![The Avoyelles pelican (Marksville, La.) 1861-03-16 [p ]](https://static.fdocuments.net/doc/165x107/61b2de373d764509cf5afdfe/the-avoyelles-pelican-marksville-la-1861-03-16-p-.jpg)

Avoyelles Parish Sheriff -...

47

RECEIVED i AT»VF AUDITOR -2 PHI2:38 AVOYELLES PARISH SHERIFF Marksville, Louisiana Financial Report Year Ended June 30,2007 Under provisions of state law, this report is a public document. Acopy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of fhe parish clerk of court. Release Date I

Transcript of Avoyelles Parish Sheriff -...

RECEIVEDi AT»VF AUDITOR

-2 PHI2:38

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Financial Report

Year Ended June 30,2007

Under provisions of state law, this report is a publicdocument. Acopy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of fhe parish clerk of court.

Release Date I

TABLE OF CONTENTS

Page

Independent Auditors' Report 1-2

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTS (GWFS)Statement of net assets 5Statement of activities 6

FUND FINANCIAL STATEMENTS (FFS)Balance sheet - governmental funds 9Reconciliation of the governmental funds balance sheet

to the statement of net assets 10Statement of revenues, expenditures, and changes in fund balances -

governmental funds 11Reconciliation of the statement of revenues, expenditures, and changes in

fund balances of governmental funds to the statement of activities 12Statement of fiduciary net assets and liabilities 13

Notes to financial statements 14-29

REQUIRED SUPPLEMENTARY INFORMATION

General Fund:Budgetary comparison schedule 31

Sales Tax Special Revenue Fund:Budgetary comparison schedule 32

OTHER SUPPLEMENTARY INFORMATION

General Fund:Budgetary comparison - schedule of expenditures 34-35

Sales Tax Special Revenue Fund:Budgetary comparison - schedule of expenditures 36

Agency Funds:Combining statement of fiduciary assets and liabilities 38Combining statement of changes in assets and liabilities 39-40

Tax Collector Agency Fund -Statement of collections, distributions, and unsettled balances 41

COMPLIANCE AND INTERNAL CONTROL

Report on Compliance and on Internal Control OverFinancial Reporting Based on an Audit of FinancialStatements Performed in Accordance withGovernment Auditing Standards 43-44

Summary schedule of current and prior year audit findingsand corrective action plan 45

KOLDER, CHAMPAGNE, SLAVEN & COMPANY, LLCC. Burton Kolder, CPA*Russell F. Champagne, CPA*Victor R. Slaven, CPA"P. Troy Courville, CPA*Gerald A. Thibodeaux, Jr., CPA*Robert S. Carter, CPA*Arthur R. Mixon, CPA*

CERTIFIED PUBLIC ACCOUNTANTS OFFICES

Tynes E. Mixon, Jr., CPAAllan J. LaBry, CPAAlbert R. Leger, CPA.PFS.CSA*Penny Angelle Scruggins, CPAChristine L. Cousin, CPAMary T. Thibodeaux, CPAMarshall W. Guidry, CPAAlan M. Taylor, CPAJames R. Roy, CPARobert J. Melz, CPAKelly M. Doucet, CPACheryl L. Bartley, CPA. CVAMandy B. Self. CPAPaul L. Delcambre, Jr. CPA

183 South Beadle Rd.Lafayette, LA 70508

Phone (337) 232-4141Fax (337) 232-8660

113 East Bridge St. 133 East Waddiil St.Breaux Bridge, LA 70517 Marksville, LA 71351Phone (337) 332-4020 Phone (318) 253-9252Fax (337) 332-2867 Fax (318) 253-8681

Retired:Conrad O. Chapman. CPA* 2006Harry J. Clostio, CPA 2007

1234 David Or. Ste 203Morgan City, LA 70380Phone (985) 384-2020Fax (985) 384-3020

332 West Sixth AvenueObertin, LA 70655Phone (337) 639-4737Fax (337) 639-4568

450 East Main StreetNew Iberia, LA 70560Phone (337) 367-9204Fax (337) 367-9208

408 West Cotton StreetVilla Plane, LA 70566

Phone (337) 363-2792Fax (337) 363-3049

200 South Main StreetAbbeville, LA 70510

Phone (337) 893-7944Fax (337) 893-7946

1013 Main StreetFranklin. LA 70538

Phone (337) 828-0272Fax (337) 828-0290

• A Professional Accounting Corporation

WEB SITE;WWW.KCSRCPAS.COM

INDEPENDENT AUDITORS1 REPORT

The Honorable Bill BeltAvoyelles Parish SheriffMarksville, Louisiana

We have audited the accompanying financial statements of the governmental activities, each majorfund, and the aggregate remaining fund information of the Avoyelles Parish Sheriff as of and for the yearended June 30,2007, which collectively comprise the Sheriffs basic financial statements as listed in the tableof contents. These financial statements are the responsibility of the Avoyelles Parish Sheriff. Ourresponsibility is to express opinions on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government Auditing Standards.issued by the Comptroller General of the United States. Those standards require that we plan and perform theaudit to obtain reasonable assurance about whether the financial statements are free of material misstatement.An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financialstatements. An audit also includes assessing the accounting principles used and significant estimates made bymanagement, as well as evaluating the overall financial statement presentation. We believe that our auditprovides a reasonable basis for our opinions.

In our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, each major fund, and the aggregate remainingfund information of the Avoyelles Parish Sheriff as of June 30, 2007, and the respective changes in financialposition for the year then ended, in conformity with accounting principles generally accepted in the UnitedStates of America.

In accordance with Government Auditing Standards, we have also issued a report dated December 20,2007, on our consideration of the Avoyelles Parish Sheriffs internal control over financial reporting and ourtests of its compliance with certain laws, regulations, contracts and grant agreements and other matters. Thepurpose of that report is to describe the scope of our testing of internal control over financial reporting and theresults of that testing and not to provide an opinion on the internal control over financial reporting or oncompliance. That report is an integral part of an audit performed in accordance with Government AuditingStandards and should be considered in assessing the results of our audit.

Member of:AMERICAN INSTITUTE OFCERTIFIED PUBLIC ACCOUNTANTS

Member of:SOCIETY OF LOUISIANA

CERTIFIED PUBLIC ACCOUNTANTS

The required supplementary information on pages 31 and 32 are not a required part of the basicfinancial statements but are supplementary information required by the accounting principles generallyaccepted in the United States of America. We have applied certain limited procedures, which consistedprincipally of inquiries of management regarding the methods of measurement and presentation of therequired supplementary information. However, we did not audit the information and express no opinion on it.

The Avoyelles Parish Sheriff has not presented management's discussion and analysis that theGovernmental Accounting Standards Board has determined is necessary to supplement, although not requiredto be a part of, the basic financial statements.

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise the Sheriffs basic financial statements. The other supplementary information on pages34 through 45 is presented for purposes of additional analysis and is not a required part of the basic financialstatements. Such information has been subjected to the auditing procedures applied in the audit of the basicfinancial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financialstatements taken as a whole.

Kolder, Champagne, Sloven & Company, LLCCertified Public Accountants

Lafayette, LouisianaDecember 20, 2007

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDEFINANCIAL STATEMENTS (GWFS)

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Statement of Net AssetsJune 30, 2007

ASSETS

Cash and interest-bearing depositsCash with paying agentReceivablesDue from other governmental unitsInventoryOther assetsCapital assets:

LandCapital assets, net

Total assets

Accounts and other accrued payablesInterest payableLong-term liabilities:

Due within one yearDue after one year

Total liabilities

LIABILITIES

NET ASSETS

Invested in capital assets, net of related debtRestrictedUnrestricted

Total net assets

2006

$ 418,102161,53560,600

1,036,12053,1466,098

174,4005,216,090

7,126,091

1,700,81424,249

165,0001,422,383

3,312,446

3,803,107296,838(286,300)

$3,813,645

The accompanying notes are an integral part of the basic financial statements.

5

13C

S" C

W ^

O- rm oo

OO

(N

^ in^o m

cs

m oo oo<N ro XO

'o o\ oCN oo

r-o

o

1c/3Ww5

OY

EL

LE

S P

/

><

1'3oJ

Mar

ksvi

lle,

£'•C3e»H

Sta

tem

ent o

CO

Cej>0)

e(-* cd

mu

»-»T3

<L>•awsiSI

</)bfl 13 §.S S '-§-+-» ™ 3cd M o

§ c/*s I-. CO rt O

^^

>nTJ-i—*p*"in

inT^-i— <^^*nm

& w

OQ

I|

8 88 gp

u

CAU

1 ItS

r-" 'ooo"

m" TJ-"O oo

m"

^

•* 1

ooo"

oo

oo"00

m"€/*

:ven

ues:

T3cwO

O

M 2O OH

<L>cubo

A"3

ecd

O

u

O

bfl S

C °-r "-SH T5J -2

u3CU

uI-H

8 8 iucubo

(JJ r—l

§ 3^ O

*5 H

Oc•s1

o0

oo(N

O

CAcd

II(A'rt•r*Q

.31

isej

T3

• ^*

• 2ocd

1u

ii>§O

*£CO(A

O

•S3OH

U

&0(2O

|toU(-(us

5oH

D-13

§oc

.S

ooocd

FUND FINANCIAL STATEMENTS (FFS)

MAJOR FUND DESCRIPTIONS

General Fund

To account for resources traditionally associated with governments which are not required to be accountedfor in another fund.

Special Revenue Fund

1994 Sales Tax FundTo account for the receipt and use of proceeds of the Sheriffs 1994 one-half percent sales and use tax.These taxes are dedicated to the following purposes: establishing, acquiring, constructing, improving,maintaining, staffing and operating equipment and facilities necessary to provide enhanced 911 emergencytelephone, ambulance, dispatch and other services for the benefit of the residents of the Parish.

Debt Service Funds

Sales Tax Bond Sinking and ReserveTo accumulate monies for repayment of the $1,460,000 Sales Tax Bonds, Series 2004, interest due semi-annually at 4.0 to 6.5 percent. Payments are derived from the one-half cent sales and use tax approved bythe voters on November 19, 1992.

Certificate of Indebtedness, Series 1999To accumulate monies for payment of the $800,000 Certificates of Indebtedness, Series 1999, due in annualinstallments, plus interest, through maturity in 2009. Payments are derived from the one-half cent sales anduse tax approved by the voters on November 19,1992.

Capital Projects FundTo account for the purchase of capital assets using a portion of the proceeds of the $1,460,000 Sales TaxBonds, Series 2004.

(N ino f>~H V)

0 OC-l O1 °.vO Om in

VO OO«*• ON

O O

SO t-» OOTf OO Tf-.00

oo

,o ONw V ONS J 2 fS

r*i"

Ov(N

ON

fA

2 3cd

ONON

-*t

&e

oo

3

o o

in(N

Oo"»n

ON ^-(N r^

5o00ON"OO

taQz<

[LIT

IES

aJ

COO

s

1

u3cd>%cd&|3

Ouo<

•3ptS1-*u•5o2u3Q

_IU

;§3^

i

d ba

„ 4>

.§ &s'o«3

£rt1>

1*ed*oT3Sb

Su1t-i<a

T3u&u«tu&

(/)•4-41•o(U&0>enU

*

'ed&

g.tH

«sT3U

£u&0up^

.topwID

*S

•rfU

&<L>CA

S

3

£

,-Mcd

•a

I

•Sa•§3-i3

&

O0

f11Ooocd<u

s

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Reconciliation of the Governmental Funds Balance Sheetto the Statement of Net Assets

June 30, 2007

Total fund balances for governmental funds at June 30, 2007

Total net assets reported for governmental activities in the statement of netassets is different because:

Capital assets used in governmental activities are not financial resourcesand, therefore, are not reported in the funds. Those assets consist of:

LandBuildings and improvements, net of $1,360,368 accumulated depreciationEquipment and furniture, net of $1,662,065 accumulated depreciationVehicles, net of $671,396 accumulated depreciation

Long-term liabilities at June 30, 2007:

Certificates of indebtedness payableSales tax bonds payableAccrued interest payable

Total net assets of governmental activities at June 30, 2007

$ 34,787

$ 174,4004,337,580418,024460,486 5,390,490

$ (285,000)(1,302,383)(24,249) (1,611,632)

$3,813,645

The accompanying notes are an integral part of the basic financial statements.

10

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Statement of Revenues, Expenditures, and Changes in Fund Balances •Governmental Funds

Year Ended June 30, 2007

Revenues:Ad valorem taxesSales taxesIntergovernmental revenues -

State grants:State revenue sharing (net)State supplemental payOther

Fees, charges, and commissionsfor services -

Civil and criminalFeeding and keeping prisoners

Miscellaneous -Indian affairsInterest incomeOther

Total revenues

Expenditures:Current -

Public safety:Personal services and related

benefitsOperating servicesOperations and maintenance

Debt service -PrincipalInterest and fiscal charges

Capital outlayTotal expenditures

Excess (deficiency) ofrevenues over expenditures

Other financing sources (uses):Transfers inTransfers out

Total other financing sources(uses)

Excess (deficiency) of revenuesand other sources overexpenditures and other uses

Fund balances, beginning

Fund balances (deficit), ending

General

$ 558,611

120,699175,74826,923

344,8598,062,496

381,397450

1,767,68911,438,872

7,310,1541,357,2123,693,846

89,12410,773

136,58412,597,693

(1,158,821)

857,514

857,514

(301,307)

3,286

$ (298,021)

Certificates of1994 Sales Tax Indebtedness

Sales Tax Bonds Series 1999

s - s - s -1,696,193 168,000 7,182

-

-

,

.8,185 1,203

12,7791,708,972 176,185 8,385

443,87049,434

281,525

70,000 90,00060,006 16,632

71,385846,214 130,006 106,632

862,758 46,179 (98,247)

(857,514)

(857,514)

5,244 46,179 (98,247)

5,977 271,279 101,876

$ 11,221 S 317,458 S 3,629

CapitalProjects Total

S - S 558,6111,871,375

120,699175,74826,923

344,8598,062,496

381,3979,838

1,780,46813,332,414

7,754,0241,406,6463,975,371

249,12487,411

207,96913,680,545

(348,131)

857,514(857,514)

(348,131)

500 382,918

$ 500 $ 34,787

The accompanying notes are an integral part of the basic financial statements.

11

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Reconciliation of the Statement of Revenues, Expenditures, andChanges in Fund Balances of Governmental Funds

to the Statement of ActivitiesYear Ended June 30, 2007

Total net changes in fund balances at June 30, 2007 perStatement of Revenues, Expenditures and Changes in Fund Balances $ (348,131)

The change in net assets reported for governmental activities in thestatement of activities is different because:

Governmental funds report capital outlays as expenditures. However,in the statement of activities, the cost of those assets is allocated overtheir estimated useful lives and reported as depreciation expense.

Capital outlay which is considered expenditures on Statementof Revenues, Expenditures and Changes in Fund Balances $ 184,705

Depreciation expense for the year ended June 30, 2007 (342,505) (157,800)

Bond principal retirement considered as an expenditure on Statement ofRevenues, Expenditures and Changes in Fund Balances 249,124

Governmental funds report the effect of issuance costs when debt is firstissued, whereas these amounts are deferred and amortized in the Statementof Activities. This amount is the net effect of the difference in treatment ofissuance costs. (1,859)

Difference between interest on long-term debt on modified accrual basisversus interest on long-term debt on an accrual basis 2 594

Total changes in net assets at June 30, 2007 per Statement of Activities $ (256,072)

The accompanying notes are an integral part of the basic financial statements.

12

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Statement of Fiduciary Assets and LiabilitiesFiduciary FundsJune 30,2007

ASSETS

Cash and interest-bearing deposits

LIABILITIES

Due to taxing bodies, prisoners and others

AgencyFunds

$447,116

$447,116

The accompanying notes are an integral part of the basic financial statements.

13

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements

INTRODUCTION

As provided by Article V, Section 27 of the Louisiana Constitution of 1974, the AvoyellesParish Sheriff (Sheriff) serves a four year term as the chief executive officer of the law enforcementdistrict and ex-officio tax collector of the parish. The Sheriff administers the parish jail system andexercises duties required by the parish court system, such as providing bailiffs, executing orders ofthe court, serving subpoenas, et cetera.

As the chief law enforcement officer of the parish, the Sheriff is responsible for enforcingstate and local laws, ordinances, et cetera, within the territorial boundaries of the parish. The Sheriffprovides protection to the residents of the parish through on-site patrols, investigations, et cetera, andserves the residents of the parish through the establishment of neighborhood watch programs, anti-drug abuse programs, et cetera. In addition, the Sheriff, when requested, provides assistance to otherlaw enforcement agencies within the parish.

As the ex-officio tax collector of the parish, the Sheriff is responsible for collecting anddistributing ad valorem property taxes, parish occupational licenses, state revenue sharing funds,sportsmen's licenses, and fines, costs, and bond forfeitures imposed by the district court.

The accounting and reporting policies of the Avoyelles Parish Sheriff conform to generallyaccepted accounting principles as applicable to governments. Such accounting and reportingprocedures conform to the requirements of the industry audit guide, Audits of State and LocalGovernments.

(1) Summary of Significant Accounting Policies

A. Reporting Entity

For financial reporting purposes, the Sheriff includes all funds, activities, etcetera that are controlled by the Sheriff as an independently elected parish official.As an independently elected parish official, the Sheriff is solely responsible for theoperations of his office, which include the hiring and retention of employees,authority over budgeting, responsibility for deficits, and the receipt and disbursementof funds. The Sheriff is not fiscally dependent on the Avoyelles Parish Police Jury.As required by generally accepted accounting principles, the financial statements ofthe reporting entity include those of the Avoyelles Parish Sheriff (the primarygovernment). There are no component units to be included in the Sheriffs reportingentity.

14

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

B. Basis of Presentation

The accompanying basic financial statements of the Avoyelles Parish Sheriffhave been prepared in conformity with governmental accounting principles generallyaccepted in the United States of America. The Governmental Accounting StandardsBoard (GASB) is the accepted standard setting body for establishing governmentalaccounting and financial reporting principles. The accompanying basic financialstatements have been prepared in conformity with GASB Statement 34, "BasicFinancial Statements-and Management's Discussion and Analysis—for State andLocal Governments", issued in June 1999. As a result, an entirely new financialpresentation format has been implemented.

Government-Wide Financial Statements (GWFS)

The Statement of Net Assets and the Statement of Activities displayinformation about the Sheriff as a whole. They include all funds of the reportingentity, which are considered to be governmental activities. Fiduciary funds arereported only in the Statement of Fiduciary Assets and Liabilities at the fundfinancial statement level.

The statement of activities presents a comparison between direct expensesand program revenues for each of the functions of the Sheriffs governmentalactivities. Direct expenses are those that are specifically associated with a programor function and, therefore, are clearly identifiable to a particular function. Programrevenues include (a) fees and charges paid by the recipients of services offered by theSheriff, and (b) grants and contributions that are restricted to meeting the operationalor capital requirements of a particular program. Revenues that are not classified asprogram revenues, including all taxes, are presented as general revenues.

Fund Financial Statements (FFS)

The Sheriff uses fluids to maintain its financial records during the year. Fundaccounting is designed to demonstrate legal compliance and to aid management bysegregating transactions related to certain Sheriff functions and activities. A fund isdefined as a separate fiscal and accounting entity with a self-balancing set ofaccounts. The various funds of the Sheriff are classified into two categories:governmental and fiduciary. The emphasis on fund financial statements is on majorfunds, each displayed in a separate column. A fund is considered major if it is theprimary operating fund of the Sheriff or its total assets, liabilities, revenues, orexpenditures of the individual governmental fund is at least 10 percent of thecorresponding total for all governmental funds.

15

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

The Sheriff reports the following major governmental funds:

The General Fund is the primary operating fund of the Sheriff. It accountsfor all financial resources except those that are required to be accounted for in otherfunds.

The Sales Tax Special Revenue Fund accounts for the proceeds of a one-halfpercent sales and use tax that is legally restricted to expenditures for specificpurposes.

The Sales Tax Bond Sinking and Reserve Debt Service Fund and theCertificates of Indebtedness, Series 1999 Debt Service Fund are used to account forthe accumulation of resources for and the payment of general long-term debtprincipal, interest and related costs.

The Capital Projects Fund is used to account for the purchase andconstruction of capital assets.

Additionally, the Sheriff reports the following fund types:

Fiduciary Funds

Fiduciary fund reporting focuses on net assets and changes in net assets. Theonly funds accounted for in this category by the Sheriff are agency funds. Theagency funds account for assets held by the Sheriff as an agent for various taxingbodies (tax collections) and for deposits held pending court action. These funds arecustodial in nature (assets equal liabilities) and do not involve measurement of resultsof operations. Consequently, the agency funds have no measurement focus, but usethe accrual basis of accounting.

C. Measurement Focus/Basis of Accounting

The amounts reflected in the governmental fund financial statements areaccounted for using a current financial resources measurement focus. With thismeasurement focus, only current assets and current liabilities are generally includedon the balance sheet. The statement of revenues, expenditures, and changes in fundbalances reports on the sources (i.e., revenues and other financing sources) and uses(i.e., expenditures and other financing uses) of current financial resources. Thisapproach is then reconciled, through adjustment, to a government-wide view of theSheriffs operations.

16

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

The amounts reflected in the governmental fund financial statements use themodified accrual basis of accounting. Under the modified accrual basis of accounting,revenues are recognized when susceptible to accrual (i.e., when they become bothmeasurable and available). Measurable means the amount of the transaction can bedetermined and available means collectible within the current period or soon enoughthereafter to pay liabilities of the current period. The Sheriff considers all revenuesavailable if they are collected within 60 days after the fiscal year end. Expendituresare recorded when the related fund liability is incurred, except for interest andprincipal payments on general long-term debt which is recognized when due, andcertain compensated absences and claims and judgments which are recognized whenthe obligations are expected to be liquidated with expendable available financialresources.

The government-wide financial statements are accounted for using an"economic resources" measurement focus. The accounting objectives of thismeasurement focus are the determination of operating income, changes in net assetsand financial position. All assets and liabilities (whether current or noncurrent)associated with their activities are reported.

The government-wide financial statements are presented using the accrualbasis of accounting. Under the accrual basis of accounting, revenues are recognizedwhen earned and expenses are recorded when the liability is incurred or economicasset used.

D. Assets, Liabilities and Equity

Cash and Interest-bearing Deposits

Cash and interest-bearing deposits include amounts in demand deposits,interest-bearing demand deposits, and time deposits. These deposits are stated atcost, which approximates market.

Interfund Receivables and Payables

During the course of operations, numerous transactions occur betweenindividual funds for goods provided or services rendered. These receivables andpayables are classified as due from other funds or due to other funds on the balancesheet.

17

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

Inventory

Inventory of the Sheriffs General Fund consists of food purchased by theSheriff and commodities granted by the United States Department of Agriculturethrough the Louisiana Department of Agriculture and Forestry. The commodities arerecorded as revenues when received; however, all inventory items are recorded asexpenses when consumed. All purchased inventory items are valued at the lower ofcost (first-in, first-out) or market, and commodities are assigned values based oninformation provided by the United States Department of Agriculture and Forestry.

Capital Assets

Capital assets are capitalized at historical cost or estimated cost if historicalcost is not available. Donated assets are recorded as capital assets at their estimatedfair market value at the date of donation. The Sheriff maintains a threshold level of$5,000 or more for capitalizing capital assets.

Capital assets are recorded in the Statement of Net Assets and Statement ofActivities. Since surplus assets are sold for an immaterial amount when declared asno longer needed for public purposes, no salvage value is taken into consideration fordepreciation purposes. All capital assets, other than land, are depreciated using thestraight-line method over the following useful lives:

EstimatedAsset Class Useful Lives

Buildings and improvements 30-60Office, equipment, and furniture 7-20Vehicles 7

Compensated Absences

Each employee of the Sheriffs office is granted 10 days of vacation leaveand 6 days of sick leave each year after one year of service. Neither vacation norsick leave may be accumulated.

There are no accumulated and vested vacation and sick leave benefits at June30, 2007, which require disclosure to conform with generally accepted accountingprinciples.

18

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

Equity Classifications

In the government-wide statements, equity is classified as net assets anddisplayed in three components:

a. Invested in capital assets, net of related debt - Consists of capitalassets including restricted capital assets, net of accumulateddepreciation and reduced by the outstanding balances of any bonds,mortgages, notes, or other borrowings that are attributable to theacquisition, construction, or improvement of those assets.

b. Restricted net assets - Consists of net assets with constraints placedon the use either by (1) external groups such as creditors, grantors,contributors, or laws or regulations of other governments; or (2) lawthrough constitutional provisions or enabling legislation.

c. Unrestricted net assets - All other net assets that do not meet thedefinition of "restricted" or "invested in capital assets, net of relateddebt."

In the fund statements, governmental fund equity is classified as fundbalance. Fund balance is further classified as reserved and unreserved, withunreserved further split between designated and undesignated.

E. Revenues, Expenditures, and Expenses

Program Revenues

Program revenues included in the Statement of Activities are deriveddirectly from the program itself or from parties outside the Sheriffs taxpayers orcitizenry, as a whole; program revenues reduce the cost of the function to befinanced from the Sheriffs general revenues.

Revenues

Ad valorem taxes and the related state revenue sharing are recorded in theyear taxes are due and payable. Ad valorem taxes are assessed on a calendar yearbasis, become due on November 15 of each year, and become delinquent onDecember 31. The taxes are generally collected in December, January and Februaryof the fiscal year.

19

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

Sales taxes are considered as "measurable" when in the hands of the sales taxcollector and are recognized as revenue at that time.

Intergovernmental revenues and fees, charges and commissions for servicesare recorded when the Sheriff is entitled to the funds.

Interest on interest-bearing deposits is recorded or accrued as revenues whenearned. Substantially all other revenues are recorded when received.

Expenditures

The Sheriffs primary expenditures include salaries and insurance, which arerecorded when the liability is incurred. Capital expenditures and purchases of variousoperating supplies are regarded as expenditures at the time purchased.

Other Financing Sources

Transfers between funds that are not expected to be repaid are accounted foras other financing sources (uses) when the transfer is authorized by the Sheriff.

F- Budget and Budgetary Accounting

The Sheriff follows these procedures in establishing the budgetary datareflected in the financial statements:

1. The chief administrative deputy prepares a proposed budget for thegeneral and special revenue fund on the modified accrual basis ofaccounting and submits it to the Sheriff for the fiscal year no later thanfifteen days prior to the beginning of each fiscal year.

2. A summary of the proposed budgets are published and the public isnotified that the proposed budgets are available for public inspection. Atthe same time, a public hearing is called.

3. A public hearing is held on the proposed budgets at least ten days afterpublication of the call for a hearing.

4. After the holding of the public hearing and completion of all actionnecessary to finalize and implement the budgets, the budgets are legallyadopted prior to the commencement of the fiscal year for which thebudgets are being adopted.

5. All budgetary appropriations lapse at the end of each fiscal year.

20

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

6. The budgets are adopted on a basis consistent with generally acceptedaccounting principles (GAAP). Budgeted amounts included in theaccompanying financial statements are as originally adopted or as finallyamended by the Sheriff.

The proposed budget for June 30, 2007 was made available for publicinspection and was published in the official journal ten days before the publichearing, which was held on June 22, 2006 at the Avoyelles Parish Sheriffs office forcomments from taxpayers. The budget was amended and published in the officialjournal ten days before the public hearing, which was held on June 25, 2007 at theAvoyelles Parish Sheriffs office for comments from taxpayers.

G. Grant Revenue

In general, grants received by the Sheriff are reimbursable type grants, andrevenues are recognized as earned only when the expenditures to be reimbursed havebeen incurred.

H. Estimates

The preparation of financial statements in conformity with accountingprinciples generally accepted in the United States of America require management tomake estimates and assumptions that affect the reported amounts of assets andliabilities and disclosure of contingent assets and liabilities at the date of the financialstatements and the reported amounts of revenues, expenditures, and expenses duringthe reporting period. Actual results could differ from those estimates.

(2) Cash and Interest - Bearing Deposits

Under state law, the Sheriff may deposit funds within a fiscal agent bank organized under thelaws of the State of Louisiana, the laws of any other state in the Union, or the laws of the UnitedStates. The Sheriff may invest in certificates and time deposits of state banks organized underLouisiana law and national banks having principal offices in Louisiana. At June 30, 2007, the Sheriffhas cash and interest-bearing deposits (book balances) totaling $865,218 as follows:

Demand depositsInterest-bearing deposits

Total cash and interest-bearing deposits

Government-wideStatement

of Net Assets

$ 1,054417,048

$418,102

Fiduciary FundsStatement

of Net Assets

$316,794130,322

$447,116

Total

$317,848547,370

$865,218

21

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

Custodial credit risk for deposits is the risk that in the event of the failure of a depositoryfinancial institution, the Sheriffs deposits may not be recovered or will not be able to recovercollateral securities that are in the possession of an outside party. These deposits are stated at cost,which approximates fair value. Under state law, these deposits, (or the resulting bank balances) mustbe secured by federal deposit insurance or the pledge of securities owned by the fiscal agent bank.The fair value of the pledged securities plus the federal deposit insurance must at all times equal theamount on deposit with the fiscal agent bank. These securities are held in the name of the pledgingfiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties. Depositbalances (bank balances) at June 30,2007, are secured as follows:

Bank balances $ 787,726

Federal deposit insurance $ 200,000Pledged securities (category 3) 587,726

Total federal insurance and pledged securities $ 787,726

As of June 30, 2007, the Sheriffs total bank balances were fully insured and collateralizedwith securities held in the name of the sheriff by the pledging financial institution's agent and,therefore, not exposed to custodial credit risk.

(3) Ad Valorem Taxes

The Sheriff is the ex-officio tax collector of the parish and is responsible for the collectionand distribution of ad valorem taxes. Ad valorem taxes attach as an enforceable lien on property as ofJanuary 1, of each year. Taxes are levied by the parish government in June and are actually billed tothe taxpayers by the Sheriff in October. Billed taxes are due by December 31, becoming delinquenton January 1 of the following year. The taxes are based on assessed values determined by the TaxAssessor of Avoyelles Parish and are collected by the Sheriff. The taxes are remitted to theappropriate taxing bodies net of deductions for assessor's compensation and pension fundcontributions.

Ad valorem taxes are budgeted and recorded in the year for which levied and billed. For theyear ended June 30, 2007, law enforcement taxes applicable to the Sheriffs General Fund, werelevied at the rate of 6.41 mills on property with assessed valuations totaling $133,284,630.

Total law enforcement taxes levied during 2007 were $527,168. There were no taxesreceivable in the General Fund at June 30,2007.

22

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

(4) Due from Other Governmental Units

Amounts due from other governmental agencies totaling $1,036,120 at June 30, 2007,consisted of the following:

(5)

General

Department of Public Safety and CorrectionsDepartment of TreasuryAvoyelles Parish Police JuryAvoyelles Parish School BoardVarious parishes and cities

$ 683,08645,22691,799

54,528

Capital Assets

Capital asset activity for the year ended June 30, 2007 was as follows:

Balance07/01/06 Additions Deletions

Governmental activities:Capital assets not being depreciated:

LandConstruction in progress

Other capital assets:Buildings and improvementsEquipment and furnitureVehicles

Totals

Less accumulated depreciationBuildings and improvementsEquipment and furnitureVehicles

Total accumulated depreciation

Governmental activities,capital assets, net

Depreciation expense in the amount of $342,505 was charged to public safety.

SpecialRevenue

$ 34,474

127,007

$ 874,639 $ 161,481

Balance06/30/07

$ 174,400191,588

5,506,3602,037,774989,492

8,899,614

1,259,1431,528,600563,581

3,351,324

$5,548,290

$ -

191,58842,315142,390

$ 376,293

$ 101,225133,465107,815

$ 342,505

$ - $ 174,400191,588

5,697,9482,080,0891,131,882

$ 191,588 9,084,319

$ - 1,360,3681,662,065671,396

$ - 3,693,829

$5,390,490

23

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

(6) Dedication of Proceeds and Flow of Funds - Sales and Use Tax

Proceeds of the one-half cent sales and use tax (2007 collections - $1,871,375) approved byvoters on November 19, 1992 and levied by the Sheriff beginning January 1, 1993 are dedicated tothe following purposes:

Establishing, acquiring, constructing, improving, maintaining, staffing andoperating equipment and facilities necessary to provide enhanced 911 emergencytelephone, ambulance, dispatch and other services for the benefit of the residents ofthe Parish.

Each month there will be set aside into a "Bond and Interest Sinking Fund", also called the"Sinking Fund", an amount consisting of 1/12 of the next maturing installment of principal andinterest on the outstanding bonds. Such transfers must be made on or before the 20th day of eachmonth to assure the prompt payment of principal and interest as they become due and may be usedonly for such payments.

During the year ended June 30, 2007, the Sheriff complied with all of the aboverequirements.

At June 30, 2007, $161,481 of sales tax receivable is reflected on the Sales Tax Fund'sbalance sheet.

(7) Retirement Commitments

All employees are members of one of the following retirement systems:

Federal Social Security SystemLouisiana Sheriffs Pension and Relief Fund

Pertinent information relative to each plan follows:

A. Federal Social Security System

All employees who are not eligible to participate in the Louisiana SheriffsPension and Relief Fund are members of the Federal Social Security System. TheSheriff and its employees contribute a percentage of each employee's compensationto the System (7.65% contributed by the Sheriff; 7.65% by the employee). TheSheriffs contribution during the year ended June 30,2007 amounted to $234,465.

24

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

B. Louisiana Sheriffs Pension and Relief Fund

Plan Description-

Substantially all employees of the Avoyelles Parish Sheriffs office aremembers of the Louisiana Sheriffs Pension and Relief Fund (Retirement System), acost-sharing multiple-employer defined benefit pension plan administered by aseparate board of trustees.

All sheriffs and all deputies who are found to be physically fit, who earn atleast $400 per month, and who were between the ages of 18 and 50 at the time oforiginal employment are required to participate in the Retirement System.Employees are eligible to retire at or after age 55 with at least 12 years of creditedservice and receive a benefit, payable monthly for life, equal to a percentage of theirfinal-average salary for each year of credited service. The percentage to be used foreach year of service is 2.5% for each year if total service is at least 12 but less than15 years, 2.75% each year if total service is at least 15 years but less than 20 years,and 3% for each year if total service is at least 20 years (Act 1117 of 1995 increasedthe accrual rate to 0.25% for all service rendered on or after January 1, 1980). In anycase, the retirement benefit cannot exceed 100% of the final-average salary. Final-average salary is the employee's average salary over the 36 consecutive or joinedmonths that produce the highest average. Employees who terminate with at least 12years of service and do not withdraw their employee contributions may retire at orafter the age 55 and receive the benefit accrued to their date of termination asindicated previously. Employees who terminate with at least 20 years of creditedservice are also eligible to elect early benefits between the ages of 50 and 55 withreduced benefits equal to the actuarial equivalent of the benefit to which they wouldotherwise be entitled at age 55. The Retirement System also provides death anddisability benefits. Benefits are established or amended by state statute.

The Retirement System issues an annual publicly available financial reportthat includes financial statements and required supplementary information for theRetirement System. That report may be obtained by writing to the Louisiana SheriffsPension and Relief Fund, Post Office Box 3163, Monroe, Louisiana 71220, or bycalling (318) 362-3191.

25

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

Funding Policy-

Plan members are required to contribute 10.0% of their annual covered salaryand the Avoyelles Parish Sheriff is required to contribute at an actuarially determinedrate. The current rate is 11% of annual covered payroll. Contributions to theRetirement System also included one-half of one percent of the taxes shown to becollectible by the tax rolls of each parish and funds as required and available frominsurance premiums. The contribution requirements of the plan members and theAvoyelles Parish Sheriff are established and may be amended by state statute. Asprovided by R.S. 11:103, the employer contributions are determined by actuarialvaluation and are subject to change each year based on the results of the valuation forthe prior fiscal year. The Avoyelles Parish Sheriffs contributions to the RetirementSystem for the years ended June 30, 2007, 2006 and 2005 were $508,021, $498,912and $673,670 respectively, equal to the required contributions for each year.

(8) Postretirement Health Care Insurance Benefits

The Sheriff provides certain health care insurance benefits for its retired employees.Substantially all of the Sheriffs employees are eligible for these benefits if they reach normalretirement age while working for the Sheriff. These benefits for retirees and similar benefits foractive employees are provided through an insurance company where the monthly premium is paid bythe Sheriff. The Sheriffs cost of providing retirees* health care insurance benefits is recognized asexpense when the monthly premiums are paid and as revenue when reimbursement is received fromthe retiree. For the year ended June 30, 2007, the amount of retiree benefits totaled $74,905 and therewere fifteen former employees qualified to receive such benefits.

In November 2004, the Governmental Accounting Standards Board (GASB) issued Statement45 "Accounting and Financial Reporting by Employers for Postemployment Benefits Other ThanPensions." This statement requires the accrual of postemployment benefits for retired employees.The Sheriff is required to implement this standard for the fiscal year ending June 30, 2009. TheSheriff has not yet determined the full impact that adoption of GASB Statement 45 will have on thefinancial statements.

26

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

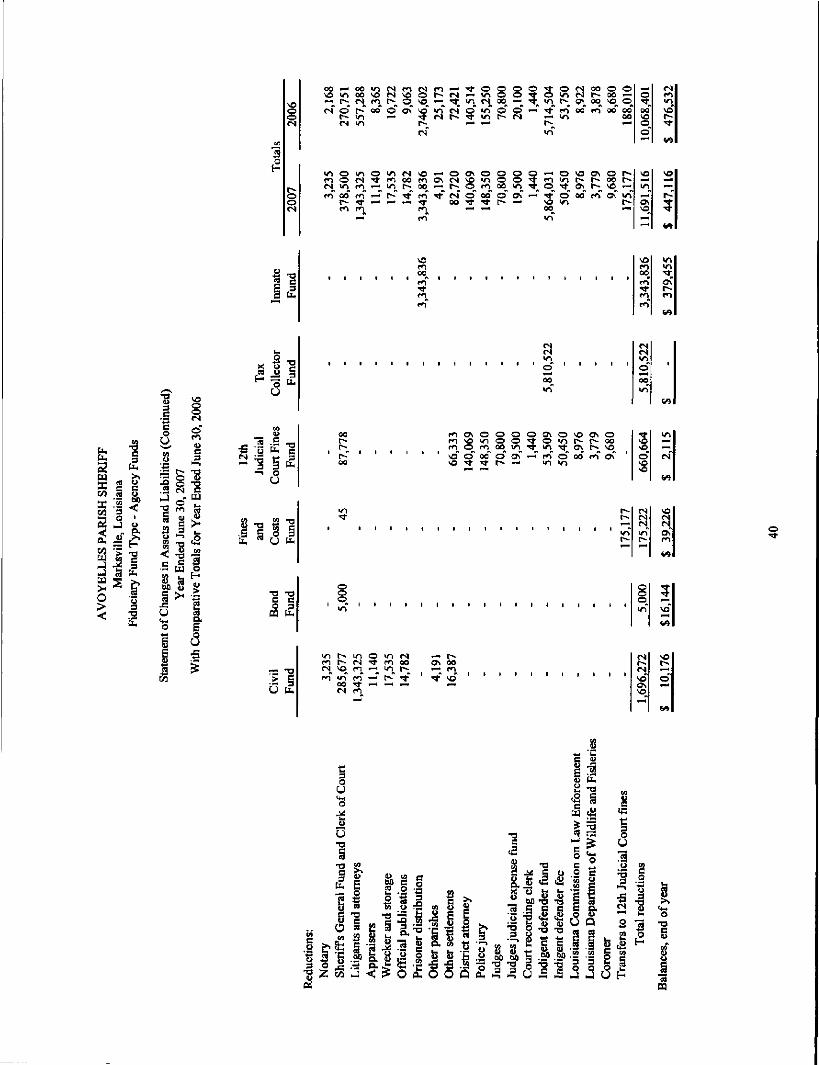

(9) Changes in Agency Fund Balances

A summary of changes in agency fund balances due to taxing bodies and others and due toprisoners follows:

Balances, July 1,2006AdditionsReductions

Civil FundBond Fines andFund Costs Fund

$ 5,5021,700,9461,696,272

$ 20,669475

5,000

$ 33,992180,456175,222

Balances, June 30,2007 $ 10,176 $ 16,144 $ 39,226

Balances, July 1,2006AdditionsReductions

Balances, June 30, 2007

12thJudicial Court

Fines Fund

$ 1,474661,305660,664

$ 2,115

TaxCollector

Fund

$5,810,5225,810,522

$

InmateFund

$ 414,8953,308,3963,343,836

$ 379,455

(10) Long-Term Debt

The Sheriffs long-term debt is attributable to governmental activities. The following is asummary of the long-term debt transactions for the year ended June 30,2007:

Certificates ofindebtedness

Sales tax bondsCapital LeaseNotes payable

Balance07/01/06 Additions

$ 375,000 $1,395,000

-89,124

Reductions

$ 90,00070,000

-89,124

Balance Due Within06/30/07 One Year

$ 285,000 $ 90,0001,325,000 75,000

--

Total $ 1,859,124 $ $ 249,124 $ 1,610,000 $ 165,000

27

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

Long-term debt outstanding at June 30,2007 is comprised of the following:

$1,460,000 Sales Tax Bonds dated September 1, 2004; due in annual installments of$65,000 to $135,000 through September 1, 2019; interest due semi-annually at 4.00to 6.50 percent; secured by an irrevocable pledge and dedication of funds derivedfrom a parishwide special tax of 6.41 mills. $ 1,325,000

$800,000 Certificates of Indebtedness dated September 1, 1999; due in annualinstallments of $60,000 to $100,000 through September 1, 2009; interest at 5.04percent; secured by an irrevocable pledge and dedication of funds derived from aparishwide special tax of 6.41 mills. 285,000

Total general long-term debt 1,610,000

Less: Unamortized issuance costs (22,617)

Net general long-term debt $1,587,383

Annual debt service requirements to maturity are as follows:

Year Ending June 30, Principal Interest Totals

20082009201020112012

2013-20172018-2020

(11) Litigation and Claims

At June 30, 2006, the Sheriff is involved in several lawsuits claiming damages which are notcovered by insurance. The Sheriffs legal advisor is unable to estimate the ultimate resolution ofthese matters. Any unfavorable resolution, if any, would not materially affect the financialstatements.

$

$

165,000170,000185,00090,00090,000525,000385,000

1,610,000

$ 68,74060,60352,03345,66941,819145,72226,700

$ 441,286

$ 233,740230,603237,033135,669131,819670,722411,700

$2,051,286

28

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Notes to the Basic Financial Statements (Continued)

(12) Risk Management

The Sheriffs office is exposed to various risks of loss related to torts; theft of, damage to, anddestruction of assets; errors and omissions; injuries to employees; and natural disasters. The Sheriffwas unable to obtain law enforcement liability insurance at a cost it considered to be economicallyjustifiable. Management believes it is more economical to manage its risk internally and set asideassets for claim settlement in its General Fund. As of June 30, 2007, no funds were designated forlaw enforcement liability claims and incidental costs. In the opinion of management and the Sheriffslegal counsel, no events have occurred that give rise to report any claim liability at June 30, 2007.

The Sheriff continues to carry commercial insurance for all other risks of loss. Settled claimsresulting from these risks have not exceeded commercial insurance coverage in any of the past fourfiscal years.

(13) Interfund Transactions

Transfers consisted of $857,514 transferred from the Sales Tax Special Revenue Fund to theGeneral Fund for reimbursement of personnel services and related benefits and other expenditures.Interfund receivables and payables consisted of $150,000 due to the General Fund from the Sales TaxFund for reimbursement of expenditures.

(14) Wireless E911 Service

The Avoyelles Parish Sheriff does not collect service charges on emergency telephoneservices. All 911 services are funded with the proceeds of the one-half percent sales and use tax nowbeing levied and collected pursuant to an election held on November 3, 1992, recorded as revenue inthe Special Revenue Fund in these financial statements. At June 30, 2007 Avoyelles Parish is notoperating a wireless E911 system.

(15) Deficit Fund Balance

The General Fund has a deficit fund balance of $298,021 as of June 30, 2007. The deficitwill be eliminated by increasing revenues and/or reducing expenditures.

(16) Contineencv

In August 2007, the Sheriff was indicted by a federal grand jury. The indictment alleges theSheriff illegally pocketed profits from phone services provided at parish jails. A court date has beenset for October 2008. Any resulting outcome form these legal proceedings cannot be determined atthis time.

29

REQUIRED SUPPLEMENTARYINFORMATION

30

AVOYELLES PARISH SHERIFFMarksville, Louisiana

General FundBudgetary Comparison Schedule

Year Ended June 30,2007

Revenues:Ad valorem taxesIntergovernmental revenues -

State grants:State revenue sharingState supplemental payOther

Fees, charges, and commissions for servicesCivil and criminalFeeding and keeping prisoners

Miscellaneous -Indian affairsInterest incomeOther

Total revenues

Expenditures:Current -

Public Safety:Personal services and related benefitsOperating servicesOperations and maintenance

Debt serviceCapital outlay

Total expenditures

Deficiency of revenues overexpenditures

Other financing sources (uses):Transfers in

Total other financing sources (uses)

Excess of revenues and other sourcesover expenditures and other uses

Fund balance, beginning

Fund balance (deficit), ending

BudgetOriginal Final Actual

Variance withFinal Budget

Positive(Negative)

$ 525,000 $ 540,000 $ 558,611 $ 18,611

120,000174,00052,400

175,0009,215,000

575,0004,000

747,500

11,587,900

120,699193,22733,575

230,0009,250,000

450,0004,000

791,700

11,613,201

120,699175,74826,923

344,8598,062,496

381,397450

1,767,689

11,438,872

-(17,479)(6,652)

114,859(1,187,504)

(68,603)(3,550)

975,989

(174,329)

7,391,0001,198,0003,320,600339,638118,000

12,367,238

(779,338)

800,000

800,000

20,662

3,286

7,306,1831,288,0003,484,55029,191192,500

12,300,424

(687,223)

804,000

804,000

116,777

3,286

7,310,1541,357,2123,693,84699,897136,584

12,597,693

(1,158,821)

857,514

857,514

(301,307)

3,286

(3,971)(69,212)(209,296)(70,706)55,916

(297,269)

(471,598)

53,514

53,514

(418,084)

$ 23,948 $ 120,063 $ (298,021) $ (418,084)

31

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Special Revenue Fund - Sales Tax FundBudgetary Comparison Schedule

Year Ended June 30,2007

Revenues:Sales taxesIntergovernmental revenues -

Federal grantMiscellaneous -

Other

Total revenues

Expenditures:Current -

Public safety:Personal services and related benefitsOperating servicesOperations and maintenance

Capital outlay

Total expenditures

Excess of revenuesover expenditures

Other financing uses:Transfers out

Excess (deficiency) of revenuesover expenditures and other uses

Fund balance, beginning

Fund balance, ending

BudgetOriginal

$1,750,000

75,000

2,000

1,827,000

450,00050,000

276,20070,000

846,200

980,800

(800,000)

180,800

5,977

$ 186,777

Final

$1,750,685

6,100

1,756,785

446,00050,000

236,18767,140

799,327

957,458

(804,000)

153,458

5,977

$ 159,435

Actual

$1,696,193

12,779

1,708,972

443,87049,434

281,52571,385

846,214

862,758

(857,514)

5,244

5,977

$ 11,221

Variance withFinal Budget

Positive(Negative)

$ (54,492)

$

6,679

(47,813)

2,130566

(45,338)(4,245)

(46,887)

(94,700)

(53,514)

(148,214)

$_d48,214)

32

OTHER SUPPLEMENTARY INFORMATION

33

AVOYELLES PARISH SHERIFFMarksville, Louisiana

General Fund

Schedule of ExpendituresAmended Budget (GAAP Basis) and Actual

Year Ended June 30,2007With Comparative Actual Amounts for Year Ended June 30,2006

2007

Public safety:Personal services and related benefits -

Sheriff salaryDeputies salariesPension and payroll taxes

Total personal services and related benefits

Operating services -Deputy liability insuranceHospitalization insuranceAuto insuranceOther insurance

Total operating services

Operations and maintenance -Auto maintenance and fuelDeputy uniforms and suppliesOffice supplies and expensesTelephonePrisoner feeding and maintenanceLegal feesOther professional feesCriminal investigationJail maintenance, utilities, and leaseDues and subscriptionsOther

Total operations and maintenance

AmendedBudget

$ 117,5306,011,6531,177,000

7,306,183

1,0001,028,000224,00035,000

1,288,000

472,50063,000194,00051,750

1,333,50075,000105,0001,000

1,159,70016,00013,100

3,484,550

Actual

$ 120,5096,014,0571,175,588

7,310,154

1,1121,039,703268,34048,057

1,357,212

561,52673,969281,96651,917

1,330,49847,92099,143

8011,155,092

11,59079,424

3,693,846

Variance -Positive(Negative)

$ (2,979)(2,404)1,412(3,971)

(112)(11,703)(44,340)(13,057)

(69,212)

(89,026)(10,969)(87,966)(167)3,00227,0805,857199

4,6084,410

(66,324)

(209,296)

2006Actual

$ 109,5585,828,2931,192,667

7,130,518

2,297870,093282,84046,360

1,201,590

468,69858,863309,93245,226

1,190,26349,06982,08311,948

1,091,28911,24877,985

3,396,604

(continued)

34

AVOYELLES PARISH SHERIFFMarksville, Louisiana

General Fund

Schedule of ExpendituresAmended Budget (GAAP Basis) and Actual (Continued)

Year Ended June 30,2007With Comparative Actual Amounts for Year Ended June 30,2006

2007

AmendedBudget Actual

Variance -Positive

(Negative)2006

Actual

Debt service -PrincipalInterest

Total debt service

Capital outlay -AutosEquipment

Total capital outlay

Total expenditures

24,6944,497

29,191

89,12410,773

99,897

(64,430)(6,276)

(70,706)

253,31317,833

271,146

120,00072,500192,500

119,64916,935

136,584

35155,565

55,916

58,90011,774

70,674

$12,300,424 $12,597,693 $ (297,269) $12,070,532

35

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Sales Tax Fund

Schedule of ExpendituresAmended Budget (GAAP Basis) and Actual

Year Ended June 30,2007With Comparative Actual Amounts for the Year Ended June 30, 2006

2007

Public safety:Personal services and

related benefits -Director salarySecretary salaryAdministrative salaryCommunication salariesPension and payroll taxes

Total personal services andrelated benefits

Operating services -Deputy hospitalization

Operations and maintenance -Ambulance serviceAuto maintenance and fuelRadio maintenanceOffice supplies and expensesComputer softwareTelephoneProfessional feesSales tax collection feePublications, dues and subscriptionsUtilitiesUniformsEducation and trainingOther

Total operations and maintenance

Capital outlay:AutomobilesRadiosEquipment

Total capital outlay

Total expenditures

AmendedBudget

$ 45,00027,000

312,00062,000

446,000

50,000

27,4929,87637,37515,000

-91,344

-26,5005,00021,500

750750600

236,187

22,74013,90030,50067,140

Actual

$ 44,40026,600

311,25361,617

443,870

49,434

27,4924,80749,82515,201

144127,1031,60526,4673,66922,579

513714

1,406

281,525

22,74017,91130,73471,385

Variance -Positive(Negative)

$ 600400

747383

2,130

566

5,069(12,450)(201)(144)

(35,759)(1,605)

331,331(1,079)23736

(806)

(45,338)

(4,011)(234)

(4,245)

2006Actual

$ 43,00025,93020,650

299,85360,096

449,529

49,358

27,4924,567

46,87219,520

399155,273

2,00027,823

6,26723,988

209400

3,608

318,418

138,249138,249

$ 799,327 $ 846,214 $ (46,887) $ 955,554

36

FIDUCIARY FUNDS

Civil FundTo account for funds held in connection with civil suits, Sheriffs sales, and garnishments and payment ofthese collections to the Sheriffs General Fund and other recipients in accordance with applicable laws.

Bond FundTo account for the collection of bonds, fines, and costs and payment of these collections to the Sheriffs 12thJudicial Court Fines Fund.

Fines and Cost FundTo account for the collection of fines and costs and payment of these collections to the Sheriffs 12thJudicial Court Fines Fund.

12th Judicial Court Fines FundTo account for the collection of fines and costs and payment of these collections to the Sheriffs GeneralFund and other recipients in accordance with applicable laws.

Tax Collector FundArticle V, Section 27 of the Louisiana Constitution of 1974, provides that the Sheriff will serve as thecollector of state and parish taxes and fees. The Tax Collector Fund is used to collect and distribute thesetaxes and fees to the appropriate taxing bodies.

Inmate FundTo account for the deposits made by, and for, inmates to their individual accounts and the appropriatedisbursements to these inmates.

37

to"33H

sooo<N

(N

*nso"

bO

r*- mfi ONso oo

3

e«

(Nff)inso"

&e

roo(N

sor-H

r-"

S

— < *nso «nso rr-" ON"

^

so1— 11— 1r-"

3w-iVI

ON ONr-o-i

Cl_

fepq

w -W gco _53K '«3

•^

1 J

PH ^co 'g

9|H ^W *5J5n ^^O

CO_W'

£C3•!-•

J

-O§w

1>COCO

1 5"»^ '.^

Age

ncy

Ft o

f Fi

duc

£D

CO00.a.s£So0

SOoo(N

o"f^to

0 <§O .-

o-|

i .>ga.IuSE?

a l lr^ *^? FT.

O

•^ V5

1

&

U3

-- Sfl • H *"OrC 'rt [Li C2

M ^5 t* r^^ I I f ao

W +J -^

.S 5 ® §

•n,_<

ri

•nT— 1

in,_i

CM"

so<N

ON"CO

SOCN(NON" 'mrf.

soCN

ON"rf*

t/J W-3 WT7

c so 3CQ to

1— t

^— t

€^^SO" '

€^

9SO"

W-

— *n'> S• -j 3u £

SO

^o"?— (

SO

«-"o"

so^o"

00m

CO

o

tbOC

COCO

U^1n4>

•»H

T3O M -Sra

U

S rtwCO

2 'C•9 P»P O•*-• *-*u u3 3Q Q

^3o

00 rf ro OOs (S TJ- OOO OO fS V>

tN Wi O^ Os rO<N t t

OS CO ^-r- - r-SO 00 SO — 00

c o ^ O O O O O t - f N S O O s O so « n r - - v > f N ~ - ( S w - > o s o sO s c O l " - C S O O s » n r N r o i Oro ro <S•* — t^

— O O 1^ O^f I"- <—< •—i Os

roroOs

VI

o"

tNro

00ro

\O Os>n Os(S COr-* o"— Os

OstNCO(S

tN(N

U

'£

oU

§ §U b

T3 T3

IICQ fe

oVO

Oo"

.u

O

cs

CO \O Oo «n r*-Os ro r*-co" ro" fN*" 'rf — r- or-

Osro

5

0>

ince

s, b

egin

ning

of 3

*e3CQ

CO

§;c'ST3<

iwOauQ

nd s

eizu

res

CO

Sher

iffs

sal

es,

suits

,A

dvan

ce d

epos

itsC

lerk

of c

ourt

fee

s

•a§m

COOU

-oiCOu.g

ent c

olle

ctio

n;

B

Out

side

and

gar

nish

1

oi-t

Tax

es,

fees

, etc

. pai

cPr

ison

er d

epos

its

6 c

Wor

k re

leas

e pr

ogra

Inte

rest

on

inve

stm

e

Tot

al a

dditi

ons

CO1

tu2pj

Xt/1

"8§

oU•

OO(N

a & 5 2 .ai 8 .2 CN C

•-» o

< Itu•u

B

I

o.£

«5

.ctN

—*

COO

£

sOO

(N

en

5oH

ootN

•krf TJ

S 2£ 3J ti.

L.3 ^x t> ^

fl| JU

COu

1§ -S T3

ir? +* 3

£ 3 ^

— ^o

W T3"2 to CS O 3M CJ tt.

c c0 3

CQ U-

— -Q*> §U h

oo i"™ oo in M c*1! r^ ro ^^*o in oo 'O <N o o f^ tN•— « t " - t N r O P 1 - O * O ' - M ^-

f S o r ^ - o o o o s s o i n t Nes m r^

<N"

« n O m O « n f S ^ o — 0f ^ l O M ^ t ' O O O f ' l O S t N( S i n m - — ' * n r * - o o * — r ^m o o m ^ - r - ^ - f i ' ^ ' t N

t-^ ^t ^- — — • -*t oor«^ rn ro

-H f^

rOJJ* • .

fi_m

1 1 1 1

oo ror- ror~- f*^1 rT ^ooo \o

m^t

i i i i i i i i

ooo1 " 1 t 1 1 1 1 1

[^ 0 tN —r*l f*- tN ^ ft OO ON OOtN ^o fi •— ' in t~- "- • r*"jr*i in r^i •— < f*- ^* ^ " % o

CS rn ^" ^ "" ^*

T f o o o o ^ o * s o o o o»™ in o O ^l* o "n <N r*^ oo ^^i n c s o o — • • ^ • i n r - o s o o v o oo « n o o ^ - ^ t m o o f ^ o o o o^r in (^ tN ^ m oo

in"

O s O O O O ^ H O s O O s O r 1 *

S ^ o o ^ ^ o S & f ^ S ^O o o o c 3 s ^ - T t o o o r o o s i n^ T^ f^ i~" so in i"""^- — oo^ — im"

i * i > i i i i i i i

tNtNino ' ' ' ' '

»,

s o m o o ^ O i n r - r ^ o oO r ' i o o i n ^ ' i n ^ - o s r - v oo" oo o" os" ~- f*T o" oo" m" o\" '•^ ^f r- — ' in in

r-r*-in"r-

• i i i i i i i i i i

i i i i i

^-o00

So"T-l

VO

^~Os^o

-voPO

en""Im"

tNino"°°m"

1ovS

tNtN

m"r-

ooin"

tstN\Q

ON

fSff)in\ar-

w

ysHr-"

*»min

Os"

m

<•

'

«

in^-ics"

w

SOtN

Os"

5

Z

^-o"

Fun

d an

d C

lerk

of

Cou

rt

2

.edu

ctio

ns:

Not

ary

She

riff

s G

en

K

&Ei•a

1_{«"£*J

0

1

App

rais

ers

Wre

cker

and

CflCQ

'fiU

Off

icia

l pu

bli

o1,0

Pri

sone

r di

str CO

Oth

er p

aris

he

acV

CO

&

&

Dis

tric

t at

torr

Pol

ice

jury

Judg

es

•o1u .,

"3 C

Judg

es ju

dici

iC

ourt

rec

ordi

•ac

1c

Indi

gent

def

e

1c

Indi

gent

def

e:is

sion

on

Law

Enf

orce

men

t

S

Lou

isia

na C

o

tien

t of

Wil

dlif

e an

d Fi

sher

iei

1o.

Lou

isia

na D

eC

oron

erJu

dici

al C

oun

fin

es

31

Tra

nsfe

rs to

1

CO

_O

1

1H

1o*ogtfui

"rtPQ

AVOYELLES PARISH SHERIFFMarksville, Louisiana

Tax Collector Agency Fund

Statement of Collections, Distributions, and Unsettled BalancesYear Ended June 30,2007

Unsettled balances, July 1,2006

Collections:Ad valorem taxesInterest on -

Interest-bearing depositsDelinquent taxes

Parish licensesState revenue sharingRedemptionsTax notices, etc.Payment in lieu of taxes

Total collections

Total

Distributions:Avoyelles Parish -

Police JurySchool BoardAssessorClerk of CourtSheriffHospital Service District No. 1

City of MarksvilleWard I Fire DistrictFire Protection District No. 2Red River Waterway District TreasurerSouthwest Water DistrictGravity Drainage DistrictLevee District TreasurerLouisiana Forestry CommissionLouisiana Tax CommissionPension fundsRedemptions

Total Distributions

Unsettled balances at June 30,2007

4,650,888

2086,897

187,722883,75428,85416,84635,353

5,810,522

5,810,522

1,432,5431,333,396

568,28125

717,27482,709

264,04438,714

705,809238,059

16,50517,052

231,25312,1844,043

125,06423,567

5,810,522

$ -

41

COMPLIANCE

AND

INTERNAL CONTROL

42

C. Burton Kolder, CPA*Russell F. Champagne, CPA"Victor R.SIaven, CPA*P. Troy Courville. CPA*Gerald A. Thibodeaux, Jr., CPA*Robert S. Carter, CPA*Arthur R. Mixon, CPA*

KOLDER, CHAMPAGNE, SLAVEN & COMPANY, LLCCERTIFIED PUBLIC ACCOUNTANTS

Tynes E. Mixon, Jr., CPAAllen J. LaBry, CPAAlbert R. Lager, CPAPFS.CSA*Penny Angelle Scrugglns, CPAChristine L. Cousin, CPAMary T. Thibodeaux, CPAMarshall W. Guidry, CPAAlan M. Taylor, CPAJames R. Roy, CPARobert J. Metz, CPAKelly M. Doucet, CPACheryl L. Bartley, CPA, CVAMandy B. Self, CPAPaul L. Delcambre, Jr. CPA

Retired:Conrad 0. Chapman, CPA* 2006Harry J. Clostio, CPA 2007

REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING AND ON COMPLIANCE

AND OTHER MATTERS BASED ON AN AUDITOF FINANCIAL STATEMENTS PERFORMED IN

OFFICES

183 South Beadle Rd.Lafayette, LA 70508

Phone (337) 232-4141Fax (337) 232-6660

113 East Bridge St. 133 East Waddill St.Breaux Bridge, LA 70517 Marksville, LA 71351Phone (337) 332-4020 Phone (318) 253-9252Fax (337) 332-2867 Fax (318) 253-8681

1234 David Dr. Ste 203Morgan City. LA 70380Phone (985) 384-2020Fax (985) 384-3020

332 West Sixth AvenueOberlin, LA 70655Phone (337) 639-4737Fax (337) 639-4568

450 East Main StreetNew Iberia, LA 70560Phone (337) 367-9204Fax (337) 367-9208

408 West Cotton StreetVille Platte, LA 70586

Phone (337) 363-2792Fax (337) 363-3049

200 South Main StreetAbbeville. LA 70510

Phone (337) 893-7944Fax (337) 893-7946

1013 Main StreetFranklin, LA 70538

Phone (337) 828-0272Fax (337) 828-0290

ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS* A Profouionaf Accounting Corporation

WEB SITE;WWW. KCSRCPAS.CO M

The Honorable Bill BeltAvoyelles Parish SheriffMarksville, Louisiana

We have audited accompanying financial statements of the governmental activities, the business-typeactivities, and each major fund of the Avoyelles Parish Sheriff (the Sheriff) as of and for the year ended June30, 2007, which collectively comprise the Sheriffs basic financial statements and have issued our reportthereon dated December 20, 2007. We conducted our audit in accordance with auditing standards generallyaccepted in the United States of America and the standards applicable to financial audits contained inGovernment Auditing Standards, issued by the Comptroller General of the United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the Sheriffs internal control over financialreporting as a basis for designing our auditing procedures for the purpose of expressing our opinions on thefinancial statements, but not for the purpose of expressing an opinion on the effectiveness of the Sheriffsinternal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness ofthe Sheriffs internal control over financial reporting.

Our consideration of internal control over financial reporting was for the limited purpose described inthe preceding paragraph and would not necessarily identify all deficiencies in internal control over financialreporting that might be significant deficiencies or material weaknesses. However, as discussed below, weidentified a certain deficiency in internal control over financial reporting that we consider to be a significantdeficiency.

A control deficiency exists when the design or operation of a control does not allow management oremployees, in the normal course of performing their assigned functions, to prevent or detect misstatements ona timely basis. A significant deficiency is a control deficiency is a control deficiency or combination ofcontrol deficiencies, that adversely affects the Sheriffs ability to initiate, authorize, record, process, or reportfinancial data reliably in accordance with generally accepted accounting principles such that there is morethan a remote likelihood that a misstatement of the Sheriffs financial statements that is more thaninconsequential will not be prevented or detected by the Sheriffs internal control. We consider the controldeficiency described in the accompanying summary schedule of current and prior year audit findings andcorrective action plan as item 07-1 to be a significant deficiency in internal control over financial reporting.

Member of:AMERICAN INSTITUTE OFCERTIFIED PUBLIC ACCOUNTANTS

Member of:SOCIETY OF LOUISIANA

CERTIFIED PUBLIC ACCOUNTANTS

43

A material weakness is a significant deficiency, or combination of significant deficiencies, that resultsin more than a remote likelihood that a material misstatement of the financial statements will not be preventedor detected by the Sheriffs internal control.

Our consideration of the internal control over financial reporting was for the limited purposedescribed in the first paragraph of this section and would not necessarily identify all deficiencies in internalcontrol that might be significant deficiencies and, accordingly, would not necessarily disclose all significantdeficiencies that are also considered to be material weaknesses. However, we believe that the significantdeficiency described above is not a material weakness.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Sheriffs financial statements are free ofmaterial misstatement, we performed tests of its compliance with certain provisions of laws, regulations,contracts and grant agreements, noncompliance with which could have a direct and material effect on thedetermination of financial statement amounts. However, providing an opinion on compliance with thoseprovisions was not an objective of our audit, and accordingly, we do not express such an opinion. The resultsof our tests disclosed one instance of noncompliance or other matters that is required to be reported underGovernment Auditing Standards and which is described in the accompanying summary schedule of currentand prior year audit findings and corrective action plan as item 07-2.

The Sheriffs response to the findings identified in our audit is described in the accompanyingsummary schedule of current and prior year audit findings. We do not audit the Sheriffs response and,accordingly, we express no opinion on it.

This report is intended solely for the information of the Avoyelles Parish Sheriffs management andfederal awarding agencies and pass-through entities and is not intended to be and should not be used byanyone other than these specified parties. Although the intended use of this report may be limited, underLouisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

Kolder, Champagne, Slaven & Company, LLCCertified Public Accountants

Lafayette, LouisianaDecember 20, 2007

44

"5? c« o

oU

I I

00

-C cco a

'3o

o

£

bM

>-O

.2 o"

•«S «c < c« O 3

C •£ ^P tj 41n o *oU o tS<*- O i.S "° 8

. i c eG 2 «

U

.£T3Cix

oco-Ca'Cuwa>Q

50 x=

oooo

03 K U

>.

S 1c c1> <U

_e

ii itE - w l S T 3 D J ) r t t f l n j C L

SOa.

H - i S C

!§ !§

.

c -« "3. '€1„

8 ^ 3 1•XJD

cin

o

IoEuIbOC

CoB-

a «

o£oU

j

om*3ofiT<u>-

OSa.

coic

"S

OauOi__

_rt'uCrt

.£

u>

*•*

IO

^

E

1

i_iuiEoct-u

SiV

r^

O

EoU