BASF Capital Market Story - BASF USA - Home Capital Market Story January 22015 150 years Cautionary...

61

BASF Capital Market Story January 2015 1 150 years We add value as one company Martin Brudermueller Vice Chairman of BASF SE Hong Kong January 2015 150 years

Transcript of BASF Capital Market Story - BASF USA - Home Capital Market Story January 22015 150 years Cautionary...

BASF Capital Market Story January 2015 1

150 years We add value as one company

Martin Brudermueller Vice Chairman of BASF SE Hong Kong January 2015

150 years

BASF Capital Market Story January 2015 2

150 years

Cautionary note regarding forward-looking statements

This presentation may contain forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. Forward-looking statements may include, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. BASF has based these forward-looking statements on its views and assumptions with respect to future events and financial performance. Actual financial performance could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements. The information contained in this presentation is subject to change without notice and BASF does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

BASF Capital Market Story January 2015 3

150 years

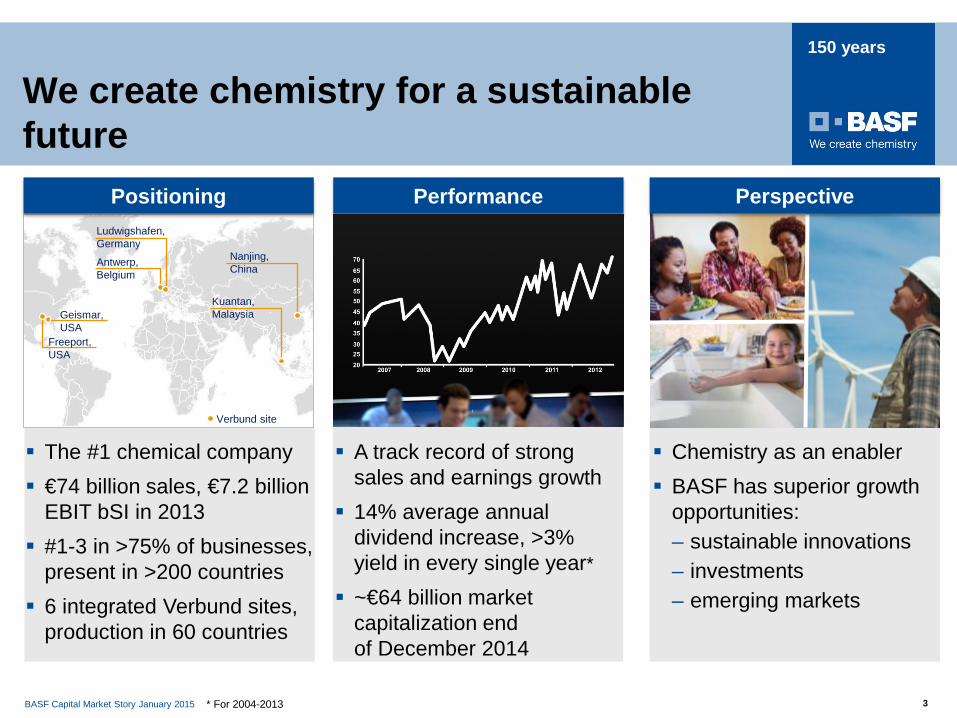

Chemistry as an enabler BASF has superior growth

opportunities: – sustainable innovations – investments – emerging markets

The #1 chemical company €74 billion sales, €7.2 billion

EBIT bSI in 2013 #1-3 in >75% of businesses,

present in >200 countries 6 integrated Verbund sites,

production in 60 countries

A track record of strong sales and earnings growth

14% average annual dividend increase, >3% yield in every single year*

~€64 billion market capitalization end of December 2014

Performance Perspective

* For 2004-2013

Ludwigshafen, Germany

Antwerp, Belgium

Nanjing, China

Kuantan, Malaysia Geismar,

USA Freeport, USA

Verbund site

Positioning

We create chemistry for a sustainable future

BASF Capital Market Story January 2015 4

150 years

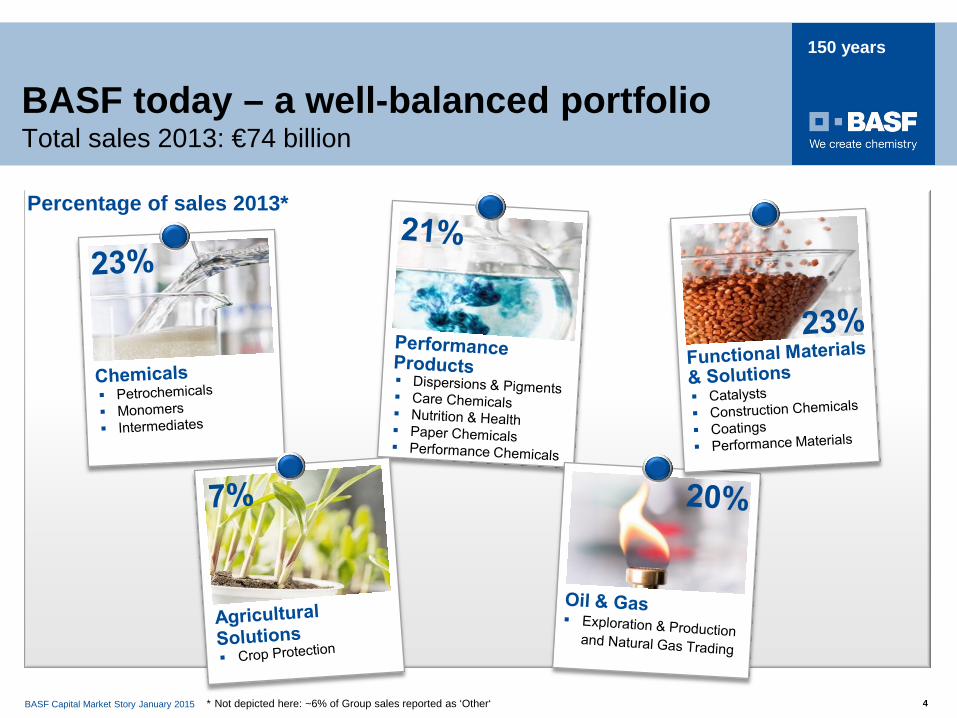

Percentage of sales 2013*

* Not depicted here: ~6% of Group sales reported as ‘Other‘

BASF today – a well-balanced portfolio Total sales 2013: €74 billion

BASF Capital Market Story January 2015 5

150 years

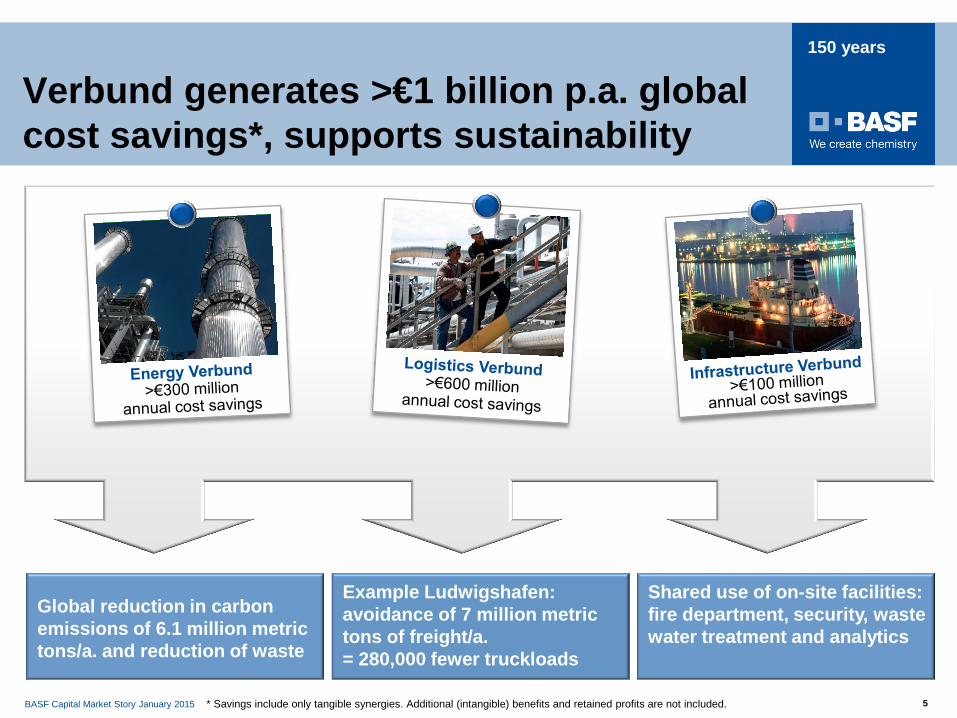

Global reduction in carbon emissions of 6.1 million metric tons/a. and reduction of waste

Example Ludwigshafen: avoidance of 7 million metric tons of freight/a. = 280,000 fewer truckloads

Shared use of on-site facilities: fire department, security, waste water treatment and analytics

Verbund generates >€1 billion p.a. global cost savings*, supports sustainability

* Savings include only tangible synergies. Additional (intangible) benefits and retained profits are not included.

BASF Capital Market Story January 2015 6

Business review

Growth Levers

BASF Capital Market Story January 2015 7

150 years

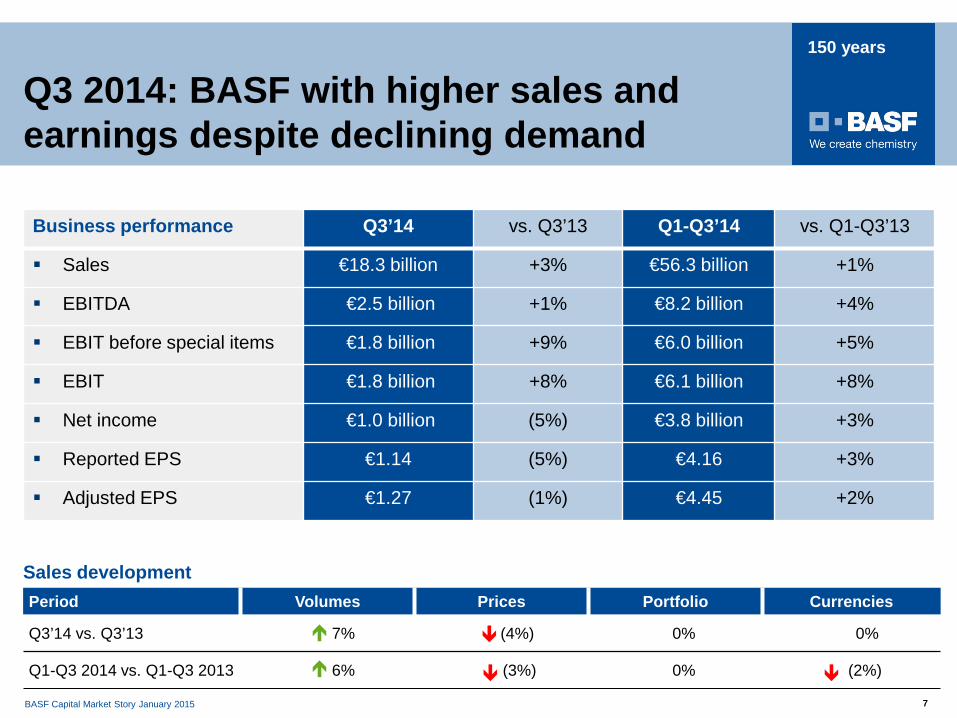

Q3 2014: BASF with higher sales and earnings despite declining demand

Sales development Period Volumes Prices Portfolio Currencies

Q3’14 vs. Q3’13 7% (4%) 0% 0%

Q1-Q3 2014 vs. Q1-Q3 2013 6% (3%) 0% (2%)

Business performance Q3’14 vs. Q3’13 Q1-Q3’14 vs. Q1-Q3’13

Sales €18.3 billion +3% €56.3 billion +1%

EBITDA €2.5 billion +1% €8.2 billion +4%

EBIT before special items €1.8 billion +9% €6.0 billion +5%

EBIT €1.8 billion +8% €6.1 billion +8%

Net income €1.0 billion (5%) €3.8 billion +3%

Reported EPS €1.14 (5%) €4.16 +3%

Adjusted EPS €1.27 (1%) €4.45 +2%

BASF Capital Market Story January 2015 8

150 years

Recent transaction with Statoil

Acquisition of participations in oil & gas fields in Norway

Purchase price amounts to US$1.25 billion

Increase of production to ~60,000 boepd in Norway

Additional reserves and resources of ~170 million boe

Transaction closed December 1st, 2014

Restructuring of Performance Products

Strengthening of R&D platforms

Important corporate developments

BASF to sell textile chemicals business to Archroma

Paper Chemicals division to be dissolved, product lines moved to other divisions

Strategic options for parts of kaolin business in evaluation

Total earnings improvement of ~€500 million by 2017

Future set up of global research platforms:

- Process Research & Chemical Engineering, led out of Europe

- Bioscience Research, led out of North America (from 2015)

- Advanced Materials & Systems Research, led out of Asia (from 2016)

BASF Capital Market Story January 2015 9

150 years

0

1

2

3

4

2004 2005 2006 2007 2008 2009** 2010 2011 2012 2013 Q1-Q32014

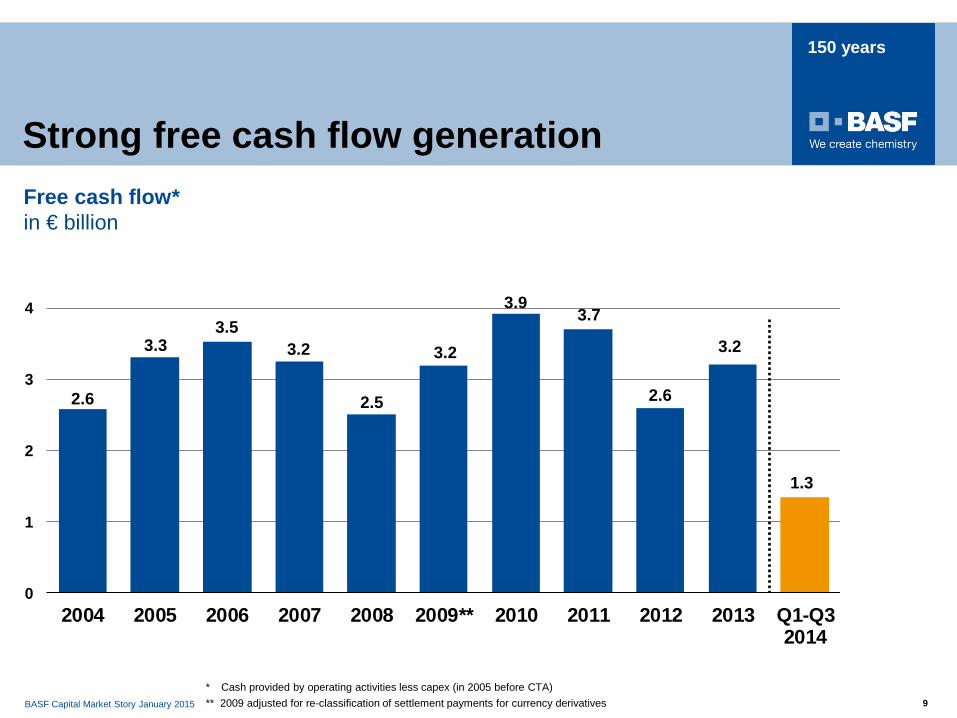

Strong free cash flow generation

* Cash provided by operating activities less capex (in 2005 before CTA) ** 2009 adjusted for re-classification of settlement payments for currency derivatives

Free cash flow* in € billion

2.6

3.3 3.5

3.2

2.5

3.2

3.9 3.7

2.6

3.2

1.3

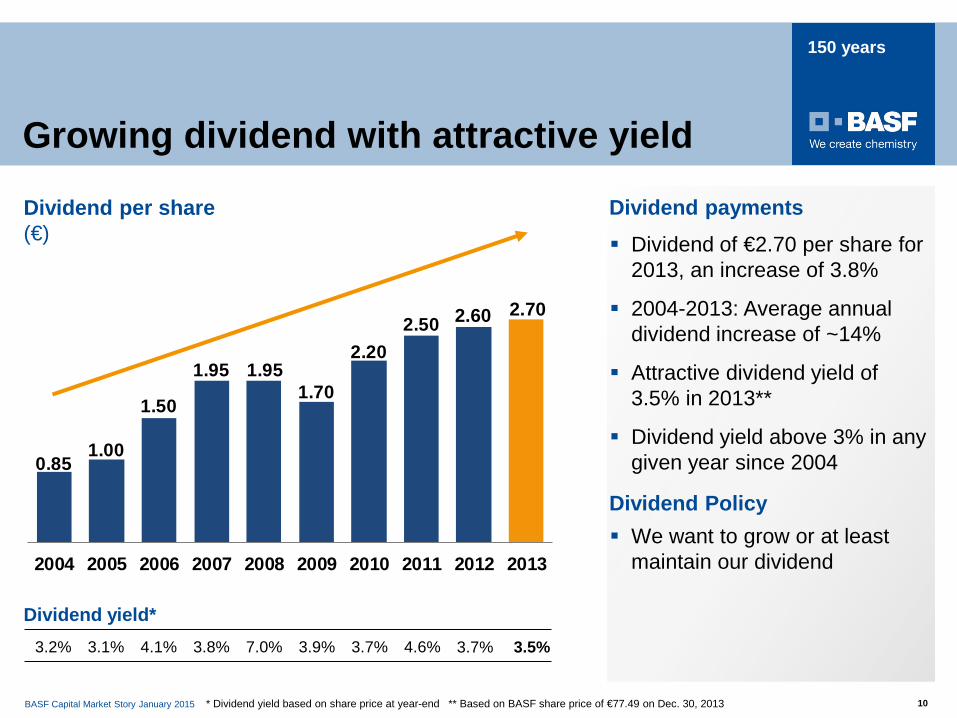

BASF Capital Market Story January 2015 10

150 years

0.851.00

1.50

1.95 1.951.70

2.202.50

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Growing dividend with attractive yield

* Dividend yield based on share price at year-end

Dividend payments

3.7% 3.2% 3.1% 4.1% 3.8% 7.0% 3.9%

Dividend yield* 4.6%

2.60 2.70

3.7%

** Based on BASF share price of €77.49 on Dec. 30, 2013

Dividend per share (€)

3.5%

Dividend Policy We want to grow or at least

maintain our dividend

Dividend of €2.70 per share for 2013, an increase of 3.8%

2004-2013: Average annual dividend increase of ~14%

Attractive dividend yield of 3.5% in 2013**

Dividend yield above 3% in any given year since 2004

BASF Capital Market Story January 2015 11

150 years

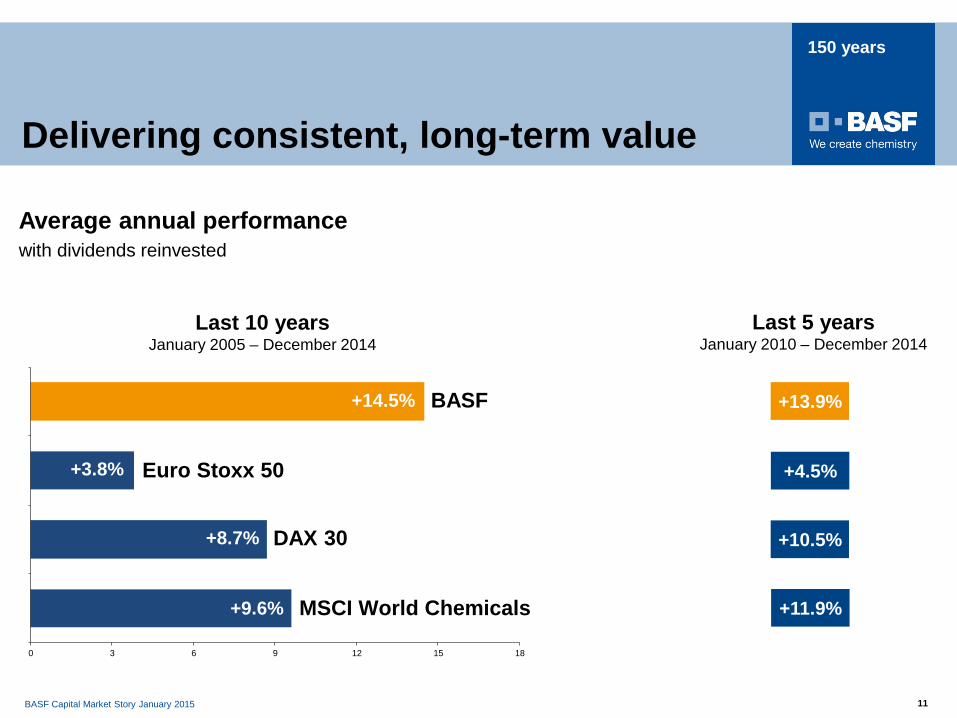

Delivering consistent, long-term value

Average annual performance with dividends reinvested

0 3 6 9 12 15 18

Euro Stoxx 50

DAX 30

MSCI World Chemicals

+8.7%

Last 5 years January 2010 – December 2014

+13.9%

+4.5%

+10.5%

+11.9%

Last 10 years January 2005 – December 2014

BASF

+9.6%

+3.8%

+14.5%

BASF Capital Market Story January 2015 12

150 years

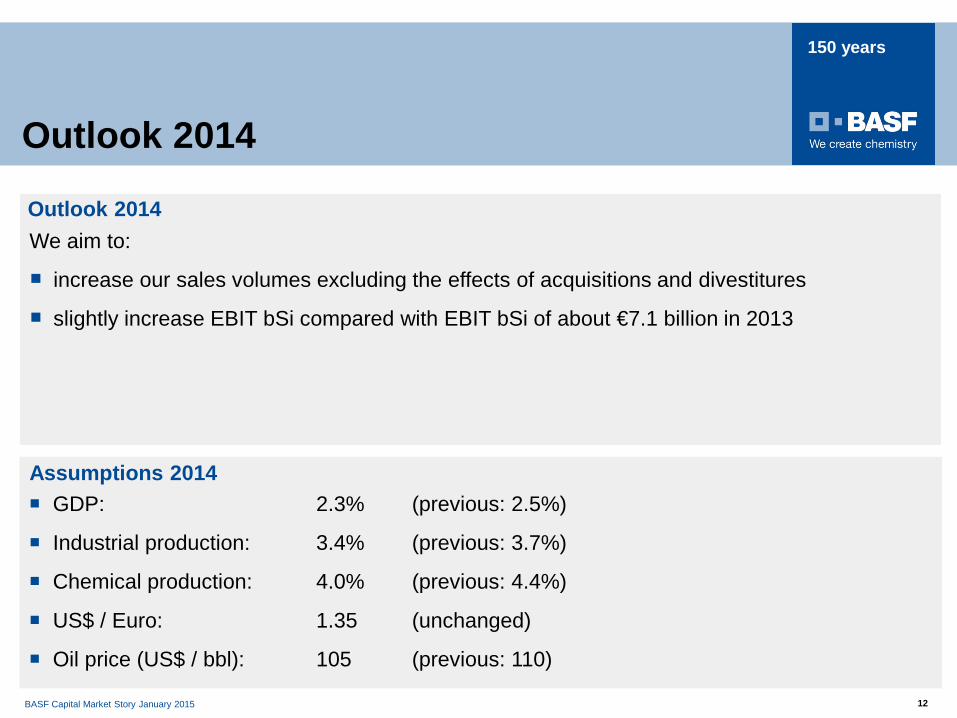

We aim to:

increase our sales volumes excluding the effects of acquisitions and divestitures

slightly increase EBIT bSi compared with EBIT bSi of about €7.1 billion in 2013

Outlook 2014

GDP: 2.3% (previous: 2.5%)

Industrial production: 3.4% (previous: 3.7%)

Chemical production: 4.0% (previous: 4.4%)

US$ / Euro: 1.35 (unchanged)

Oil price (US$ / bbl): 105 (previous: 110)

Assumptions 2014

Outlook 2014

BASF Capital Market Story January 2015 13

Business review

Growth levers – Portfolio development

– Market approach – Innovations for a sustainable future – Investments – Acquisitions – Operational excellence

BASF Capital Market Story January 2015 14

150 years

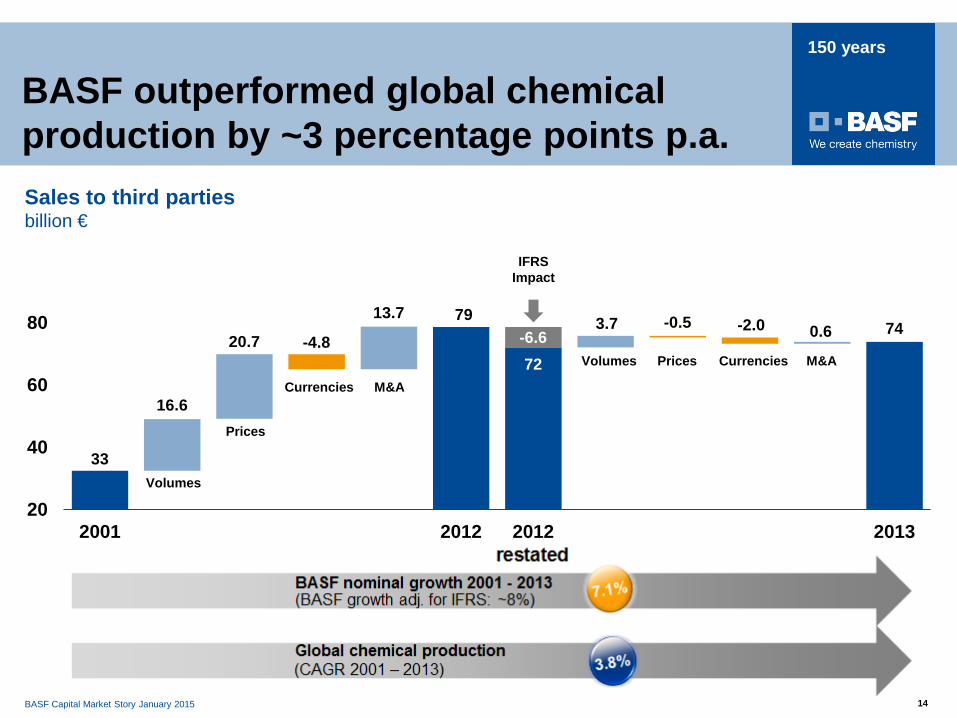

BASF outperformed global chemical production by ~3 percentage points p.a. Sales to third parties billion €

33

79

72

74

16.6

20.7 -4.8

13.7 -6.6

3.7 -0.5 -2.0 0.6

20

40

60

80

2001 2012 2012 restated

2013

Volumes

Prices

Currencies M&A

Volumes Prices Currencies M&A

IFRS Impact

BASF Capital Market Story January 2015 15

150 years

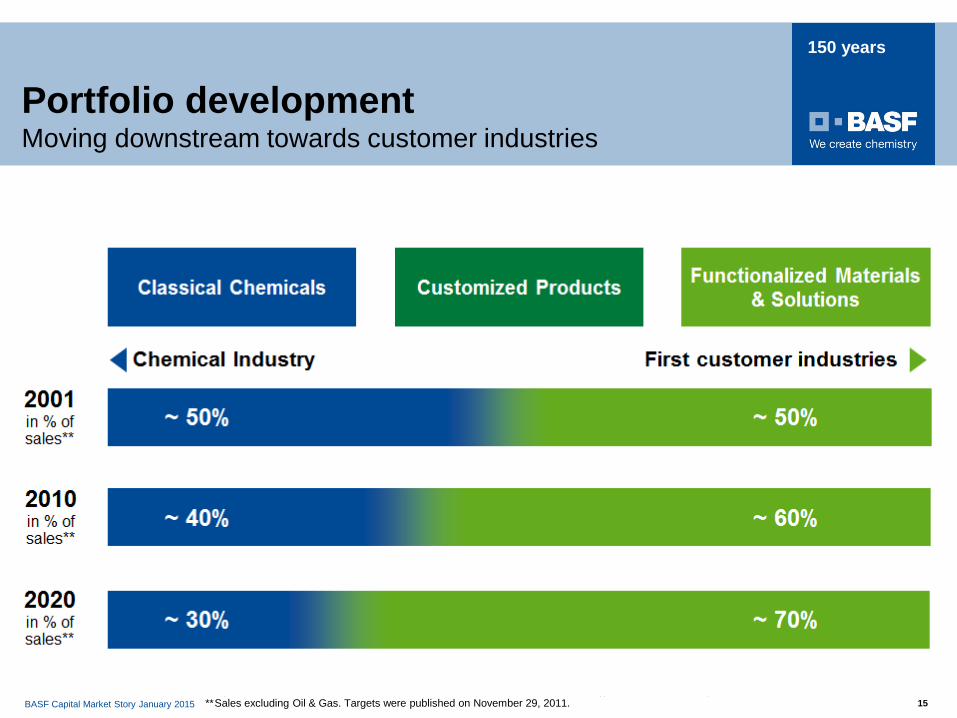

Portfolio development Moving downstream towards customer industries

* Agriculture, Construction, Consumer Goods, Health & Nutrition, Electronics, Energy & Resources, Transportation ** Sales excluding Oil & Gas. Targets were published on November 29, 2011.

BASF Capital Market Story January 2015 16

150 years

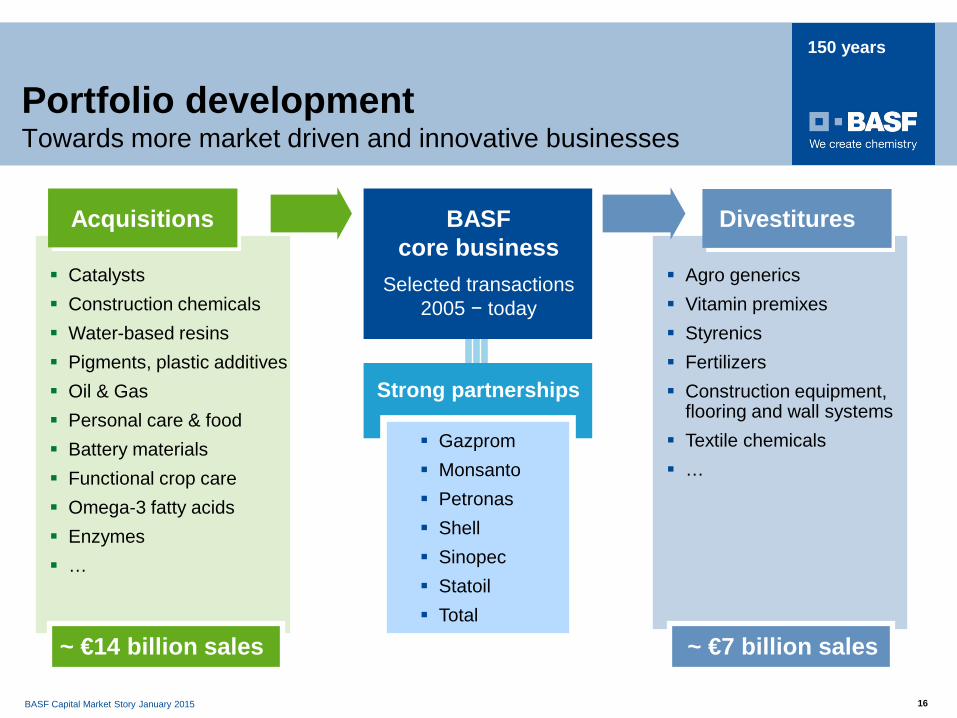

Catalysts Construction chemicals Water-based resins Pigments, plastic additives Oil & Gas Personal care & food Battery materials Functional crop care Omega-3 fatty acids Enzymes …

BASF core business

Strong partnerships

Gazprom Monsanto Petronas Shell Sinopec Statoil Total

Selected transactions 2005 − today

Acquisitions

~ €14 billion sales

Divestitures

Agro generics Vitamin premixes Styrenics Fertilizers Construction equipment,

flooring and wall systems Textile chemicals …

~ €7 billion sales

Portfolio development Towards more market driven and innovative businesses

BASF Capital Market Story January 2015 17

150 years

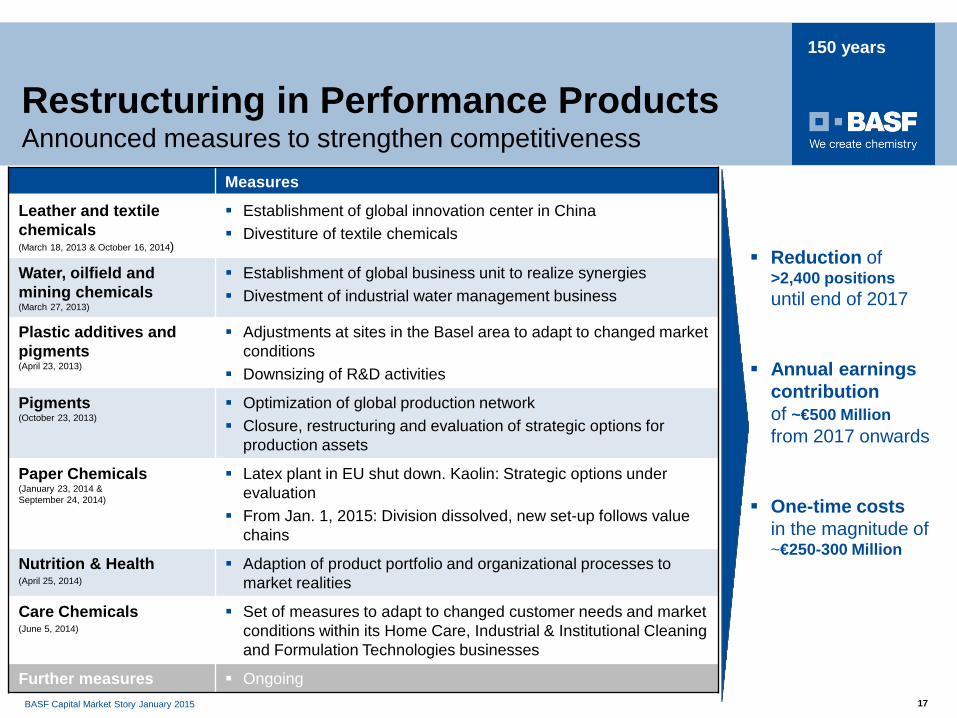

Restructuring in Performance Products Announced measures to strengthen competitiveness

Measures

Leather and textile chemicals (March 18, 2013 & October 16, 2014)

Establishment of global innovation center in China Divestiture of textile chemicals

Water, oilfield and mining chemicals (March 27, 2013)

Establishment of global business unit to realize synergies Divestment of industrial water management business

Plastic additives and pigments (April 23, 2013)

Adjustments at sites in the Basel area to adapt to changed market conditions

Downsizing of R&D activities

Pigments (October 23, 2013)

Optimization of global production network Closure, restructuring and evaluation of strategic options for

production assets

Paper Chemicals (January 23, 2014 & September 24, 2014)

Latex plant in EU shut down. Kaolin: Strategic options under evaluation

From Jan. 1, 2015: Division dissolved, new set-up follows value chains

Nutrition & Health (April 25, 2014)

Adaption of product portfolio and organizational processes to market realities

Care Chemicals (June 5, 2014)

Set of measures to adapt to changed customer needs and market conditions within its Home Care, Industrial & Institutional Cleaning and Formulation Technologies businesses

Further measures Ongoing

Reduction of >2,400 positions until end of 2017

Annual earnings contribution of ~€500 Million from 2017 onwards

One-time costs in the magnitude of ~€250-300 Million

BASF Capital Market Story January 2015 18

150 years

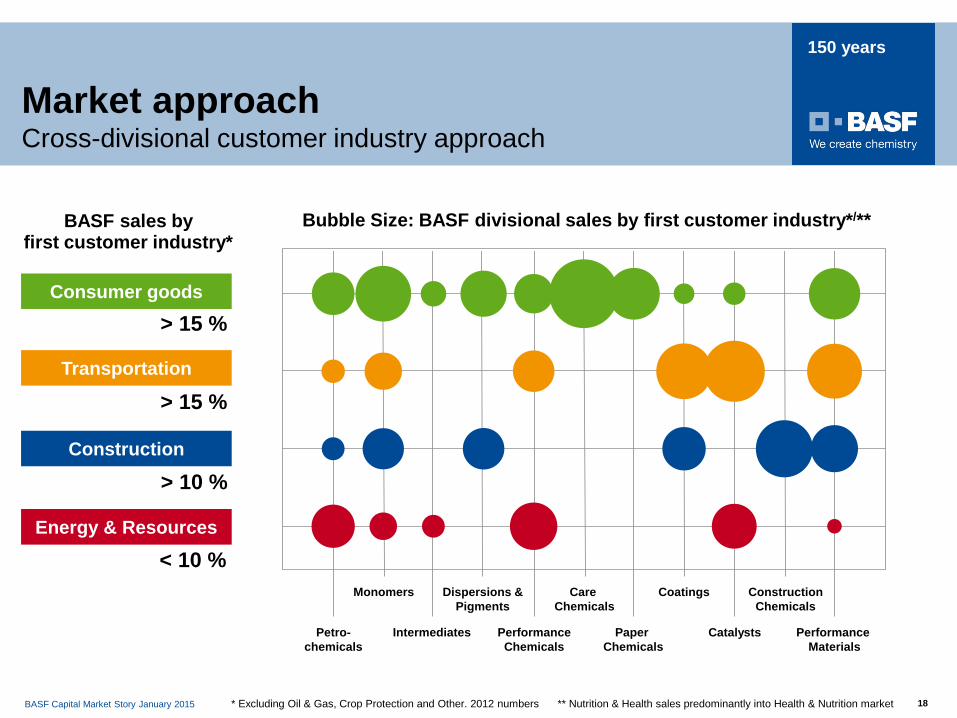

Monomers

Intermediates

Dispersions & Pigments

Performance Chemicals

Care Chemicals

Paper Chemicals

Coatings

Catalysts

Construction Chemicals

BASF sales by first customer industry*

> 15 %

> 10 %

< 10 %

> 15 %

Consumer goods

Transportation

Construction

Energy & Resources

Market approach Cross-divisional customer industry approach

* Excluding Oil & Gas, Crop Protection and Other. 2012 numbers

Petro- chemicals

Performance Materials

Bubble Size: BASF divisional sales by first customer industry*/**

** Nutrition & Health sales predominantly into Health & Nutrition market

BASF Capital Market Story January 2015 19

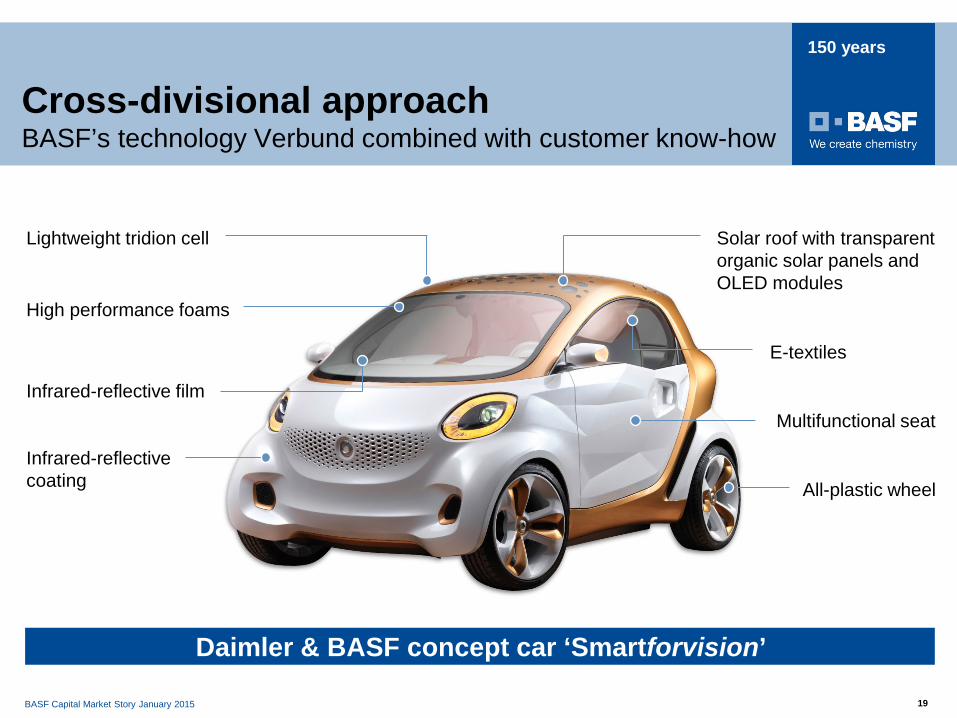

150 years

E-textiles

Solar roof with transparent organic solar panels and OLED modules

Multifunctional seat

Infrared-reflective coating

Infrared-reflective film

High performance foams

Lightweight tridion cell

All-plastic wheel

Cross-divisional approach BASF’s technology Verbund combined with customer know-how

Daimler & BASF concept car ‘Smartforvision’

BASF Capital Market Story January 2015 20

150 years

Customer Verbund - adidas and BASF Working together for disruptive innovation: Infinergy™

BASF Capital Market Story January 2015 21

150 years

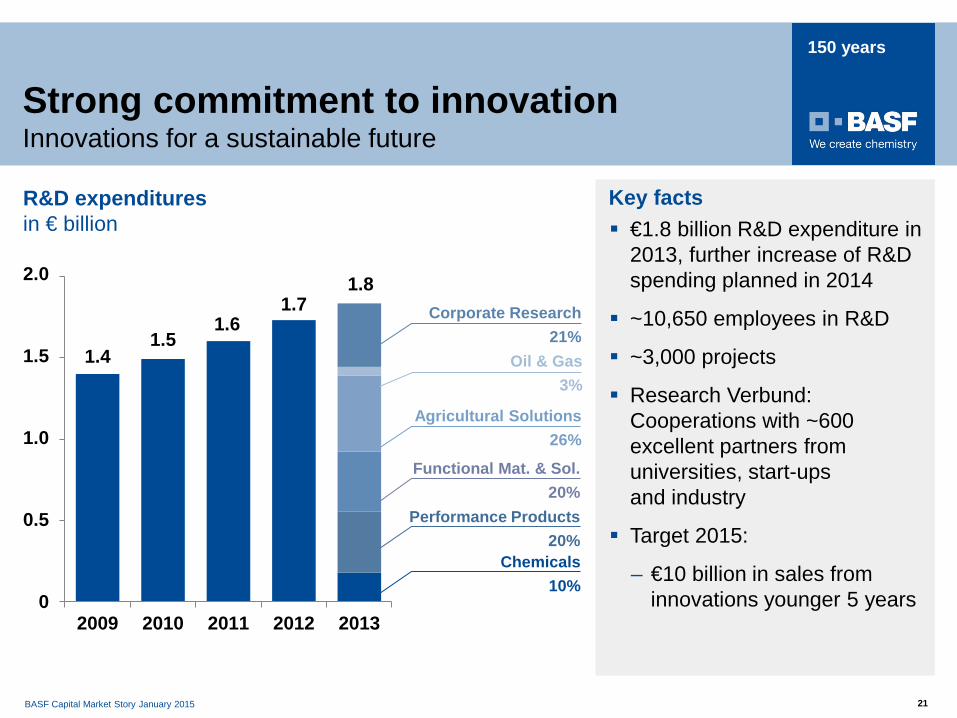

Strong commitment to innovation Innovations for a sustainable future

1.4 1.5

1.6 1.7

1.8

0,0

0,5

1,0

1,5

2,0

2009 2010 2011 2012 2013

€1.8 billion R&D expenditure in 2013, further increase of R&D spending planned in 2014

~10,650 employees in R&D

~3,000 projects

Research Verbund: Cooperations with ~600 excellent partners from universities, start-ups and industry

Target 2015:

– €10 billion in sales from innovations younger 5 years

R&D expenditures in € billion

Chemicals 10%

Performance Products 20%

Functional Mat. & Sol. 20%

Agricultural Solutions 26%

Oil & Gas 3%

Corporate Research 21%

Key facts

2.0

1.5

1.0

0.5

0

BASF Capital Market Story January 2015 22

150 years

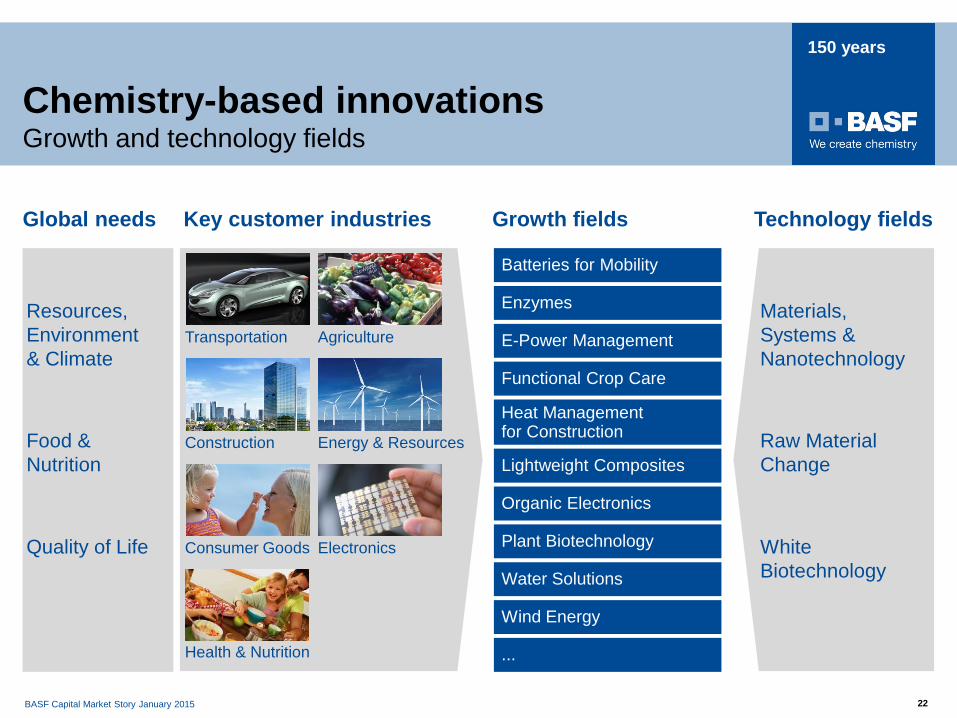

Chemistry-based innovations Growth and technology fields

Growth fields

Resources, Environment & Climate

Food & Nutrition

Quality of Life White Biotechnology

Materials, Systems & Nanotechnology

Raw Material Change

Key customer industries

Health & Nutrition

Consumer Goods

Transportation

Energy & Resources

Electronics

Agriculture

Construction

Technology fields Global needs

...

Batteries for Mobility

Enzymes

Heat Management for Construction

Organic Electronics

Functional Crop Care

Plant Biotechnology

E-Power Management

Wind Energy

Lightweight Composites

Water Solutions

BASF Capital Market Story January 2015 23

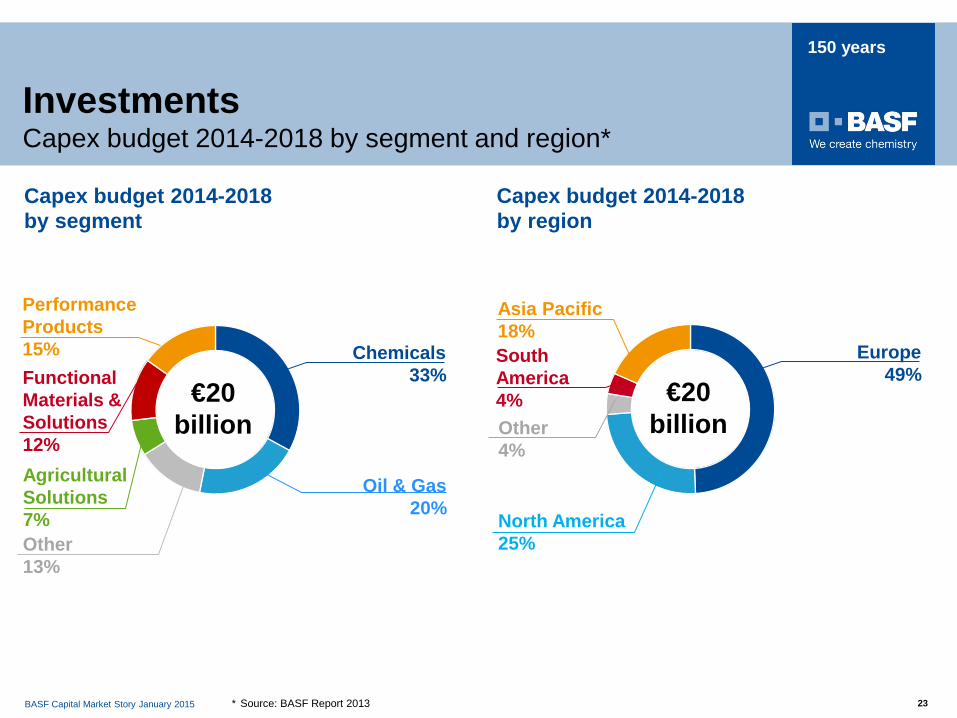

150 years

Performance Products 15%

Oil & Gas 20%

€20 billion

Functional Materials & Solutions 12%

Capex budget 2014-2018

Other 13%

Chemicals 33%

Capex budget 2014-2018

Asia Pacific 18%

€20 billion

South America 4%

North America 25%

Europe 49%

Agricultural Solutions 7%

Other 4%

by segment by region

Investments Capex budget 2014-2018 by segment and region*

* Source: BASF Report 2013

BASF Capital Market Story January 2015 24

150 years

Expansion oil & gas activities

Aroma Ingredients Kuantan, Malaysia

Investments Major projects

Ammonia and gas-to-propylene in USA*

MDI plant Chongqing, China

Acrylic acid complex Camacari, Brazil

TDI plant Ludwigshafen, Germany

* Under evaluation

BASF Capital Market Story January 2015 25

150 years

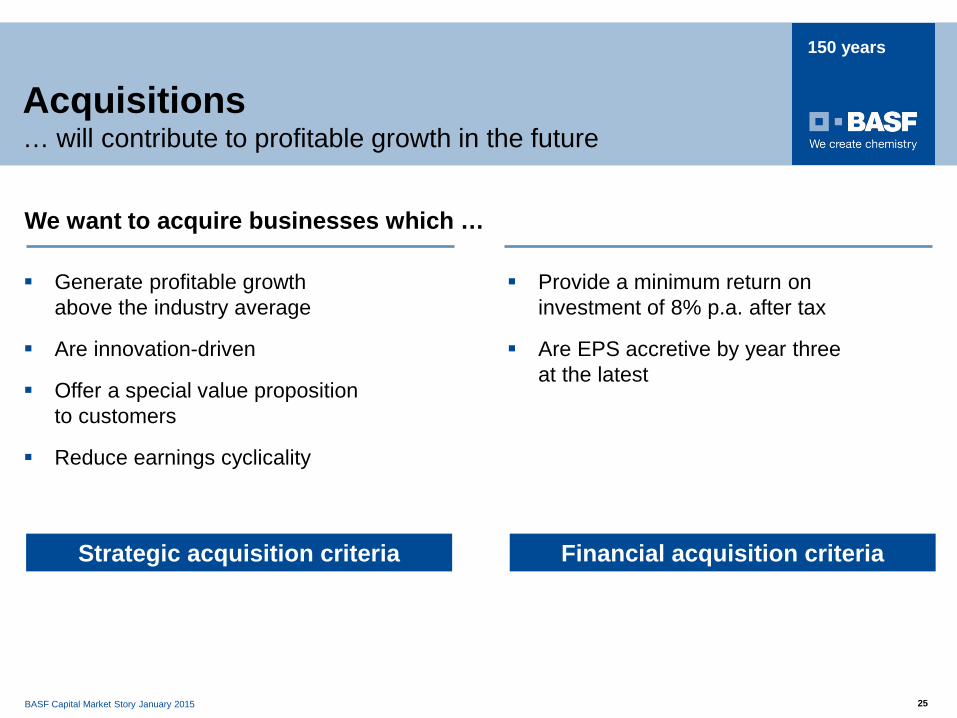

Acquisitions … will contribute to profitable growth in the future

Provide a minimum return on investment of 8% p.a. after tax

Are EPS accretive by year three at the latest

Financial acquisition criteria

Generate profitable growth above the industry average

Are innovation-driven

Offer a special value proposition to customers

Reduce earnings cyclicality

Strategic acquisition criteria

We want to acquire businesses which …

BASF Capital Market Story January 2015 26

150 years

0

1,000

2,000

3,000

4,000

2013 2015

Former cost saving programs NEXT STEP

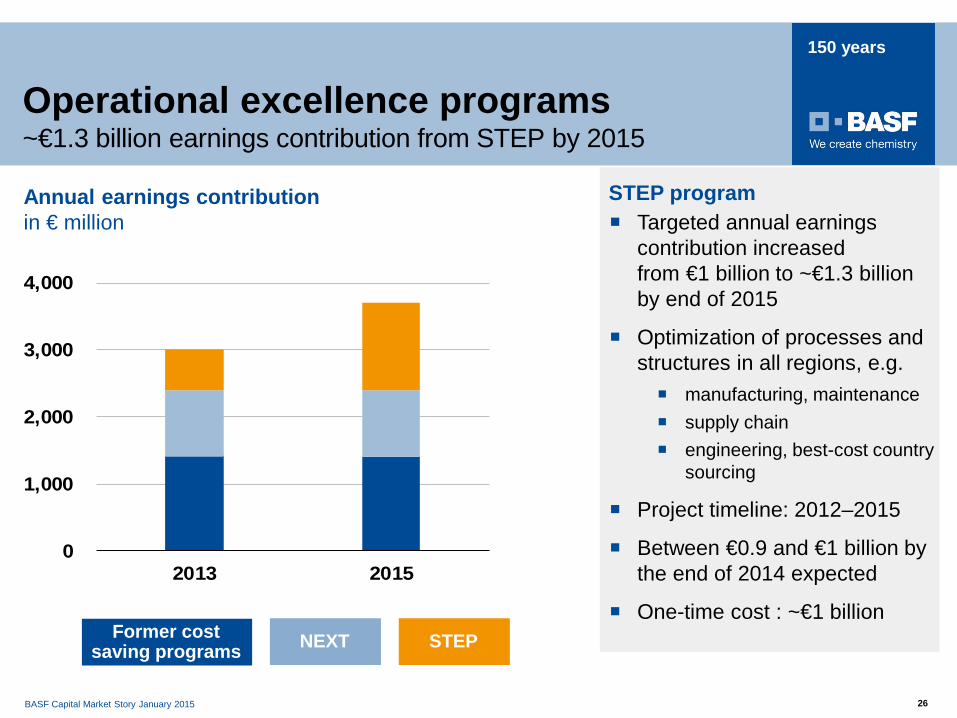

Operational excellence programs ~€1.3 billion earnings contribution from STEP by 2015

Annual earnings contribution in € million Targeted annual earnings

contribution increased from €1 billion to ~€1.3 billion by end of 2015

Optimization of processes and structures in all regions, e.g. manufacturing, maintenance supply chain engineering, best-cost country

sourcing

Project timeline: 2012–2015

Between €0.9 and €1 billion by the end of 2014 expected

One-time cost : ~€1 billion

STEP program

BASF Capital Market Story January 2015 27

150 years

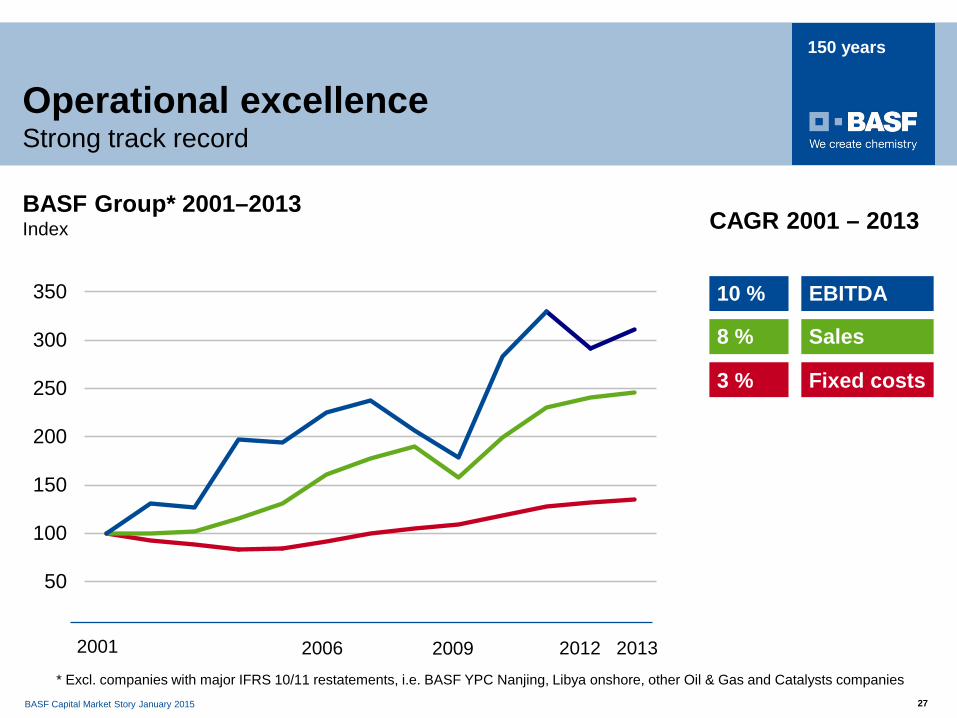

Operational excellence Strong track record

BASF Group* 2001–2013 Index

50

100

150

200

250

300

350

2001 2006 2009 2012

CAGR 2001 – 2013

10 %

8 %

3 %

EBITDA

Sales

Fixed costs

* Excl. companies with major IFRS 10/11 restatements, i.e. BASF YPC Nanjing, Libya onshore, other Oil & Gas and Catalysts companies

2013

BASF Capital Market Story January 2015 28

Appendix I:

Chemicals Day

BASF Capital Market Story January 2015 29

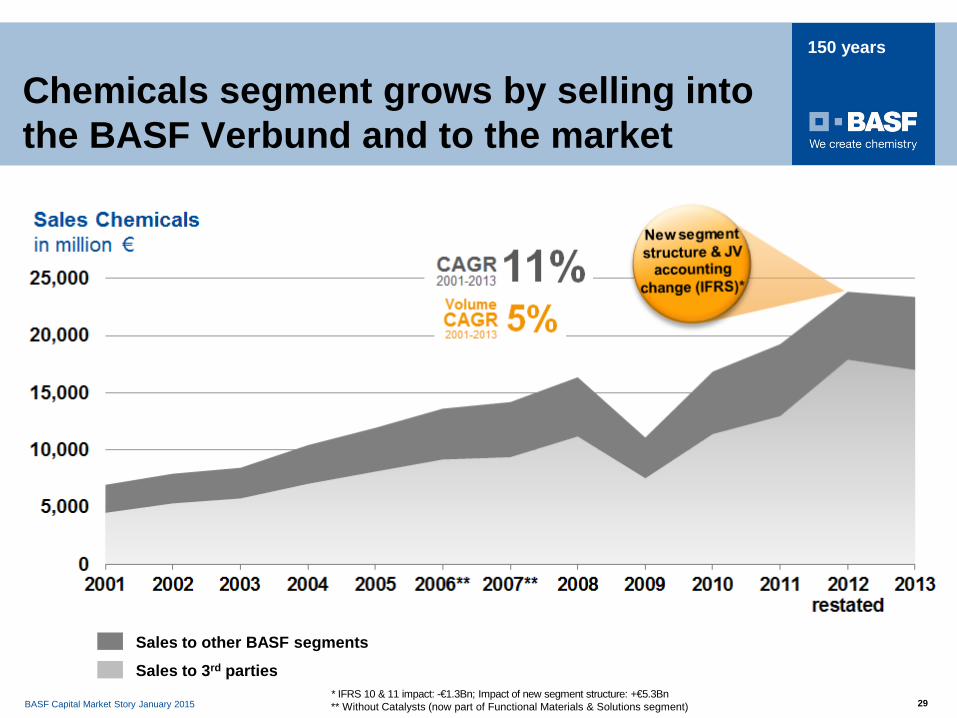

150 years

Sales to other BASF segments

Sales to 3rd parties

Chemicals segment grows by selling into the BASF Verbund and to the market

* IFRS 10 & 11 impact: -€1.3Bn; Impact of new segment structure: +€5.3Bn ** Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Capital Market Story January 2015 30

150 years

0

100

200

300

400

500

2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012restated

2013

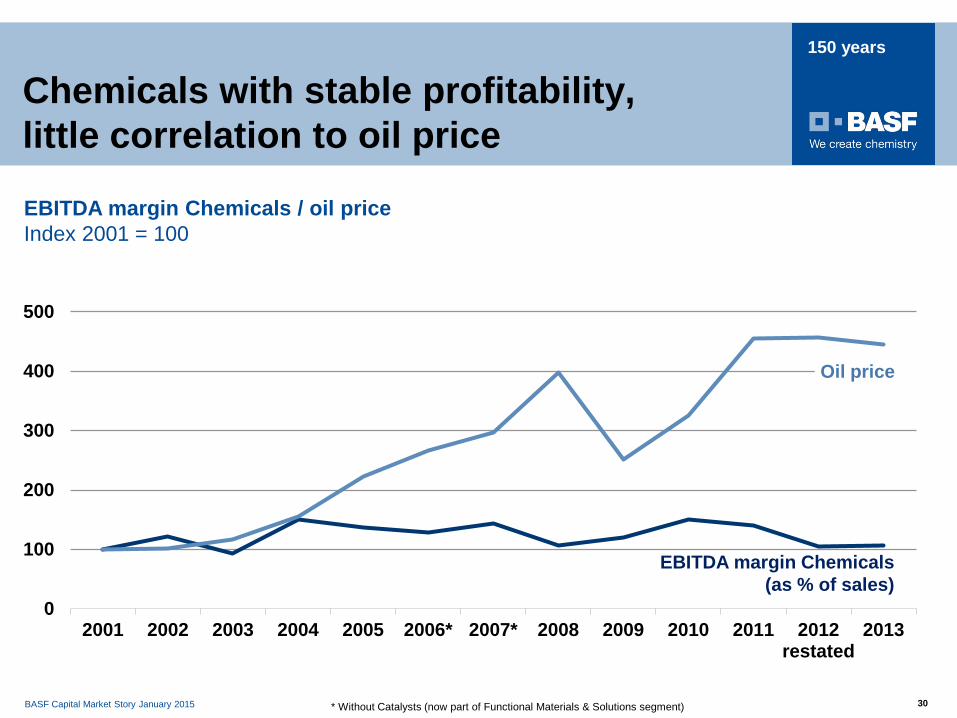

EBITDA margin Chemicals / oil price Index 2001 = 100

Chemicals with stable profitability, little correlation to oil price

EBITDA margin Chemicals (as % of sales)

Oil price

* Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Capital Market Story January 2015 31

150 years

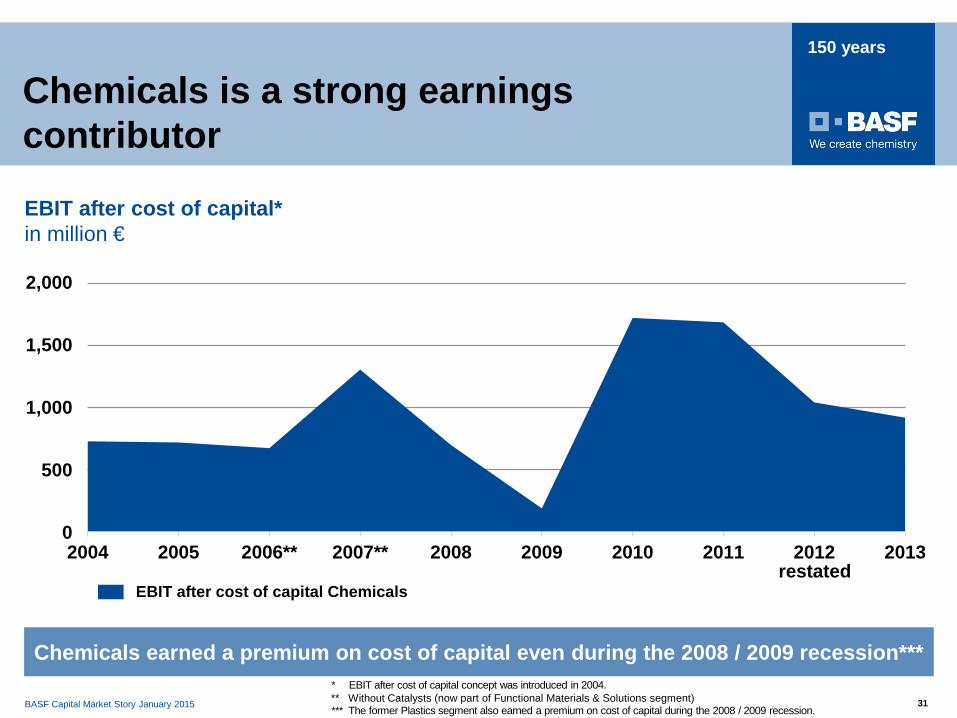

EBIT after cost of capital Chemicals

EBIT after cost of capital* in million €

restated

Chemicals earned a premium on cost of capital even during the 2008 / 2009 recession*** * EBIT after cost of capital concept was introduced in 2004.

*** The former Plastics segment also earned a premium on cost of capital during the 2008 / 2009 recession.

Chemicals is a strong earnings contributor

0

500

1.000

1.500

2.000

2004 2005 2006** 2007** 2008 2009 2010 2011 2012 2013

2,000

1,500

1,000

500

0

** Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Capital Market Story January 2015 32

150 years

2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012restated

2013

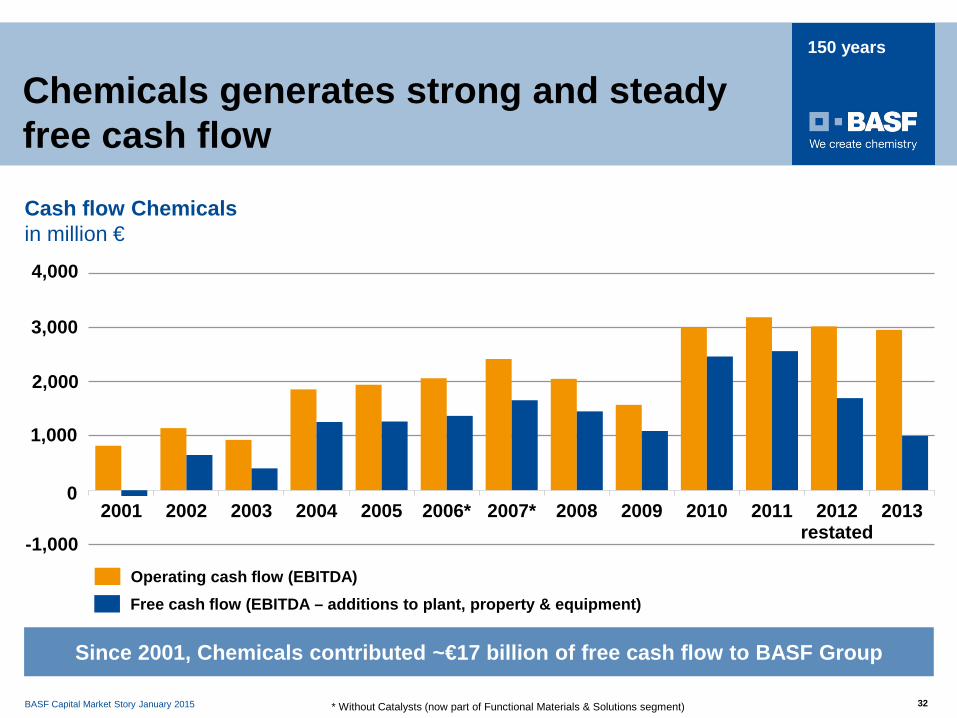

Chemicals generates strong and steady free cash flow

Cash flow Chemicals in million €

* Without Catalysts (now part of Functional Materials & Solutions segment)

Free cash flow (EBITDA – additions to plant, property & equipment)

Since 2001, Chemicals contributed ~€17 billion of free cash flow to BASF Group

Operating cash flow (EBITDA)

2,000

3,000

4,000

1,000

-1,000

0

BASF Capital Market Story January 2015 33

150 years

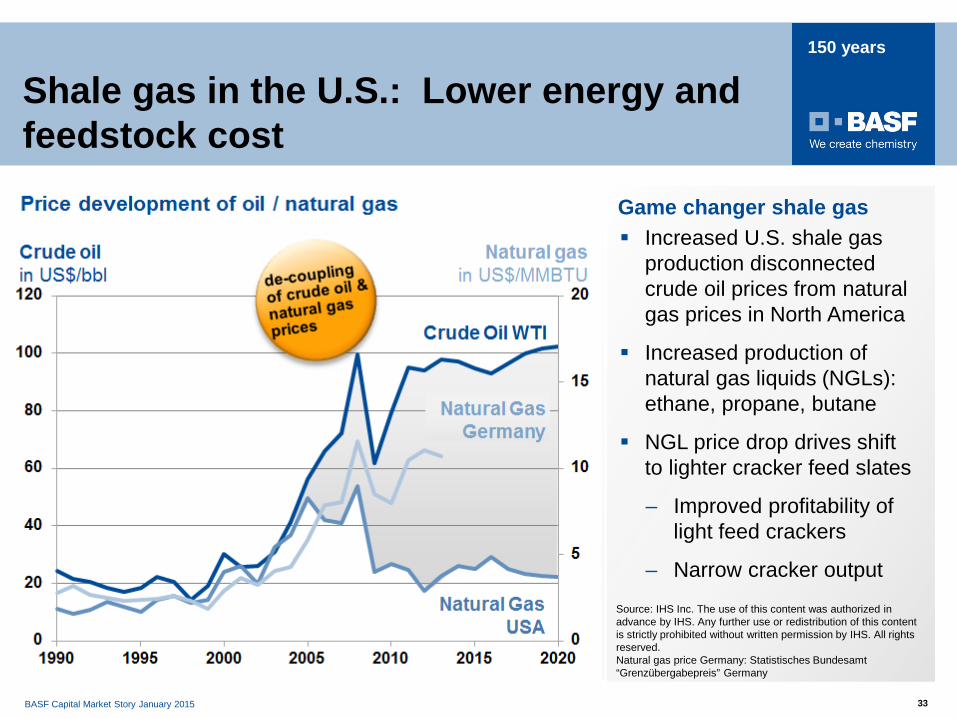

Shale gas in the U.S.: Lower energy and feedstock cost

Increased U.S. shale gas production disconnected crude oil prices from natural gas prices in North America

Increased production of natural gas liquids (NGLs): ethane, propane, butane

NGL price drop drives shift to lighter cracker feed slates

– Improved profitability of light feed crackers

– Narrow cracker output

Game changer shale gas

Source: IHS Inc. The use of this content was authorized in advance by IHS. Any further use or redistribution of this content is strictly prohibited without written permission by IHS. All rights reserved. Natural gas price Germany: Statistisches Bundesamt “Grenzübergabepreis” Germany

BASF Capital Market Story January 2015 34

150 years

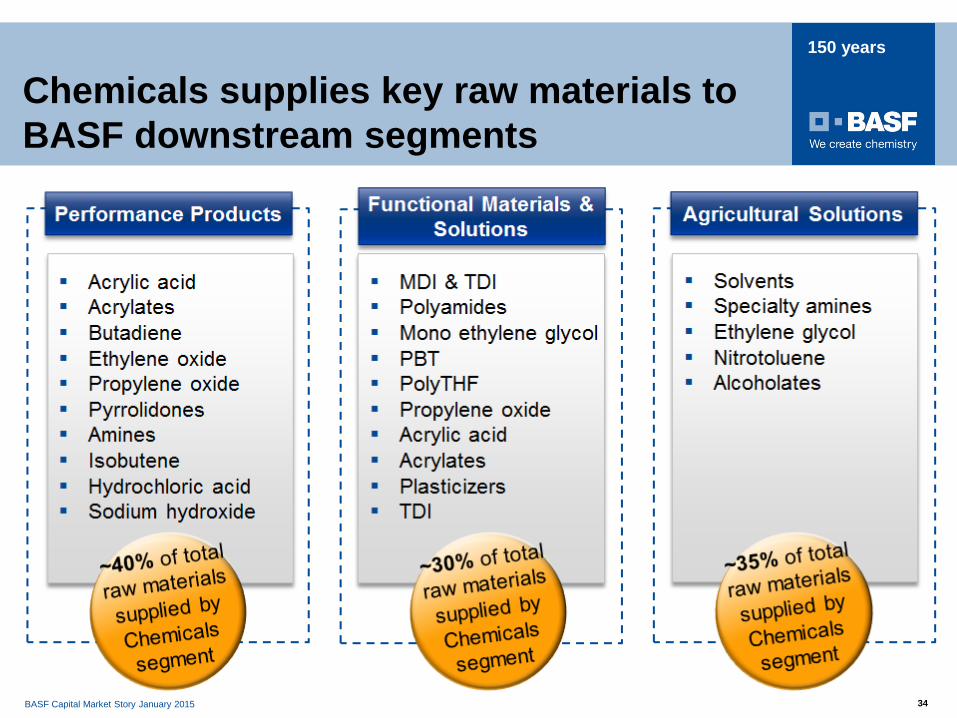

Chemicals supplies key raw materials to BASF downstream segments

BASF Capital Market Story January 2015 35

150 years

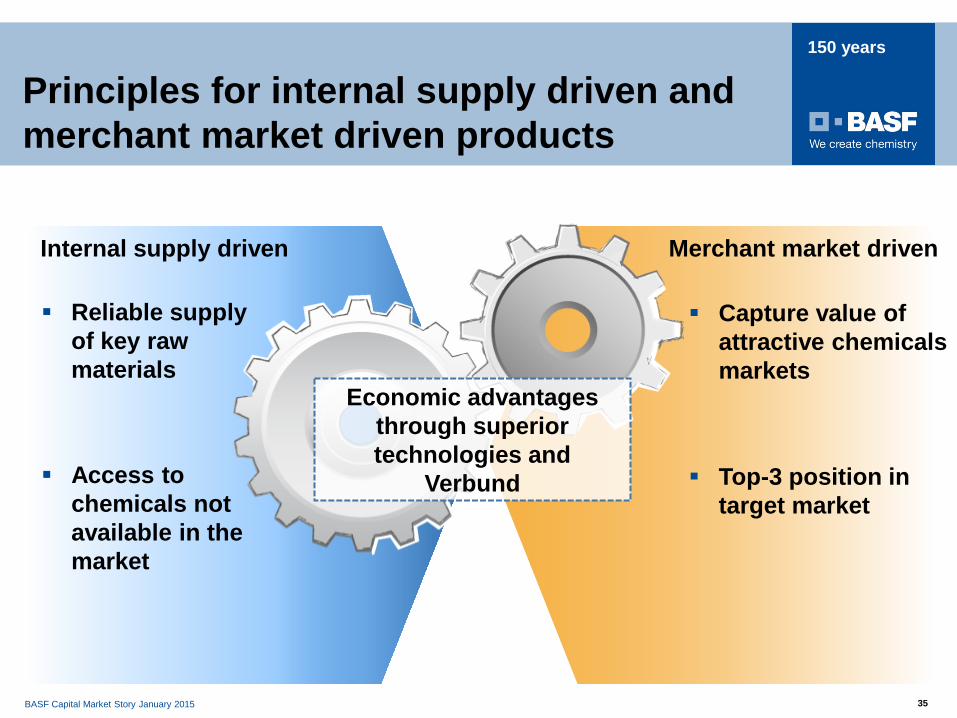

Principles for internal supply driven and merchant market driven products

Reliable supply of key raw materials

Access to chemicals not available in the market

Internal supply driven

Capture value of attractive chemicals markets

Top-3 position in target market

Merchant market driven

Economic advantages through superior technologies and

Verbund

BASF Capital Market Story January 2015 36

150 years

Merchant Market

Value chains of the BASF

Verbund

Ethylene Propylene Butadiene

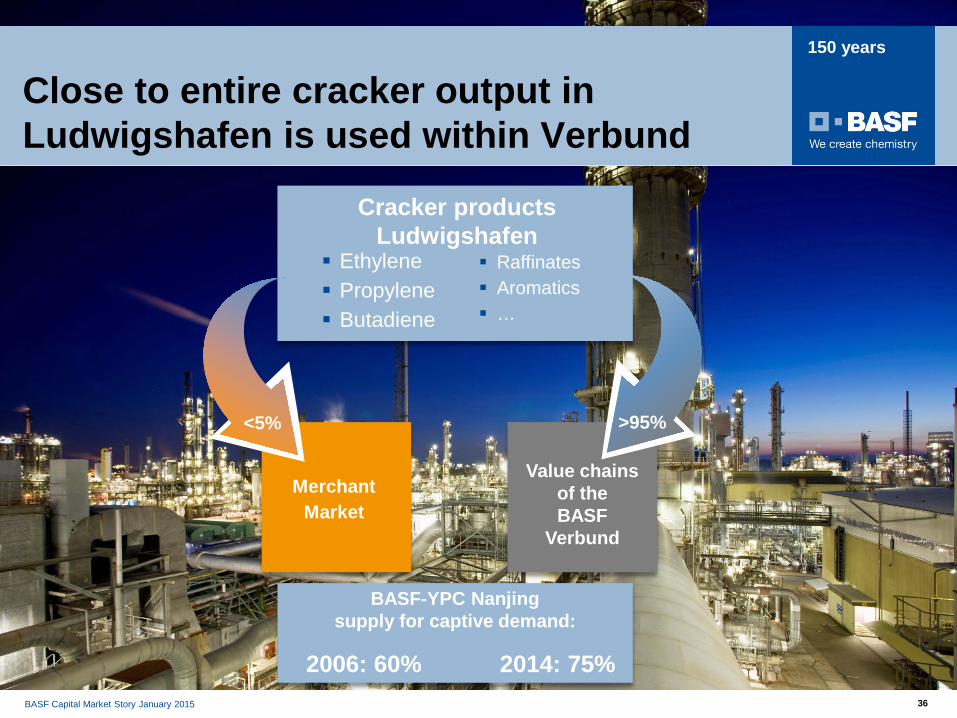

Close to entire cracker output in Ludwigshafen is used within Verbund

<5%

Raffinates Aromatics …

Cracker products Ludwigshafen

>95%

BASF-YPC Nanjing supply for captive demand:

2006: 60% 2014: 75% BASF SE, Ludwigshafen, Germany

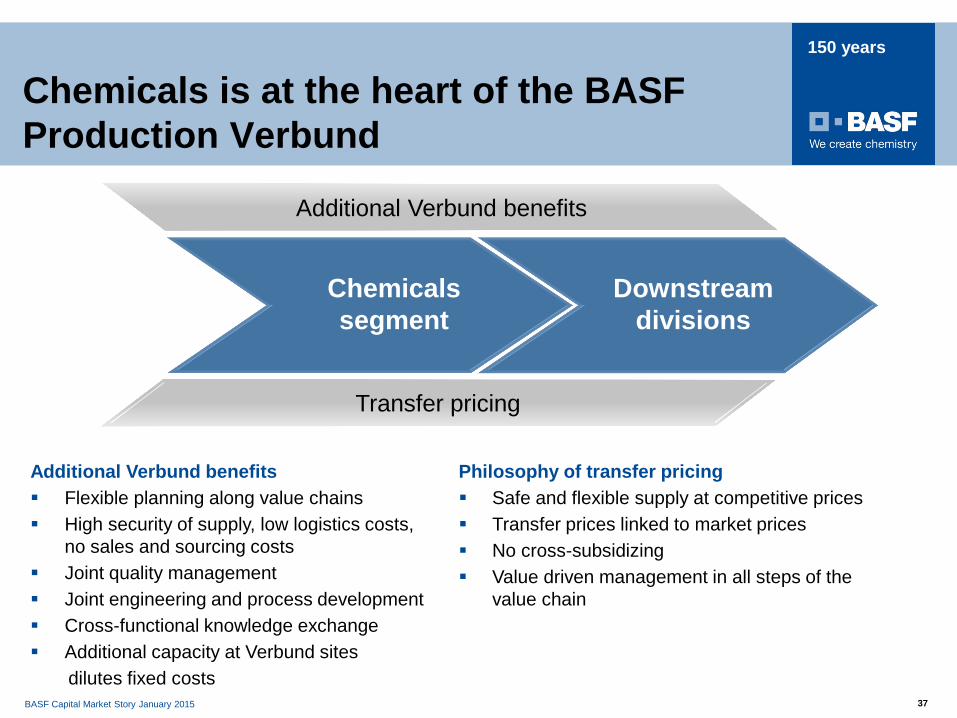

BASF Capital Market Story January 2015 37

150 years

Philosophy of transfer pricing Safe and flexible supply at competitive prices Transfer prices linked to market prices No cross-subsidizing Value driven management in all steps of the

value chain

Additional Verbund benefits Flexible planning along value chains High security of supply, low logistics costs,

no sales and sourcing costs Joint quality management Joint engineering and process development Cross-functional knowledge exchange Additional capacity at Verbund sites dilutes fixed costs

Chemicals is at the heart of the BASF Production Verbund

Additional Verbund benefits

Transfer pricing

Downstream divisions

Chemicals segment

BASF Capital Market Story January 2015 38

150 years

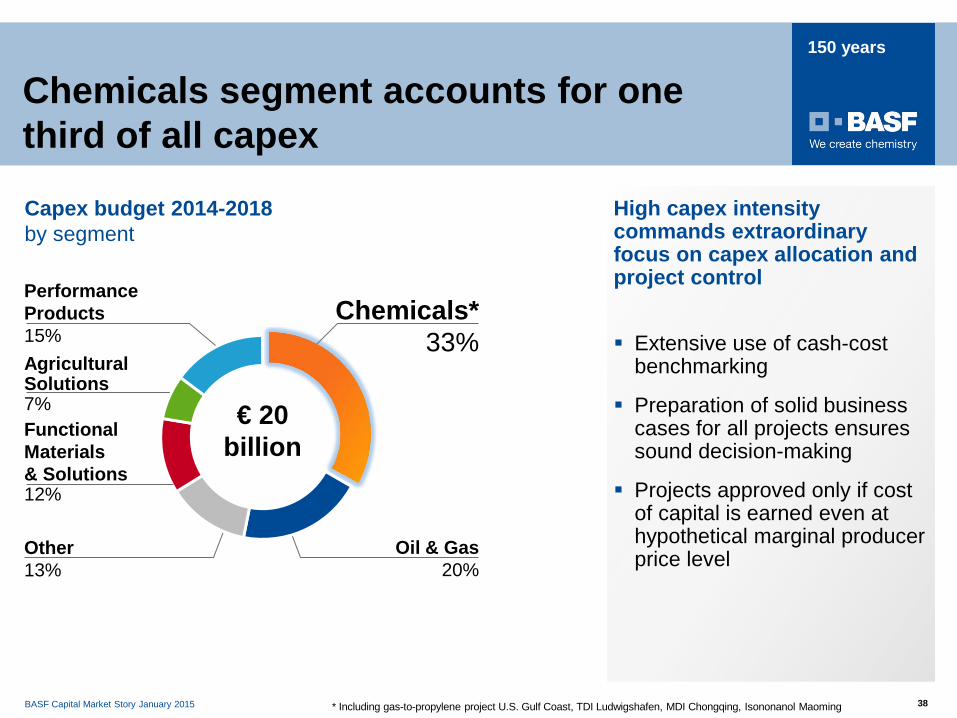

High capex intensity commands extraordinary focus on capex allocation and project control

Extensive use of cash-cost benchmarking

Preparation of solid business cases for all projects ensures sound decision-making

Projects approved only if cost of capital is earned even at hypothetical marginal producer price level

Chemicals segment accounts for one third of all capex

Capex budget 2014-2018 by segment

Other 13%

Chemicals* 33%

Performance Products 15%

€ 20 billion

Agricultural Solutions 7%

Oil & Gas 20%

Functional Materials & Solutions 12%

* Including gas-to-propylene project U.S. Gulf Coast, TDI Ludwigshafen, MDI Chongqing, Isononanol Maoming

BASF Capital Market Story January 2015 39

150 years

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012 2013 2014 2015 2016restated

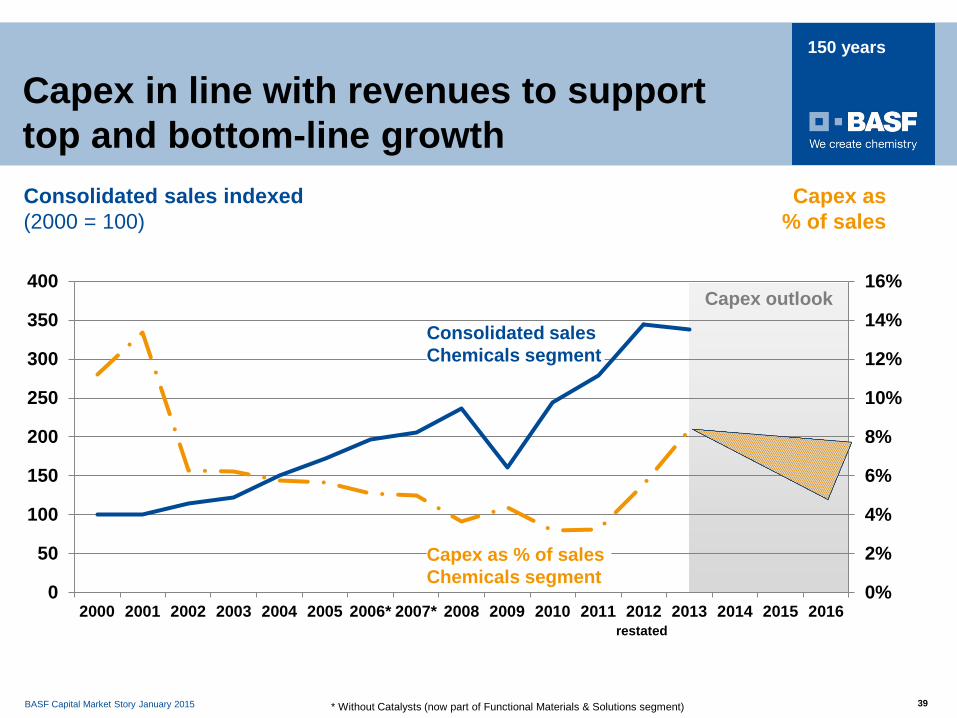

Consolidated sales indexed (2000 = 100)

Capex as % of sales

Capex in line with revenues to support top and bottom-line growth

Capex as % of sales Chemicals segment

Consolidated sales Chemicals segment

Capex outlook

* Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Capital Market Story January 2015 40

150 years

Major investment projects in the Chemicals segment

Ammonia and gas-to-propylene in USA*

MDI plant Chongqing, China

Acrylic acid complex Camacari, Brazil

TDI plant Ludwigshafen, Germany

* Under evaluation

Isononanol plant Maoming, China

Polyamides plant Caojing, China

BASF Capital Market Story January 2015 41

150 years

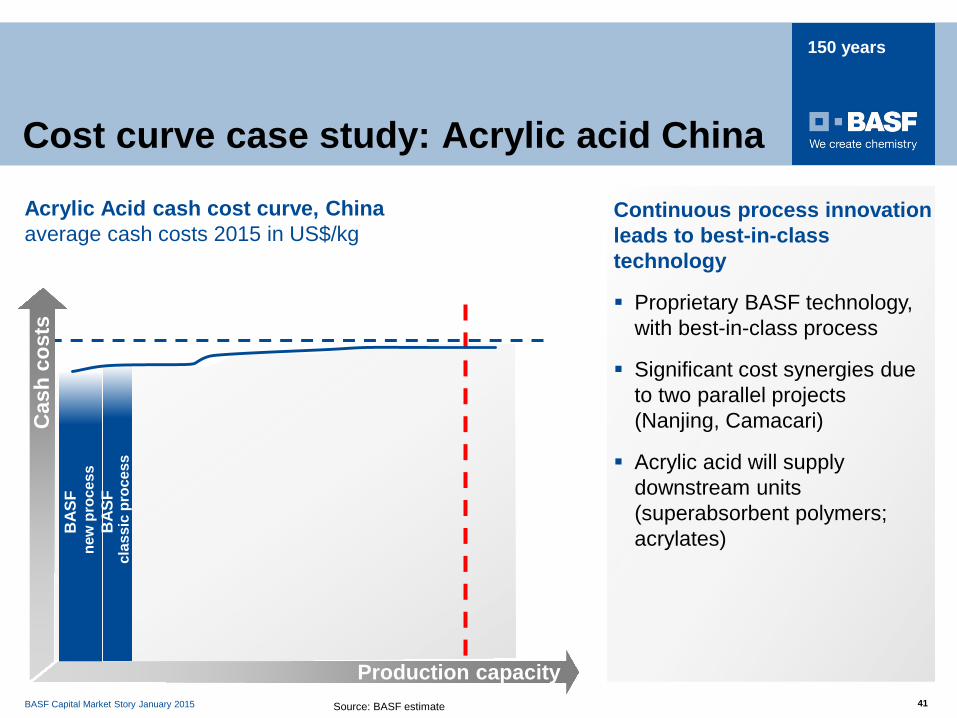

Continuous process innovation leads to best-in-class technology

Proprietary BASF technology, with best-in-class process

Significant cost synergies due to two parallel projects (Nanjing, Camacari)

Acrylic acid will supply downstream units (superabsorbent polymers; acrylates)

Cost curve case study: Acrylic acid China

Acrylic Acid cash cost curve, China average cash costs 2015 in US$/kg

Cas

h co

sts

BAS

F

clas

sic

proc

ess

BAS

F

new

pro

cess

Source: BASF estimate

Production capacity

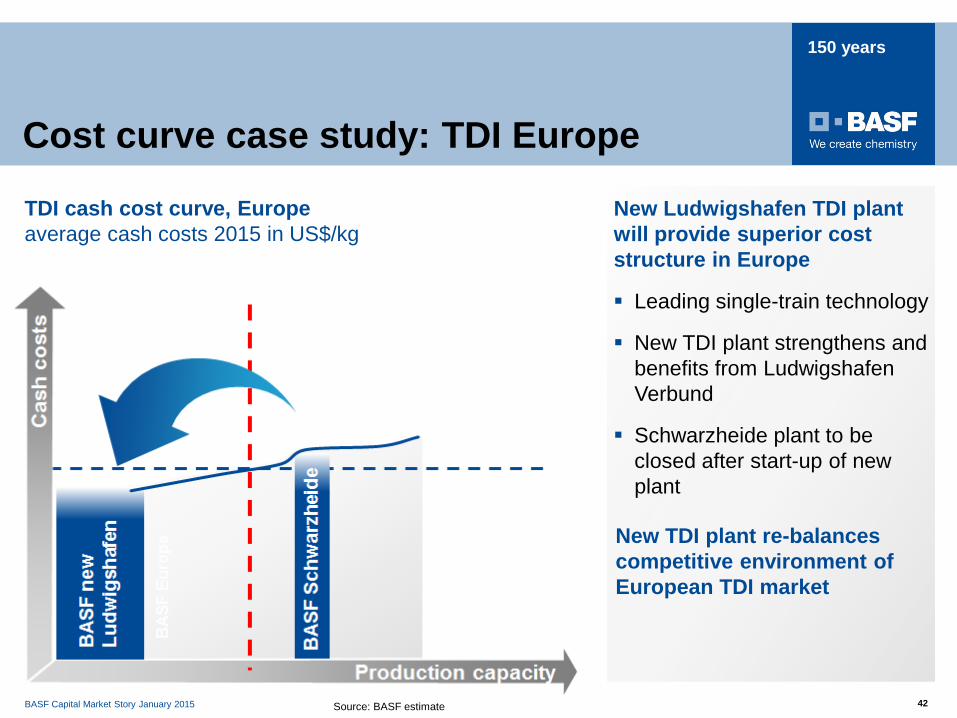

BASF Capital Market Story January 2015 42

150 years

Leading single-train technology

New TDI plant strengthens and benefits from Ludwigshafen Verbund

Schwarzheide plant to be closed after start-up of new plant

New TDI plant re-balances competitive environment of European TDI market

Source: BASF estimate

TDI cash cost curve, Europe average cash costs 2015 in US$/kg

New Ludwigshafen TDI plant will provide superior cost structure in Europe

Cost curve case study: TDI Europe

BASF Capital Market Story January 2015 43

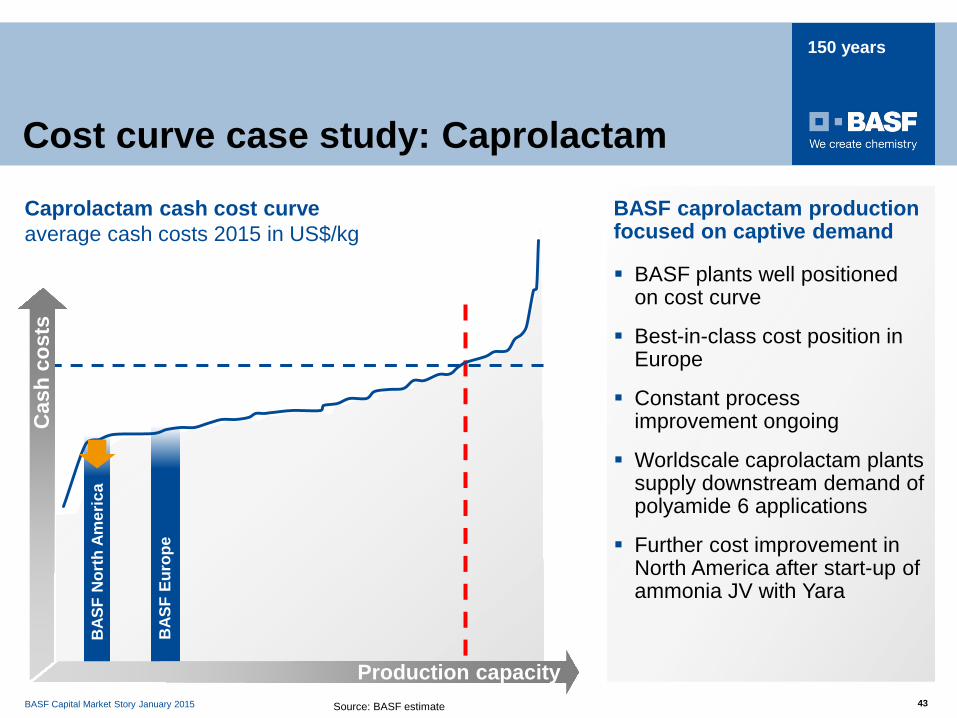

150 years

BASF caprolactam production focused on captive demand

BASF plants well positioned on cost curve

Best-in-class cost position in Europe

Constant process improvement ongoing

Worldscale caprolactam plants supply downstream demand of polyamide 6 applications

Further cost improvement in North America after start-up of ammonia JV with Yara

Caprolactam cash cost curve average cash costs 2015 in US$/kg

BAS

F N

orth

Am

eric

a

BAS

F Eu

rope

Production capacity

Cas

h co

sts

Cost curve case study: Caprolactam

Source: BASF estimate

BASF Capital Market Story January 2015 44

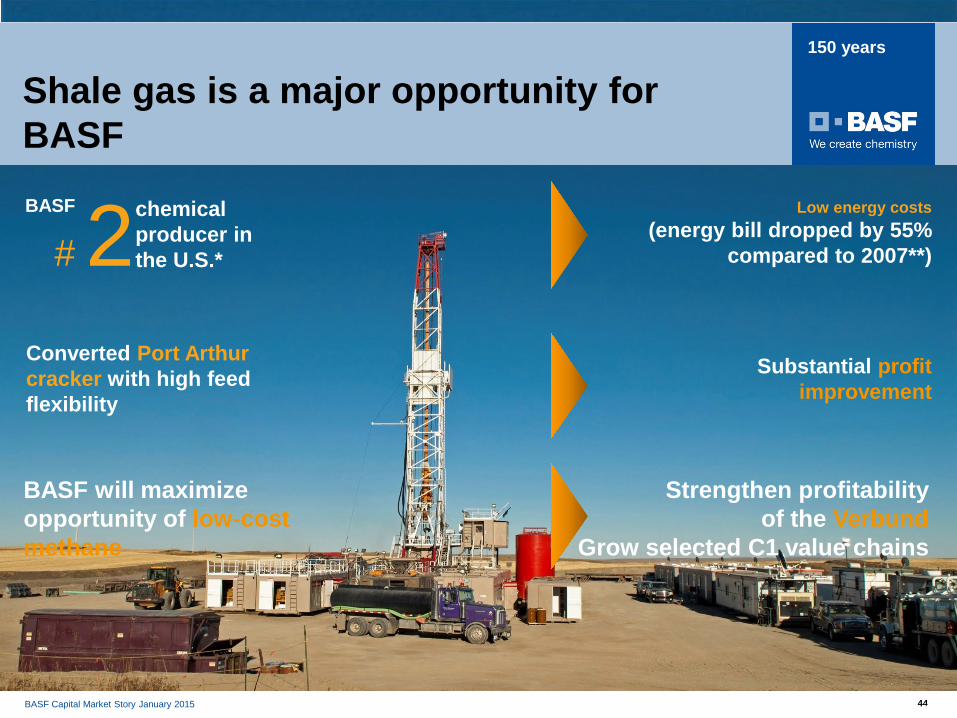

150 years

Converted Port Arthur cracker with high feed flexibility

# 2 chemical producer in the U.S.*

BASF

Shale gas is a major opportunity for BASF

Low energy costs (energy bill dropped by 55%

compared to 2007**)

Substantial profit improvement

BASF will maximize opportunity of low-cost methane

Strengthen profitability of the Verbund

Grow selected C1 value chains

* Based on sales to local customers ** U.S. data only, normalized costs for natural gas for energy production 44

BASF Capital Market Story January 2015 45

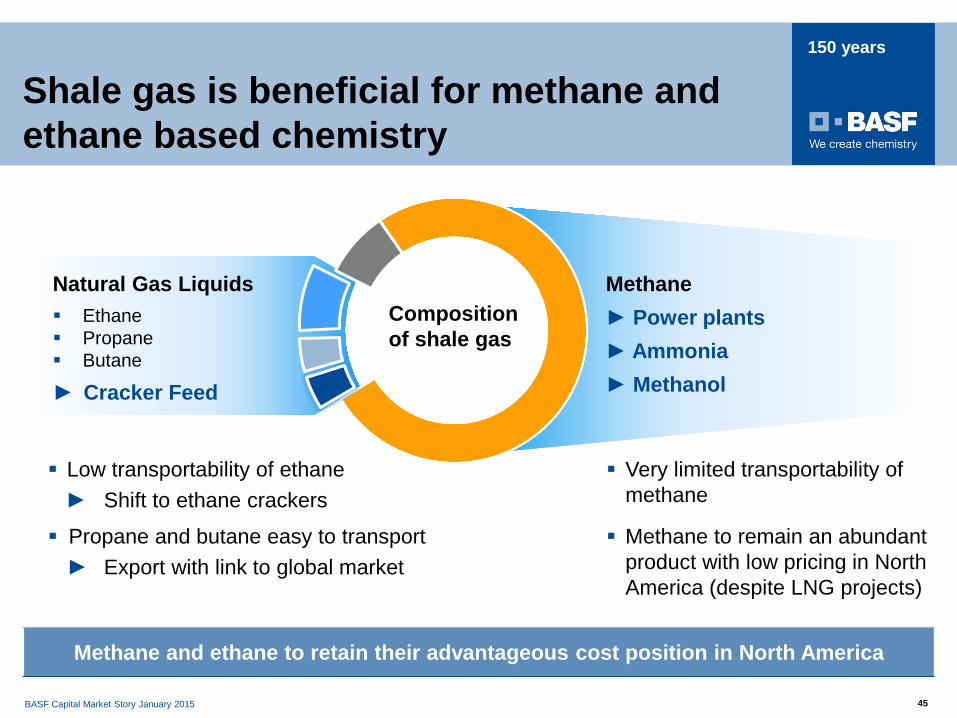

150 years

Natural Gas Liquids Ethane Propane Butane

► Cracker Feed

Shale gas is beneficial for methane and ethane based chemistry

Methane and ethane to retain their advantageous cost position in North America

Low transportability of ethane ► Shift to ethane crackers

Propane and butane easy to transport ► Export with link to global market

Very limited transportability of methane

Methane to remain an abundant product with low pricing in North America (despite LNG projects)

Methane ► Power plants ► Ammonia ► Methanol

Composition of shale gas

BASF Capital Market Story January 2015 46

150 years

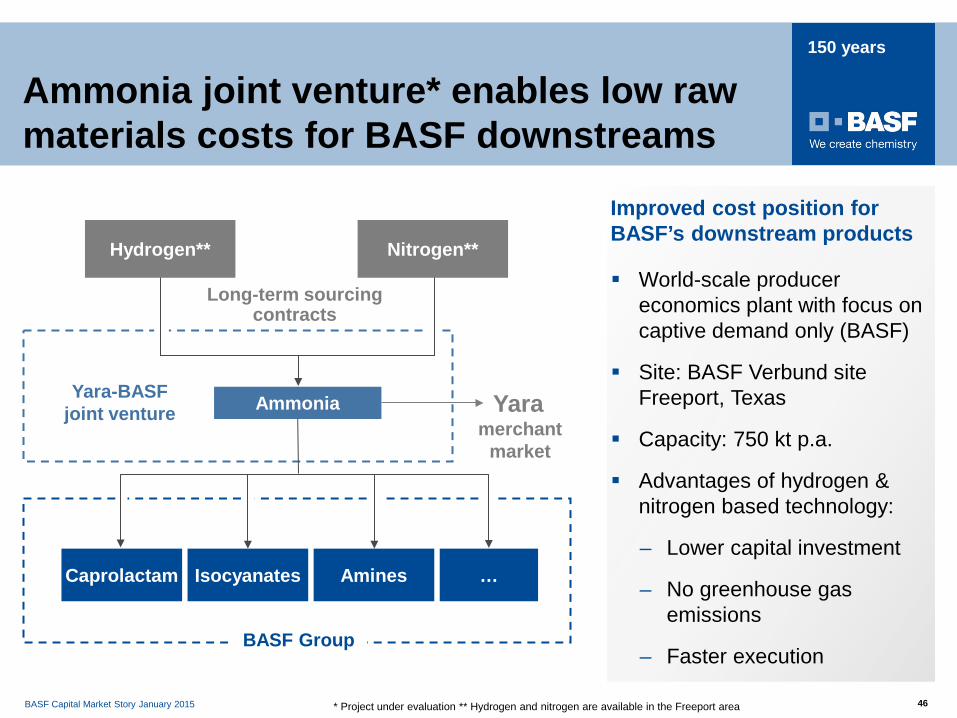

Ammonia joint venture* enables low raw materials costs for BASF downstreams

World-scale producer economics plant with focus on captive demand only (BASF)

Site: BASF Verbund site Freeport, Texas

Capacity: 750 kt p.a.

Advantages of hydrogen & nitrogen based technology:

– Lower capital investment

– No greenhouse gas emissions

– Faster execution

Improved cost position for BASF’s downstream products

Caprolactam Isocyanates Amines

Yara

…

Long-term sourcing contracts

Yara-BASF joint venture

BASF Group

Ammonia

Nitrogen** Hydrogen**

merchant market

* Project under evaluation ** Hydrogen and nitrogen are available in the Freeport area

BASF Capital Market Story January 2015 47

150 years

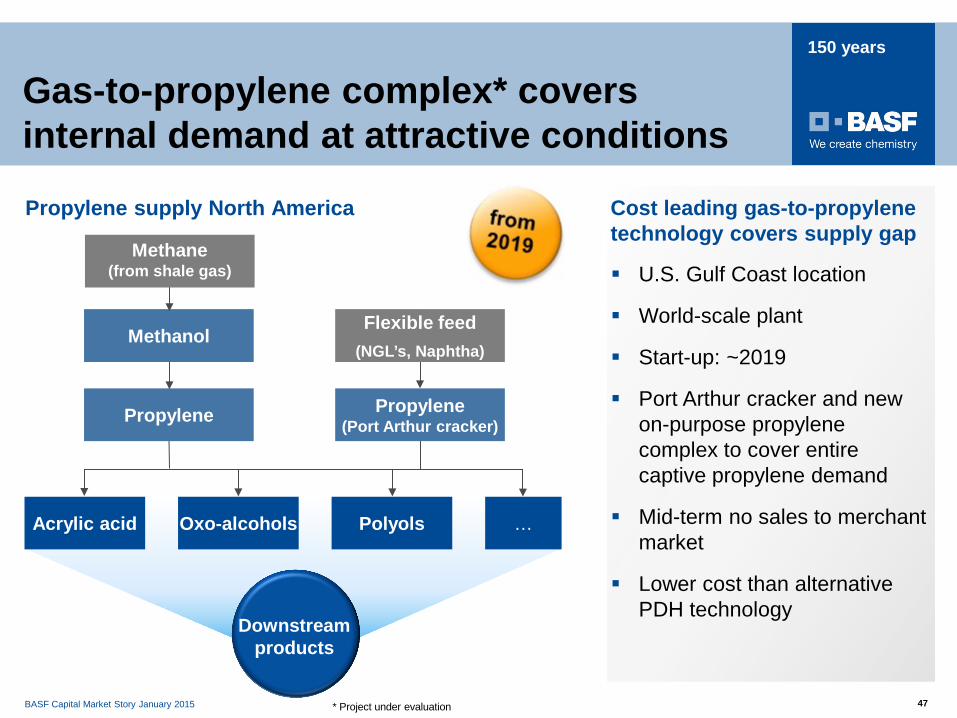

Gas-to-propylene complex* covers internal demand at attractive conditions

U.S. Gulf Coast location

World-scale plant

Start-up: ~2019

Port Arthur cracker and new on-purpose propylene complex to cover entire captive propylene demand

Mid-term no sales to merchant market

Lower cost than alternative PDH technology

Cost leading gas-to-propylene technology covers supply gap

Propylene supply North America

Acrylic acid Oxo-alcohols Polyols …

Propylene Propylene (Port Arthur cracker)

Downstream products

Methanol

Methane (from shale gas)

Flexible feed (NGL’s, Naphtha)

* Project under evaluation

BASF Capital Market Story January 2015 48

Appendix II:

Oil & Gas

BASF Capital Market Story January 2015 49

150 years

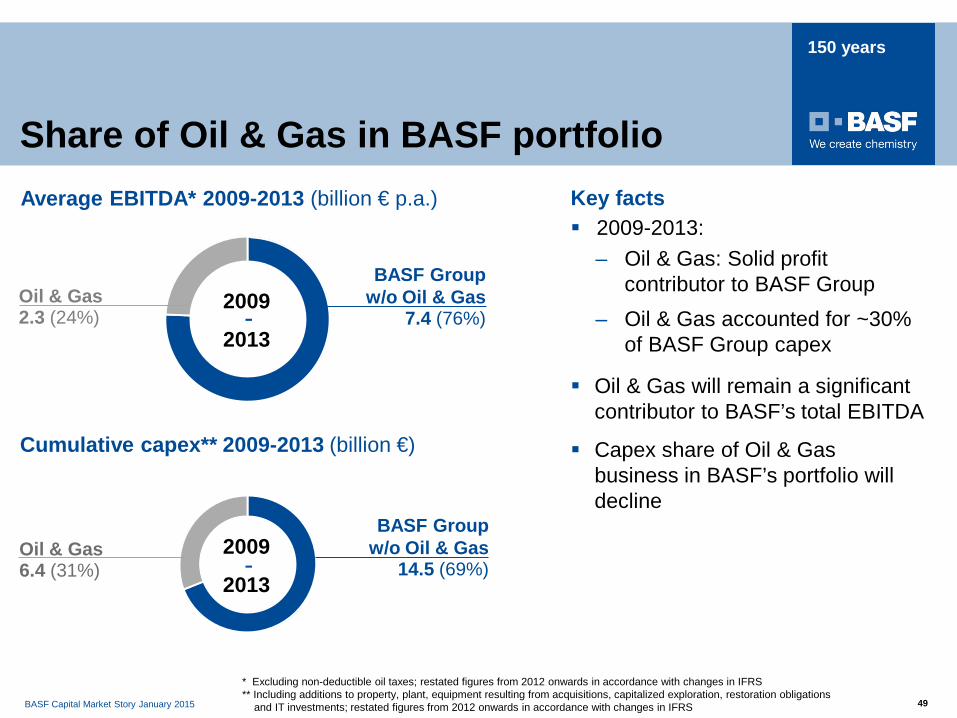

2009

2013

Cumulative capex** 2009-2013 (billion €)

BASF Group w/o Oil & Gas

7.4 (76%)

BASF Group w/o Oil & Gas

14.5 (69%)

Oil & Gas 2.3 (24%)

Oil & Gas 6.4 (31%)

2009

2013 -

-

Average EBITDA* 2009-2013 (billion € p.a.)

* Excluding non-deductible oil taxes; restated figures from 2012 onwards in accordance with changes in IFRS ** Including additions to property, plant, equipment resulting from acquisitions, capitalized exploration, restoration obligations and IT investments; restated figures from 2012 onwards in accordance with changes in IFRS

2009-2013: – Oil & Gas: Solid profit

contributor to BASF Group – Oil & Gas accounted for ~30%

of BASF Group capex

Oil & Gas will remain a significant contributor to BASF’s total EBITDA

Capex share of Oil & Gas business in BASF’s portfolio will decline

Key facts

Share of Oil & Gas in BASF portfolio

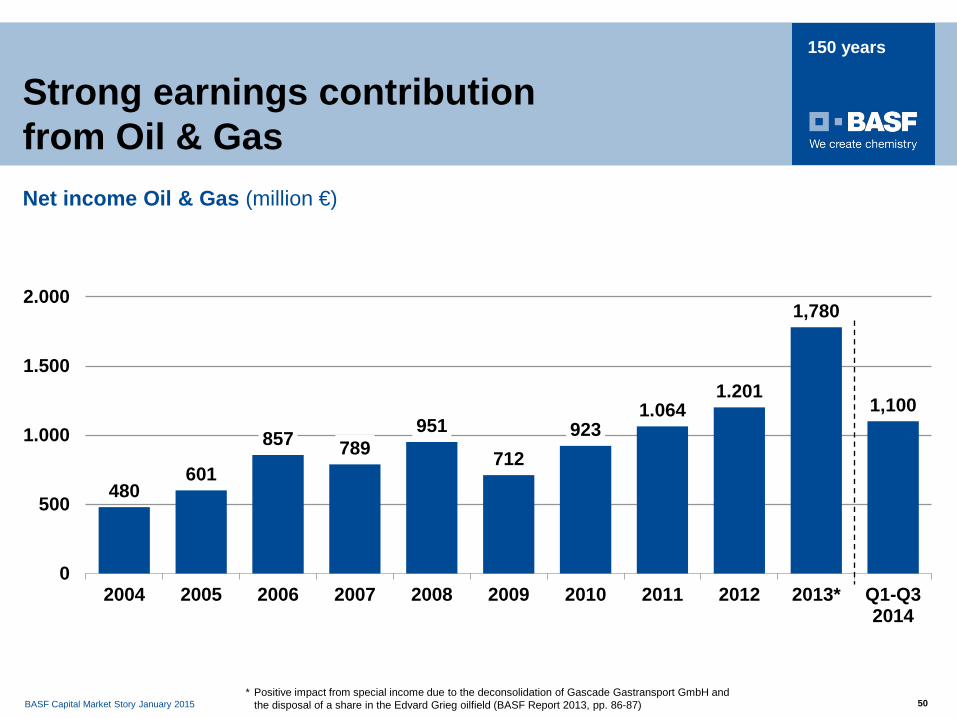

BASF Capital Market Story January 2015 50

150 years

Strong earnings contribution from Oil & Gas

* Positive impact from special income due to the deconsolidation of Gascade Gastransport GmbH and the disposal of a share in the Edvard Grieg oilfield (BASF Report 2013, pp. 86-87)

480 601

857 789 951

712 923

1.064 1.201

1,780

1,100

0

500

1.000

1.500

2.000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013* Q1-Q32014

Net income Oil & Gas (million €)

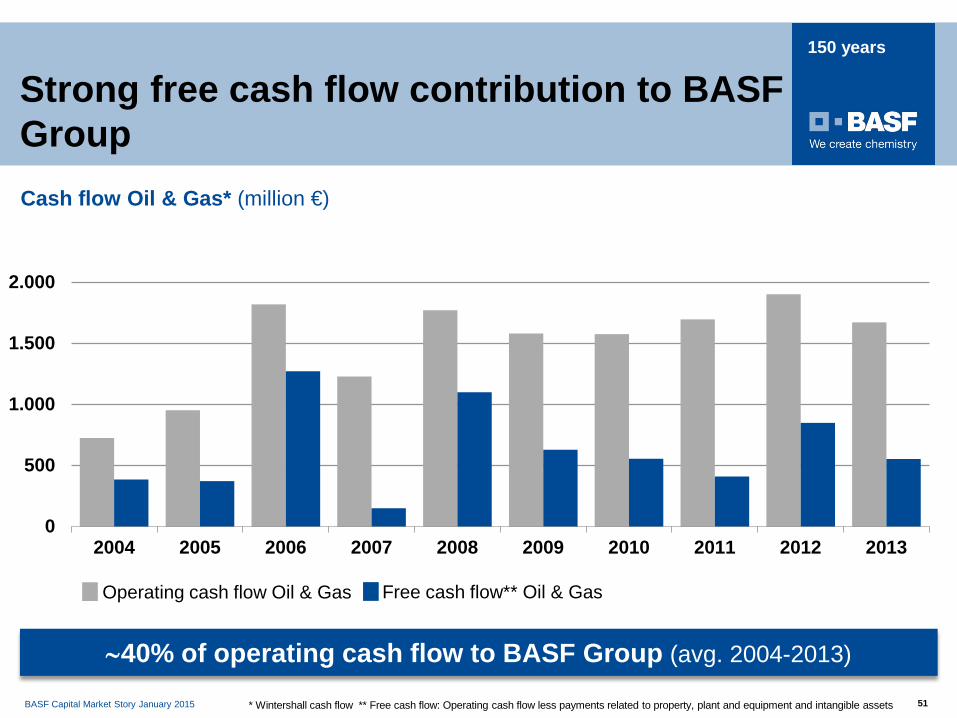

BASF Capital Market Story January 2015 51

150 years

Strong free cash flow contribution to BASF Group

Cash flow Oil & Gas* (million €)

0

500

1.000

1.500

2.000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Operating cash flow Oil & Gas

* Wintershall cash flow ** Free cash flow: Operating cash flow less payments related to property, plant and equipment and intangible assets

Free cash flow** Oil & Gas

∼40% of operating cash flow to BASF Group (avg. 2004-2013)

BASF Capital Market Story January 2015 52

150 years

Oil & Gas value chain

Upstream Downstream

Exploration / Development / Production Transport Storage / Trading

Midstream Upstream

Oil & Gas – Focus on upstream activities

BASF Capital Market Story January 2015 53

150 years

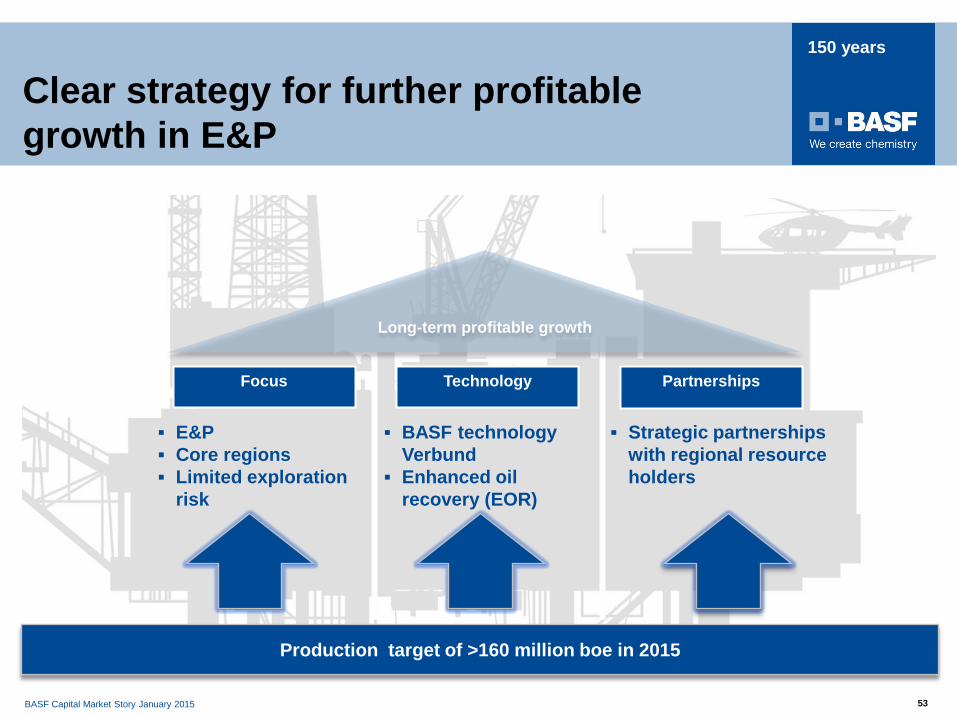

Clear strategy for further profitable growth in E&P

Production target of >160 million boe in 2015

Focus Technology Partnerships

BASF technology Verbund

Enhanced oil recovery (EOR)

Strategic partnerships with regional resource holders

Long-term profitable growth

E&P Core regions Limited exploration

risk

BASF Capital Market Story January 2015 54

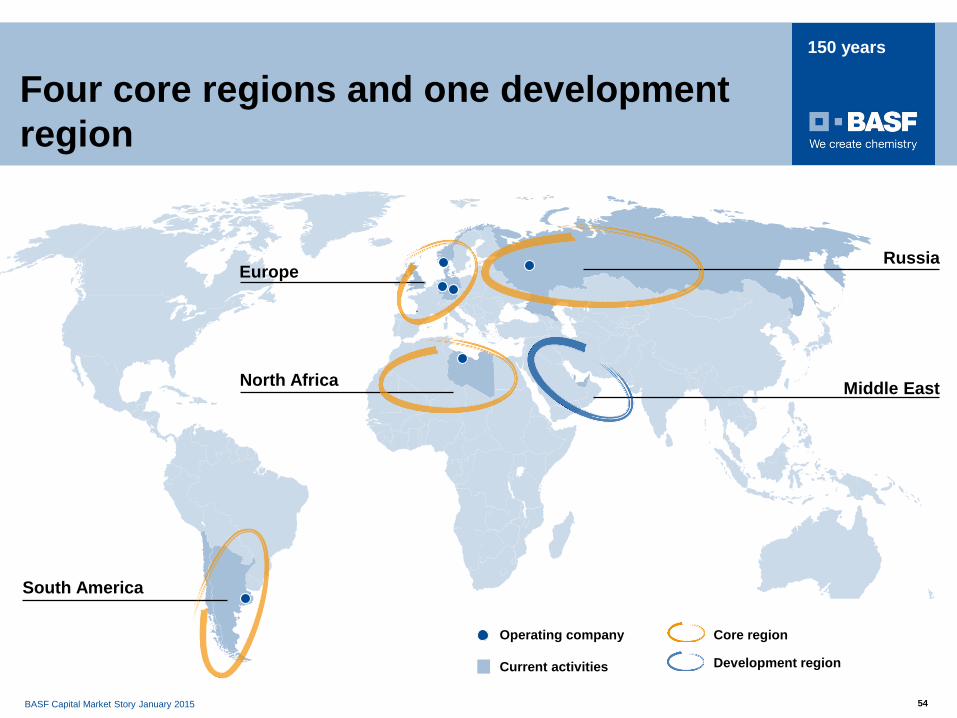

150 years

Four core regions and one development region

North Africa

Europe Russia

Middle East

South America

Core region

Development region

Operating company

Current activities

.

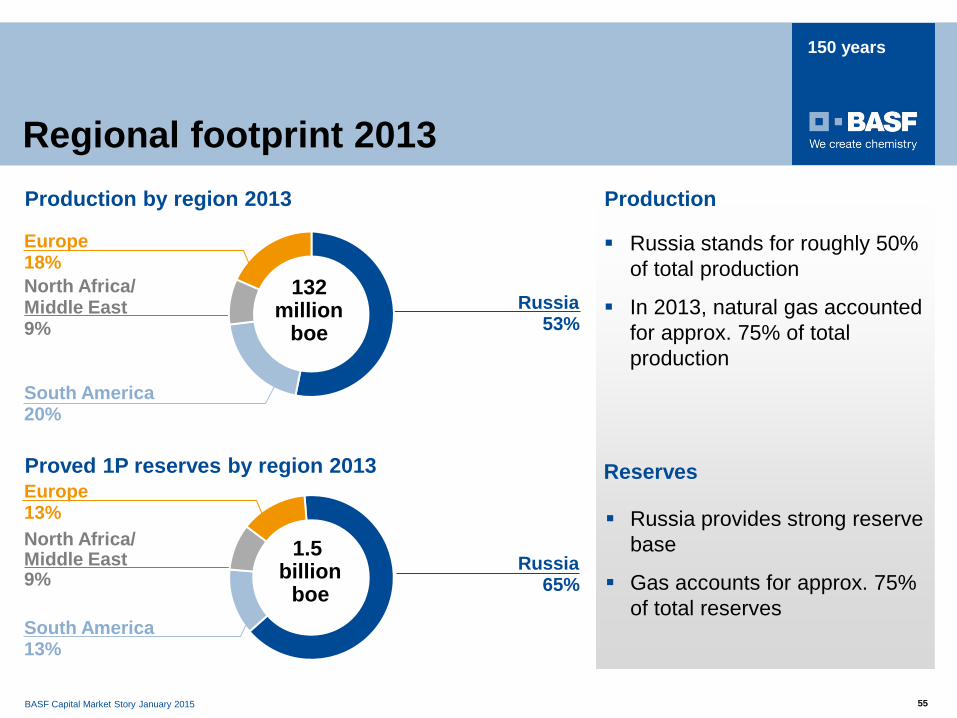

BASF Capital Market Story January 2015 55

150 years

Regional footprint 2013

Russia stands for roughly 50% of total production

In 2013, natural gas accounted for approx. 75% of total production

Production

Russia provides strong reserve base

Gas accounts for approx. 75% of total reserves

Reserves

Russia 53%

North Africa/ Middle East 9%

Europe 18%

South America 20%

132 million

boe

North Africa/ Middle East 9%

Europe 13%

South America 13%

Proved 1P reserves by region 2013

1.5 billion

boe Russia

65%

Production by region 2013

BASF Capital Market Story January 2015 56

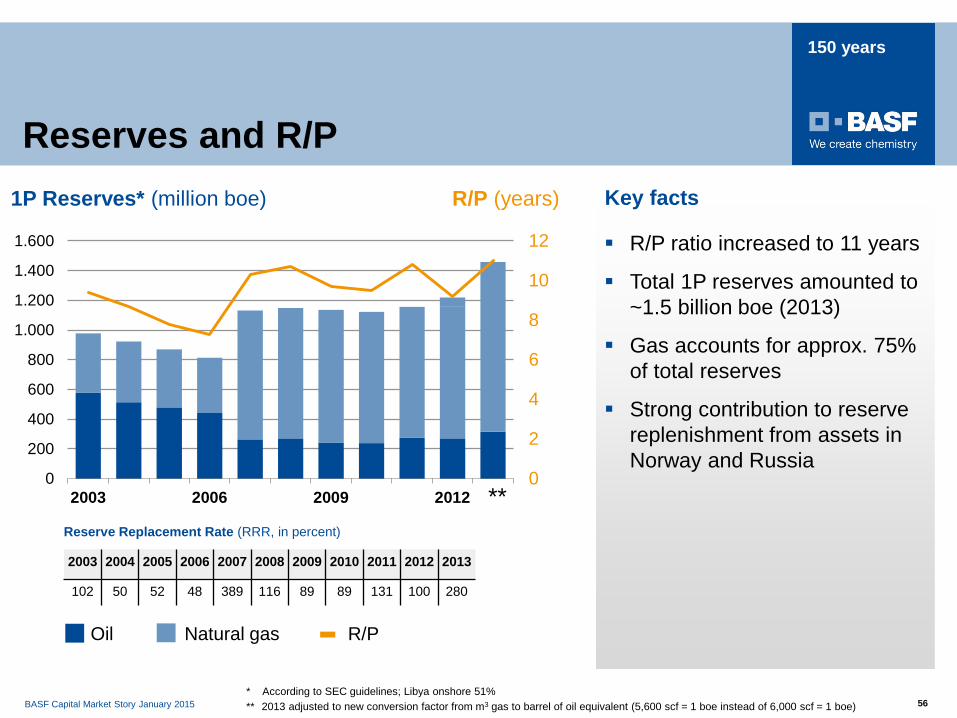

150 years

R/P ratio increased to 11 years

Total 1P reserves amounted to ~1.5 billion boe (2013)

Gas accounts for approx. 75% of total reserves

Strong contribution to reserve replenishment from assets in Norway and Russia

Key facts 1P Reserves* (million boe) R/P (years)

Oil Natural gas R/P

* According to SEC guidelines; Libya onshore 51%

Reserve Replacement Rate (RRR, in percent)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

102 50 52 48 389 116 89 89 131 100 280

** 2013 adjusted to new conversion factor from m3 gas to barrel of oil equivalent (5,600 scf = 1 boe instead of 6,000 scf = 1 boe)

0

2

4

6

8

10

12

0

200

400

600

800

1.000

1.200

1.400

1.600

2003 2006 2009 2012 **

Reserves and R/P

BASF Capital Market Story January 2015 57

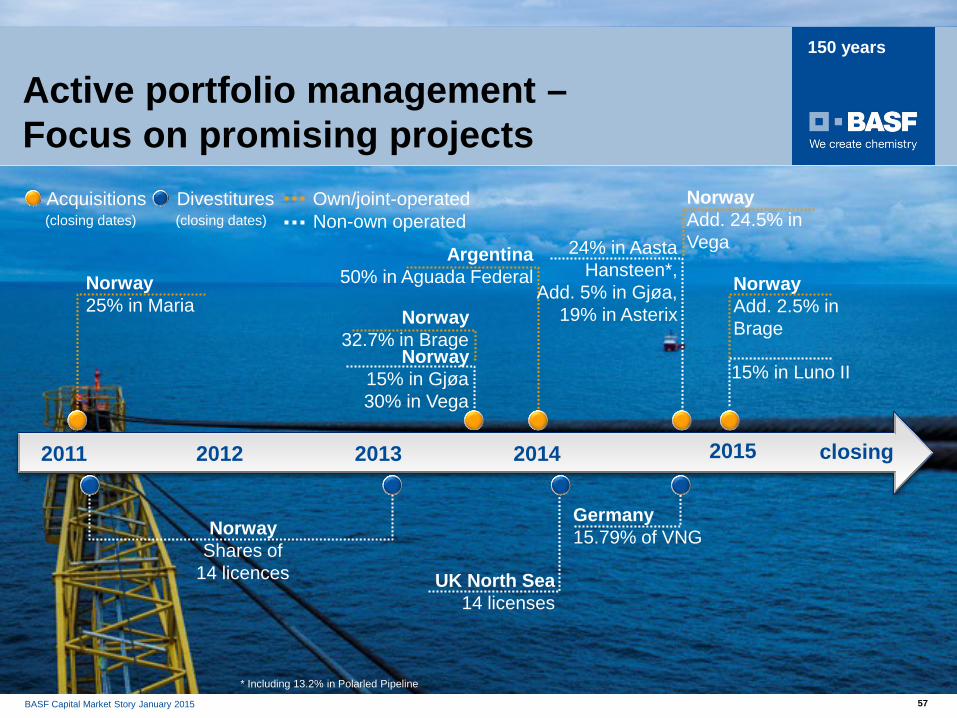

150 years

Norway 25% in Maria Norway

32.7% in Brage

Active portfolio management – Focus on promising projects

UK North Sea 14 licenses

15% in Luno II

Norway Add. 2.5% in Brage

Argentina 50% in Aguada Federal

Germany 15.79% of VNG

Acquisitions

57

Norway 15% in Gjøa 30% in Vega

(closing dates) Own/joint-operated Divestitures

(closing dates) Norway Add. 24.5% in Vega 24% in Aasta

Hansteen*, Add. 5% in Gjøa,

19% in Asterix

Non-own operated

Norway Shares of

14 licences

* Including 13.2% in Polarled Pipeline

2011 2013 2012 2014 2015 closing

BASF Capital Market Story January 2015 58

150 years

Recent transaction with Statoil Strategic rationale of the transaction

* Pipeline project will provide route for produced gas from Aasta Hansteen field to onshore processing facilities

To strengthen Wintershall’s position in Norway by increasing participation in producing oil and gas fields

To participate jointly with Statoil in promising development project “Aasta Hansteen”

To get access to additional reserves and resources (2P/2C) of ~170 million boe and assets with material exploration perspectivity

To increase production of Wintershall Norge from currently around 40,000 boe/day to about 60,000 boe/day

To expand position as field operator in Norway and to gain experience with subsea operations by taking over operatorship in the Vega field*

To significantly increase Wintershall’s EBIT and future operating cash flow

BASF Capital Market Story January 2015 59

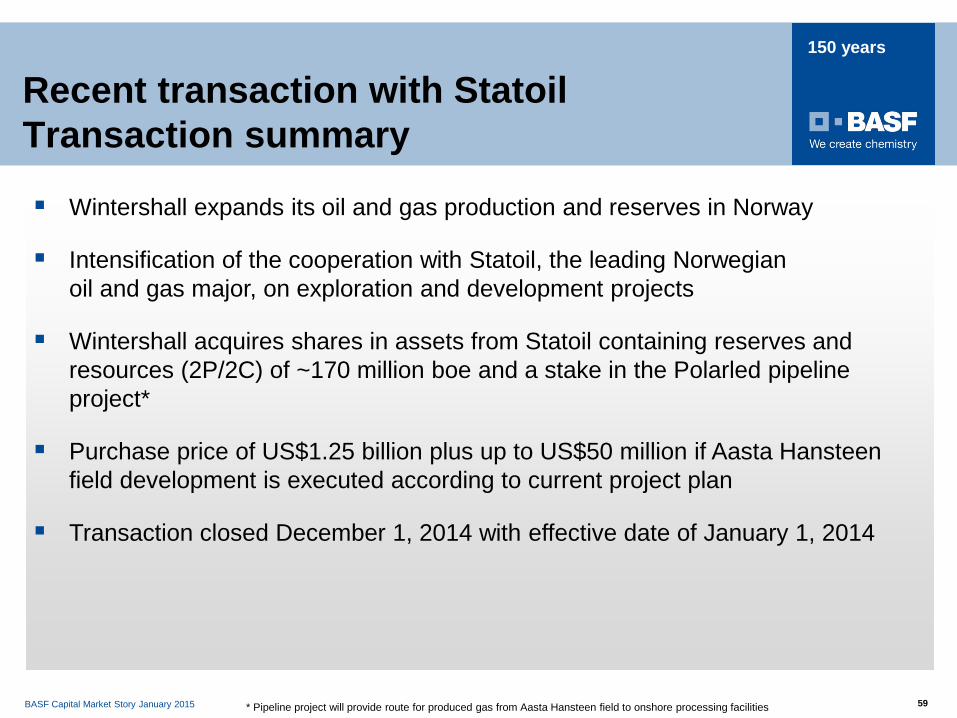

150 years

Wintershall expands its oil and gas production and reserves in Norway

Intensification of the cooperation with Statoil, the leading Norwegian oil and gas major, on exploration and development projects

Wintershall acquires shares in assets from Statoil containing reserves and resources (2P/2C) of ~170 million boe and a stake in the Polarled pipeline project*

Purchase price of US$1.25 billion plus up to US$50 million if Aasta Hansteen field development is executed according to current project plan

Transaction closed December 1, 2014 with effective date of January 1, 2014

Recent transaction with Statoil Transaction summary

* Pipeline project will provide route for produced gas from Aasta Hansteen field to onshore processing facilities

BASF Capital Market Story January 2015 60

150 years

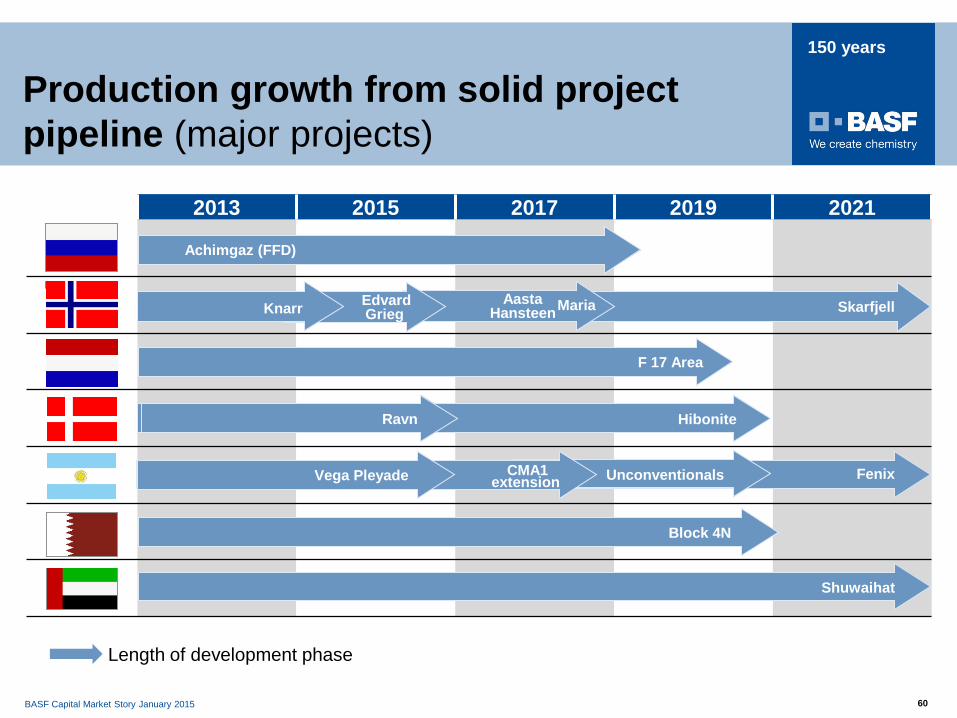

Production growth from solid project pipeline (major projects)

2013 2015 2017 2019 2021

Norway

Length of development phase

Skarfjell

Achimgaz (FFD)

Block 4N

Shuwaihat

F 17 Area

Hibonite Ravn

Fenix Unconventionals CMA1 extension Vega Pleyade

Maria Aasta Hansteen

Edvard Grieg Knarr

BASF Capital Market Story January 2015 61

150 years

150 years