Barry B. Bannister, CFA Managing Director, Equity Research Stifel Nicolaus & Co....

35

Barry B. Bannister, CFA Managing Director, Equity Research Stifel Nicolaus & Co. [email protected] All relevant disclosures and certifications can be found on page 33-34 of this report and on the research page at stifel.com. Macro-Trends Update for Financial Sense Newshour “In the spring, there will be growth*” March 1, 2010 * Paraphrasing Chauncey Gardener in “Being There,” United Artists Films, 1980.

-

date post

20-Dec-2015 -

Category

Documents

-

view

226 -

download

4

Transcript of Barry B. Bannister, CFA Managing Director, Equity Research Stifel Nicolaus & Co....

Barry B. Bannister, CFAManaging Director, Equity Research

Stifel Nicolaus & [email protected]

All relevant disclosures and certifications can be found on page 33-34 of this report and on the research page at stifel.com.

Macro-Trends Update for

Financial Sense Newshour

“In the spring, there will be growth*”

March 1, 2010

* Paraphrasing Chauncey Gardener in “Being There,” United Artists Films, 1980.

2

• Barry B. Bannister, CFA – Managing Director, Equity Research, Stifel Nicolaus & Co. of Baltimore, MD provides investment research to financial institutions globally in the areas of Engineering, Machinery and associated strategy related to commodity markets served by companies in those industries.

• He is a five-time winner of the Wall Street Journal All-Star analyst award, four-time winner of the Forbes Magazine/Financial Times/Starmine top analyst award, Top-10 U.S. Stock Pick analyst for CNBC/Zacks and two-time Institutional Investor magazine All Star Analyst (2007, 2008).

• Prior to joining Stifel Nicolaus and its predecessor Legg Mason Capital Markets in 1998, he was a senior analyst providing North American Machinery industry coverage and later co-head of U.S. equity research in the New York office of the UK investment bank S.G. Warburg & Company (Now UBS) from 1992 to 1998. Prior to that he served as an equity analyst for the buy-side firm FTIM/Highland Capital Management (1990-1992), and before that he was an equity analyst for the mutual funds and trusts of AmSouth Investment Management (now Regions Financial) from 1987-1990.

• He holds an MBA (1987) from the Emory University School of Business Administration, and a BA from Emory College (1984). He has held a Chartered Financial Analyst (CFA) designation since 1991.

Barry B. Bannister, CFAManaging Director, Equity ResearchStifel Nicolaus & [email protected]

3

Summary

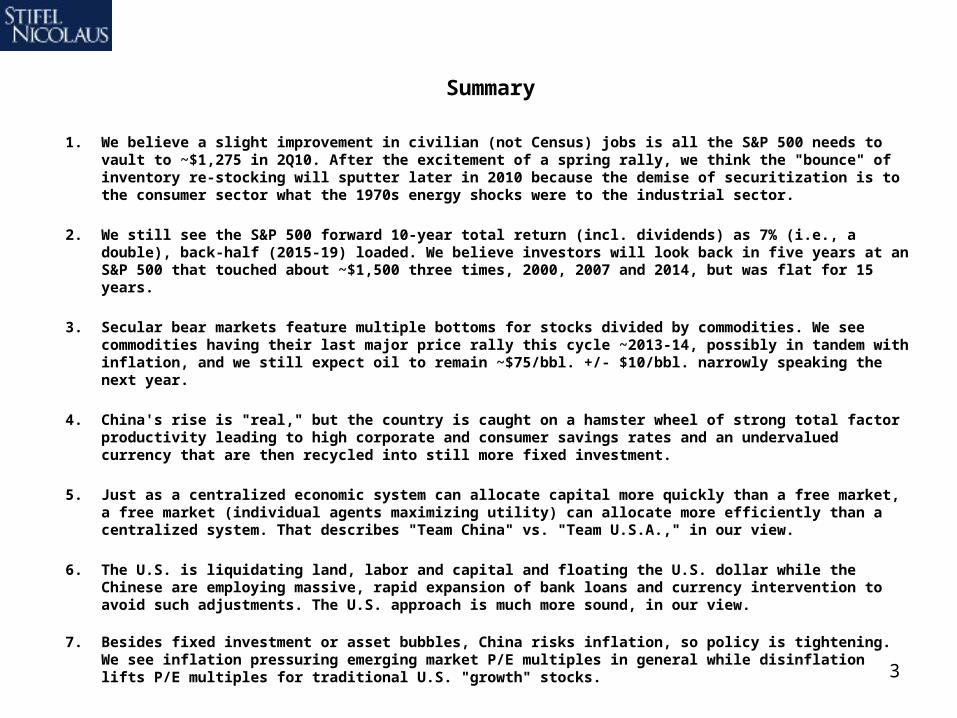

1. We believe a slight improvement in civilian (not Census) jobs is all the S&P 500 needs to vault to ~$1,275 in 2Q10. After the excitement of a spring rally, we think the "bounce" of inventory re-stocking will sputter later in 2010 because the demise of securitization is to the consumer sector what the 1970s energy shocks were to the industrial sector.

2. We still see the S&P 500 forward 10-year total return (incl. dividends) as 7% (i.e., a double), back-half (2015-19) loaded. We believe investors will look back in five years at an S&P 500 that touched about ~$1,500 three times, 2000, 2007 and 2014, but was flat for 15 years.

3. Secular bear markets feature multiple bottoms for stocks divided by commodities. We see commodities having their last major price rally this cycle ~2013-14, possibly in tandem with inflation, and we still expect oil to remain ~$75/bbl. +/- $10/bbl. narrowly speaking the next year.

4. China's rise is "real," but the country is caught on a hamster wheel of strong total factor productivity leading to high corporate and consumer savings rates and an undervalued currency that are then recycled into still more fixed investment.

5. Just as a centralized economic system can allocate capital more quickly than a free market, a free market (individual agents maximizing utility) can allocate more efficiently than a centralized system. That describes "Team China" vs. "Team U.S.A.," in our view.

6. The U.S. is liquidating land, labor and capital and floating the U.S. dollar while the Chinese are employing massive, rapid expansion of bank loans and currency intervention to avoid such adjustments. The U.S. approach is much more sound, in our view.

7. Besides fixed investment or asset bubbles, China risks inflation, so policy is tightening. We see inflation pressuring emerging market P/E multiples in general while disinflation lifts P/E multiples for traditional U.S. "growth" stocks.

4

Deflation vs. Inflation

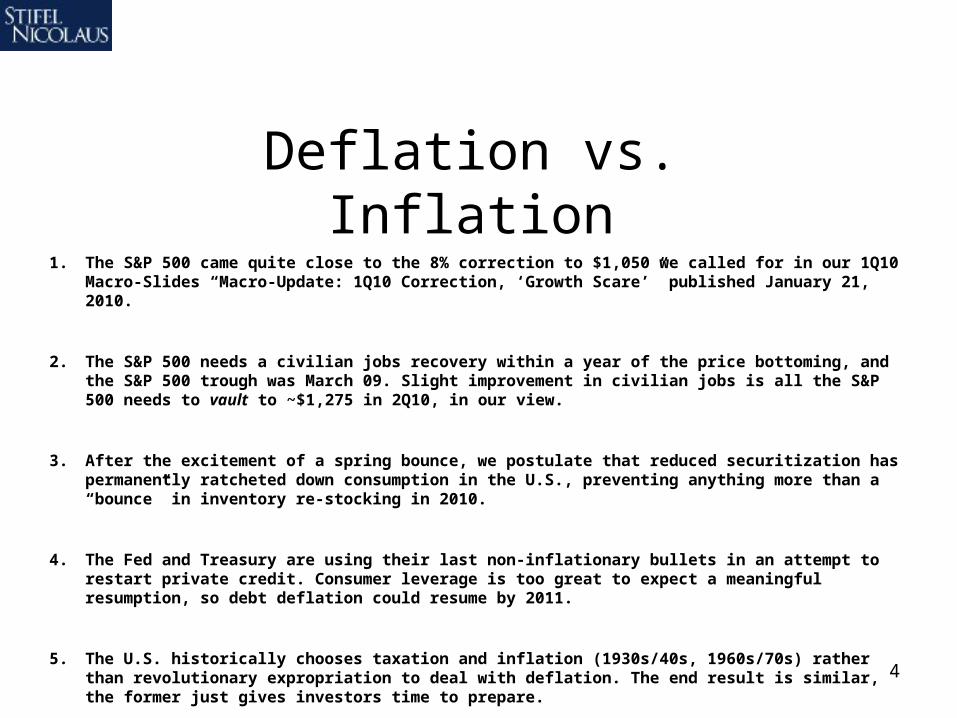

1. The S&P 500 came quite close to the 8% correction to $1,050 we called for in our 1Q10 Macro-Slides “Macro-Update: 1Q10 Correction, ‘Growth Scare’” published January 21, 2010.

2. The S&P 500 needs a civilian jobs recovery within a year of the price bottoming, and the S&P 500 trough was March 09. Slight improvement in civilian jobs is all the S&P 500 needs to vault to ~$1,275 in 2Q10, in our view.

3. After the excitement of a spring bounce, we postulate that reduced securitization has permanently ratcheted down consumption in the U.S., preventing anything more than a “bounce” in inventory re-stocking in 2010.

4. The Fed and Treasury are using their last non-inflationary bullets in an attempt to restart private credit. Consumer leverage is too great to expect a meaningful resumption, so debt deflation could resume by 2011.

5. The U.S. historically chooses taxation and inflation (1930s/40s, 1960s/70s) rather than revolutionary expropriation to deal with deflation. The end result is similar, the former just gives investors time to prepare.

5

Debt as a Percentage of U.S. GDP, by Category

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

1952

Q1

1955

Q3

1959

Q1

1962

Q3

1966

Q1

1969

Q3

1973

Q1

1976

Q3

1980

Q1

1983

Q3

1987

Q1

1990

Q3

1994

Q1

1997

Q3

2001

Q1

2004

Q3

2008

Q1

2011

Q3

2015

Q1

Financial Debt / US GDP

Public Nonfinancial Debt / US GDP

Private Nonfinancial Household Debt / US GDPPrivate Nonfinancial Business Debt / US GDP

Change in debt since the peak as a % of GDP (bps):

Financial debt Peak: 1Q09 Change: -700 bpsPrivate household Peak: 2Q09 Change: -100 bpsPrivate business Peak: 2Q09 Change: -100 bpsPublic debt Bottom: 2Q08 Change: +1,700 bps= Total debt/GDP up from 354% (2Q08) to 370% (3Q09)

Civilian Non-Institutional* Employment to Population Ratio versus S&P 500 Index (log scale)

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

Jan

-70

Jan

-72

Jan

-74

Jan

-76

Jan

-78

Jan

-80

Jan

-82

Jan

-84

Jan

-86

Jan

-88

Jan

-90

Jan

-92

Jan

-94

Jan

-96

Jan

-98

Jan

-00

Jan

-02

Jan

-04

Jan

-06

Jan

-08

Jan

-10

Jan

-12

10

100

1,000

10,000

Civilian Employment to Population Ratio (Left Axis)

S&P 500 Index (log Scale, Right Axis)

?

12 mos. 9

mos.

9 mos.

14mos.

12mos.

*The civilian non-institutional population consists of persons 16 years of age and older residing in the 50 States and the District of Columbia who are not inmates of institutions (for example, penal and mental facilities and homes for the aged) and who are not on active duty in the Armed Forces.

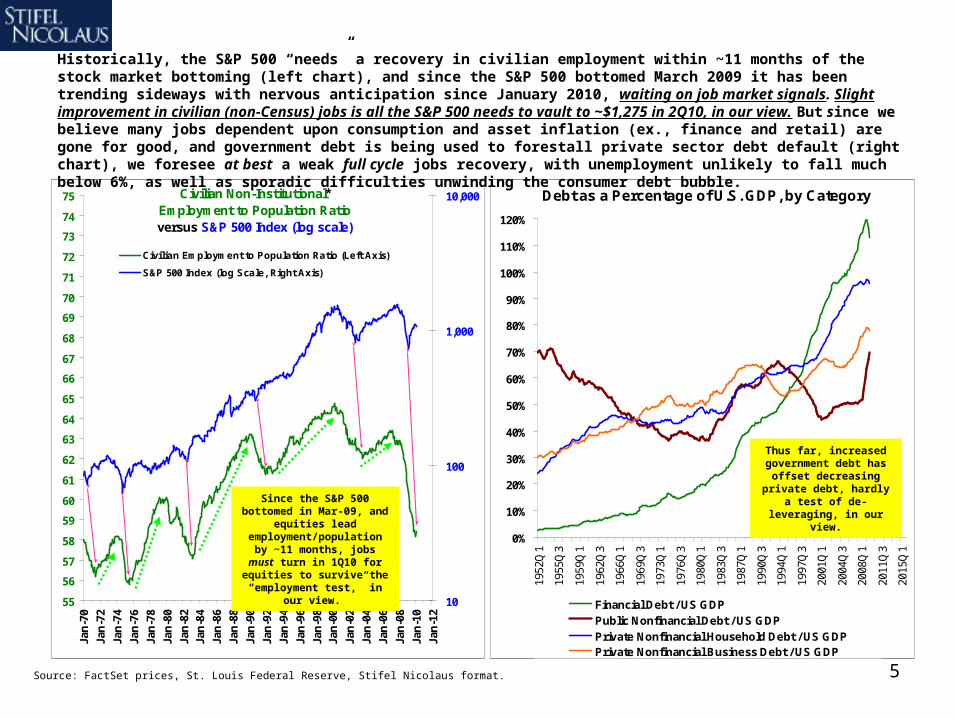

Historically, the S&P 500 “needs” a recovery in civilian employment within ~11 months of the stock market bottoming (left chart), and since the S&P 500 bottomed March 2009 it has been trending sideways with nervous anticipation since January 2010, waiting on job market signals. Slight improvement in civilian (non-Census) jobs is all the S&P 500 needs to vault to ~$1,275 in 2Q10, in our view. But since we believe many jobs dependent upon consumption and asset inflation (ex., finance and retail) are gone for good, and government debt is being used to forestall private sector debt default (right chart), we foresee at best a weak full cycle jobs recovery, with unemployment unlikely to fall much below 6%, as well as sporadic difficulties unwinding the consumer debt bubble.

Source: FactSet prices, St. Louis Federal Reserve, Stifel Nicolaus format.

Since the S&P 500 bottomed in Mar-09, and equities lead employment/population by ~11 months, jobs must turn

in 1Q10 for equities to survive the “employment

test,” in our view.

Thus far, increased government debt has

offset decreasing private debt, hardly a test of de-leveraging, in our view.

6Source: Bank Credit Analyst

Most of the arguments for domestic GDP recovery that we hear involve an inventory re-stocking argument. (Commodity recovery appears to depend on Chinese bank loans, but we discuss that later). We postulate that the demise of securitization (issuance of securities that ‘package’ many individual consumer debts such as credit cards and mortgages) in the current era is analogous to the 1970s energy shocks. Recall that the 1973-1974 first energy shock rendered a large swath of industrial America effectively obsolete in the 1970s due to its inefficient energy intensity (think Chrysler’s first bail-out). That capacity limped along until it was finished off by the second oil shock in 1979-1980 as well as U.S. Fed moves to deal with price inflation (high real interest rates, a strong dollar). We suspect that the demise of securitization has permanently ratcheted down U.S. consumer spending, reducing the need for anything more than a “bounce” in inventory. Weaker retail and financial capacity may limp along for a few years until it is finished off in a shake-out, in our view.

7Source: Historical Statistics of the United States, Millennial Edition, U.S. Census.

U.S. GDP per capita for 209 years has grown at 1.6%/year, with population growth of 2.0% and real GDP growth of 3.6%. Recent trends have supported at least 2% growth in productivity, and for the past decade the U.S. population has grown at a fairly consistent 1.0%. This indicates that at least 3.0% (2% + 1%) U.S. real GDP growth can be maintained in a normal credit environment, in our view. If deleveraging the consumption side of the U.S. economy causes U.S. per capita real GDP to converge on the long-term trend shown in the chart below; however, such a process would be a headwind for growth shaving perhaps 150bps/year from U.S. real GDP/capita over perhaps five years, which is not “fatal,” in our view.

Log of U.S. Real GDP per Capita, 1800 to 2009Trend growth since 1800 of 1.6%, with population growth of 2.0% and U.S. real GDP growth of 3.6%

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

18

00

18

10

18

20

18

30

18

40

18

50

18

60

18

70

18

80

18

90

19

00

19

10

19

20

19

30

19

40

19

50

19

60

19

70

19

80

19

90

20

00

20

10

E

Trend 1.6%U.S. GDP/capita

growth

To return to trend U.S.

GDP would have to

decline 12% (twelve

percent) at once, or

somewhat less over

time.

8

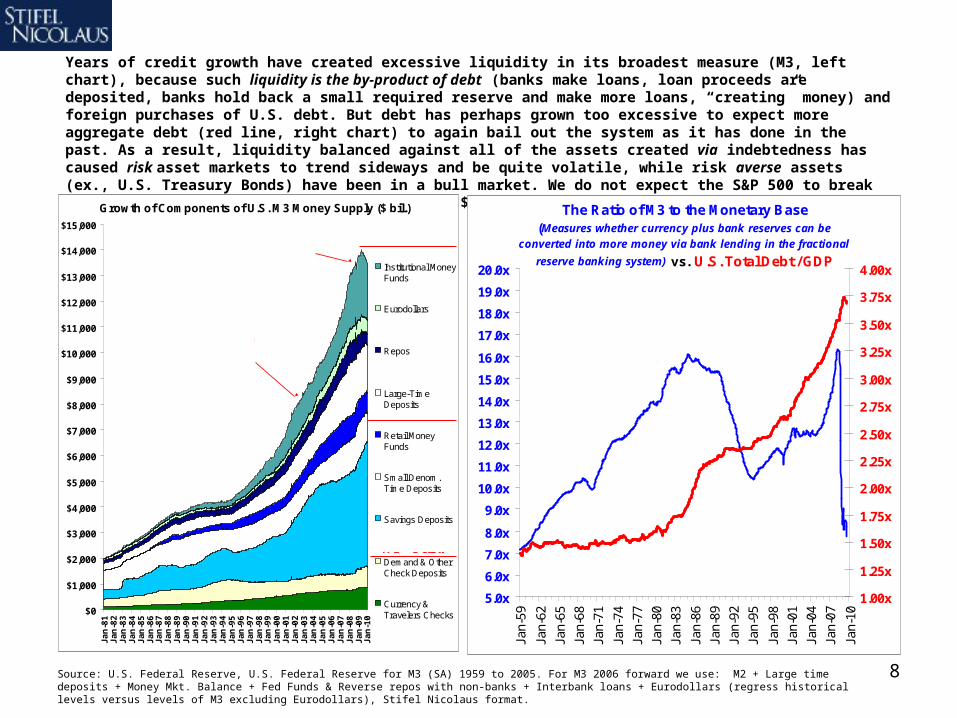

Years of credit growth have created excessive liquidity in its broadest measure (M3, left chart), because such liquidity is the by-product of debt (banks make loans, loan proceeds are deposited, banks hold back a small required reserve and make more loans, “creating” money) and foreign purchases of U.S. debt. But debt has perhaps grown too excessive to expect more aggregate debt (red line, right chart) to again bail out the system as it has done in the past. As a result, liquidity balanced against all of the assets created via indebtedness has caused risk asset markets to trend sideways and be quite volatile, while risk averse assets (ex., U.S. Treasury Bonds) have been in a bull market. We do not expect the S&P 500 to break out of its 2000 to 2010 price range of ~$667-$1,576 until 2015.

Source: U.S. Federal Reserve, U.S. Federal Reserve for M3 (SA) 1959 to 2005. For M3 2006 forward we use: M2 + Large time deposits + Money Mkt. Balance + Fed Funds & Reverse repos with non-banks + Interbank loans + Eurodollars (regress historical levels versus levels of M3 excluding Eurodollars), Stifel Nicolaus format.

The Ratio of M3 to the Monetary Base (Measures whether currency plus bank reserves can be

converted into more money via bank lending in the fractional

reserve banking system) vs. U.S. Total Debt / GDP

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

15.0x

16.0x

17.0x

18.0x

19.0x

20.0x

Jan-

59

Jan-

62

Jan-

65

Jan-

68

Jan-

71

Jan-

74

Jan-

77

Jan-

80

Jan-

83

Jan-

86

Jan-

89

Jan-

92

Jan-

95

Jan-

98

Jan-

01

Jan-

04

Jan-

07

Jan-

10

1.00x

1.25x

1.50x

1.75x

2.00x

2.25x

2.50x

2.75x

3.00x

3.25x

3.50x

3.75x

4.00x

M3/Monetary Base (Left)

Total Debt/GDP

(Right)

Growth of Components of U.S. M3 Money Supply ($ bil.)

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$12,000

$13,000

$14,000

$15,000

Ja

n-8

1J

an

-82

Ja

n-8

3J

an

-84

Ja

n-8

5J

an

-86

Ja

n-8

7J

an

-88

Ja

n-8

9J

an

-90

Ja

n-9

1J

an

-92

Ja

n-9

3J

an

-94

Ja

n-9

5J

an

-96

Ja

n-9

7J

an

-98

Ja

n-9

9J

an

-00

Ja

n-0

1J

an

-02

Ja

n-0

3J

an

-04

Ja

n-0

5J

an

-06

Ja

n-0

7J

an

-08

Ja

n-0

9J

an

-10

Institutional MoneyFunds

Eurodollars

Repos

Large-TimeDeposits

Retail MoneyFunds

Small Denom.Time Deposits

Savings Deposits

Demand & OtherCheck Deposits

Currency &Travelers Checks

M2 = Below

Sum = M3

M1 = Below

A combination of importing the

savings of emerging markets and using leverage (money

multiplier) to grow money supply.

The multiplier has subsided, hence

fiscal stimulus and quantitative easing.

9

S&P 500 y/y% Earnings Growth (Trailing 4-quarter Sum)

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%19

55Q

1

1956

Q3

1958

Q1

1959

Q3

1961

Q1

1962

Q3

1964

Q1

1965

Q3

1967

Q1

1968

Q3

1970

Q1

1971

Q3

1973

Q1

1974

Q3

1976

Q1

1977

Q3

1979

Q1

1980

Q3

1982

Q1

1983

Q3

1985

Q1

1986

Q3

1988

Q1

1989

Q3

1991

Q1

1992

Q3

1994

Q1

1995

Q3

1997

Q1

1998

Q3

2000

Q1

2001

Q3

2003

Q1

2004

Q3

2006

Q1

2007

Q3

2009

Q1

1955Q1 through 2009Q4

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1955

Q1

1956

Q3

1958

Q1

1959

Q3

1961

Q1

1962

Q3

1964

Q1

1965

Q3

1967

Q1

1968

Q3

1970

Q1

1971

Q3

1973

Q1

1974

Q3

1976

Q1

1977

Q3

1979

Q1

1980

Q3

1982

Q1

1983

Q3

1985

Q1

1986

Q3

1988

Q1

1989

Q3

1991

Q1

1992

Q3

1994

Q1

1995

Q3

1997

Q1

1998

Q3

2000

Q1

2001

Q3

2003

Q1

2004

Q3

2006

Q1

2007

Q3

2009

Q1

S&P 500 Price y/y% Change(Trailing 4-quarter Average)

1955Q1 through 2010Q1

4Q2009 = 246.2%

Sou

rce:

Fac

tSet

, S

tifel

Nic

olau

s, S

tand

ard

& P

oor’s

.

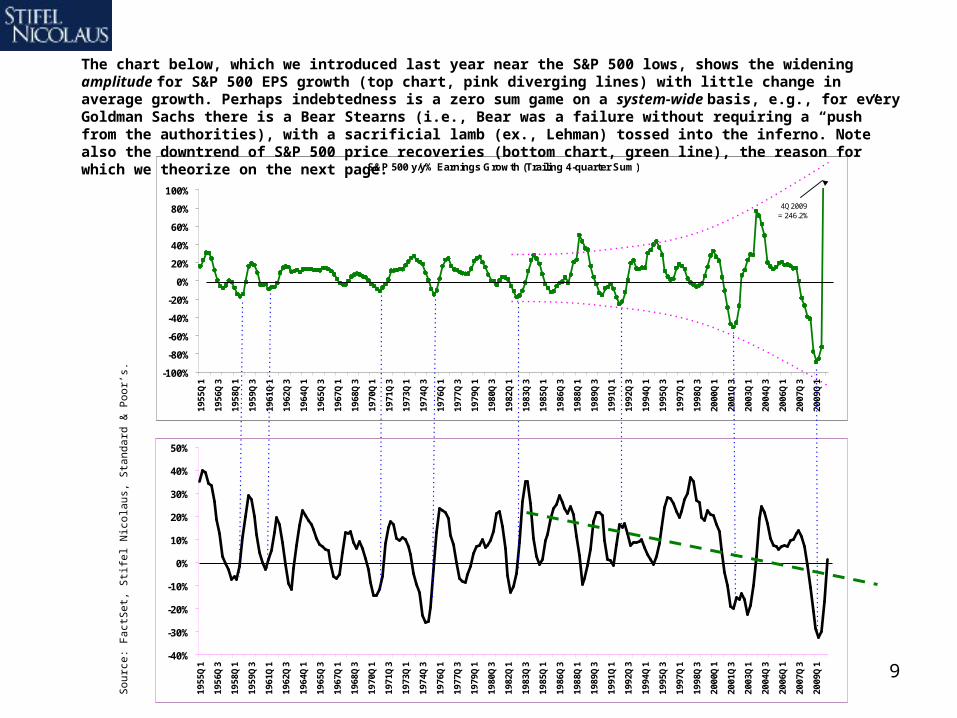

The chart below, which we introduced last year near the S&P 500 lows, shows the widening amplitude for S&P 500 EPS growth (top chart, pink diverging lines) with little change in average growth. Perhaps indebtedness is a zero sum game on a system-wide basis, e.g., for every Goldman Sachs there is a Bear Stearns (i.e., Bear was a failure without requiring a “push” from the authorities), with a sacrificial lamb (ex., Lehman) tossed into the inferno. Note also the downtrend of S&P 500 price recoveries (bottom chart, green line), the reason for which we theorize on the next page.

10

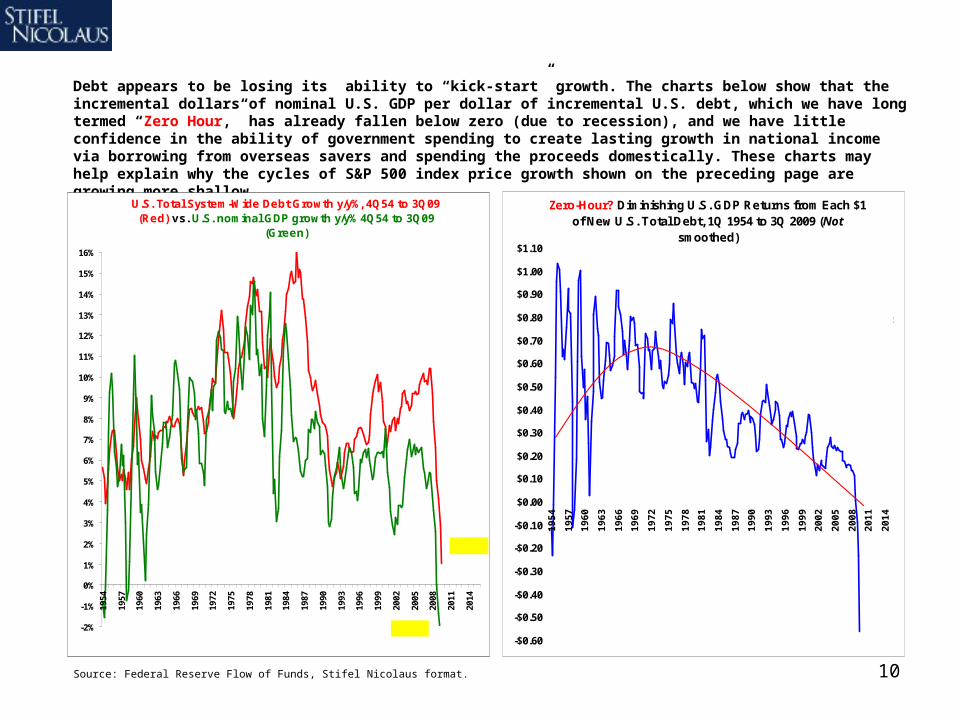

Debt appears to be losing its ability to “kick-start” growth. The charts below show that the incremental dollars of nominal U.S. GDP per dollar of incremental U.S. debt, which we have long termed “Zero Hour,” has already fallen below zero (due to recession), and we have little confidence in the ability of government spending to create lasting growth in national income via borrowing from overseas savers and spending the proceeds domestically. These charts may help explain why the cycles of S&P 500 index price growth shown on the preceding page are growing more shallow.

Source: Federal Reserve Flow of Funds, Stifel Nicolaus format.

U.S. Total System-Wide Debt Growth y/y%, 4Q54 to 3Q09 (Red) vs. U.S. nominal GDP growth y/y% 4Q54 to 3Q09

(Green)

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

One...

Two?

Zero-Hour? Diminishing U.S. GDP Returns from Each $1 of New U.S. Total Debt, 1Q 1954 to 3Q 2009 (Not

smoothed)

-$0.60

-$0.50

-$0.40

-$0.30

-$0.20

-$0.10

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

19

54

19

57

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

20

08

20

11

20

14

Dollar change y/y in U.S. Nominal GDP divided by dollar change y/y

in U.S. Debt equals the dollar increase in GDP per $1.00

increase in U.S. Total Debt. It went below zero in 1Q09.

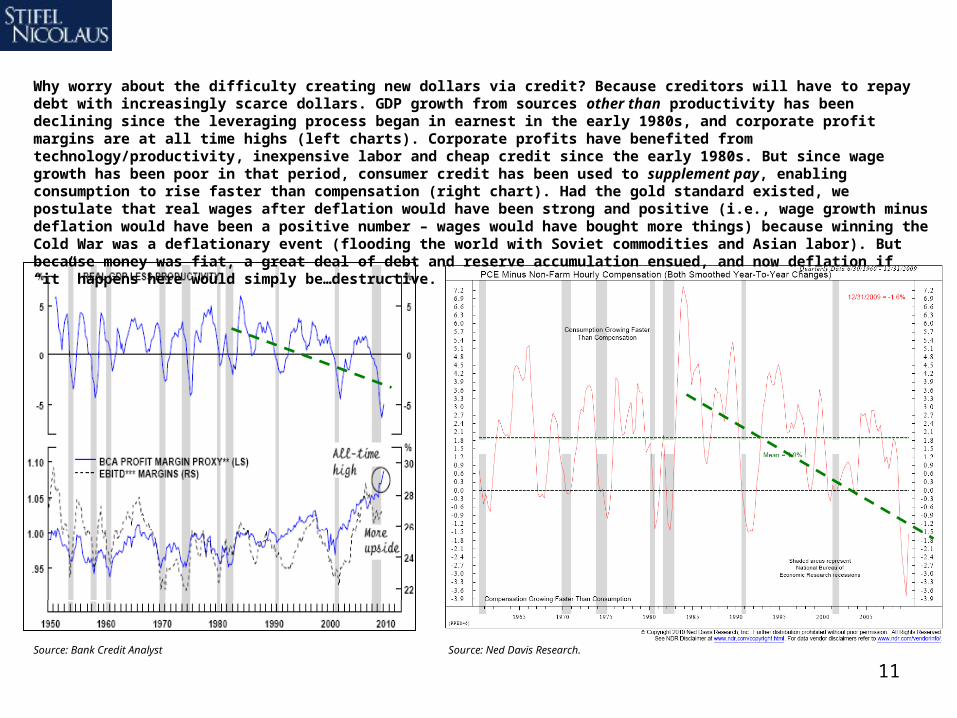

11Source: Ned Davis Research.Source: Bank Credit Analyst

Why worry about the difficulty creating new dollars via credit? Because creditors will have to repay debt with increasingly scarce dollars. GDP growth from sources other than productivity has been declining since the leveraging process began in earnest in the early 1980s, and corporate profit margins are at all time highs (left charts). Corporate profits have benefited from technology/productivity, inexpensive labor and cheap credit since the early 1980s. But since wage growth has been poor in that period, consumer credit has been used to supplement pay, enabling consumption to rise faster than compensation (right chart). Had the gold standard existed, we postulate that real wages after deflation would have been strong and positive (i.e., wage growth minus deflation would have been a positive number – wages would have bought more things) because winning the Cold War was a deflationary event (flooding the world with Soviet commodities and Asian labor). But because money was fiat, a great deal of debt and reserve accumulation ensued, and now deflation if “it” happens here would simply be…destructive.

12

Federal Reserve Bank Assets & Liabilities

-$2,500

-$2,000

-$1,500

-$1,000

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

5-S

ep-0

7

5-N

ov-

07

5-Ja

n-0

8

5-M

ar-0

8

5-M

ay-0

8

5-Ju

l-08

5-S

ep-0

8

5-N

ov-

08

5-Ja

n-0

9

5-M

ar-0

9

5-M

ay-0

9

5-Ju

l-09

5-S

ep-0

9

5-N

ov-

09

Liquidity Facilities

Other

Repurchase Agreements

Term Auction Credit

Securities Held Outright

Reserve Balances withFederal Reserve Banks

Treasury SupplementaryFinancing Program (SPF)

Other

Currency in Circulation

Assets

Liabilities

$ Billion

In an attempt to restart the credit process the Fed has been a large purchaser of assets (mortgages). After sterilizing early intervention in 1H08 with a $300B Treasury sale (point “A”), the Fed repurchased those Treasuries in 1Q09 (i.e., so-called Quantitative Easing, shown as point “B”) and that restarted the market’s engine, helping the S&P 500 put in its March 6, 2009 low of $667. The market liked the Fed’s actions so much that the Fed kept going, buying Agency debt (point “C”). As liquidity facilities have been wound down (point “D”) the lender of last resort has simply become the buyer of last resort, hardly a testament to strength.

Source: U.S. Federal Reserve.

A B

C

D

13Source: Ned Davis Research.

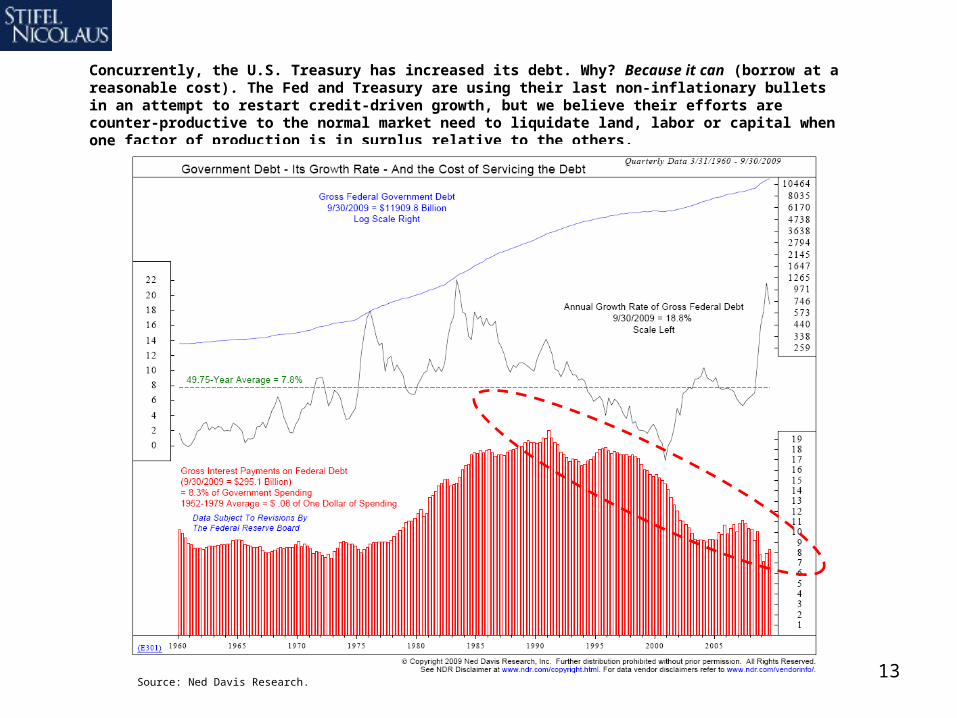

Concurrently, the U.S. Treasury has increased its debt. Why? Because it can (borrow at a reasonable cost). The Fed and Treasury are using their last non-inflationary bullets in an attempt to restart credit-driven growth, but we believe their efforts are counter-productive to the normal market need to liquidate land, labor or capital when one factor of production is in surplus relative to the others.

14

Source: Ned Davis Research.

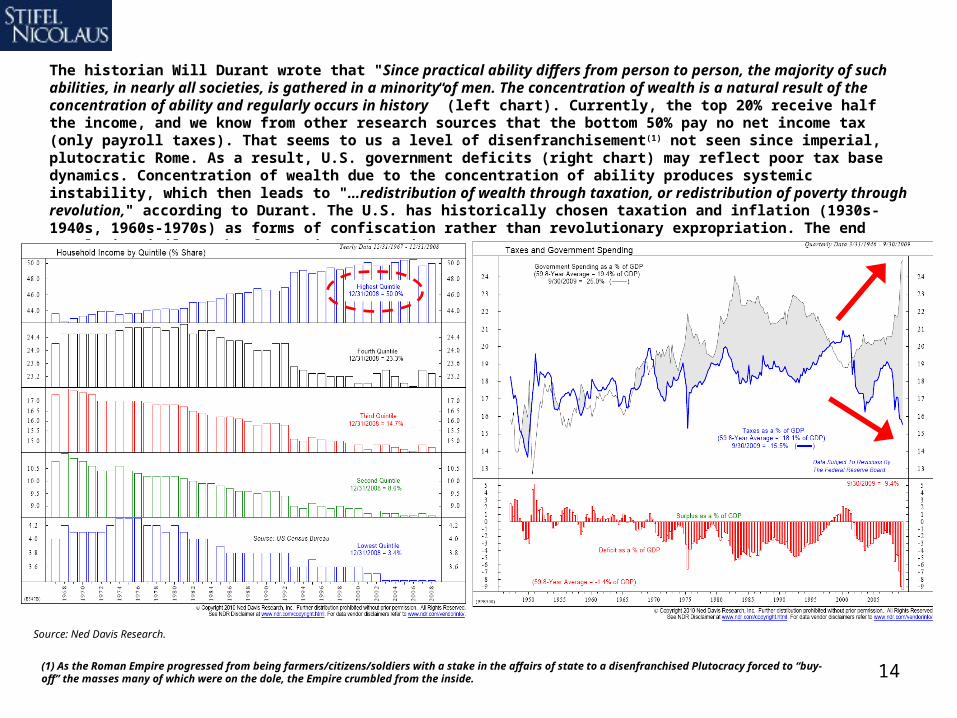

The historian Will Durant wrote that "Since practical ability differs from person to person, the majority of such abilities, in nearly all societies, is gathered in a minority of men. The concentration of wealth is a natural result of the concentration of ability and regularly occurs in history” (left chart). Currently, the top 20% receive half the income, and we know from other research sources that the bottom 50% pay no net income tax (only payroll taxes). That seems to us a level of disenfranchisement(1) not seen since imperial, plutocratic Rome. As a result, U.S. government deficits (right chart) may reflect poor tax base dynamics. Concentration of wealth due to the concentration of ability produces systemic instability, which then leads to "…redistribution of wealth through taxation, or redistribution of poverty through revolution," according to Durant. The U.S. has historically chosen taxation and inflation (1930s-1940s, 1960s-1970s) as forms of confiscation rather than revolutionary expropriation. The end result is similar, the former just gives investors more time to prepare.

(1) As the Roman Empire progressed from being farmers/citizens/soldiers with a stake in the affairs of state to a disenfranchised Plutocracy forced to “buy-off” the masses many of which were on the dole, the Empire crumbled from the inside.

15Source: “A New Historical Database for the NYSE 1815 to 1925: Performance and Predictability” William N. Goetzmann, Roger G. Ibbotson, Liang Peng, Yale School of Management; 1925-to-present are Ibbotson Associates large-cap total return and Standard & Poor’s data.

In closing this section of our report, investors in 2008 & 2009 were whipsawed by the best and worst years, back-to-back, in a half century for stocks relative to long-term U.S. government bonds. The U.S. dollar mirrored those moves, soaring and plunging. We think this turn of events marks the end, or at least the terminal phase, of credit-driven asset inflation and moral hazard related to guarantees. At this point we are simply interested in the mechanics of de-leveraging and the implications of consumer credit retrenchment for the U.S. equity market.

Total Return of Large Cap Stocks Minus Total Return of Long-Term Government Bonds

-80%

-60%

-40%

-20%

0%

20%

40%

60%

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

E

2008: Worst year in a half century for U.S.

stocks relative to long-term Treasuries.

2009: Best year in a half century for U.S.

stocks relative to long-term Treasuries.

16

U.S. Equity Market Outlook1. Longer term, from Dec-2009 to Dec-2019, we expect the S&P 500, dividends reinvested, to produce a back-

half (i.e., mostly 2015 to 2019) loaded 7% CAGR return (i.e., a price double with dividends reinvested).

2. Intermediate term, we do not expect the S&P 500 to break out of its 2000 to 2010 price range of ~$667-$1,576 until 2015, thus forming a classic secular bear market 15-year trading range.

3. An S&P 500 price of ~$1,100 (close to the current price) is the midpoint of the 10-year secular bear market range. This price may be thought of as a “ledge” or a “step,” depending on the investor’s outlook.

4. Short-term, we believe the S&P 500 price moves up from the $1,100 midpoint outlined above, but we remain alert and have no intention of fighting the tape (a wise strategy in a range-bound market).

5. The nominal low in a secular bear market is usually ~7-10 years before a new secular bull market begins; Mar-09 ($667) appears to us to have been the nominal low, although inflation could produce a deeper “real” or inflation-adjusted low by 2015. We are taking a wait-and-see approach to inflation.

17

S&P Stock Market Composite 10-Year Compound Annual Total Return (Incl. Reinvested Dividends) Data 1830 to February-23-2010

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

1839

1849

1859

1869

1879

1889

1899

1909

1919

1929

1939

1949

1959

1969

1979

1989

1999

2009

Source: “A New Historical Database for the NYSE 1815 to 1925: Performance and Predictability” William N. Goetzmann, Roger G. Ibbotson, Liang Peng, Yale School of Management; 1925-to-present are Ibbotson Associates large-cap total return and Standard & Poor’s data.

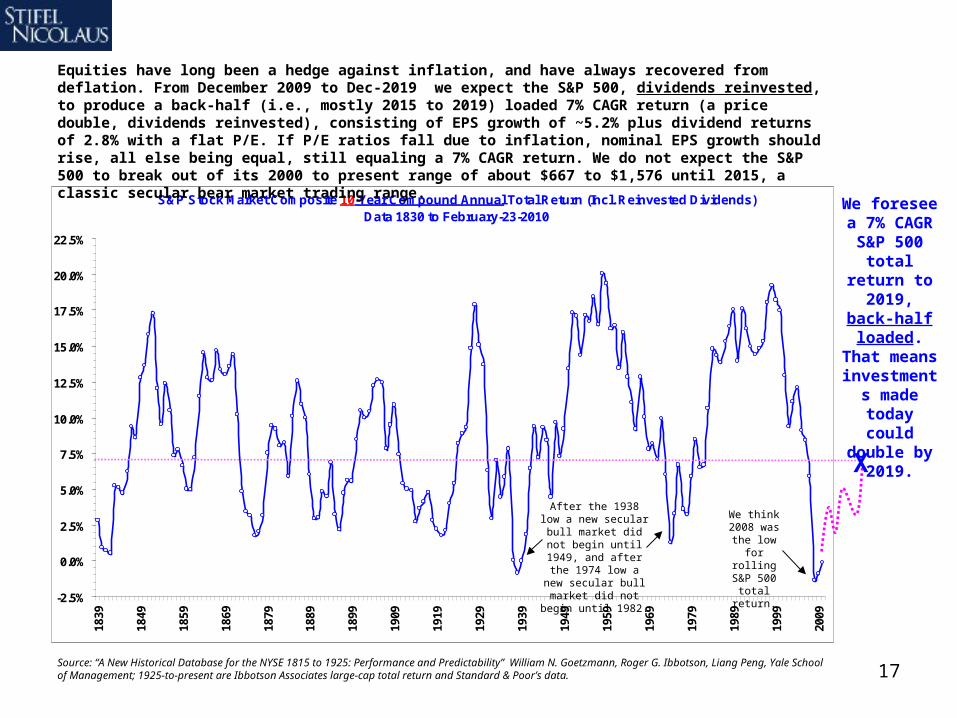

Equities have long been a hedge against inflation, and have always recovered from deflation. From December 2009 to Dec-2019 we expect the S&P 500, dividends reinvested, to produce a back-half (i.e., mostly 2015 to 2019) loaded 7% CAGR return (a price double, dividends reinvested), consisting of EPS growth of ~5.2% plus dividend returns of 2.8% with a flat P/E. If P/E ratios fall due to inflation, nominal EPS growth should rise, all else being equal, still equaling a 7% CAGR return. We do not expect the S&P 500 to break out of its 2000 to present range of about $667 to $1,576 until 2015, a classic secular bear market trading range.

We foresee a 7% CAGR S&P 500

total return to 2019,

back-half loaded. That

means investments made today

could double by 2019.

X

After the 1938 low a new secular bull

market did not begin until 1949, and after the 1974 low a new

secular bull market did not begin until 1982.

We think 2008 was the low

for rolling S&P 500 total return.

18

Secular bear markets flatten in nominal terms (but decline in real terms, after inflation) for ~14 years (average of the past cycles below), and this secular bear began in 2000. The nominal low in a secular bear is usually seen ~7-10 years before a new secular bull begins, and we believe 2009 may have been the nominal low in this cycle. We believe secular bear markets end when equity has been de-capitalized as a percentage of GDP and all types of investors have been impacted, e.g., buy and hold loses capital or purchasing power, momentum buys high/sells low several times, and market timers lose because increased awareness of the secular bear market causes rallies to expend the bulk of their return quickly (ex., the 2009 rally).

Source: Dow Jones, U.S. Census, Stifel Nicolaus format.

Real (Inflation-adjusted) Dow Jones Industrial Average (2008$) versus Nominal Dow Jones Industrial Average - Chart is through most current data

$10

$100

$1,000

$10,000

$100,000

1896

1901

1906

1911

1916

1921

1926

1931

1936

1941

1946

1951

1956

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

1907 to 19211929 to 1942

1966 to 1982

2000 to ….Inflation-adjusted Dow

Jones Industrial Average

Dow Jones Industrial Average

1914wasthelow

1921new

secularbull

market

1932wasthelow

1942new

secularbull

market

1974wasthelow

1982new

secularbull

market

2009wasthe

secular bear

nominallow, in

our view.

19

M2 Growth vs. CPI GrowthAverage Annual Growth

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11%

M2 Money Supply (Average Annual Percent Growth)

CP

I Gro

wth

(A

vera

ge

An

nu

al P

erce

nt

Gro

wth

)

1920s

1940s

1950s

1930s

1960s

1990s

1980s

1970s1910s

2000s

Trailing 2-year range of actual M2 growth = 5% to 10% y/y

Source: Standard & Poor’s, U.S. Census, NBER.org Macro-history Database, Federal Reserve.

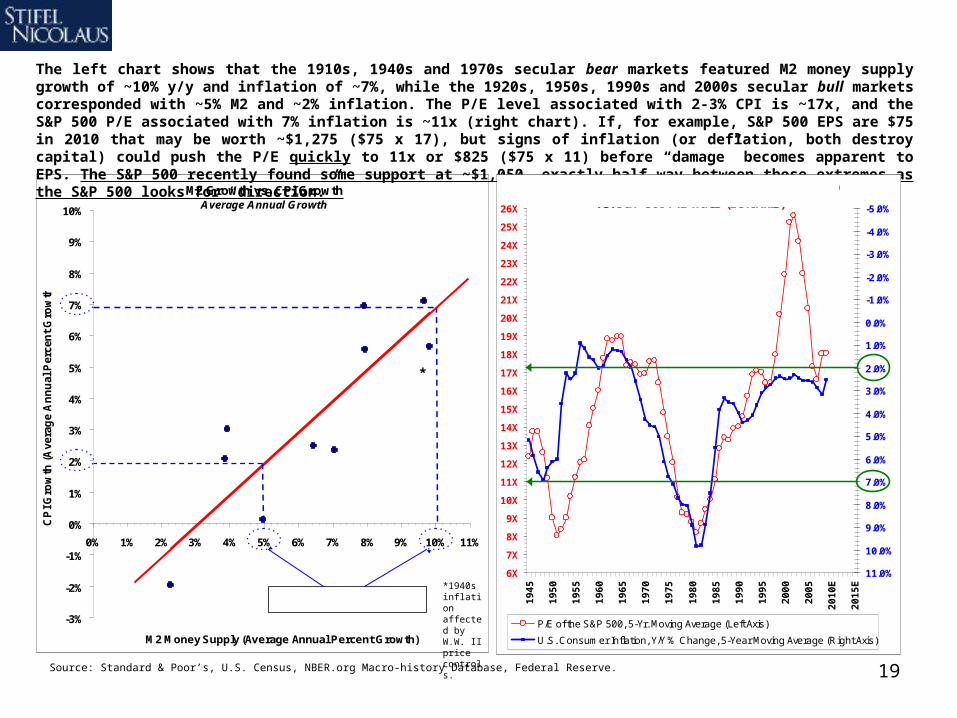

The left chart shows that the 1910s, 1940s and 1970s secular bear markets featured M2 money supply growth of ~10% y/y and inflation of ~7%, while the 1920s, 1950s, 1990s and 2000s secular bull markets corresponded with ~5% M2 and ~2% inflation. The P/E level associated with 2-3% CPI is ~17x, and the S&P 500 P/E associated with 7% inflation is ~11x (right chart). If, for example, S&P 500 EPS are $75 in 2010 that may be worth ~$1,275 ($75 x 17), but signs of inflation (or deflation, both destroy capital) could push the P/E quickly to 11x or $825 ($75 x 11) before “damage” becomes apparent to EPS. The S&P 500 recently found some support at ~$1,050, exactly half way between those extremes as the S&P 500 looks for “direction.”

*

*1940s inflation affected by W.W. II price controls.

6X

7X

8X

9X

10X

11X

12X

13X

14X

15X

16X

17X

18X

19X

20X

21X

22X

23X

24X

25X

26X

19

45

19

50

19

55

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

E

20

15

E

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

P/E of the S&P 500, 5-Yr. Moving Average (Left Axis)

U.S. Consumer Inflation, Y/Y % Change, 5-Year Moving Average (Right Axis)

U.S. Consumer Price Inflation (Inverted, Right Axis) vs. S&P 500 P/E Ratio (Left Axis)

20

Crude Oil Factors to Consider

1. The balance of years in the next several probably favor the price return of U.S. equities over commodities until such time that inflation materializes, which we do not expect until ~2013, if at all.

2. Secular bear markets featured multiple bottoms for stocks relative to commodities before a sustained bull market for equities may begin. We see commodities their last major price rally ~2013-14 for this cycle.

3. We’re nimbly “trend following” rather than making hard projections, but we think oil has more down than upside, while the S&P 500 only needs modest – not strong – recovery in civilian jobs to vault higher.

4. We expect oil to remain ~$75/bbl. +/- $10/bbl. narrowly speaking, and at most $53/bbl. to $89/bbl. very broadly speaking through 2012. Equities closely correlated to oil prices may follow the trend in oil.

21

U.S. Commodity Price Index*, y/y% change, 1912 to 2010 latest, 5-yr. M.A. versus Deere relative to the S&P 500 1927 to Present

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

1912

1918

1924

1930

1936

1942

1948

1954

1960

1966

1972

1978

1984

1990

1996

2002

2008

2014

E

Co

mm

od

ity

Pri

ce

s,

y/y

%,

5-y

r. m

ov

. a

vg

.

0%

1%

2%

3%

4%

5%

6%

7%

Dee

re s

tock

div

ided

by

the

S&

P 5

00

Commodity Price Index, y/y % change, 5-yr. moving average, left axis

Deere stock relative to the S&P 500 (S&P Composite in earliest periods), right axis

* P roducer P rice Index for Commodities 1907-56, CRB Futures 1957-present

Crude oil and FLR stock relative strength versus the S&P 500, 1965 to 2010 latest

0%

5%

10%

15%

20%

25%

30%

35%

40%

De

c-6

5

De

c-6

7

De

c-6

9

De

c-7

1

De

c-7

3

De

c-7

5

De

c-7

7

De

c-7

9

De

c-8

1

De

c-8

3

De

c-8

5

De

c-8

7

De

c-8

9

De

c-9

1

De

c-9

3

De

c-9

5

De

c-9

7

De

c-9

9

De

c-0

1

De

c-0

3

De

c-0

5

De

c-0

7

De

c-0

9

WT

I o

il p

rice

rel

ativ

e to

th

e S

&P

500

0%

3%

5%

8%

10%

13%

15%

18%

20%

23%

25%

28%

FL

R p

rice

rel

ativ

e to

th

e S

&P

500

WTI oil price relative to the S&P 500 FLR price relative to the S&P 500

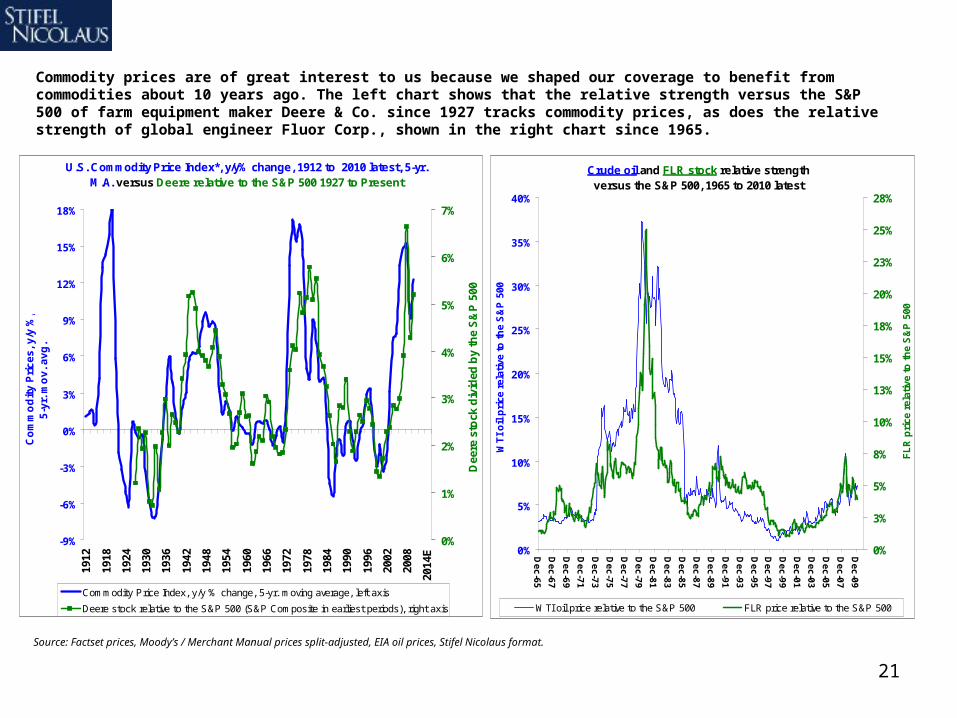

Commodity prices are of great interest to us because we shaped our coverage to benefit from commodities about 10 years ago. The left chart shows that the relative strength versus the S&P 500 of farm equipment maker Deere & Co. since 1927 tracks commodity prices, as does the relative strength of global engineer Fluor Corp., shown in the right chart since 1965.

Source: Factset prices, Moody’s / Merchant Manual prices split-adjusted, EIA oil prices, Stifel Nicolaus format.

22

Commodity price momentum appears to be coming off a cyclical high (left chart), while the S&P 500 total return (price change + dividend) momentum appears to be coming off a cyclical low (right chart). The balance of years in the next several probably favor U.S. equities over commodities until (if) inflation materializes, which we do not expect until ~2013.

Source: Stifel Nicolaus format, data Historical Statistics of the United States, a U.S. Census publication.

S&P Stock Market Composite 10-Year Compound Annual Total Return (Incl. Reinvested Dividends),

Data 1830 to Feb-23, 2010

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

1839

1849

1859

1869

1879

1889

1899

1909

1919

1929

1939

1949

1959

1969

1979

1989

1999

2009

Commodity prices are cyclical and move in unisonCommodities by category, data 1795 to January-2010, 10-yr. M.A.

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

1805

1810

1815

1820

1825

1830

1835

1840

1845

1850

1855

1860

1865

1870

1875

1880

1885

1890

1895

1900

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

All Commodities Fuels & Lighting

Cold War/Bretton Woods/OPEC

War of 1812

W.W. I I &

Korean Conflict

W.W. I

CivilWar

U.S. industrial

revolution & overheating / gold surplus.

Easy credit speculativeboom.

23

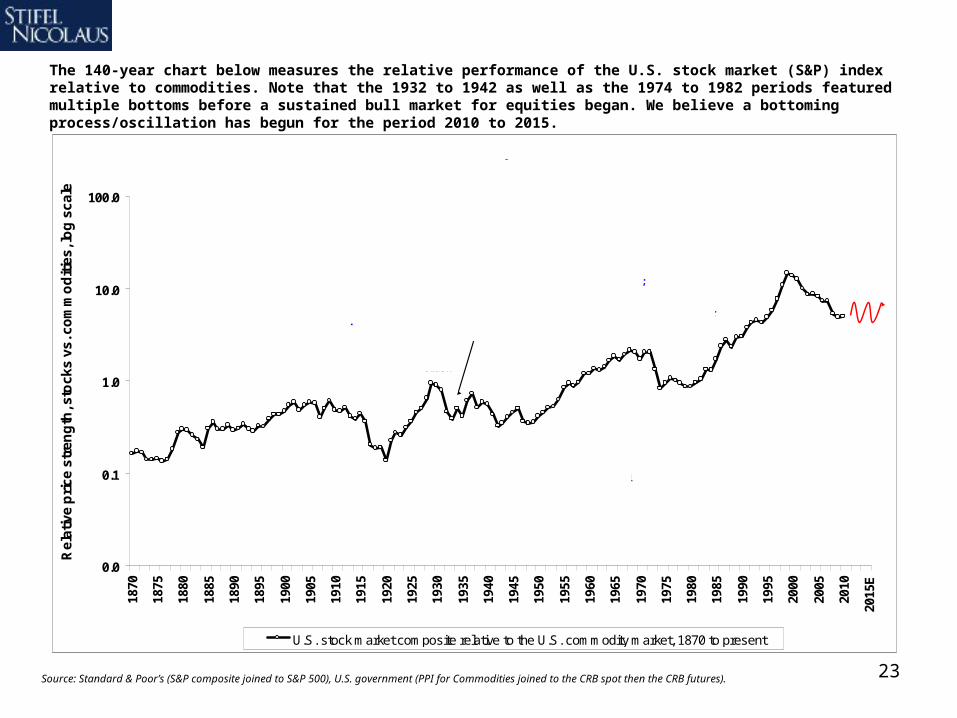

The 140-year chart below measures the relative performance of the U.S. stock market (S&P) index relative to commodities. Note that the 1932 to 1942 as well as the 1974 to 1982 periods featured multiple bottoms before a sustained bull market for equities began. We believe a bottoming process/oscillation has begun for the period 2010 to 2015.

Source: Standard & Poor’s (S&P composite joined to S&P 500), U.S. government (PPI for Commodities joined to the CRB spot then the CRB futures).

0.0

0.1

1.0

10.0

100.0

1870

1875

1880

1885

1890

1895

1900

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

E

Re

lati

ve

pri

ce

str

en

gth

, sto

ck

s v

s. c

om

mo

dit

ies

, lo

g s

ca

le

U.S. stock market composite relative to the U.S. commodity market, 1870 to present

Key: When the line is rising, the S&P stock market index beats the commodity price index and inflation eventually falls. When the line is falling, the opposite occurs.

U.S. Stock Market Relative to The Commodity Market, 1870 to December 1, 2009.

Post-Civil War Reconstruction ends in

1877, gold standard begins 1879,

deflationary boom, stocks rally.

Pearl Harbor, WW2

1939-45

Gold nationalized

U.S.$ devalued in 1933. FDR's "New Deal" &

reflation begins.

'29 Crash

Post-WW 1 commodity

bubble bursts, deflation ensues

in 1920, bull market begins.

WW11914 to

1918

OPEC '73 embargo;

1973-74 Bear Market, Iran

fell '79.

LBJ's Great Society +

Vietnam 1960s; Nixon closed gold window

1971, all inflationary.

Post-WW 2 commodity &

inflation bubble bursts ca. 1950,

disinflation ensues,

Eisenhower bull market begins.

OPEC overplays hand and oil prices collapse 1981, Volcker stops inflation

1981-82, then Reagan tax cuts, long Soviet

collapse, disinflation & bull market begin.

Tech Bubble 2000, 9/11, Mid-East wars, Asian oil use, strong global U.S.$ demand

after the 1990s emerging markets debt crisis, credit

crisis in U.S.

Populism in U.S. politics.

Panic of 1907, a banking crisis &

stock market crash.

24Source: Factset prices, Stifel Nicolaus format.

One asset’s 50% retracement……could be another asset’s

head-and-shoulders.

In the spirit of this momentum market, we’re nimbly “following the trend” rather than making projections, but if we had to speculate we believe oil is vulnerable for currency (U.S. dollar strength) and fundamental (OPEC 6mb/d over-capacity, as well as refined product over-capacity), whereas the S&P 500 only needs modest – not at all strong – recovery in civilian jobs to vault higher, especially if the “tax” on consumption of oil prices were to moderate.

S&P 500Daily price 1/1/05 to 2/18/10

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

50% retracecomplete

WTI Oil $/bbl. (blue)Daily price 1/1/05 to 2/18/10

$5

$15

$25

$35

$45

$55

$65

$75

$85

$95

$105

$115

$125

$135

$145

$155

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

An emerging head-and-

shoulders?

?

25

Nominal Trade-Weighted U.S.$ Major Currency Index, 1935 to 2009 (Left) versus U.S. GDP as a share of global GDP expressed in U.S. $, 1950 to 2010E (Right)

30

40

50

60

70

80

90

100

110

120

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

E

2015

E

No

min

al t

rad

e-w

eig

hte

d U

.S. $

12%

14%

16%

18%

20%

22%

24%

26%

28%

U.S

. GD

P s

har

e o

f g

lob

al G

DP

(ex

pre

ssed

in

U.S

. $)

Bretton WoodsAgreement

began U.S. dollar bubble; U.S. share

of world GDP dominates. Vietnam, social

programs, EU and Japan recovery weigh on dollar resulting is

gold outflows.

Emerging markets reserves increase,

dollar rallies.

Fed tightens 1969, dollar rallies, Martin > Burns Fed transition 1970 then Bretton

Woods abandoned 1971

Fed's Volcker hikes rates sharply.

Source: U.S. GDP with a base year 1990 links the OECD Geary-Khamis 1950 to 1979 series to the IMF World Economic Outlook 1980 to present series, including 2009 & 2010 estimates. U.S. dollar data is from the U.S. Federal Reserve 1971 to present, for 1970 and prior we use R.L. Bidwell - “Currency Conversion Tables - 100 Years of Change,” Rex Collins, London, 1970, and B.R. Mitchell - British Historical Statistics - Cambridge Press, pp. 700-703. For trade weightings pre-1971 we use “Historical Statistics of the United States, Colonial Times to 1970,” a U.S. Census publication.

We see the U.S. status as a debtor nation as the spoils of war, the benefit of defeating the fascists (WW2) and collectivists (Cold War). The dollar surged after WW2 with the Bretton Woods Agreement in which the U.S. dollar tied to gold and the world’s currencies floated (usually down) versus the dollar. As capitalism and/or democracy (the debate rages over whether one can exist without the other) have proliferated, the U.S. dollar has fallen since the early 1970s (break in the blue line, the end of Bretton Woods), mirroring the falling U.S. share of world GDP (red line), the result not of U.S. “decline” but rather rising wealth in the rest of the world. As the reserve currency country, the U.S. logically chose to accumulate debt as well as gradually inflate. Given poor debt fundamentals we see emerging overseas, a rally in the U.S. dollar beyond what we have seen in 2010 would not surprise us.

26Source: U.S. Federal Reserve, FactSet, Stifel Nicolaus.

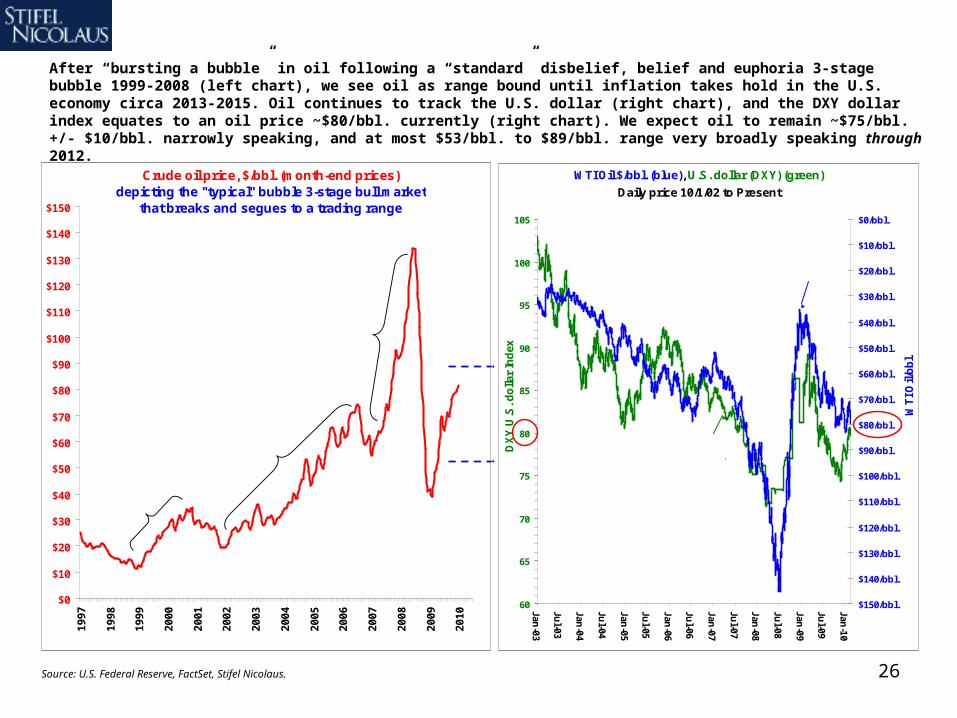

After “bursting a bubble” in oil following a “standard” disbelief, belief and euphoria 3-stage bubble 1999-2008 (left chart), we see oil as range bound until inflation takes hold in the U.S. economy circa 2013-2015. Oil continues to track the U.S. dollar (right chart), and the DXY dollar index equates to an oil price ~$80/bbl. currently (right chart). We expect oil to remain ~$75/bbl. +/- $10/bbl. narrowly speaking, and at most $53/bbl. to $89/bbl. range very broadly speaking through 2012.

Crude oil price, $/bbl. (month-end prices)depicting the "typical" bubble 3-stage bull market

that breaks and segues to a trading range

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Disbelief~$11 to $34

= ~3x

Euphoria ~$55 to $147 (high)

= ~3x

Belief~$24 to $74

= ~3x

WTI Oil $/bbl. (blue), U.S. dollar (DXY) (green)

Daily price 10/1/02 to Present

60

65

70

75

80

85

90

95

100

105

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

DX

Y U

.S. d

olla

r In

dex

$0/bbl.

$10/bbl.

$20/bbl.

$30/bbl.

$40/bbl.

$50/bbl.

$60/bbl.

$70/bbl.

$80/bbl.

$90/bbl.

$100/bbl.

$110/bbl.

$120/bbl.

$130/bbl.

$140/bbl.

$150/bbl.

WT

I Oil/

bb

l.

DXY dollar index

WTI Oil $/bbl.

27

Real Crude Oil prices (left axis, solid area) vs. y/y GDP converted to monthly (right axis)

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

$110.00

$120.00

$130.00

$140.00

Jan-

73Ja

n-74

Jan-

75Ja

n-76

Jan-

77Ja

n-78

Jan-

79Ja

n-80

Jan-

81Ja

n-82

Jan-

83Ja

n-84

Jan-

85Ja

n-86

Jan-

87Ja

n-88

Jan-

89Ja

n-90

Jan-

91Ja

n-92

Jan-

93Ja

n-94

Jan-

95Ja

n-96

Jan-

97Ja

n-98

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Jan-

07Ja

n-08

Jan-

09

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Inflation- adjusted Crude Oil $ per bbl U.S. Real GDP Monthly y/y % chng (left)

If oil doesn’t actually cause a recession, we believe it certainly renders the coup de grâce by causing already slowing GDP to “go negative.” As a result, following oil is critical for any industrial analyst. This chart also shows that particularly deep U.S. recessions occur at ~$85/bbl. and higher (in inflation-adjusted terms), consistent with our earlier charts.

Source: U.S. Department of Commerce, BEA, NYMEX.

28

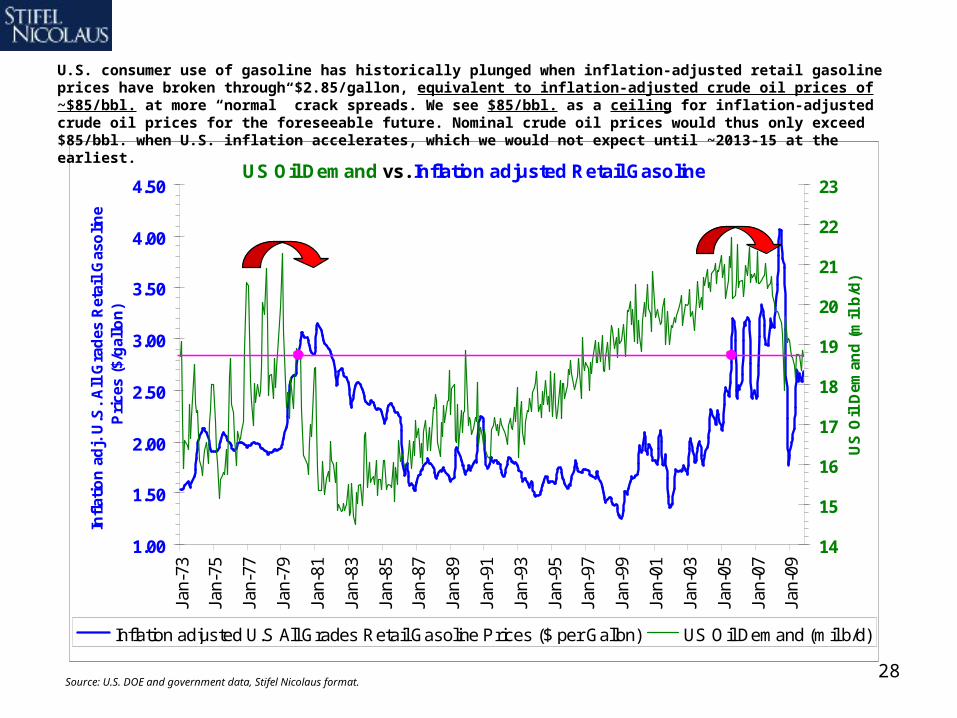

US Oil Demand vs. Inflation adjusted Retail Gasoline

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50Ja

n-73

Jan-

75

Jan-

77

Jan-

79

Jan-

81

Jan-

83

Jan-

85

Jan-

87

Jan-

89

Jan-

91

Jan-

93

Jan-

95

Jan-

97

Jan-

99

Jan-

01

Jan-

03

Jan-

05

Jan-

07

Jan-

09

Infl

atio

n a

dj.

U.S

. A

ll G

rad

es R

etai

l G

aso

lin

e P

rice

s ($

/gal

lon

)

14

15

16

17

18

19

20

21

22

23

US

Oil

Dem

and

(m

il b

/d)

Inflation adjusted U.S All Grades Retail Gasoline Prices ($ per Gallon) US Oil Demand (mil b/d)

Source: U.S. DOE and government data, Stifel Nicolaus format.

U.S. consumer use of gasoline has historically plunged when inflation-adjusted retail gasoline prices have broken through $2.85/gallon, equivalent to inflation-adjusted crude oil prices of ~$85/bbl. at more “normal” crack spreads. We see $85/bbl. as a ceiling for inflation-adjusted crude oil prices for the foreseeable future. Nominal crude oil prices would thus only exceed $85/bbl. when U.S. inflation accelerates, which we would not expect until ~2013-15 at the earliest.

29

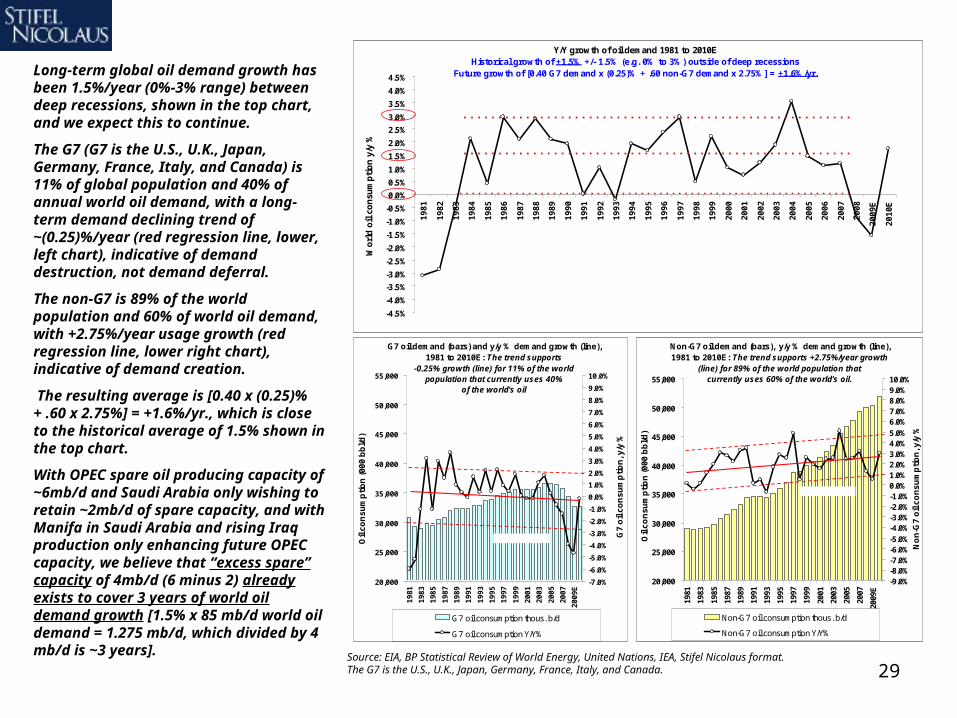

Long-term global oil demand growth has been 1.5%/year (0%-3% range) between deep recessions, shown in the top chart, and we expect this to continue.

The G7 (G7 is the U.S., U.K., Japan, Germany, France, Italy, and Canada) is 11% of global population and 40% of annual world oil demand, with a long-term demand declining trend of ~(0.25)%/year (red regression line, lower, left chart), indicative of demand destruction, not demand deferral.

The non-G7 is 89% of the world population and 60% of world oil demand, with +2.75%/year usage growth (red regression line, lower right chart), indicative of demand creation.

The resulting average is [0.40 x (0.25)% + .60 x 2.75%] = +1.6%/yr., which is close to the historical average of 1.5% shown in the top chart.

With OPEC spare oil producing capacity of ~6mb/d and Saudi Arabia only wishing to retain ~2mb/d of spare capacity, and with Manifa in Saudi Arabia and rising Iraq production only enhancing future OPEC capacity, we believe that “excess spare” capacity of 4mb/d (6 minus 2) already exists to cover 3 years of world oil demand growth [1.5% x 85 mb/d world oil demand = 1.275 mb/d, which divided by 4 mb/d is ~3 years]. Source: EIA, BP Statistical Review of World Energy, United Nations, IEA, Stifel Nicolaus format.

The G7 is the U.S., U.K., Japan, Germany, France, Italy, and Canada.

Y/Y growth of oil demand 1981 to 2010EHistorical growth of +1.5% +/- 1.5% (e.g. 0% to 3%) outside of deep recessions

Future growth of [0.40 G7 demand x (0.25)% + .60 non-G7 demand x 2.75%] = +1.6%/yr.

-4.5%

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9E

201

0E

Wo

rld

oil

co

nsu

mp

tio

n y

/y %

Non-G7 oil demand (bars), y/y % demand growth (line), 1981 to 2010E: The trend supports +2.75%/year growth

(line) for 89% of the world population that currently uses 60% of the world's oil.

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

E

Oil

co

nsu

mp

tion

(00

0 b

bl/d

)

-9.0%-8.0%-7.0%-6.0%-5.0%-4.0%-3.0%-2.0%-1.0%0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%10.0%

No

n-G

7 o

il c

on

sum

ptio

n, y

/y %

Non-G7 oil consumption thous. b/d

Non-G7 oil consumption Y/Y%

+ 1 st. deviation

- 1 st. deviation

G7 oil demand (bars) and y/y % demand growth (line), 1981 to 2010E: The trend supports

-0.25% growth (line) for 11% of the world population that currently uses 40%

of the world's oil

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

E

Oil

co

nsu

mp

tion

(00

0 b

bl/d

)

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

G7

oil

con

sum

pti

on

, y/y

%G7 oil consumption thous. b/d

G7 oil consumption Y/Y%

+ 1 st. deviation

- 1 st. deviation

30

China: Aspiring or Expiring?1. China’s rise is “real,” but the country is caught on a hamster wheel of strong total factor productivity leading

to high corporate and consumer savings rates that are then recycled into still more fixed investment.

2. Just as a centralized economic system can allocate capital more quickly than a free market, a free market (individual agents maximizing utility) can allocate more efficiently than a centralized system.

3. That is why the U.S. is liquidating land, labor & capital and floating the U.S. $ while the Chinese are employing massive expansion of bank loans and fixing their currency to avoid such adjustments. The U.S. approach is more sound, in our view.

4. China’s lending surge is not new, the country pumped up lending in the last recession eight years ago. The problem is at the margin - ever larger amounts of lending are required to achieve the same effect.

5. Chinese bank lending ($1.4 trillion in 2009, 29% of GDP) and currency policies are driving rapid Chinese M1 growth. Besides fixed investment or asset bubbles, China risks inflation, so policy is tightening.

6. We see inflation pressuring emerging market P/E multiples while disinflation lifts P/E multiples for traditional U.S. “growth” stocks, punishing the herd that is heavily invested in emerging market equities.

31

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

Sep

-01

Mar

-02

Sep

-02

Mar

-03

Sep

-03

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

3%

6%

9%

12%

15%

18%

21%

24%

27%

30%

33%

36%

China bank loans (bil. yuan/month, bars, left axis) vs. China oil usage (LTM, mil. bbls./day, line, right axis)

12,500B Yuan

15,000B Yuan

17,500B Yuan

20,000B Yuan

22,500B Yuan

25,000B Yuan

27,500B Yuan

30,000B Yuan

32,500B Yuan

35,000B Yuan

37,500B Yuan

40,000B Yuan

42,500B Yuan

45,000B Yuan

Jan

-04

Ma

y-04

Se

p-0

4

Jan

-05

Ma

y-05

Se

p-0

5

Jan

-06

Ma

y-06

Se

p-0

6

Jan

-07

Ma

y-07

Se

p-0

7

Jan

-08

Ma

y-08

Se

p-0

8

Jan

-09

Ma

y-09

Se

p-0

9

Jan

-10

5.5mb/d

5.8mb/d

6.0mb/d

6.3mb/d

6.5mb/d

6.8mb/d

7.0mb/d

7.3mb/d

7.5mb/d

7.8mb/d

8.0mb/d

8.3mb/d

8.5mb/d

8.8mb/d

9.0mb/d

9.3mb/d

9.5mb/d

China bank loans (billion yuan, bars, left axis) vs. China net coal* imports (LTM tons, mil., line, right axis)

12,500B Yuan

15,000B Yuan

17,500B Yuan

20,000B Yuan

22,500B Yuan

25,000B Yuan

27,500B Yuan

30,000B Yuan

32,500B Yuan

35,000B Yuan

37,500B Yuan

40,000B Yuan

42,500B Yuan

45,000B Yuan

Jan

-04

Ma

y-04

Se

p-0

4

Jan

-05

Ma

y-05

Se

p-0

5

Jan

-06

Ma

y-06

Se

p-0

6

Jan

-07

Ma

y-07

Se

p-0

7

Jan

-08

Ma

y-08

Se

p-0

8

Jan

-09

Ma

y-09

Se

p-0

9

Jan

-10

-100.0mt/y

-90.0mt/y

-80.0mt/y

-70.0mt/y

-60.0mt/y

-50.0mt/y

-40.0mt/y

-30.0mt/y

-20.0mt/y

-10.0mt/y

0.0mt/y

10.0mt/y

20.0mt/y

30.0mt/y

40.0mt/y

50.0mt/y

60.0mt/y

70.0mt/y

80.0mt/y

90.0mt/y

100.0mt/y

110.0mt/y

*Met coal + anthracite + steam coal

China bank loans (billion yuan, bars, left axis) vs. China iron ore imports (LTM tons, mil., line, right axis)

12,500B Yuan

15,000B Yuan

17,500B Yuan

20,000B Yuan

22,500B Yuan

25,000B Yuan

27,500B Yuan

30,000B Yuan

32,500B Yuan

35,000B Yuan

37,500B Yuan

40,000B Yuan

42,500B Yuan

45,000B Yuan

Jan

-04

Ma

y-04

Se

p-0

4

Jan

-05

Ma

y-05

Se

p-0

5

Jan

-06

Ma

y-06

Se

p-0

6

Jan

-07

Ma

y-07

Se

p-0

7

Jan

-08

Ma

y-08

Se

p-0

8

Jan

-09

Ma

y-09

Se

p-0

9

Jan

-10

5.0mt/y

10.0mt/y

15.0mt/y

20.0mt/y

25.0mt/y

30.0mt/y

35.0mt/y

40.0mt/y

45.0mt/y

50.0mt/y

55.0mt/y

60.0mt/y

65.0mt/y

70.0mt/y

China bank loans (billion yuan, bars, left axis) vs. China bank loans y/y % change (line, right axis)

10,000B Yuan

12,500B Yuan

15,000B Yuan

17,500B Yuan

20,000B Yuan

22,500B Yuan

25,000B Yuan

27,500B Yuan

30,000B Yuan

32,500B Yuan

35,000B Yuan

37,500B Yuan

40,000B Yuan

42,500B Yuan

45,000B Yuan

Fe

b-0

1Ju

n-0

1O

ct-0

1F

eb

-02

Jun

-02

Oct

-02

Fe

b-0

3Ju

n-0

3O

ct-0

3F

eb

-04

Jun

-04

Oct

-04

Fe

b-0

5Ju

n-0

5O

ct-0

5F

eb

-06

Jun

-06

Oct

-06

Fe

b-0

7Ju

n-0

7O

ct-0

7F

eb

-08

Jun

-08

Oct

-08

Fe

b-0

9Ju

n-0

9O

ct-0

9

0%

5%

10%

15%

20%

25%

30%

35%

40%

Just as a centralized economic system can allocate capital more quickly than a free market, a free market (of individual agents acting to maximize their own utility) can allocate more efficiently than a centralized system. The U.S. is liquidating land, labor and capital and floating the U.S. dollar while the Chinese are employing massive, rapid expansion of bank loans and currency intervention to avoid such adjustments. The U.S. approach is much more sound, in our view. Chinese bank loan growth the past year has been driving exuberance for minerals, especially those used in construction. We spot “bubble trouble,” however, and note that the PBOC and Chinese banking regulators have already announced measures to curb loan growth.

Surge in lending

coincides with surge in net coal imports.

Surge in lending

coincides with surge in iron ore imports.

Source: People’s Bank of China, National Bureau of Statistics of China, FactSet, Stifel Nicolaus Metals & Mining research.

No such surge in oil usage,

because the lending program

was geared toward

“infrastructure.”

32

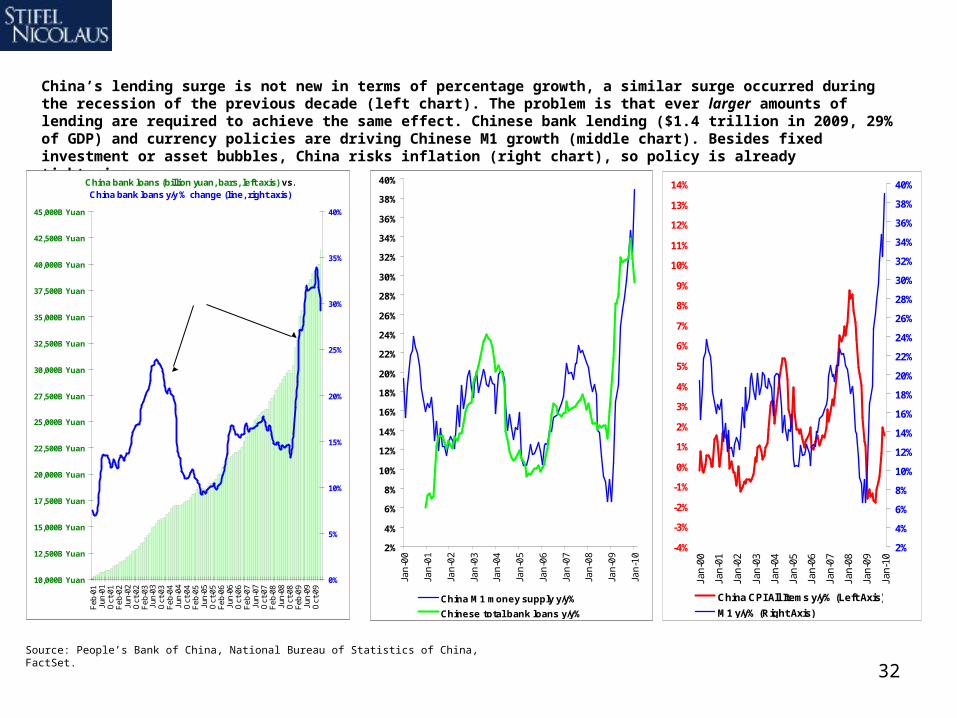

China’s lending surge is not new in terms of percentage growth, a similar surge occurred during the recession of the previous decade (left chart). The problem is that ever larger amounts of lending are required to achieve the same effect. Chinese bank lending ($1.4 trillion in 2009, 29% of GDP) and currency policies are driving Chinese M1 growth (middle chart). Besides fixed investment or asset bubbles, China risks inflation (right chart), so policy is already tightening.

China bank loans (billion yuan, bars, left axis) vs. China bank loans y/y % change (line, right axis)

10,000B Yuan

12,500B Yuan

15,000B Yuan

17,500B Yuan

20,000B Yuan

22,500B Yuan

25,000B Yuan

27,500B Yuan

30,000B Yuan

32,500B Yuan

35,000B Yuan

37,500B Yuan

40,000B Yuan

42,500B Yuan

45,000B Yuan

Feb

-01

Jun-

01O

ct-0

1F

eb-0

2Ju

n-02

Oct

-02

Feb

-03

Jun-

03O

ct-0

3F

eb-0

4Ju

n-04

Oct

-04

Feb

-05

Jun-

05O

ct-0

5F

eb-0

6Ju

n-06

Oct

-06

Feb

-07

Jun-

07O

ct-0

7F

eb-0

8Ju

n-08

Oct

-08

Feb

-09

Jun-

09O

ct-0

9

0%

5%

10%

15%

20%

25%

30%

35%

40%The issue isn’t that loan growth is strong, it was similarly strong in

response to the recession a decade ago. The issue is the ever larger amounts of debt, and the

circular role debt plays in growth, leading to more lending capacity.

Source: People’s Bank of China, National Bureau of Statistics of China, FactSet.

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

38%

40%

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

China M1 money supply y/y%

Chinese total bank loans y/y%

Chinese bank loans (and currency

policy) are driving extraordinary M1

money supply growth...

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

38%

40%

China CPI All Items y/y% (Left Axis)

M1 y/y% (Right Axis)

…and despite claims of an output gap, extraordinary

M1 growth is historically inflationary.

33Source: Bank Credit Analyst

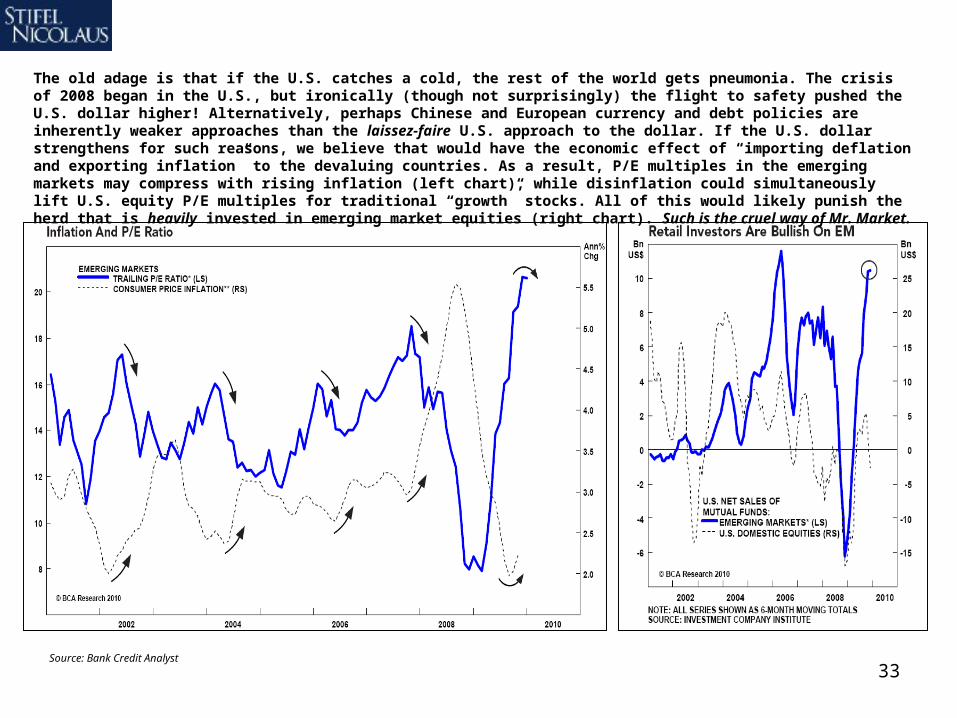

The old adage is that if the U.S. catches a cold, the rest of the world gets pneumonia. The crisis of 2008 began in the U.S., but ironically (though not surprisingly) the flight to safety pushed the U.S. dollar higher! Alternatively, perhaps Chinese and European currency and debt policies are inherently weaker approaches than the laissez-faire U.S. approach to the dollar. If the U.S. dollar strengthens for such reasons, we believe that would have the economic effect of “importing deflation and exporting inflation” to the devaluing countries. As a result, P/E multiples in the emerging markets may compress with rising inflation (left chart), while disinflation could simultaneously lift U.S. equity P/E multiples for traditional “growth” stocks. All of this would likely punish the herd that is heavily invested in emerging market equities (right chart). Such is the cruel way of Mr. Market.

34

Important Disclosures and Certifications

I , Barry Bannister, certify that the views expressed in this research report accurately reflect my personal views about the subject securities or issuers; and I, Barry Bannister, certify that no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views contained in this research report.

Stifel, Nicolaus & Company, Inc.'s research analysts receive compensation that is based upon (among other factors) Stifel Nicolaus' overall investment banking revenues.

Our investment rating system is three tiered, defined as follows:

BUY - We expect this stock to outperform the S&P 500 by more than 10% over the next 12 months. For higher-yielding equities such as REITs and Utilities, we expect a total return in excess of 12% over the next 12 months.

HOLD - We expect this stock to perform within 10% (plus or minus) of the S&P 500 over the next 12 months. A Hold rating is also used for those higher-yielding securities where we are comfortable with the safety of the dividend, but believe that upside in the share price is limited.

SELL - We expect this stock to underperform the S&P 500 by more than 10% over the next 12 months and believe the stock could decline in value.

Of the securities we rate, 37% are rated Buy, 59% are rated Hold, and 4% are rated Sell.

Within the last 12 months, Stifel, Nicolaus & Company, Inc. or an affiliate has provided investment banking services for 11%, 10% and 3% of the companies whose shares are rated Buy, Hold and Sell, respectively.

35

Additional Disclosures

Please visit the Research Page at www.stifel.com for the current research disclosures applicable to the companies mentioned in this publication that are within Stifel Nicolaus’ coverage universe. For a discussion of risks to target price please see our stand-alone company reports and notes for all Buy-rated stocks.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and is not a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred to herein. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation or needs of individual investors. Employees of Stifel, Nicolaus & Company, Inc. or its affiliates may, at times, release written or oral commentary, technical analysis or trading strategies that differ from the opinions expressed within. Past performance should not and cannot be viewed as an indicator of future performance.

Stifel, Nicolaus & Company, Inc. is a multi-disciplined financial services firm that regularly seeks investment banking assignments and compensation from issuers for services including, but not limited to, acting as an underwriter in an offering or financial advisor in a merger or acquisition, or serving as a placement agent in private transactions. Moreover, Stifel Nicolaus and its affiliates and their respective shareholders, directors, officers and/or employees, may from time to time have long or short positions in such securities or in options or other derivative instruments based thereon.

These materials have been approved by Stifel Nicolaus Limited, authorized and regulated by the Financial Services Authority (UK), in connection with its distribution to professional clients and eligible counterparties in the European Economic Area. (Stifel Nicolaus Limited home office: London +44 20 7557 6030.) No investments or services mentioned are available in the European Economic Area to retail clients or to anyone in Canada other than a Designated Institution. This investment research report is classified as objective for the purposes of the FSA rules. Please contact a Stifel Nicolaus entity in your jurisdiction if you require additional information.

The use of information or data in this research report provided by or derived from Standard & Poor’s Financial Services, LLC is Copyright © 2010, Standard & Poor’s Financial Services, LLC (“S&P”). Reproduction of Compustat data and/or information in any form is prohibited except with the prior written permission of S&P. Because of the possibility of human or mechanical error by S&P’s sources, S&P or others, S&P does not guarantee the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. S&P GIVES NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. In no event shall S&P be liable for any indirect, special or consequential damages in connection with subscriber’s or others’ use of Compustat data and/or information. For recipient’s internal use only.

Additional information is available upon request

© 2010 Stifel, Nicolaus & Company, Incorporated, One South Street, Baltimore, MD 21202. All rights reserved.