BAD DEBT PROVISIONS - IFRSbox – Making IFRS Easy · 1 Impairment of financial assets under IFRS 9...

5

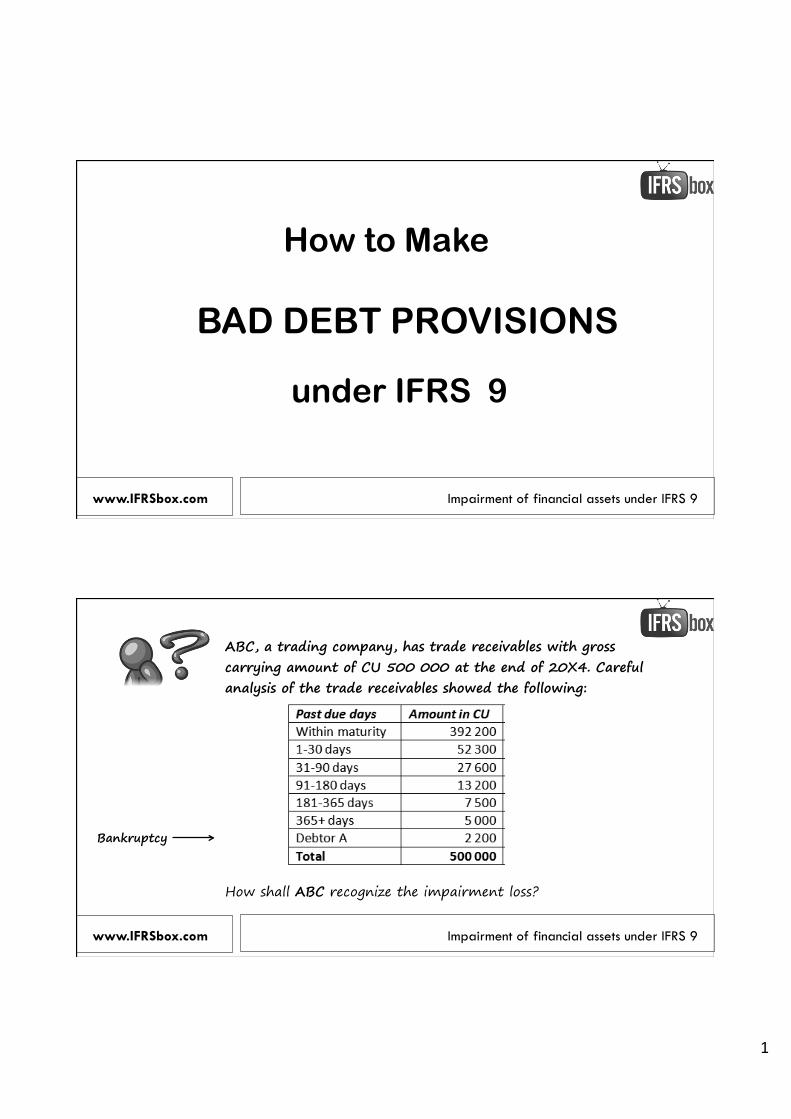

1 www.IFRSbox.com Impairment of financial assets under IFRS 9 How to Make BAD DEBT PROVISIONS under IFRS 9 www.IFRSbox.com Impairment of financial assets under IFRS 9 ABC, a trading company, has trade receivables with gross carrying amount of CU 500 000 at the end of 20X4. Careful analysis of the trade receivables showed the following: How shall ABC recognize the impairment loss? Bankruptcy

Transcript of BAD DEBT PROVISIONS - IFRSbox – Making IFRS Easy · 1 Impairment of financial assets under IFRS 9...

1

www.IFRSbox.com Impairment of financial assets under IFRS 9

How to Make

BAD DEBT PROVISIONS

under IFRS 9

www.IFRSbox.com Impairment of financial assets under IFRS 9

ABC, a trading company, has trade receivables with gross carrying amount of CU 500 000 at the end of 20X4. Careful analysis of the trade receivables showed the following:

How shall ABC recognize the impairment loss?

Bankruptcy

2

www.IFRSbox.com

IFRS 9 IAS 39

Choice until 1 January 2018

Impairment of financial assets under IFRS 9

Impairment of financial assets

Incurred credit loss Expected credit loss

www.IFRSbox.com Impairment of financial assets under IFRS 9

Bankruptcy

IAS 39 Incurred credit loss = CU 2 200

3

www.IFRSbox.com

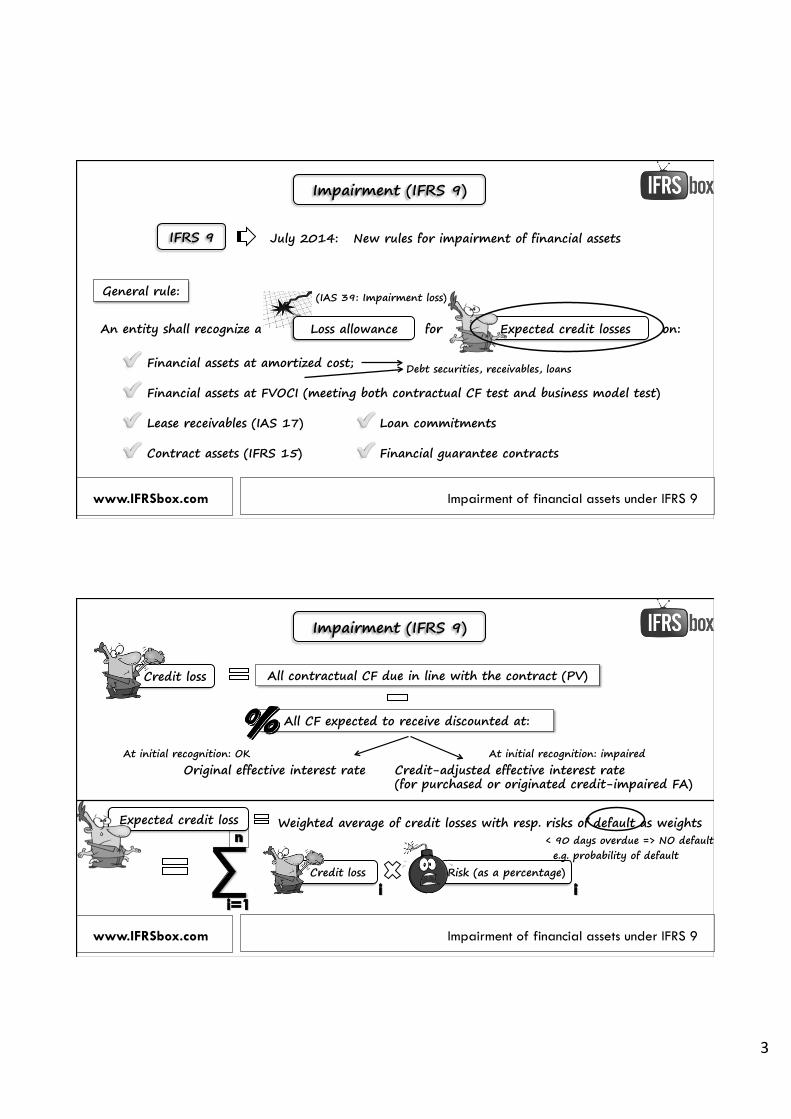

Impairment (IFRS 9)

IFRS 9 July 2014:

General rule:

An entity shall recognize a

(IAS 39: Impairment loss)

Financial assets at amortized cost;

Lease receivables (IAS 17)

Loss allowance

Loan commitments

New rules for impairment of financial assets

Contract assets (IFRS 15)

for Expected credit losses on:

Financial assets at FVOCI (meeting both contractual CF test and business model test)

Financial guarantee contracts

Debt securities, receivables, loans

Impairment of financial assets under IFRS 9

Risk (as a percentage)

www.IFRSbox.com

Impairment (IFRS 9)

All contractual CF due in line with the contract (PV)

Original effective interest rate

Credit loss

Weighted average of credit losses with resp. risks of default as weights Expected credit loss

At initial recognition: OK

All CF expected to receive discounted at:

Credit-adjusted effective interest rate (for purchased or originated credit-impaired FA)

At initial recognition: impaired

Credit loss e.g. probability of default

< 90 days overdue => NO default

Impairment of financial assets under IFRS 9

4

www.IFRSbox.com

Impairment (IFRS 9)

3 stages of FA

Trade receivables 12-month ECL

• Do NOT contain significant financing component

Life-time ECL

Lease receivables (IAS 17)

Simplified approach General approach

Contract assets (IFRS 15)

• Contain significant financing component, but chosen to measure loss allowance at lifetime ECL

• If chosen to measure loss allowance at lifetime ECL

No stage

= Life-time ECL

(Lots of assessment not necessary)

All financial assets subject to impairment

Loss allowance Loss allowance

Except for: Trade receivables or contract assets (IFRS 15) without significant financing component

Impairment of financial assets under IFRS 9

www.IFRSbox.com Impairment of financial assets under IFRS 9

Bankruptcy

IAS 39 Incurred credit loss

= CU 2 200

IFRS 9 Expected credit loss = CU 12 323

= CU 2 200

5

www.IFRSbox.com

The IFRS Kit

100 Video Lectures 130+ Case Studies

170+ Pages of Handouts

IFRS Quizzes “IFRS In 1 Day”

IFRS Conversion Course

ü

ü

ü ü

ü ü

Impairment of financial assets under IFRS 9