Back to the Future Part II - The Greater Cumberland...

41

By: Anirban Basu Sage Policy Group, Inc. September 4 th , 2014 Back to the Future Part II On Behalf of The Greater Cumberland Committee

Transcript of Back to the Future Part II - The Greater Cumberland...

By: Anirban Basu Sage Policy Group, Inc.

September 4th, 2014

Back to the Future Part II

On Behalf of

The Greater Cumberland Committee

Raging Bull (1980)

Estimated Growth in Output by Select Global Areas 2014 Projected*

2.4% 1.3%

2.0% 3.1%

5.4% 7.4%

6.4% 0.2%

2.8% 5.4%

4.7% 1.7%

2.2% 3.2%

1.6% 1.2%

0.3% 1.9%

0.7% 1.1%

1.8%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0%

Mexico Brazil

Latin America and Caribbean Middle East, North Africa, Afghanistan, & Pakistan

India** China

Developing Asia Russia

Central/eastern Europe Sub-Saharan Africa

Emerging/developing countries United States

Canada United Kingdom

Japan Spain

Italy Germany

France Euro area

Advanced economies

Annual % Change

Source: International Monetary Fund, July 2014 WEO Update

*The IMF’s global and regional growth figures for 2014 are based on new purchasing power parity (PPP)

weights derived from the recently released 2011 International Comparison Program survey (see box) and are not

comparable to the 2013 figures reported in the April 2014 WEO

**For India, data and forecasts are presented on a fiscal year basis and output growth is based on GDP at

market prices. Corresponding growth forecasts for GDP at factor cost are 5.4 percent for 2014.

Debt by Selected Country 2013 Estimates*

0.0 50.0 100.0 150.0 200.0 250.0

Saudi Arabia

Russia

China

Indonesia

South Africa

Mexico

Argentina

Brazil

India

Germany

Canada

United Kingdom

France

Spain

United States

Italy

Japan

General Government Gross Debt in Percent of GDP

*IMF Staff Estimates

Source: International Monetary Fund, April 2014 WEO

Rank Exchange Index % Change

4 Tokyo SE Nikkei 225 56.7%

2 Nasdaq NASDAQ Composite 38.3%

1 NYSE Group DJI A 26.5%

6 Frankfurt SE DAX 25.5%

8 Bolsa De Madrid Madrid General 21.4%

12 Swiss Exchange Swiss Market 20.2%

5 Euronext CAC 40 18.0%

10 BorsaItaliana FTSE MIB 16.6%

3 London SE FTSE 100 12.0%

9 TSX Group S&P TSX Composite 9.6%

11 Hong Kong Exchanges Hang Seng Index 2.9%

7 Shanghai SE Shanghai Composite -6.8%

Top 12 Stock Exchanges 2013 Growth*

Source: Yahoo! Finance

*Change from the 2012 close to the 2013 close.

S&P Select Sector Performance 12-Month Percent Change as of August 22, 2014

Source: Standard & Poor’s

0% 5% 10% 15% 20% 25% 30%

Telecommunication Services

Consumer Staples

Utilities

Financials

Consumer Discretionary

Energy

Industrials

Materials

Health Care

Information Technology

5.4%

12.2%

13.7%

15.3%

17.3%

19.0%

19.6%

22.9%

26.7%

29.2%

12-month percent change

Federal Reserve Balance Sheet v. S&P 500 Index May 2008 – August 2014*

Source: Federal Reserve Bank; Yahoo Finance

S&P 500 index depicted in orange

500

700

900

1100

1300

1500

1700

1900

2100

0.8

1.3

1.8

2.3

2.8

3.3

3.8

4.3

4.8

May

-08

Ju

l-0

8

Sep

-08

N

ov-

08

Ja

n-0

9

Mar

-09

M

ay-0

9

Jul-

09

S

ep-0

9

No

v-0

9

Jan

-10

M

ar-1

0

May

-10

Ju

l-10

S

ep-1

0

No

v-10

Ja

n-1

1 M

ar-1

1 M

ay-1

1 Ju

l-11

S

ep-1

1 N

ov-

11

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-12

Ja

n-1

3 M

ar-1

3 M

ay-1

3 Ju

l-13

S

ep-1

3 N

ov-

13

Jan

-14

M

ar-1

4

May

-14

Ju

l-14

S&P 500 FRB Credit Reserve $Trillions

*Through 8/27/2014

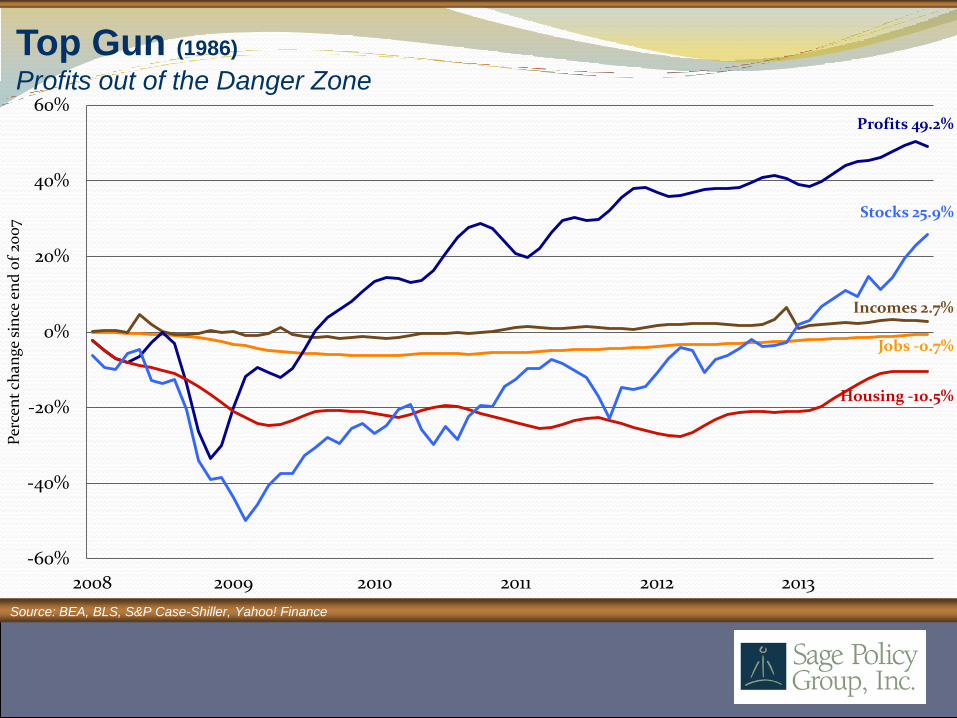

Jobs -0.7%

Incomes 2.7%

Profits 49.2%

Housing -10.5%

Stocks 25.9%

-60%

-40%

-20%

0%

20%

40%

60%

2008 2009 2010 2011 2012 2013

Per

cen

t ch

ange

sin

ce e

nd

of

200

7

Top Gun (1986)

Profits out of the Danger Zone

Source: BEA, BLS, S&P Case-Shiller, Yahoo! Finance

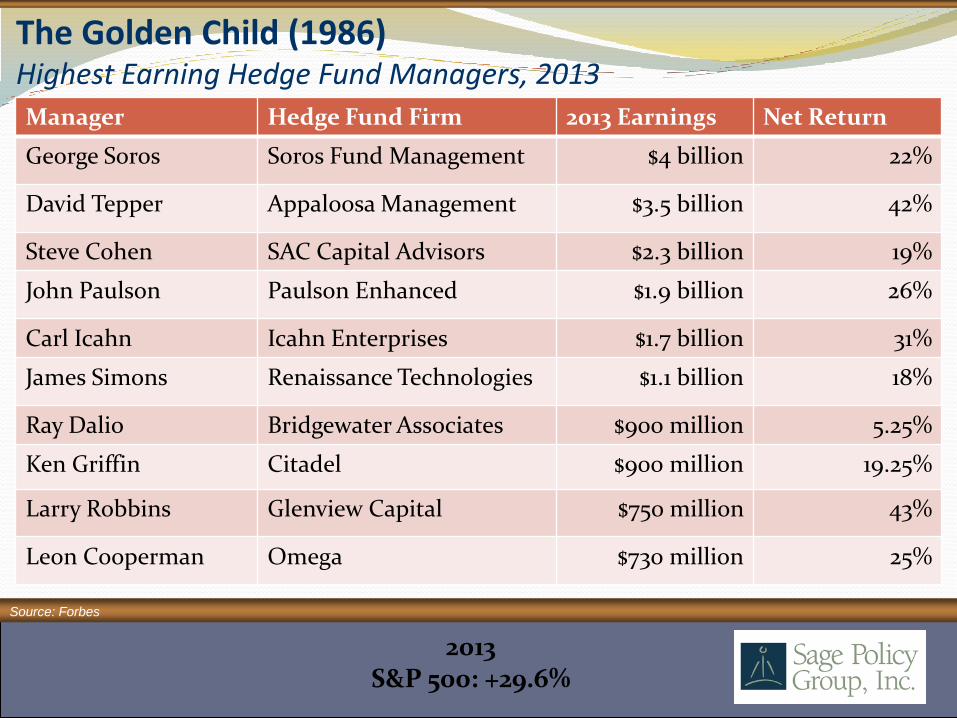

The Golden Child (1986) Highest Earning Hedge Fund Managers, 2013

Source: Forbes

Manager Hedge Fund Firm 2013 Earnings Net Return

George Soros Soros Fund Management $4 billion 22%

David Tepper Appaloosa Management $3.5 billion 42%

Steve Cohen SAC Capital Advisors $2.3 billion 19%

John Paulson Paulson Enhanced $1.9 billion 26%

Carl Icahn Icahn Enterprises $1.7 billion 31%

James Simons Renaissance Technologies $1.1 billion 18%

Ray Dalio Bridgewater Associates $900 million 5.25%

Ken Griffin Citadel $900 million 19.25%

Larry Robbins Glenview Capital $750 million 43%

Leon Cooperman Omega $730 million 25%

2013 S&P 500: +29.6%

Airplane! (1980) David Tepper’s Move against the Market

Source: Forbes, Bloomberg

2013 Appaloosa Management: +$3.5 billion (29.6%)

“Our big play versus the market is airlines. That’s a big play. We’re the biggest holder of all these different airlines. No hedge fund owned as many airlines as we did and not too many people did. Delta, UAL, LCC, US Air, AMR. We owned big percentages in all those stocks. And you know what, they did pretty good… pretty freaking good.” -David Tepper

Source: U.S. Bureau of Labor Statistics

Median Weekly Earnings, Full-Time U.S. Workers* 2000Q2 through 2014Q2

*SA, Constant 1982-1984 dollars (adjusted to CPI-U) Wage and salary workers ages 16+

$320

$325

$330

$335

$340

$345

$350

200

0Q

2

200

0Q

4

200

1Q2

200

1Q4

200

2Q2

200

2Q4

200

3Q2

200

3Q4

200

4Q

2

200

4Q

4

200

5Q2

200

5Q4

200

6Q

2

200

6Q

4

200

7Q2

200

7Q4

200

8Q

2

200

8Q

4

200

9Q

2

200

9Q

4

2010

Q2

2010

Q4

2011

Q2

2011

Q4

2012

Q2

2012

Q4

2013

Q2

2013

Q4

2014

Q2

Source: Moody’s Economy

Recession Watch as of May 2014

Industrial Production January 2001 through July 2014

Source: Federal Reserve

The industrial production index measures the real output of the manufacturing, mining, and electric and gas utilities industries.

80

85

90

95

100

105

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Ind

ex

(20

07

= 1

00

)

(Base year: 2007)

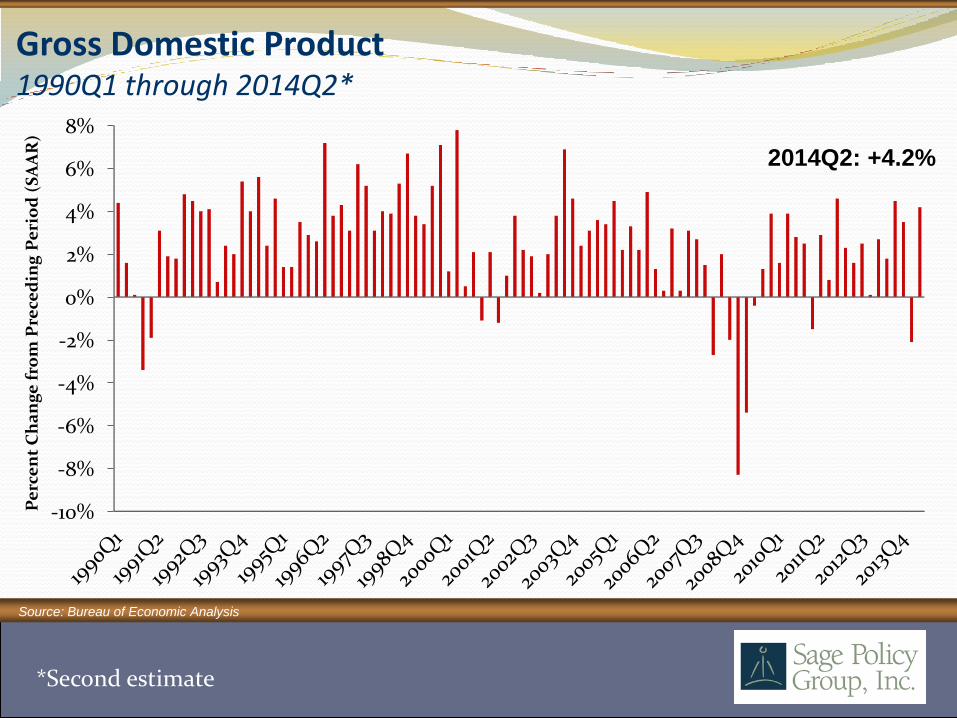

Gross Domestic Product 1990Q1 through 2014Q2*

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Pe

rce

nt

Ch

an

ge

fro

m P

rece

din

g P

eri

od

(S

AA

R)

2014Q2: +4.2%

Source: Bureau of Economic Analysis

*Second estimate

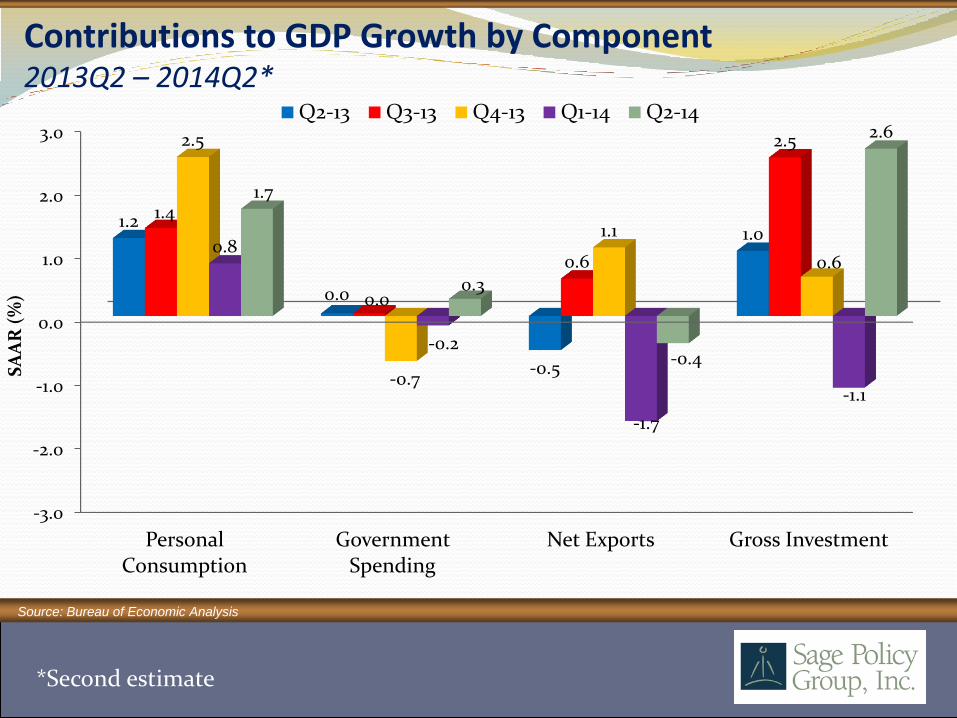

Contributions to GDP Growth by Component 2013Q2 – 2014Q2*

Source: Bureau of Economic Analysis

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Personal Consumption

Government Spending

Net Exports Gross Investment

1.2

0.0

-0.5

1.0 1.4

0.0

0.6

2.5 2.5

-0.7

1.1

0.6 0.8

-0.2

-1.7

-1.1

1.7

0.3

-0.4

2.6

SA

AR

(%

)

Q2-13 Q3-13 Q4-13 Q1-14 Q2-14

*Second estimate

Ordinary People (1980)

-1000

-800

-600

-400

-200

0

200

400

600 F

eb-0

2 Ju

n-0

2 O

ct-0

2 F

eb-0

3 Ju

n-0

3 O

ct-0

3 F

eb-0

4

Jun

-04

O

ct-0

4

Feb

-05

Jun

-05

Oct

-05

Feb

-06

Ju

n-0

6

Oct

-06

F

eb-0

7 Ju

n-0

7 O

ct-0

7 F

eb-0

8

Jun

-08

O

ct-0

8

Feb

-09

Ju

n-0

9

Oct

-09

F

eb-1

0

Jun

-10

O

ct-1

0

Feb

-11

Jun

-11

Oct

-11

Feb

-12

Jun

-12

Oct

-12

Feb

-13

Jun

-13

Oct

-13

Feb

-14

Ju

n-1

4

Th

ou

san

ds

Source: U.S. Bureau of Labor Statistics

July 2014: +209K

Net Change in U.S. Jobs, BLS January 2002 through July 2014

National Nonfarm Employment by Industry Sector July 2013 v. July 2014

-31

48

49

50

91

178

211

375

375

576

648

-200 0 200 400 600 800

Information

Other Services

Mining and Logging

Financial Activities

Government

Manufacturing

Construction

Education and Health Services

Leisure and Hospitality

Trade, Transportation, and Utilities

Professional and Business Services

Thousands, SA

All told 2,570K Jobs gained

Source: U.S. Bureau of Labor Statistics

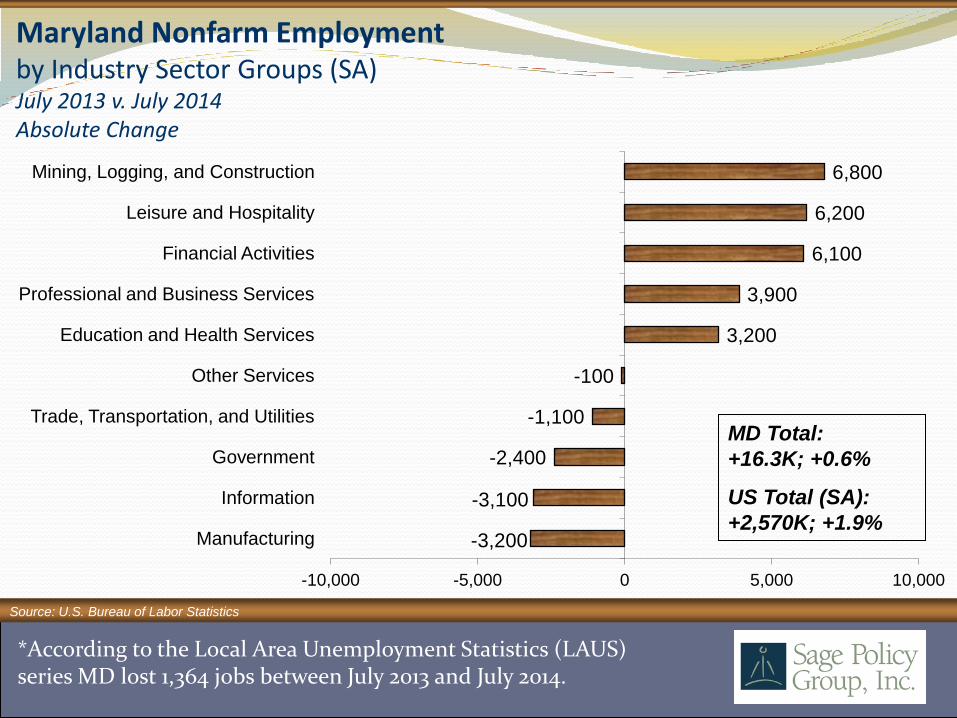

Maryland Nonfarm Employment by Industry Sector Groups (SA) July 2013 v. July 2014 Absolute Change

-3,200

-3,100

-2,400

-1,100

-100

3,200

3,900

6,100

6,200

6,800

-10,000 -5,000 0 5,000 10,000

Manufacturing

Information

Government

Trade, Transportation, and Utilities

Other Services

Education and Health Services

Professional and Business Services

Financial Activities

Leisure and Hospitality

Mining, Logging, and Construction

MD Total:

+16.3K; +0.6%

US Total (SA):

+2,570K; +1.9%

*According to the Local Area Unemployment Statistics (LAUS) series MD lost 1,364 jobs between July 2013 and July 2014.

Source: U.S. Bureau of Labor Statistics

-4,100

-3,800

-2,000

2,100

2,500

3,900

5,600

6,900

13,200

14,500

15,300

-6,000 -1,000 4,000 9,000 14,000

Manufacturing

Information

Government

Mining and Logging

Other Services

Financial Activities

Professional and Business Services

Leisure and Hospitality

Education and Health Services

Trade, Transportation, and Utilities

Construction

Pennsylvania Nonfarm Employment by Industry Sector Groups (NSA) July 2013 v. July 2014 Absolute Change

PA Total (SA):

+54.1K; +0.9%

US Total (SA):

+2,570K; +1.9%

Source: U.S. Bureau of Labor Statistics

-2,200

-2,000

-800

100

200

600

700

1,100

1,900

3,500

4,600

-4,000 -2,000 0 2,000 4,000 6,000

Government

Construction

Trade, Transportation, and Utilities

Other Services

Information

Education and Health Services

Manufacturing

Mining and Logging

Financial Activities

Leisure and Hospitality

Professional and Business Services

West Virginia Nonfarm Employment by Industry Sector Groups (NSA) July 2013 v. July 2014 Absolute Change

WV Total (SA):

+7.7K; +1.0%

US Total (SA):

+2,570K; +1.9%

Source: U.S. Bureau of Labor Statistics

U.S. Year-over-year Percent Change: 1.9%

Employment Growth, U.S. States (SA) July 2013 v. July 2014 Percent Change

RANK STATE % RANK STATE % RANK STATE %

1 NORTH DAKOTA 4.4 18 OKLAHOMA 1.8 31 SOUTH DAKOTA 1.1

2 NEVADA 3.8 19 GEORGIA 1.7 36 KANSAS 1.0

3 UTAH 3.6 19 SOUTH CAROLINA 1.7 36 WEST VIRGINIA 1.0

4 TEXAS 3.5 21 LOUISIANA 1.6 38 PENNSYLVANIA 0.9

5 COLORADO 2.7 21 MINNESOTA 1.6 39 ALABAMA 0.8

5 DELAWARE 2.7 21 WISCONSIN 1.6 39 HAWAII 0.8

5 FLORIDA 2.7 24 KENTUCKY 1.4 39 WYOMING 0.8

8 OREGON 2.6 24 MICHIGAN 1.4 42 VERMONT 0.7

9 ARIZONA 2.4 26 ARKANSAS 1.3 43 CONNECTICUT 0.6

10 WASHINGTON 2.3 26 NEW YORK 1.3 43 ILLINOIS 0.6

11 INDIANA 2.2 28 MAINE 1.2 43 MARYLAND 0.6

11 NORTH CAROLINA 2.2 28 NEW HAMPSHIRE 1.2 43 VIRGINIA 0.6

13 CALIFORNIA 2.1 28 RHODE ISLAND 1.2 47 OHIO 0.5

14 MASSACHUSETTS 2.0 31 DISTRICT OF COLUMBIA 1.1 48 NEBRASKA 0.3

14 MISSOURI 2.0 31 IDAHO 1.1 48 NEW JERSEY 0.3

14 MONTANA 2.0 31 IOWA 1.1 48 NEW MEXICO 0.3

17 TENNESSEE 1.9 31 MISSISSIPPI 1.1 51 ALASKA -0.7

Source: U.S. Bureau of Labor Statistics

U.S. Unemployment Rate: 6.2%

Unemployment Rates, U.S. States (SA) July 2014 RANK STATE % RANK STATE % RANK STATE %

1 NORTH DAKOTA 2.8 17 VIRGINIA 5.4 32 NORTH CAROLINA 6.5

2 NEBRASKA 3.6 19 MAINE 5.5 36 CONNECTICUT 6.6

2 UTAH 3.6 20 MASSACHUSETTS 5.6 36 NEW MEXICO 6.6

4 SOUTH DAKOTA 3.7 20 WASHINGTON 5.6 36 NEW YORK 6.6

4 VERMONT 3.7 22 OHIO 5.7 39 ILLINOIS 6.8

6 HAWAII 4.4 22 PENNSYLVANIA 5.7 40 OREGON 6.9

6 NEW HAMPSHIRE 4.4 22 SOUTH CAROLINA 5.7 41 ALABAMA 7.0

6 WYOMING 4.4 25 WISCONSIN 5.8 41 ARIZONA 7.0

9 IOWA 4.5 26 INDIANA 5.9 43 TENNESSEE 7.1

9 MINNESOTA 4.5 27 MARYLAND 6.1 44 CALIFORNIA 7.4

11 MONTANA 4.6 28 ARKANSAS 6.2 44 DISTRICT OF COLUMBIA 7.4

11 OKLAHOMA 4.6 28 DELAWARE 6.2 44 KENTUCKY 7.4

13 IDAHO 4.8 28 FLORIDA 6.2 47 MICHIGAN 7.7

14 KANSAS 4.9 31 WEST VIRGINIA 6.3 47 NEVADA 7.7

15 TEXAS 5.1 32 ALASKA 6.5 47 RHODE ISLAND 7.7

16 COLORADO 5.3 32 MISSOURI 6.5 50 GEORGIA 7.8

17 LOUISIANA 5.4 32 NEW JERSEY 6.5 51 MISSISSIPPI 8.0 Source: U.S. Bureau of Labor Statistics

Unemployment Rates, 20 Largest Metros (NSA) July 2014

Rank MSA UR Rank MSA UR

1 Minneapolis-St. Paul-Bloomington, MN-WI Metropolitan Statistical Area 4.2 11

Philadelphia-Camden-Wilmington, PA-NJ-DE-MD Metropolitan Statistical Area 6.7

2 Seattle-Tacoma-Bellevue, WA Metropolitan Statistical Area 5.2 12

Chicago-Joliet-Naperville, IL-IN-WI Metropolitan Statistical Area 6.8

3 Washington-Arlington-Alexandria, DC-VA-MD-WV Metropolitan Statistical Area 5.4 12

Tampa-St. Petersburg-Clearwater, FL Metropolitan Statistical Area 6.8

4 Boston-Cambridge-Quincy, MA-NH Metropolitan NECTA 5.5 14

Baltimore-Towson, MD Metropolitan Statistical Area 6.9

4 Dallas-Fort Worth-Arlington, TX Metropolitan Statistical Area 5.5 15

New York-Northern New Jersey-Long Island, NY-NJ-PA Metropolitan Statistical Area 7.0

4 Houston-Sugar Land-Baytown, TX Metropolitan Statistical Area 5.5 16

St. Louis, MO-IL Metropolitan Statistical Area 7.1

7 San Francisco-Oakland-Fremont, CA Metropolitan Statistical Area 5.7 17

Atlanta-Sandy Springs-Marietta, GA Metropolitan Statistical Area 8.0

8 Phoenix-Mesa-Glendale, AZ Metropolitan Statistical Area 6.3 17

Los Angeles-Long Beach-Santa Ana, CA Metropolitan Statistical Area 8.0

9 Miami-Fort Lauderdale-Pompano Beach, FL Metropolitan Statistical Area 6.4 19

Riverside-San Bernardino-Ontario, CA Metropolitan Statistical Area 9.2

10 San Diego-Carlsbad-San Marcos, CA Metropolitan Statistical Area 6.6 20

Detroit-Warren-Livonia, MI Metropolitan Statistical Area 9.8

Source: U.S. Bureau of Labor Statistics

MD County Unemployment Rates July 2014

Rank Jurisdiction UR Rank Jurisdiction UR

1 Montgomery County 5.1 11 Kent County 6.5

2 Howard County 5.2 14 Cecil County 6.6

3 Queen Anne's County 5.5 15 Baltimore County 6.7

4 Frederick County 5.6 16 Prince George's County 6.9

5 Carroll County 5.8 17 Worcester County 7.0

6 Talbot County 5.9 18 Caroline County 7.2

7 Anne Arundel County 6.0 19 Washington County 7.4

8 Calvert County 6.1 20 Allegany County 7.5

9 St. Mary's County 6.3 21 Wicomico County 7.7

10 Garrett County 6.4 22 Dorchester County 8.7

11 Charles County 6.5 23 Somerset County 9.8

11 Harford County 6.5 24 Baltimore City 9.9

Source: U.S. Bureau of Labor Statistics

Source: U.S. Bureau of Labor Statistics

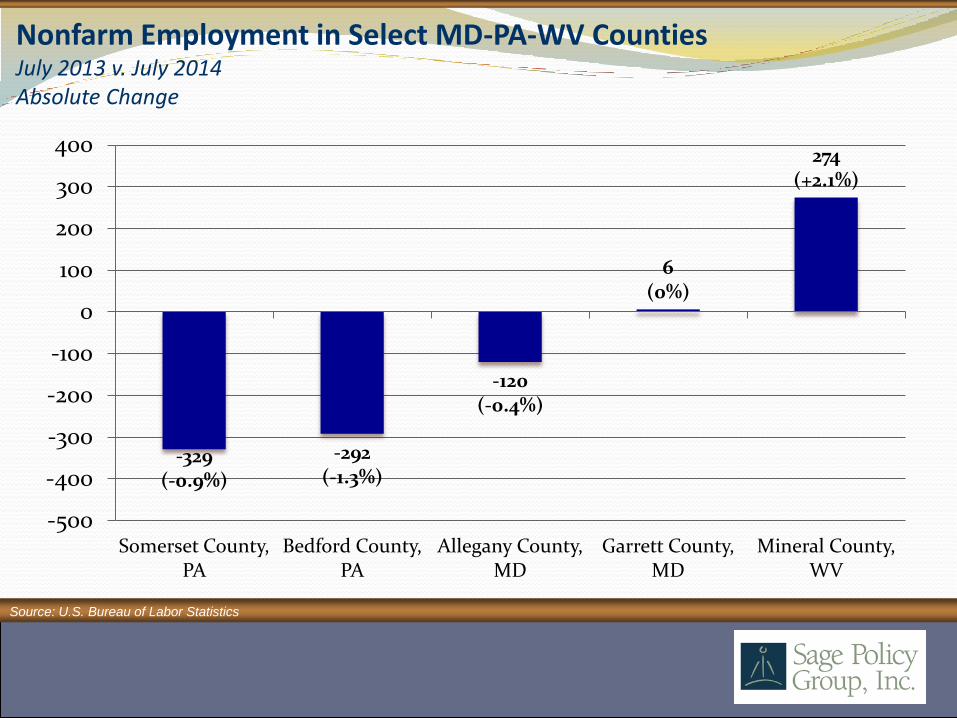

-329 (-0.9%)

-292 (-1.3%)

-120 (-0.4%)

6 (0%)

274 (+2.1%)

-500

-400

-300

-200

-100

0

100

200

300

400

Somerset County, PA

Bedford County, PA

Allegany County, MD

Garrett County, MD

Mineral County, WV

Nonfarm Employment in Select MD-PA-WV Counties July 2013 v. July 2014 Absolute Change

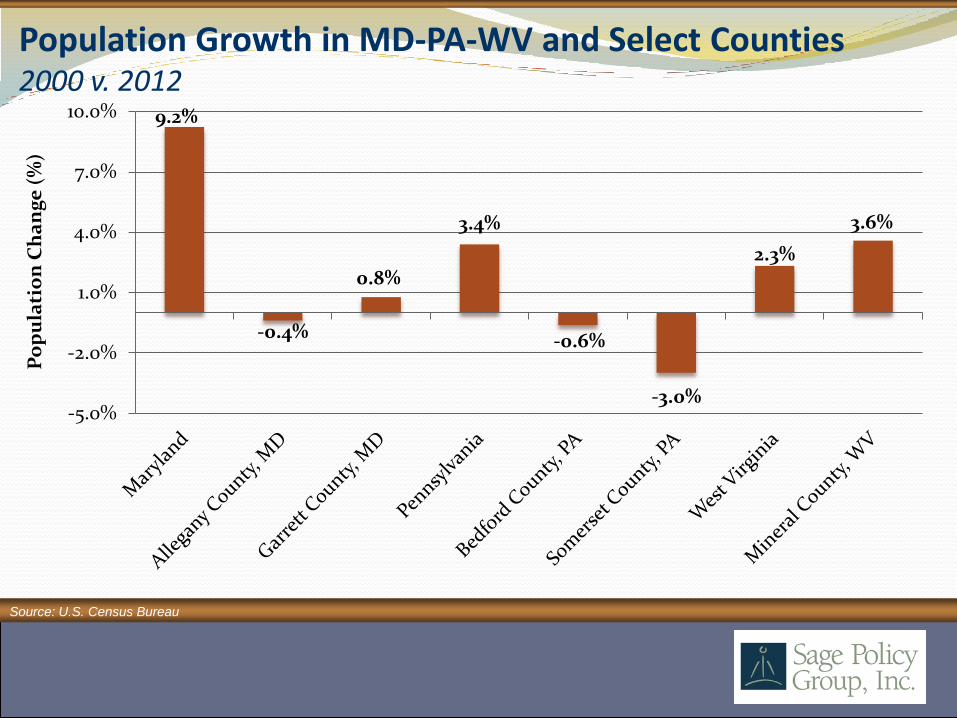

Population Growth in MD-PA-WV and Select Counties 2000 v. 2012

Source: U.S. Census Bureau

9.2%

-0.4%

0.8%

3.4%

-0.6%

-3.0%

2.3%

3.6%

-5.0%

-2.0%

1.0%

4.0%

7.0%

10.0%

Po

pu

lati

on

Ch

an

ge

(%

)

Unemployment Rates in Select MD-PA-WV Counties June 2009 through July 2014

5

6

7

8

9

10

11

12

13

14

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Allegany County, MD Garrett County, MD Bedford County, PA Somerset County, PA Mineral County, WV

Source: U.S. Bureau of Labor Statistics

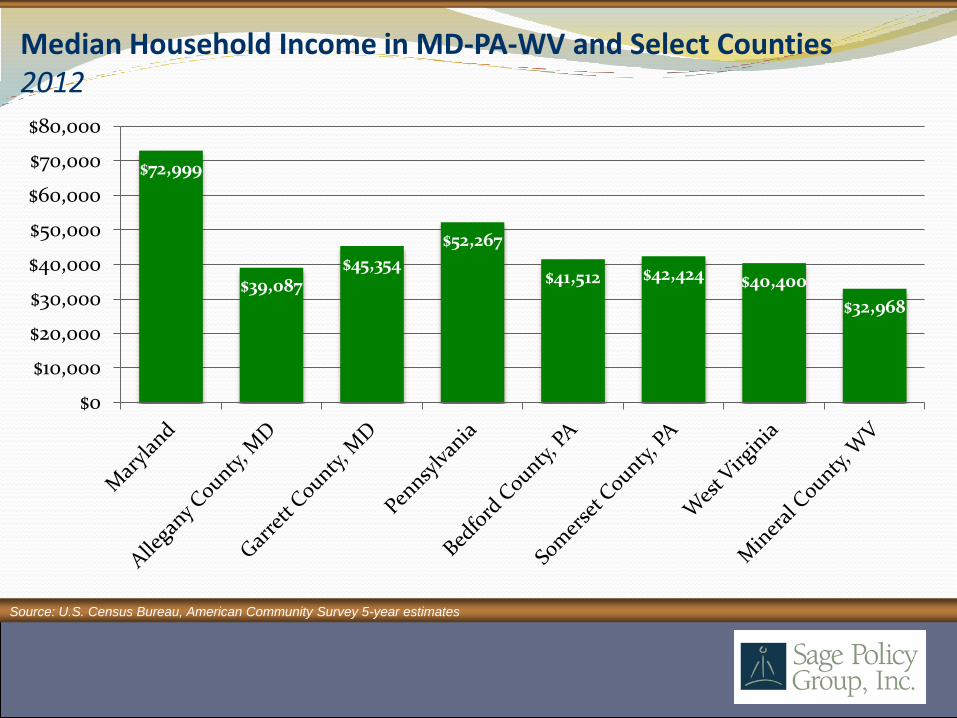

Median Household Income in MD-PA-WV and Select Counties 2012

Source: U.S. Census Bureau, American Community Survey 5-year estimates

$72,999

$39,087 $45,354

$52,267

$41,512 $42,424 $40,400

$32,968

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

Field of Dreams (1989)

15-Year & 30-Year Fixed Mortgage Rates February 1995 through August 2014*

Source: Freddie Mac

3.23%

4.10%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Feb

-95

Au

g-9

5

Feb

-96

A

ug

-96

Feb

-97

Au

g-9

7

Feb

-98

A

ug

-98

Feb

-99

A

ug

-99

Feb

-00

A

ug

-00

Feb

-01

Au

g-0

1

Feb

-02

Au

g-0

2

Feb

-03

Au

g-0

3 Feb

-04

A

ug

-04

Feb

-05

Au

g-0

5

Feb

-06

A

ug

-06

Fe

b-0

7 A

ug

-07

Feb

-08

A

ug

-08

Feb

-09

A

ug

-09

Feb

-10

A

ug

-10

Feb

-11

Au

g-1

1

Feb

-12

Au

g-1

2

Feb

-13

Au

g-1

3

Feb

-14

A

ug

-14

Rat

e

15-yr 30-yr

*Week ending 8/21/2014

U.S. New Home Sales January 1999 through July 2014

Source: U.S. Census Bureau

July 2014 412K

0

200

400

600

800

1,000

1,200

1,400

1,600

Th

ou

san

ds,

SA

AR

U.S. Housing Starts January 1999 through July 2014

Source: U.S. Census Bureau

0

500

1,000

1,500

2,000

2,500

Jan

-99

Jul-

99

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Th

ou

san

ds,

SA

AR

1 Unit 5 units or more

July 2014: 1 Unit: 656K 5 Units or more: 423K

U.S. Housing Building Permits January 1999 through July 2014

Source: U.S. Census Bureau

0

500

1,000

1,500

2,000

2,500

Jan

-99

Jul-

99

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Th

ou

san

ds,

SA

AR

1 Unit 5 units or more

July 2014: 1 Unit: 640K 5 Units or more: 382K

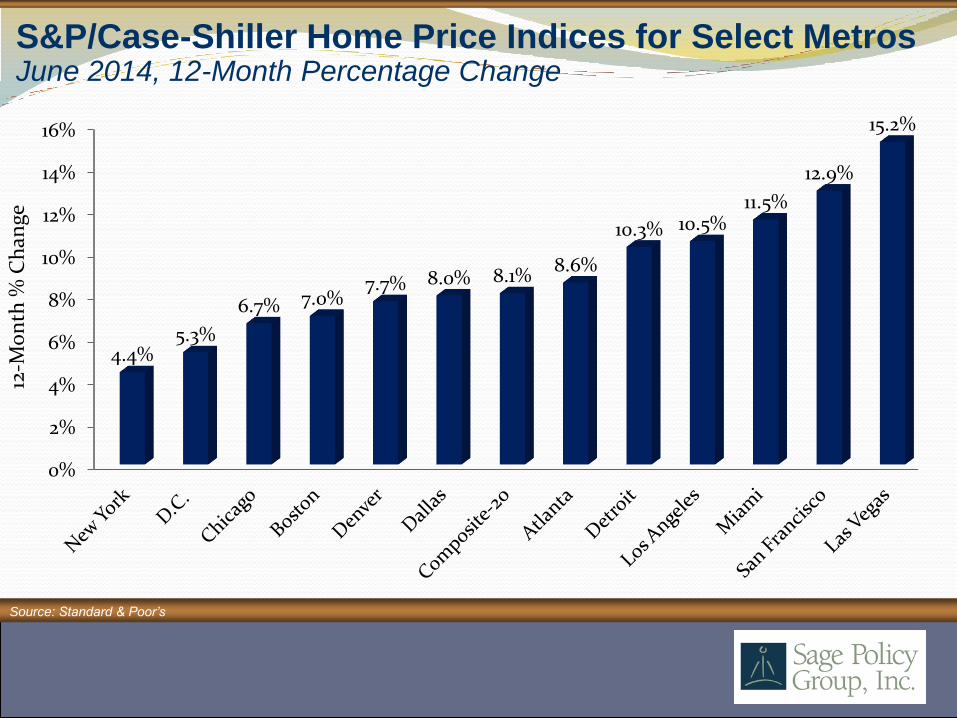

0%

2%

4%

6%

8%

10%

12%

14%

16%

4.4% 5.3%

6.7% 7.0% 7.7% 8.0% 8.1%

8.6%

10.3% 10.5% 11.5%

12.9%

15.2%

12-M

on

th %

Ch

ange

S&P/Case-Shiller Home Price Indices for Select Metros June 2014, 12-Month Percentage Change

Source: Standard & Poor’s

The Shining (1980)

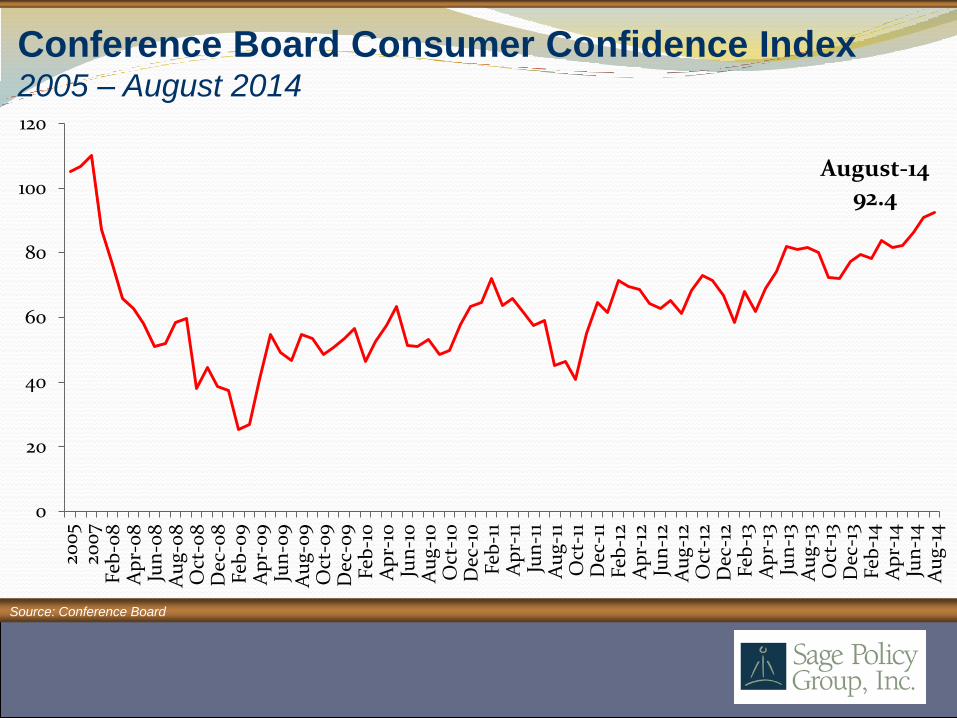

August-14 92.4

0

20

40

60

80

100

120

200

5 20

07

Feb

-08

A

pr-

08

Ju

n-0

8

Au

g-0

8

Oct

-08

D

ec-0

8

Feb

-09

A

pr-

09

Ju

n-0

9

Au

g-0

9

Oct

-09

D

ec-0

9

Feb

-10

A

pr-

10

Jun

-10

A

ug

-10

O

ct-1

0

Dec

-10

F

eb-1

1 A

pr-

11

Jun

-11

Au

g-1

1 O

ct-1

1 D

ec-1

1 F

eb-1

2 A

pr-

12

Jun

-12

Au

g-1

2 O

ct-1

2 D

ec-1

2 F

eb-1

3 A

pr-

13

Jun

-13

Au

g-1

3 O

ct-1

3 D

ec-1

3 F

eb-1

4

Ap

r-14

Ju

n-1

4

Au

g-1

4

Conference Board Consumer Confidence Index 2005 – August 2014

Source: Conference Board

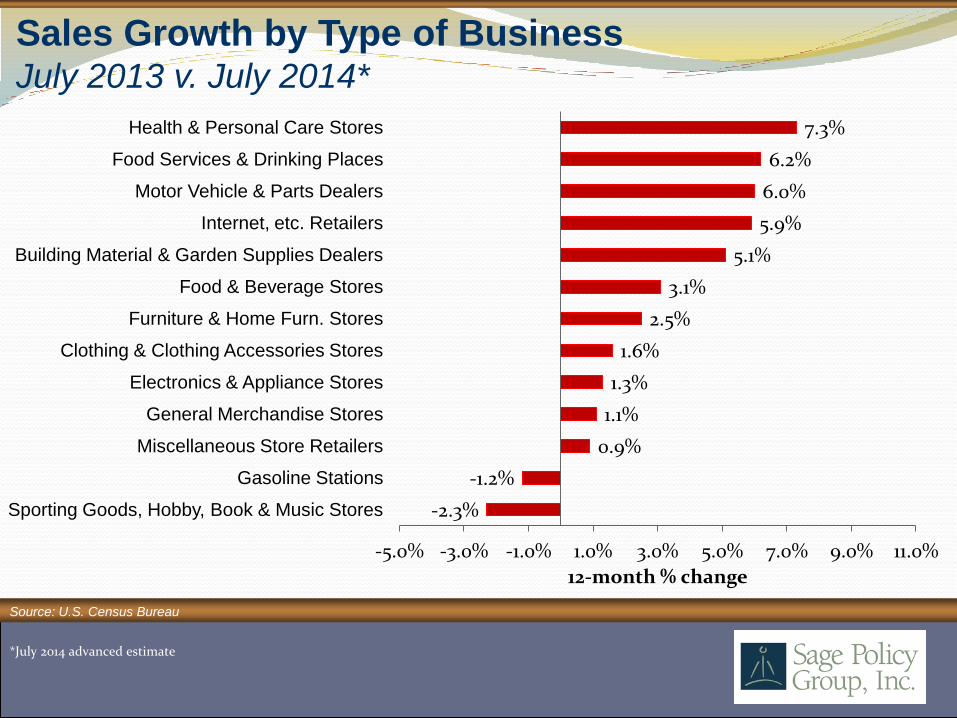

-2.3%

-1.2%

0.9%

1.1%

1.3%

1.6%

2.5%

3.1%

5.1%

5.9%

6.0%

6.2%

7.3%

-5.0% -3.0% -1.0% 1.0% 3.0% 5.0% 7.0% 9.0% 11.0%

Sporting Goods, Hobby, Book & Music Stores

Gasoline Stations

Miscellaneous Store Retailers

General Merchandise Stores

Electronics & Appliance Stores

Clothing & Clothing Accessories Stores

Furniture & Home Furn. Stores

Food & Beverage Stores

Building Material & Garden Supplies Dealers

Internet, etc. Retailers

Motor Vehicle & Parts Dealers

Food Services & Drinking Places

Health & Personal Care Stores

12-month % change

Sales Growth by Type of Business July 2013 v. July 2014*

Source: U.S. Census Bureau

*July 2014 advanced estimate

Conference Board Leading Economic Indicators Index August 2007 through July 2014

Source: Conference Board

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5% A

ug

-07

No

v-0

7

Feb

-08

May

-08

Au

g-0

8

No

v-0

8

Feb

-09

May

-09

Au

g-0

9

No

v-0

9

Feb

-10

May

-10

Au

g-1

0

No

v-10

Feb

-11

May

-11

Au

g-1

1

No

v-11

Feb

-12

May

-12

Au

g-1

2

No

v-12

Feb

-13

May

-13

Au

g-1

3

No

v-13

Feb

-14

May

-14

On

e-m

on

th P

erc

en

t C

ha

ng

e

July 2014 = 103.3 where 2004=100

Coming to America (1988)

• Nationally, we are likely approaching the peak of the business cycle;

• Tailwinds include booming stock market, lower gasoline prices, stabilizing global economy, and consumer expenditures on interest rate sensitive durable goods like autos;

• The current year is associated with greater certainty regarding federal budgeting and monetary policy – that helps;

• The world is not perfect - black swan threats remain: (1) Iran (2) Israel/Iran (3) Europe (4) contagion (5) cyber (6) EMP;

• Longer term question is how do we increase incomes and family stability in the Greater Cumberland area?; &

• Regions with rapid population growth and/or significant import/export activity, industrial output and energy production will lead the way.

Thank You

Follow us on Twitter @SagePolicyGroup

You can always reach me at [email protected]

Please look for updates of information at www.sagepolicy.com.

Also, if you need us in a hurry, we are at 410.522.7243 (410.522.SAGE)

Please contact us when you require economic research & policy analysis.