BCG - healthed.govt.nz BCG... · • အိ ... ႏွာေခ်ျခင္း တို႔အားျဖင့္ ...

BCG Retail Banking Benchmarking,U.S. Bank S.T.A.R.T. Example

March 14, 2012

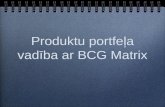

Almost one-half of the 40 largest banks participatedOver $14 Trillion in assets, 400 M customers, 50K branches

1

Note: Largest banks ranked by deposits; excludes investment banks and processing banksSource: The Banker Top 1000 World Banks 2011, Company documents

Four main levers for Operational Excellence in Retail Banking

Client excellence

1

Branch excellence

Online excellence

End-To-End performance

Multi-channel delivery

Call center excellence

y

2 3Efficient and effective processes

Streamlined organization

Efficient new product

processes

Efficient administration

processes

Process

Leanorganization

Sales focused FTE distribution

Adequate Opsautomation &

sharing

4

q pfootprint (loca-

tions, sourcing)

Underlying capabilities

2

Complexity management

Performance management

Continuous improvement

Effective front/back office

collaboration

Four levers of Operational ExcellenceRetail Banking Process & Productivity Benchmarking overview

What is this benchmarking about?

Four levers to achieveOperational Excellence

Key Performance cockpit

Top 30 retail banks• North America• Europe• Asia-Pacific

U i b h ki

Client excellence • Maximized customer facing

resources• Aligned with profitability• High utilization

7.5%4.5%5.6%

5.42.64.1

Customer attrition rate

Call handling time (minutes) S

ampl

e K

IPIs1

Unique benchmarking• All retail products• Operations and customer-facing

activities• Activity-based FTE mapping,

rather than organization-based16%2% 4%

803219460

New product sales per sales FTE

Sales conversion per inbound call S

ampl

e K

IPIsEfficient and effective processes• High level of industrialization• Processes simplified• Harmonized activities

2

rather than organization-based, applicable to all business models

Banks covering• $14.5 trillion in assets• 450 million customers 87%51%

1,270307437

Customers per total FTE

Share of sales & ser-vice as % of FTEs S

ampl

e K

IPIsStreamlined organization

• Reduced complexity; clarified accountabilities

• Sub-scale units consolidated

3

• 51,000 branches

Number of products 21726

58

87%51% 71%vice as % of FTEs

Incentives for i i O

Sm

ple

KIP

Is

• Effective use of sourcing/shoring

Underlying capabilities• Continuous complexity reduction • Rigorous people performance mgmt

across sales and operations

4

3

improving Ops performance

"None" "Aggres-sive" S

am

BestWorstMedian

across sales and operations• Transparency on performance, cost

Benchmarking summary across full value chain and linked to four levers of Operational Excellence

Benchmarking overviewValue chain data collection

4

Detailed insights

Critical capabilities and practices

Customer facing FTEs/rolesCustomer-facing FTEs/roles

Call centers service levels

Client excellence KPIs

5

From academic to reality, from theoretical to practical

Benchmarking Action

Ranking

Issue identification

Identified the problem

Formed a team to figure out a

Anecdotal lessons from top performers

gsolution across at least six silos/groups• Retail banking• Credit cards

Implication for US Bank• Not a cost issue at all• Sales force effectiveness

• Credit cards• Technology• Finance• Marketing

• Growth• Innovation

• Enterprise revenue office

CEO mandate• New value proposition to grow

6

New value proposition to grow

Context and objectives of the effort

Context Objectives

Competitors launching new products

Create a powerful value proposition

Positive impact on consumer Highly profitable, but no core relationship growth, lack "hook"

C h th t t

engagement

Generate excitement, strong desire t ll f fi ld / b h dConsumer research– they want to

save and need help doing it

Lack of collaboration across silos

to sell for field / branch and corporate employees

Provide a compelling example toLack of collaboration across silos, inhibiting integrated offering

Focus on delivering value in

Provide a compelling example to reinforce innovation theme

Provide a structure to facilitate

7

Focus on delivering value in current fiscal with full roll within a year

Provide a structure to facilitate cross-silos work

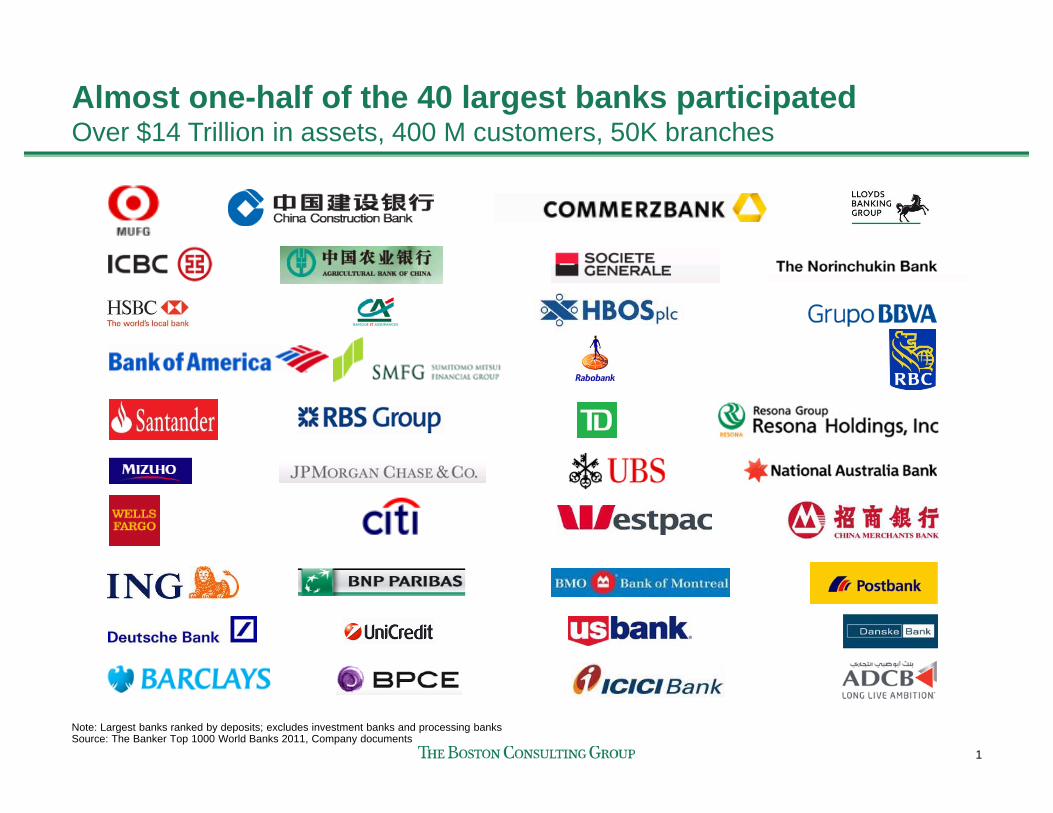

New product developed using rigorous customer research process

Over 20 concepts brainstormedby senior leaders New product candidatesy

Tested concepts through over 30 one-on-one customer interviews

p

One-on-one interviews

Identified and refined high-potential concepts based on interviews Final

Tested concepts in a quantitative ( i t " t l" t )

Concepts

survey (against "control" concepts)

Analyzed survey results and id tifi d t f k t l h

Survey

8

identified concept for market launch

Final Product

Consumer responses to further probing informing development of functional product features

Qualitative research

Wary, quick to detect

gimmicks

Desire help with 'forced'

• Idea must be simple enough to fully communicate

• Avoid "too-good-to-be-true"• Simple to communicate• Avoid "too-good-to-be-true" gimmicks,

'fine print'savings

Do not want toCreating

Avoid too good to be true kickers or language

• Avoid focus on 'goal • Disliked slow savings options Do not want to much bank exposure

Creating significant

value

identification • Very negative reaction to

"name" use of funds

Disliked slow savings options• A few mentioned low balance

generation from "Keep the Change"

Coupons not viewed as true

way to save

Choice, control,

flexibility

• Discounts typically had to be in 15%+ range

• Preferred store selection varies considerably

• Not want to feel "forced" • Need to be able to change their

mind later y

Aversion to f dit

y

Simplicity (despite

varies considerably

• Trying to avoid further spend

• "Single-feature" concepts performed well

9

use of credit cards,

( pwanting

everything)• Mass affluent still seeking

rewards maximization

performed well• Refer back to a single

reference/sticking point often

Auto Savings and Rewards candidates for further testing

Qualitative research

Neutral UnfavorableFavorable

Flexible rewards 67 14 19

Cash back rewards only 71 14 14Auto SaveSelected f

Rewards & Auto Sweep 48 19

Choice in Auto Sweep only 57 29 14

Travel rewards only 62 14

33

Flexible rewards 67 14 19

24Rewards

Auto Save

for quan-titative

and banker testing specific

Cash & Gift Cards only1 50 50

Silver Package 33 24 43

Pick Your Perk 38 33 29

Lock w Reward 40 30 30Pick Your Perk

Control

Goal Save

Rewards

g pexamplesremoved

forconfidentiality

as

Locked - Branch unlock 27 18 55

Coupons 29 48

Dollar a Day1 33 17

CD - Incrementing Rate2 40 40 20Auto Save

Discount Savings

Goal SaveDe-

prioritized for further

t ti

as manystill are

attractive

CD - Tiered 10 40 50

Combination 335214

Reward choice only 18 73 9

Locked - Branch unlock 27 18 55

Goal Save

testing

10

80604020

Auto sweep choice only 67 33

1000

%

Discovered consumer resonant concept that compared favorably with competitive offerings

Quantitative research

NoveltyPurchase intent versus novelty for mass/middle-income subjects

60

50

SAV-1KR

Novelty

ControlTurboSavings

Peer B50

40

C-W2S C-KTC

SAV-RSCBS

Control

Peer A

30

C-P

TL-F

TL-T

SAV-SRPeer C

0605040300

C PC-S

Current offering

11

Purchase intentNote: Matrix represents share of respondents with top-2 responses for initial purchase intent, novelty. Crosshairs represent arithmetic mean values on each axis for control concepts. Top-2 responses for purchase intent "Definitely" and "Probably would sign up for;" for novelty "Extremely" and "Very new and different."Source: Consumer survey (~2,500 completes)

S.T.A.R.T. Video

12

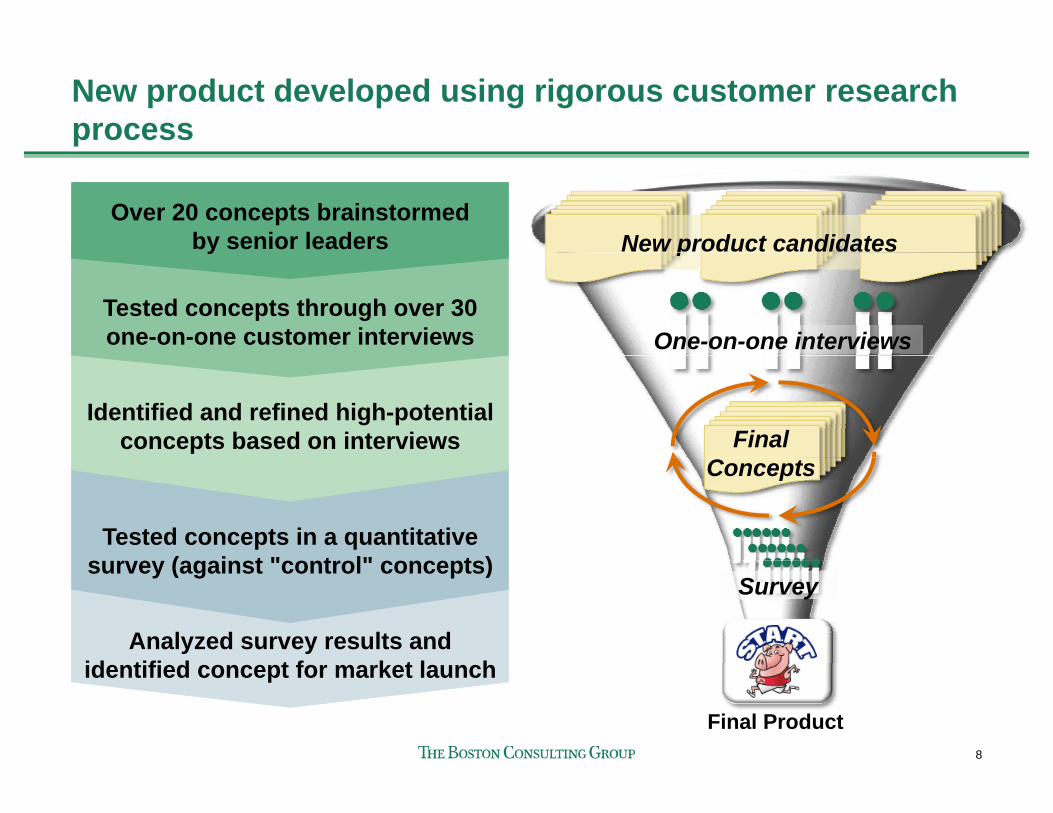

Product featuresSavingsAccount

SavingsAccount SavingsAccount

SavingsAccount

4000 1234 5678 9010

Bank

Pat Anderson

4000 1234 5678 9010

Bank

DebitBank

Customers build savings through an automatic plan• Prescheduled transfer

1 Cash back to savings• Debit card

2

Pat Anderson

4000 1234 5678 9010

Bank

Pat Anderson

• With debit transactions ($ / transaction)• With credit card transaction (% / $ / transaction)

S T A R T rewards card

Congratulations

S T A R T rewards card

Congratulations

• Credit card

SavingsSavings

Customers earn Customers earn

Reward

Congratulations

Reward

63 4 Customers"ThinkTwice5

Sav

AccountSav

Account

Customers earn a Prepaid Card when they build their savings

Customers earn Prepaid Card when keep savings for a year

63 4 Customers automatically qualify for banking package

"ThinkTwice hold" that customers can install and remove

5

13

year remove

Tested better than BofA Keep the Change on novelty and purchase intent

Product description

Savings Today And Rewards Tomorrow™S T A R T makes it simple for you to “start” a savings planS.T.A.R.T. makes it simple for you to start a savings plan that’s right for you, stay on track to meet your savings goals and earn rewards along the way.

All d t d i t i t f fAll you need to do is set up recurring transfers from your U.S. Bank Package Checking account into your U.S. Bank Package Money Market Savings account. You can save a little every week, with every paycheck, or with every credit y , y p y , yor check card purchase. And without even thinking, you can save $1,000!

When you do you’ll earn a $50 U S Bank Rewards VisaWhen you do, you’ll earn a $50 U.S. Bank Rewards Visa Card. Keep a balance of $1,000 or more for a year and earn another $50 Rewards Card.

14

Tested better than all other competing offers in marketSource: USBank Web site

Best practices that drove success

Early organizational commitment allowed a "full speed ahead" approach (with appropriate senior touchpoints for regular evaluation/redirection of program)

• Enables rapid marshalling of resources and short time-to-market

Seniorleadership

commitment

Key success factor1

p g• Empowers team to take creative risks

Understanding of customer needs

commitment

Development of customer knowledge thoroughly research-driven• Provides hard facts to inform discussions and provides a level of confidence as team makes decisions • Provides credibility with the field and increases engagement• Leads to discovery of counterintuitive results

2

• Leads to discovery of counterintuitive results

Willingness totry new approaches

3 Team was willing to "do things differently" and take creative risks at several stages of the project – a result of senior management mandate and confidence in the research and process

• Allows for true breakthroughs (rather than incremental change)• Creates opportunities for experimentation and learning

Constantdialogue with

the market

4 Solicited input from bankers / local leadership early and continued to engage them throughout the process

• Avoids a "think tank" approach to product design and implementation• Provides continuous reality checks throughout process• Builds engagement and credibility with the field

Early & activecross-BU

engagement

All involved parties across functional silos were at the table from day one as active members of project team, each with early opportunities to provide input and clearly articulated responsibilities

• Minimizes ambiguity by facilitating coordination and planning across silos• Allows for rapid problem-solving

5

g g y

15

Coordinatedinternal and

external communication

Consistent messages and coordinated timing in all communications were critical to securing engagement• Creates simple, straightforward product identity consistent with the US Bank brand• Allows leveraging of materials for multiple purposes and avoids duplication of efforts

6

Results

More than $2 7 billion saved byMore than $2.7 billion saved by customers enrolled in program

$20 illi iEnrollment Goals Exceeded

$20 million in rewards earned

56% of non-customers surveyed said S.T.A.R.T. was important in

16

2009 Year End 2010 Mid 2010 Year End 2011 Mid 2011 Year End account opening decision