BANCASSURANCE IN THE REGION OF FORMER YUGOSLAVIA.

21

BANCASSURANCE IN THE REGION OF FORMER YUGOSLAVIA

-

Upload

gertrude-robertson -

Category

Documents

-

view

219 -

download

0

Transcript of BANCASSURANCE IN THE REGION OF FORMER YUGOSLAVIA.

BANCASSURANCEIN THE REGION OF

FORMER YUGOSLAVIA

Outline

1. Why bancassurance?

2. Market overview – Austria, Slovenia, Croatia, Serbia

3. Case studies – Serbia & Macedonia

4. Roadmap of bancassurance

5. Best practice

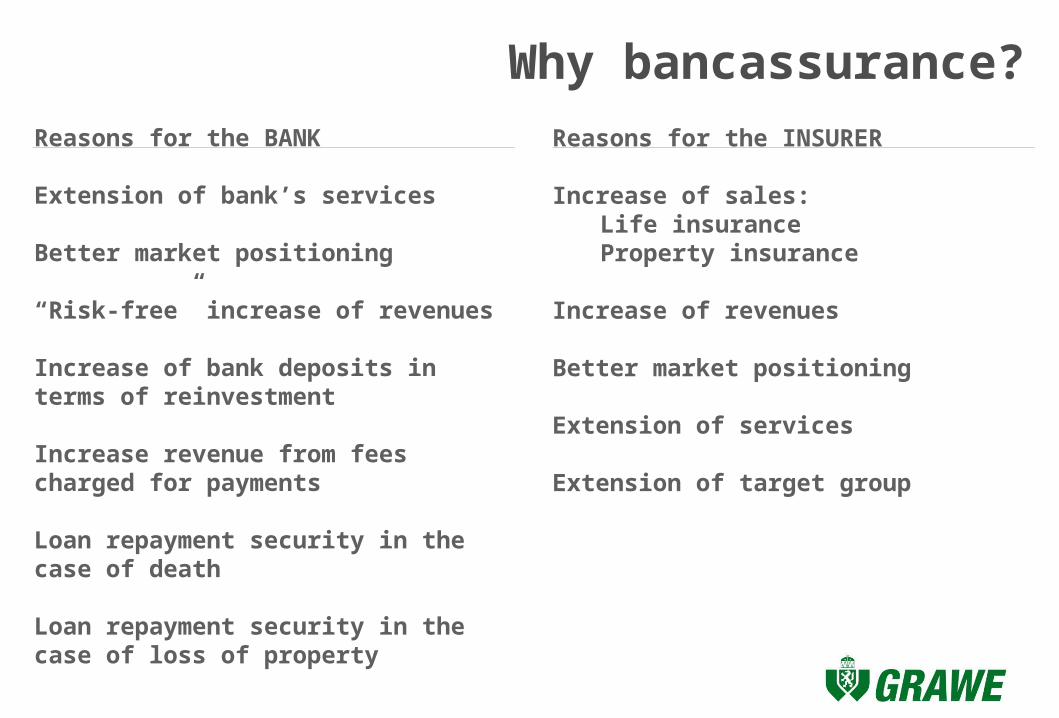

Why bancassurance?Reasons for the INSURER

Increase of sales: Life insurance Property insurance

Increase of revenues

Better market positioning

Extension of services

Extension of target group

Reasons for the BANK

Extension of bank’s services

Better market positioning

“Risk-free” increase of revenues

Increase of bank deposits in terms of reinvestment

Increase revenue from fees charged for payments

Loan repayment security in the case of death

Loan repayment security in the case of loss of property

AUSTRIA

Own sales network; 14.30%

Agencies; 2.70%

Brokers; 13.40%

Bankassurance; 64,80%

Other; 4.80%

Life InsuranceOwn sales network; 35.00%

Agencies; 12.80%Brokers;

39.40%

Bankassurance; 5,50%

Other; 7.30%

Non-life insurance

NON-LIFE MARKET

Group accident / Group health / Travel insuranceProperty – Home / Household insurance, SME

LIFE MARKET

CPI – Death, Permanent Total Disability , Temporarily Total DisabilityTraditional Life insurance – Endowment, Unit-linked + riders (primarily Accident)

SLOVENIA

Own sales network; 2.30%

Agencies; 60.30%Brokers; 9.60%

Bankassurance; 5,40%

Other; 22.40%

Life InsuranceOwn sales network; 27.90%

Agencies; 65.40%

Brokers; 4.60%

Bankassurance; 0,50%Other; 1.60%

Non-life insurance

LIFE MARKET

CPI – Death, Permanent Total Disability , Temporarily Total DisabilityTraditional Life insurance – Endowment, Unit-linked + riders (Accident, Dread Disease)

NON-LIFE MARKET

Group accident / Group health / Travel insuranceProperty – Home / Household insurance, SMECar – MTPL, Casco

CROATIA

Own sales network; 40.20%

Agencies; 41.60%

Brokers; 1.50%

Bankassurance; 16,10%

Other; 0.60%

Life Insurance

Own sales network; 72.40%

Agencies; 21.30%

Brokers; 2.20%

Bankassurance; 1,60% Other; 2.50%

Non-life insurance

NON-LIFE MARKET

Group accident / Group health / Travel insuranceUnemploymentProperty – Home / Household insurance, SMECar – MTPL, Casco

LIFE MARKET

CPI – Death, Permanent Total Disability , Temporarily Total DisabilityTraditional Life insurance – Endowment, Unit-linked + riders (Accident, Dread Disease)

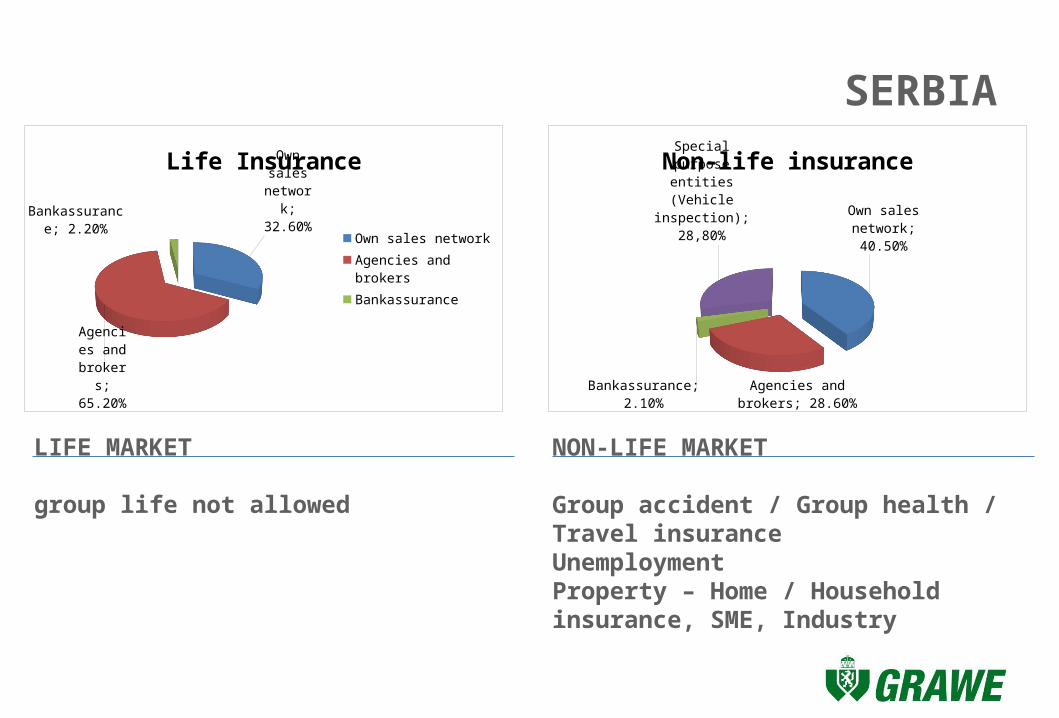

SERBIA

NON-LIFE MARKET

Group accident / Group health / Travel insuranceUnemploymentProperty – Home / Household insurance, SME, Industry

LIFE MARKET

group life not allowed

Own sales net-

work; 32.60%

Agencies and

brokers; 65.20%

Bankassurance; 2.20%

Life Insurance

Own sales networkAgencies and brokersBankassurance

Own sales network; 40.50%

Agencies and brokers; 28.60%

Bankassurance; 2.10%

Special purpose entities (Vehicle

inspection); 28,80%

Non-life insurance

CASE STUDIESSerbia & Macedonia

MacroeconomicsMACEDONIASERBIA

Population 7.181.505 (Census 2012)

Active populationEmployed

Around 2,200,000 Around 1,700,000

Number of unemployed 792,344

Average salary 385 EUR

Average pension 200 EUR

Average debt per capita 818 EUR

Average savings per capita Around 45 EUR per month

Number of banks 30

Number of insurance companies

28 (life and non-life)

Average insurance premium per capita

75.5 EUR

Average non-life insurance premium per capita

Around 60 EUR

Average life insurance premium per capita

Around 12 EUR

Population 2,045,262 (Census 2002)

Active population 637,855 (2011)

Number of unemployed 294,963Average salary 360 EURAverage pension 144 EURAverage debt per capita 650 EURAverage savings per capita Around 40 EUR per month

Number of banks 16 + 4 savings banksNumber of insurance companies

14

Average insurance premium per capita

56 EUR

Average non-life insurance premium per capita

Around 50 EUR

Average life insurance premium per capita

Around 5 EUR

Group Accident

Case Study - SERBIA

Serbia

Focus of the project group accidental insurance incl. death from sickness CPI for pensioners’ loans

partner OPPORTUNITY Bank, Novi Sad start of project: May 2011 Development of insured:

6-20

11

7-20

11

8-20

11

9-20

11

10-2

011

11-2

011

12-2

011

1-20

12

2-20

12

3-20

12

4-20

12

5-20

12

6-20

12

7-20

12

8-20

12

9-20

12

10-2

012

11-2

012

12-2

012

1-20

13

2-20

13

3-20

13

4-20

13

5-20

13

6-20

13

7-20

13

8-20

13

9-20

13

10-2

013

0

1000

2000

3000

4000

5000

6000

7000

Voditelj i član tima trebaju iste sposobnosti i vještine ?

Group LIFE

Case Study - MACEDONIA

Macedonia

Focus of the project group life insurance

Death from accident/sickness Permanent Total Disability Total and Irreversible Loss of Abilities

CPI for all sorts of loans partner OHRIDSKA BANKA SOCIETE GENERALE Bank, Skopje start of project: January 2013

January February March April May June July August September October November December0

50

100

150

200

250

RoadmapHIGH

involvment of sales force

training intensive

LOWinvolvment of

sales force„easy to sell“

LOWpremium /

commission margin

HIGHpremium /

commission margin

group accident / travel insurance

property / car / SME / UE

risk life

traditional lifeC

red

it p

rote

cti

on

Pa

ym

en

t p

rote

cti

on

Ad

dit

ion

to

De

po

sit

sC

ard

sO

ve

rdra

fts

Cre

dit

pro

tec

tio

nC

ard

s -

Assistance

Ad

dit

ion

to

de

po

sit

s

Cre

dit

pro

tec

tio

nK

ey

pe

rso

ns

in

SM

Es

Aff

lue

nt

cli

en

tsD

ep

os

its

Best practice

Technical Support

Sales Processes WEB-portal (info on products, application form data, premium calculation, health

questions, acceptance,…) Production reports (daily, weekly, monthly + specific campaigns) incorporation of premium calculation and underwriting (health

declaration/questionnaire) into bank‘s software and processes

Policy issuing process electronic data transfer bank-insurer (WEB-portal or incorporated software) underwriting with fast response rates – feed-back on acceptance policy issuing to bank and/or policyholder

Ongoing business processes payment procedures – standing orders/direct debit reminder/cancellation procedures

Sales Force Trainings and Support

Centralized and on-site trainings trainers provided by insurer advisors/mentors per branche office e-learning product trainings – hard skills sales skills trainings – soft skills expert trainings (claims handeling, prevention of cancellations/surrenders/…) dedicated sales trainings (e.g. best sellers club)

Call centers / Support centers claims handling clarification and conciliation for on-site questions by sellers or customers

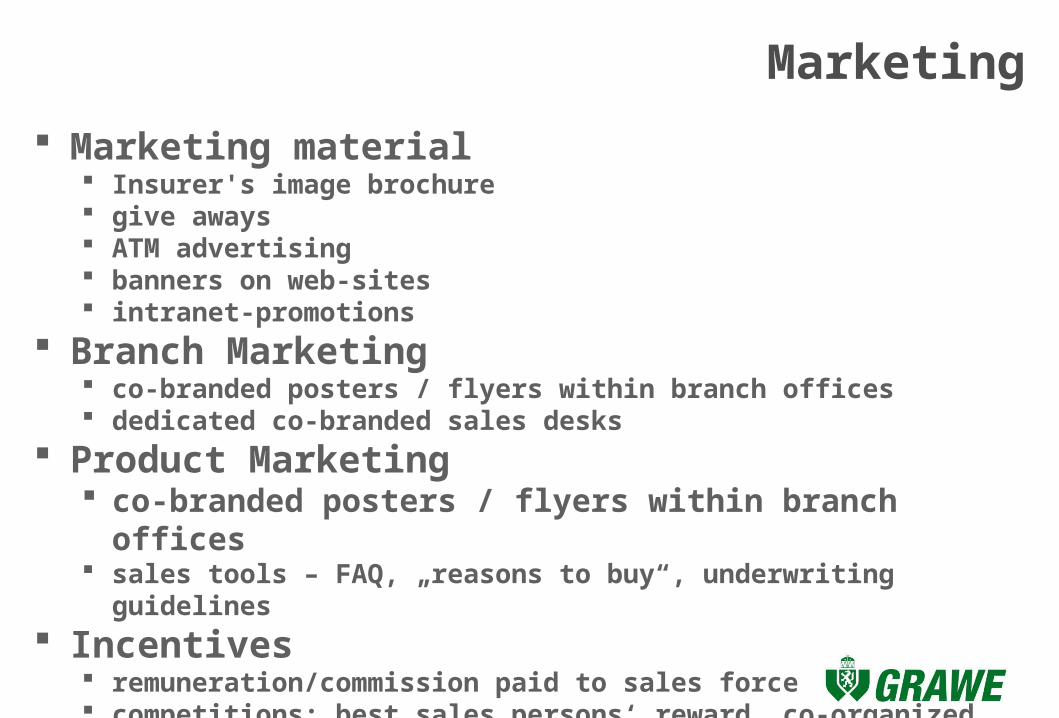

Marketing

Marketing material Insurer's image brochure give aways ATM advertising banners on web-sites intranet-promotions

Branch Marketing co-branded posters / flyers within branch offices dedicated co-branded sales desks

Product Marketing co-branded posters / flyers within branch offices sales tools – FAQ, „reasons to buy“, underwriting guidelines

Incentives remuneration/commission paid to sales force competitions: best sales persons‘ reward, co-organized events/trips

Side Business

Commission schemes clear definitions per product / product line

Incentives profit sharing bonus commission schemes

Bank to act as Depot bank for the respective investment portfolios

Premium collection / recommendation to insurers existing clients

BANCASSURANCEIN THE REGION OF

FORMER YUGOSLAVIA