Bank Secrecy Act Compliance - FFIEC Home Page

24

Federal Deposit Insurance Corporation 550 17th Street NW, Washington, D.C. 20429-9990 Division of Supervision and Consumer Protection Bank Secrecy Act Compliance FIL-120-98 November 16, 1998 TO: CHIEF EXECUTIVE OFFICER SUBJECT: New Currency Transaction Reporting Exemption Rule The Department of the Treasury's Financial Crimes Enforcement Network (FinCEN) has announced a final rule that represents the second part of its effort to significantly reduce the number of times depository institutions must report large currency transactions. The rule further simplifies the way banks can exempt large currency transactions by retail and other businesses from the reporting requirements. The new rule is aimed at exemption of non-public companies, especially smaller businesses, which represent a majority of reports filed. It permits banks to exempt a domestic business that has a routine need for large amounts of currency by simply filing a form stating the business is exempt, as long as the business has been a bank customer for one year. The new rule does not allow for exemption of certain categories of businesses, such as real estate brokers, automobile dealers, and money transmitters, and it does not exempt banks from reporting suspicious activity involving exempted entities. The rule applies to all depository institutions, banks, thrifts, and credit unions, but not to other financial institutions. Banks have until July 1, 2000, to phase in compliance with the simplified procedures, although they may adopt the procedures beginning October 21, 1998. The exemption of the businesses covered by the new rule must be renewed every two years, but a proposed requirement that banks include information about a customer's total currency transactions on the renewal form has been eliminated as unduly burdensome and unnecessary. Banks must simply indicate they have maintained a system of monitoring the transactions in the account for reportable suspicious activity. A copy of the Federal Register notice containing the new rule is attached. If you have any questions, please contact your FDIC Division of Supervision Regional Office. Nicholas J. Ketcha Jr. Director Attachment: Federal Register, Sept. 21, pages 50147-50159. Distribution: FDIC Supervised Banks (Commercial and Savings) NOTE: Paper copies of FDIC financial institution letters may be obtained through the FDIC's Public Information Center, 801 17th Street, NW, Room 100, Washington, DC 20434 (800-276-6003 or 202- 416-6940).

Transcript of Bank Secrecy Act Compliance - FFIEC Home Page

Federal Deposit Insurance Corporation550 17th Street NW, Washington, D.C. 20429-9990 Division of Supervision and Consumer Protection

Bank Secrecy Act Compliance

FIL-120-98November 16, 1998

TO: CHIEF EXECUTIVE OFFICER SUBJECT: New Currency Transaction Reporting Exemption Rule

The Department of the Treasury's Financial Crimes Enforcement Network (FinCEN) has announced a final rule that represents the second part of its effort to significantly reduce the number of times depository institutions must report large currency transactions. The rule further simplifies the way banks can exempt large currency transactions by retail and other businesses from the reporting requirements.

The new rule is aimed at exemption of non-public companies, especially smaller businesses, which represent a majority of reports filed. It permits banks to exempt a domestic business that has a routine need for large amounts of currency by simply filing a form stating the business is exempt, as long as the business has been a bank customer for one year. The new rule does not allow for exemption of certain categories of businesses, such as real estate brokers, automobile dealers, and money transmitters, and it does not exempt banks from reporting suspicious activity involving exempted entities.

The rule applies to all depository institutions, banks, thrifts, and credit unions, but not to other financial institutions. Banks have until July 1, 2000, to phase in compliance with the simplified procedures, although they may adopt the procedures beginning October 21, 1998. The exemption of the businesses covered by the new rule must be renewed every two years, but a proposed requirement that banks include information about a customer's total currency transactions on the renewal form has been eliminated as unduly burdensome and unnecessary. Banks must simply indicate they have maintained a system of monitoring the transactions in the account for reportable suspicious activity.

A copy of the Federal Register notice containing the new rule is attached. If you have any questions, please contact your FDIC Division of Supervision Regional Office.

Nicholas J. Ketcha Jr. Director

Attachment: Federal Register, Sept. 21, pages 50147-50159.

Distribution: FDIC Supervised Banks (Commercial and Savings)

NOTE: Paper copies of FDIC financial institution letters may be obtained through the FDIC's Public Information Center, 801 17th Street, NW, Room 100, Washington, DC 20434 (800-276-6003 or 202-416-6940).

[Federal Register: September 21, 1998 (Volume 63, Number 182)] [Rules and Regulations] [Page 50147-50159] From the Federal Register Online via GPO Access [wais.access.gpo.gov] [DOCID:fr21se98-13] ======================================================================= ----------------------------------------------------------------------- DEPARTMENT OF THE TREASURY Financial Crimes Enforcement Network 31 CFR Part 103 RIN 1506-AA12 Amendment to the Bank Secrecy Act Regulations--Exemptions from the Requirement To Report Transactions in Currency--Phase II AGENCY: Financial Crimes Enforcement Network, Treasury. ACTION: Final rule. ----------------------------------------------------------------------- SUMMARY: This document contains a final rule that further reforms and simplifies the process by which depository institutions may exempt transactions of retail and other businesses from the requirement to report transactions in currency in excess of $10,000, and restates generally, to reflect such changes, the text of the Bank Secrecy Act regulation requiring the reporting by financial institutions of transactions in currency. The final rule, as issued by the Financial Crimes Enforcement Network (``FinCEN''), constitutes a further step in achieving the reduction set by the Money Laundering Suppression Act of 1994 in the number of currency transaction reports required to be filed annually by depository institutions, as part of a continuing program to reduce unnecessary burdens imposed upon financial institutions by the Bank Secrecy Act and increase the cost-effectiveness of the counter- money laundering policies of the Department of the Treasury. DATES: Effective date. October 21, 1998. Applicability date. See Sec. 103.22(d)(11) of the final rule contained in this document. FOR FURTHER INFORMATION CONTACT: Peter Djinis, Associate Director, FinCEN, (703) 905-3930; Charles Klingman, Financial Institutions Policy Specialist, FinCEN, (703) 905-3602; Stephen R. Kroll, Chief Counsel, Cynthia L. Clark, Deputy Chief Counsel, and Albert R. Zarate, Attorney- Advisor, Office of Chief Counsel, FinCEN, (703) 905-3590. SUPPLEMENTARY INFORMATION: [[Page 50148]] I. Statutory Provisions

The Bank Secrecy Act, Titles I and II of Pub. L. 91-508, as amended, codified at 12 U.S.C. 1829b, 12 U.S.C. 1951-1959, and 31 U.S.C. 5311-5330, authorizes the Secretary of the Treasury, inter alia, to issue regulations requiring financial institutions to keep records and file reports that are determined to have a high degree of usefulness in criminal, tax, and regulatory matters, and to implement counter-money laundering programs and compliance procedures. Regulations implementing Title II of the Bank Secrecy Act (codified at 31 U.S.C. 5311-5330) appear at 31 CFR Part 103. The authority of the Secretary to administer Title II of the Bank Secrecy Act has been delegated to the Director of FinCEN. The reporting by financial institutions of transactions in currency in excess of $10,000 has long been a major component of the Department of the Treasury's implementation of the Bank Secrecy Act. The reporting requirement is imposed by 31 CFR 103.22, a rule issued under the broad authority granted to the Secretary of the Treasury by 31 U.S.C. 5313(a) to require reports of domestic coin and currency transactions. Four new provisions (31 U.S.C. 5313(d) through (g)) concerning exemptions from the currency transaction reporting requirement were added to 31 U.S.C. 5313 by the Money Laundering Suppression Act of 1994 (the ``Money Laundering Suppression Act''), Title IV of the Riegle Community Development and Regulatory Improvement Act of 1994, Pub. L. 103-325 (September 23, 1994). 31 U.S.C. 5313(d) provides that the Secretary of the Treasury shall exempt a depository institution from the requirement to report currency transactions with respect to transactions between the depository institution and four categories of entities. The requirements of that subsection are at present reflected in the terms of 31 CFR 103.22(h) (which is amended and redesignated as 31 CFR 103.22(d) by the final rule published in this document). 31 U.S.C. 5313(e) authorizes the Secretary of the Treasury to exempt a depository institution from the requirement to report transactions in currency between a depository institution and a qualified business customer of the institution. Subsection (e)(2) defines a “qualified business customer'' as a business that (A) maintains a transaction account (as defined in section 19(b)(1)(C) of the Act) at the depository institution; (B) frequently engages in transactions with the depository institution which are subject to the reporting requirements of subsection (a); and (C) meets criteria which the Secretary determines are sufficient to ensure that the purposes of this subchapter are carried out without requiring a report with respect to such transactions. Subsection (e)(3) provides that the Secretary of the Treasury shall establish, by regulation, the criteria for granting and maintaining an exemption under subsection (e)(1). Subsection (e)(4)(A) provides that the Secretary of the Treasury shall establish guidelines for depository institutions to follow in selecting customers for an exemption under subsection (e). Under subsection (e)(4)(B), those guidelines may include a description of the type of businesses for which no exemption will be granted under this subsection. Subsection (e)(5) provides that the Secretary of the Treasury shall prescribe regulations requiring each depository institution to (A) review, at least once each year, the qualified business customers of such institution with respect to whom an exemption has been granted under this subsection; and (B) upon the completion of such review, resubmit information about such customers, with such modifications as the institution determines to be appropriate, to the Secretary for the Secretary's approval. Subsection (e)(6) states that during the two-year period beginning on the date of enactment of the Money Laundering Suppression Act, the discretionary exemption rules shall be applied by the

Secretary of the Treasury on the basis of such criteria as the Secretary determines to be appropriate to achieve an orderly implementation of the requirements of this subsection. Subsection (f) places limits on the liability of a depository institution in connection with a transaction that has been exempted from reporting under either 31 U.S.C. 5313 (d) or (e) and provides for the coordination of any exemption with other Bank Secrecy Act provisions, especially those relating to the reporting of suspicious transactions. Finally, subsection (g) defines “depository institution'' for purposes of the new exemption provisions. Section 402(b) of the Money Laundering Suppression Act states simply that in administering the new statutory exemption provisions: The Secretary of the Treasury shall seek to reduce, within a reasonable period of time, the number of reports required to be filed in the aggregate by depository institutions pursuant to section 5313(a) of title 31 * * * by at least 30 percent of the number filed during the year preceding [September 23, 1994,] the date of enactment of [the Money Laundering Suppression Act]. The enactment of 31 U.S.C. 5313 (d) through (g) reflects a Congressional intention to “reform * * * the procedures for exempting transactions between depository institutions and their customers.'' See H.R. Rep. 103-652, 103d Cong., 2d Sess. 186 (August 2, 1994). The administrative exemption procedures at which the statutory changes are directed are found in 31 CFR 103.22(b)(2) and (c) through (f); those procedures have not succeeded in eliminating the reporting of routine currency transactions by businesses. Several reasons have been given for this lack of success. These include the retention by banks of liability for making incorrect exemption determinations, and the complexity of the administrative exemption procedures (which require banks, for example, to assign dollar limits to each exemption based on the amounts of currency projected to be needed for the customary conduct of the exempt customer's lawful business, and which increase the risk of liability to banks that grant exemptions). Finally, advances in technology have made it less costly for some banks simply to report all currency transactions rather than to incur the administrative costs (and risks) of exempting customers and then administering the terms of particular exemptions properly. The problems created by the prior administrative exemption system also include that system's failure to provide the Treasury with information needed for thoughtful administration of the Bank Secrecy Act. Although banks are required to maintain a centralized list of exempt customers and to make that list available upon request, see 31 CFR 103.22(f) and (g), there is no way short of a bank-by-bank request for lists (with the time and cost such a request would entail both for banks and government) for Treasury to learn the extent to which routine transactions are effectively screened out of the system or (for that matter) the extent to which exemptions have been granted in situations in which they are not justified. In crafting the 1994 statutory provisions relating to mandatory and discretionary exemptions, Congress sought to alter the burden of liability and uncertainty that the administrative exemption system created. The statutory provisions embraced several categories of transactions that were either already partially exempt or plainly eligible for exemption under the prior administrative exemption system.1 --------------------------------------------------------------------------- \1\ As noted below, transactions in currency between domestic banks were already exempt from reporting, see 31 CFR 103.22(b)(1)(ii), and “[d]eposits or withdrawals, exchanges of currency or other payments and transfers by local or state governments, or the United States or any of its agencies or instrumentalities'' were one of the categories of transactions specifically described as eligible for exemption by banks. See 31 CFR 103.22(b)(2)(iii).

--------------------------------------------------------------------------- II. Phase I--Final Rule On September 8, 1997, a final rule revising paragraph (h) of 31 CFR 103.22 was published in the Federal Register. See 62 FR 47141. The final rule modified (and as modified, superseded) an interim rule on exemptions (collectively, “Phase I'') that FinCEN published with request for comments in April 1996. See 61 FR 18204. The Phase I final rule exempted from the requirement to report transactions in currency in excess of $10,000, transactions between banks 2 and (i) other banks operating in the United States; (ii) government departments and agencies, and entities that otherwise exercise governmental authority; (iii) entities listed on certain national stock exchanges; and (iv) certain subsidiaries of those listed entities. --------------------------------------------------------------------------- \2\ The Phase I interim and final rules, as well as the notice of proposed rulemaking to which the final rule contained in this document relates, used the term “bank'' to define the class of financial institutions to which the rules respectively applied. As defined in 31 CFR 103.11(c), that term includes both commercial banks and other classes of depository institutions at which the language of 31 U.S.C. 5313 is directed. The final rule contained in this document continues to use the term “bank,'' rather than depository institution. --------------------------------------------------------------------------- As FinCEN explained when the Phase I interim rule was published, the transactions in currency of bank customers in those categories were either required to be exempt from reporting by statute, were already effectively exempt from reporting under the terms of 31 CFR Part 103, or, in the case of listed entities and certain of their subsidiaries, involved enterprises whose routine currency transaction reports are of little or no value to law enforcement officials. Recognition of exemption under the Phase I interim and final rules required simply the filing of a single document identifying the exempt person and the depository institution that exempts it. Transactions in currency, like other transactions, remained subject to the requirement that banks report suspicious transactions. III. Phase II--Notice of Proposed Rulemaking On the same day the Phase I final rule was published in the Federal Register, FinCEN published a notice of proposed rulemaking (the “Notice'') to further reform and simplify the process by which banks may exempt, from the requirement to report transactions in currency in excess of $10,000, transactions involving certain of their customers. See 62 FR 47156. As FinCEN stated in the Notice, the objective of the second stage reform (“Phase II'') was to provide, to the extent possible, a blanket relief, similar to that contained in Phase I, for those categories of business enterprise that could not easily be described in a single phrase and that were not subject to the sorts of regulatory and marketplace oversight that shape the environment of publicly-held companies. To accomplish that goal, while still providing federal authorities with the tools to monitor and prevent abuse, FinCEN proposed a pared-down exemption system. In the Notice, FinCEN specifically proposed the following changes: (i) The addition of two new classes of exempt persons, non-listed businesses and payroll customers; (ii) the addition of special requirements governing the exemption of non-listed businesses and payroll customers, namely, an initial projection of such exempt person's annual currency needs and an annual filing listing the aggregate currency deposits and withdrawals of such exempt person during the preceding year; (iii) the addition of five new operating rules governing the exemption of non-listed businesses and payroll customers; (iv) the deletion of paragraphs (b) through (g) of present section 103.22 (the “prior'' administrative exemption system); (v) the redesignation of paragraph (h) (reflecting the terms of the Phase I final rule) of section 103.22 as paragraph (d) of that section; and (vi) the addition of certain conforming changes to the redesignated paragraph (d).

On November 28, 1997, FinCEN published a notice (the “November Extension'') in the Federal Register extending the comment period for the Notice and soliciting additional comments on certain matters relating to the Notice. See 62 FR 63298. The decision to extend the comment period and the request for additional comments resulted from discussions held at an open meeting to discuss the Notice on November 7, 1997.3 --------------------------------------------------------------------------- \3\ FinCEN announced the public meeting in the Federal Register on October 31, 1997. See 62 FR 58909. --------------------------------------------------------------------------- In the November Extension, FinCEN stated that, in light of the comments made at the open meeting, it did not believe additional comments concerning the proposed estimation and aggregate currency reporting provisions were necessary. FinCEN did, however, indicate that it was important that alternatives to those proposals be brought forward by interested parties, and it specifically sought comments on an alternative described in the November Extension. That alternative would have required a bank, when designating a non-listed business or a payroll customer as an exempt person, to (i) include on its initial designation form a statement of the manner in which it applies its “know-your-customer'' standards to customers whose currency transactions it exempts from the currency transaction report requirements, and (ii) certify in an annual renewal of exempt status filing that during the preceding year there were no transactions involving any accounts of the person at the bank that would have required the filing of a suspicious activity report. FinCEN also sought comments on the impact of changing the word “shall'' to “may'' in proposed 103.22(d)(5)(v), to provide a bank with the option, but not the necessity, of exempting a customer on a bank-wide basis. Lastly, FinCEN repeated its request, made in the Notice, for comments relating to the treatment for exemption purposes of currency deposits that commingle funds derived from eligible business activities with funds derived from ineligible business activities. IV. Summary of Comments and Revisions A. Comments on the Notice--Overview FinCEN received 70 written responses to the Notice. Of these, 51 were submitted by banks or bank holding companies, 8 by financial institution trade associations, 4 by credit unions, 2 by law firms, 2 by private individuals, and 1 by a compliance software designer. Comments on the Notice focused primarily on the following proposed provisions: (i) The projection and annual aggregate currency reporting requirements (including possible alternatives); (ii) the twelve-month waiting period governing the designation of non-listed businesses and payroll customers as exempt persons; (iii) the operating rule making a sole proprietorship eligible for exemption only to the extent of its business (as opposed to personal) transactions; (iv) the operating rule making certain businesses ineligible for designation as exempt persons to the extent they engage in one or more listed ineligible business activities; and (v) the limitation on exemption with respect to transactions carried out by an exempt person as an agent for a third party. Regarding the latter three provisions, commenters expressed particular concern over the application of those provisions to situations where their customers commingle funds derived from personal transactions or ineligible business activities with eligible business activities. After full and careful consideration of all of the comments, 31 CFR 103.22 is revised to read as stated in the final rule. B. Final Rule

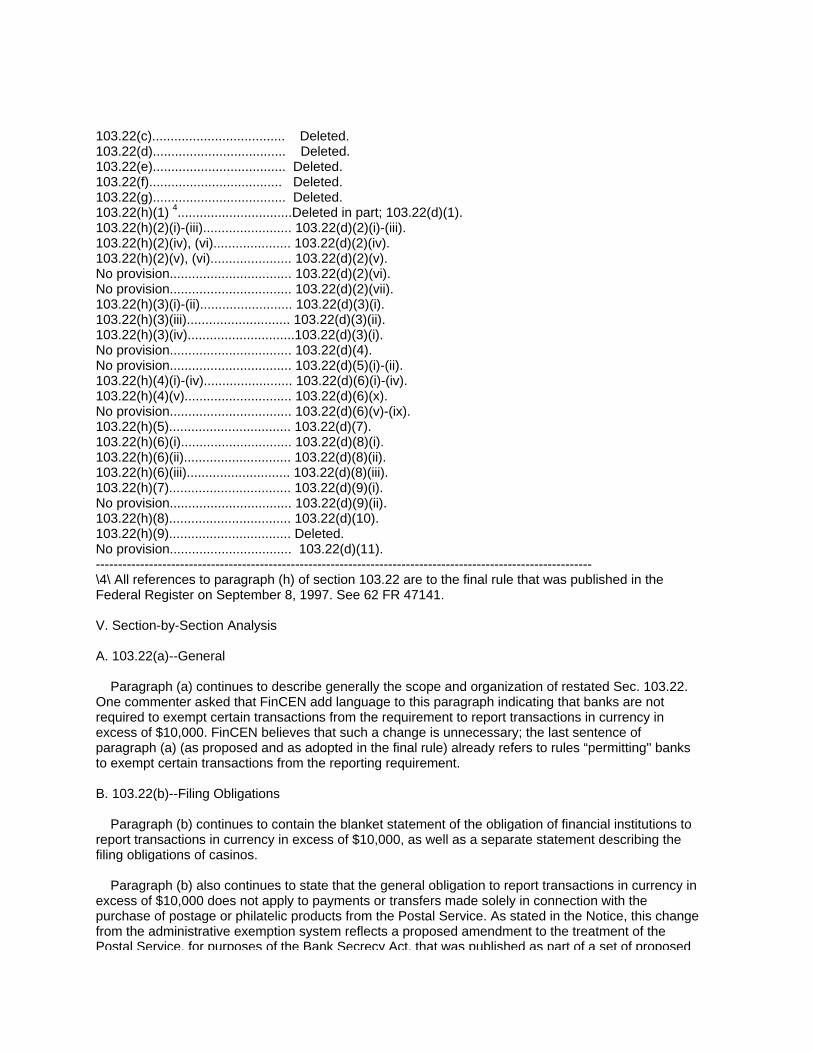

The format of the final rule is generally consistent with the Notice. The terms of the final rule, however, differ from the terms of the Notice in the following significant respects: Banks are not required to initially estimate and then report annually the aggregate currency deposits and withdrawals of any customer that is designated as a non-listed business or payroll customer; Banks are required to renew exemptions for non-listed business and payroll customers every two years rather than every year; Banks must maintain a system of monitoring the transactions in currency of each exempt customer for any and all reportable suspicious activity; As part of the required biennial renewal, banks must certify that they have complied with the requirement to maintain a system of monitoring for reportable suspicious activity; Banks may, but need not, treat all eligible accounts of a person at a single institution as exempt; Banks are not required to segregate funds derived from non-business activities when exempting a transaction in currency of a sole proprietorship; and Banks may treat a business that engages in multiple activities as a non-listed business so long as that business does not engage primarily in one or more of those activities described in paragraph (d)(6)(viii). The changes adopted in the final rule are intended to improve, clarify, and refine the rule's provisions in light of the objectives for implementation of 31 U.S.C. 5313(d)-(g) that FinCEN outlined when the Phase I interim rule was published. Those objectives are reducing the burden of currency transaction reporting, requiring reporting only of information that is of value to law enforcement and regulatory authorities, and, perhaps most importantly, creating an exemption system that is cost-effective and that works. See 61 FR 18205. Eliminating the administrative exemption system in section 103.22 requires the deletion of the bulk of that section, paragraphs (b)-(g). Because that is so, and because the structure and many of the rules of section 103.22(h) also apply to the proposed reformed exemption system for other customers, the final rule completely restates section 103.22 so that its terms may be presented clearly. For convenience, the redistribution of the provisions of prior section 103.22 may be summarized as follows: Distribution Table ---------------------------------------------------------------------------------------------------------------- Prior 103.22 New 103.22 ---------------------------------------------------------------------------------------------------------------- No provision................................. 103.22(a). 103.22(a)(1): Sentences 1-2............................Deleted in part; 103.22(b)(1). Sentences 3-4............................103.22(c)(2). 103.22(a)(2)(i)-(ii)......................... 103.22(b)(2)(i)-(ii). 103.22(a)(2)(iii)............................ 103.22(c)(3). 103.22(a)(3)................................. Deleted in part; 103.22(b)(1), 103.22(c)(2). 103.22(a)(4)................................. 103.22(c)(1). 103.22(b).................................... Deleted, except 103.22(b)(1)(iii) and 103.22(b)(2)(iv). 103.22(b)(1)(iii)............................ 103.22(d)(1). 103.22(b)(2)(iv)............................. 103.22(d)(2)(vii).

103.22(c).................................... Deleted. 103.22(d).................................... Deleted. 103.22(e).................................... Deleted. 103.22(f).................................... Deleted. 103.22(g).................................... Deleted. 103.22(h)(1) 4...............................Deleted in part; 103.22(d)(1). 103.22(h)(2)(i)-(iii)........................ 103.22(d)(2)(i)-(iii). 103.22(h)(2)(iv), (vi)..................... 103.22(d)(2)(iv). 103.22(h)(2)(v), (vi)...................... 103.22(d)(2)(v). No provision................................. 103.22(d)(2)(vi). No provision................................. 103.22(d)(2)(vii). 103.22(h)(3)(i)-(ii)......................... 103.22(d)(3)(i). 103.22(h)(3)(iii)............................ 103.22(d)(3)(ii). 103.22(h)(3)(iv).............................103.22(d)(3)(i). No provision................................. 103.22(d)(4). No provision................................. 103.22(d)(5)(i)-(ii). 103.22(h)(4)(i)-(iv)........................ 103.22(d)(6)(i)-(iv). 103.22(h)(4)(v)............................. 103.22(d)(6)(x). No provision................................. 103.22(d)(6)(v)-(ix). 103.22(h)(5)................................. 103.22(d)(7). 103.22(h)(6)(i).............................. 103.22(d)(8)(i). 103.22(h)(6)(ii)............................. 103.22(d)(8)(ii). 103.22(h)(6)(iii)............................ 103.22(d)(8)(iii). 103.22(h)(7)................................. 103.22(d)(9)(i). No provision................................. 103.22(d)(9)(ii). 103.22(h)(8)................................. 103.22(d)(10). 103.22(h)(9)................................. Deleted. No provision................................. 103.22(d)(11). ---------------------------------------------------------------------------------------------------------------- \4\ All references to paragraph (h) of section 103.22 are to the final rule that was published in the Federal Register on September 8, 1997. See 62 FR 47141. V. Section-by-Section Analysis A. 103.22(a)--General Paragraph (a) continues to describe generally the scope and organization of restated Sec. 103.22. One commenter asked that FinCEN add language to this paragraph indicating that banks are not required to exempt certain transactions from the requirement to report transactions in currency in excess of $10,000. FinCEN believes that such a change is unnecessary; the last sentence of paragraph (a) (as proposed and as adopted in the final rule) already refers to rules “permitting'' banks to exempt certain transactions from the reporting requirement. B. 103.22(b)--Filing Obligations Paragraph (b) continues to contain the blanket statement of the obligation of financial institutions to report transactions in currency in excess of $10,000, as well as a separate statement describing the filing obligations of casinos. Paragraph (b) also continues to state that the general obligation to report transactions in currency in excess of $10,000 does not apply to payments or transfers made solely in connection with the purchase of postage or philatelic products from the Postal Service. As stated in the Notice, this change from the administrative exemption system reflects a proposed amendment to the treatment of the Postal Service, for purposes of the Bank Secrecy Act, that was published as part of a set of proposed

rules relating to money services businesses (“MSBs'') on May 21, 1997. See 62 FR 27890. FinCEN received no comment on this change. C. 103.22(c)--Aggregation Paragraph (c) continues to restate the reporting rules applicable to multiple branches of financial institutions and multiple transactions of their customers. Those rules reflect, with one exception relating to recordkeeping facilities, the terms of prior paragraphs (a)(1) and (a)(4) of section 103.22. As an analogue to a change (discussed below) that permits affiliated banks to make a single designation of each exempt person, the Notice proposed a change clarifying that for purposes of the currency transaction reporting requirements, a financial institution includes not only all domestic branch offices, but also any recordkeeping facility, wherever located, that contains records relating to the transactions of the institution's domestic branch offices. The only comment that FinCEN received concerning recordkeeping facilities stated that the change would create an excessive burden on large banks because such banks typically have central recordkeeping facilities. Given the utility of treating a recordkeeping facility as a financial institution, particularly in cases in which affiliated banks make a single designation of exempt person, and that the commenter did not explain how central recordkeeping could lead to an excessive reporting burden on banks, the proposal regarding recordkeeping facilities is adopted in the final rule. D. 103.22(d)--Transactions of Exempt Persons 1. General Paragraph (d)(1) continues to state generally that, subject to the limitation on exemption set forth in paragraph (d)(7), no bank is required to file a currency transaction report otherwise required by paragraph (b) with respect to any transaction in currency between an exempt person and such bank.5 This paragraph also adopts the language set forth in the Notice that states that a non-bank financial institution need not file a currency transaction report with respect to a transaction in currency between the institution and a commercial bank. That provision is reflected in paragraph (b)(1)(iii) of prior section 103.22. --------------------------------------------------------------------------- \5\ FinCEN anticipates that Internal Revenue Service Form 4789 (the form currently used to file a currency transaction report) may be revised at some point to require that a bank check a box when it files a currency transaction report with respect to a transaction conducted by an exempt person. The purpose of such a requirement would be to provide FinCEN with a more accurate estimate of the number of currency transactions reports required to be filed under the revised exemption system. --------------------------------------------------------------------------- At least one commenter suggested that FinCEN clarify, in light of, inter alia, the Right to Financial Privacy Act, 12 USC 3413 et seq., that a bank must continue to file currency transaction reports for particular customers otherwise eligible for treatment as exempt persons if it elects not to use the reformed exemption system for those customers. The retention in paragraph (d)(1) of the phrase “otherwise required by paragraph (b)'' is meant to convey that very point--namely, that a bank is required to file a currency transaction report regarding a transaction in currency in excess of $10,000 unless the bank follows the procedures set forth in paragraph (d) for designating the customer involved as an exempt person so that transactions by that customer are exempt from the currency transaction reporting requirement. 2. Exempt Person The final rule adopts the two classes of exempt person introduced in the Notice--namely, non-listed businesses and payroll customers. In addition, the final rule restates, with two minor technical changes, the existing classes of exempt person (set forth in prior section 103.22(h)(2)). First, the phrase “or analogous equity interest'' has been added after the term ``common stock'' in paragraph

(d)(2)(v) to make clear that any subsidiary of any listed entity may be treated as an exempt person, regardless of whether the subsidiary has adopted the corporate form of business. Thus, any subsidiary of a listed entity may be treated as an exempt person so long as 51 per cent of the subsidiary's equity interest is owned by the listed entity. Second, the terms of prior paragraph (h)(2)(vi), stating that in the case of non-bank financial institutions, listed entities and their subsidiaries may be treated as exempt persons only to the extent of their domestic operations, have been incorporated into paragraphs (d)(2)(iv) and (v). Paragraphs (d)(2)(vi) and (vii) continue to require that any business must have been a bank customer for twelve months before it is eligible for exemption as a non-listed business or a payroll customer. Several commenters argued that this twelve-month period was excessive (particularly compared to the two-month minimum period that has evolved administratively under prior paragraphs (b)(2) and (d) of section 103.22) and would discourage customers from changing banks. As stated in the Notice, the ten-month difference in time periods is justified by the elimination of virtually all of the other requirements of the prior administrative exemption system. Under the reformed system, a bank will be able to exempt the transactions in currency of a non-listed business or payroll customer simply by the one-time filing of a form that identifies the exempt person and the exempting bank, and by renewing that initial designation every two years. Thus, banks no longer will be confined to exempting only those transactions falling within certain “permitted'' ranges. In addition, banks will no longer be required to prepare and submit signed exempt statements, or to maintain mandatory exemption lists. Given the removal of these time-consuming procedures, coupled with the need to keep some “tension'' in the liberalized exemption system so that it does not become a vehicle for more efficient money laundering, FinCEN believes that a ten-month difference is warranted. The final rule also adopts in paragraph (d)(2)(vi), with one minor change, the definition of a non-listed business set forth in the Notice. The definition, based in large part on 31 U.S.C. 5313(e)(2), confines permissible exemptions to bank customers located in the United States that have transaction account relationships with the exempting bank involving the recurring use of currency in amounts exceeding $10,000. The term “United States'' has been added to the clause after the comma in paragraph (d)(2)(vi)(C), to make clear that a non-listed business must be incorporated or organized under the laws of the United States or a State, or must be registered as and eligible to do business within the United States or a State. The term “United States'' is specifically defined in 31 CFR 103.11(nn) to include, among other things, the District of Columbia and the Territories and Insular Possessions of the United States. The final rule also continues to track the structure described above in the context of defining a payroll customer. Thus, paragraph (d)(2)(vii) requires that any person must have been a bank customer for at least twelve months before it is eligible for exemption as a payroll customer, and limits such designation to bank customers who regularly withdraw more than $10,000 to pay their United States employees. For consistency with the preceding paragraph, and in response to at least one comment that sought clarification of the term “U.S. resident'' in the Notice, paragraph (d)(2)(vii) has been changed to state that an exemptible payroll customer must be incorporated or organized under the laws of the United States or a State, or must be registered as and eligible to do business within the United States or a State. 3. Initial Designation of Exempt Persons Paragraph (d)(3) continues to state generally that, when initially designating one of its customers as an exempt person, a bank must make a one-time filing (using the form now used to file a currency transaction report, until such time as FinCEN issues a form specifically for this purpose) that identifies the exempt person and the exempting bank. With respect to its bank customers who are themselves banks, the exempting bank will have the option in the future of filing its current list of bank customers in such a format and manner as FinCEN may specify.

The Notice included a provision that would have required a bank, when designating a non-listed

business or payroll customer as an exempt person, to include a projection of the exempt person's annual currency deposits and withdrawals. Most commenters objected to this proposal. According to these commenters, any projections of currency activity would amount to “little more than guesswork'' because banks do not have in place the systems capable of tracking currency activity in this manner. A few commenters also expressed apprehension over a bank incurring liability if it should significantly underestimate the currency activity of one of its customers. Several commenters also expressed reservations about the alternative that FinCEN outlined in the November Extension. That alternative would have required a bank to describe the manner in which it applies its “know-your-customer'' standards to the tracking of currency deposits of its commercial customers. At least one commenter noted that this requirement would be superfluous, given that a bank's exemption process and currency tracking system is reviewed in detail during its BSA examination and that any application of a bank's know-your-customer policy will be monitored by bank examiners in any event. Based on these comments, and mindful of the goal to create a reformed exemption system that is cost-effective and efficient, the final rule includes neither a requirement that a bank include in its initial designation a projection of its exempt customers' currency activity, nor a requirement that the bank describe in that designation the manner in which the bank applies its “know-your-customer'' policies to exempt customers. 4. Annual Review Paragraph (d)(4) makes explicit the requirement that a bank verify, at least once each year, the status of all those entities it has designated as exempt persons. This annual review requirement was implicit in the terms of proposed paragraph (d)(7)(iii), which would have required that, absent specific knowledge of any information that would be grounds for revocation, a bank verify the status of those entities it has designated as exempt persons only once each year. FinCEN notes that this requirement to annually review customers designated as exempt persons is reflected both in the terms of 31 U.S.C. 5313(e)(5) and in the administrative practice surrounding the superseded exemption system. Paragraph (d)(4) also states that a bank must review at least annually the application to each account of a non-listed business or payroll customer of the monitoring system required to be maintained by paragraph (d)(9)(ii). This language has been added to help ensure that the reformed system is not exploited by criminals as a more efficient vehicle for money laundering. 5. Biennial Filing With Respect to Certain Exempt Persons The Notice would have required banks, in the case of non-listed businesses and payroll customers, to file annual updates containing a statement of the exempt person's annual currency deposits and withdrawals through all transaction accounts for the preceding year. Many commenters argued adamantly against an annual aggregate currency reporting requirement. Those commenters stressed that banks do not have the automated systems in place to comply with such a requirement, and that the cost of implementing such systems would be unreasonably high. Many commenters also maintained that, rather than comply with an annual aggregate currency reporting requirement, banks would choose to continue to file currency transaction reports on transactions involving exempt persons. Several commenters also voiced their dissatisfaction with the alternative that FinCEN outlined in the November Extension. That alternative would have required a bank to certify that, during the preceding year, there was no transaction involving any accounts of the exempt person at the bank that would have required the bank to file a suspicious transaction report with respect to that person under 31 CFR 103.21. At least one commenter expressed the fear that this certification would be viewed as a warranty that no suspicious activity occurred, and that banks would be unwilling to risk civil or criminal liability by making such a statement.

In response to these comments, FinCEN has deleted the provision requiring annual statements of the aggregate currency deposits and withdrawals of non-listed businesses and payroll customers. Instead of requiring annual currency statements, the final rule requires simply that banks maintain a system of monitoring the transactions in currency of non-listed businesses and payroll customers for suspicious activity, see paragraph (d)(9)(ii), and renew the exempt status of those customers every two years. See paragraph (d)(5)(ii). As part of that biennial renewal, banks must certify that their system of monitoring the transactions in currency of such exempt persons for suspicious activity has been applied as necessary, but at least annually, to the account of the exempt person to whom the biennial renewal applies. See id. The filing required by paragraph (d)(5) need only be made once every two years. While the terms of 31 U.S.C. 5313(e)(5) contemplate an annual review, the statute does not explicitly set a time for the filing of updated information garnered as a result of that review. In light of at least a few comments suggesting that banks be required to file updated information less frequently than once a year, the final rule requires banks to renew exemption status every two years. The date on which renewals must be filed also has changed from the Notice. At least one commenter suggested that the proposed date of February 28 be changed because it coincides with the time period in which banks must make other regulatory filings. The final rule therefore adopts the date of March 15 as the date on which biennial renewals must be filed. Consistent with the Notice, paragraph (d)(5) states that biennial renewals also must include information about any change in control of the exempt person of which the bank knows or should know based on its records. At least one commenter contended that the “should know'' standard essentially requires a bank to review constantly the information it possesses on each of its exempt customers, and therefore would unreasonably burden large banks where there are potentially many points of contact between the customer and the bank. That the “should know'' standard requires a bank to exercise some degree of due diligence when renewing the exempt status of one of its customers is wholly intentional. This concept of due diligence is entirely consistent with the language set forth in the Phase I final rule, which states that a bank must, when applying the terms of the reformed exemption system, take such steps that a reasonable and prudent bank would take and document to protect itself from loan or other fraud or loss based on misidentification of a person's status. Indeed, as one commenter noted, “no institution would exempt a customer, either under the new or old system, without first engaging in extensive due diligence.'' Thus, the final rule requires biennial renewals to include information concerning a change in control of which a bank knows or should know based on its records. 6. Operating Rules The final rule adopts, with a few modifications, the five operating rules introduced in the Notice relating to the Phase II rules. a. Paragraph (d)(6)(v) states that a bank may aggregate all customer accounts to apply the exemption provisions to that customer. In response to several comments, the word “shall'' in the Notice has been changed to “may,'' to provide a bank with the option of exempting a customer on a bank-wide basis and counting all accounts to determine, for example, whether a customer's cash withdrawals or deposits exceed $10,000. To ensure consistency in the treatment of their exempt customers by banks, a sentence has been added in the final rule that makes clear that if a bank elects to treat all transaction accounts of a customer as a single account, the bank must continue to treat the accounts as a single account for Bank Secrecy Act purposes thereafter.

b. Paragraph (d)(6)(vi) permits affiliated banks to make a single designation of an exempt person,

that will apply to all accounts of the person at all banks within the affiliated group. The language in the Notice pertaining to projected and annual currency transaction activity has been deleted. c. Paragraph (d)(6)(vii) states that sole proprietorships may be treated as either non-listed businesses or payroll customers if they otherwise meet the requirements for treatment as such exempt persons. The Notice included provisions that would have made certain accounts of a sole proprietorship ineligible for exemption to the extent they are “personal'' accounts, or otherwise commingle personal and business funds. Several commenters argued against these limitations, stating that it would be difficult, if not impossible, for banks to distinguish between personal and business-related transactions in currency. Again, mindful of the goal to create a reformed exemption system that works, and given that banks are under an obligation to report suspicious activity concerning the transactions in currency of their exempt customers, including sole proprietorships, the final rule does not include a provision that would require banks to track commingled funds. However, it should be noted that only “commercial accounts'' are eligible; nothing in the final rule permits the exemption of a sole proprietor's personal bank accounts. d. Paragraph (d)(6)(viii) lists those businesses that may not be exempted under the reformed exemption system as non-listed companies (although they may qualify for exemption under the more limited payroll customer definition). The Notice sought comments on the treatment of businesses with multiple activities of which one is an activity for which an exemption is barred. In addition, both the Notice and the November Extension solicited comments on the advisability of requiring multiple-activity businesses to segregate funds derived from eligible business activity from those derived from ineligible business activity, in order to be eligible for treatment as an exempt person. Several commenters suggested that a multiple-activity business should be eligible for treatment as an exempt person because a contrary rule would make many of its customers ineligible for treatment as exempt persons, in particular grocery stores. According to those commenters, such multiple-activity businesses, as a matter of common practice, commingle funds derived from different activities, and would not pay the cost of maintaining multiple accounts in order to avail themselves of the advantages of the reformed exemption system. In light of these comments, the final rule simply states that a business that engages in multiple business activities may be treated as a non-listed business so long as that business does not engage primarily in one or more of those activities described in paragraph (d)(6)(viii)--i.e., no more than 50% of its gross revenues is derived from ineligible business activity. FinCEN believes that this change will benefit banks by providing them with a bright-line test (the same one, FinCEN notes, that has evolved around the administrative practice surrounding the prior exemption system) for determining whether to treat multi-activity businesses as exemptible non-listed businesses. To further facilitate the use of the reformed exemption system, the final rule does not include a provision that would require a multiple-activity business to segregate commingled funds to be eligible for treatment as an exempt person. e. Paragraph (d)(6)(ix) defines a transaction account for purposes of proposed paragraph (d) as any account described in section 19(b)(1)(C) of the Act, 12 U.S.C. 461(b)(1)(C). As stated in the Notice, this definition does not include any other accounts not described in 12 U.S.C. 461(b)(1)(C), such as money market accounts. Thus, the definition of a transaction account in the proposed rule is narrower than the definition of the same term that is set forth at 31 CFR 103.11(hh). Paragraph (d)(6)(ix) also provides, consistent with the Notice, that a person may be exempt either as a non-listed business or as a payroll customer only to the extent of such person's transaction accounts. FinCEN received several comments requesting that the definition of a transaction account be broadened. Because the terms of 31 U.S.C. 5313(e)(2)(A) specifically define a transaction account by reference to 12 U.S.C. 461(b)(1)(C), the final rule adopts the definition of a transaction account set

forth in the Notice. Should the above definition of a transaction account prove too difficult to apply, FinCEN will entertain requests for administrative relief from the application of that definition. 7. Limitation on Exemption Paragraph (d)(7) carries over the terms of prior paragraph 103.22(h)(5) and states that the exemption from reporting contained in paragraph (d)(1) does not apply to a transaction carried out by an exempt person as an agent of another person who is the beneficial owner of the funds that are the subject of a transaction in currency.6 With regard to exempt customers acting as agents for third parties, a few commenters noted that it was common practice for those customers to commingle the funds derived from their agent activities with those funds derived from their other business activities. Because of the difficulty in distinguishing between the two kinds of funds, FinCEN was asked not to adopt a rule that would require customers to segregate funds derived from agent activities to be eligible for treatment as an exempt person. --------------------------------------------------------------------------- \6\ FinCEN indicated that it would consider additional comments on this subject when it issued the Phase I final rule. See 62 FR 47141, 47146. --------------------------------------------------------------------------- Given these comments, the final rule does not require that an exempt person segregate agent-derived funds to be eligible for treatment as an exempt person. However, the language of paragraph (d)(7)(relating to transactions carried out by an exempt person as an agent for another), has not been deleted. The exemption procedures will apply only to transactions conducted for the account of the exempt person, not for the account of a third party who is not otherwise an exempt person. See 31 U.S.C. 5313(f)(1)(B) and paragraph (d)(8)(ii) of the final rule. It should be noted that a bank customer that commingles funds from, e.g., the sale of money orders or of goods sold on consignment, with its normal business receipts, for deposit purposes into its own general account engages in a transaction that is exempt or not depending upon the customer's own status, regardless of the fact that a portion of the funds are subject to a potential equitable or other lien by a third party (the issuer of the money orders or the consignor of the goods) if the customer does not pay an amount equal to the money order or consignment sales proceeds over to the issuer or consignor. If instead, the business selling the money orders or consigned goods deposits the funds directly into an account opened by the money order issuer or the goods' consignor, the eligibility of the transaction for exemption would depend upon the status of the issuer or consignor. 8. Limitation on Liability Paragraph (d)(8)(i) generally states, consistent with the Notice, that once a bank has complied with the requirements of paragraph (d), it is protected from any penalty for failure to file a currency transaction report concerning a transaction in currency by an exempt person. Paragraph (d)(8)(ii) states that subject to the specific terms of paragraph (d), and absent any specific knowledge of any information indicating that a customer no longer meets the requirements of an exempt person, a bank satisfies the requirements of paragraph (d) if it continues to treat that customer as an exempt person until the date of that customer's next periodic review. This language is meant to harmonize the requirement, contained in paragraph (d)(4), that banks review the status of their exempt customers at least once a year, with the provisions relating to the revocation of a customer's exempt status that are set forth at paragraph (d)(10). 9. Obligations to File Suspicious Activity Reports and Maintain a System to Monitor Transactions in Currency Paragraph 103.22(d)(9)(i) states that the reformed exemption system does not create any exemption from, or have any negative effect at all on, the requirement that banks file suspicious

transaction reports with respect to transactions that satisfy the requirements of the rules of FinCEN (31 CFR 103.21), the federal bank supervisory agencies, or both, relating to suspicious activity reporting. See 12 CFR 21.11 (Office of the Comptroller of the Currency); 12 CFR 208.20 (Federal Reserve System); 12 CFR 353.3 (Federal Deposit Insurance Corporation); 12 CFR 563.180 (Office of Thrift Supervision); 12 CFR 748.1 (National Credit Union Administration). Indeed, as pointed out in the notice of proposed rulemaking, the operation of a coordinated and uniform suspicious transaction reporting system is a basis for the revision and simplification of the exemption rules contained in this final rule. In the context of the revised CTR exemption system, the indicia of suspicious activity can include both specific transactions and overall transaction volume substantially inconsistent with the sort in which the particular customer normally would be expected to engage. Thus, as stated in the text of the rule itself, anomalous transaction trends or patterns (such as a sharp increase from one year to the next in the gross total of currency transactions made by an exempt person) may trigger the obligations of a bank under section 103.21. Paragraph (d)(9)(ii) has been added to make explicit that the continuing obligation to file suspicious activity reports (where appropriate) necessarily requires a bank to establish and maintain a monitoring system for non-listed business and payroll customers that is reasonably designed to detect those transactions in currency that would require a bank to file a suspicious transaction report with respect to an exempt person.7 FinCEN purposely has not attempted to describe the exact contours of an acceptable monitoring system. Because the situation of each bank and each customer are different, FinCEN believes that mandating a uniform monitoring system would be ill-advised. From FinCEN's perspective, a monitoring system meets the requirements of paragraph (d)(9)(ii) if it is reasonably designed to detect, for each exempt account, those transactions in currency that would require a bank to file a suspicious transaction report. --------------------------------------------------------------------------- \7\ The Bank Secrecy Act provides Treasury with the authority to condition the grant of discretionary exemptions. See 31 U.S.C. 5313(e). --------------------------------------------------------------------------- The adoption of the monitoring system requirement is intended to advance the objectives of creating an exemption system that is simple and as cost-effective as possible, while still keeping some tension in the liberalized system. FinCEN believes that an increased emphasis on suspicious activity reporting with respect to transactions in currency of exempt persons should provide that needed tension. FinCEN further notes that maintaining a monitoring system reasonably designed to detect suspicious activity, and certifying compliance with that requirement, should not pose additional burdens on banks, because they remain subject in any event to the requirement to file reports of suspicious activity with respect to any transaction they exempt from the requirement to file currency transaction reports under the reformed exemption system. As explained above, the statement of the requirement to maintain a specific currency transaction monitoring program for accounts of exempt persons is limited to accounts of non-listed businesses and payroll customers, the classes of exempt persons with respect to which annual review requirements are specifically imposed by the final rule. However, banks are required to report suspicious transactions, including transactions in currency, in the accounts of all exempt persons (as in all other accounts) and paragraph (d)(9)(ii)'s more detailed specification does not by implication lessen the suspicious transaction reporting obligations or procedures of banks generally under paragraph (d)(9)(i) and 31 CFR 103.21. 10. Revocation Paragraph (d)(10) states that the status of an exempt person automatically ceases, without any action by the Department of the Treasury, when an entity ceases to be listed on the applicable stock exchange or a subsidiary of a listed entity ceases to have at least 51 per cent of its common stock or analogous equity interest owned by a listed entity. The phrase “analogous equity interest'' has been added to reflect the change made to the definition of an exempt subsidiary set forth in paragraph (d)(2)(v).

11. Transitional Rule Paragraph 103.22(d)(11) states the transitional rules governing the use of the reformed exemption system. A few commenters requested that FinCEN provide ample time for banks to move from the prior administrative exemption system to the reformed system, particularly given that banks will need some time to address year 2000 computer issues. In light of these comments, the transition period stated in the Notice--that, in effect, provides banks until the end of the calendar year 1999 to make the transition to the reformed system--has been extended in the final rule to July 1, 2000. Provided that banks comply with the transition period set forth in the final rule, they may treat a customer as exempt under either the prior administrative exemption rules or the reformed exemption procedures set forth in paragraph 103.22(d) (so long as they do so consistently) during the transitional period. V. Executive Order 12866 The Department of the Treasury has determined that this final rule is not a significant regulatory action under Executive Order 12866. VI. Unfunded Mandates Act of 1995 Statement Section 202 of the Unfunded Mandates Reform Act of 1995 (“Unfunded Mandates Act''), Pub. L. 104-4 (March 22, 1995), requires that an agency prepare a budgetary impact statement before promulgating a rule that includes a federal mandate that may result in expenditure by state, local and tribal governments, in the aggregate, or by the private sector, of $100 million or more in any one year. If a budgetary impact statement is required, section 202 of the Unfunded Mandates Act also requires an agency to identify and consider a reasonable number of regulatory alternatives before promulgating a rule. FinCEN has determined that it is not required to prepare a written statement under section 202 and has concluded that on balance this final rule provides the most cost-effective and least burdensome alternative to achieve the objectives of the rule. VII. Regulatory Flexibility Act FinCEN certifies that this amendment to the regulations implementing the Bank Secrecy Act will not have a significant, adverse financial impact on a substantial number of small depository institutions. By adding two new classes of customers, non-listed businesses and payroll customers, to the list of exempt persons, the final rule represents a significant decrease in the reporting burden imposed on all depository institutions. FinCEN anticipates that the addition of these two new classes of exempt persons can contribute to at least a 2 million reduction in the number of currency transaction reports filed annually, and a cost reduction to depository institutions of $16 million. Further, the requirements placed upon depository institutions under the reformed exemption system, as laid out in the final rule, represent a substantial net decrease in the burdens associated with the prior exemption process. For example, depository institutions will no longer be required to prepare and submit signed exemption statements, or to maintain customer exempt lists. Under the reformed system, a depository institution will be able to exempt the transactions in currency of an exempt person simply by the one-time filing of a currency transaction report form that identifies the exempt customer and the exempting depository institution, and, in the case of non-listed businesses and payroll customers, renewing the exempt status of its exempt customers every two years. VIII. Paperwork Reduction Act In accordance with requirements of the Paperwork Reduction Act of 1995, 44 U.S.C. 3501, et seq., and its implementing regulations, 5 CFR part 1320, the following information concerning the collection of information on Internal Revenue Service Form 4789 is presented to assist those persons wishing to comment on the information collection.

FinCEN anticipates that this final rule, if used by banks, can result in at least a 2 million reduction in the number of currency transaction reports required to be filed annually, and a cost reduction to banks of $16 million. FinCEN believes that these estimated reductions are reasonable, and probably conservative. Title: Currency Transaction Report. OMB Number: 1506-0004. Description of Respondents: All financial institutions, except casinos. Estimated Number of Respondents: 250,000. Frequency: As required. Estimate of Burden: Reporting average of 19 minutes per response; recordkeeping average of 5 minutes per response. Estimate of Total Annual Burden on Respondents: 10,000,000 responses. Reporting burden estimate = 3,166,667 hours; recordkeeping burden estimate = 833,333 hours. Estimated combined total of 4,000,000 hours. Estimate of Total Annual Cost to Respondents for Hour Burdens: Based on $20 per hour, the total cost to the public is estimated to be $80,000,000. Estimate of Total Other Annual Costs to Respondents: None. Type of Review: Extension. In accordance with the requirements of the Paperwork Reduction Act of 1995, 44 U.S.C. 3501 et seq., and its implementing regulations, 5 CFR part 1320, the following information concerning the collection of information as required by 31 CFR 103.22 is presented to assist those persons wishing to comment on the information collection. FinCEN anticipates that this final rule will result in a reduction in hours spent complying with exemption requirements of 350,000 hours, and a reduction in cost to banks of $7,500,000. This is a conservative estimate, based on comments and discussions with banking industry representatives of the cost of complying with the administrative exemption system requirements. Title: Currency transaction reporting exemption recordkeeping (31 CFR 103.22). OMB Number: 1506-0009. Description of Respondents: All banks. Estimated Number of Respondents: 19,000. Frequency: As required. Estimate of Burden: Recordkeeping average of 2 hours per respondent. Estimate of Total Annual Burden on Respondents: Recordkeeping burden estimate = 38,000 hours.

Estimate of Total Annual Cost to Respondents for Hour Burdens: Based on $20 per hour, the total cost to the public is estimated to be $760,000. Estimate of Total Other Annual Costs to Respondents: None. Type of Request: Extension. List of Subjects in 31 CFR Part 103 Administrative practice and procedure, Authority delegations (Government agencies), Banks and banking, Currency, Foreign banking, Foreign currencies, Gambling, Investigations, Law enforcement, Penalties, Reporting and recordkeeping requirements, Securities, Taxes. Amendment For the reasons set forth above in the preamble, 31 CFR part 103 is amended as follows: PART 103--FINANCIAL RECORDKEEPING AND REPORTING OF CURRENCY AND FOREIGN TRANSACTIONS 1. The authority citation for part 103 continues to read as follows: Authority: 12 U.S.C. 1829b and 1951-1959; 31 U.S.C. 5311-5330. 2. Section 103.22 is revised to read as follows: Sec. 103.22 Reports of transactions in currency. (a) General. This section sets forth the rules for the reporting by financial institutions of transactions in currency. The reporting obligations themselves are stated in paragraph (b) of this section. The reporting rules relating to aggregation are stated in paragraph (c) of this section. Rules permitting banks to exempt certain transactions from the reporting obligations appear in paragraph (d) of this section. (b) Filing obligations--(1) Financial institutions other than casinos. Each financial institution other than a casino shall file a report of each deposit, withdrawal, exchange of currency or other payment or transfer, by, through, or to such financial institution which involves a transaction in currency of more than $10,000, except as otherwise provided in this section. In the case of the Postal Service, the obligation contained in the preceding sentence shall not apply to payments or transfers made solely in connection with the purchase of postage or philatelic products. (2) Casinos. Each casino shall file a report of each transaction in currency, involving either cash in or cash out, of more than $10,000. (i) Transactions in currency involving cash in include, but are not limited to:

(A) Purchases of chips, tokens, and plaques; (B) Front money deposits; (C) Safekeeping deposits; (D) Payments on any form of credit, including markers and counter checks; (E) Bets of currency; (F) Currency received by a casino for transmittal of funds through wire transfer for a customer; (G) Purchases of a casino's check; and (H) Exchanges of currency for currency, including foreign currency.

(ii) Transactions in currency involving cash out include, but are not limited to:

(A) Redemptions of chips, tokens, and plaques; (B) Front money withdrawals; (C) Safekeeping withdrawals; (D) Advances on any form of credit, including markers and counter checks; (E) Payments on bets, including slot jackpots; (F) Payments by a casino to a customer based on receipt of funds through wire transfer for credit to a customer; (G) Cashing of checks or other negotiable instruments; (H) Exchanges of currency for currency, including foreign currency; and (I) Reimbursements for customers' travel and entertainment expenses by the casino.

(c) Aggregation--(1) Multiple branches. A financial institution includes all of its domestic branch offices, and any recordkeeping facility, wherever located, that contains records relating to the transactions of the institution's domestic offices, for purposes of this section's reporting requirements. (2) Multiple transactions--general. In the case of financial institutions other than casinos, for purposes of this section, multiple currency transactions shall be treated as a single transaction if the financial institution has knowledge that they are by or on behalf of any person and result in either cash in or cash out totaling more than $10,000 during any one business day (or in the case of the Postal Service, any one day). Deposits made at night or over a weekend or holiday shall be treated as if received on the next business day following the deposit. (3) Multiple transactions--casinos. In the case of a casino, multiple currency transactions shall be treated as a single transaction if the casino has knowledge that they are by or on behalf of any person and result in either cash in or cash out totaling more than $10,000 during any gaming day. For purposes of this paragraph (c)(3), a casino shall be deemed to have the knowledge described in the preceding sentence, if: any sole proprietor, partner, officer, director, or employee of the casino, acting within the scope of his or her employment, has knowledge that such multiple currency transactions have occurred, including knowledge from examining the books, records, logs, information retained on magnetic disk, tape or other machine-readable media, or in any manual system, and similar documents and information, which the casino maintains pursuant to any law or regulation or within the ordinary course of its business, and which contain information that such multiple currency transactions have occurred. (d) Transactions of exempt persons--(1) General. No bank is required to file a report otherwise required by paragraph (b) of this section with respect to any transaction in currency between an exempt person and such bank, or, to the extent provided in paragraph (d)(6)(vi) of this section, between such exempt person and other banks affiliated with such bank. In addition, a non-bank financial institution is not required to file a report otherwise required by paragraph (b) of this section with respect to a transaction in currency between the institution and a commercial bank. (A limitation on the exemption described in this paragraph (d)(1) is set forth in paragraph (d)(7) of this section.) (2) Exempt person. For purposes of this section, an exempt person is: (i) A bank, to the extent of such bank's domestic operations; (ii) A department or agency of the United States, of any State, or of any political subdivision of any State; (iii) Any entity established under the laws of the United States, of any State, or of any political subdivision of any State, or under an interstate compact between two or more States, that exercises governmental authority on behalf of the United States or any such State or political subdivision; (iv) Any entity, other than a bank, whose common stock or analogous equity interests are listed on the New York Stock Exchange or the American Stock Exchange or whose common stock or analogous equity interests have been designated as a Nasdaq National Market Security listed on the Nasdaq Stock Market (except stock or interests listed under the separate “Nasdaq Small-Cap Issues''

heading), provided that, for purposes of this paragraph (d)(2)(iv), a person that is a financial institution, other than a bank, is an exempt person only to the extent of its domestic operations; (v) Any subsidiary, other than a bank, of any entity described in paragraph (d)(2)(iv) of this section (a “listed entity'') that is organized under the laws of the United States or of any State and at least 51 percent of whose common stock or analogous equity interest is owned by the listed entity, provided that, for purposes of this paragraph (d)(2)(v), a person that is a financial institution, other than a bank, is an exempt person only to the extent of its domestic operations; (vi) To the extent of its domestic operations, any other commercial enterprise (for purposes of this paragraph (d), a “non-listed business''), other than an enterprise specified in paragraph (d)(6)(viii) of this section, that: (A) Has maintained a transaction account at the bank for at least 12 months; (B) Frequently engages in transactions in currency with the bank in excess of $10,000; and (C) Is incorporated or organized under the laws of the United States or a State, or is registered as and eligible to do business within the United States or a State; or (vii) With respect solely to withdrawals for payroll purposes from existing transaction accounts, any other person (for purposes of this paragraph (d), a “payroll customer'') that: (A) Has maintained a transaction account at the bank for at least 12 months; (B) Operates a firm that regularly withdraws more than $10,000 in order to pay its United States employees in currency; and (C) Is incorporated or organized under the laws of the United States or a State, or is registered as and eligible to do business within the United States or a State. (3) Initial designation of exempt persons--(i) General. A bank must designate each exempt person with which it engages in transactions in currency by the close of the 30-day period beginning after the day of the first reportable transaction in currency with that person sought to be exempted from reporting under the terms of this paragraph (d). Except where the person sought to be exempted is another bank as described in paragraph (d)(2)(i) of this section, designation by a bank of an exempt person shall be made by a single filing of Internal Revenue Service Form 4789, in which line 36 is marked “Designation of Exempt Person'' and items 2-14 (Part I, Section A) and items 37-49 (Part III) are completed, or by filing any form specifically designated by FinCEN for this purpose. The designation must be made separately by each bank that treats the person in question as an exempt person, except as provided in paragraph (d)(6)(vi) of this section. The designation requirements of this paragraph (d)(3) apply whether or not the particular exempt person to be designated has previously been treated as exempt from the reporting requirements of prior Sec. 103.22(a) under the rules contained in 31 CFR 103.22(a) through (g), as in effect on October 20, 1998 (see 31 CFR Parts 0 to 199 revised as of July 1, 1998). A special transitional rule, which extends the time for initial designation for customers that have been previously treated as exempt under such prior rules, is contained in paragraph (d)(11) of this section. (ii) Special rules for banks. When designating another bank as an exempt person, a bank must either make the filing required by paragraph (d)(3)(i) of this section or file, in such a format and manner as FinCEN may specify, a current list of its domestic bank customers. In the event that a bank files its current list of domestic bank customers, the bank must make the filing as described in paragraph (d)(3)(i) of this section for each bank that is a new customer and for which an exemption is sought under this paragraph (d). (4) Annual review. The information supporting each designation of an exempt person, and the application to each account of an exempt person described in paragraphs (d)(2)(vi) or (d)(2)(vii) of this section of the monitoring system required to be maintained by paragraph (d)(9)(ii) of this section, must be reviewed and verified at least once each year. (5) Biennial filing with respect to certain exempt persons--(i) General. A biennial filing, as described in paragraph (d)(5)(ii) of this section, is required for continuation of the treatment as an exempt person of a customer described in paragraph (d)(2)(vi) or (vii) of this section. No biennial filing is required for continuation of the treatment as an exempt person of a customer described in paragraphs (d)(2)(i)