systems (KRS) under the provision of Kentucky Revised Statute 61.645. The plan covers all regular full-time members employed in nonhazardous and hazardous duty positions of each participating county, city, and any additional eligible local agencies electing to participate in CERS. Benefits provided: These systems provide for retirement, disability, and death benefits to system members. Retirement benefits may be extended to beneficiaries of plan members under certain circumstances.

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

28

NOTE 7 - PENSION PLANS (Continued) Nonhazardous Plan:

Age Years of Service Allowance Reduction

65 4 NoneAny 27 None55 5 6.5% per year for first five years, and 4.5% for next five years before

age 65 or 27 years of service.Any 25 6.5% per year for first five years, and 4.5% for next five years before

age 65 or 27 years of service.

Age Years of Service Allowance Reduction

65 5 None57 Rule of 87 None60 10 6.5% per year for first five years, and 4.5% for next five years before

age 65 or Rule of 87 (age plus years of service).

Age Years of Service Allowance Reduction

65 5 None57 Rule of 87 None

Retirement Eligibility for Members Whose Participation Began Before 09/01/2008

On or After 09/01/2008 but before 01/01/2014

Retirement Eligibility for Members Whose Participation Began On or After 01/01/2014

Retirement Eligibility for Members Whose Participation Began

Final Compensation X X Years of Service

2.20% if: Member begins participating prior to 08/01/2004.

2.00% if:Member begins participating on or after 08/01/2004 and before

09/01/2008.

Average of the last complete five if

participation began on or after 09/01/2008 but

before 01/01/2014.

Increasing percent based on service at

retirement* plus 2.00% for each year of service

over 30 if:

Member begins participating on or after 09/01/2008.

* Service (and Benefit Factor): 10 years or less (1.10%); 10 - 20 years (1.30%); 20 - 26 years (1.50%); 26 - 30 years (1.75%)

Benefit Formula for Tiers 1 & 2Benefit Factor

Average of the five highest if participation

began before 09/01/2008.

Includes earned service, purchased

service, prior service, and sick

leave service (if the member's employer

participates in an approved sick leave

program).

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

29

NOTE 7 - PENSION PLANS (Continued) Tier 3 member begins participating on or after 01/01/2014. Each year that a member is an active contributing member to the System, the member and the member’s employer will contribute 5.00% and 4.00% of creditable compensation respectively into a hypothetical account. This hypothetical account will earn interest annually on both the member’s and employer’s contribution at a minimum rate of 4.00%. If the System’s geometric average net investment return for the previous five years exceeds 4.00%, then the hypothetical account will be credited with an additional amount of interest equal to 75% of the amount of the return which exceeds 4.00%. All interest credits will be applied to the hypothetical account balance on June 30 based on the account balance as of June 30 of the previous year. Upon retirement the hypothetical account which includes member contributions, employer contributions, and interest credits can be withdrawn from the System as a lump sum or annuitized into a single life annuity option. Hazardous Plan:

Age Years of Service Allowance Reduction

55 5 NoneAny 20 None50 15 6.5% per year for first five years, and 4.5% for next five years before

age 55 or 20 years of service.

Age Years of Service Allowance Reduction

60 5 NoneAny 25 None50 15 6.5% per year for first five years, and 4.5% for next five years before

age 60 or 25 years of service.

Age Years of Service Allowance Reduction

60 5 NoneAny 25 None

Retirement Eligibility for Members Whose Participation Began On or After 01/01/2014

Retirement Eligibility for Members Whose Participation Began Before 09/01/2008

On or After 09/01/2008 but before 01/01/2014Retirement Eligibility for Members Whose Participation Began

Final Compensation X X Years of Service

Average of the three highest if participation

began before 09/01/2008.

2.50% if: Member begins participating before 09/01/2008.

Average of the three highest complete

years if participation began on or after

09/01/2008.

Increasing percent based on service at retirement* if:

Member begins participating on or after 09/01/2008 but before

01/01/2014.

* Service (and Benefit Factor): 10 years or less (1.30%); 10 - 20 years (1.50%); 20 - 25 years (2.25%); 25 + years (2.50%)

Benefit Factor

Includes earned service, purchased

service, prior service, and sick

leave service (if the member's employer

participates in an approved sick leave

program).

Benefit Formula

BEECHWOOD INDEPENDENT SCHOOL DISTRICT

30