2Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

What is a Digital Platforms Ecosystem?

An interconnected set of services enabling users to fulfil a variety of needs

in one integrated experience.

It can scale easily and allows multiple participants ( producers and consumers ) to connect with it,

interact with each other, create and exchange value.

3Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

Global Digital Platforms

ATKearny - Towards an Internet of Payments — Global platforms redefining the payments landscape

Presenter

Presentation Notes

The global payments landscape has reached an inflection point. Global platforms such as Apple, Amazon, Google, Facebook and Alibaba have become major players in the most recent era of context-based payments, resulting in disruptive change across the payments sector. Such non-banking players have raised the bar by changing the way consumers “experience” payments, offering innovative end-to-end services that are quick, efficient and personalised – and where the payment may be incidental to the buying experience. Today, we are moving towards an “Internet of Payments”, where payments are everywhere and invisible. The source of competitive advantage is shifting towards customer value, and payments architectures are becoming more modular. Payments providers face a new choice: do they continue to “do it all” or focus on infrastructure provision and partner with other businesses such as the global platforms that can provide the expertise in delivering great customer experiences? Modular architectures allow global platforms better access to underlying infrastructure, and they also enable new business models for infrastructure providers based on creating global scale in value-added services.

4Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

Payment Evolution

B mre bu of tim

ATKearny - Towards an Internet of Payments — Global platforms redefining the payments landscape

Presenter

Presentation Notes

The most recent payments era has been a shift towards context-based payments, where the payment becomes incidental or invisible to the broader customer experience and the service being provided. Global platforms’ increasing influence arises from their ability to control the context of the transaction and access to the end customer. In one of the most striking early examples of an invisible payment, Amazon removed friction for buyers by providing physical Dash Buttons.

5Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

Why do banks need platforms /ecosystems?

Improve customer experience

Predict customer needs

Reduce customer acquisition &

operating costs

Enable open banking &

ecosystem based business models

Access and monetize data

Presenter

Presentation Notes

Ecosystems act as gateways that reduce the friction customers encounter when they have to switch between related services. Ecosystems use network effects that give companies a strategic scale advantage. Ecosystems integrate data that helps companies create value-added products and services, and superior experiences, for their customers.

6Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

Projected Ecosystem Valuation

Source: IHS World Industry Service; Panorama by McKinsey; McKinsey analysis

Presenter

Presentation Notes

By 2025, as this revolution gains speed, McKinsey expects 12 distinctive and massive ecosystems to emerge around fundamental human and organizational needs . These 12 ecosystems will account for $60 trillion in revenues by 2025, or roughly 30 percent of all global revenues. The actual shape and composition of these ecosystems will vary by country and region, both because of the effects of regulations and as a result of more subtle, cultural customs and tastes.

External assessment An external assessment of industry opportunities and outlook can provide a view on how much value is on the table. Important factors include: Market size. The current sizes of industries in the ecosystem, and the penetration rate of the integrated network economy. Growth potential. The prospects for expansion, including the number of new customers and the amount of revenue growth. Profitability. The relative level of profitability of industries in the ecosystem. Competitive strategy. The extent to which global or local competitors have begun building ecosystems. Internal assessment The second assessment measures the strengths of the company to see if it is a natural owner of a given opportunity. Important factors include: Existing customer base and access to valuable data. Companies need to consider whether they possess—or might acquire—the customer data that is critical to a succesful ecosystem. Such data can include personal health data for the health-care industry or SKU data for the business-to-consumer marketplace. Relevance to core business and capabilities. The company must consider the potential for collaboration with its core businesses and the compatibility with their capabilities. Existing partnerships, networks, or sister companies to leverage. Without a sufficient customer base, it is difficult to attract partners. By leveraging resources from existing partnerships, networks, or sister companies, a firm can put itself in a better position for ecosystem development.

8Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

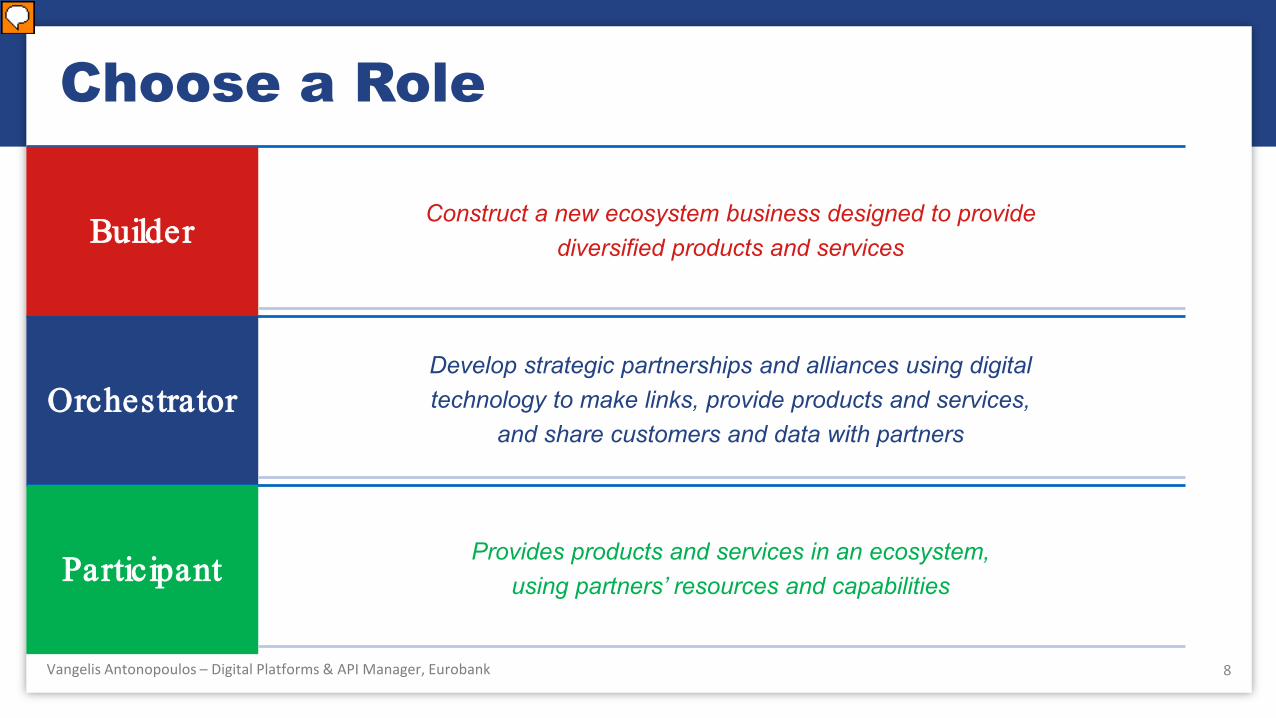

Choose a Role

Builder Construct a new ecosystem business designed to provide diversified products and services

OrchestratorDevelop strategic partnerships and alliances using digitaltechnology to make links, provide products and services,

and share customers and data with partners

Participant Provides products and services in an ecosystem, using partners’ resources and capabilities

Presenter

Presentation Notes

Participant: to not only enhance their own business but also upgrade products to adapt to ecosystems and meet customers’ needs

9Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

Choose a Business Model

Profitability

Topline

Customer Acquisition

Digital Platforms

Multibusiness Ownership

Data Monetization

Bottomline

Resource Synergy

Infrastructure Enabler

Presenter

Presentation Notes

Acquisition : Capture new customers and ultimately maximize core revenues. Requires strong customer management capabilities. Platform : Develop digital platforms that enable third parties to offer products and services or participate as providers. Requires a large customer base as an orchestrator or competitive advantages in products or services as a participant. Multibusiness ownership: Build new businesses outside the traditional scope of the company. Requires large investments. Data monetization: Use data collected to develop new data-led businesses. Requires advanced proprietary data and data management capabilities resource synergy: Combine existing assets and resources to achieve operational eciencies. Infrastructure enabler: Monetize existing infrastructural, technology, and other capabilities to decrease investment costs per unit. Banks are pursuing greater profitability through a mix of cost-efficiency improvement and top-line growth. Typically, they tend to serve as ecosystem participants or orchestrators, and prefer the following three business models: the platform model (for boosting revenue), the asset/ resource synergy model and infrastructure/ capability enabler model (for cost savings).

Governance : Should a player set up one or multiple organizations to support ecosystem development? Product offerings : How to know where to play in a given ecosystem? What are the key factors to consider for products or services development? How to sequence the products or services? Customer management : How to attract more customers in an ecosystem? How to increase customer retention and enhance customer loyalty? Partnerships : How to choose a partnership model? What are the key capabilities/ mechanisms required for building a successful partnership? As a product/ service provider, how to develop competitive advantages? Technology : How to best use technology? analytics : What are key factors in embedding advanced analytics in an ecosystem?

11

The success will depend on the degree to which the ecosystem is customer-obsessed and solves real problems, because this is what will help banks build a relationship.

Vangelis Antonopoulos – Digital Platforms & API Manager, Eurobank

Thank You

Athens, May 19th, 2017Group Digital Banking /Vangelis Antonopoulos