From Basel 2 to Basel 3 Sergio Lugaresi, Public Affairs Milan, October 26, 2012.

Upload

george-lekatisCategory

view

219download

0

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 1/218

1

Basel iii Compliance Professionals Association(BiiiCPA) 1200 G Street NW Suite 800 Washington, DC

20005-6705 USA Tel: 202-449-9750 Web: www.basel-iii-association.com

Dear Member,

Today we will start from the disclosure requirements on thecomposition of banks' capital.

Composition of capital disclosure requirements - Rulestext June 2012

The Basel Committee onBanking Supervision haspublished a set of disclosurerequirements on thecomposition of banks' capital.

During the financial crisis, marketparticipants and supervisors werehampered in their efforts toundertake detailed assessments of

banks' capital positions and makecross-jurisdictional comparisons.

The source of this difficulty wasinsufficiently detailed disclosureby banks and a lack of consistency in reporting betweenbanks and across jurisdictions.

This lack of clarity may have

contributed to uncertainty duringthe financial crisis.

The disclosure requirements aim to improve market disciplinethrough enhancing both transparency and comparability.Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 2/218

2

Composition of capital disclosurerequirements Introduction

During the financial crisis, many market participants andsupervisors attempted to undertake detailed assessments of the

capital positions of banks and comparisons of their capitalpositions on a cross jurisdictional basis.

The level of detail of the disclosure and the lack of consistency inthe way that it was reported typically made this task difficult and

often made it impossible to do with any accuracy.

It is often suggested that lack of clarity on the quality of

capital contributed to uncertainty during the financialcrisis.

Furthermore, the interventions carried out by the authoritiesmay have been more effective if capital positions of the banks

were more transparent.

To ensure that banks back their risk exposures with a high qualitycapital base, Basel I I I introduced a set of detailed requirements to

raise the quality and consistency of capital in the banking sector.

In addition, Basel I I I established certain high level disclosurerequirements to improve transparency of regulatory capital and

enhance market discipline and noted that more detailed Pillar 3disclosure requirements would be forthcoming.

This document sets out these detailed requirements.

To enable market participants to compare the capital adequacy of banks across jurisdictions it is essential that banks disclose the

full list of regulatory capital items and regulatory adjustments.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 3/218

3

In addition, to improve consistency and ease of use of disclosuresrelating to the composition of regulatory capital, and to mitigate

the risk of inconsistent formats undermining the objective of enhanced disclosure, the Basel Committee has agreed that

internationally-active banks across Basel member jurisdictions willbe required to publish their capital positions according tocommon templates.

The requirements are set out in the following 5 sections:

Section 1: Post 1 January 2018 disclosure template

A common template is established that banks must use to

report the breakdown of their regulatory capital when thetransition period for the phasing-in of deductions ends on 1January 2018.

It is designed to meet the Basel I I I requirement to disclose allregulatory adjustments, including amounts falling below

thresholds for deduction, and thus enhance consistency andcomparability in the disclosure of the elements of capital between

banks and across jurisdictions.

This template may be used in advance of 1 January 2018 incertain circumstances, which are set out in Section 1.

Section 2: reconciliation requirements

A 3 step approach for banks to follow is established to ensurethat the Basel I I I requirement to provide a full reconciliation of all regulatory capital elements back to the published financial

statements is met in a consistent manner.

This approach is not based on a common template because thestarting point for reconciliation, the bank’s reported balance

sheet, will vary between jurisdictions due to the application of different accounting standards.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 4/218

4

Section 3: main features template

A common template is established that banks must use to meetthe Basel I I I requirement to provide a description of the main

features of regulatory capital instruments issued.

Section 4: other disclosure requirements

This section sets out what banks must do to meet the Basel I I Irequirement to provide the full terms and conditions of regulatorycapital instruments on their websites and the requirement toreport the calculation of any ratios involving components of regulatory capital.

Section 5: template during the transitional period

This section requires banks to use a modified version of the post 1 January 2018 template in Section 1 during thetransitional phase.

This template is established to meet the Basel I I Irequirement for banksto disclose the components of capital that are benefitingfrom the transitional arrangements.

Implementation date and frequency of reporting

National authorities will give effect to the disclosure requirementsset out in this document by no later than 30 June 2013.

Banks will be required to comply with the disclosure requirementsfrom the date of publication of their first set of financial statementsrelating to a balance sheet date on or after 30 June 2013 (with theexception of the Post 1 January 2018 template set out in Section1).

Furthermore, except as required in paragraph 7, banks mustpublish this disclosure with the same frequency as, andconcurrent with, the publication of their financial statements,irrespective of whether the financial statements are audited (iedisclosure will typically be quarterly or half yearly).

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 5/218

5

In the case of the main features template (Section 3) and provisionof the full terms and conditions of capital instruments (Section 4),

banks are required to update these disclosures whenever a newcapital instrument is issued and included in capital and whenever

there is a redemption, conversion/ write-down or other materialchange in the nature of an existing capital instrument.

Under Pillar 3, large banks are required to make certain minimumdisclosures with respect to certain defined key capital ratios and

elements on a quarterly basis, regardless of the frequency of financial statement publication.

The disclosure of key capital ratios/elements for thesebanks will continue to be required under Basel I I I.

Banks’ disclosures required by this document must either beincluded in banks’ published financial statements or, at aminimum, these statements must provide a direct link to thecompleted disclosure on their websites or on publicly availableregulatory reports.

Banks must also make available on their websites, or throughpublicly available regulatory reports, an archive (for a suitable

retention period determined by the relevant national authority) of all templates relating to prior reporting periods.

Irrespective of the location of the disclosure (published financialreports, bank websites or publicly available regulatory reports), alldisclosures must be in the format required by this document.

Section 1: Post 1 January 2018 disclosure template

The common template that the Basel Committee has developed isset out in Annex 1, along with an explanation of its design.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 6/218

6

The template is designed to capture the capital positions of banks after the transition period for the phasing-in of deductionsends on 1 January 2018 and must be used by banks for reporting

periods on or after this date.

If a jurisdiction permits or requires its banks to apply the full BaselI I I deductions in advance of 1 January 2018 (ie does not phase-inthe deductions or accelerates the phase-in period of deductions),

it can permit or require its banks to use the template in Annex 1 asan alternative to the transitional template described in Section 5

from the date of application of at least the full Basel I I Ideductions.

In such cases the relevant banks must clearly disclose that theyare using this template because they are fully applying the Basel

I I I deductions.

Section 2: Reconciliation requirements

This section sets out a common approach that banks mustfollow to comply with the requirement of paragraph 91 of the

Basel I I I rules text, which states that banks should disclose “afull reconciliation of all regulatory capital elements back to the

balance sheet in the audited financial statements.”

This requirement aims to address the problem that at presentthere is a disconnect in many banks’ disclosure between thenumbers used for the calculation of regulatory capital and the

numbers used in the published financial statements.

Banks are required to take a 3 step approach to show the linkbetween their balance sheet in their published financial

statements and the numbers that are used in the composition of capital disclosure template set out in Section 1.

The 3 steps require banks to:

Step 1: Disclose the reported balance sheet under the regulatoryscope of consolidation.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 7/218

7

Step 2: Expand the lines of the balance sheet under theregulatory scope of consolidation to display all of the

components that are used in the composition of capitaldisclosure template.

Step 3: Map each of the components that are disclosed in Step2 to the composition of capital disclosure template set out in

Section 1.

The 3 step approach outlined below is designed to offer thefollowing benefits:

The level of disclosure is proportionate, varying with the

complexity of the balance sheet of the reporting bank (ie banksare not subject to a fixed template that is designed to fit the most

complex banks.

A bank can skip a step if there is no further information addedby that step).

Market participants and supervisors can trace the origin of theelements of the regulatory capital back to their exact location on

the balance sheet under the regulatory scope of consolidation.

The approach is flexible enough to be used under anyaccounting standard: firms are required to map all thecomponents of the regulatory capital disclosure templates back tothe balance sheet under the regulatory scope of consolidation,regardless of whether the accounting standards require thesource to be reported on the balance sheet.

Step 1: Disclose the reported balance sheet under theregulatory scope of consolidation

The scope of consolidation for accounting purposes and for regulatory purposes are often dif ferent.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 8/218

8

This factor often explains much of the difference between thenumbers used in the calculation of regulatory capital and thenumbers used in a bank’s published financial statements.

Therefore, a key element in any reconciliation involves disclosinghow the balance sheet in the published financial statementschanges when the regulatory scope of consolidation is applied.

Step 1 is illustrated in Annex 2.

If the scope of regulatory consolidation and accountingconsolidation is identical for a particular banking group, it wouldnot need to undertake Step 1.

The banking group could simply state that there is no differencebetween the regulatory consolidation and the accountingconsolidation and move to Step 2.

In addition to Step 1, banks are required to disclose the list thelegal entities that are included within accounting scope of consolidation but excluded from the regulatory scope of consolidation.

This will better enable supervisors and market participants toinvestigate the risks posed by unconsolidated subsidiaries.

Similarly, banks are required to list the legal entities included inthe regulatory consolidation that are not included in theaccounting scope of consolidation.

Finally, if some entities are included in both the regulatory scope

of consolidation and accounting scope of consolidation, but themethod of consolidation differs between these two scopes, banksare required to list these legal entities separately and explain thedifferences in the consolidation methods.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 9/218

9

Regarding each legal entity that is required to be disclosed bythis paragraph, banks must also disclose its total balance sheet

assets and total balance sheet equity (as stated on theaccounting balance sheet of the legal entity) and a description of

the principle activities of the entity.

Step 2: Expand the lines of the regulatory balance sheetto display all of the components used in the definition

of capital disclosure template

Many of the elements used in the calculation of regulatory capitalcannot be readily identified from the face of the balance sheet.

Therefore, banks should expand the rows of the regulatory-scopebalance sheet such that all of the components used in the

composition of capital disclosure template (described in Section1) are displayed separately.

For example, paid-in share capital may be reported as one lineon the balance sheet.

However, some elements of this may meet the requirements for

inclusion in Common Equity Tier 1 (CET1) and other elementsmay only meet the requirements for Additional Tier 1 (AT1) or Tier

2 (T2), or may not meet the requirements for inclusion inregulatory capital at all.

Therefore, if the bank has some paid-in capital that feeds into thecalculation of CET1 and some that feeds into the calculation of

AT1, it should expand the ‘paid-in share capital’ line of thebalance sheet in the following way (also illustrated in Annex 2

(step 2)):In addition, as illustrated above, each element of the expanded

balance sheet must be given a reference number/letter for use inStep 3.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 10/218

10

As another example, one of the regulatory adjustments is thededuction of intangible assets.

While at first it may seem as if this can be taken straight off the

face of the balance sheet, there are a number of reasons why thisis unlikely to be the case.

Firstly, the amount on the balance sheet may combinegoodwill, other intangibles and mortgage services rights.

MSRs are not to be deducted in full (they are insteadsubject to the threshold deduction treatment).

Secondly, the amount to be deducted is net of any relateddeferred tax liability.

This deferred tax liability will be reported on the liability side of the balance sheet and is likely to be reported in combinationwith other deferred tax liabilities that have no relation togoodwill or intangibles.

Therefore, the bank should expand the balance sheet in thefollowing way:

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 11/218

11

It is important to note that banks will only need to expandelements of the balance sheet to the extent that this is necessaryto reach the components that are used in the composition of capital disclosure template.

So, for example, if all of the paid-in capital of the bank met therequirements to be included in CET1, the bank would not need toexpand this line.

The level of disclosure is proportionate, varying with thecomplexity of the bank’s balance sheet and its capitalstructure.

Step 2 is illustrated in Annex 2.

Step 3: Map each of the components that are disclosed inStep 2 to the composition of capital disclosure templates

When reporting the disclosure template, described in Section 1and Section 5, the bank is required to use the referencenumbers/ letters from Step 2 to show the source of every input.

For example, the composition of capital disclosure templateincludes the line “goodwill net of related deferred tax liability”.

Next to the disclosure of this item in the definition of capitaldisclosure template the bank should put “a–d” to illustrate howthese components of the balance sheet under the regulatoryscope of consolidation have been used to calculate this item inthe disclosure template.

Additional comments on the 3 step approachThe Basel Committee considered requiring banks to use acommon template to disclose the reconciliation between banks’balance sheets and their regulatory capital.Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 12/218

12

However, it does not feel that this would be possible at thisstage given that banks balance sheets are not reported in a

common way across jurisdictions due to the application of different accounting standards.

Within a single jurisdiction, the use of a common templatemay be possible.

Therefore, the relevant authorities may design a commontemplate that is consistent with the 3 step approach set out aboveand require banks use this in order to achieve greater consistency

in the way the 3 step approach is implemented within their jurisdiction.

Section 3: Main features template

Basel I I I requires banks to disclose a description of the mainfeatures of regulatory capital instruments issued.

While banks will also be required to make available the fullterms and conditions of their regulatory capital instruments

(see section 4), the length of these documents makes theextraction of the key features a burdensome task.

The issuing bank is better placed to undertake this task thanmarket participants and supervisors that want an overview of the

capital structure of the bank.

Basel I I Pillar 3 guidance already includes a requirement thatbanks provide qualitative disclosure that sets out “Summary

information on the terms and conditions of the main features of all capital instruments, especially in the case of innovative,

complex or hybrid capital instruments.”

However, the Basel Committee has found that this Basel I Irequirement is not met in a consistent way by banks.Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 13/218

13

The lack of consistency in both the level of detail provided andthe format of the disclosure makes the analysis and monitoring of

this information difficult.

To ensure that banks meet the Basel I I I requirement to disclosethe main features of regulatory capital instruments in a consistentand comparable way, banks are required to complete a ‘mainfeatures template’.

This template represents the minimum level of summarydisclosure that banks are required to report in respect of eachregulatory capital instrument issued.

The template is set out in Annex 3 of this report, along with adescription of each of the items to be reported.

Some key points to note about the template are:

- It has been designed to be completed by banks from whenthe Basel I I I framework comes into effect on 1 January 2013.

It therefore also includes disclosure relating to instruments

that are subject to the transitional arrangements.

- Banks are required to report each regulatory capital instrument,including common shares, in a separate column of thetemplate, such that the completed template would provide a‘main features report’ that summarises all of the regulatorycapital instruments of the banking group.

- The list of main features represents a minimum level of

required summary disclosure.

In implementing this minimum requirement, each BaselCommittee member authority is encouraged to add to this listif there are features that it is important to disclose in thecontext of the banks they supervise.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 14/218

14

- Banks are required to keep the completed main featuresreport up-to-date, such that the report is updated and

made publiclyavailable whenever a bank issues or repays a capital

instrument and whenever there is a redemption,conversion/ write-down or other material change in the nature

of an existing capital instrument.

- Given that the template includes information on the amountrecognised in regulatory capital at the latest reporting date, the

main features report should either be included in the bank’spublished financial reports or, at a minimum, these financialreports must provide a direct link to where the report can be

found on the bank’s website or publicly available regulatoryreporting.

Section 4: Other disclosure requirements

In addition to the disclosure requirements set out in Sections 1 to3, and aside from the transitional disclosure requirements set out

in Section 5, the Basel I I I rules text makes the followingrequirements in respect of the composition of capital:

Non-regulatory ratios

Banks which disclose ratios involving components of regulatorycapital (eg “Equity Tier 1”, “Core Tier 1” or “Tangible Common

Equity” ratios) must accompany such disclosures with acomprehensive explanation of how these ratios are calculated.

Full terms and conditions

Banks are required to make available on their websites the fullterms and conditions of all instruments included in regulatory

capital.

The requirement for banks to make available the full terms andconditions of regulatory capital instruments on their websites will

allow market participants and supervisors to investigate thespecific features of individual capital instruments.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 15/218

15

An additional related requirement is that all banks must maintaina Regulatory Disclosures section of their websites, where all of

the information relating to disclosure of regulatory capital ismade available to market participants.

In cases where disclosure requirements set out in this documentare met via publication through publicly available regulatory

reports, the regulatory disclosures section of the bank’s websiteshould provide specific links to the relevant regulatory reports

that relate to the bank.

This requirement stems from the supervisory experience that,in many cases, the benefit of Pillar 3 disclosures is severely

diminished by the challenge of finding the disclosure in the

first place.

Ideally much of the information that would be reported in theRegulatory Disclosures section of the website would also included

in the published financial reports of the bank.

The Basel Committee has agreed that, at minimum, the publishedfinancial reports must direct users to the relevant section of their

websites where the full set of required regulatory disclosure isprovided.

Section 5: Template during the transitional period

The Basel I I I rules text states that: “During the transition phasebanks are required to disclose the specific components of

capital, including capital instruments and regulatoryadjustments that are benefiting from the transitional provisions.”

The transitional arrangements for Basel I I I phase in theregulatory adjustments between 1 January 2014 and 1January 2018.

They require 20% of the adjustments to be made according toBasel I I I in 2014, with the residual subject to existing national

treatment.

In 2015 this increases to 40%, and so on, until the full amount of

the Basel

I I I adjustments are applied from 1 January2018.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 16/218

16

These transitional arrangements create an additional layer of complexity in the definition of capital in the period between 1

January 2013 and 1 January 2018, especially due to the fact thatexisting national treatments of the residual regulatory

adjustments vary considerably.

This complexity suggests that there would be particular benefitsin setting out detailed disclosure requirements during this period

to ensure that banks do not adopt different approaches that makecomparisons between them difficult.

This section of the composition of capital disclosure rules textaims to ensure that disclosure during the transitional period is

consistent and comparable across banks in different

jurisdictions.

Banks will be required to use a modified version of the Post 1January 2018 Disclosure Template, set out in Section 1, in a waythat captures existing national treatments for the regulatoryadjustments.

The use of a modified version of the Post 1 January 2018Disclosure Template, rather than the development of acompletely separate set of reporting requirements, should helpto reduce systems costs for banks.

The template is modified in just two ways:

(1)An additional column indicates the amounts of the regulatoryadjustments that will be subject to the existing nationaltreatment; and

(2)Each jurisdiction will insert additional rows in four separateplaces to indicate where the adjustment amounts reported in theadded column actually affect capital during the transition period.

The modifications to the template are set out in Annex 4, alongwith some examples of how the template will work in practice.

Banks are required to use the template for all reporting periods on

or after

the implementation date set out in paragraph 5, and banks arerequired to

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 17/218

17

report the template with the same frequency as the publicationof their financial statements (typically quarterly or half yearly).

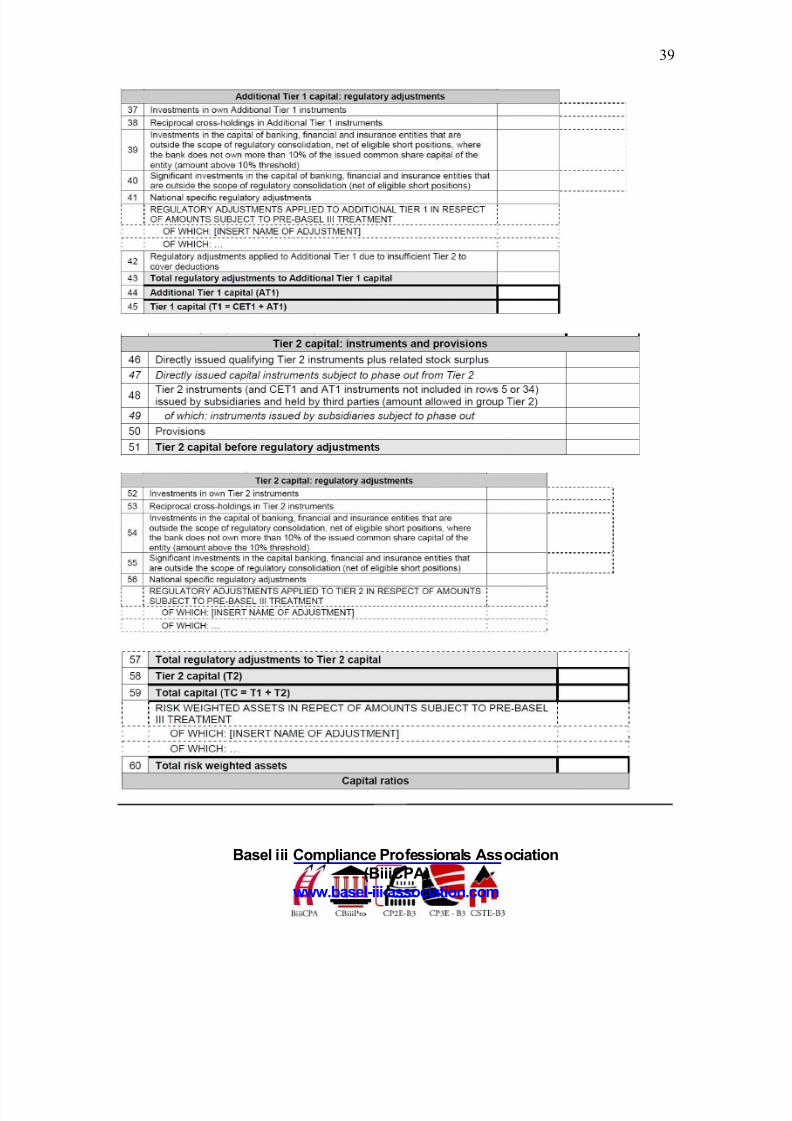

Annex 1

Post 1 January 2018 Disclosure Template

Key points to note about the template set out in this Annex are:

- The template is designed to capture the capital positions of

banks after the transition period for the phasing-in of deductions ends on 1 January 2018 (the template for banks touse to report their capital positions during this transitional

phase is set out in Section 5).

- Certain rows are in italics. These rows will be deleted after all the ineligible capital instruments have been fully phased

out (ie from 1 January 2022 onwards).

- The reconciliation requirements included in Section 2

result in the decomposition of certain regulatoryadjustments.

For example, the disclosure template below includes theadjustment ‘Goodwill net of related tax liability’.

The requirements in Section 2 will lead to the disclosure of both the goodwill component and the related tax liability

component of this regulatory adjustment.

- Regarding the shading: Each dark grey row introduces a newsection

detailing a certain component of regulatory capital.

The light grey rows with no thick border represent the sum cellsin the relevant section.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 18/218

18

The light grey rows with a thick border show the maincomponents of regulatory capital and the capital ratios.

- Also provided below is a table that sets out an explanation of

each line of the template, with references to the appropriateparagraphs of the Basel I I I text.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 19/218

19

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 20/218

20

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 21/218

21

Set out in the following table is an explanation of each row of thetemplate above.

Regarding the regulatory adjustments banks are required toreport deductions from capital as positive numbers andadditions to capital as negative numbers.

For example, goodwill (row 8) should be reported as a positivenumber, as should gains due to the change in the own credit riskof the bank (row 14).

However, losses due to the change in the own credit risk of thebank should be reported as a negative number as these areadded back in the calculation of Common Equity Tier 1.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 22/218

22

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 23/218

23

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 24/218

24

41. In general, to ensure that the common templates remaincomparable across jurisdictions there should be no adjustmentsto the version banks use to disclose their regulatory capitalposition.

However, the following exceptions apply to take account of language differences and to reduce the reporting of unnecessary information:

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 25/218

25

- The common template and explanatory table above can betranslated by the relevant national authorities into the relevant

national language(s) that implement the Basel standards.

The translated version of the template will retain all of therows included the template above.

- Regarding the explanatory table, the national version canreference the national rules that implement the relevant

sections of Basel I I I.

- Banks are not permitted to add, delete or change thedefinitions of any rows from the common reporting template

implemented in their jurisdiction.

This will prevent a divergence of templates that couldundermine the objectives of consistency and comparability.

- This national version of the template will retain the same rownumbering used in the first column of the template above,such that market participants can easily map the national

templates to the common version above.

However, the common template includes certain rows thatreference national specific regulatory adjustments (row 26, 41,

and 56).

The relevant national authority should insert rows after eachof these to provide rows for banks to disclose each of the

relevant national specific adjustments (with the totals reportedin rows 26, 41 and 56).

The insertion of any rows must leave the numbering of theremaining rows unchanged, eg rows detailing national specific

regulatory adjustments to common equity Tier 1 could belabelled Row 26a, Row 26b etc, to ensure that the subsequent

row numbers are not affected.

- In cases where the national implementation of Basel I I I appliesa

more conservative definition of an element listed in thetemplate

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 26/218

26

above, national authorities may choose between oneof two approaches:

Approach 1: in the national version of the template maintain the

same definitions of all rows as set out in the template above,and require banks to report the impact of the more

conservative national definition in the designated rows for national specific adjustments (ie row 26, row 41, row 56).

Approach 2: in the national version of the template use thedefinitions of elements as implemented in that jurisdiction,

clearly labelling them as being different from the Basel I I Iminimum definition, and require banks to separately disclose

the impact of each of these different definitions in the notes tothe template.

The aim of both approaches is to provide all the informationnecessary to enable market participants to calculate the capital

of banks on a common basis.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 27/218

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 28/218

28

Step 2

Under Step 2 banks are required to expand the balance sheetunder the regulatory scope of consolidation (revealed in Step 1) toidentify all the elements that are used in the definition of capitaldisclosure template set out in Annex 1.

Set out below are some examples of elements that mayneed to be expanded for a particular banking group.

The more complex the balance sheet of the bank, the more itemswould need to be disclosed.

Each element must be given a reference number / letter that canbe used in Step 3.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 29/218

29

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 30/218

30

Step 3

Under Step 3 banks are required to complete a column added tothe post 1 January 2018 disclosure template to show the source of

every input.

For example, the Post 1 January 2018 Disclosure Templateincludes the line “goodwill net of related deferred tax liability”.

Next to the disclosure of this item in the template the bank wouldbe required to put “a–d” to show that row 7 of the template hasbeen calculated as the difference between component “a” of the

balance sheet under the regulatory scope of consolidation,

illustrated in step 2, and component “d”.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 31/218

31

Annex 3

Main features template

Set out below is the template that banks must use to ensure thatthe key features of all regulatory capital instruments are

disclosed.

Banks will be required to complete all of the shaded cells for each outstanding regulatory capital instrument (banks should

insert “NA” if the question is not applicable).

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 32/218

32

This template was developed in a spreadsheet that will be madeavailable to banks on the Basel Committee’s website.

To complete most of the cells banks simply need to select anoption from a drop down menu.

Using the reference numbers in the left column of the tableabove, the following table provides a more detailed explanation of what banks are required to report in each of the grey cells,including, where relevant, the list of options contained in thespreadsheet’s drop down menu.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 33/218

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 34/218

34

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 35/218

35

Annex 4

Disclosure template during the transition phase

The template that banks must use during the transition phase is

the same as the Post 1 January 2018 disclosure template set out inSection 1 except for the following additions (all of which are

highlighted in the template below using cells with dotted bordersand capitalised text):

- A new column has been added for banks to report the amountof each regulatory adjustment that is subject to the existing

national treatment during the transition phase (labelled as the“pre-Basel III treatment”).

Example 1: In 2014 banks will be required to make 20% of theregulatory adjustments in accordance with Basel I I I .

Consider a bank with “Goodwill, net of related tax liability” of $100 mn and assume that the bank is in a jurisdiction that doesnot currently require this to be deducted from common equity.

The bank will report $20 mn in the first of the two empty cells in

row 8 and report $80 mn in the second of the two cells.

The sum of the two cells will therefore equal the total Basel I I Iregulatory adjustment.

- While the new column shows the amount of eachregulatory adjustment that is subject to the existingnational treatment, it is necessary to show how this

amount is included under existing national treatment in

the calculation of regulatory capital.

Therefore, new rows have been added in each of the threesections on regulatory adjustments to allow each jurisdiction

to set out their existing national treatment.Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 36/218

36

Example 2: Assume that the bank described in the bullet pointabove is in a jurisdiction that currently requires goodwill to bededucted from Tier 1. This jurisdiction will insert a new row inbetween rows 41 and 42, to indicate that during the transition

phase some goodwill will continue to be deducted from Tier 1 (ineffect Additional Tier 1).

The $80 mn that the bank had reported in the last cell of row 8,will then need to be reported in this new row inserted between

rows 41 and 42.

In addition to the phasing-in of some regulatory adjustmentsdescribed above, the transition period of Basel I I I will in some

cases result in the phasing-out of previous prudentialadjustments.

In these cases the new rows added in each of the three sectionson regulatory adjustments will be used by jurisdictions to set out

the impact of the phase-out.

Example 3: Consider a jurisdiction that currently filters outunrealised gains and losses on holdings of AFS debt securitiesand consider a bank in that jurisdiction that has an unrealised

loss of $50 mn.

The transitional arrangements require this bank to recognise 20%of this loss (ie $10 mn) in 2014.

This means that 80% of this loss (ie $40 mn) is notrecognised. The jurisdiction will therefore include a row

between rows 26 and 27 that allows banks to add back thisunrealised loss.

The bank will then report $40 mn in this row as an addition toCommon Equity Tier 1.

- To take account of the fact that the existing nationaltreatment of a Basel I I I regulatory adjustment may be to apply a

risk weighting, jurisdictions will also be able to add new rowsimmediately prior to the row on risk weighted assets (row 60).

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 37/218

37

These rows will need to be defined by each jurisdiction to listthe Basel III regulatory adjustments that are currently risk

weighted.

Example 4: Consider a jurisdiction that currently risk weightsdefined benefit pension fund net assets at 200% and in 2014 a

bank has $50 mn of these assets.

The transitional arrangements require this bank to deduct 20%of the assets in 2014.

This means that the bank will report $10 mn in the first empty cellin row 15 and $40 mn in the second empty cell (the total of the two

cells therefore equals the total Basel I I I regulatory adjustment).

The jurisdiction will disclose in one of the inserted rows betweenrow 59 and 60 that such assets are risk weighted at 200% duringthe transitional phase.

The bank will then be required to report a figure of $80 mn ($40mn * 200%) in that row.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 38/218

38

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 39/218

39

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 40/218

40

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 41/218

41

MAS Consults on Proposed Review of Risk-basedCapital Framework for Insurance Business

Singapore, 22 June 2012

The Monetary Authority of Singapore (MAS) today releaseda consultation paper on the review of the Risk-Based

Capital (RBC) framework for insurance business.

The RBC framework was first introduced in Singapore in 2004. Itadopts a risk-focused approach to assessing capital adequacy andseeks to reflect the relevant risks that insurance companies face.

MAS is reviewing the framework, given evolving market practicesin the insurance industry and in international accounting andregulatory standards.

The review aims to improve the comprehensiveness of the riskcoverage and risk sensitivity of the framework, and is notexpected to result in a significant overhaul to the currentframework. Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 42/218

42

1. The RBC framework for insurance companies was firstintroduced in Singapore in 2004.

It adopts a risk-focused approach to assessing capital adequacy

and seeks to reflect the relevant risks that insurance companiesface.

The minimum capital prescribed under the framework serves as abuffer to absorb losses.

The RBC framework also provides clearer information on thefinancial strength of insurers and facilitates early and effective

intervention by MAS, if necessary.

3. Whilst the RBC framework has served us well, MAS is embarkingon a review (“RBC 2”) of the framework in light of evolving market

practices and global regulatory developments.

The review will take into account the revised I nsurance CorePrinciples and Standards issued by the International

Association of Insurance Supervisors last year.

5. A risk-focused approach to capital adequacy continuesto be appropriate and relevant in the supervision of

insurers.

As such, the RBC 2 review is not expected to result in asignificant overhaul to the current framework.

Rather, the review aims to improve the comprehensiveness of therisk coverage and the risk sensitivity of the framework, as well as

defining more specifically, MAS supervisory approach with respectto the solvency intervention levels.

7. Section 2 of the paper details the proposed review in theareas of required capital.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 43/218

43

This touches on the expansion of the current framework toaddress more risk types, the introduction of target criteria for riskcalibration, the diversification benefits from correlations between

risk types, and the usage of internal models.

5. Section 3 elaborates on the components of available capital.These include the treatment for negative reserves and aggregate

provisions for non-guaranteed benefits.

In addition, it is envisaged that there will be some degree of convergence with Basel I I I global capital standards, as MAS seeks

to improve the alignment of capital standards between thebanking and insurance industries.

7. Section 4 sets out the two explicit solvency interventionlevels, the Prescribed Capital Requirement as well as the

Minimum Capital Requirement.

Having clear and transparent solvency intervention levels isuseful for insurers.

MAS expectations on the type of corrective capital actions to be

taken by insurers, and the urgency which these actions should betaken, will be referenced against these solvency levels.

9. Section 5 sets out the proposed approach with regards to risk-free discount rate, and consults on an alternative approach to the

derivation of the provision for adverse deviation (or risk margin).

10.The RBC 2 review will not just focus solely on the quantitativeaspects of capital requirements.

It also seeks to enhance insurers’ risk management

practices. As such, the scope of the review includes

qualitative aspects on

Enterprise Risk Management, as outlined in Section 6.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 44/218

44

1.9 MAS hopes to work closely with the industry on the review, aswas the case when the RBC framework was first developed.

We anticipate that the industry will be involved through

workgroup participation, quantitative impact studies andconsultation feedback.

COMPONENTS OF REQUIRED CAPITAL

1. The RBC framework requires insurers to hold capital againsttheir risk exposures known as the Total Risk Requirements

(“TRR”).

Risks arising from an insurer’s assets and liabilities are groupedin to

three distinct components:

2. Component 1 (C1) requirement relates to insurance risksundertaken by insurers.

C1 requirement for general insurance business isdetermined by applying specific risk charges on an

insurer ’s premium and claims liabilities.

Risk charges applicable to different business lines varywith the volatility of the underlying business.

The requirement for life insurance business is calculated byapplying specific risk margin to key parameters affecting policyliabilities such as mortality, morbidity, expenses and policy

termination rates.

3.Component 2 (C2) requirement relates to risks inherent in aninsurer’s asset portfolio, such as market risk and credit risk.

It is calculated based on an insurer's exposure to variousmarkets including equity, debt, property and foreignexchange.

The C2 requirement also captures the extent of asset-liability mismatch present in an insurer ’s portfolio.

Basel iii Compliance Pr ofessionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 45/218

45

- Component 3 (C3) requirement relates to assetconcentration risks in certain types of assets, counterparties

or groups of counterparties.C3 charges are computed based on an insurer’s exposure in

excess of the concentration limits as prescribed under the Insurance

(Valuation and Capital) Regulations 2004.

2. The following paragraphs set out where enhancements areexpected.

Inclusion of New Risk Types

4.The current RBC framework already captures most of the materialrisks such as market risk, credit risk, underwriting risk and

concentration risk.

For risks which are not specifically quantified under RBC, they areconsidered qualitatively under MAS risk based supervision and

MAS has the powers under the Insurance Act to imposeadditional capital requirements if necessary.

For the RBC 2 review, MAS is reviewing the risk coverage inline with evolving global regulatory and market developments.

Spread risk

6. The current RBC framework takes into account the creditrisk of corporate bonds but does not capture credit spread

risk.

In MAS annual stress testing exercise, insurers were found tobe

susceptible to credit spread shocks.

This is not surprising given that insurers hold a highproportion of

corporate bonds.

MAS proposes to explicitly capture credit spread risk under theRBC 2 framework.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 46/218

46

This is similar to the credit spread shocks applied during stresstesting.

Spread risk results from the sensitivity of the value of assets and

liabilities to changes in the level or in the volatility of creditspreads over the

risk-free interest rate.

Proposal 1

MAS proposes to incorporate an explicit risk charge to capturespread risk within the RBC 2 framework.

Liquidity risk

5. Liquidity risk is the exposure to loss in the event thatinsufficient liquid assets are available from the assets supporting

the policy liabilities, to meet the cash flow requirements of policyholder obligations, or assets may be available, but can onlybe liquidated to meet policyholder obligations at excessive cost.

6. However, we do not propose to impose an explicit risk charge

for liquidity risk as there is no well-established methodology toquantify capital requirements for liquidity risk. MAS will

continue to assess the robustness of insurers’ liquidity riskmanagement through supervision.

Proposal 2

MAS proposes not to impose an explicit risk charge for liquidityrisk. MAS will work with the industry to conduct liquidity stress-

testing, and assess the soundness of the insurer ’s liquidity riskmanagement practices as part of MAS risk-based supervision.

Operational risk

9. Operational risk refers to the risk of loss arising fromcomplex operations, inadequate internal controls, processes

and information

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 47/218

47

systems, organisation changes, fraud or human errors, (or unforeseen catastrophes including terrorist attacks).

Operational risk is recognised as a relevant and material risk that

needs to be addressed in a supervisory framework.

Currently there is no explicit risk charge for operational riskunder the RBC framework, though operational risk is assessed

as part of MAS ongoing supervision of insurers.

However, both Basel I I and a number of major jurisdictionshave explicitly introduced capital requirements for operational

risk in their capital framework.

8. Methodologies to quantify operational risk continue toevolve globally.

The insurance industry also does not presently collectsufficient operational risk data.

As such, MAS intends to start off with a simplified and pragmaticmethod to quantify the operational risk charge, and refine its

methodology in future as more data becomes available andpractices are more established internationally.

The proposed method is broadly similar to some of theapproaches used in other jurisdictions such as the EuropeanEconomic Area (under the standardised formula approach of

Solvency I I ) and Australia.

10.MAS proposes to put a cap on the amount of operational risk

charge such that it will not be larger than 10% of an insurer ’stotal risk requirements.

This is based on our observation on banks’ operational riskcharge as a percentage of the total capital requirements.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 48/218

48

There is no evidence to suggest that an insurer ’s operationalrisk would be vastly different from that experienced by a bank.

Proposal 3

MAS proposes to incorporate an explicit risk charge tocapture operational risk within the RBC 2 framework,

calculated as:

x% of the higher of the past 3 years’ averages of (a) earnedpremium income; and (b) gross policy liabilities, subject to a

maximum of 10% of the total risk requirements.

Where x = 4% (except for investment-linked business, where x= 0.25% given that most of the management of investment-

linked fund is outsourced)

Consultation Question 1

Is this formula or bases chosen appropriate? Should we be usingwritten premium or net policy liabilities instead? Should there be

differences in the formula for different types of insurers, for example, direct life, direct general and reinsurers?

Consultation Question 2

What type of data can the insurance industry start to collect inorder to build up sufficient data to better quantify or model

operational risks? Insurance catastrophe risk

2.10 While concentration risk is covered under the existingframework (as C3 risk requirements), it is only confined to asset

concentration risk.

The RBC framewor k does not capture insurance catastrophe risk,which is the risk that a catastrophe causes a one-time spike in

claims experience, with a corresponding impact on claims and/ or liabilities.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 49/218

49

Such claims experience can have a significant impact on aninsurer ’s solvency, particularly if the insurer has a concentration

of risks written in a particular area or business line.

Recent natural catastrophes in the region have shown thatinsurance catastrophe risk is a real and relevant risk to

insurers here which write risks in the region.

11.There are a few options to explicitly address this risk under theRBC 2 framework.

One option would be to require insurers to construct acatastrophe scenario that is most relevant to them and has the

greatest impact, benchmarked to some target criteria (e.g. 1 in200 year event), and work out the capital that has to be set asideto meet that event net of reinsurance arrangements.

This is similar to the approach of allowing the use of internalmodels (As adopted under Swiss Solvency Test in Switzerland).

The second option (As adopted in Bermuda and in EuropeanEconomic Area under Solvency I I ) would be for the regulator to

prescribe a number of man-made and natural catastrophescenarios.

An explicit risk charge is then computed accordingly from acombination of these scenarios.

The third option would be to get the insurers to stress test on anumber of standardised catastrophe scenarios, and additionalcapital requirements would only be imposed for the insurers thatare more vulnerable.

This would, however, be less transparent.

13.As a target, MAS is of the view that it would be appropriate toadopt the first option, which is similar to allowing the use of internal models.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 50/218

50

This option would ensure that the catastrophe scenarioconstructed by each insurer is relevant to its own business and

circumstances.

However, we recognise that insurers would need time to buildtheir own catastrophic risk modeling capabilities.

As such, for a start, MAS proposes to adopt the second optionto begin imposing specific risk charges for catastrophe risks.

Under this option, MAS intends to work with the industryassociations, reinsurance brokers and the other risk

institutes/ academia in Singapore to design relevant standardised

catastrophic scenarios to derive explicit risk charges for insurance catastrophe risk.

2.13 For the life business, the explicit insurance catastrophe riskcharge can be derived based on a pandemic event.

It is noted that a few major jurisdictions have used 1.5 deaths per 1,000 in deriving the insurance catastrophe risk charge for its life

business.

We propose to adopt a similar approach.

Proposal 4

MAS proposes to incorporate an explicit insurancecatastrophe risk charge in the RBC 2 framework.

This would be done through prescribing a number of man-made and natural catastrophe scenarios, with an explicit riskcharge computed accordingly from a combination of thesescenarios.

MAS intends to wor k with the industry associations, reinsurancebrokers and the other risk institutes/ academia in Singapore todesign relevant standardised catastrophic scenarios.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 51/218

51

For life business, the explicit insurance catastrophic risk chargecan be derived based on a pandemic event.

14.Currently, the offshore insurance fund of reinsurers is

subject to either a simplified solvency regime (in the case of locally incorporated reinsurers) or exempted from any capital or

solvency requirements altogether (in the case of reinsurancebranches).

MAS will, in consultation with the affected players, be reviewingthe capital treatment of the offshore insurance fund for all

reinsurers, whether locally or foreign incorporated, under RBC 2.

There will be a separate consultation paper on this.

Target Criteria for Calibration of Risk Requirements

16.The RBC framework relies on the Fund Solvency Ratio (“FSR)and the Capital Adequacy Ratio (“CAR”) as indicators of solvency

at the fund and company level respectively.

These ratios provide a snapshot of the insurer ‟s financialcondition at a point in time, without any consideration of the

confidence level and time horizon.

Under RBC 2, MAS intends to recalibrate the risk requirementsbased on a specified risk measure, confidence level and time

horizon.

18. There are 2 common risk measures used internationally:

- Value at Risk (“VaR”) – this is the expected value of loss at a predefined confidence level (e.g. 99.5%).

Thus, if the insurer holds capital equivalent to VaR, it will havesufficient assets to meet its regulatory liabilities with

probability of a confidence level of 99.5% over a one year timehorizon; and

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 52/218

52

- Tail Value at Risk (“tVaR”) – this is the expected value of the average loss where it exceeds the predefined confidence

level (eg 99.5%).

It is also known as the conditional tail expectation (“CTE”),expected shortfall or expected tail loss.

If an insurer holds capital equivalent to tVAR, it will havesufficient assets to meet the average losses that exceed the

predefined confidence level (of say 99.5%).

17.The VaR approach, while it has its limitations, is a generallyacceptedrisk measure for financial risk management.

It is easier to calibrate the risks under a VaR approach comparedto using tVaR. However, VaR, unlike tVaR, tends to underestimatethe exposure to tail events.

19.On balance, MAS proposes to adopt the VaR measure as it iseasier to calibrate.

Tail VaR can be considered under the internal model approach(see paragraphs 2.25 and 2.26), if insurers deem it to be moreappropriate for their business or risks.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 53/218

53

Tail event analysis can also be done during the annual industrywide stress testing exercise or the insurer ’s own risk and

solvency assessment (see Section 6).

19.MAS also proposes to adopt a time horizon of one year,and a confidence level of 99.5%.

This corresponds to an investment grade credit rating andis used commonly by most of the other major jurisdictions.

21.There will be a change in the approach in deriving mostof the asset-related risk requirements under RBC 2.

Instead of applying a fixed factor on the market value (e.g. 16% onthe equity market value for equity risk requirement) as per currentapproach, we will now apply a shock to the Net Asset (Assets less

Liabilities) and measure the impact of the shock.

The shock is calibrated at a VaR of 99.5% confidence level over aone year period.

The new risk requirement will be equivalent to the amount of change in Net Asset for each respective risk.

23. For insurance risk requirements, the approach will be similar.

For life business, the current insurance risk requirement iscomputed by applying prescribed loadings on best estimate

assumptions such as mortality, lapse and expense.

Under the new approach, the best estimate assumptions will beloaded up by some prescribed factors which will be calibrated at aVaR of 99.5% confidence level over a one year period which is the

proposed target criteria.Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 54/218

54

For general business, prescribed factors will still be applied to thepremium and claims liabilities, though the factors will now be

calibrated at the new target criteria.

22.MAS will consult separately on the data and methodology to beused for calibration, as well as on the recommended calibrationfactors or shock scenarios to be used to achieve the proposed

new target criteria.

Proposal 5

MAS proposes to recalibrate risk requirements using the Valueat Risk (“VaR”) measure of 99.5% confidence level over a one

year period.

MAS will be engaging the industry on the calibration exercise, andtarget to finalise the calibration factors /shock scenarios by 1Q

2013.

Data would need to be collected for this purpose. Therecommended calibration factors or scenarios will be consulted

prior to its finalisation.

Diversification Benefits

24.Under RBC, the total risk requirements are obtained bysumming the C1, C2 and C3 risk requirements.

Within the C1 or C2 risk requirements, the underlying riskrequirements are also added together, without allowing for any

diversification effects with the help of correlation matrices.

Some major jurisdictions such as the European Economic Area(under Solvency II ), Australia and Bermuda have moved towardsallowing for diversification effects when combining various riskmodules, and even within sub-modules, using prescribedcorrelation matrices.

This has the effect of reducing the overall regulatory capitalrequirements.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 55/218

55

The level of sophistication of the correlation matrices varies, andis based to some degree, on judgment.

24.MAS looked into the possibility of recognising

diversification benefits when aggregating the riskrequirements under RBC 2.

However, dependencies between different risks will vary asmarket conditions change and correlation has been shown to

increase significantly during periods of stress or whenextreme events occur.

In the absence of any conclusive studies to show

otherwise, MAS proposes not to take into accountdiversification effects for the aggregation of risk

requirements under RBC 2.

This approach is consistent with the capital framework for banks,where we do not allow for any diversification benefits when risks

are combined.

Proposal 6

MAS proposes not to allow for diversification benefits whenaggregating the capital risk requirements. MAS is, however,

prepared to consider diversification benefits if the industry is beable to substantiate, with robust studies and research conducted

on the local insurance industry, that there are applicablecorrelations which can relied on during normal and stressed

times.

Use of Internal Model

26.MAS intends to allow insurers to use partial or full internalmodels to determine the regulatory capital requirements in the

longer run, in line with international best practices.

The internal models will have to be calibrated at the same targetcriteria as the standardised approach, and be subject to MAS

approval.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 56/218

56

2.26 The use of internal model will be looked at under the nextphase of the review, after the standardised approach has been

rolled out.

This will allow the larger and more complex insurers time toprepare themselves for a more sophisticated and tailored

approach.

MAS would also be able to check the reasonableness of theinternal model assumptions and results against the experience of

the standardised approach.

Proposal 7

MAS proposes to allow the use of partial or internal model in thenext phase of the RBC 2 review, after the implementation of the

standardised approach.

The internal model, which will be subject to approval by MAS, willhave to be calibrated at the same level as the standardised

approach.

COMPONENTS OF AVAILABLE CAPITAL

3.1 The amount of capital available to meet the TRR is referredto as “financial resources” (“FR”) under the RBC framework.

FR comprises three components, namely Tier 1 resources,Tier 2

resources and the provision for non-guaranteed benefits.

-Tier 1 resources are capital resources of the highest

quality.

These capital instruments are able to absorb losses on anon-going basis.

They have no maturity date and, if redeemable, can only beredeemed at the option of the insurer.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 57/218

57

They should be issued and fully paid-up and non-cumulative innature. They should be ranked junior to policyholders, general

creditors, and subordinated debt holders of the insurer.

Tier 1 resources should neither be secured nor covered by aguarantee of the issuer or related entity or other arrangementthat may legally or economically enhance the seniority of the

claims vis-à-vis the policyholders.

Tier 1 resources are generally represented by theaggregate of the surpluses of an insurer ’s insurance

funds.

A locally incorporated insurer may add to its Tier 1resources its paid-up ordinary share capital, its surplusesoutside of insurance funds and irredeemable and

noncumulative preference shares.

- Tier 2 resources are only applicable to locally incorporatedinsurers and consist of capital instruments that are of a lower

quality than that of Tier 1 resources but may be available toserve as a buffer against losses incurred by the insurer.

Examples of these instruments include redeemable or cumulative preference shares and certain subordinated

debt.Tier 2 resources in excess of 50% of Tier 1 resources will

not berecognised as FR.

- The allowance for provision for non-guaranteed benefits is

applicable only to insurers who maintain a participating fund.

As the allowance for provision for non-guaranteed benefits isonly available to absorb losses of the participating fund, theallowance is adjusted to ensure that the unadjusted capital

ratio10 of the insurer is not greater than its adjusted ratio.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 58/218

58

Alignment with Basel I I I

2. As an integrated supervisor overseeing banking and insuranceentities in Singapore, MAS seeks to ensure a level playing field

across the financial sectors by having a consistent regulatory andsupervisory framework for the regulated financial institutions.

The Tier 1 and Tier 2 capital components are largely alignedbetween the existing RBC framework for insurers and the capital

adequacy framework for banks under Basel I I I , with the exceptionof surpluses in the insurance funds or balance in the surplus

account, which are insurance-specific in nature.

However, Basel I I I has strengthened the “equity-like”characteristics needed for a hybrid capital instrument to be

included in Tier 1 regulatory capital (i.e. capital of the highestquality).

Besides having to show greater capacity to absorb losses, thesehybrid capital instruments also need to have features that clearly

enable the instrument to undergo a principle write down or toconvert into common equity in the event of a bank stress.

4. To align with the capital adequacy framework for banks, MASproposes to incorporate the same Basel I I I features (i.e. equity

conversion or write-down on breach of regulatory capitalrequirements) as conditions for a capital instrument to be

approved by MAS as a Tier 1 resource (“Approved Tier 1Resource”).

Proposal 8

MAS proposes to incorporate the same Basel I I I features (i.e.equity conversion or write-down on breach of regulatory capital

requirements) for the Approved Tier 1 resource.Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 59/218

59

This means that instruments that qualifies as Approved Tier 1resource must:

(a)Automatically convert to ordinary share capital, as and when

the insurer needs to absorb losses, and in any case, when theinsurer breaches its regulatory capital requirement;

(b)Be sub ject to write down as long as losses persist, as and whenthe insurer needs to absorb losses, and in any case when the

insurer breaches its regulatory capital requirement.

The limits on the amount of Approved Tier 1 resource that can berecognised, as set out in the existing Insurance (Valuation and

Capital) Regulations 2004, will remain unchanged.

Treatment of Negative Reserves

4. For life business, policy liability is derived policy-by-policy bydiscounting the best estimate cash flows of future benefit

payments, expense payments and receipts, with allowance for provision for adverse deviation.

It is possible for the discounted value to be negative when theexpected present value of the future receipts (like premium andcharges) exceed the expected present value of the future outgo

(such as benefit payments and expense payments), resulting ina negative reserve.

6.However, regulation 20(4) of the I nsurance (Valuation and Capital)Regulations 2004 states that “A registered insurer shall not value

the liability in respect of any liability to be less than zero, unless

there are moneys due to the insurer when the policy is terminatedon valuation date, in which even the value of the liability in respect

of that policy may be negative to the extent of the amount due tothe insurer.”Basel iii Compliance Professionals Association

(BiiiCPA)www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 60/218

60

This means that negative reserves are not recognised unless oneexpects a recovery of monies (for example, surrender penalty in

the case of investment-linked policies).

6. Practices with regards to treatment of negative reservesdiffer internationally.

Under Solvency I I , the European Economic Area is consideringrecognising negative reserves as Tier 1 capital, while Canada

recognises part of the negative reserves as Tier 2 capital.

8. MAS current position of not recognising negative reserves as aform of capital is a conservative one because it is akin to

assuming a 100% lapse on all the policies, such that futurepremium receipts and charges are not recognised.

In practice, the lapse rate would not be 100%. Therefore, there isscope to reconsider the current position given that under RBC 2,

an insurer ’s net asset value will be shocked for insurance risk, andspecifically, lapse risk, at a 1-in-200 year level.

10.Hence, MAS would like to consult on recognising a part

of the negative reserves as financial resources.

We propose for this to be in the form of a positive financialresource adjustment, rather than as Tier 1 or Tier 2 capital.

As the amount of negative reserves are currently sizeable in somelife insurers, MAS will need to carefully review and establish a

framework for calibrating the level of negative reserves that maybe recognised.

Proposal 9

MAS proposes to allow a part of the negative reserves to berecognised as a form of positive financial resource adjustment

under Financial Resources.

Basel iii Compliance Professionals Association(BiiiCPA)

www.basel-iii-association.com

7/28/2019 Basel 3 August 2012

http://slidepdf.com/reader/full/basel-3-august-2012 61/218

61

MAS will consult further on the amount to be recognised.

Treatment of Aggregate of Allowances for Provision for Non- Guaranteed Benefits

9. When assessing the quality of capital resources, insuranceregulators are required under international standards to give

consideration to its characteristics, including “the extent to whichthe resource is available to absorb losses, the extent of the

permanent and/ or perpetual nature of the capital and theexistence of anymandatory servicing costs in relation to the

capital”.

10.Under the current RBC framework, as highlighted in Paragraph3.1, an insurer maintaining any participating fund is allowed to

count as financial resources, the aggregate of allowances for provision for

non-guaranteed benefits (“APNGB”), subject to the unadjustedcapital ratio of the insurer remaining below the adjusted ratio.

However, as these allowances do not meet the qualities required of a capital instrument, MAS will be reclassifying APNGB as a form of

positive financial resource adjustment (“FRA”), instead of acapital item.

Proposal 10

MAS proposes to classify Aggregate of Allowances for Provision for Non-Guaranteed Benefits, where applicable, asa form of positive financial resource adjustment, rather than

as a capital item.

This applies to an insurer maintaining any participating fund, andsubject to the condition that the unadjusted capital ratio remains

below the adjusted capital ratio, where: