BANK MERGERS IN THE FINANCIAL CRISIS – A COMPETITION ...

23

BANK MERGERS IN THE FINANCIAL CRISIS – A COMPETITION POLICY PERSPECTIVE Michael Hellwig ZEW – Leibniz Centre for European Economic Research Falk Laser Goethe University Graduate School of Economics, Finance and Management, Technische Universität Darmstadt

Transcript of BANK MERGERS IN THE FINANCIAL CRISIS – A COMPETITION ...

BANK MERGERS IN THE FINANCIAL CRISIS – A COMPETITION POLICY

PERSPECTIVE

Michael Hellwig ZEW – Leibniz Centre for European Economic Research

Falk Laser Goethe University Graduate School of Economics, Finance and Management, Technische Universität Darmstadt

OVERVIEW

2

Focus on the importance of competition policy in times of unstable financial markets

Investigate the competition effects of the merger between ABN AMRO and Fortis Bank Nederland in 2010

Estimate a structural model to analyze demand substitution patterns and pricing decisions

Simulate price effects of a merger between two Dutch banks with ex-ante info

Merger simulation … based on disaggregated data (like Goldberg 1995, in contrast to literature following

Berry/Levinsohn/Pakes 1995 using aggregated (market share) data (e.g. Ivaldi/Verboven 2005))

… in the banking sector (first to our knowledge)

SETTING

3

Merger between ABN AMRO and Fortis Bank Nederland in 2010 Interesting case: Largest bank takeover (71.1 billion euro in October 2007) Affected by financial crisis (Fortis was nationalized in October 2008 putting

the merger on hold) Involving state aid (Dutch state completed the merger in July 2010)

EC cleared the merger (2007) and approved state aid (2011) EC only had concerns regarding commercial banking; retail banking was not

considered to be affected by the merger (ABN AMRO 3rd, Fortis 4th)

Motivation to investigate price effects of the merger in retail banking sector Specifically: market for savings accounts

When the Dutch state made its state-aid decision, was it a good decision to continue the merger instead of keeping the banks separated?

APPROACH I

4

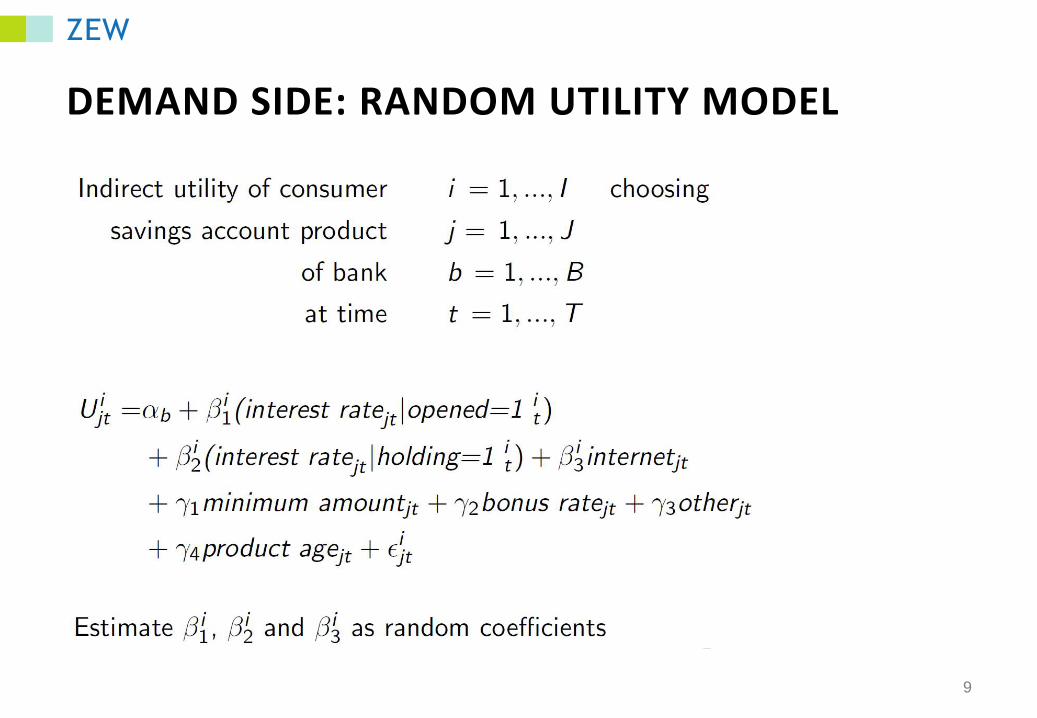

Merger simulation based on structural model Demand: Random utility model: discrete choice of a differentiated good (savings

account) Random-coefficients mixed logit model (flexible substitution patterns and

no IIA) Disaggregated approach: account for characteristics of products and

consumers Aggregation to retrieve elasticities (using population weights)

Supply: Bertrand Nash competition in a multiproduct oligopoly Choice variable: deposit rate ( negative effect on profits)

APPROACH II

5

Simulation: Change in ownership matrix Calibrate model with pre-merger data and simulate both scenarios

(merger/no-merger) for the actual merger year (ex-ante approach)

Calibration (2007-2009): 1. Demand: Estimate

price elasticities 2. Supply: Assume type

of competition

Simulation (2010): 1. Simulate interest rates

for merger case 2. Simulate interest rates

for no-merger case

Results: Obtain simulated changes in the interest rates induced by the merger

DATA

6

DNB Household Survey Dutch panel survey containing detailed information on asset and debt holding of

households and their characteristics Representative, about 2000 households interviewed each year Savings amount, income, age, having legacy accounts

Deposits rates for savings accounts from price comparison website Including information on type of account (internet-only or not) and other

constraints (minimum deposit, minimum holding time etc.)

Bank-related information from annual reports Financial figures, number of branches, other cost shifters, Euribor

Years: 2006-2014, but main focus on 2007-2010

DEVELOPMENT OF INTEREST RATES

7

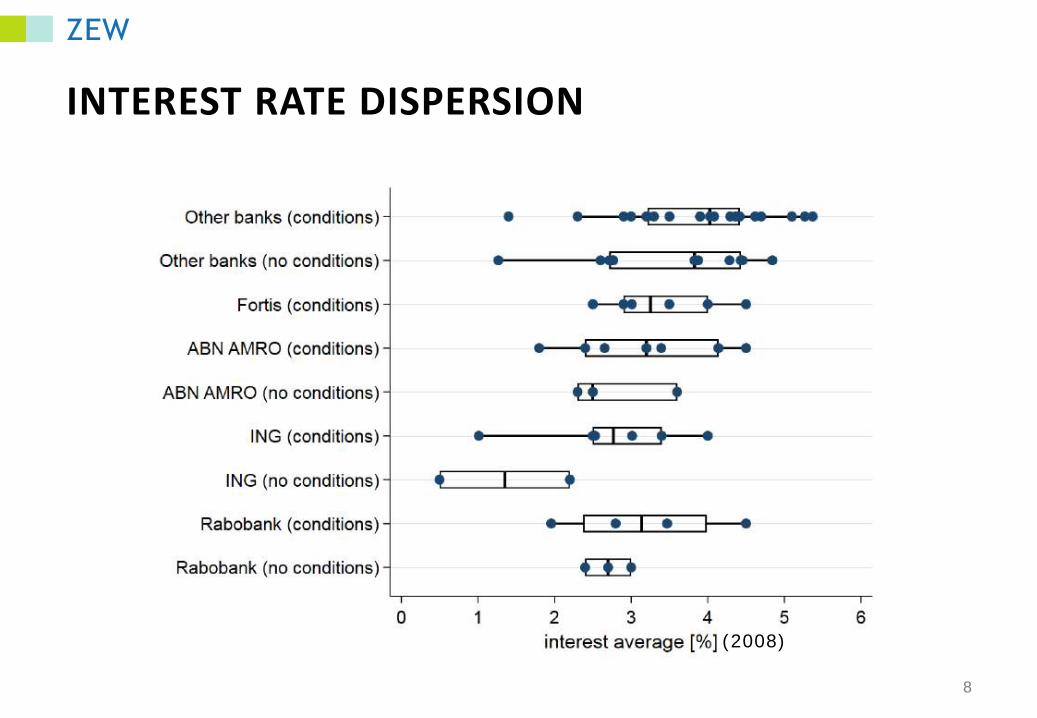

INTEREST RATE DISPERSION

8

(2008)

DEMAND SIDE: RANDOM UTILITY MODEL

9

ESTIMATION RESULTS

10

MERGER EFFECTS

11

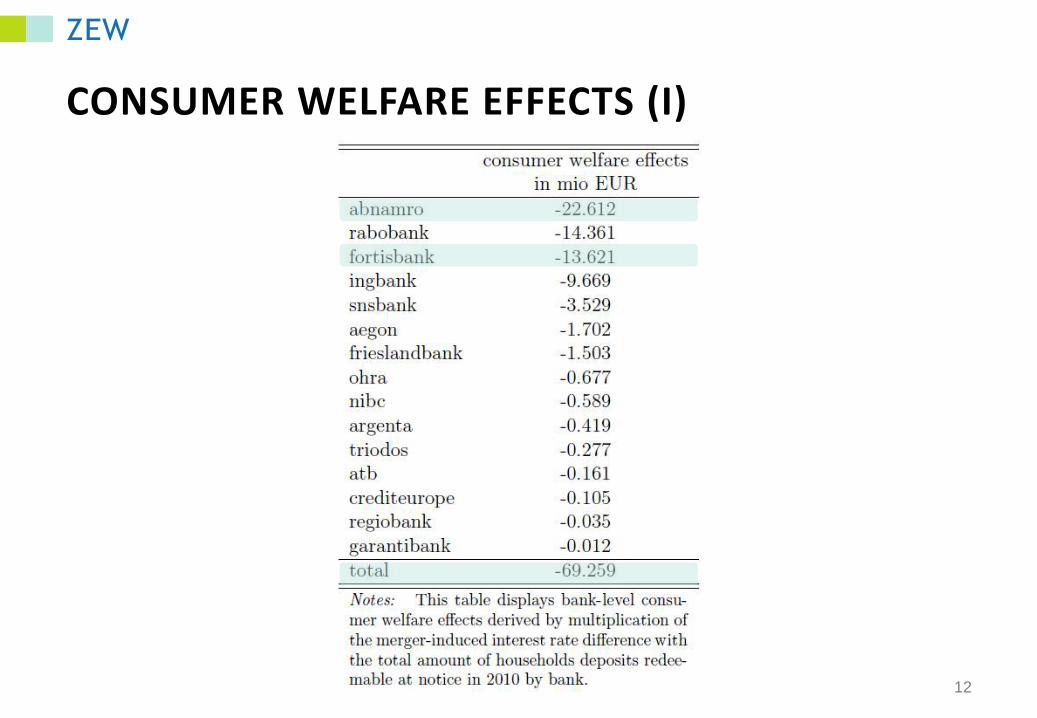

CONSUMER WELFARE EFFECTS (I)

12

CONSUMER WELFARE EFFECTS (II)

13

CONCLUSION

14

We use a structural model to simulate merger induced changes in the interest rates in the Dutch retail banking market induced by the merger between ABN AMRO and Fortis Bank NL

We predict significant merger-induced decreases in the interest rates for merging and non-merging banks ABN AMRO: -5% Fortis Bank NL: -3% Customer welfare loss: 69 mio EUR

Our results highlight taking into account the additional social costs due to lower competition next to the direct (fiscal) costs of stabilizing distressed financial markets

Michael Hellwig Phone: +49 621 1235 233 E-mail: [email protected] ZEW – Leibniz Centre for European Economic Research L7, 1 68161 Mannheim www.zew.eu

APPENDIX

THE MERGER BETWEEN ABN AMRO AND FORTIS

17

DEMAND SIDE: ELASTICITIES

18

SUPPLY SIDE

19

SIMULATE PRICE EFFECTS

20

-

SUPPLY SIDE: EXPECTED NET LOAN RATE

21

REGRESSING EXPECTED NET LOAN RATE ON EURIBOR

22

MERGER EFFECTS: PRODUCT LEVEL (EXTRACT)

23