Bank Indonesia Strengthening External Resilience ......1 BBB / Stable Baa2 / Stable BBB / Stable Apr...

41

July 2019 Bank Indonesia Strengthening External Resilience, Maintaining Stability

Transcript of Bank Indonesia Strengthening External Resilience ......1 BBB / Stable Baa2 / Stable BBB / Stable Apr...

July 2019

Bank Indonesia

Strengthening External Resilience, Maintaining Stability

1

BBB / Stable

Baa2 / Stable

BBB / Stable

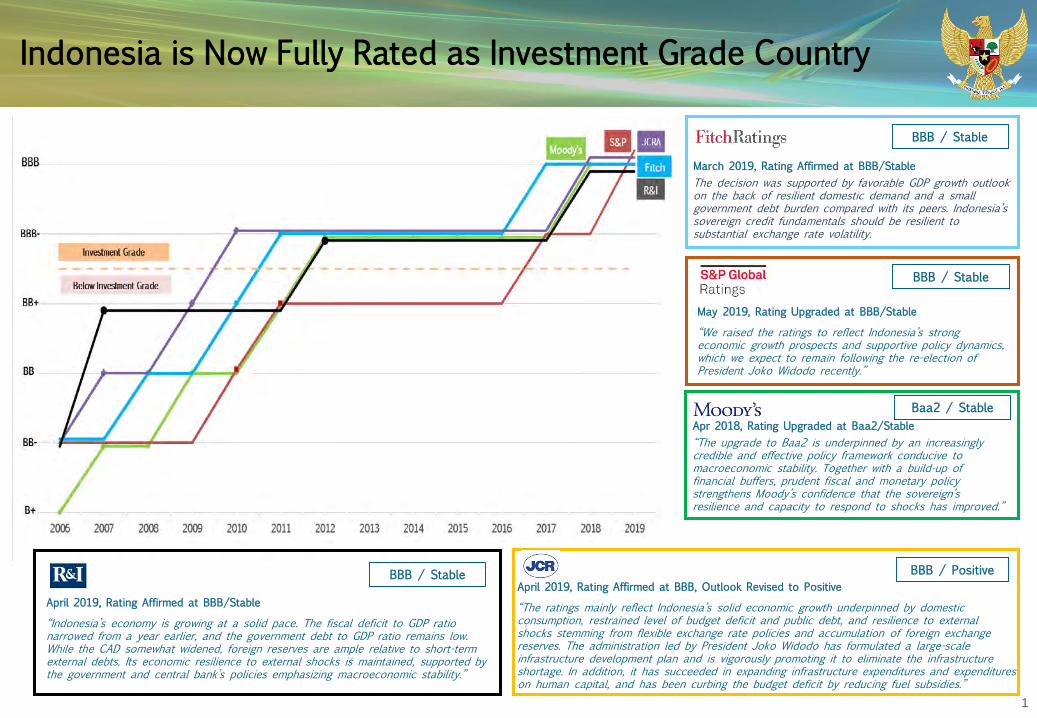

Apr 2018, Rating Upgraded at Baa2/Stable“The upgrade to Baa2 is underpinned by an increasingly credible and effective policy framework conducive to macroeconomic stability. Together with a build-up of financial buffers, prudent fiscal and monetary policy strengthens Moody’s confidence that the sovereign’s resilience and capacity to respond to shocks has improved.”

May 2019, Rating Upgraded at BBB/Stable

“We raised the ratings to reflect Indonesia’s strong economic growth prospects and supportive policy dynamics, which we expect to remain following the re-election of President Joko Widodo recently.”

March 2019, Rating Affirmed at BBB/StableThe decision was supported by favorable GDP growth outlook on the back of resilient domestic demand and a small government debt burden compared with its peers. Indonesia’s sovereign credit fundamentals should be resilient to substantial exchange rate volatility.

BBB / PositiveApril 2019, Rating Affirmed at BBB, Outlook Revised to Positive

“The ratings mainly reflect Indonesia’s solid economic growth underpinned by domestic consumption, restrained level of budget deficit and public debt, and resilience to external shocks stemming from flexible exchange rate policies and accumulation of foreign exchange reserves. The administration led by President Joko Widodo has formulated a large-scale infrastructure development plan and is vigorously promoting it to eliminate the infrastructure shortage. In addition, it has succeeded in expanding infrastructure expenditures and expenditures on human capital, and has been curbing the budget deficit by reducing fuel subsidies.”

BBB / Stable

April 2019, Rating Affirmed at BBB/Stable

“Indonesia’s economy is growing at a solid pace. The fiscal deficit to GDP ratio narrowed from a year earlier, and the government debt to GDP ratio remains low. While the CAD somewhat widened, foreign reserves are ample relative to short-term external debts. Its economic resilience to external shocks is maintained, supported by the government and central bank’s policies emphasizing macroeconomic stability.”

Indonesia is Now Fully Rated as Investment Grade Country

2

Indonesia’s Strong GDP

Growth Prospect

Strong GDP Growth1

%

Institutions 2019 GDP growth (%YoY)

2019 Budget 5.3

Bank Indonesia 5.0 – 5.4

IMF (WEO April 2019) 5.2

World Bank 5.2

ADB 5.2

Consensus Forecast (June 2019) 5.1

Favourable GDP Growth Compared to Peers2

1. Source: Central Bureau of Statistics of Indonesia (BPS), ** Including non-profit household consumption2. Source: World Economic Outlook Database – April 2019; * indicates estimated figure

%

• Solid national economic growth was recorded at 5.07% (yoy) in thefirst quarter of 2019, pointing to maintained domestic economicperformance despite retreating from 5.18% (yoy) in the fourthquarter of 2018. Seasonal factors at the beginning of the year aswell as the impact of weaker-than-expected global economic gainscontributed to the moderate economic downturn in Indonesia.

• Economic growth in the first quarter of 2019 was primarily driven bydomestic demand on the back of consumption by non-profitinstitutions serving households (NPISH) and households.

• Furthermore, domestic demand has also been supported by robustbuilding investment. Net exports maintained a positive position asimports declined, although exports also softened in line with globaleconomic moderation and sliding international commodity prices.

0.04

3.83 3.27

(2.07)

(0.16)

3.74 3.31

(1.73)

(0.36)

4.01 3.14

(1.81)

(0.30)

4.01 3.19

(1.70)

(0.42)

4.21

3.09

(1.69)(0.52)

5.12 4.94 4.93 5.05 4.82 4.74 4.77 5.17 4.92 5.18 5.01 4.94 5.01 5.01 5.06 5.19 5.06 5.27 5.17 5.18 5.07

-3.0

-1.0

1.0

3.0

5.0

7.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2014 2015 2016 2017 2018 2019

QoQ YoY

3.3 3.03.5 3.6

7.37.5

5.25.2

6.56.6

0.01.02.03.04.05.06.07.08.09.0

2012 2013 2014 2015 2016 2017 2018 2019* 2020*

Bulgaria Colombia India Indonesia Philippines

3

GDP Growth Breakdown

GDP Growth by Sector (%, YoY)

By sectors2014 2015 2016 2017 2018 2019

Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot Q1Agriculture, forestry, and fishery 5.2 4.9 3.6 3.3 4.2 3.7 6.5 2.9 1.6 3.8 1.5 3.5 3.2 5.5 3.4 7.1 3.3 2.8 2.4 3.9 3.3 4.7 3.7 3.9 3.9 1.8

Mining and Quarrying -1.2 0.7 0.7 1.5 0.4 0.6 (3.6) (4.4) (6.0) (3.4) 1.2 1.0 0.2 1.4 0.9 (1.3) 2.1 1.8 0.0 0.7 1.1 2.6 2.7 2.2 2.2 2.3Manufacturing 4.5 4.9 5.0 4.2 4.6 4.1 4.2 4.6 4.4 4.3 4.7 4.6 4.5 3.3 4.3 4.3 3.5 4.9 4.5 4.3 4.6 3.9 4.4 4.2 4.3 3.9Construction 7.2 6.5 6.5 7.7 7.0 6.0 5.4 6.8 7.1 6.4 6.8 5.1 5.0 4.2 5.2 6.0 7.0 7.0 7.2 6.8 7.4 5.7 5.8 5.6 6.1 5.9Wholesale and Retail Trade, Repair of Car and Motorcycle

6.1 5.1 5.2 4.4 5.2 3.8 1.6 1.4 3.5 2.5 4.3 4.3 3.7 3.9 4.0 4.6 3.5 5.2 4.5 4.5 5.0 5.2 5.3 4.4 5.0 5.3

Transportation and Storage 7.0 7.6 7.7 7.2 7.4 6.3 6.0 7.0 7.5 6.7 7.4 6.5 8.2 7.6 7.4 8.1 8.8 8.9 8.2 8.5 8.6 8.7 5.6 5.3 7.0 5.3

Information and communication 9.9 10.7 9.8 10.1 10.1 9.7 9.3 10.6 9.2 9.7 7.6 9.3 8.9 9.6 8.9 10.5 11.1 8.8 8.3 9.6 7.8 5.1 8.1 7.2 7.0 9.0

Financial service 3.6 5.5 1.9 7.9 4.7 8.6 2.6 10.3 12.8 8.6 9.3 13.6 9.0 4.2 8.9 6.0 5.9 6.1 3.8 5.5 4.2 3.1 3.1 6.3 4.2 7.3Other Services* 5.4 4.7 5.9 6.5 5.7 5.1 6.5 4.8 5.5 5.4 6.0 5.6 4.5 3.8 4.9 4.2 3.5 4.8 6.0 4,6 5.4 6.2 6.7 6.4 6.2 6.8GDP 5.1 4.9 4.9 5.0 5.0 4.8 4.7 4.8 5.2 4.9 4.9 5.2 5.0 4.9 5.0 5.0 5.0 5.1 5.2 5.1 5.1 5.3 5.2 5.2 5.2 5.1

Source: Central Bureau of Statistics of Indonesia (BPS)*Other services consist of 10 sectors (according to Standard National 2008)

GDP Growth Based on Expenditures (%, YoY)1

By expenditure2014 2015 2016 2017 2018 2019

Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot. Q1 Q2 Q3 Q4 Tot Q1 Q2 Q3 Q4 Tot Q1HH. Consumption 5.2 5.2 5.1 5.1 5.1 5.0 5.0 5.0 4.9 5.0 5.0 5.1 5.0 5.0 5.0 4.9 5.0 4.9 5.0 4.9 4.9 5.2 5.0 5.1 5.0 5.0Non profit HH. consumption 23.2 22.4 5.8 (0.5) 12.2 (8.1) (8.0) 6.6 8.3 (0.6) 6.4 6.7 6.7 6.7 6.6 8.1 8.5 6.0 5.3 6.9 8.1 8.8 8.6 10.8 9.1 16.9

Government consumption 6.1 (1.8) 1.2 0.9 1.2 2.9 2.6 7.1 7.1 5.3 3.4 6.2 (3.0) (4.0) (0.1) 2.7 (1.9) 3.5 3.8 2.1 2.7 5.2 6.3 4.6 4.8 5.2

Gross Fixed Cap. Formation

5.4 4.0 4.4 4.1 4.4 4.6 4.0 4.9 6.4 5.0 4.7 4.2 4.2 4.8 4.5 4.8 5.3 7.1 7.3 6.2 7.9 5.9 7.0 6.0 6.7 5.0

Exports 3.1 1.5 4.9 (4.4) 1.1 (0.6) (0.3) (1.0) (6.4) (2.1) (3.1) (1.5) (5.8) 4.1 (1.6) 8.4 2.7 16.5 8.4 8.9 5.9 7.6 8.1 4.3 6.5 (2.1)

Imports 5.1 0.4 0.2 3.0 2.1 (2.6) (7.1) (6.5) (8.6) (6.2) (5.0) (3.5) (4.1) 2.7 (2.4) 4.8 0.2 15.4 11.9 8.1 12.6 15.2 14.0 7.1 12.0 (7.8)

GDP 5.1 4.9 4.9 5.0 5.0 4.8 4.7 4.8 5.2 4.9 4.9 5.2 5.0 4.9 5.0 5.0 5.0 5.1 5.2 5.1 5.1 5.3 5.2 5.2 5.2 5.1

1. Source: Central Bureau of Statistics of Indonesia (BPS), ** Including non-profit household consumption

4

Regional Economic GrowthRegional growth in Java, Kalimantan, and Papua was weighed down by restrained manufacturingexports and minig sector performance.

Source: Central Bureau of Statistics of Indonesia (BPS)

External Factor:Improved External Resilience

Section 1

6

1.87

(8.10)

(1.79)

1.06

(6.97)

-12-10-8-6-4-202468

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1*Q2*Q3*Q4*Q1**

2013 2014 2015 2016 2017 2018* 2019**

Goods Services Primary Income Secondary Income Current Account

US$bn

- 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

50

60

70

80

90

100

110

120

130

1 3 5 7 911

1 3 5 7 911

1 3 5 7 911

1 3 5 7 911

1 3 5 7 911

1 3 5 7 911

1 3 5

2013 2014 2015 2016 2017 2018 2019

FX Reserves (LHS) Month of Import & Debt Service (RHS) MonthUS$bn

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5

2013 2014 2015 2016 2017 2018 2019

OG Non-OG Total

External Balance under Control Supported by Adequate Reserves

Current Account Deficit within Safe ThresholdBalance of Payments Portrait

Substantial FX Reserves to Mitigate External ChallengesTrade Balance Portrait

Source: Bank IndonesiaSource: Bank Indonesia

Source: BPS* Preliminary Figure ** Very Preliminary Figure

2015:Surplus

US$7.59bn

2013:Deficit

(US$4.10bn)

2014:Deficit

(US$2.37bn)

2016: Surplus

US$8.83bn

2017: Surplus

US$11.83bn

Source: Bank Indonesia

FX Reserves as of May 2019: US$120.3 bn (Equiv. to 6.7 months of imports + servicing of government debt)

US$bn

2015:CA Deficit(US$17.5bn)

2013:CA Deficit(US$29.1bn)

2014:CA Deficit(US$27.5bn)

2016:CA Deficit(US$17.0bn)

2017:CA Deficit(US$16.2bn)

2018:Deficit

(US$8.57bn)

2018:CA Deficit(US$31.1bn)

-7.0

10.1

2.4

124.5

0

40

80

120

160

-15

-10

-5

0

5

10

15

20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1*Q2*Q3*Q4*Q1**

2013 2014 2015 2016 2017 2018* 2019**

Current Account Capital and Financial AccountOverall Balance Reserve Asset (rhs)

US$bn US$bn

7

2.08

0.20

0.83

0.37

-4.73

-2.32

-2.26

-0.69

-1.91

-6.33

-4.49

-3.71

-13.18

3.51

1.51

1.28

0.77

0.54

0.06

-0.37

-0.38

-0.93

-1.09

-2.16

-5.53

-9.77

-16.0 -14.0 -12.0 -10.0 -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0

THBJPYPHPIDRBRLINRCNYSGDMYRZAREURKRWTRY

point-to-point average

%Data as of June 19th, 2019

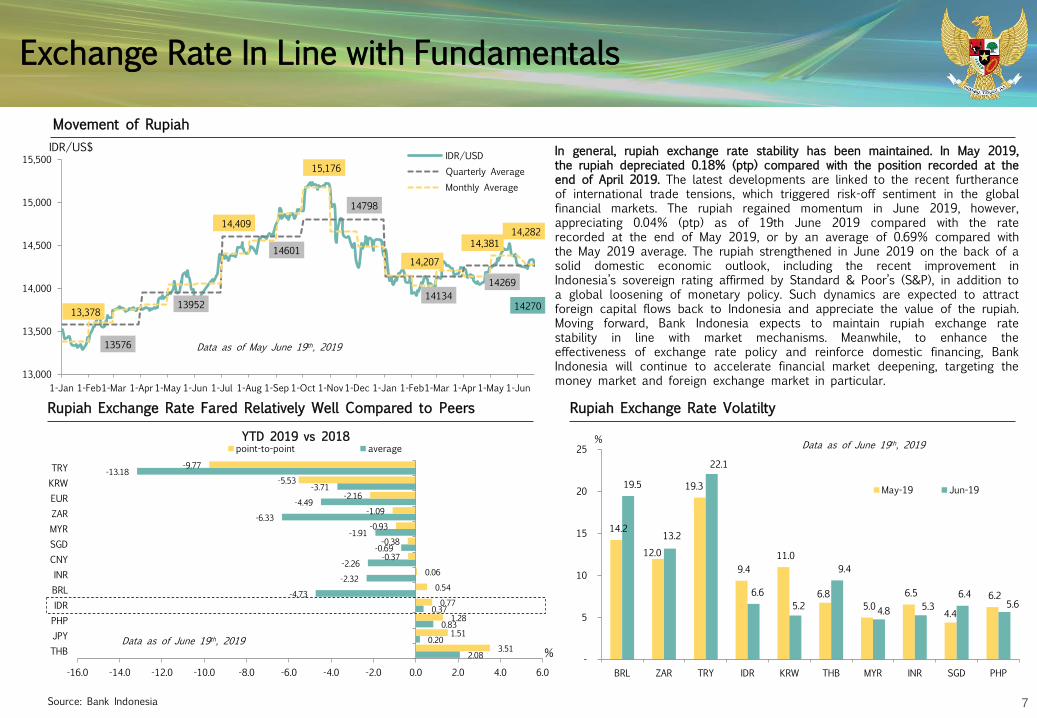

Exchange Rate In Line with Fundamentals

Movement of Rupiah

Rupiah Exchange Rate Fared Relatively Well Compared to Peers

IDR/US$ In general, rupiah exchange rate stability has been maintained. In May 2019,the rupiah depreciated 0.18% (ptp) compared with the position recorded at theend of April 2019. The latest developments are linked to the recent furtheranceof international trade tensions, which triggered risk-off sentiment in the globalfinancial markets. The rupiah regained momentum in June 2019, however,appreciating 0.04% (ptp) as of 19th June 2019 compared with the raterecorded at the end of May 2019, or by an average of 0.69% compared withthe May 2019 average. The rupiah strengthened in June 2019 on the back of asolid domestic economic outlook, including the recent improvement inIndonesia’s sovereign rating affirmed by Standard & Poor’s (S&P), in addition toa global loosening of monetary policy. Such dynamics are expected to attractforeign capital flows back to Indonesia and appreciate the value of the rupiah.Moving forward, Bank Indonesia expects to maintain rupiah exchange ratestability in line with market mechanisms. Meanwhile, to enhance theeffectiveness of exchange rate policy and reinforce domestic financing, BankIndonesia will continue to accelerate financial market deepening, targeting themoney market and foreign exchange market in particular.

Source: Bank Indonesia

YTD 2019 vs 2018

Rupiah Exchange Rate Volatilty

14270

13576

13952

14601

14798

1413414269

13,378

14,409

15,176

14,207

14,381 14,282

13,000

13,500

14,000

14,500

15,000

15,500

1-Jan 1-Feb1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Aug 1-Sep 1-Oct 1-Nov1-Dec 1-Jan 1-Feb1-Mar 1-Apr 1-May 1-Jun

IDR/USDQuarterly AverageMonthly Average

Data as of May June 19th, 2019

14.2

12.0

19.3

9.4 11.0

6.8 5.0

6.5

4.4

6.2

19.5

13.2

22.1

6.65.2

9.4

4.8 5.36.4

5.6

-

5

10

15

20

25

BRL ZAR TRY IDR KRW THB MYR INR SGD PHP

May-19 Jun-19

% Data as of June 19th, 2019

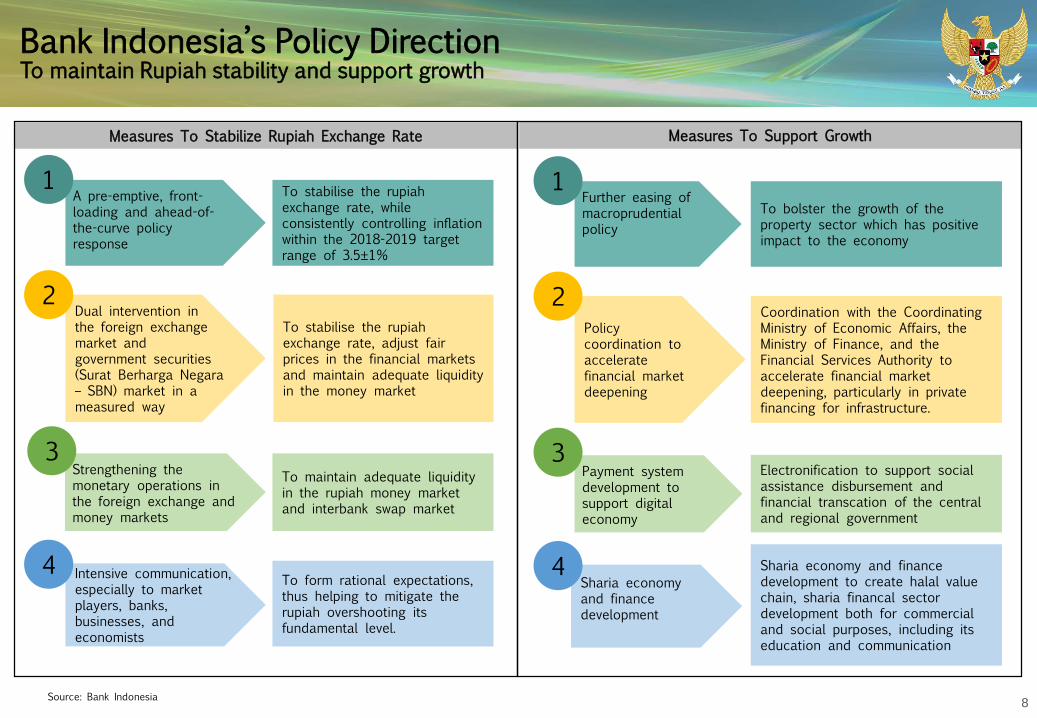

8

Bank Indonesia’s Policy DirectionTo maintain Rupiah stability and support growth

A pre-emptive, front-loading and ahead-of-the-curve policy response

Strengthening the monetary operations in the foreign exchange and money markets

To stabilise the rupiah exchange rate, while consistently controlling inflation within the 2018-2019 target range of 3.5±1%

To stabilise the rupiah exchange rate, adjust fair prices in the financial markets and maintain adequate liquidity in the money market

To maintain adequate liquidity in the rupiah money market and interbank swap market

To form rational expectations, thus helping to mitigate the rupiah overshooting its fundamental level.

Dual intervention in the foreign exchange market and government securities (Surat Berharga Negara – SBN) market in a measured way

Intensive communication, especially to market players, banks, businesses, and economists

4

3

2

Measures To Stabilize Rupiah Exchange Rate Measures To Support Growth

Further easing of macroprudential policy

Payment system development to support digital economy

To bolster the growth of the property sector which has positive impact to the economy

Coordination with the Coordinating Ministry of Economic Affairs, the Ministry of Finance, and the Financial Services Authority to accelerate financial market deepening, particularly in private financing for infrastructure.

Electronification to support social assistance disbursement and financial transcation of the central and regional government

Sharia economy and finance development to create halal valuechain, sharia financal sector development both for commercial and social purposes, including its education and communication

Policy coordination to accelerate financial market deepening

Sharia economy and finance development

4

3

2

11

Source: Bank Indonesia

9

Ample Lines of Defense Against External Shocks

Ample level of FX reserves to buffer against external shock FX Reserves as of May 2019: US$120.3 billion

South Korea Renewed a 3 year KRW / IDR swap arrangement with the size of up to KRW 10.7 trillion / IDR 115 trillion in March 2017

Australia Renewed a 3 year A$/IDR swap arrangement of up to A$10 billion or IDR 100 trillion in August 2018

Chiang Mai Initiative

Multilateralization (CMIM) Agreement

Entitled to a maximum swap amount of US$ 22.76 bn under the ASEAN+3 (Japan, China, and Korea) FX reserves pool created under the agreement

Came into effect in 2010 with a pool of US$120 bn Doubled to US$240 bn effective July 2014

Japan Renewed a 3 year USD22.76 billion swap line with Japan on October 14th, 2018 The facility is available in USD and JPY

IMF Global Financial Safety

Net - GSFN

Indonesia is entitled to access IMF facilities for crisis prevention to address potential (actual) BOP problem Such facilities include Flexible Credit Line (FCL) and Precautionary and Liquidity Line (PLL)

Bilateral

Region

alGlob

al

FX Reserve

Ample Reserves

Swap Arrangement

Source: Bank Indonesia

ASEAN Swap Arrangement (ASA)

Entitled to a maximum swap amount of USD600 million under ASA The first MoU on the ASA was signed in 1977 among 5 ASEAN Central Banks with total facility USD100 million Doubled to USD2 billion in 2005

Singapore Established a one year SGD/IDR swap arrangement with a size up to USD10 billion (equivalent) in November 2018

China Renewed a 3 year swap arrangement and increased the size of swap line up to CNY 200 bn / USD 30 billion in November 2018

10

Solid Policy Coordination In Managing Financial Markets Volatility

Source: Ministry of Finance

First Line of Defense

State’s BudgetBuyback fund at DG of Budget Financing and Risk ManagementInvestment fund at Public Service Agency (BLU) (min. level Aware)

State Owned Enterprises (BUMN)’s Budget Related SOEs (min. level Aware)

Social Security Organizing Agency (BPJS)’s Budget

BPJS (min. level Aware)

Second Line of Defense

State’s Budget

State General Treasury Account (Rekening KUN) (min. level Alert)Accumulated cash surplus (SAL) (min. Level Crisis)

Gov’t Securities Crisis Management Protocol (CMP) Indicators:

- Yield of benchmark series;- Exchange rate;- Jakarta Composite Index;- Foreign ownership in government securities

Policies to address the crisis at every level :- Repurchase the government securities at secondary market- Postpone or stop the issuance

Bond Stabilization Framework

The enactment of Law No. 9/2016 regarding Prevention and Mitigation of Financial System Crises as a legal foundation for the government to serves at the time of financial crisis in the form of Financial System Stability Committee (KSSK)

KSSK members: the Ministry of Finance, Bank Indonesia, the Financial Services Authority, and the Deposit Insurance Corporation

Swap facility arrangements based on internationalcooperation

Enhancing coordination between government institutions and continuous dialogue with market participants

Implementing Crisis Management Protocol (CMP)CMP

Implementing Bond Stabilization Framework (BSF)BSF

11

23.3

34.8

20.3

39.6

68.8

21.9

35.2

19.5

40

63.5

20.8

34.4

21.5

39.6

62.7

0 10 20 30 40 50 60 70 80

Philippines

Indonesia

India

Colombia

Bulgaria

2019F 2018F 2017

Strengthened Private External Debt Risk Management

Regulation Key PointsPhase 1

Jan 1,2015 –Dec 31,2015

Phase 2Jan 1,2016 –Dec 31,2016

Phase 3Jan 1, 2017 & beyond

Object of Regulation Governs all Foreign Currency Debt

Hedging Ratio

< 3 months 20%* 25%**

> 3 – 6 months 20%* 25%**

Liquidity Ratio (< 3 months) 50% 70%

Credit Rating Not applicable Minimum rating of BB-

Hedging transaction to meet hedge ratio

not necessarily be done with a bank in Indonesia

Must be done with a bank in

Indonesia

Sanction As of Q IV-2015 Applied

External Debt/GDP (%)

Debt Burden Indicator (External Debt/GDP) Remains Comparable to Peers Rating Encouraging Corporates Compliance on Hedging Ratio & Liquidity Ratio

Source: Bank Indonesia

Liquidity Ratio*

Hedging Ratio*

*Data as of Q4 2018, with total population 2.726 corporates

Regulation on Prudential Principle in Managing External Debt

Source: Bank Indonesia

Source: Moody’s Statistical Handbook, November 2018

2,466 ,

90.5%

260 , 9.5%

≤ 3 months

2,545 , 93.4%

181 , 6.6%

> 3 - 6 months

2,418 , 88.7%

308 , 11.3%

Comply Not Comply

12

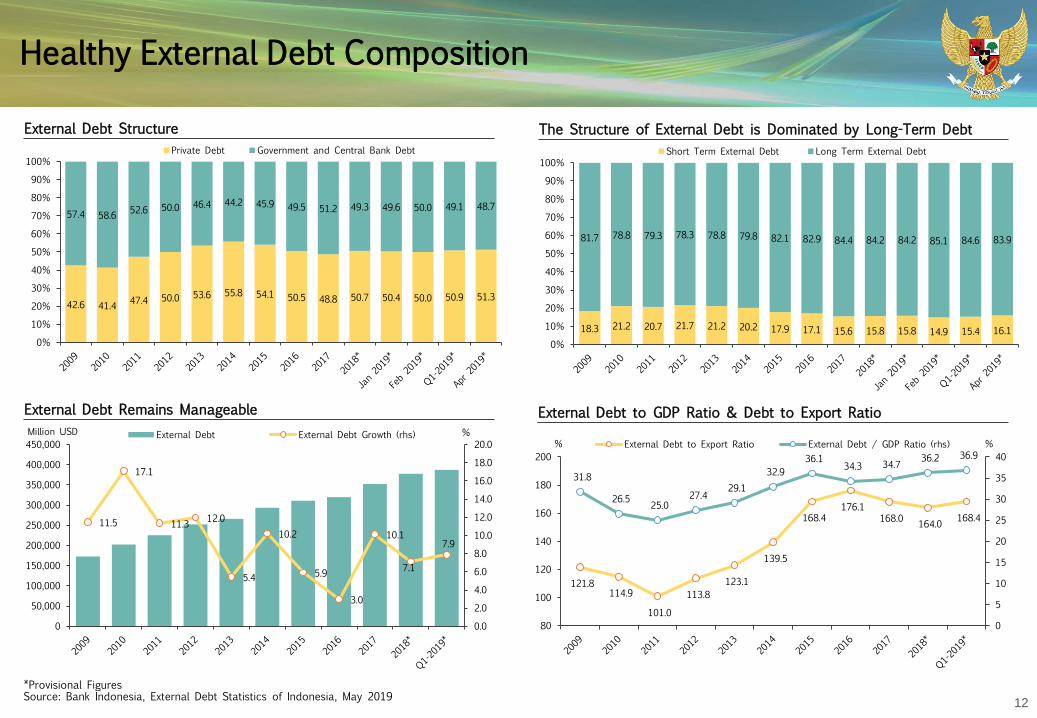

Healthy External Debt Composition

External Debt Structure

Source: Bank Indonesia, External Debt Statistics of Indonesia, May 2019*Provisional Figures

The Structure of External Debt is Dominated by Long-Term Debt

External Debt Remains Manageable External Debt to GDP Ratio & Debt to Export Ratio

11.5

17.1

11.3 12.0

5.4

10.2

5.9

3.0

10.1

7.1

7.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000%Million USD External Debt External Debt Growth (rhs)

121.8 114.9

101.0

113.8 123.1

139.5

168.4 176.1

168.0 164.0 168.4

31.8

26.5 25.0 27.4

29.1 32.9

36.1 34.3 34.7 36.2 36.9

0

5

10

15

20

25

30

35

40

80

100

120

140

160

180

200%% External Debt to Export Ratio External Debt / GDP Ratio (rhs)

18.3 21.2 20.7 21.7 21.2 20.2 17.9 17.1 15.6 15.8 15.8 14.9 15.4 16.1

81.7 78.8 79.3 78.3 78.8 79.8 82.1 82.9 84.4 84.2 84.2 85.1 84.6 83.9

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Short Term External Debt Long Term External Debt

42.6 41.4 47.4 50.0 53.6 55.8 54.1 50.5 48.8 50.7 50.4 50.0 50.9 51.3

57.4 58.6 52.6 50.0 46.4 44.2 45.9 49.5 51.2 49.3 49.6 50.0 49.1 48.7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Private Debt Government and Central Bank Debt

13

Manageable External Debt ProfileShort term non-bank corporate debt (non affiliation) represents only 8.4% of total private external debt

Private

Short-Term1

Private Non-Bank

External DebtPosition

Affiliation

Non Affiliation

US$145.2bnor

72.8%of Private Ext.

Debt

US$26.7bnor

13.4%of Private Ext. Debt

US$10.9bnor

5.5%of Private Ext. Debt

US$16.8bnor

8.4%of Private Ext. Debt

Public Long Term 1 Private Bank

US$27.7bnor

13.9%of Private Ext. Debt

US$199.6bnor

51.3%of total Ext. Debt

US$54.4bnor

27.2%of Private Ext. Debt

External Debt Position as of April 20191 Based on remaining maturity

Source: External Debt Statistics of Indonesia, June 2019

US$389.3bn

US$189.7bnor

48.7%of Total Ext.

Debt

Monetary and Financial Factor:Credible Monetary Policy Track Record and Favourable Financial Sector

Section 2

15

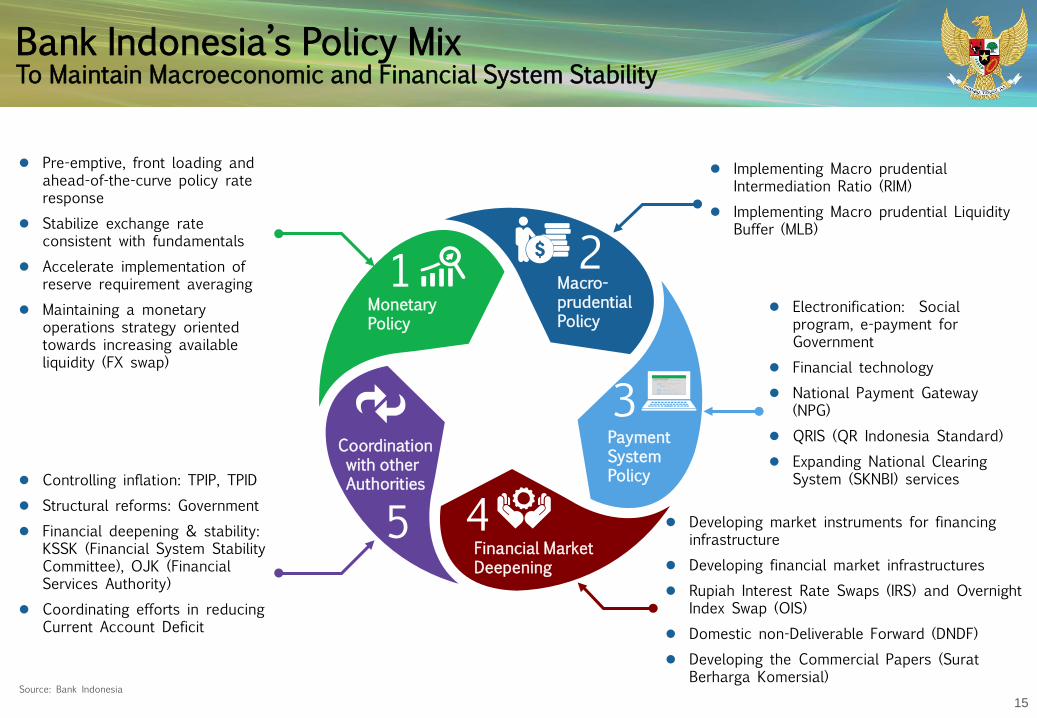

Bank Indonesia’s Policy MixTo Maintain Macroeconomic and Financial System Stability

Source: Bank Indonesia

Implementing Macro prudential Intermediation Ratio (RIM)

Implementing Macro prudential Liquidity Buffer (MLB)

Electronification: Social program, e-payment for Government

Financial technology National Payment Gateway

(NPG) QRIS (QR Indonesia Standard) Expanding National Clearing

System (SKNBI) services

Developing market instruments for financing infrastructure

Developing financial market infrastructures Rupiah Interest Rate Swaps (IRS) and Overnight

Index Swap (OIS) Domestic non-Deliverable Forward (DNDF) Developing the Commercial Papers (Surat

Berharga Komersial)

Controlling inflation: TPIP, TPID Structural reforms: Government Financial deepening & stability:

KSSK (Financial System Stability Committee), OJK (Financial Services Authority)

Coordinating efforts in reducing Current Account Deficit

Pre-emptive, front loading and ahead-of-the-curve policy rate response

Stabilize exchange rate consistent with fundamentals

Accelerate implementation of reserve requirement averaging

Maintaining a monetary operations strategy oriented towards increasing available liquidity (FX swap)

MonetaryPolicy

Coordinationwith otherAuthorities

Financial MarketDeepening

Macro-prudentialPolicy

PaymentSystem Policy

1 2

3

45

16

Bank Indonesia Policy Mix: June 2019

The BI Board of Governors agreed on 19th and 20th June 2019 to hold the BI 7-Day Reverse Repo Rate at 6.00%* and to lower Rupiah Reserve Requirement by 50bps.

Constantly monitors global financial market dynamics and the external stability of the

national economy when considering reductions to the policy rate in line with low inflation and the current need to stimulate domestic economic

growth.

Holds the BI 7-DayReverse

Repo Rate at 6.00%.

Bolsters payment system policy and financial

market deepening efforts to support economic

growth, while strengthening

coordination with the Government and other relevant authorities to

sustain economic stability, stimulate domestic demand,

increase exports and tourism as well as

attract foreign capital flows.

Source: Bank Indonesia

Continues to focus the monetary operations strategy towards ensuring adequate liquidity is

available in the money market.

Maintains an accommodative macroprudentialpolicy stance to catalyse bank lending and

expand economic financing.

Has decided to lower the rupiah reserve requirement for

conventional and Islamic banks by 50bps to 6.0% and 4.5% respectively,

with the average reserve requirements remaining at 3.0%, to ensure

adequate liquidity in the banking industry in order

to finance economic activity, effective from

1st July 2019.

*while also maintaining the Deposit Facility (DF) and Lending Facility (LF) rates at 5.25% and 6.75%, respectively.

17

Principles of Domestic Non Deliverable Forward (DNDF) Transaction

Purposes

1. To support the effort of stabilizing the Rupiah exchange rate through the additional of alternative hedging instruments

2. To support the development and deepening of the domestic financial market

3. To increase the confidence of exporters, importers, and investors in conducting economic and investment activities through the flexibility of hedging transactions against Rupiah currency risk

General Provisions

Domestic Non-Deliverable Forward Transaction (DNDF Transaction)Plain vanilla derivatif transaction of foreign exchange against rupiah in the form of forward transaction with fixing mechanism in the domestic market

Forward TransactionsForward Transactions are sell/purchase foreign currencies againts rupiah whereas the delivery of funds shall be performed in more than 2 days after the transaction date

Fixing MechanismTransaction settlement mechanism without full movement of funds by calculating the difference between rate on the transaction date and reference rate in JISDOR on a specified future time agreed in the contract (fixing date)

Other DefinitionsThe definition of derivative transaction of foreign exchange againts rupiah, Forward Transaction, Spot Transaction, Customers, Foreign Party is referring to Bank Indonesia regulations regarding foreign exchange transaction againtsrupiah

Source: Bank Indonesia

18

Principles of Domestic Non Deliverable Forward (DNDF) Transaction

Bank can perform DNDF Transactions as follows:

Bank – Customer

Bank – Foreign Party

Bank – Bank

Transaction between:

Can only be performed to hedge rupiah exchange rate

risk.

1. Must have Underlying Transactions:

Including all following activities :a. Trade of goods and servicesb. Investments, loans, capital, and other

investements.c. Banks credit or financing in foreign currencies

(specifically for transactions between bank and customers)

Excluding following activities:a. Bank Indonesia certificates;b. Placement of funds with bank;c. Unwithdrawn credit facilities;d. Documents of foreign currencies sales againts

rupiah;e. Money transfer by fund transfer companiesf. Intercompany loang. Money changer activities.

2. Nominal of DNDF Transactions ≤ Nominal of Underlying Transactions

3. Tenor of DNDF Transactions ≤ Tenor of Underlying Transactions

Source: Bank Indonesia

19

Principles of Domestic Non Deliverable Forward (DNDF) Transaction

Transaction Settlement• Use Fixing mechanism• Reference rate: JISDOR for USD/IDR and BI FX Transaction MidRate for non-USD/IDR• Settlement currency : IDR• Roll over and early termination are not allowed

Roll over and early termination for DNDF is prohibitedHowever, unwind can be done by opening the reverse DNDF transactions

Cover HedgingBank may conduct DNDF Transactions with Bank Overseas for cover hedging purpose.• Underlying Transactions: DNDF Transaction between Bank and Customer/Foreign • Purpose: Hedging

Customer / Foreign Party Bank Overseas

BankHedging

Notes:Customer A conduct DNDF transactions with Bank B, and so Bank B can conduct DNDFtransactions with overseas Bank for the purpose of cover hedge.

Cover Hedging

Source: Bank Indonesia

20

Overnight Index Swaps (OIS) & Interest Rate Swaps (IRS)

Source: Bank Indonesia

As hedging instruments against Rupiah interest rate changes IRS is a contract between two parties toperiodically exchange rupiah interest rateflows during the contract period or at thecompletion of the contract based on certainnotional amount. IRS pricing is based onJIBOR.

OIS is an interest rate swap agreement basedon a daily overnight reference rate (IndoNIA)

Encourage price transparency in the rupiah money market

Strengthen monetary policy transmission

Provide alternative hedging instruments against rupiah interest rate changes

Support securities market deepening in Indonesia

1

2

3

4

IndoNIA & JIBOR

OIS transaction with IndoNIA as benchmark rate

Alignment between JIBOR and OIS interest rate

Improvement of IRS transaction liquidity

Strengthening reference rate based on realtransactions

21

OIS and IRS Transactions: General Provisions

Source: Bank Indonesia

Market Players. Banks, bank clients, both individualand non-bank institutions, and also foreign parties.

Transaction Needs Analysis. A bank performing anIRS or OIS transaction with a customer and/orforeign party on behalf of the customer and/orforeign party is required to have an analysis on theneed of rupiah interest rate derivative transactions.

Market Conventions. When performing IRS and OIStransactions, the respective bank is bound bymarket conventions agreed upon by market playersthrough industry association including theIndonesian Foreign Exchange Market Committee.

Settlement. Settlement can be performed as anetting payment and every transaction has to besettled in Rupiah. Close-out netting can be appliedunder predetermined conditions.

Market Conventions

Calculation Base

ACT/360

IndONIAIndex with 5

decimals

Compound Floating Rates (CFR) based

on 5 decimals

Interest Payment based on Netting

Notional of Net interest payment in

IDR with 0 decimals

Settlement Date = 1 business days

after Maturity Date (MD)

OIS Quotation rates based on 2 decimals

Quotation : 1W, 2W, 1M, 2M, 3M,

4M, 5M, 6M

At the 1st phase, OIS settlement will only be done at the

end of the OIS tenor (MD+1bd).

22

Bank Indonesia Policy Mix: 2015 – 2017

Further relaxation of LTV for property loans (Sept)

Strengthening systemic surveillance & Crisis Management Protocol (April)

E-money for social transfer (Nov)

Financial Technology (FinTech) Office (Nov)

New Rupiah issuance (Dec)

Obligation to use IDR in domestic transaction (March)

Non-cash movement (GNNT)

Market-based exchange rate stability consistent with fundamental Dual intervention in the FX market and purchases of government bonds from secondary market in

time of distress (capital reversal) or large mis-alignment

• BI 7-day RR Rate cut of 25bps to 4.50% (Aug)

• Further BI 7-day RR Rate cut of 25 bps to 4.25% (Sept)

• Further lowering RR by 100bps to 6.5% (Feb)

• Lowering RR by 50bps to 7.5% (Nov)

Policy Rate cuts of 150bps Moving from BI Rate (12

month) to BI 7-day Reverse Repo Rate (Aug)

1. Monetary Policy

Policy Rate

Reserve Requirement

2. Exchange Rate Policy

3. Macroprudential Policy

• Relaxation of LTV for property and automotive loans (June)

• BI Rate cut of 25bps (Feb)

• Implementation of RR Averaging (Aug): RR fixed 5%; RR Averaging 1.5%

Initiative to issue macroprudential regulation on Financing to Funding Ratio (FFR)

4. Payment System Policy

National Payment Gateway (June)

Modernized cash management underway

2015 2016 2017

Source: Bank Indonesia

23

3.00

4.00

5.00

6.00

7.00

8.00

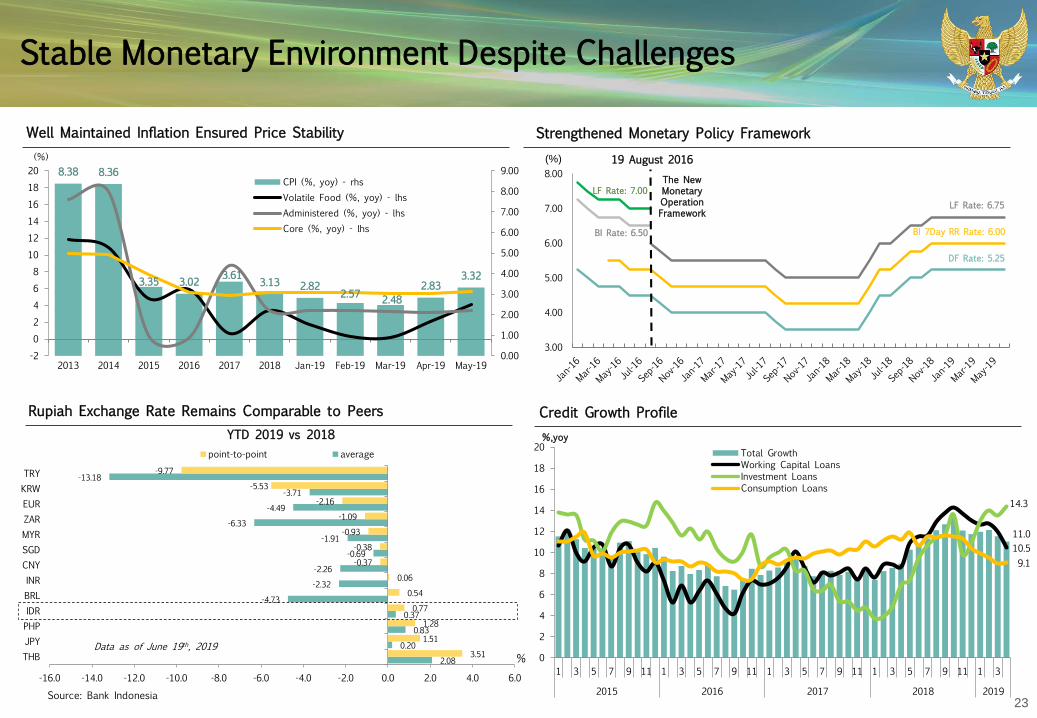

Stable Monetary Environment Despite Challenges

Rupiah Exchange Rate Remains Comparable to Peers

Well Maintained Inflation Ensured Price Stability Strengthened Monetary Policy Framework

Credit Growth Profile

BI 7Day RR Rate: 6.00

(%)

LF Rate: 7.00LF Rate: 6.75

BI Rate: 6.50

DF Rate: 5.25

19 August 2016

The New MonetaryOperation Framework

Source: Bank Indonesia

YTD 2019 vs 2018

8.38 8.36

3.35 3.02 3.613.13 2.82

2.57 2.482.83

3.32

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

-2

0

2

4

6

8

10

12

14

16

18

20

2013 2014 2015 2016 2017 2018 Jan-19 Feb-19 Mar-19 Apr-19 May-19

(%)

CPI (%, yoy) - rhsVolatile Food (%, yoy) - lhsAdministered (%, yoy) - lhsCore (%, yoy) - lhs

11.010.5

14.3

9.1

0

2

4

6

8

10

12

14

16

18

20

1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3

2015 2016 2017 2018 2019

%,yoyTotal GrowthWorking Capital LoansInvestment LoansConsumption Loans

2.08

0.20

0.83

0.37

-4.73

-2.32

-2.26

-0.69

-1.91

-6.33

-4.49

-3.71

-13.18

3.51

1.51

1.28

0.77

0.54

0.06

-0.37

-0.38

-0.93

-1.09

-2.16

-5.53

-9.77

-16.0 -14.0 -12.0 -10.0 -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0

THBJPYPHPIDRBRLINRCNYSGDMYRZAREURKRWTRY

point-to-point average

%Data as of June 19th, 2019

24

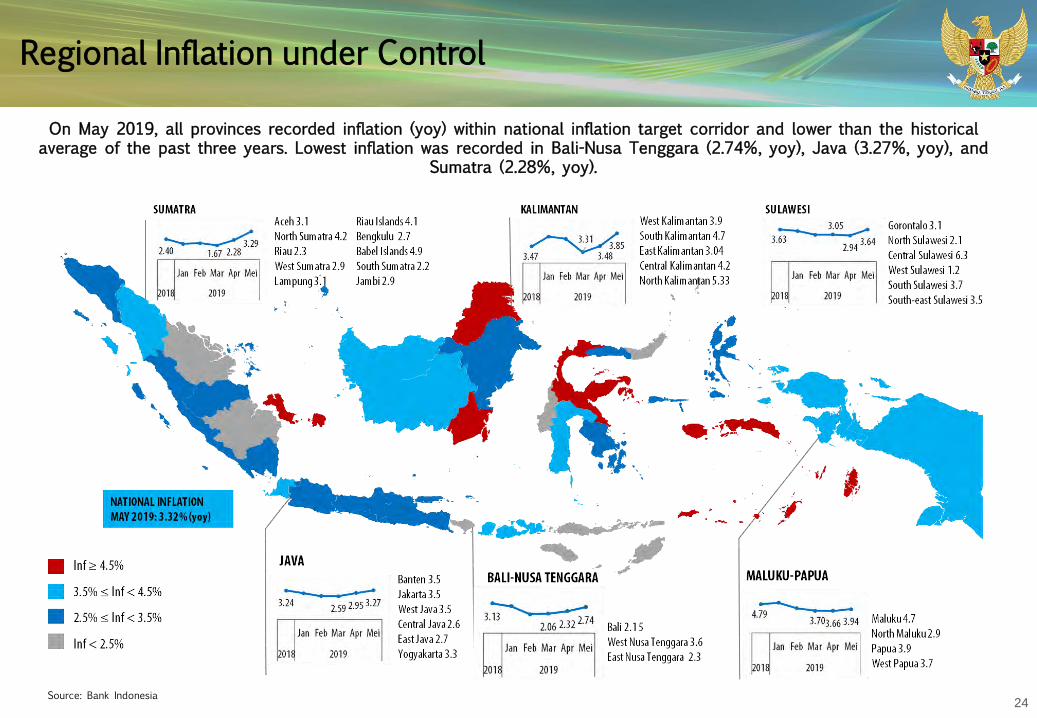

Regional Inflation under Control

On May 2019, all provinces recorded inflation (yoy) within national inflation target corridor and lower than the historical average of the past three years. Lowest inflation was recorded in Bali-Nusa Tenggara (2.74%, yoy), Java (3.27%, yoy), and

Sumatra (2.28%, yoy).

Source: Bank Indonesia

25

4 Strategies to Achieve the Inflation Target

Achieving inflation at 3,5%±1%• Maintaining core inflation• Maintaining volatile food stability at 4-5%• Controlling administered price inflation

2018-2019 Target

Stabilizing the price

1. Price Affordability

Achieving inflation at 3,0%±1%• Maintaining core inflation• Maintaining volatile food inflation less than 4%• Controlling administered price inflation

2020-2021 Target

Managing demand side

Strengthening production, Government food reserves

and food export-import management

2. Supply Availability

Strengthening institution

Encouraging trade

cooperation between regions

3. Well Managed Distribution

Improving trade

infrastructureImproving data

quality

4. Effective Communication

Strengthening central-regional coordination

Source: Bank Indonesia

4 Strategies

26

Improving the Effectiveness of Monetary Policy Transmission

Bank Indonesia has instituted a Reformulation of Monetary Policy Operations Framework which consists of 3 pillars; (1) implementation of BI 7day Reverse Repo Rate;

(2) implementation of reserve requirement averaging; and (3) continue to implement money market deepening program.

Enhancement of monetary policy signal

Enhancement of banking liquidity management

Implementation of BI 7 Day Reverse Repo Rate

Implementation of Reserve Requirement (RR)

Averaging

Reformulation of Monetary Policy Operational Framework

Enhancement of instruments and transactions

Implementation of Money Market Deepening

Program

Source: Bank Indonesia

27

Enhancement of Monetary Operations Framework

• Can be traded among contributor banks for 10 minutes.

• Up to the amount of Rp10 billion.• Up to 1-month tenor.

• Can be traded among contributor banks for 20 minutes.

• Up to a total of Rp20 billion.• Up to 3-month tenor.

CURRENT JIBOR (as per June 1st, 2016)

PREVIOUS JIBOR

Source: Bank Indonesia

28

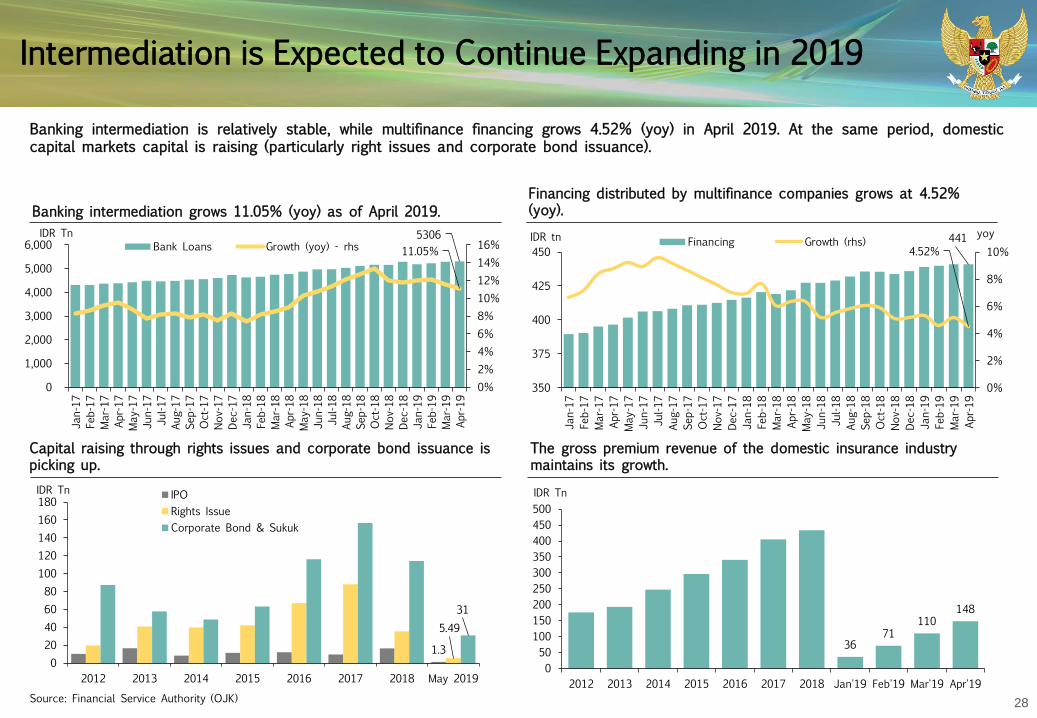

Intermediation is Expected to Continue Expanding in 2019

Banking intermediation is relatively stable, while multifinance financing grows 4.52% (yoy) in April 2019. At the same period, domesticcapital markets capital is raising (particularly right issues and corporate bond issuance).

Source: Financial Service Authority (OJK)

Financing distributed by multifinance companies grows at 4.52% (yoy).

The gross premium revenue of the domestic insurance industry maintains its growth.

Capital raising through rights issues and corporate bond issuance is picking up.

Banking intermediation grows 11.05% (yoy) as of April 2019.5306

11.05%

0%2%4%6%8%10%12%14%16%

0

1,000

2,000

3,000

4,000

5,000

6,000

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

IDR TnBank Loans Growth (yoy) - rhs

1.3

5.4931

020406080

100120140160180

2012 2013 2014 2015 2016 2017 2018 May 2019

IDR Tn IPORights IssueCorporate Bond & Sukuk

3671

110148

050

100150200250300350400450500

2012 2013 2014 2015 2016 2017 2018 Jan'19 Feb'19 Mar'19 Apr'19

IDR Tn

441 4.52%

0%

2%

4%

6%

8%

10%

350

375

400

425

450

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

yoyIDR tn Financing Growth (rhs)

29

Financial Institutions Remain Robust

CAR of the banking sector remained stable at a high level. As of Apr-19, CAR & Tier-1 Capital was 23.78% & 21.98% respectively.

Risk-based capital (RBC) of the insurance industry slightly increased, well above the minimum threshold (120%).

Gearing ratio of multifinance companies was 2.82 times, providing ample room for future growth.Profitability of the banking sector was relatively stable.

Domestic financial institutions maintained a generally robust condition capital is steadily well above the minimum requirements, while profitability and leverage are still constantly at a sufficient level.

Source: Financial Service Authority (OJK)

23.7821.98

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

CAR Tier 1

4.87

2.42

1.0

2.0

3.0

4.0

5.0

6.0

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

%Net Interest Margin Return on Assets

2.82

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

437%

310%

200%

230%

260%

290%

320%

350%

350%

400%

450%

500%

550%

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

Life Insurance (Lhs) General Insurance (rhs)

30

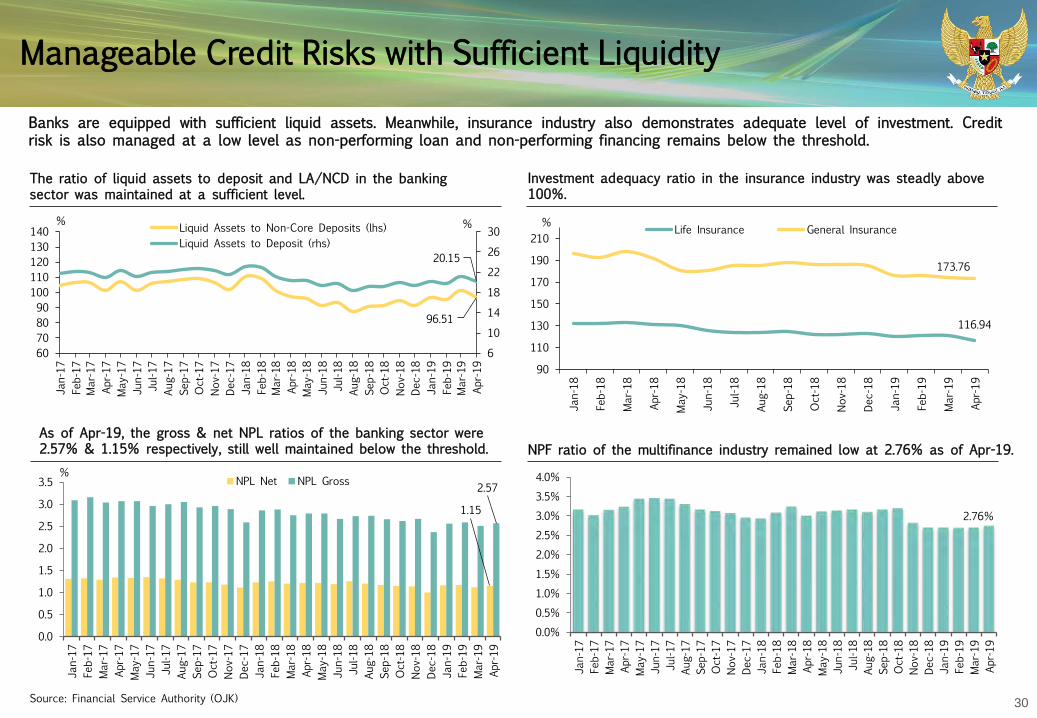

Manageable Credit Risks with Sufficient Liquidity

Banks are equipped with sufficient liquid assets. Meanwhile, insurance industry also demonstrates adequate level of investment. Creditrisk is also managed at a low level as non-performing loan and non-performing financing remains below the threshold.

The ratio of liquid assets to deposit and LA/NCD in the banking sector was maintained at a sufficient level.

As of Apr-19, the gross & net NPL ratios of the banking sector were 2.57% & 1.15% respectively, still well maintained below the threshold. NPF ratio of the multifinance industry remained low at 2.76% as of Apr-19.

Investment adequacy ratio in the insurance industry was steadly above 100%.

Source: Financial Service Authority (OJK)

96.51

20.15

6

10

14

18

22

26

30

60708090

100110120130140

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

%% Liquid Assets to Non-Core Deposits (lhs)Liquid Assets to Deposit (rhs)

1.15

2.57

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

%NPL Net NPL Gross

2.76%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

116.94

173.76

90

110

130

150

170

190

210

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

% Life Insurance General Insurance

31

Manageable Market Risks

Financial institutions’ risk profile are still manageable. Investment value of domestic institutional investors (mutual funds, insurers, andpension funds) is relatively stable, and the Net Open Position of Banks are maintained at a safe level.

Net open position in the banking sector kept far below the maximumlimit (20%).

The investment value of insurance & pension funds were still in increasing trend.

Multifinance companies’ exposures to foreign debt has generally been mitigated through company hedging measures.

Mutual funds’ net asset value (NAV) was at a steady level with lowvolatility.

Source: Financial Service Authority (OJK)

2.04

0

1

2

3

4

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

%

1072.1

268.2

200

225

250

275

300

800

850

900

950

1,000

1,050

1,100

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

IDR TnIDR Tn Insurance Pension Funds (rhs) 174.483

102.849

60

80

100

120

140

160

180

Jan-17

Feb-17

Mar-17

Apr-17

May

-17

Jun-17

Jul-1

7Au

g-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8Au

g-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

IDR tn

Domestic Debt Foreign Debt

5,0005,2005,4005,6005,8006,0006,2006,4006,6006,800

260290320350380410440470500530

Jul-1

8

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

May

-19

Jun-19

IDR Tn NAV Mutual Funds IDX (rhs)

32

Domestic Capital Markets Maintained Positive Growth

Capital markets is still growing despite the ongoing global pressure.

Source: Bloomberg, IBPA, Indonesia Stock Exchange, Ministry of Finance

Domestic capital markets performance is contracted, due to global pressure, but maintain to stabilize

Nonresident recorded net inflow in the market started from beginning of June 2019 after the public holiday

The IDX Stock Composite Index has maintained positive growth since early 2019

While government bond yields remains stable

Stock Index Performance 10 Jun 2019 (compared to 31 Dec’18)

3.1010.90

15.7611.73

13.285.59

-2.0814.36

7.763.89

6.701.54

2.876.45

12.44

-4 -2 0 2 4 6 8 10 12 14 16 18

TURKBRAZRUSAS

EUROJPNMALCHINPHILSINHKNINDO

KOREATHAI

WORLD

%

0.360

0.480

-40

-20

0

20

40

Jan-18

Feb-18

Mar-18

Apr-18

May

-18

Jun-18

Jul-1

8

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

May

-19

10 J

une-19

IDR Tn Gov't Debt Securities Equity

4,500

5,000

5,500

6,000

6,500

7,000

180

200

220

240

260

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

May

-19

Jun-19

Comp Bond Index Comp Stock Index (rhs)

13,000

13,500

14,000

14,500

15,000

15,500

5

6

7

8

9

10

Jul-1

8

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

May

-19

Jun-19

Yield (%)

5-yr Yield 10-yr Yield 20-yr Yield IDR (rhs)

33

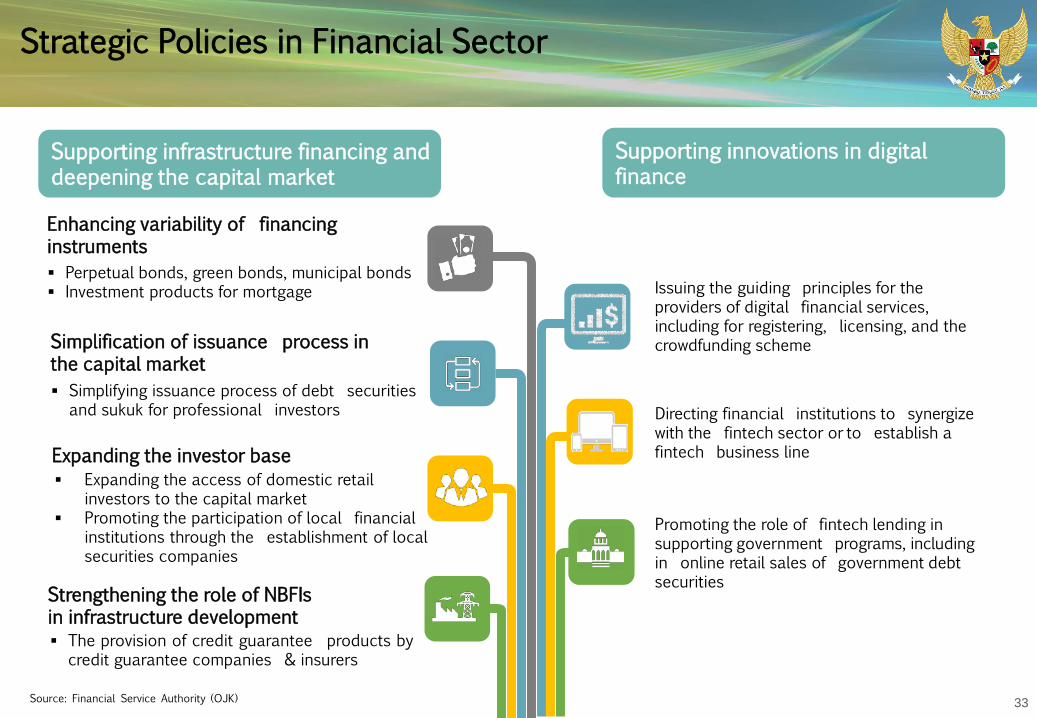

Strategic Policies in Financial Sector

Source: Financial Service Authority (OJK)

Supporting infrastructure financing anddeepening the capital market

Enhancing variability of financing instruments Perpetual bonds, green bonds, municipal bonds Investment products for mortgage

Simplification of issuance process in the capital market Simplifying issuance process of debt securities

and sukuk for professional investors

Expanding the investor base Expanding the access of domestic retail

investors to the capital market Promoting the participation of local financial

institutions through the establishment of local securities companies

Strengthening the role of NBFIsin infrastructure development The provision of credit guarantee products by

credit guarantee companies & insurers

Supporting innovations in digital finance

Issuing the guiding principles for the providers of digital financial services, including for registering, licensing, and the crowdfunding scheme

Directing financial institutions to synergize with the fintech sector or to establish a fintech business line

Promoting the role of fintech lending in supporting government programs, including in online retail sales of government debt securities

34

Strategic Policies in Financial SectorEnhancing financial literacy & inclusion

Source: Financial Service Authority (OJK), June 2017

OJK has also built a strong foundation for financial inclusion programs, to ensure access to financial products & services by Indonesians of all social classes. Such initiatives also include the enhancement of

financial literacy and financial consumer protection.

Developing financial education

models utilizing various delivery

channels

Enhancing the role of the “Investment

Alert Taskforce”

The result of OJK’s 2016 national survey demonstrated an improvement in financial literacy & inclusion among Indonesians compared to that of 2013, but there is still room for further improvement.

Financial Literacy

Financial Inclusion

21.8% 29.7%

2013 2016

59.7% 67.8%

2013 2016

Developing micro-credit products with additional

business support(“KUR Klaster”)

Promoting the establishment

of Islamic microfinance institutions (“Bank Wakaf

Mikro”)

Strengthening the role of

Financial Access Acceleration

Taskforce (TPAKD) in local areas

35

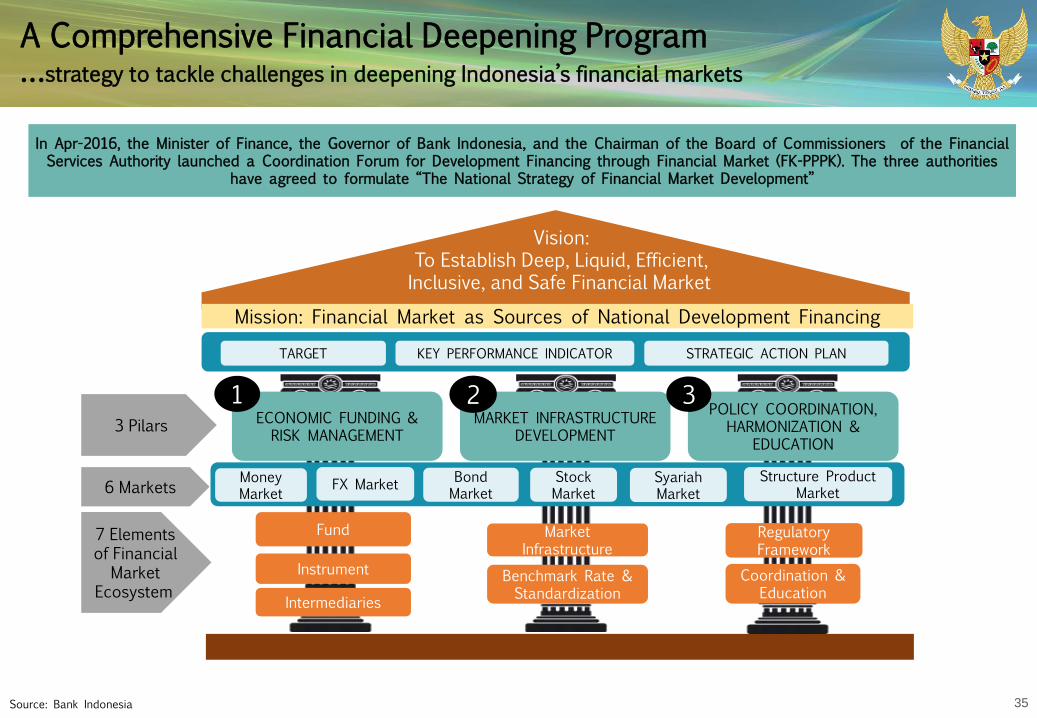

A Comprehensive Financial Deepening Program…strategy to tackle challenges in deepening Indonesia’s financial markets

Source: Bank Indonesia

In Apr-2016, the Minister of Finance, the Governor of Bank Indonesia, and the Chairman of the Board of Commissioners of the Financial Services Authority launched a Coordination Forum for Development Financing through Financial Market (FK-PPPK). The three authorities

have agreed to formulate “The National Strategy of Financial Market Development”

Vision: To Establish Deep, Liquid, Efficient, Inclusive, and Safe Financial Market

ECONOMIC FUNDING & RISK MANAGEMENT

MARKET INFRASTRUCTUREDEVELOPMENT

POLICY COORDINATION, HARMONIZATION &

EDUCATION

Benchmark Rate & Standardization

Instrument

Fund Regulatory Framework

Market Infrastructure

Intermediaries

Coordination & Education

Mission: Financial Market as Sources of National Development Financing

1 2 3

Money Market FX Market Bond

MarketStock Market

SyariahMarket

Structure Product Market

3 Pilars

6 Markets

7 Elements of Financial

Market Ecosystem

TARGET KEY PERFORMANCE INDICATOR STRATEGIC ACTION PLAN

36

Continuous Program on Capital Market Deepening…continuously strengthened, including through capital market deepening initiatives

Strengthening market infrastructure

Expansion of Single Investor Identification (SID) coverage Development of electronic trading platform (ETP) in the

debt market Development of Integrated Investment Management

System (S-INVEST) Enhancing the clearing and settlement process Enhancement of capital market data warehouse Development of Extensible Business Reporting Language

(XBRL) for issuers

Enhancing the supply-side

Simplification of public-offering requirements and procedures

Development of debt market Development of mutual fund industry Development of other products, including those to

support infrastructure development (private equity funds, REITs, ABS)

Development of Islamic capital market Development of municipal bonds

Enhancing the demand-side Strengthening governance

Development of market players’ capacity Enhancement of GCG for publicly-listed companies Development of repo regulations and infrastructure

Source: Financial Service Authority (OJK)

Enhancing the role of the domestic institutional investors (insurers & pension funds) in capital markets

Development of the domestic investor base (conducting investor education programs)

Expansion of distribution channels of market products

37

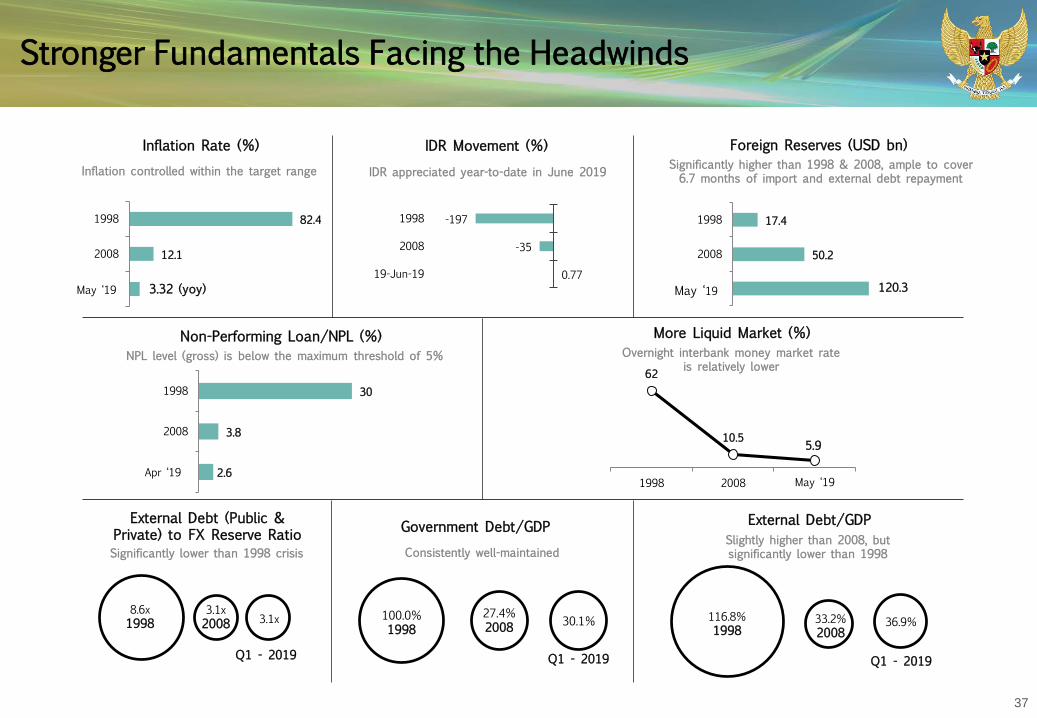

Stronger Fundamentals Facing the Headwinds

82.4

12.1

6.8

1998

2008

Sep-15

30

3.8

2.8

1998

2008

Aug-15

17.4

50.2

1998

2008

Sep-15

Inflation Rate (%) IDR Movement (%)

Non-Performing Loan/NPL (%)

Government Debt/GDP

Foreign Reserves (USD bn)

100.0%1998

27.4%2008 30.1%

Q1 - 2019

8.6x1998

3.1x2008 3.1x

Q1 - 2019

116.8%1998

33.2%2008

36.9%

Q1 - 2019

More Liquid Market (%)

External Debt (Public & Private) to FX Reserve Ratio

External Debt/GDP

Inflation controlled within the target range IDR appreciated year-to-date in June 2019

NPL level (gross) is below the maximum threshold of 5%

Consistently well-maintained

Significantly higher than 1998 & 2008, ample to cover 6.7 months of import and external debt repayment

Significantly lower than 1998 crisisSlightly higher than 2008, but significantly lower than 1998

May ‘19 120.3May ‘19 3.32 (yoy)

Apr ‘19 2.6

62

10.5 5.7

1998 2008 Jul-15

Overnight interbank money market rate is relatively lower

May ‘19

5.9

(ytd) 0.77

-35

-197

19-Jun-19

2008

1998

38

Outlook of Domestic Economy Remains Robust...domestic economic growth is predicted to be higher in 2019

2019 Economic Outlook

Bank Indonesia projects national economic growth in the 5.0-5.4% range in 2019, buoyed by domestic demand andimprovements in terms of net exports.

Bank Indonesia will consistently maintain price stability and strengthen policy coordination with the Central Government andLocal Administrations to maintain low and stable inflation, which is projected within the inflation target of 3.5±1% in 2019.

Bank Indonesia projects credit growth in 2019 at 10-12% (yoy), while predicting deposit growth in the 8-10% (yoy) range.Bank Indonesia will continue to monitor liquidity adequacy and distribution in the banking system in conjunction with theother relevant authorities consistent with efforts to help maintain financial system stability.

Economic Growth Inflation CAD (% of GDP) Credit Growth

Source : Bank Indonesia

2018Realization 5.17% 3.13% 2.98% 11.75%

2019 5.0–5.4 % 3.5±1% ±2.5% 10.0-12.0%

39

40