BBA UST Topic2 Accounting Concept & Practice

41

Accounting Concept and Practice Topic 2

-

date post

14-Apr-2018 -

Category

Documents

-

view

223 -

download

0

Transcript of BBA UST Topic2 Accounting Concept & Practice

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 1/41

Accounting Concept and Practice

Topic 2

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 2/41

To provide information useful

for making investment andlending decisions

Generally Accepted

Accounting Principles• What is the primary objective of financial

reporting?

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 3/41

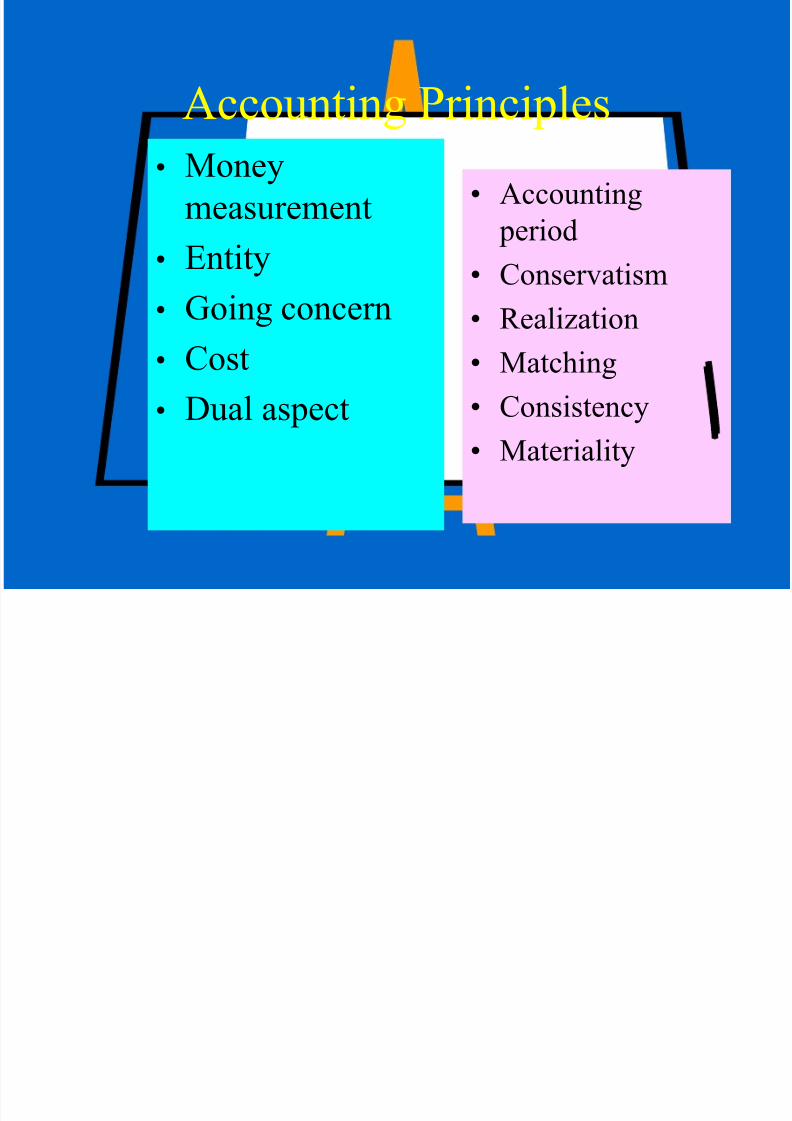

Accounting Principles

• Accounting

period

• Conservatism• Realization

• Matching

• Consistency• Materiality

Basic Concepts

• Money

measurement

•Entity

• Going concern

• Cost

• Dual aspect

Slide 2-1

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 4/41

Owner

The Entity Concept

The owner of a clothing store removes $100 from the store’scash register for personal use. Should the store’s accounting

records show that the owner took this cash?

Slide 2-2

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 5/41

The Entity Concept

Yes, because of the entity concept . This conceptrequires that the accounting records of the

clothing store show that the business has less

cash than it had previously.

Slide 2-3

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 6/41

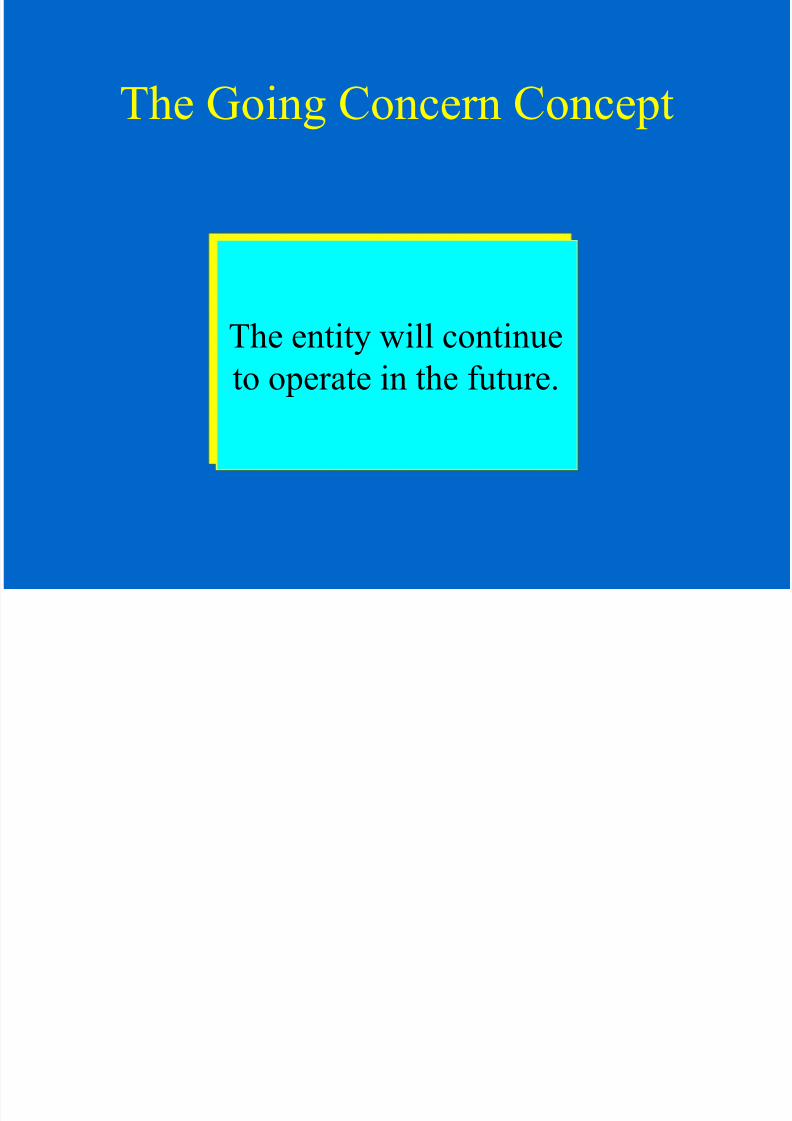

The entity will continue

to operate in the future.

The Going Concern Concept

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 7/41

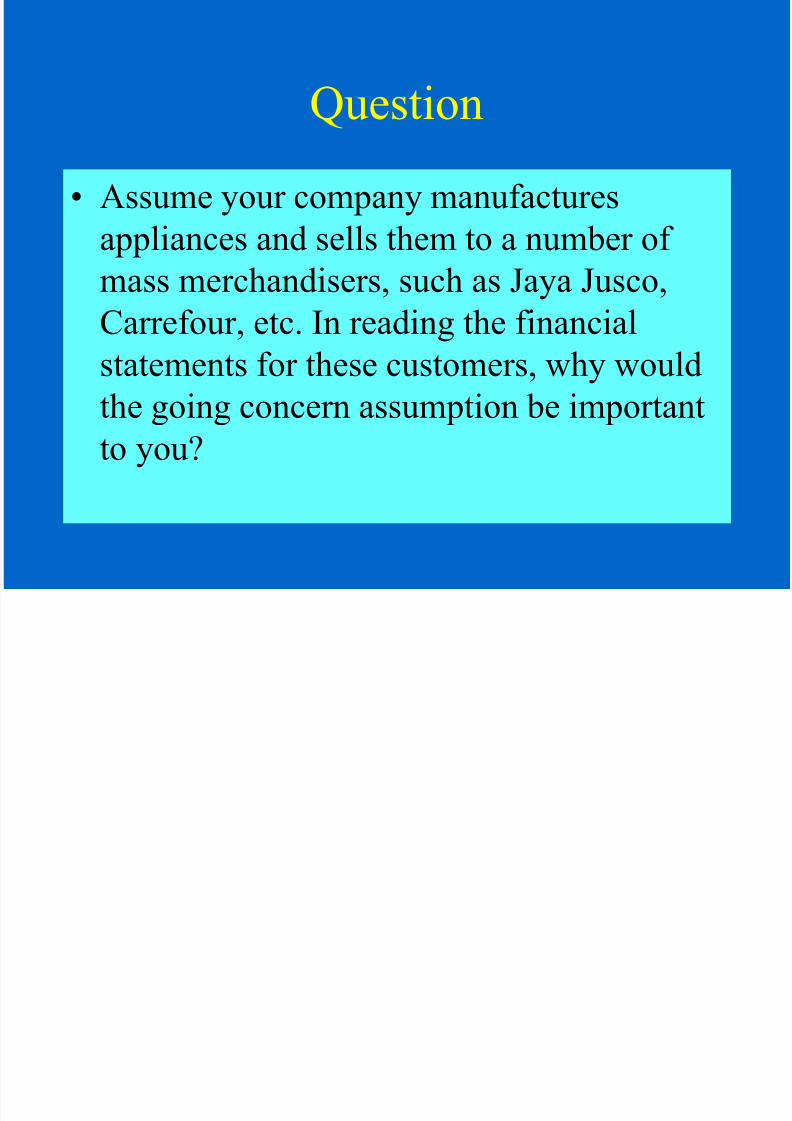

Question

• Assume your company manufactures

appliances and sells them to a number of

mass merchandisers, such as Jaya Jusco,Carrefour, etc. In reading the financial

statements for these customers, why would

the going concern assumption be importantto you?

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 8/41

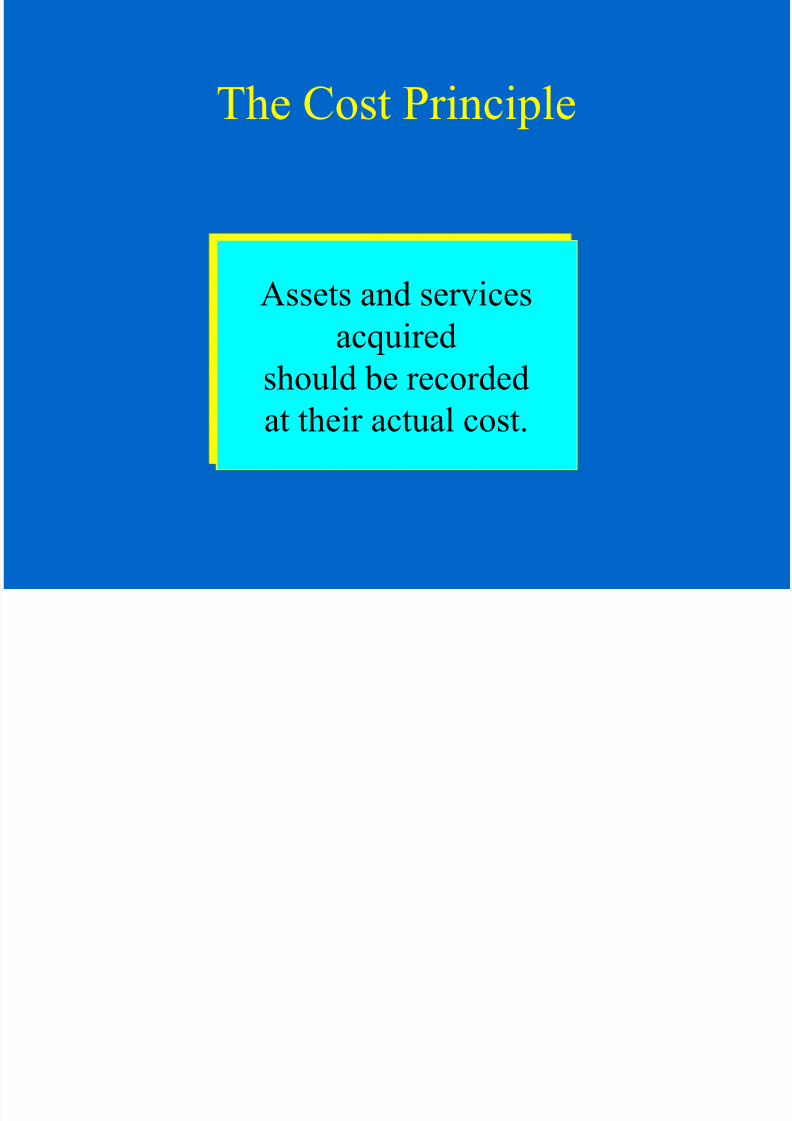

Assets and services

acquired

should be recorded

at their actual cost.

The Cost Principle

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 9/41

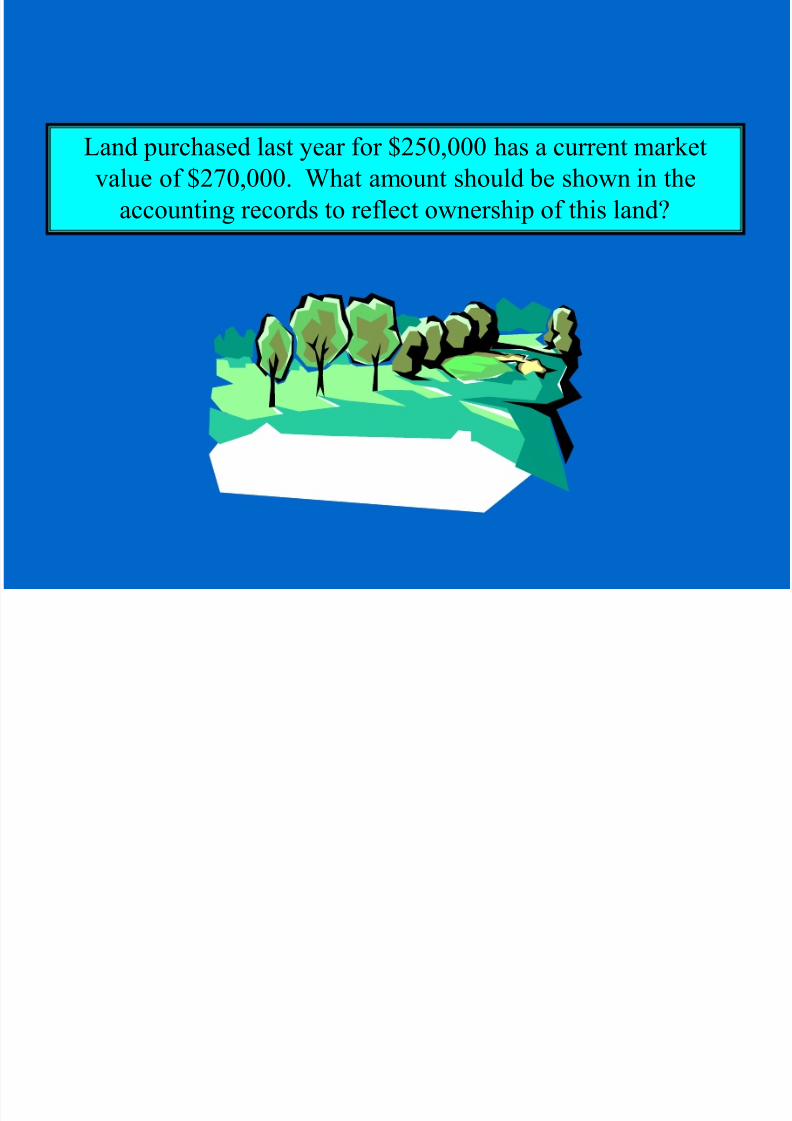

The Cost Concept--Nonmonetary Assets

Land purchased last year for $250,000 has a current marketvalue of $270,000. What amount should be shown in the

accounting records to reflect ownership of this land?

Slide 2-6

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 10/41

The Cost Concept--Nonmonetary Assets

The land should be shown at the original purchase price of $250,000 because of the cost concept.

Slide 2-7

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 11/41

The Cost Concept--Monetary Assets

A company invested surplus cash in 100,000 shares of thecommon stock of General Electric. The cost of per share was

$60; therefore, the firm spent $6,000,000. By the end of the

fiscal period, the stock had a fair market value of $65 per share.

What amount should be shown on the balance sheet?

Slide 2-8

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 12/41

The Cost Concept--Monetary Assets

The fair value of the stocks is $6,500,000.

This is the amount that should be shown for this monetary asset.

Slide 2-9

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 13/41

Exercise

(1) Timberland Bhd is now in its 30th year of

business. The founder of the company is

planning to retire at the end of the year and turn the business over to his daughter.

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 14/41

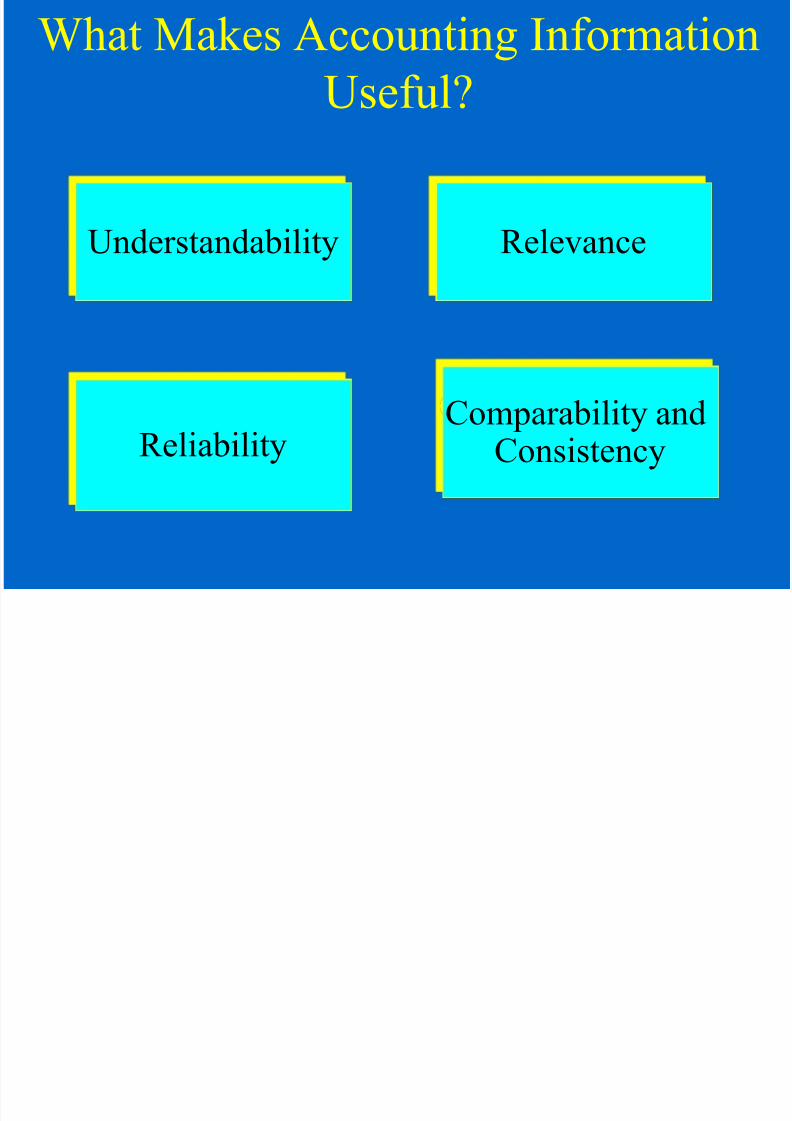

Understandability Relevance

Reliability Comparability andConsistency

What Makes Accounting Information

Useful?

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 15/41

Accounting Limitation (Constraints)

• Information limited to quantitative terms.- Matters such as morale of workforce and skill not included

• Largely confined to analysis of past events

- Financial forecast maybe unreliable

• Accounting not an exact science – Financial statementsinvolve the exercise of judgment and maybe less reliable tousers e.g. estimate remaining useful life of machine or theability of customer who owes the business to pay up

• The financial statement is expressed in monetary unit subjectto changing in value especially in time of high inflationwhere the price of goods become very high.

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 16/41

What is an Account?

• A record used to summarise all increases

and decreases in particular asset, such as

cash, or any other type of asset, liability,owners equity, revenue or expenses

• The famous accounting equation:-

Assets = Capital + Liabilities

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 17/41

.

Assets:-Assets are possessions or resources

owned by an entity; includes physical or

tangible possessions such as property, plant,machinery, stock, cash. Intangible Assets such

as copyright and patent rights and debts owed.

Capital:- The amount owners have invested

in an entity

Liabilities:- Amount owed by the entity to

outside parties. Include loans, bank overdrafts,

creditors

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 18/41

The Dual-Aspect Concept Slide 2-10

Ms. Jones opens a bank account for

the business by depositing $40,000.

Assets = Liabilities + Owners’ equity Assets = Equities

+ $40,000 + $40,000 =

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 19/41

The Dual-Aspect Concept Slide 2-11

The business borrows

$15,000 from the bank.

+ $40,000 = $40,000

Assets = Liabilities + Owners’ equity

+ 15,000 + 15,000

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 20/41

Assets = Liabilities + Owners’ equity

The Dual-Aspect Concept Slide 2-12

Assets = Equities

+ $40,000 = $40,000

+ 15,000 + 15,000

$55,000 $15,000 $40,000

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 21/41

Economic

Resources

Claims to

Economic

Resources

The Accounting Equation

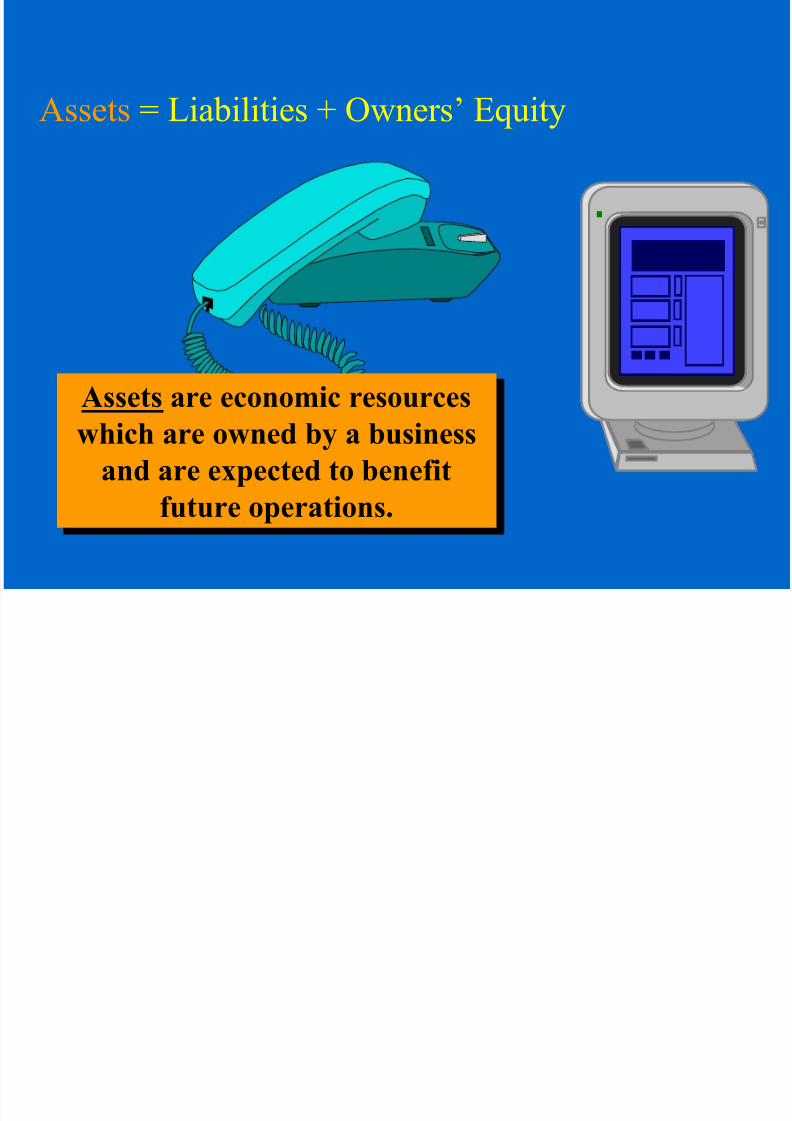

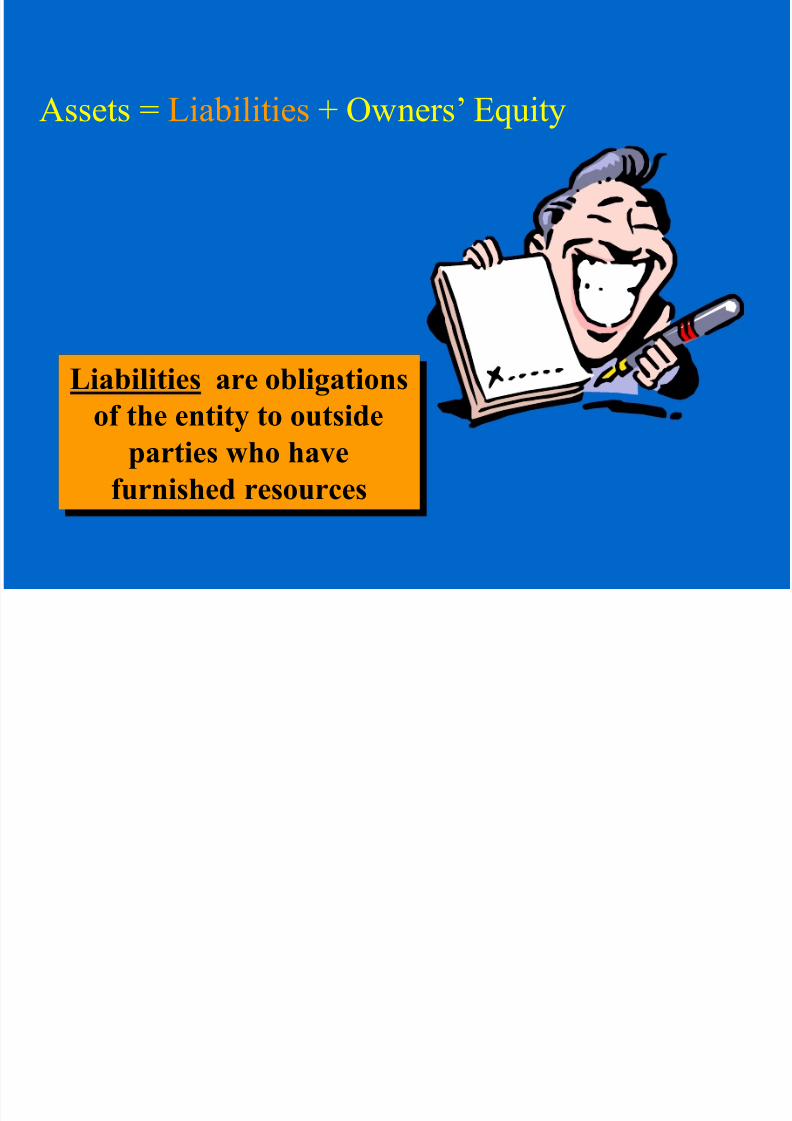

Assets = Liabilities + Owner’s Equity

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 22/41

Assets are economic resources

which are owned by a business

and are expected to benefit

future operations.

The Accounting Equation Slide 1-10

Assets = Liabilities + Owners’ Equity

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 23/41

The Accounting Equation

Liabilities are obligations

of the entity to outsideparties who have

furnished resources

Slide 1-11

Assets = Liabilities + Owners’ Equity

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 24/41

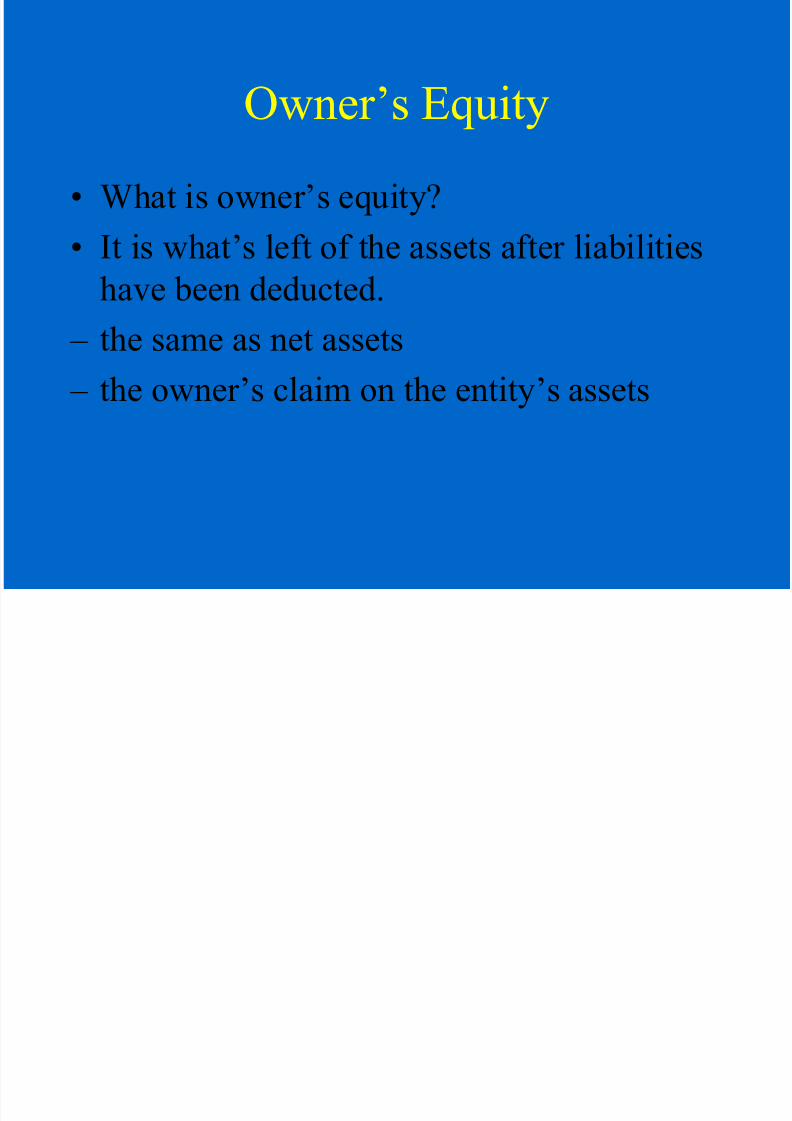

Owner’s Equity

• What is owner’s equity?

• It is what’s left of the assets after liabilities

have been deducted.

– the same as net assets

– the owner’s claim on the entity’s assets

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 25/41

Transactions that Affect

Owner’s Equity OWNER’S EQUITY

INCREASESOWNER’S EQUITY

DECREASES

Owner Investmentsin the Business

Revenues Expenses

Owner Withdrawalsfrom the Business

Owner’s Equity

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 26/41

Revenues

• What are revenues?

• They are amounts received or to be

received from customers for sales of products or services.

– sales

– performance of services – rent

– interest

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 27/41

Expenses

• What are expenses?

• They are amounts that have been paid or

will be paid later for costs that have beenincurred to earn revenue.

– salaries and wages

– utilities – supplies used

– advertising

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 28/41

Accounting for Business

Transactions• What is a transaction?

• It is any event that both affects the financial

position of the business and can be reliablyrecorded.

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 29/41

Accounting for Business

Transactions1 Gay Gillen invests $30,000 to begin Gay

Gillen eTravel.

2 Gillen purchases an office location, paying$20,000 in cash.

3 She buys office supplies, agreeing to pay

$500 in 30 days.

4 She earns and collects $5,500 revenues.

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 30/41

Accounting for Business

Transactions5 Gillen performs services, and the client

agrees to pay RM 3,000 within one month.

6 During the month, she pays RM 3,100 for expenses incurred.

7 Gillen pays RM 300 to the store from whichshe purchased RM 500 worth of supplies.

• What is the effect of these transactions onthe accounting equation?

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 31/41

Owner’s Assets = Liabilities + Equity

1) Cash +RM30,000 +RM30,000

2) Cash – 20,000Land + 20,000

3) Supplies + 500 + 500

4) Cash + 5,500 + 5,500

5) Receivable + 3,000 + 3,0006) Cash – 3,100 – 3,100

7) Cash – 300 – 300

Totals + RM35,600 + 200 +RM35,400

Accounting for Business

Transactions

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 32/41

Accounting for Business

Transactions• Notice that the equation always stays in

balance.

• Each transaction affects at least twoaccounts, sometimes more.

• Some transactions affect only one side of

the equation; some affect both sides.

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 33/41

Accounting for Business

Transactions• Other transactions that took place were

as follows:

• The business collected $1,000 from theclient.

• She sold some land at cost for $9,000.

• She withdrew $2,100 from the business.

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 34/41

– are the final

product of theaccounting process.

– tell how the business is performing

and where it stands.

Financial Statements...

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 35/41

Financial Statements

– income statement

– balance sheet

– statement of cash flows

F i i l St t t Obj ti

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 36/41

Useful to present and potential investors and creditorsin making rational investment and credit decisions

Comprehensible to those who have a reasonable

understanding of business and economic activities andare willing to study the information with reasonablediligence

About the economic resources of an enterprise, theclaims to those resources, and the effects of

transactions and events that change resources andclaims to those resources

About an enterprise’s financial performance during aperiod

F inancial Statement Objectives Financial reporting should provide

information:

Slide 1-13

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 37/41

NET SOLUTIONS

INCOME STATEMENTFor the Month Ended November 30. 2005

$ $

Fees earned 7500.000

Operating expenses

Wage expense 2125.000Rent expense 800.000

Supplies expense 800.000

Utilities expense 450.000

Miscellaneous expense 275.000

Total operating expenses 4450.000

Net Income 3050.000

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 38/41

NET SOLUTIONS

STATEMENT OF OWNER'S EQUITYFor the Month Ended November 30. 2005

Chris Clark, capital, November 1, 2005 $ $Investment on November 1, 2005 25000.00

Net Income for November 3050.0028050.00

Less withdrawals 2000.00Increase in owner's equity 26050.00Chris Clark, capital November 30, 2005 26050.00

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 39/41

NET SOLUTIONS

BALANCE SHEETNOVEMBER 30,2005

Assets Liabilities

Cash 5900.00 Accounts Payable 400.00

Supplies 550.00Land 20000.00 Owner's Equity

Chris Clark, capital 26050.00

Total Assets 26450.00 Total Liabilities and Owner's equity 26450.00

NET SOLUTIONSINCOME STATEMENT

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 40/41

NET SOLUTIONS

BALANCE SHEETNOVEMBER 30,2005

Assets Liabilities

Cash 5900.00 Accounts Payable 400.00

Supplies 550.00

Land 20000.00 Owner's Equity

Chris Clark, capital 26050.00

Total Assets 26450.00 Total Liabilities and Owner's equity 26450.00

NET SOLUTIONS

STATEMENT OF OWNER'S EQUITY

For the Month Ended November 30. 2005

Chris Clark, capital, November 1, 2005 $ $

Investment on November 1, 2005 25000.00

Net Income for November 3050.00

28050.00

Less withdrawals 2000.00

Increase in owner's equity 26050.00

Chris Clark, capital November 30, 2005 26050.00

For the Month Ended November 30. 2005

$ $

Fees earned 7500.000

Operating expensesWage expense 2125.000

Rent expense 800.000

Supplies expense 800.000Utilities expense 450.000

Miscellaneous expense 275.000

Total operating expenses 4450.000

Net Income 3050.000

7/30/2019 BBA UST Topic2 Accounting Concept & Practice

http://slidepdf.com/reader/full/bba-ust-topic2-accounting-concept-practice 41/41

End of Topic 2