bajaj_ppt (1)

15

CONCEPT OF WORKING CAPIT AL Working capital is the amount of capital that a business has available to meet the day- to-day cash requirements of its operations, or more specially, for financing the conversion of raw material into finished goods, which the company sells for payment. WORKING CAPIT AL MANAGEMENT It is concerned with the problem that arise in attempting to manage the current assets and liabilities and the inter relationship that exists between them.

-

Upload

manasa-murthy -

Category

Documents

-

view

216 -

download

0

Transcript of bajaj_ppt (1)

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 1/15

CONCEPT OF WORKING CAPITAL

Working capital is the amount of capital that a business has

available to meet the day- to-day cash requirements of itsoperations, or more specially, for financing the conversionof raw material into finished goods, which the companysells for payment.

WORKING CAPITAL MANAGEMENT

It is concerned with the problem that arise in attempting to

manage the current assets and liabilities and the inter relationship that exists between them.

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 2/15

CLASSIFICATION OF WORKING CAPITAL

WORKING CAPITAL

BASIS OF CONCEPT BASIS OF TIME

Grossworkingcapital

Networkingcapital

Permanent/fixed

workingcapital

Fluctuating/variableworkingcapital

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 3/15

Current ratio Current assets AZHAR

Current liabilities

It gives a picture about the companies ability to pay back its liabilities

with its short term assets. It can give a sense o efficiencyocompany¶s opearting cycle or its ability to turn product into cash.

PARTICULARS 2009 2010

CURRENT ASSETS 30284 23019

CURRENTLIABLITIES

24581 42812

CURRENT RATIO 1.23 0.53

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 4/15

QU ICK RATIO AZHAR

Also known as acid test ratio. It measures acompany¶s ability to meet short term obligations withits most liquid assets.

=current assets-stock (quick assets)

current liablities

PARTICULARS 2009 2010

Q UICK ASSETS 20863 38829

Q UICK LIABILITIES 24581 42812

Q UICK RATIO 0.84 0.90

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 5/15

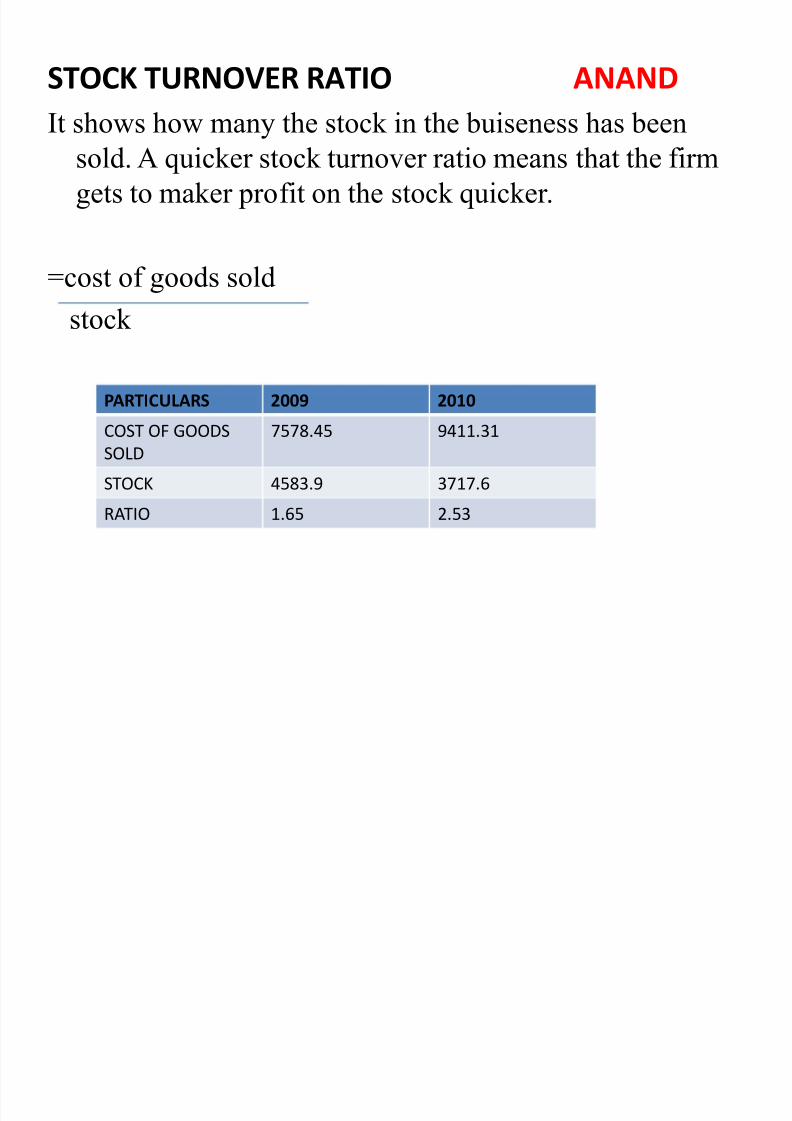

STOCK TURNOVER RATIO ANAND

It shows how many the stock in the buiseness has beensold. A quicker stock turnover ratio means that the firmgets to maker profit on the stock quicker.

=cost of goods soldstock

PARTICULARS 2009 2010

COST OF GOODSSOLD

7578.45 9411.31

STOCK 4583.9 3717.6

RATIO 1.65 2.53

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 6/15

DEBTORS TURNOVER RATIO ANAND

= average debtorsCredit sales/365

PARTCULARS 2009 2010

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 7/15

W ORKING CAPITAL TURNOVER RATIOMANSA

= Net salesNet working capital

PARTICULARS 2009 2010

NET SALES 84460 115431

NETW ORKINGCAPITAL

-1832 -12528

RATIO -4610 -9.16

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 8/15

OPERATING CYCLE MANSA

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 9/15

RAW MATERIAL HOLDING PERIOD RICHA

=360 days x stock of raw material

Cost of raw material

PARTICULARS 2009 2010

RAW MATERIALHOLDING PERIOD

83.53 47.35

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 10/15

W IP HOLDNG PERIOD RICHA=360 days x stock of W IP

Cost of goods manufactured

PARTICULARS 2009 2010

HOLDING PERIOD 19.57 42.85

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 11/15

DEBTORS COLLECTION PERIOD ROHAN

=360 days x debtorsCredit sales

PARTICULARS 2009 2010

COLLECTIONPERIOD

11.97 8.479

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 12/15

CREDITORS PAYMENT PERIOD ROHAN

360 DAYS X CREDITORSPurchases

PARTICULARS 2009 2010

HOLDING PERIOD 48.53 73.5

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 13/15

FINISHED GOODS HOLDING PERIOD DIVANSHU

360 X Stock of finished goodsCost of goods sold

PARTICULARS 2009 2010

HOLDING PERIOD 10.053 9.956

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 14/15

2009 2010

RM Conversion Period 83.53 47.35

-Creditors payment period 48.53 73.5

W IP Holding Period 19.57 46.76

FG Holding Period 10.053 9.956

Debtors Collection Period 11.97 8.479

76.59 39.03

MANAS

8/7/2019 bajaj_ppt (1)

http://slidepdf.com/reader/full/bajajppt-1 15/15

![[XLS]fmism.univ-guelma.dzfmism.univ-guelma.dz/sites/default/files/le fond... · Web view1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1](https://static.fdocuments.net/doc/165x107/5b9d17e509d3f2194e8d827e/xlsfmismuniv-fond-web-view1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1-1.jpg)