Banking in Luxembourg - PwC · Luxembourg. The questions and issues encountered during such...

40

1 PwC Luxembourg Live long and prosper pwc.lu/banking Banking in Luxembourg

Transcript of Banking in Luxembourg - PwC · Luxembourg. The questions and issues encountered during such...

1PwC Luxembourg

Live long and prosper

pwc.lu/banking

Banking inLuxembourg

2Banking in Luxembourg

Since 1856 banks have shaped the Luxembourg financial centre. Today, more than 160 years later, the banking industry is one of its key pillars. The reason for the long-standing success story is that banks in Luxembourg have been able to repeatedly reinvent themselves to adapt to continuously changing environments.

From supporting Luxembourg’s growing trade business and thereby substantially contributing to Luxembourg’s economic and social development, banks have over time progressively expanded into international finance, among others through the Eurobond business, the investment funds industry and private banking. Always by adapting to the most stringent international standards.

Today, the industry continues to be faced with numerous challenges of a regulatory, economic, technological, and political nature. Currently one of the most, if not the most important topic, is climate change. I truly believe banks in Luxembourg and elsewhere will have a major role to play both in financing the transition to a sustainable economy as well as in helping to achieve the United Nations’ climate goals. I am convinced that banks and their employees can successfully help to shape a more purposeful future.

More and more, the effects of the continuing digitisation of the sector are altering our talents’ work environment. They have been key driver for our long-standing success and have been confronted with numerous challenges in the recent past, notably with substantial regulatory shifts considerably impacting their daily lives. It is of outmost importance to accompany them during the many change processes, to support and help them to develop their skills in order to successfully achieve the many transformation processes the industry is facing.

The ABBL will continue to encourage and help its members to successfully meet these challenges.

Guy HoffmannABBL Chairman

3PwC Luxembourg

Table of contentsForeword 4

1. Luxembourg: a competitive financial centre 6

2. A diversified and evolving environment 8

3. Setting up a credit institution in Luxembourg 20

4. Supervision and control of credit institutions 22

5. Regulatory provisions 24

6. External audit requirements 26

7. Taxation in Luxembourg 28

8. Payments Services Directive 2 32

Appendix - Useful Luxembourg addresses 36

Contacts 38

4Banking in Luxembourg

ForewordThe Luxembourg financial centre has established its reputation as an international banking place since the 1960s and has been able to remain at the top among all financial centres across the world thanks to its resilience and ability to rapidly comply with new regulations.

Roxane HaasBanking Leader

5PwC Luxembourg

However, for a few years now, the global financial industry has been facing drastic changes and Luxembourg has definitely not been spared by this revolution. New technologies leading to evolving and fast changing customer behaviours as well as the arrival of new market entrants attracted by this favourable environment have turned the Luxembourg banking landscape upside down. Traditional banks are forced to rethink the way they interact with their customers, which is leading to a new generation of service offerings.

The need to keep control over costs and compliance matters has never been so crucial. Defining new target operating models, adapting to an ever evolving environment or revamping existing procedures or processes, as well as reconsidering IT infrastructure, systems and applications are permanent challenges for banks operating in Luxembourg. The questions and issues encountered during such exercises are multidimensional and wide ranging.

Throughout this publication, we will explain how rapidly advancing technologies using Smart Identity, Data Analytics and Artificial Intelligence but also FinTech, Blockchain and Cryptocurrencies are reshaping the banking industry. Regulatory pressure - partially - linked to these new players or tools is higher than ever before; GDPR and PSD2 among others have a tremendous impact on banks in Luxembourg. Data and security are definitively as well at the heart of all current concerns.

This dynamic environment is profitable for all players within financial services. On the one hand, FinTechs represent a real pool of disruption; they put pressure on banks to deploy better and faster products and services and then accelerate the pace of innovation but also provide a source of inspiration and capabilities through partnerships and acquisitions. On the other hand, the deployment of externalisation of some services represents an opportunity for banks to better focus on their core business and invest in their product offerings to develop new activities.

At the same time, in a world shaped by technology and digitisation there is a crucial need to upskill the current workforce and to find the right people armed with the relevant skills to address all these topics. Today, banks need to recruit profiles who did not even exist a few years ago and simultaneously consider a requalification in new areas of expertise for part of their workforce in order to support their own digital transformation.

Banks have also a responsibility towards the society as a whole and sustainable banking cannot and will not be averted.

Time has come now to embrace all these new challenges in order to transform them into business opportunities. At PwC, we are looking forward to supporting you through your transformation.

6Banking in Luxembourg

Luxembourg’s financial services centre is unique. With its exceptional range of services, world-class financial infrastructure and expertise, the country’s banking industry is competitive.

1. LuxembourgA competitive

financial centre

A fast growing and competitive economy

On top of a stable political environment and sound public finances, Luxembourg’s main strength lies in its ability to adapt its economic strategies quickly. As the first EU country to adopt UCITS legislation into national law in 1988, Luxembourg achieved a turning point in its history by becoming a major centre for investment funds in Europe and in the world. The Grand Duchy made the most of its expertise in the financial services, and quickly became a hub for banks. In 2007, it demonstrated once again its pioneer spirit by launching the first ever Green Bond.

From adoption of major European regulations, to the digitisation of the financial services and the rise of sustainable finance, the Luxembourg financial sector proved on many occasions over the years its capacity to react quickly to new challenges. Nowadays, the financial sector is the strongest component of the Luxembourg economy. Nevertheless, the country continues to diversify its economy by investing in niche markets, such

as infrastructure and debt funds, logistics business, as well as technology through ICT (Information and Communications Technologies), data centres and also by supporting the local implementation of GAFAs.

For a few years now, Luxembourg secured a place among the top countries in the areas of innovation and technology. The European Innovation Scoreboard ranked it 6th 1 among the European countries for its innovation performance.

With the digital wave that recently took over the world, Luxembourg succeeded in positioning the country and its financial sector as European and worldwide leaders. It ranked 5th in the Digital Economy and Society Index2 (DESI) published by the European Commission and which measures the digital performance and Member States, one of the country’s strongest point being Digital Skills (1st place). Luxembourg also succeeded where many failed when it comes to gender equality in the digital field as it ranked 3rd in the first edition of the Women in Digital Index3, a supplement to the DESI.

3rd in the first edition of the Women in Digital Index6th The European Innovation

Scoreboard ranked

1 Source: http://www.inspiringluxembourg.public.lu/en/outils/benchmarks/2018/26-scoreboard/index.html2 Source: http://www.inspiringluxembourg.public.lu/en/outils/benchmarks/2018/18-desi/index.html3 Source: http://www.inspiringluxembourg.public.lu/en/outils/benchmarks/2018/17-womendigital/index.html

7PwC Luxembourg

“The Global Competitiveness Report 2017-2018” from the World Economic Forum confirms its competitiveness as Luxembourg is ranked 19th out of 140 countries”, 6th among European countries.

Luxembourg economic model remains one of the most competitive in the world. The Global Competitiveness Report 2018 ranked Luxembourg 19th out of 140 countries in terms of competitiveness, and 6th at European level. Following its most recent analysis based on more than 68 different indicators, the Observatory for Competitiveness also considers Luxembourg as a high-level performer in terms of competitiveness, ranking it 9th in the European Union.

These factors largely contribute to the attraction of the Grand Duchy on the international place and help the country attract, grow and retain talents and investors.

Luxembourg is continuing to attract major multinational groups, and encouraging them in developing their activities in the country.

Luxembourg – a favourable business environment

1. Located at the crossroads of Europe

Luxembourg is ideally located within driving distance of the continent’s major business centres.

An estimated 60% of the European Union’s wealth is concentrated within a 700 km radius of Luxembourg.

4. Expertise in managing cross-border funds distribution5

61% of the Domicile share of authorisations for cross-border distribution in Luxembourg

More than 2 out of 3 asset management giants have chosen Luxembourg as first domicile to set up their funds

2. An international and productive workforce

About 45%1 of Luxembourg’s workers are foreigners - most of them speak two or more languages.

Labour productivity in Luxembourg has been ranked in the Top 3 of European countries (EU28) for more than 10 years, according to Eurostat.

5. Favourable taxation and regulatory frameworks

Luxembourg has over 80 double tax treaties with its international partners (and 16 under negociation).

Luxembourg also offers one of the lowest total tax rates4 in Western Europe, according to the World Bank.

3. Healthy public finances and a stable political environment

Luxembourg has the second lowest debt to GDP ratio² in Europe with 20%, and benefits from a AAA credit rating.

Luxembourg’s political environment has been very stable for decades – ensuring continuity for business actors.

6. A state-of-the art ICT infrastructure

Luxembourg offers the latest technology in communication. 25% of all European Tier IV certified data centres (highest reliability level of data centres) are located in Luxembourg, ranking it in first position in terms of Tier IV density in Europe. The country is also ranked 1st for Technological Readiness worldwide by the World Economic Forum.

1 Source: Statec² Source: IMF3 Source: Eurostat4 Source: Paying Taxes 2018, PwC in conjunction with the World Bank5 Source: Benchmark your Global Fund Distribution 2019

2. A diversifiedand evolving

environment

With its unparalleled range of services, financial infrastructure and expertise, Luxembourg is a financial global hub. Despite a major transformation wave hitting global financial markets combined with an increasingly complex regulatory context, the local financial sector is still resilient, competitive and growing.

Luxembourg market dynamics

Luxembourg offers a wide range of financial products and services, combined with a constant innovation in financial solutions, including pension funds, hedge funds, real estate vehicles, securitisation vehicles and private equity structures such as the “Société d’Investissement à Capital Risque” (SICAR) as well as “Reserved Alternative Investment Fund” (RAIF). All form the basis for a comprehensive ‘toolbox’ used by institutional investors as well as wealth managers.

The Luxembourg financial market place has always known how to deal and adapt itself with market trends, one of the last indicator being the rise of the FinTech industry, making of Luxembourg a new technological hub for the finance industry in Europe.

The country is also well-positioned to make the most of the increase in cross-border activities, in terms of both investment and distribution. It has the key attributes to become the leading global AIF platform - as it did with UCITS - and to help alternative fund managers and institutional investors turn alternative investment fund regulations into an opportunity.

9PwC Luxembourg

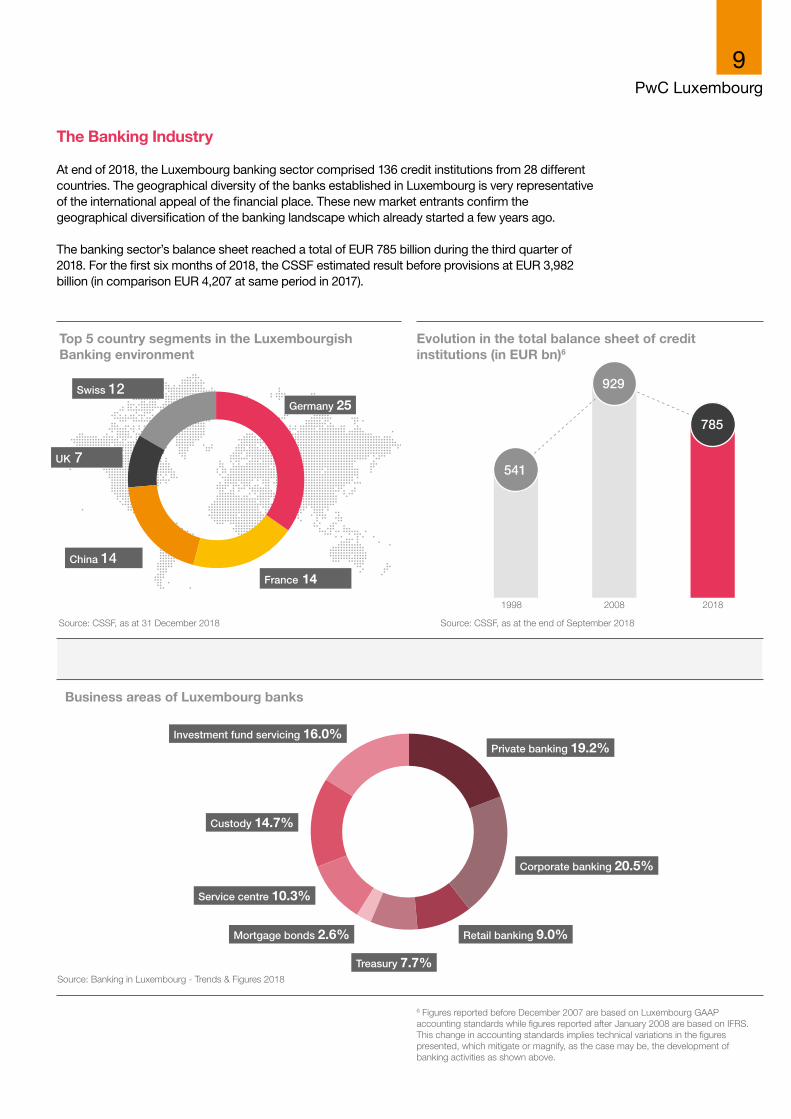

Evolution in the total balance sheet of credit institutions (in EUR bn)6

Business areas of Luxembourg banks

Source: CSSF, as at the end of September 2018

Source: Banking in Luxembourg - Trends & Figures 2018

Top 5 country segments in the Luxembourgish Banking environment

Source: CSSF, as at 31 December 2018

1998 2008 2018

541

929

785Germany 25

France 14

China 14

UK 7

Swiss 12

6 Figures reported before December 2007 are based on Luxembourg GAAP accounting standards while figures reported after January 2008 are based on IFRS. This change in accounting standards implies technical variations in the figures presented, which mitigate or magnify, as the case may be, the development of banking activities as shown above.

Private banking 19.2%

Retail banking 9.0%

Treasury 7.7%

Mortgage bonds 2.6%

Service centre 10.3%

Custody 14.7%

Investment fund servicing 16.0%

Corporate banking 20.5%

The Banking Industry

At end of 2018, the Luxembourg banking sector comprised 136 credit institutions from 28 different countries. The geographical diversity of the banks established in Luxembourg is very representative of the international appeal of the financial place. These new market entrants confirm the geographical diversification of the banking landscape which already started a few years ago.

The banking sector’s balance sheet reached a total of EUR 785 billion during the third quarter of 2018. For the first six months of 2018, the CSSF estimated result before provisions at EUR 3,982 billion (in comparison EUR 4,207 at same period in 2017).

10Banking in Luxembourg

The Wealth Management Industry

Luxembourg has been an international centre of excellence in Wealth Management and Private Banking services for more than 40 years. Luxembourg is ranked among the top countries, worldwide, and reached the first place in the Eurozone with cross border Private Banking’s assets under management (AuM) amounting to EUR 363.4 billion, a steady and positive evolution of +0.7% compared to the end of 2017.

The Luxembourg Wealth Management industry is adapting to global trends, notably to the shift of wealth: wealthy individuals are now more international and younger with a noticeable part of clients being either self-made entrepreneurs or family businesses being transferred to the next generation. To serve this more versatile and demanding range of clients, Wealth Management players are diversifying and structuring into an innovative ecosystem.

The Luxembourg pioneering legislation is a competitive advantage for Wealth Management players. With heavier regulatory and compliance requirements worldwide, Luxembourg is becoming a growing operational hub for wealthy families and family businesses. They come to Luxembourg to set up their alternative investment platforms or their worldwide/European headquarters under the form of investment funds or family offices, thus taking advantage of Luxembourg’s developed financial sector.

The Private Banking industry combines this new offering with its traditional fund and insurance services offering, as Luxembourg is a global distribution platform for investment funds and life insurance products.

7 Source: CSSF/ABBL Private Banking Survey 2018

Corporate Banking

The Luxembourg corporate banking market is thriving, providing a broad range of services to both already established and new companies in Luxembourg, as well as foreign companies and groups.

Some corporate groups also acquire a banking licence to operate financing activities out of Luxembourg. Examples include:• A specialised platform for electronic payments between professionals and individuals at the European

level• A leading producer of agricultural equipment whose primary activity in Luxembourg is the provision of

financing to clients who want to purchase its equipment• Others are looking to settle in Luxembourg to benefit from the EU passport and for operating activities

throughout Europe

11PwC Luxembourg

Electronic money institutions and payment institutions

Electronic money institutions

An Electronic Money Institution is a legal person that has been granted authorisation to issue electronic money as per article 24-2 (non-EU undertakings) of the Law of 10 November 2009 as amended by the Law of 20 May 2011. EU Electronic Money issuers duly authorised in their home member state and acting through a branch, an agent or free provision of services, do not need formal authorisation from Luxembourg authorities as they benefit from EU rules on freedom of provision of services (article 24-15 of the law).

Authorisation requires a fully subscribed and paid-in capital of EUR 350,000.

Electronic Money Issuer can be one of the following entities:• Credit Institutions;• Electronic Money Institutions;• Post office giro institutions;• European and National Central Banks;• Member state or regional authorities.

Payment institutions

These institutions provide and execute payment services in accordance with article 7 (Luxembourg undertaking) or 22 (non-EU undertakings) of the Law of 10 November 2009 (as amended by the Law of 20 May 2011) and may grant credits under certain conditions if linked to the payment services. They are not allowed to receive deposits from the public and may not issue electronic money.

Authorisation requires a fully subscribed and paid-in capital of EUR 20,000 or EUR 50,000 or EUR 125,000 depending on the services provided as described within the law of 10 November 2009 as amended.

Categories of credit institutions

In the Luxembourg law, two types of licences are possible for credit institutions:• Universal Banking Licence; • Mortgage Bonds Banking Licence.

Credit institutions operating out of the Grand Duchy are granted an operating licence by the Ministry of Finance.

Among the 136 authorised banks, 133 have a universal banking licence while 3 have a mortgage-bond banking licence.

Numbers of credit institutions by type

87

3

32

14

Source: CSSF, as at 31 December 2018

█ Banks under Luxembourg law █ Banks issuing mortgage bonds█ Branches of banks originating from a member state of the EU█ Branches of banks originating from a non-member state of the EU

6 Electronic money institutions

10 Payment institutions

Source: CSSF, as at 31 December 2018

12Banking in Luxembourg

The transformation of the Banking industry – new challenges and opportunities ahead

A variety of forces have put tremendous pressure on the financial services industry in recent years, leaving many institutions with unsustainable cost–income ratios. And several of these challenging trends — from new regulatory mandates to augmented capital requirements and aggressive fintech competitors — are strengthening.

Transformation of the workforce - Look inside & out

More than 60% of Banking and Capital Markets (BCM) CEOs interviewed for our global CEO survey believe that it has become more difficult to hire workers with the right talent. The challenges are heightened by the fact that many of the people with the right capabilities — empathy, innovation and engagement skills, as well as digital familiarity — may need to be sourced from outside the BCM industry. Technology is clearly a focus, as are sectors that are seen as leaders in innovation, such as the automotive industry, or leaders in customer engagement, such as the retail or healthcare industries. In other words, you should reach out to candidates who might not have considered a career in BCM.

Yet few see hiring from outside as the best way to close the skills gap. The reluctance to bring in fresh blood is often compounded by many regulators’ misgivings about allowing people with no BCM experience to take up authorised roles within the industry. It’s important as well to work with regulators to explain how your business is changing and to ease any concerns about hiring people from other sectors.

Although hiring can help bridge the capabilities gap, retraining and up-skilling are even more important. Using AI-generated sources of information to enable compliance teams to move from after-the-fact, paper-based oversight to monitoring and managing risks in real time, for example, would be a valuable shift in skills. Programmes are in place, but new ways of working often can come up against resistance from a ‘frozen middle.’ This highlights the importance of bottom-up buy-in as well as direction from the top. Involving your people in making the plans for change can go a long way to winning their support —people adopt what they create.

AI and machine learning are revolutionising customer intelligence and experience within both corporate and retail banking. Yet it’s people who drive transformation and derive the value. Setting the pace demands a clear understanding of what kind of skills and culture offer foundations for success, as well as an understanding of how your company can harness these necessary capabilities. You must also ensure that customers have the confidence and trust to engage with you on a new level. The most successful strategies will cut across technology, data and humanity.

Other key sources of talent may include service providers, strategic partners and contingent workers, a trend that is accelerating due to pressure to reduce fixed costs (and, therefore, in-house workforces). This underlines the need for agile collaboration with a range of different partners.

Source: PwC’s 22nd Annual Global CEO Survey trends series – Banking and Capital Markets

13PwC Luxembourg

Outsourcing

In a complex and changing regulatory environment led by global competition, cost reduction and flexibility required to serve clients’ needs, outsourcing activities to service providers in Luxembourg or abroad can help a bank decrease non-value-added activities and focus on its core business. Recently implemented regulatory and governmental changes also affecting professional secrecy requirements have further boosted the attractiveness of sourcing strategies, including outsourcing to cloud-based solutions.

60%Sourcing Strategy Survey of 2018 showed, that 60% of the respondents either already rely or are considering the utilisation of cloud-based solutions.

Which regulatory requirements need to be complied with?

How is a proper monitoring of the delegated services ensured?

What happens in case the delegation of activities comes to an end?

Which roles and responsibilities should be included in the contractual agreement?

To what extent do the bank’s clients need to be informed or even provide their consent?

Which due diligence procedures need to be performed to identify the ideal service provider?

14Banking in Luxembourg

General Data Protection Regulation (GDPR)

The General Data Protection Regulation came into effect on the 25th of May 2018, in an attempt to harmonise legislative frameworks of protection of personal data across the EU. GDPR has been discussed and formalised throughout more than four years. The main principles of the GDPR are the same as in the previous legislation, but the differences are in the application and enforcement of the regulation.

More than 6 months after the entry in effect of the GDPR, companies, including banks, are still in the process of ensuring their compliance with the regulation. Having started with the core items of the regulation, such as having a proper list of all processing of personal data within the organisation, or appointing a data protection officer, most of the financial companies have embarked on a long-lasting journey, reviewing the operations, upgrading their systems and enforcing compliance monitoring programmes tailored to the GDPR.

While the number of requests from individuals to exercice their rights of information, modification, etc. remains quite low at the Luxembourg level, one should not under-estimate the associated risks linked to the inadequate capacity to address such requests, without mentioning the impacts of potential data leakage. What is at stake here is not only the financial and administrative sanctions, which can be imposed in certain cases of compliance failure, but above all the reputation of the bank, which constitutes one of its key assets.

What’s the risk of non-compliance?

The biggest risk of non-compliance with regards to GDPR is financial: CNPD or another data protection authority in the EU could issue fines as high as 4% of the annual global turnover of a company or EUR 20 million, whichever comes higher. One other type of risks is operational, consisting in the restriction of processing of personal data.

Cybersecurity and Privacy

Banks handle some of the most sensitive information, from account and credit-card data to personal identification. Cybersecurity is essential for banking institutions with the financial health of both individuals and business at stake. Unfortunately, it is also under attack more than ever before. Cyber-related incidents represent a growing threat to the reputation and economic stability of financial institutions. The initial question is no longer “if”, but “when” a cyberattack will occur. Finally, the question is “how much” it will cost the bank (both directly and indirectly).

GDPR impacts many stakeholdersThe requirements imposed by GDPR are not industry specific, and have an

impact over many areas of an organisation.

Privacy Office

• Considering a Data Privacy Officer• Enhancing notice & transparency• Enforcing Privacy by Design and by Default• Conducting Privacy Impact Assessments

CISO/IT

• Promoting security throughout the data lifecycle• Enabling data portability• Ensuring rights of access, authentication• Managing consent indicators and logs• Driving incident response process• Enabling rights of access & rectification• Permitting the right to be forgotten

Marketing

• Respecting consent • Automating decision-making processes• Limiting access to data

HR

• Training and awareness on privacy matters• Implementing data subjects rights of employees

Customer Service & Ops

• Ensuring rights of access & remediation• Permitting the right to be forgotten• Fielding questions, inquiries, concerns

Legal

• Enacting data transfer mechanisms• Defining data controllers & processors• Managing contract process and clauses• Driving data breach notification

RegulatoryRisk

• Fines and penalties (4% annual global turnover or EUR 20 million)

• Data protection audits

ReputationalRisk

• Brand damage• Loss of consumer trust• Loss of employee trust• Consumer attrition

FinancialRisk

• Loss of revenue• Litigation costs• Private right of action• Remediation costs

OperationalRisk

• Restricted EU operations• Invalidated data transfer

15PwC Luxembourg

Cryptocurrency and Blockchain

The blockchain technology and its leading practical use-case, the crypto-assets, are expected to soon disrupt activities such as payments, back-office processes, contracts and agreements, record keeping, reconciliation and settlement. In fact, this disruption could already be witnessed thanks to the efforts of numerous state and central banks, regulators, as well as major stakeholders of the financial sector in exploring the opportunities and risks associated to this evolving domain.

Recently, EBA released a report after examining the applicability of EMD2 and PSD2 to crypto-assets, issues arising with respect to custodian wallets and crypto-assets trading platforms, as well as the risks related to money laundering and terror financing. The fifth AML Directive adopted last year by the European Parliament foresees a set of rules applicable to virtual currency exchange platforms and custodian wallet providers. In Luxembourg, on 14 February 2019, the Chamber of Deputies passed a bill to offer greater certainty for investors and to make the transfer of securities more efficient by reducing the number of intermediaries. This bill essentially updates the umbrella of dematerialised securities to include the circulation of securities based on blockchain technology.

Such developments are bound to generate higher adoption of blockchain and crypto-assets.

In this context, you may face challenges such as the following:• Which blockchain use cases could transform my business processes and improve transparency and trust across

the value chain?• What is the impact of joining the blockchain ecosystem comprising my partners and/or clients?• What tokenization will change in my current business?• How to on-board a crypto millionaire and how to assess a crypto gain’s source of wealth?• How to safe-keep crypto for my clients?• Which set of tools are useful to track assets?

Every experience in our lives gains a digital element and the customer banking-journey is no exception. With the increasing use of connected mobile devices, adopting a customer-centric digital strategy is essential to overcome the challenges posed by the digitisation of the financial sector. Digital Bank, Mobile Banking, Banking platform... In these times of immediate gratification, organisations are under a heightened sense of urgency to create solutions faster, rise above market expectations and stand out if they want to keep their customers. Banks are forced, among traditional players, to reconsider their role and anticipate the evolution of demand by investing in customer driven innovations and disruptive products and services. Understanding the evolution in customers’ needs and behaviours is a priority to address generational shifts and rapid adoption of technology.

16Banking in Luxembourg

Data Analytics

The game changing era of AI is upon us, it is transforming the way businesses operate. Adopting AI is not an option; you can do it voluntarily, or be forced by the competition to do so. For banks, as for other operating entities, AI offers great advantages and benefits

Data provides the basis for innovation and intelligent action. Ironically, despite its growing volumes, the gap of needed and provided data since 2009 hasn’t changed, and CEOs continue to complain about data adequacy.

Data is more than about what happened in the past. Data predictive analytics opens the window into the future. Banks with predictive analytics can assess what might happen. They can weigh scenarios, prepare responses, influence outcomes and get ahead of the risks. Some Luxembourgish banks are already using advanced data techniques to enhance customer experiences and detect fraud. Over time, trusted data will increase its revenue potential as it is used for other regulatory reporting and AML remediation processes.Data is at the centre of banking transformation considerations. It impacts everyone; front and back offices, risk, control and internal audit functions. Data is what fuels data analytics, machine learning and AI; without large amounts of high-quality data, it is virtually impossible to get insights from AI models. The idea is straightforward, successful digital strategies are built on data. The better your data management, the more effective your digital strategy will be.

Bank regulators recognise advanced AI-based technologies, and expect them to be incorporated in the next evolution in

the Banking systems framework. They also expect any risks associated with AI-influenced decisions to have been identified and managed. Data collectors, such as the ECB and CSSF, will also make use of AI techniques to increase the efficiency and quality of their supervision (offsite and onsite) and to anticipate risks in the banking environment. Meanwhile, the current situation in Luxembourg is that complex and heterogeneous legacy IT systems, with multiple data providers and weak data governance, impede the use of data analytics and AI. The opportunity for banks is to decentralise data and make it accessible to all departments, at all levels. To fully benefit from the AI advantage, data management, over time, needs to be as easy and widespread as use of spreadsheets. Bank staff need to comfortably manipulate, visualise and analyse data. A further opportunity for banks, as a long-term commitment to their employees and to fill current skills gaps, is to embark on corporate-wide data upskilling strategy. A well-developed and executed upskilling program will go a long way to ensure efficiencies through the adoption of advanced techniques.

In God we trust, all others must bring data” Dr. W. Edwards Deming, US

According to PwC’s 22nd Annual Global CEO Survey (October 2018), 63% of CEO’s believe that data analytics and artificial intelligence will have larger impact than the internet revolution.

95%

94%

15%

41%

24% 22%29%

18% 17%21%

16%

89% 90% 87% 86% 84%

70%66%

42%

21% 35%31%

23%30%

20% 23% 26%17%

92% 92% 93%88% 85%

72% 73%

38%

Data about your customers’ and clients’

preferences and needs

Critical/important

Comprehensive

Financial forecasts and projections

Data about your brand and

reputation

Data about the risks to which the business is

exposed

Data about your employees’ views and

needs

Benchmarking data on the

performance of your industry

peers

Data about the effectiveness of your R&D processes

Data about your supply

chain

Data about the impact of

climate change on the business

2019 Critical/important2019 Comprehensive

2009 Critical/important2009 Comprehensive

17PwC Luxembourg

Smart Identity

Rapidly advancing technologies, evolving customer expectations and a changing regulatory landscape are opening new doors yet also create challenges for financial services providers. How to leverage on cutting-edge technologies, respond to growing demands while also limiting risks?

Smart IdentityWhat is it all about?Smart Identity is enabled by unlocking the power of three key technologies:

1Biometrics

& identity management

Instantly know who your traveller is, with certainty

2Automation and live risk assessment

Automate low added-value tasks, and respond to situations when they occur.

3AI & Machine

learning

Rapidly learn from past events and continually improve.

What is at stake?The following key challenges need to be addressed by financial services in order for them to remain competitive:

Improve client processes and customer satisfactionFrom onboarding (i.e. KYC) to service provision – how to meet customer demands without impacting profitability?

Prevent regulatory risks With PSD2, AML and other regulations changing the end-user interaction in the banking world – how to streamline compliance in processes?

Enhance security without disrupting the experience Recent security threats and data breaches have dramatically impacted security requirements – how to enhance security without negatively impacting client experience?

62%of millennials are interested in using

biometrics for payments

17is the number of passwords the average customer has to remember (and forget)

+22%in the use of biometrics within financial

services between 2017 and 2024

18Banking in Luxembourg

Impact Banking

In the past decade, the banking sector in Luxembourg has changed. Many of the industry’s traditional and previously successful business models have reached their limits and their profitability is decreasing steadily. This is – among other reasons – why today’s business models vary from the previous ones. The need for a vitalisation of the market – e.g. through new products or services, new client segments and markets – is increasingly recognised. Based on market insights, sustainable finance might be one of the most important trends in modern banking – with the potential to provide answers for the currently indistinct future of banking.

Besides the already broader role of banks in today’s society, rising market-, regulatory- and portfolio risk pressure force the whole sector to start thinking in entirely new ways. Environmental, social and governance (ESG) criteria increasingly influence investment decisions. The demand for according products and services grows significantly. Several banks have already started an active, sustainability-driven portfolio management to enable profitability in the future. In other words, sustainable banking cannot and will not be averted.

But how can banks act responsible while many of their clients do not? Additionally, when more and more banks incorporate sustainability in their corporate governance and, for instance, apply ESG-criteria in their credit counterparty screening – what does that mean for non-sustainable banking clients? For banks, it is worth critically assessing ESG-impacts when determining a client’s credit default risk. Considering these factors verifiably leads to fewer individual value adjustments and a lower amount of realised losses. As a result, it can be expected that banks, which position themselves sustainably will start to reject non-sustainable companies in their credit approval process. Consequently, it will become increasingly difficult for these companies to obtain loans.

PwC Luxembourg and ABBL (The Luxembourg Bankers’ Association) first developed the concept of Impact Banking in 2018.

The concept of Impact Banking will empower banks to utilise Luxembourg’s USPs – e.g. its globally unique financial ecosystem, its regulatory agility, its market access or its specialised human capital – to:• rapidly develop new – sustainable – business models, products and services,• actively shape and influence the development of new regulations in the field of

sustainable finance,• benefit from the ‘first mover’ implementation of new EU regulations and requirements

– long before international competitors do, and• drive sustainable revenues within their group as sustainable finance competence

centre.

Accordingly, Luxembourg as a worldwide leading financial centre contributes to a more sustainable global economy. For instance, this is reflected in the latest Global Green Finance Index (GGFI), which ranks the country among the top green financial centres worldwide.8 In addition, forecasts of the GGFI indicate that Luxembourg’s green finance offerings will yet improve significantly in the short - to medium - term.

8 The Global Green Finance Index 2: https://www.greenfinanceindex.net/static/pdf/ggfi2_report.pdf

19PwC Luxembourg

20Banking in Luxembourg

Banking activity in Luxembourg can either take the form of a branch or of a legal entity in the country (e.g. subsidiary of a foreign credit institution). The shareholders of the legal entity can be institutional or private investors. Several foreign credit institutions operate in Luxembourg as a branch or a subsidiary.

3. Setting up acredit institutionin Luxembourg

Licensing Authorisation Process

Introduction File submission Authorisation License

CSSF notification to the European Central Bank (ECB) on receipt of an application for

authorisation.Examination by the CSSF of the application file and proposition to the ECB of a draft decision containing its assessment and

recommendations.Final decision is with the ECB.

Submission to the CSSF of the application file, satisfying the

local regulatory requirements in force, and including mandatory

information based on the amended Law of 5 April 1993.

Introductory meeting between senior representatives of the

applicant and the CSSF.

Authorisation from the ECB*, based on CSSF proposition.

European PassportPossibility for a Luxembourg incorporated bank to provide banking services to European Union residents, either by the establishment of a branch, or by way of free provision of services, in each EU country via a notification procedure summarised below.

- Filing of a specific questionnaire (“notification file”) related to the future bank/branch’s programme of operations in the host EU country, list of investment services, financial instruments, internal organisation, etc.

- Communication by the CSSF of the required information to the foreign competent authority. - The bank/branch may start providing its services in the host EU country.

* For a Luxembourg legal entity (S.A.) set up

21PwC Luxembourg

MonthsProject

milestones

Project Timeline

2 4 6 8 10 12 14 16 18

Introductory meeting with

CSSF

Submission of application file to CSSF

Preparation for CSSF meeting

Preparation of application file

Preparation for business

commencement

Post-application submission Licensing: 12 to 14 months (estimate)

Green light from the CSSFFiling of the application

file to the ECB

ECB formal approval

“Go Live” Day

Internal Governance Requirements: Illustrative example for a less significant institution

* Luxembourg branches of non-EU banks contribute to the Luxembourg Resolution Fund

Shareholding

• Notification of the identity of all shareholders and ultimate beneficial owners• “Fit & proper” test for qualified shareholders

Bank

• Available legal forms S.A., S.C.A., Société coopérative, establishment under public law

• Minimum share capital of EUR 8.7 million• Decision-making centre in Luxembourg • Minimum organisational requirements• Participation in: Luxembourg deposit guarantee

scheme; Luxembourg investor indemnification system and the Single Resolution Fund*

• Data and IT infrastructure requirements• Mandatory control functions

Authorised Management (“AM”)

• Minimum two managers• Luxembourg residents• “Fit & proper” test• Sufficient time commitment to perform their duties

Optional - Specialised Committee 1: Audit Committee

• Minimum three directors • Chairman = person with knowledge in the relevant

areas• Invitees (external experts, CIA, CCO,CRO)

Compliance Function

• Headed by the Chief Compliance Officer (CCO)• Permanent and independent function • Oversight, detection and assessment of the

Compliance risks• “Fit & proper” test

Optional - Specialised Committee 2 (Risk, Compliance, Remuneration,

Nomination, etc.)

• Minimum three directors• Chairman = person with knowledge in the relevant

areas• Invitees (external experts, CCO, CRO, etc.)

Internal Audit Function

• Headed by the Chief Internal Auditor (CIA)• Permanent and independent function• Evaluation of the effectiveness of the internal control,

central administration and governance requirements• Delegation possible under certain conditions• “Fit & proper” test

Board of Directors (“BoD”)

• Minimum three reputable and experienced directors• Not mandatorily Luxembourg residents• Approved by the CSSF/ECB• Composed of a majority of non-executive members• Chairman of the BoD cannot be member of the

Authorised Management (AM)• Fit & proper test• Sufficient time commitment to perform their duties

Risk Management Function

• Headed by the Chief Risk Officer (CRO)• Permanent and independent function • Oversight, detection, evaluation, follow-up, control and

assessment of all existing and potential risks• “Fit & proper” test

Direct access and reporting

Direct access and reporting

Reporting, counsel and advice Reporting, counsel and adviceReporting, counsel and advice

Regular reporting

Assistance and advice

Assistance and advice

The bank can start the preparation work in advance while waiting for the regulator’s in-principle approval to reduce the time needed to set up the infrastructure and frameworks thereafter.

22Banking in Luxembourg

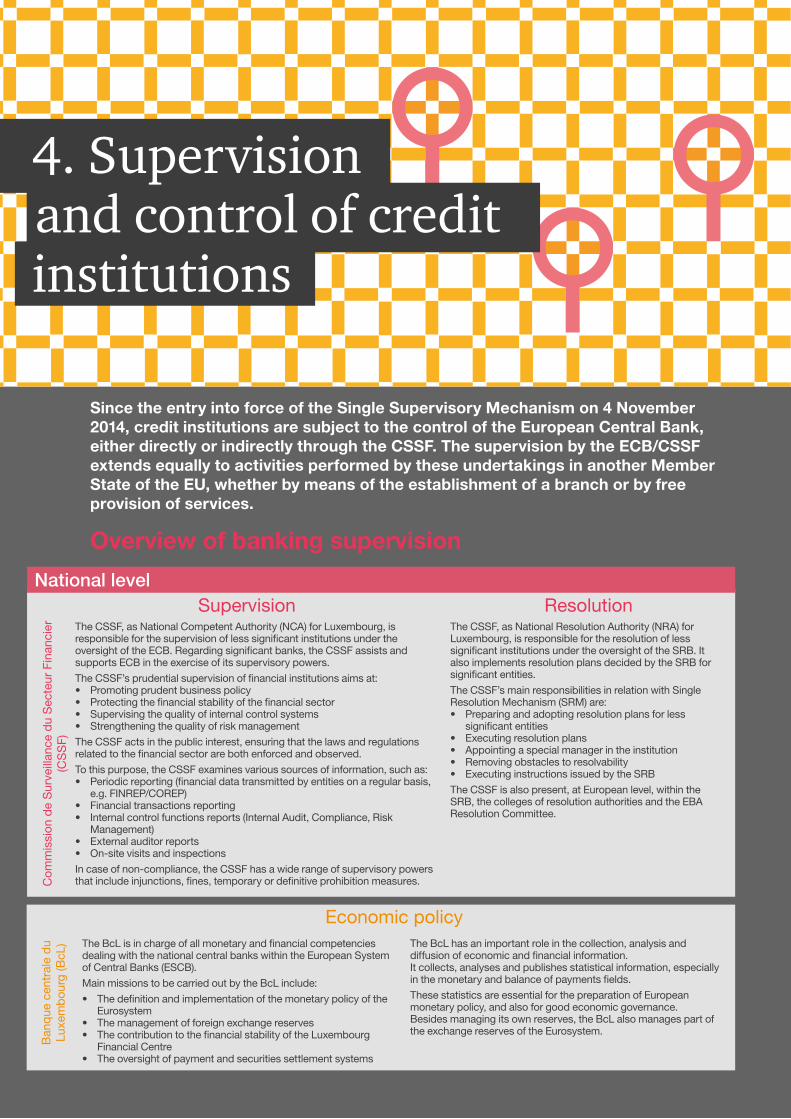

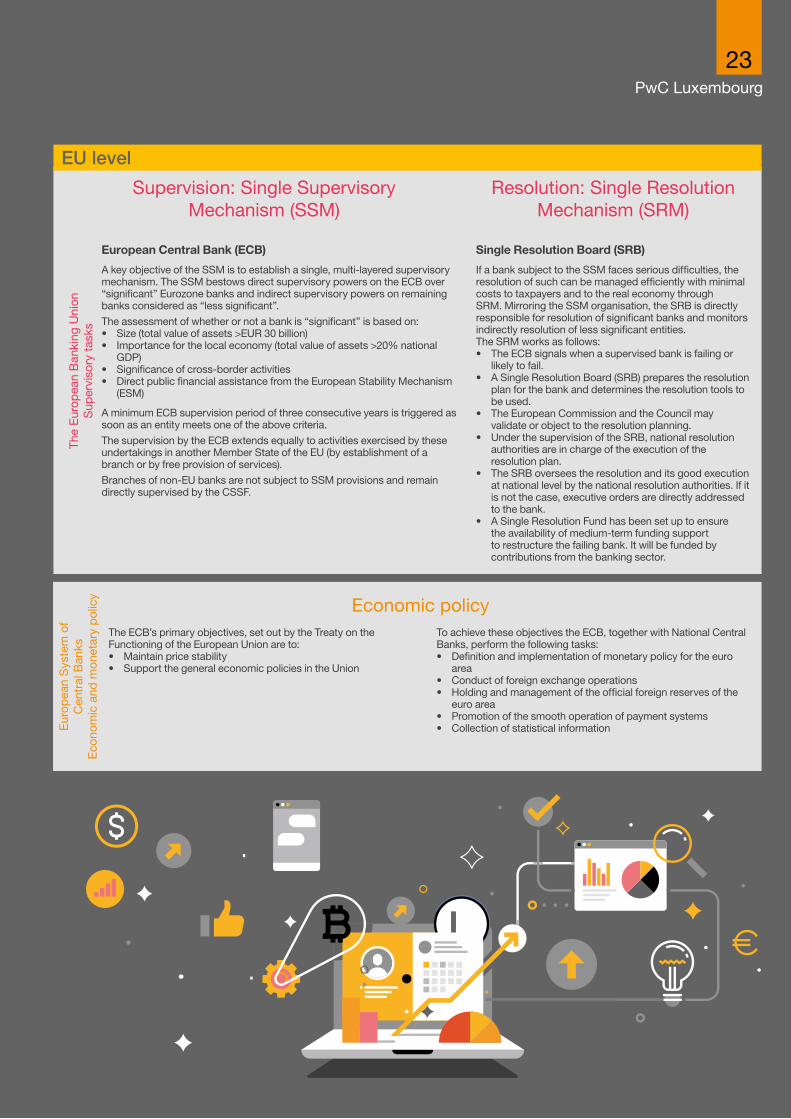

Since the entry into force of the Single Supervisory Mechanism on 4 November 2014, credit institutions are subject to the control of the European Central Bank, either directly or indirectly through the CSSF. The supervision by the ECB/CSSF extends equally to activities performed by these undertakings in another Member State of the EU, whether by means of the establishment of a branch or by free provision of services.

4. Supervisionand control of creditinstitutions

Overview of banking supervision

National level

The CSSF, as National Competent Authority (NCA) for Luxembourg, is responsible for the supervision of less significant institutions under the oversight of the ECB. Regarding significant banks, the CSSF assists and supports ECB in the exercise of its supervisory powers.

The CSSF’s prudential supervision of financial institutions aims at:• Promoting prudent business policy• Protecting the financial stability of the financial sector• Supervising the quality of internal control systems• Strengthening the quality of risk management

The CSSF acts in the public interest, ensuring that the laws and regulations related to the financial sector are both enforced and observed.

To this purpose, the CSSF examines various sources of information, such as:• Periodic reporting (financial data transmitted by entities on a regular basis,

e.g. FINREP/COREP)• Financial transactions reporting • Internal control functions reports (Internal Audit, Compliance, Risk

Management) • External auditor reports• On-site visits and inspections

In case of non-compliance, the CSSF has a wide range of supervisory powers that include injunctions, fines, temporary or definitive prohibition measures.

The CSSF, as National Resolution Authority (NRA) for Luxembourg, is responsible for the resolution of less significant institutions under the oversight of the SRB. It also implements resolution plans decided by the SRB for significant entities.

The CSSF’s main responsibilities in relation with Single Resolution Mechanism (SRM) are:• Preparing and adopting resolution plans for less

significant entities• Executing resolution plans• Appointing a special manager in the institution• Removing obstacles to resolvability• Executing instructions issued by the SRB

The CSSF is also present, at European level, within the SRB, the colleges of resolution authorities and the EBA Resolution Committee.

The BcL is in charge of all monetary and financial competencies dealing with the national central banks within the European System of Central Banks (ESCB).

Main missions to be carried out by the BcL include:

• The definition and implementation of the monetary policy of the Eurosystem

• The management of foreign exchange reserves• The contribution to the financial stability of the Luxembourg

Financial Centre• The oversight of payment and securities settlement systems

The BcL has an important role in the collection, analysis and diffusion of economic and financial information.It collects, analyses and publishes statistical information, especially in the monetary and balance of payments fields.

These statistics are essential for the preparation of European monetary policy, and also for good economic governance.Besides managing its own reserves, the BcL also manages part of the exchange reserves of the Eurosystem.

Com

mis

sion

de

Sur

veill

ance

du

Sec

teur

Fin

anci

er

(CS

SF)

Ban

que

cen

tral

e d

u Lu

xem

bou

rg (B

cL)

Supervision Resolution

Economic policy

EU level

European Central Bank (ECB)

A key objective of the SSM is to establish a single, multi-layered supervisory mechanism. The SSM bestows direct supervisory powers on the ECB over “significant” Eurozone banks and indirect supervisory powers on remaining banks considered as “less significant”.

The assessment of whether or not a bank is “significant” is based on:• Size (total value of assets >EUR 30 billion)• Importance for the local economy (total value of assets >20% national

GDP)• Significance of cross-border activities• Direct public financial assistance from the European Stability Mechanism

(ESM)

A minimum ECB supervision period of three consecutive years is triggered as soon as an entity meets one of the above criteria.

The supervision by the ECB extends equally to activities exercised by these undertakings in another Member State of the EU (by establishment of a branch or by free provision of services).

Branches of non-EU banks are not subject to SSM provisions and remain directly supervised by the CSSF.

Single Resolution Board (SRB)

If a bank subject to the SSM faces serious difficulties, the resolution of such can be managed efficiently with minimal costs to taxpayers and to the real economy through SRM. Mirroring the SSM organisation, the SRB is directly responsible for resolution of significant banks and monitors indirectly resolution of less significant entities.The SRM works as follows:• The ECB signals when a supervised bank is failing or

likely to fail. • A Single Resolution Board (SRB) prepares the resolution

plan for the bank and determines the resolution tools to be used.

• The European Commission and the Council may validate or object to the resolution planning.

• Under the supervision of the SRB, national resolution authorities are in charge of the execution of the resolution plan.

• The SRB oversees the resolution and its good execution at national level by the national resolution authorities. If it is not the case, executive orders are directly addressed to the bank.

• A Single Resolution Fund has been set up to ensure the availability of medium-term funding support to restructure the failing bank. It will be funded by contributions from the banking sector.

The ECB’s primary objectives, set out by the Treaty on the Functioning of the European Union are to:• Maintain price stability• Support the general economic policies in the Union

To achieve these objectives the ECB, together with National Central Banks, perform the following tasks:• Definition and implementation of monetary policy for the euro

area• Conduct of foreign exchange operations• Holding and management of the official foreign reserves of the

euro area• Promotion of the smooth operation of payment systems• Collection of statistical information

The

Eur

opea

n B

anki

ng U

nion

Sup

ervi

sory

tas

ks

Eur

opea

n S

yste

m o

f C

entr

al B

anks

Eco

nom

ic a

nd m

onet

ary

pol

icy

Supervision: Single Supervisory Mechanism (SSM)

Resolution: Single Resolution Mechanism (SRM)

Economic policy

23PwC Luxembourg

24Banking in Luxembourg

5. Regulatoryprovisions

The financial sector becomes increasingly regulated by European regulations and directives, in addition to national laws. Credit institutions need to comply with many requirements.

To be able to provide you with the most up to date information, we decided to include a separate flyer including all the most important laws, directives, regulations and circulars. We will update this flyer on a regular basis and keep you informed.

25PwC Luxembourg

26Banking in Luxembourg

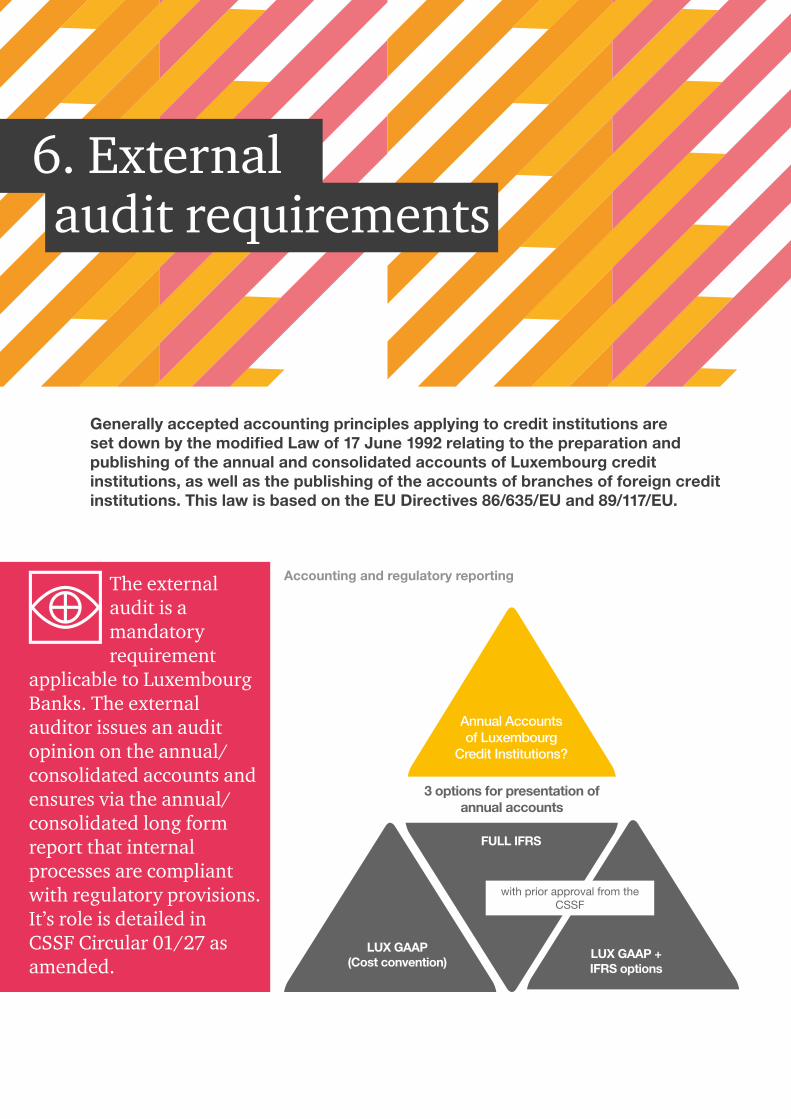

Generally accepted accounting principles applying to credit institutions are set down by the modified Law of 17 June 1992 relating to the preparation and publishing of the annual and consolidated accounts of Luxembourg credit institutions, as well as the publishing of the accounts of branches of foreign credit institutions. This law is based on the EU Directives 86/635/EU and 89/117/EU.

6. External audit requirements

The external audit is a mandatory requirement

applicable to Luxembourg Banks. The external auditor issues an audit opinion on the annual/consolidated accounts and ensures via the annual/consolidated long form report that internal processes are compliant with regulatory provisions. It’s role is detailed in CSSF Circular 01/27 as amended.

Accounting and regulatory reporting

3 options for presentation of annual accounts

Annual Accounts of Luxembourg

Credit Institutions?

LUX GAAP(Cost convention)

LUX GAAP +IFRS options

FULL IFRS

with prior approval from the CSSF

27PwC Luxembourg

28Banking in Luxembourg

The transposition of EU Directives and OECD recommendations into domestic law continues to be the focus of the Luxembourg government, following the ever-growing need for transparency on a global scale with respect to tax.

7. Taxation in Luxembourg

Luxembourg, well-known for its stability in terms of legislation and tax environment, is nonetheless adapting its legislation to translate into its national law the EU Directives and OECD recommendations that have been quite numerous for the past few years.

The EU Anti-Tax Avoidance Directive (ATAD Directive) was implemented in 2018. The attention of the Luxembourg government for the year 2019 will focus on the introduction of the Multilateral Instrument (MLI) and the EU Directive on Administrative Cooperation (DAC 6) into domestic law.

In 2017, Luxembourg was one of the original 68 jurisdictions to sign the OECD-sponsored Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting – commonly referred to as the “Multilateral Convention” or “MLI”.

This MLI should significantly change the tax practice when tax treaties are involved, while DAC6 should enhance the exchange of information between Member States through the mandatory disclosure by intermediaries of certain cross-border transactions.

Transfer pricing rules introduced since 2015 continue to evolve, strengthening the basic arm’s length principles. The transposition into Luxembourg law of article 80 of the EU VAT Directive is a notable example of this trend.

The efforts made by Luxembourg to comply with OECD requirements should however not hide its dedication to the improvement of the Luxembourg tax system, illustrated in 2018 by the introduction of the VAT grouping regime in Luxembourg law and the decrease of the corporate tax rate, a decrease that will continue in 2019 to reach a 24.94% nominal tax rate.

Thanks to the pro-active and constant business-minded approach taken by the Luxembourg government in turning international political intentions into reality for more transparency and tax compliance, Luxembourg is fully compliant with the new OECD rules, which set global standards to ensure the balance between transparency, compliance and the client’s needs for a high level of privacy protection.

29PwC Luxembourg

Latest tax developments

We do not expect Financial Institutions to be impacted significantly by the transposition of the EU Directive on Anti-Tax Avoidance measures. It goes differently for the other EU and OECD measures that Luxembourg will continue to implement. In this respect, the introduction of the DAC6, the MLI and the Transfer Pricing provisions in VAT law will impact Financial Institutions in Luxembourg. On the other hand, the introduction of the VAT Group, the decrease of the corporate income tax rate, the revision of the tax regime for expatriates and stock option plans as well as the flexibility given to cross-borders worker will maintain Luxembourg as an attractive EU country.

ATAD – EU Anti-Tax Avoidance Directive

As from 1 January 2019, a new set of rules aiming at fighting tax avoidance has been translated into Luxembourg domestic law. Those rules focus on the following areas:• Interest limitation rule• Controlled foreign company (CFC) rule• General anti-abuse rule (GAAR)• Intra-EU anti hybrid rule• Exit taxation rule (entry into force as from 2020).

The purpose of the interest limitation rule is to limit excessive base erosion through tax deductible interest. To this end, the deduction of excess borrowings costs should be denied when they exceed 30% of the EBITDA. The law however excludes several taxpayers from the scope of the limitation, including credit institutions. The law also excludes securitisation vehicles that are governed by Article 2 point 2 of Regulation (EU) 2017/2402 but it is still unclear whether this should include Luxembourg securitisation vehicle falling under the law of 22 March 2004.

Controlled foreign company rules apply for companies having a controlled entity or a permanent establishment in a low tax jurisdiction (i.e., where effective tax rate is less than half of Luxembourg’s corporate income tax of 18% - expected to be 17% in 2019). Taxpayers should include in their tax base the non-distributed income of the CFC deemed to have arised from non-genuine arrangements when computing corporate income tax.

The general anti-abuse rule (“GAAR”) does not bring significant change to Luxembourg law as it already included an abuse of law rule with similar provisions. The latter was reworded to match more precisely the ATAD version of the GAAR.

The purpose of the intra-EU anti-hybrid rule is to eliminate hybrid mismatches within the EU leading to double non-taxation or deduction without inclusion in the other country. This rule will however be significantly reshaped as from 1 January 2020 with the entry into force of the law transposing ATAD II.

DAC 6 – EU Directive on Administrative Cooperation

On 13 March 2018, the ECOFIN Council voted political agreement in the field of taxation in relation to reportable cross-border arrangements (DAC 6). The main purpose of DAC 6 is to strengthen tax transparency and the fight against aggressive tax planning through the disclosure of cross-border arrangements, Common Reporting Standards (CRS) avoidance schemes and offshore structures.

The first reportable transactions will be those whose first implementation step occurs between 25 June 2018 and 1 July 2020 (i.e. the date of application of the Directive).

This information will be reported to tax authorities by 31 August 2020, leaving only one month to collect and report information.

The impacts of the Directive for Financial Institutions could be significant and further guidance from the Luxembourg Tax Authorities is expected.

Introduction of the VAT Group

Starting July 2018, Luxembourg has introduced the VAT Grouping regime into its domestic law further to a CJEU decision restricting the application of the cost-sharing / Independent Group of Persons (“IGP”) VAT exemption. The VAT Grouping regime offers an alternative to the Individual Group of Persons (IGP) regime since transactions between the VAT group members are disregarded for VAT purposes and are not subject to VAT. The VAT Group is optional and limited to Luxembourg entities (including Luxembourg permanent establishments of foreign entities) bound by financial, economic and organisational links.

This regime could be attractive for Financial Institutions sharing resources between different entities in Luxembourg.

30Banking in Luxembourg

Transfer pricing provisions in VAT law

Since July 2018, Luxembourg has transposed article 80 of the EU VAT Directive into domestic law. It provides that the VAT Authorities may disregard the consideration or price agreed between related parties when this consideration or price does not reflect the open market value that would be agreed upon in a transaction between independent parties.

Amendments to the favorable tax regime for Expats/Revision of the stock options/warrants tax regime

The programme of the Luxembourg Government foresees the revision of the current special tax regime for expats to make it more attractive. It foresees as well amendments to the current favorable stock options / warrants tax treatment.

Employment in Luxembourg

Being located at the crossroads of Europe, Luxembourg attracts every day 186,649 cross-border commuters from France, Belgium and Germany. With most of them speaking two or more languages and the educational background acquired in their home country, Luxembourg is able to offer diversified services to a broad range of clients across the EU.

Luxembourg and neighboring countries clarified certain tax rules applicable to cross-border commuters allowing commuters to work up to 19 days outside Luxembourg for German tax residents and 24 days for Belgian tax residents while the taxation rights on the salary remain attributable to Luxembourg (subject to the provisions of the income tax conventions concluded between the country of residence and countries where the non-Luxembourg workdays are exercised). A similar arrangement has been agreed on with France in the new Income Tax Convention signed between the two countries in 2018, allowing French residents to work maximum 29 days outside Luxembourg while remaining taxable on their entire compensation in Luxembourg. It is expected that the new French/Luxembourg Income Tax Convention will enter into force as from 1 January 2020.

Luxembourg offers the 5th lowest tax wedge in the EU (for a single person without children at the income level of the average worker).

In particular, Luxembourg has the 7th lowest average rate of employer social security contributions within the EU (15% of the gross remuneration capped at EUR 10,355.50 per month in 2019).

Cross-border commuters (in %) Tax wedge as a percentage of labour costs (2017)

France 51%

Belgium 25%

Germany 24%

Belgium

Germany

Italy

France

Austria

Hungary

Czech Republic

Slovenia

Finland

Sweden

Latvia

Slovakia

Portugal

Greece

Spain

Estonia

Netherlands

Luxembourg

Denmark

Poland

United Kingdom

Ireland

Source: OECD (information not available regarding Bulgaria, Croatia, Cyprus, Lithuania, Malta and Romania)

Source: Statec

█ Income Tax █ Employer SSC█ Employee SSC

60%50%40%30%20%10%0%

14.92% 10.97%10.84%

31PwC Luxembourg

Evolution of corporate income tax rates (2015 to 2019)

VAT in the EU - Normal rates (2018)

Lowest VAT rate in the EU• General VAT rate of 17%• 14% applicable for management/

safekeeping of securities• Various exemptions and reliefs in respect

of certain financial services transactions• Management of a collective investment

fund generally VAT exempt (note: the VAT exemption for investment fund management is widely drawn in Luxembourg)

• Exemptions lead to a restriction on the recovery of VAT on costs

• Special partial exemption methods for input tax recovery can be agreed

Favorable tax regime for impatriates and efficient remuneration tools• Beneficial tax regime for qualifying international employees transferred to or recruited in

Luxembourg, including the partial or full exemption of allowances/refund of expenses paid by the employer (housing cost, tax equalisation, cost of living allowance, tuition fees, etc.)

• Upfront taxation at 20% for employer’s contributions to occupational pension plans (to be borne by the employer). Tax free exit in the form of capital payment

• Payment of bonuses in the form of options/warrants: the granting of unconditional, freely tradeable options may be taxed based on a lump-sum valuation method and allow access to an efficient effective tax rate

• If certain conditions are met, the gain at exit of a long term incentive plan may be treated as a capital gain, potentially tax free

Low effective personal tax/personal social security contributions• Progressive personal tax rates from

0-45.78% (including surcharge for unemployment fund)

• Employer social charges amounting to roughly 15% of gross salary, calculated on a basis capped at approx. EUR 125,000 per year

Other attractive measures• Luxembourg transfer pricing rules follow

OECD principles. Advanced pricing agreements may be obtained

• 13% Investment tax credits, 8% on acquisition of softwares

• No bank levy, no financial transaction tax, no stamp duty

• Functional currency allowed in case of non EUR-denominated accounts

• Incentives for transactions having impact on the economic development, including interest subsidies and tax credits

Attractive corporate tax framework• 26.01% corporate tax rate in Luxembourg

City (expected to be 24.94% for Luxembourg City in 2019)

• 0.5% - 0.05% annual wealth tax (may be reduced)

• Withholding tax on dividends: 15%, reduced or exempt under Double Tax Treaties (DTTs) and EU Parent/Subsidiary Directive

• 0% withholding tax on interest and royalties• 20% withholding tax on directors fees• Advance Tax Clearances may be obtained• 83 DTTs in force

Tax

201520%

25%

30%

35%

2016 2017 2018 2019

Netherlands Luxembourg ItalyGermany France Belgium

Source: PwC, OECD Source: European Commission

0%

5%

10%

15%

17%20%

25%

30%

Luxe

mb

ourg

Mal

taC

ypru

sFr

ance

Ger

man

yR

oman

iaU

nite

d K

ingd

omE

ston

iaA

ustr

iaS

lova

kia

Bul

garia

Latv

iaLi

thua

nia

Net

herla

nds

Bel

gium

Cze

ch R

epub

licS

pai

nIta

lyS

love

nia

Pol

and

Por

tuga

lIre

land

Gre

ece

Finl

and

Cro

atia

Sw

eden

Den

mar

kH

unga

ry

• Luxembourg has the second lowest corporate tax rate in 2018 amongst EU founding members (i.e. 26.01%).

• Luxembourg corporate income tax rate is expected to be lowered in the course of 2019 to reach 24.94%.

• Luxembourg has the lowest VAT normal rate (i.e. 17%) within the EU.

32Banking in Luxembourg

The revised Payment Services Directive (PSD2) entered into force in Europe in January 2018. By law, banks have to make customer data available to third parties in a secure manner. Apart from new compliance challenges to be addressed, banks will also need to reflect on their future business strategy. How do they organise themselves and operate in a world of “open banking”?

8. Payment Services

Directive 2

The context in which PSD2 entered into force: payments market and trends

Global non-cash transactions broke a record last year, reaching almost 483 billion transactions with a 10.1% growth. According to World Payment Report 2018, global non-cash transaction volumes will record a Compound Annual Growth Rate of 21.6% during 2016–2021.

The increasing digitisation was favoured mainly by three areas:

1 2 3

an increased readiness of users, from all population groups, in using tech devices

a change in consumer habits, who find these paying methods more efficient

an evolution of the market offered by players that adopt marketing strategies aimed at increasing the use of electronic tools and collecting information on customers’ behaviour

33PwC Luxembourg

Furthermore, the emergence of new players is increasing the level of competition, the over-the-top players, e.g. Google, Amazon, and Apple and new Third Party Providers (TPP), e.g. Sofort and Trustly, are changing the traditional context of the banking services, creating new business models for banks to deal with.

In Europe, new competitors are gaining market share. Case in point: in Germany, Sofort has become leader in e-commerce payments with over 2 million transactions per month and 35,000 merchants in less than 10 years.

In this context, the PSD2 takes care of encouraging the use of innovative digital tools and, at the same time, of regulating services and payment practices already in force, such as apps which aggregate the balances of several bank accounts or sending money via social networks.

PSD2

Encourage market dynamics

Increase competition

Foster Innovation

Improve Consumer protection

PSD2 interdependency with other regulations

Another striking element of PSD2 lies in the interdependencies with other regulations. The General Data Protection Regulation (GDPR) represents a complex implementation with multiple stakeholders. For many banks, compliance proved to be a challenge. But mere compliance – though, challenging in itself, cannot be banks’ only concern. As of today, few banks have experienced granting third parties access to customer data or payment functionality via application programming interfaces, so-called APIs. However, banks shall provide such access, for testing purposes, to third parties by 14 March 2019. The opening up to third parties is understandably associated with operational and security risks, which need to be addressed by mitigating measures as defined by the regulatory technical standards for strong customer authentication and common and secure open standards of communication. Banks will also need to find a proper strategic response to avoid becoming disintermediated by more customer-oriented third-party offerings. Furthermore, real revenues are at stake. We can mention the lucrative card business, since third-party providers could offer low-cost “payment initiation services” to compete for that business.

Additionally, banks are required to fulfil several reporting obligations, namely reporting of any major incident, annual reporting of fraudulent transactions, as well as reporting on measures to mitigate operational and security risks. Such has to be performed already for 2018.

The bottom line is that it is time for banks to move beyond talk and analysis – they should take decisive steps.

34Banking in Luxembourg

New business models

Encouragingly, two out of three banks in a recent PwC study say they want to use PSD2 to change their strategic positioning. In order to do so, banks will need to analyse the emerging payments landscape bearing in mind their main strengths as well as FinTech players’. They can then begin to identify new revenue opportunities for services. This can include AISPs (Account Information Service Providers) or PISPs (Payment Initiation Service Providers), and consider new business models.

Comparing strengths of Banks and FinTechs

25% New technologies

24% Secure infrastucture

4% Other

3% Other

7% Less liability

9% Customer demands 13%

Data availability

14% Lighter regulation

18% Professional experience

19% Improved user experiences

20% Knowledge of customers

22% Customer experience

22% Existing customer base

Fin

Tech

’s m

ain

stre

ngth

s

Ban

ks’ m

ain

stre

ngth

s

Source: PwC, Waiting until the Eleventh Hour, European Bank’s reaction to PSD2, October 2017

35PwC Luxembourg

Strategic conversation & the future of Open-Banking

Banks, which will limit themselves to ensuring compliance with the extensive requirements of the Directive, will only generate additional effort and related costs, while facing the risk of disintermediation from their client base. It is therefore also important for banks to consider strategic alternatives, such as creating a partnership with other financial players or building up new innovative technologies in-house, based on their size, their customer base and their abilities to innovate.

The concept of open-banking, as a collaborative model among several players, both financial as well as non-financial, using open technological platforms, sharing knowledge, work environments, data and customer bases should be explored by banks as a long term alternative for the benefit of creating additional services and products.

An open-banking approach will allow players to extend their offering, enhance internal processes and systems, enlarge customer bases as well as digitalise and improve products and services. The opportunities do not stop at the retail customer, but commercial clients carry even bigger potential.

£7.2bnrevenue opportunity created by Open Banking by 2022

71%of SMEs expected to adopt it by 2022

64%of adults expected to be adopters by 2022

48%of retail banking customers & 54% of SMEs state secu-rity is their biggest concern with Open Banking data sharing

Which strategic positioning are Banks aiming to achieve in the long term?

Add

ed v

alue

to th

e pr

opos

ition

of t

he b

anks

Data Openness

High

HighLow

Compliant player

• Reactive approach• The service is developed from other

bank• Giving data to other bank

Bank-as-a-Platform

• Open API platform• Cooperation with Financial (or not) com-

panies• Providing data to third parties to build up

new services and value-added services

Bank-as-an-Aggregator

• Assembly of new business ideas and data

• Expansion of product offering• Flexible sourcing of new functionalities

through third parties

Bank-as-Platform-Aggregator

• Expanding banking to new use cases by enabling partners to integrate bank modules in own offerings

• Support innovation through collaboration with external partners

• Assembly of new business ideas and data

7% 14%

29% 50%

Source: PwC, Roles for Banks and payment operators: How the scenario might evolve in the future, October 2017

36Banking in Luxembourg

9. Appendix

Administration des contributions directes45, boulevard RooseveltL-2982 LuxembourgTel.: +352 247-52440 www.impotsdirects.public.lu

Administration de l’Enregistrement et des Domaines1-3, avenue GuillaumeL-1651 LuxembourgTel.: +352 247 808 00www.aed.public.lu

Association des Banques et Banquiers, Luxembourg (ABBL)12, rue ErasmeL-1468 LuxembourgTel.: +352 46 36 60-1www.abbl.lu

Association Luxembourgeoise des Compliance Officers (ALCO)12, Rue ErasmeL-1468 LuxembourgTel.: +352 289 925 00www.alco.lu

Association Luxembourgeoise des Fonds d’Investissement (ALFI)12, rue ErasmeL-1468 LuxembourgTel.: +352 22 30 26-1www.alfi.lu

Conseil de Protection des Deposants et des Investisseurs (CPDI)283, route d’ArlonL-1150 LuxembourgTel.: +352 26 251-1www.cssf.lu

Banque centrale du Luxembourg (BcL)2, Boulevard RoyalL-2983 LuxembourgTel.: +352 47 74-1www.bcl.lu

Parquet Economique et Financier - Cellule de Renseignement FinancierBâtiment PL, Cité JudiciaireL-2080 LuxembourgTel.: +352 47 59 81 501

Chambre de Commerce du Grand-Duché de Luxembourg7, rue Alcide de GasperiL-2981 LuxembourgTel.: +352 42 39 39-1www.cc.lu

Haut Comité de la Place financière3, rue de la CongrégationL-1352 LuxembourgTel.: +352 247-82600

Useful Luxembourg addresses

37PwC Luxembourg

Commissariat aux Assurances (CAA)7, boulevard Joseph IIL-1840 LuxembourgTel.: +352 22 69 11-1www.commassu.lu

Commission de Surveillance du Secteur Financier (CSSF)283, route d’ArlonL-1150 LuxembourgTel.: +352 26 251-1www.cssf.lu

Institut Luxembourgeois des Administrateurs (ILA)19, rue de BitbourgL-1273 LuxembourgTel.: +352 26 00 21 487www.ila.lu

Fédération des professionnels du secteur financier, Luxembourg (PROFIL)12, rue ErasmeL-2010 LuxembourgTel.: +352 27 20 37-1www.profil-luxembourg.lu

House of Training7, rue Alcide de GasperiL-1615 LuxembourgTel.: +352 46 50 16-1www.houseoftraining.lu

Institut des Réviseurs d’Entreprises (IRE)7, Alcide de GasperiL-1615 LuxembourgTel.: +352 29 11 39-1www.ire.lu

Luxembourg For Finance (LFF)12, rue ErasmeL-1468 LuxembourgTel.: + 352 27 20 21 1www.luxembourgforfinance.lu

Faculté de Droit, d’Économie et de FinanceLuxembourg School of FinanceBâtiment K24, rue Albert BorschetteL-1246 Luxembourg-KirchbergT.: + 352 46 66 44 6460wwwfr.uni.lu/luxembourg_school_of_finance

Société de la Bourse de Luxembourg S.A.35 Boulevard Joseph IIL-1840 LuxembourgTel.: +352 47 79 36-1www.bourse.lu

Luxembourg House of Financial Technology (LHoFT) 9 Rue du Laboratoire, 1911 LuxembourgTéléphone: +352 28 81 02 01www.lhoft.com

38Banking in Luxembourg

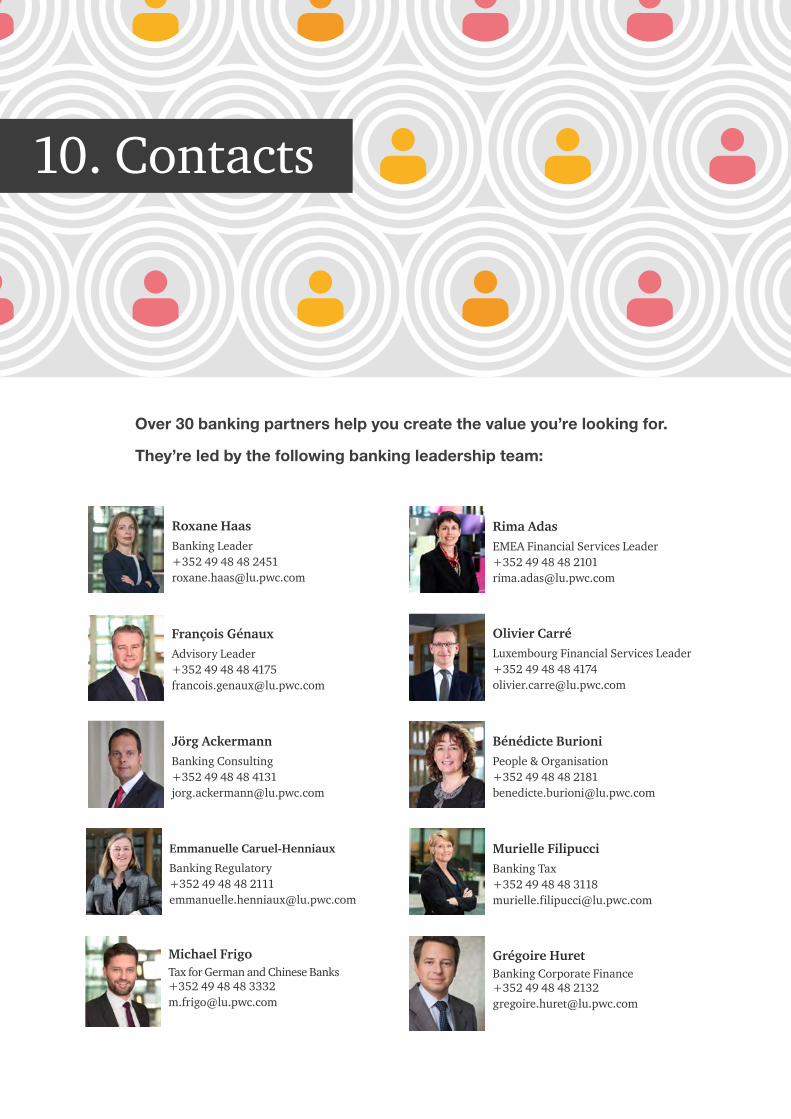

10. Contacts

Over 30 banking partners help you create the value you’re looking for.

They’re led by the following banking leadership team:

Rima AdasEMEA Financial Services Leader+352 49 48 48 [email protected]

François GénauxAdvisory Leader+352 49 48 48 [email protected]

Murielle FilipucciBanking Tax+352 49 48 48 [email protected]

Grégoire HuretBanking Corporate Finance+352 49 48 48 [email protected]

Roxane HaasBanking Leader+352 49 48 48 [email protected]

Michael FrigoTax for German and Chinese Banks+352 49 48 48 [email protected]

Emmanuelle Caruel-Henniaux

Banking Regulatory+352 49 48 48 [email protected]

Bénédicte BurioniPeople & Organisation+352 49 48 48 [email protected]

Jörg AckermannBanking Consulting +352 49 48 48 [email protected]

Olivier CarréLuxembourg Financial Services Leader+352 49 48 48 [email protected]

39PwC Luxembourg

Patrice WitzDigital Consulting Services+352 49 48 48 [email protected]

Frédéric Vonner Cybersecurity & privacy +352 49 48 48 [email protected]

Serge Hanssens Smart Identity +352 49 48 48 [email protected]